Exhibit 99.1

OSISKO DEVELOPMENT CORP.

. . . . . . . . . . . . . . . . . .

Condensed Consolidated Financial Statements

For the three and nine months ended

September 30, 2023

Osisko Development Corp.

Consolidated Statements of Financial Position

As at September 30, 2023 and December 31, 2022

(Unaudited)

(Expressed in thousands of Canadian dollars)

| | |

| September 30, |

| December 31, |

| | | | 2023 | | 2022 |

|

| Notes |

| $ |

| $ |

Assets |

|

| |

| |

|

| | | | | | |

Current assets |

|

| |

| |

|

| | | | | | |

Cash and cash equivalents |

| 4 | | 71,498 | | 105,944 |

Amounts receivable |

| 5 | | 6,417 | | 11,046 |

Inventories |

| 6 | | 11,467 | | 17,641 |

Other current assets |

| | | 7,027 | | 6,621 |

| | | | 96,409 | | 141,252 |

Non-current assets |

|

| |

| |

|

| | | | | | |

Investments in associates |

| 7 | | 8,353 | | 8,833 |

Other investments |

| 7 | | 22,516 | | 33,819 |

Mining interests |

| 8 | | 603,205 | | 580,479 |

Property, plant and equipment |

| 9 | | 114,931 | | 111,696 |

Exploration and evaluation |

| 10 | | 67,988 | | 55,126 |

Other assets | | 11 | | 39,861 | | 36,994 |

| | | | 953,263 | | 968,199 |

Liabilities |

|

| |

| |

|

| | | | | | |

Current liabilities |

|

| |

| |

|

| | | | | | |

Accounts payable and accrued liabilities |

| 12 | | 22,436 | | 31,106 |

Lease liabilities |

| | | 493 | | 1,208 |

Contract liability |

| 15 | | 361 | | 941 |

Current portion of long-term debt |

| 13 | | 12,349 | | 4,663 |

Environmental rehabilitation provision |

| 16 | | 19,000 | | 9,738 |

Deferred consideration and contingent payments |

| 14 | | 3,380 | | 3,386 |

| | | | 58,019 | | 51,042 |

Non-current liabilities |

|

| |

| |

|

| | | | | | |

Long term debt |

| 13 | | 6,092 | | 12,256 |

Lease liabilities |

| | | 755 | | 962 |

Contract liability |

| 15 | | 63,883 | | 54,252 |

Environmental rehabilitation provision |

| 16 | | 53,678 | | 66,032 |

Warrant liability | | 17 | | 9,322 | | 16,395 |

Deferred Consideration and contingent payments |

| 14 | | 10,578 | | 13,252 |

Deferred income taxes |

| | | 21,881 | | 23,574 |

Other non-current liabilities | | | | 863 | | — |

| | | | 225,071 | | 237,765 |

Equity |

|

| |

| |

|

| | | | | | |

Share capital |

| 18 | | 1,079,640 | | 1,032,786 |

Warrants |

| 18 | | 11,859 | | 1,573 |

Contributed surplus | | | | 17,304 | | 12,857 |

Accumulated other comprehensive income | | | | (7,904) | | 7,166 |

Deficit | | | | (372,707) | | (323,948) |

| | | | 728,192 | | 730,434 |

| | | | 953,263 | | 968,199 |

Going concern (Note 1)

APPROVED ON BEHALF OF THE BOARD | |

(signed) Sean Roosen, Director | (signed), Charles Page, Director |

The notes are an integral part of these condensed consolidated financial statements.

2

Osisko Development Corp.

Consolidated Statements of Loss

For the three and nine months ended September 30, 2023 and 2022

(Unaudited)

(Expressed in thousands of Canadian dollars, except per share amounts)

| | | | Three months ended | | Nine months ended | ||||

| | | | September 30, | | September 30, | ||||

| | | | 2023 | | 2022 | | 2023 | | 2022 |

|

| Notes |

| $ |

| $ |

| $ |

| $ |

Revenues |

| | | 10,421 | | 22,791 | | 24,719 | | 44,821 |

Operating expenses |

|

| | | | | | | | |

Cost of sales |

| 20 | | (10,087) | | (23,435) | | (25,900) | | (44,811) |

Other operating costs |

| 20 | | (6,759) | | (21,444) | | (20,788) | | (57,292) |

General and administrative |

| 21 | | (9,382) | | (8,710) | | (29,926) | | (26,451) |

Exploration and evaluation, net of tax credits |

| | | (646) | | (90) | | (1,686) | | (367) |

Impairment of assets |

| | | — | | (81,000) | | — | | (81,000) |

Operating loss |

| | | (16,453) | | (111,888) | | (53,581) | | (165,100) |

Finance costs |

| | | (3,748) | | (1,410) | | (10,594) | | (3,625) |

Share of loss of associates |

| | | (291) | | (103) | | (480) | | (575) |

Change in fair value of warrant liability |

| 17 | | 12,978 | | 2,565 | | 6,968 | | 21,946 |

Other income, net |

| 22 | | 849 | | 7,104 | | 13,416 | | 21,280 |

Income (loss) before income taxes |

| | | (6,665) | | (103,732) | | (44,271) | | (126,074) |

| | | | | | | | | | |

Income tax recovery (expense) |

| | | (458) | | 1 | | 493 | | (1,489) |

Net loss |

| | | (7,123) | | (103,731) | | (43,778) | | (127,563) |

| | | | | | | | | | |

Basic and diluted loss per share |

| | | — | | — | | — | | — |

Weighted average number of shares outstanding-basic and diluted |

| 23 | | (0.08) | | (1.37) | | (0.53) | | (2.13) |

The notes are an integral part of these condensed consolidated financial statements.

3

Osisko Development Corp.

Consolidated Statements of Comprehensive Loss

For the three and nine months ended September 30, 2023 and 2022

(Unaudited)

(Expressed in thousands of Canadian dollars)

| | Three months ended | | Nine months ended | ||||

| | September 30, | | September 30, | ||||

|

| 2023 |

| 2022 |

| 2023 |

| 2022 |

|

| $ |

| $ | | $ | | $ |

| | | | | | | | |

Net loss | | (7,123) | | (103,731) | | (43,778) | | (127,563) |

| | | | | | | | |

Other comprehensive income (loss) | |

| |

| |

| |

|

| | | | | | | | |

Items that will not be reclassified to the consolidated statements of loss | |

| |

| |

| |

|

| | | | | | | | |

Changes in fair value of financial assets at fair value through comprehensive income (loss) | | (2,494) | | (3,349) | | (9,555) | | (5,223) |

Income tax effect | | 1,112 | | 266 | | 1,112 | | 299 |

Share of other comprehensive loss of associates | | — | | — | | — | | (294) |

| | | | | | | | |

Items that may be reclassified to the consolidated statements of loss | |

| |

| |

| |

|

| | | | | | | | |

Currency translation adjustments | | 4,480 | | 14,413 | | (7,945) | | 17,657 |

Other comprehensive income (loss) | | 3,098 | | 11,330 | | (16,388) | | 12,439 |

Comprehensive loss | | (4,025) | | (92,401) | | (60,166) | | (115,124) |

The notes are an integral part of these condensed consolidated financial statements.

4

Osisko Development Corp.

Consolidated Statements of Cash Flows

For the three and nine months ended September 30, 2023 and 2022

(Unaudited)

(Expressed in thousands of Canadian dollars)

| |

| | Three months ended | | Nine months ended | ||||

| | | | September 30, | | September 30, | ||||

|

| |

| 2023 |

| 2022 |

| 2023 |

| 2022 |

| | Notes | | $ | | $ | | $ | | $ |

Operating activities |

| | | | | | | | | |

Net loss |

| | | (7,123) | | (103,731) | | (43,778) | | (127,563) |

Adjustments for: |

| | | | | | | | | |

Share-based compensation |

| | | 1,865 | | 2,192 | | 6,263 | | 5,389 |

Depreciation |

| 21 | | 2,646 | | 2,569 | | 9,030 | | 9,883 |

Finance Costs |

| | | 3,766 | | 2,411 | | 10,616 | | 3,625 |

Gain on deemed disposal of associate |

| | | — | | — | | — | | (11,854) |

Share of loss of associates |

| 7 | | 291 | | 104 | | 480 | | 576 |

Change in fair value of financial assets at fair value through profit and loss |

| 7 | | 25 | | — | | (6) | | 384 |

Change in fair value of warrant liability |

| | | (12,978) | | (2,561) | | (6,968) | | (21,942) |

Unrealized Foreign exchange gain | | | | 449 | | (8,336) | | (9,776) | | (10,433) |

Deferred income tax expense (recovery) |

| | | 458 | | — | | (493) | | 1,490 |

Impairment of assets | | | | — | | 81,000 | | | | 81,000 |

Premium on flow-through shares |

| | | — | | — | | — | | (914) |

Cumulative catch-up adjustment on contract liability |

| | | (456) | | — | | (192) | | — |

Proceeds from contract liability |

| | | (384) | | 26,112 | | (1,824) | | 26,112 |

Other |

| | | 3,114 | | — | | 3,246 | | — |

Environmental rehabilitation obligations paid | | | | (1,119) | | (36) | | (2,044) | | 1,779 |

Net cash flows used in operating activities before changes in non-cash working capital items |

| | | (9,446) | | (276) | | (35,446) | | (42,468) |

Changes in non-cash working capital items |

| 24 | | 365 | | 13,360 | | 1,797 | | 3,466 |

Net cash flows used in operating activities |

| | | (9,081) | | 13,084 | | (33,649) | | (39,002) |

Investing activities |

| | | | | | | | | |

Additions to Mining interests |

| | | (6,215) | | (12,820) | | (30,800) | | (37,746) |

Additions to Property, plant and equipment |

| | | (1,549) | | (5,541) | | (12,983) | | (14,619) |

Additions to Exploration and evaluation expenses | | | | (3,984) | | (1,555) | | (13,694) | | (2,241) |

Proceeds on disposals of investments |

| 7 | | 2,445 | | 353 | | 3,447 | | 21,634 |

Cash payments on deferred consideration and contingent payments |

| | | — | | — | | (334) | | — |

Acquisition of other investments | | | | — | | (212) | | — | | (212) |

Acquisition of Tintic, net of cash acquired |

| | | — | | — | | — | | (66,627) |

Reclamation deposit |

| | | 4,772 | | — | | 4,748 | | (13,371) |

Other |

| | | — | | (765) | | — | | (1,803) |

Net cash flows used in investing activities |

| | | (4,531) | | (20,540) | | (49,616) | | (114,985) |

Financing activities |

| | | | | | | | | |

Proceeds from equity financings |

| | | — | | — | | 51,756 | | 255,543 |

Other issuance of common shares |

| | | 33 | | 114 | | 102 | | 114 |

Share issue expense |

| | | (91) | | — | | (3,365) | | (7,238) |

Capital payments on lease liabilities |

| | | (105) | | (396) | | (927) | | (6,295) |

Long term debt | | 13 | | — | | 1,202 | | 5,878 | | 8,738 |

Repayment of long–term debt |

| 13 | | (1,541) | | (1,082) | | (4,339) | | (3,662) |

Withholding taxes on settlement of restricted units |

| | | — | | — | | (337) | | — |

Net cash flows (used) provided by financing activities |

| | | (1,704) | | (162) | | 48,768 | | 247,200 |

Increase (decrease) in cash and cash equivalents before impact of exchange rate |

| | | (15,316) | | (7,618) | | (34,497) | | 93,213 |

Effects of exchange rate changes on cash and cash equivalents |

| | | (90) | | 4,454 | | 51 | | 6,518 |

Increase (decrease) in cash and cash equivalents |

| | | (15,406) | | (3,164) | | (34,446) | | 99,731 |

Cash and cash equivalents – Beginning of period |

| | | 86,904 | | 136,302 | | 105,944 | | 33,407 |

Cash and cash equivalents – end of period |

| | | 71,498 | | 133,138 | | 71,498 | | 133,138 |

The notes are an integral part of these condensed consolidated financial statements.

5

Osisko Development Corp.

Consolidated Statements of Changes in Equity

For the nine months ended September 30, 2023

(Unaudited)

(Expressed in thousands of Canadian dollars except number of shares)

| | | | Number of | | | | | | | | Accumulated | | | | |

| | | | common | | | | | | | | other | | | | |

| | | | shares | | Share | | | | Contributed | | comprehensive | | | | |

|

| Notes |

| outstanding |

| capital |

| Warrants | | Surplus | | income (loss) | | Deficit | | Total |

| | | | | | ($) | | ($) | | ($) | | ($) | | ($) | | ($) |

Balance – January 1, 2023 |

| 18 |

| 75,629,849 |

| 1,032,786 | | 1,573 |

| 12,857 | | 7,166 | | (323,948) | | 730,434 |

| | | | | | | | | | | | | | | | |

Net loss |

| | | — | | — | | — | | — | | — | | (43,778) | | (43,778) |

Other comprehensive loss, net |

| | | — | | — | | — | | — | | (16,388) | | — | | (16,388) |

Comprehensive loss |

| | | — | | — | | — | | — | | (16,388) | | (43,778) | | (60,166) |

Transfer of realized loss on financial assets at fair value through other comprehensive loss, net of taxes |

| | | — | | — | | — | | — | | 1,318 | | (1,277) | | 41 |

Bought deal financing |

| 18 | | 7,841,850 | | 45,545 | | 6,211 | | — | | — | | — | | 51,756 |

Shares issued for the settlement of Deferred consideration | | 18 | | 454,026 | | 2,986 | | — | | — | | — | | — | | 2,986 |

Shares issued to Williams Lake First Nation |

| 18 | | 10,000 | | 75 | | — | | — | | — | | — | | 75 |

Share issue expense |

| 18 | | — | | (2,988) | | (408) | | — | | — | | — | | (3,396) |

Change in fair value related to warrants modification |

| 18 | | — | | — | | 4,483 | | — | | — | | (4,483) | | — |

Share-based compensation | | | | | | | | | | | | | | | | |

-Share options |

| | | — | | — | | — | | 3,250 | | — | | — | | 3,250 |

-Restricted and deferred share units |

| | | — | | — | | — | | 3,286 | | — | | — | | 3,286 |

Shares issued - employee share purchase plan |

| | | 44,184 | | 263 | | — | | — | | — | | — | | 263 |

Share issued from RSU/DSU redemption |

| | | 44,466 | | 973 | | — | | (2,089) | | — | | 779 | | (337) |

Balance – September 30, 2023 |

| | | 84,024,375 | | 1,079,640 | | 11,859 | | 17,304 | | (7,904) | | (372,707) | | 728,192 |

The notes are an integral part of these consolidated financial statements.

6

Osisko Development Corp.

Consolidated Statements of Changes in Equity

For the nine months ended September 30, 2022

(Unaudited)

(Expressed in thousands of Canadian dollars except number of shares)

|

| |

| Number of |

|

|

|

| | | | Accumulated | | | | |

| | | | common | | | | | | | | other | | | | |

| | | | shares | | Share | | | | Contributed | | comprehensive | | | | |

| | Notes | | outstanding | | capital | | Warrants | | Surplus | | income (loss) | | Deficit | | Total |

| | | | | | ($) | | ($) | | ($) | | ($) | | ($) | | ($) |

Balance – January 1, 2022 |

| 18 | | 44,400,854 |

| 714,373 |

| — | | 6,436 | | 6,764 | | (143,371) | | 584,202 |

| | | | | | | | | | | | | | | | |

Net loss |

| | | — |

| — |

| — | | — | | — | | (127,563) | | (127,563) |

Other comprehensive loss |

| | | — |

| — |

| — | | — | | 12,439 | | — | | 12,439 |

Comprehensive income |

| | | — |

| — |

| — | | — | | 12,439 | | (127,563) | | (115,124) |

Transfer of realized loss on financial assets at fair value through other comprehensive income, net of taxes | | | | — | | — | | — | | — | | (11,693) | | 11,693 | | — |

Private placements – Brokered |

| 18 | | 7,752,917 |

| 101,873 |

| 1,628 | | — | | — | | — | | 103,501 |

Private placements – Non-Brokered |

| 18 |

| 11,363,933 |

| 112,207 |

| — | | — | | — | | — | | 112,207 |

Share-issue costs |

| |

| — |

| (6,231) |

| (55) | | — | | — | | — | | (6,286) |

Share-based compensation |

| |

| | | | | | | | | | | | | |

-Share options |

| | | — |

| — |

| — | | 2,511 | | — | | — | | 2,511 |

-Restricted and deferred share units |

| | | — |

| — |

| — | | 3,166 | | — | | — | | 3,166 |

Shares issued - employee share purchase plan |

| | | 25,778 |

| 310 |

| — | | — | | — | | — | | 310 |

Shares issued on Acquisition of Tintic |

| | | 12,049,449 |

| 109,657 |

| — | | — | | — | | — | | 109,657 |

Share issued from RSU/DSU Redemption |

| | | 27,651 |

| 608 |

| — | | (1,320) | | — | | 406 | | (306) |

Balance – September 30, 2022 |

| | | 75,620,582 |

| 1,032,797 |

| 1,573 | | 10,793 | | 7,510 | | (258,835) | | 793,838 |

The notes are an integral part of these consolidated financial statements.

7

Osisko Development Corp.

Notes to the Condensed Consolidated Financial Statements

For the three and nine months ended September 30, 2023 and 2022

(Unaudited)

(Tabular amounts expressed in thousands of Canadian dollars, except per share amounts)

1. | Nature of operations and going concern |

Osisko Development Corp. (“Osisko Development” or the “Company”) is a mineral exploration and development company focused on the acquisition, exploration and development of precious metals resource properties in North America. The common shares of Osisko Development began trading under the symbol ODV on the TSX Venture Exchange (“TSX-V”) on December 2, 2020 and on the New York Stock Exchange (“NYSE”) on May 27, 2022. Osisko Development is focused on exploring and developing its mining assets, including the Cariboo Gold Project in British Columbia, the San Antonio gold project in Mexico and the Trixie test mine in the USA.

The Company’s registered and business address is 1100, avenue des Canadiens-de-Montréal, suite 300, Montreal, Québec. The common shares outstanding presented have been retroactively adjusted to reflect the effect of the 3:1 share consolidation that took place on May 4, 2022. Common share warrants and per share amounts have been adjusted retroactively for the 3:1 share consolidation unless noted otherwise.

On September 30, 2023, the former parent Company, Osisko Gold Royalties (“OGR”) held an interest of 39.7% (compared to 44.1% as at December 31, 2022) in Osisko Development Corp.

The principal subsidiaries of the Company and their geographic locations at September 30, 2023 were as follows:

Entity |

| Jurisdiction |

| % ownership |

|

Barkerville Gold Mines Ltd. (“Barkerville”) |

| British Columbia |

| 100 | % |

Sapuchi Minera, S. de R.L. de C.V. (“Sapuchi”) |

| Mexico |

| 100 | % |

Tintic Consolidated Metals LLC (“Tintic”) |

| USA |

| 100 | % |

These condensed consolidated financial statements have been prepared on the basis of accounting principles applicable to a going concern, which contemplates the realization of assets and settlement of liabilities in the normal course of business as they come due. In assessing whether the going concern assumption is appropriate, Management takes into account all available information about the future, which is at least, but not limited to twelve months from the end of the reporting period. As at September 30, 2023, the Company’s working capital was $38.4 million, which included cash and cash equivalent balance of $71.5 million. The Company also has an accumulated deficit of $373 million and incurred a loss of $44 million for the nine month period ended September 30, 2023

The working capital position as at September 30, 2023 will not be sufficient to meet the Company’s obligations, commitments and forecasted expenditures up to the period ending September 30, 2024. Management is aware, in making its assessment, of material uncertainties related to events and conditions that may cast a substantial doubt upon the Company's ability to continue as a going concern as described in the preceding paragraph, and accordingly, the appropriateness of the use of accounting principles applicable to a going concern. These condensed consolidated financial statements do not reflect the adjustments to the carrying values of assets and liabilities, expenses and financial position classifications that would be necessary if the going concern assumption was not appropriate. These adjustments could be material.

The Company’s ability to continue future operations and fund its planned activities is dependent on Management’s ability to secure additional financing in the future, which may be completed in several ways including, but not limited to, a combination of selling additional investments from its portfolio, project debt finance, offtake or royalty financing and other capital market alternatives. Failure to secure future financings may impact and/or curtail the planned activities for the Company, which may include, but are not limited to, the suspension of certain development activities and the disposal of certain investments to generate liquidity. While Management has been successful in securing financing in the past, there can be no assurance that it will be able to do so in the future or that these sources of funding or initiatives will be available to the Company or that they will be available on terms which are acceptable to the Company. If Management is unable to obtain new funding, the Company may be unable to continue its operations, and amounts realized for assets might be less than the amounts reflected in these condensed consolidated financial statements.

8

Osisko Development Corp.

Notes to the Condensed Consolidated Financial Statements

For the three and nine months ended September 30, 2023 and 2022

(Unaudited)

(Tabular amounts expressed in thousands of Canadian dollars, except per share amounts)

2. | Basis of presentation and Statement of compliance |

These condensed interim consolidated financial statements have been prepared in accordance with the International Financial Reporting Standards as issued by the International Accounting Standards Board (“IASB”) (“IFRS”) and as applicable to the preparation of interim financial statements, including IAS 34 Interim Financial Reporting. Accordingly, certain disclosures included in the annual financial statements prepared in accordance with IFRS have been condensed or omitted and these condensed interim consolidated financial statements should be read in conjunction with the Company’s audited consolidated financial statements for the year ended December 31, 2022. The accounting policies, methods of computation and presentation applied in the preparation of these condensed interim consolidated financial statements are consistent with those of the previous financial year, unless otherwise noted.

. The Board of Directors approved these condensed interim consolidated financial statements on November 8, 2023.

3. | New accounting standards and policies |

New accounting policy

Cash and cash equivalents include cash on hand and short-term highly liquid investments with an initial maturity of three months or less that are readily convertible to known amounts of cash and which are exposed to an insignificant risk of changes in value.

New accounting standards and amendments

The following pronouncements to existing accounting standards were effective on January 1, 2023:

| • | Amendment to IAS 12 Income taxes requires companies to recognize deferred tax on particular transactions that, on initial recognition, give rise to equal amounts of taxable and deductible temporary differences. |

| • | Narrow scope amendment to IAS 1 Presentation of Financial Statements to improve accounting policy disclosures. |

| • | Narrow scope amendment to IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors to distinguish changes in accounting estimates from changes in accounting policies. |

No material impact was identified in connection with the adoption of these amendments.

New accounting standards, amendments and interpretations not yet adopted

The Company has not yet adopted certain standards, interpretations to existing standards and amendments which have been issued but have an effective date of later than December 31, 2023. Some of these updates are not expected to have any significant impact on the Company and are therefore not discussed herein.

Classification of liabilities as current or non-current (Amendments to IAS 1)

The IASB has published amendments to IAS 1 (Classification of liabilities as current or non-current and non-current liabilities with covenants) which clarify the guidance on whether a liability should be classifies as either current or non-current. The amendments:

| • | Clarify that the classification of liabilities as current or non-current should only be based on rights that are in place “at the end of the reporting period”; |

| • | Clarify that classification is unaffected by intentions or expectations about whether an entity will exercise its right to defer settlement of a liability; and |

9

Osisko Development Corp.

Notes to the Condensed Consolidated Financial Statements

For the three and nine months ended September 30, 2023 and 2022

(Unaudited)

(Tabular amounts expressed in thousands of Canadian dollars, except per share amounts)

| • | Make clear that settlement includes transfers to the counterparty of cash, equity instruments, other assets or services that result in extinguishment of the liability. |

In addition, the IASB confirmed that only covenants with which an entity must comply on or before the reporting date affect the classification of a liability as current or non-current. Covenants with which an entity must comply within twelve months of the reporting date (“Future Covenants”) do not affect a liability’s classification at the reporting date. However, when non-current liabilities are subject to Future Covenants, entities will need to disclose information in the notes that enables users of the condensed consolidated financial statements to understand the risk that the liability could become repayable within twelve months of the reporting date.

The amendments to IAS 1 are effective for annual periods beginning on or after January 1, 2024 and should be applied retrospectively in accordance with IAS 8. The adoption of the amendments to IAS 1 is expected to impact the classification of the Warrant liability from non-current to current liability.

4. | Cash and cash equivalents |

As at September 30, 2023 and December 31 2022, the consolidated cash and cash equivalents position was as follows:

|

| September 30, | | December 31, |

| | 2023 |

| 2022 |

|

| $ |

| $ |

Cash and cash equivalents held in Canadian dollars | | 29,058 | | 32,444 |

| | | | |

Cash and cash equivalents held in U.S. dollars | | 31,355 | | 54,242 |

Cash and cash equivalents held in U.S. dollars (Canadian equivalent) | | 42,392 | | 73,465 |

| | | | |

Cash held and cash equivalents in Mexican Pesos | | 645 | | 565 |

Cash held and cash equivalents in Mexican Pesos (Canadian equivalent) | | 48 | | 35 |

Total cash and cash equivalents | | 71,498 | | 105,944 |

5. | Amounts receivable |

|

| September 30, | | December 31, |

| | 2023 |

| 2022 |

|

| $ |

| $ |

Trade receivables | | 3,711 | | 1,777 |

Exploration tax credits | | 1,579 | | 8,360 |

Sales taxes | | 743 | | 889 |

Interest income receivable | | 133 | | 20 |

Other | | 251 | | — |

| | 6,417 | | 11,046 |

10

Osisko Development Corp.

Notes to the Condensed Consolidated Financial Statements

For the three and nine months ended September 30, 2023 and 2022

(Unaudited)

(Tabular amounts expressed in thousands of Canadian dollars, except per share amounts)

6. | Inventories |

|

| September 30, | | December 31, |

| | 2023 |

| 2022 |

|

| $ |

| $ |

Ore in stockpiles | | — | | 5,943 |

Tailings | | 4,135 | | 2,616 |

Gold-in-circuit inventory | | 637 | | 4,451 |

Refined precious metals | | 1,139 | | 37 |

Supplies and other | | 5,556 | | 4,594 |

Total inventories | | 11,467 | | 17,641 |

Refined precious metals, gold-in-circuit and ore in stockpiles are measured at the lower of weighted average production cost and net realizable value. Net realizable value is calculated as the difference between the estimated selling price and estimated costs to complete processing into a saleable form plus variable selling expenses. For the nine-month period ended September 30, 2023, an amount of $5,625,000 was recorded to evaluate the inventories to net realizable value. Production costs include the cost of materials, labour, mine site production overheads and depreciation to the applicable stage of processing.

7. | Investments in associates and other investments |

Investments in associates

|

| September 30, | | December 31, |

| | 2023 |

| 2022 |

|

| $ |

| $ |

Balance – Beginning of period | | 8,833 | | 12,964 |

Transfer to Other investments | | — | | (15,344) |

Share of loss and comprehensive loss, net | | (480) | | (641) |

Gain on deemed disposal(i) | | — | | 11,854 |

Balance – End of period | | 8,353 | | 8,833 |

| (i) | In 2022, the gain on deemed disposal is related to an investment in an associate that was transferred to other assets as the Company has considered that it has lost its significant influence over the investee. |

11

Osisko Development Corp.

Notes to the Condensed Consolidated Financial Statements

For the three and nine months ended September 30, 2023 and 2022

(Unaudited)

(Tabular amounts expressed in thousands of Canadian dollars, except per share amounts)

Other investments

|

| September 30, | | December 31, |

| | 2023 |

| 2022 |

|

| $ |

| $ |

Fair value through profit or loss (warrants & convertible loan) | |

| |

|

Balance – Beginning of period | | 18 | | 6,952 |

Acquisitions | | — | | 4,438 |

Exercises | | — | | (117) |

Acquisition of Tintic | | — | | (10,827) |

Change in fair value | | 6 | | (480) |

Foreign exchange | | — | | 52 |

Balance – End of period | | 24 | | 18 |

| | | | |

Fair value through other comprehensive income (shares) | | | |

|

Balance – Beginning of period | | 33,801 | | 42,564 |

Acquisitions | | — | | 329 |

Consideration received from disposal of exploration properties | | 1,694 | | — |

Disposals | | (3,447) | | (22,585) |

Change in fair value | | (9,556) | | (1,849) |

Transfer from associates | | — | | 15,342 |

Balance – End of period | | 22,492 | | 33,801 |

Total | | 22,516 | | 33,819 |

Other investments comprise of common shares and warrants, almost exclusively from publicly traded companies.

12

Osisko Development Corp.

Notes to the Condensed Consolidated Financial Statements

For the three and nine months ended September 30, 2023 and 2022

(Unaudited)

(Tabular amounts expressed in thousands of Canadian dollars, except per share amounts)

8. | Mining interests |

|

| September 30, | | December 31, |

| | 2023 |

| 2022 |

|

| $ |

| $ |

Cost – Beginning of period | | 583,669 | | 475,621 |

Acquisition of Tintic | | — | | 169,175 |

Additions | | 22,731 | | 49,297 |

Mining tax credit | | 152 | | (6,404) |

Asset retirement obligation | | (4,532) | | 9,248 |

Depreciation capitalized | | 3,442 | | 1,141 |

Share-based compensation capitalized | | 217 | | 530 |

Impairment | | — | | (140,000) |

Other adjustments | | — | | 5,579 |

Currency translation adjustments | | 2,225 | | 19,482 |

Cost – End of period | | 607,904 | | 583,669 |

Accumulated depreciation – Beginning of period | | 3,190 | | — |

Depreciation | | 1,036 | | 2,964 |

Currency translation adjustments | | 473 | | 226 |

Accumulated depreciation – End of period | | 4,699 | | 3,190 |

| | | | |

Cost | | 607,904 | | 583,669 |

Accumulated depreciation | | (4,699) | | (3,190) |

Net book value | | 603,205 | | 580,479 |

13

Osisko Development Corp.

Notes to the Condensed Consolidated Financial Statements

For the three and nine months ended September 30, 2023 and 2022

(Unaudited)

(Tabular amounts expressed in thousands of Canadian dollars, except per share amounts)

9. | Property, plant and equipment |

|

| |

| Machinery |

| |

|

|

|

|

| | Land and | | and | | Construction- | | September 30, | | December 31, |

| | Buildings | | Equipment | | in-progress | | 2023 | | 2022 |

|

| $ |

| $ |

| $ |

| $ |

| $ |

Cost– Beginning of period | | 27,980 | | 80,208 | | 23,721 | | 131,909 | | 93,241 |

Acquisition of Tintic | | — | | — | | — | | — | | 13,054 |

Additions | | 1,122 | | 7,989 | | 3,722 | | 12,833 | | 29,409 |

Disposals | | — | | (126) | | (101) | | (227) | | (1,351) |

Write-off | | (108) | | (138) | | — | | (246) | | (5,455) |

Other adjustments | | (220) | | (92) | | — | | (312) | | (896) |

Transfers | | 2,030 | | 690 | | (2,720) | | — | | — |

Currency translation adjustments | | 67 | | 1,938 | | 1,217 | | 3,222 | | 3,907 |

Cost – End of period | | 30,871 | | 90,469 | | 25,839 | | 147,179 | | 131,909 |

| | | | | | | | | | |

Accumulated depreciation – Beginning of period | | 4,468 | | 15,745 | | — | | 20,213 | | 9,529 |

Depreciation | | 2,312 | | 9,003 | | — | | 11,315 | | 12,869 |

Disposal | | — | | (19) | | — | | (19) | | (192) |

Write-off | | (13) | | (78) | | — | | (91) | | (2,687) |

Currency translation adjustments | | 55 | | 775 | | — | | 830 | | 694 |

Accumulated depreciation – End of period | | 6,822 | | 25,426 | | — | | 32,248 | | 20,213 |

| | | | | | | | | | |

Net book value | | 24,049 | | 65,043 | | 25,839 | | 114,931 | | 111,696 |

Property, plant and equipment includes right-of-use assets with a net carrying value of $3.3 million as at September 30, 2023 ($3.8 million as at December 31, 2022).

10. | Exploration and evaluation |

| | September 30, | | December 31, |

| | 2023 | | 2022 |

|

| ($) |

| ($) |

Net book value - Beginning of period |

| 55,126 |

| 3,635 |

Acquisition of Tintic |

| — |

| 38,508 |

Additions |

| 12,562 |

| 10,786 |

Depreciation capitalized |

| 337 |

| 80 |

Other adjustments |

| — |

| (460) |

Currency translation adjustments |

| (37) |

| 2,577 |

Net book value – End of period |

| 67,988 |

| 55,126 |

| | | | |

Cost |

| 168,195 |

| 155,333 |

Accumulated impairment |

| (100,207) |

| (100,207) |

Net book value – End of period |

| 67,988 |

| 55,126 |

14

Osisko Development Corp.

Notes to the Condensed Consolidated Financial Statements

For the three and nine months ended September 30, 2023 and 2022

(Unaudited)

(Tabular amounts expressed in thousands of Canadian dollars, except per share amounts)

11. Other Assets

|

| September 30, | | December 31, |

| | 2023 |

| 2022 |

|

| $ |

| $ |

Sales tax recoverable | | 20,411 | | 17,467 |

Reclamation deposits | | 12,647 | | 16,761 |

Deferred financing fees | | 94 | | — |

Other | | 6,709 | | 2,766 |

|

| 39,861 |

| 36,994 |

12. | Accounts payable and accrued liabilities |

|

| September 30, | | December 31, |

| | 2023 | | 2022 |

|

| $ |

| $ |

Trade payables |

| (11,826) |

| 18,057 |

Other payables |

| (5,053) |

| 5,005 |

Income taxes payable |

| — |

| 716 |

Accrued liabilities |

| (5,557) |

| 7,328 |

|

| (22,436) |

| 31,106 |

13. | Long-term debt |

|

| September 30, | | December 31, |

| | 2023 |

| 2022 |

|

| ($) |

| ($) |

Balance – Beginning of period |

| 16,919 |

| 3,764 |

Additions- mining equipment financing |

| 5,878 |

| 17,772 |

Repayment of liabilities |

| (4,337) |

| (4,860) |

Currency translation adjustments |

| (19) |

| 243 |

Balance – End of period |

| 18,441 |

| 16,919 |

| | | | |

Current long–term debt |

| 12,349 |

| 4,663 |

Non-current long–term debt |

| 6,092 |

| 12,256 |

|

| 18,441 |

| 16,919 |

15

Osisko Development Corp.

Notes to the Condensed Consolidated Financial Statements

For the three and nine months ended September 30, 2023 and 2022

(Unaudited)

(Tabular amounts expressed in thousands of Canadian dollars, except per share amounts)

14. | Deferred consideration and contingent payments |

|

| September 30, | | December 31, |

| | 2023 |

| 2022 |

|

| ($) |

| ($) |

Balance – Beginning of period |

| 16,638 |

| — |

Additions |

| — |

| 15,109 |

Interest Capitalized |

| 725 |

| 577 |

Repayment |

| (334) |

| — |

Settlement |

| (2,986) |

| — |

Foreign exchange |

| (85) |

| 952 |

Balance – End of period |

| 13,958 |

| 16,638 |

| | | | |

Current portion of deferred consideration and contingent payments |

| 3,380 |

| 3,386 |

Non-current portion of deferred consideration and contingent payments |

| 10,578 |

| 13,252 |

|

| 13,958 |

| 16,638 |

15. | Royalty and Contract liability |

OGR and through its wholly owned subsidiaries, holds a 5% NSR royalty on the Cariboo Gold Project (“Cariboo”) and Bonanza Ledge properties, owned by Barkerville.The Cariboo and Bonanza Ledge properties 5% NSR royalty is perpetual and is secured by a debenture on all of Barkerville movable and immovable assets, including Barkerville’s interest in the property and mineral rights, in an amount of not less than $150 million. The security shall be first ranking, subject to permitted encumbrances.

On November 20, 2020, the Company’s wholly owned subsidiary Sapuchi completed a gold and silver stream agreement with Osisko Bermuda Ltd, a subsidiary of OGR, for US$15.0 million ($19.1 million). An amount of US$10.5 million was contributed in November 2020 and the remaining US$4.5 million was paid in February 2021.

Under the terms of the stream agreement, Osisko Bermuda Ltd will purchase 15% of the payable gold and silver from the San Antonio gold project at a price equal to 15% of the daily per ounce gold and silver market price. The initial term of the stream agreement is for 40 years and can be renewed for successive 10-year periods. The stream is also secured with (i) a first priority lien in all of the collateral now owned or hereafter acquired; (ii) a pledge by Osisko Development of its shares of Sapuchi Minera Holdings Two B.V. and (iii) a guarantee by Osisko Development. The interest rate used to calculate the accretion on the contract liability’s financing component is 24%.

On September 26, 2022, Tintic completed a metals stream agreement with Osisko Bermuda Ltd, for US$20 million ($26.1 million).

Under the terms of the stream agreement, Osisko Bermuda Ltd will receive 2.5% of the refined metal production from Tintic until 27,150 ounces of refined gold have been delivered, and thereafter Osisko Bermuda Ltd will receive 2.0% of the refined metal production from Tintic. Osisko Bermuda Ltd will make ongoing cash payments to Tintic equal to 25% of the applicable spot metal price on the business day immediately preceding the date of delivery for each ounce of refined metal delivered pursuant to the stream agreement. The interest rate used to calculate the accretion on the contract liability’s financing component is 5%.

16

Osisko Development Corp.

Notes to the Condensed Consolidated Financial Statements

For the three and nine months ended September 30, 2023 and 2022

(Unaudited)

(Tabular amounts expressed in thousands of Canadian dollars, except per share amounts)

The movement of the contract liability is as follows:

|

| September 30, | | December 31, |

| | 2023 |

| 2022 |

|

| ($) |

| ($) |

Balance – Beginning of period |

| 55,193 |

| 24,820 |

Deposits |

| — |

| 26,112 |

Proceeds from contract liability | | (1,822) | | (2,792) |

Accretion on the contract liability’s financing component |

| 7,532 |

| 7,377 |

Cumulative catch-up adjustment |

| (204) |

| (4,362) |

Currency translation adjustment |

| 3,545 |

| 4,038 |

Balance – End of period |

| 64,244 |

| 55,193 |

| | | | |

Current liabilities |

| 361 |

| 941 |

Non-current liabilities |

| 63,883 |

| 54,252 |

|

| 64,244 |

| 55,193 |

Under IFRS 15, the stream agreements are considered to have a significant financing component. The Company therefore records notional non-cash interest.

16. | Environmental rehabilitation provision |

|

| September 30, | | December 31, |

| | 2023 |

| 2022 |

|

| ($) |

| ($) |

Balance – Beginning of period |

| 75,770 |

| 53,236 |

Acquisition of Tintic |

| — |

| 4,599 |

New liabilities |

| (137) |

| 22,353 |

Revision of estimates |

| (4,318) |

| (5,637) |

Accretion expense |

| 2,242 |

| 3,223 |

Settlement of liabilities / payment of liabilities |

| (2,042) |

| (3,409) |

Currency translation adjustment |

| 1,163 |

| 1,405 |

Balance – End of period |

| 72,678 |

| 75,770 |

| | | | |

Current liabilities |

| 19,000 |

| 9,738 |

Non-current liabilities |

| 53,678 |

| 66,032 |

|

| 72,678 |

| 75,770 |

The environmental rehabilitation provision represents the legal and contractual obligations associated with the eventual closure of the Company’s mining interests, property, plant and equipment and exploration and evaluation assets. As at September 30, 2023, the estimated inflation-adjusted undiscounted cash flows required to settle the environmental rehabilitation amounts to $84.9 million. The weighted average actualization rate used is 4.75% and the disbursements are expected to be made between 2023 and 2030 as per the current closure plans.

17. | Warrant Liability |

The Company completed a non-brokered private placement, issuing non-brokered subscription receipts on May 27, 2022, each non-brokered subscription receipt holder received one unit comprised of one common share and one common share purchase warrant, upon the listing of Osisko Development’s common shares on the NYSE. Each warrant entitling the holder to purchase one additional common share at a price of USD$18.00 per common share for

17

Osisko Development Corp.

Notes to the Condensed Consolidated Financial Statements

For the three and nine months ended September 30, 2023 and 2022

(Unaudited)

(Tabular amounts expressed in thousands of Canadian dollars, except per share amounts)

a period of 5 years from the date of issue. On March 17, 2023, the Company received the required approvals to reduce the exercise price of the common share purchase warrants issued in 2022 under the non-brokered private placements from US$18.00 to US$10.70 per share.

These warrants include an embedded derivative as they are exercisable in U.S. dollars and, therefore, fail the “fixed for fixed” requirements prescribed in IAS 32 Financial Instruments: presentation. As a result, they are classified as a liability and measured at fair value. The liability is revalued at its estimated fair value using the Black-Scholes model at the end of each reporting period, and the variation in the fair value is recognized on the consolidated statements of loss under other gains (losses), net.

|

| September 30, |

| December 31, |

| | 2023 | | 2022 |

| | $ | | $ |

Fair value through profit or loss (warrants) | |

|

|

|

Balance – Beginning of period | | 16,395 | | — |

Additions | | — | | 39,841 |

Change in fair value | | (6,968) | | (25,008) |

Foreign exchange | | (104) | | 1,562 |

Balance – End of period | | 9,322 | | 16,395 |

In absence of quoted market prices, the valuation of the warrants exercisable in USD, when granted and re-measured at fair value is determined by the Black-Scholes option pricing model based on the following range of assumptions:

| | September 30, | | December 31, |

| ||

| | 2023 | | 2022 | | ||

Dividend per share | | | — | | | — | |

Expected volatility | | | 66.7 | % | | 69.0 | % |

Risk-free interest rate | | | 4.62 | % | | 4.00 | % |

Expected life | | | 3.6 years | | | 4.4 years | |

Exercise price (USD) | | $ | 10.70 | | $ | 18.00 | |

Share price (USD) | | $ | 2.94 | | $ | 4.30 | |

18. | Share Capital and Warrants |

Shares

Authorized: unlimited number of common shares, without par value

Issued and fully paid: 84,024,375 common shares

Employee Share Purchase Plan

The Company offers an employee share purchase plan to its employees. Under the terms of the plan, the Company contributes an amount equal to 60% of the eligible employee’s contribution towards the acquisition of common shares from treasury on a quarterly basis. Under this plan, no employee shall acquire common shares which exceed 10% of the issued and outstanding common shares of the issuer at the time of the purchase of the common shares.

18

Osisko Development Corp.

Notes to the Condensed Consolidated Financial Statements

For the three and nine months ended September 30, 2023 and 2022

(Unaudited)

(Tabular amounts expressed in thousands of Canadian dollars, except per share amounts)

2023 Bought Deal Financing

On March 2, 2023, the Company completed a public offering on a bought deal basis issuing 7,841,850 units at a price of $6.60 per unit for aggregate gross proceeds of $51.8 million (the “Bought Deal Financing”). Each unit is comprised of one common share and one warrant, with each warrant entitling the holder to purchase one additional common share at a price of $8.55 per common share for a period of 3 years following the closing date of the Bought Deal Financing. The fair value of the warrants issued was evaluated using the residual method and were valued at $6.2 million. Share issue expense related to the Bought Deal Financing amounted to $3.4 million of which $3.2 million were paid during the nine months ended September 30, 2023 and have been allocated against the common shares and warrants issued.

Participation Agreement with Williams Lake First Nation

On March 2, 2023, the Company issued 10,000 common shares in accordance with the terms of a participation agreement dated June 10, 2022 with Williams Lake First Nation relating to the Company’s Cariboo Gold Project. The fair value of the common shares issued is calculated with reference to the share price of the Company’s common shares.

19

Osisko Development Corp.

Notes to the Condensed Consolidated Financial Statements

For the three and nine months ended September 30, 2023 and 2022

(Unaudited)

(Tabular amounts expressed in thousands of Canadian dollars, except per share amounts)

Warrants

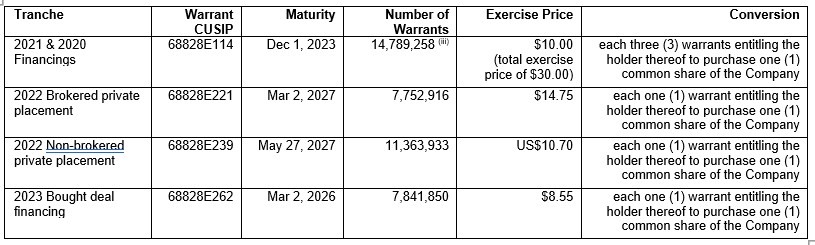

The following table summarizes the Company’s movements for the warrants outstanding:

| | September 30, 2023 | | December 31, 2022 | ||||

| | | | Weighted | | | | Weighted |

| | Number of | | average | | Number of | | average |

|

| Warrants |

| exercise price |

| Warrants(iii) |

| exercise price |

| | |

| $ | | |

| $ |

Balance – Beginning of period |

| 24,046,640 |

| 17.86 | | 4,929,791 |

| 30.00 |

Issued – Brokered private placement |

| — | | — | | 7,752,916 | | 22.80 |

Issued – Non-brokered private placement(i) |

| — | | — | | 11,363,933 | | 13.53 |

Issued – Bought deal financing(ii) | | 7,841,850 | | 8.55 | | — | | — |

Balance – End of period |

| 31,888,490 | | 15.57 | | 24,046,640 | | 17.86 |

The outstanding warrants have the following maturity dates and exercise terms:

| (i) | Exercise price of warrants issued in non-brokered private placement is in USD. |

| (ii) | On March 17, 2023, the Company received the required approvals to reduce the exercise price of the common share purchase warrants issued in 2022 under the brokered and non-brokered private placements. The exercise price to purchase one additional common share was reduced from $22.80 to $14.75 for the brokered private placement and from US$18.00 to US$10.70 for the non-brokered private placements. |

The increase in fair value of the amended share purchase warrants classified as equity instruments was estimated to $4.5 million and recorded directly in the Deficit, considering the fair value of the original warrants left at the date of the modification, using the Black-Scholes option pricing model based on the following assumptions:

Dividend per share |

| | — | |

Expected volatility |

| | 66 | % |

Risk-free interest rate |

| | 2.9 | % |

Expected life |

| | 4 years | |

Share price | | $ | 6.20 | |

20

Osisko Development Corp.

Notes to the Condensed Consolidated Financial Statements

For the three and nine months ended September 30, 2023 and 2022

(Unaudited)

(Tabular amounts expressed in thousands of Canadian dollars, except per share amounts)

| (iii) | The number of warrants presented for 2022 have been adjusted to reflect the effect of the 3:1 share consolidation that took place on May 4, 2022. The consolidation is not reflected for 20202 and 2021 warrants. |

19. | Share-based compensation |

Share options

The Company offers a share option plan to directors, officers, management, employees and consultants.

The following table summarizes information about the movement of the share options outstanding under the Company’s plan:

| | September 30, 2023 |

| December 31, 2022 | ||||

| | | | Weighted | | | | Weighted |

| | | | average | | | | average |

| | Number of | | exercise | | Number of | | exercise |

|

| options |

| price |

| options(i) |

| price |

| | | | $ | | |

| $ |

Balance – Beginning of period |

| 1,812,450 | | 11.52 |

| 697,841 | | 21.21 |

Granted |

| 1,202,400 | | 6.59 |

| 1,245,400 | | 6.43 |

Forfeited |

| (215,494) | | 9.01 |

| (130,791) | | 14.74 |

Balance – End of period |

| 2,799,356 | | 9.60 |

| 1,812,450 | | 11.52 |

Options exercisable – End of period |

| 531,242 | | 13.75 |

| 205,229 | | 21.32 |

| (i) | The number of options presented for 2022 have been adjusted to reflect the effect of the 3:1 share consolidation that took place on May 4, 2022. |

The following table summarizes the share options outstanding as at September 30, 2023:

|

| |

| Options outstanding |

| Options exercisable | ||||

| | | | | | Weighted | | | | Weighted |

| | | | | | average | | | | average |

| | Exercise | | | | remaining contractual | | | | remaining contractual |

Grant date |

| price |

| Number |

| life (years) | | Number |

| life (years) |

|

| $ | | |

| | | | |

|

December 22, 2020 |

| 22.86 | | 327,199 |

| 2.23 | | 112,051 | | 2.23 |

February 5, 2021 |

| 24.30 | | 10,533 |

| 2.35 | | 3,511 | | 2.35 |

June 23, 2021 |

| 21.30 | | 160,030 |

| 2.73 | | 107,079 | | 2.73 |

August 16, 2021 |

| 16.89 | | 34,533 |

| 2.88 | | 24,135 | | 2.88 |

November 12, 2021 |

| 16.20 | | 37,894 |

| 3.12 | | 12,633 | | 3.12 |

June 30, 2022 |

| 6.49 | | 774,167 |

| 3.75 | | 271,833 | | 3.75 |

November 18, 2022 |

| 6.28 | | 282,700 |

| 4.13 | | - | | - |

April 3, 2023 | | 6.59 | | 1,172,300 | | 4.51 | | - | | - |

|

| 9.60 | | 2,799,356 |

| 3.85 | | 531,242 | | 3.16 |

21

Osisko Development Corp.

Notes to the Condensed Consolidated Financial Statements

For the three and nine months ended September 30, 2023 and 2022

(Unaudited)

(Tabular amounts expressed in thousands of Canadian dollars, except per share amounts)

The options, when granted, are accounted for at their fair value determined by the Black-Scholes option pricing model based on the vesting period and on the following weighted average assumptions:

|

| September 30, 2023 |

| December 31, 2022 | | ||

Dividend per share |

| | — |

| | — | |

Expected volatility |

| | 66% | | | 64% | |

Risk-free interest rate |

| | 3.2% | | | 3.3% | |

Expected life |

| | 48 months | | | 47 months | |

Weighted average share price | | $ | 6.59 | | $ | 6.43 | |

Weighted average fair value of options granted | | $ | 3.43 | | $ | 3.27 | |

The expected volatility is estimated by benchmarking with companies having businesses similar to Osisko Development. The historical volatility of the common share price of these companies was used for benchmarking back from the date of grant and for a period corresponding to the expected life of the options.

The fair value of the share options is recognized as compensation expense over the vesting period. During the three and nine months ended September 30, 2023, the total share-based compensation related to share options granted under the Osisko Development’s plan amounted to $1.1 million and $3.3 million, respectively ($1.1 million and $2.5 million for the three and nine months ended September 30, 2022, respectively).

Deferred and restricted share units (“DSU” and “RSU”)

The following table summarizes information about the DSU and RSU movements:

| | September 30, 2023 | | December 31, 2022 | ||||

|

| DSU |

| RSU |

| DSU(i) |

| RSU |

Balance – Beginning of period |

| 206,426 |

| 1,054,194 |

| 79,781 |

| 345,377 |

Granted |

| 99,170 |

| 261,900 |

| 137,528 |

| 794,500 |

Settled |

| — |

| (95,459) |

| (10,883) |

| (49,118) |

Forfeited |

| — |

| (99,484) |

| — |

| (36,565) |

Balance – End of period |

| 305,596 |

| 1,121,151 |

| 206,426 |

| 1,054,194 |

Balance – Vested |

| 206,426 |

| — |

| 68,898 |

| — |

| (i) | The number of DSU/RSU presented for 2022 have been adjusted to reflect the effect of the 3:1 share consolidation that took place on May 4, 2022. |

| (ii) | Unless otherwise decided by the board of directors of the Company, the DSU vest the day prior to the next annual general meeting and are payable in common shares, cash or a combination of common shares and cash, at the sole discretion of the Company, to each director when he or she leaves the board or is not re-elected. The value of the payout is determined by multiplying the number of DSU expected to be vested at the payout date by the closing price of the Company’s shares on the day prior to the grant date. The fair value is recognized over the vesting period. On the settlement date, one common share will be issued for each DSU, after deducting any income taxes payable on the benefit earned by the director that must be remitted by the Company to the tax authorities. |

The total share-based compensation expense related to the Osisko Development’s DSU and RSU plans for the three and nine months ended September 30, 2023 amounted to $0.9 million and $3.3 million, respectively ($1.1 million and $3.2 million for the three and nine months ended September 30, 2022, respectively).

22

Osisko Development Corp.

Notes to the Condensed Consolidated Financial Statements

For the three and nine months ended September 30, 2023 and 2022

(Unaudited)

(Tabular amounts expressed in thousands of Canadian dollars, except per share amounts)

Based on the closing price of the common shares at September 30, 2023 ($3.90), and considering a marginal income tax rate of 53.3%, the estimated amount that Osisko Development is expected to transfer to the tax authorities to settle the employees’ tax obligations related to the vested RSU and DSU to be settled in equity amounts to $ 0.4 million ($0.2 million as at December 31, 2022) and to $2.9 million based on all RSU and DSU outstanding ($3.9 million as at December 31, 2022).

20. | Cost of sales and other operating costs |

|

| Three months ended |

| Nine months ended | ||||

| | September 30, | | September 30, | ||||

| | 2023 | | 2022 | | 2023 |

| 2022 |

|

| ($) | | ($) | | ($) |

| ($) |

Salaries and benefits | | 3,502 | | 5,198 | | 9,197 | | 14,259 |

Share-based compensation |

| (94) | | 26 | | 93 |

| 211 |

Royalties |

| 256 | | 254 | | 719 |

| 1,242 |

Contract Services |

| 3,195 | | 14,259 | | 9,160 |

| 36,579 |

Raw materials and consumables |

| 3,306 | | 4,460 | | 7,980 |

| 13,879 |

Operational overhead and write-downs(Note 6) |

| 4,104 | | 17,011 | | 10,684 |

| 25,050 |

Depreciation |

| 2,577 | | 3,671 | | 8,855 |

| 10,883 |

|

| 16,846 | | 44,879 | | 46,688 |

| 102,103 |

21. | General and administrative expenses |

|

| Three months ended |

| Nine months ended | ||||

| | September 30, | | September 30, | ||||

| | 2023 |

| 2022 | | 2023 |

| 2022 |

| | ($) | | ($) | | ($) | | ($) |

Salaries and benefits | | 3,724 | | 2,517 | | 10,977 | | 6,670 |

Share-based compensation |

| 1,959 | | 2,176 | | 6,171 |

| 5,163 |

Insurance |

| 1,253 | | 1,247 | | 4,302 |

| 2,447 |

Depreciation |

| 48 | | 41 | | 175 |

| 121 |

Transaction costs |

| — | | 1,046 | | — |

| 5,598 |

Legal and other Consulting fees | | 2,869 | | 213 | | 6,406 | | 2,998 |

NYSE and TSX | | 426 | | 589 | | 1,246 | | 655 |

Other |

| (897) | | 880 | | 649 |

| 2,799 |

|

| 9,382 | | 8,710 | | 29,926 |

| 26,451 |

22. | Other income, net |

|

| Three months ended |

| Nine months ended | ||||

| | September 30, | | September 30, | ||||

| | 2023 |

| 2022 | | 2023 |

| 2022 |

| | ($) | | ($) | | ($) | | ($) |

Interest income, net |

| 1,270 | | 443 | | 3,641 |

| 960 |

Foreign exchange gain (loss) |

| 745 | | 6,267 | | 9,822 |

| 8,327 |

Premium on flow-through shares |

| — | | — | | — |

| 914 |

Gain on deemed disposal of investment |

| — | | — | | — |

| 11,854 |

Other |

| (1,166) | | 394 | | (47) |

| (775) |

|

| 849 | | 7,104 | | 13,416 |

| 21,280 |

23

Osisko Development Corp.

Notes to the Condensed Consolidated Financial Statements

For the three and nine months ended September 30, 2023 and 2022

(Unaudited)

(Tabular amounts expressed in thousands of Canadian dollars, except per share amounts)

23. | Loss per share |

|

| Three months ended |

| Nine months ended | ||||

| | September 30, | | September 30, | ||||

| | 2023 |

| 2022 | | 2023 |

| 2022 |

Net loss attributable to shareholders of the Company | | (7,123) | | (103,731) | | (43,778) | | (127,563) |

| | | | | | | | |

Basic and diluted weighted average number of common shares outstanding | | 83,997,968 | | 75,615,861 | | 81,919,028 | | 59,810,489 |

| | | | | | | | |

Net loss per share, basic and diluted | | (0.08) | | (1.37) | | (0.53) | | 2.13 |

The weighted average basic and diluted shares outstanding for 2022 presented have been adjusted to reflect the effect of the 3:1 share consolidation that took place on May 4, 2022.

Excluded from the calculation of the diluted loss per share are all common share purchase warrants and stock options, as their effect would be anti-dilutive.

24. | Supplementary cash flows information |

|

| Three months ended |

| Nine months ended | ||||

| | September 30, | | September 30, | ||||

| | 2023 |

| 2022 | | 2023 |

| 2022 |

| | ($) | | ($) | | ($) | | ($) |

Changes in non-cash working capital items |

| | | | |

|

|

|

Decrease (increase) in amounts receivable |

| (1,396) | | 1,675 | | 5,693 |

| 870 |

Decrease (Increase) in inventory |

| (292) | | 15,383 | | 1,030 |

| 9,438 |

Increase in other current assets |

| (111) | | (5,694) | | 47 |

| (8,723) |

Decrease in accounts payable and accrued liabilities |

| 2,164 | | 1,996 | | (4,973) | | 1,881 |

| | 365 | | 13,360 | | 1,797 | | 3,466 |

24

Osisko Development Corp.

Notes to the Condensed Consolidated Financial Statements

For the three and nine months ended September 30, 2023 and 2022

(Unaudited)

(Tabular amounts expressed in thousands of Canadian dollars, except per share amounts)

25. | Fair value of financial instruments |

The following table provides information about financial assets and liabilities measured at fair value in the consolidated statements of financial position and categorized by level according to the significance of the inputs used in making the measurements.

Level 1– Unadjusted quoted prices in active markets for identical assets or liabilities;

Level 2– Inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly (that is, as prices) or indirectly (that is, derived from prices); and

Level 3–Inputs for the asset or liability that are not based on observable market data (that is, unobservable inputs).

| | September 30, 2023 | ||||||

| | Level 1 | | Level 2 | | Level 3 | | Total |

|

| $ | | $ | | $ | | $ |

Recurring measurements | |

|

|

|

|

|

|

|

Financial assets at fair value through profit or loss | | | | | | | | |

Convertible loan receivable | | — |

| — |

| — |

| — |

Warrants on equity securities | |

|

|

|

|

|

|

|

Publicly traded mining exploration and development companies | |

|

|

|

|

|

|

|

Precious metals | | — |

| — |

| 24 |

| 24 |

Other minerals | | — |

| — |

| — |

| — |

Financial assets at fair value through other comprehensive loss | |

|

|

|

|

|

|

|

Equity securities | |

|

|

|

|

|

|

|

Publicly traded mining exploration and development companies | |

|

|

|

|

|

|

|

Precious metals | | 5,882 |

| — |

| — |

| 5,882 |

Other minerals | | 16,610 |

| — |

| — |

| 16,610 |

| | 22,492 |

| — |

| 24 |

| 22,516 |

| | December 31, 2022 | ||||||

| | Level 1 | | Level 2 | | Level 3 | | Total |

|

| $ |

| $ |

| $ |

| $ |

Recurring measurements | |

| |

| |

| |

|

Financial assets at fair value through profit or loss | | | | | | | | |

Convertible loan receivable | | — |

| — |

| — |

| — |

Warrants on equity securities | |

|

|

|

|

|

|

|

Publicly traded mining exploration and development companies | |

|

|

|

|

|

|

|

Precious metals | | — |

| — |

| 18 |

| 18 |

Other minerals | | — |

| — |

| — |

| — |

Financial assets at fair value through other comprehensive loss | |

|

|

|

|

|

|

|

Equity securities | |

|

|

|

|

|

|

|

Publicly traded mining exploration and development companies | |

|

|

|

|

|

|

|

Precious metals | | 9,537 |

| — |

| — |

| 9,537 |

Other minerals | | 24,264 |

| — |

| — |

| 24,264 |

| | 33,801 |

| — |

| 18 |

| 33,819 |

During the period ended September 30, 2023 and 2022 there were no transfers among Level 1, Level 2 and Level 3.

25

Osisko Development Corp.

Notes to the Condensed Consolidated Financial Statements

For the three and nine months ended September 30, 2023 and 2022

(Unaudited)

(Tabular amounts expressed in thousands of Canadian dollars, except per share amounts)

The following table presents the changes in the Level 3 investments (warrants and convertible loan) for the three months ended September 30, 2023 and the year ended December 31, 2022:

|

| September 30, | | December 31, |

| | 2023 | | 2022 |

| | $ | | $ |

Balance – Beginning of period | | 18 |

| 6,952 |

Acquisitions | | — |

| 4,438 |

Warrants exercised | | — |

| (117) |

Acquisition of Tintic | | — |

| (10,827) |

Change in fair value – warrants exercised (i) | | 6 |

| 49 |

Change in fair value – expired (i) | | — |

| (287) |

Change in fair value – held at the end of the year (i) | | — |

| (241) |

Foreign exchange | | — |

| 51 |

Balance – End of period | | 24 |

| 18 |

The fair value of the financial instruments classified as Level 3 depends on the nature of the financial instruments.

The fair value of the warrants on equity securities of publicly traded mining exploration and development companies and the convertible debentures, classified as Level 3, is determined using the Black-Scholes option pricing model or discounted cash flows. The main non-observable input used in the model is the expected volatility. An increase/decrease in the expected volatility used in the models of 10% would lead to an insignificant variation in the fair value of the warrants as at September 30, 2023 and December 31, 2022.

Financial instruments not measured at fair value on the consolidated statements of financial position

Financial instruments that are not measured at fair value on the consolidated statement of financial position are represented by cash and cash equivalents, trade receivables, amounts receivable from associates and other receivables, notes receivable, accounts payable and accrued liabilities and long-term debt. The fair values of cash and cash equivalents, trade receivables, amounts receivable from associates and other receivables, accounts payable and accrued liabilities and short-term debt approximate their carrying values due to their short-term nature. The carrying value of the long-term debt approximates its fair value given that its interest rates are similar to the rates the Company would obtain under similar conditions at the reporting date.

26

Osisko Development Corp.

Notes to the Condensed Consolidated Financial Statements

For the three and nine months ended September 30, 2023 and 2022

(Unaudited)

(Tabular amounts expressed in thousands of Canadian dollars, except per share amounts)

26. | Segmented information |

The chief operating decision-maker organizes and manages the business under geographic segments, being the acquisition, exploration and development of mineral properties. The assets related to the exploration, evaluation and development of mining projects are located in Canada, in Mexico, and in the USA and are detailed as follows as at September 30, 2023 and December 31, 2022:

| | September 30, 2023 | ||||||

| | Canada | | Mexico | | USA | | Total |

|

| $ |

| $ |

| $ |

| $ |

Other assets (non-current) | | 15,711 | | 20,430 | | 3,720 | | 39,861 |

Mining interest | | 383,837 | | 18,599 | | 200,769 | | 603,205 |

Property, plant and equipment | | 60,854 | | 21,760 | | 32,317 | | 114,931 |

Exploration and evaluation assets | | 3,653 | | — | | 64,335 | | 67,988 |

Total non-current assets (Excluding investments) | | 464,055 | | 60,789 | | 301,141 | | 825,985 |

| | December 31, 2022 | ||||||

| | Canada | | Mexico | | USA | | Total |

|

| $ |

| $ |

| $ |

| $ |

Other assets (non-current) | | 16,252 |

| 17,485 |

| 3,257 |

| 36,994 |

Mining interest | | 372,061 |

| 16,822 |

| 191,596 |

| 580,479 |

Property, plant and equipment | | 63,655 |

| 21,688 |

| 26,353 |

| 111,696 |

Exploration and evaluation assets | | 3,653 |

| — |

| 51,473 |

| 55,126 |

Total non-current assets (Excluding investments) | | 455,621 |

| 55,995 |

| 272,679 |

| 784,295 |

27

Osisko Development Corp.

Notes to the Condensed Consolidated Financial Statements

For the three and nine months ended September 30, 2023 and 2022

(Unaudited)

(Tabular amounts expressed in thousands of Canadian dollars, except per share amounts)

|

| Canada | | Mexico | | USA | | Total |

| | $ | | $ | | $ | | $ |

For the three months ended September 30, 2023 | |

|

|

|

|

|

|

|

| | | | | | | | |

Revenues | | 3,266 |

| 2,050 |

| 5,105 |

| 10,421 |

Cost of Sales | | (3,713) |

| (1,610) |

| (4,764) |

| (10,087) |

Other operating costs | | (4,368) |

| (2,412) |

| 21 |

| (6,759) |

General and administrative expenses | | (5,696) |

| (587) |

| (3,099) |

| (9,382) |

Exploration and evaluation | | (586) |

| (60) |

| — |

| (646) |

Operating Gain (Loss) | | (11,097) |

| (2,619) |

| (2,737) |

| (16,453) |

| | | | | | | | |

For the three months ended September 30, 2022 | |

|

|

|

|

|

| |

| | | | | | | | |

Revenues | | 2,262 |

| 12,876 |

| 7,653 |

| 22,791 |

Cost of Sales | | (2,262) |

| (12,876) |

| (8,297) |

| (23,435) |

Other operating costs | | (19,564) |

| (1,862) |

| (18) |

| (21,444) |

General and administrative expenses | | (7,425) |

| (151) |

| (1,134) |

| (8,710) |

Exploration and evaluation | | (90) |

| — |

| — |

| (90) |

Impairment of assets | | — | | (81,000) | | — | | (81,000) |

Operating Gain (Loss) | | (27,079) |

| (83,013) |

| (1,796) |

| (111,888) |

|

| Canada |

| Mexico |

| USA |

| Total |

| | $ | | $ | | $ | | $ |

For the nine months ended September 30, 2023 | |

|

|

|

|

|

|

|

Revenues | | 6,401 | | 8,028 |

| 10,290 |

| 24,719 |

Cost of Sales | | (6,344) |

| (8,690) |

| (10,866) |

| (25,900) |

Other operating costs | | (17,691) |

| (2,818) |

| (279) |

| (20,788) |

General and administrative expenses | | (22,040) |

| (1,950) |

| (5,936) |

| (29,926) |

Exploration and evaluation | | (1,530) |

| (156) |

| — |

| (1,686) |

Operating Gain (Loss) | | (41,204) |

| (5,586) |

| (6,791) |

| (53,581) |

| | | | | | | | |

For the nine months ended September 30, 2022 | | | | | | | | |

Revenues | | 20,416 | | 12,876 | | 11,529 | | 44,821 |

Cost of Sales | | (20,416) | | (12,876) | | (11,519) | | (44,811) |

Other operating costs | | (43,826) | | (13,448) | | (18) | | (57,292) |

General and administrative expenses | | (23,153) | | (2,059) | | (1,239) | | (26,451) |

Exploration and evaluation | | (367) | | — | | — | | (367) |

Impairment of assets | | — | | (81,000) | | — | | (81,000) |

Operating Gain (Loss) | | (67,346) | | (96,507) | | (1,247) | | (165,100) |

28