As filed with the Securities and Exchange Commission on December 21, 2020.

Registration Statement No. 333-251238

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1 to

FORM F-4

Registration Statement

Under

the Securities Act of 1933

Cosan S.A.

(Exact Name of Registrant as Specified in its Charter)

Cosan Inc.

(Translation of Registrant’s Name into English)

|

Federative Republic of Brazil (State or Other Jurisdiction of

|

2860 (Primary Standard Industrial Classification Code Number) |

Not Applicable (I.R.S. Employer

|

Avenida Brigadeiro Faria Lima, 4,100 – 16th floor

São Paulo – SP, 04538-132, Brazil

Telephone: +55 (11) 3897-9797

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

Cogency Global Inc.

122 East 42nd Street, 18th Floor

New York, NY 10168

(212) 947-7200

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent For Service)

Copies to:

Manuel Garciadiaz

Daniel Brass

Davis Polk & Wardwell LLP

450 Lexington Avenue

New York, New York 10017

Approximate date of commencement of proposed sale of the securities to the public: As soon as practicable after the effective date of this Registration Statement.

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

| Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer) | ☐ | |

| Exchange Act Rule 14d-1(d) (Cross-Border Third-Party Tender Offer) | ☐ |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

| Emerging growth company | ☐ |

If an emerging growth company that prepares its financial statements in accordance with IFRS, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

| CALCULATION OF REGISTRATION FEE | ||||

| Title

Of Each Class Of Securities To Be Registered(1)(2) |

Amount To Be Registered(3) | Proposed Maximum Offering Price Per Share | Proposed Maximum Aggregate Offering Price(4) | Amount

Of Registration Fee(5)(6) |

| Common shares, no par value | 308,554,969 | Not applicable | U.S.$4,470,892,087.50 | U.S.$487,774.33 |

| Notes: |

| (1) | The securities being offered hereby may be issued in the form of American Depositary Shares of the registrant, referred to as CSAN ADSs. Each CSAN ADS represents one common share, nominal no par value of Cosan S.A., referred to as CSAN Shares. The CSAN ADSs will be issuable upon deposit of CSAN Shares with J.P. Morgan Chase Bank, N.A., acting as the depositary and will be registered under a registration statement on Form F-6 (Registration No. 333- ). |

| (2) | Pursuant to Rule 416 under the Securities Act of 1933, as amended (the “Securities Act”), this Registration Statement also covers an indeterminate number of additional CSAN Shares as may be issuable as a result of stock splits, stock dividends or similar transactions. |

| (3) | Represents the maximum number of the registrant’s common shares estimated to be issuable upon completion of the transaction described in the prospectus contained herein and is based upon the product of (a) (i) 142,115,534 Class A common shares of Cosan Limited (“CZZ”), plus (ii) 96,332,044 Class B series 1 common shares of CZZ (collectively, the “Total Shares”) and (b) 1.29401595263, which is the exchange ratio under the Merger Documents (as defined herein). |

| (4) | Pursuant to Rules 457(c) and 457(f)(1) promulgated under the Securities Act and solely for the purpose of calculating the registration fee, the proposed aggregate maximum offering price is (i) the product of (x) U.S.$18.75 (the average of the high and low prices of CZZ Class A common shares as reported on the New York Stock Exchange on December 15, 2020) times (y) the Total Shares. |

| (5) | Determined in accordance with Section 6(b) of the Securities Act at a rate equal to U.S.$109.10 per $1,000,000 of the proposed maximum aggregate offering price. |

| (6) | The registration fee was partially paid by Cosan S.A., in the amount of U.S.$449,923.04, in connection with its Registration Statement on Form F-4 (File No. 333-251238) filed on December 9, 2020. An additional amount of U.S.$37,851.29 is being paid with this amendment. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Information contained in this prospectus is subject to completion and may be changed. A registration statement relating to these securities has been filed with the U.S. Securities and Exchange Commission. These securities may not be sold nor may offers to buy be accepted prior to the time the registration statement becomes effective. This document shall not constitute an offer to sell or the solicitation of any offer to buy nor shall there be any sale of these securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction.

SUBJECT TO AMENDMENT AND COMPLETION, DATED DECEMBER 21 , 2020

PRELIMINARY PROSPECTUS

Merger of Cosan Limited with and into Cosan S.A.

Cosan

S.A.

(incorporated in the Federative Republic of Brazil as a sociedade anônima)

This prospectus relates to the common shares, or “CSAN Shares,” of Cosan S.A., or “CSAN,” including common shares in the form of American Depositary Shares, or the “CSAN ADSs.” CSAN ADSs are to be issued to holders of Class A common shares (“Class A Shares”) of Cosan Limited, or “CZZ,” an exempted company incorporated in Bermuda, and CSAN Shares are to be issued to holders of Class B Common Shares (“Class B Shares”) of CZZ, in each case subject to the satisfaction of certain conditions in connection with the merger of CZZ with and into CSAN, a corporation (sociedade anônima) incorporated under the laws of the Federative Republic of Brazil pursuant to section 104B of the Bermuda Companies Act 1981, or the “Merger.”

The Merger is part of a reorganization of the Cosan Group (as defined herein), as more fully described below. The business carried out by CSAN following the Merger will be the same as the business currently carried out by CZZ prior to the Merger. In this prospectus, “Cosan Group” refers to the economic entity currently represented by CZZ and its subsidiaries prior to the Merger, which, following the Merger, will be represented by CSAN and its subsidiaries, as the context requires. Subject to requisite shareholders’ approval, CZZ shareholders will receive in the Merger 1.29401595263 CSAN ADSs for each one Class A Share that they hold and 1.29401595263 CSAN Shares for each one Class B Share that they hold.

Holders of CZZ shares are to vote on the Merger at an extraordinary general meeting of CZZ scheduled for January 22 , 2021. The Merger must be approved at the extraordinary general meeting of CZZ shareholders by a majority vote of at least 75% of those CZZ shareholders voting at the meeting. The Merger is subject to the satisfaction and/or waiver of certain conditions, including obtaining all of the required authorizations.

Upon effectiveness of the Merger, the pre-Merger shareholders of CZZ will hold 308,554,969 of CSAN Shares (including CSAN Shares in the form of CSAN ADSs) as they held of CZZ shares before the Merger. The Merger is expected to become fully effective once the CZZ shareholders approve the Merger and the conditions precedent to closing are satisfied.

If you hold CZZ Class A Shares through an intermediary such as a broker/dealer or clearing agency, you should consult with that intermediary about how to obtain information on the relevant shareholders’ meeting of CZZ.

CSAN will apply to list the CSAN ADSs on the NYSE, where trading is expected to commence by the Closing Date (as defined herein). Up to the first date of trading of the CSAN ADSs, shareholders will continue to be able to trade CZZ Class A Shares. See “The Merger.” The CSAN Shares are listed on the B3 S.A. – Brasil, Bolsa, Balcão or the “B3.”

Neither the Securities and Exchange Commission, or the “SEC,” nor any state securities commission has approved or disapproved of the securities offered in this prospectus, passed on the merits or fairness of the transaction or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

We encourage you to read this prospectus carefully in its entirety, including the “Risk Factors” section that begins on page 10.

Prospectus dated ,

2020

ABOUT THIS PROSPECTUS

This document, which forms part of a registration statement on Form F-4 filed with the U.S. Securities and Exchange Commission (the “SEC”) by Cosan S.A., a corporation (sociedade anônima) incorporated under the laws of Brazil, or “CSAN,” (File No. 333-251238), and constitutes a prospectus of CSAN under Section 5 of the U.S. Securities Act of 1933, as amended (the “Securities Act”), with respect to the shares of common stock of CSAN, or the “CSAN Shares,” to be deposited with JPMorgan Chase Bank, N.A., or the “ADS Depositary,” or issued to common shareholders of Cosan Limited, an exempted company incorporated in Bermuda, or “CZZ,” pursuant to the transactions contemplated by the Merger and Justification Protocol to be entered into by and among CZZ and CSAN, or the “Merger Protocol” and the Deed of Merger to be entered into by and among CZZ and CSAN, or the “Deed of Merger.” The Merger Protocol and the Deed of Merger, together, are referred to in this prospectus as the “Merger Documents.” The ADS Depositary will file a registration statement on Form F-6 (Reg. No. 333- ) with respect to the American Depositary Shares of CSAN, each representing one CSAN Share, or the “CSAN ADSs.”

Information contained in or incorporated by reference into this prospectus relating to CZZ has been supplied by CZZ and information contained in this prospectus relating to CSAN has been provided by CSAN. Except as specifically incorporated by reference into this prospectus, any reference to a website address does not constitute incorporation by reference of the information contained at or available through such website, and you should not consider it to be a part of this prospectus.

You should rely only on the information contained in or incorporated by reference into this prospectus. No person has been authorized to provide you with information that is different from what is contained in, or incorporated by reference into, this prospectus, and, if given or made by any person, such information must not be relied upon as having been authorized. You should not assume that the information contained in this prospectus is accurate as of any date other than its date as specified on the cover unless otherwise specifically provided herein. Further, you should not assume that the information contained in or incorporated by reference into this prospectus is accurate as of any date other than the date of the incorporated document. Neither the mailing of this prospectus to CZZ shareholders nor the issuance by CSAN of CSAN Shares or CSAN ADSs pursuant to the Merger Documents will create any implication to the contrary.

None of the SEC, the Brazilian Securities Commission (Comissão de Valores Mobiliários) (the “CVM”), nor any securities commission of any jurisdiction has approved or disapproved any of the transactions described in this prospectus or the securities to be issued under this document or passed upon the adequacy or accuracy of this document. Any representation to the contrary is a criminal offense. This prospectus does not constitute an offer to buy or sell, or a solicitation of an offer to buy or sell, any securities, or a solicitation of a proxy, in any jurisdiction to or from any person to whom it is unlawful to make any such offer or solicitation in such jurisdiction. For the avoidance of doubt, this prospectus does not constitute an offer to buy or sell securities or a solicitation of an offer to buy or sell any securities in Brazil or a solicitation of a proxy under the laws of Brazil, and it is not intended to be, and is not, a prospectus or an offer document within the meaning of Brazilian law and the rules of the CVM. You should inform yourself about and observe any such restrictions, and none of CZZ or CSAN accepts any liability in relation to any such restrictions.

Page

i

ii

Cautionary Statement Concerning Forward-Looking Statements

This prospectus contains forward-looking statements concerning CZZ, CSAN, the Merger (as defined herein) and other matters. These statements may discuss goals, intentions and expectations as to future plans, trends, events, results of operations or financial conditions, or other matters, based on current beliefs of the management of CZZ, CSAN as well as assumptions made by, and information currently available to the management of both companies. Forward-looking statements can be identified by the fact that they do not relate only to historical or current facts and may be accompanied by words such as “aim,” “anticipate,” “believe,” “plan,” “could,” “would,” “should,” “estimate,” “expect,” “forecast,” “future,” “guidance,” “intend,” “may,” “will,” “possible,” “potential,” “predict,” “project” or similar words, phrases or expressions, although the absence of any such words or expressions does not mean that a particular statement is not a forward-looking statement. These statements are subject to various risks and uncertainties, many of which are outside the parties’ control. Therefore, you should not place undue reliance on these statements. Factors that could cause actual plans and results to differ materially from those in these statements include, but are not limited to, risks and uncertainties detailed in the section of this prospectus entitled “Risk Factors,” and CZZ’s periodic public filings with the SEC, including those discussed in the section of this prospectus entitled “Risk Factors” and under “Item 3. Key Information—D. Risk Factors” in the CZZ 2019 Form 20-F and the CZZ Q3 Form 6-Ks, factors contained or incorporated by reference into such documents and in subsequent filings by CZZ with the SEC and factors described in CSAN’s annual reports, registration documents and other documents filed with the CVM, and the following factors:

| · | general economic, political, demographic and business conditions in Brazil and in the world and the cyclicality affecting our selling prices; |

| · | the effects of global financial and economic crises in Brazil; |

| · | our ability to implement our expansion strategy in other regions of Brazil and international markets through organic growth, acquisitions or joint ventures; |

| · | our ability to successfully compete in all segments and geographical markets where we currently conduct business or may conduct businesses in the future; |

| · | competitive developments in the segments in which we operate; |

| · | our ability to implement our capital expenditure plan, including our ability to arrange financing when required and on reasonable terms; |

| · | government intervention resulting in changes in the economy, taxes and tariffs affecting the markets in which we operate; |

| · | price of natural gas, ethanol and other fuels, as well as sugar; |

| · | equipment failure and service interruptions; |

| · | our ability to compete and conduct our businesses in the future; |

| · | adverse weather conditions; |

| · | changes in customer demand; |

| · | changes in our businesses; |

| · | our ability to work together successfully with our partners to operate our partnerships (such as the Joint Venture); |

| · | technological advances in the natural gas sector, including developments of natural gas for use in other applications, and advances in the development of alternatives to natural gas; |

| · | technological advances in the ethanol sector and advances in the development of alternatives to ethanol; |

iii

| · | changes in global energy usage; |

| · | government intervention and trade barriers, resulting in changes in the economy, taxes, rates, prices or regulatory environment including in relation to our regulated businesses such as Comgás; |

| · | inflation, depreciation, appreciation and depreciation of the real; |

| · | the duration and severity of the COVID-19 outbreak and its impacts on our business (see “Item 3. Key Information–D. Risk Factors—Risks Related to Our Businesses and the Industries in Which We Operate Generally—Our business, operations and results may be adversely impacted by Covid-19” and “Item 4. Information on the Company—A. History and Development of the Company—Recent Developments—Covid-19 Pandemic” in the CZZ 2019 Form 20-F); |

| · | other factors that may affect our financial condition, liquidity and results of our operations; and |

| · | other risk factors as set forth under “Risk Factors” in this prospectus. |

The foregoing list of factors is not exhaustive. You should carefully consider the foregoing factors and the other risks and uncertainties that affect the parties’ businesses, including those described in this prospectus, and information contained in or incorporated by reference into this prospectus. See the section of this prospectus entitled “Where You Can Find More Information.”

Nothing in this prospectus is intended, or is to be construed, as a profit projection or to be interpreted to mean that earnings per CZZ Class A Share, CSAN Share and CSAN ADSs for the current or any future financial years, will necessarily match or exceed the historical published earnings per CZZ Class A Share and CSAN Share, as applicable.

The Companies are under no obligation, and each expressly disclaims any obligation, to update, alter or otherwise revise any forward-looking statements, whether written or oral, that may be made from time to time, whether as a result of new information, future events or otherwise. Persons reading this document are cautioned not to place undue reliance on these forward-looking statements, which only speak as of the date hereof.

iv

Certain Defined Terms and Conventions Used in This Prospectus

In this prospectus, the “Company,” “we,” “us” and “our” refer to CSAN and its subsidiaries, unless the context otherwise requires. All references herein to the “real,” “reais” or “R$” are to the Brazilian real, the official currency of Brazil. All references to “U.S. dollars,” “dollars” or “U.S.$” are to United States dollars, the official currency of the United States.

In addition, as used in this prospectus, the following defined terms have the following respective meanings:

“B3” means the B3 S.A. – Brasil, Bolsa, Balcão, or São Paulo Stock Exchange.

“BNDES” means the Banco Nacional de Desenvolvimento Econômico e Social, or the Brazilian National Economic and Social Development Bank.

“Brazil” means the Federative Republic of Brazil and the phrase “Brazilian government” refers to the federal government of Brazil.

“Brazilian Central Bank” means the Central Bank of Brazil (Banco Central do Brasil).

“Brazilian Corporation Law” means the Brazilian Law No. 6,404/76, as amended.

“CDI,” or the Interbank Deposit Certificate (Certificado de Depósito Interbancário), means the “over extra group” daily average rate for interbank deposits, expressed as an annual percentage, based on 252 business days, calculated daily and published by B3, or any other index as may be further used in substitution thereof.

“Class A Shares” means Class A common shares of CZZ.

“Class B Shares” means Class B common shares of CZZ.

“CMN” means the Conselho Monetário Nacional, or the Brazilian Monetary Council.

“Comgás” means Companhia de Gás de São Paulo – COMGÁS.

“Companies” means CZZ, CSAN and CLOG.

“Companies Act” means the Companies Act 1981 of Bermuda (as amended).

“Compass” means Compass Gás e Energia S.A.

“Court” means the Supreme Court of Bermuda.

“CVM” means the Comissão de Valores Mobiliários, or the Brazilian Securities Commission.

“CZZ Shares” means the Class A Shares and Class B Shares.

“Exchange Act” means the U.S. Securities Exchange Act of 1934, as amended.

“Exchange Ratio” means one Class A Share for 1.29401595263 CSAN ADSs and one Class B Share for 1.29401595263 CSAN Shares (or 0.772788 CZZ Shares for each CSAN Share or CSAN ADS, as applicable).

“FGV” means the Fundação Getúlio Vargas.

“IASB” means the International Accounting Standards Board.

“IBGE” means the Brazilian Institute of Geography and Statistics (Instituto Brasileiro de Geografia e Estatística).

“IFRS” means International Financial Reporting Standards as issued by the IASB.

v

“Joint Venture” means the joint ventures formed on June 1, 2011 by CZZ and Shell Brazil Holdings B.V. for a combined 50/50 investment, under the names Raízen Combustíveis and Raízen Energia.

“Merger Consideration” means the consideration to be paid to the holders of CZZ Shares in respect of the Merger as detailed in the section of this prospectus entitled “Summary—Merger Consideration.”

“Moove” means Cosan Lubrificantes e Especialidades S.A., or “CLE”, Stanbridge Group Limited, or “Stanbridge,” Moove Lubricants Limited, or “Moove Lubricants,” (previously known as Comma Oil Chemicals Limited), TTA – SAS Techniques et Technologie Appliquées, or “TTA,” LubrigrupoII– Comércio e Distribuição de Lubrificantes, S.A., or “LubrigrupoII,” Cosan Lubricantes S.R.L, or “Cosan S.R.L” and Commercial Lubricants Moove Corp, or “Moove Corp,” (previously known as Commercial Lubricants, LLC (d/b/a Metrolube), or “Metrolube”).

“Novo Mercado Rules” means the listing rules of the Novo Mercado segment of the B3.

“NYSE” means the New York Stock Exchange.

“Raízen” means Raízen Energia and Raízen Combustíveis collectively.

“Raízen Argentina” means Shell Compañía Argentina de Petróleo S.A. and Energina Compañía Argentina de Petróleo S.A.

“Raízen Combustíveis” means Raízen Combustíveis S.A.

“Raízen Energia” means Raízen Energia S.A.

“Rumo” means Rumo S.A.

“Securities Act” means the U.S. Securities Act of 1933, as amended.

“United States” or “U.S.” means the United States of America.

vi

Presentation of Financial and Certain Other Information

Financial Statements

CZZ Financial Statements

The consolidated financial information of CZZ presented in this prospectus has been derived from the following:

| · | unaudited interim condensed consolidated financial statements of CZZ as of September 30, 2020 and for the three and nine months ended September 30, 2020 and 2019 and the related notes thereto, included in the September 2020 Financials 6-K, incorporated by reference in this prospectus; |

| · | audited consolidated financial statements of CZZ as of December 31, 2019 and 2018 and for each of the years in the three-year period ended December 31, 2019 and the related notes thereto, included in the CZZ 2019 Form 20-F, incorporated by reference in this prospectus; and |

| · | consolidated financial statements of CZZ as of and for the years ended December 31, 2016 and 2015 and the related notes thereto, not included or incorporated by reference in this prospectus. |

The consolidated financial statements of CZZ are prepared in accordance with IFRS as issued by the IASB and are presented in Brazilian reais. However, the functional currency of CZZ is the U.S. dollar. The Brazilian real is the currency of the primary economic environment in which CSAN, Cosan Logística S.A., or “CLOG,” and their respective subsidiaries and jointly-controlled entities, located in Brazil, operate and generate and expend cash. The functional currency for the subsidiaries located outside Brazil is the U.S. dollar, British pound or the Euro. The unaudited condensed interim consolidated financial statements of CZZ are prepared in accordance with IAS 34 – Interim Financial Reporting as issued by the IASB and are presented in Brazilian reais.

CSAN and CLOG Financial Statements

We have not included in this prospectus the financial statements of CSAN and its subsidiaries, or the “CSAN Group,” or of CLOG and its subsidiaries, or the “CLOG Group,” because no financial statements audited in accordance with the standards of the Public Company Accounting Oversight Board (PCAOB) exist for either the CSAN Group or the CLOG Group. We refer to the CZZ Group, the CSAN Group and the CLOG Group together as the “Cosan Group.” The Cosan Group intends to carry out an intra-group corporate restructuring consisting of a merger of companies under common control, as provided for by art. 264, paragraph 4th, of Brazilian Law No. 6,404, pursuant to which CZZ and CLOG will be merged into CSAN, or the “Proposed Transaction.” The Proposed Transaction is an intra-group restructuring (1) involving only entities which are under common control, and (2) in which all of the entities involved are already being presented to investors under CZZ. CZZ is the parent company of CSAN and CLOG. It is also the current holding company of the Cosan Group, of which both the CSAN Group and the CLOG Group are part. The combined effect of the exchange of shares in CZZ for shares in CSAN and of CSAN becoming the sole holding company of the Cosan Group as part of the Proposed Transaction is therefore that, in terms of financial presentation, it will be as if CZZ changed its name to CSAN with no further changes other than certain non-controlling interest amounts. Accordingly, we believe that the financial statements of the CZZ Group are sufficient to provide investors the necessary financial information regarding the Cosan Group both before and after the Proposed Transaction. CZZ is the current holding company of the Cosan Group. As a result, the financial statements of the CZZ Group will reflect the activities of the entire Cosan Group (including, without limitation, those of both the CSAN Group and the CLOG Group) at the date of effectiveness of the registration statement on Form F-4, which includes this prospectus, and following the implementation of the Merger.

Currency Conversions

On September 30, 2020, the exchange rate for reais into U.S. dollars was R$5.641 to U.S.$1.00, based on the selling rate as reported by the Brazilian Central Bank. The selling rate was R$5.641 to U.S.$1.00 as of September 30, 2020, R$4.031 to U.S.$1.00 as of December 31, 2019, R$3.875 to U.S.$1.00 as of December 31, 2018, R$3.308 to U.S.$1.00 as of December 29, 2017 and R$3.259 to U.S.$1.00 as of December 30, 2016, in each case, as reported by the Brazilian Central Bank. The real/U.S. dollar exchange rate fluctuates widely, and the selling rate as of

vii

September 30, 2020 may not be indicative of future exchange rates. See “Exchange Rates” for information regarding exchange rates for the Brazilian currency since January 1, 2015.

Solely for the convenience of the reader, we have translated certain amounts included in “Selected Financial Data of CZZ” and elsewhere in this prospectus from reais into U.S. dollars using the selling rate as reported by the Brazilian Central Bank as of September 30, 2020 of R$5.641 to U.S.$1.00. These translations should not be considered representations that any such amounts have been, could have been or could be converted into U.S. dollars at that or at any other exchange rate.

Rounding

We have made rounding adjustments to reach some of the figures included in this prospectus. Accordingly, numerical figures shown as totals in some tables may not be an arithmetic aggregation of the figures that preceded them.

Market Data

We obtained market and competitive position data, including market forecasts, used throughout this prospectus or incorporated by reference into this prospectus from market research, publicly available information and industry publications, as well as internal surveys. We include data from reports prepared by LMC International Ltd., the Brazilian Central Bank, the Sugarcane Agroindustry Association of the state of São Paulo (União da Agroindústria Canavieira de São Paulo), or “UNICA,” the Brazilian Ministry of Agriculture, Livestock, and Supply (Ministério da Agricultura, Pecuária e Abastecimento), or “MAPA,” the Brazilian Institute of Geography and Statistics (Instituto Brasileiro de Geografia e Estatística), or “IBGE,” the Brazilian Ministry of Development, Industry and Foreign Trade (Ministério do Desenvolvimento e do Comércio Exterior), or “MDIC,” the Brazilian Ministry of Infrastructure (Ministério da Infraestrutura), or “MI,” the Food and Agriculture Organization of the United Nations, or “FAO,” the National Traffic Agency (Departamento Nacional de Trânsito—DENATRAN), the Brazilian Association of Vehicle Manufactures (Associação Nacional dos Fabricantes de Veículos Automotores—ANFAVEA), Datagro Publicações Ltda., F.O. Licht, Czarnikow, Apoio e Vendas Procana Comunicações Ltda., the B3, the CVM, the International Sugar Organization, the Brazilian National Economic and Social Development Bank (Banco Nacional de Desenvolvimento Econômico e Social), or “BNDES,” the New York Board of Trade, or “NYBOT,” the New York Stock Exchange, or “NYSE,” the Brazilian Agricultural Research Corporation (Empresa Brasileira de Pesquisa Agropecuária), or “Embrapa,” the Brazilian Secretariat for Foreign Trade (Secretaria de Comércio Exterior), or “Secex,” the National Supply Company (Companhia Nacional de Abastecimento), or “Conab,” the United States Department of Agriculture, or “USDA,” the London Stock Exchange, the National Agency of Petroleum, Natural Gas and Biofuels (ANP - Agência Nacional do Petróleo, Gás Natural e Biocombustíveis), or “ANP,” the Brazilian antitrust authority (Superintendência-Geral do Conselho Administrativo de Defesa Econômica), or “CADE,” the National Union of Distributors of Fuels and Lubricants (Sindicato Nacional das Empresas Distribuidoras de Combustíveis e de Lubrificantes), or “Sindicom,” the ARSESP, the Brazilian Gas Distributors Association (Associação Brasileira das Empresas Distribuidoras de Gás), or “ABEGÁS,” the Agriculture School of the University of São Paulo (Escola Superior de Agricultura Luiz de Queiroz), or “ESALQ,” the National Waterway Transportation Agency (Agência Nacional de Transportes Aquaviários), or “ANTAQ,” the Brazilian Transportation Authority (Agência Nacional de Transporte Terrestre), or “ANTT,” Estação da Luz Participações, or “EDLP,” the National Electric Energy Agency (Agência Nacional de Energia Elétrica), or “ANEEL,” and the Chamber of Electric Energy Commercialization (Câmara de Comercialização de Energia Elétrica), or “CCEE.” We believe that all market data contained in or incorporated by reference into this prospectus is reliable, accurate and complete.

viii

Incorporation of Certain Documents by Reference

This prospectus incorporates important business and financial information about us and CZZ that is not included in or delivered with the prospectus. The SEC allows us to “incorporate by reference” information filed with the SEC, which means that we can disclose important information to you by referring you to those documents. The information incorporated by reference is considered to be part of this prospectus, and certain later information that CZZ files with the SEC will automatically update and supersede this information. We incorporate by reference the following documents and any future filings that CZZ makes with the SEC under Sections 13(a), 13(c) and 15(d) of the Securities Exchange Act of 1934, as amended, until we complete the offering using this prospectus:

| · | Annual report of CZZ on Form 20-F for the fiscal year ended December 31, 2019 filed on May 28, 2020, as amended on June 22, 2020, or the “CZZ 2019 Form 20-F”; |

| · | CZZ’s report on Form 6-K furnished to the SEC on November 17, 2020 at 5:14:19 p.m. EST relating to CZZ’s third quarter 2020 results, or the “September 2020 Earnings Release 6-K,” and CZZ’s report on Form 6-K furnished to the SEC on November 17, 2020 at 4:47:51 p.m. EST including its financial statements prepared in accordance with IAS 34 – Interim Financial Reporting as issued by the IASB, as of and for the three and nine months ended September 30, 2020 and 2019, or the “September 2020 Financials 6-K.” The September 2020 Earnings Release 6-K and the September 2020 Financials 6-K are collectively referred to as the “CZZ Q3 Form 6-Ks;” and |

| · | CZZ’s reports on Form 6-K furnished to the SEC on January 21, 2020, March 11, 2020, March 16, 2020, April 29, 2020, April 30, 2020, May 28, 2020, June 11, 2020, July 6, 2020, July 7, 2020, July 27, 2020, August 3, 2020, September 28, 2020, October 2, 2020, December 4, 2020, December 17, 2020 at 7:47:09 a.m. EST and December 18, 2020. |

We may also incorporate by reference any Form 6-K that CZZ furnishes to the SEC after the date of this prospectus and prior to the termination of this offering by identifying in such Form 6-K that it is being incorporated by reference into this prospectus. Unless expressly incorporated by reference, nothing in this prospectus shall be deemed to incorporate by reference information furnished to, but not filed with, the SEC.

All subsequent reports that CZZ files on Form 20-F under the Exchange Act after the date of this prospectus and prior to the termination of the offering shall also be deemed to be incorporated by reference into this prospectus and to be a part hereof from the date of filing such documents.

Any statement contained in a document incorporated or deemed to be incorporated by reference herein shall be deemed to be modified or superseded for purposes of this prospectus to the extent that a statement contained in this prospectus modifies or supersedes such statement. Any such statement so modified or superseded shall not be deemed, except as so modified or superseded, to constitute a part of this prospectus.

These documents are available on the SEC’s website at www.sec.gov and from other sources. You may read and copy any materials filed with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. You may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. Additionally, the SEC maintains an Internet site that contains reports and information statements, and other information regarding issuers that file electronically with the SEC (http://www.sec.gov).

None of the Companies has authorized anyone to give any information or make any representation about the Merger Documents and the transactions contemplated thereby or any of the Companies that is different from, or in addition to, that contained in this prospectus or in any of the materials that have been incorporated by reference into this prospectus. If you are in a jurisdiction where offers to exchange or sell, or solicitations of offers to exchange or purchase, the securities offered by this prospectus or the solicitation of proxies pursuant to this prospectus is unlawful, or if you are a person to whom it is unlawful to direct these types of activities, then the offer presented in this prospectus does not extend to you. The information contained in this prospectus is accurate only as of the date of this prospectus unless the information specifically indicates that another date applies.

ix

Where You Can Find More Information

CSAN has filed a registration statement on Form F-4, including the Exhibits thereto, with the SEC under the Securities Act to register the CSAN Shares that will be deposited with the ADS Depositary on behalf of holders of CZZ Shares or issued to CSAN shareholders and holders of CZZ Shares in connection with the Merger. CSAN may also file amendments to the registration statement. This prospectus does not contain all of the information set forth in the registration statement, and some parts have been omitted in accordance with the rules and regulations of the SEC. You should read the registration statement on Form F-4 and the Exhibits filed with the registration statement as they contain important information about the Companies as well as the CSAN Shares and CSAN ADSs. Statements made in this prospectus, or in any document incorporated by reference into this prospectus, regarding the contents of any contract, agreement or other document are not necessarily complete and each such statement is qualified in its entirety by reference to that contract, agreement or other document filed as an exhibit with the SEC.

CZZ files annual reports on Form 20-F and furnishes reports to the SEC on Form 6-K under the rules and regulations that apply to foreign private issuers. You may read and copy any materials filed by CZZ with, or furnished by CZZ to, the SEC at its Public Reference Room at 100 F Street, N.E., Washington, D.C., 20549. You may obtain information on the operation of the Public Reference Room by calling the SEC at +1 (800) SEC-0330. The SEC maintains a website at http://www.sec.gov that contains reports and other information regarding issuers that file electronically with the SEC. The reports and other information filed by CZZ with the SEC are also available at CZZ’s website at http://ir.cosanlimited.com/en. We have included the web address of the SEC and CZZ as inactive textual references only. Except as specifically incorporated by reference into this prospectus, information on those websites is not part of this document.

CSAN and CLOG are subject to the informational requirements of the CVM and the B3 and file reports and other information relating to their respective businesses, financial condition and other matters with the CVM and the B3. You may read these reports, statements and other information about CSAN at the public reference facilities maintained by the CVM at Rua Sete de Setembro, 111, 2nd floor, in the city of Rio de Janeiro, State of Rio de Janeiro, Brazil, and Rua XV de Novembro, 275, Centro, city of São Paulo, state of São Paulo, Brazil. Some filings of CSAN or CLOG with the CVM and the B3 are also available at the website maintained by the CVM at http://www.cvm.gov.br and the website maintained by the B3 at http://www.b3.com.br.

The public filings of CSAN and CLOG with the CVM are also available to the public free of charge through our internet website at https://ri.cosan.com.br/en/en and https://ri.cosanlogistica.com/en/, respectively. You may also request a copy of CSAN and CLOG filings at no cost by contacting CSAN and CLOG at the following address: Avenida Brigadeiro Faria Lima, 4,100 – 16th floor, São Paulo – SP, 04538-132, Brazil.

Information that we or CZZ file with or furnish to the SEC after the date of this prospectus, and that is incorporated by reference herein, will automatically update and supersede the information in this prospectus. You should review the SEC filings and reports that we incorporate by reference to determine if any of the statements in this prospectus, or in any documents previously incorporated by reference, have been modified or superseded.

You may also request copies of this prospectus and other information concerning CSAN, without charge, by written or telephonic request directed to CSAN at Avenida Brigadeiro Faria Lima, 4,100 – 16th floor, Room 1, São Paulo – SP, 04538-132, Brazil, by email at ri@cosan.com or by telephone at +55 11 3897-9797. In order for you to receive timely delivery of the documents in advance of the meeting of CZZ shareholders (together with any adjournments or postponements thereof, the “CZZ Special Meeting”), at which CZZ shareholders will be asked to consider and vote upon the proposals relating to the Merger, CSAN should receive your request no later than January 14 , 2021, which is five business days prior to the CZZ Special Meeting.

The information included on the websites of the SEC, CSAN, CZZ or any other entity or that might be accessed through such websites is not included in this prospectus or the registration statement and is not incorporated into this prospectus or the registration statement by reference unless otherwise specifically noted herein. We are providing the information about how you can obtain certain documents that are incorporated by reference into this prospectus at these websites only for your convenience.

x

The Brazilian foreign exchange system allows the purchase and sale of foreign currency and the international transfer of reais by any person or legal entity, regardless of the amount, subject to certain regulatory procedures.

Since 1999, the Brazilian Central Bank has allowed the real/U.S. dollar exchange rate to float freely, which resulted in increasing exchange rate volatility. Until early 2003, the real declined against the U.S. dollar. Between 2006 and 2008, the real strengthened against the U.S. dollar, except in the most severe periods of the global economic crisis. The real depreciated against the U.S. dollar from mid-2011 to early 2016 due to turmoil in international markets and the Brazilian macroeconomic outlook at the time. In particular, during 2015, due to the poor economic conditions in Brazil, including as a result of political instability, the real has devalued at a rate that is much higher than in previous years. On September 24, 2015, the real fell to the lowest level since the introduction of the currency, at R$4.195 per U.S.$1.00. Overall in 2015, the real depreciated 45.0%, reaching R$3.905 per U.S.$1.00 on December 31, 2015. Beginning in early 2016 through the end of 2016, the real appreciated against the U.S. dollar, primarily as a result of Brazil’s changing political conditions. In 2017, 2018 and 2019, the real depreciated 1.5%, 17.1% and 4.0% against the U.S. dollar, respectively. The real exchange rate was R$5.641 per US$1.00 on September 30, 2020, which reflected a 39.9% depreciation in the real against the U.S. dollar during the first nine months of 2020.

The Brazilian Central Bank has intervened in the foreign exchange market in the past to attempt to control instability in foreign exchange rates. We cannot predict whether the Brazilian Central Bank or the Brazilian government will continue to allow the real to float freely or will intervene in the exchange rate market by re-implementing a currency band system or otherwise. There can be no assurance that the real will not depreciate or appreciate further against the U.S. dollar and the real may depreciate or appreciate substantially against the U.S. dollar in the future. Furthermore, Brazilian law provides that, whenever there is a serious imbalance in Brazil’s balance of payments or there are serious reasons to foresee a serious imbalance, temporary restrictions may be imposed on remittances of foreign capital abroad. We cannot assure you that such measures will not be taken by the Brazilian government in the future.

The following tables set forth the exchange rate, expressed in reais per U.S. dollar (R$/U.S.$) for the periods indicated, as reported by the Brazilian Central Bank.

| Year | Period-end | Average(1) | Low | High | ||||||||||||

| 2015 | 3.905 | 3.339 | 2.575 | 4.195 | ||||||||||||

| 2016 | 3.259 | 3.483 | 3.119 | 4.156 | ||||||||||||

| 2017 | 3.308 | 3.656 | 3.051 | 3.381 | ||||||||||||

| 2018 | 3.875 | 3.656 | 3.139 | 4.188 | ||||||||||||

| 2019 | 4.031 | 3.946 | 3.652 | 4.260 | ||||||||||||

| Month | Period-end | Average(2) | Low | High | ||||||||||||

| May 2020 | 5.426 | 5.643 | 5.299 | 5.937 | ||||||||||||

| June 2020 | 5.476 | 5.197 | 4.889 | 5.476 | ||||||||||||

| July 2020 | 5.203 | 5.280 | 5.111 | 5.429 | ||||||||||||

| August 2020 | 5.471 | 5.461 | 5.276 | 5.651 | ||||||||||||

| September 2020 | 5.641 | 5.399 | 5.253 | 5.653 | ||||||||||||

| October 2020 | 5.772 | 5.626 | 5.521 | 5.780 | ||||||||||||

| November 2020 | 5.332 | 5.418 | 5.282 | 5.693 | ||||||||||||

| December 2020 (through December 17, 2020) | 5.061 | 5.125 | 5.058 | 5.279 | ||||||||||||

Source: Brazilian Central Bank.

| (1) | Represents the average of the exchange rates on the closing of each day during the year. |

| (2) | Represents the average of the exchange rates on the closing of each day during the month. |

xi

Questions and Answers About the Merger and the CZZ Special Meeting

The following questions and answers are intended to briefly address some commonly asked questions regarding the Merger Documents, the transactions contemplated thereby and the CZZ Special Meeting. These questions and answers only highlight some of the information contained in this prospectus and may not contain all of the information that is important to you. Please further refer to the section of this prospectus entitled “Summary” and the more detailed information contained elsewhere in this prospectus, the Exhibits to this prospectus and the documents referred to in this prospectus, which you should read carefully and in their entirety. You may obtain the information incorporated by reference into this prospectus without charge by following the instructions under the section of this prospectus entitled “Where You Can Find More Information.”

Questions and Answers About the Merger

| Q: | What is the proposed merger, why are CSAN and CZZ proposing it and what will happen to CZZ as a result of the merger? |

| A: | On July 3, 2020, CSAN, CZZ and CLOG, or collectively, the “Companies,” announced that their respective boards of directors had authorized the senior officers of the Companies to consider a Proposed Transaction proposal, which is intended to simplify Cosan Group’s corporate structure, unify and consolidate the current Companies’ free floats, increase stock liquidity and unlock value within the Cosan Group’s portfolio. |

The Proposed Transaction will consist of a merger of companies under common control, as provided for by art. 264, paragraph 4th, of Brazilian Law No. 6,404, pursuant to which CZZ and CLOG will be merged into CSAN. The merger of CZZ and CSAN is also subject to compliance with sections 104B to 109 of the Companies Act. Following completion of the Proposed Transaction, outstanding shares of CSAN will be directly owned by all shareholders of CSAN, CZZ and CLOG as of immediately prior to the completion of the Proposed Transaction, and CSAN will continue to be controlled by Aguassanta Investimentos S.A., or “Aguassanta,” which is Mr. Rubens Ometto Silveira Mello’s investment vehicle.

Once the Proposed Transaction is approved, CSAN will be consolidated as the group’s sole holding company, becoming the universal successor of (i) its subsidiary, CLOG; and (ii) its holding company, CZZ. Subject to the terms and conditions of the (i) Merger Documents between CZZ and CSAN, regarding the Merger; and (ii) the merger and justification protocol between the managements of CLOG and CSAN, regarding the merger of CLOG into CSAN, or the CSAN/CLOG Merger Protocol, the Proposed Transaction is expected to become effective during the first quarter of 2021, i.e., when the Merger is finally consummated, or the “Closing Date.” We refer to the Merger Protocol and the CSAN/CLOG Merger Protocol as the “Merger Protocols.”

The Proposed Transaction is being proposed by CSAN and CZZ to streamline and simplify the corporate governance structure of the Cosan Group, specifically by (i) centralizing decision-making across the Cosan Group, instead of the current situation in which each of CZZ, CSAN and CLOG have separate board of directors and executive officers; (ii) providing a simpler corporate structure within which fewer corporate and other approvals are necessary to conduct transactions as compared to the current situation in which there are multiple entities and corporate bodies involved in decision-making; and (iii) having a single class of shares in the holding company of the Cosan Group. We also expect that it will promote the unified structure of the group, consolidating the corporate interest held in the other companies of the group within one holding company. After the Merger, CZZ will cease to exist and all of its assets will be held by CSAN.

Pursuant to the terms and subject to the conditions set forth in the Merger Documents, upon the completion of the Merger each Class A Share, issued and outstanding immediately prior to the consummation of the Merger (other than as provided in the Merger Documents) will be automatically converted into the right to receive 1.29401595263 CSAN ADSs, and each Class B Share issued and outstanding immediately prior to the consummation of the Merger (other than as provided in the Merger Documents) will be automatically converted into the right to receive 1.29401595263 validly issued and allotted, fully paid-up CSAN Shares, in each case subject to approval of the terms of the Proposed Transaction by the boards of directors and shareholders of each of CSAN and CZZ. Following the Merger, any holder of CSAN ADSs may cause such CSAN ADSs to be cancelled and to have an equal number of validly issued and allotted, fully paid-up CSAN Shares issued to such holder in replacement thereof. The ADS Depositary has agreed to waive the cancellation fee for cancellations completed during the period of fifteen (15) calendar days after the completion of the Merger.

xii

CSAN and CLOG’s board of directors have established special independent committees in accordance with CVM’s Guidance Opinion No. 35, or “CVM Opinion No. 35,” to negotiate the exchange ratios for the exchange of (i) CZZ Shares for CSAN Shares or CSAN ADSs, as applicable, and (ii) common shares of CLOG, or “CLOG Shares” for CSAN Shares. CZZ also has its own independent committee, formed of independent directors of CZZ. For more details regarding these committees, see the questions “What are the special independent committees?” and “What factors will the Companies’ special independent committees consider in determining the exchange ratios for the exchange of (i) CZZ Shares for CSAN Shares or CSAN ADSs, as applicable and (ii) CLOG Shares for CSAN Shares?” below.

If the Merger is completed, CZZ will be merged with and into CSAN, with CSAN being the surviving corporation of the Merger. CZZ will be struck off by the Bermuda Registrar of Companies and will no longer exist as a separate company. Based on the number of CZZ Class A Shares and equity awards exercisable into CZZ Class A Shares, in each case issued and outstanding as of December 17, 2020 , it is anticipated that, immediately following completion of the Merger, former holders of CZZ Shares will own approximately 64 % of CSAN on a fully diluted basis.

In the course of reaching their decisions to approve the Merger Documents, the Merger and all of the other transactions and documents contemplated by the Merger, the board of directors of each CSAN and CZZ considered a number of important factors in their separate deliberations. For more details on these factors, see the sections of prospectus entitled “Summary—Reasons for the Proposed Transaction” and “The Merger—Recommendation of the CZZ Board of Directors, CZZ’s Reasons for the Merger.”

It is important that your shares be represented and voted at the CZZ Special Meeting.

| Q: | What is this document? |

| A: | This document, which we refer to as the prospectus: |

| · | serves as a prospectus of CSAN used to offer CSAN ADSs in exchange for Class A Shares and CSAN Shares in exchange for Class B Shares pursuant to the terms of the Merger Documents; |

| · | informs holders of CZZ Shares of the upcoming CZZ Special Meeting at which CZZ shareholders will vote on, among other things, the Merger Proposal, and provides details of the Merger Documents and the consideration CZZ shareholders will receive upon completion of the Merger; and |

| · | provides CZZ shareholders with important details about CSAN and their rights as potential holders of CSAN Common Shares or CSAN ADSs. |

| Q: | Why did I receive this prospectus and proxy card? |

| A: | You are receiving this prospectus because you are a shareholder of record of CZZ. This document serves as a prospectus of CSAN used to offer CSAN ADSs in exchange for Class A Shares and CSAN Shares in exchange for Class B Shares pursuant to the terms of the Merger Documents. In order to complete the Merger, among other things, CZZ shareholders must approve the Merger. CZZ is holding the CZZ Special Meeting to ask its shareholders to vote on the Merger. This document contains important information about the Merger and the CZZ Special Meeting, and you should read it carefully and in its entirety. The enclosed voting materials allow CZZ shareholders to vote their shares by proxy without attending the CZZ Special Meeting virtually. |

xiii

| Q: | Who is CSAN? |

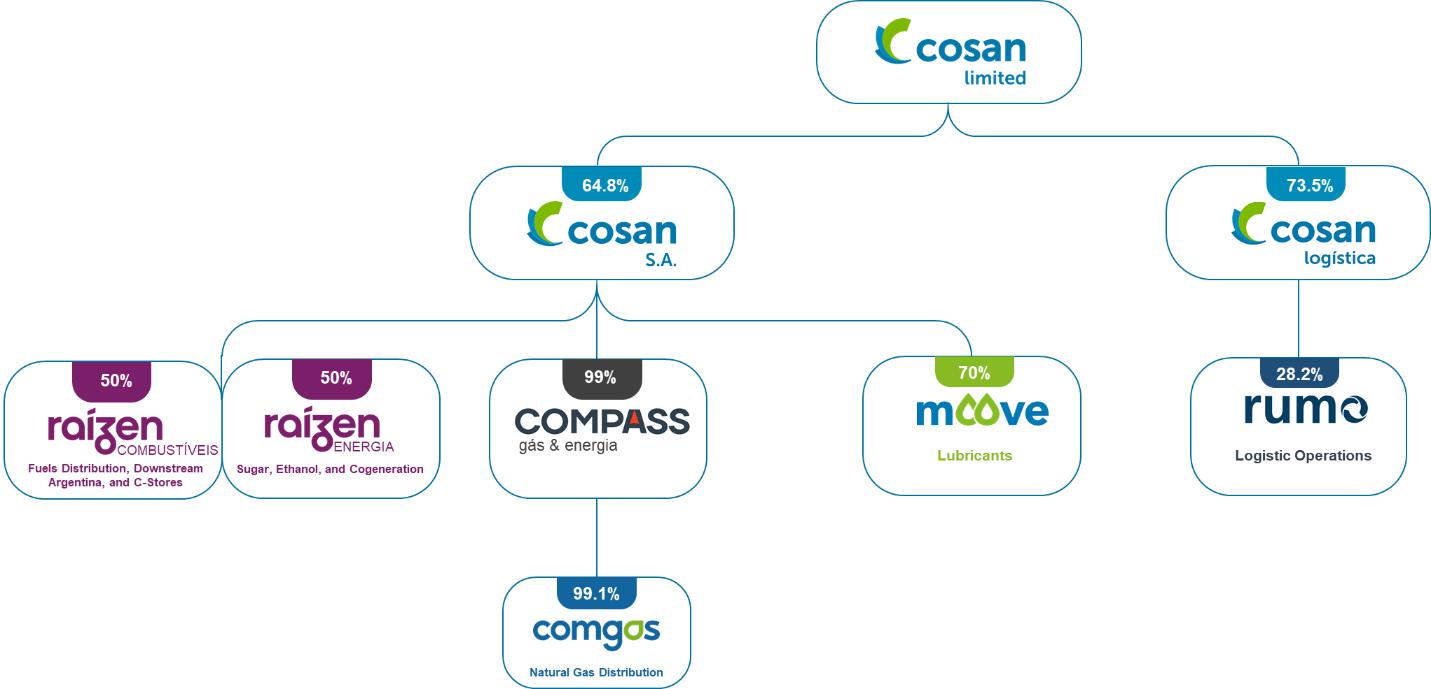

| A: | CSAN is a direct subsidiary of CZZ and one of the largest companies in Brazil, investing on strategic sectors such as the agribusiness, supply of fuel, natural gas and lubricants. CSAN has been in the market for over 80 years and during this period it has diversified its operations and its portfolio currently gathers companies such as Raízen Combustíveis, Raízen Energia, Comgás and Moove, reference companies in their respective sectors. |

Its principal place of business is located at Avenida Brigadeiro Faria Lima, No. 4,100 – 16th floor, São Paulo – SP, 04538-132, Brazil, telephone +55 11 3897-9797. Our website address is https://ri.cosan.com.br/en/.

See also the sections entitled “Information about the Companies—Cosan S.A./CSAN,” “Information About CSAN,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations of CSAN” and “Management and Compensation of CSAN” for further information regarding CSAN.

| Q: | Who is CLOG? |

| A: | CLOG is a direct subsidiary of CZZ and focuses on logistics services for rail transportation, storage and port loading of commodities, mainly for grains and sugar, leasing of locomotives, wagons and another railway equipment. |

CLOG’s principal place of business is located at Avenida Brigadeiro Faria Lima, No. 4,100 – 16th floor, São Paulo – SP, 04538-132, Brazil, telephone +55 11 3897-9797. Its website address is https://ri.cosanlogistica.com/en/.

See also the sections entitled “Information about the Companies—Cosan Logística S.A./CLOG” for further information regarding CLOG.

| Q: | What are the special independent committees? |

| A: | CSAN and CLOG’s board of directors have established special independent committees on a provisional basis, in accordance with CVM Opinion No. 35, to negotiate the exchange ratios for the exchange of (i) CZZ Shares for CSAN Shares or CSAN ADSs, as applicable, and (ii) CLOG Shares for CSAN Shares. The special independent committees of CSAN and CLOG were required by CVM Opinion No. 35 to assess the Proposed Transaction and make a recommendation with respect to the Proposed Transaction to the boards of directors of CSAN and CLOG, as applicable, to ensure that the Proposed Transaction is in the best interests of CSAN and CLOG, as applicable, and, that the Proposed Transaction is carried out on an arm’s length basis. |

The members of the CSAN and CLOG committees are all independent non-managers with relevant experience. The members were appointed by CSAN and CLOG’s board of directors in meetings held on August 4, 2020. CZZ also has its own independent committee, formed of independent directors of CZZ.

The members of the independent committees were appointed to: (i) assess the terms and conditions of the Proposed Transaction; (ii) negotiate the exchange ratios for the exchange of (a) CZZ Shares for CSAN Shares or CSAN ADSs, as applicable, (b) CLOG Shares for CSAN Shares, as well as the other terms and conditions of the Proposed Transaction; and (iii) make a recommendation to the boards of directors of CSAN and CLOG, as applicable, to comply with CVM Opinion No. 35, in order to protect the interests of minority shareholders of CSAN and CLOG.

| Q: | What factors will the Companies’ special independent committees consider in determining the exchange ratios for the exchange of (i) CZZ Shares for CSAN Shares or CSAN ADSs, as applicable, (ii) CLOG Shares for CSAN Shares? |

| A: | The Companies’ management recommended that the special committees take into account the following factors in determining the exchange ratio: (i) no holding discounts should apply; (ii) group entities and |

xiv

their underlying assets should be considered at fair market value; and (iii) the shareholders of all entities involved should be treated equally.

In addition, the Companies’ special independent committees took into account a number of factors following to determine the exchange ratios in connection with the Proposed Transaction including, among others, the recent and historical trading prices of the shares of each of CZZ, CSAN and CLOG.

See also “The Merger—Overview.”

| Q: | What are the exchange ratios? |

| A: | The exchange ratio for the exchange of CZZ Class A Shares for CSAN ADSs is 1.29401595263 CSAN ADSs for one CZZ Class A Share. The exchange ratio for the exchange of CZZ Class B Shares for CSAN Shares is 1.29401595263 CSAN Shares for one CZZ Class B Share. The exchange ratio for the exchange of CLOG Shares for CSAN Shares is 0.25360679585 CSAN Shares for one CLOG Share. |

This is equivalent to 0.772788 CZZ Shares for each CSAN Share or CSAN ADS, as applicable, and 3.943112 CLOG Shares for each CSAN Share.

| Q: | What will CZZ shareholders receive from the Merger? |

| A: | Pursuant to the terms and subject to the conditions set forth in the Merger Documents, upon the completion of the Merger, each Class A Share issued and outstanding immediately prior to the consummation of the Merger (other than as provided in the Merger Documents) will be automatically converted into the right to receive 1.29401595263 CSAN ADSs, and each Class B Share issued and outstanding immediately prior to the consummation of the Merger (other than as provided in the Merger Documents) will be automatically converted into the right to receive 1.29401595263 validly issued and allotted, fully paid-up CSAN Shares, in each case subject to approval of the terms of the Proposed Transaction by the boards of directors and shareholders of each of CSAN and CZZ. Following the Merger, any holder of CSAN ADSs may cause such CSAN ADSs to be cancelled and to have an equal number of validly issued and allotted, fully paid-up CSAN Shares issued to such holder in replacement thereof. The ADS Depositary has agreed to waive the cancellation fee for cancellations completed during the period of fifteen (15) calendar days after the completion of the Merger. |

| Q: | What percentage ownership will former CZZ shareholders hold in CSAN following completion of the Merger? |

| A: | If the Merger is completed, CZZ will be merged with and into CSAN, with CSAN being the surviving corporation of the Merger. CZZ will be struck off by the Bermuda Registrar of Companies and will no longer exist as a separate company. Based on the number of CZZ Class A Shares and equity awards exercisable into CZZ Class A Shares, in each case issued and outstanding as of December 17, 2020 , it is anticipated that, immediately following completion of the Merger, former holders of CZZ Shares will own approximately 64 % of CSAN on a fully diluted basis. |

| Q: | If the Merger is completed, will the CSAN ADSs be listed for trading? |

| A: | Yes. The CSAN ADSs which CZZ common shareholders will receive in the Merger are expected to be listed on the NYSE on the Closing Date. Completion of the Merger is subject to the CSAN ADSs being approved for listing on the NYSE, subject to official notice of issuance. CSAN ADSs received by CZZ common shareholders in the Merger are expected to be freely transferable subject to applicable securities laws. |

| Q: | When do you expect the Merger and the Proposed Transaction to be completed? |

| A: | The Merger and the Proposed Transaction are expected to close in the first quarter of 2021, subject to the approvals of CSAN, CLOG and CZZ shareholders, regulatory approvals and consents and other customary closing conditions. |

| Q: | What happens if the Merger and/or the Proposed Transaction are not completed? |

| A: | If CZZ’s shareholders do not approve the Merger, or if the Proposed Transaction is not completed for any other reason, CLOG and CZZ will remain independent public companies and CLOG Shares and CZZ Class |

xv

A Shares will continue to be listed and traded on the B3 and the NYSE, respectively. CZZ will continue to be registered under the Exchange Act and file periodic reports with the SEC.

| Q: | What regulatory approvals are needed to complete the Merger? |

| A: | In order to complete the Merger, CZZ is required to apply to the Minister of Finance (acting through the Registrar of Companies) in Bermuda to have Brazil approved as a jurisdiction pursuant to section 104B(2)(d)(iii) of the Companies Act and the Minister will need to provide such approval. |

Questions and Answers About the CZZ Special Meeting

| Q: | When and where will the special meetings be held? |

| A: | The CZZ Special Meeting will be held on January 22 , 2021, at 10 a.m., São Paulo time on a digital platform provided by Computershare Trust Company, N.A. |

| Q: | Why are you holding a virtual meeting instead of a physical meeting? |

| A: | CZZ is excited to embrace the latest technology to provide expanded access, improved communication and cost savings for CZZ and its shareholders. CZZ believes that hosting a virtual meeting will enable more of its shareholders to attend and participate in the meeting since CZZ’s shareholders can participate from any location around the world with Internet access. In addition, CZZ believes that hosting the meeting virtually is safer for all parties involved given the ongoing COVID-19 pandemic. |

| Q: | Who is entitled to vote at the special meetings? |

| A: | Only holders of record of Class A Shares and Class B Shares of CZZ at the close of business on January 4, 2021 , the Record Date for voting at the CZZ Special Meeting, or the “Record Date,” are entitled to vote at the CZZ Special Meeting. |

| Q: | How can I attend the CZZ Special Meeting? |

| A: | The CZZ Special Meeting will be a completely virtual meeting of shareholders, which will be conducted exclusively by webcast. You will only be entitled to participate in the CZZ Special Meeting if you are a shareholder of CZZ as of the close of business on the Record Date, or if you hold a valid proxy for the CZZ Special Meeting. No physical meeting will be held. |

You will be able to attend the CZZ Special Meeting online and submit your questions during the meeting. You also will be able to vote your shares online by attending the CZZ Special Meeting by webcast.

To participate in the CZZ Special Meeting, you will need to review the information included on your notice, on your proxy card or on the instructions that accompanied your proxy materials. Instructions for accessing the digital platform, including the necessary password, will be sent to shareholders who contact Georgeson LLC, the Information Agent for the Merger, indicating their interest in participating virtually by email to cosan@georgeson.com by 5:00 p.m., Eastern Time, on January 19, 2021 .

xvi

If you hold your CZZ Shares through an intermediary, such as a bank or broker, you must register in advance using the instructions below under “How do I register to attend the CZZ Special Meeting virtually on the Internet?”

The online meeting will begin promptly on January 22 , 2021 at 10 a.m., São Paulo time . We encourage you to access the meeting prior to the start time leaving ample time for the check in. Please follow the registration instructions as outlined in this prospectus.

| Q: | How do I register to attend the CZZ Special Meeting virtually on the Internet? |

| A: | If you are a registered shareholder (i.e., you hold your CZZ Shares through CZZ’s transfer agent, Computershare Trust Company, N.A.), you do not need to register to attend the CZZ Special Meeting virtually on the Internet. Please follow the instructions on the notice or proxy card that you received. |

If you hold your CZZ Shares through an intermediary, such as a bank or broker, you must register in advance to attend the CZZ Special Meeting virtually on the Internet.

To register to attend the CZZ Special Meeting online by webcast you must submit proof of your proxy power (legal proxy) reflecting your holdings in CZZ Shares along with your name and email address to Computershare Trust Company, N.A., the Tabulation Agent for the Merger. Requests for registration must be labeled as “Legal Proxy” and be received no later than 5:00 p.m., Eastern Time, on January 19, 2021 .

You will receive a confirmation of your registration by email after your registration materials are received.

Requests for registration should be directed to Computershare at the following:

By email

Forward the email from your broker, or attach

an image of your legal proxy, to

legalproxy@computershare.com

By mail

Computershare

Cosan Limited Legal Proxy

P.O. Box 43001

Providence, RI 02940-3001

| Q: | What proposals will be considered at the CZZ special meeting? |

| A: | At the CZZ Special Meeting, CZZ shareholders will be asked to consider and vote on a proposal to approve the Merger Documents and the transactions contemplated therein, including the Merger, which we refer to as the Merger Proposal. |

| Q: | How does the CZZ board of directors recommend that I vote? |

| A: | The CZZ board of directors unanimously approved the rationale behind the Proposed Transaction and instructed management to further assess its adoption and implementation. The Merger Documents are yet to be prepared and negotiated and the board of directors of CZZ will deliberate whether such Merger Documents are advisable, fair and in the best interests of CZZ in due course. |

The CZZ board unanimously recommends that the CZZ shareholders vote “FOR” the Merger Proposal.

xvii

| Q: | How do I vote? |

| A: | If you are a holder of record of Class A Shares or Class B Shares of CZZ as of the close of business on the Record Date for the CZZ Special Meeting, you may vote virtually by attending the CZZ Special Meeting or, to ensure your shares are represented at the CZZ Special Meeting, you may vote by marking, signing, dating and returning the enclosed proxy card in the postage-paid envelope provided. Proxy cards, accompanied by their respective proof of representation and shareholding, must be sent to Computershare Trust Company, N.A., the Tabulation Agent for the Merger at its address set forth below: |

By

Express Mail, Courier, or Other Expedited Service:

Computershare Trust

Company, N.A.

Proxy Services

462 South 4th Street, Suite 1600, Louisville, KY, 40202, United States

By

Mail:

Proxy Services

c/o Computershare

PO Box 505008 Louisville, KY 40233-9814

If your shares are held in street name, through a broker, bank, trustee or other nominee, please follow the instructions on a voting instruction card furnished by the record holder.

| Q: | What is a “broker non-vote”? |

| A: | Under NYSE rules, banks, brokers and other nominees may use their discretion to vote “uninstructed” shares (i.e., shares held of record by banks, brokerage firms or other nominees but with respect to which the beneficial owner of such shares has not provided instructions on how to vote on a particular proposal) with respect to matters that are considered to be “routine,” but not with respect to “non-routine” matters. “Non-routine” matters are matters that may substantially affect the rights or privileges of shareholders, such as mergers, shareholder proposals, elections of directors (even if not contested), executive compensation (including any advisory shareholder votes on executive compensation) and certain corporate governance proposals, even if management-supported. A “broker non-vote” occurs on an item when (i) a broker, nominee or intermediary has discretionary authority to vote on one or more proposals to be voted on at a meeting of shareholders, but is not permitted to vote on other proposals without instructions from the beneficial owner of the shares and (ii) the beneficial owner fails to provide the broker, nominee or intermediary with such instructions. Because none of the proposals to be voted on at the CZZ Special Meeting are routine matters for which brokers may have discretionary authority to vote, CZZ does not expect there to be any broker non-votes at the CZZ Special Meeting. |

| Q: | What vote is required to adopt the Merger Proposal? |

| A: | Approving the Merger Proposal requires the affirmative vote of a majority of 75% of the outstanding Class A Shares and Class B Shares in attendance and voting on the matter at the CZZ Special Meeting, voting together as a single class. Accordingly, a CZZ shareholder’s failure to submit a proxy card or to vote virtually at the CZZ Special Meeting, an abstention from voting, or a broker non-vote will have the same effect as a vote “AGAINST” the Merger Proposal. |

As of the close of business on December 17, 2020, Mr. Rubens Ometto Silveira Mello controlled CZZ Shares representing approximately 90.19% of the total voting power of the shares entitled to vote at the CZZ Special Meeting. It is currently expected that Mr. Rubens Ometto Silveira Mello will vote in favor of the Merger Proposal. The affirmative vote of all CZZ Shares controlled by Mr. Rubens Ometto Silveira Mello in favor of the Merger Proposal constitutes sufficient votes to approve the Merger Proposal at the CZZ Special Meeting.

xviii

| Q: | How many votes do I have? |

| A: | You are entitled to cast one vote for each Class A Share and 10 votes for each of Class B Share that you owned as of the close of business on the Record Date for the CZZ Special Meeting. As of the close of business on December 17, 2020 , there were 142,115,534 Class A Shares issued and outstanding entitled to vote at the CZZ Special Meeting and 96,332,044 Class B Shares issued and outstanding entitled to vote at the CZZ Special Meeting. |

| Q: | What constitutes a quorum? |

| A: | A quorum of shareholders is necessary to transact business at the CZZ Special Meeting. The presence at the meeting, virtually or by proxy, of two shareholders at least holding or representing by proxy more than forty-five percent (45%) of the issued shares of CZZ outstanding as of the close of business on the Record Date and entitled to vote at the CZZ Special Meeting will constitute a quorum for the CZZ Special Meeting. |

| Q: | If my shares are held in “street name” by my broker, will my broker automatically vote my shares for me? |

| A: | No. If you hold your CZZ Shares in a stock brokerage account or if your shares are held by a bank or nominee, that is, in “street name,” your broker, bank, trust company or other nominee cannot vote your shares on “non-routine” matters without instructions from you. You should instruct your broker, bank, trust company or other nominee as to how to vote your shares, following the directions provided by your broker, bank, trust company or other nominee to you. Please check the voting form used by your broker, bank, trust company or other nominee. |

If you do not provide your broker, bank, trust company or other nominee with instructions, your broker, bank, trust company or other nominee will not submit a proxy, your CZZ shares will not be counted for purposes of determining a quorum at the CZZ Special Meeting, and will not be voted on the Merger Proposal.

| Q: | What will happen if I return my proxy card without indicating how to vote? |

| A: | If you are a registered holder of record and you return your signed proxy card but do not indicate your voting preferences, the persons named in the proxy card will vote the shares represented by that proxy as recommended by the CZZ board of directors. |

Please note that you may not vote shares held in street name by returning a proxy card directly to CZZ, or by voting virtually at the CZZ Special Meeting unless you provide a “legal proxy”, which you must obtain from your broker, bank, trust company or other nominee.

If you do not instruct your broker on how to vote your CZZ shares, your broker may not vote your CZZ shares, which will have the same effect as a vote “AGAINST” the Merger Proposal. However, because the Merger Proposal to be voted on at the CZZ Special Meeting is not a routine matter for which brokers may have discretionary authority to vote, CZZ does not expect any broker non-votes at the CZZ Special Meeting.

| Q: | Can I change my vote after I have returned a proxy or voting instruction card? |

| A: | Yes. You can change your vote or revoke your proxy at any time before it is exercised at the CZZ Special Meeting by doing any of the following: |

| · | by sending a written notice of revocation to Georgeson LLC, the Information Agent for the Merger, at 1290 Avenue of the Americas, 9th Floor New York, NY 10104, or by email to cosan@georgeson.com, which notice must be received at least three business days before the CZZ Special Meeting; |

xix

| · | by properly submitting a later-dated, new proxy card, which must be received by the Tabulation Agent before your CZZ Shares are voted at the CZZ Special Meeting (in which case only the later-dated proxy is counted and the earlier proxy is revoked); |

| · | attending the CZZ Special Meeting virtually by accessing the digital platform and voting via the digital platform. Attendance at the CZZ Special Meeting will not, however, in and of itself, constitute a vote or revocation of a prior proxy. |

If you hold your CZZ Shares in street name, then you must change your voting instruction by submitting new voting instructions to the broker, bank or other nominee that holds your CZZ Shares.

| Q: | What happens if I transfer my CZZ Shares before the CZZ Special Meeting? |

| A: | The Record Date for the CZZ Special Meeting is earlier than both the date of the CZZ Special Meeting and the date that the Merger is expected to be completed. If you transfer your CZZ Shares after the Record Date but before the CZZ Special Meeting, you will retain your right to vote at the CZZ Special Meeting. |

| Q: | Do CZZ shareholders have appraisal or dissenters’ rights? |

| A: | The holders of CZZ Shares of record, under Bermuda law, are entitled to appraisal rights in connection with the Merger. See “The Merger—Dissenters’ Rights of Appraisal for CZZ Shareholders.” |

| Q: | Where can I find the voting results of the CZZ Special Meeting? |

| A: | The preliminary voting results are expected to be announced at the CZZ Special Meeting. In addition, within two business days following certification of the final voting results, CZZ intends to furnish on Form 6-K the final voting results of its special meeting with the SEC. |

| Q: | What do I need to do now? |

| A: | Carefully read and consider the information contained in and incorporated by reference into this prospectus. |

If you are a holder of record, in order for your shares to be represented at your special meeting, you must:

| · | attend the CZZ Special Meeting virtually; |

| · | vote through the Internet (if applicable) or by telephone by following the instructions included on your proxy card; or |

| · | indicate on the enclosed proxy card how you would like to vote and return the proxy card in the accompanying pre-addressed postage paid envelope. |

If you hold your CZZ Shares in street name, in order for your shares to be represented at your special meeting, you should instruct your broker, bank, trust company or other nominee as to how to vote your shares, following the directions provided to you by your broker, bank, trust company or other nominee.

| Q: | Who can help answer my questions? |

| A: | CZZ shareholders who have questions about the Merger Documents or the Merger, who need assistance submitting their proxy or voting shares or who desire additional copies of this prospectus or additional proxy cards should contact Georgeson LLC, the Information Agent for the Merger: |

xx

Georgeson

LLC

1290 Avenue of the Americas, 9th Floor

New York, NY 10104

cosan@georgeson.com

Shareholders, Banks and Brokers may call toll free: (866) 257-5415

xxi

The following is a summary that highlights information contained in this prospectus. This summary may not contain all the information that is important to you. For a more complete description of the Merger and the Merger Documents, we encourage you to read carefully this entire prospectus, including the Exhibits to the registration statement of which this prospectus is a part. In addition, we encourage you to read the information incorporated by reference into this prospectus, which includes important business and financial information about CZZ that has been filed with the SEC. You may obtain the information incorporated by reference into this prospectus without charge by following the instructions in the section of this prospectus entitled “Where You Can Find More Information.”

Cosan S.A./CSAN