UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

(Mark One) | |

þ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2016 | |

OR | |

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to . | |

Commission file number: 001-35120

CVR Partners, LP

(Exact name of registrant as specified in its charter)

Delaware | 56-2677689 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

2277 Plaza Drive, Suite 500 | |

Sugar Land, Texas (Address of principal executive offices) | 77479 (Zip Code) |

(281) 207-3200

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer o | Accelerated filer þ | Non-accelerated filer o | Smaller reporting company o | |||

(Do not check if smaller reporting company.) | ||||||

Indicate by check mark whether the registrant is a shell company (as defined by Rule 12b-2 of the Exchange Act). Yes o No þ

There were 113,282,973 common units outstanding at October 25, 2016.

CVR PARTNERS, LP AND SUBSIDIARIES

INDEX TO QUARTERLY REPORT ON FORM 10-Q

For The Quarter Ended September 30, 2016

Page No. | ||

2

GLOSSARY OF SELECTED TERMS

The following are definitions of certain terms used in this Quarterly Report on Form 10-Q for the quarter ended September 30, 2016 (this "Report"):

2015 Form 10-K | The Partnership's Annual Report on Form 10-K for the year ended December 31, 2015, filed with the SEC on February 18, 2016. |

2021 Notes | $320.0 million aggregate principal amount of 6.50% Senior Notes due 2021, which were issued by CVR Nitrogen and CVR Nitrogen Finance. In June 2016 the majority of the Notes were repaid. $4.2 million aggregate principal amount of the Notes remain outstanding as of September 30, 2016. |

2023 Notes | $645.0 million aggregate principal amount of 9.25% Senior Notes due 2023, which were issued through CVR Partners and CVR Nitrogen Finance. |

ABL Credit Facility | The Partnership's senior secured asset based revolving credit facility with a group of lenders and UBS AG, Stamford Branch, as administrative agent and collateral agent. |

ammonia | Ammonia is a direct application fertilizer and is primarily used as a building block for other nitrogen products for industrial applications and finished fertilizer products. |

capacity | Capacity is defined as the throughput a process unit is capable of sustaining, either on a calendar or stream day basis. The throughput may be expressed in terms of maximum sustainable, nameplate or economic capacity. The maximum sustainable or nameplate capacities may not be the most economical. The economic capacity is the throughput that generally provides the greatest economic benefit based on considerations such as feedstock costs, product values and downstream unit constraints. |

catalyst | A substance that alters, accelerates, or instigates chemical changes, but is neither produced, consumed nor altered in the process. |

Change of Control Offer | The offer commenced on April 29, 2016 by the CVR Nitrogen and CVR Nitrogen Finance to purchase any and all of the outstanding 2021 Notes at 101% of par value. |

Coffeyville Facility | CVR Partners' nitrogen fertilizer manufacturing facility located in Coffeyville, Kansas. |

common units | Common units representing limited partner interests of CVR Partners. |

corn belt | The primary corn producing region of the United States, which includes Illinois, Indiana, Iowa, Minnesota, Missouri, Nebraska, Ohio and Wisconsin. |

Credit Agreement | CRNF's $125.0 million term loan, $25.0 million revolving and $50.0 million uncommitted incremental credit facility, guaranteed by the Partnership, entered into with a group of lenders including Goldman Sachs Lending Partners LLC, as administrative and collateral agent, which was repaid in full and terminated on April 1, 2016. |

Credit Parties | The Partnership and certain subsidiaries party to the ABL Credit Facility. |

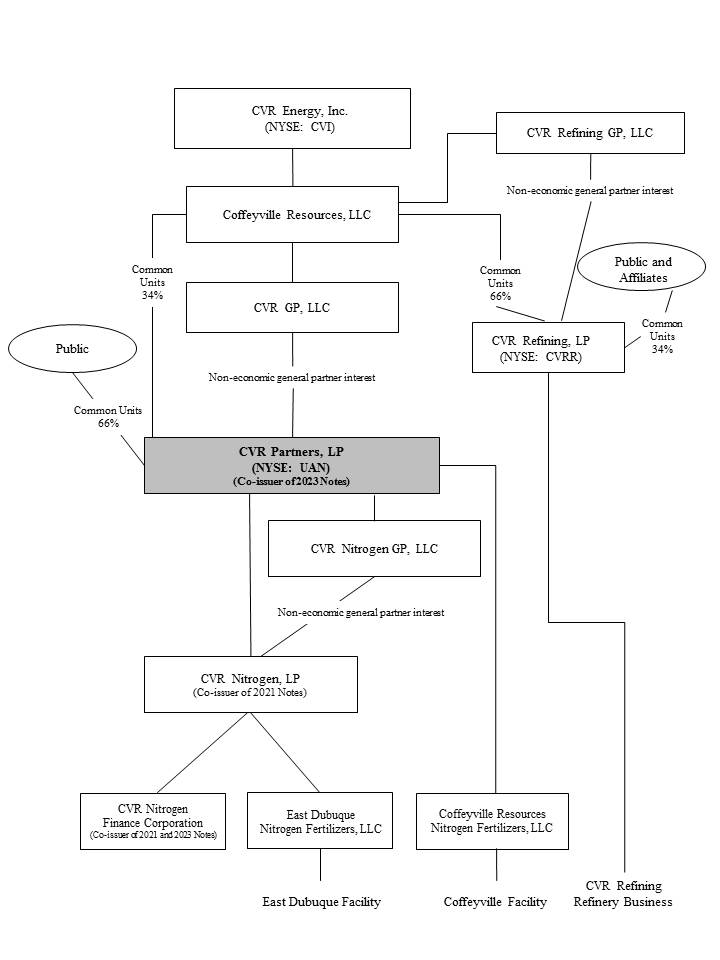

CRLLC | Coffeyville Resources, LLC, the subsidiary of CVR Energy which directly owns our general partner and 38,920,000 common units. |

CRLLC Facility | The Partnership's $300.0 million senior term loan credit facility with CRLLC, which was repaid in full and terminated on June 10, 2016. |

CRNF | Coffeyville Resources Nitrogen Fertilizers, LLC. |

CVR Energy | CVR Energy, Inc., a publicly traded company listed on the New York Stock Exchange under the ticker symbol "CVI," which indirectly owns our general partner and the common units owned by CRLLC. |

CVR Nitrogen Finance | CVR Nitrogen Finance Corporation, an indirect wholly-owned subsidiary of the Partnership (formerly known as East Dubuque Finance Corporation and also formerly known as Rentech Nitrogen Finance Corporation). |

3

CVR Nitrogen | CVR Nitrogen, LP (formerly known as East Dubuque Nitrogen Partners, L.P. and also formerly known as Rentech Nitrogen Partners L.P.). |

CVR Nitrogen GP | CVR Nitrogen GP, LLC (formerly known as East Dubuque Nitrogen GP, LLC and also formerly known as Rentech Nitrogen GP, LLC). |

CVR Partners | CVR Partners, LP. |

CVR Refining | CVR Refining, LP, a publicly traded limited partnership listed on the New York Stock Exchange under the ticker symbol "CVRR," which currently owns and operates a complex full coking medium-sour crude oil refinery with a rated capacity of 115,000 barrels per calendar day (bpcd) in Coffeyville, Kansas, a complex crude oil refinery with a rated capacity of 70,000 bpcd in Wynnewood, Oklahoma and ancillary businesses. |

East Dubuque Facility | CVR Partners' nitrogen fertilizer manufacturing facility located in East Dubuque, Illinois. |

East Dubuque Merger | The transactions contemplated by the Merger Agreement, whereby the Partnership acquired CVR Nitrogen and CVR Nitrogen GP on April 1, 2016. |

EDNF | East Dubuque Nitrogen Fertilizers, LLC (formerly known as Rentech Nitrogen, LLC). |

farm belt | Refers to the states of Illinois, Indiana, Iowa, Kansas, Minnesota, Missouri, Nebraska, North Dakota, Ohio, Oklahoma, South Dakota, Texas and Wisconsin. |

GAAP | U.S. generally accepted accounting principles. |

general partner | CVR GP, LLC, our general partner, which is a wholly-owned subsidiary of CRLLC. |

Merger Agreement | The Agreement and Plan of Merger, dated as of August 9, 2015, whereby the Partnership acquired CVR Nitrogen and CVR Nitrogen GP. |

Mid Corn Belt | Primarily includes Illinois, Indiana, Iowa, Missouri, Nebraska and Kansas. |

MMBtu | One million British thermal units: a measure of energy. One Btu of heat is required to raise the temperature of one pound of water one degree Fahrenheit. |

MSCF | One thousand standard cubic feet, a customary gas measurement. |

netback | Netback represents net sales less freight revenue divided by product sales volume in tons. Netback is also referred to as product pricing at gate. |

on-stream | Measurement of the reliability of the gasification, ammonia and UAN units, defined as the total number of hours operated by each unit divided by the total number of hours in the reporting period. |

Partnership | CVR Partners, LP. |

pet coke | Petroleum coke - a coal-like substance that is produced during the oil refining process. |

product pricing at gate | Product pricing at gate represents net sales less freight revenue divided by product sales volume in tons. Product pricing at gate is also referred to as netback. |

Southern Plains | Primarily includes Oklahoma, Texas and New Mexico. |

Tender Offer | The cash tender offer commenced on April 29, 2016 by CVR Nitrogen and CVR Nitrogen Finance to purchase any and all of the outstanding 2021 Notes at 101.5% of par value. |

throughput | The volume processed through a unit. |

ton | One ton is equal to 2,000 pounds. |

turnaround | A periodically required standard procedure to refurbish and maintain a facility that involves the shutdown and inspection of major processing units. |

UAN | UAN is an aqueous solution of urea and ammonium nitrate used as a fertilizer. |

4

Wells Fargo Credit Agreement | CVR Nitrogen's credit agreement with Wells Fargo Bank, National Association, as successor-in-interest by assignment from General Electric Company, as administrative agent, which was repaid in April 2016 and terminated. |

wheat belt | The primary wheat producing region of the United States, which includes Oklahoma, Kansas, North Dakota, South Dakota and Texas. |

5

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements

CVR PARTNERS, LP AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

September 30, 2016 | December 31, 2015 | ||||||

(unaudited) | |||||||

(in thousands, except unit data) | |||||||

ASSETS | |||||||

Current assets: | |||||||

Cash and cash equivalents | $ | 65,296 | $ | 49,967 | |||

Accounts receivable, net of allowance for doubtful accounts of $41 and $27, at September 30, 2016 and December 31, 2015, respectively | 12,710 | 7,187 | |||||

Inventories | 56,888 | 37,529 | |||||

Prepaid expenses and other current assets, including $701 and $883 from affiliates at September 30, 2016 and December 31, 2015, respectively | 4,992 | 3,862 | |||||

Total current assets | 139,886 | 98,545 | |||||

Property, plant, and equipment, net of accumulated depreciation | 1,140,165 | 393,133 | |||||

Goodwill | 40,969 | 40,969 | |||||

Other long-term assets, including $643 and $777 with affiliates at September 30, 2016 and December 31, 2015, respectively | 5,837 | 3,608 | |||||

Total assets | $ | 1,326,857 | $ | 536,255 | |||

LIABILITIES AND PARTNERS’ CAPITAL | |||||||

Current liabilities: | |||||||

Accounts payable, including $1,980 and $1,940 due to affiliates at September 30, 2016 and December 31, 2015, respectively | $ | 22,190 | $ | 11,103 | |||

Personnel accruals, including $2,181 and $1,974 with affiliates at September 30, 2016 and December 31, 2015, respectively | 8,103 | 5,999 | |||||

Deferred revenue | 5,294 | 3,129 | |||||

Accrued expenses and other current liabilities, including $2,305 and $2,334 with affiliates at September 30, 2016 and December 31, 2015, respectively | 26,065 | 5,683 | |||||

Total current liabilities | 61,652 | 25,914 | |||||

Long-term liabilities: | |||||||

Long-term debt, net of current portion | 624,497 | 124,773 | |||||

Other long-term liabilities | 1,257 | 16 | |||||

Total long-term liabilities | 625,754 | 124,789 | |||||

Commitments and contingencies | |||||||

Partners’ capital: | |||||||

Common unitholders, 113,282,973 and 73,128,269 units issued and outstanding at September 30, 2016 and December 31, 2015, respectively | 639,450 | 385,670 | |||||

General partner interest | 1 | 1 | |||||

Accumulated other comprehensive loss | — | (119 | ) | ||||

Total partners’ capital | 639,451 | 385,552 | |||||

Total liabilities and partners’ capital | $ | 1,326,857 | $ | 536,255 | |||

See accompanying notes to the condensed consolidated financial statements.

6

CVR PARTNERS, LP AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||||||

(unaudited) | |||||||||||||||

(in thousands, except per unit data) | |||||||||||||||

Net sales | $ | 78,474 | $ | 49,325 | $ | 271,363 | $ | 223,190 | |||||||

Operating costs and expenses: | |||||||||||||||

Cost of product sold (exclusive of depreciation and amortization) — Affiliates | 529 | 1,147 | 1,886 | 5,149 | |||||||||||

Cost of product sold (exclusive of depreciation and amortization) — Third parties | 19,282 | 13,354 | 70,355 | 50,545 | |||||||||||

19,811 | 14,501 | 72,241 | 55,694 | ||||||||||||

Direct operating expenses (exclusive of depreciation and amortization) — Affiliates | 1,106 | 1,030 | 3,207 | 3,252 | |||||||||||

Direct operating expenses (exclusive of depreciation and amortization) — Third parties | 31,460 | 32,149 | 107,193 | 79,487 | |||||||||||

32,566 | 33,179 | 110,400 | 82,739 | ||||||||||||

Selling, general and administrative expenses (exclusive of depreciation and amortization) — Affiliates | 3,560 | 3,661 | 10,939 | 10,289 | |||||||||||

Selling, general and administrative expenses (exclusive of depreciation and amortization) — Third parties | 3,701 | 2,381 | 11,057 | 4,859 | |||||||||||

7,261 | 6,042 | 21,996 | 15,148 | ||||||||||||

Depreciation and amortization | 16,452 | 7,409 | 40,987 | 21,238 | |||||||||||

Total operating costs and expenses | 76,090 | 61,131 | 245,624 | 174,819 | |||||||||||

Operating income (loss) | 2,384 | (11,806 | ) | 25,739 | 48,371 | ||||||||||

Other income (expense): | |||||||||||||||

Interest expense and other financing costs | (15,633 | ) | (1,727 | ) | (32,820 | ) | (5,141 | ) | |||||||

Interest income | — | 10 | 4 | 34 | |||||||||||

Loss on extinguishment of debt | — | — | (5,116 | ) | — | ||||||||||

Other income, net | 26 | 54 | 83 | 65 | |||||||||||

Total other expense | (15,607 | ) | (1,663 | ) | (37,849 | ) | (5,042 | ) | |||||||

Income (loss) before income tax expense | (13,223 | ) | (13,469 | ) | (12,110 | ) | 43,329 | ||||||||

Income tax expense | 207 | 9 | 284 | 17 | |||||||||||

Net income (loss) | $ | (13,430 | ) | $ | (13,478 | ) | $ | (12,394 | ) | $ | 43,312 | ||||

Net income (loss) per common unit – basic | $ | (0.12 | ) | $ | (0.18 | ) | $ | (0.12 | ) | $ | 0.59 | ||||

Net income (loss) per common unit – diluted | $ | (0.12 | ) | $ | (0.18 | ) | $ | (0.12 | ) | $ | 0.59 | ||||

Weighted-average common units outstanding: | |||||||||||||||

Basic | 113,283 | 73,123 | 99,947 | 73,123 | |||||||||||

Diluted | 113,283 | 73,123 | 99,947 | 73,131 | |||||||||||

See accompanying notes to the condensed consolidated financial statements.

7

CVR PARTNERS, LP AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||||||

(unaudited) | |||||||||||||||

(in thousands) | |||||||||||||||

Net income (loss) | $ | (13,430 | ) | $ | (13,478 | ) | $ | (12,394 | ) | $ | 43,312 | ||||

Other comprehensive income (loss): | |||||||||||||||

Change in fair value of interest rate swaps | — | (22 | ) | — | (132 | ) | |||||||||

Net loss reclassified into income on settlement of interest rate swaps | — | 265 | 119 | 798 | |||||||||||

Other comprehensive income | — | 243 | 119 | 666 | |||||||||||

Total comprehensive income (loss) | $ | (13,430 | ) | $ | (13,235 | ) | $ | (12,275 | ) | $ | 43,978 | ||||

See accompanying notes to the condensed consolidated financial statements.

8

CVR PARTNERS, LP AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENT OF PARTNERS’ CAPITAL

Common Units | General Partner Interest | Accumulated Other Comprehensive Income/(Loss) | Noncontrolling Interest | Total | ||||||||||||||||||

Issued | Amount | |||||||||||||||||||||

(unaudited) | ||||||||||||||||||||||

(in thousands, except unit data) | ||||||||||||||||||||||

Balance at December 31, 2015 | 73,128,269 | $ | 385,670 | $ | 1 | $ | (119 | ) | $ | — | $ | 385,552 | ||||||||||

Cash distributions to common unitholders – Affiliates | — | (27,633 | ) | — | — | — | (27,633 | ) | ||||||||||||||

Cash distributions to common unitholders – Non-affiliates | — | (41,956 | ) | — | — | — | (41,956 | ) | ||||||||||||||

Share-based compensation – Affiliates | — | (1 | ) | — | — | — | (1 | ) | ||||||||||||||

Issuance of common units for the merger consideration | 40,154,704 | 335,693 | — | — | — | 335,693 | ||||||||||||||||

Noncontrolling interest | — | — | — | — | 4,564 | 4,564 | ||||||||||||||||

Contribution from affiliates | — | — | — | — | 507 | 507 | ||||||||||||||||

Purchase of noncontrolling interest | — | 71 | — | — | (5,071 | ) | (5,000 | ) | ||||||||||||||

Net income (loss) | — | (12,394 | ) | — | — | — | (12,394 | ) | ||||||||||||||

Other comprehensive income | — | — | — | 119 | — | 119 | ||||||||||||||||

Balance at September 30, 2016 | 113,282,973 | $ | 639,450 | $ | 1 | $ | — | $ | — | $ | 639,451 | |||||||||||

See accompanying notes to the condensed consolidated financial statements.

9

CVR PARTNERS, LP AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

Nine Months Ended September 30, | |||||||

2016 | 2015 | ||||||

(unaudited) | |||||||

(in thousands) | |||||||

Cash flows from operating activities: | |||||||

Net income (loss) | $ | (12,394 | ) | $ | 43,312 | ||

Adjustments to reconcile net income to net cash provided by operating activities: | |||||||

Depreciation and amortization | 40,987 | 21,238 | |||||

Allowance for doubtful accounts | 14 | (13 | ) | ||||

Amortization of deferred financing costs and original issue discount | 1,024 | 721 | |||||

Amortization of debt fair value adjustment | 1,250 | — | |||||

(Gain) loss on disposition of fixed assets | 127 | (24 | ) | ||||

Loss on extinguishment of debt | 5,116 | — | |||||

Share-based compensation – Affiliates | 1,178 | 1,480 | |||||

Share-based compensation | 653 | 305 | |||||

Change in assets and liabilities: | |||||||

Accounts receivable | 3,404 | (716 | ) | ||||

Inventories | 32,244 | (1,102 | ) | ||||

Prepaid expenses and other current assets | 4,218 | 3,680 | |||||

Other long-term assets | (489 | ) | (169 | ) | |||

Accounts payable | 1,580 | 3,326 | |||||

Deferred revenue | (27,672 | ) | (11,212 | ) | |||

Accrued expenses and other current liabilities | (4,008 | ) | (3,736 | ) | |||

Other long-term liabilities | 277 | — | |||||

Net cash provided by operating activities | 47,509 | 57,090 | |||||

Cash flows from investing activities: | |||||||

Capital expenditures | (18,268 | ) | (12,428 | ) | |||

Acquisition of CVR Nitrogen, LP, net of cash acquired | (63,869 | ) | — | ||||

Proceeds from sale of assets | — | 78 | |||||

Net cash used in investing activities | (82,137 | ) | (12,350 | ) | |||

10

Nine Months Ended September 30, | |||||||

2016 | 2015 | ||||||

(unaudited) | |||||||

(in thousands) | |||||||

Cash flows from financing activities: | |||||||

Principal and premium payments on 2021 Notes | (320,539 | ) | — | ||||

Principal payment on CRLLC Facility | (300,000 | ) | — | ||||

Principal payments on long-term debt | (125,000 | ) | — | ||||

Payment of revolving debt | (49,100 | ) | — | ||||

Payment of financing costs | (10,191 | ) | — | ||||

Proceeds on issuance of 2023 Notes, net of original issue discount | 628,869 | — | |||||

Proceeds on CRLLC Facility | 300,000 | — | |||||

Contribution from affiliate | 507 | — | |||||

Cash distributions to common unitholders – Affiliates | (27,633 | ) | (48,650 | ) | |||

Cash distributions to common unitholders – Non-affiliates | (41,956 | ) | (42,754 | ) | |||

Purchase of noncontrolling interest | (5,000 | ) | — | ||||

Net cash provided by (used in) financing activities | 49,957 | (91,404 | ) | ||||

Net increase (decrease) in cash and cash equivalents | 15,329 | (46,664 | ) | ||||

Cash and cash equivalents, beginning of period | 49,967 | 79,914 | |||||

Cash and cash equivalents, end of period | $ | 65,296 | $ | 33,250 | |||

Supplemental disclosures: | |||||||

Cash paid for income taxes, net | $ | 14 | $ | 35 | |||

Cash paid for interest, net of capitalized interest of $422 and $9 in 2016 and 2015, respectively | $ | 22,304 | $ | 4,419 | |||

Non-cash investing and financing activities: | |||||||

Construction in progress additions included in accounts payable | $ | 1,394 | $ | 3,911 | |||

Change in accounts payable related to construction in progress | $ | (3,816 | ) | $ | 2,845 | ||

Reduction of proceeds from 2023 Notes from original issue discount | $ | 16,131 | $ | — | |||

Fair value of common units issued in a business combination | $ | 335,693 | $ | — | |||

Fair value of debt assumed in a business combination | $ | 367,500 | $ | — | |||

See accompanying notes to the condensed consolidated financial statements.

11

CVR PARTNERS, LP AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

September 30, 2016

(unaudited)

(1) Formation of the Partnership, Organization and Nature of Business

Organization

CVR Partners, LP (referred to as "CVR Partners" or the "Partnership") is a Delaware limited partnership, formed by CVR Energy, Inc. (together with its subsidiaries, but excluding the Partnership and its subsidiaries, "CVR Energy") to own, operate and grow its nitrogen fertilizer business. Nitrogen fertilizer is used by farmers to improve the yield and quality of their crops, primarily corn and wheat. The Partnership principally produces ammonia and urea ammonium nitrate ("UAN"), an aqueous solution of urea and ammonium nitrate. The Partnership's product sales are sold on a wholesale basis in North America.

The Partnership produces nitrogen fertilizer products at two manufacturing facilities, which are located in Coffeyville, Kansas (the "Coffeyville Facility") and East Dubuque, Illinois (the "East Dubuque Facility"). On April 1, 2016, the Partnership completed the merger (the "East Dubuque Merger") with CVR Nitrogen, LP (formerly known as East Dubuque Nitrogen Partners, L.P. and also formerly known as Rentech Nitrogen Partners, L.P.) ("CVR Nitrogen") and with CVR Nitrogen GP, LLC (formerly known as East Dubuque Nitrogen GP, LLC and also formerly known as Rentech Nitrogen GP, LLC) ("CVR Nitrogen GP"), whereby the Partnership acquired the East Dubuque Facility. See Note 4 ("East Dubuque Merger") for further discussion.

The Partnership's subsidiaries include Coffeyville Resources Nitrogen Fertilizers, LLC ("CRNF"), which owns and operates the Coffeyville Facility, and East Dubuque Nitrogen Fertilizers, LLC ("EDNF"), which owns and operates the East Dubuque Facility. Both facilities manufacture ammonia and are able to further upgrade to other nitrogen fertilizer products, principally UAN.

As of September 30, 2016, public security holders held approximately 66% of the Partnership's outstanding limited partner interests and Coffeyville Resources, LLC ("CRLLC"), a wholly-owned subsidiary of CVR Energy, held approximately 34% of the Partnership's outstanding limited partner interests and 100% of the noneconomic general partner interest. As of September 30, 2016, Icahn Enterprises L.P. ("IEP") and its affiliates owned approximately 82% of the shares of CVR Energy.

Management and Operations

CVR GP, LLC ("CVR GP" or the "general partner") manages and operates the Partnership. Common unitholders have only limited voting rights on matters affecting the Partnership. In addition, common unitholders have no right to elect the general partner's directors on an annual or continuing basis.

The Partnership is operated by a combination of the general partner's senior management team and CVR Energy's senior management team pursuant to a services agreement among CVR Energy, CVR GP and the Partnership. The various rights and responsibilities of the Partnership's partners are set forth in the limited partnership agreement. The Partnership also is party to a number of agreements with CVR Energy and CVR GP to regulate certain business relations between the Partnership and the other parties thereto. See Note 15 ("Related Party Transactions") for further discussion.

(2) Basis of Presentation

The accompanying Partnership condensed consolidated financial statements include the accounts of CVR Partners and its subsidiaries. All intercompany accounts and transactions have been eliminated in consolidation. The accompanying condensed consolidated financial statements were prepared in accordance with U.S. generally accepted accounting principles ("GAAP") and in accordance with the rules and regulations of the Securities and Exchange Commission ("SEC"). These condensed consolidated financial statements should be read in conjunction with the December 31, 2015 audited consolidated financial statements and notes thereto included in CVR Partners’ Annual Report on Form 10-K for the year ended December 31, 2015, which was filed with the SEC on February 18, 2016 (the "2015 Form 10-K").

The condensed consolidated financial statements include certain selling, general and administrative expenses and direct operating expenses that CVR Energy and its subsidiaries incurred on behalf of the Partnership. These related party transactions are governed by

12

CVR PARTNERS, LP AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

September 30, 2016

(unaudited)

the services agreement. See Note 15 ("Related Party Transactions") for additional discussion of the services agreement and billing and allocation of certain costs.

In the opinion of the Partnership’s management, the accompanying condensed consolidated financial statements and related notes reflect all adjustments (consisting only of normal recurring adjustments) that are necessary to fairly present the financial position of the Partnership as of September 30, 2016 and December 31, 2015, the results of operations and comprehensive income (loss) of the Partnership for the three and nine months ended September 30, 2016 and 2015, the cash flows of the Partnership for the nine months ended September 30, 2016 and 2015 and the changes in partners’ capital for the Partnership for the nine months ended September 30, 2016.

The preparation of condensed consolidated financial statements in conformity with GAAP requires management to make certain estimates and assumptions that affect the reported amounts of assets, liabilities, revenues, expenses and the disclosure of contingent assets and liabilities. Actual results could differ from those estimates. Results of operations and cash flows for the interim periods presented are not necessarily indicative of the results that will be realized for the year ending December 31, 2016 or any other interim or annual period.

Planned Major Maintenance Costs

The direct-expense method of accounting is used for maintenance activities, including planned major maintenance activities and other less extensive shutdowns. Maintenance costs are recognized as expense when maintenance services are performed. Planned major maintenance activities generally occur every two to three years.

During the second quarter of 2016, the East Dubuque Facility completed a major scheduled turnaround. Overall results were negatively impacted due to the lost production during the downtime that resulted in reduced sales and certain reduced variable expenses included in cost of product sold (exclusive of depreciation and amortization) and direct operating expenses (exclusive of depreciation and amortization). Costs of approximately $6.6 million associated with the 2016 East Dubuque Facility turnaround are included in direct operating expenses (exclusive of depreciation and amortization) in the Condensed Consolidated Statements of Operations for the nine months ended September 30, 2016.

During the third quarter of 2015, the Coffeyville Facility completed a major scheduled turnaround. Overall results were negatively impacted due to the lost production during the downtime that resulted in reduced sales and certain reduced variable expenses included in cost of product sold (exclusive of depreciation and amortization) and direct operating expenses (exclusive of depreciation and amortization). Costs of approximately $6.6 million and $7.0 million, respectively, associated with the 2015 Coffeyville Facility turnaround are included in direct operating expenses (exclusive of depreciation and amortization) in the Condensed Consolidated Statements of Operations for the three and nine months ended September 30, 2015.

Cost Classifications

Cost of product sold (exclusive of depreciation and amortization) consist primarily of freight and distribution expenses, feedstock expenses, purchased ammonia and purchased hydrogen.

Direct operating expenses (exclusive of depreciation and amortization) consist primarily of energy and other utility costs, direct costs of labor, property taxes, plant-related maintenance services and environmental and safety compliance costs as well as catalyst and chemical costs. Direct operating expenses also include allocated share-based compensation from CVR Energy and its subsidiaries, as discussed in Note 5 ("Share‑Based Compensation").

Selling, general and administrative expenses (exclusive of depreciation and amortization) consist primarily of direct and allocated legal expenses, treasury, accounting, marketing, human resources, information technology and maintaining the corporate offices. Selling, general and administrative expenses also include allocated share-based compensation from CVR Energy and its subsidiaries, as discussed in Note 5 ("Share‑Based Compensation").

13

CVR PARTNERS, LP AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

September 30, 2016

(unaudited)

Cost of product sold, direct operating expenses, and selling, general and administrative expenses are presented exclusive of depreciation and amortization on the Condensed Consolidated Statements of Operations. Depreciation and amortization consisted of the following:

Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

2016 | 2015 | 2016 | 2015 | ||||||||||||

(in millions) | |||||||||||||||

Depreciation and amortization excluded from direct operating expenses | $ | 16.1 | $ | 7.3 | $ | 40.3 | $ | 20.8 | |||||||

Depreciation and amortization excluded from cost of product sold | 0.2 | 0.1 | 0.5 | 0.4 | |||||||||||

Depreciation and amortization excluded from selling, general and administrative expenses | 0.1 | — | 0.2 | — | |||||||||||

$ | 16.4 | $ | 7.4 | $ | 41.0 | $ | 21.2 | ||||||||

Income Taxes

CVR Partners is treated as a partnership for U.S. federal income tax purposes. The income tax liability of the common unitholders is not reflected in the consolidated financial statements of the Partnership. Generally, each common unitholder is required to take into account its respective share of CVR Partners' income, gains, loss and deductions. The Partnership is not subject to income taxes, except for a franchise tax in the State of Texas and a replacement tax in the State of Illinois.

CVR Nitrogen Holdings, LLC, a corporate entity wholly owned by CVR Partners, generates income or loss based on its own activities. As a limited liability company electing tax treatment as a corporation, the entity is subject to federal and state income taxes.

Under the Financial Accounting Standards Board ("FASB") Accounting Standards Codification Topic ("ASC") 740, Income Taxes, both the Partnership (for taxes based on income such as the Texas franchise tax and the Illinois replacement tax) and the corporate entity account for income taxes using the asset and liability method under which deferred income taxes are recognized for the future tax effects of temporary differences between the financial statement carrying amounts and the tax basis of existing assets and liabilities using the enacted statutory tax rates in effect at the end of the period. A valuation allowance for deferred tax assets is recorded when it is more likely than not that the benefit from the deferred tax asset will not be realized. When applicable, penalties and interest related to uncertain tax positions are recorded as income tax expense.

(3) Recent Accounting Pronouncements

In May 2014, the FASB issued Accounting Standard Update ("ASU") No. 2014-09, "Revenue from Contracts with Customers", which requires an entity to recognize the amount of revenue to which it expects to be entitled for the transfer of promised goods or services to customers. The standard was originally effective for interim and annual periods beginning after December 15, 2016 and permits the use of either the retrospective or cumulative effect transition method. Early adoption is not permitted. On July 9, 2015, the FASB approved a one-year deferral of the effective date making the standard effective for interim and annual periods beginning after December 15, 2017. The FASB will continue to permit entities to adopt the standard on the original effective date if they choose. The Partnership will adopt this standard as of January 1, 2018 using the modified retrospective application method. Given the complexity of this new guidance, the Partnership is continuing to evaluate the impact of the standard on its consolidated financial statements and footnote disclosures.

In April 2015, the FASB issued ASU 2015-03, "Simplifying the Presentation of Debt Issuance Costs" ("ASU 2015-03"). The new standard required that all costs incurred to issue debt be presented in the balance sheet as a direct deduction from the carrying value of the debt. The standard was effective for interim and annual periods beginning after December 15, 2015 and was required to be applied on a retrospective basis. Early adoption was permitted. The Partnership adopted ASU 2015-03 as of January 1, 2016 and applied the standard retrospectively to the Condensed Consolidated Balance Sheet. Refer to Note 12 ("Debt") for further details.

In February 2016, the FASB issued ASU 2016-02, "Leases" ("ASU 2016-02"). The new standard revises accounting for operating leases by a lessee, among other changes, and requires a lessee to recognize a liability to make lease payments and an asset representing its right to use the underlying asset for the lease term in the balance sheet. The standard is effective for the first interim and annual

14

CVR PARTNERS, LP AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

September 30, 2016

(unaudited)

periods beginning after December 15, 2018, with early adoption permitted. At adoption, ASU 2016-02 will be applied using the modified retrospective application method. The Partnership is currently evaluating the standard and the impact on its consolidated financial statements and footnote disclosures.

(4) East Dubuque Merger

On April 1, 2016, the Partnership completed the East Dubuque Merger as contemplated by the Agreement and Plan of Merger, dated as of August 9, 2015 (the "Merger Agreement"), whereby the Partnership acquired CVR Nitrogen and CVR Nitrogen GP. Pursuant to the East Dubuque Merger, the Partnership acquired the East Dubuque Facility.

CVR Nitrogen was required to sell or spin off its facility located in Pasadena, Texas (the "Pasadena Facility") as a condition to closing of the East Dubuque Merger. On March 14, 2016, CVR Nitrogen completed the sale to a third party of 100% of the issued and outstanding membership interests of its subsidiary that owned the Pasadena Facility. Holders of common units representing limited partner interests in CVR Nitrogen ("CVR Nitrogen common units") of record as of March 28, 2016 received consideration for the Pasadena Facility and may receive additional consideration in the future according to the terms of the purchase agreement. The Partnership did not receive and will not receive any consideration relating to the sale of the Pasadena Facility.

Under the terms of the Merger Agreement, holders of CVR Nitrogen common units eligible to receive consideration received 1.04 common units (the "unit consideration") representing limited partner interests in CVR Partners ("CVR Partners common units") and $2.57 in cash, without interest, (the "cash consideration" and together with the unit consideration, the "merger consideration") for each CVR Nitrogen common unit. Pursuant to the Merger Agreement, CVR Partners issued approximately 40.2 million CVR Partners common units and paid approximately $99.2 million in cash consideration to CVR Nitrogen common unitholders and certain holders of CVR Nitrogen phantom units discussed below.

Phantom units granted and outstanding under CVR Nitrogen’s equity plans and held by an employee who continued in the employment of a CVR Partners-affiliated entity upon closing of the East Dubuque Merger were canceled and replaced with new incentive awards of substantially equivalent value and on similar terms. See Note 5 ("Share‑Based Compensation") for further discussion. Each phantom unit granted and outstanding and held by (i) an employee who did not continue in employment of a CVR Partners-affiliated entity, or (ii) a director of CVR Nitrogen GP, upon closing of the East Dubuque Merger, vested in full and the holders thereof received the merger consideration.

In accordance with the FASB’s ASC Topic 805 — Business Combinations ("ASC 805"), the Partnership accounted for the East Dubuque Merger as an acquisition of a business with CVR Partners as the acquirer. ASC 805 requires that the consideration transferred be measured at the current market price at the date of the closing of the East Dubuque Merger. The aggregate merger consideration was approximately $802.4 million, including the fair value of CVR Partners common units issued of $335.7 million, a cash contribution of $99.2 million and $367.5 million fair value of assumed debt. The East Dubuque Facility contributed net sales of $32.3 million and $92.0 million, respectively, and operating income of $3.9 million and operating loss of $4.3 million, respectively, to our Condensed Consolidated Statements of Operations for the three and nine months ended September 30, 2016.

In March 2016, CVR Energy purchased 400,000 CVR Nitrogen common units, representing approximately 1% of the outstanding CVR Nitrogen limited partner interests. CVR Energy did not receive merger consideration for these designated CVR Nitrogen common units. The Partnership recorded the noncontrolling interest fair value of $4.6 million in the purchase price consideration on April 1, 2016. Subsequent to the East Dubuque Merger, CVR Energy contributed $0.5 million to CVR Nitrogen, and the Partnership purchased the 400,000 CVR Nitrogen common units from CVR Energy during the second quarter of 2016 for $5.0 million. The transaction eliminated the noncontrolling interest, and the net impact of $0.1 million was recorded as an increase to partners' capital on the Condensed Consolidated Statement of Partners' Capital for the nine months ended September 30, 2016. The Partnership owns 100% of the outstanding limited partners interests of CVR Nitrogen as of September 30, 2016.

15

CVR PARTNERS, LP AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

September 30, 2016

(unaudited)

Purchase Price Consideration

A summary of the total purchase price is as follows:

Purchase Price | ||||

(in millions) | ||||

Fair value of CVR Partners common units issued, as of the close of the East Dubuque Merger | $ | 335.7 | ||

Cash payment to CVR Nitrogen common unitholders and certain phantom unitholders | 99.2 | |||

Fair value of consideration transferred | 434.9 | |||

Fair value of noncontrolling interest for parent affiliate units (1) | 4.6 | |||

Total purchase price consideration to be allocated | $ | 439.5 | ||

The fair value of the unit consideration was determined as follows:

Fair Value of Unit Consideration | ||||

(units in thousands) | ||||

CVR Nitrogen common units outstanding, as of the close of the East Dubuque Merger | 38,985 | |||

Less: Noncontrolling interest from parent affiliate units (1) | 400 | |||

Net units subject to merger consideration | 38,585 | |||

Unit consideration per CVR Nitrogen common unit | 1.04 | |||

Number of CVR Partners common units issued for merger consideration | 40,129 | |||

Number of CVR Partners common units issued for CVR Nitrogen phantom units issued to noncontinuing employees and CVR Nitrogen board members (2) | 26 | |||

Total number of CVR Partners units issued | 40,155 | |||

Fair value per CVR Partners common unit, as of the close of the East Dubuque Merger | $ | 8.36 | ||

Fair value of CVR Partners common units issued (in millions) | $ | 335.7 | ||

_____________

(1) | See above for discussion of parent affiliate units. |

(2) | As discussed above, each phantom unit granted and outstanding and held by (i) an employee who did not continue in the employment of a CVR Partners-affiliated entity, or (ii) a director of CVR Nitrogen GP, upon closing of the East Dubuque Merger, vested in full and the holders thereof received the merger consideration. |

Merger-Related Indebtedness

CVR Nitrogen’s debt arrangements that remained in place after the closing date of the East Dubuque Merger included $320.0 million of its 6.5% notes due 2021 (the "2021 Notes"). The majority of the 2021 Notes were repurchased in June 2016, as discussed further in Note 12 ("Debt").

Immediately prior to the East Dubuque Merger, CVR Nitrogen also had outstanding balances under a credit agreement with Wells Fargo Bank, National Association, as successor-in-interest by assignment from General Electric Company, as administrative agent (the "Wells Fargo Credit Agreement"). The Wells Fargo Credit Agreement consisted of a $50.0 million senior secured revolving credit facility with a $10.0 million letter of credit sublimit. In connection with the closing of the East Dubuque Merger, the Partnership paid $49.4 million for the outstanding balance, accrued interest and fees under the Wells Fargo Credit Agreement, and the Wells Fargo Credit Agreement was canceled.

16

CVR PARTNERS, LP AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

September 30, 2016

(unaudited)

Preliminary Purchase Price Allocation

Under the acquisition method of accounting, the purchase price was allocated to CVR Nitrogen's net tangible assets based on their fair values as of April 1, 2016. The Partnership obtained a preliminary independent appraisal of the net assets acquired. Determining the fair value of net tangible assets requires judgment and involves the use of significant estimates and assumptions. The Partnership based its fair value estimates on assumptions it believes to be reasonable but are inherently uncertain. Although the Partnership believes the estimates of fair value of the assets and liabilities acquired are accurate, these estimates are preliminary and are subject to change during the measurement period. This measurement period may extend up to one year from the acquisition date.

The following table, set forth below, displays the estimated purchase price allocated to CVR Nitrogen's net tangible assets based on their fair values as of April 1, 2016. There were no identifiable intangible assets.

Purchase Price Allocation | ||||

(in millions) | ||||

Cash | $ | 35.4 | ||

Accounts receivable | 8.9 | |||

Inventories | 49.5 | |||

Prepaid expenses and other current assets (1) | 5.2 | |||

Property, plant and equipment | 774.9 | |||

Other long-term assets | 1.1 | |||

Deferred revenue | (29.8 | ) | ||

Other current liabilities (2) | (37.0 | ) | ||

Long-term debt | (367.5 | ) | ||

Other long-term liabilities | (1.2 | ) | ||

Total fair value of net assets acquired | 439.5 | |||

Less: Cash acquired | 35.4 | |||

Total consideration transferred, net of cash acquired | $ | 404.1 | ||

_____________

(1) | Includes $4.0 million for the estimated fair value of insurance proceeds related to an event that occurred prior to the East Dubuque Merger. The Partnership received $4.0 million during the second quarter of 2016, which was included in operating activities on the Condensed Consolidated Statement of Cash Flows for the nine months ended September 30, 2016. |

(2) | Includes an assumed liability of $11.8 million for third-party financial advisory services provided to CVR Nitrogen that became payable upon the closing of the East Dubuque Merger, and was subsequently paid by CVR Partners on April 1, 2016, which was included in operating activities on the Condensed Consolidated Statement of Cash Flows for the nine months ended September 30, 2016. |

Pro Forma Financial Information

The summary pro forma financial information for the periods presented below gives effect to the East Dubuque Merger as if it had occurred at January 1, 2015. The pro forma financial information for all periods presented were adjusted to give effect to pro forma events that are i) directly attributable to the East Dubuque Merger, ii) factually supportable and iii) expected to have a continuing impact on the consolidated results of operations.

Pro forma net income (loss) has been adjusted to exclude $0.7 million and $4.0 million, respectively, of merger-related costs incurred during the three months ended September 30, 2016 and 2015 and to exclude $3.9 million and $4.5 million, respectively, of merger-related costs incurred during the nine months ended September 30, 2016 and 2015. Pro forma net income (loss) has also been

17

CVR PARTNERS, LP AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

September 30, 2016

(unaudited)

adjusted to exclude $13.0 million of nonrecurring expenses related to the fair value adjustment to acquisition-date inventory and deferred revenue for the nine months ended September 30, 2016.

Incremental interest expense for financing the cash merger consideration and financing the payoff of the Wells Fargo Credit Agreement has also been adjusted for in the pro forma financial information, as well as incremental depreciation resulting from increased fair value of the property, plant and equipment as noted in the preliminary purchase price allocation.

The summary pro forma financial information is for informational purposes only and does not purport to represent what the Partnership's consolidated results of operations actually would have been if the East Dubuque Merger had occurred at any date, and such data does not purport to project the Partnership's results of operations for any future period. The basic and diluted units outstanding used to calculate the pro forma net income (loss) per unit amounts presented below have been adjusted to assume units issued at the closing of the East Dubuque Merger were outstanding since January 1, 2015.

Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

2016 | 2015 | 2016 | 2015 | |||||||||||||

(in thousands, except per unit data) | ||||||||||||||||

Net sales | $ | 78,473 | $ | 96,129 | $ | 306,210 | $ | 378,806 | ||||||||

Net income (loss) | (12,257 | ) | (10,404 | ) | (75 | ) | 70,698 | |||||||||

Net income (loss) per common unit, basic and diluted | (0.11 | ) | (0.09 | ) | 0.00 | 0.62 | ||||||||||

Expenses Associated with the East Dubuque Merger

During the three months ended September 30, 2016 and 2015, the Partnership incurred approximately $0.7 million and $1.5 million, respectively, of legal and other professional fees and other merger-related expenses, which were included in selling, general and administrative expenses (exclusive of depreciation and amortization). During the nine months ended September 30, 2016 and 2015, the Partnership incurred approximately $3.1 million and $1.5 million, respectively, of legal and other professional fees and other merger-related expenses, which were included in selling, general and administrative expenses (exclusive of depreciation and amortization).

(5) Share‑Based Compensation

Certain employees of CVR Partners and employees of CVR Energy who perform services for the Partnership under the services agreement with CVR Energy participate in equity-based compensation plans of CVR Partners' affiliates. Accordingly, CVR Partners has recorded compensation expense for these plans. All compensation expense related to these plans for full-time employees of CVR Partners has been allocated 100% to the Partnership. For employees of CVR Energy, the Partnership records share-based compensation relative to the percentage of time spent by each employee providing services to the Partnership as compared to the total calculated share-based compensation by CVR Energy. The Partnership is not responsible for payment of the allocated share-based compensation for certain plans. Allocated expense amounts related to plans for which the Partnership is not responsible for payment are immaterial and are reflected as an increase or decrease to partners' capital.

Long-Term Incentive Plan – CVR Energy

CVR Energy has a Long-Term Incentive Plan ("CVR Energy LTIP") that permits the grant of options, stock appreciation rights, restricted shares, restricted stock units, dividend equivalent rights, share awards and performance awards (including performance share units, performance units and performance based restricted stock). As of September 30, 2016, only performance units remain outstanding under the CVR Energy LTIP. Individuals who are eligible to receive awards and grants under the CVR Energy LTIP include CVR Energy’s or its subsidiaries’ (including the Partnership) employees, officers, consultants and directors.

18

CVR PARTNERS, LP AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

September 30, 2016

(unaudited)

Performance Unit Awards

In December 2015, CVR Energy entered into a performance unit award agreement (the "2015 Performance Unit Award Agreement") with its Chief Executive Officer. Compensation cost for the 2015 Performance Unit Award Agreement will be recognized over the performance cycle from January 1, 2016 to December 31, 2016. The performance unit award represents the right to receive, upon vesting, a cash payment equal to a defined threshold in accordance with the award agreement, multiplied by a performance factor that is based upon the achievement of certain operating objectives. The Partnership will be responsible for reimbursing CVR Energy for its allocated portion of the performance unit award. Assuming a target performance threshold and that the allocation of costs from CVR Energy remains consistent with the allocation percentages in place at September 30, 2016, there was approximately $0.1 million of total unrecognized compensation cost related to the 2015 Performance Unit Award Agreement to be recognized over a weighted-average period of approximately 0.3 years. Compensation expense recorded for the three and nine months ended September 30, 2016 related to the awards was approximately $0.2 million and $0.4 million, respectively. The Partnership will be responsible for reimbursing CVR Energy for its allocated portion of the awards. As of September 30, 2016, the Partnership had a liability of $0.4 million, for its allocated portion of the 2015 Performance Unit Award Agreement, which is recorded in accrued expenses and other current liabilities on the Condensed Consolidated Balance Sheets.

Incentive Unit Awards – CVR Energy

CVR Energy has granted awards of incentive units and distribution equivalent rights to certain employees of CRLLC, CVR Energy and the Partnership's general partner who provide shared services to CVR Energy and its subsidiaries (including the Partnership). The awards are generally graded-vesting awards, which are expected to vest over three years, with one-third of the award vesting each year. Compensation expense is recognized on a straight-line basis over the vesting period of the respective tranche of the award. Each incentive unit and distribution equivalent right represents the right to receive, upon vesting, a cash payment equal to (i) the average fair market value of one common unit of CVR Refining, LP ("CVR Refining") in accordance with the award agreement, plus (ii) the per unit cash value of all distributions declared and paid by CVR Refining from the grant date to and including the vesting date. The awards, which are liability-classified, are remeasured at each subsequent reporting date until they vest.

Assuming the allocation of costs from CVR Energy remains consistent with the allocation percentages in place at September 30, 2016, there was approximately $0.5 million of total unrecognized compensation cost related to the incentive units and associated distribution equivalent rights to be recognized over a weighted-average period of approximately 1.0 year. Inclusion of a vesting table would not be meaningful due to changes in allocation percentages that may occur from time to time. The unrecognized compensation expense has been determined by the number of incentive units and respective allocation percentage for individuals for whom, as of September 30, 2016, compensation expense has been allocated to the Partnership. Compensation expense recorded for both the three months ended September 30, 2016 and 2015 related to the awards was approximately $0.2 million. Compensation expense recorded for the nine months ended September 30, 2016 and 2015 related to the awards was approximately $0.2 million and $0.6 million, respectively. The Partnership will be responsible for reimbursing CVR Energy for its allocated portion of the awards.

As of September 30, 2016 and December 31, 2015, the Partnership had a liability of $0.7 million and $0.5 million, respectively, for its allocated portion of non-vested incentive units and associated distribution equivalent rights, which is recorded in accrued expenses and other current liabilities on the Condensed Consolidated Balance Sheets.

Long-Term Incentive Plan – CVR Partners

The Partnership has a long-term incentive plan ("CVR Partners LTIP") that provides for the grant of options, unit appreciation rights, distribution equivalent rights, restricted units, phantom units and other unit-based awards, each in respect of common units. Individuals eligible to receive awards pursuant to the CVR Partners LTIP include (i) employees of the Partnership and its subsidiaries, (ii) employees of the general partner, (iii) members of the board of directors of the general partner, and (iv) certain CVR Partners' parent's employees, consultants and directors who perform services for the benefit of the Partnership.

Through the CVR Partners LTIP, phantom unit awards outstanding include awards granted to employees of both the Partnership and the general partner. Phantom unit awards made to employees of the general partner are considered non-employee equity based-awards. The phantom unit awards outstanding vest over a three-year period and are required to be remeasured each reporting period until they vest. The maximum number of common units issuable under the CVR Partners LTIP is 5,000,000. As of September 30, 2016, there

19

CVR PARTNERS, LP AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

September 30, 2016

(unaudited)

were 4,820,215 common units available for issuance under the CVR Partners LTIP. As all phantom unit awards discussed below are cash settled awards, they do not reduce the number of common units available for issuance.

Certain Units and Phantom Units Awards

Awards of phantom units and distribution equivalent rights have been granted to certain employees of the Partnership and its subsidiaries' employees and the employees of the general partner. The awards are generally graded-vesting awards, which are expected to vest over three years with one-third of the award vesting each year. Compensation expense is recognized on a straight-line basis over the vesting period of the respective tranche of the award. Each phantom unit and distribution equivalent right represents the right to receive, upon vesting, a cash payment equal to (i) the average fair market value of one unit of the Partnership's common units in accordance with the award agreement, plus (ii) the per unit cash value of all distributions declared and paid by the Partnership from the grant date to and including the vesting date. The awards, which are liability-classified, are remeasured at each subsequent reporting date until they vest.

In connection with the East Dubuque Merger as described in Note 4 ("East Dubuque Merger"), 195,980 phantom units were granted to certain CVR Nitrogen employees. A related liability of $0.6 million was recorded as part of the opening balance sheet and included in personnel accruals in the purchase price allocation in Note 4 ("East Dubuque Merger"). Subsequent to the East Dubuque Merger, 79,654 awards were subject to an accelerated vesting date and were paid in full resulting in the early recognition of $0.4 million as compensation expense in selling, general and administrative expenses (exclusive of depreciation and amortization) for the nine months ending September 30, 2016.

A summary of the phantom unit activity during the nine months ended September 30, 2016 is presented below:

Phantom Units | Weighted-Average Grant Date Fair Value | |||||

Non-vested at January 1, 2016 | 391,903 | $ | 8.71 | |||

Granted | 199,455 | 8.07 | ||||

Vested | (79,654 | ) | 8.08 | |||

Forfeited | (8,299 | ) | 8.72 | |||

Non-vested at September 30, 2016 | 503,405 | $ | 8.56 | |||

Unrecognized compensation expense associated with the unvested phantom units at September 30, 2016 was approximately $1.4 million and is expected to be recognized over a weighted average period of 1.0 year. Compensation benefit recorded for the three months ended September 30, 2016 related to the awards under the CVR Partners LTIP was approximately $0.2 million. Compensation expense recorded for the three months ended September 30, 2015 related to the awards under the CVR Partners LTIP was approximately $0.1 million. Compensation expense recorded for the nine months ended September 30, 2016 and 2015 related to the awards under the CVR Partners LTIP was approximately $1.2 million and $1.1 million, respectively. Compensation expense related to the awards to employees of the Partnership and its subsidiaries under the CVR Partners LTIP has been recorded in selling, general and administrative expenses (exclusive of depreciation and amortization) - third parties and direct operating expenses (exclusive of depreciation and amortization) - third parties. Compensation expense related to the awards issued to employees of the general partner under the CVR Partners LTIP has been recorded in selling, general and administrative expenses (exclusive of depreciation and amortization) - affiliates and direct operating expenses (exclusive of depreciation and amortization) - affiliates. As of September 30, 2016 and December 31, 2015 the Partnership had a liability of $1.8 million and $0.7 million, respectively, for cash settled non-vested phantom unit awards and associated distribution equivalent rights, which is recorded in personnel accruals on the Condensed Consolidated Balance Sheets.

Performance-Based Phantom Unit Award

In May 2014, the Partnership entered into a Phantom Unit Agreement with Mark A. Pytosh, the Chief Executive Officer and President of the general partner, that included performance-based phantom units and distribution equivalent rights. Compensation cost for these awards is being recognized over the performance cycles of May 1, 2014 to December 31, 2014, January 1, 2015 to December 31, 2015 and January 1, 2016 to December 31, 2016, as the services are provided. Each phantom unit and distribution equivalent right

20

CVR PARTNERS, LP AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

September 30, 2016

(unaudited)

represents the right to receive, upon vesting, a cash payment equal to (i) the average closing price of the Partnership's common units in accordance with the agreement, multiplied by a performance factor that is based upon the level of the Partnership’s production of UAN, and (ii) the per unit cash value of all distributions declared and paid by the Partnership from the grant date to and including the vesting date. Compensation expense for the three and nine months ended September 30, 2016 and 2015 related to the awards was nominal. Based on current estimates of performance thresholds for the remaining performance cycles, unrecognized compensation expense and the liability associated with the unvested phantom units as of September 30, 2016 was nominal. The unrecognized compensation expense and the liability associated with the unvested phantom units as of December 31, 2015 were nominal.

(6) Inventories

Inventories consisted of the following:

September 30, 2016 | December 31, 2015 | ||||||

(in thousands) | |||||||

Finished goods | $ | 14,533 | $ | 9,589 | |||

Raw materials and precious metals | 9,319 | 9,055 | |||||

Parts and supplies | 33,036 | 18,885 | |||||

Total inventories | $ | 56,888 | $ | 37,529 | |||

(7) Property, Plant and Equipment

A summary of costs and accumulated depreciation for property, plant and equipment is as follows:

September 30, 2016 | December 31, 2015 | ||||||

(in thousands) | |||||||

Land and improvements | $ | 12,971 | $ | 5,441 | |||

Buildings and improvements | 14,881 | 3,049 | |||||

Machinery and equipment | 1,341,361 | 574,326 | |||||

Automotive equipment | 569 | 448 | |||||

Furniture and fixtures | 1,355 | 918 | |||||

Railcars | 16,261 | 16,315 | |||||

Construction in progress | 4,516 | 1,641 | |||||

$ | 1,391,914 | $ | 602,138 | ||||

Less: Accumulated depreciation | 251,749 | 209,005 | |||||

Total property, plant and equipment, net | $ | 1,140,165 | $ | 393,133 | |||

Capitalized interest recognized as a reduction of interest expense was approximately $21,000 and $9,000 for the three months ended September 30, 2016 and 2015, respectively. For the nine months ended September 30, 2016 and 2015, capitalized interest recognized as a reduction of interest expense was $0.4 million and $9,000, respectively.

(8) Partners’ Capital and Partnership Distributions

The Partnership has two types of partnership interests outstanding:

• | common units; and |

• | a general partner interest, which is not entitled to any distributions, and which is held by the general partner. |

21

CVR PARTNERS, LP AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

September 30, 2016

(unaudited)

As of September 30, 2016, the Partnership had a total of 113,282,973 common units issued and outstanding, of which 38,920,000 common units were owned by CRLLC, representing approximately 34% of the total Partnership common units outstanding.

The board of directors of the Partnership's general partner has a policy for the Partnership to distribute all available cash generated on a quarterly basis. Cash distributions will be made to the common unitholders of record on the applicable record date, generally within 60 days after the end of each quarter. Available cash for each quarter will be determined by the board of directors of the general partner following the end of such quarter.

Available cash begins with Adjusted EBITDA reduced for cash needed for (i) net cash interest expense (excluding capitalized interest) and debt service and other contractual obligations; (ii) maintenance capital expenditures; and (iii) to the extent applicable, major scheduled turnaround expenses, reserves for future operating or capital needs that the board of directors of the general partner deems necessary or appropriate, and expenses associated with the East Dubuque Merger, if any. Adjusted EBITDA is defined as EBITDA (net income before interest expense, net, income tax expenses, depreciation and amortization) further adjusted for the impact of non-cash share-based compensation, and, when applicable, major scheduled turnaround expense, loss on disposition of assets, expenses associated with the East Dubuque Merger and business interruption insurance recovery. Available cash for distribution may be increased by the release of previously established cash reserves, if any, at the discretion of the board of directors of the general partner, and available cash is increased by the business interruption insurance proceeds and the impact of purchase accounting. Actual distributions are set by the board of directors of the general partner. The board of directors of the general partner may modify the cash distribution policy at any time, and the partnership agreement does not require the board of directors of the general partner to make distributions at all.

The following is a summary of cash distributions paid to the Partnership's unitholders during 2016 for the respective quarters to which the distributions relate:

December 31, 2015 | March 31, 2016(1) | June 30, 2016 | Total Cash Distributions Paid in 2016 | ||||||||||||

($ in millions, except per common unit amounts) | |||||||||||||||

Amount paid to CRLLC | $ | 10.5 | $ | 10.5 | $ | 6.6 | $ | 27.6 | |||||||

Amount paid to public unitholders | 9.2 | 20.1 | 12.7 | 42.0 | |||||||||||

Total amount paid | $ | 19.7 | $ | 30.6 | $ | 19.3 | $ | 69.6 | |||||||

Per common unit | $ | 0.27 | $ | 0.27 | $ | 0.17 | $ | 0.71 | |||||||

Common units outstanding (in thousands) | 73,128 | 113,283 | 113,283 | ||||||||||||

_____________________________

(1) The distribution per common unit for the three months ended March 31, 2016 is calculated based on the post-merger common units outstanding.

(9) Net Income (Loss) per Common Unit

The Partnership's net income (loss) is allocated wholly to the common units, as the general partner does not have an economic interest. Basic and diluted net income (loss) per common unit is calculated by dividing net income (loss) by the weighted-average number of common units outstanding during the period and, when applicable, gives effect to certain units granted under the CVR Partners LTIP. The common units issued during the period are included on a weighted-average basis for the days in which they were outstanding.

22

CVR PARTNERS, LP AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

September 30, 2016

(unaudited)

(10) Goodwill

The Partnership evaluates the carrying value of goodwill annually as of November 1 and between annual evaluations if events occur or circumstances change that would more likely than not reduce the fair value of the reporting unit below its carrying amount. The Partnership's goodwill reporting unit is the Coffeyville Facility.

Based on a significant decline in market capitalization and lower cash flow forecasts resulting from weakened fertilizer pricing trends during the third quarter of 2016, the Partnership identified a triggering event and therefore performed an interim goodwill impairment test as of September 30, 2016. The goodwill impairment quantitative testing involves a two-step process. Step 1 compares the fair value of the reporting unit to its carrying value. The Coffeyville Facility reporting unit fair value is based upon consideration of various valuation methodologies, including guideline public company multiples and projected future cash flows discounted at rates commensurate with the risk involved. The carrying amount of the reporting unit was less than its fair value; therefore, a Step 2 was not required to be completed and no impairment was recorded.

The fair value of the reporting unit exceeded its carrying value by approximately 17 percent based upon the results of the Step 1 test as of September 30, 2016. Judgments and assumptions are inherent in management’s estimates used to determine the fair value of the reporting unit. Assumptions used in the discounted cash flows ("DCF") require the exercise of significant judgment, including judgment about appropriate discount rates and terminal values, growth rates, and the amount and timing of expected future cash flows. The discount rates used in the DCF, which are intended to reflect the risks inherent in future cash flow projections, are based on estimates of the weighted-average cost of capital of a market participant. Such estimates are derived from analysis of peer companies and consider the industry weighted average return on debt and equity from a market participant perspective. The most significant assumption to determining the fair value of the reporting unit was forecasted fertilizer pricing. Changes in assumptions may result in a change in management's estimates and may result in an impairment in future periods, including, but not limited to, further declines in the forecasted fertilizer pricing.

(11) Accrued Expenses and Other Current Liabilities

Accrued expenses and other current liabilities were as follows:

As of September 30, 2016 | As of December 31, 2015 | ||||||

(in thousands) | |||||||

Property taxes | $ | 2,271 | $ | 1,371 | |||

Current interest rate swap liabilities | — | 119 | |||||

Accrued interest | 18,521 | 458 | |||||

Railcar maintenance accruals | 1,280 | 209 | |||||

Affiliates (1) | 2,305 | 2,334 | |||||

Other accrued expenses and liabilities | 1,688 | 1,192 | |||||

$ | 26,065 | $ | 5,683 | ||||

____________

(1) | Accrued expenses and other current liabilities include amounts owed by the Partnership to CVR Energy and its subsidiaries, which are related parties, under the feedstock and shared services agreement and the services agreement. Refer to Note 15 ("Related Party Transactions") for additional discussion. |

23

CVR PARTNERS, LP AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

September 30, 2016

(unaudited)

(12) Debt

Long-term debt consisted of the following:

As of September 30, 2016 | As of December 31, 2015 | ||||||

(in thousands) | |||||||

9.25% senior secured notes, due 2023 | $ | 645,000 | $ | — | |||

6.50% notes, due 2021 | 4,195 | — | |||||

Credit Agreement term loan, due 2016 | — | 125,000 | |||||

Total long-term debt, before debt issuance costs and discount | 649,195 | 125,000 | |||||

Less: | |||||||

Unamortized discount | 15,635 | — | |||||

Unamortized debt issuance costs | 9,063 | 227 | |||||

Total long-term debt, net of current portion | $ | 624,497 | $ | 124,773 | |||

As discussed in Note 3 ("Recent Accounting Pronouncements"), the Partnership adopted ASU 2015-03, "Simplifying the Presentation of Debt Issuance Costs", which requires that all costs incurred to issue debt be presented in the balance sheet as a direct deduction from the carrying value of the debt. As a result of adoption of the standard, debt issuance costs of $0.2 million were reclassified as a direct deduction from the carrying value of the related debt balances in the Condensed Consolidated Balance Sheets as of December 31, 2015. A nominal amount of debt issuance costs related to the revolving credit facility was presented as assets in the Condensed Consolidated Balance Sheet as of December 31, 2015.

For the three months ended September 30, 2016 and 2015, amortization of the discount on debt and amortization of deferred financing costs reported as interest expense and other financing costs totaled approximately $0.6 million and $0.2 million, respectively. For the nine months ended September 30, 2016 and 2015, amortization of the discount on debt and amortization of deferred financing costs reported as interest expense and other financing costs totaled approximately $1.0 million and $0.7 million, respectively.

2023 Notes

On June 10, 2016, the Partnership and CVR Nitrogen Finance Corporation, an indirect wholly-owned subsidiary of the Partnership, (together the "2023 Notes Issuers"), certain subsidiary guarantors named therein and Wilmington Trust, National Association, as trustee and as collateral trustee, completed a private offering of $645.0 million aggregate principal amount of 9.250% Senior Secured Notes due 2023 (the "2023 Notes"). The 2023 Notes mature on June 15, 2023, unless earlier redeemed or repurchased by the issuers. Interest on the 2023 Notes is payable semi-annually in arrears on June 15 and December 15 of each year, beginning on December 15, 2016. The 2023 Notes are guaranteed on a senior secured basis by all of the Partnership’s existing subsidiaries.

The 2023 Notes were issued at a $16.1 million discount, which is being amortized over the term of the 2023 Notes as interest expense using the effective-interest method. The Partnership received approximately $622.9 million of cash proceeds, net of the original issue discount and underwriting fees, but before deducting other third-party fees and expenses associated with the offering. The net proceeds from the sale of the 2023 Notes were used to: (i) repay all amounts outstanding under the CRLLC Facility (defined and discussed below); (ii) finance the 2021 Notes Tender Offer (defined and discussed below) and (iii) to pay related fees and expenses.

The debt issuance costs of the 2023 Notes totaled approximately $9.4 million and are being amortized over the term of the 2023 Notes as interest expense using the effective-interest amortization method.

The 2023 Notes contain customary covenants for a financing of this type that, among other things, restrict the Partnership’s ability and the ability of certain of its subsidiaries to: (i) sell assets; (ii) pay distributions on, redeem or repurchase the Partnership’s units or

24

CVR PARTNERS, LP AND SUBSIDIARIES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Continued)

September 30, 2016

(unaudited)

redeem or repurchase its subordinated debt; (iii) make investments; (iv) incur or guarantee additional indebtedness or issue preferred units; (v) create or incur certain liens; (vi) enter into agreements that restrict distributions or other payments from the Partnership’s restricted subsidiaries to the Partnership; (vii) consolidate, merge or transfer all or substantially all of the Partnership’s assets; (viii) engage in transactions with affiliates; and (ix) create unrestricted subsidiaries. As of September 30, 2016, the Partnership was in compliance with the covenants contained in the 2023 Notes.

Included in other current liabilities on the Condensed Consolidated Balance Sheets is accrued interest payable totaling approximately $18.4 million as of September 30, 2016 related to the 2023 Notes. At September 30, 2016, the estimated fair value of the 2023 Notes was approximately $624.0 million. This estimate of fair value is Level 2 as it was determined by quotations obtained from a broker-dealer who makes a market in these and similar securities.

2021 Notes

The $320.0 million 2021 Notes were issued by CVR Nitrogen and CVR Nitrogen Finance (the "2021 Notes Issuers") prior to the East Dubuque Merger. The 2021 Notes bear interest at a rate of 6.5% per annum, payable semi-annually in arrears on April 15 and October 15 of each year. The 2021 Notes are scheduled to mature on April 15, 2021, unless repurchased or redeemed earlier in accordance with their terms.