U. S. SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-Q

| þ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2017

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission File Number 001-36860

IOVANCE BIOTHERAPEUTICS, INC.

(Exact name of small business issuer as specified in its charter)

| Delaware |

75-3254381 |

| (State or other jurisdiction of | (I.R.S. employer |

| incorporation or organization) | identification number) |

999 Skyway Road, Suite 150, San Carlos, CA 94070

(Address of principal executive offices and zip code)

(650) 260-7120

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer þ |

| Non-accelerated filer ¨ ( Do not check if a smaller reporting company ) | Smaller reporting company ¨ |

| Emerging growth company ¨ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

At October 31, 2017, the issuer had 72,632,717 shares of common stock, par value $0.000041666 per share, outstanding.

IOVANCE BIOTHERAPEUTICS, INC.

FORM 10-Q

For the Quarter Ended September 30, 2017

Table of Contents

PART I. FINANCIAL INFORMATION

| Item 1. | Financial Statements |

IOVANCE BIOTHERAPEUTICS, INC.

Condensed Consolidated Balance Sheets

(in thousands, except share information)

| September 30, | December 31, | |||||||

| 2017 | 2016 | |||||||

| (unaudited) | ||||||||

| ASSETS | ||||||||

| Current Assets | ||||||||

| Cash and cash equivalents | $ | 163,380 | $ | 106,717 | ||||

| Short-term investments | - | 59,753 | ||||||

| Prepaid expenses and other current assets | 7,995 | 3,042 | ||||||

| Total Current Assets | 171,375 | 169,512 | ||||||

| Property and equipment, net | 2,595 | 2,374 | ||||||

| Total Assets | $ | 173,970 | $ | 171,886 | ||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| Current Liabilities | ||||||||

| Accounts payable | $ | 2,905 | $ | 863 | ||||

| Accrued expenses | 5,624 | 4,105 | ||||||

| Total Current Liabilities | 8,529 | 4,968 | ||||||

| Commitments and contingencies (Note 9) | ||||||||

| Stockholders’ Equity | ||||||||

| Series A Convertible Preferred stock, $0.001 par value; 17,000 shares authorized, 1,694 shares issued and outstanding, as of September 30, 2017 and December 31, 2016, respectively (aggregate liquidation value of $1,694) | - | - | ||||||

| Series B Convertible Preferred stock, $0.001 par value; 11,500,000 shares authorized, 7,946,673 shares issued and outstanding as of September 30, 2017 and December 31, 2016, respectively (aggregate liquidation value of $37,747) | 8 | 8 | ||||||

| Common stock, $0.000041666 par value; 150,000,000 shares authorized, 71,954,843 and 62,248,074 shares issued and outstanding as of September 30, 2017 and December 31, 2016, respectively | 3 | 3 | ||||||

| Additional paid-in capital | 388,756 | 323,994 | ||||||

| Accumulated other comprehensive income | - | 29 | ||||||

| Accumulated deficit | (223,326 | ) | (157,116 | ) | ||||

| Total Stockholders’ Equity | 165,441 | 166,918 | ||||||

| Total Liabilities and Stockholders’ Equity | $ | 173,970 | $ | 171,886 | ||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

2

IOVANCE BIOTHERAPEUTICS, INC.

Condensed Consolidated Statements of Operations

(unaudited; in thousands, except per share information)

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| 2017 | 2016 | 2017 | 2016 | |||||||||||||

| Revenues | $ | - | $ | - | $ | - | $ | - | ||||||||

| Costs and expenses | ||||||||||||||||

| Research and development | 17,753 | 8,481 | 54,029 | 17,200 | ||||||||||||

| General and administrative | 4,590 | 10,498 | 12,777 | 20,517 | ||||||||||||

| Total costs and expenses | 22,343 | 18,979 | 66,806 | 37,717 | ||||||||||||

| Loss from operations | (22,343 | ) | (18,979 | ) | (66,806 | ) | (37,717 | ) | ||||||||

| Other income | ||||||||||||||||

| Interest income | 194 | 221 | 596 | 511 | ||||||||||||

| Net Loss | $ | (22,149 | ) | $ | (18,758 | ) | $ | (66,210 | ) | $ | (37,206 | ) | ||||

| Deemed dividend related to beneficial conversion feature of convertible preferred stock | - | (49,454 | ) | - | (49,454 | ) | ||||||||||

| Net Loss Attributable to Common Stockholders | (22,149 | ) | (68,212 | ) | (66,210 | ) | (86,660 | ) | ||||||||

| Net Loss Per Common Share, Basic and Diluted | $ | (0.35 | ) | $ | (1.15 | ) | $ | (1.06 | ) | $ | (1.64 | ) | ||||

| Weighted-Average Common Shares Outstanding, Basic and Diluted | 63,332 | 59,113 | 62,697 | 52,963 | ||||||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

3

IOVANCE BIOTHERAPEUTICS, INC.

Condensed Consolidated Statements of Comprehensive Loss

(unaudited; in thousands)

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| 2017 | 2016 | 2017 | 2016 | |||||||||||||

| Net Loss | $ | (22,149 | ) | $ | (18,758 | ) | $ | (66,210 | ) | $ | (37,206 | ) | ||||

| Other comprehensive income: | ||||||||||||||||

| Unrealized (loss) gain on short-term investments | - | 85 | (29 | ) | 115 | |||||||||||

| Comprehensive Loss | $ | (22,149 | ) | $ | (18,673 | ) | $ | (66,239 | ) | $ | (37,091 | ) | ||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

4

IOVANCE BIOTHERAPEUTICS, INC.

Condensed Consolidated Statements of Cash Flows

(unaudited; in thousands)

| Nine Months Ended September 30, | ||||||||

| 2017 | 2016 | |||||||

| Cash Flows From Operating Activities | ||||||||

| Net loss | $ | (66,210 | ) | $ | (37,206 | ) | ||

| Adjustments to reconcile net loss to net cash used in operating activities: | ||||||||

| Depreciation and amortization | 710 | 688 | ||||||

| Amortization of discount (premium) on investments | 19 | (69 | ) | |||||

| Stock-based compensation expense | 9,208 | 15,781 | ||||||

| Changes in assets and liabilities: | ||||||||

| Prepaid expenses and other current assets | (4,953 | ) | (997 | ) | ||||

| Accounts payable | 2,148 | (730 | ) | |||||

| Accrued expenses | 1,333 | 2,024 | ||||||

| Net cash used in operating activities | (57,745 | ) | (20,509 | ) | ||||

| Cash Flows From Investing Activities | ||||||||

| Purchase of short- term investments | - | (110,249 | ) | |||||

| Maturities of short- term investments | 59,705 | 94,159 | ||||||

| Purchase of property and equipment | (1,086 | ) | (781 | ) | ||||

| Net cash provided by (used in) investing activities | 58,619 | (16,871 | ) | |||||

| Cash Flows From Financing Activities | ||||||||

| Tax payments related to shares withheld for vested restricted stock awards | (1,203 | ) | (354 | ) | ||||

| Proceeds from the issuance of common stock upon exercise of warrants | 388 | 879 | ||||||

| Proceeds from the issuance of common stock upon exercise of options | 2,554 | 478 | ||||||

| Proceeds from the issuance of preferred stock and common stock, net | 54,050 | 95,685 | ||||||

| Net cash provided by financing activities | 55,789 | 96,688 | ||||||

| Net increase in cash and cash equivalents | 56,663 | 59,308 | ||||||

| Cash and Cash Equivalents, Beginning of Period | 106,717 | 33,587 | ||||||

| Cash and Cash Equivalents, End of Period | $ | 163,380 | $ | 92,895 | ||||

| Supplemental Disclosures of Cash Flow Information: | ||||||||

| Cash paid for income taxes | $ | - | $ | - | ||||

| Interest paid | - | - | ||||||

| Supplemental disclosure of non-cash investing and financing activities: | ||||||||

| Unrealized (loss) gain on short-term investments | $ | (29 | ) | $ | 115 | |||

| Acquisitions of property and equipment under accounts payable | (155 | ) | - | |||||

| Offering costs under accounts payable and accrued expenses | 235 | - | ||||||

| Deemed dividend related to a beneficial conversion feature | - | 49,454 | ||||||

| Conversion of convertible preferred stock to common stock | - | 3 | ||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

5

IOVANCE BIOTHERAPEUTICS, INC.

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

NOTE 1. GENERAL ORGANIZATION AND BUSINESS

Iovance Biotherapeutics, Inc. (the “Company,” “we,” “us” or “our”) is a biopharmaceutical company focused on the development and commercialization of novel cancer immunotherapy products designed to harness the power of a patient’s own immune system to eradicate cancer cells. Our lead program is an adoptive cell therapy (ACT) utilizing tumor-infiltrating lymphocytes (TIL), which are T cells derived from patients’ tumors, for the treatment of metastatic melanoma. The TIL are extracted from the tumor tissue, expanded in our manufacturing suites and then infused back into the patient to fight their cancer. On June 1, 2017, the Company reincorporated to become a Company governed by Delaware corporation laws. On June 27, 2017, we changed our name to Iovance Biotherapeutics, Inc.

Basis of Presentation of Unaudited Condensed Consolidated Financial Information

The unaudited condensed consolidated financial statements of the Company for the three and nine months ended September 30, 2017 and 2016 have been prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”) for interim financial information and pursuant to the requirements for reporting on Form 10-Q and Regulation S-K. Accordingly, they do not include all the information and footnotes required by GAAP for complete financial statements. However, such information reflects all adjustments (consisting solely of normal recurring adjustments), which are, in the opinion of management, necessary for the fair presentation of the financial position and the results of operations. Results shown for interim periods are not necessarily indicative of the results to be obtained for a full fiscal year. The balance sheet information as of December 31, 2016, was derived from the audited financial statements included in the Company's financial statements as of and for the year ended December 31, 2016 included in the Company’s Annual Report on Form 10-K filed with the Securities and Exchange Commission (the “SEC”) on March 8, 2017. These financial statements should be read in conjunction with that report.

Liquidity

The Company is currently engaged in the development of therapeutics to fight cancer, specifically solid tumors. We do not have any commercial products and have not yet generated any revenues from our business. We currently do not anticipate that we will generate any revenues during the upcoming 12 months, from the sale or licensing of any products. As shown in the accompanying financial statements, we have incurred a net loss of $66.2 million for the nine months ended September 30, 2017 and used $57.7 million of cash in our operating activities during the nine months ended September 30, 2017. As of September 30, 2017, we had $163.4 million of cash and cash equivalents.

The Company expects to further increase its research and development activities, which will increase the amount of cash used during the remainder of 2017 and beyond. Specifically, we expect continued spending on clinical trials, continued and expansion of manufacturing activities, higher payroll expenses as we increase our professional and scientific staff and research and development activities. Based on the funds we have available, we believe that we have sufficient capital to fund our anticipated operating expenses for at least 12 months from the date that these financial statements are issued.

NOTE 2. SUMMARY OF SIGNIFICANT ACCOUNTING PRACTICES

Short-term Investments

The Company's short-term investments are classified as “available-for-sale”. The Company includes these investments in current assets and carries them at fair value. Unrealized gains and losses on available-for-sale securities are included in accumulated other comprehensive income. The amortized cost of debt securities is adjusted for the amortization of premiums and accretion of discounts to maturity. Such amortization is included in interest income. Gains and losses on securities sold are recorded based on the specific identification method and are included in interest income in the statement of operations. We have not incurred any realized gains or losses from sales of securities to date.

Loss per Share

Basic net loss per share is computed using the weighted average number of common shares outstanding during the period. Diluted net loss per share is computed using the weighted average number of shares of common stock outstanding during the period increased to include the number of additional shares of common stock that would have been outstanding if the potentially dilutive securities had been issued.

6

At September 30, 2017 and 2016, the following outstanding common stock equivalents have been excluded from the calculation of net loss per share because their impact would be anti-dilutive.

| September 30, | ||||||||

| 2017 | 2016 | |||||||

| Stock options | 6,706,964 | 4,945,358 | ||||||

| Warrants | 6,411,216 | 6,808,216 | ||||||

| Series A Convertible Preferred* | 847,000 | 847,000 | ||||||

| Series B Convertible Preferred* | 7,946,673 | 7,946,673 | ||||||

| Restricted stock awards | 834 | 9,167 | ||||||

| Restricted stock units | 126,041 | 550,000 | ||||||

| 22,038,728 | 21,106,414 | |||||||

* on an as-converted basis

The dilutive effect of potentially dilutive securities is reflected in diluted earnings per common share by application of the treasury stock method. Under the treasury stock method, an increase in the fair market value of the Company's common stock can result in a greater dilutive effect from potentially dilutive securities.

Fair Value Measurements

Under Financial Accounting Standards Board (FASB) Accounting Standards Codification (ASC) 820, Fair Value Measurements and Disclosures, fair value is defined as the price at which an asset could be exchanged or a liability transferred in a transaction between knowledgeable, willing parties in the principal or most advantageous market for the asset or liability. Where available, fair value is based on observable market prices or parameters or derived from such prices or parameters. Where observable prices or parameters are not available, valuation models are applied.

Assets and liabilities recorded at fair value in our financial statements are categorized based upon the level of judgment associated with the inputs used to measure their fair value. Hierarchical levels directly related to the amount of subjectivity associated with the inputs to fair valuation of these assets and liabilities, are as follows:

Level 1—Inputs are unadjusted, quoted prices in active markets for identical assets at the reporting date. Active markets are those in which transactions for the asset or liability occur in sufficient frequency and volume to provide pricing information on an ongoing basis.

Level 2—Are inputs, other than quoted prices included in Level 1, that are either directly or indirectly observable for the asset or liability through correlation with market data at the reporting date and for the duration of the instrument’s anticipated life.

The fair valued assets we held and have held are generally assessed under Level 2 were corporate bonds and commercial paper. We utilize third party pricing services in developing fair value measurements where fair value is based on valuation methodologies such as models using observable market inputs, including benchmark yields, reported trades, broker/dealer quotes, bids, offers and other reference data. We use quotes from external pricing service providers and other on-line quotation systems to verify the fair value of investments provided by our third-party pricing service providers. We review independent auditor’s reports from our third-party pricing service providers particularly regarding the controls over pricing and valuation of financial instruments and ensure that our internal controls address certain control deficiencies, if any, and complementary user entity controls are in place.

Level 3—Unobservable inputs that are supported by little or no market activity and that are significant to the fair value of the assets or liabilities and which reflect management’s best estimate of what market participants would use in pricing the asset or liability at the reporting date. Consideration is given to the risk inherent in the valuation technique and the risk inherent in the inputs to the model.

We do not have fair valued assets classified under Level 3.

As of September 30, 2017, there were no financial assets measured at fair value.

7

Financial assets measured at fair value on a recurring basis are categorized in the tables below based upon the lowest level of significant input to the valuations (in thousands):

| Assets at Fair Value as of December 31, 2016 | ||||||||||||||||

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| Commercial paper | $ | - | $ | 29,178 | $ | - | $ | 29,178 | ||||||||

| Corporate debt securities | - | 26,578 | - | 26,578 | ||||||||||||

| US Government agency securities | - | 3,997 | - | 3,997 | ||||||||||||

| Total | $ | - | $ | 59,753 | $ | - | $ | 59,753 | ||||||||

Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the reporting period. Actual results could differ from those estimates. Significant estimates include valuation of short-term investments, accounting for potential liabilities, the valuation allowance associated with the Company’s deferred tax assets, and the assumptions made in valuing stock instruments issued for services.

Principles of Consolidation

The accompanying condensed consolidated financial statements include the accounts of Iovance Biotherapeutics, Inc. and its wholly-owned subsidiary, Iovance Biotherapeutics GmbH (formerly Lion Biotechnologies GmbH). All intercompany accounts and transactions have been eliminated. The U.S. dollar is the functional currency for all the Company's consolidated operations.

Stock-Based Compensation

The Company periodically grants stock options and warrants to employees and non-employees in non-capital raising transactions as compensation for services rendered. The Company accounts for stock option grants to employees based on the authoritative guidance provided by the FASB where the value of the award is measured on the date of grant and recognized over the vesting period. The Company accounts for stock option grants to non-employees in accordance with the authoritative guidance of the FASB where the value of the stock compensation is determined based upon the measurement date at either a) the date at which a performance commitment is reached, or b) at the date at which the necessary performance to earn the equity instruments is complete. Non-employee stock-based compensation charges generally are amortized over the vesting period on a straight-line basis. In certain circumstances where there are no future performance requirements by the non-employee, option grants are immediately vested and the total stock-based compensation charge is recorded in the period of the measurement date.

The fair value of the Company's common stock option grants is estimated using a Black-Scholes option pricing model, which uses certain assumptions related to risk-free interest rates, expected volatility, expected life of the common stock options, and future dividends. Compensation expense is recorded based upon the value derived from the Black-Scholes option pricing model, and based on actual experience. The assumptions used in the Black-Scholes option pricing model could materially affect compensation expense recorded in future periods.

The Company has in the past issued restricted shares of its common stock for share-based compensation programs. The Company measures the compensation cost with respect to restricted shares issued to employees based upon the estimated fair value of the equity instruments at the date of the grant, and is recognized as expense over the period which an employee is required to provide services in exchange for the award.

The fair value of restricted stock units is based on the closing price of the Company’s common stock on the grant date.

Total stock-based compensation expense related to all our stock-based awards was recorded on the statements of operations as follows (in thousands):

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| 2017 | 2016 | 2017 | 2016 | |||||||||||||

| Research and development | $ | 1,053 | $ | 640 | $ | 4,336 | $ | 1,818 | ||||||||

| General and administrative | 1,566 | 8,005 | 4,872 | 13,963 | ||||||||||||

| Total stock-based compensation expense | $ | 2,619 | $ | 8,645 | $ | 9,208 | $ | 15,781 | ||||||||

8

Total stock-based compensation broken down based on each individual instrument was as follows (in thousands):

| Three Months Ended September 30, | Nine Months Ended September 30, | |||||||||||||||

| 2017 | 2016 | 2017 | 2016 | |||||||||||||

| Stock option expense | $ | 2,562 | $ | 7,877 | $ | 8,193 | $ | 13,944 | ||||||||

| Restricted stock award expense | 6 | 145 | 33 | 976 | ||||||||||||

| Restricted stock unit expense | 51 | 623 | 982 | 861 | ||||||||||||

| Total stock-based compensation expense | $ | 2,619 | $ | 8,645 | $ | 9,208 | $ | 15,781 | ||||||||

Preferred Stock

The Company applies the accounting standards for distinguishing liabilities from equity when determining the classification and measurement of its preferred stock. Preferred shares subject to mandatory redemption are classified as liability instruments and are measured at fair value. Conditionally redeemable preferred shares (including preferred shares that feature redemption rights that are either within the control of the holder or subject to redemption upon the occurrence of uncertain events not solely within the Company’s control) are classified as temporary equity. At all other times, preferred shares are classified as stockholders’ equity.

Convertible Instruments

The Company applies the accounting standards for derivatives and hedging and for distinguishing liabilities from equity when accounting for hybrid contracts that feature conversion options. The accounting standards require companies to bifurcate conversion options from their host instruments and account for them as free-standing derivative financial instruments per certain criteria. The criteria includes circumstances in which (i) the economic characteristics and risks of the embedded derivative instrument are not clearly and closely related to the economic characteristics and risks of the host contract, (ii) the hybrid instrument that embodies both the embedded derivative instrument and the host contract is not re-measured at fair value under otherwise applicable generally accepted accounting principles with changes in fair value reported in earnings as they occur and (iii) a separate instrument with the same terms as the embedded derivative instrument would be considered a derivative instrument. The derivative is subsequently marked to market at each reporting date based on current fair value, with the changes in fair value reported in results of operations.

Conversion options that contain variable settlement features such as provisions to adjust the conversion price upon subsequent issuances of equity or equity linked securities at exercise prices more favorable than that featured in the hybrid contract generally result in their bifurcation from the host instrument.

The Company also records, when necessary, deemed dividends for the intrinsic value of the conversion options embedded in preferred stock based upon the difference between the fair value of the underlying common stock at the commitment date of the transaction and the effective conversion price embedded in the preferred stock.

Recent Accounting Standards

In March 2016, the FASB issued ASU No. 2016-09, Compensation - Stock Compensation (Topic 718): Improvements to Employee Share-Based Payment Accounting. This ASU identifies areas for simplification involving several aspects of accounting for share-based payment transactions, including the income tax consequences, classification of awards as either equity or liabilities, an option to recognize gross stock compensation expense with actual forfeitures recognized as they occur, as well as certain classifications on the statement of cash flows. This ASU will be effective for fiscal years beginning after December 15, 2016, and interim periods within those annual periods. The Company adopted this ASU and it did not have a material impact on the Company’s disclosures in the footnotes to its financial statements.

In May 2017, the FASB issued ASU No. 2017-09, Compensation–Stock Compensation (Topic 718): Scope of Modification Accounting, clarifying when a change to the terms or conditions of a share-based payment award must be accounted for as a modification. The new guidance requires modification accounting if the fair value, vesting condition or the classification of the award is not the same immediately before and after a change to the terms and conditions of the award. The new guidance is effective for the Company on a prospective basis beginning on January 1, 2018, with early adoption permitted. The Company is currently evaluating the impact that ASU 2017-09 will have on its consolidated financial statements and related disclosures.

Subsequent Events

The Company evaluates events that have occurred after the balance sheet date but before the financial statements are issued. Based upon the evaluation, the Company did not identify any recognized or non-recognized subsequent events that would have required adjustment or disclosure in the condensed consolidated financial statements.

9

Reclassifications

Certain amounts within the statements of cash flows for the prior periods have been reclassified to conform with the current period presentation. These reclassifications had no impact on the Company's previously reported financial position or cash flows for any of the periods presented.

NOTE 3. CASH AND CASH EQUIVALENTS AND SHORT-TERM INVESTMENTS

Cash and cash equivalents and short-term investments consist of the following (in thousands):

| September 30, | December 31, | |||||||

| 2017 | 2016 | |||||||

| Cash - Demand deposits | $ | 72,286 | $ | 76,071 | ||||

| Cash equivalents - Money market funds | 91,094 | 30,646 | ||||||

| Cash and cash equivalents total | $ | 163,380 | $ | 106,717 | ||||

| September 30, | December 31, | |||||||

| 2017 | 2016 | |||||||

| Commercial paper | $ | - | $ | 29,178 | ||||

| Corporate debt securities | - | 26,578 | ||||||

| US Government agency securities | - | 3,997 | ||||||

| Short-term investments total | $ | - | $ | 59,753 | ||||

Money market funds and short-term investments include the following securities with gross unrealized gains and losses (in thousands):

| Gross | Gross | |||||||||||||||

| Unrealized | Unrealized | |||||||||||||||

| As of September 30, 2017 | Cost | Gains | Losses | Fair Value | ||||||||||||

| Money market funds | $ | 91,094 | $ | - | $ | - | $ | 91,094 | ||||||||

Unrealized gains and losses are included in Accumulated other comprehensive income.

| Gross | Gross | |||||||||||||||

| Unrealized | Unrealized | |||||||||||||||

| As of December 31, 2016 | Cost | Gains | Losses | Fair Value | ||||||||||||

| Money market funds | $ | 30,646 | $ | - | $ | - | $ | 30,646 | ||||||||

| Commercial paper | 29,118 | 60 | - | 29,178 | ||||||||||||

| Corporate debt securities | 26,606 | 1 | (29 | ) | 26,578 | |||||||||||

| US Government agency securities | 4,000 | - | (3 | ) | 3,997 | |||||||||||

| Total | $ | 90,370 | $ | 61 | $ | (32 | ) | $ | 90,399 | |||||||

At September 30, 2017, the Company did not have any short-term investments.

The Company’s investment policy limits investments to certain types of instruments such as certificates of deposit, money market instruments, obligations issued by the U.S. government and U.S. government agencies as well as corporate debt securities, and places restrictions on maturities and concentration by type and issuer.

10

NOTE 4. BALANCE SHEET COMPONENTS

Property and equipment, net consists of the following (in thousands):

| September 30, | December 31, | |||||||

| 2017 | 2016 | |||||||

| Lab equipment | $ | 3,064 | $ | 2,405 | ||||

| Leasehold improvements | 1,707 | 1,381 | ||||||

| Computer equipment | 331 | 245 | ||||||

| Office furniture and equipment | 179 | 148 | ||||||

| Construction in progress | 105 | 276 | ||||||

| Total Property and equipment, cost | 5,386 | 4,455 | ||||||

| Less: Accumulated depreciation and amortization | (2,791 | ) | (2,081 | ) | ||||

| Property and equipment, net | $ | 2,595 | $ | 2,374 | ||||

Accrued liabilities consist of the following (in thousands):

| September 30, | December 31, | |||||||

| 2017 | 2016 | |||||||

| Accrued payroll and employee related expenses | $ | 1,556 | $ | 1,581 | ||||

| Legal and related services | 1,236 | 927 | ||||||

| Clinical related | 735 | 614 | ||||||

| Manufacturing related | 1,352 | 437 | ||||||

| Deferred rent | 459 | 422 | ||||||

| Accrued other | 286 | 124 | ||||||

| $ | 5,624 | $ | 4,105 | |||||

NOTE 5. STOCKHOLDERS’ EQUITY

Public Offering

On September 25, 2017, the Company sold 8,846,154 shares of its common stock in an underwritten public offering at $6.50 per share for net proceeds of $53.8 million after deducting underwriting discounts and expenses of the offering.

Preferred stock

The Company’s certificate of incorporation authorizes the issuance of up to 50,000,000 shares of “blank check” preferred stock. At September 30, 2017 and December 31, 2016, 17,000 shares have been designated as Series A Convertible Preferred Stock and 11,500,000 designated as Series B Convertible Preferred Stock.

Series A Convertible Preferred Stock

A total of 17,000 shares of Series A Convertible Preferred Stock (“Series A Preferred Stock”) have been authorized for issuance under the Certificate of Designation of Preferences and Rights of Series A Convertible Preferred Stock. The shares of Series A Preferred Stock have a stated value of $1,000 per share and are initially convertible into shares of common stock at a price of $2.00 per share, subject to adjustment.

The Series A Preferred Stock may, at the option of each investor, be converted into fully paid and non-assessable shares of common stock. The holders of shares of Series A Preferred Stock do not have the right to vote on matters that come before stockholders. In the event of any dissolution or winding up of the Company, proceeds shall be paid pari passu among the holders of the shares of common stock and preferred stock, pro rata based on the number of shares held by each holder. The Company may not declare, pay or set aside any dividends on shares of capital stock of the Company (other than dividends on shares of common stock payable in shares of common stock) unless the holders of the Series A Preferred Stock shall first receive an equal dividend on each outstanding share of Series A Preferred Stock. The common shares issued were determined on a formula basis of 500 common shares for each share of Series A Preferred Stock converted. During the three and nine months ended September 30, 2017 and 2016, no Series A Preferred stock was converted into common stock, respectively.

11

Series B Preferred Stock

In June 2016, the Company created a new class of Preferred Stock designated as Series B Convertible Preferred Stock (the “Series B Preferred”). The rights of the Series B Preferred are set forth in the Certificate of Designation of Rights, Preferences and Privileges of Series B Preferred Stock (the “Series B Certificate of Designation”). A total of 11,500,000 shares of Series B Preferred are authorized for issuance under the Series B Certificate of Designation. The shares of Series B Preferred have a stated value of $4.75 per share and are convertible into shares of common stock at an initial conversion price of $4.75 per share.

Holders of the Series B Preferred are entitled to dividends on an as-if-converted basis in the same form as any dividends actually paid on shares of the Company’s Series A Preferred Stock or the Company’s common stock. So long as any Series B Preferred remains outstanding, the Company may not redeem, purchase or otherwise acquire any material amount of our Series A Preferred Stock or any junior securities.

During the three and nine months ended September 30, 2017 and 2016, zero and 3,421,960 Series B Preferred were converted into common stock. At September 30, 2017, 7,946,673 shares of Series B Preferred Stock remained outstanding.

Warrants

The following table summarizes the Company’s stock warrant activity for the nine months ended September 30, 2017:

| Weighted | ||||||||

| Shares | Average | |||||||

| Under | Exercise | |||||||

| Warrants | Price | |||||||

| Outstanding at January 1, 2017 | 6,566,216 | $ | 2.51 | |||||

| Issued | - | - | ||||||

| Exercised | (155,000 | ) | 2.50 | |||||

| Expired/Cancelled | - | - | ||||||

| Outstanding at September 30, 2017 | 6,411,216 | $ | 2.51 | |||||

The warrants have a weighted average remaining life of 1.1 years at September 30, 2017.

NOTE 6. STOCK BASED COMPENSATION

Stock Plans

On September 19, 2014, the Company’s Board of Directors adopted the Iovance Biotherapeutics, Inc. 2014 Equity Incentive Plan (the “2014 Plan”). The 2014 Plan was approved by our stockholders at the annual meeting of stockholders held in November 2014. The 2014 Plan as approved by the stockholders authorized the issuance up to an aggregate of 2,350,000 shares of common stock. On April 10, 2015, the Board amended the 2014 Plan to increase the total number of shares that can be issued under the 2014 Plan by 1,650,000 from 2,350,000 shares to 4,000,000 shares. The increase in shares available for issuance under the 2014 Plan was approved by stockholders on June 12, 2015.

On August 16, 2016, the stockholders approved the increase the total number of shares that can be issued under the 2014 Plan by 5,000,000 from 4,000,000 shares to 9,000,000 shares. At September 30, 2017, 2,608,830 shares were available for grant under the Company’s 2014 Plan.

Restricted Stock Units

On June 1, 2016, the Company entered into a restricted stock unit agreement with the Company’s Chief Executive Officer (Maria Fardis, Ph.D.) pursuant to which the Company granted Dr. Fardis 550,000 non-transferrable restricted stock units at fair market value of $5.87 per share as an inducement of employment pursuant to the exception to The NASDAQ Global Market rules that generally require stockholder approval of equity incentive plans. Of the 550,000 restricted stock units 137,500 restricted stock units vested on the first anniversary of the effective date of Dr. Fardis’ employment agreement, and 275,000 restricted stock units vested in 2017 upon the satisfaction of certain clinical trial and manufacturing milestones. The remaining 137,500 restricted stock units will vest in equal monthly installments over the 36-month period that commenced on June 1, 2017 (the first anniversary of the effective date of Dr. Fardis’ employment), provided that Dr. Fardis has been continuously employed with the Company as of such vesting dates. As of September 30, 2017, 126,041 restricted stock units remained unvested.

Stock-based compensation expense for restricted stock units is measured based on the closing fair market value of the Company's common stock on the date of grant. The stock compensation expense was $0.1 million and $0.6 million for the three months ended September 30, 2017 and 2016, respectively and was $1.0 million and $0.9 million for the nine months ended September 30, 2017 and 2016, respectively.

As of September 30, 2017, there is $0.7 million of total unrecognized compensation expense related to the restricted stock units to be recognized over a weighted average period of 2.7 years.

12

Stock Options

The following table summarizes the Company’s stock options activity for the nine months ended September 30, 2017:

| Weighted | ||||||||

| Number | Average | |||||||

| of | Exercise | |||||||

| Options | Price | |||||||

| Outstanding at January 1, 2017 | 6,233,150 | $ | 7.24 | |||||

| Granted | 2,044,400 | 6.59 | ||||||

| Exercised | (484,850 | ) | 5.27 | |||||

| Expired/Forfeited | (1,085,736 | ) | 6.36 | |||||

| Outstanding at September 30, 2017 | 6,706,964 | $ | 7.33 | |||||

The Company recorded stock-based compensation costs related to options of $2.6 million and $7.9 million for the three months ended September 30, 2017 and 2016, respectively and $8.2 million and $13.9 million for the nine months ended September 30, 2017 and 2016, respectively. As of September 30, 2017, there was $22.1 million of total unrecognized compensation expense related to the options to be recognized over a weighted average period of 2.0 years.

The weighted-average grant date fair value per share of options granted under the Plan was $5.81 and $8.97 for the three months ended September 30, 2017 and 2016, respectively and was $6.46 and $6.75 for the nine months ended September 30, 2017 and 2016, respectively.

Restricted Common Stock Awards

The following table summarizes the Company’s restricted common stock awards activity for the nine months ended September 30, 2017:

| Weighted Average | ||||||||

| Number | Grant Date | |||||||

| of Shares | Fair Value | |||||||

| Non-vested shares, January 1, 2017 | 7,084 | $ | 6.48 | |||||

| Granted | - | - | ||||||

| Vested | (6,250 | ) | 6.53 | |||||

| Forfeited | - | - | ||||||

| Non-vested shares, September 30, 2017 | 834 | $ | 6.10 | |||||

The Company recorded stock compensation costs related to restricted stock awards of $0.0 million and $0.2 million for the three months ended September 30, 2017 and 2016, respectively and was $0.0 million and $1.0 million for the nine months ended September 30, 2017 and 2016, respectively. As of September 30, 2017, the amount of unvested compensation related to the unvested outstanding shares of restricted common stock was immaterial.

NOTE 7. AGREEMENTS

National Institutes of Health (NIH) and the National Cancer Institute (NCI)

Cooperative Research and Development Agreement (CRADA)

In August 2011, the Company signed a five-year CRADA with the NCI to work with Dr. Steven Rosenberg on developing adoptive cell immunotherapies that are designed to destroy metastatic melanoma cells using a patient’s tumor infiltrating lymphocytes.

In January 2015, the Company executed an amendment (the “Amendment”) to the CRADA to include four new indications. As amended, in addition to metastatic melanoma, the CRADA included the development of TIL therapy for the treatment of patients with bladder, lung, triple-negative breast, and HPV-associated cancers.

In August 2016, the NCI and the Company entered into a second amendment to the CRADA. The principal changes effected by the second amendment included (i) extending the term of the CRADA by another five years to August 2021, and (ii) modifying the focus on the development of unmodified TIL as a stand-alone therapy or in combination with U.S. Food and Drug Administration (“FDA”) licensed products and commercially available reagents routinely used for adoptive cell therapy. The parties will continue the development of improved methods for the generation and selection of TIL with anti-tumor reactivity in metastatic melanoma, bladder, lung, breast, and HPV-associated cancers.

13

Pursuant to the terms of the CRADA, we are currently required to make quarterly payments of $0.5 million to the NCI for support of research activities. To the extent we license patent rights relating to a TIL-based product candidate, we will be responsible for all patent-related expenses and fees, past and future, relating to the TIL-based product candidate. In addition, we may be required to supply certain test articles, including TIL, grown and processed under cGMP conditions, suitable for use in clinical trials, where we hold the investigational new drug application for such clinical trial. The extended CRADA has a five-year term expiring in August 2021. The Company or the NCI may unilaterally terminate the CRADA for any reason or for no reason at any time by providing written notice at least 60 days before the desired termination date. The Company recorded costs associated with the CRADA of $0.5 million for the three months ended September 30, 2017 and 2016, respectively and was $1.5 million for the nine months ended September 30, 2017 and 2016, respectively. These costs were recorded as research and development expenses.

Patent License Agreement Related to the Development and Manufacture of TIL

Effective October 5, 2011, the Company entered into a Patent License Agreement with the National Institutes of Health, an agency of the United States Public Health Service within the Department of Health and Human Services (NIH), which Patent License Agreement was subsequently amended on February 9, 2015 and October 2, 2015. Pursuant to the Patent License Agreement as amended, the NIH granted the Company licenses, including exclusive, co-exclusive, and non-exclusive licenses, to certain technologies relating to autologous tumor infiltrating lymphocyte adoptive cell therapy products for the treatment of metastatic melanoma, lung, breast, bladder and HPV-positive cancers. The Patent License Agreement requires the Company to pay royalties based on a percentage of net sales (which percentage is in the mid-single digits), a percentage of revenues from sublicensing arrangements, and lump sum benchmark royalty payments on the achievement of certain clinical and regulatory milestones for each of the various indications and other direct costs incurred by the NIH pursuant to the agreement.

Exclusive Patent License Agreement Related to TIL Selection

On February 10, 2015, the Company entered into an Exclusive Patent License Agreement with the NIH under which the Company received an exclusive license to the NIH’s rights to patent-pending technologies related to methods for improving adoptive cell therapy through more potent and efficient production of TIL from melanoma tumors by selecting for T-cell populations that express various inhibitory receptors. Unless terminated sooner, the license shall remain in effect until the last licensed patent right expires.

In consideration for the exclusive rights granted under the Exclusive Patent License Agreement, the Company agreed to pay the NIH a non-refundable upfront licensing fee in the amount of $0.8 million. The Company also agreed to pay customary royalties based on a percentage of net sales of a licensed product (which percentage is in the mid-single digits), a percentage of revenues from sublicensing arrangements, and lump sum benchmark payments upon the successful completion of clinical studies involving licensed technologies, the receipt of the first FDA approval or foreign equivalent for a licensed product or process resulting from the licensed technologies, the first commercial sale of a licensed product or process in the United States, and the first commercial sale of a licensed product or process in any foreign country. The Company will also be responsible for all costs associated with the preparation, filing, maintenance and prosecution of the patent applications and patents covered by the License. The costs associated with this agreement were immaterial for the three and nine month periods.

H. Lee Moffitt Cancer Center

Research Collaboration and Clinical Grant Agreements with Moffitt

In September 2014, we entered into a research collaboration agreement with Moffitt to jointly engage in translational research and development of adoptive tumor-infiltrating lymphocyte cell therapy with improved anti-tumor properties and process.

In December 2016, we entered into a new three-year Sponsored Research Agreement with Moffitt (the “Moffitt SRA”). At the same time, we entered into a Clinical Grant Agreement with Moffitt to support an ongoing clinical trial at Moffitt that combines TIL therapy with Opdivo® (nivolumab) for the treatment of patients with metastatic melanoma. In June 2017, we entered into a second Clinical Grant Agreement with Moffitt to support a new clinical trial at Moffitt that combines TIL therapy with Opdivo for the treatment of patients with non-small cell lung cancer.

Exclusive License Agreement with Moffitt

The Company entered into a license agreement with Moffitt (the “Moffitt License”), effective as of June 28, 2014, under which the Company received a world-wide license to Moffitt’s rights to patent-pending technologies related to methods for improving TIL for adoptive cell therapy. Unless earlier terminated, the term of the license extends until the earlier of the expiration of the last issued patent related to the licensed technology or 20 years after the effective date of the license agreement.

14

Pursuant to the Moffitt License, the Company paid an upfront licensing fee in the amount of $0.1 million. A patent issuance fee will also be payable under the Moffitt License, upon the issuance of the first U.S. patent covering the subject technology. In addition, the Company agreed to pay milestone license fees upon completion of specified milestones, customary royalties based on a specified percentage of net sales (which percentage is in the low single digits) and sublicensing payments, as applicable, and annual minimum royalties beginning with the first sale of products based on the licensed technologies, which minimum royalties will be credited against the percentage royalty payments otherwise payable in that year. The Company will also be responsible for all costs associated with the preparation, filing, maintenance and prosecution of the patent applications and patents covered by the Moffitt License related to the treatment of any cancers in the United States, Europe and Japan and in other countries designated by the Company in agreement with Moffitt. The Company recorded costs associated with Moffitt of $2.0 million and $0.0 million for the three months ended September 30, 2017 and 2016, respectively and $4.3 million and $0.4 million for the nine months ended September 30, 2017 and 2016, respectively. These costs were recorded as research and development expenses.

PolyBioCept and Karolinska University Hospital

PolyBioCept Exclusive and Co-Exclusive License Agreement

On September 14, 2016, the Company entered into an Exclusive and Co-Exclusive License Agreement (the “PolyBioCept Agreement”) with PolyBioCept AB, a corporation organized under the laws of Sweden (“PolyBioCept”). PolyBioCept has filed two patent applications with claims related to a cytokine cocktail for use in expansion of lymphocytes, one of which has been abandoned. Under the PolyBioCept Agreement, the Company received the exclusive right and license to PolyBioCept’s intellectual property to develop, manufacture, market and genetically engineer TIL produced by expansion, selection and enrichment using a proprietary cytokine cocktail. The Company also received a co-exclusive license (with PolyBioCept) to develop, manufacture and market genetically engineered TIL under the same intellectual property. The licenses are for the use in all cancers and are worldwide in scope, with the exception that the uses in melanoma are not included for certain countries of the former Soviet Union.

The Company paid PolyBioCept a total of $2.5 million as an up-front exclusive license payment. The Company will also have to make additional milestone payments to PolyBioCept under the PolyBioCept Agreement if, and when, (i) certain product development milestones are achieved, (ii) certain regulatory approvals have been obtained from the FDA and/or the European Medicines Agency, and (iii) certain product sales targets are achieved. The milestone payments will be payable both in cash (U.S. dollars) and in shares of the Company’s common stock. If all of the foregoing product development, regulatory approval and sales milestone payments are met, the Company will have to pay PolyBioCept an additional $8.7 million and will have to issue to PolyBioCept a total 2,219,376 shares of unregistered common stock. In addition to these potential payments, the Company will reimburse PolyBioCept up to $0.2 million in expenses related to the transfer of know-how and will pay PolyBioCept $0.1 million as a clinical trials management fee. The Company also separately engaged PolyBioCept as a consultant to provide certain product development and research related services in a one-year agreement for up to $0.2 million, subject to the consent of the Karolinska Institute to the services to be performed by its employees thereunder. The PolyBioCept Agreement has an initial term of 30 years, and may be extended for additional five-year periods. The Company recorded costs associated with the PolyBioCept of $0.0 million and $2.4 million for the three months ended September 30, 2017 and 2016, respectively and $0.2 million and $2.5 million for the nine months ended September 30, 2017 and 2016, respectively. These costs were recorded as research and development expenses.

Karolinska University Hospital and Karolinska Institute Agreements

In connection with the execution of the PolyBioCept Agreement, the Company also (i) entered into a clinical trials agreement with the Karolinska University Hospital to conduct clinical trials in glioblastoma and pancreatic cancer at the Karolinska University Hospital, and (ii) agreed to enter into a sponsored research agreement with the Karolinska Institute for the research of the cytokine cocktail in additional indications. The Company agreed to enter into the sponsored research agreement within 90 days after the date of the PolyBioCept Agreement, which date has been extended by amendments to the PolyBioCept Agreement. Failure to enter into the sponsored research agreement or further amend the PolyBioCept Agreement will give PolyBioCept the right to terminate the PolyBioCept Agreement (and the Company shall have the right to repayment of $2.2 million of the payments it made). The Company will pay the Karolinska Institute an additional $2.6 million in connection with these other related agreements. In 2016 the Company paid Karolinska University Hospital $1.6 million under this agreement to conduct the clinical trials. The $1.6 million payment has been classified as prepaid expense and will be expensed in accordance with the Company’s Research and Development Expense significant accounting practices. The Company had no costs associated with the Karolinska University Hospital for the three months ended September 30, 2017 and 2016, respectively and was $0.7 million and $0.0 million for the nine months ended September 30, 2017 and 2016, respectively. These costs were recorded as research and development expenses.

M.D. Anderson Cancer Center

Strategic Alliance Agreement

On April 17, 2017, the Company entered into a Strategic Alliance Agreement (the “SAA”) with M.D. Anderson Cancer Center (“M.D. Anderson”) under which the Company and M.D. Anderson agreed to conduct clinical and preclinical research studies. The Company agreed in the SAA to provide total funding not to exceed approximately $14.2 million for the performance of the multi-year studies under the SAA. In return, we will acquire all rights to inventions resulting from the studies and have been granted a non-exclusive, sub-licensable, royalty-free, and perpetual license to specified background intellectual property of M.D. Anderson reasonably necessary to exploit, including the commercialization of, any invention. We have also been granted certain rights in clinical data generated by M.D. Anderson outside of the clinical trials to be performed under the SAA. The SAA’s term shall continue in effect until the later of the fourth anniversary of the SAA or the completion or termination of the research and receipt by us of all deliverables due from M.D. Anderson thereunder. As of September 30, 2017, the Company had paid $1.4 million under this agreement. This amount has been recorded as a prepaid asset, and will be amortized to research and development expenses based on enrollment and other factors. The Company has not recorded any expense associated with the M.D. Anderson SAA for the three and nine months ended September 30, 2017.

15

MedImmune

In December 2015, the Company entered into a collaboration to conduct clinical and preclinical research in immuno-oncology with MedImmune, the global biologics research and development arm of AstraZeneca. Under the terms of the agreement, the Company will fund and conduct at least one Phase 2a clinical trial combining MedImmune's PD-L1 inhibitor, IMFINZI™ (durvalumab)with TIL for the treatment of patients. MedImmune will supply IMFINZI for the clinical trials. The purpose of the studies is to establish a dosing regimen for this combination therapy and assess its safety and efficacy.

NOTE 8. LEGAL PROCEEDINGS

Class Action Lawsuits . On April 10, 2017, the SEC announced settlements with us and with other public companies and unrelated parties in the In the Matter of Certain Stock Promotion investigation. Our settlement with the SEC is consistent with our previous disclosures (including in our Form 10-K that we filed with the SEC on March 9, 2017). On April 14 2017, a purported shareholder filed a class action complaint in the United States District Court, Northern District of California for violations of the federal securities laws (Leonard DeSilvio v. Lion Biotechnologies, Inc., et al., case no: 3:17cv2086 ) against our company and three of our former officers and directors. On April 19, 2017, a second class action complaint (Amra Kuc vs. Lion Biotechnologies, Inc., et al., case no: 3:17cv2086) was filed in the same court. Both complaints allege, among other things, that the defendants violated the federal securities laws by making materially false and misleading statements, or by failing to make certain disclosures, regarding the actions taken by Manish Singh, our former CEO, and our former investor relations firm that were the subject of the In the Matter of Certain Stock Promotions SEC investigation. On July 20, 2017 the plaintiff in the Kuc case filed a notice to voluntarily dismiss that case. The Court entered an order dismissing the Kuc complaint on July 21, 2017. On July 26, 2017, the court appointed a movant as lead plaintiff. On September 8, 2017, the lead plaintiff filed an amended complaint that alleges, among other things, that the defendants violated the federal securities laws by making materially false and misleading statements, or by failing to make certain disclosures, regarding the actions taken by Manish Singh and our former investor relations firm that were the subject of the In the Matter of Certain Stock Promotions SEC investigation. On October 6, 2017, the court entered an order setting a schedule for the case, which includes a briefing schedule for motions to dismiss and a hearing date of December 22, 2017.

We intend to vigorously defend against the foregoing complaints. Based on the very early stage of the litigation, it is not possible to estimate the amount or range of possible loss that might result from an adverse judgment or a settlement of these matters.

Solomon Capital, LLC. On April 8, 2016, a lawsuit titled Solomon Capital, LLC, Solomon Capital 401(K) Trust, Solomon Sharbat and Shelhav Raff v. Lion Biotechnologies, Inc. was filed by Solomon Capital, LLC, Solomon Capital 401(k) Trust, Solomon Sharbat and Shelhav Raff against the Company in the Supreme Court of the State of New York, County of New York (index no. 651881/2016). The plaintiffs allege that, between June and November 2012 they provided to the Company $0.1 million and that they advanced and paid on our behalf an additional $0.2 million. The complaint further alleges that the Company agreed to (i) provide them with promissory notes totaling $0.2 million, plus interest, (ii) issue a total of 111,425 shares to the plaintiffs (before the 1-for-100 reverse split of our common stock effected in September 2013), and (iii) allow the plaintiffs to convert the foregoing funds into our securities in the next transaction. The plaintiffs allege that they should have been able to convert their advances and payments into shares of the Company’s common stock in the restructuring that was effected in May 2013. Based on the foregoing, the plaintiffs allege causes for breach of contract and unjust enrichment and demand judgment against the Company in an unspecified amount exceeding $1.5 million, plus interest and attorneys’ fees.

On June 3, 2016, the Company filed an answer and counterclaims in the lawsuit. In its counterclaims, the Company alleges that the plaintiffs misrepresented their qualifications to assist it in fundraising and that they failed to disclose that they were under investigation for securities laws violations. The Company is seeking damages in an amount exceeding $0.5 million and an order rescinding any and all agreements that the plaintiffs contend entitled them to obtain stock in the Company.

On April 19, 2017, the Court granted plaintiffs’ counsel’s motion to withdraw from the case. On May 25, 2017, plaintiffs filed a notice that they had hired new counsel. On June 7, 2017, the judge presiding over the case recused herself because of a conflict of interest arising from her relationship with plaintiffs’ new attorneys. The case has been assigned to a new judge, but the court has not yet scheduled a status conference or otherwise set a schedule for the case.

The Company intends to vigorously defend the complaint and pursue its counterclaims.

Litigation Involving Dr. Steven Fischkoff. On June 13, 2017, in an action titled Steven Fischkoff v. Lion Biotechnologies, Inc. and Maria Fardis, Dr. Steven Fischkoff, our former Vice President and Chief Medical Officer, filed a lawsuit against the Company in the Supreme Court of the State of New York County of New York. Dr. Fischkoff was dismissed by the Company on March 28, 2017. Dr. Fischkoff was terminated “for cause” as that term is defined in his employment agreement. In his complaint, Dr. Fischkoff alleges breaches of his employment agreement and violation of New York Labor Law for failure to pay monies purportedly owed to him, and seeks to recover amounts including severance pay and retention bonus (totaling $300,000), a prorated incentive bonus, and amounts relating to unvested options to 150,000 shares of our common stock, together with prejudgment interest, costs, expenses and attorneys’ fees. On July 5, 2017, the Company filed a removal petition and removed the lawsuit to the United States District Court for the Southern District of New York, where the case has been assigned case no. 17-cv-05041. On July 14, 2017, the Company filed a partial answer and counterclaims against Dr. Fischkoff, denying his allegations, and alleging breach of contract and related claims, breach of fiduciary duty, and state and federal trade secret misappropriation and related claims, and sought a temporary restraining order and preliminary injunction against Dr. Fischkoff. On July 18, 2017, the court issued a temporary restraining order against Dr. Fischkoff requiring him to return Company materials, prohibiting him from disclosing or using Company materials, and granting expedited discovery, which is currently proceeding.

16

We intend to vigorously defend against Dr. Fischkoff’s lawsuit and pursue the Company’s counterclaims. Based on the very early stage of the litigation, it is not possible to estimate the amount or range of (i) a possible loss that might result from an adverse judgment or settlement of this action, or (ii) the potential recovery that might result from a favorable judgment or a settlement of this action.

Other Matters. During the second quarter of 2016, warrants representing 128,500 shares were exercised. The 128,500 shares of common stock had previously been registered for re-sale. However, we believe that these 128,500 warrant shares were sold by the holders in open market transactions in May 2016 at a time when the registration statement was ineffective. Accordingly, those sales were not made in accordance with Sections 5 and 10(a)(3) of the Securities Act, and the purchasers of those shares may have rescission rights (if they still own the shares) or claims for damages (if they no longer own the shares). The amount of any such liability is uncertain and as such, an accrual for any potential loss has not been made. The Company believes that any claims brought against it would not result in a material impact to the Company’s financial position or results of operations. The Company has not accrued a loss for a potential claim associated with this matter as it is unable to estimate any at this time.

The Company may be involved, from time to time, in legal proceedings and claims arising in the ordinary course of its business. Such matters are subject to many uncertainties and outcomes are not predictable with assurance. The Company accrues amounts, to the extent they can be reasonably estimated, that it believes are adequate to address any liabilities related to legal proceedings and other loss contingencies that the Company believes will result in a probable loss. While there can be no assurances as to the ultimate outcome of any legal proceeding or other loss contingency involving the Company, management does not believe any pending matter will be resolved in a manner that would have a material adverse effect on the Company’s financial position, results of operations or cash flows.

NOTE 9. COMMITMENTS AND CONTINGENCIES

Facilities Leases

Tampa Lease

In December 2014, the Company commenced a five-year non-cancellable operating lease with the University of South Florida Research Foundation for a 5,115 square foot facility located in Tampa, Florida. The facility is part of the University of South Florida research park and is used as the Company’s research and development facilities. The Company has the option to extend the lease term of this facility for an additional five-year period on the same terms and conditions, except that the base rent for the renewal term will be increased in accordance with the applicable consumer price index.

In April 2015, the Company amended the original lease agreement to increase the rentable space to 6,043 square feet. In September 2016, the Company further increased the rentable space to 8,673 square feet. The per square foot cost and term of the lease were unchanged.

San Carlos Lease

On August 4, 2016, the Company entered into an agreement to lease 8,733 square feet in San Carlos, California. The term of the lease is 54 months subsequent to the commencement date, and total expected rental payments under the lease are expected to be $2.1 million.

On April 28, 2017, the Company entered into a sublease agreement with Teradata US, Inc., pursuant to which the Company agreed to sublease certain office space located adjacent to the Company's headquarters in San Carlos, California. The space consists of approximately 11,449 rentable square feet in the building located in San Carlos, California and will expire on October 31, 2018.

New York Lease

The Company leases office space in New York for a monthly rental of approximately $18,000 a month through July 2017. On June 5, 2017, the Company entered into an agreement whereby the Company will lease office space from August 1, 2017 to July 31, 2018 for approximately $9,000 a month.

17

The Company recognizes rental expense on the facilities on a straight-line basis over the lease term. Differences between the straight-line rent expense and rent payments are classified as deferred rent liability on the balance sheet. As of September 30, 2017, the Company's future minimum lease payments under non-cancelable operating leases are as follows (in thousands):

| Year | Operating Lease Commitments | |||

| 2017 (remaining three months) | $ | 276 | ||

| 2018 | 1,023 | |||

| 2019 | 700 | |||

| 2020 | 495 | |||

| 2021 | 169 | |||

| $ | 2,663 | |||

Rent expense was $0.3 million and $0.2 million for the three months ended September 30, 2017 and 2016, respectively and was $0.7 million and $0.4 million for the nine months ended September 30, 2017 and 2016, respectively.

NOTE 10. RELATED PARTY TRANSACTIONS

Sanford J. Hillsberg, one of the Company’s directors, is an attorney at TroyGould PC. TroyGould PC rendered and continues to render legal services to the Company. The Company paid TroyGould PC $0.1 million and $0.4 million for the three months ended September 30, 2017 and 2016, respectively and $0.5 million and $0.7 million for the nine months ended September 30, 2017 and 2016, respectively. Mr. Hillsberg did not directly provide any legal services to the Company during the periods noted. As of September 30, 2017, the Company had $0.1 million in liabilities owing to TroyGould PC related to legal services.

On September 14, 2017, we entered into a three-year consulting agreement with Iain Dukes, D. Phil, the Chairman of our Board of Directors. As compensation for his consulting services, we granted Dr. Dukes a stock option to purchase up to 150,000 shares of our common stock, at an exercise price of $7.30 per share. Under the Consulting Agreement, Dr. Dukes agreed to provide the Company with services regarding business development opportunities, licensing transactions and technology acquisitions by the Company, and any such strategic initiatives appropriate for the Company that Dr. Dukes may identify. The granted stock options vest in 12 quarterly installments (with 1/12th of the option shares having vested on the date of grant). The vesting of the granted stock options will accelerate, and the entire award will become fully vested upon the closing of a significant licensing transaction, a material product acquisition, a material strategic transaction, or upon a Change of Control transaction. The Company recognized $0.1 million for the three months ended September 30, 2017, and $0.1 million for the nine months ended September 30, 2017.

18

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations. |

In this section, “we,” “our,” “ours” and “us” refer to Iovance Biotherapeutics, Inc.

This management’s discussion and analysis of financial condition as of September 30, 2017 and results of operations for the three and nine months ended September 30, 2017 and 2016, should be read in conjunction with management’s discussion and analysis of financial condition and results of operations included in our Annual Report on Form 10-K for the year ended December 31, 2016 which was filed with the SEC on March 8, 2017.

Forward-Looking Statements

The discussion below includes forward-looking statements based upon current expectations that involve risks and uncertainties, such as our plans, objectives, expectations and intentions. Actual results and the timing of events could differ materially from those anticipated in these forward-looking statements as a result of a number of factors. We use words such as “anticipate,” “estimate,” “plan,” “project,” “continuing,” “ongoing,” “expect,” “believe,” “intend,” “may,” “will,” “should,” “could,” and similar expressions to identify forward-looking statements. All forward-looking statements included in this Quarterly Report are based on information available to us on the date hereof and, except as required by law, we assume no obligation to update any such forward-looking statements. For a discussion of some of the factors that may cause actual results to differ materially from those suggested by the forward-looking statements, please read carefully the information in the “Risk Factors” section in our Form 10-K for the year ended December 31, 2016. The identification in this Quarterly Report of factors that may affect future performance and the accuracy of forward-looking statements is meant to be illustrative and by no means exhaustive. All forward-looking statements should be evaluated with the understanding of their inherent uncertainty.

Background on the Company

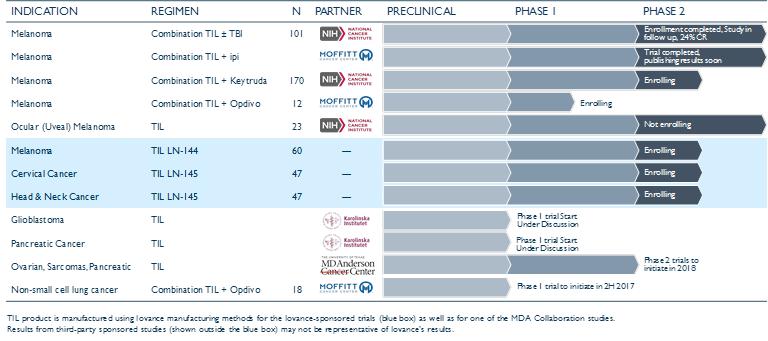

We are a clinical-stage biopharmaceutical company focused on the development and commercialization of novel cancer immunotherapy products designed to harness the power of a patient’s own immune system to eradicate cancer cells. Our lead program is an adoptive cell therapy utilizing tumor-infiltrating lymphocytes (TIL), which are T cells derived from patients’ tumors, for the treatment of metastatic melanoma as a lead indication as well as other cancer types.

A patient's immune system, particularly their TIL, can play an important role in identifying and killing cancer cells. TIL consist of a polyclonal population of T cells that can recognize a wide variety of cancer-specific antigens. TIL therapy involves growing a patient's TIL in special culture conditions outside of the patient's body, or ex vivo, and then infusing the T cells back into the patient followed by infusion of up to six doses of interleukin-2 (IL-2). By expanding a patient’s TIL ex vivo, away from the immunosuppressive tumor microenvironment, the T cells can rapidly proliferate in the presence of IL-2. As a result, billions of TIL, when infused back into the patient subsequent to administration of non-myeloablative chemotherapy to remove the patient’s hostile microenvironment, are expected to be better able to potentially eradicate the tumor.

We have an on-going Phase 2 clinical trial of our lead product candidate, autologous TIL product (LN-144), for the treatment of metastatic melanoma. This three-arm study is enrolling patients with melanoma whose disease has progressed following treatment with at least one systemic therapy which include anti-PD-1 and if BRAF mutated, a BRAF inhibitor. The trial opened for enrollment during the second half of 2015 and is being conducted at eleven U.S. sites. The purpose of the study is to evaluate the efficacy, as defined by overall response rate (ORR), as a primary endpoint, and to evaluate safety and efficacy as secondary endpoints. An interim update from cohort one of this Phase 2 trial was presented at the American Society of Clinical Oncology (ASCO) 2017 conference. In June 2017, we reported data from 16 patients enrolled in the first cohort of this study. The data reported showed clinically-meaningful outcomes of the evaluable patients, with a 29% ORR (per RECIST v1.1) including one complete response continuing beyond 15 months post-administration of a single TIL treatment, and 77% of patients had reduction in target tumor size. The Phase 2 study was conducted in a heavily pre-treated patient group, all of which had received prior anti-PD-1 therapy and 88% of which had received prior anti-CTLA-4 checkpoint inhibitors, with a median of three prior therapies. The most common treatment emergent serious adverse events observed were febrile neutropenia and decreases in neutrophil count and platelet count.

During 2015, we received an orphan drug designation for LN-144 in the United States to treat malignant melanoma stages IIB-IV. This designation provides seven years of market exclusivity in the United States, subject to certain limited exceptions. However, the orphan drug designation does not convey any advantage in, or shorten the duration of, the regulatory review or approval process.

We are pursuing metastatic melanoma as our first target indication because of the promising initial results in this indication generated by Dr. Steven Rosenberg, M.D., Ph.D., Chief of the Surgery Branch of the National Cancer Institute (NCI) and the commercial opportunity inherent in the significant unmet need of this patient population. Melanoma is a common type of skin cancer, accounting for approximately 87,110 patients diagnosed and 9,730 deaths in 2017 in the United States according to the American Cancer Society’s Cancer Estimates for 2017. According to the NCI’s Surveillance, Epidemiology and End Results (SEER) program, about 2-5% of patients with melanoma have metastatic disease. Patients with metastatic melanoma following treatment under the current standards of care have a particularly dire prognosis with very few curative treatment options.

19

In addition to our ongoing trial in metastatic melanoma, we have initiated clinical trials of TIL therapy in recurrent, metastatic, or persistent cervical cancer and in recurrent and/or metastatic squamous cell carcinoma of the head and neck. In the future, we plan to initiate clinical studies in additional indications by the company as well as through collaborations.

Our current product candidate pipeline is summarized in the graphic below:

Recent Events Affecting our Financial Condition and Operations

On April 17, 2017, we entered into a Strategic Alliance Agreement (the “SAA”) with M.D. Anderson Cancer Center (“M.D. Anderson”) under which we and M.D. Anderson agreed to conduct clinical and preclinical research studies. Initially, we plan to conduct multi-arm clinical trials to evaluate tumor-infiltrating lymphocyte, or TIL, technology in several different cancers using two different TIL manufacturing processes. We have agreed in the SAA to provide total funding not to exceed approximately $14.2 million for the performance of the multi-year studies under the SAA.

On June 1, 2017, we reincorporated from a Nevada corporation to a Delaware corporation.

On June 27, 2017, we changed our name from “Lion Biotechnologies, Inc.” to “Iovance Biotherapeutics, Inc.”

On August 31, 2017, we were granted Fast Track designation by the U.S. Food and Drug Administration (FDA) for LN-144, TIL in advanced melanoma.

On September 7, 2017, we entered into a preclinical research collaboration with The Ohio State University Comprehensive Cancer Center – Arthur G. James Cancer Hospital and Richard J. Solove Research Institute (OSUCCC – James) focused on TIL, marrow-infiltrating lymphocyte (MIL) and peripheral blood-associated lymphocyte technologies. The collaboration will initially focus on hematologic malignancies in areas of poor prognostic cancers with high unmet medical need, which include acute myeloid leukemia (AML) and chronic lymphocytic leukemia (CLL).

In September 2017, we completed an underwritten public offering, in which we sold 8,846,154 shares of common stock at a public offering price of $6.50 per share. We received gross proceeds of approximately $57.5 million and net proceeds of approximately $54 million, net of underwriting discounts and offering expenses.

The Company has previously disclosed its clinical trials agreement to conduct clinical trials in glioblastoma and pancreatic cancer at Karolinska University Hospital. As a result of personnel changes at the Karolinska University Hospital, the Company expects that the start of those clinical trials will be delayed to dates that have not yet been determined.

20

Results of Operations

Revenues

As a development stage company that is currently engaged in the development of novel cancer immunotherapy products, we have not yet generated any revenues from our biotechnology business or otherwise since our formation. We currently do not anticipate that we will generate any revenues during 2017 from the sale or licensing of our products. Our ability to generate revenues in the future will depend on our ability to complete the development of our product candidates and to obtain regulatory approval for them.

Research and Development (in thousands)

| Three months ended September 30, | Increase (Decrease) | Nine months ended September 30, | Increase (Decrease) | |||||||||||||||||||||||||||||