As filed electronically with the Securities and Exchange Commission on or about July 29, 2021

Registration No. 333-255787

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

_________________________________________

FORM N-14

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

[X] Pre-Effective Amendment No. 1 [ ] Post-Effective Amendment

No. ___

| FIRST TRUST EXCHANGE-TRADED FUND III |

(Exact Name of Registrant as Specified in Charter)

| 120 East Liberty Drive Suite 400 Wheaton, Illinois 60187 |

(Address of Principal Executive Offices) (Zip Code)

| (630) 765-8000 |

(Registrant’s Area Code and Telephone Number)

|

W. Scott Jardine

First Trust Advisors L.P. Suite 400 120 East Liberty Drive Wheaton, Illinois 60187 |

(Name and Address of Agent for Service)

With copies to:

Eric F. Fess

Chapman and Cutler LLP

111 West Monroe Street

Chicago, Illinois 60603

TITLE OF SECURITIES BEING REGISTERED:

Shares of beneficial interest ($0.01

par value per share) of

First Trust RiverFront Dynamic Developed International ETF, a Series of

the Registrant.

Approximate date of proposed public offering: As soon as practicable after the effective date of this Registration Statement.

No filing fee is required because of reliance on Section 24(f) and an indefinite number of shares have previously been registered pursuant to Rule 24f-2 under the Investment Company Act of 1940.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

First Trust RiverFront Dynamic Asia

Pacific ETF

A Message from the Chairman of the Board of Trustees

[ ], 2021

Dear Shareholder:

I am writing to inform you about a transaction that will affect your investment in First Trust RiverFront Dynamic Asia Pacific ETF (“RFAP”). Enclosed is an information statement and prospectus (“Information Statement/Prospectus”) containing information regarding the planned reorganization transaction (the “Reorganization”) whereby RFAP will be combined with First Trust RiverFront Dynamic Developed International ETF (“RFDI”), an exchange-traded fund (“ETF”) organized as a separate series of First Trust Exchange-Traded Fund III, an open-end management investment company, pursuant to which shareholders of RFAP will become shareholders of RFDI.

Through the Reorganization, shares of RFAP will be exchanged, on a tax-free basis for federal income tax purposes (although the RFAP shareholders who receive cash in lieu of fractional shares of RFDI may incur certain tax liabilities) as further described herein, for shares of RFDI with an equal aggregate net asset value, and RFAP shareholders will become shareholders of RFDI.

In determining to approve the Reorganization, the Board of Trustees of RFAP considered the following factors, among others:

| · | RFAP and RFDI utilize similar investment strategies and are both sub-advised by RiverFront Investment Group, LLC; |

| · | the Reorganization is expected to allow shareholders of RFAP to hold shares of a fund with significantly greater net assets; and |

| · | the Reorganization is expected to qualify as a tax-free reorganization for federal income tax purposes. |

The Board of Trustees of RFAP has approved the Agreement and Plan of Reorganization (the “Plan”) and the transactions it contemplates. A form of the Plan is attached as Exhibit A to the enclosed Information Statement/Prospectus.

Also included in this booklet is an Information Statement/Prospectus, which provides detailed information on RFDI and why the Reorganization is being effected, including the differences between RFAP and RFDI.

We urge you to review the enclosed materials thoroughly.

Sincerely yours,

James A. Bowen

Chairman of the Board of Trustees,

First Trust RiverFront Dynamic Asia Pacific ETF

First

Trust RiverFront Dynamic Asia Pacific ETF

Questions & Answers

[ ], 2021

Although we recommend that you read the entire Information Statement/Prospectus, for your convenience, we have provided a brief overview of the reorganization of First Trust RiverFront Dynamic Asia Pacific ETF into First Trust RiverFront Dynamic Developed International ETF including the reasons for the reorganization.

| Q. | What is happening? |

| A. | First Trust RiverFront Dynamic Asia Pacific ETF (“RFAP”) is being reorganized into First Trust RiverFront Dynamic Developed International ETF (“RFDI,” and RFAP and RFDI are each a “Fund” and, together, the “Funds”), both of which are a series of First Trust Exchange-Traded Fund III (the “Trust”), pursuant to an Agreement and Plan of Reorganization (the “Plan”) between the Trust, on behalf of RFAP, and the Trust, on behalf of RFDI, pursuant to which the assets and liabilities of RFAP will be transferred to RFDI, and shareholders of RFAP will become shareholders of RFDI (collectively, the “Reorganization”). RFDI will be the accounting survivor in the Reorganization. |

| Q. | How will the Reorganization be effected? |

| A. | RFAP will be reorganized into RFDI. Upon the closing of the reorganization of RFAP into RFDI, RFAP shareholders will receive newly issued shares of RFDI. Shareholders of RFAP will receive a number of RFDI shares equal in aggregate net asset value to the aggregate net asset value of the RFAP shares held by such shareholders (and cash in lieu of fractional shares of RFDI), each computed as of the close of regular trading on the New York Stock Exchange on the business day immediately prior to the date of the closing of the Reorganization (the “Valuation Time”). Aggregate net asset value is the value of a fund’s assets minus it liabilities and should not be confused with the market value of a fund’s shares. |

Immediately following the reorganization, RFAP will be terminated as a series of the Trust.

| Q. | Why is the Reorganization being recommended? |

| A. | Since its inception in April 2016, RFAP has failed to attract assets or achieve scale. This may be partially due to the fact that, over the 1-year and 3-year periods ended December 31, 2020 and since inception through December 31, 2020, RFAP has underperformed its peer funds and benchmark. RFAP’s management has regularly monitored the size and performance of RFAP and considered a variety of alternatives to increase its assets and has sought to develop a viable approach to attempt to address RFAP’s lack of scale. RFDI has significantly greater assets than RFAP and has seen better performance relative to its benchmark and peer average. Since the Funds’ inception date in 2016, RFDI has returns of 7.64% while RFAP has returns of 4.88%. The Board of Trustees and management of RFAP believe the Reorganization may allow RFAP shareholders who become shareholders of RFDI to experience the benefits associated with holding shares in a fund with significantly greater assets than RFAP while allowing RFAP’s shareholders the opportunity to continue their investment in a similar strategy with the same adviser, sub-adviser and portfolio managers that, although not specifically focused in the Asia Pacific region like RFAP’s strategy, also provides exposure to Asian Pacific companies. When the Reorganization is consummated, RFAP’s shareholders will receive RFDI shares equal in aggregate net asset value to the aggregate net asset value of their RFAP shares as of the Valuation Time. In addition, RFDI has and is expected to maintain the same total operating expense ratio as RFAP following the Reorganization. No assurances can be given that RFDI’s total operating expense ratio will remain at its current rate. |

| Q. | Will shareholders of the Funds have to pay any fees or expenses in connection with the Reorganization? |

| A. | Yes. The direct costs associated with the Reorganization will be borne by First Trust Advisors, L.P., the investment adviser of the Funds (“First Trust” or the “Advisor”) and RiverFront Investment Group, LLC, the investment sub-adviser of the Funds (“RiverFront” or the “Sub-Advisor”). However, the indirect expenses of the Reorganization, primarily relating to the repositioning of the assets of RFAP, will be borne by RFAP and will impact the net asset value of RFAP prior to the Reorganization. Please see the question “Will the value of my investment change as a result of the Reorganization?” below for additional information regarding the repositioning of the assets of RFAP. |

| Q. | Will the shares held by RFAP shareholders continue to be listed on the Nasdaq following the Reorganization? |

| A. | Yes. RFAP shares and RFDI shares are both currently listed and trade on the Nasdaq Stock Market (“Nasdaq”), and RFDI shares will continue to be listed and trade on the Nasdaq following the Reorganization. Shareholders will bear no costs in connection with the delisting of RFAP or the listing of additional shares of RFDI in connection with the Reorganization. |

| Q. | Do the Funds have similar investment strategies and risks? |

| A. | Yes. The investment strategies of RFAP and RFDI are similar in certain respects, but have some important differences. As a result of such similarities, the Funds are subject to many of the same investment risks. |

Both RFAP and RFDI are actively managed exchange-traded funds (“ETFs”) whose investment objective is to provide capital appreciation.

Under normal market conditions, RFAP pursues its investment objective by investing at least 80% of its net assets (including investment borrowings) in a portfolio of equity securities of “Asian Pacific companies” (as defined below), through investments in common stock, depositary receipts, and common and preferred shares of real estate investment trusts (“REITs”), and forward foreign currency exchange contracts and currency spot transactions used to hedge its exposure to the currencies in which the equity securities of such Asian Pacific companies are denominated (each, an “Asian Pacific currency” and, collectively, the “Asian Pacific currencies”). Asian Pacific companies are those companies (i) whose securities are traded principally on a stock exchange in an Asian Pacific country, (ii) that have a primary business office in an Asian Pacific country, or (iii) that have at least 50% of their assets in, or derive at least 50% of their revenues or profits from, an Asian Pacific country. Asian Pacific countries include the countries located in Asia and the Pacific Islands as well as Australia and New Zealand. RFAP generally focuses its Asian Pacific company investments in Australia, Hong Kong, Japan, New Zealand and/or Singapore. The securities in which RFAP may invest must be listed on a U.S. or non-U.S. securities exchange. RFAP may invest in small, mid and large capitalization companies.

-2-

Under normal market conditions, RFDI pursues its investment objective by investing at least 80% of its net assets (including investment borrowings) in a portfolio of equity securities of developed market companies, including through investments in common stock, depositary receipts and common and preferred shares of REITs, and forward foreign currency exchange contracts and currency spot transactions used to hedge its exposure to the currencies in which the equity securities of such developed market companies are denominated (each, a “Developed Market currency” and, collectively, the “Developed Market currencies”). Developed market companies are those companies (i) whose securities are traded principally on a stock exchange in a developed market country, (ii) that have a primary business office in a developed market country, or (iii) that have at least 50% of their assets in, or derive at least 50% of their revenues or profits from, a developed market country. Developed market countries currently include the countries comprising the Morgan Stanley Capital International World Index or countries considered to be developed by the World Bank, the International Finance Corporation or the United Nations. Under normal market conditions, RFDI will invest in at least three countries and at least 40% of its net assets in countries other than the United States. The securities in which RFDI may invest must be listed on a U.S. or non-U.S. securities exchange. RFDI may invest in small, mid and large capitalization companies.

The principal differences between the investment strategies of RFAP and RFDI are that RFAP invests primarily in Asian Pacific companies whereas RFDI invests in developed market countries throughout the world, including certain Asian Pacific Companies, that RFAP has significant exposure to companies in Australia and greater exposure to companies in Japan, with more than a majority of its assets invested in Japanese companies, while RFDI has significant exposure to companies in Europe generally and companies in the United Kingdom and Switzerland specifically, and that RFDI has significant exposure to industrials companies. As a result of such differences, RFAP and RFDI are subject to different risks associated with such different investments and strategies.

| Q. | Are the Funds managed by the same portfolio management team? |

| A. | Yes. First Trust serves as the investment adviser, and RiverFront serves as the investment sub-adviser, to both RFAP and RFDI. For both Funds, RiverFront is responsible for the selection and ongoing monitoring of the securities in each Fund’s investment portfolio and First Trust is responsible for overseeing RiverFront in the investment of the Funds’ assets, managing the Funds’ business affairs and providing certain clerical, bookkeeping and other administrative services. |

-3-

| Q. | Will there be federal income tax consequences as a direct result of the Reorganization? |

| A. | No. The Reorganization is expected to qualify as a tax-free reorganization for federal income tax purposes, other than with respect to the cash paid in lieu of fractional shares of RFDI as discussed below, and will not occur unless RFAP’s counsel provides a tax opinion to that effect. RFAP shareholders may incur certain tax liabilities if they receive cash in lieu of fractional shares of RFDI. See “Information About the Reorganization —Terms of the Reorganization” in the Information Statement/Prospectus for a further discussion of the tax liabilities RFAP shareholders may incur. If a shareholder chooses to sell RFAP shares prior to the Reorganization, the sale will generate taxable gain or loss; therefore, such shareholder may wish to consult a tax advisor before doing so. Of course, the shareholder also may be subject to periodic capital gains as a result of the normal operations of RFAP whether or not the Reorganization occurs. |

RFAP, if requested by RFDI, will attempt to dispose of assets that do not conform to RFDI’s investment objective, policies and restrictions in advance of the Reorganization. It is anticipated that 75% of RFAP’s assets will be disposed of prior to the Reorganization at the request of RFDI and that such portfolio repositioning will result in transaction costs payable by RFAP in advance of the Reorganization of approximately $15,000, or $0.100 per share, or 0.172% of its net assets as of the date hereof. RFAP intends to pay a dividend of any undistributed realized net investment income, if any, immediately prior to the closing of the Reorganization of RFAP into RFDI. The amount of dividends actually paid, if any, will depend on a number of factors, such as changes in the value of RFAP’s holdings and the extent of the liquidation of securities between the date hereof and the closing of the Reorganization. Any net investment income realized prior to the Reorganization will be distributed to RFAP’s shareholders as ordinary dividends (to the extent of net realized short-term capital gains distributed) during or with respect to the year of sale, and such distributions will be taxable to RFAP’s shareholders. Such distributions are estimated as of the date hereof to be between approximately $0.60 and $0.65 per share of realized net investment income. As of the date hereof, no long-term capital gains distributions are expected to be paid by RFAP prior to the Reorganization.

| Q. | Will the value of my investment change as a result of the Reorganization? |

| A. | Shareholders of RFAP will receive a number of RFDI shares equal in aggregate net asset value to the aggregate net asset value of the RFAP shares held as of the Valuation Time (with cash being distributed in lieu of any fractional shares of RFDI). It is estimated that portfolio repositioning will result in transaction costs payable by RFAP in advance of the Reorganization of approximately $15,000, or $0.100 per share, or 0.172% of its net assets as of the date hereof, based on average costs normally incurred in such transactions. It is likely that the number of shares an RFAP shareholder owns will change as a result of the Reorganization because shares of RFAP will be exchanged for shares of RFDI at an exchange ratio based on the Funds’ relative net asset values, which will likely differ from one another at the Valuation Time. |

| Q. | When would the Reorganization be effective? |

| A. | The Reorganization is expected to occur on August 27, 2021 or as soon thereafter as practicable. Shortly after completion of the Reorganization, shareholders of RFAP will receive notice indicating that the Reorganization was completed. |

-4-

| Q. | Why is no shareholder vote necessary to approve the Reorganization? |

| A. | The Trust’s Declaration of Trust permits a series to be reorganized into another series by a vote of a majority of the Trustees of the Trust without the approval of shareholders. The Reorganization also satisfies the requisite conditions of Rule 17a-8 under the Investment Company Act of 1940, as amended (the “1940 Act”), such that shareholder approval is not required by the 1940 Act. In addition, given the relative sizes of the Funds, Nasdaq’s listing rules do not require that shareholders of RFDI vote approve the issuance of additional shares in the Reorganization. |

| Q. | Whom should I call for additional information about the Information Statement/Prospectus? |

| A. | Please call 630-517-7665. |

-5-

The information contained in this Information Statement/Prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective.

SUBJECT TO COMPLETION, DATED JULY 29, 2021

First Trust RiverFront Dynamic Asia Pacific ETF

120

East Liberty Drive, Suite 400

Wheaton, Illinois 60187

(630) 765-8000

INFORMATION STATEMENT/PROSPECTUS

| [ | ], 2021 |

This Information Statement/Prospectus is being furnished to shareholders of First Trust RiverFront Dynamic Asia Pacific ETF (“RFAP”), an exchange-traded fund organized as a separate series of First Trust Exchange-Traded Fund III, an open-end management investment company (the “Trust”). After careful consideration, the Board of Trustees of RFAP (the “Board of Trustees”) has approved an Agreement and Plan of Reorganization by and between the Trust, on behalf of RFAP, the Trust, on behalf of First Trust RiverFront Dynamic Developed International ETF (“RFDI”), an exchange-traded fund organized as a separate series of the Trust, and First Trust Advisors, L.P., the investment adviser of the Funds (“First Trust” or the “Advisor”), a copy of which is attached to this Information Statement/Prospectus as Exhibit A (the “Plan”), pursuant to which RFAP will (i) transfer all of its assets to RFDI in exchange solely for newly issued shares of RFDI and RFDI’s assumption of all of the liabilities of RFAP and (ii) immediately distribute such newly issued shares of RFDI to RFAP shareholders (collectively, the “Reorganization”). RFAP and RFDI are referred to herein collectively as the “Funds” and each is referred to herein individually as a “Fund.”

This Information Statement/Prospectus explains concisely what you should know before investing in RFDI. Please read it carefully and keep it for future reference.

The Board of Trustees has approved the Plan and the Reorganization as being in the best interests of RFAP. The Board of Trustees believes the Reorganization will allow RFAP shareholders to hold shares in a fund with significantly greater assets while allowing RFAP’s shareholders the opportunity to continue their investment in a similar investment strategy.

The Reorganization will combine the Funds, which have similar investment strategies and risks, but also have important distinctions. The Plan provides for the reorganization of RFAP into RFDI, pursuant to which RFAP will (i) transfer all of its assets to RFDI in exchange solely for newly issued shares of RFDI and RFDI’s assumption of all of the liabilities of RFAP and (ii) immediately distribute such newly issued shares of RFDI to RFAP shareholders. Shareholders of RFAP will receive a number of RFDI shares equal in aggregate net asset value to the aggregate net asset value of the RFAP shares held as of the close of regular trading on the New York Stock Exchange on the business day immediately prior to the closing of the reorganization of RFAP into RFDI (the “Valuation Time”) (with cash being distributed in lieu of any fractional shares of RFDI). Through the Reorganization, shares of RFAP will be exchanged on a tax-free basis for federal income tax purposes for shares of RFDI (although RFAP shareholders who receive cash in lieu of fractional shares of RFDI may incur certain tax liabilities).

The securities offered by this Information Statement/Prospectus have not been approved or disapproved by the Securities and Exchange Commission (the “SEC”), nor has the SEC passed upon the accuracy or adequacy of this Information Statement/Prospectus. Any representation to the contrary is a criminal offense.

RFDI lists and trades its shares on the Nasdaq Stock Exchange (“Nasdaq”). Shares of RFDI are not redeemable individually and therefore liquidity for individual shareholders of RFDI will be realized only through a sale on any national securities exchange on which the shares are traded at market prices that may differ to some degree from the net asset value of the RFDI shares. Reports and other information concerning RFDI can be inspected at the offices of the Nasdaq.

The following documents contain additional information about RFAP and RFDI, have been filed with the SEC and are incorporated by reference into this Information Statement/Prospectus:

(i) the prospectus and Statement of Additional Information of RFDI, dated March 1, 2021, including all amendments thereto, relating to shares of RFDI (SEC File No. 333-176976);

(ii) the prospectus and Statement of Additional Information of RFAP, dated March 1, 2021, including all amendments thereto, relating to shares of RFAP (SEC File No. 333-176976);

(iii) the audited financial statements and related independent registered public accounting firm’s report for RFDI and the financial highlights for RFDI contained in RFDI’s Annual Report to Shareholders for the fiscal year ended October 31, 2020 (SEC File No. 811-22245);

(iv) the unaudited financial statements for RFDI contained in RFDI’s Semi-Annual Report to Shareholders for the six months ended April 30, 2021 (SEC File No. 811-22245);

(v) the audited financial statements and related independent registered public accounting firm’s report for RFAP and the financial highlights for RFAP contained in RFAP’s Annual Report to Shareholders for the fiscal year ended October 31, 2020 (SEC File No. 811-22245); and

(vi) the unaudited financial statements for RFAP contained in RFAP’s Semi-Annual Report to Shareholders for the six months ended April 30, 2021 (SEC File No. 811-22245).

A copy of the RFDI prospectus accompanies this Information Statement/Prospectus. The Statement of Additional Information to this Information Statement/Prospectus is also incorporated by reference and legally deemed to be part of this document, and is available upon oral or written request at no charge by calling First Trust Advisors L.P. (“First Trust” or the “Advisor”) at (800) 621-1675 or by writing to First Trust at 120 E. Liberty Drive, Suite 400, Wheaton, Illinois 60187. In addition, RFDI will furnish, without charge, a copy of its prospectus, most recent Annual Report or Semi-Annual Report to a RFAP shareholder upon request. RFAP’s prospectus dated March 1, 2021, and Annual Report to Shareholders for the fiscal year ended October 31, 2020, containing audited financial statements, have been previously made available or mailed to shareholders. Copies of these documents are available upon request and without charge by writing to First Trust at the address listed above or by calling (800) 621-1675.

-ii-

The Funds are subject to the informational requirements of the Securities Exchange Act of 1934, as amended, and the Investment Company Act of 1940, as amended (the “1940 Act”), and in accordance therewith are required to file reports and other information with the SEC. These reports, proxy or information statement materials and other information filed by the Funds can be inspected and copied at the public reference facilities maintained by the SEC at 100 F. Street NE, Washington, DC 20549, and copies of such material can be obtained from the Public Reference Branch, Office of Consumer Affairs and Information Services, Securities and Exchange Commission, after paying a duplicating fee, or by electronic request at publicinfo@sec.gov. In addition, copies of these documents may be viewed online or downloaded without charge from the SEC’s website at www.sec.gov. Reports, proxy or information statement materials and other information concerning RFAP and RFDI may be inspected at the offices of the Nasdaq.

This Information Statement/Prospectus serves as a prospectus of RFDI in connection with the issuance of the RFDI shares in the Reorganization. In this connection, no person has been authorized to give any information or make any representation not contained in this Information Statement/Prospectus and, if so given or made, such information or representation must not be relied upon as having been authorized. This Information Statement/Prospectus does not constitute an offer to sell or a solicitation of an offer to buy any securities in any jurisdiction in which, or to any person to whom, it is unlawful to make such offer or solicitation.

-iii-

TABLE OF CONTENTS

| INTRODUCTION | 1 |

| A. Synopsis | 1 |

| B. Risk Factors | 6 |

| C. Information About the Reorganization | 16 |

| D. Additional Information About the Investment Policies | 25 |

| ADDITIONAL INFORMATION ABOUT RFAP AND RFDI | 36 |

| GENERAL INFORMATION | 39 |

| EXHIBIT A AGREEMENT AND PLAN OF REORGANIZATION | A-1 |

INTRODUCTION

This Information Statement/Prospectus provides information regarding the reorganization of RFAP into RFDI.

A. Synopsis

The following is a summary of certain information contained elsewhere in this Information Statement/Prospectus with respect to the Reorganization and shareholders should reference the more complete information contained in this Information Statement/Prospectus and in the Statement of Additional Information contained in this registration statement (the “Reorganization SAI”) and the appendices thereto. Shareholders should read the entire Information Statement/Prospectus carefully. Certain capitalized terms used but not defined in this summary are defined elsewhere in this Information Statement/Prospectus.

The Reorganization

The Board of Trustees of RFAP, including the trustees who are not “interested persons” of the Fund (as defined in the 1940 Act), has approved the Reorganization, including the Plan. As soon as reasonably practicable, RFAP will reorganize into RFDI, pursuant to which RFAP will (i) transfer all of its assets to RFDI in exchange solely for newly issued shares of RFDI and RFDI’s assumption of all of the liabilities of RFAP and (ii) immediately distribute such newly issued shares of RFDI to RFAP shareholders. In connection with the Reorganization, RFDI will issue to RFAP shareholders book entry interests for the shares of RFDI registered in a “street name” brokerage account held for the benefit of such shareholders. Shareholders of RFAP will receive a number of RFDI shares equal in aggregate net asset value to the aggregate net asset value of the RFAP shares held as of the Valuation Time (with cash being distributed in lieu of any fractional shares of RFDI). Through the Reorganization, shares of RFAP will be exchanged on a tax-free basis for federal income tax purposes for shares of RFDI (although RFAP shareholders who receive cash in lieu of fractional shares of RFDI may incur certain tax liabilities). See “Information About the Reorganization —Terms of the Reorganization” below for a further discussion of the tax liabilities RFAP shareholders may incur. RFDI will be the accounting survivor in the Reorganization. Like shares of RFAP, shares of RFDI are not deposits or obligations of, or guaranteed or endorsed by, any financial institution, are not insured by the Federal Deposit Insurance Corporation, the Federal Reserve Board or any other agency, and involve risk, including the possible loss of the principal amount invested.

Background and Reasons for the Reorganization

Since its inception in April 2016, RFAP has failed to attract assets or achieve scale. This may be partially due to the fact that, over 1-year and 3-year periods ended December 31, 2020 and since inception through December 31, 2020, RFAP has underperformed its peer funds and benchmark. RFAP’s management has regularly monitored the size and performance of RFAP and considered a variety of alternatives to increase its assets and has sought to develop a viable approach to attempt to address RFAP’s lack of scale. RFDI has significantly greater assets than RFAP and has seen better performance relative to its benchmark and peer average. The Board of Trustees and management of RFAP believe the Reorganization may allow RFAP shareholders who become shareholders of RFDI to experience the benefits associated with holding shares in a fund with significantly greater assets than RFAP while allowing RFAP’s shareholders the opportunity to continue their investment in a similar strategy that, although not specifically focused in the Asia Pacific region like RFAP’s strategy, also provides exposure to Asian Pacific Companies. When the Reorganization is consummated, RFAP’s shareholders will receive RFDI shares equal in aggregate net asset value to the aggregate net asset value of their RFAP shares as of the Valuation Time. Immediately after the Reorganization, RFDI will have a greater asset base than RFAP prior to the Reorganization. In addition, RFDI has and is expected to maintain the same total operating expense ratio as RFAP following the Reorganization. No assurances can be given that RFDI’s total operating expense ratio will remain at its current rate.

Board Considerations Relating to the Reorganization

Based on information provided by First Trust, the Board of Trustees of each Fund considered the following factors, among others, in determining to approve the Plan and the Reorganization it contemplates on behalf of each Fund:

| · | Compatibility of Investment Objectives and Policies. The Board noted that RFAP and RFDI are both actively managed exchange-traded funds that seek to provide capital appreciation and have similar investment strategies and the same quantitative model selection process, although RFAP invests specifically in Asia Pacific markets while RFDI invests across developed international markets. The Board also considered that approximately 40% of RFAP’s assets consisted of securities also held by RFDI as of January 12, 2021. |

| · | Comparison of Fees and Expense Ratios. The Board considered comparative expense information for RFAP and RFDI, including comparisons between the current unitary management fee rates and expense ratios for RFAP and RFDI and the estimated pro forma unitary management fee rate and expense ratio of the combined fund. The Board noted that each Fund’s unitary management fee rate is 0.83% of its average daily net assets and would not change as a result of the Reorganization. |

| · | Expenses of the Reorganization. The Board noted that the Advisor and the Sub-Advisor proposed to bear the direct costs of the Reorganization. The Board also noted the indirect costs to be borne by RFAP as a result of portfolio repositioning prior to the Reorganization. |

| · | Potential Improved Trading and Liquidity. The Board considered the larger asset size of RFDI as compared to RFAP and that shareholders of RFAP may benefit from becoming shareholders of a larger fund with higher trading volume, potentially resulting in improved liquidity and narrower bid-ask spreads experienced as shareholders of RFDI. The Board also considered the Advisor’s statement indicating that additional assets in RFDI could benefit shareholders of RFDI, as larger funds with more trading volume tend to trade at tighter spreads and funds with a higher profile among the investment community due to size or being highlighted in an investment model may continue to have success gathering assets which could further improve trading volumes and spreads. |

| · | Fund Performance. The Board reviewed the historical performance of RFAP and RFDI, noting that each Fund had underperformed its respective benchmark over the three-year period ended December 31, 2020 and over the period since the Funds’ inception on April 13, 2016 through December 31, 2020, with RFDI outperforming RFAP on an absolute basis for the three-year and since-inception periods. The Board also considered information from the Advisor indicating that, following the adjustments to the Funds’ quantitative model selection process in 2019 to improve performance, RFDI outperformed its benchmark while RFAP underperformed its benchmark for the one-year period ended December 31, 2020, although RFAP outperformed RFDI on absolute basis. |

-2-

| · | Portfolio Management. The Board noted that each Fund is managed by the Sub-Advisor’s portfolio management team, which consists of the same three individuals for each Fund. The Board noted that the Sub-Advisor’s portfolio management team would continue to manage RFDI following the closing of the Reorganization. |

| · | Anticipated Tax-Free Reorganization; Capital Loss Carryforwards. The Board noted the Advisor’s statement that the Reorganization will be structured with the intention that it qualify as a tax-free reorganization for federal income tax purposes and that RFAP and RFDI will obtain an opinion of counsel substantially to this effect (based on certain factual representations and certain customary assumptions). In addition, the Board noted information provided by the Advisor indicating that RFAP’s capital loss carryforwards would offset projected realized gains relating to portfolio repositioning and that remaining capital loss carryforwards could be transferred in the Reorganization, which, subject to certain limitations, could then be used by RFDI. |

| · | Terms and Conditions of the Reorganization. The Board considered the terms and conditions of the Reorganization and whether the Reorganization would result in the dilution of the interests of existing shareholders of RFAP and RFDI in light of the basis on which shares of RFDI would be issued to shareholders of RFAP. |

Please see “Information About the Reorganization—Background and Trustees’ Considerations Relating to the Reorganization” below for a further discussion of the deliberations and considerations undertaken by the Board of Trustees of each Fund in connection with the Reorganization.

The Board of Trustees of each Fund has concluded that the Reorganization is in the best interests of its respective Fund and that the interests of the existing shareholders of each Fund will not be diluted as a result of the Reorganization.

Material Federal Income Tax Consequences of the Reorganization

For federal income tax purposes, no gain or loss is expected to be recognized by RFAP or its shareholders as a direct result of the Reorganization other than with respect to the cash paid in lieu of fractional shares of RFDI as explained below. However, RFAP expects to reposition its portfolio prior to the Reorganization which is expected to result in net investment income. Any undistributed net investment income realized prior to the Reorganization will be distributed to RFAP’s shareholders as ordinary dividends (to the extent of net realized short-term capital gains distributed) during or with respect to the year of sale, and such distributions will be taxable to RFAP’s shareholders. It is estimated that portfolio repositioning will result in transaction costs payable by RFAP in advance of the Reorganization of approximately $15,000, or $0.100 per share, or 0.172% of its net assets as of the date hereof, based on average costs normally incurred in such transactions. As of the date hereof, no long-term capital gains dividends are expected to be paid by RFAP prior to the Reorganization. Through the Reorganization, RFAP shares will be exchanged, on a tax-free basis for federal income tax purposes (although RFAP shareholders who receive cash in lieu of fractional shares of RFDI may incur certain tax liabilities), for shares of RFDI with an equal aggregate net asset value, and RFAP shareholders will become shareholders of RFDI.

-3-

Comparison of the Funds

General. Both RFAP and RFDI are diversified, actively managed ETFs that were created as series of the Trust, an open-end management investment company organized as a Massachusetts business trust on January 9, 2008.

Investment Objectives, Policies and Strategies. The investment strategies of RFAP and RFDI are similar, but have some important distinctions, each as discussed and summarized below. The principal differences between the investment strategies of RFAP and RFDI are as follows: (i) RFAP invests primarily in Asian Pacific Companies whereas RFDI invests in developed market countries throughout the world, including certain Asian Pacific Companies, (ii) RFAP has significant exposure to companies in Australia and greater exposure to companies in Japan, with more than a majority of its assets invested in Japanese companies, while RFDI has significant exposure to companies in Europe generally and companies in the United Kingdom and Switzerland specifically, and (iii) RFDI has significant exposure to industrials companies. As a result of such differences, RFAP and RFDI are subject to the different risks associated with such different investments and strategies. The similarities and differences between the Funds’ investment objectives, principal strategies and policies and non-principal and other investment strategies and policies are highlighted below.

Each Fund’s investment objective is a fundamental policy of the Fund and may not be changed without the approval of a “majority of the outstanding voting securities” of the respective Fund. A “majority of the outstanding voting securities” means the lesser of (i) 67% or more of the shares represented at a meeting at which more than 50% of the outstanding shares are represented, or (ii) more than 50% of the outstanding shares.

Purchase, Redemption and Distribution. RFAP and RFDI issue and redeem shares on a continuous basis, at net asset value, only in large specified blocks of shares (each a “Creation Unit”). RFAP and RFDI shares are not individually redeemable securities of RFAP and RFDI, respectively, except when aggregated as Creation Units. Shares of RFAP and RFDI are listed and traded on the Nasdaq under the ticker symbols “RFAP” and “RFDI,” respectively, to provide liquidity for individual shareholders of RFAP and RFDI in amounts less than the size of a Creation Unit. Shareholders of RFAP and RFDI are entitled to dividends as declared by their respective Trustees. Each of RFAP and RFDI distribute their net investment income quarterly and their net realized capital gains at least annually, if any.

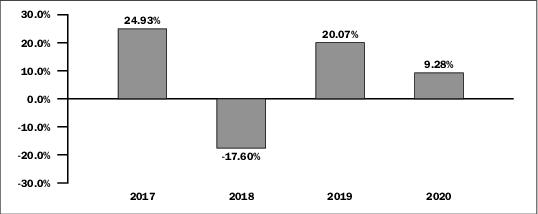

Past Performance. The bar charts and tables below provide some indication of the risks of investing in the Funds by showing you how the performance of each Fund has varied from year to year, and how the average total returns of the Funds for different periods compare. A Fund’s past performance (before and after taxes) is not necessarily an indication of how the Fund will perform in the future. Performance information for RFDI is provided below.

First Trust RiverFront Dynamic Developed International ETF

Calendar Year Total Returns as of 12/31(1)

| (1) | The Fund’s calendar year-to-date total return based on net asset value for the period January 1, 2021 to June 30, 2021 was 10.36%. |

-4-

During the period shown in the chart above:

| Best Quarter | Worst Quarter | ||

| 18.15% June 30, 2020 | -23.89% March 31, 2020 |

RFDI’s past performance (before and after taxes) is not necessarily an indication of how RFDI will perform in the future.

Returns before taxes do not reflect the effects of any income or capital gains taxes. All after-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of any state or local tax. Returns after taxes on distributions reflect the taxed return on the payment of dividends and capital gains. Returns after taxes on distributions and sale of shares assume a shareholder sold their shares at period end, and, therefore, are also adjusted for any capital gains or losses incurred. Returns for the market indices do not include expenses, which are deducted from RFDI returns, or taxes.

A shareholder’s own actual after-tax returns will depend on their specific tax situation and may differ from what is shown here. After-tax returns are not relevant to investors who hold, or will hold, RFDI shares in tax-deferred accounts such as individual retirement accounts (“IRAs”) or employee-sponsored retirement plans.

RFDI will be the accounting survivor in the Reorganization.

| Average Annual Total Returns for the Periods Ended December 31, 2020 | ||

| RFDI | 1 Year | Since Inception(1) |

| Return Before Taxes | 9.28% | 7.64% |

| Return After Taxes on Distributions | 8.57% | 6.69% |

| Return After Taxes on Distributions and Sale of Fund Shares | 5.42% | 5.52% |

| MSCI EAFE Index (reflects no deduction for fees, expenses or taxes) | 7.82% | 8.37% |

| (1) | Inception Date 4/13/2016 |

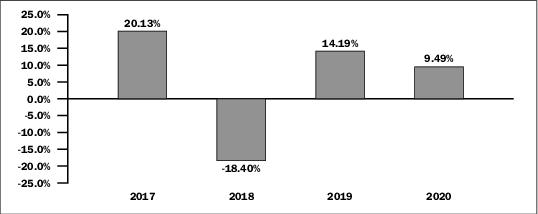

Performance information for RFAP is provided below.

First Trust RiverFront Dynamic Asia Pacific ETF

Calendar Year Total Returns as of 12/31(1)

| (1) | The Fund’s calendar year-to-date total return based on net asset value for the period January 1, 2021 to June 30, 2021 was 2.02%. |

-5-

During the period shown in the chart above:

| Best Quarter | Worst Quarter | ||

| 15.43% June 30, 2020 | -21.84% March 31, 2020 |

RFAP’s past performance (before and after taxes) is not necessarily an indication of how RFAP will perform in the future.

Returns before taxes do not reflect the effects of any income or capital gains taxes. All after-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of any state or local tax. Returns after taxes on distributions reflect the taxed return on the payment of dividends and capital gains. Returns after taxes on distributions and sale of shares assume a shareholder sold their shares at period end, and, therefore, are also adjusted for any capital gains or losses incurred. Returns for the market indices do not include expenses, which are deducted from RFAP returns, or taxes.

A shareholder’s own actual after-tax returns will depend on their specific tax situation and may differ from what is shown here. After-tax returns are not relevant to investors who hold RFAP shares in tax-deferred accounts such as IRAs or employee-sponsored retirement plans.

| Average Annual Total Returns for the Periods Ended December 31, 2020 | ||

| RFAP | 1 Year | Since Inception(1) |

| Return Before Taxes | 9.49% | 4.88% |

| Return After Taxes on Distributions | 8.68% | 3.86% |

| Return After Taxes on Distributions and Sale of Fund Shares | 5.57% | 3.30% |

| MSCI Pacific Index (reflects no deduction for fees, expenses or taxes) | 11.93% | 10.00% |

| (1) | Inception Date 4/13/2016 |

B. Risk Factors

The investment strategies of RFAP and RFDI are similar, but have some important distinctions, as discussed in this Information Statement/Prospectus. The principal differences between the investment strategies of RFAP and RFDI are as follows: (i) RFAP invests primarily in Asian Pacific Companies whereas RFDI invests in developed market countries throughout the world, including certain Asian Pacific Companies, (ii) RFAP has significant exposure to companies in Australia and greater exposure to companies in Japan, with more than a majority of its assets invested in Japanese companies, while RFDI has significant exposure to companies in Europe generally and companies in the United Kingdom and Switzerland specifically, and (iii) RFDI has significant exposure to industrials companies. As a result of such differences, RFAP and RFDI are subject to different risks associated with such different investments and strategies.

Aside from these differences, as investment companies following similar strategies, many of the principal risks applicable to an investment in RFAP are also applicable to an investment in RFDI. Shares of each Fund may change in value, and an investor could lose money by investing in either Fund. The Funds may not achieve their investment objectives. An investment in a Fund is not a deposit with a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Risk is inherent in all investing.

As noted above, although many of the principal risks applicable to an investment in RFAP are also applicable to an investment in RFDI, there are some differences in the risks applicable to each Fund. RFDI has significant holdings in European companies, companies in the United Kingdom and Switzerland specifically, and industrials companies making it more susceptible to risks associated with those countries and that sector than funds without such significant holdings, such as RFAP, and RFAP has significant holdings in Australian companies and greater exposure to Japanese companies, with more than a majority of its assets invested in Japanese companies, making it more susceptible to risks associated with Australia and Japan than funds without such significant holdings there, such as RFDI.

-6-

Because the Funds have substantially similar investment strategies, the Funds’ principal risks are substantially similar. The principal risks below should be considered by shareholders of RFAP in connection with the Reorganization.

General Risks of Investing in the Funds

The following risks are applicable to both RFDI and RFAP.

Asia Risk

The Funds are subject to certain risks specifically associated with investments in the securities of Asian issuers. Many Asian economies have experienced rapid growth and industrialization, and there is no assurance that this growth rate will be maintained. Some Asian economies are highly dependent on trade, and economic conditions in other countries within and outside Asia can impact these economies. Certain of these economies may be adversely affected by trade or policy disputes with its major trade partners. There is also a high concentration of market capitalization and trading volume in a small number of issuers representing a limited number of industries, as well as a high concentration of investors and financial intermediaries. Certain Asian countries have experienced and may in the future experience expropriation and nationalization of assets, confiscatory taxation, currency manipulation, political instability, armed conflict and social instability as a result of religious, ethnic, socio-economic and/or political unrest. In particular, escalated tensions involving North Korea and any outbreak of hostilities involving North Korea could have a severe adverse effect on Asian economies. Governments of certain Asian countries have exercised, and continue to exercise, substantial influence over many aspects of the private sector. In certain cases, the government owns or controls many companies, including the largest in the country. Accordingly, government actions could have a significant effect on the issuers of the Fund’s securities or on economic conditions generally. Recent developments in relations between the U.S. and China have heightened concerns of increased tariffs and restrictions on trade between the two countries. An increase in tariffs or trade restrictions, or even the threat of such developments, could lead to a significant reduction in international trade, which could have a negative impact on the economy of Asian countries and a commensurately negative impact on the Funds.

Authorized Participant Concentration Risk

Only an authorized participant may engage in creation or redemption transactions directly with a Fund. A limited number of institutions act as authorized participants for a Fund. To the extent that these institutions exit the business or are unable to proceed with creation and/or redemption orders and no other authorized participant steps forward to create or redeem, a Fund’s shares may trade at a premium or discount to a Fund’s net asset value and possibly face delisting.

Counterparty Risk

Fund transactions involving a counterparty are subject to the risk that the counterparty will not fulfill its obligation to a Fund. Counterparty risk may arise because of the counterparty’s financial condition (i.e., financial difficulties, bankruptcy, or insolvency), market activities and developments, or other reasons, whether foreseen or not. A counterparty’s inability to fulfill its obligation may result in significant financial loss to a Fund. A Fund may be unable to recover its investment from the counterparty or may obtain a limited recovery, and/or recovery may be delayed.

Currency Risk

Changes in currency exchange rates affect the value of investments denominated in a foreign currency, and therefore the value of such investments in a Fund’s portfolio. A Fund’s net asset value could decline if a currency to which such Fund has exposure depreciates against the U.S. dollar or if there are delays or limits on repatriation of such currency. Currency exchange rates can be very volatile and can change quickly and unpredictably. As a result, the value of an investment in a Fund may change quickly and without warning.

-7-

Cyber Security Risk

Each Fund is susceptible to operational risks through breaches in cyber security. A breach in cyber security refers to both intentional and unintentional events that may cause a Fund to lose proprietary information, suffer data corruption or lose operational capacity. Such events could cause a Fund to incur regulatory penalties, reputational damage, additional compliance costs associated with corrective measures and/or financial loss. Cyber security breaches may involve unauthorized access to a Fund’s digital information systems through “hacking” or malicious software coding but may also result from outside attacks such as denial-of-service attacks through efforts to make network services unavailable to intended users. In addition, cyber security breaches of the securities issuers or a Fund’s third-party service providers, such as its administrator, transfer agent, custodian, or sub-advisor, as applicable, or issuers in which a Fund invests, can also subject a Fund to many of the same risks associated with direct cyber security breaches. Although each Fund has established risk management systems designed to reduce the risks associated with cyber security, there is no guarantee that such efforts will succeed, especially because each Fund does not directly control the cyber security systems of issuers or third-party service providers.

Derivatives Risk

The use of derivative instruments involves risks different from, or possibly greater than, the risks associated with investing directly in securities and other traditional investments. These risks include: (i) the risk that the counterparty to a derivative transaction may not fulfill its contractual obligations; (ii) risk of mispricing or improper valuation; and (iii) the risk that changes in the value of the derivative may not correlate perfectly with the underlying asset. Derivative prices are highly volatile and may fluctuate substantially during a short period of time. Such prices are influenced by numerous factors that affect the markets, including, but not limited to: changing supply and demand relationships; government programs and policies; national and international political and economic events, changes in interest rates, inflation and deflation and changes in supply and demand relationships. Trading derivative instruments involves risks different from, or possibly greater than, the risks associated with investing directly in securities. Derivative contracts ordinarily have leverage inherent in their terms. The low margin deposits normally required in trading derivatives, including futures contracts, permit a high degree of leverage. Accordingly, a relatively small price movement may result in an immediate and substantial loss. The use of leverage may also cause a Fund to liquidate portfolio positions when it would not be advantageous to do so in order to satisfy its obligations or to meet collateral segregation requirements. The use of leveraged derivatives can magnify potential for gain or loss and, therefore, amplify the effects of market volatility on share price.

Dynamic Hedging Risk

Because of the Funds’ utilization of the dynamic currency hedging strategy, the Funds may have lower returns than an equivalent non-currency hedged investment when the component currencies are rising relative to the U.S. dollar. As such, contracts to sell foreign currency will generally be expected to limit any potential gain that might be realized by the Funds if the value of the hedged currency increases. In addition, the use of currency hedging will not necessarily eliminate exposure to all currency fluctuations. Hedging against a decline in the value of a currency does not eliminate fluctuations in the value of a portfolio security traded in that currency or prevent a loss if the value of the security declines. Moreover, it may not be possible for the Funds to hedge against a devaluation that is so generally anticipated that the Funds are not able to contract to sell the currency at a price above the devaluation level it anticipates.

-8-

Equity Securities Risk

The value of a Fund’s shares will fluctuate with changes in the value of the equity securities in which it invests. Equity securities prices fluctuate for several reasons, including changes in investors’ perceptions of the financial condition of an issuer or the general condition of the relevant equity market, such as market volatility, or when political or economic events affecting an issuer occur. Common stock prices may be particularly sensitive to rising interest rates, as the cost of capital rises and borrowing costs increase. Equity securities may decline significantly in price over short or extended periods of time, and such declines may occur in the equity market as a whole, or they may occur in only a particular country, company, industry or sector of the market.

Forward Contracts Risk

A forward contract is an over-the-counter derivative transaction between two parties to buy or sell a specified amount of an underlying reference at a specified price (or rate) on a specified date in the future. Forward contracts are negotiated on an individual basis and are not standardized or traded on exchanges. The market for forward contracts is substantially unregulated and can experience lengthy periods of illiquidity, unusually high trading volume and other negative impacts, such as political intervention, which may result in volatility or disruptions in such markets. A relatively small price movement in a forward contract may result in substantial losses to a Fund, exceeding the amount of the margin paid. Forward contracts can increase a Fund’s risk exposure to underlying references and their attendant risks, such as credit risk, currency risk, market risk, and interest rate risk, while also exposing a Fund to counterparty risk, liquidity risk and valuation risk, among others.

Forward Foreign Currency Exchange Contracts Risk

In connection with their trading in forward foreign currency contracts, the Funds will contract with a foreign or domestic bank, or a foreign or domestic securities dealer, to make or take future delivery of a specified amount of a particular currency. There are no limitations on daily price moves in such forward contracts, and banks and dealers are not required to continue to make markets in such contracts. There have been periods during which certain banks or dealers have refused to quote prices for such forward contracts or have quoted prices with an unusually wide spread between the price at which the bank or dealer is prepared to buy and that at which it is prepared to sell. Governmental imposition of credit controls might limit any such forward contract trading. Forward foreign currency exchange contracts involve certain risks, including the risk of failure of the counterparty to perform its obligations under the contract and the risk that the use of forward contracts may not serve as a complete hedge because of an imperfect correlation between movements in the prices of the contracts and the prices of the currencies hedged. Forward foreign currency exchange contracts may limit any potential gain that might result should the value of the underlying currencies increase. In addition, because forward currency exchange contracts are privately negotiated transactions, there can be no assurance that a Fund will have flexibility to roll-over a forward foreign currency exchange contract upon its expiration if it desires to do so.

-9-

Index Constituent Risk

A Fund may be a constituent of one or more indices. As a result, a Fund may be included in one or more index-tracking exchange-traded funds or mutual funds. Being a component security of such a vehicle could greatly affect the trading activity involving a Fund’s shares, the size of a Fund and the market volatility of a Fund. Inclusion in an index could increase demand for a Fund and removal from an index could result in outsized selling activity in a relatively short period of time. As a result, a Fund’s net asset value could be negatively impacted and such Fund’s market price may be below such Fund’s net asset value during certain periods. In addition, index rebalances may potentially result in increased trading activity in a Fund’s shares.

Japan Risk

The Funds are subject to certain risks specifically associated with investments in the securities of Japanese issuers. The Japanese economy may be subject to considerable degrees of economic, political and social instability, which could have a negative impact on Japanese securities. Japan’s economy is characterized by government intervention and protectionism, reliance on oil imports, an unstable financial services sector and relatively high unemployment. Since 2000, Japan has experienced relatively low economic growth, and it may remain low in the future. Its economy is heavily dependent on international trade and has been adversely affected by trade tariffs and competition from emerging economies. As such, economic growth is heavily dependent on continued growth in international trade, relatively low commodities prices, government support of the financial services sector and other government policies. Any changes or trends in these economic factors could have a significant impact on Japanese markets overall and may negatively affect the Funds’ investments. Japan’s economy and equity market also share a strong correlation with U.S. markets and the Japanese economy may be affected by economic problems in the U.S. Despite a strengthening in the economic relationship between Japan and China, the countries’ political relationship has at times been strained. Should political tension increase, it could adversely affect the economy and destabilize the region as a whole. Additionally, escalated tensions involving North Korea and any outbreak of hostilities involving North Korea could have a severe adverse effect on Japan’s economy. Japan’s geography also subjects it to an increased risk of natural disasters, such as earthquakes, volcanic eruptions, typhoons and tsunamis, all of which could negatively impact the Funds’ investments.

Liquidity Risk

Certain Fund investments may be subject to restrictions on resale, trade over-the-counter market or in limited volume, or lack an active trading market. Accordingly, the Funds may not be able to sell or close out of such investments at favorable times or prices (or at all), or at the prices approximating those at which the Funds currently value them. Illiquid securities may trade at a discount from comparable, more liquid investments and may be subject to wide fluctuations in market value.

-10-

Management Risk

The Funds are subject to management risk because they are actively managed portfolios. In managing the Funds’ investment portfolios, the Sub-Advisor will apply investment techniques and risk analyses that may not have the desired result. There can be no guarantee that the Funds will meet their investment objectives.

The Sub-Advisor specializes in managing asset allocation portfolios, which invest in various investment vehicles, including the Funds and other ETFs, to obtain targeted amounts of exposure to different asset classes. The Funds were developed to serve as, and will serve as, investment vehicles for such asset allocation portfolios. As the manager of the Funds and the portfolios, the Sub-Advisor is likely to encounter conflicts of interest. For example, the Sub-Advisor may need to reduce its asset allocation portfolios’ exposure to an asset class to which the portfolios obtain exposure by investing in the Funds. Under such circumstances, the Sub-Advisor would liquidate some or all of the portfolios’ investments in the Funds, which could adversely affect the Funds.

Market Maker Risk

A Fund faces numerous market trading risks, including the potential lack of an active market for Fund shares due to a limited number of market markers. Decisions by market makers or authorized participants to reduce their role or step away from these activities in times of market stress could inhibit the effectiveness of the arbitrage process in maintaining the relationship between the underlying values of a Fund’s portfolio securities and a Fund’s market price. A Fund may rely on a small number of third-party market makers to provide a market for the purchase and sale of shares. Any trading halt or other problem relating to the trading activity of these market makers could result in a dramatic change in the spread between a Fund’s net asset value and the price at which a Fund’s shares are trading on the Exchange, which could result in a decrease in value of a Fund’s shares. This reduced effectiveness could result in a Fund’s shares trading at a discount to net asset value and also in greater than normal intraday bid-ask spreads for a Fund’s shares.

Market Risk

Market risk is the risk that a particular security, or shares of a Fund in general, may fall in value. Securities are subject to market fluctuations caused by such factors as economic, political, regulatory or market developments, changes in interest rates and perceived trends in securities prices. Shares of a Fund could decline in value or underperform other investments. In addition, local, regional or global events such as war, acts of terrorism, spread of infectious diseases or other public health issues, recessions, or other events could have a significant negative impact on a Fund and its investments. For example, the coronavirus disease 2019 (COVID-19) global pandemic and the aggressive responses taken by many governments, including closing borders, restricting international and domestic travel, and the imposition of prolonged quarantines or similar restrictions, has had negative impacts, and in many cases severe impacts, on markets worldwide. Such events may affect certain geographic regions, countries, sectors and industries more significantly than others. Such events could adversely affect the prices and liquidity of a Fund’s portfolio securities or other instruments and could result in disruptions in the trading markets. Any of such circumstances could have a materially negative impact on the value of a Fund’s shares and result in increased market volatility. During any such events, a Fund’s shares may trade at increased premiums or discounts to their net asset value.

Model Risk

The Funds’ portfolio managers use quantitative models to help construct the Funds’ portfolios. The utilization of quantitative models entails the risk that a model may be limited or incorrect, that the data on which a model relies may be incorrect or incomplete and that the portfolio managers may not be successful in selecting companies for investment or determining the weighting of particular stocks in the Funds’ portfolios. To the extent that the model is based upon incorrect or incomplete data, the Funds could be induced to buy certain investments at prices that are too high, to sell certain other investments at prices that are too low or to miss favorable opportunities altogether. Any of these factors could cause the Funds to underperform funds with similar strategies that do not rely on quantitative analysis for portfolio construction.

-11-

Non-U.S. Securities Risk

Non-U.S. securities are subject to higher volatility than securities of domestic issuers due to possible adverse political, social or economic developments, restrictions on foreign investment or exchange of securities, capital controls, lack of liquidity, currency exchange rates, excessive taxation, government seizure of assets, the imposition of sanctions by foreign governments, different legal or accounting standards, and less government supervision and regulation of securities exchanges in foreign countries.

Operational Risk

The Funds are subject to risks arising from various operational factors, including, but not limited to, human error, processing and communication errors, errors of the Funds’ service providers, counterparties or other third-parties, failed or inadequate processes and technology or systems failures. Although the Funds and the Advisor seek to reduce these operational risks through controls and procedures, there is no way to completely protect against such risks.

OTC Derivatives Risk

The Funds may utilize derivatives that are traded over-the-counter, or “OTC.” In general, OTC derivatives are subject to the same risks as derivatives generally, as described above. However, because OTC derivatives do not trade on an exchange, the parties to an OTC derivative face heightened levels of counterparty risk, liquidity risk and valuation risk. To the extent that a Fund utilizes OTC derivatives, such Fund’s counterparty risk will be higher if it only trades with a single or small number of counterparties. The secondary market for OTC derivatives may not be as deep as for other instruments and such instruments may experience periods of illiquidity. In addition, some OTC derivatives may be complex and difficult to value.

Portfolio Turnover Risk

High portfolio turnover may result in a Fund paying higher levels of transaction costs and may generate greater tax liabilities for shareholders. Portfolio turnover risk may cause a Fund’s performance to be less than expected.

Premium/Discount Risk

The market price of a Fund’s shares will generally fluctuate in accordance with changes in a Fund’s net asset value as well as the relative supply of and demand for shares on the exchange on which it trades. Each Fund’s investment advisor cannot predict whether shares will trade below, at or above their net asset value because the shares trade on an exchange at market prices and not at net asset value. Price differences may be due, in large part, to the fact that supply and demand forces at work in the secondary trading market for shares will be closely related, but not identical, to the same forces influencing the prices of the holdings of the Funds trading individually or in the aggregate at any point in time. However, given that shares can only be issued and redeemed in Creation Units, and only to and from broker-dealers and large institutional investors that have entered into participation agreements (unlike shares of closed-end funds, which frequently trade at appreciable discounts from, and sometimes at premiums to, their net asset value), each Fund’s investment advisor believes that large discounts or premiums to the net asset value of shares should not be sustained. During stressed market conditions, the market for a Fund’s shares may become less liquid in response to deteriorating liquidity in the market for a Fund’s underlying portfolio holdings, which could in turn lead to differences between the market price of a Fund’s shares and their net asset value.

-12-

Significant Exposure Risk

To the extent that a Fund invests a large percentage of its assets in a single asset class or the securities of issuers within the same country, state, region, industry or sector, an adverse economic, business or political development may affect the value of a Fund’s investments more than if a Fund were more broadly diversified. A significant exposure makes a Fund more susceptible to any single occurrence and may subject a Fund to greater market risk than a fund that is more broadly diversified.

Smaller Companies Risk

Small and/or mid capitalization companies may be more vulnerable to adverse general market or economic developments, and their securities may be less liquid and may experience greater price volatility than larger, more established companies as a result of several factors, including limited trading volumes, fewer products or financial resources, management inexperience and less publicly available information. Accordingly, such companies are generally subject to greater market risk than larger, more established companies.

Trading Issues Risk

Trading in Fund shares on an exchange may be halted due to market conditions or for reasons that, in the view of the exchange, make trading in shares inadvisable. In addition, trading in Fund shares on an exchange is subject to trading halts caused by extraordinary market volatility pursuant to the exchange’s “circuit breaker” rules. There can be no assurance that the requirements of an exchange necessary to maintain the listing of a Fund will continue to be met or will remain unchanged. A Fund may have difficulty maintaining its listing on the Exchange in the event a Fund’s assets are small, the Fund does not have enough shareholders, or if the Fund is unable to proceed with creation and/or redemption orders.

Valuation Risk

The Funds may hold securities or other assets that may be valued on the basis of factors other than market quotations. This may occur because the asset or security does not trade on a centralized exchange, or in times of market turmoil or reduced liquidity. There are multiple methods that can be used to value a portfolio holding when market quotations are not readily available. The value established for any portfolio holding at a point in time might differ from what would be produced using a different methodology or if it had been priced using market quotations. Portfolio holdings that are valued using techniques other than market quotations, including “fair valued” assets or securities, may be subject to greater fluctuation in their valuations from one day to the next than if market quotations were used. In addition, there is no assurance that a Fund could sell or close out a portfolio position for the value established for it at any time, and it is possible that a Fund would incur a loss because a portfolio position is sold or closed out at a discount to the valuation established by a Fund at that time. The Funds’ ability to value investments may be impacted by technological issues or errors by pricing services or other third-party service providers.

-13-

Principal Risks Exclusive to RFDI

The following specific factors have been identified as the principal risks of investing in RFDI that are not principal risks of investing in RFAP. These risks should be considered by shareholders of RFAP in connection with the Reorganization. An investment in RFDI may not be appropriate for all investors. RFDI is not intended to be a complete investment program. Investors should consider their long-term investment goals and financial needs when making an investment decision with respect to RFDI. Shares of RFDI at any point in time may be worth less than an investor’s original investment.

Europe Risk

RFDI is subject to certain risks specifically associated with investments in the securities of European issuers. Political or economic disruptions in European countries, even in countries in which the Fund is not invested, may adversely affect security values and thus the Fund’s holdings. A significant number of countries in Europe are member states in the European Union (the ”EU”), and the member states no longer control their own monetary policies by directing independent interest rates for their currencies. In these member states, the authority to direct monetary policies, including money supply and official interest rates for the Euro, is exercised by the European Central Bank. In a 2016 referendum, the United Kingdom elected to withdraw from the EU (“Brexit”). After years of negotiations between the United Kingdom and the EU, a withdrawal agreement was reached whereby the United Kingdom formally left the EU. As the second largest economy among EU members, the implications of the United Kingdom’s withdrawal are difficult to gauge and cannot be fully known. Its departure may negatively impact the EU and Europe as a whole by causing volatility within the EU, triggering prolonged economic downturns in certain European countries or sparking additional member states to contemplate departing the EU (thereby perpetuating political instability in the region).

Industrials Companies Risk

Industrials companies convert unfinished goods into finished durables used to manufacture other goods or provide services. Examples of industrials companies include companies involved in the production of electrical equipment and components, industrial products, manufactured housing and telecommunications equipment, as well as defense and aerospace companies. General risks of industrials companies include the general state of the economy, exchange rates, commodity prices, intense competition, consolidation, domestic and international politics, government regulation, import controls, excess capacity, consumer demand and spending trends. In addition, industrials companies may also be significantly affected by overall capital spending levels, economic cycles, rapid technological changes, delays in modernization, labor relations, environmental liabilities, governmental and product liability and e-commerce initiatives.

-14-

United Kingdom Risk

RFDI is subject to certain risks specifically associated with investments in the securities of United Kingdom issuers. Investments in issuers located in the United Kingdom may subject RFDI to regulatory, political, currency, security and economic risk specific to the United Kingdom. The United Kingdom has one of the largest economies in Europe and is heavily dependent on trade with the EU, and to a lesser extent the United States and China. As a result, the economy of the United Kingdom may be impacted by changes to the economic health of EU member counties, the United States and China. In 2016, the United Kingdom voted via referendum to leave the EU. After years of negotiations between the United Kingdom and the EU, a withdrawal agreement was reached whereby the United Kingdom formally left the EU. The precise impact on the United Kingdom’s economy as a result of its departure from the EU depends to a large degree on its ability to conclude favorable trade deals with the EU and other countries, including the United States, China, India and Japan. While new trade deals may boost economic growth, such growth may not be able to offset the increased costs of trade with the EU resulting from the United Kingdom’s loss of its membership in the EU single market. Certain sectors within the United Kingdom’s economy may be particularly affected by Brexit, including the automotive, chemicals, financial services and professional services.

Principal Risks Exclusive to RFAP

The investment objectives and strategies of RFAP and RFDI are similar, but they also have some important distinctions, as discussed in this Information Statement/Prospectus. As a result of such differences, RFAP is subject to some additional risks that may not be associated with RFDI.

Australia Risk

Investing in securities of Australian companies may involve additional risks. The Australian economy is heavily dependent on the Asian, European and U.S. markets. Reduced spending by any of these economies on Australian products may adversely affect the Australian market. Additionally, Australia is located in a geographic region that has historically been prone to natural disasters. The occurrence of a natural disaster in the region could negatively impact the Australian economy and affect the value of the securities held by RFAP.

Principal Risks Related to the Reorganization

The following are principal risks related to the Reorganization and are applicable to both RFDI and RFAP:

Anticipated Benefits Risk