UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

For the fiscal year ended

or

For the transition period from ___________ to ___________

Commission file number

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification No.) |

(Address of principal executive offices) (Zip Code)

(Registrant’s telephone number, including area code)

Securities Registered Pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

Securities Registered Pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a

well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not

required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant

(1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months

(or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements

for the past 90 days. Yes ☐

Indicate by check mark whether the registrant

has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulations S-T (§232.405

of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☒

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☒ | Smaller reporting company | ||

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on

and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section

404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting fi rm that prepared or issued its audit report.

Indicate by check mark whether the registrant

is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No

The

aggregate market value of voting common stock held by non-affiliates of the registrant as of December 31, 2021, the last business day

of the registrant’s second fiscal quarter, was approximately $

The number of shares of common stock outstanding as of March 3,

2023 was

DOCUMENTS INCORPORATED BY REFERENCE:

None.

SINGULARITY FUTURE TECHNOLOGY LTD.

FORM 10-K

INDEX

i

INTRODUCTION

Unless the context otherwise requires, in this annual report on Form 10-K (this “Report”):

| ● | “We,” “us,” “our,” and “our Company” refer to Singularity Future Technology Ltd., a Virginia company incorporated in September 2007, and all of its direct and indirect consolidated subsidiaries; |

| ● | “Singularity” refers to Singularity Future Technology, Ltd; |

| ● | “Sino-China” refers to Sino-Global Shipping Agency Ltd., a Chinese legal entity; |

| ● | “PRC” refers to the People’s Republic of China, excluding Taiwan for the purpose of this Report; |

| ● | “US” or “U.S.” refers to the United States of America; |

| ● | “RMB” or “Renminbi” refers to the legal currency of China, and “$” or “U.S. dollars” refers to the legal currency of the United States. |

Names of certain PRC companies provided in this Report are translated or transliterated from their original PRC legal names. Discrepancies, if any, in any table between the amounts identified as total amounts and the sum of the amounts listed therein are due to rounding.

ii

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Report contains certain statements that constitute “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Such forward-looking statements, including but not limited to statements regarding our projected growth, trends and strategies, future operating and financial results, financial expectations and current business indicators are based upon current information and expectations and are subject to change based on factors beyond our control. Forward-looking statements typically are identified by the use of terms such as “look,” “may,” “will,” “should,” “might,” “believe,” “plan,” “expect,” “anticipate,” “estimate” and similar words, although some forward-looking statements are expressed differently. The accuracy of such statements may be impacted by a number of business risks and uncertainties we face that could cause our actual results to differ materially from those projected or anticipated, including but not limited to the following:

| ● | our ability to timely and properly deliver our services; |

| ● |

our dependence on a limited number of major customers and suppliers;

| |

| ● | our ability to resume our business of sales of crypto mining machines and to expand our operations after the conclusion of the investigation; |

| ● | current and future political and economic factors in the United States and China and the relationship between the two countries; |

| ● | our ability to explore and enter into new business opportunities and the acceptance in the marketplace of our new lines of business; |

| ● | unanticipated changes in general market conditions or other factors which may result in cancellations or reductions in the need for our services; |

| ● | the demand for warehouse, shipping and logistics services; |

| ● | the foreign currency exchange rate fluctuations; |

| ● | possible disruptions in commercial activities caused by events such as natural disasters, health epidemics, terrorist activity and armed conflict; |

| ● | our ability to identify and successfully execute cost control initiatives; |

| ● | the impact of quotas, tariffs or safeguards on our customer products that we service; |

| ● | our ability to attract, retain and motivate qualified management team members and skilled personnel; |

| ● | relevant governmental policies and regulations relating to our businesses and industries; | |

| ● | developments in, or changes to, laws, regulations, governmental policies, incentives and taxation affecting our operations; | |

| ● | our reputation and ability to do business may be impacted by the improper conduct of our employees, agents or business partners; and | |

| ● | the outcome of litigation or investigation in which we are involved is unpredictable, and an adverse decision in any such matter could have a material adverse effect on our financial condition, results of operations, cash flows and equity. |

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. The Company undertakes no obligation to update the forward-looking statements. Nonetheless, the Company reserves the right to make such updates from time to time by press release, periodic report or other method of public disclosure without the need for specific reference to this Report. No such update shall be deemed to indicate that other statements not addressed by such update remain correct or create an obligation to provide any other updates.

iii

PART I

Item 1. Business.

Overview

We are a global logistics integrated solution provider that was founded in the United States in 2001. We primarily focus on providing freight logistics services, which mainly include shipping, warehouse, resources, equipment, and other logistical support to steel companies and e-commerce businesses.

We previously focused on providing customized freight logistic services until 2017 when we began exploring new opportunities to expand our business and generate more revenue. These opportunities ranged from complementary businesses to other new service and product initiatives. In the fiscal year 2022, while we continued to provide our traditional freight business, we expanded our services to include warehousing services provided by our U.S. subsidiary Brilliant Warehouse Service Inc since August 2021. On January 3, 2022, we changed our corporate name to Singularity Future Technology Ltd. to align with our entry into the digital assets business through our U.S. subsidiaries. During 2022, we were engaged in purchases and sales of cryptocurrency mining machines through our U.S. subsidiaries and ceased this line of business in December 2022 following our settlement with SOSNY, as more fully described below under the heading “– Recent Developments – Settlement with SOS Information Technology New York, Inc.”

We are currently engaged in providing freight logistics services including warehouse services, which are operated by our subsidiaries Trans Pacific Shipping Limited and Ningbo Saimeinuo Supply Chain Management Ltd in China and Gorgeous Trading Ltd and Brilliant Warehouse Service Inc in the United States. Our range of services include transportation, warehouse, collection, first-mile delivery, drop shipping, customs clearance, and overseas transit delivery.

Since the publication of the Hindenburg Report (as defined below), we have devoted substantial resources and efforts in the cooperation with the investigation of the Special Committee and U.S. governmental authorities, as well as the settlements with investors and vendor and the defense of lawsuits, which are fully described below. As a result, our business operations have been materially and adversely impacted, including suspension of our business developments in North America. We are currently exploring new business opportunities while continuing to provide freight logistics services, which include shipping and warehouse services.

Recent Developments

Special Committee Investigation

On May 5, 2022, an entity named Hindenburg Research issued a report (the “Hindenburg Report”) regarding the Company alleging, among other things, that the Company’s then Chief Executive Officer, Yang Jie, was a fugitive on the run from Chinese authorities for running an alleged $300 million Ponzi scheme that lured in over 20,000 victims. The report also raised questions regarding the Company’s joint venture to produce crypto mining equipment announced in October 2021, as well as a $200 million order purportedly received by the joint venture in January 2022. Further, the report was critical of the Company’s April 2022 announcement of a $250 million partnership with an entity named Golden Mainland Inc. On May 6, 2022, the Board of Directors of the Company (the “Board”) formed a special committee of its Board of Directors (the “Special Committee”) to investigate claims of alleged fraud, misrepresentation, and inadequate disclosure related to the Company and certain of its management personnel raised in the Hindenburg Report and other related matters. The Special Committee then retained Blank Rome LLP to serve as independent legal counsel and advise the Committee on the investigation. The Special Committee completed the fact-finding portion of its investigation prior to December 31, 2022. The Special Committee’s preliminary findings corroborate certain of the allegations made in the Hindenburg Report and the investigation has resulted in the terminations and resignations of certain executive officers and directors of the Company, including but not limited to, the following:

On June 16, 2022, Ms. Tuo Pan, Chief Financial Officer of the Company, without proper authorization by the Board, directed that funds be wired to satisfy an invoice for legal services that were rendered or to be rendered to Ms. Pan personally. Ms. Pan was suspended by the Board for cause and without pay effective June 20, 2022. On August 31, 2022, Ms. Tuo Pan was terminated for cause as an employee and Chief Financial Officer of the Company and from any other position at any subsidiary of the Company to which she has been appointed in accordance with the terms of her Employment Agreement dated November 9, 2021 and will not receive any salary or benefits from the Company except those earned through August 31, 2022.

1

On August 9, 2022, Mr. Yang Jie tendered his resignation from his positions as the Chief Executive Officer and director of the Company to the Board, following the Board’s decision on August 8, 2022, which adopted the Special Committee’s recommendation that Mr. Jie be suspended immediately as the Company’s Chief Executive Officer, pending the Special Committee’s further investigation into allegations raised in the report of Hindenburg Report and other related matters.

On August 16, 2022, the Staff and attorneys from Blank Rome LLP, counsel for the Special Committee, held a conference call, during which counsel represented that Yang Jie had provided documentation to the SEC that indicated that the charges against him in China had been dropped, but the Special Committee’s investigation raised questions regarding the authenticity of such documents. The Special Committee has concluded that Mr. Jie was in fact issued a “Red Notice” in China. In terms of remediating this issue, after being suspended by the Special Committee on August 8, 2022, Mr. Yang Jie had resigned from his positions as Chief Executive Officer and as a director of the Company on August 9, 2022.

On January 9, 2023, the Company entered into an Executive Separation Agreement and General Release (the “Separation Agreement”), with Lei Cao, an employee of the Company and a member of the Board, setting forth the terms and conditions related to (1) the termination of Mr. Cao’s employment with the Company and the termination of the employment agreement dated as of November 1, 2021 as well as cancellation and/or termination of certain other agreements relating to Mr. Cao’s employment with the Company; and (2) Mr. Cao’s resignation from the Board, effective as of January 9, 2023.

Pursuant to the Separation Agreement, Mr. Cao submitted a letter of resignation from the Board on January 9, 2023. In addition, he agreed to forfeit and return to the Company the 600,000 shares of common stock of the Company granted to him on August 13, 2021 under the terms of the 2014 Equity Incentive Plan of the Company (the “2021 Shares”). Mr. Cao also agreed to cooperate with the Company regarding certain investigations and proceedings set forth in the Separation Agreement, and/or any other matters arising out of or related to Mr. Cao’s relationship with or service to the Company. In consideration, the Company agreed to provide the following benefits to which Mr. Cao was not otherwise entitled: (1) payment of reasonable attorneys’ fees and costs incurred by Mr. Cao up through January 9, 2023 associated with Mr. Cao’s personal legal representation in matters relating to Mr. Cao’s tenure with the Company, the investigations and proceedings set forth in the Separation Agreement, and the negotiation and drafting of the Separation Agreement; (2) the release of claims in Mr. Cao’s favor contained in the Separation Agreement; and (3) payment of Mr. Cao’s reasonable and necessary legal fees to the extent incurred by Mr. Cao as a result of his cooperation as required by the Company under the terms of the Separation Agreement. Additionally, the Separation Agreement contains mutual general releases and waiver of claims from Mr. Cao and the Company.

On February 23, 2023, the Board approved the dissolution of the Special Committee upon conclusion of the committee’s investigation. On the same day, John Levy resigned as a director and member of the Audit Committee, Compensation Committee and Nominating Committee of the Board, effective immediately.

Nasdaq Listing Deficiencies

On May 24, 2022, the Company received a delinquency notice from Nasdaq indicating that the Company was not in compliance with Nasdaq Listing Rule 5250(c)(1) due to its delay in filing its Quarterly Report on Form 10-Q for the quarter ended March 31, 2022. The Company was provided 60 days to submit a plan to regain compliance. On July 25, 2022 and September 14, 2022, the Company submitted its plan to regain compliance and supplementary information related to the plan, respectively (collectively, the “Compliance Plan”). Based on the review of the Compliance Plan as well as telephone conversations with outside counsel to the Company and counsel to the Company’s Special Committee, the Staff has determined that the Company did not provide a definitive plan evidencing its ability to file the Quarterly Report on Form 10-Q for the quarter ended March 31, 2022 and the Annual Report on Form 10-K for the fiscal year ended June 30, 2022 (collectively, the “Reports”) within the 180 calendar day period available to the Staff under the Nasdaq Listing Rules.

2

Specifically, the delisting determination referenced several aspects of the Compliance Plan that raise substantial doubts about the Company’s ability to regain compliance: (i) the unreasonably short timeframe for the Company to file the Reports based on the anticipated timeframe the Special Committee needs to substantially complete its investigation; (ii) the Company’s ability to engage a new independent registered public accounting firm; and (iii) the departure of both the Company’s Chief Executive Officer and Chief Financial Officer.

On November 16, 2022, the Company received an additional staff determination notice from Nasdaq, advising that it had not received the Company’s Form 10-Q for the quarterly period ended September 30, 2022, which served as an additional basis for delisting the Company’s securities and that the Nasdaq Hearings Panel (the “Panel”) will consider the additional deficiency in rendering a determination regarding the Company’s continued listing on The Nasdaq Capital Market. The Company has submitted to the Panel a plan to regain compliance with the continued listing requirements, including the filing of the Form 10-Q for the quarterly period ended September 30, 2022.

On January 5, 2023, the Company received a deficiency notice from Nasdaq informing the Company that its common stock, no par value, fails to comply with the $1 minimum bid price required for continued listing on The Nasdaq Capital Market under Nasdaq Listing Rule 5550(a)(2) based upon the closing bid price of the common stock for the 30 consecutive business days prior to the date of the notice from Nasdaq. The Company has been provided an initial compliance period of 180 calendar days, or until July 5, 2023, to regain compliance with the minimum bid price requirement.

On February 21, 2023, the Company received an additional staff determination notice from Nasdaq, advising that it had not received the Company’s Form 10-Q for the quarterly period ended December 31, 2022, which served as an additional basis for delisting the Company’s securities. The notice stated that the Nasdaq Hearings Panel will consider the additional deficiency in rendering a determination regarding the Company’s continued listing on Nasdaq. The Company has submitted to the Panel a plan to regain compliance with the continued listing requirements and has been granted a grace period to file all the delinquent reports, including the filing of the Form 10-Q for the quarterly period ended December 31, 2022, on or before February 28, 2023.

Settlement with SOS Information Technology New York, Inc.

SOS Information Technology New York, Inc. (“SOSNY”), a company incorporated under the laws of state of New York and a wholly owned subsidiary of SOS Ltd., filed a lawsuit in the New York State Supreme Court on December 9, 2022 against Thor Miner, Inc., which is the Company’s joint venture (“Thor Miner,” together with the Company, referred to as the “Corporate Defendants”), Lei Cao, Yang Jie, John F. Levy, Tieliang Liu, Tuo Pan, Shi Qiu, Jing Shan, and Heng Wang (jointly referred to as the “Individual Defendants”) (collectively, the Individual Defendants and the Corporate Defendants are the “Defendants”). SOSNY and Thor Miner entered into a Purchase and Sale Agreement dated January 10, 2022 (the “PSA”) for the purchase of $200,000,000 in crypto mining rigs, which SOSNY claims was breached by the Defendants.

SOSNY and Defendants entered into a certain settlement agreement and general mutual release with an Effective Date of December 28, 2022 (the “Settlement Agreement”). Pursuant to the Settlement Agreement, Thor Miner agreed to pay a sum of $13,000,000 (the “Settlement Payment”) to SOSNY in exchange for SOSNY dismissing the lawsuit with prejudice as to the settling Defendants and without prejudice as to all others. The full Settlement Payment was received by SOSNY on December 28, 2022. SOSNY dismissed the lawsuit with prejudice against Singularity (and other Defendants) on December 28, 2022.

The Company and Thor Miner further covenanted and agreed that if they receive additional funds from HighSharp (Shenzhen Gaorui) Electronic Technology Co., Ltd. (“HighSharp”) related to the PSA, they will promptly transfer such funds to SOSNY in an amount not to exceed $40,560,569 (which is the total amount paid by SOSNY pursuant to the PSA less the price of the machines actually received by SOSNY pursuant to the PSA). The Settlement Payment and any payments subsequently received by SOSNY from HighSharp shall be deducted from the total amount of $40,560,569 previously paid by, and now due and owing to SOSNY. In further consideration of the Settlement Agreement, Thor Miner agreed to execute and provide to SOSNY, within seven (7) business days after SOSNY’s receipt of the Settlement Payment, an assignment of all claims it may have against HighSharp or otherwise to the proceeds of the PSA.

Litigations

Lawsuits in connection with the Securities Purchase Agreement

On September 23, 2022, Hexin Global Limited and Viner Total Investments Fund filed a lawsuit against the Company and other defendants in the United States District Court for the Southern District of New York (the “Hexin lawsuit”). On December 5, 2022, St. Hudson Group LLC, Imperii Strategies LLC, Isyled Technology Limited, and Hsqynm Family Inc. filed a lawsuit against the Company and other defendants in the United States District Court for the Southern District of New York (the “St. Hudson lawsuit,” and together with the Hexin lawsuit, the “Investor Actions”). The plaintiffs in the Investor Actions are investors that entered into a securities purchase agreement with the Company in December 2021 as more fully described below. Each of these plaintiffs asserts causes of action for, among other things, violations of federal securities laws, breach of fiduciary duty, fraudulent inducement, breach of contract, conversion, and unjust enrichment, and seeks monetary damages and specific performance to remove legends from certain securities sold pursuant to the Securities Purchase Agreement. The Hexin lawsuit claims monetary damages of “at least $6 million,” plus interest, costs, fees, and attorneys’ fees. The St. Hudson lawsuit claims monetary damages of “at least $4.4 million,” plus interest, costs, fees, and attorneys’ fees.

3

Lawsuit in connection with the Financial Advisory Agreement

On October 6, 2022, Jinhe Capital Limited (“Jinhe”) filed a lawsuit against the Company in the United States District Court for the Southern District of New York, asserting causes of actions for, among other things, breach of contract, breach of the covenant of good faith and fair dealing, conversion, quantum meruit, and unjust enrichment, in connection with a financial advisory agreement entered into by and between Jinhe and the Company on November 10, 2021. Jinhe claims monetary damages of “at least $575,000” and “potentially exceeding $1.8 million,” plus interest, costs, and attorneys’ fees.

On January 10, 2023, St. Hudson lawsuit was consolidated with this lawsuit and Hexin lawsuit; on February 24, 2023, all three consolidated actions were dismissed without prejudice by the court, in furtherance of the parties having reached an agreement in principle to settle their disputes.

Putative Class Action

On December 9, 2022, Piero Crivellaro, purportedly on behalf of the persons or entities who purchased or acquired publicly traded securities of the Company between February 2021 and November 2022, filed a putative class action against the Company and other defendants in the United States District Court for the Eastern District of New York, alleging violations of federal securities laws related to alleged false or misleading disclosures made by the Company in its public filings. The plaintiff seeks unspecified damages, plus interest, costs, fees, and attorneys’ fees. On February 7, 2023, two additional plaintiffs moved to be appointed as the lead class plaintiff in this action; those motions remain under the Court’s consideration. As this action is still in the early stage, the Company cannot predict the outcome.

In addition to the above litigations, the Company is also subject to additional contractual litigations as to which it is unable to estimate the outcome.

Government Investigations

Following a publication of the Hindenburg Report, the Company received subpoenas from the United States Attorney’s Office for the Southern District of New York and the United States Securities and Exchange Commission. The Company is cooperating with the government regarding these matters. At this early stage, the Company is not able to estimate the outcome or duration of the government investigations.

Recent Financings

December 2021 Securities Purchase Agreement

On December 14, 2021, the Company entered into a securities purchase agreement (the “December 2021 SPA”) with certain non-U.S. investors and accredited investors (the “Investors”) pursuant to which the Company sold to the Investors an aggregate of 3,228,807 shares of common stock and warrants to purchase 4,843,210 shares of common stock. The purchase price for each share of common stock and one and a half warrants is $3.26, and the exercise price per warrant is $4.00. The warrants will be exercisable at any time during the period beginning on or after June 14, 2022 and ending on or prior to 5:00 p.m. (New York City time) on December 13, 2026; provided, however, that the total number of the Company’s issued and outstanding shares of common stock, multiplied by the Nasdaq official closing bid price of the common stock shall equal or exceed $150,000,000 for a three consecutive month period prior to an exercise. This transaction is the subject of the Investor Actions described above.

On December 14, 2021, the transaction contemplated by the December 2021 SPA closed because all the closing conditions of the agreement were satisfied. The issuance and sale of the shares and warrants issued by the December 2021 SPA are exempt from the registration requirements of the Securities Act pursuant to Regulation S promulgated thereunder.

December 2021 Convertible Notes

On December 19, 2021, the Company issued two senior convertible notes (the “December 2021 Convertible Notes”) to two non-U.S. investors for an aggregate purchase price of $10,000,000. The December 2021 Convertible Notes bear interest at 5% annually and may be converted into shares of the Company’s common stock per share at a conversion price of $3.76 per share, the closing price of the common stock on December 17, 2021. The December 2021 Convertible Notes are unsecured senior obligations of the Company, and the maturity date of the convertible notes is December 18, 2023. The Company may repay any portion of the outstanding principal, accrued and unpaid interest, without penalty for early repayment. The Company may make any repayment of principal and interest in (a) cash, (b) common stock at the conversion price or (c) a combination of cash or common stock at the conversion price. The investors may convert any conversion amount into common stock on any date beginning on June 19, 2022.

4

At the investors’ request, the Company prepaid $5,000,000 in aggregate of the principal amount, without interest, of the December 2021 Convertible Notes on March 8, 2022. On March 8, 2022, the Company issued two Amended and Restated Senior Convertible Notes (the “March 2022 Amended and Restated Convertible Notes”) to the investors to change the principal amount of the December 2021 Convertible Notes to $5,000,000. The terms of the March 2022 Amended and Restated Convertible Notes are the same as that of the December 2021 Convertible Notes, except for the reduced principal amount and the waiver of interest for the $5,000,000 payment made on March 8, 2022.

January 2022 Warrant Purchase Agreement

On January 6, 2022, the Company entered into warrant purchase agreements with certain warrant holders (the “Sellers”) pursuant to which the Company repurchased an aggregate of 3,870,800 warrants (the “January 2022 Warrants”) from the Sellers. These warrants were sold to these Sellers in three previous transactions that closed on February 11, 2021, February 10, 2021, and March 14, 2018. The purchase price for each warrant was $2.00. Following announcement of the warrant purchase agreement, on January 6, 2022, the Company repurchase an additional 103,200 warrants from other Sellers on the same terms as the previously announced warrant purchase agreements. The aggregate number of warrants repurchased under the warrant purchase agreements was 3,974,000.

On January 7, 2022, the Company wired the purchase price to each Seller. Each Seller agreed to deliver the January 2022 Warrants to the Company for cancellation as soon as practicable following the closing date, but in no event later than January 13, 2022 . The January 2022 Warrants were deemed cancelled upon the receipt by the Sellers of the purchase price.

Corporate History and Our Business Segments

From inception in 2001 to our fiscal year ended June 30, 2013, our sole business was providing shipping agency services. In general, we provided two types of shipping agency services: loading/discharging services and protective agency services, in which we acted as a general agent to provide value added solutions to our customers. For loading/discharging agency services, we received the total payment from our customers in U.S. dollars and paid the port charges on behalf of our customers in RMB. For protective agency services, we charged a fixed amount as agent fee while customers were responsible for the payment of port costs and expenses.

In January 2016, we expanded our business to include freight logistics services to provide import security filing services with the U.S. Customs and Department of Homeland Security, on behalf of importers who ship goods into the U.S. and also provided inland transportation services to these importers in the U.S.

In the fiscal year ended June 30, 2017, we also expanded into container trucking services as new business sectors to provide related transportation logistics services to customers in the U.S. and in China.

As an effort to further diversify our business, in the second quarter of the fiscal year ended June 30, 2018, we developed our bulk cargo container services segment. Bulk cargo container shipment refers to using containers to ship commodities that are traditionally shipped by freight cargo. Freight cargo rates are usually lower than container freight rates; however, the transit time is much longer and has high minimum quantity requirements. We temporarily suspended this service in the fiscal year ended June 30, 2019 due to market environment factors in 2019, and we have discontinued this service in light of the worldwide impact of the coronavirus pandemic.

In the fiscal year ended June 30, 2018, we established a wholly owned subsidiary, Ningbo Saimeinuo Supply Chain Management Ltd., which is 100% owned by Sino-Global Shipping New York Inc. (“SG Shipping NY”), a New York corporation and a wholly owned subsidiary of the Company, and primarily engages in transportation management and freight logistics services, including overseas shipping.

Since the fiscal year ended June 30, 2019, trade dynamics have made it more expensive for shipping carrier clients to cost-effectively move cargo into U.S. ports, and as a result, we realized lower shipping volumes, which has caused us to shift our focus back to the shipping agency business.

On January 10, 2020, the Company entered into a cooperation agreement with Mr. Shanming Liang, a stockholder of the Company and set up a joint venture with Mr. Liang in New York named LSM Trading Ltd., in which the Company holds a 40% equity interest. For the year ended June 30, 2022, the Company invested $210,000. The joint venture has not commenced any business operations as of the date of this Report.

5

On July 7, 2020, the Company effected a l-for-5 reverse stock split of its issued and outstanding shares of common stock. The split did not change the number of authorized shares of common stock or preferred stock, or the par value of common stock or preferred stock. As a result, all the issued and outstanding common stock share amounts included in this filing have been retroactively reduced by a factor of five, and all common stock per share amounts have been increased by a factor of five.

On December 14, 2020, the Company incorporated a new entity named Blumargo IT Solution Ltd. (“Blumargo”) in the U.S. SG Shipping NY held an 80% ownership interest in Blumargo, which was established in partnership with Tianjin Anboweiye Technology Co., to build up hi-tech and information-based logistics services to meet the demand of its customers. On June 30, 2021, SG Shipping NY acquired the additional 20% from Tianjin Anboweiye Technology Co. and increased its ownership to 100%.

From March to June 2021, the Company engaged in cryptocurrency mining in China. On March 2, 2021, the Company entered into a purchase agreement with Hebei Yanghuai Technology Co., Ltd. (“Yanghuai”) for the purchase of 2,783 digital currency mining machines for a total purchase price of approximately $4.6 million. After the purchase, Yanghuai would manage and operate the servers at its site with no further charge from March 10, 2021 to March 9, 2022, after which time the Company may engage Yanghuai to continue providing service for a fee. The first cash payment of approximately $0.9 million was paid within 15 days after the date of signing the Agreement.

Over the last two months of the Company’s 2021 fiscal year, national and local governments in China started to restrict and ban cryptocurrency mining operations, causing owners of mining machines to cease mining operations. Based on the amended agreement signed by the Company and Yanghuai on September 17, 2021, the Company is not liable to perform under the remainder of the contract and has title to half of the products. The Company recorded impairment for the mining equipment in the last quarter of 2021 in the amount of approximately $0.9 million. the two parties have restructured the Purchase Agreement to reduce the purchase price from RMB 30 million to RMB 6 million and to allocate the purchased mining equipment between the Company and the Seller. The Seller transported digital currency mining machines representing half of the agreed 50,440 terahashes per second (th/s) in computing power (or a total of 25,220 th/s in computing power) to Ningbo, China first, and then shipped to the U.S.

On April 21, 2021, the Company set up a joint venture in Texas, U.S. under the name of “Brilliant Warehouse Service Inc.” to support its freight logistics services in the U.S., pursuant to a cooperation agreement with Mr. Bangpin Yu. SG Shipping NY has a 51% equity interest in the joint venture.

In July 2021, the Company registered a new company, Gorgeous Trading Ltd. (“Gorgeous Trading”), which is 100% owned by SG Shipping NY. Gorgeous Trading is mainly engaged in smart warehouse and related business in Texas.

On August 31, 2021, the Company formed a joint venture, Phi Electric Motor, Inc. in New York, which is 51% owned by SG Shipping NY. Phi Electric Motor, Inc. had no operations as of the date of this Report.

On September 29, 2021, the Company formed a 100% owned subsidiary, SG Shipping & Risk Solution Inc., in New York. On December 23, 2021, SG Shipping & Risk Solution Inc. formed SG Link LLC in New York, of which it is a 100% owner. As of the date of this Report, the two companies have had no operations.

On October 3, 2021, the Company entered into a Strategic Alliance Agreement with HighSharp to establish a joint venture for collaborative engineering, technical development and commercialization of a bitcoin mining machine under the name Thor Miner Inc., granting Thor Miner exclusive rights covering design production, intellectual property, branding, marketing and sales. On October 11, 2021, Thor Miner was formed in Delaware, which is 51% owned by the Company and 49% owned by HighSharp.

6

On December 31, 2021, the Company entered into a series of agreements to terminate its variable interest entity (“VIE”) structure and deconsolidated its formerly controlled entity Sino-Global Shipping Agency Ltd. (“Sino-China”). The Company controlled Sino-China through its wholly owned subsidiary Trans Pacific Shipping Limited. The Company made the decision to dissolve the VIE structure and Sino-China because Sino-China has no active operations and the Company wanted to remove any potential risks associated with any VIE structures. In addition, the Company dissolved its subsidiary Sino-Global Shipping LA, Inc.

On April 10, 2022, the Company entered into a joint venture agreement with Golden Mainland Inc., a Georgia corporation (“Golden Mainland”) to establish a joint venture for building Bitcoin mining sites in Texas, Ohio, and other states. The joint venture has not been set up as of the date of this Report. The Company has no plan to pursue this business.

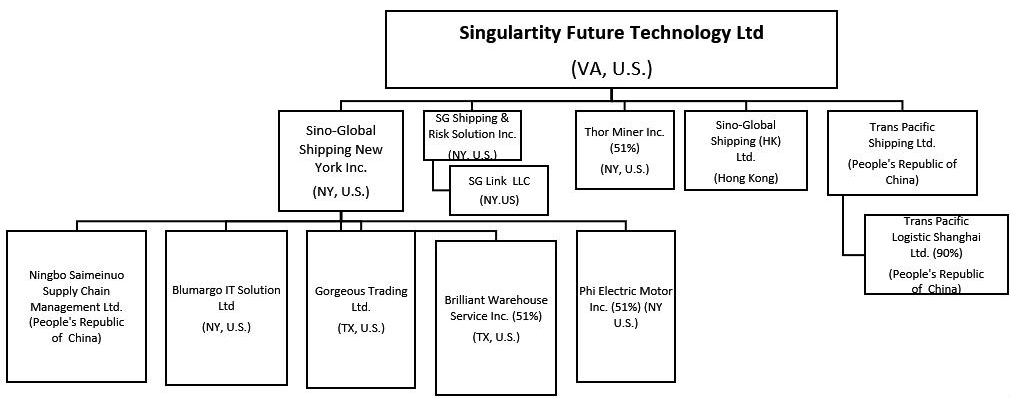

Our Corporate Structure

The diagram below shows our corporate structure as of the date of this Report.

| * | Unless otherwise indicated in the diagram, all the subsidiaries of the Company are wholly owned. |

Our Customers

Our main customers for the two fiscal years ended June 30, 2022 and 2021 is Chongqing Iron & Steel Ltd. and SOSNY. For the years ended June 30, 2022 and 2021, Chongqing Iron & Steel Ltd. accounted for 45.6% and 94.4% of the Company’s revenues, respectively. For the year ended June 30, 2022, SOSNY accounted for 27.9% of the Company’s gross revenue.

Our Suppliers

Our operations consist of working directly with our customers to understand in detail their needs and expectations and then managing local suppliers to ensure that our customers’ needs are met.

For the year ended June 30, 2022, two suppliers accounted for approximately 26.3% and 24.1% of our total purchases, respectively. For the year ended June 30, 2021, two suppliers accounted for approximately 55.4% and 28.6% of our total purchases, respectively.

7

Our Competition

The market segment that we now operate in, which is freight logistics services including warehouse services, does not have high entry barriers. In terms of our competition in China, there are many companies ranging from small to large that provide freight logistics services, and the state-owned companies in China generate a significant portion of the revenues in the industry. Our primary competitors in China are the China branches of international shipping companies or their exclusive agents in China. These companies include Evergreen Marine Corp., Orient Overseas Container Line, Ocean Network Express which includes Kawasaki Kisen Kaisha, Ltd, Mitsui O.S.K. Lines and Nippon Yusen Kabushiki Kaisha. The competition is intense due to the significant excess capacity. These companies have greater service capabilities, a larger customer base and more financial, marketing, network and human resources than we do. Most of them engage in a wide range of businesses and involve many aspects of the industry chain. However, we focus on providing tailored solutions and value-added services to customers in freight logistic services. As a boutique company with limited resources and history, we face intense competition. Our ability to grow in our industry depends on (1) our deep understanding of the complexity of industry issues and challenges and (2) our ability to develop optimal solutions to respond to the identified issues and provide effective problem-solving strategies to our targeted customers.

In terms of our competition in the United States, the freight logistics services industry is well developed, highly fragmented, and competition is fierce nationwide. Our primary competitors in the U.S. are local warehouse services providers and freight forwarding companies in Houston, for example, Bizto LLC, Golden Eagle Guns LLC, and Smart Supply Chain. Competition in the freight logistics services industry is driven by factors such as price, service quality, technology, and geographic reach. Companies that can offer a combination of these factors are often more competitive in the market. Additionally, companies that can adapt to changing customer demands and market trends, such as the shift towards e-commerce, are likely to be more successful in the long term. We aim at providing tailored and valued-added services for our international clients with needs for U.S. domestic logistics services.

Employees

As of the date of this Report, we have 39 full-time employees, 13 of whom are based in China and 26 are based in the United States. Of the total full-time employees, nine are in management, 17 are in operations, nine are in finance and accounting related and four are in administration and technical support. We believe that our relationship with our employees is good. We have never had a work stoppage, and our employees are not subject to a collective bargaining agreement.

Intellectual Property

As of the date of this Report, we do not have any registered patents, copyrights, or trademarks other than two pending trademark applications for “Thor” and “Thor Miner.” We have seven registered domain names, including our corporate website https://www.singularity.us/.

Item 1A. Risk Factors.

As a smaller reporting company, we are not required to include risk factors in this Report. However, below is a number of material risks, uncertainties and other factors that could have a material effect on the Company and its operations as a result of recent developments. You should carefully consider the risks described below before purchasing our common stock. The risks highlighted here are not the only ones that we may face. For example, additional risks presently unknown to us or that we currently consider immaterial or unlikely to occur could also impair our operations. If any of the risks or uncertainties described below or any such additional risks and uncertainties actually occur, our business, prospects, financial condition, or results of operations could be negatively affected, and you might lose all or part of your investment.

We are, and may continue to be, subject to litigation including individual and class action lawsuits, as well as investigations and enforcement actions by regulators and governmental authorities. These matters are often expensive and time consuming, and, if resolved adversely, could harm our business, financial condition, and operating results.

As discussed in “Item 1. Business – Recent Developments,” we are, and from time to time may become, subject to litigation and various legal proceedings, including litigation and proceedings related to stockholder derivative suits, class action lawsuits and other matters, that involve claims for substantial amounts of money or for other relief or that might necessitate changes to our business or operations. In addition to this, we have been, currently are, and may from time to time become subject to, government and regulatory investigations, inquiries, actions or requests, other proceedings and enforcement actions alleging violations of laws, rules, and regulations, both foreign and domestic. The defense of these actions may be both time consuming and expensive. We evaluate these litigation claims and legal proceedings to assess the likelihood of unfavorable outcomes and to estimate, if possible, the monetary amount of potential losses. Based on these assessments and estimates, we may establish reserves and/or disclose the relevant litigation claims or legal proceedings, as and when required or appropriate. These assessments and estimates are based on information available to management at the time of such assessment or estimation and involve a significant amount of judgment. As a result, actual outcomes or losses could differ materially from those envisioned by our current assessments and estimates. Our failure to successfully defend or settle any of these litigations or legal proceedings could result in liability that, to the extent not covered by our insurance, could have an adverse effect on our business, financial condition and results of operations.

8

The scope, determination, and impact of claims, lawsuits, government and regulatory investigations, enforcement actions, disputes, and proceedings to which we are subject cannot be predicted with certainty, and may result in:

| ● | substantial payments to satisfy judgments, fines, or penalties; | |

| ● | substantial outside counsel, advisor, and consultant fees and costs; | |

| ● | substantial administrative costs, including arbitration fees; | |

| ● | loss of productivity and high demands on employee time; | |

| ● | criminal sanctions or consent decrees; | |

| ● | termination of certain employees, including members of our executive team; | |

| ● | barring of certain employees from participating in our business in whole or in part; | |

| ● | orders that restrict our business or prevent us from offering certain products or services; | |

| ● | changes to our business model and practices | |

| ● | delays to planned transactions, service launches or improvements; and | |

| ● | damage to our brand and reputation. |

We are, and may continue to be, subject to securities litigation, which is expensive and could divert management attention, cause harm to our reputation and result in significant damages for which we could be responsible.

We are subject to securities class action litigation, which is expensive, could divert our management’s attention, harm our reputation, and leave us liable for substantial damages. For example, as discussed in “Item 1. Business – Recent Developments,” on December 9, 2022, Piero Crivellaro, purportedly on behalf of the persons or entities who purchased or acquired publicly traded securities of the Company between February 2021 and November 2022, filed a putative class action against the Company, certain of our officers and directors, and other defendants in the United States District Court for the Eastern District of New York, alleging violations of federal securities laws related to alleged false or misleading disclosures made by the Company in its public filings. The plaintiff seeks unspecified damages, plus interest, costs, fees, and attorneys’ fees. As this action is still in the early stage, the Company cannot predict the outcome, and certain of our officers in the U.S. District Court for the Eastern District of New York.

Litigation of this type could result in substantial costs and diversion of management’s attention and resources, which could adversely impact our business. Any adverse determination in litigation could also subject us to significant liabilities.

We are responsible for the indemnification of our officers and directors.

Should our officers and/or directors require us to contribute to their defense, we may be required to spend significant amounts of our capital. Our Certificate of Incorporation and bylaws also provide for the indemnification of our directors, officers, employees, and agents, under certain circumstances, against attorney’s fees and other expenses incurred by them in any litigation to which they become a party arising from their association with or activities on behalf of our company. This indemnification policy could result in substantial expenditures, which we may be unable to recoup. If these expenditures are significant or involve issues which result in significant liability for our key personnel, we may be unable to continue operating as a going concern.

9

We depend on a limited number of major customers who are able to exert a high degree of influence over us and the loss of a major customer could adversely impact our business.

For the years ended June 30, 2022 and 2021, one customer, Chongqing Iron & Steel Ltd., accounted for 60.8% and 89.7% of our revenues, respectively. There can be no assurance that our major customer will continue to purchase our services in the same amount that it has in the past. The loss of our major customer or a material reduction in sales to a major customer could have a material adverse effect on our sales and results of operations. Additionally, given the high concentration of our customer base, a default by or a significant reduction in future transactions with our major customer could materially reduce our revenues, profitability, liquidity and growth prospects.

We depend on a limited number of suppliers who are able to exert a high degree of influence over us and the loss of our major suppliers could adversely impact our business.

For the year ended June 30, 2022, two suppliers accounted for approximately 26.3% and 24.1% of our total purchases, respectively. For the year ended June 30, 2021, two suppliers accounted for approximately 55.4% and 28.6% of our total purchases, respectively. There can be no assurance that our major suppliers will continue to supply us with the materials or services required to operate our business in the same amount that they have in the past. The loss of our major suppliers or a material reduction in the materials or services they provide to us could have a material adverse effect on our business and results of operations.

Additionally, due to the unpredictable nature of COVID-19 regulations in China, our suppliers based in China may be affected by COVID-19 related issues such as shutdowns and delays. This may cause us to become unable to fulfill our customer orders on a timely basis, which may cause us to cancel orders and provide refunds, as demonstrated in our settlement with SOSNY.

The restatement of our prior financial statements may affect investor confidence and raise reputational issues and may subject us to additional risks and uncertainties, including increased professional costs and the increased possibility of legal proceedings and regulatory inquiries.

As discussed in our Current Form on Form 8-K filed on February 28, 2023, as amended by Amendment No. 1 filed on March 6, 2023, we determined to restate our financial statements as of and for the year ended June 30, 2021, three and six months ended September 30, 2021 and three and nine months ended December 31, 2021 after we identified errors related to, incorrect accounting treatment of related party loan receivable, incorrect recognition of revenue from freight shipping services and incorrect accounting treatment of recovery (provision) for doubtful accounts. As a result of these errors and the resulting restatements of our financial statements for the impacted periods, we have incurred, and may continue to incur, unanticipated costs for accounting and legal fees in connection with or related to the restatements, and have become subject to a number of additional risks and uncertainties, including the increased possibility of litigation and regulatory inquiries. Any of the foregoing may affect investor confidence in the accuracy of our financial disclosures and may raise reputational risks for our business, both of which could harm our business and financial results.

We have identified material weaknesses in our internal control over financial reporting and have determined to restate our previously issued financial statements. If our remediation of these material weaknesses is not effective, or if we fail to develop and maintain an effective system of disclosure controls and internal control over financial reporting, our ability to produce timely and accurate financial statements or comply with applicable laws and regulations could be impaired. In addition, the presence of material weaknesses increases the risk of a material misstatement of our consolidated financial statements.

As a public company, we are required, pursuant to Section 404(a) of the Sarbanes-Oxley Act, to furnish a report by management on, among other things, the effectiveness of our internal control over financial reporting in our Annual Report on Form 10-K. Effective internal control over financial reporting is necessary for reliable financial reports and, together with adequate disclosure controls and procedures, such internal controls are designed to prevent fraud. Any failure to implement required new or improved controls, or difficulties encountered in their implementation, could cause our Company to fail to meet our reporting obligations. Ineffective internal controls could also cause investors to lose confidence in reported financial information, which could have a negative effect on the trading price of our common stock.

Our management’s assessment must include disclosure of any material weaknesses identified by management in our internal control over financial reporting. Our management’s assessment could detect problems with internal controls. Undetected material weaknesses in internal controls could lead to financial statement restatements and require our Company to incur the expense of remediation.

A material weakness is a deficiency or combination of deficiencies in a company’s internal control over financial reporting such that there is a reasonable possibility that a material misstatement of its consolidated financial statements would not be prevented or detected on a timely basis. This deficiency could result in additional misstatements to its consolidated financial statements that would be material and would not be prevented or detected on a timely basis.

As discussed in “Item 9.A Controls and Procedures – Disclosure Controls and Procedures,” under the supervision and with the participation of our management, we conducted an assessment of the effectiveness of our disclosure controls and procedures as of June 30, 2022. Based on the foregoing evaluation, our Chief Operating Officer concluded that the Company’s disclosure controls and procedures were not effective due to ineffective internal controls over financial reporting that stemmed from the following material weaknesses for the year ended and as of June 30, 2022:

| ● | Lack of segregation of duties for accounting personnel who prepared and reviewed the journal entries in some of the subsidiaries within the consolidation, lack of supervision, coordination and communication of financial information between different entities within the Group; |

| ● | Lack of a full time U.S. GAAP personnel in the accounting department to monitor the recording of the transactions which led to error in revenue recognition in previously issued financial statements; |

| ● | Lack of resources with technical competency to address, review and record non-routine or complex transactions under U.S. GAAP; |

10

| ● | Lack of management control reviews of the budget against actual with analysis of the variance with a precision that can be explained through the analysis of the accounts; |

| ● | Lack of proper procedures in identifying and recording related party transactions which led to restatement of previously issued financial statements (See Note 1 of the accompanying consolidated financial statement footnotes); |

| ● | Lack of proper procedures to maintain supporting documents for accounting record; and |

| ● | Lack of proper oversight for the Company’s cash disbursement process that led to misuse of the Company funds by its former executive. |

In order to remediate the material weaknesses stated above, we intend to implement the following policies and procedures:

| ● | Hiring additional accounting staff to report the internal financial timely; | |

| ● | Hiring of CEO and CFO to properly set up the Company’s internal control and oversight process; |

| ● | Reporting other material and non-routine transactions to the Board and obtain proper approval; |

| ● | Recruiting additional qualified professionals with appropriate levels of U.S. GAAP knowledge and experience to assist in resolving accounting issues in non-routine or complex transactions; |

| ● | Developing and conducting U.S. GAAP knowledge, SEC reporting and internal control training to senior executives, management personnel, accounting departments and the IT staff, so that management and key personnel understand the requirements and elements of internal control over financial reporting mandated by the U.S. securities laws; |

| ● | Setting up budgets and developing expectations based on understanding of the business operations, compare the actual results with the expectations periodically and document the reasons for the fluctuations with further analysis. This should be done by CFO and reviewed by CEO upon their communications with the Board; | |

| ● | Strengthening our corporate governance; |

| ● | Setting up policies and procedures for the Company’s related party identification to properly identify, record and disclose related party transactions; and |

| ● | Setting up proper procedures for the Company’s fund disbursement process to ensure that cash is disbursed only upon proper authorization, for valid business purposes, and that all disbursements are properly recorded. |

We cannot provide assurance that these or other measures will fully remediate our material weaknesses in a timely manner. If our remediation of these material weaknesses is not effective, it may cause our Company to become subject to investigation or sanctions by the SEC. It may also adversely affect investor confidence in our Company and, as a result, the value of our common stock. There can be no assurance that all existing material weaknesses have been identified, or that additional material weaknesses will not be identified in the future. In addition, if we are unable to continue to meet our financial reporting obligations, we may not be able to remain listed on Nasdaq.

Our ability to maintain compliance with Nasdaq continued listing requirements, including whether we are able to maintain the closing bid price of our common stock, could result in the delisting of our common stock.

Our common stock is currently listed on The Nasdaq Capital Market (“Nasdaq”). To maintain this listing, we must satisfy minimum financial and other requirements.

On May 24, 2022, the Company received a delinquency notice from Nasdaq indicating that the Company was not in compliance with Nasdaq Listing Rule 5250(c)(1) due to its delay in filing its Quarterly Report on Form 10-Q for the quarter ended March 31, 2022. The Company was provided 60 days to submit a plan to regain compliance. On July 25, 2022 and September 14, 2022, the Company submitted its Compliance Plan. Based on the review of the Compliance Plan as well as telephone conversations with outside counsel to the Company and counsel to the Company’s Special Committee, the Staff has determined that the Company did not provide a definitive plan evidencing its ability to file the Reports within the 180 calendar day period available to the Staff under the Nasdaq Listing Rules.

On November 16, 2022, the Company received an additional staff determination notice from Nasdaq, advising that it had not received the Company’s Form 10-Q for the quarterly period ended September 30, 2022, which served as an additional basis for delisting the Company’s securities and that the Panel will consider the additional deficiency in rendering a determination regarding the Company’s continued listing on Nasdaq. The Company has submitted to the Panel a plan to regain compliance with the continued listing requirements, including the filing of the Form 10-Q for the quarterly period ended September 30, 2022.

On January 5, 2023, the Company received a deficiency notice from Nasdaq informing the Company that its common stock, no par value, fails to comply with the $1 minimum bid price required for continued listing on The Nasdaq Capital Market under Nasdaq Listing Rule 5550(a)(2) based upon the closing bid price of the common stock for the 30 consecutive business days prior to the date of the notice from Nasdaq. The Company has been provided an initial compliance period of 180 calendar days, or until July 5, 2023, to regain compliance with the minimum bid price requirement.

11

On February 21, 2023, the Company received an additional staff determination notice from Nasdaq, advising that it had not received the Company’s Form 10-Q for the quarterly period ended December 31, 2022, which served as an additional basis for delisting the Company’s securities. The notice stated that the Panel will consider the additional deficiency in rendering a determination regarding the Company’s continued listing on Nasdaq. The Company has submitted to the Panel a plan to regain compliance with the continued listing requirements and has been granted a grace period to file all the delinquent reports, including the filing of the Form 10-Q for the quarterly period ended December 31, 2022, on or before February 28, 2023.Given we did not file all the Reports within the grace period granted by the Panel, we may be delisted from Nasdaq. There can be also no assurance that our stock price will meet the minimum bid price requirement or we will meet other requirements for continued listing on Nasdaq. If our common stock is delisted from Nasdaq and we are unable to list our common stock on another national securities exchange, we expect our common stock would be quoted on an over-the-counter market. If this were to occur, we and our stockholders could face significant material adverse consequences, including the limited availability of market quotations for our common stock; substantially decreased trading in our common stock; decreased market liquidity of our common stock as a result of the loss of market efficiencies associated with Nasdaq and the loss of federal preemption of state securities laws; an adverse effect on our ability to issue additional securities or obtain additional financing in the future on acceptable terms, if at all; potential loss of confidence by investors, suppliers, partners, and employees and fewer business development opportunities; and limited news and analyst coverage. Additionally, the market price of our common stock may decline further, and stockholders may lose some or all of their investment.

For additional risks relating to our operations, see the section titled “Risk Factors” contained in our Registration Statement on Form S-3, filed with the SEC on March 3, 2021 and other filings we file with the SEC from time to time.

Item 1B. Unresolved Staff Comments.

The Company does not have any unresolved or outstanding staff comments.

Item 2. Properties.

We currently rent six facilities in the PRC and the United States. Our PRC headquarters is in Shanghai and our U.S. headquarters is in New York.

| Office | Address | Rental Term | Space | |||

| New York, USA |

98 Cutter Mill Rd Suite 322 Great Neck, New York 11021 |

Expires 07/31/2026 | 3,033 ft2 | |||

| Texas, USA |

6161 Savoy Dr Suite 409 Houston, Texas 77036 |

Expires 07/31/2023 | 2,456 ft2 | |||

| Texas, USA |

6161 Savoy Dr, Suite 1040 Houston, Texas 77036 |

Expires 06/30/2024 | 954 ft2 | |||

| Texas, USA |

12733 Stafford Road, Suite 400 Stafford, Texas 77477 |

Expires 07/31/2024 | 46,463 ft2 | |||

| Shanghai, PRC |

Rm 12D & 12E, No.359 Dongdaming Road, Hongkou District, Shanghai, PRC 200080 |

Expires 12/31/2023 | 3,078 ft2 | |||

| Ningbo, PRC |

B 525 Hebang Building, Ningbo, Zhejiang, PRC 315000

|

Expires 07/06/2025 | 840 ft2 |

Item 3. Legal Proceedings.

See “Item 1. Business – Recent Developments” for a description of legal proceedings the Company is currently involved in, which is incorporated herein by reference.

Item 4. Mine Safety Disclosures.

This item is not applicable to the Company.

12

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Market for Our Common Stock

Our common stock is traded on the Nasdaq Capital Market under the symbol SGLY.

Holders of Our Common Stock

As of March 3, 2023, there were 20 holders of record of our common stock. This number does not include stockholders who hold their shares of common stock in street name.

Dividend Policy

We have never declared or paid any cash dividends on our common stock. We anticipate that we will retain any earnings to support operations and to finance the growth and development of our business. Therefore, we do not expect to pay cash dividends in the foreseeable future. Any future determination relating to our dividend policy will be made at the discretion of our Board and will depend on a number of factors, including future earnings, capital requirements, financial conditions and future prospects and other factors the Board may deem relevant. Payments of dividends by our PRC subsidiaries to our company are subject to restrictions including primarily the restriction that foreign invested enterprises may only buy, sell and/or remit foreign currencies at those banks authorized to conduct foreign exchange business after providing valid commercial documents.

Recent Sales of Unregistered Securities and Issuer Purchases of Equity Securities

None.

Item 6. [Reserved]

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

The following discussion and analysis of the Company’s financial condition and results of operations should be read in conjunction with our consolidated financial statements and the related notes included elsewhere in the Report. This discussion contains forward-looking statements that involve risks and uncertainties. Actual results and the timing of selected events could differ materially from those anticipated in these forward-looking statements as a result of various factors.

Overview

We previously focused on providing customized freight logistics services, but starting in 2017, we began exploring new opportunities to expand our business and generate more revenue. These opportunities ranged from complementary businesses to other new service and product initiatives. In the fiscal years 2021 and 2022, while we continued to provide our freight logistics business, we expanded our services to include warehousing services provided by our US subsidiary Brilliant Warehouse Service Inc. On January 3, 2022, we changed our corporate name to Singularity Future Technology Ltd. to align with our entry into the digital assets business through our U.S. subsidiaries. During 2022, we engaged in purchases and sales of cryptocurrency mining machines through our U.S. subsidiaries.

For the fiscal year ended June 30, 2022, we operated in two operating segments, including (1) freight logistics services, through our subsidiaries in the U.S and PRC; and (2) purchase and sales of crypto mining machines, through our subsidiary Thor Miner. For the year ended June 30, 2021, the Company also engaged in shipping agency and management services, which were carried out by its subsidiary in the U.S. The Company no longer operates in the shipping agency segment because it did not receive any new orders for its services due to the uncertainty of the shipping management market which was negatively impacted by the COVID-19 pandemic.

Recent Developments

The following events had a material impact on our financial statements. For other recent developments, see “Item 1. Business – Recent Developments.”

13

On January 10, 2022, Thor Miner entered into a purchase agreement with HighSharp. Pursuant to the agreement, Thor Miner agreed to purchase certain cryptocurrency mining equipment from HighSharp. In January and April 2022, Thor Miner made a total prepayment of $35,406,649 for the order. Thor Miner also entered into a PSA with SOSNY for the purchase of $200,000,000 in crypto mining rigs and received deposit form SOSNY in the amount of $48,930,000.

Due to production issue from HighSharp, Thor Miner was not able to timely deliver the products to SOSNY according to the delivery terms of the PSA and was sued by SOSNY for breach of contract on December 9, 2022. On December 23, 2022, the Company entered into the Settlement Agreement with SOSNY pursuant to which the Company paid $13.0 million to SOSNY in exchange for SOSNY dismissing the lawsuit and will transfer any additional funds it receives from HighSharp to SOSNY in an amount not to exceed $40,560,569.

As of December 22, 2022, the balance of advance to HighSharp and deposit from SOSNY amounted to $27,927,583 and $40,560,569, respectively. Thor Miner paid $13.0 million on December 28, 2022 to SOSNY and wrote off the balance of the deposit it received from SOSNY and the balance of its payment to HighSharp.

Restatement of Previously Issued Financial Statements

From March to June 2019, the Company’s subsidiary Trans Pacific Logistic Shanghai Ltd (“Trans Pacific Shanghai”) received approximately $6.2 million (RMB 40 million) from a related party, Shanghai Baoyin Industrial Co., Ltd. (“Shanghai Baoyin”), to pay for accounts receivable of six different customers totaling RMB 40 million. Shanghai Baoyin is 30% owned by Wang Qinggang, the CEO and legal representative of Trans Pacific Shanghai. Trans Pacific Shanghai subsequently paid RMB 20 million and RMB 10 million to Zhangjiakou Baoyu Trading Co. Ltd. (“Baoyu”), a third party, in April 2019 and July 2019, respectively, and it made an additional payment of RMB 10 million to Hebei Baoxie Trading Co., Ltd. (“Hebei Baoxie”), a third party, in July 2019.

As such, for the fiscal year ended June 30, 2019, accounts receivable was understated by RMB 40 million, advance to supplier was overstated by RMB 20 million, and other payables from Shanghai Baoyin, a related party, were understated by RMB 20 million. There was an overstatement of RMB 20 million in total assets and an understatement of total liabilities of RMB 20 million.

During the fiscal year ended June 30, 2021, Hebei Baoxie repaid a total of RMB 10 million to Trans Pacific Shanghai, and Trans Pacific Shanghai advanced the RMB 10 million to Shanghai Baoyin. The RMB 10 million paid to Shanghai Baoyin was recorded as other receivable, and the RMB 30 million advance to Baoyu was reclassified from an advance to supplier to other receivable. The Company provided a full allowance of its receivables totaling RMB 40 million. The Company evaluated this transaction and determined there is no impact on its assets, liabilities, or retained earnings as of June 30, 2020.

During the fiscal year ended June 30, 2021, Baoyu repaid a total of RMB 30 million to Trans Pacific Shanghai. The RMB 30 million received was recorded as recovery of bad debt. Trans Pacific Shanghai then loaned the same amount to Shanghai Baoyin. Shanghai Baoyin subsequently repaid RMB 4 million to Trans Pacific Shanghai, and Trans Pacific Shanghai loaned the same amount to Wang Qinggang. The RMB 30 million received was recorded as recovery of bad debt for other receivable and the RMB 30 million paid was recorded as a related party loan receivable.

The Company analyzed the transactions and determined the RMB 30 million was originally from Shanghai Baoyin and eventually paid back to the same related parties. Recovery of bad debt and related party loan receivable was overstated by RMB 30 million for the fiscal year 2021.

The Company restated its fiscal year 2021 financial statements to restate related party loans receivable and bad debt recovery.

Effects of the restatement are as follows:

| As Previously Reported | Adjustments | As Restated | ||||||||||

| Consolidate balance sheet as of June 30, 2021 | ||||||||||||

| Loan receivable - related parties | $ | 4,644,969 | $ | (4,644,969 | ) | $ | - | |||||

| Total assets | $ | 52,803,116 | $ | (4,644,969 | ) | $ | 48,158,147 | |||||

14

| As Previously Reported | Adjustments | As Restated | ||||||||||

| Consolidated Statement of Stockholder’s Equity as of June 30, 2021 | ||||||||||||

| Accumulated deficit | $ | (30,244,937 | ) | $ | (4,076,825 | ) | $ | (34,321,762 | ) | |||

| Accumulated other comprehensive income (loss) | (625,449 | ) | (103,647 | ) | (729,096 | ) | ||||||

| Non-controlling Interest | (6,951,134 | ) | (464,497 | ) | (7,415,631 | ) | ||||||

| Total equity | $ | 47,069,142 | $ | (4,644,969 | ) | $ | 42,424,173 | |||||

| As Previously Reported | Adjustments | As Restated | ||||||||||

| Consolidated statement of oeprations for the year ended June 30, 2021 | ||||||||||||

| Recovery (provision) for doubtful accounts, net | $ | 321,168 | $ | (4,529,806 | ) | $ | (4,208,638 | ) | ||||

| Net loss | $ | (6,773,047 | ) | $ | (4,529,806 | ) | $ | (11,302,853 | ) | |||

| Other comprehensive loss - foreign currency | (488 | ) | (115,163 | ) | $ | (115,651 | ) | |||||

| Comprehensive loss | $ | (6,773,535 | ) | $ | (4,644,969 | ) | $ | (11,418,504 | ) | |||

| As Previously Reported | Adjustments | As Restated | ||||||||||

| Consolidated statement of cash flow for the year ended June 30, 2021 | ||||||||||||

| Cash flows from operating activities: | ||||||||||||

| Net loss | $ | (6,773,047 | ) | $ | (4,529,806 | ) | $ | (11,302,853 | ) | |||

| (Recovery)/ Provision for doubtful accounts | (321,168 | ) | 4,529,806 | 4,208,638 | ||||||||

| Other receivable | 4,227,239 | (4,529,806 | ) | (302,567 | ) | |||||||

| Cash flows from investing activities: | ||||||||||||

| Loan receivable - related parties | $ | (4,529,806 | ) | $ | 4,529,806 | $ | - | |||||

Impact of COVID-19

The outbreak of the COVID-19 starting from late January 2020 in the PRC has spread rapidly to many parts of the world. In March 2020, the World Health Organization declared the COVID-19 as a pandemic. Given the continually expanding of COVID-19 pandemic in China and United States, our business, results of operations, and financial condition are still adversely affected.

In early December 2022, Chinese government eased the strict control measure for COVID-19, which has led to surge in increased infections and disruption in our business operations. Any future impact of COVID-19 on the Company’s China operation results will depend on, to a large extent, future developments and new information that may emerge regarding the duration and resurgence of COVID-19 variants and the actions taken by government authorities to contain COVID-19 or treat its impact, almost all of which are beyond our control.

The impacts of COVID-19 on our business, financial condition, and results of operations include, but are not limited to, the following:

| ● | Our customers have been negatively impacted by the pandemic, which reduced their demand for freight logistics services. As a result, our revenue for the year ended June 30, 2022 was down by approximately $1.2 million, or 22.6%. |

| ● | Due to travel restrictions between US and China, our new business development for existing segments or new ventures has been slowed down. | |

| ● | Our sales of crypto mining machines were materially adversely affected by COVID-19. Specifically, Crypto mining machine manufacturers have been impacted by the constrained supply of the semiconductors used in the production of the highly specialized crypto mining machines; COVID-related issues have exacerbated port congestion and intermittent supplier shutdowns and delays, resulting in delayed shipments and additional expenses to expedite delivery; as a result, we were unable to fulfil our customer orders on a timely basis, resulting cancellation of orders and partial refund of purchase price, as evident from the settlement in SOSNY. |

15

We have been, and may continue to be, negatively impacted by the ongoing COVID-19, which may continually impact our cost of freight, or result in higher cost of revenue, which may in turn materially adversely affect our financial condition and operating results in coming months.

Any future impact of COVID-19 on the Company’s operation results will depend on, to a large extent, future developments and new information that may emerge regarding the duration and resurgence of COVID-19 variants and the actions taken by government authorities to contain COVID-19 or treat its impact, almost all of which are beyond our control.

Results of Operations

Comparison of the Years Ended June 30, 2022 and 2021

The following table sets forth the results of our operations for the periods indicated:

| For the Years Ended June 30, | ||||||||||||||||||||||||

| 2022 | 2021(restated) | Change | ||||||||||||||||||||||

| US $ | % | US $ | % | US $ | % | |||||||||||||||||||