U.S. SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-Q

☒ Quarterly report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the period ended December 31, 2020

☐ Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from ___________ to ___________.

Commission File Number 001-34024

Sino-Global Shipping America, Ltd.

(Exact name of registrant as specified in its charter)

| Virginia | 11-3588546 | |

| (State or other jurisdiction of | (I.R.S. employer | |

| Incorporation or organization) | identification number) |

1044 Northern Boulevard, Suite 305 Roslyn, New York |

11576-1514 | |

| (Address of principal executive offices) | (Zip Code) |

(718) 888-1814

(Registrant’s telephone number, including area code)

Securities Registered Pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| Common Stock | SINO | NASDAQ Capital Market |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ | |

| Non-accelerated filer ☒ | Smaller reporting company ☒ | |

| Emerging Growth Company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of February 11, 2021, the Company had 13,309,244 shares of common stock issued and outstanding.

SINO-GLOBAL SHIPPING AMERICA, LTD .

FORM 10-Q

INDEX

i

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This document contains certain statements of a forward-looking nature. Such forward-looking statements, including but not limited to projected growth, trends and strategies, future operating and financial results, financial expectations and current business indicators are based upon current information and expectations and are subject to change based on factors beyond our control. Forward-looking statements typically are identified by the use of terms such as “look”, “may”, “will”, “should”, “might”, “believe”, “plan”, “expect”, “anticipate”, “estimate” and similar words, although some forward-looking statements are expressed differently. The accuracy of such statements may be impacted by a number of business risks and uncertainties that could cause actual results to differ materially from those projected or anticipated, including but not limited to the following:

| ● | Our ability to timely and properly deliver our services; |

| ● | Our dependence on a limited number of major customers and related parties; |

| ● | Political and economic factors in the People’s Republic of China (“PRC”); |

| ● | Our ability to expand and grow our lines of business; |

| ● | Unanticipated changes in general market conditions or other factors, which may result in cancellations or reductions in the need for our services; |

| ● | Economic conditions which would reduce demand for services provided by us and could adversely affect profitability; |

| ● | The effect of terrorist acts, or the threat thereof, on the demand for the shipping and logistic industry which could, adversely affect our operations and financial performance; |

| ● | The acceptance in the marketplace of our new lines of business; |

| ● | Foreign currency exchange rate fluctuations; |

| ● | Hurricanes, outbreak of contagious diseases or other natural disasters; and |

| ● | Our ability to attract, retain and motivate skilled personnel. |

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. We undertake no obligation to update this forward-looking information unless required by applicable law or regulations.

ii

SINO-GLOBAL SHIPPING AMERICA, LTD. AND AFFILIATES

CONDENSED CONSOLIDATED BALANCE SHEETS

(UNAUDITED)

| December 31, | June 30, | |||||||

| 2020 | 2020 | |||||||

| Assets | ||||||||

| Current assets | ||||||||

| Cash | $ | 4,473,000 | $ | 131,182 | ||||

| Accounts receivable, net | 1,262,138 | 1,155,948 | ||||||

| Other receivables, net | 583,916 | 51,034 | ||||||

| Advances to suppliers - third parties | 80,804 | 48,875 | ||||||

| Prepaid expenses and other current assets | 63,125 | 90,382 | ||||||

| Due from related party, net | 345,898 | 435,898 | ||||||

| Total Current Assets | 6,808,881 | 1,913,319 | ||||||

| Property and equipment, net | 424,326 | 523,290 | ||||||

| Right-of-use assets | 224,950 | 300,114 | ||||||

| Intangible assets, net | - | 26,389 | ||||||

| Other long-term assets - deposits | 3,204,323 | 2,974,990 | ||||||

| Total Assets | $ | 10,662,480 | $ | 5,738,102 | ||||

| Liabilities and Equity | ||||||||

| Current Liabilities | ||||||||

| Deferred revenue | $ | 470,996 | $ | 67,083 | ||||

| Accounts payable | 564,495 | 487,692 | ||||||

| Lease liabilities - current | 166,572 | 204,391 | ||||||

| Taxes payable | 3,561,551 | 3,280,348 | ||||||

| Accrued expenses and other current liabilities | 855,188 | 1,643,319 | ||||||

| Loan payable - current | 132,468 | 126,032 | ||||||

| Total current liabilities | 5,751,270 | 5,808,865 | ||||||

| Lease liabilities - noncurrent | 78,660 | 132,699 | ||||||

| Loan payable - noncurrent | 148,002 | 154,438 | ||||||

| Total liabilities | 5,977,932 | 6,096,002 | ||||||

| Commitments and Contingencies | ||||||||

| Equity (Deficiency) | ||||||||

| Preferred stock, 2,000,000 shares authorized, no par value, 860,000 and nil shares issued and outstanding as of December 31, 2020 and June 30, 2020, respectively | 1,427,600 | - | ||||||

| Common stock, 50,000,000 shares authorized, no par value; 5,998,788 and 3,718,788 shares issued and outstanding as of December 31, 2020 and June 30, 2020, respectively* | 33,788,522 | 28,414,992 | ||||||

| Additional paid-in capital | 2,334,962 | 2,334,962 | ||||||

| Subscription receivable | - | (59,869 | ) | |||||

| Accumulated deficit | (25,258,304 | ) | (23,421,594 | ) | ||||

| Accumulated other comprehensive loss | (656,914 | ) | (1,084,030 | ) | ||||

| Total Sino-Global Shipping America Ltd. Stockholders' Equity | 11,635,866 | 6,184,461 | ||||||

| Non-controlling Interest | (6,951,318 | ) | (6,542,361 | ) | ||||

| Total Equity (Deficiency) | 4,684,548 | (357,900 | ) | |||||

| Total Liabilities and Equity (Deficiency) | $ | 10,662,480 | $ | 5,738,102 | ||||

| * | Shares and per share data are presented on a retroactive basis to reflect the 1-for-5 reverse stock split on July 7, 2020. |

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

1

SINO-GLOBAL SHIPPING AMERICA, LTD. AND AFFILIATES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE INCOME (LOSS)

(UNAUDITED)

| For the Three Months Ended | For the Six Months Ended | |||||||||||||||

| December 31, | December 31, | |||||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||

| Net revenues | 1,884,440 | 2,021,124 | $ | 3,021,239 | $ | 3,807,350 | ||||||||||

| Cost of revenues | (1,688,464 | ) | (755,645 | ) | (2,783,690 | ) | (1,439,049 | ) | ||||||||

| Gross profit | 195,976 | 1,265,479 | 237,549 | 2,368,301 | ||||||||||||

| Selling expenses | (73,462 | ) | (126,125 | ) | (142,392 | ) | (256,154 | ) | ||||||||

| General and administrative expenses | (1,314,235 | ) | (702,064 | ) | (2,017,669 | ) | (1,793,519 | ) | ||||||||

| Impairment loss of fixed assets and intangible asset | - | - | - | (327,632 | ) | |||||||||||

| Provision for doubtful accounts, net of recovery | 15,891 | (278,676 | ) | (2,462 | ) | (1,167,754 | ) | |||||||||

| Stock-based compensation | - | (491,609 | ) | - | (906,317 | ) | ||||||||||

| Total operating expenses | (1,371,806 | ) | (1,598,474 | ) | (2,162,523 | ) | (4,451,376 | ) | ||||||||

| Operating loss | (1,175,830 | ) | (332,995 | ) | (1,924,974 | ) | (2,083,075 | ) | ||||||||

| Other income (loss), net | 85,720 | (15,613 | ) | 86,408 | (14,157 | ) | ||||||||||

| Net loss before provision for income taxes | (1,090,110 | ) | (348,608 | ) | (1,838,566 | ) | (2,097,232 | ) | ||||||||

| Income tax expense | (3,450 | ) | (14,747 | ) | (3,450 | ) | (14,747 | ) | ||||||||

| Net loss | (1,093,560 | ) | (363,355 | ) | (1,842,016 | ) | (2,111,979 | ) | ||||||||

| Net income (loss) attributable to non-controlling interest | 9,359 | 43,978 | (5,306 | ) | (77,293 | ) | ||||||||||

| Net loss attributable to Sino-Global Shipping America, Ltd. | $ | (1,102,919 | ) | $ | (407,333 | ) | $ | (1,836,710 | ) | $ | (2,034,686 | ) | ||||

| Comprehensive loss | ||||||||||||||||

| Net loss | $ | (1,093,560 | ) | $ | (363,355 | ) | $ | (1,842,016 | ) | $ | (2,111,979 | ) | ||||

| Other comprehensive income (loss) - foreign currency | 31,038 | 256,206 | 23,465 | (247,461 | ) | |||||||||||

| Comprehensive loss | (1,062,522 | ) | (107,149 | ) | (1,818,551 | ) | (2,359,440 | ) | ||||||||

| Less: Comprehensive loss attributable to non-controlling interest | (195,468 | ) | (49,831 | ) | (408,957 | ) | (28,558 | ) | ||||||||

| Comprehensive loss attributable to Sino-Global Shipping America, Ltd. | $ | (867,054 | ) | $ | (57,318 | ) | $ | (1,409,594 | ) | $ | (2,330,882 | ) | ||||

| Loss per share | ||||||||||||||||

| Basic and diluted* | $ | (0.23 | ) | $ | (0.12 | ) | $ | (0.42 | ) | $ | (0.62 | ) | ||||

| Weighted average number of common shares used in computation | ||||||||||||||||

| Basic and diluted* | 4,828,788 | 3,363,802 | 4,328,571 | 3,289,674 | ||||||||||||

| * | Shares and per share data are presented on a retroactive basis to reflect the 1-for-5 reverse stock split on July 7, 2020. |

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

2

SINO-GLOBAL SHIPPING AMERICA, LTD. AND AFFILIATES

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY (DEFICIENCY)

(UNAUDITED )

| Preferred Stock | Common Stock | Additional paid-in | Treasury Stock | Subscription | Accumulated | Accumulated other comprehensive | Noncontrolling | |||||||||||||||||||||||||||||||||||||||||

| Shares | Amount | Shares* | Amount | capital | Shares* | Amount | receivable | deficit | loss | interest | Total | |||||||||||||||||||||||||||||||||||||

| BALANCE, June 30, 2019 | - | $ | - | 3,210,907 | $ | 26,523,830 | $ | 2,066,906 | (35,099 | ) | $ | (417,538 | ) | $ | - | $ | (6,968,700 | ) | $ | (671,106 | ) | $ | (5,173,622 | ) | $ | 15,359,770 | ||||||||||||||||||||||

| Stock based compensation to employee | - | - | 18,000 | 63,000 | - | - | - | - | - | - | - | 63,000 | ||||||||||||||||||||||||||||||||||||

| Stock based compensation to consultants | - | - | 48,000 | 200,300 | - | - | - | - | - | - | - | 200,300 | ||||||||||||||||||||||||||||||||||||

| Amortization of shares issued to consultants | - | - | - | - | 180,209 | - | - | - | - | - | - | 180,209 | ||||||||||||||||||||||||||||||||||||

| Foreign currency translation | - | - | - | - | - | - | - | - | - | (646,211 | ) | 142,544 | (503,667 | ) | ||||||||||||||||||||||||||||||||||

| Net loss | - | - | - | - | - | - | - | - | (1,627,353 | ) | - | (121,271 | ) | (1,748,624 | ) | |||||||||||||||||||||||||||||||||

| BALANCE, September 30, 2019 | - | - | 3,276,907 | 26,787,130 | 2,247,115 | (35,099 | ) | (417,538 | ) | - | (8,596,053 | ) | (1,317,317 | ) | (5,152,349 | ) | 13,550,988 | |||||||||||||||||||||||||||||||

| Stock based compensation to employees | - | - | 46,000 | 156,400 | - | - | - | - | - | - | - | 156,400 | ||||||||||||||||||||||||||||||||||||

| Stock based compensation to consultants | - | - | 70,000 | 282,500 | - | - | - | - | - | - | - | 282,500 | ||||||||||||||||||||||||||||||||||||

| Amortization of shares issued to consultants | - | - | - | - | 52,708 | - | - | - | - | - | - | 52,708 | ||||||||||||||||||||||||||||||||||||

| Issuance of common stock to private investor | - | - | 100,100 | 500,500 | - | - | - | - | - | - | - | 500,500 | ||||||||||||||||||||||||||||||||||||

| Cancellation of treasury stock | - | - | (35,099 | ) | (417,538 | ) | - | 35,099 | 417,538 | - | - | - | - | - | ||||||||||||||||||||||||||||||||||

| Foreign currency translation | - | - | - | - | - | - | - | - | - | 350,015 | (93,809 | ) | 256,206 | |||||||||||||||||||||||||||||||||||

| Net loss | - | - | - | - | - | - | - | - | (407,333 | ) | - | 43,978 | (363,355 | ) | ||||||||||||||||||||||||||||||||||

| BALANCE, December 31, 2019 | - | $ | - | 3,457,908 | $ | 27,308,992 | $ | 2,299,823 | - | $ | - | $ | - | $ | (9,003,386 | ) | $ | (967,302 | ) | $ | (5,202,180 | ) | $ | 14,435,947 | ||||||||||||||||||||||||

| Preferred Stock | Common Stock | Additional paid-in | Treasury Stock | Subscription | Accumulated | Accumulated other comprehensive | Noncontrolling | |||||||||||||||||||||||||||||||||||||||||

| Shares | Amount | Shares* | Amount | capital | Shares | Amount | receivable | deficit | loss | interest | Total | |||||||||||||||||||||||||||||||||||||

| BALANCE, June 30, 2020 | - | $ | - | 3,718,788 | $ | 28,414,992 | $ | 2,334,962 | - | $ | - | $ | (59,869 | ) | $ | (23,421,594 | ) | $ | (1,084,030 | ) | $ | (6,542,361 | ) | $ | (357,900 | ) | ||||||||||||||||||||||

| Issuance of common stock to private investor | - | - | 720,000 | 1,051,200 | - | - | - | 59,869 | - | - | - | 1,111,069 | ||||||||||||||||||||||||||||||||||||

| Foreign currency translation | - | - | - | - | - | - | - | - | - | 191,251 | (198,824 | ) | (7,573 | ) | ||||||||||||||||||||||||||||||||||

| Net loss | - | - | - | - | - | - | - | - | (733,791 | ) | - | (14,665 | ) | (748,456 | ) | |||||||||||||||||||||||||||||||||

| BALANCE, September 30, 2020 | - | - | 4,438,788 | 29,466,192 | 2,334,962 | - | - | - | (24,155,385 | ) | (892,779 | ) | (6,755,850 | ) | (2,860 | ) | ||||||||||||||||||||||||||||||||

| Issuance of preferred stock to private investor | 860,000 | 1,427,600 | - | - | - | - | - | - | - | - | - | 1,427,600 | ||||||||||||||||||||||||||||||||||||

| Issuance of common stock to private investor | - | - | 1,560,000 | 4,322,330 | - | - | - | - | - | - | - | 4,322,330 | ||||||||||||||||||||||||||||||||||||

| Foreign currency translation | - | - | - | - | - | - | - | - | - | 235,865 | (204,827 | ) | 31,038 | |||||||||||||||||||||||||||||||||||

| Net loss | - | - | - | - | - | - | - | - | (1,102,919 | ) | - | 9,359 | (1,093,560 | ) | ||||||||||||||||||||||||||||||||||

| BALANCE, December 31, 2020 | 860,000 | $ | 1,427,600 | 5,998,788 | $ | 33,788,522 | $ | 2,334,962 | - | $ | - | $ | - | $ | (25,258,304 | ) | $ | (656,914 | ) | $ | (6,951,318 | ) | $ | 4,684,548 | ||||||||||||||||||||||||

| * | Shares and per share data are presented on a retroactive basis to reflect the 1-for-5 reverse stock split on July 7, 2020. |

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

3

SINO-GLOBAL SHIPPING AMERICA, LTD. AND AFFILIATES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(UNAUDITED)

| For the Six Months Ended | ||||||||

| December 31, | ||||||||

| 2020 | 2019 | |||||||

| Operating Activities | ||||||||

| Net income (loss) | $ | (1,842,016 | ) | $ | (2,111,979 | ) | ||

| Adjustments to reconcile net income (loss) to net cash used in operating activities: | ||||||||

| Stock-based compensation | - | 906,317 | ||||||

| Depreciation and amortization | 165,128 | 237,011 | ||||||

| Non-cash lease expense | 76,716 | 78,405 | ||||||

| Provision for doubtful accounts, net of recovery | 2,462 | 1,167,754 | ||||||

| Impairment loss of fixed assets and intangible asset | - | 327,632 | ||||||

| Changes in assets and liabilities | ||||||||

| Notes receivable | - | 386,233 | ||||||

| Accounts receivable | (190,033 | ) | 1,629,174 | |||||

| Other receivables | (881,628 | ) | (5,855,492 | ) | ||||

| Advances to suppliers - third parties | (28,770 | ) | (66,691 | ) | ||||

| Prepaid expenses and other current assets | 27,277 | 160,497 | ||||||

| Other long-term assets - deposits | (100,746 | ) | 96,281 | |||||

| Due from related parties | 86,000 | 413,408 | ||||||

| Deferred revenue | 401,966 | - | ||||||

| Advances from customers | - | 5,580 | ||||||

| Accounts payable | 57,265 | (63,131 | ) | |||||

| Taxes payable | 140,633 | (76,110 | ) | |||||

| Lease liabilities | (93,459 | ) | (77,118 | ) | ||||

| Accrued expenses and other current liabilities | (788,780 | ) | (233,414 | ) | ||||

| Net cash used in operating activities | (2,967,985 | ) | (3,075,643 | ) | ||||

| Investing Activities | ||||||||

| Acquisition of property and equipment | - | (7,020 | ) | |||||

| Net cash used in investing activities | - | (7,020 | ) | |||||

| Financing Activities | ||||||||

| Proceeds from issuance of preferred stock | 1,427,600 | - | ||||||

| Proceeds from issuance of common stock | 5,433,399 | 500,500 | ||||||

| Net cash provided by financing activities | 6,860,999 | 500,500 | ||||||

| Effect of exchange rate fluctuations on cash | 448,804 | (440,820 | ) | |||||

| Net increase (decrease) in cash | 4,341,818 | (3,022,983 | ) | |||||

| Cash at the beginning of period | 131,182 | 3,142,650 | ||||||

| Cash at the end of period | $ | 4,473,000 | $ | 119,667 | ||||

| Supplemental information | ||||||||

| Income taxes paid | $ | - | $ | 38,498 | ||||

| Non-cash transactions of operating and investing activities | ||||||||

| Transfer of prepayment to intangible asset | $ | - | $ | 218,678 | ||||

| Initial recognition of right-of-use assets and lease liabilities | $ | - | $ | 462,361 | ||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

4

SINO-GLOBAL SHIPPING AMERICA, LTD. AND AFFILIATES

NOTES TO THE CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

Note 1. ORGANIZATION AND NATURE OF BUSINESS

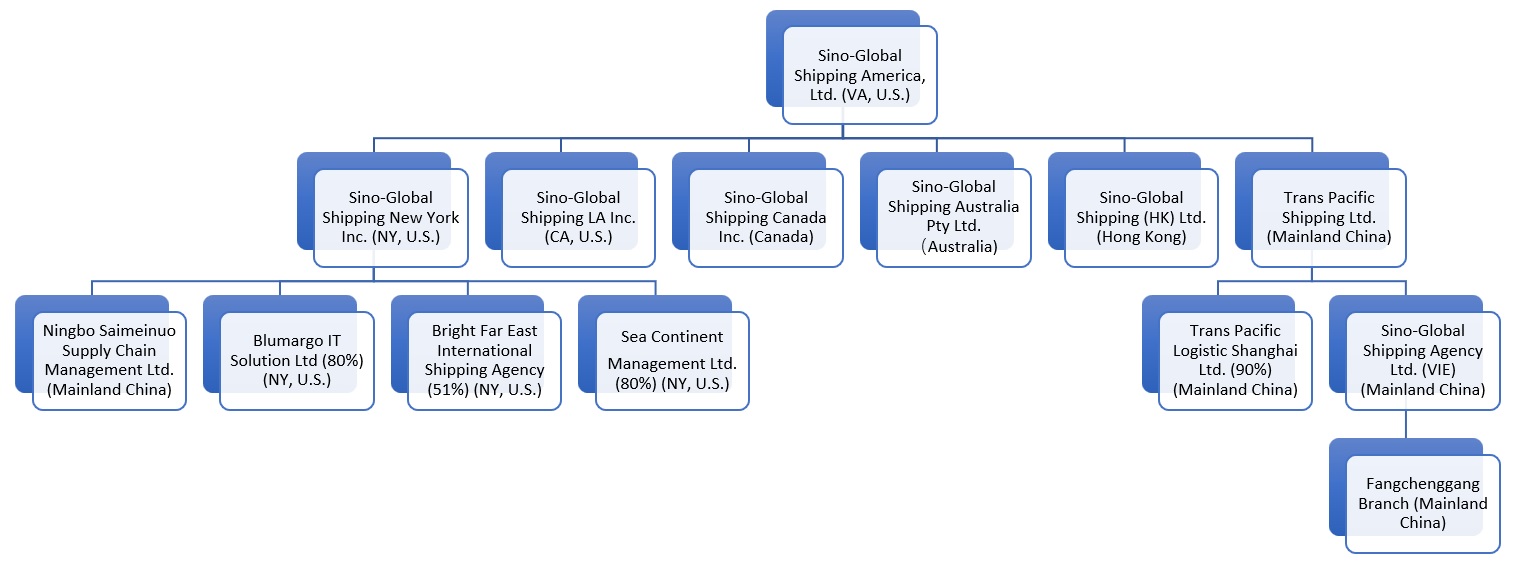

Founded in the United States (the “U.S.”) in 2001, Sino-Global Shipping America, Ltd., a Virginia corporation (“Sino-Global” or the “Company”), is a global shipping and freight logistics integrated solution provider. The Company provides tailored solutions and value-added services to its customers to drive efficiency and control in related steps throughout the entire shipping and freight logistics chain. The Company conducts its business primarily through its wholly-owned subsidiaries in the People’s Republic of China (the “PRC” or “China”) (including Hong Kong) and the U.S. where a majority of the Company’s clients are located.

The Company operates in three operating segments including (1) shipping agency and management services, which are operated by its subsidiary in the U.S.; (2) freight logistics services, which are operated by its subsidiary in the PRC; (3) container trucking services, which are operated by its subsidiary in the U.S.

The outbreak of the novel coronavirus (COVID-19) starting from late January 2020 in the PRC has spread rapidly to many parts of the world. In March 2020, the World Health Organization declared the COVID-19 as a pandemic and has resulted in quarantines, travel restrictions, and the temporary closure of stores and business facilities in China and the U.S. for the past few months. Given the rapidly expanding nature of the COVID-19 pandemic, and because substantially all of the Company’s business operations and its workforce are concentrated in China and the U.S., the Company’s business, results of operations, and financial condition have been adversely affected for the six months ended December 31, 2020. The situation remains highly uncertain for any further outbreak or resurgence of the COVID-19. It is therefore difficult for the Company to estimate the impact on the business or operating results that might be adversely affected by any further outbreak or resurgence of COVID-19.

After the close of the stock market on July 7, 2020, the Company effected a l-for-5 reverse stock split of its common stock in order to satisfy continued listing requirements of its common stock on the NASDAQ Capital Market. The reverse stock split was approved by the Company’s board of directors and stockholders and was intended to allow the Company to meet the minimum share price requirement of $1.00 per share for continued listing on the NASDAQ Capital Market. As a result all common stock share amounts included in this filing have been retroactively reduced by a factor of five, and all common stock per share amounts have been increased by a factor of five. Amounts affected include common stock outstanding, including those that have resulted from the stock options, and warrants that convert to common stock.

On December 14, 2020, the Company incorporated a new entity named “Blumargo IT Solution Ltd.” with 80% ownership in partner with Tianjin Anboweiye Technology Co. to build up hi-tech and information-based logistic services enhance to meet the higher and complicate demand of customers.

Note 2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(a) Basis of Presentation

The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with generally accepted accounting principles in the United States of America (“US GAAP”) pursuant to the rules and regulations of the Securities and Exchange Commission (“SEC”). The unaudited condensed consolidated financial statements include the accounts of the Company and include the assets, liabilities, revenues and expenses of the subsidiaries and VIEs. All intercompany transactions and balances have been eliminated in consolidation.

5

Sino-Global Shipping Agency Ltd., a PRC corporation (“Sino-China”), is considered a variable interest entity (“VIE”), with the Company as the primary beneficiary. The Company, through Trans Pacific Shipping Ltd., entered into certain agreements with Sino-China, pursuant to which the Company receives 90% of Sino-China’s net income. Sino-China was designed to operate in China for the benefit of the Company. The Company does not receive any payment from Sino-China unless Sino-China recognizes net income during its fiscal year. These agreements do not entitle the Company to any consideration if Sino-China incurs a net loss during its fiscal year. If Sino-China incurs a net loss during its fiscal year, the Company is not required to absorb such net loss.

As a VIE, Sino-China’s revenues are included in the Company’s total revenues, and any income/loss from operations is consolidated with that of the Company. Because of contractual arrangements between the Company and Sino-China, the Company has a pecuniary interest in Sino-China that requires consolidation of the financial statements of the Company and Sino-China.

The Company has consolidated Sino-China’s operating results in accordance with Accounting Standards Codification (“ASC”) 810-10, “Consolidation”. The agency relationship between the Company and Sino-China and its branches is governed by a series of contractual arrangements pursuant to which the Company has substantial control over Sino-China. Management makes ongoing reassessments of whether the Company remains the primary beneficiary of Sino-China.

The carrying amount and classification of Sino-China’s assets and liabilities included in the Company’s unaudited condensed consolidated balance sheets were as follows:

| December 31, | June 30, | |||||||

| 2020 | 2020 | |||||||

| Current assets: | ||||||||

| Cash | $ | 5,183 | $ | 5,022 | ||||

| Total current assets | 5,183 | 5,022 | ||||||

| Deposits | 1,740 | 1,608 | ||||||

| Property and equipment, net | 37,241 | 41,171 | ||||||

| Total assets | $ | 44,164 | $ | 47,801 | ||||

| Current liabilities: | ||||||||

| Other payables and accrued liabilities | $ | 43,406 | $ | 39,919 | ||||

| Total liabilities | $ | 43,406 | $ | 39,919 | ||||

(b) Fair Value of Financial Instruments

The Company follows the provisions of ASC 820, Fair Value Measurements and Disclosures, which clarifies the definition of fair value, prescribes methods for measuring fair value, and establishes a fair value hierarchy to classify the inputs used in measuring fair value as follows:

Level 1 — Observable inputs such as unadjusted quoted prices in active markets for identical assets or liabilities available at the measurement date.

Level 2 — Inputs other than quoted prices that are observable for the asset or liability in active markets, quoted prices for identical or similar assets and liabilities in markets that are not active, inputs other than quoted prices that are observable, and inputs derived from or corroborated by observable market data.

Level 3 — Unobservable inputs that reflect management’s assumptions based on the best available information.

The carrying value of accounts receivable, other receivables, other current assets, and current liabilities approximate their fair values because of the short-term nature of these instruments.

6

(c) Use of Estimates and Assumptions

The preparation of the Company’s unaudited condensed consolidated financial statements in conformity with US GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the dates of the financial statements and the reported amounts of revenues and expenses during the reporting periods. Estimates are adjusted to reflect actual experience when necessary. Significant accounting estimates reflected in the Company’s unaudited condensed consolidated financial statements include revenue recognition, fair value of stock based compensation, cost of revenues, allowance for doubtful accounts, impairment loss, deferred income taxes, income tax expense and the useful lives of property and equipment. The inputs into the Company’s judgments and estimates consider the economic implications of COVID-19 on the Company’s critical and significant accounting estimates. Since the use of estimates is an integral component of the financial reporting process, actual results could differ from those estimates.

(d) Translation of Foreign Currency

The accounts of the Company and its subsidiaries are measured using the currency of the primary economic environment in which the entity operates (the “functional currency”). The Company’s functional currency is the U.S. dollar (“USD”) while its subsidiaries in the PRC, including Sino-China, Trans Pacific Shipping Ltd. and Trans Pacific Logistic Shanghai Ltd. report their financial positions and results of operations in Renminbi (“RMB”), its subsidiary Sino-Global Shipping Australia Pty Ltd., reports its financial positions and results of operations in Australian dollar (“AUD”), its subsidiary Sino-Global Shipping Hong Kong reports its financial positions and results of operations in Hong Kong dollar (“HKD”) and its subsidiary Sino-Global Shipping Canada, Inc. reports its financial positions and results of operations in Canadian Dollar (“CAD”). The accompanying unaudited condensed consolidated financial statements are presented in USD. Foreign currency transactions are translated into USD using the fixed exchange rates in effect at the time of the transaction. Generally, foreign exchange gains and losses resulting from the settlement of such transactions are recognized in the consolidated statements of operations. The Company translates the foreign currency financial statements in accordance with ASC 830-10, “Foreign Currency Matters”. Assets and liabilities are translated at current exchange rates quoted by the People’s Bank of China at the balance sheets’ dates and revenues and expenses are translated at average exchange rates in effect during the year. The resulting translation adjustments are recorded as other comprehensive loss and accumulated other comprehensive loss as a separate component of equity of the Company, and also included in non-controlling interests.

The exchange rates as of December 31, 2020 and June 30, 2020 and for the three and six months ended December 31, 2020 and 2019 are as follows:

| December 31, 2020 | June 30, 2020 | Three months ended December 31, | Six months ended December 31, | |||||||||||||||||||||

| Foreign currency | Balance Sheet | Balance Sheet | 2020 Profits/Loss | 2019 Profits/Loss | 2020 Profits/Loss | 2019 Profits/Loss | ||||||||||||||||||

| RMB:1USD | 6.5286 | 7.0651 | 6.6254 | 7.0446 | 6.7736 | 7.0296 | ||||||||||||||||||

| AUD:1USD | 1.2974 | 1.4514 | 1.3688 | 1.4630 | 1.3840 | 1.4611 | ||||||||||||||||||

| HKD:1USD | 7.7536 | 7.7505 | 7.7520 | 7.8256 | 7.7513 | 7.8278 | ||||||||||||||||||

| CAD:1USD | 1.2754 | 1.3617 | 1.3038 | 1.3200 | 1.3181 | 1.3200 | ||||||||||||||||||

(e) Cash

Cash consists of cash on hand and cash in bank which are unrestricted as to withdrawal or use. The Company maintains cash with various financial institutions mainly in the PRC, Australia, Hong Kong, Canada and the U.S. As of December 31, 2020 and June 30, 2020, cash balances of $4,462,063 and $126,720, respectively, were maintained at financial institutions. In China, the deposit insurance system only insured each depositor at one bank for a maximum of approximately $70,000 (RMB 500,000). For the balance maintained at U.S. financial institutions, the Federal Deposit Insurance Corporation as it only insured deposits up to $250,000. The Hong Kong Deposit Protection Board pays compensation up to a limit of HKD 500,000 (approximately $64,000) if the bank with which an individual/a company holds its eligible deposit fails. As of December 31, 2020 and June 30, 2020, amount of deposits the Company had not covered by insurance amounted to $3,881,953 and $8,780, respectively.

7

(f) Receivables and Allowance for Doubtful Accounts

Accounts receivable are presented at net realizable value. The Company maintains allowances for doubtful accounts and for estimated losses. The Company reviews the accounts receivable on a periodic basis and makes general and specific allowances when there is doubt as to the collectability of individual receivable balances. In evaluating the collectability of individual receivable balances, the Company considers many factors, including the age of the balances, customers’ historical payment history, their current credit-worthiness and current economic trends. Receivables are generally considered past due after 180 days. The Company reserves 25%-50% of the customers balance aged between 181 days to 1 year, 50%-100% of the customers balance over 1 year and 100% of the customers balance over 2 years. Accounts receivable are written off against the allowances only after exhaustive collection efforts. As the Company has focused its development in the shipping management segment, its customer base will be more from smaller privately owned companies that will pay more timely than state owned companies. The Company also considers the economic implications of COVID-19 on its estimates of the allowance and made additional $2,609 and $258,561 of allowance for doubtful accounts of accounts receivable for the three months ended December 31, 2020 and 2019, $33,418 and $1,282,492 of allowance for doubtful accounts of accounts receivable for the six months ended December 31, 2020 and 2019. The Company recovered nil and $22,869 of accounts receivable for the three months ended December 31, 2020 and 2019, respectively. The Company recovered $2,456 and $22,869 of accounts receivable for the six months ended December 31, 2020 and 2019, respectively. For the three and six months ended December 31, 2019 the Company wrote off nil and $99,366. There was no write off for the three and six months ended December 31, 2020.

Other receivables represent mainly customer advances, prepaid employee insurance and welfare benefits, which will be subsequently deducted from the employee payroll, guarantee deposits on behalf of ship owners as well as office lease deposits. Management reviews its receivables on a regular basis to determine if the bad debt allowance is adequate, and adjusts the allowance when necessary. Delinquent account balances are written-off against allowance for doubtful accounts after management has determined that the likelihood of collection is not probable. Other receivables are written off against the allowances only after exhaustive collection efforts. The Company made $11,673 allowance for doubtful accounts of other receivables for the three and six months ended December 31, 2020. There was no allowance of other receivables for the three and six months ended December 31, 2019. For the three and six months ended December 31, 2020, $11,673 was written off against other receivables. For the three and six months ended December 31, 2019, nil and $1,763 was written off against other receivables, respectively. The Company recovered $30,173 of other receivables for the three and six months ended December 31, 2020. There was no recovery against other receivables for the three and six months ended December 31, 2019.

(g) Property and Equipment, net

Property and equipment are stated at historical cost less accumulated depreciation. Historical cost comprises its purchase price and any directly attributable costs of bringing the assets to its working condition and location for its intended use. Depreciation is calculated on a straight-line basis over the following estimated useful lives:

| Buildings | 20 years |

| Motor vehicles | 3-10 years |

| Computer and office equipment | 1-5 years |

| Furniture and fixtures | 3-5 years |

| System software | 5 years |

| Leasehold improvements | Shorter of lease term or useful lives |

The carrying value of a long-lived asset is considered impaired by the Company when the anticipated undiscounted cash flows from such asset is less than its carrying value. If impairment is identified, a loss is recognized based on the amount by which the carrying value exceeds the fair value of the long-lived asset. Fair value is determined primarily using the anticipated cash flows discounted at a rate commensurate with the risk involved or based on independent appraisals. There was no impairment for the three months ended December 31, 2020 and 2019. For the six months ended December 31, 2020 and 2019, an impairment of nil and $127,177 were recorded, respectively.

8

(h) Intangible Assets, net

Intangible assets are recorded at cost less accumulated amortization. Amortization is calculated on a straight-line basis over the following estimated useful lives:

| Logistics platform | 3 years |

The Company evaluates intangible assets for impairment whenever events or changes in circumstances indicate that the assets might be impaired. There was no impairment for the three months ended December 31, 2020 and 2019. For the six months ended December 31, 2020 and 2019, an impairment of nil and $200,455 were recorded, respectively.

(i) Revenue Recognition

The Company recognizes revenue which represents the transfer of goods and services to customers in an amount that reflects the consideration to which the Company expects to be entitled in such exchange. The Company identifies contractual performance obligations and determines whether revenue should be recognized at a point in time or over time, based on when control of goods and services transfers to a customer. The Company’s revenue streams are recognized at a point in time.

The Company uses a five-step model to recognize revenue from customer contracts. The five-step model requires that the Company (i) identify the contract with the customer, (ii) identify the performance obligations in the contract, (iii) determine the transaction price, including variable consideration to the extent that it is probable that a significant future reversal will not occur, (iv) allocate the transaction price to the respective performance obligations in the contract, and (v) recognize revenue when (or as) the Company satisfies the performance obligation.

The Company continues to derive its revenues from sales contracts with its customers with revenues being recognized upon performance of services. Persuasive evidence of an arrangement is demonstrated via sales contract and invoice; and the sales price to the customer is fixed upon acceptance of the sales contract and there is no separate sales rebate, discount, or other incentive. The Company’s revenues are recognized at a point in time after all performance obligations are satisfied.

Contract balances

The Company records receivables related to revenue when the Company has an unconditional right to invoice and receive payment.

Deferred revenue consists primarily of customer billings made in advance of performance obligations being satisfied and revenue being recognized.

The Company’s disaggregated revenue streams are described as follows:

| For the Three Months Ended | For the Six Months Ended | |||||||||||||||

| December 31, | December 31, | December 31, | December 31, | |||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||

| Shipping and management agency services | $ | - | $ | 500,000 | $ | 206,845 | $ | 1,000,000 | ||||||||

| Freight logistics services | 1,884,440 | 1,503,500 | 2,814,394 | 2,745,641 | ||||||||||||

| Container trucking services | - | 17,624 | - | 61,709 | ||||||||||||

| Total | $ | 1,884,440 | $ | 2,021,124 | $ | 3,021,239 | $ | 3,807,350 | ||||||||

| ● | Revenues from shipping and management agency services are recognized upon completion of services, which coincides with the date of departure of the relevant vessel from port. Advance payments and deposits received from customers prior to the provision of services and recognition of the related revenues are presented as deferred revenue. |

9

| ● | Revenues from freight logistics services are recognized when the related contractual services are rendered.

For certain freight logistics contracts that the Company entered into with customers starting in the first quarter of fiscal year 2020, the Company (i) acts as an agent in arranging the relationship between the customer and the third-party service provider and (ii) does not control the services rendered to the customers, revenues related to this contracts are presented net of related costs. For the three months ended December 31, 2019, gross revenue and gross cost of revenue related to these contracts not presented in the table above amounted to approximately $12.9 million and $12.0 million, respectively. For the six months ended December 31, 2019, gross revenue and gross cost of revenue related to these contracts amounted to approximately $22.0 million and $20.5 million, respectively. There was no such transaction for the three and six months ended December 31, 2020. |

| ● | Revenues from container trucking services are recognized when the related contractual services are rendered. |

Disaggregated information of revenues by geographic locations are as follows:

| For the Three Months Ended | For the Six Months Ended | |||||||||||||||

| December 31, | December 31, | December 31, | December 31, | |||||||||||||

| 2020 | 2019 | 2020 | 2019 | |||||||||||||

| PRC | $ | 1,884,440 | 1,503,500 | 2,814,394 | 2,745,641 | |||||||||||

| U.S. | - | 517,624 | 206,845 | 1,061,709 | ||||||||||||

| Total revenues | $ | 1,884,440 | $ | 2,021,124 | $ | 3,021,239 | $ | 3,807,350 | ||||||||

(j) Taxation

Because the Company and its subsidiaries and Sino-China were incorporated in different jurisdictions, they file separate income tax returns. The Company uses the asset and liability method of accounting for income taxes in accordance with U.S. GAAP. Deferred taxes, if any, are recognized for the future tax consequences of temporary differences between the tax basis of assets and liabilities and their reported amounts in the unaudited condensed consolidated financial statements. A valuation allowance is provided against deferred tax assets if it is more likely than not that the asset will not be utilized in the future.

The Company recognizes the tax benefit from an uncertain tax position only if it is more likely than not that the tax position will be sustained on examination by the taxing authorities, based on the technical merits of the position. The Company recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense. The Company had no uncertain tax positions as of December 31, 2020 and June 30, 2020.

Income tax returns for the years prior to 2017 are no longer subject to examination by U.S. tax authorities.

PRC Enterprise Income Tax

PRC enterprise income tax is calculated based on taxable income determined under the PRC Generally Accepted Accounting Principles (“PRC GAAP”) at 25%. Sino-China and Trans Pacific are registered in PRC and governed by the Enterprise Income Tax Laws of the PRC.

PRC Value Added Taxes and Surcharges

The Company is subject to value added tax (“VAT”). Revenue from services provided by the Company’s PRC subsidiaries and affiliates, including Sino-China and Trans Pacific are subject to VAT at rates ranging from 9% to 13%. Entities that are VAT general taxpayers are allowed to offset qualified VAT paid to suppliers against their VAT liability. Net VAT liability is recorded in taxes payable on the unaudited condensed consolidated balance sheets.

10

In addition, under the PRC regulations, the Company’s PRC subsidiaries and affiliates are required to pay the city construction tax (7%) and education surcharges (3%) based on the net VAT payments.

(k) Earnings (loss) per Share

Basic earnings (loss) per share is computed by dividing net income (loss) attributable to holders of common stock of the Company by the weighted average number of shares of common stock of the Company outstanding during the applicable period. Diluted earnings (loss) per share reflect the potential dilution that could occur if securities or other contracts to issue common stock of the Company were exercised or converted into common stock of the Company. Common stock equivalents are excluded from the computation of diluted earnings per share if their effects would be anti-dilutive.

For the three and six months ended December 31, 2020 and 2019, there was no dilutive effect of potential shares of common stock of the Company because the Company generated a net loss.

(l) Comprehensive Income (Loss)

The Company reports comprehensive income (loss) in accordance with the authoritative guidance issued by Financial Accounting Standards Board (the “FASB”) which establishes standards for reporting comprehensive income (loss) and its component in financial statements. Other comprehensive income (loss) refers to revenue, expenses, gains and losses that under US GAAP are recorded as an element of Stockholders’ equity but are excluded from net income. Other comprehensive income (loss) consists of a foreign currency translation adjustment resulting from the Company not using the U.S. dollar as its functional currencies.

(m) Stock-based Compensation

The Company accounts for stock-based compensation awards to employees in accordance with FASB ASC Topic 718, “Compensation – Stock Compensation”, which requires that stock-based payment transactions with employees be measured based on the grant-date fair value of the equity instrument issued and recognized as compensation expense over the requisite service period. The Company records stock-based compensation expense at fair value on the grant date and recognizes the expense over the employee’s requisite service period.

The Company accounts for stock-based compensation awards to non-employees in accordance with FASB ASC Topic 718 amended by ASU 2018-07. Under FASB ASC Topic 718, stock compensation granted to non-employees has been determined as the fair value of the consideration received or the fair value of equity instrument issued, whichever is more reliably measured and is recognized as an expense as the goods or services are received.

Valuations of stock based compensation are based upon highly subjective assumptions about the future, including stock price volatility and exercise patterns. The fair value of share-based payment awards was estimated using the Black-Scholes option pricing model. Expected volatilities are based on the historical volatility of the Company’s stock. The Company uses historical data to estimate option exercise and employee terminations. The expected term of options granted represents the period of time that options granted are expected to be outstanding. The risk-free rate for periods within the expected life of the option is based on the U.S. Treasury yield curve in effect at the time of the grant.

(n) Risks and Uncertainties

The Company’s business, financial position and results of operations may be influenced by the political, economic, health and legal environments in the PRC, as well as by the general state of the PRC economy. The Company’s operations in the PRC are subject to special considerations and significant risks not typically associated with companies in North America and Western Europe. These include risks associated with, among others, the political, economic, health and legal environments and foreign currency exchange. The Company’s results may be adversely affected by changes in the political, regulatory and social conditions in the PRC, and by changes in governmental policies or interpretations with respect to laws and regulations, anti-inflationary measures, currency conversion, remittances abroad, and rates and methods of taxation, among other things.

11

In March 2020, the World Health Organization declared the COVID-19 as a pandemic. Given the rapidly expanding nature of the COVID-19 pandemic, and because substantially all of the Company’s business operations and the workforce are concentrated in China and United States, the Company’s business, results of operations, and financial condition have been adversely affected for the three months ended September 30, 2020. The situation remains highly uncertain for any further outbreak or resurgence of the COVID-19. It is therefore difficult for the Company to estimate the impact on the business or operating results that might be adversely affected by any further outbreak or resurgence of COVID-19.

(o) Liquidity

In assessing the Company’s liquidity, the Company monitors and analyzes its cash on-hand and its operating and capital expenditure commitments. The Company’s liquidity needs are to meet its working capital requirements, operating expenses and capital expenditure obligations. As of December 31, 2020, the Company’s working capital was approximately $1.1 million and the Company had cash of approximately $4.5 million. The Company believes its revenues and operations will continue to grow and the current working capital is sufficient to support its operations and debt obligations as they become due one year through report date.

The Company expects to realize the balance of its current assets within the normal operating cycle of a twelve month period. If the Company is unable to realize its current assets within the normal operating cycle of a twelve month period, the Company had considered supplementing its available sources of funds through the following sources:

| ● | the Company will continuously seek equity financing to support its working capital. On January 27, 2021, the Company entered into a securities purchase agreement with the non-U.S. persons to purchase 1,086,956 shares at a per share purchase price of $3.68 for aggregate proceeds of approximately $4.0 million. The Company has received the full amount of payment in January 2021. On February 6, 2021, the Company entered into a securities purchase agreement with the investors to purchase an aggregate of 1,998,500 shares at a per share purchase price of $6.805 for aggregate net proceeds of approximately $12.3 million after deducting estimated offering expenses and placement agent fees. The Company has received the full amount of payment in February 2021. On February 9, 2021, the Company entered into a securities purchase agreement with the investors to purchase an aggregate of 3,655,000 shares at a per share purchase price of $7.80 for aggregate net proceeds of approximately $26.2 million after deducting estimated offering expenses and placement agent fees. The Company has received the full amount of payment in February 2021; | |

| ● | other available sources of financing from PRC banks and other financial institutions; and | |

| ● | financial support and credit guarantee commitments from the Company’s shareholders and directors. |

Based on the above considerations, the Company’s management is of the opinion that it has sufficient funds to meet the Company’s future liquidity requirements for at least twelve months from issuance of these unaudited condensed consolidated financial statements.

(p) Recent Accounting Pronouncements

Pronouncements adopted

In August 2018, the FASB issued ASU 2018-13, “Fair Value Measurement (Topic 820): Disclosure Framework—Changes to the Disclosure Requirements for Fair Value Measurement” (“ASU 2018-13”). ASU 2018-13 removes, modifies and adds certain disclosure requirements in Topic 820 “Fair Value Measurement”. ASU 2018-13 eliminates certain disclosures related to transfers and the valuations process, modifies disclosures for investments that are valued based on net asset value, clarifies the measurement uncertainty disclosure, and requires additional disclosures for Level 3 fair value measurements. The Company adopted this ASU on July 1, 2020 and the adoption has no significant impact to the Company’s unaudited condensed consolidated financial statements as a whole.

Pronouncements not yet adopted

In May 2019, the FASB issued ASU 2019-05, which is an update to ASU Update No. 2016-13, Financial Instruments—Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments, which introduced the expected credit losses methodology for the measurement of credit losses on financial assets measured at amortized cost basis, replacing the previous incurred loss methodology. The amendments in Update 2016-13 added Topic 326, Financial Instruments—Credit Losses, and made several consequential amendments to the Codification. Update 2016-13 also modified the accounting for available-for-sale debt securities, which must be individually assessed for credit losses when fair value is less than the amortized cost basis, in accordance with Subtopic 326-30, Financial Instruments— Credit Losses—Available-for-Sale Debt Securities. The amendments in this ASU address those stakeholders’ concerns by providing an option to irrevocably elect the fair value option for certain financial assets previously measured at amortized cost basis. For those entities, the targeted transition relief will increase comparability of financial statement information by providing an option to align measurement methodologies for similar financial assets. Furthermore, the targeted transition relief also may reduce the costs for some entities to comply with the amendments in Update 2016-13 while still providing financial statement users with decision-useful information. In November 2019, the FASB issued ASU No. 2019-10, which to update the effective date of ASU No. 2016-13 for private companies, not-for-profit organizations and certain smaller reporting companies applying for credit losses standard. The new effective date for these preparers is for fiscal years beginning after July 1, 2023, including interim periods within those fiscal years. The Company has not early adopted this update and it will become effective on July 1, 2023 assuming the Company will remain eligible to be smaller reporting company. The Company is currently evaluating the impact of this new standard on Company’s unaudited condensed consolidated financial statements and related disclosures.

12

In December 2019, the FASB issued ASU 2019-12, “Income Taxes (Topic 740): Simplifying the Accounting for Income Taxes”. The amendments in this Update simplify the accounting for income taxes by removing certain exceptions to the general principles in Topic 740. The amendments also improve consistent application of and simplify GAAP for other areas of Topic 740 by clarifying and amending existing guidance. ASU 2019-12 is effective for the Company for annual and interim reporting periods beginning July 1, 2021. Early adoption of the amendments is permitted, including adoption in any interim period for public business entities for periods for which financial statements have not yet been issued. An entity that elects to early adopt the amendments in an interim period should reflect any adjustments as of the beginning of the annual period that includes that interim period. Additionally, an entity that elects early adoption must adopt all the amendments in the same period. The Company is currently evaluating the impact of this new standard on Company’s unaudited condensed consolidated financial statements and related disclosures.

In August 2020, the FASB issued ASU 2020-06, “Debt—Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging—Contracts in Entity’s Own Equity (Subtopic 815-40): Accounting for Convertible Instruments and Contracts in an Entity’s Own Equity”. The amendments in this Update to address issues identified as a result of the complexity associated with applying generally accepted accounting principles for certain financial instruments with characteristics of liabilities and equity. ASU 2020-06 is effective for the Company for annual and interim reporting periods beginning July 1, 2022. Early adoption is permitted, but no earlier than fiscal years beginning after July 1, 2021, including interim periods within those fiscal years. An entity that elects to early adopt the amendments in an interim period should reflect any adjustments as of the beginning of the annual period that includes that interim period. The Company is currently evaluating the impact of this new standard on Company’s unaudited condensed consolidated financial statements and related disclosures.

In October 2020, the FASB issued ASU 2020-08, “Codification Improvements to Subtopic 310-20, Receivables—Nonrefundable Fees and Other Costs”. The amendments in this Update represent changes to clarify the Codification. The amendments make the Codification easier to understand and easier to apply by eliminating inconsistencies and providing clarifications. ASU 2020-08 is effective for the Company for annual and interim reporting periods beginning July 1, 2021. Early application is not permitted. All entities should apply the amendments in this Update on a prospective basis as of the beginning of the period of adoption for existing or newly purchased callable debt securities. These amendments do not change the effective dates for Update 2017-08. The Company is currently evaluating the impact of this new standard on Company’s unaudited condensed consolidated financial statements and related disclosures.

The Company does not believe other recently issued but not yet effective accounting standards, if currently adopted, would have a material effect on the Company’s unaudited condensed consolidated financial statements.

Note 3. ACCOUNTS RECEIVABLE, NET

The Company’s net accounts receivable are as follows:

| December 31, | June 30, | |||||||

| 2020 | 2020 | |||||||

| Trade accounts receivable | $ | 3,720,087 | $ | 3,453,439 | ||||

| Less: allowances for doubtful accounts | (2,457,949 | ) | (2,297,491 | ) | ||||

| Accounts receivable, net | $ | 1,262,138 | $ | 1,155,948 | ||||

13

Movement of allowance for doubtful accounts are as follows:

| December 31, 2020 | June 30, 2020 | |||||||

| Beginning balance | $ | 2,297,491 | $ | 5,670,274 | ||||

| Provision for doubtful accounts, net of recovery | 30,962 | 4,896,640 | ||||||

| Less: write-off | - | (8,220,754 | ) | |||||

| Exchange rate effect | 129,496 | (48,669 | ) | |||||

| Ending balance | $ | 2,457,949 | $ | 2,297,491 | ||||

For the three months ended December 31, 2020 and 2019, the provision for doubtful accounts was $2,609 and $258,561, respectively. For the six months ended December 31, 2020 and 2019, the provision for doubtful accounts was $33,418 and $1,282,492, respectively. The Company recovered $2,456 and $76,497 of accounts receivable for the six months ended December 31, 2020 and 2019, respectively.

Note 4. OTHER RECEIVABLES, NET

The Company’s other receivables are as follows:

| December 31, | June 30, | |||||||

| 2020 | 2020 | |||||||

| Advances to customers* | $ | 11,375,759 | $ | 10,004,893 | ||||

| Employee business advances | 4,241 | 51,334 | ||||||

| Total | 11,380,000 | 10,056,227 | ||||||

| Less: allowances for doubtful accounts | (10,796,084 | ) | (10,005,193 | ) | ||||

| Other receivables, net | $ | 583,916 | $ | 51,034 | ||||

| * | As of December 31, 2020 and June 30, 2020, the Company entered into certain contracts with customers (state-owned entities) where the Company’s services included freight costs and cost of commodities to be shipped to customers’ designated locations. The Company prepaid the costs of commodities and recognized as advance payments on behalf of its customers. These advance payments on behalf of the customers will be repaid to the Company when either the contract terms are expired or the contracts are terminated by the Company. As aforementioned customers were negatively impacted by the pandemic and required additional time to execute existing contracts, they required additional time to pay. Due to significant uncertainty on whether the delayed contracts will be executed timely. As such, the Company had provided an allowance due to contract delay and recorded allowances of approximately $11.0 million. On December 31, 2020, the Company entered another contract to advance $580,000 as deposit on behalf of customer and it will be repaid to the Company when the contract is fulfilled. |

Movement of allowance for doubtful accounts are as follows:

| December 31, 2020 | June 30, 2020 | |||||||

| Beginning balance | $ | 10,005,193 | $ | - | ||||

| Provision for doubtful accounts, net of recovery | (18,500 | ) | 10,055,203 | |||||

| Less: write-off | (11,673 | ) | (1,763 | ) | ||||

| Exchange rate effect | 821,064 | (48,247 | ) | |||||

| Ending balance | $ | 10,796,084 | $ | 10,005,193 | ||||

For the three and six months ended December 31, 2020, the provision for doubtful accounts of other receivables was $11,673 with recovery of $30,173. There was no additional allowance or recovery of other receivables for the three and six months ended December 31, 2019. The Company wrote off $11,673 and nil of other receivables for the three months ended December 31, 2020 and 2019, respectively. The Company wrote off $11,673 and $1,763 of other receivables for the six months ended December 31, 2020 and 2019, respectively.

14

Note 5. ADVANCES TO SUPPLIERS

The Company’s advances to suppliers – third parties are as follows:

| December 31, | June 30, | |||||||

| 2020 | 2020 | |||||||

| Freight fees (1) | $ | 80,804 | $ | 48,875 | ||||

| (1) | The advanced freight fee is the Company’s prepayment made for various shipping costs for shipments from January to March 2021. |

Note 6. PREPAID EXPENSES AND OTHER CURRENT ASSETS

The Company’s prepaid expenses and other assets are as follows:

| December 31, | June 30, | |||||||

| 2020 | 2020 | |||||||

| Prepaid income taxes | $ | 11,929 | $ | 48,924 | ||||

| Other (including prepaid professional fees, rent, listing fees) | 51,196 | 41,458 | ||||||

| Total | $ | 63,125 | $ | 90,382 | ||||

Note 7. OTHER LONG-TERM ASSETS - DEPOSITS

The Company’s other long-term assets – deposits are as follows:

| December 31, | June 30, | |||||||

| 2020 | 2020 | |||||||

| Rental and utilities deposits | $ | 56,478 | $ | 64,663 | ||||

| Freight logistics deposits (1) | 3,147,845 | 2,910,327 | ||||||

| Total other long-term assets - deposits | $ | 3,204,323 | $ | 2,974,990 | ||||

| (1) | Certain customers require the Company to pay certain deposits for the security of shipments and merchandise. These deposits are refundable at the end of their respective contract term. Approximately $3.1 million (RMB 20 million) of the balance was paid to BaoSteel Resources Co., Ltd. according to the agreement entered in March 2018. This refundable deposit is to cover any possible loss of merchandise, as well as any non-performance on the part of the Company and its vendors. The restricted deposit is expected be repaid to the Company when either the contract terms are expired by March 2023 or the contract is terminated by the Company. |

15

Note 8. PROPERTY AND EQUIPMENT, NET

The Company’s net property and equipment as follows:

| December 31, | June 30, | |||||||

| 2020 | 2020 | |||||||

| Buildings | $ | 206,174 | $ | 190,518 | ||||

| Motor vehicles* | 561,462 | 516,999 | ||||||

| Computer equipment* | 104,638 | 97,172 | ||||||

| Office equipment* | 47,169 | 43,587 | ||||||

| Furniture and fixtures* | 77,589 | 71,697 | ||||||

| System software* | 116,778 | 107,911 | ||||||

| Leasehold improvements | 851,398 | 786,745 | ||||||

| Total | 1,965,208 | 1,814,629 | ||||||

| Less: Accumulated depreciation and amortization | (1,540,882 | ) | (1,291,339 | ) | ||||

| Property and equipment, net | $ | 424,326 | $ | 523,290 | ||||

Depreciation and amortization expenses for the three months ended December 31, 2020 and 2019 were $70,853 and $66,601, respectively. Depreciation and amortization expenses for the six months ended December 31, 2020 and 2019 were $138,739 and $187,121, respectively.

| * | For the three and six months ended December 31, 2019, an impairment of $127,177 was recorded due to continued decrease in revenues from the inland transportation management segment, no impairment was recorded for same period 2020. |

Note 9. INTANGIBLE ASSETS, NET

Net intangible assets consisted of the following:

| December 31, | June 30, | |||||||

| 2020 | 2020 | |||||||

| Full service logistics platforms | $ | 190,000 | $ | 190,000 | ||||

| Less: Accumulated amortization | (190,000 | ) | (163,611 | ) | ||||

| Intangible assets, net | $ | - | $ | 26,389 | ||||

The full service logistics platform was placed in services in December 2017. The platforms are being amortized over three years. Amortization expenses amounted to $10,556 and $15,833 for the three months ended December 31, 2020 and 2019, respectively. Amortization expenses amounted to $26,389 and $49,890 for the six months ended December 31, 2020 and 2019, respectively.

In addition, first phase of the ERP system was placed in use in July 2019 and is being amortized over three years. However, due to the continued decrease in revenues from the inland transportation management segment, the Company recorded an impairment of $200,455 for the three and six months ended December 31, 2019. No impairment was recorded for same period 2020.

Note 10. ACCRUED EXPENSES AND OTHER CURRENT LIABILITIES

| December 31, | June 30, | |||||||

| 2020 | 2020 | |||||||

| Salary and reimbursement payable | $ | 504,022 | $ | 795,855 | ||||

| Professional fees payable | 345,631 | 629,524 | ||||||

| Credit card payable | 5,535 | 217,940 | ||||||

| Total | $ | 855,188 | $ | 1,643,319 | ||||

16

Note 11. LOANS PAYABLE

On May 11, 2020, the Company received loan proceeds in the amount of approximately $124,570 under the U.S. Small Business Administration (“SBA”) Paycheck Protection Program (“PPP”). The PPP, established as part of the Coronavirus Aid, Relief and Economic Security Act (“CARES Act”), provides for loans to qualifying businesses for amounts up to 2.5 times of the average monthly payroll expenses of the qualifying business. The loans and accrued interest are forgivable after eight weeks (or an extended 24-week covered period) as long as the borrower uses the loan proceeds for eligible purposes, including payroll, benefits, rent and utilities, and maintains its payroll levels. The loan forgiveness amount will be reduced for any Economic Injury Disaster Loan (“EIDL”) advance that the Company receives. The amount of loan forgiveness will be further reduced if the borrower terminates employees or reduces salaries during the eight-week period. The Company intends to use the proceeds for purposes consistent with the PPP. While the Company currently believes that its use of the loan proceeds will meet the conditions for forgiveness of the loan and intends to file for loan forgiveness in fiscal year of 2021, there can be no assurance that the full amount of the loan will be forgiven. As of December 31, 2020, $124,570 of loan payable remains outstanding.

On May 26, 2020, the Company received an advance in the amount of $155,900 from under the SBA EIDL program administered by the SBA pursuant to the CARES Act. Such advance amount will reduce the Company’s PPP loan forgiveness amount described above. In accordance with the requirements of the CARES Act, the Company will use proceeds from the SBA loans primarily for working capital to alleviate economic injury caused by disaster occurring in the month of January 31, 2020 and continuing thereafter. The SBA loans are scheduled to mature on May 22, 2050 and have a 3.75% interest rate and are subject to the terms and conditions applicable to loans administered by the SBA under the CARES Act. The monthly payable including principal and interest, of $731 commencing on May 22, 2021. The balance of principal and interest will be payable 30 years from the date of May 22, 2020. $5,900 of the loan will be forgiven. As of December 31, 2020, $155,900 of loan payable remains outstanding. Interest expense for the three and six months ended December 31, 2020 for this loan was $1,418 and $2,820, respectively.

Loan repayment schedule for the EIDL loans is as follows:

| Twelve Months Ending December 31, | Loan Amount | |||

| 2021 | $ | 7,898 | ||

| 2022 | 3,092 | |||

| 2023 | 3,210 | |||

| 2024 | 3,332 | |||

| 2025 | 3,460 | |||

| Thereafter | 134,908 | |||

| Total loan payments | $ | 155,900 | ||

Note 12. LEASES

The Company determines if a contract contains a lease at inception. US GAAP requires that the Company’s leases be evaluated and classified as operating or finance leases for financial reporting purposes. The classification evaluation begins at the commencement date and the lease term used in the evaluation includes the non-cancellable period for which the Company has the right to use the underlying asset, together with renewal option periods when the exercise of the renewal option is reasonably certain and failure to exercise such option which result in an economic penalty. All of the Company’s leases are classified as operating leases.

The Company has several vehicle lease agreements and office lease agreements with lease terms ranging from two to three years. Upon adoption of ASU 2016-02, the Company recognized lease liabilities of approximately $0.2 million, with corresponding ROU assets of approximately the same amount based on the present value of the future minimum rental payments of leases, using a weighted average discount rate of approximately 9.38%. As of December 31, 2020, ROU assets and lease liabilities amounted to $224,950 and $245,232 (including $166,572 from lease liabilities current portion and $78,660 from lease liabilities noncurrent portion), respectively.

The Company’s lease agreements do not contain any material residual value guarantees or material restrictive covenants. The leases generally do not contain options to extend at the time of expiration and the weighted average remaining lease terms are 1.49 years.

17

For the three months ended December 31, 2020 and 2019, rent expense amounted to approximately $81,000 and $80,000, respectively. For the six months ended December 31, 2020 and 2019, rent expense amounted to approximately $157,000 and $160,000, respectively.

The three-year maturity of the Company’s lease obligations is presented below:

| Twelve Months Ending December 31, | Operating Lease Amount | |||

| 2021 | $ | 181,667 | ||

| 2022 | 81,596 | |||

| Total lease payments | 263,263 | |||

| Less: Interest | (18,031 | ) | ||

| Present value of lease liabilities | $ | 245,232 | ||

Note 13. EQUITY

Stock issuance:

On September 17, 2020, the Company entered into certain securities purchase agreement with certain “non-U.S. Persons” as defined in Regulation S of the Securities Act of 1933, as amended, pursuant to which the Company agreed to sell an aggregate of 720,000 shares of the Company’s common stock, no par value, and warrants to purchase 720,000 Shares at a per share purchase price of $1.46. The net proceeds to the Company from such Offering were approximately $1.05 million. The warrants will be exercisable on March 16, 2021 at an exercise price of $1.825 for cash. The warrants may also be exercised cashlessly if at any time after March 16, 2021, there is no effective registration statement registering, or no current prospectus available for, the resale of the warrant shares. The warrants will expire on March 16, 2026. The warrants are subject to anti-dilution provisions to reflect stock dividends and splits or other similar transactions. The warrants contain a mandatory exercise right for the Company to force exercise the warrants if the Company’s common stock trades at or above $4.38 for 20 consecutive trading days, provided, among other things, that the shares issuable upon exercise of the are registered or may be sold pursuant to Rule 144 and the daily trading volume exceeds 60,000 shares of common stock per trading day on each trading day in a period of 20 consecutive trading days prior to the applicable date.

On November 2 and November 3, 2020, the Company issued an aggregate of 860,000 shares of Series A Convertible Preferred Stock (the “Series A Preferred Stock”), each convertible into one share of common stock, no par value, of Company, upon the terms and subject to the limitations and considerations set forth in the Certificate of Designation of the Series A Preferred Stock, and warrants to purchase up to 1,032,000 shares of common stock. The purchase price for each share of Series A Preferred Stock and accompanying warrants is $1.66. The net proceeds to the Company from this offering was approximately $1.43 million, not including any proceeds that may be received upon cash exercise of the warrants. The warrants will be exercisable six (6) months following the date of issuance at an exercise price of $1.99 for cash. The warrants may also be exercised cashlessly if at any time after the six-month anniversary of the issuance date, there is no effective registration statement registering, or no current prospectus available for, the resale of the warrant Shares. The warrants will expire five and a half (5.5) years from the date of issuance. The warrants are subject to anti-dilution provisions to reflect stock dividends and splits or other similar transactions. The warrants contain a mandatory exercise right for the Company to force exercise of the warrants if the closing price of the common stock equals or exceeds $5.97 for twenty (20) consecutive trading days, provided, among other things, that the shares issuable upon exercise of the warrants are registered or may be sold pursuant to Rule 144 and the daily trading volume exceeds 60,000 shares of common stock per trading day on each trading day in a period of 20 consecutive trading days prior to the applicable date. As of December 31, 2020, the Series A Preferred Stock have not been converted to common stock of the Company.

18

On December 8, 2020, the Company entered into a securities purchase agreement with the investors specified on the signature page thereto pursuant to which the Company agreed to sell to the investors, and the investors agreed to purchase from the Company, in a registered direct offering, an aggregate of 1,560,000 shares of the common stock of the Company, no par value per share, at a purchase price of $3.10 per share, for aggregate gross proceeds to the Company of $4,836,000. The Company also agreed to sell to the Investors warrants to purchase up to an aggregate of 1,170,000 shares of common stock at an exercise price of $3.10 per share. The warrants shall be initially exercisable beginning on December 11, 2020 and expire three and a half (3.5) years from the date of issuance. The exercise price and the number of shares of common stock issuable upon exercise of the warrants are subject to adjustment in the event of stock splits or dividends, or other similar transactions, but not as a result of future securities offerings at lower prices.

The Company’s outstanding warrants are classified as equity since they qualify for exception from derivative accounting as they are considered to be indexed to the Company’s own stock and require net share settlement. The fair value of the warrants were recorded as additional paid-in capital from common stock

Following is a summary of the status of warrants outstanding and exercisable as of December 31, 2020:

| Warrants | Weighted Average Exercise Price | |||||||

| Warrants outstanding, as of June 30, 2020 | 400,000 | $ | 8.75 | |||||

| Issued | 2,922,000 | 2.39 | ||||||

| Exercised | - | - | ||||||

| Expired | - | - | ||||||

| Warrants outstanding, as of December 31, 2020 | 3,322,000 | $ | 3.16 | |||||

| Warrants exercisable, as of December 31, 2020 | 3,322,000 | $ | 3.16 | |||||

| Warrants Outstanding | Warrants Exercisable | Weighted Average Exercise Price | Average Remaining Contractual Life | |||||||

| 2018 Series A, 400,000 | 400,000 | $ | 8.75 | 2.70 years | ||||||

| 2020 warrants, 720,000 | 720,000 | $ | 1.825 | 5.21 years | ||||||

| 2020 warrants, 1,032,000 | 1,032,000 | $ | 1.99 | 5.34 years | ||||||

| 2020 warrants, 1,170,000 | 1,170,000 | $ | 3.10 | 3.44 years | ||||||

On December 9, 2019, the Company authorized the cancellation of the 35,099 of the Company’s treasury shares. The shares were cancelled as of June 30, 2020. The cancellation has no effect on the Company’s total shareholders’ equity and earnings per share.

After the close of the stock market on July 7, 2020, the Company effected a l-for-5 reverse stock split of its common stock in order to satisfy continued listing requirements of its common stock on the NASDAQ Capital Market. The reverse stock split was approved by the Company’s board of directors and stockholders and was intended to allow the company to meet the minimum share price requirement of $1.00 per share for continued listing on the NASDAQ Capital Market. As a result all common stock share amounts included in this filing have been retroactively reduced by a factor of five, and all common stock per share amounts have been increased by a factor of five. Amounts affected include common stock outstanding, including those that have resulted from the stock options, and warrants that convert to common stock.

19

Stock based compensation:

In March 2017, the Company entered into a consulting and advisory services agreement with a consulting entity, which provides management consulting services that include marketing program design and implementation and cooperative partner selection and management. The service period began in March 2017 and will end in February 2020. The Company issued 50,000 shares of common stock as remuneration for the services, which were issued as restricted shares at $12.65 per share on March 22, 2017 to the consultant. These shares were valued at $632,500 and the consulting expense was $52,709 and $105,417 for the three and six months ended December 31, 2019, respectively.

On June 7, 2018, the Company issued 80,000 shares of common stock with a fair value of $508,000 to a consulting entity pursuant to a service agreement. The scope of services primarily covers legal consultation in PRC during the two-year service period from July 2018 to June 2020. The consulting entity is entitled to be granted the common stock on a quarterly basis in eight equal installments. The Company recorded legal expense of $63,500 and $127,000 for the three and six months ended December 31, 2019, respectively.