UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended June 30, 2020

or

☐ TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ___________to ___________

Commission file number 001-34024

Sino-Global

Shipping America, Ltd.

(Exact name of registrant as specified in its charter)

| Virginia | 11-3588546 | |

| (State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification No.) |

1044 Northern Boulevard, Suite 305

Roslyn,

New York 11576-1514

(Address of principal executive offices) (Zip Code)

(718)

888-1814

(Registrant’s telephone number, including area code)

Securities Registered Pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| Common Stock, no par value | SINO | NASDAQ Capital Market |

Securities Registered Pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulations S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☒ | Smaller reporting company | ☒ |

| Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of voting common stock held by non-affiliates of the registrant as of December 31, 2019, the last business day of the registrant’s second fiscal quarter, was approximately $6,479,999.

The number of shares of common stock outstanding as of October 9, 2020 was 4,438,788.

DOCUMENTS INCORPORATED BY REFERENCE:

None.

SINO-GLOBAL SHIPPING AMERICA, LTD.

FORM 10-K

INDEX

i

INTRODUCTION

Unless the context otherwise requires, in this annual report on Form 10-K (this “Report”):

| ● | “We,” “us,” “our,” and “our Company” refer to Sino-Global Shipping America, Ltd., a Virginia company incorporated in April 2001, and all of its direct and indirect consolidated subsidiaries; |

| ● | “Sino-Global” or “Sino” refers to Sino-Global Shipping America, Ltd; |

| ● | “Sino-China” refers to Sino-Global Shipping Agency Ltd., a Chinese legal entity; |

| ● | “Trans Pacific” refers to and relates collectively to Trans Pacific Shipping Ltd., our wholly-owned subsidiary located in China, and Trans Pacific Logistics Shanghai Ltd., 90% of whose equity is owned by Trans Pacific Shipping Ltd.; |

| ● | “Shares” refers to shares of our common stock, without par value per share; |

| ● | “PRC” refers to the People’s Republic of China, excluding, for the purpose of this annual report, Taiwan, Hong Kong and Macau; |

| ● | “US” or “U.S.” refers to United States of America; |

| ● | “HK” refers to Hong Kong; and |

| ● | “RMB” or “Renminbi” refers to the legal currency of China, and “$” or “U.S. dollars” refers to the legal currency of the United States. |

Names of certain PRC companies provided in this Report are translated or transliterated from their original PRC legal names. Discrepancies, if any, in any table between the amounts identified as total amounts and the sum of the amounts listed therein are due to rounding.

ii

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Report contains certain statements that constitute “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Such forward-looking statements, including but not limited to statements regarding our projected growth, trends and strategies, future operating and financial results, financial expectations and current business indicators are based upon current information and expectations and are subject to change based on factors beyond our control. Forward-looking statements typically are identified by the use of terms such as “look,” “may,” “will,” “should,” “might,” “believe,” “plan,” “expect,” “anticipate,” “estimate” and similar words, although some forward-looking statements are expressed differently. The accuracy of such statements may be impacted by a number of business risks and uncertainties we face that could cause our actual results to differ materially from those projected or anticipated, including but not limited to the following:

| ● | Our ability to timely and properly deliver our services among others; |

| ● | Our dependence on a limited number of major customers and related parties; |

| ● | Political and economic factors in China and its relationship with U.S.; |

| ● | Our ability to expand and grow our lines of business; |

| ● | Unanticipated changes in general market conditions or other factors which may result in cancellations or reductions in the need for our services; |

| ● | The effect of terrorist acts, or the threat thereof, on consumer confidence and spending or the production and distribution of product and raw materials which could, as a result, adversely affect our services, operations and financial performance; |

| ● | The acceptance in the marketplace of our new lines of services; |

| ● | The foreign currency exchange rate fluctuations; |

| ● | Hurricanes or other natural disasters; |

| ● | Our ability to identify and successfully execute cost control initiatives; |

| ● | The impact of quotas, tariffs or safeguards on our customer products that we service; |

| ● | Our ability to attract, retain and motivate skilled personnel; or |

| ● | Our expansion and growth into other areas of the shipping industry. |

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. The Company undertakes no obligation to update this forward-looking information. Nonetheless, the Company reserves the right to make such updates from time to time by press release, periodic report or other method of public disclosure without the need for specific reference to this Report. No such update shall be deemed to indicate that other statements not addressed by such update remain correct or create an obligation to provide any other updates.

iii

Overview

Sino-Global Shipping America, Ltd. (“Sino,” the “Company,” or “we”), a Virginia corporation, was founded in the United States (the “U.S.”) in 2001. Sino is a non-asset based global shipping and freight logistics integrated solution provider. Sino provides tailored solutions and value-added services to its customers to drive effectiveness and control in related aspects throughout the entire shipping and freight logistics chain. We operate in four operating segments, including (1) shipping agency and management services, operated by our subsidiary in Hong Kong and the U.S.; (2) inland transportation management services, operated by our subsidiaries in the U.S.; (3) freight logistics services, operated by our subsidiaries in the PRC and the U.S.; and (4) container trucking services, operated by our subsidiaries in the PRC and the U.S.

We conduct our business primarily through our wholly-owned subsidiaries in the People’s Republic of China (the “PRC”) (including Hong Kong) and the U.S., where a majority of our clients are located.

Company Structure

The Company conducts its business primarily through its wholly-owned subsidiaries in the People’s Republic of China (the “PRC”) (including Hong Kong) and the U.S., where a majority of its clients are located.

Our subsidiary in China, Trans Pacific Shipping Limited (“Trans Pacific Beijing”), a wholly owned foreign enterprise, invested in one 90%-owned subsidiary, Trans Pacific Logistics Shanghai Limited (“Trans Pacific Shanghai”. Trans Pacific Beijing and Trans Pacific Shanghai are referred to collectively as “Trans Pacific”). As PRC laws and regulations restrict foreign ownership of local shipping agency service businesses, we provided our shipping agency services in the PRC through Sino-Global Shipping Agency Ltd. (“Sino-China” or “VIE”), a Chinese legal entity, which holds the licenses and permits necessary to operate local shipping agency services in the PRC. Trans Pacific Beijing and Sino-China do not have a parent-subsidiary relationship. Trans Pacific Beijing has contractual arrangements with Sino-China and its shareholders that enable us to substantially control Sino-China. Through Sino-China, we were able to provide local shipping agency services in all commercial ports in the PRC. Sino-China is one of the committee members of China Association of Shipping Agencies & Non-Vessel-Operating Common Carriers (“CASA”). CASA was approved to form by China Ministry of Communications. Sino-China is also our only entity that is qualified to do shipping agency business in China. We keep the VIE to prepare ourselves for the market to turn around.

1

Corporate History and Our Business Segments

Since inception in 2001 and through our fiscal year ended June 30, 2013, our sole business was providing shipping agency services. In general, we provided two types of shipping agency services: loading/discharging services and protective agency services, in which we acted as a general agent to provide value added solutions to our customers. For loading/discharging agency services, we received the total payment from our customers in U.S. dollars and paid the port charges on behalf of our customers in RMB. For protective agency services, we charged a fixed amount as agent fee while customers are responsible for the payment of port costs and expenses. Under these circumstances, we generally required a portion of a customer’s payment in advance and billed the remaining balance within 30 days after the transaction was completed. We believe the most significant factors that directly or indirectly affected our shipping agency service revenues were:

| ● | the number of ship-times to which we provide port loading/discharging services; |

| ● | the size and types of ships we serve; |

| ● | the type of services we provide; |

| ● | the rate of service fees we charge; |

| ● | the number of ports at which we provide services; and |

| ● | the number of customers we serve. |

In January 2016, we expanded our business to freight logistics service to provide import security filing services with U.S. Customs and Department of Homeland Security, on behalf of importers who ship goods into the U.S. and also providing inland transportation services to these importers in the U.S.

In fiscal year 2017, we also expanded into container trucking services as new business sectors to provide related transportation logistics services to customers in the U.S. and in China. We have signed a cooperation agreement with Sino-Trans Guangxi Logistics Co. Ltd. (“Sinotrans”), which is a state-owned enterprise of China, with a service period from July 1, 2017 to December 31, 2020, to provide freight logistics services and container trucking services to them in the U.S. To ensure effective and high-quality services provided to our customers in the U.S., we established a joint venture, ACH Trucking Center Corp., in the third quarter of fiscal 2017 with a U.S. local freight forwarder, Jetta Global Logistics Inc. The joint venture ended in December 2017 and we continue to operate our trucking business through our other subsidiaries. Since ACH Center’s operating revenue was less than 1% of the Company’s consolidated revenue and the termination did not constitute a strategic shift that would have a major effect on the Company’s operations and financial results, the results of operations for ACH Center was not reported as discontinued operations in the financial statements.

As an effort to further diversify our business, in the second quarter of fiscal 2018, we have developed our bulk cargo container services segment. Bulk cargo container shipment refers to using containers to ship commodities that traditionally are shipped by freight cargo. Freight cargo rate is usually lower than that of container freight rate; however, the transit time is much longer and has high minimum quantity requirements. With the Chinese government banning the import of environmental wastes by the end of 2017, the empty container rate of COSCO Group's container shipping from the United States to China has been further reduced. Therefore with the signing of a strategic cooperation agreement COSCO Shipping Beijing International Freight Co., Ltd., we are able to take advantage of the low container rate to jointly promote bulk cargo container transportation. Revenue from bulk cargo container services amounted to $638,227 for the fiscal 2018 while we didn’t have such business in 2017. We temporarily suspended to provide this service in fiscal year 2019 due to market environment factors in 2019 and have continued this suspension in light of the worldwide impact of the coronavirus pandemic.

In the first quarter of fiscal 2018, we established a wholly-owned subsidiary, Ningbo Saimeinuo Supply Chain Management Ltd. which primarily engages in transportation management and freight logistics services.

Starting with fiscal year 2019, current trade dynamics have made it more expensive for shipping carrier clients to cost-effectively move cargo into U.S. ports, and as a result, we realized a lower shipping volumes and less utilization of its online platform, which has caused us to shift our focus back to shipping agency business. The shipping agency industry in China has improved and the number of shipping agencies in overall in the country has decreased, due to both price and the inability of competitors to embrace technology as a resource in serving client needs.

2

On September 3, 2018, the Company entered into a cooperation agreement with Ningbo Far-East Universal Shipping Agency Co., Ltd to set up a joint venture in Hong Kong named Bright Far East International Shipping Agency Co., Ltd., to engage in worldwide shipping agency operations. The Company has a 51% equity interest in the joint venture. On May 23, 2019, Bright Far East International Shipping Agency Co., Ltd. was incorporated in New York and its registration in Hong Kong was terminated. There have been no major operations of the joint venture for the year ended June 30, 2020. Currently, we are conducting the shipping agency business through our wholly-owned Hong Kong subsidiary.

On April 10, 2019, the Company entered into a cooperation agreement with Mr. Weijun Qin, the Chief Executive Officer of a shipping management company in China, to set up a joint venture in New York named State Priests Management Ltd. (“State Priests”), in which the Company will hold a 20% equity interest. On July 26, 2019, the Company signed a revised cooperation agreement with Mr. Weijun Qin, which changed the Company’s equity interest in State Priests from 20% to 90%. The Company has not provided any cash contribution to the joint venture and there has been no operation of the joint venture pending the International Ship Safety Management Certificate from the China Classification Society (the “Certificate”). As of the date of this filing, the Company has not yet received the Certificate. Sino-Global Shipping New York Inc. started providing shipping management related services that do not require certification, which include arranging and coordinating for ship maintenance and inspection this quarter.

On November 6, 2019, the Company signed a revised cooperation agreement with Mr. Weijun Qin to restructure their equity interest in State Priests. Given that State Priests failed to timely obtain the necessary approval from related authorities, Mr. Weijun Qin agreed to exchange 80% equity interest in Sea Continent Management Ltd. (“Sea Continent”), another New York entity Mr. Qin owns for the Company’s 90% equity interest in State Priests. The equity transfer has been consummated. Sea Continent already has the Certificate but has no operations as of June 30, 2020. There has been no capital injection nor operations of State Priests and Sea Continent as of June 30, 2020; therefore, no gain or loss has been recognized in the transaction.

On January 10, 2020, the Company entered into a cooperation agreement with Mr. Shanming Liang, a shareholder of the Company, to set up a joint venture in New York named LSM Trading Ltd., in which the Company holds a 40% equity interest. No investment has been made by the Company as of the date of this report. The new joint venture will facilitate the purchase agricultural related commodities in the U.S. for customers in China and the Company will provide comprehensive supply chain and logistics solutions.

On April 6, 2020, the Company entered into a share purchase agreement with Mr. Kelin Wu and Mandarine Ocean Ltd (“Mandarine”), a shipping company registered in the Marshall Islands, to purchase 75% of the equity of Mandarine from Mr. Wu for a purchase price of up to USD 3,750,000, payable in cash equivalent and/or restricted shares of common stock of the Company. On June 17, 2020, the parties amended the stock purchase agreement to reduce the purchase price and related changes to be up to USD 1,500,000. On September 3, 2020, the Company and Mr. Wu signed a termination agreement to terminate the amended stock purchase agreement. Neither party owes the other party any termination penalty in connection with the termination. The transfer of equity and issuance of stock contemplated in the amended stock purchase agreement have not occurred and no party has any obligation to transfer or to pay any amount to any other party under the Amendment.

After the close of the stock market on July 7, 2020, the Company effected a l-for-5 reverse stock split of its common stock to maintain its listing of its common stock on the NASDAQ Capital Market. As a result all common stock share amounts included in this filing have been retroactively reduced by a factor of five, and all common stock per share amounts have been increased by a factor of five. Amounts affected include common stock outstanding, including those that have resulted from the stock options, and warrants that convert to common stock.

On September 17, 2020, the Company entered into a securities purchase agreement with certain “non-U.S. Persons” as defined in Regulation S of the Securities Act of 1933, as amended, pursuant to which the Company agreed to sell an aggregate of 720,000 shares of the Common Stock, and warrants to purchase 720,000 shares of Common Stock at a per share purchase price of $1.46. The offering closed on September 23, 2020. The net proceeds to the Company from such offering were approximately $1.05 million.

3

The outbreak of the novel coronavirus (COVID-19) starting from late January 2020 in the PRC has spread rapidly to many parts of the world. In March 2020, the World Health Organization declared the COVID-19 as a pandemic and has resulted in quarantines, travel restrictions, and the temporary closure of stores and business facilities in China and the U.S. for the past few months. Given the rapidly expanding nature of the COVID-19 pandemic, and because substantially all of the Company’s business operations and its workforce are concentrated in China and the U.S., the Company’s business, results of operations, and financial condition have been adversely affected for the year ended June 30, 2020.

Our Strategy

Our strategy is to:

| ● | Provide better solutions for issues and challenges faced by the entire shipping and freight logistics chain to better serve our customers and explore additional growth avenues. |

| ● | Diversify our current service offerings organically or through acquisitions and/or strategic alliance; continue to grow our business in the U.S. market; |

| ● | Continue to streamline our business practice, optimize our cost structure and improve our operating efficiency through effective planning, budgeting, execution and cost control and strengthening our IT infrastructure; |

| ● | Continue to reduce our dependency on our legacy business and few key customers; and |

| ● | Continue to monetize our relationships with our strategic partners and leverage their support and our innovation to expand our business. |

With the establishment of our subsidiary in Los Angeles, we added cargo forwarding services to our service platform in the second quarter of fiscal 2017, which is included in our inland transportation business line for the year ended June 30, 2016. As we are developing our cargo forwarding services, the Company provides freight logistics services and container trucking services as two new business segments in fiscal 2017. During fiscal year 2018, the Company began to provide bulk cargo container services to the customers. On November 13, 2019, the Company entered into a cooperation agreement with Shanming Liang, a director of Guangxi Jinqiao Industrial Group Co., Ltd., to cooperate and expand the bulk cargo container services business.

Our Goals and Strategic Plan

By leveraging our fine reputation, extensive business relationships, technical ability and in-depth knowledge of the shipping industry, our goal is to further strengthen our position as a leading global logistics solution provider who offers innovative resolutions to better address complex issues in different aspects in the entire shipping and freight logistics chain.

We historically focused our business on providing our customers with customized shipping agency services. In the past, our business came predominately from our strong business relationships with our key strategic partners in China. To reduce our dependency on a single business line, we have leveraged, and will continue to leverage, our business relationships with strategic partners to introduce new service offerings to the market and to diversify our business. Our strategic plan for the next five years is to continue to diversify our service mix and actively seek new growth opportunities to expand our business footprint in the U.S. market to reduce our dependency on the revenue generated from China. For decades, the shipping industry has been operated under traditional business models without many meaningful changes. Today, technological innovation has already played a big role in changing every conventional industry. We believe the internet will be a big part of the future logistics chain services and a transformative era in shipping and freight logistics business is coming. As an innovative solution provider, we plan to apply our technical ability, industry expertise and cutting-edge information technology in the conventional shipping business to better connect supply and demand and to develop seamless linkages in logistics chains.

4

As a result of our plan to diversify, we continued to provide on inland transportation management services and logistics between the U.S. and China, such as providing freight logistics services, container trucking services and bulk cargo container services. During this process, we will continue to adjust and develop our strategic plans based on the change of business environment.

However, with our decades of experience in shipping agency business and solid business relationships with Baosteel Group and Shougang Group, who are among the biggest importers of iron ore in China, we believe it is to the Company’s best interest to redirect our focus on this segment in 2019 based on our assessment of current global trading environments. To our understanding, we are one of few shipping agents specialized in providing a full range of general shipping agency services in China and the only shipping agency company listed on a public exchange in the U.S. while other shipping agencies are much smaller and more fragmented. With the setup of the Ningbo joint venture, we are able to use our resources such as our customer base, our currently developing IT infrastructure and our business insight to build a global network of shipping agencies. In addition, our current business segments like freight logistics and container trucking can also be integrated and enable us to provide more comprehensive logistics services for our customers.

Our plan is to develop a shipping agency network in China and South East Asia for the next three years and expand our shipping agency network worldwide. We plan to build the network through acquisitions or strategic partnership with other shipping agencies. Our shipping agency business will be mostly conducted through our China, Hong Kong and Australia subsidiaries.

In fiscal year 2020, we entered into a general shipping agency service agreement with Mandarine Bulk Ltd. as the sole general shipping agency and a shipping management services agreement with Qingdao Lizhou Ship Management Co., Ltd. We have expanded our business to increase sales revenue in the United States and get more customers who can settle in U.S. dollars.

In fiscal 2021, while we continue to provide our current traditional logistics business, we will integrate the traditional business with modern technology to develop a brand-new business model. On September 27, 2020, we signed a MOU with EMB Technology Co., LTD (“EMB”). Our company and EMB will combine the advantages of traditional logistics business/new technology and match the marketing economic requirements of the post-covid-19 world, gathering our many years of industry experience and customer group, with big data analysis, artificial intelligence, machine learning technologies, research and development platforms for the new business model, joint business partner's data interface, to change the traditional business model from delivery to businesses into delivery directly to customers. At the same time, we plan to strengthen the research and development force to complete the transformation of the company's business model and profit model step by step. After deep market research and demand analysis, with the actual situation in North America, iterative developing a certain popular App of high customer coupling, easy to form the functional industrial chain and derivative products and related services. We also expect to make achievements in the remote service industry include the service industry of enterprise portal, and the service industry of ERP customization/implementation/maintenance for small and medium-sized businesses, try to create a new milestone in the company's business.

Our Customers

In light of our strategic relationship with Zhiyuan Investment Group that began with the signing of a 5-year global logistics service agreement in June 2013, we expanded our business platform to include additional service offerings. We started to provide inland transportation management services to a third-party customer, Tengda Northwest Ferroalloy Co., Ltd. (“Tengda Northwest”), during the quarter ended September 30, 2014. As we continue to diversify our service platform, we endeavor to reduce our dependency on a few customers for which we provide freight logistics, container trucking services, and shipping agency services. Our main customers in the freight logistic service segment include Shanghai Baoding Energy Ltd. and Chongqing Iron & Steel Ltd. Our main customer of shipping agency and management service are Mandarine Bulk Ltd. and Qingdao Lizhou Ship Management Co., Ltd. We began to provide services to Mandarine Bulk Ltd. and Qingdao Lizhou Ship Management Co., Ltd. since fiscal year 2020.

For the year ended June 30, 2020, three customers accounted for approximately 42%, 23% and 22% of the Company’s revenues, respectively. As of June 30, 2020, one customer accounted for approximately 87% of the Company’s accounts receivable, net. For the year ended June 30, 2019, three customers accounted for approximately 35%, 16% and 13% of the Company’s revenues, respectively. As of June 30, 2019, all of these customers accounted for approximately 26% of the Company’s accounts receivable, net.

5

Our Suppliers

Our operations consist of working directly with our customers to understand in detail their needs and expectations and then managing local suppliers to ensure that our customers’ needs are met. For the year ended June 30 2020, three suppliers accounted for approximately 26%, 18% and 16% of the total costs of revenue, respectively. For the year ended June 30, 2019, three suppliers accounted for 23%, 12% and 10% of the total costs of revenue, respectively.

Our Strengths

We believe that the following strengths differentiate us from our competitors:

| ● | Proven industry experience and problem-solving reputation. We are a non-asset based global shipping and freight logistics solution provider. We provide tailored solutions and value-added services to our customers to drive effectiveness and control in related aspects throughout the entire shipping and freight logistic chain. We believe that our years of successful track record of applying integrated solutions to complex issues in the global shipping logistics business gives us a competitive advantage in attracting large clients and helps us maintain strong long terms business relationship with them. |

| ● | Strong leadership and a competent professional team. Our CEO is an industry veteran with more than thirty years of extensive industry experience including ten years working for COSCO, one of the largest shipping companies in the world. Most of our employees have marine business experience, and many of our managers/chief operators served in other large Chinese shipping companies prior to joining us. With these professionals and experienced staff, we believe that we provide the best services to our customers at competitive prices. |

| ● | Extensive network and positive industry recognition. Doing business in China often requires a strong business network and support of key strategic partners. The Company served as one of the executive directors of China Association of Shipping Agencies & Non-Vessel-Operating Common Carriers (CASA), the authoritative industry association in China. We are the only non-state-owned enterprise represented on the CASA board guiding the development of the industry. Our good reputation and industry recognition enables us to maintain strong relationships with our business partners and have an extensive network of contacts throughout the industry, which helps us gain necessary support to execute our business plans. |

| ● | Lean organization and a flexible business model. Although we are a small business with limited resources, we have a cohesive and effective organizational structure with the goal of maximizing customer value while minimizing waste. Our unique flexible business model allows us to quickly respond to changing market demand and offer our customers innovative problem-solving solutions, quality customer service, and competitive prices to achieve greater market acceptance and gain additional market share. |

| ● | U.S.-registered and NASDAQ-listed public company. We believe our status as a U.S. corporation gives us more credibility among existing and potential customers, suppliers, and other business partners than a privately owned company would have in our industry. Our ability to raise capital through the capital market or use our common stock as “currency” to facility potential merger and acquisition transactions can also help us carry out or accelerate our growth strategies. |

6

Our Opportunities

For more than thirty years, the shipping and freight logistics industry has been operated under traditional business models without meaningful change. Many of these business practices are inefficient and problematic; therefore, maintaining an innovative mindset is critical to achieving continuous business success and growth. We are a value-added logistics solution provider with successful past performance and individuals that have been in the industry for a long time. Instead of playing the traditional logistics broker role, we focus on providing technology solutions and innovative leading-edge services to bridge the asset-based world with the digital world. We shape our industry practice and profit model by analyzing wider developments both in the global markets and the technology industry so we can address unique problems that are currently pervasive across the shipping and freight logistics industry.

We believe we can capture the business opportunity and grow our business organically or through acquisitions or strategic alliance by:

| ● | Continuing to streamline our business operations and improve our operating efficiency through innovative technology, effective planning, budgeting, execution and cost control; |

| ● | Diversifying our business to focus on providing innovative technology based solution to our customers to promote our sustainable business growth; |

| ● | The current market of China's shipping agency industry is mature comparing to what it was ten years ago when the shipping agency industry was fueled by the massive construction of China's infrastructure, yet the over-supply of shipping agencies has also shrunk the profits of the industry. Many shipping agencies were constrained by the small size and the limited services. We have the professionalism and are the pioneers and leaders in the shipping agency industry in China. SINO is a NASDAQ-listed company that already has more flexibility in capital raise comparing to companies that are not on a U.S. major stock exchange or private companies. We already have a network that covers the US East coast, West coast, Canada, Australia, Hong Kong, Beijing, and Ningbo. We maintain strong relationships with customers and market resources. The current shipping agency market is more competitive yet enable companies like us who has better resources in this market niche to expand. |

Our Challenges

We face significant challenges when executing our strategy, including:

| ● | Given the complexity and length of restructuring our business, we face the challenge of generating sufficient cash from our current business activities to support our daily operations during the transition; |

| ● | We may not be able to establish a separate department to solve critical issues in today’s shipping logistics industry; |

| ● | We may not be able to manage our growth when we form more joint ventures for our shipping agency business as we need to better our standard operating and control procedures which may pose more challenges to our management. |

| ● | We may not have or not be able to get the necessary funds to continue to expand our service and market our services successfully; |

| ● | Our ability to respond to increasing competitive pressure on our growth and margins; |

| ● | Our ability to gain further expertise and to serve new customers in new service areas; |

| ● | From time to time, we may have difficulty carrying out services effectively and in a profitable way due to the cyclical nature of the shipping industry, which could lead to a prolonged period of sluggish demand for our services; |

| ● | Our ability to respond promptly to a changing regulatory environment, macroeconomic conditions, industry trends, and competitive landscape; and |

| ● | Developing a winning business model takes time and a new business model may not be recognized by the market immediately. As a publicly traded company, management may be forced to fulfill near-term performance goals that may not be consistent with the Company’s long-term vision. |

7

Our Competition

The market segments that we serve do not have high entry barriers. There are many companies ranging from small to large in China that provide shipping and freight-related logistics services. At present, the state-owned companies in China still dominate the industry and generate a majority of the revenues in the industry. These companies have greater service capabilities, a larger customer base and more financial, marketing, network and human resources than we do. Most of them engage in a wide range of businesses and involve many aspects of the industry chain. However, we focus on providing tailored solutions and value-added services to select high-profile customers to drive effectiveness and control in related aspects throughout the entire shipping and freight logistic chain. As a boutique company that provides specialized services with limited resources and history, we face intense competition in the particular market segments that we serve. Our ability to be successful in our industry depends on our deep understanding of the complexity of industry issues and challenges and our technical ability to develop best solutions to respond to the identified issues and provide effective problem-solving strategies to our targeted customers to achieve the fastest and most cost-effective outcomes. Our value-added services and innovative approaches are highly recognized by our customers, which helps us to gain additional market share and compete effectively with the companies that may be better capitalized than we are or may provide services we do not or cannot provide to our customers.

Employees

As of the date of this report, we have 19 full-time employees and one part-time employee, 11 of whom are based in China. Of the total full time employees, 4 are in management, 9 are in operations, 3 are in finance and accounting and 3 are in administration and technical support. We believe that our relationship with our employees is good. We have never had a work stoppage, and our employees are not subject to a collective bargaining agreement.

Recent Development

On September 3, 2018, the Company entered into a co-operation agreement with Ningbo Far-East Universal Shipping Agency Co., Ltd to set up a joint venture in Hong Kong named Bright Far East International Shipping Agency Co., Ltd. (“Bright Far HK”), to engage in worldwide shipping agency operations. The Company has a 51% equity interest in the joint venture. On May 23, 2019, Bright Far East International Shipping Agency Co., Ltd. was incorporated in New York and the registration of Bright Far HK was terminated in Hong Kong.

On April 10, 2019, we entered into a cooperation agreement with Mr. Weijun Qin, the Chief Executive Officer of a shipping management company in China, to set up a joint venture in New York named State Priests Management Ltd., of which we hold a 90% equity interest. We have not provided any cash contribution to the joint venture pending the certification and approval from related authorities. On November 6, 2019, the Company signed a revised cooperation agreement with Mr. Weijun Qin to restructure their equity interest in State Priests. Given that State Priests failed to timely obtain the necessary approval from related authorities, Mr. Weijun Qin agreed to exchange 80% equity interest in Sea Continent Management Ltd. (“Sea Continent”), another New York entity Mr. Qin owns for the Company’s 90% equity interest in State Priests. The equity transfer has been consummated. Sea Continent already has the Certificate but has no operations as of June 30, 2020. There has been no capital injection nor operations of State Priests and Sea Continent as of June 30, 2020, therefore no gain or loss has been recognized in the transaction.

On November 13, 2019, the Company entered into a cooperation agreement with Shanming Liang, a director of Guangxi Jinqiao Industrial Group Co., Ltd., to cooperate and expand the bulk cargo container services business. Shanming Liang agreed to purchase 200,000 shares of the Company’s common stock at a purchase price of $5.00 per share for aggregate proceeds of $1.0 million. The Company and Mr. Liang further entered into a Share Purchase Agreement on November 14, 2019 to memorialize the transaction aforementioned.

On January 10, 2020, the Company entered into a cooperation agreement with Mr. Liang, to set up a joint venture in New York named LSM Trading Ltd. (“LSM Trading”) to engage in trading business, of which we hold 40% equity interest. No investment has been made by the Company as of the date of this report.

8

On April 6, 2020, the Company entered into a Share Purchase Agreement (the “Original SPA”) with Mr. Kelin Wu, a PRC investor (the “Seller”) and Mandarine Ocean Ltd (“Hanyang Shipping”), a shipping company registered in the Marshall Islands, pursuant to which the Company agreed to purchase 75% of the equity of Hanyang Shipping from the Seller for a purchase price of up to $3,750,000, payable in cash equivalent and/or restricted shares of common stock of the Company, subject to completion of a third-party valuation of Hanyang Shipping. On June 17, 2020, the Company entered into an amended share purchase agreement (the “Amendment”) with the Seller to acquire 75% of the capital stock of Hanyang Shipping held by the Seller for an aggregate consideration of up to $1.5 million to be paid in cash and the Company’s restricted shares. On September 3, 2020, the Company and the Seller signed a Termination Agreement to terminate the Amendment mutually. Neither party will owe the other party any termination penalty in connection with the Termination Agreement.

On September 17, 2020, the Company entered into certain securities purchase agreement (the “SPA”) with certain “non-U.S. Persons” (the “Purchasers”) as defined in Regulation S of the Securities Act of 1933, as amended, pursuant to which the Company agreed to sell an aggregate of 720,000 shares (the “Shares”) of the Company’s common stock, no par value (“Common Stock”), and warrants (the “Warrants”) to purchase 720,000 Shares at a per share purchase price of $1.46 (the “Offering”). The net proceeds to the Company from such Offering will be approximately $1.05 million. The Warrants will be exercisable six (6) months following the date of issuance at an exercise price of $1.825 for cash (the “Warrant Shares”). The Warrants may also be exercised cashlessly if at any time after the six-month anniversary of the issuance date, there is no effective registration statement registering, or no current prospectus available for, the resale of the Warrant Shares. The Warrants will expire five and a half (5.5) years from its date of issuance. The Warrants are subject to anti-dilution provisions to reflect stock dividends and splits or other similar transactions. The Warrants contain a mandatory exercise right for the Company to force exercise the Warrants if the Company’s common stock trades at or above $4.38 for 20 consecutive trading days, provided, among other things, that the shares issuable upon exercise of the are registered or may be sold pursuant to Rule 144 and the daily trading volume exceeds 60,000 shares of Common Stock per trading day on each trading day in a period of 20 consecutive trading days prior to the applicable date. On September 21 and September 22, 2020, the Company received total gross proceeds of $1.05 million.

This item is not applicable to a smaller reporting company such as us.

Item 1B. Unresolved Staff Comments.

The Company does not have any unresolved or outstanding staff comments.

We currently rent four facilities in the PRC, Hong Kong and the United States. Our PRC headquarter is in Beijing, and our U.S. headquarter is in New York.

| Office | Address | Rental Term | Space | |||

| Shanghai, PRC | Rm 12D & 12E, No.359 Dongdaming Road, Hongkou District, Shanghai, PRC 200080 |

Expires 07/31/2021 | 285.99 m2 | |||

| New York, USA | 1044 Northern Boulevard, Suite 305 Roslyn, New York 11576-1514 |

Expires 09/30/2022 | 179 m2 | |||

| Hong Kong | 20/F, Hoi Kiu Commercial Building, 158 Connaught Road Central, HK |

Expires 05/17/2021 | 77 m2 | |||

| Ningbo, PRC | Rm 606 Building 2 | Expires 06/30/2022 | 633.66 m2 | |||

No.1 Qianyang Star Plaza 999 Changxing Rd, Jiangbei District Ningbo, Zhejiang, PRC 315000 |

As of the date hereof, we know of no material pending legal proceedings to which we, or any of our subsidiaries, are a party. There are no proceedings in which any of our directors, executive officers or affiliates, or any registered or beneficial shareholder, is an adverse party or has a material interest adverse to our interest. From time to time, we may be subject to various claims, legal actions and regulatory proceedings arising in the ordinary course of business.

Item 4. Mine Safety Disclosures.

This item is not applicable to the Company.

9

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Market for Our Common Stock

Our common stock is traded on the NASDAQ Stock Market under the symbol SINO.

Approximate Number of Holders of Our Common Stock

As of October 9, 2020, there are 12 holders of record of our common stock. This number does not include shareholders who hold their shares of common stock in street name.

Dividend Policy

We have never declared or paid any cash dividends on our common stock. We anticipate that we will retain any earnings to support operations and to finance the growth and development of our business. Therefore, we do not expect to pay cash dividends in the foreseeable future. Any future determination relating to our dividend policy will be made at the discretion of our Board of Directors (the “Board”) and will depend on a number of factors, including future earnings, capital requirements, financial conditions and future prospects and other factors the Board may deem relevant. Payments of dividends by Trans Pacific to our company are subject to restrictions including primarily the restriction that foreign invested enterprises may only buy, sell and/or remit foreign currencies at those banks authorized to conduct foreign exchange business after providing valid commercial documents.

Recent Sales of Unregistered Securities and Issuer Purchases of Equity Securities

Recent Sales of Unregistered Securities

On May 9, 2019, the Company entered into a cooperation agreement with Xuben Lu, a major shareholder of Fangchenggang China Global International Shipping Agency Co., Ltd., to cooperate and expand the shipping agency services business. Xuben Lu purchased 66,667 shares of the Company’s common stock at a purchase price of $1.5 per share for aggregate proceeds of $100,000. The shares were issued on July 29, 2019 in reliance on an exemption from registration under the Securities Act in Section 4(a)(2) thereof.

10

On May 29, 2019, the Company entered into an operation management cooperation agreement with Yueliang Pan, owner of multiple shipping agency companies in China, to cooperate and expand the shipping agency services business. Yueliang Pan purchased 166,667 shares of the Company’s common stock at a purchase price of $1.5 per share for aggregate proceeds of $250,000. The shares were issued on July 29, 2019 in reliance on an exemption from registration under the Securities Act in Section 4(a)(2) thereof.

On November 19, 2019, the Company entered into a share purchase agreement with Shanming Liang, pursuant to which the Company agreed to issue 200,000 Shares at a price of $5.00 per share (giving effect to the 1-for-5 reverse split completed on July 7, 2020). The placement closed on January 29, 2020. The issuance was determined to be exempt from registration under the Securities Act in reliance on Section 4(a)(2) thereof.

On April 6, 2020, the Company entered into a share purchase agreement with Kelin Wu that would, among other things, resulted in the issuance of up to 729,561restricted Shares (giving effect to the 1-for-5 reverse split completed on July 7, 2020) in connection with the acquisition of 75% of the equity of Mandarine Ocean Ltd, a shipping company registered in the Marshall Islands. The issuance was determined to be exempt from registration under the Securities Act in reliance on Section 4(a)(2) thereof. Notwithstanding the foregoing, the issuance was never completed, and the parties entered a termination agreement on September 3, 2020.

On September 17, 2020, the Company entered into a securities purchase agreement with certain non-U.S. Persons to purchase 720,000 Shares for aggregate proceeds of $1.05 million. The issuance of Shares was made pursuant to a registration statement on Form S-3. Concurrently with the registered offering of shares, the Company issued warrants to purchase 720,000 Shares for an exercise price of $1.46 per Share. The issuance of warrants was determined to be exempt from registration under the Securities Act in reliance on Regulation S.

Item 6. Selected Financial Data

The Company is not required to provide the information required by this item because the Company is a smaller reporting company.

11

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

The following discussion and analysis of our company’s financial condition and results of operations should be read in conjunction with our consolidated financial statements and the related notes included elsewhere in the report. This discussion contains forward-looking statements that involve risks and uncertainties. Actual results and the timing of selected events could differ materially from those anticipated in these forward-looking statements as a result of various factors.

Overview

Sino-Global has focused on providing customers with customized shipping agency and freight logistic services but has since begun looking aggressively at diversifying its revenue and service mix by seeking new growth opportunities to expand its business due to increased margin compression. These opportunities have ranged from complementary businesses to other service and product initiatives.

With the hope of bringing us back to the shipping management business, on April 10, 2019, the Company entered into a cooperation agreement with Mr. Weijun Qin, CEO of a shipping management company in China, to set up a joint venture in New York named State Priests Management Ltd. (“State Priests”), of which we hold 90% equity interest. On November 6, 2019, we signed a revised cooperation agreement with Mr. Qin to restructure our equity interest in State Priests. Due to State Priests’ failure to timely obtain the necessary approval from related authorities, Mr. Qin agreed to exchange 80% equity interest in Sea Continent Management Ltd. (“Sea Continent”), another entity he owns, for 90% equity interest that we hold in State Priests. Sea Continent already has the International Ship Safety Management certificate from the China Classification Society for its operations.

To adapt to the changing China market, which has a high demand for agricultural products and agricultural by-products, one of the Company’s business strategies is to provide services in connection with the purchase of the U.S agricultural products and the shipment of these products to China using its overall supply chain logistics. On January 10, 2020, the Company entered into a cooperation agreement with Mr. Shanming Liang, a director of Guangxi Jinqiao Industrial Group Co., Ltd., to set up a joint venture in New York named LSM Trading Ltd. (“LSM Trading”) to engage in trading business, of which we hold 40% equity interest. No investment has been made by the Company as of the date of this report. LSM Trading will facilitate the purchase of the agricultural commodities and agricultural by-products in the U.S. for customers in China and the Company will provide comprehensive supply chain and logistics solutions.

Due to uncertainty in current trade environment and the impact of novel coronavirus, the Company has not made any investment in the aforementioned joint ventures and no significant operations has commenced. The Company has started shipping management services by its US subsidiary through fiscal year 2020.

The outbreak of the novel coronavirus (COVID-19) starting from late January 2020 in the PRC has spread rapidly to many parts of the world. The pandemic has resulted in quarantines, travel restrictions, and the temporary closure of stores and business facilities in China and United States for the past few months. In March 2020, the World Health Organization declared the COVID-19 as a pandemic. Given the rapidly expanding nature of the COVID-19 pandemic, and because substantially all of our business operations and our workforce are concentrated in China and United States, our business, results of operations, and financial condition have been materially and adversely affected. Potential impact to our results of operations beyond fiscal year 2020 will also depend on future developments and new information that may emerge regarding the duration and severity of the COVID-19 and the actions taken by government authorities and other entities to contain the COVID-19 or mitigate its impact, almost all of which are beyond our control.

The impacts of COVID-19 on our business, financial condition, and results of operations include but are not limited to, the following:

| ● | We temporarily closed our Chinese and U.S. offices and implemented work-from-home policy beginning from late January to March 2020 for our China offices and from March to June 2020 for our U.S. offices, as required by relevant PRC and U.S. regulatory authorities, respectively. Our office closure and limited activity had caused business interruption which led to a slower growth for our operations. |

12

| ● | Our customers have been negatively impacted by the outbreak, which reduced demand for the shipping agency and management as well as freight logistics services in 2020. As a result, our revenue, gross profit and net income has been negatively impacted in 2020. Our revenue and gross profit for the year ended June 30, 2020 were down by approximately 35.2 million or 84.4% and 2.9 million or 50.4%, respectively, and net loss increased by approximately 5.9 million or 84.0% from the same period last year. |

| ● | Our customers required additional time to pay us or failed to pay us, which required us to record additional allowances. We are currently working with customers to resolve the delinquency issues and made $4,996,006 of allowance for doubtful accounts in the year ended June 30, 2020. We wrote off $8,220,754 of accounts receivable in the year ended June 30, 2020. We will monitor our collections closely throughout the rest of calendar year 2020. |

| ● | We prepaid the costs of commodities and recognized as advance payments on behalf of our customers. As our customers were negatively impacted by the pandemic and required additional time to execute existing contracts, they required additional time to pay us. Due to significant uncertainty on whether the delayed contracts will be executed timely. As such, we provided an allowance due to contract delay and recorded allowances of approximately $10.0 million. We are currently working with customers to resolve the repayment issues and will monitor collection closely. |

| ● | Our suppliers have been and could continue to be negatively impacted by the COVID-19 outbreak, which may negatively impact our cost of freight, or result in higher cost of revenue, which may in turn materially adversely affect our financial condition and operating results in coming months. |

On April 6, 2020, the Company entered into a Share Purchase Agreement (the “Original SPA”) with Mr. Kelin Wu, a PRC investor (the “Seller”) and Mandarine Ocean Ltd (“Hanyang Shipping”), a shipping company registered in the Marshall Islands, pursuant to which the Company agreed to purchase 75% of the equity of Hanyang Shipping from the Seller for a purchase price of up to $3,750,000, payable in cash equivalent and/or restricted shares of common stock of the Company, subject to completion of a third-party valuation of Hanyang Shipping. On June 17, 2020, the Company entered into an amended share purchase agreement (the “Amendment”) with the Seller to acquire 75% of the capital stock of Hanyang Shipping held by the Seller for an aggregate consideration of up to $1.5 million to be paid in cash and the Company’s restricted shares. On September 3, 2020, the Company and the Seller signed a Termination Agreement to terminate the Amendment mutually. Neither party will owe the other party any termination penalty in connection with the Termination Agreement.

Recent developments

After the close of the stock market on July 7, 2020, we effected a l-for-5 reverse stock split of our common stock in order to satisfy continued listing requirements of our common stock on the NASDAQ Capital Market. The reverse stock split was approved by our board of directors and stockholders and was intended to allow the company to meet the minimum share price requirement of $1.00 per share for continued listing on the NASDAQ Capital Market. As a result all common stock share amounts included in this filing have been retroactively reduced by a factor of five, and all common stock per share amounts have been increased by a factor of five. Amounts affected include common stock outstanding, including those that have resulted from the stock options, and warrants that convert to common stock.

On September 17, 2020, the Company entered into certain securities purchase agreement (the “SPA”) with certain “non-U.S. Persons” (the “Purchasers”) as defined in Regulation S of the Securities Act of 1933, as amended, pursuant to which the Company agreed to sell an aggregate of 720,000 shares (the “Shares”) of the Company’s common stock, no par value (“Common Stock”), and warrants (the “Warrants”) to purchase 720,000 Shares at a per share purchase price of $1.46 (the “Offering”). The net proceeds to the Company from such Offering will be approximately $1.05 million. The Warrants will be exercisable six (6) months following the date of issuance at an exercise price of $1.825 for cash (the “Warrant Shares”). The Warrants may also be exercised cashlessly if at any time after the six-month anniversary of the issuance date, there is no effective registration statement registering, or no current prospectus available for, the resale of the Warrant Shares. The Warrants will expire five and a half (5.5) years from its date of issuance. The Warrants are subject to anti-dilution provisions to reflect stock dividends and splits or other similar transactions. The Warrants contain a mandatory exercise right for the Company to force exercise the Warrants if the Company’s common stock trades at or above $4.38 for 20 consecutive trading days, provided, among other things, that the shares issuable upon exercise of the are registered or may be sold pursuant to Rule 144 and the daily trading volume exceeds 60,000 shares of Common Stock per trading day on each trading day in a period of 20 consecutive trading days prior to the applicable date. On September 21 and September 22, 2020, the Company received total gross proceeds of $1.05 million.

13

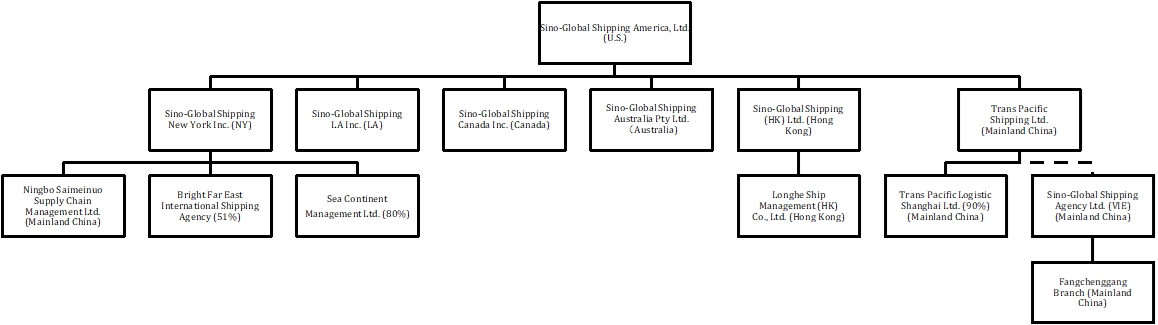

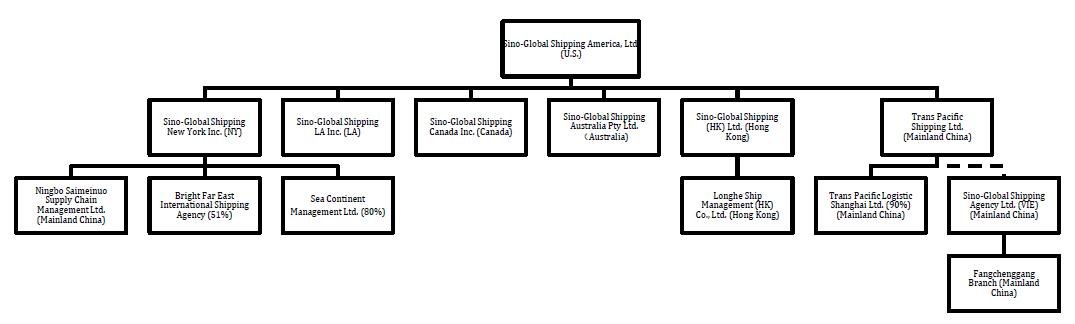

Company Structure

The Company, founded in 2001, is a non-asset based global shipping and freight logistics integrated solutions provider. We provide tailored solutions and value-added services for our customers to drive efficiency and control in related steps throughout the entire shipping and freight logistics chain. We conduct our business primarily through our wholly-owned subsidiaries in the People’s Republic of China (the “PRC”) (including Hong Kong) and the U.S., where a majority of our clients are located.

We operate in four operating segments, including (1) shipping agency and management services, operated by our subsidiary in Hong Kong and the U.S.; (2) inland transportation management services, operated by our subsidiaries in the U.S.; (3) freight logistics services, operated by our subsidiaries in the PRC and the U.S.; and (4) container trucking services, operated by our subsidiaries in the PRC and the U.S.

Our corporate structure diagram as of the date of this report is as below:

Results of Operations

Comparison of the Years ended June 30, 2020 and 2019

Revenues

Revenues decreased by $35,235,091 or approximately 84.4%, from $41,771,047 for the year ended June 30, 2019 to $6,535,956 for the same period in 2020. The decrease was primarily due to the fact that in certain freight logistics contracts that we entered into with customers starting from the first quarter of fiscal year 2020, we only acted as an agent and did not control the services rendered to the customers as we are not the primary responsible party to fulfill the services in order to reduce possible risks as a result of the uncertainties in current trade environments. As such our revenues on these contracts are accounted for on a net basis. The decrease was also due to the decrease in revenues from inland transportation management services as our service contracts with customers have expired and there was no new business for this segment. In addition, as a result of COVID-19, which caused business interruption staring third quarter of fiscal year 2020 had slowed our revenue growth than expected across all segments.

The following tables present summary information by segments mainly regarding the top-line financial results for the years ended June 30, 2020 and 2019:

| For the Year Ended June 30, 2020 | ||||||||||||||||||||

| Shipping Agency and Management Services |

Inland Transportation Management Services | Freight Logistics Services |

Container Trucking Services | Total | ||||||||||||||||

| Revenues | ||||||||||||||||||||

| - Related party | $ | - | $ | - | $ | - | $ | - | $ | - | ||||||||||

| - Third parties | $ | 2,105,651 | $ | - | $ | 4,368,596 | * | $ | 61,709 | $ | 6,535,956 | |||||||||

| Total revenues | $ | 2,105,651 | $ | - | $ | 4,368,596 | $ | 61,709 | $ | 6,535,956 | ||||||||||

| Cost of revenues | $ | 827,690 | $ | - | $ | 2,795,859 | * | $ | 55,314 | $ | 3,678,863 | |||||||||

| Gross profit | $ | 1,277,961 | $ | - | $ | 1,572,737 | $ | 6,395 | $ | 2,857,093 | ||||||||||

| Depreciation and amortization | $ | 340,421 | $ | - | $ | 7,684 | $ | 54,189 | $ | 402,294 | ||||||||||

| Total capital expenditures | $ | 6,984 | $ | - | $ | - | $ | - | $ | 6,984 | ||||||||||

| Gross margin% | 60.7 | % | - | 36.0 | % | 10.4 | % | 43.7 | % | |||||||||||

| * | For the year ended June 30, 2020, gross revenue and gross cost of revenue related to the contracts where we acted as agents amounted to approximately $25.8 million and $24.3 million, respectively. |

14

| For the Year Ended June 30, 2019 | ||||||||||||||||||||

| Shipping Agency Services |

Inland Transportation Management Services | Freight Logistics Services |

Container Trucking Services | Total | ||||||||||||||||

| Revenues | ||||||||||||||||||||

| - Related party | $ | - | $ | 433,383 | $ | - | $ | - | $ | 433,383 | ||||||||||

| - Third parties | $ | 2,093,680 | $ | 1,036,416 | $ | 37,725,136 | $ | 482,432 | $ | 41,337,664 | ||||||||||

| Total revenues | $ | 2,093,680 | $ | 1,469,799 | $ | 37,725,136 | $ | 482,432 | $ | 41,771,047 | ||||||||||

| Cost of revenues | $ | 1,894,332 | $ | 128,624 | $ | 33,556,109 | $ | 427,445 | $ | 36,006,510 | ||||||||||

| Gross profit | $ | 199,348 | $ | 1,341,175 | $ | 4,169,027 | $ | 54,987 | $ | 5,764,537 | ||||||||||

| Depreciation and amortization | $ | - | $ | 110,821 | $ | 1,902 | $ | 18,197 | $ | 130,920 | ||||||||||

| Total capital expenditures | $ | - | $ | - | $ | 125,817 | $ | 17,675 | $ | 143,492 | ||||||||||

| Gross margin% | 9.5 | % | 91.2 | % | 11.1 | % | 11.4 | % | 13.8 | % | ||||||||||

| % Changes For the Year Ended June 30, 2020 to 2019 | ||||||||||||||||||||

| Shipping Agency and Management Services | Inland Transportation Management Services | Freight Logistics Services | Container Trucking Services | Total | ||||||||||||||||

| Revenues | ||||||||||||||||||||

| - Related party | - | (100.0 | )% | - | - | (100.0 | )% | |||||||||||||

| - Third parties | 0.6 | % | (100.0 | )% | (88.4 | )% | (87.2 | )% | (84.2 | )% | ||||||||||

| Total revenues | 0.6 | % | (100.0 | )% | (88.4 | )% | (87.2 | )% | (84.4 | )% | ||||||||||

| Cost of revenues | (56.3 | )% | (100.0 | )% | (91.7 | )% | (87.1 | )% | (89.8 | )% | ||||||||||

| Gross profit | 541.1 | % | (100.0 | )% | (62.3 | )% | (88.4 | )% | (50.4 | )% | ||||||||||

| Depreciation and amortization | 100.0 | % | (100.0 | )% | 304.0 | % | 197.8 | % | 207.3 | % | ||||||||||

| Total capital expenditures | 100.0 | % | - | (100.0 | )% | (100.0 | )% | (95.1 | )% | |||||||||||

| Gross margin% | 51.2 | % | (91.2 | )% | 24.9 | % | (1.0 | )% | 29.9 | % | ||||||||||

Disaggregated information of revenues by geographic locations are as follows:

| June 30, | June 30, | |||||||

| 2020 | 2019 | |||||||

| PRC | $ | 4,368,596 | $ | 37,755,310 | ||||

| U.S. | 2,167,360 | 1,922,057 | ||||||

| Hong Kong | - | 2,093,680 | ||||||

| Total revenues | $ | 6,535,956 | $ | 41,771,047 | ||||

Revenues

(1) Shipping Agency and Management Services

For the years ended June 30, 2020 and 2019, shipping agency and management services generated revenues of $2,105,651 and $2,093,680, respectively, representing an approximately 0.6% increase in revenues. The increase in this segment was because we entered into a general shipping agency service agreement with Mandarine Bulk as the sole general shipping agency and a shipping management services agreement with Qingdao Lizhou Ship Management Co., Ltd. for the year ended June 30, 2020. Our integrated services included arranging and coordinating ship maintenance and inspection, repairs, and other services. With Sea Continent, our 80% owned joint venture, we expect to perform more services such as ship insurance, crew recruitment, training and supply and ship spare parts sales. Our gross margin increased to 60.7% for the year ended June 30, 2020 from 9.5% for the same period in 2019. The increase was mainly because we started to provide shipping management service utilizing our operational staffs in 2020 as compared to the 2019 cost of revenue for shipping agency which included service fees from subcontractors at a much higher costs.

15

(2) Revenues from Inland Transportation Management Services

For the years ended June 30, 2020 and 2019, inland transportation management services generated related-party revenue of $0 and $433,383, respectively. Revenue generated from Tengda Northwest for the years ended June 30, 2020 and 2019 amounted to $0 and $1,036,416, respectively. The overall decrease in revenues generated from this segment amounted to $1,469,799 or 100.0% due to the expiration of our inland transportation management service contracts with the aforementioned customers. We expect limited growth in this segment in the coming years due to the current trade dynamics.

(3) Revenues from Freight Logistics Services

Freight logistics services primarily consist of cargo forwarding, brokerage and other freight services. During the year ended June 30, 2020, revenues decreased by $33,356,540 or approximately 88.4%. The decrease was primarily due to the fact that in certain freight logistic contracts that we entered into with customers starting from the first quarter of fiscal year 2020, we acted as an agent in arranging the relationship between the customer and the third-party service provider and did not control the services rendered to the customer. For the year ended June 30, 2020, gross revenue and gross cost of revenue related to these contracts amounted to approximately $25.8 million and $24.3 million, respectively. However, as we only acted as an agent, our revenues on these contacts were accounted for on a net basis.

Our gross profit margin increased by approximately 24.9% from approximately 11.1% for year ended June 30, 2019 to approximately 36.0% for the same period in 2020. The increase in gross margin was due to the following factors: 1) the aforementioned freight logistic contracts where we acted as agents usually have lower margins than those where we control the services provided; 2) change in the mix of services provided. Even with the same customer, every transaction has a unique gross margin due to differing service scopes. Generally, an engagement where we provide a broader set of services generates a higher gross margin, and an engagement of a more limited scope of services has a lower gross margin.

(4) Revenues from Container Trucking Services

For the years ended June 30, 2020 and 2019, revenues generated from container trucking services were $61,709 and $482,432, respectively. Overall revenues from this segment decreased by $420,723 or approximately 87.2%. The decrease in revenues from this segment was primarily due to the pending trade negotiations between the U.S. and China, which decreased container shipments from China to the U.S. The related gross profit decreased by $48,592 from $54,987 gross profit for the year ended June 30, 2019 to $6,395 for the same period in 2020. Gross profit margin for both periods remained relatively consistent.

Operating Costs and Expenses

Operating costs and expenses decreased by $23,467,433 or approximately 49.2%, from $47,741,493 for the year ended June 30, 2019 to $24,274,060 for the year ended June 30, 2020. This decrease was mainly due to the decrease in cost of revenue, selling expenses, general and administrative expenses and stock-based compensation as discussed below.

The following table sets forth the components of the Company’s costs and expenses for the periods indicated:

| For the Years Ended June 30, | ||||||||||||||||||||||||

| 2020 | 2019 | Change | ||||||||||||||||||||||

| US$ | % | US$ | % | US$ | % | |||||||||||||||||||

| Revenues | 6,535,956 | 100.0 | % | 41,771,047 | 100.0 | % | (35,235,091 | ) | (84.4 | )% | ||||||||||||||

| Cost of revenues | 3,678,863 | 56.3 | % | 36,006,510 | 86.2 | % | (32,327,647 | ) | (89.8 | )% | ||||||||||||||

| Gross margin | 43.7 | % | N/A | 13.8 | % | N/A | 29.9 | % | N/A | |||||||||||||||

| Selling expenses | 393,617 | 6.0 | % | 718,754 | 1.7 | % | (325,137 | ) | (45.2 | )% | ||||||||||||||

| General and administrative expenses | 3,386,690 | 51.8 | % | 4,344,435 | 10.4 | % | (957,745 | ) | (22.0 | )% | ||||||||||||||

| Impairment loss of fixed assets and intangible asset | 327,632 | 5.0 | % | - | - | % | 327,632 | 100.0 | % | |||||||||||||||

| Impairment loss of deposit for leasehold improvement | - | - | % | 425,068 | 1.0 | % | (425,068 | ) | (100.0 | )% | ||||||||||||||

| Provision for doubtful accounts | 14,910,502 | 228.1 | % | 3,978,893 | 9.5 | % | 10,931,609 | 274.7 | % | |||||||||||||||

| Stock-based compensation | 1,576,756 | 24.1 | % | 2,267,833 | 5.4 | % | (691,077 | ) | (30.5 | )% | ||||||||||||||

| Total Costs and Expenses | 24,274,060 | 371.3 | % | 47,741,493 | 114.2 | % | (23,467,433 | ) | (49.2 | )% | ||||||||||||||

16

Cost of Revenues

Cost of revenues consisted primarily of freight costs to various freight carriers, cost of labor, other overhead and sundry costs. Cost of revenues was $3,678,863 for the year ended June 30, 2020, a decrease of $32,327,647, or approximately 89.8%, as compared to $36,006,510 for the same period in 2019. The overall cost of revenues as a percentage of our revenues decreased from approximately 86.2% for the year ended June 30, 2019, to approximately 56.3% for the same period in 2020. Cost of revenues for freight logistics and container trucking services consists primarily of freight costs to various freight carriers. The decrease of costs was mainly due to the aforementioned certain freight logistic contracts in which only acted as an agent and did not control the services rendered to the customers for the year ended June 30, 2020.

Selling Expenses

Our selling expenses consisted primarily of salaries and travel expenses for our sales representatives. For the year ended June 30, 2020, we had $393,617 of selling expenses, as compared to $718,754 for the same period in 2019, which represents a decrease of $325,137 or approximately 45.2%. The decrease was mainly due to approximately $299,000 decrease in business development expenses as limited activities for our selling team under COVID-19.

General and Administrative Expenses

Our general and administrative expenses consist primarily of salaries and benefits, travel expenses for administration department, software development expenses, office expenses, regulatory filing and professional service fees including audit, legal and IT consulting. For the year ended June 30, 2020, we had $3,386,690 of general and administrative expenses, as compared to $4,344,435 for the same period in 2019, representing a decrease of $957,745, or approximately 22.0%. The decrease was mainly due to the decrease in IT expenses of approximately $601,000, the decrease in professional service fees of approximately $131,000 as we incurred less expenses on management consulting and advisory services and the decrease in travel and office expenses of approximately $497,000 as we incurred less travel and office expenses due to our office closure and limited activity under COVID-19. The decrease was offset by the approximately $271,000 increase in depreciation and amortization expenses.

Impairment loss of fixed assets and intangible asset

For the year ended June 30, 2020, we recorded $327,632 of impairment loss of fixed assets and intangible asset due to the continued decrease in revenues generated from the inland transportation management segment. There was no such transaction for year ended June 30, 2019.

Impairment loss of deposit for leasehold improvement

For the year ended June 30, 2019, we recorded a $425,068 impairment loss on the deposit as we paid a $422,381 deposit for leasehold improvements on our IT infrastructure facility including upgrading the server room of its Shanghai office. The design plan for the leasehold improvement was not approved by the building management due to power supply issues and we planned to move the IT infrastructure facility to our Ningbo office. There was no such transaction for year ended June 30, 2020.

17

Provision for Doubtful Accounts

We made $15,051,209 provision for doubtful accounts and offset by the recoveries of accounts receivable of $99,366 and other receivable - related party of $41,341 for the year ended June 30, 2020 compared to $3,978,893 with no recovery for the same period in 2019, an increase of $10,931,609, or approximately 274.7%. This increase of provision for doubtful accounts was mainly because the recent outbreak of COVID-19 has adversely affected our customers’ business operations, which in turn adversely affected our ability to collect accounts receivable and other receivables from our customers.

Stock-based Compensation

Stock-based compensation was $1,576,756 for the year ended June 30, 2020, a decrease of $691,077 or approximately 30.5%, as compared to $2,267,833 for the same period in 2019. Stock-based compensation decreased significantly from the year ended June 30, 2019 to the same period in 2020 due to less stock award was granted as a result of the decline in revenue as well as lower average stock prices in the year ended June 30, 2020 compared to the same period of the prior year.

Operating Loss

We had an operating loss of $17,738,104 for the year ended June 30, 2020, compared to an operating loss of $5,970,446 for the same period in 2019. Such change was the result of the combination of the changes discussed above.

Taxation

We recorded an income tax expense of $186,021 for the year ended June 30, 2020, compared to income tax expense of $920,869 for the same period in 2019. For the year ended June 30, 2020, income tax decreased by $734,848 or approximately 79.8%, as compare to the same period in 2019 due to the decrease in taxable income, mainly in the Company’s PRC entity conducting freight logistic services.

We have incurred a cumulative U.S. federal net operating loss (“NOL”) of approximately $3,781,000 as of June 30, 2019, which may reduce future federal taxable income. The NOL generated prior to the year ended June 30, 2017 amounted to approximately $1,400,000 will expire in 2037 and the remaining balance carried forward indefinitely. During the year ended June 30, 2020, approximately $2,675,000 of additional NOL was generated and the tax benefit derived from such NOL was approximately $562,000.

Our operations in China have incurred a cumulative a cumulative NOL of approximately $5,828,000 as of June 30, 2019, which may reduce future taxable income. The NOL amounted to approximately $281,000 start expiring from 2021 and the remaining balance of NOL will be expired by 2025. During the year ended June 30, 2020, approximately $133,000 of additional NOL was generated and the tax benefit derived from such NOL was approximately $33,000.