UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended June 30, 2017

or

☐ TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ___________to ___________

Commission file number 001-33997

Sino-Global

Shipping America, Ltd.

(Exact name of registrant as specified in its charter)

| Virginia | 11-3588546 | |

| (State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification No.) |

1044 Northern Boulevard, Suite 305

Roslyn,

New York 11576-1514

(Address of principal executive offices) (Zip Code)

(718)

888-1814

(Registrant’s telephone number, including area code)

Securities Registered Pursuant to Section 12(b) of the Act:

| Common Stock, Without Par Value Per Share | NASDAQ Capital Market | |

| (Title of each class) | (Name of exchange on which registered) |

Securities Registered Pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulations S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ |

| Non-accelerated filer ☐ | Smaller reporting company ☒ |

| Emerging growth company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of voting common stock held by non-affiliates of the registrant as of December 31, 2016, the last business day of the registrant’s second fiscal quarter, was approximately $11,404,369.90.

The number of shares of common stock outstanding as of September 25, 2017 was 10,105,535.

DOCUMENTS INCORPORATED BY REFERENCE:

None.

SINO-GLOBAL SHIPPING AMERICA, LTD.

FORM 10-K

INDEX

INTRODUCTION

Unless the context otherwise requires, in this annual report on Form 10-K:

| ● | “We,” “us,” “our,” and “our Company” refer to Sino-Global Shipping America, Ltd., a Virginia company incorporated in April 2001, and all of its direct and indirect consolidated subsidiaries; | |

| ● | “Sino-Global” or “Sino” refers to Sino-Global Shipping America, Ltd; | |

| ● | “Sino-China” refers to Sino-Global Shipping Agency Ltd., a Chinese legal entity, | |

| ● | “Trans Pacific” refers to and relates collectively to Trans Pacific Shipping Ltd., our wholly-owned subsidiary located in China, and Trans Pacific Logistics Shanghai Ltd., 90% of whose equity is owned by Trans Pacific Shipping Ltd.; | |

| ● | “Shares” refers to shares of our common stock, without par value per share; | |

| ● | “PRC” refers to the People’s Republic of China, excluding, for the purpose of this annual report, Taiwan, Hong Kong and Macau; | |

| ● | “US” refers to United States of America; | |

| ● | “HK” refers to Hong Kong; and | |

| ● | “RMB” or “Renminbi” refers to the legal currency of China, and “$” or “U.S. dollars” refers to the legal currency of the United States. |

Names of certain PRC companies provided in this Form 10-K are translated or transliterated from their original PRC legal names. Discrepancies, if any, in any table between the amounts identified as total amounts and the sum of the amounts listed therein are due to rounding.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Form 10-K contains certain statements that constitute “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Such forward-looking statements, including but not limited to statements regarding our projected growth, trends and strategies, future operating and financial results, financial expectations and current business indicators are based upon current information and expectations and are subject to change based on factors beyond our control. Forward-looking statements typically are identified by the use of terms such as “look,” “may,” “will,” “should,” “might,” “believe,” “plan,” “expect,” “anticipate,” “estimate” and similar words, although some forward-looking statements are expressed differently. The accuracy of such statements may be impacted by a number of business risks and uncertainties we face that could cause our actual results to differ materially from those projected or anticipated, including but not limited to the following:

| ● | Our ability to timely and properly deliver shipping agency, shipping and chartering, inland transportation management and ship management services; | |

| ● | Our dependence on a limited number of major customers and related parties; | |

| ● | Political and economic factors in China; | |

| ● | Our ability to expand and grow our lines of business; | |

| ● | Unanticipated changes in general market conditions or other factors which may result in cancellations or reductions in the need for our services; | |

| ● | The effect of terrorist acts, or the threat thereof, on consumer confidence and spending or the production and distribution of product and raw materials which could, as a result, adversely affect our services, operations and financial performance; | |

| ● | The acceptance in the marketplace of our new lines of services; | |

| ● | The foreign currency exchange rate fluctuations; | |

| ● | Hurricanes or other natural disasters; | |

| ● | Our ability to identify and successfully execute cost control initiatives; | |

| ● | The impact of quotas, tariffs or safeguards on our customer products that we service; | |

| ● | Our ability to attract, retain and motivate skilled personnel; or | |

| ● | Our expansion and growth into other areas of the shipping industry. |

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. The Company undertakes no obligation to update this forward-looking information. Nonetheless, the Company reserves the right to make such updates from time to time by press release, periodic report or other method of public disclosure without the need for specific reference to this Report. No such update shall be deemed to indicate that other statements not addressed by such update remain correct or create an obligation to provide any other updates.

| Item 1. | Business. |

Overview

Sino-Global Shipping America, Ltd. (“Sino” or the “Company”), a Virginia corporation, was founded in the United States (the “U.S.”) in 2001. Sino is a non-asset based global shipping and freight logistics integrated solution provider. Sino provides tailored solutions and value-added services to its customers to drive effectiveness and control in related aspects throughout the entire shipping and freight logistic chain. Our current service offerings consist of inland transportation management services, freight logistics services, and container trucking services. We suspended our shipping agency and ship management services from the beginning of the fiscal year 2016, primarily due to changes in market condition. We also suspended our shipping and chartering services primarily as a result of the termination of vessel acquisition in December 2015.

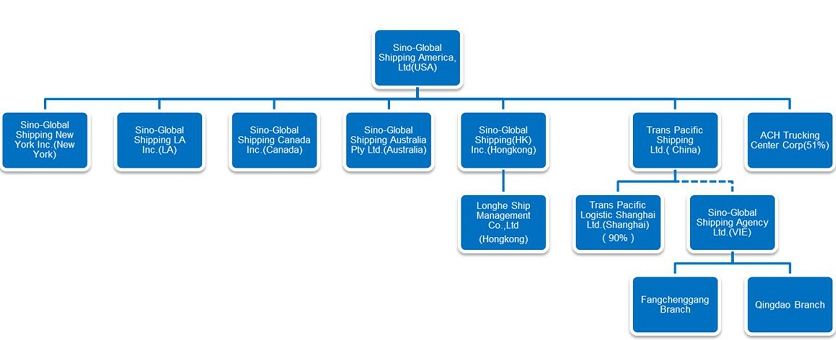

The Company conducts its business primarily through its wholly-owned subsidiaries in the U.S. (New York and Los Angeles), the People’s Republic of China (the “PRC” or “China”), including Hong Kong, Australia and Canada. Currently, a significant portion of our business is generated from the clients located in the PRC. In the third quarter of fiscal year 2017, the Company established ACH Trucking Center Corp. in New York as a joint venture with Jetta Global Logistics Inc. The Company owns 51% of ACH Trucking Center Corp.

Company Structure and Function

The Company conducts its business primarily through its wholly-owned subsidiaries in the U.S. (New York and Los Angeles), China (including Hong Kong), Australia, and Canada.

The Company’s subsidiary in China, Trans Pacific Shipping Limited (“Trans Pacific Beijing”), a wholly owned foreign enterprise, invested in one 90%-owned subsidiary, Trans Pacific Logistics Shanghai Limited (“Trans Pacific Shanghai”. Trans Pacific Beijing and Trans Pacific Shanghai are referred to collectively as “Trans Pacific”). As PRC laws and regulations restrict foreign ownership of local shipping agency service businesses, the Company provided its shipping agency services in the PRC through Sino-Global Shipping Agency Ltd. (“Sino-China” or “VIE”), a Chinese legal entity, which holds the licenses and permits necessary to operate local shipping agency services in the PRC. Trans Pacific Beijing and Sino-China do not have a parent-subsidiary relationship. Trans Pacific Beijing has contractual arrangements with Sino-China and its shareholders that enable the Company to substantially control Sino-China. Through Sino-China, the Company was able to provide local shipping agency services in all commercial ports in the PRC. In light of the Company’s decision not to pursue the local shipping agency business, the Company has suspended its shipping agency services through its VIE and has not undertaken any business through or with Sino-China since June 2014. Nevertheless, the Company continues to maintain its contractual relationship with the VIE because Sino-China is one of the committee members of China Association of Shipping Agencies & Non-Vessel-Operating Common Carriers (“CASA”). CASA was approved to form by China Ministry of Communications. Sino-China is also our only entity that is qualified to do shipping agency business in China. We keep the VIE to prepare ourselves for the market to turn around.

Currently, the Company’s inland transportation management services are operated by its subsidiaries in the PRC (including Hong Kong) and the U.S. Our freight logistic services are operated by the Company’s subsidiaries in the PRC, New York and Los Angeles. Our container trucking services are mainly operated by our subsidiaries and joint venture company in the PRC, New York and Los Angeles.

| 1 |

Corporate History and Our Business

Since inception in 2001 and through our fiscal year ended June 30, 2013, our sole business was providing shipping agency services. In general, we provided two types of shipping agency services: loading/discharging services and protective agency services, in which we acted as a general agent to provide value added solutions to our customers. For loading/discharging agency services, we received the total payment from our customers in U.S. dollars and paid the port charges on behalf of our customers in RMB. For protective agency services, we charged a fixed amount as agent fee while customers are responsible for the payment of port costs and expenses. Under these circumstances, we generally required a portion of a customer’s payment in advance and billed the remaining balance within 30 days after the transaction were completed. We believe the most significant factors that directly or indirectly affected our shipping agency service revenues were:

| ● | the number of ship-times to which we provide port loading/discharging services; | |

| ● | the size and types of ships we serve; | |

| ● | the type of services we provide; | |

| ● | the rate of service fees we charge; | |

| ● | the number of ports at which we provide services; and | |

| ● | the number of customers we serve. |

While we were able to consistently generate net revenues from shipping agency business, this business was not profitable largely due to the rising operating costs associated with doing business in China including the appreciation of RMB against U.S. dollar. In light of consecutive years of operating losses and concerns raised by the U.S. regulators over our VIE structure, the Company decided to reorganize its business structure in fiscal year 2013. Commencing the later part of fiscal year 2013 and continuing in fiscal year 2014, we took various actions to restructure our business with the goal of achieving a certain level of profitability. As a result of these business reorganization efforts, we optimized our cost structure, reduced our dependency on shipping agency business, and shifted our shipping agency operation from our VIE to our wholly-owned subsidiaries in China and Hong Kong.

In June 2013, the Company executed a 5-year global logistics service agreement with TEWOO Chemical & Light Industry Zhiyuan Trade Co., Ltd, which is controlled by Tianjin Zhiyuan Investment Group Co., Ltd (“Zhiyuan”). Zhiyuan is controlled by Mr. Zhong Zhang. Mr. Zhang purchased 1,800,000 shares of our common stock for approximately $3 million in April 2013 as approved by our Board of Directors and shareholders, which made Mr. Zhang our largest shareholder. Leveraging our business relationship with Zhiyuan, we expanded our service offerings to include shipping and chartering services and inland transportation management services to diversify our business. Leveraging our in-depth knowledge of the shipping industry, inland transportation management services are our tailored value-added solution developed for Zhiyuan to prevent high-priced bulk from damage or loss during its inland transportation from warehouses to factories. Given the industry norm of 12% of loss rate during transportation, our integrated inland transportation solution significantly reduces bulk losses and effectively addresses issues in the freight logistics chain. In August 2017, the Company entered into a supplemental agreement with Zhiyuan to extend the service period until September 1, 2018. Furthermore, after we have conducted an effective trial for Zhiyuan to reduce their bulk losses at the end of September 2014, Tengda Northwest Ferroalloy Co., Ltd. (“Tengda Northwest”) signed a contract with us to mitigate their bulk losses through our inland transportation management services. In July 2017 the Company entered into a supplemental agreement with Tengda Northwest to extend the service period until July 3, 2018.

In May 2014, the Company signed a strategic cooperation agreement with Qingdao Zhenghe Shipping Group Limited (“Zhenghe”), one of the largest shipping and transportation companies in China, to jointly explore mutually beneficial business development opportunities. In June 2014, Mr. Deming Wang, a major owner of Zhenghe, acquired 200,000 shares of the Company’s common stock. In August 2014, the Company executed an agreement to acquire all of the equity of Longhe Ship Management (Hong Kong) Co., Limited (“LSM”) through its subsidiary, Sino-Global Shipping (HK) Inc. from Mr. Wang, to further broaden our scope of services and expertise in the ship management business. Due to market condition and high operating costs associated with this business line, the Company decided to suspend the ship management business starting from the fiscal year 2016.

On April 10, 2015, the Company entered into an Asset Purchase Agreement with Rong Yao International Shipping Limited, a Hong Kong company (the “Vessel Seller”), pursuant to which the Company agreed to acquire, subject to a number of closing conditions, “Rong Zhou”, an 8,818 gross tonnage oil/chemical transportation tanker (the “Vessel”) from the Vessel Seller; and in connection therewith, the Company issued to the Vessel Seller 1.2 million shares of its restricted common stock representing $2,220,000 of the $10.5 million purchase price for the Vessel. On December 7, 2015, the Company and the Vessel Seller entered into a supplemental agreement to terminate the proposed Vessel acquisition.

The Company received $330,000 from the Vessel Seller in December 2015 in connection with the termination. The 1.2 million shares were returned to the Company on February 12, 2016 and were thereafter cancelled. In connection with the termination of the acquisition of Rong Yao International Shipping Limited (“Rong Yao”) on December 7, 2015, the Company realigned its development strategy and suspended shipping and chartering services until the economy is improved.

| 2 |

In January 2016, the Company formed a new subsidiary, Sino-Global Shipping LA Inc. (“Sino LA”), for the purpose of expanding its business to provide import security filing services with U.S Customs and Department of Homeland Security, on behalf of importers who ship goods into the U.S. and also providing inland transportation services to these importers in the U.S. On April 18, 2016, Sino LA signed a Memorandum of Understanding (“MOU”) with Yaxin International Co., Ltd. (“Yaxin”), pursuant to which Sino LA will provide logistics services to Yaxin, who ship goods via containers into the U.S. and places them on Amazon.com. The services include cargo forwarding, customs filing and declaration, trucking and other services.

In May 2016, the Company entered into a strategic partnership with Shandong Hi-speed TEU Logistics Co., LTD. (“Shandong Hi-speed TEU”), which belongs to one of China’s largest state-owned enterprises, Shandong Hi-Speed Group Co., Ltd., to jointly establish a platform for coordinated transport between China and North America. The Company and Shandong Hi-speed TEU intend to cooperate in creating a standardized network that will unite carriers of the twenty-foot equivalent units or TEUs in China via sea and rail and coordinate with parties in North America and Australia. The companies will serve both upstream and downstream customers through the platform, establish a door-to-door logistics and provide supply chain service.

During our fiscal year 2017, Sino continued to provide inland transportation services. In addition, Sino added freight logistics services and container trucking services as new business sectors to provide related transportation logistics services to customers in the U.S. and in China. Sino has signed cooperation agreements with COSCO China and Sinotrans, two state-owned enterprises of China, to provide freight logistics services and container trucking services to them in the U.S. To ensure effective and high-quality services providing to our customers in the U.S., Sino established a joint venture, ACH Trucking Center Corp., in the third quarter of fiscal 2017 with U.S. local freight forwarder, Jetta Global Logistics Inc. This will increase our quantities of commodity transported and improve the quality of service provided to our customers in the eastern region of the U.S.

Our Strategy

Our strategy is to:

| ● | Provide better solutions for issues and challenges faced by the entire shipping and freight logistic chain to better serve our customers and explore additional growth avenues. |

| ● | Diversify our current service offerings organically or through acquisitions and/or strategic alliance; continue to grow our business in the U.S. market; |

| ● | Continue to streamline our business practice, optimize our cost structure and improve our operating efficiency through effective planning, budgeting, execution and cost control; |

| ● | Continue to reduce our dependency on our legacy business and few key customers; and |

| ● | Continue to monetize our relationships with our strategic partners and leverage their support and our innovation to expand our business. |

Our Management Team

We believe we have a strong and experienced management team including our Chief Executive Officer and Chairman, Mr. Lei Cao; our Acting Chief Financial Officer, Ms. Tuo Pan; our Chief Operating Officer, Mr. Zhikang Huang; and our Chief Technical Officer, Mr. Yafei Li, who, together as a team, have many years of experience, extensive business connections in the shipping industry in China, and substantial experience in SEC reporting and compliance, business reorganization, mergers and acquisitions, accounting, risk management and operations of both public and private companies.

| 3 |

Business Segments

As of June 30, 2017, Sino-Global delivers inland transportation management services, freight logistics services and container trucking services to our customers.

Historically, the Company was in the business of solely providing shipping agency services. In fiscal year 2014, by leveraging the support of Sino-Global’s largest shareholder, Mr. Zhang and the company he controls, Zhiyuan Investment Group, the Company expanded its service platform to include shipping and chartering services during the quarter ended September 30, 2013 and inland transportation management services during the quarter ended December 31, 2013. We suspended shipping and chartering services as a result of the termination of the vessel acquisition in December 2015. With the acquisition of LSM in 2014, we added ship management services to our service platform but we suspended it together with shipping agency services in 2016 primarily due to market conditions. With the establishment of Sino-LA, we added cargo forwarding services to our service platform in the second quarter of fiscal 2017, which is included in our inland transportation business line at the end of June 30, 2016. As we are developing our cargo forwarding services, the Company provides freight logistics services and container trucking services as two new business segments during this fiscal year.

Our Goals and Strategic Plan

By leveraging our fine reputation, extensive business relationships, technical ability and in-depth knowledge of the shipping industry, our goal is to further strengthen our position as a leading global logistic solution provider who offers innovative resolutions to better address complex issues in different aspects in the entire shipping and freight logistic chain.

We historically focused our business on providing our customers with customized shipping agency services. In the past, our business came predominately from our strong business relationships with our key strategic partners in China. To reduce our dependency on a single business line, we have leveraged, and will continue to leverage, our business relationships with strategic partners to introduce new service offerings to the market and to diversify our business. In light of the slowdown of the Chinese economy and its negative impact on the shipping business across Pacific Ocean, our strategic plan for the next 5 years is to continue to diversify our service mix and actively seek new growth opportunities to expand our business footprint in the U.S. market to reduce our dependency on the revenue generated from China. For decades, the shipping industry has been operated under traditional business models without many meaningful changes. Today, technological innovation has already played a big role in changing every conventional industry. We believe the internet will be a big part of the future logistics chain services and a transformative era in shipping and freight logistic business is coming. As an innovative solution provider, we plan to apply our technical ability, industry expertise and cutting-edge information technology in the conventional shipping business to better connect supply and demand and to develop seamless linkages in logistic chains.

After going through one and half years on our business restructuring, Sino changed its business models from providing traditional shipping agency services to providing solutions and services focused on inland transportation logistics between the U.S. and China, such as providing freight logistics services or container trucking services. As a result of our continued restructuring efforts, we turned an operating loss for the year ended June 30, 2016 to a profit for the year ended June 30, 2017. As shown in the table below, our current business operating revenue is primarily focused on inland transportation management services as compared to the two previous fiscal years.

| Fiscal Year 2017 | Fiscal Year 2016 | Fiscal Year 2015 | ||||||||||||||||||||||

| Key Services | Revenue | % | Revenue | % | Revenue | % | ||||||||||||||||||

| Shipping Agency & Ship Management | $ | - | - | $ | 2,507,800 | 34 | % | $ | 6,185,653 | 55 | % | |||||||||||||

| Shipping & Chartering | - | - | 462,218 | 7 | % | 349,125 | 3 | % | ||||||||||||||||

| Inland Transportation Management | 5,758,600 | 50 | % | 4,340,522 | 59 | % | 4,785,850 | 42 | % | |||||||||||||||

| Freight Logistic Services | 4,815,450 | 42 | % | - | - | - | - | |||||||||||||||||

| Container Trucking Services | 871,563 | 8 | % | - | - | - | - | |||||||||||||||||

| Total | $ | 11,445,613 | 100 | % | $ | 7,310,540 | 100 | % | $ | 11,320,628 | 100 | % | ||||||||||||

The business restructuring of Sino is gradually on track. During this process, we will continue to adjust and develop our strategic plans based on the change of business environment. In the future, we will provide more services to our customers, and we will use our internet platform to connect our worldwide businesses to our customers.

| 4 |

Our Customers

In light of our strategic relationship with Zhiyuan Investment Group that began with the signing of a 5-year global logistics service agreement in June 2013, we expanded our business platform to include additional service offerings. We started to provide inland transportation management services to a third-party customer, Tengda Northwest Ferroalloy Co., Ltd. (“Tengda Northwest”), during the quarter ended September 30, 2014. As we continue to diversify our service platform, we have reduced our dependency on a few customers which we provide freight logistics and container trucking services.

For the year ended June 30, 2017, three customers accounted for 26%, 24% and 19% of the Company’s revenues, respectively. For the year ended June 30, 2016, two customers accounted for 31% and 27% of the Company’s revenues, respectively.

Our Suppliers

Our operations consist of working directly with our customers to understand in detail their needs and expectations and then managing local suppliers to ensure that our customers’ needs are met. Our major suppliers include Oldendorff Carriers, Baoshan Iron and Steel Co., Ltd. and Shanghai Gangcheng Dangerous Goods Logistics Co., Ltd. For the year ended June 30, 2017, two suppliers accounted for 42% and 11% of the total cost of revenue, respectively. For the year ended June 30, 2016, three suppliers accounted for 27%, 15% and 10% of the total cost of revenues, respectively.

Our Strengths

We believe that the following strengths differentiate us from our competitors:

| ● | Proven industry experience and problem-solving reputation. We are a non-asset based global shipping and freight logistics solution provider. Unlike a traditional shipping agent, we provide tailored solutions and value-added services to our customers to drive effectiveness and control in related aspects throughout the entire shipping and freight logistic chain. We believe that our years of successful track record of applying integrated solutions to complex issues in the global shipping logistics business gives us a competitive advantage in attracting large clients and helps us maintain strong long terms business relationship with them. |

| ● | Strong leadership and a competent professional team. Our CEO is an industry veteran with more than thirty years of extensive industry experiences including ten years’ working for COSCO, one of the largest shipping companies in the world. Most of our employees have marine business experience, and many of our managers/chief operators served in other large Chinese shipping companies prior to joining us. With these professionals and experienced staff, we believe that we provide the best services to our customers at competitive prices. |

| ● | Extensive network and positive industry recognition. Doing business in China often requires a strong business network and support of key strategic partners. The Company served as one of the executive directors of China Association of Shipping Agencies & Non-Vessel-Operating Common Carriers (CASA), the authoritative industry association in China. We are the only non-state-owned enterprise represented on the CASA board guiding the development of the industry. Our good reputation and industry recognition enables us to maintain strong relationships with our business partners and have an extensive network of contacts throughout the industry, which helps us gain necessary support to execute our business plans. |

| 5 |

| ● | Lean organization and a flexible business model. Although we are a small business with limited resources, we have a cohesive and effective organizational structure with the goal of maximizing customer value while minimizing waste. Our unique flexible business model allows us to quickly respond to changing market demand and offer our customers innovative problem-solving solutions, quality customer service, and competitive prices to achieve greater market acceptance and gain additional market share. |

| ● | U.S.-registered and NASDAQ-listed public company. We believe our status as a U.S. corporation gives us more credibility among existing and potential customers, suppliers, and other business partners than a privately owned company would have in our industry. Our ability to raise capital through the capital market or use our common stock as “currency” to facility potential merger and acquisition transactions can also help us carry out or accelerate our growth strategies. |

Our Opportunities

For more than thirty years, the shipping and freight logistic industry has been operated under traditional business models without meaningful change. Many of these business practices are inefficient and problematic; therefore, maintaining an innovative mindset is critical to achieving continuous business success and growth. We are a value-added logistics solution provider with successful past performance and individuals that have been in the industry for a long time. Instead of playing the traditional logistics broker role, we focus on providing technology solutions and innovative leading-edge services to bridge the asset-based world with the digital world. We shape our industry practice and profit model by analyzing wider developments both in the global markets and the technology industry so we can address unique problems that are currently pervasive across the shipping and freight logistics industry.

We believe we can capture the business opportunity and grow our business organically or through acquisitions or strategic alliance by:

| ● | Continuing to streamline our business operations and improve our operating efficiency through innovative technology, effective planning, budgeting, execution and cost control; |

| ● | Restructuring our business to focus on providing innovative technology based solution to our customers to promote our sustainable business growth; |

| ● | Developing new service lines along the shipping and freight logistic industry value chain, and leveraging our relationships with COSCO, Zhiyuan Investment Group and other potential strategic business partners to expand our global business footprint. |

Our Challenges

We face significant challenges when executing our strategy, including:

| ● | Given the complexity and length of restructuring our business, we face the challenge of generating sufficient cash from our current business activities to support our daily operations during the transition; |

| ● | We may not be able to establish a separate department to solve critical issues in today’s shipping logistics industry; |

| ● | We may not have or not be able to get the necessary funds to continue to expand our service and market our services successfully; |

| ● | Our ability to respond to increasing competitive pressure on our growth and margins; |

| ● | Our ability to gain further expertise and to serve new customers in new service areas; |

| ● | From time to time, we may have difficulty carrying out services effectively and in a profitable way due to the cyclical nature of the shipping industry, which could lead to a prolonged period of sluggish demand for our services; |

| ● | Our ability to respond promptly to a changing regulatory environment, macroeconomic conditions, industry trends, and competitive landscape; and |

| ● | Developing a winning business model takes time and a new business model may not be recognized by the market immediately. As a publicly traded company, management may be forced to fulfill near-term performance goals that may not be consistent with the Company’s long-term vision. |

Our Competition

The market segments that we serve do not have high entry barriers. There are many companies ranging from small to large in China that provide shipping and freight-related logistics services. At present, the state-owned companies in China still dominate the industry and generate a majority of the revenues in the industry. These companies have greater service capabilities, a larger customer base and more financial, marketing, network and human resources than we do. Most of them concentrate their business on shipping agency services to meet general market demand. However, we focus on providing tailored solutions and value-added services to select high-profile customers to drive effectiveness and control in related aspects throughout the entire shipping and freight logistic chain. As a boutique company that provides specialized services with limited resources and history, we face intense competition in the particular market segments that we serve. Our ability to be successful in our industry depends on our deep understanding of the complexity of industry issues and challenges and our technical ability to develop best solutions to respond to the identified issues and provide effective problem-solving strategies to our targeted customers to achieve the fastest and most cost-effective outcomes. Our value-added services and innovative approaches are highly recognized by our customers, which helps us to gain additional market share and compete effectively with the companies that may be better capitalized than we are or may provide services we do not or cannot provide to our customers.

| 6 |

Employees

As of the date of this report, we have 24 employees, 14 of whom are based in China. Of the total, four are in management, twelve are in operations, five are in finance and accounting and three are in administration and technical support. We believe that our relationship with our employees is good. We have never had a work stoppage, and our employees are not subject to a collective bargaining agreement.

Recent Development

Sino has signed joint project agreements with Sinotrans Guangxi and COSFRE Beijing during the fourth quarter of fiscal year 2017. The project will involve a shift from the current bulk cargo transportation model to a containerized model. The Company has started a trial by facilitating the delivery of Sulphur from Long Beach, California, in the U.S., to Fangcheng Port, Guangxi, PRC and ultimately to the warehouse of the customer. At the end of the fiscal year 2017, there was no revenue or cost of revenue recognized from this business model. Management expects the transportation of cargo via a containerized model will become a new business segment in incoming years.

On August 24, 2017, Sino signed a marketing promoting service agreement with COSCO Qingdao. According to this agreement, COSCO Qingdao will help Sino to promote shipping and multimodal transportation, including inland trucking container transportation services, switch bill of lading and freight collection services.

Sino plans to establish a subsidiary in Ningbo, China, to connect with local small commodities businesses to establish overseas warehouses for them. Sino will provide a service model similar to Amazon, including unloading commodities from the U.S. ports, providing transportation services, providing warehouse space in the U.S., and providing inland transportation logistics services to the door of the end customers.

| Item 1A. | Risk Factors. |

This item is not applicable to a smaller reporting company such as us.

| Item 1B. | Unresolved Staff Comments. |

The Company does not have any unresolved or outstanding Staff Comments.

| Item 2. | Properties. |

We currently rent five facilities in the PRC, Hong Kong and the United States. Our PRC headquarter is in Beijing, and our U.S. headquarter is in New York.

| Office | Address | Rental Term | Space | |||

| Beijing, PRC | Room 502, Tower C YeQing Plaza No. 9, Wangjing North Road Chaoyang District Beijing, PRC 100102 |

Expires 12/14/2017 | 160 m 2 | |||

| Shanghai, PRC | Rm 12D & 12E, No.359 Dongdaming Road, Hongkou District, Shanghai, PRC 200080 |

Expires 07/31/2018 | 285.99 m 2 | |||

| New York, USA | 1044 Northern Boulevard, Suite 305 Roslyn, New York 11576-1514 |

Expires 08/31/2019 | 179 m 2 | |||

| Hong Kong | 20/F, Hoi Kiu Commercial Building, 158 Connaught Road Central, HK |

Expires 05/17/2019 | 77 m 2 | |||

| Los Angeles, USA | 21680 Gateway Center Drive, Suite 330 Diamond Bar, California 91765 |

Expires 04/30/2020 | 121.24 m2 |

| Item 3. | Legal Proceedings. |

From time to time, we may become involved in various lawsuits and legal proceedings, which arise in the ordinary course of business. However, litigation is subject to inherent uncertainties, and an adverse result in these or other matters may arise from time to time and may harm our business. However, we are currently not aware of any such legal proceedings or claims that we believe will have, individually or in the aggregate, a material adverse effect on our business, financial condition or operating results.

| Item 4. | Mine Safety Disclosures. |

This item is not applicable to the Company.

| 7 |

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. |

Market for Our Common Stock

Our common stock is traded on the NASDAQ Stock Market under the symbol SINO. The high and low common stock sales prices per share during the periods indicated were as follows:

| Quarter Ended | Sep. 30 | Dec. 31 | Mar. 31 | June 30 | Year | |||||||||||||||

| Fiscal year 2017 | ||||||||||||||||||||

| Common stock price per share: | ||||||||||||||||||||

| High | $ | 2.24 | $ | 6.73 | $ | 4.70 | $ | 3.45 | $ | 6.73 | ||||||||||

| Low | $ | 0.64 | $ | 0.97 | $ | 2.34 | $ | 2.57 | $ | 0.64 | ||||||||||

| Fiscal year 2016 | ||||||||||||||||||||

| Common stock price per share: | ||||||||||||||||||||

| High | $ | 1.60 | $ | 1.29 | $ | 0.88 | $ | 1.33 | $ | 1.60 | ||||||||||

| Low | $ | 0.81 | $ | 0.69 | $ | 0.40 | $ | 0.58 | $ | 0.40 | ||||||||||

Approximate Number of Holders of Our Common Stock

As of September 12, 2017, there are 7 holders of record of our common stock. This number does not include shareholders who hold their shares of common stock in street name.

Dividend Policy

We have never declared or paid any cash dividends on our common stock. We anticipate that we will retain any earnings to support operations and to finance the growth and development of our business. Therefore, we do not expect to pay cash dividends in the foreseeable future. Any future determination relating to our dividend policy will be made at the discretion of our Board of Directors and will depend on a number of factors, including future earnings, capital requirements, financial conditions and future prospects and other factors the Board of Directors may deem relevant. Payments of dividends by Trans Pacific to our company are subject to restrictions including primarily the restriction that foreign invested enterprises may only buy, sell and/or remit foreign currencies at those banks authorized to conduct foreign exchange business after providing valid commercial documents.

Recent Sales of Unregistered Securities and Issuer Purchases of Equity Securities

Recent Sales of Unregistered Securities

In March 2017, the Company entered into a consulting and advisory services agreement with Jianwei Li, who will provide management consulting services that include marketing program, designing and implementation, and cooperative partner selection and management. The service period is from March 2017 to February 2020. The Company issued 250,000 shares of common stock as the remuneration of the service in reliance on the exemption under Section 4(2) of the Securities Act, which were issued as restricted shares on March 22, 2017.

| 8 |

Other Information

On July 26, 2016, the Company granted options to purchase an aggregate of 150,000 shares of common stock to two employees with a two-year vesting period, one half of which shall vest on October 26, 2016, and the other half shall vest on July 26, 2017. The exercise price of such options was $1.10 per share. Please refer to Item 12 for the table on Equity Compensation Plan Information, which is incorporated by reference herein.

On December 14, 2016, the Company granted a total of 800,000 options to purchase an aggregate of 800,000 shares of Common Stock to seven employees, with a vesting period from one to three years. With the seven employees’ consent, the Company cancelled the 800,000 options, effective February 16, 2017 and nil was recorded as part of general and administrative expenses related to these options for the year ended June 30, 2017.

| Item 6. | Selected Financial Data |

The Company is not required to provide the information required by this item because the Company is a smaller reporting company.

| Item 7. | Management’s Discussion and Analysis or Plan of Operation. |

The following discussion and analysis of our company’s financial condition and results of operations should be read in conjunction with our audited consolidated financial statements and the related notes included elsewhere in the Annual Report. This discussion contains forward-looking statements that involve risks and uncertainties. Actual results and the timing of selected events could differ materially from those anticipated in these forward-looking statements as a result of various factors.

Overview

Fiscal year 2017 Highlights

Sales for the year ended June 30, 2017 increased by $4,135,073, or 56.6%, from $7,310,540 for the year ended June 30, 2016, to $11,445,613 for the comparable period in 2017. The increase was mainly due to:

| ● | The Company’s subsidiary, Trans Pacific Shanghai, began providing container trucking services in the second quarter of fiscal year 2017. In addition to the launch of our full-service logistics platform, Trans Pacific Shanghai signed a service agreement with Shanghai International Port (Group) Co. Ltd., resulting in a significant increase in the subsidiary’s revenues. Trans Pacific Shanghai’s revenues generated by its container trucking services and revenues from freight logistic services were $573,341 and $2,964,226 for the year ended June 30, 2017, respectively. |

| ● | Pursuant to the Strategic Cooperation Agreement signed with COSCO Logistics (Americas) Inc. (“COSCO Logistics”), in July 2016, starting in the third quarter of fiscal year 2017, the Company’s subsidiary in Los Angeles, California began providing freight logistic services and container trucking services to COSCO Logistics. |

| ● | Pursuant to an agreement signed in December 2016, the Company and Jetta Global Logistics Inc. (“Jetta Global”) established ACH Trucking Center Corp. (“ACH Center”), a joint venture based in New York that provides trucking services. During the year ended June 30, 2017, ACH Center began to provide freight logistics services and container trucking services to COSCO Beijing International Freight Co., Ltd. (“COSFRE Beijing”) in the New York and New Jersey areas. |

| 9 |

| ● | As an extension of the two agreements the Company signed with Sinotrans Guangxi and COSFRE Beijing, Sino has signed joint project agreements with Sinotrans Guangxi and COSFRE Beijing during the fourth quarter of fiscal year 2017. The project will involve a shift from the current bulk cargo transportation model to a containerized model. The Company has started a trial by facilitating the delivery of Sulphur from Long Beach, California, in the U.S., to Fangcheng Port, Guangxi, PRC and ultimately to the warehouse of the customer. By the end of the fiscal year 2017, there was no revenue or cost of revenue recognized from this business model. Management expects the transportation of cargo via a containerized model to become a new business segment in incoming year. |

On February 16, 2017, the Company raised capital by issuing 1.5 million shares of common stock to three institutional investors at a purchase price of $3.18 per share. The aggregate gross proceeds of the sale to the Company totaled $4.77 million, and net proceeds after deducting offering expenses and placement agent fees equaled approximately $4.3 million. The Company will use the funds for working capital and general corporate purposes.

Other 2017 Highlights:

| ● | In July 2016, the Company signed a Strategic Cooperation Agreement with COSCO Logistics, which is owned by the PRC’s largest integrated shipping company, China COSCO Holdings Company Ltd. Pursuant to the agreement, both parties will provide logistics services between the PRC and the U.S. and develop shipping customers as an end-to-end global logistics service. Starting in the third quarter of fiscal year 2017, the Company and COSCO Logistics began providing container trucking services on the west coast of the U.S. The Company expects to increase its cooperation with COSCO Logistics and to provide inland transportation services in the U.S. for shipments to and from the PRC. According to the agreement, the two companies will also assess locations in the U.S. to potentially establish warehouse and/or distribution facilities in the coming months and share pricing information for short-haul trucking services across selected regions of the U.S. |

| ● | In December 2016, the Company completed the development of its full-service logistics platform, and a website portal to seamlessly connect shipping customers with short-haul trucking transportation services throughout the U.S. is now accessible through the Company’s website. In connection with the new platform, the Company signed strategic cooperation agreements with one major Chinese shipping company, China Ocean Shipping Company (“COSCO”) (consisting of both COSFRE Beijing and COSCO Qingdao) in December 2016 and January 2017. We believe that the Company’s cooperation with COSCO will increase door-to-door short-haul trucking volumes and boost revenues from inland transportation services in the U.S. |

| ● | On April 20, 2017, the Company signed a Strategic Cooperation Agreement with Ningbo Xinyang Shipping Co., Ltd (“COSCO Xinyang”). This agreement with COSCO Xinyang is a continuation of the Company’s ongoing partnership with COSCO. Pursuant to the agreement with COSCO Xinyang, which is similar with the Company’s previously announced inland transportation agreements with COSCO; Sino-Global will receive a percentage of the total amount of each transportation fee for arranging inland transportation services for COSCO Xinyang’s container shipments into U.S. ports. The Company continues to work to expand its business to provide logistics services to customers who ship goods into the U.S. |

| 10 |

Fiscal year 2018 Trends

In the fiscal year of 2018, we will continue marketing ourselves to state-owned shipping companies in the PRC, promoting our inland transportation services in the PRC as well as freight logistics and container trucking services in both the PRC and the U.S., and using containers for our bulk shipping projects. In the interim, we will continue to establish our services network in the U.S. in order to increase our revenues and leverage our fundamentals using our new profit model, i.e., developing inland transportation services (including freight logistics and container tracking service). Since Sino began its business restructuring in 2017, the business channels between the U.S. and China have been established, and we are currently at the stage of filling in substantial business. This stage mainly involves the following three aspects:

1.) For goods exported from China to the U.S., Sino will provide inland transportation services in the U.S.

2.) For small commodity exports from China to the U.S., Sino will provide services similar to that of Amazon.com by helping small commodity traders in China establish warehouses in the U.S. and providing inland transportation services and other value-added services to them, including: the receipt of commodities at U.S. ports, transportation of commodities, providing warehouse space in the U.S., and logistical services to the door of the final customers.

3.) For those products or commodities exported from the U.S. to China, such as grain and grain by-products and petroleum by-products, Sino will provide container transportation services.

Sino plans to set up business channels between the U.S. and Australia, Singapore and Thailand during fiscal year 2018. The Company expects to provide shipping and multimodal transportation, including inland container trucking transportation services, switch bill, and freight collection services to importers and exporters between the U.S. and Australia, Singapore and Thailand.

Results of Operations

Revenues

Total revenues increased by $4,135,073, or 56.6%, from $7,310,540 for the year ended June 30, 2016 to $11,445,613 for the comparable period in 2017. This increase was primarily due to the Company’s efforts to diversify its business in the inland transportation management, freight logistic, and container trucking services, resulting in an increase in revenues since the first and second quarters of fiscal year 2017. The increase was partially offset by the decreased revenue from shipping agency and ship management services sector due to the decrease in the number of ships served, and the decreased revenue from our shipping and chartering services sector as a result of the termination of a planned vessel acquisition.

The following tables present summary information by segment for the years ended June 30, 2017 and 2016:

| For the year ended June 30, 2017 | ||||||||||||||||||||||||

| Shipping Agency and Ship Management Services | Shipping and Chartering Services | Inland Transportation Management Services | Freight Logistic Services | Container Trucking Services | Total | |||||||||||||||||||

| Revenues | ||||||||||||||||||||||||

| - Related party | $ | - | $ | - | $ | 2,746,423 | $ | - | $ | - | $ | 2,746,423 | ||||||||||||

| - Third parties | $ | - | $ | - | $ | 3,012,177 | $ | 4,815,450 | $ | 871,563 | $ | 8,699,190 | ||||||||||||

| Cost of revenues | $ | - | $ | - | $ | 620,259 | $ | 3,710,364 | $ | 649,968 | $ | 4,980,591 | ||||||||||||

| Gross profit | $ | - | $ | - | $ | 5,138,341 | $ | 1,105,086 | $ | 221,595 | $ | 6,465,022 | ||||||||||||

| GM% | - | % | - | % | 89.2 | % | 22.9 | % | 25.4 | % | 56.5 | % | ||||||||||||

| For the year ended June 30, 2016 | ||||||||||||||||

| Shipping Agency and Ship Management Services | Shipping and Chartering Services | Inland Transportation Management Services | Total | |||||||||||||

| Revenues | ||||||||||||||||

| - Related party | $ | - | $ | - | $ | 2,269,346 | $ | 2,269,346 | ||||||||

| - Third parties | $ | 2,507,800 | $ | 462,218 | $ | 2,071,176 | $ | 5,041,194 | ||||||||

| Cost of revenues | $ | 2,175,109 | $ | 212,510 | $ | 1,350,370 | $ | 3,737,989 | ||||||||

| Gross profit | $ | 332,691 | $ | 249,708 | $ | 2,990,152 | $ | 3,572,551 | ||||||||

| GM % | 13.3 | % | 54.0 | % | 68.9 | % | 48.9 | % | ||||||||

| 11 |

Revenues

(1) Revenues from Shipping Agency and Ship Management Services

For the years ended June 30, 2017 and June 30, 2016, our revenues generated from the shipping agency segment were nil and $2,507,800, respectively. As the Company has stated in its previous annual report for the fiscal year ended June 30, 2016, management decided to suspend the shipping agency services because the shipping industry is experiencing a downturn. The decline in revenues in this service sector was due to this suspension. As a result, there was a decrease in the total number of ships the Company served from 19 ships for the year ended June 30, 2016 to nil for the year ended June 30, 2017. Our decision to suspend our shipping agency business was based on reduced market demand for imported iron ore as a result of an across-the-board general economic slow-down, decreased manufacturing activities, rising labor costs in the PRC and intense competition in the shipping industry with established and new competitors offering rates that in many cases are lower than the rates we can offer. Rising labor costs and increased overhead costs also reduced our profitability in this segment. However, we plan to resume providing shipping agency services once the shipping industry outlook turns positive.

We did not generate any revenue from providing ship management services for the years ended June 30, 2017 and 2016 as management decided to suspend the ship management business segment at the beginning of fiscal year 2016.

(2) Revenues from Shipping and Chartering Services

In connection with the termination of the acquisition of Rong Yao International Shipping Limited (“Rong Yao”) on December 7, 2015, the Company realigned its development strategy and temporarily suspended its shipping and chartering services. As a result, we reported nil and $462,218 in revenue from this segment for the years ended June 30, 2017 and 2016, respectively.

Temporary suspension of the two above business sectors are not treated as discontinued operations since management believes they will continue to operate through these segments once the shipping business market recovers and the overall economy improves. Management is still actively identifying new potential relationships with targets for generating ship management service revenue, as well as developing the shipping agency sales network. The Company has also retained the employees who previous handled the business in relation to these two sectors. Although there is no current revenue from these two business sectors, the employees who previously were employed in the shipping agency and ship management business currently participate in the organization and development of inland transportation management services, freight logistics services and container trucking services. Once the shipping agency and ship management services and shipping and chartering services restarts again, the employees who previously worked for these sectors will revert to their previous positions to service theses business segments.

| 12 |

(3) Revenues from Inland Transportation Management Services

In September 2013, the Company executed an inland transportation management service contract with Zhiyuan Investment Group, a related party, whereby the Company agreed to provide certain solutions to help control the potential loss of commodities during the transportation process. The Company also began providing inland transportation management services to a third-party customer, Tengda Northwest, following the quarter ended September 2014. As a result, for the years ended June 30, 2017 and 2016, inland transportation management services revenue generated from related-party was $2,746,423 and $2,269,346, respectively, and revenue generated from third-party was $3,012,177 and $2,071,176, respectively. For the years ended June 30, 2017 and 2016, gross profits from inland transportation management services amounted to $5,138,341 and $2,990,152, respectively.

The increase in total revenues from this segment is due to the increase in the amount of commodities transported through both Zhiyuan Investment Group and Tengda Northwest. For Tengda Northwest, the service fee was RMB 32 per ton. Transported quantities were 648,739 tons for the year ended June 30, 2017 compared to 365,104 tons for the year ended June 30, 2016. For Zhiyuan Investment Group, the service fee was RMB 38 per ton. Transported quantities were 498,210 tons for the year ended June 30, 2017 compared to 442,757 tons for the year ended June 30, 2016.

Overall gross margin for this segment increased to 89.2% for the year ended June 30, 2017 from 68.9% for the year ended June 30, 2016. The increase in gross margin is mainly due to:

| 1) | Increased efficiency: When the Company takes in a new customer in this segment, the majority of the costs are incurred upfront when the Company uses its professional expertise to assist the customer in setting up efficient and sound procedures and policies to minimize losses in the transportation process. Once the process is set up, marginal cost is needed as the Company is only required to spend labor costs to monitor and improve the operation process and handling specific issues as needed.

The component of the costs associated with inland transportation management services is primarily the salaries of the employees who are assigned to maintain the transportation services. The logistic transportation fees made directly by the end customers to the logistics companies. During the door-to-door transportation progress, the assigned personnel will monitor the progress of transportation, coordinate with the logistics companies and warehouses in order for the products to be transported safely to the agreed destination. The Company has been providing such business services since 2014. Throughout the three years of development, the employees familiarized with the tasks in providing such services and the Company’s network with those logistics companies has matured. The Company has also become more effective and efficient in handling such business. During the year ended June 30, 2017, only two employees in Beijing and Hong Kong were authorized by management in Company headquarters to spend a limited number of hours per day handling inland transportation services. For the same period in 2016, a greater number of employees were assigned to work on such services. The cost of revenues for providing inland transportation management services are measured based on the number of hours allocated to perform such services. As the number of employees assigned for the services decreased and the hours assigned for each employee per day also decreased, the total hours related to perform such services decreased accordingly, which led to the significant decrease in cost of revenues. |

| 2) | Increased transportation volume: Due to the increase of price in Chrome ore and Chrome iron in the commodity market, our customers have increased demand for shipments resulting increased transportation volume we managed. As discussed above, no substantial costs were incurred to handle the extra volume; economies of scale led to further increases of our gross margin. |

(4) Revenues from Freight Logistic Services

Since we formed our new subsidiary, Sino-Global Shipping LA, Inc., in January 2016, we began providing freight logistic services, including cargo forwarding and truck transportation services. During the year ended June 30, 2017, the portion of revenues generated from freight logistic services has increased significantly, and the Company presents the related revenue as a separate business segment. The Company has signed agreements with non-related parties, LJC Trading New York Ltd. and Zhiyuan (Hong Kong) Chromium Group Co., to provide freight logistic services.

| 13 |

Pursuant to the strategic cooperation agreement with COSCO Logistics, signed in July 2016, Sino-Global Shipping LA, Inc. began to provide logistic services to COSCO Logistics beginning the third quarter of fiscal year 2017. These services include cargo forwarding, trucking and customs declaration and filings.

In the third quarter of fiscal year 2017, the Company entered into an agreement with COSFRE Beijing, pursuant to which the Company formed a new joint venture company, ACH Trucking Center, with Jetta Global to provide short-haul trucking transportation and freight logistics services to customers located in the New York and New Jersey areas. Benefitting from the Company’s new logistics platform, strategic cooperation with COSCO Logistics and the new joint venture, revenue generated from freight logistic services was $4,815,450, and the related gross profit was $1,105,086 for the year ended June 30, 2017.

(5) Revenues from Container Trucking Services

Since we completed our website version of short distance container truck service platform in December 2016, we began to generate revenue from short distance trucking and containers services through the service platform and presents this as a new segment, “Container Trucking Services” beginning in the second quarter of 2017. Since the second quarter of fiscal year 2017, the Company has provided container trucking services in the PRC, and began to provide related services in the U.S. beginning in the third quarter of fiscal year 2017. This new business segment is based on a modified and improved version of our freight logistics services business segment. For the year ended June 30, 2017, revenue generated from container trucking services was $871,563 and the related gross profit was $221,595.

Operating Costs and Expenses

Total operating costs and expenses decreased by $215,336 or 2.5%, from $8,559,767 for the year ended June 30, 2016 to $8,344,431 for the year ended June 30, 2017. This decrease was primarily due to the decrease in general and administrative expenses and selling expenses partially offset by the increase in cost of revenues as discussed below.

The following table sets forth the components of the Company’s costs and expenses for the periods indicated:

| For the years ended June 30, | ||||||||||||||||||||||||

| 2017 | 2016 | Change | ||||||||||||||||||||||

| US$ | % | US$ | % | US$ | % | |||||||||||||||||||

| Revenues | 11,445,613 | 100.0 | % | 7,310,540 | 100.0 | % | 4,135,073 | 56.6 | % | |||||||||||||||

| Cost of revenues | 4,980,591 | 43.5 | % | 3,737,989 | 51.1 | % | 1,242,602 | 33.2 | % | |||||||||||||||

| Gross margin | 56.5 | % | 48.9 | % | 7.6 | % | ||||||||||||||||||

| General and administrative expenses | 3,152,336 | 27.5 | % | 4,346,159 | 59.5 | % | (1,193,823 | ) | (27.5 | )% | ||||||||||||||

| Selling expenses | 211,504 | 1.8 | % | 475,619 | 6.5 | % | (264,115 | ) | (55.5 | )% | ||||||||||||||

| Total Costs and Expenses | 8,344,431 | 72.8 | % | 8,559,767 | 117.1 | % | (215,336 | ) | (2.5 | )% | ||||||||||||||

| 14 |

Costs of Revenues

Cost of revenues was $4,980,591 for the year ended June 30, 2017, an increase of $1,242,602, or 33.2%, as compared to $3,737,989 for the year ended June 30, 2016. The overall cost of revenues as a percentage of our revenues decreased from 51.1% for the year ended June 30, 2016, to 43.5% for the year ended June 30, 2017. The decrease in the overall costs of revenues in percentage terms for the year ended June 30, 201 7is due to the fact that the majority of our revenues during the year ended June 30, 2017 came from the more profitable inland transportation services and freight logistics services rather than the less profitable shipping agency service sector. Since revenue from shipping agency services has been decreased to nil, inland transportation management services and freight logistic services are now considered to be our essential revenue sources.

General and Administrative Expenses

Our general and administrative expenses consist primarily of salaries and benefits, office rent, office expenses, regulatory filing and listing fees, amortization of stock-based compensation expenses, legal, accounting and other professional service fees. For the year ended June 30, 2017, we had $3,152,336 of general and administrative expenses, as compared to $4,346,159 for the year ended June 30, 2016, a decrease of $1,193,823, or 27.5%. The decrease was mainly due to decreased stock-based compensation for common stock issued to consultants, decreased stock compensation for management, a recovery on allowance for doubtful accounts, and fewer legal fees incurred during the year ended June 30, 2017 compared to the corresponding period in 2016. As a result of the substantial reduction in general and administrative expenses and the increase in revenues, our general and administrative expenses, as a percentage of revenue, decreased from 59.5% for the year ended June 30, 2016 to 27.5% for the corresponding period in 2017.

Selling Expenses

The Company’s selling expenses consist primarily of business development costs and salaries and commissions for our operating staff at the ports at which we provide services. For the year ended June 30, 2017, we had $211,504 of selling expenses as compared to $475,619 for the year ended June 30, 2016, a decrease of $264,115, or 55.5%. The decrease was mainly attributable to the suspension of shipping agency services during the year ended June 30, 2017. No salaries and commissions were made for the operating staff at the ports. On the other hand, the Company clarified responsibilities for the sales personnel and centralized major sales activities functions in our headquarters in order to decrease selling expenses incurred in different subsidiaries in 2016. As a percentage of revenue, our selling expenses decreased from 6.5% for the year ended June 30, 2016, to 1.8% for the corresponding period in 2017.

Operating Income (Loss)

The Company had an operating income of $3,101,182 for the year ended June 30, 2017, compared to an operating loss of $1,249,227 for the comparable period ended June 30, 2016. The increase was mainly due to increased revenue generated from inland transportation management services and freight logistic services with strong gross profit contributions, and the significant decline in general and administrative expenses and selling expenses discussed above.

Financial Income (Expense), Net

The Company’s net financial income was $30,278 for the year ended June 30, 2017, compared to net financial expense of $247,530 for the same period of 2016. We have operations in the U.S., Canada, Australia, Hong Kong and the PRC, and our financial income (expenses) for the years ended June 30, 2017 and 2016 mainly reflects the foreign currency transaction income expressed in USD.

Taxation

The Company’s income tax benefit was $472,084 for the year ended June 30, 2017, compared to an income tax expense of $812,593 for the year ended June 30, 2016. During the year ended June 30, 2017, the amount of net operating loss (“NOL”) utilized was $1,853,000 and the tax benefit derived from such NOL was $630,000; in the corresponding period for the year ended June 30, 2016, the utilization of NOL was nil and no tax benefit was derived from NOL. During the year ended June 30, 2017, the Company provided an allowance against the deferred tax assets based on the Company’s projected taxable income and resulted in a net deferred tax asset of approximately $749,000; in the corresponding period of 2016, the Company provided a 100% valuation allowance against the deferred tax assets and no tax benefit was derived therefrom. The decrease in income tax expense was also attributable to a decrease in the taxable income of Trans Pacific during the year ended June 30, 2017 in comparison to the same period in 2016.

| 15 |

Net Income (Loss)

As a result of the foregoing, the Company had a net income of $3,603,544 for the year ended June 30, 2017, compared to a net loss of $2,301,522 for the year ended June 30, 2016. After the deduction of non-controlling interest, net income attributable to Sino-Global was $3,624,892 for the year ended June 30, 2017; for the year ended June 30, 2016, the Company had a net loss of $1,965,929. Comprehensive income attributable to the Company was $3,491,235 for the year ended June 30, 2017, compared to a comprehensive loss of $2,338,268 for the year ended June 30, 2016.

Liquidity and Capital Resources

Cash Flows and Working Capital

As of June 30, 2017, we had $8,733,742 in cash and cash equivalents. We held approximately 28.2% of our cash in banks located in New York, Los Angeles, Canada, Australia and Hong Kong and held approximately 71.8% of our cash in banks located in the PRC.

The following table sets forth a summary of our cash flows for the periods indicated:

| For the years ended June 30, | ||||||||

| 2017 | 2016 | |||||||

| Net cash provided by (used in) operating activities | $ | 2,994,770 | $ | (121,048 | ) | |||

| Net cash provided by (used in) investing activities | $ | (62,412 | ) | $ | 294,376 | |||

| Net cash provided by financing activities | $ | 4,402,488 | $ | 646,589 | ||||

| Net increase in cash and cash equivalents | $ | 7,347,748 | $ | 655,672 | ||||

| Cash and cash equivalents at the beginning of year | $ | 1,385,994 | $ | 730,322 | ||||

| Cash and cash equivalents at the end of year | $ | 8,733,742 | $ | 1,385,994 | ||||

The following table sets forth a summary of our working capital:

| June 30, 2017 | June 30, 2016 | Variation | % | |||||||||||||

| Total Current Assets | $ | 16,754,888 | $ | 8,651,985 | $ | 8,102,903 | 93.7 | % | ||||||||

| Total Current Liabilities | $ | 3,086,496 | $ | 2,437,382 | $ | 649,114 | 26.6 | % | ||||||||

| Working Capital | $ | 13,668,392 | $ | 6,214,603 | $ | 7,453,789 | 119.9 | % | ||||||||

| Current Ratio | 5.43 | 3.55 | 1.88 | 53.0 | % | |||||||||||

We finance our ongoing operating activities primarily by using funds from our operations. We routinely monitor current and expected operational requirements to evaluate the use of available funding sources. In assessing liquidity, Management monitors and analyzes the Company’s cash on-hand, its ability to generate sufficient revenue sources in the future and the Company’s operating and capital expenditure commitments. The Company plans to fund continuing operations through identifying new prospective joint ventures and strategic alliance opportunities for new revenue sources, and by reducing costs to improve profitability and replenish working capital. Considering our existing working capital position and our ability to access other funding sources, management believes that the foregoing measures will provide sufficient liquidity for the Company to meet its future liquidity and capital obligations.

| 16 |

Operating Activities

Our net cash derived from operating activities was $2,994,770 for the year ended June 30, 2017, including net income of $3.60 million from increased revenue generated from inland transportation management services, freight logistics services with strong margin contributions and decreased general and administrative expenses and sales expenses. In addition, advances to third party suppliers- decreased by $2.09 million because we received certain freight services prepayments pursuant to our Memorandum of Understanding with Singapore Metals & Minerals Pte Ltd. and Galasi Jernsih Sdn BHD in the third and fourth quarter of 2017. However, advances to related-party suppliers increased by $3.32 million as a result of Cooperative Transportation Agreement signed with Zhiyuan International Investment & Holding Group (Hong Kong) Co., Ltd. (“Zhiyuan Hong Kong”), a related party, pursuant to which we advanced transportation payments of approximately $3.33 million during the year ended June 30, 2017. Cash inflows from operating activities for the year ended June 30, 2017 reflect the above mentioned major factors.

Net cash used in operating activities was $121,048 for the year ended June 30, 2016, which included our operating loss of $2.30 million due to our decreased revenue in the shipping agency service sector and increased selling expenses. In addition, the advances to third-party suppliers increased by $2.14 million because we prepaid freight fees of RMB 14.58 million (approximately $2.2 million) based on our Memorandum of Understanding (“MOU”) with Singapore Metals & Minerals Pte Ltd. (“the Buyer”) and Galasi Jernsih Sdn BHD (“the Seller”), the accounts receivable decreased by $0.62 million because we strengthened our cash collection efforts and received a payment of RMB 13.4 million (approximately $2.0 million) from Tengda Northwest, our major third-party customer of inland transportation services, and due from related parties decreased by $1.16 million because we collected RMB 22.2 million (approximately $3.3 million) from our related party customer, Zhiyuan. The Company’s cash outflows from operating activities for the year ended June 30, 2016 reflected the above mentioned factors.

Investing Activities

The Company’s net cash used in investing activities was $62,412 for the year ended June 30, 2017 compared to net cash provided by investing activities of $294,376 for the same period of 2016. For the year ended June 30, 2017, we purchased a vehicle in the amount of $55,339. For the year ended June 30, 2016, the amount was mainly generated by cash collection from the termination of our $326,035 vessel acquisition.

Financing Activities

The Company’s net cash derived from financing activities was $4,402,488 for the year ended June 30, 2017, compared to $646,589 for the year ended June 30, 2016. During the year ended June 30, 2017, 75,000 stock options were exercised by the two employees of the Company with an exercise price of $1.10. As a result, net proceeds of $82,500 were recognized as net proceeds from exercise of stock options by the Company. In addition, the Company received net proceeds in the amount of $4,319,988 from a registered direct sale of 1.5 million shares of its common stock to three institutional investors.

Net cash provided by financing activities was $646,589 for the year ended June 30, 2016, of which $691,600 resulted from the proceeds from the issuance of common stock to one individual investor in a private sale transaction on July 10, 2015. During the year ended June 30, 2016, the Company repurchased 50,306 common shares and recorded such shares as treasury stock, with a payment of $45,011.

| 17 |

Critical Accounting Policies

We prepare our consolidated financial statements in accordance with U.S. GAAP. These accounting principles require us to make judgments, estimates and assumptions on the reported amounts of assets and liabilities at the end of each fiscal period, and the reported amounts of revenues and expenses during each fiscal period. We continually evaluate these judgments and estimates based on our own historical experience, knowledge and assessment of current business and other conditions, our expectations regarding the future based on available information and assumptions that we believe to be reasonable.

There have been no material changes during the year ended June 30, 2017 in our accounting policies from those previously disclosed in the Company’s annual report for the fiscal year ended June 30, 2016.

The selection of critical accounting policies, the judgments and other uncertainties affecting application of those policies and the sensitivity of reported results to changes in conditions and assumptions are factors that should be considered when reviewing our financial statements. We believe the following accounting policies involve the most significant judgments and estimates used in the preparation of our consolidated financial statements.

Revenue Recognition

| ● | Revenues from shipping agency services are recognized upon completion of services, which coincides with the date of departure of the relevant vessel from port. Advance payments and deposits received from customers prior to the provision of services and recognition of the related revenues are presented as advances from customers. |

| ● | Revenues from shipping and chartering services are recognized upon performance of services as stipulated in the underlying contracts. |

| ● | Revenues from inland transportation management services are recognized when commodities are being released from the customer’s warehouse. |

| ● | Revenues from ship management services are recognized when the related contractual services are rendered. |

| ● | Revenues from freight logistics services are recognized when the related contractual services are rendered. |

| ● | Revenues from container trucking services are recognized when the related contractual services are rendered. |

Basis of Consolidation