Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

(Mark One)

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2015

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

OR

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

Commission file number 001-37384

GALAPAGOS NV

(Exact name of Registrant as specified in its charter and translation of Registrant’s name into English)

Belgium

(Jurisdiction of incorporation or organization)

Generaal De Wittelaan L11 A3

2800 Mechelen, Belgium

(Address of principal executive offices)

Onno van de Stolpe

Chief Executive Officer

Galapagos NV

Generaal De Wittelaan L11 A3

2800 Mechelen, Belgium

Tel: +32 1 534 29 00 Fax: +32 1 534 29 01

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Title of each class |

Name of each exchange on which registered | |

| American Depositary Shares, each representing one ordinary share, no par value per share |

The Nasdaq Stock Market LLC | |

| Ordinary shares, no par value per share* | The Nasdaq Stock Market LLC* |

* Not for trading, but only in connection with the registration of the American Depositary Shares.

Securities registered or to be registered pursuant to Section 12(g) of the Act. None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act. None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the Annual Report.

Ordinary shares, no par value per share: 39,076,342 as of December 31, 2015

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ¨ Yes x No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files. ¨ Yes x No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ¨ Accelerated filer ¨ Non-accelerated filer x

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ¨ | International Financial Reporting Standards as issued by the International Accounting Standards Board x |

Other ¨ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. ¨ Item 17 ¨ Item 18

If this is an Annual Report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ¨ Yes x No

Table of Contents

| Page | ||||||||

| 1 | ||||||||

| 3 | ||||||||

| Item 1. | 3 | |||||||

| Item 2. | 3 | |||||||

| Item 3. | 3 | |||||||

| A. | 3 | |||||||

| B. | 5 | |||||||

| C. | 5 | |||||||

| D. | 5 | |||||||

| Item 4. | 46 | |||||||

| A. | 46 | |||||||

| B. | 46 | |||||||

| C. | 94 | |||||||

| D. | 94 | |||||||

| Item 4A. | 94 | |||||||

| Item 5. | 95 | |||||||

| A. | 104 | |||||||

| B. | 117 | |||||||

| C. | 121 | |||||||

| D. | 122 | |||||||

| E. | 122 | |||||||

| F. | 122 | |||||||

| G. | 123 | |||||||

| Item 6. | 123 | |||||||

| A. | 123 | |||||||

| B. | 127 | |||||||

| C. | 135 | |||||||

| D. | 139 | |||||||

| E. | 139 | |||||||

| Item 7. | 139 | |||||||

| A. | 139 | |||||||

| B. | 141 | |||||||

| C. | 145 | |||||||

| Item 8. | 145 | |||||||

| A. | 145 | |||||||

| B. | 145 | |||||||

| Item 9. | 146 | |||||||

| A. | 146 | |||||||

| B. | 147 | |||||||

| C. | 147 | |||||||

Table of Contents

| Page | ||||||||

| D. | 147 | |||||||

| E. | 147 | |||||||

| F. | 147 | |||||||

| Item 10. | 148 | |||||||

| A. | 148 | |||||||

| B. | 148 | |||||||

| C. | 148 | |||||||

| D. | 148 | |||||||

| E. | 148 | |||||||

| F. | 160 | |||||||

| G. | 160 | |||||||

| H. | 160 | |||||||

| I. | 160 | |||||||

| Item 11. | 160 | |||||||

| Item 12. | 162 | |||||||

| A. | 162 | |||||||

| B. | 162 | |||||||

| C. | 163 | |||||||

| D. | 163 | |||||||

| 165 | ||||||||

| Item 13. | 165 | |||||||

| Item 14. | Material Modifications to the Rights of Security Holders and Use of Proceeds. |

165 | ||||||

| Item 15. | 165 | |||||||

| Item 15T. | 165 | |||||||

| Item 16. | 166 | |||||||

| Item 16A. | 166 | |||||||

| Item 16B. | 166 | |||||||

| Item 16C. | 166 | |||||||

| Item 16D. | 167 | |||||||

| Item 16E. | Purchases of Equity Securities by the Issuer and Affiliated Purchasers. |

167 | ||||||

| Item 16F. | 167 | |||||||

| Item 16G. | 167 | |||||||

| Item 16H. | 168 | |||||||

| 169 | ||||||||

| Item 17. | 169 | |||||||

| Item 18. | 169 | |||||||

| Item 19. | 169 | |||||||

ii

Table of Contents

Unless otherwise indicated, “GLPG,” “the company,” “our company,” “we,” “us,” and “our” refer to Galapagos NV and its consolidated subsidiaries.

We own various trademark registrations and applications, and unregistered trademarks, including GALAPAGOS, FIDELTA, and our corporate logo. All other trade names, trademarks and service marks referred to in this Annual Report on Form 20-F, or this Annual Report, are the property of their respective owners. Trade names, trademarks and service marks of other companies appearing in this Annual Report are the property of their respective holders. Solely for convenience, the trademarks and trade names in this Annual Report may be referred to without the ® and ™ symbols, but such references should not be construed as any indicator that their respective owners will not assert, to the fullest extent under applicable law, their rights thereto. We do not intend to use or display other companies’ trademarks and trade names to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

Our audited consolidated financial statements have been prepared in accordance with International Financial Reporting Standards, or IFRS, as issued by the International Accounting Standards Board, or IASB. Our consolidated financial statements are presented in euros. All references in this Annual Report to “$,” “US$,” “U.S.$,” “U.S. dollars,” “dollars,” and “USD” mean U.S. dollars and all references to “€” and “euros” mean euros, unless otherwise noted. Throughout this Annual Report, references to “ADSs” mean American Depositary Shares or ordinary shares represented by American Depositary Shares, as the case may be.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act, that are based on our management’s beliefs and assumptions and on information currently available to our management. All statements other than present and historical facts and conditions contained in this Annual Report, including statements regarding our future results of operations and financial positions, business strategy, plans and our objectives for future operations, are forward-looking statements. When used in this Annual Report, the words “anticipate,” “believe,” “can,” “could,” “estimate,” “expect,” “intend,” “is designed to,” “may,” “might,” “plan,” “potential,” “predict,” “objective,” “should,” or the negative of these and similar expressions identify forward-looking statements. Forward-looking statements include, but are not limited to, statements about:

| • | the initiation, timing, progress and results of our pre-clinical studies and clinical trials, and our research and development programs; |

| • | our ability to advance product candidates into, and successfully complete, clinical trials; |

| • | our reliance on the success of our product candidate filgotinib and certain other product candidates; |

| • | the timing or likelihood of regulatory filings and approvals; |

| • | our ability to develop sales and marketing capabilities; |

| • | the commercialization of our product candidates, if approved; |

| • | the pricing and reimbursement of our product candidates, if approved; |

| • | the implementation of our business model, strategic plans for our business, product candidates and technology; |

| • | the scope of protection we are able to establish and maintain for intellectual property rights covering our product candidates and technology; |

| • | our ability to operate our business without infringing the intellectual property rights and proprietary technology of third parties |

Table of Contents

| • | cost associated with defending intellectual property infringement, product liability, and other claims |

| • | regulatory development in the United States, Europe, and other jurisdictions; |

| • | estimates of our expenses, future revenues, capital requirements and our needs for additional financing; |

| • | the potential benefits of strategic collaboration agreements and our ability to enter into strategic arrangements; |

| • | our ability to maintain and establish collaborations or obtain additional grant funding; |

| • | the rate and degree of market acceptance of our product candidates if approved by regulatory authorities; |

| • | our financial performance; |

| • | developments relating to our competitors and our industry, including competing therapies; |

| • | our ability to effectively manage and anticipated growth; |

| • | our ability to attract and retain qualified employees and key personnel; |

| • | our expectations regarding the period during which we qualify as an emerging growth company under the JOBS Act; |

| • | statements regarding future revenue, hiring plans, expenses, capital expenditures, capital requirements and share performance; and |

| • | other risks and uncertainties, including those listed in the section of this Annual Report titled “Item 3.D.—Risk Factors.” |

You should refer to the section of this Annual Report titled “Item 3.D.—Risk Factors” for a discussion of important factors that may cause our actual results to differ materially from those expressed or implied by our forward-looking statements. As a result of these factors, we cannot assure you that the forward-looking statements in this Annual Report will prove to be accurate. Furthermore, if our forward-looking statements prove to be inaccurate, the inaccuracy may be material. In light of the significant uncertainties in these forward-looking statements, you should not regard these statements as a representation or warranty by us or any other person that we will achieve our objectives and plans in any specified time frame or at all. We undertake no obligation to publicly update any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

You should read this Annual Report and the documents that we reference in this Annual Report and have filed as exhibits to this Annual Report completely and with the understanding that our actual future results may be materially different from what we expect. We qualify all of our forward-looking statements by these cautionary statements.

This Annual Report contains market data and industry forecasts that were obtained from industry publications. These data involve a number of assumptions and limitations, and you are cautioned not to give undue weight to such estimates. We have not independently verified any third-party information. While we believe the market position, market opportunity and market size information included in this Annual Report is generally reliable, such information is inherently imprecise.

2

Table of Contents

| Item 1. | Identity of Directors, Senior Management and Employee. |

Not applicable.

| Item 2. | Offer Statistics and Expected Timetable. |

Not applicable.

| Item 3. | Key Information. |

| A. | Selected Financial Data |

Our consolidated audited financial statements have been prepared in accordance with IFRS, as issued by the IASB. We derived the selected statements of consolidated operations data, selected statements of consolidated financial position and selected statements of consolidated cash flows, each as of December 31, 2012, 2013, 2014 and 2015 from our consolidated audited financial statements. This data should be read together with, and is qualified in its entirety by reference to, “Item 5—Operating and Financial Review and Prospects” as well as our financial statements and notes thereto appearing elsewhere in this Annual Report. Our historical results are not necessarily indicative of the results to be expected in the future.

| Consolidated Statement of Operations: | Year Ended December 31, | |||||||||||||||

| 2015 | 2014 | 2013 | 2012 | |||||||||||||

| (Euro, in thousands, except share and per share data) | ||||||||||||||||

| Revenues . |

€ | 39,563 | € | 69,368 | € | 76,625 | € | 74,504 | ||||||||

| Other income |

21,017 | 20,653 | 19,947 | 17,722 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total revenues and other income |

60,579 | 90,021 | 96,572 | 92,226 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Service cost of sales |

(5,584 | ) | ||||||||||||||

| Research and development expenditure |

(129,714 | ) | (111,110 | ) | (99,380 | ) | (80,259 | ) | ||||||||

| General and administrative expenses |

(19,127 | ) | (13,875 | ) | (12,353 | ) | (12,118 | ) | ||||||||

| Sales and marketing expenses |

(1,182 | ) | (992 | ) | (1,464 | ) | (1,285 | ) | ||||||||

| Restructuring and integration costs |

— | (669 | ) | (290 | ) | (2,506 | ) | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating loss |

(89,444 | ) | (36,624 | ) | (16,915 | ) | (9,526 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Fair value re-measurement of share subscription agreement |

(30,632 | ) | ||||||||||||||

| Other financial income |

1,987 | 2,291 | 2,182 | 3,103 | ||||||||||||

| Other financial expenses |

(1,539 | ) | (867 | ) | (1,402 | ) | (1,176 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Loss before tax |

(119,627 | ) | (35,201 | ) | (16,135 | ) | (7,599 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income taxes . |

1,218 | (2,103 | ) | (676 | ) | 164 | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net loss from continuing operations |

(118,410 | ) | (37,303 | ) | (16,811 | ) | (7,435 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income from discontinued operations |

— | 70,514 | 8,732 | 1,714 | ||||||||||||

| Net income / loss (-) |

€ | (118,410 | ) | € | 33,211 | € | (8,079 | ) | € | (5,721 | ) | |||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income / loss (-) attributable to: |

||||||||||||||||

| Owners of the parent |

(118,410 | ) | 33,211 | (8,079 | ) | (5,721 | ) | |||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Basic and diluted income / loss (-) per share |

€ | (3.32 | ) | € | 1.10 | € | (0.28 | ) | € | (0.22 | ) | |||||

|

|

|

|

|

|

|

|

|

|||||||||

| Basic and diluted loss per share from continuing operations |

€ | (3.32 | ) | € | (1.24 | ) | € | (0.58 | ) | € | (0.28 | ) | ||||

| Weighted average number of shares (in ‘000 shares) |

35,700 | 30,108 | 28,787 | 26,545 | ||||||||||||

3

Table of Contents

| Condensed Consolidated Statement of Financial Position: | ||||||||||||||||

| December 31, | ||||||||||||||||

| 2015 | 2014 | 2013 | 2012 | |||||||||||||

| (Euro, in thousands) | ||||||||||||||||

| Cash and cash equivalents |

€ | 340,314 | € | 187,712 | € | 138,175 | € | 94,369 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total assets |

442,514 | 270,467 | 287,374 | 94,369 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Share capital |

185,399 | 157,274 | 154,542 | 139,347 | ||||||||||||

| Share premium account |

357,402 | 114,182 | 112,484 | 72,876 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total equity / net assets |

364,999 | 206,135 | 167,137 | 118,447 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total non-current liabilities |

5,103 | 3,976 | 7,678 | 7,867 | ||||||||||||

| Total current liabilities |

72,412 | 60,356 | 112,559 | 109,014 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total liabilities |

77,515 | 64,332 | 120,237 | 116,881 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total liabilities and equity |

€ | 442,514 | € | 270,467 | € | 287,374 | € | 235,328 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Condensed Consolidated Statement of Cash Flows: | ||||||||||||||||

| Year Ended December 31, | ||||||||||||||||

| 2015 | 2014 | 2013 | 2012 | |||||||||||||

| (Euro, in thousands) | ||||||||||||||||

| Cash and cash equivalents at beginning of the period |

€ | 187,712 | € | 138,175 | € | 94,369 | € | 32,277 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net cash flows generated / used (-) in operating activities |

(114,590 | ) | (75,555 | ) | 1,846 | 65,873 | ||||||||||

| Net cash flows generated / used (-) in investing activities |

(4,297 | ) | 120,606 | (11,988 | ) | (6,437 | ) | |||||||||

| Net cash flows generated in financing activities |

271,370 | 4,214 | 54,495 | 2,265 | ||||||||||||

| Effect of exchange rate differences on cash and cash equivalents |

118 | 271 | (548 | ) | 391 | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Cash and cash equivalents at end of the period |

€ | 340,314 | € | 187,712 | € | 138,175 | € | 94,369 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

Exchange Rate Information

The following table sets forth, for each period indicated, the low and high exchange rates of U.S. dollars per euro, the exchange rate at the end of such period and the average of such exchange rates on the last day of each month during such period, based on the noon buying rate of the Federal Reserve Bank of New York for the euro. As used in this document, the term “noon buying rate” refers to the rate of exchange for the euro, expressed in U.S. dollars per euro, as certified by the Federal Reserve Bank of New York for customs purposes. The exchange rates set forth below demonstrate trends in exchange rates, but the actual exchange rates used throughout this Annual Report may vary.

| Year Ended December 31, | ||||||||||||||||||||

| 2011 | 2012 | 2013 | 2014 | 2015 | ||||||||||||||||

| High |

1.4875 | 1.3463 | 1.3816 | 1.3927 | 1.2015 | |||||||||||||||

| Low |

1.2926 | 1.2062 | 1.2774 | 1.2101 | 1.0524 | |||||||||||||||

| Rate at end of period |

1.2973 | 1.3186 | 1.3779 | 1.2101 | 1.0859 | |||||||||||||||

| Average rate per period |

1.3931 | 1.2859 | 1.3281 | 1.3297 | 1.1096 | |||||||||||||||

The following table sets forth, for each of the last six months, the low and high exchange rates for euros expressed in U.S. dollars and the exchange rate at the end of the month based on the noon buying rate as described above.

| September 2015 |

October 2015 |

November 2015 |

December 2015 |

January 2016 |

February 2016 |

|||||||||||||||||||

| High |

1.1358 | 1.1437 | 1.1026 | 1.1025 | 1.0964 | 1.1323 | ||||||||||||||||||

| Low |

1.1104 | 1.0963 | 1.0562 | 1.0573 | 1.0743 | 1.0873 | ||||||||||||||||||

| Rate at end of period |

1.1162 | 1.1042 | 1.0562 | 1.0859 | 1.0832 | 1.0873 | ||||||||||||||||||

4

Table of Contents

On December 31, 2015, the noon buying rate of the Federal Reserve Bank of New York for the euro was €1.00 = US$1.0859. Unless otherwise indicated, currency translations in this Annual Report reflect the December 31, 2015 exchange rate.

On March 18, 2016, the noon buying rate of the Federal Reserve Bank of New York for the euro was €1.00 = $1.1292.

| B. | Capitalization and Indebtedness |

Not applicable.

| C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

| D. | Risk Factors |

Our business faces significant risks. You should carefully consider all of the information set forth in this Annual Report and in our other filings with the U.S. Securities and Exchange Commission, or the SEC, including the following risk factors which we face and which are faced by our industry. Our business, financial condition or results of operations could be materially adversely affected by any of these risks. This report also contains forward-looking statements that involve risks and uncertainties. Our results could materially differ from those anticipated in these forward-looking statements, as a result of certain factors including the risks described below and elsewhere in this Annual Report and our other SEC filings. See “Special Note Regarding Forward-Looking Statements” above.

Risks Related to Product Development, Regulatory Approval and Commercialization

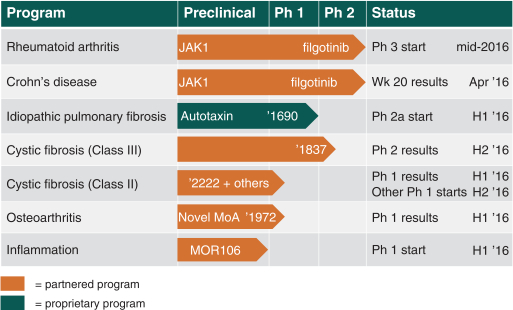

We are heavily dependent on the success of our product candidate filgotinib. We are also dependent on the success of our other product candidates, such as GLPG1837, GLPG2222, GLPG1690 and GLPG1972. We cannot give any assurance that any product candidate will successfully complete clinical trials or receive regulatory approval, which is necessary before it can be commercialized.

Filgotinib is currently being prepared for Phase 3 studies in rheumatoid arthritis, or RA, and in Crohn’s disease, or CD, by our collaboration partner Gilead Sciences, Inc., or Gilead. Our business and future success is substantially dependent on our ability to develop, either alone or in partnership, successfully, obtain regulatory approval for, and then successfully commercialize our product candidate filgotinib, which has completed the DARWIN 1 and 2 trials and still is in the DARWIN 3 trial for RA and reported 10-week data from a Phase 2 trial for CD. Our business and future success also depend on our ability to develop successfully, obtain regulatory approval for, and then successfully commercialize our other product candidates, such as GLPG1837, GLPG2222, GLPG1690 and GLPG1972. We initiated Phase 2 trials with potentiator GLPG1837 in Class III mutation patients in February 2016 in cystic fibrosis, or CF; we have initiated a Phase 1 trial with GLPG2222 in CF; we have initiated a Phase 1 first-in-human trial with GLPG1972 in osteoarthritis, or OA and GLPG1690 will enter a Phase 2a trial in idiopathic pulmonary fibrosis, or IPF. Our product candidates will require additional clinical development, management of clinical and manufacturing activities, regulatory approval in multiple jurisdictions (if regulatory approval can be obtained at all), securing sources of commercial manufacturing supply, building of, or partnering with, a commercial organization, substantial investment and significant marketing efforts before any revenues can be generated from product sales. We are not permitted to market or promote any of our product candidates before we receive regulatory approval from the U.S. Food and Drug Administration, or FDA, the European Medicines Agency, or EMA, or any other comparable regulatory authority, and we may never receive such regulatory approval for any of our product candidates. We cannot assure you that our clinical trials for filgotinib, GLPG1837, GLPG2222, GLPG1690 or GLPG1972 will be completed in a timely manner, or at all, or

5

Table of Contents

that we will be able to obtain approval from the FDA, the EMA or any other comparable regulatory authority for any of these product candidates. We cannot be certain that we will advance any other product candidates into clinical trials. If any of filgotinib, GLPG1837, GLPG2222, GLPG1690, GLPG1972 or any future product candidate is not approved and commercialized, we will not be able to generate any product revenues for that product candidate. Moreover, any delay or setback in the development of any product candidate could adversely affect our business and cause the price of the ADSs or our ordinary shares to fall.

Due to our limited resources and access to capital, we must and have in the past decided to prioritize development of certain product candidates; these decisions may prove to have been wrong and may adversely affect our revenues.

Because we have limited resources and access to capital to fund our operations, we must decide which product candidates to pursue and the amount of resources to allocate to each. As such, we are currently primarily focused on the development of filgotinib, GLPG1837, GLPG2222, GLPG1690 and GLPG1972. Our decisions concerning the allocation of research, collaboration, management and financial resources toward particular compounds, product candidates or therapeutic areas may not lead to the development of viable commercial products and may divert resources away from better opportunities. Similarly, our potential decisions to delay, terminate or collaborate with third parties in respect of certain product development programs may also prove not to be optimal and could cause us to miss valuable opportunities. If we make incorrect determinations regarding the market potential of our product candidates or misread trends in the pharmaceutical industry, our business, financial condition and results of operations could be materially adversely affected.

The regulatory approval processes of the FDA, the EMA and other comparable regulatory authorities are lengthy, time consuming and inherently unpredictable, and if we are ultimately unable to obtain regulatory approval for our product candidates, our business will be substantially harmed.

The time required to obtain approval by the FDA, the EMA and other comparable regulatory authorities is unpredictable but typically takes many years following the commencement of clinical trials and depends upon numerous factors, including the substantial discretion of the regulatory authorities. In addition, approval policies, regulations, or the type and amount of clinical data necessary to gain approval may change during the course of a product candidate’s clinical development and may vary among jurisdictions. We have not obtained regulatory approval for any product candidate and it is possible that none of our existing product candidates or any product candidates we may seek to develop in the future will ever obtain regulatory approval.

Our product candidates could fail to receive regulatory approval for many reasons, including the following:

| • | the FDA, the EMA or other comparable regulatory authorities may disagree with the design or implementation of our clinical trials; |

| • | we may be unable to demonstrate to the satisfaction of the FDA, the EMA or other comparable regulatory authorities that a product candidate is safe and effective for its proposed indication; |

| • | the results of clinical trials may not meet the level of statistical significance required by the FDA, the EMA or other comparable regulatory authorities for approval; |

| • | we may be unable to demonstrate that a product candidate’s clinical and other benefits outweigh its safety risks; |

| • | filgotinib and our other product candidates (except for our CF program) are developed to act against targets discovered by us, and because our product candidates are novel mode of action products, they carry an additional risk regarding desired level of efficacy and safety profile; |

| • | the FDA, the EMA or other comparable regulatory authorities may disagree with our interpretation of data from pre-clinical studies or clinical trials; |

6

Table of Contents

| • | the data collected from clinical trials of our product candidates may not be sufficient to support the submission of a new drug application, or NDA, supplemental NDA, or other submission or to obtain regulatory approval in the United States, Europe or elsewhere; |

| • | the FDA, the EMA or other comparable regulatory authorities may fail to approve the manufacturing processes or facilities of third-party manufacturers with which we contract for clinical and commercial supplies or such processes or facilities may not pass a pre-approval inspection; and |

| • | the approval policies or regulations of the FDA, the EMA or other comparable regulatory authorities may change or differ from one another significantly in a manner rendering our clinical data insufficient for approval. |

This lengthy approval process as well as the unpredictability of future clinical trial results may result in our or our collaboration partners’ failure to obtain regulatory approval to market filgotinib, GLPG1837, GLPG2222, GLPG1690, GLPG1972 and/or other product candidates, which would harm our business, results of operations and prospects significantly. In addition, even if we were to obtain approval, regulatory authorities may approve any of our product candidates for fewer or more limited indications than we request, may grant approval contingent on the performance of costly post-marketing clinical trials, or may approve a product candidate with a label that does not include the labeling claims necessary or desirable for the successful commercialization of that product candidate. In certain jurisdictions, regulatory authorities may not approve the price we intend to charge for our products. Any of the foregoing scenarios could materially harm the commercial prospects for our product candidates.

We have not previously submitted an NDA, a marketing authorization application, or any similar drug approval filing to the FDA, the EMA or any comparable regulatory authority for any product candidate, and we cannot be certain that any of our product candidates will be successful in clinical trials or receive regulatory approval. Further, our product candidates may not receive regulatory approval even if they are successful in clinical trials. If we do not receive regulatory approvals for our product candidates, we may not be able to continue our operations. Even if we successfully obtain regulatory approvals to market one or more of our product candidates, our revenues will be dependent, to a significant extent, upon the size of the markets in the territories for which we gain regulatory approval and have commercial rights or share in revenues from the exercise of such rights. If the markets for patient subsets that we are targeting (such as RA, CD or CF) are not as significant as we estimate, we may not generate significant revenues from sales of such products, if approved.

In connection with our global clinical trials, local regulatory authorities may have differing perspectives on clinical protocols and safety parameters, which impacts the manner in which we conduct these global clinical trials and could negatively impact our chances for obtaining regulatory approvals or marketing authorization in these jurisdictions, or for obtaining the requested dosage for our product candidates, if regulatory approvals or marketing authorizations are obtained.

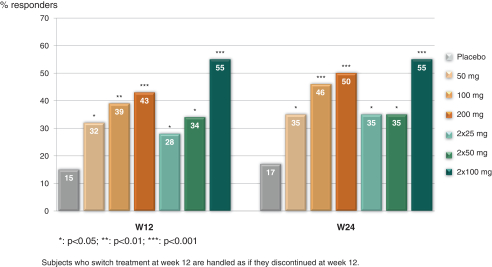

In connection with our global clinical trials, we are obliged to comply with the requirements of local regulatory authorities in each jurisdiction where we execute and locate a clinical trial. Local regulatory authorities can request specific changes to the clinical protocol or specific safety measures that differ from the positions taken in other jurisdictions. For example, in our DARWIN Phase 2 clinical trials for filgotinib in subjects with RA, we agreed with the FDA to exclude the 200 mg filgotinib daily dose for male subjects enrolled in the United States pending further data to demonstrate a wider exposure margin in patients versus the safe exposure in animal studies, while there is no such restriction by health authorities outside the United States. We cannot assure you that this view will not be adopted by other regulatory authorities in later stage trials or at the marketing authorization stage, if filgotinib successfully completes the registrational trials. Even if filgotinib does receive regulatory approval or marketing authorization, the FDA or other regulatory authorities may impose dosing restrictions that differ from the approved dosing regimen in other jurisdictions, and these differences could have a material adverse effect on our ability to commercialize our products in these jurisdictions.

7

Table of Contents

Even if we receive regulatory approval for any of our product candidates, we will be subject to ongoing obligations and continued regulatory review, which may result in significant additional expense. Additionally, our product candidates, if approved, could be subject to labeling and other restrictions and market withdrawal and we may be subject to penalties if we fail to comply with regulatory requirements or experience unanticipated problems with our products.

Any regulatory approvals that we receive for our product candidates may also be subject to limitations on the approved indicated uses for which the product may be marketed or to the conditions of approval, or contain requirements for potentially costly post-marketing testing, including Phase 4 clinical trials, and surveillance to monitor the safety and efficacy of the product candidate, and we may be required to include labeling that includes significant use or distribution restrictions or significant safety warnings, including boxed warnings.

If the FDA, EMA or any other comparable regulatory authority approves any of our product candidates, the manufacturing processes, labeling, packaging, distribution, adverse event reporting, storage, advertising, promotion and recordkeeping for the product will be subject to extensive and ongoing regulatory requirements. These requirements include submissions of safety and other post-marketing information and reports, registration requirements and continued compliance with current good manufacturing practices, or cGMPs, and good clinical practices, or GCPs, for any clinical trials that we conduct post-approval. Later discovery of previously unknown problems with a product, including adverse events of unanticipated severity or frequency, or with our third-party manufacturers or manufacturing processes, or failure to comply with regulatory requirements, may result in, among other things:

| • | restrictions on the marketing or manufacturing of the product, withdrawal of the product from the market, or voluntary product recalls; |

| • | fines, untitled or warning letters or holds on clinical trials; |

| • | refusal by the FDA, the EMA or any other comparable regulatory authority to approve pending applications or supplements to approved applications filed by us, or suspension or revocation of product approvals; |

| • | product seizure or detention, or refusal to permit the import or export of products; and |

| • | injunctions or the imposition of civil or criminal penalties. |

The policies of the FDA, the EMA and other comparable regulatory authorities may change and additional government regulations may be enacted that could prevent, limit or delay regulatory approval of our product candidates. If we are slow or unable to adapt to changes in existing requirements or the adoption of new requirements or policies, or if we are not able to maintain regulatory compliance, we may lose any marketing approval that we may have obtained, which would adversely affect our business, prospects and ability to achieve or sustain profitability.

Filgotinib, if approved, may be subject to box warnings, labeling restrictions or dose limitations in certain jurisdictions, which could have a material adverse impact on our ability to market filgotinib in these jurisdictions.

Based on pre-clinical findings, we expect that filgotinib, if approved, may have a labeling statement warning female patients of child-bearing age to take precautionary measures of birth control to protect against pregnancy, similar to warnings included with other frequently used medications in RA, such as methotrexate, or MTX.

In addition, there may be dose limitations imposed for male patients that are prescribed filgotinib, if approved. In connection with the DARWIN clinical program, we agreed with the FDA to exclude the 200 mg filgotinib daily dose for male subjects in the U.S.; males received a maximum daily dose of 100 mg in the U.S. sites in these trials. This limitation was not imposed by any other regulatory agency in any other jurisdiction in which the DARWIN clinical program is being conducted. We agreed to this limitation because in both rat and dog toxicology studies,

8

Table of Contents

filgotinib induced adverse effects on the male reproductive system and the FDA determined there was not a sufficient safety margin between the filgotinib exposure at the no-observed-adverse-effect-level observed in these studies and the anticipated human exposure at the 200 mg daily filgotinib dose. Accordingly, in connection with the DARWIN 3 clinical trial, in the United States, male subjects are dosed at 100-mg-daily-dose only. Male participants in this study and their partners are required to use highly effective contraceptive measures for the duration of the study and during a washout period thereafter. As an additional safety measure, we monitor clinical laboratory changes in hormone levels for subjects in the DARWIN 3 clinical trial.

Recently generated non-clinical data showed filgotinib did not induce any macroscopic or microscopic findings in the male reproductive system in animals with higher filgotinib exposure versus previous studies. Although this data has been shared with the FDA, the selection of doses for the filgotinib Phase 3 development program will be based on an overall risk/benefit assessment, taking into account all available non-clinical findings as well as clinical safety and efficacy data (including data from male subjects treated with the 200 mg daily dose of filgotinib outside of the United States). Therefore, the FDA or other regulatory authorities may still impose dosing restrictions.

Even if filgotinib does receive regulatory approval or marketing authorization, the FDA or other regulatory authorities may impose dosing restrictions that differ from the approved dosing regimen in other jurisdictions.

Box warnings, labeling restrictions, dose limitations and similar restrictions on use could have a material adverse effect on our ability to commercialize filgotinib in those jurisdictions where such restrictions apply.

Clinical development is a lengthy and expensive process with an uncertain outcome, and results of earlier studies and trials as well as data from any interim analysis of ongoing clinical trials may not be predictive of future trial results. Clinical failure can occur at any stage of clinical development. We have never completed a Phase 3 trial or submitted an NDA.

Clinical testing is expensive and can take many years to complete, and its outcome is inherently uncertain. Failure can occur at any time during the clinical trial process. Although product candidates may demonstrate promising results in early clinical (human) trials and pre-clinical (animal) studies, they may not prove to be effective in subsequent clinical trials. For example, testing on animals may occur under different conditions than testing in humans and therefore the results of animal studies may not accurately predict human experience. Likewise, early clinical studies may not be predictive of eventual safety or effectiveness results in larger-scale pivotal clinical trials. The results of pre-clinical studies and previous clinical trials as well as data from any interim analysis of ongoing clinical trials of our product candidates, as well as studies and trials of other products with similar mechanisms of action to our product candidates, may not be predictive of the results of ongoing or future clinical trials. For example, the positive results generated to date in pre-clinical studies and Phase 1, Phase 2a and Phase 2b clinical trials for filgotinib in RA or Phase 2b clinical trials for CD do not ensure that later clinical trials will continue to demonstrate similar results or observations. Product candidates in later stages of clinical trials may fail to show the desired safety and efficacy traits despite having progressed through pre-clinical studies and earlier clinical trials. In addition to the safety and efficacy traits of any product candidate, clinical trial failures may result from a multitude of factors including flaws in trial design, dose selection, placebo effect and patient enrollment criteria. A number of companies in the pharmaceutical industry have suffered significant setbacks in advanced clinical trials due to lack of efficacy or adverse safety profiles, notwithstanding promising results in earlier trials, and it is possible that we will as well. Based upon negative or inconclusive results, we or our collaboration partners may decide, or regulators may require us, to conduct additional clinical trials or pre-clinical studies. In addition, data obtained from trials and studies are susceptible to varying interpretations, and regulators may not interpret our data as favorably as we do, which may delay, limit or prevent regulatory approval.

9

Table of Contents

We may experience delays in our ongoing clinical trials and we do not know whether planned clinical trials will begin on time, need to be redesigned, enroll patients on time or be completed on schedule, if at all. Clinical trials can be delayed for a variety of reasons, including delays related to:

| • | obtaining regulatory approval to commence a trial; |

| • | reaching agreement on acceptable terms with prospective contract research organizations, or CROs, and clinical trial sites, the terms of which can be subject to extensive negotiation and may vary significantly among different CROs and trial sites; |

| • | obtaining Institutional Review Board, or IRB, or ethics committee approval at each site; |

| • | obtaining regulatory concurrence on the design and parameters for the trial; |

| • | obtaining approval for the designs of our clinical development programs for each country targeted for trial enrollment; |

| • | recruiting suitable patients to participate in a trial, which may be impacted by the number of competing trials that are enrolling patients; |

| • | having patients complete a trial or return for post-treatment follow-up; |

| • | clinical sites deviating from trial protocol or dropping out of a trial; |

| • | adding new clinical trial sites; |

| • | manufacturing sufficient quantities of product candidate or obtaining sufficient quantities of comparator drug for use in clinical trials; or |

| • | the availability of adequate financing and other resources. |

We could encounter delays if a clinical trial is suspended or terminated by us, by the IRBs or ethics committees of the institutions in which such trials are being conducted, by the Data Monitoring Committee, or the DMC, for such trial or by the FDA, the EMA or other comparable regulatory authorities. A suspension or termination may be imposed due to a number of factors, including failure to conduct the clinical trial in accordance with regulatory requirements or our clinical protocols, inspection of the clinical trial operations or trial site by the FDA, the EMA or other comparable regulatory authorities resulting in the imposition of a clinical hold, safety issues or adverse side effects, failure to demonstrate a benefit from using a drug, changes in governmental regulations or administrative actions, manufacturing issues or lack of adequate funding to continue the clinical trial. For example, it is possible that safety issues or adverse side effects could be observed in trials for filgotinib in RA and CD, for GLPG1837 in CF or for GLPG1690 in IPF, which could result in a delay, suspension or termination of the ongoing trials of filgotinib (in one or both indications), GLPG1837, or GLPG1690. If we experience delays in the completion of, or termination of, any clinical trial of our product candidates, the commercial prospects of our product candidates will be harmed, and our ability to generate product revenues from any of these product candidates will be delayed. In addition, any delays in completing our clinical trials will increase our costs, slow down our product candidate development and approval process and jeopardize our ability to commence product sales and generate revenues. Any of these occurrences may harm our business, financial condition and prospects significantly. In addition, many of the factors that cause or lead to a delay in the commencement or completion of clinical trials may also ultimately lead to the denial of regulatory approval of our product candidates.

If filgotinib, GLPG1837, GLPG2222, GLPG1690, GLPG1972 or any other product candidate is found to be unsafe or lack efficacy, we will not be able to obtain regulatory approval for it and our business would be materially harmed. For example, if the results of ongoing or future trials for filgotinib do not achieve the primary efficacy endpoints or demonstrate unexpected safety findings, the prospects for approval of filgotinib, as well as the price of the ADSs or our ordinary shares and our ability to create shareholder value could be materially and adversely affected.

10

Table of Contents

In some instances, there can be significant variability in safety and/or efficacy results between different trials of the same product candidate due to numerous factors, including changes in trial protocols, differences in composition of the patient populations, adherence to the dosing regimen and other trial protocols and the rate of dropout among clinical trial participants. We do not know whether any Phase 2, Phase 3 or other clinical trials we or any of our collaboration partners may conduct will demonstrate consistent or adequate efficacy and safety to obtain regulatory approval to market our product candidates. If we are unable to bring any of our current or future product candidates to market, our ability to create long-term shareholder value will be limited.

We initiated our first clinical study in 2009 and for five of our compounds, Phase 2 studies have been initiated. Filgotinib was our first Phase 2b program, and we have yet to initiate a Phase 3 study.

The rates at which we complete our scientific studies and clinical trials depend on many factors, including, but not limited to, patient enrollment.

Patient enrollment, a significant factor in the timing of clinical trials, is affected by many factors including the size and nature of the patient population, the proximity of patients to clinical sites, the eligibility criteria for the trial, the design of the clinical trial, competing clinical trials and clinicians’ and patients’ perceptions as to the potential advantages of the drug being studied in relation to other available therapies, including any new drugs that may be approved for the indications we are investigating. With respect to our clinical development of GLPG1837 in CF, the availability of Kalydeco® (ivacaftor), which is a drug developed by Vertex to be used to treat patients with a certain mutation of CF, may cause patients to be less willing to participate in our clinical trial for an oral therapy in regions in which an oral therapy has been approved. Since CF is a competitive market in certain regions such as the United States and the European Union with a number of product candidates in development, patients may have other choices with respect to potential clinical trial participation and we may have difficulty in reaching our enrollment targets. In addition, the relatively limited number of patients worldwide (estimated to be 80,000) may make enrollment more challenging. Any of these occurrences may harm our clinical trials and by extension, our business, financial condition and prospects.

We may not be successful in our efforts to use and expand our novel, proprietary target discovery platform to build a pipeline of product candidates.

A key element of our strategy is to use and expand our novel, proprietary target discovery platform to build a pipeline of product candidates and progress these product candidates through clinical development for the treatment of a variety of diseases. Although our research and development efforts to date have resulted in a pipeline of product candidates directed at various diseases, we may not be able to develop product candidates that are safe and effective. Even if we are successful in continuing to build our pipeline, the potential product candidates that we identify may not be suitable for clinical development, including as a result of being shown to have harmful side effects or other characteristics that indicate that they are unlikely to be products that will receive marketing approval and achieve market acceptance. If we do not continue to successfully develop and begin to commercialize product candidates, we will face difficulty in obtaining product revenues in future periods, which could result in significant harm to our financial position and adversely affect the price of the ADSs or our ordinary shares.

Our commercial success depends upon attaining significant market acceptance of our product candidates, if approved, among physicians, healthcare payors, patients and the medical community.

Even if we obtain regulatory approval for one or more of our product candidates, the product may not gain market acceptance among physicians, healthcare payors, patients and the medical community, which is critical to commercial success. Market acceptance of any product candidate for which we receive approval depends on a number of factors, including:

| • | the efficacy and safety as demonstrated in clinical trials; |

11

Table of Contents

| • | the timing of market introduction of the product candidate as well as competitive products; |

| • | the clinical indications for which the product candidate is approved; |

| • | acceptance by physicians, the medical community and patients of the product candidate as a safe and effective treatment; |

| • | the convenience of prescribing and initiating patients on the product candidate; |

| • | the potential and perceived advantages of such product candidate over alternative treatments; |

| • | the cost of treatment in relation to alternative treatments, including any similar generic treatments; |

| • | the availability of coverage and adequate reimbursement and pricing by third-party payors and government authorities; |

| • | relative convenience and ease of administration; |

| • | the prevalence and severity of adverse side effects; and |

| • | the effectiveness of sales and marketing efforts. |

If our product candidates are approved but fail to achieve an adequate level of acceptance by physicians, healthcare payors, patients and the medical community, we will not be able to generate significant revenues, and we may not become or remain profitable.

We currently have no marketing and sales organization. To the extent any of our product candidates for which we maintain commercial rights is approved for marketing, if we are unable to establish marketing and sales capabilities or enter into agreements with third parties to market and sell our product candidates, we may not be able to effectively market and sell any product candidates, or generate product revenues.

We currently do not have a marketing or sales organization for the marketing, sales and distribution of pharmaceutical products. In order to independently commercialize any product candidates that receive marketing approval and for which we maintain commercial rights, we would have to build marketing, sales, distribution, managerial and other non-technical capabilities or make arrangements with third parties to perform these services, and we may not be successful in doing so. In the event of successful development of GLPG1837, GLPG2222, GLPG1690, GLPG1972 or any other product candidates for which we maintain commercial rights, we may elect to build a targeted specialty sales force which will be expensive and time consuming. Any failure or delay in the development of our internal sales, marketing and distribution capabilities would adversely impact the commercialization of these products. With respect to our product candidates, we may choose to partner with third parties that have direct sales forces and established distribution systems, either to augment our own sales force and distribution systems or in lieu of our own sales force and distribution systems. In the instance of filgotinib, under our collaboration agreement with Gilead, if we exercise our co-promotion option with respect to licensed products, we would assume a portion of the co-promotion effort in The United Kingdom, Germany, France, Italy, Spain, The Netherlands, Belgium, and/or Luxembourg and share equally in the net profit and net losses in these territories instead of receiving royalties in those territories during the period of co-promotion. If we are unable to enter into collaborations with third parties for the commercialization of approved products, if any, on acceptable terms or at all, or if any such partner does not devote sufficient resources to the commercialization of our product or otherwise fails in commercialization efforts, we may not be able to successfully commercialize any of our product candidates that receive regulatory approval. If we are not successful in commercializing our product candidates, either on our own or through collaborations with one or more third parties, our future revenue will be materially and adversely impacted.

12

Table of Contents

Coverage and reimbursement decisions by third-party payors may have an adverse effect on pricing and market acceptance.

There is significant uncertainty related to the third-party coverage and reimbursement of newly approved drugs. To the extent that we retain commercial rights following clinical development, we would seek approval to market our product candidates in the United States, the European Union and other selected jurisdictions. Market acceptance and sales of our product candidates, if approved, in both domestic and international markets will depend significantly on the availability of adequate coverage and reimbursement from third-party payors for any of our product candidates and may be affected by existing and future healthcare reform measures. Government authorities and third-party payors, such as private health insurers and health maintenance organizations, decide which drugs they will cover and establish payment levels. We cannot be certain that coverage and adequate reimbursement will be available for any of our product candidates, if approved. Also, we cannot be certain that reimbursement policies will not reduce the demand for, or the price paid for, any of our product candidates, if approved. If reimbursement is not available or is available on a limited basis for any of our product candidates, if approved, we may not be able to successfully commercialize any such product candidate. Reimbursement by a third-party payor may depend upon a number of factors, including, without limitation, the third-party payor’s determination that use of a product is:

| • | a covered benefit under its health plan; |

| • | safe, effective and medically necessary; |

| • | appropriate for the specific patient; |

| • | cost-effective; and |

| • | neither experimental nor investigational. |

Obtaining coverage and reimbursement approval for a product from a government or other third-party payor is a time consuming and costly process that could require us to provide supporting scientific, clinical and cost- effectiveness data for the use of our products to the payor. We may not be able to provide data sufficient to gain acceptance with respect to coverage and reimbursement or to have pricing set at a satisfactory level. If reimbursement of our future products, if any, is unavailable or limited in scope or amount, or if pricing is set at unsatisfactory levels such as may result where alternative or generic treatments are available, we may be unable to achieve or sustain profitability.

In the United States, the Medicare Prescription Drug, Improvement, and Modernization Act of 2003, or MMA, changed the way Medicare covers and pays for pharmaceutical products. The legislation established Medicare Part D, which expanded Medicare coverage for outpatient prescription drug purchases by the elderly but provided authority for limiting the number of drugs that will be covered in any therapeutic class. The MMA also introduced a new reimbursement methodology based on average sales prices for physician-administered drugs. Any negotiated prices for any of our product candidates, if approved, covered by a Part D prescription drug plan will likely be lower than the prices we might otherwise obtain outside of the Medicare Part D prescription drug plan. Moreover, while Medicare Part D applies only to drug benefits for Medicare beneficiaries, private payors often follow Medicare coverage policy and payment limitations in setting their own payment rates. Any reduction in payment under Medicare Part D may result in a similar reduction in payments from non-governmental payors.

In certain countries, particularly in the European Union, the pricing of prescription pharmaceuticals is subject to governmental control. In these countries, pricing negotiations with governmental authorities can take considerable time after the receipt of marketing approval for a product candidate. To obtain reimbursement or pricing approval in some countries, we may be required to conduct additional clinical trials that compare the cost-effectiveness of our product candidates to other available therapies. If reimbursement of any of our product candidates, if approved, is unavailable or limited in scope or amount in a particular country, or if pricing is set at unsatisfactory levels, we may be unable to achieve or sustain profitability of our products in such country.

13

Table of Contents

The delivery of healthcare in the European Union, including the establishment and operation of health services and the pricing and reimbursement of medicines, is almost exclusively a matter for national, rather than EU, law and policy. National governments and health service providers have different priorities and approaches to the delivery of healthcare and the pricing and reimbursement of products in that context. In general, however, the healthcare budgetary constraints in most EU member states have resulted in restrictions on the pricing and reimbursement of medicines by relevant health service providers. Coupled with ever-increasing EU and national regulatory burdens on those wishing to develop and market products, this could prevent or delay marketing approval of our product candidates, restrict or regulate post-approval activities and affect our ability to commercialize any products for which we obtain marketing approval.

Recent legislative and regulatory activity may exert downward pressure on potential pricing and reimbursement for any of our product candidates, if approved, that could materially affect the opportunity to commercialize.

The United States and several other jurisdictions are considering, or have already enacted, a number of legislative and regulatory proposals to change the healthcare system in ways that could affect our ability to sell any of our product candidates profitably, if approved. Among policy-makers and payors in the United States and elsewhere, there is significant interest in promoting changes in healthcare systems with the stated goals of containing healthcare costs, improving quality and/or expanding access to healthcare. In the United States, the pharmaceutical industry has been a particular focus of these efforts and has been significantly affected by major legislative initiatives. There have been, and likely will continue to be, legislative and regulatory proposals at the federal and state levels directed at broadening the availability of healthcare and containing or lowering the cost of healthcare. We cannot predict the initiatives that may be adopted in the future.

The continuing efforts of the government, insurance companies, managed care organizations and other payors of healthcare services to contain or reduce costs of healthcare may adversely affect:

| • | the demand for any of our product candidates, if approved; |

| • | the ability to set a price that we believe is fair for any of our product candidates, if approved; |

| • | our ability to generate revenues and achieve or maintain profitability; |

| • | the level of taxes that we are required to pay; and |

| • | the availability of capital. |

In 2010, the Patient Protection and Affordable Care Act, as amended by the Health Care and Education Reconciliation Act, or, collectively, the ACA, became law in the United States. The goal of the ACA is to reduce the cost of healthcare and substantially change the way healthcare is financed by both governmental and private insurers. The ACA may result in downward pressure on pharmaceutical reimbursement, which could negatively affect market acceptance of any of our product candidates, if they are approved. Provisions of the ACA relevant to the pharmaceutical industry include the following:

| • | an annual, nondeductible fee on any entity that manufactures or imports certain branded prescription drugs and biologic agents, apportioned among these entities according to their market share in certain government healthcare programs; |

| • | an increase in the rebates a manufacturer must pay under the Medicaid Drug Rebate Program to 23.1% and 13% of the average manufacturer price for branded and generic drugs, respectively; |

| • | a new Medicare Part D coverage gap discount program, in which manufacturers must agree to offer 50% point-of-sale discounts on negotiated prices of applicable brand drugs to eligible beneficiaries during their coverage gap period, as a condition for the manufacturer’s outpatient drugs to be covered under Medicare Part D; |

14

Table of Contents

| • | extension of manufacturers’ Medicaid rebate liability to covered drugs dispensed to individuals who are enrolled in Medicaid managed care organizations; |

| • | expansion of eligibility criteria for Medicaid programs by, among other things, allowing states to offer Medicaid coverage to additional individuals and by adding new mandatory eligibility categories for certain individuals with income at or below 133% of the Federal Poverty Level, thereby potentially increasing manufacturers’ Medicaid rebate liability; |

| • | expansion of the entities eligible for discounts under the Public Health Service pharmaceutical pricing program; |

| • | new requirements under the federal Open Payments program and its implementing regulations; |

| • | expansion of healthcare fraud and abuse laws, including the federal False Claims Act and the federal Anti- Kickback Statute, new government investigative powers and enhanced penalties for noncompliance; |

| • | a licensure framework for follow-on biologic products; and |

| • | a new Patient-Centered Outcomes Research Institute to oversee, identify priorities in and conduct comparative clinical effectiveness research, along with funding for such research. |

In addition, other legislative changes have been proposed and adopted since the ACA was enacted. These changes include aggregate reductions to Medicare payments to providers of up to 2% per fiscal year, which went into effect in April 2013. In January 2013, President Obama signed into law the American Taxpayer Relief Act of 2012, which, among other things, reduced Medicare payments to several types of providers, and increased the statute of limitations period for the government to recover overpayments to providers from three to five years. These new laws may result in additional reductions in Medicare and other healthcare funding.

We face significant competition for our drug discovery and development efforts, and if we do not compete effectively, our commercial opportunities will be reduced or eliminated.

The biotechnology and pharmaceutical industries are intensely competitive and subject to rapid and significant technological change. Our drug discovery and development efforts may target diseases and conditions that are already subject to existing therapies or that are being developed by our competitors, many of which have substantially greater resources, larger research and development staffs and facilities, more experience in completing pre-clinical testing and clinical trials, and formulation, marketing and manufacturing capabilities than we do. As a result of these resources, our competitors may develop drug products that render our products obsolete or noncompetitive by developing more effective drugs or by developing their products more efficiently. Our ability to develop competitive products would be limited if our competitors succeeded in obtaining regulatory approvals for drug candidates more rapidly than we were able to or in obtaining patent protection or other intellectual property rights that limited our drug development efforts. Any drug products resulting from our research and development efforts, or from our joint efforts with collaboration partners or licensees, might not be able to compete successfully with our competitors’ existing and future products, or obtain regulatory approval in the United States, European Union or elsewhere. Further, we may be subject to additional competition from alternative forms of treatment, including generic or over-the-counter drugs.

In the field of RA, therapeutic approaches have traditionally relied on disease-modifying anti-rheumatic drugs, or DMARDS, such as MTX and sulphasalazine as first-line therapy. These oral drugs work primarily to suppress the immune system and, while effective in this regard, the suppression of the immune system leads to an increased risk of infections and other side effects. Accordingly, in addition to DMARDS, monoclonal antibodies targeting tumor necrosis factor, or TNF, like AbbVie’s Humira, or IL-6 like Roche’s Actemra, have been developed. These biologics, which must be delivered via injection, are currently the standard of care as first- and second-line therapies for RA patients who have an inadequate response to DMARDS. In November 2012, Xeljanz (tofacitinib citrate), marketed by Pfizer, was approved by the FDA as an oral treatment for the treatment

15

Table of Contents

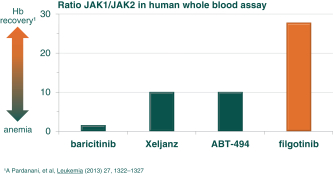

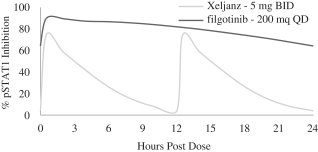

of adult patients with RA who have had an inadequate response to, or who are intolerant of, MTX. Xeljanz is the first and only Janus kinase, or JAK, inhibitor for RA approved for commercial sale in the United States. We are aware of other JAK inhibitors in development for patients with RA, including a once-daily JAK1/2 inhibitor called baricitinib which is being developed by Lilly and expected to be approved as early as 2016, a JAK3/2/1 inhibitor called ASP015k which is being developed in Japan by Astellas, and a JAK inhibitor called ABT-494 which is being developed by AbbVie. Filgotinib, a selective JAK1 inhibitor, was developed in collaboration with AbbVie until AbbVie terminated the collaboration agreement on September 25, 2015. On December 16, 2015, we entered into a collaboration agreement with Gilead, under which we plan to initiate a Phase 3 trial for filgotinib. We expect that filgotinib, which we are developing to treat patients with moderate to severe RA who have an inadequate response to MTX, will compete with all of these therapies. If generic or biosimilar versions of these therapies are approved we would expect to also compete against these versions of the therapies.

In the field of inflammatory bowel disease, or IBD, first line therapies are oral (or local) treatments with several low-cost generic compounds like mesalazine, more effective in ulcerative colitis, or UC, and azathioprine, more effective in CD. Steroids like budesonide are used in both UC and CD. Companies like Santarus have developed controlled-release oral formulation with the aim to have local intestinal delivery of budesonide thereby limiting systemic side effects. For more advanced therapy, monoclonal antibodies with various targets such as TNF and more recently, integrins by vedoluzimab (Entyvio) are approved. We are also aware of other biologics in clinical development for these indications, such as: ustekinumab, developed by Johnson & Johnson, which is in Phase 3 clinical trials and RPC1063, which is being developed by Receptos and has shown efficacy in a Phase 2 trial in UC. There are also several novel oral treatments being explored in Phase 2 and Phase 3, including Pfizer’s Xeljanz. The large number of treatments for UC, and somewhat less for CD, presents a substantial level of competition for any new treatment entering the IBD market.

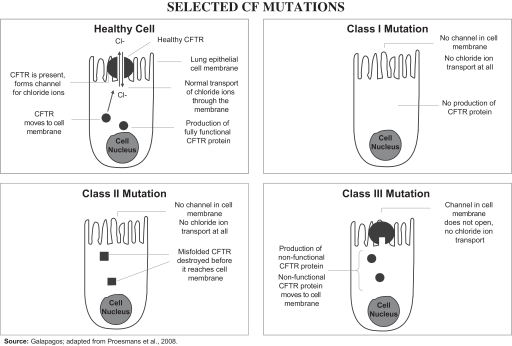

In the field of CF, all but two of the approved therapies to treat CF patients have been designed to treat the symptoms of the disease rather than its cause. Kalydeco, marketed by Vertex, is currently the only approved therapy to address the cause of Class III mutation CF. Kalydeco is a CF transmembrane conductance regulator, or CFTR, potentiator to treat CF in patients with a Class III (G551D) mutation of the CFTR gene. Vertex also markets Orkambi, which is Kalydeco and lumacaftor, a corrector molecule for patients with a Class II (F508del) mutation of the CFTR gene, a broader patient population. Vertex obtained FDA approval in July 2015 for Orkambi in the United States and obtained European Commission Marketing Authorization for Orkambi in Europe in November 2015. We are also aware of other companies, including Novartis, Nivalis, Pfizer, Proteostasis and ProQR, and not-for-profit organizations like Flatley Discovery Lab, which are actively developing drug candidates for the treatment of CF. These typically target the CFTR protein as potentiators, correctors, or other modulators of its activity.

In the field of IPF there are two approved disease modifying drugs: pirfenidone, marketed by Genentech, and nintedanib, marketed by Boehringer Ingelheim. These drugs prolong life for IPF patients by months, leaving an unmet medical need for those developing disease-modifying drugs in this field.

In the field of OA, there are currently no disease-modifying drugs approved. Current treatment involves weight loss, physical therapy, and pain management.

Our product candidates may cause undesirable side effects or have other properties that could delay or prevent their regulatory approval, limit the commercial profile of an approved label, or result in significant negative consequences following marketing approval, if any.

Undesirable side effects caused by our product candidates could cause us or regulatory authorities to interrupt, delay or halt clinical trials and could result in a more restrictive label or the delay or denial of regulatory approval by the FDA, the EMA or other comparable regulatory authorities. Results of our trials could reveal a high and unacceptable severity and prevalence of certain side effects. In such an event, our trials could be suspended or terminated and the FDA, the EMA or comparable regulatory authorities could order us to cease

16

Table of Contents

further development of or deny approval of our product candidates for any or all targeted indications. The drug- related side effects could affect patient recruitment or the ability of enrolled patients to complete the trial or result in potential product liability claims. Any of these occurrences may harm our business, financial condition and prospects significantly.

If one or more of our product candidates receives marketing approval, and we or others later identify undesirable side effects caused by such products, a number of potentially significant negative consequences could result, including:

| • | regulatory authorities may withdraw approvals of such product; |

| • | regulatory authorities may require additional warnings on the label; |

| • | we may be required to create a medication guide outlining the risks of such side effects for distribution to patients; |

| • | we could be sued and held liable for harm caused to patients; and |

| • | our reputation may suffer. |

Any of these events could prevent us from achieving or maintaining market acceptance of the particular product candidate, if approved, and could significantly harm our business, results of operations and prospects.

Risks Related to Our Financial Position and Need for Additional Capital

We are a clinical-stage company with no approved products and no historical product revenues, which makes it difficult to assess our future prospects and financial results.

We are a clinical-stage biotechnology company and we have not yet generated any product income. Pharmaceutical product development is a highly speculative undertaking and involves a substantial degree of uncertainty. Our operations to date have been limited to developing our technology and undertaking pre-clinical studies and clinical trials of our product candidates, including filgotinib, GLPG1837, GLPG2222, GLPG1690 and GLPG1972. We may not have the ability to overcome many of the risks and uncertainties frequently encountered by companies in new and rapidly evolving fields, particularly in the pharmaceutical area. Consequently, the ability to predict our future operating results or business prospects is more limited than if we had a longer operating history or approved products on the market.

We have incurred significant losses since our inception and anticipate that we will continue to incur significant losses for the foreseeable future. We have never generated any revenue from product sales and may never be profitable.

We have incurred significant operating losses since our inception in 1999. We have incurred net losses of €8.1 million for the year ended December 31, 2013, net profit of €33.2 million for the year ended December 31, 2014 and net losses of €118.4 million for the year ended December 31, 2015. Our prior losses, combined with expected future losses, have had and will continue to have an adverse effect on our shareholders’ equity and working capital. In April 2014, we sold our service division for net proceeds of €130.8 million. The sale of the service division will continue to impact future results as the service division contributed to the net result of €8.7 million for the year ended December 31, 2013, the last full calendar year where the service division was part of our company. We expect to continue incurring significant research, development and other expenses related to our ongoing operations, and to continue incurring losses for the foreseeable future. We also expect these losses to increase, due to higher costs of later stage development, as we continue our development of, and to seek regulatory approvals for, our product candidates.

We do not anticipate generating revenues from sales of products for the foreseeable future, if ever. If any of our product candidates fail in clinical trials or do not gain regulatory approval, or if any of our product

17

Table of Contents