UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

For the fiscal year ended:

For the transition period from _____________ to _____________

Commission File No.

(Exact name of registrant as specified in its charter)

|

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

(Address of Principal Executive Offices; Zip Code)

(

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(g) of the Exchange Act: Common Stock

Indicate by check

mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ¨

Indicate by check mark whether the registrant

(1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months

(or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements

for the past 90 days.

Indicate by check mark whether the registrant

has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405

of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol | Exchange on which registered |

| NONE | ---- | ---- |

| 1 |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or “emerging growth company”. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |

| ¨ | Smaller reporting company | |||

| Emerging Growth Company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether

the registrant has filed a report on and attestation its management’s assessment of the effectiveness of its internal control over

financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C 7262(b)) by the registered public accounting firm that

prepared or issued its audit report.

Indicate by check mark whether registrant is a

shell company (as defined in Rule 12b-2 of the Act). Yes ¨

The aggregate market value of the Registrant's common stock held by

non-affiliates of the Registrant at June 30, 2022 (the last business day of the Registrant's most recently completed fiscal year) was

$

As of March 31, 2023, there were shares of common stock issued and outstanding. The trading symbol of the common stock is VEII.

DOCUMENTS INCORPORATED BY REFERENCE

| 2 |

Annual Report on Form 10-K

For the Year Ended December 31, 2022

TABLE OF CONTENTS

| PART I | Page No. | |

| Item 1. | Business | 6 |

| Item 1A. | Risk Factors | 15 |

| Item 1B. | Unresolved Staff Comments | 23 |

| Item 2. | Properties | 23 |

| Item 3. | Legal Proceedings | 23 |

| Item 4. | Mine Safety Disclosures | 23 |

| PART II | ||

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 23 |

| Item 6. | [RESERVED] | 24 |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 25 |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 37 |

| Item 8. | Financial Statements and Supplementary Data | 37 |

| Item 9. | Changes In and Disagreements with Accountants on Accounting and Financial Disclosure. | 37 |

| Item 9A. | Controls and Procedures | 37 |

| Item 9B. | Other Information | 38 |

|

Item 9C. |

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections |

38 |

| PART III | ||

| Item 10. | Directors, Executive Officers and Corporate Governance | 39 |

| Item 11. | Executive Compensation | 44 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 47 |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | 48 |

| Item 14. | Principal Accounting Fees and Services | 50 |

| PART IV | ||

| Item 15. | Exhibits, Financial Statement Schedules | 51 |

|

SIGNATURES |

53 | |

| 3 |

Special Note Regarding Forward Looking Statements

This Annual Report on Form 10-K (“Form 10-K”) contains forward-looking statements, which are identified by the fact that they do not relate strictly to historical or current facts. These statements often include words such as “may,” “will,” “estimate,” “intend,” “seek,” “expect,” “project,” “anticipate,” “believe,” “plan,” “could,” “target,” “predict,” “likely,” “should,” “forecast,” “outlook,” “model,” “continue,” “ongoing” or other similar terminology. Forward-looking statements are based on our current expectations, estimates, assumptions or projections concerning future results or events. Forward-looking statements are neither predictions nor guarantees of future events, circumstances or performance and are inherently subject to known and unknown risks, uncertainties and assumptions that could cause our actual results and events to differ materially from those indicated by those forward-looking statements. We cannot assure you that any of our expectations, estimates, assumptions or projections will be achieved. Factors that could cause actual results and events to differ materially from our expectations, estimates, assumptions or projections include (i) the risks and uncertainties described in the Risk Factors included in Part I, Item 1A of this Form 10-K and (ii) the factors described in Management’s Discussion and Analysis of Financial Condition and Results of Operations included in Part II, Item 7 of this Form 10-K. These forward-looking statements include, among other things, statements relating to:

| · | our expectations regarding growth in the information technologies industries in China, Hong Kong and Philippines or any other markets; |

| · | our expectation regarding increasing demand for our products and services in China, Hong Kong, Philippines and any new markets; |

| · | any belief that we will be able to effectively compete with our competitors and increase our market share in the face of possible technological advances or superior resources and market share by competitors, or aggressive pricing by competitors; |

| · | our expectations with respect to increased revenue growth and our ability to achieve and sustain profitability resulting from any increases in our productivity; |

| · | our ability to fund operations and business and product growth and the availability of sufficient, affordable funding when required; |

| · | whether we can expand or operate successfully in a market outside of our traditional market of China and Hong Kong; |

| · | our ability to determine appropriate new products or services and then expand and fund our offerings of products and services to new geographical markets and operate profitably in such new markets; |

| · | the success and cost of new product or service initiatives in existing or new markets; |

| · | the disruption or failure of our or those of our customers’ computer systems, networks, information systems or technologies that we install, service or maintain as a result of computer hacking, computer viruses, malware, “cyber-attacks,” misappropriation of data, outages, natural disasters and other material events; |

| · | continuation of key strategic relationships, which can be essential for a small reporting company like us; and |

| · | our future business development, results of operations and financial condition. |

You should not place undue reliance on forward-looking statements, which speak only as of the date hereof. We disclaim any obligation to publicly update any forward-looking statement to reflect subsequent events or circumstances, except as required by law.

Certain numerical figures included in this Form 10-K may be subject to rounding adjustments. Accordingly, such numerical figures shown as totals in various tables may not be arithmetic aggregations of the figures that precede them. Also, forward-looking statements represent our estimates and assumptions only as of the date of this Form 10-K. You should read this Form 10-K and the documents that we reference and filed as exhibits to the Form 10-K completely and with the understanding that our actual future results may be materially different from what we expect or historical results. Except as required by law, we assume no obligation to update any forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in any forward-looking statements, even if new information becomes available in the future.

Use of Certain Defined Terms

Except as otherwise indicated by the context, references in this Form 10-K to:

Unless the context requires otherwise, all references to “we,” “our,” “us,” “VEII” and “Company” refer to the Company and its consolidated subsidiaries (unless stated otherwise or the context indicates otherwise) and “Company’s operating subsidiaries” or “its operating subsidiaries” refers to Company’s consolidated subsidiaries (as identified in the Corporate Organization section of Item 1 Business below at page 6). References to “China,” “PRC” and “Chinese” refers to People’s Republic of China. References to “Chinese government” refers to PRC central government and “Chinese laws” refers to PRC laws. “Hong Kong“ as used below means the Hong Kong SAR. Hong Kong is a special administrative region or “SAR” of China under the Basic Law, which is the “constitution” of Hong Kong as established as part of the transfer of Hong Kong to China by the United Kingdom in 1997, and is treated as such in the disclosures below. However, the operational risks faced by the Company and its subsidiaries and associated with China also apply to Company and its subsidiaries in Hong Kong due to the demonstrated ability and willingness of the Chinese government to impose Chinese laws and policies in Hong Kong, even if those actions are in conflict with the Basic Law. As such, Hong Kong is not independent of Chinese government control and influence and our operations and assets in Hong Kong can be subjected to Chinese government regulation and decisions.

| 4 |

“VEI CHN” refers to Value Exchange Int’l (China) Limited, and its consolidated subsidiaries, namely Value Exchange Int’l (Hong Kong) Limited (“VEI HKG”) and Cucumbuy.com Limited (“CUCUMBUY”), formerly known as Ke Dao Solutions Limited, both are companies incorporated in Hong Kong as limited liability companies, and Value Exchange Int’l (Shanghai) Limited (“VEI SHG”), a wholly Foreign Owned Enterprise (“WFOE”) registered in Shanghai, PRC. VEI HKG, CUCUMBUY, all of which Hong Kong SAR subsidiaries are collectively referred to as “HKG subsidiaries” and VEI SHG is referred to as “PRC Subsidiary” (collectively PRC Subsidiary and HKG subsidiaries may be referred to as “VEI CHN Group”). WFOE is a form of company owned by foreign investors recognized under Chinese laws.

References to “OTCQB” means The OTC Markets Group, Inc.’s QB Venture Market Tier, a national quotation system with web site at www.otcmarkets.com.

References to the “Bulletin Board” and the “OTC Bulletin Board” are to the Over-the-Counter Bulletin Board, a securities quotation service, which is accessible at the website http://www.finra.org/industry/otcbb/otc-bulletin-board-otcbb.

References to PRC Subsidiary’s “registered capital” are to the equity securities of PRC Subsidiary, which under PRC law is measured not in terms of shares owned but in terms of the amount of capital that has been contributed to a company by a particular shareholder or all shareholders. The portion of a limited liability company’s total capital contributed by a particular shareholder represents that shareholder’s ownership of the company, and the total amount of capital contributed by all shareholders is the company’s total equity. Capital contributions are made to a company by deposits into a dedicated account in the company’s name, which the company may access in order to meet its financial needs. When a company’s accountant certifies to PRC authorities that a capital contribution has been made and the company has received the necessary government permission to increase its contributed capital, the capital contribution is registered with regulatory authorities and becomes a part of the company’s “registered capital.”

“IT Business” means select services and solutions in computer software programming and integration, and computer systems, Internet and information technology systems engineering, consulting, administration, installation and maintenance, including e-commerce and payment processing to the Retail Sector.

“IT” means information technologies, which includes software programs and applications, computer and network hardware and systems, telecommunications systems and automation technologies used in business, financial, commercial or information processing/database transactions, applications and purposes. “IT” services consist of software programming, hardware and network configuration, software and hardware maintenance/repair and upgrades, design and engineering consulting, business and customer need analysis, administration of systems (including database management), repair and maintenance and testing.

“POS” means point of sale computer programs and systems used to record retail or Internet sales, process payments and make corresponding inventory record adjustments. POS systems can include cybersecurity or systems security technologies as well.

“Retail Sector” means commercial concerns selling products and/or services to the general public through brick and mortar stores and/or e-commerce web sites.

All references to “Renminbi” or “RMB” are to the legal currency of China.

All references to “Hong Kong dollars” or “HK$” are to the legal currency of the Special Administrative Region of Hong Kong.

All references to “U.S. dollars,” “dollars,” or “$” are to the legal currency of the United States of America.

“Exchange Act” means the Securities Exchange Act of 1934, as amended.

“Securities Act” means the Securities Act of 1933, as amended.

“SEC” or “Commission” means the U.S. Securities and Exchange Commission.

| 5 |

PART I

ITEM 1. BUSINESS. Overview

History of Value Exchange International, Inc.

History. We were incorporated in the State of Nevada on June 26, 2007. We changed to our current corporate name, “Value Exchange International, Inc.”, on December 5, 2017.

Current Business Focus. We are a provider of customer-centric technology solutions for the retail industry in Hong Kong SAR and certain regions of China and Philippines. Due to impact of Coronavirus/COVID-19 pandemic (“COVID 19 pandemic”) and lack of adequate funding for business expansion into Southeast Asia, our strategic plan to expand our business into Southeast Asia made no progress in fiscal year 2022.

By integrating market-leading Point-of-Sale/Point-of-Interaction (“POS/POI”), Merchandising, Customer Relations Management or “CRM” and related rewards, Locational Based (GPS & Indoor Positioning System (“IPS”)) Marketing, Customer Analytics, Business Intelligence solutions, our products and services are intended to provide retailers with the capability to offer a consistent shopping experience across all channels, enabling them to easily and effectively manage the customer lifecycle on a one-to-one basis. We promote ourselves as a single IT source for retailers who want to extend existing traditional transaction processing to multiple points of interaction, including the Internet, kiosks and wireless devices. Our products and services are focused on helping retailers realize the full benefits of Customer Chain Management with its suite of solutions that focus on the customer, on employees, and the infrastructure that supports the selling channel. Company is headquartered in Hong Kong and with offices in Shenzhen, Guangzhou, Shanghai, Beijing, China; Manila, Philippines; and Kuala Lumpur, Malaysia.

We believe that the IT Business often presents opportunities to expand a provider’s market reach or customer base by acquisitions of existing businesses or operating assets. The Company’s business strategy includes reviewing possible acquisitions of existing businesses or operating assets in existing or adjacent markets and to do so when and if such an acquisition appears to be compatible and an enhancement of our core business lines and can be consummated with available cash and other resources. Our ability to pursue and consummate acquisitions may be limited, and has been limited, by available cash for mergers and acquisitions and other resources and the perceived cost and burdens of acquiring and integrating the target business or new operating assets into our operations. The availability of funding and cash flow are the most significant limitations on our ability to expand through acquisitions of businesses and assets – both in terms of money on hand and ability to finance acquisitions, but the estimated business hurdles in successfully penetrating a new market is also a factor in deciding whether to proceed with that expansion. The limited liquidity and bid price of our Common Stock in the public stock market also hampers our ability to use shares of Common Stock as attractive consideration to target companies in a merger or acquisition.

Initial Business Focus. Our initial intended, primary business was to operate a credit card processing and merchant-acquiring services company that provide credit card clearing services to merchants and financial institutions in PRC. From inception, we strove unsuccessfully to create and establish a proposed Global Processing Platform concept to support the credit card processing services (“SinoPay GPP”). Specifically, the Company’s Internet Protocol business was to be a provider of Internet Protocol (“IP”) processing services in Asia to bank card-accepting merchants (“IP Business”). The Company efforts to establish a viable IP Business did not succeed.

The acquisition of VEI CHN in 2014 shifted the primary business focus to the IT Business because IT Business provided a more readily attainable revenue generating business line and because of our strategic decision that IT Business presented a greater growth and profit potential than IP Business. Further, we believe that the SinoGPP system would require ongoing and potentially expensive marketing and sales effort as well as extensive technical upgrades and function enhancements due to the highly competitive market for Point Of Sale (“POS”) systems and longer sales cycle for POS systems than IT Business project and consulting sales. VEI CHN was acquired in a stock-for-stock exchange (“VEI CHN Share Exchange”).

Smart Baggage Tags. Through a cooperative effort with another company, Company has the ability to market a smart baggage tag that allows consumers to track the location of their baggage through a smart phone or device using the smart baggage tag and related application. Efforts to promote the smart baggage tag were suspended in 2021 and 2022 due to impact of COVID-19 pandemic on air travel. As of the filing of this Form 10-K, there are no current plans to make any dedicated marketing effort for expanding the market for or sales of the smart baggage tags in 2023.

| 6 |

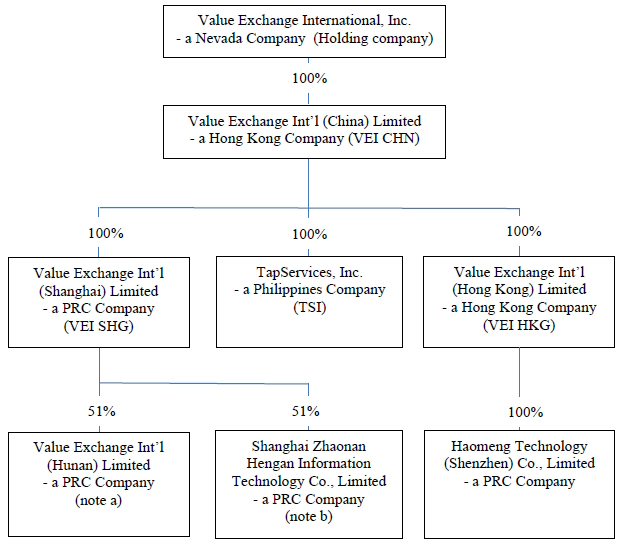

History of Value Exchange Int’l (China) Limited. VEI CHN was first established on November 16, 2001 in Hong Kong as a limited liability company. VEI CHN is a holding company with two subsidiaries established in Hong Kong, namely TAP Services (HK) Limited which was incorporated on August 25, 2003 and acquired by VEI CHN on September 25, 2008, and subsequently changed to its current name as Value Exchange Int’l (Hong Kong) Limited (“VEI HKG”) on May 13, 2013, and Cucumbuy.com Limited (“CUCUMBUY”), which was incorporated on May 14, 2013 and disposed on May 21, 2018 with consideration of HK$1. VEI CHN also set up a Wholly-owned Foreign Enterprise (WOFE) in Shanghai, PRC, in September 2, 2008 in the name of Value Exchange Int’l (Shanghai) Limited (“VEI SHG”). In January 2017, VEI CHN acquired TapServices, Inc., a corporation organized under the laws of the Republic of the Philippines (the “TSI”). Prior to acquisition of TSI, the Company provided extensive consulting services to TSI and, from such relationship, the Company was familiar with TSI operations. In January 2019, VEI SHG completed the setup procedures of a subsidiary with 51% ownership in Hunan, PRC, in the name of Value Exchange Int’l (Hunan) Limited (“VEI HN”). In February 2020, VEI SHG completed the setup procedures of a subsidiary with 51% ownership in Shanghai, PRC, in the name of Shanghai Zhaonan Hengan Information Technology Co., Limited (“SZH”). In January 2022, VEI HKG completed the setup procedures of a subsidiary with 100% ownership in Shenzhen, PRC, in the name of Haomeng Technology (Shenzhen) Co., Limited. (“HTS”).

Principal business of VEI and its Subsidiaries

VEII is a holding company for its operating subsidiaries. VEI CHN operations are the primary operations of the Company. The principal business of VEI CHN for more than 15 years is to provide the IT Business (consisting of select services and solutions in computer software programming and integration, and computer systems, Internet and information technology systems engineering, consulting, administration, installation and maintenance, including e-commerce and payment processing) to the Retail Sector, primarily to retailers in Hong Kong SAR, Macau SAR and PRC and as more fully described below. As is customary in the industry, such services and solutions are provided by both company employees, contractors and consultants. The primary services and products of the IT Business are:

| a) | Systems maintenance and related service |

VEI CHN Group provides development and customization of software and hardware, enhancements thereto and maintenance services for installed POS system. VEI CHN Group markets, sells and maintains its own brand POS software – edgePOS as well as third party brands (e.g. NCR/Retalix), which is one of the leading POS software programs in the Chinese-Hong Kong market. These software enhancements and programming can integrate with different IP systems.

Systems maintenance services consist of: i) software maintenance service, including software patches and software code revisions; ii) installing, testing and implementing software; iii) training of customer personnel for the use of software; and iv) technical support for software systems.

Other services include system installation and implementation, including i) project planning; ii) analysis of customer information and business needs from a IT perspective (“System Analysis”); iii) design of the entire system; iv) hardware and consumables selection advice and sales; and v) system hardware maintenance. These services typically consist of customer projects for New Store Opening (“NSO”) and Install, Move, Add and Change (“IMAC”) for retail, and ad-hoc custom system projects for other business sectors. Our primary focus is the retail sector in Hong Kong, PRC and Philippines.

| b) | Systems development and integration |

VEI CHN Group provides value-added software, which integrates with customer owned or licensed software, and ad-hoc software development projects for other business sectors. Besides use of proprietary, custom software code, our services may from time to time license standard third party software programs.

Business partner and customers

The main business partner of the IT Business group is the Chinese and Hong Kong subsidiary operations (“WN”) of Diebold Nixdorf Inc. (formerly, “Wincor Nixdorf AG”, a German public company), a U.S.-German public company subject to the reporting requirements of the Exchange Act, (“DN”). Since 1990’s, VEI CHN Group served the AS Watson Group, a retail conglomerate including Watsons, Parknshop and Fortress, directly and through a sub-contracting arrangement with WN in the China-Hong Kong region. This contributes almost half of the gross sales revenue each year to VEI CHN.

In recent years, VEI CHN has striven to broaden its clientele in retail sector and to other business sectors. VEI CHN Group secured a number of service contracts for leading retail groups, Robinson Retails Group in Philippines and Dairy Farm in Hong Kong. PCCW, a leading telecommunication company in Hong Kong, and Inland Revenue Department of the Hong Kong Government have also become major customers of the VEI CHN Group. The focus on expanding clientele in the retail sector is a current priority of Company’s growth strategy.

| 7 |

The annual sales of VEI CHN Group have been increasing over the past few years in its IT Business by expanding its customer base and its scope of services. VEI CHN Group solution now runs in over 10,000 POS in the region and provides a solid foundation to VEII’s services for IP systems. Also, VEI CHN Group is seeking to leverage its existing POS solution customer base to expand into the mobile Customer Relationship Management and Rewards market. The importance of the mobile market in commerce is globally recognized. Even through the Mobile Customer Relationship Management and Rewards programs has not produced any significant revenues to the VEI CHN Group, the programs seek to exploit the increasing use of mobile devices to shop and purchase products and services, to sustain consumer loyalty by rewards for repeat purchases by mobile devices and to permit companies to develop consumer profile databases used to fashion targeted marketing to the consumers based on purchasing habits. We provide no assurances that we will be able to develop a profitable or significant mobile market program or operation. Further, mobile applications and products and services may contain defects in design, manufacture, or operation that make them insecure or ineffective for their intended purposes. Mobile application products and services may have multiple layers of hardware, sensors, processors, software, and firmware, several of which we may not develop or control. Each layer, including the weakest layer, can impact the security of the whole system.

We will evaluate the merits of this business and growth strategy from time to time and may elect in the future to continue our IT Business focus, or focus more on one segment than the other, including seek business opportunities in the applications of digital technology which we believe can raise our customers’ competitive edge leading to possible increase in market share and profitability in their business sectors. Any change in business focus will be based on current economic conditions, competitive environment, our available cash and infrastructure resources, current customer demand trends and financial results of each segment of our post-VEI CHN Share Exchange business plan. As of the date of the filing of this Form 10-K, we are pursuing our emphasis on IT Business in our core Hong Kong SAR and PRC market while also exploring expansion opportunities in adjacent Asia Pacific markets. Our ability to exploit adjacent market opportunities for expansion will be limited and governed by available, affordable funding and cash flow as well as consideration of business and regulatory hurdles in penetrating a new market.

| 8 |

Health and Cosmetic Retailer Agreement. On February 16, 2018, VEI SHG, signed a January 24, 2018 stores equipment support agreement (“Agreement”) with the largest health care and beauty retailer (“Retailer”) in China. Under the Agreement, the Retailer has contracted for site and preventive maintenance and support for computer and point of sale systems (“Systems”) as well as new store and store renovation install and migration services for Systems from the VEI SHG. The Agreement is non-exclusive, covers Retailer’s stores in the northern and eastern region of China and runs through since December 2019. In March 2020, a renewal agreement signed with the Retailer, and related service extended to March 31, 2023.

In fiscal year 2022, VEI SHG realized $4.35 million in gross revenues from the work under the Agreement.

| 9 |

CORPORATE STRUCTURE

Our corporate organizational chart, as of December 31, 2022, is as follows:

Note a: The remaining 49% share equity of VEI HN is owned by Li Gongyuan, a Chinese national.

Note b: The remaining 49% share equity of SZH is owned by Shanghai Nanan Cosmeceutical Technology Development Limited, a Chinese company, which 54.6% share is effectively controlled by Li Chengliang, a Chinese national.

Marketing

Marketing activities are designed to inform potential clients about the benefits of using our services and include and will include the following: face-to-face sales and marketing (including online presentations); development and distribution of marketing literature; direct mail and email; advertising; promotion of our web site; attendance at trade shows or product seminars; and industry analyst relations campaign.

Sales are managed at the subsidiary level by each subsidiary. The Company has a Sales and Marketing team in each regional office of its existing China/Hong Kong and Manilla markets to promote and maintain good business relationships with our customers. We strive to provide high quality and fast response services to our customers in our Help Centre, Maintenance Support Team and Professional IT Engineer to help customers solve their problems and satisfy their IT needs.

VEI CHN Group has been serving in IT Business sectors for over 15 years, focusing on POS maintenance and support to retail sector. The VEI CHN Group will continue its key business and seek to expand its client base to gain more market share in PRC, Hong Kong, and certain other areas of Asia Pacific. VEII may consider acquiring companies in the Asia Pacific region with similar business, subject to financial wherewithal to do so and subject to a suitable and affordable acquisition opportunity. The perceived cost of market penetration will also be a factor in deciding whether to pursue any acquisition opportunities, which calculation includes strength of competition and other business hurdles as well as regulatory hurdles in establishing a new market. While the Company has secured a convertible credit line for $1.5 million in late January 2023 and revolving credit line for $1 million in July 2022, the Company and its subsidiaries do not currently have ready access to funding dedicated for acquisitions and would have to locate sufficient, affordable funding to pursue any acquisition or merger with a significant cash consideration requirement. Funding from the credit lines is primarily dedicated as of the date of the filing of this Form 10-K to operating expenses and business development of operations in existing markets. The Company evaluates the use of funding from credit lines from time to time and the use of proceeds, which may include business expansion, may be applied to future expansion into new markets in the future. The Company and its subsidiaries may be unable to locate the funding, whether equity or increased debt funding, needed to consummate a merger or acquisition requiring a significant cash consideration or significant post-acquisition working capital, especially since the Company is a small reporting company with a “penny stock” common stock that is not typically suitable for significant equity funding and Company lacks the tangible assets usually required for securing significant debt financing.

| 10 |

We use strategic partnerships as another way of marketing and selling our IT Business. The operating subsidiaries will also cooperate with strategic partners in the local markets to secure and provide maintenance services to major retail customers and as a basis for attempting to expand our business in our markets. In fiscal year 2022, we had over 10 strategic partner arrangements engaged in providing our services to customers in our China/Hong Kong markets.

Competition

We operate in a highly competitive, customer-driven industry and we compete against a variety of local and regional competitors of varying operational sizes, product/service offerings and resources. In some instances, our competitors have greater market share and consumer loyalty and brand-name recognition, fewer regulatory burdens, easier access to financing (whether debt or equity funding and greater and easier access to equity funding through sales of their equity securities to the public), greater operating resources, greater operating capabilities and efficiencies of scale (including technology personnel, research and development capabilities, joint venture partners and marketing-sales channels), longstanding relationships with regulatory authorities and customers, more customers, and more flexibility to offer discounted services or products.

We face significant competition from large multinational service providers, such as DN, NCR, Fujitsu IBM, Toppan Forms and large national companies, such as Octopus card, an electronic payment in online or offline system in Hong Kong. Though VEI CHN Group faces keen competition in the maintenance service market, it believes that it has a well-trained technical team that offers services to the satisfaction of our customers, and as is the case with many smaller companies in the IT segment, we believe we can offer more customized and cost effective services to certain customers than larger competitors. Without extensive teaming with strategic partners, we lack the capabilities to compete directly with larger competitors in projects or work requiring capabilities of a large company. This can from time to time limit the number and nature projects that we can pursue or handle. VEII may also experience a competitive disadvantage in bids or prospective work where extensive and broad prior projects in certain areas of IT are required to bid and to win bids. An instance of such a competitive disadvantage would be technical work in which we do not have extensive prior experience and cannot attain the required technical proficiency, or we do not have a prior relationship with the customer in question.

We also face competition from companies that are of comparable size and resources. In such competition, price and scope of services or qualification of personnel often determines the winning provider. Competition for qualified personnel is an ongoing and significant challenge faced by all companies in the IT Business industry.

Preservation and growth of our business depends on maintaining sufficient, competent staff and attractive pricing.

Some of our competitors in our industry have substantially greater capital and technical resources than we have and, operate as subsidiaries of financial institutions or bank holding companies, which may allow them on a consolidated basis to own and conduct depository and other banking activities that we do not have the regulatory authority to own or conduct. Since they are affiliated with financial institutions or banks, these competitors do not incur the costs associated with being sponsored by a bank for registration with card networks and they can settle transactions quickly for their own merchants. We do not, however, currently contemplate pursuing an acquisition or strategic relationship with a financial institution in order to increase our competitiveness and such an acquisition or strategic relationship is not prominent in our current business and growth strategy. Our current operational focus is to improve the efficiency and profitability of existing IT Business.

Cybersecurity and Security of Computer Networks

We maintain certain computer networks, computer systems and databases in connection with our business operations and services. We use readily available third party security programs to protect these systems and databases and we periodically review security measures. Any security system or program may be vulnerable to hacking or security breaches, especially since hacking and malicious programs are constantly evolving to overcome new security measures. Like any company’s computer and network systems and databases, our systems and databases could be vulnerable to security hacking or malicious programs. We may also be vulnerable to security leaks and violations by employees and contractors, which is a threat faced by all IT Business companies. We have not experienced any significant security breaches or problems as of the date of filing of this Form 10-K. VEII technical staff typically evaluates cybersecurity and security measures from time to time as new threats become known to us.

| 11 |

There can be no assurance that our efforts to protect our computer systems, networks and other information systems will prevent any of the problems identified as cyber security attacks or problems. The problem of this type might be caused by events such as computer hacking, computer viruses, worms and other destructive or disruptive software, "cyber-attacks" and other malicious activity, defects in the hardware and software comprising our network and information systems, as well as natural disasters, power outages, terrorist attacks and similar events. Such events could have an adverse impact on us and our customers, including degradation of service, service disruption, excessive call volume to help centers and damage to our or customers’ equipment and data. Operational or business delays for our operations or customer operations may result from the disruption of computer systems, network or information systems and the subsequent remediation activities. These events may create negative publicity resulting in reputation or brand damage with customers and our results of operations could suffer. Since we provide computer, software and system services and products to customers, cyber security attacks on our computer systems, networks and other information systems may affect our customers’ computer systems, networks and other information systems and produce liabilities on our part to such customers.

Due to the evolving and often very sophisticated nature of cyber security threats, cyber security is an ongoing challenge for all IT Business companies like us. Even the most diligent compliance with industry standards for cybersecurity can fail to defeat all cyber security attacks.

Key Personnel

The following personnel are considered critical to our operations: Kenneth Tan and Benny Lee, who provide executive management services and strategic direction. Mr. Lee serves as a director of VEI SHG. We do not have key man insurance to fund replacement of any key personnel. We also frequently use third party consultants acting as independent contractors to assist in the completion of various projects, which consultants are usually hired on a project-by-project basis. Third parties are instrumental to keep the development of projects on time and on budget. Reliance on independent contractors is common in technology services businesses. We do not anticipate and have not experienced any significant problem in securing needed technical expertise, but the inability to secure needed technical expertise is a risk faced by IT service companies like our company.

The Company has not developed a formal succession plan in the event of the retirement, disability or death of key personnel. In the event of the loss of the services of any key personnel, the Company would in all likelihood be forced to recruit an outside person to fill a key personnel position or rely on existing officers to perform the duties of key personnel. The Company may lack sufficient cash and benefits to attract qualified personnel for key personnel positions.

A common problem in our industry is key or important contractors and employees being lured to more attractive or lucrative work opportunities. VEII cannot typically match the level and scope of financial incentives offered by larger competitors to workers. VEII has to rely on active recruitment coupled with offering projects that match workers’ skills and interests as well as providing an appealing work environment and competitive base compensation in order to maintain or create an adequate work force on a project-by-project basis. VEII adopted a 2022 Equity Incentive Plan in 2022, but VEII has not issued any stock-based compensation under that plan as of the date of the filing of this Form 10-K. Company will evaluate the need or benefit of granting incentive company under the 2022 Equity Incentive Plan in 2023. Since the Company’s Common Stock is a penny stock, incentive compensation may not be a significant benefit to attract or retain personnel.

Insurance

Except the Company’s subsidiaries in (i) PRC are required to cover its employees with medical, retirement and unemployment insurance programs, and (ii) Hong Kong are required to cover its employees with labor insurance programs under the prevailing laws and regulations of the PRC and in Hong Kong, we do not maintain other insurance. Because we may not have sufficient insurance, if we are made a party to a liability legal action, we may not have sufficient funds to defend the litigation or may suffer another liability. If that occurs a judgment or liability that is not covered by any insurance or covered by available cash or funding, could cause us to cease or reduce operations. We did not experience any significant claims against our insurance in fiscal year 2022.

Government Regulation

We are subject to U.S. federal securities laws and the corporate laws of the State of Nevada. With respect to regulation of our IT Business, especially in segments related to the Internet, the Internet is increasingly popular and essential on a global basis and is subject to changing and sometimes expanding regulation. As a result, it is possible that a number of international and local laws and regulations may be adopted with respect to the Internet applications and transactions, including ones used in or serviced by our service. These laws may cover issues such as user privacy, freedom of expression, pricing, content and quality of products and services, taxation, advertising, intellectual property rights and information security. Furthermore, the growth of electronic commerce may prompt calls for more stringent consumer protection laws. Existing and future laws and regulations governing the privacy of end users or their customers’ information is or may become part of the regulatory burden of conducting our business lines. We do not provide our services in the U.S. as of the date of this Form 10-K, but the global nature of the Internet and e-commerce and financial transactions means that any company may become subject from time to time to U.S. or foreign laws on privacy, financial regulation, business regulation or tax law.

| 12 |

We are not certain how our existing business may be affected by the application of existing, evolving laws, or extension of foreign laws to our operations and, governing issues such as property ownership, copyrights, encryption and other intellectual property issues, taxation, libel, obscenity and export or import matters. The vast majority of such laws were adopted prior to the advent of the Internet or are typically aimed at Internet providers or Internet IT companies with international operations. However, we may become subject and affected by Internet related laws and regulation in the future, especially in China and Hong Kong where the Chinese government has a heightened concern about national security threats through the Internet. Changes in laws intended to address such issues could create uncertainty in the Internet market place, including areas affecting our business lines. Such uncertainty could reduce demand for services or increase the cost of doing business as a result of litigation or regulatory costs or increased service delivery costs. In addition, because our services could be available over the Internet in multiple states and foreign countries, other jurisdictions may claim that we are required to qualify to do business in each such state or foreign country. Our failure to qualify a business in a jurisdiction where it is required to do so could subject it to taxes and penalties. It could also hamper our ability to enforce contracts in such jurisdictions. The application of laws or regulations from jurisdictions whose laws do not currently apply to our business could have a material adverse effect on our business, results of operations and financial condition.

Like many companies, and from time to time, the Company may review the economic and tax advantages of various jurisdictions for businesses like the Company business in order to determine if there are any significant long-term advantages in relocating or expanding the Company operations to another jurisdiction, whether in whole or in part. Any such review is part of the customary strategic planning of the Company.

As a U.S. incorporated company, we are subject to the Foreign Corrupt Practice Act, or “FCPA,” and other laws that prohibit improper payments or offers of payments to foreign governments and their officials and political parties by U.S. persons and issuers as defined by the statute for the purpose of obtaining or retaining business. Our activities in Asia create the risk of unauthorized payments or offers of payments by consultants or agents of our company, because these parties are not always subject to our control. It is our policy to implement safeguards to discourage these practices by our employees. Also, our existing safeguards and any future improvements may prove to be less than effective, and consultants, sales agents of our Company may engage in conduct for which we might be held responsible. Violations of the FCPA may result in severe criminal or civil sanctions, and we may be subject to other liabilities, which could negatively affect our business, operating results and financial condition. The U.S. government may seek to hold our Company liable for successor liability for any FCPA violations committed by companies in which we invest or that we acquire.

Holding Foreign Companies Accountable Act. (“HFCAA”); PCAOB Vacates Determination regarding Inability to Fully Investigate and Inspect Chinese and Hong Kong Auditors. On December 15, 2022, the Public Company Accounting Oversight Board or “PCAOB” announced it was able to secure complete access to inspect and investigate public audit firms in the China and Hong Kong SAR for the first time. On December 15, 2022, the PCAOB Board voted to vacate previous determinations that it was unable to fully inspect and investigate Chinese and Hong Kong public auditors of companies reporting under the Exchange Act. As originally enacted, the HFCAA required the SEC to initially prohibit trading in the securities of an issuer that is a Commission-identified issuer for three consecutive years. On December 29, 2022, the President signed into law the Consolidated Appropriations Act 2023, which, among other things, amends the HFCAA to reduce this timeframe from three consecutive years to two consecutive years. On December 18, 2022, the SEC announced that due to the December 15, 2022 action by the PCAOB, and until such time as the PCAOB issues any new determination, there are no SEC-reporting companies at risk of having their securities subject to a trading prohibition under the HFCAA. As such, as of the date of this filing of this Form 10-K, the Company is not a Commission Identified Issuer under the HFCAA and is not subject to having its Common Stock delisted under HFCAA.

The following is a discussion of events prior to the SEC December 18, 2022 determination that there were no longer any Commission-identified issuers subject to HFCAA and possible delisting of their equity securities on U.S. public markets.

Prior Developments under HFCAA and Related SEC Rules. As of May 13, 2022, the SEC conclusively identified the Company as a Commission Identified Issuer under the HFCAA and underlying SEC rules. As a result of our identification as a Commission Identified Issuer, our Common would have been delisted from the OTCQB if Company’s current public auditor was not able to be fully audited and inspected by the PCAOB for three consecutive fiscal years (shortened to two years by the Consolidated Appropriations Act 2023), commencing with the fiscal year ended December 31, 2021, and listing and trading in Company our Common Stock would have been prohibited in United States as early as 2024. Our current public auditor was identified by the PCAOB as being an auditor that cannot be fully audited and investigated by the PCAOB due to Chinese government policies. The risks and uncertainty associated with being identified as a Commission Identified Issuer and possible delisting of our Common Stock under the HFCAA could have had a negative impact on investors’ confidence in our Common Stock as an investment and thereby adversely impacted the price of our Common Stock, which adverse impact could have resulted in volatility in trading price of our Common Stock or possibly rendered illiquid an investment in our Common Stock.

| 13 |

Compromise by PCAOB and China on HFCAA. On August 26, 2022, the SEC issued a Statement on Agreement Governing Inspections and Investigations of Audit Firms Based in China and Hong Kong (“August 26, 2022 Compromise”). Under the August 26, 2022 Compromise, the PCAOB, China Securities Regulatory Commission (“CSRC”), and Ministry of Finance of People’s Republic of China established a framework that allowed the PCAOB to inspect and investigate registered public accounting firms in mainland China and Hong Kong. The PCAOB began efforts in the last calendar quarter of 2022 to investigate and audit public auditors in China and Hong Kong in accordance with the August 26, 2022 Compromise and, as discussed above, PCAOB determined that it could fully investigate and audit Chinese and Hong Kong public auditors in December 2022.

Chinese and Hong Kong Business Permits and Regulation. As a general business legal requirement, Company’s Chinese subsidiaries are required to obtain a business license from the State Administration for Market Regulation (“SAMR”). Each of our Chinese subsidiaries has obtained a valid business license from the SAMR, and no application for any such license has been denied. Further, to operate our general business activities currently conducted in China, our relevant Chinese subsidiaries may also be required to obtain other permits from the Chinese government. Company’s Chinese subsidiaries have obtained the necessary permits applicable to them and no application for such permits has been denied by authorities. Our Hong Kong and Philippines subsidiaries likewise have all local government permits to operate their respective businesses. As of the date of the filing of this Form 10-K, the Company and each of its subsidiaries have obtained all licenses and permits required to conduct their respective businesses in all jurisdictions in which those businesses are conducted. Further, except for grants or awards of equity based incentive compensation to Chinese nationals employed by the Company or any of its subsidiaries, which has not occurred as of the date of the filing of this Form 10-K, the Company has all necessary permits and licenses from Chinese and Hong Kong governments to issue securities to foreign investors. Any permits or licenses necessary to operation of the Company and its subsidiaries that are not usual and customary business licenses and permits required of all for-profit businesses in the locality in question are described in this section.

With respect to Chinese and Hong Kong requirements for business or other operational approvals, permits, licenses, or registration requirements necessary to operate our businesses in China and Hong Kong (collectively, “Permits”), the Company and its subsidiaries have not historically been adversely affected by any difficulty, delay or failure to obtain required Permits. However, we cannot predict the effect that the compliance with Chinese and Hong Kong laws and regulations and changes in those laws and regulations may have on our ability to obtain required Permits in the future, especially in light of increasing Chinese government intervention and unilateral modification of Hong Kong laws, regulations and policies.

Based on consultation with Company’s Hong Kong legal counsel as to Chinese and Hong Kong laws, the Company does not believe that: (1) the laws and regulations of China have had an adverse impact on our business, financial condition or results of operations in Hong Kong in fiscal year 2022, (2) that Company has a requirement to obtain any permission or approval from the China Securities Regulatory Commission (“CSRC”), Cyberspace Administration of China (“CAC”) or any other regulatory authority in China for the Company or subsidiary operations for the trading of our common stock or other securities on the OTCQB and the issuance of our securities to foreign investors, except, based on guidance from our Hong Kong legal counsel, that: the Chinese government’s Central State Administration of Foreign Exchange (“SAFE") adopted regulations in 2007 that require the registration with SAFE of any grants of equity based incentive compensation to Chinese nationals employed by a foreign (non-Chinese) company with its securities listed on a foreign exchange or employed by a Chinese subsidiary of such a foreign listed company. Chinese nationals serving as officers and directors are included in the definition of “Chinese employees.” Grants to non-Chinese nationals or a permanent residency permit in another country do not require approval or registration under the 2007 regulations. Under 2012 regulations adopted by SAFE for equity-based grants to Chinese employees by foreign companies with securities listed on foreign exchanges: (1) the scope of registration includes grants or issuances of stock options, stock purchase rights, stock appreciation rights, phantom awards, performance awards, restricted stock (units) and a catch-all "other type of awards” to Chinese employees to be registered with SAFE; and (2) nationals of Hong Kong, Macau and Taiwan working for the foreign company in China may be included, but are not required to be included, in the registration with SAFE. The registration is filed in the SAFE office in the province in which the foreign company’s Chinese subsidiary is located. The main purpose of the 2007 and 2012 regulations is to allow the Chinese government to monitor incentive compensation received by Chinese nationals from foreign companies with securities listed on foreign exchanges. The Company adopted an incentive plan in July 2022, the 2022 Equity Incentive Plan (“Plan”), but has not granted or issued any equity based grants or awards under the Plan. The Company will register any equity-based grants or awards under the Plan to Chinese employees (including officers and directors) prior to approving any such grants or awards. Registration of awards to Chinese employees will also require the Company to file quarterly and annual reports on equity-based awards to Chinese employees with SAFE as well as renew the SAFE registration of the equity based plan on an annual basis.

Based on guidance from Hong Kong legal counsel to the Company, the Company and its operations are not subject to and not impacted by the Chinese cybersecurity-data laws described in this Chinese and Hong Kong Business Permits and Regulation in 2022. The Company and its subsidiaries in China and Hong Kong do not collect the kind of data or act as a data center for information that is the focus of and under the purview of the Chinese national security and cybersecurity laws. Due to the uncertainty of the application or changes in law and regulation in China and Hong Kong, there is no assurance that the Company or its Chinese or Hong Kong operations will not become subject to Chinese cybersecurity-data laws.

| 14 |

The impact of Chinese laws and regulations on the Company and its Hong Kong operations and subsidiaries are subject to the uncertainties created by the Chinese government’s growing intervention and imposition of Chinese laws, regulations and policies, in Hong Kong since 2017 and Chinese government’s willingness to ignore or invalidate conflicting Hong Kong laws, regulations and policies. See following risk factors in Item 1A Risk Factors for potential impact of possible changes in the impact of Chinese laws, regulations and policies on the Company and its Hong Kong and Chinese subsidiaries: We operate primarily in Hong Kong SAR and China are subject to significant political and economic uncertainties if Chinese government significantly alters the laws governing Hong Kong, page 18; Chinese Government or Hong Kong Government may restrict our ability to transfer cash held in or from operations in China or Hong Kong. , at page 18; and Investors may experience difficulties in effecting service of legal process, enforcing foreign judgments or bringing original actions in China or Hong Kong based upon U.S. laws, including the federal securities laws or other foreign laws, against us or our directors and executive officers who reside in China or Hong Kong, at age 18.

Employees

We have more than 300 full time employees as of December 31, 2022, including officers of the Company and including employees and officers of VEI CHN and its subsidiaries. There is no labor dispute affecting our operations and Company believes it has good relationship with its work force. Our employees are not organized into a labor union.

ITEM 1A. RISK FACTORS

An investment in our common stock involves a high degree of risk. Any investor should carefully consider the risks described below, together with all of the other information included in this Form 10-K, before making an investment decision. If any of the following risks actually occurs, our business, financial condition or results of operations could suffer or be undermined. In that case, the trading price of our common stock could decline, and any investor may lose all or part of the investor’s investment. You should read the section entitled “Special Note Regarding Forward-Looking Statements” above for a discussion of what types of statements are forward-looking statements, as well as the significance of such statements in the context of this Form 10-K.

Risks Related to Our Business

A substantial amount of our sales revenue is derived from sales to a limited number of customers, and our business will suffer if sales to these customers decline. We have derived a significant portion of our revenue from a limited number of customers. For the year ended December 31, 2022, our revenue was concentrated in our largest customer that accounted for approximately 22.3% of annual revenues. As of December 31, 2022, $46,788 or 4.1% of our accounts receivable, was due from our largest customer. We do not have long term contractual arrangements or regular negotiation with most of these customers. The loss of one or more of these customers could damage our business, financial condition and results of operations. We are endeavoring but may not succeed expanding our customer base in order to reduce reliance on major customers. We do not conduct business in U.S.A. or European Union, which are major markets for IT Business. As a smaller IT Business, the loss of a single significant customer can have significant, adverse impact on our business and financial conditions, especially since we lack the resources to aggressively, effectively compete for new clients against larger competitors.

Impact of Coronavirus/COVID-19. By late December 2019, China advised the World Health Organization (“WHO”) of a new strain of the coronavirus had arisen in Wuhan, China and spread throughout China. From China, Coronavirus/COVID-19 (“COVID 19”) has spread by March 2020 to almost all other parts of the developed world, including Hong Kong SAR, the Philippines and the United States. On January 30, 2020, WHO declared the outbreak of COVID-19 a “Public Health Emergency of International Concern,” and then, on March 11, 2020, declared the COVID-19 outbreak as a “pandemic”.

As of the date of the filing of this Form 10-K, our operations are located primarily in Hong Kong with other operations in China and Philippines. Spikes in COVID 19 new case infections continued from time to time in Hong Kong and in parts of China in 2022. While new COVID 19 cases in Hong Kong have dropped to no new reported cases in February 2023 (according to Hong Kong government) and Hong Kong has eased some COVID 19 restrictions in February and March 2023, and Hong Kong has a high first and second doses of COVID 19 vaccination rates (above 90% of adults), and China has ramped up efforts to get older citizens vaccinated in 2023 (according to World Health Organization), the ability of COVID 19 to rapidly develop new variants with differing vulnerability to existing vaccinations makes COVID 19 an ongoing risk to disrupt our business operations, especially in terms of in-person direct sales and marketing efforts to increase or sustain business with customers and win new customers. Due to the unpredictability of COVID 19 mutations, it is uncertain what the full lasting and long term impact of COVID-19 on the future business of the Company and the impact on the demand for IT services in the Company’s key markets of Hong Kong, China and Philippines. As of the date of the filing of this Form 10-K, the adverse impact on usual and customary business development efforts are generally easing in Hong Kong. The Company has not experienced significant disruptions in operations in 2022 from COVID 19 pandemic, which has mostly impacted efforts to meet and pitch existing customers and new prospective customers about using our services or products.

| 15 |

While we have not experienced a significant loss of personnel from COVID 19 pandemic as of the date of the filing of this Form 10-K, this pandemic, which may impact areas in waves and not in a single occurrence, or may mutate into a vaccine resistant strain, may cause a shortage of qualified personnel. Adequacy of qualified staffing is key to maintenance and growth of our IT Business and our IT Business is key to our financial condition and performance. While performing work by staffs in parts of the world outside of our key markets is a possible solution to any shortages of qualified staff in our key markets, we have not yet developed a contingency plan for remote personnel support of our IT Business or devoted resources to that endeavor. We have no significant experience in using personnel outside of our current market regions.

Our success depends on certain key personnel. We rely on highly skilled and qualified personnel, and if we are unable to continue to attract and retain such qualified personnel it will adversely affect our business. Our performance to date has been and will continue to be largely dependent on the talents, efforts and performance of our senior management and key technical personnel, who generally have, in our opinion, significant experience with our company and substantial relationships and reputations within the industry of our services. Certain of our executive officers and top technical personnel may enter into employment and noncompetition agreements. However, while it is customary in the industry to use employment agreements as a method of retaining the services of key executive personnel, these agreements do not guarantee us the continued services of such employees. We do not currently have an employment agreement with our key personnel, or with most of our key technical and engineering personnel. The loss of our executive officers or our other key personnel, particularly with little or no notice, could cause delays on business developments and projects and could have an adverse impact on our customers and industry relationships, our business, operating results or financial condition. While we may rely on independent contractors or consultants for technical needs, we may also experience an inability to hire such expertise in the future. The job market for experienced IT personnel is competitive in PRC and Hong Kong, our primary markets, as well as globally. We also lack the resources or funding to match more established competitors’ compensation packages for the kind of personnel that is critical to our company’s survival and success.

Our success depends to a significant extent on our ability to identify, attract, hire, train and retain qualified creative, technical and managerial personnel or to contract with such personnel as independent contractors. We expect competition for personnel with the specialized technical skills needed to create our products and provide our services will continue to intensify in our business because commerce’s reliance on technology increases in order to meet the competitive need for operational efficiencies and related automation and connectivity. We plan to hire individuals on a project-by-project basis, and individuals who work on one or more projects for us may not be available to work on future projects. If we have difficulty identifying, attracting, hiring, training and retaining such qualified personnel, or incur significant costs in order to do so, our business and financial results could be negatively impacted.

The Company has not developed a succession plan for key personnel and does not have key man life insurance. While VEII has adopted the Plan for incentive compensation, it has not issued any incentive compensation as of the date of the filing of this Form 10-K. The Company will evaluate issuance of incentive compensation in 2023.

Our successful pursuit of profitable business faces various risks and challenges, including:

| * | A lessening of the impact of spikes in infections in the COVID 19 pandemic in China, Hong Kong and Philippines economies and mitigation of any possible loss of or shortage of qualified personnel due to illness from COVID-19 is a key factor; |

| * | the success of our business will be primarily dependent on customer acceptance of our services and products, which is extremely difficult to predict, and our ability to obtain affordable, adequate funding to support efforts to promote our services and products and fund any expansion of business. As a microcap with a lightly traded stock, we have to rely on private placements of stock or debt funding to acquire working capital for expansion of business. While we have obtained two credit lines, there is no assurance that these credit lines will adequately or timely fund any urgent need to develop and sustain new services or products; |

| * | achieving sustainable operating revenues in our core IT Business that is sufficient to support our business without equity or debt funding; |

| * | the business can be capital-intensive in terms of labor costs and our capacity to generate cash from our operations may be insufficient to meet our anticipated capital requirements, especially the capital needs of penetrating new markets and developing our services to meet customer demands; |

| * | technological developments could render obsolete our technologies, services and products and undermine our services and products in the industry and we may be unable to license or acquire the new technologies, services and products; |

| * | the need to access expertise and technical resources in each market in which we may operate presents high capital costs that may be beyond our ability to fund – as such, we may be unable to bid for highly profitable, but high labor cost, projects or contract opportunities, which inability can limit our growth and profitability potential; |

| * | we may be unable to compete for or afford key personnel in our industry that pays a premium for talent, especially since our common stock has a limited market price and limited liquidity; |

| 16 |

| * | a shortage of qualified personnel, could delay or halt our business operations; |

| * | technologies and customer tastes and demands can shift or change unexpectedly in the rapidly evolving IT industry and we may lack the wherewithal to respond to such changes; and |

| * | acquisitions we pursue in our industry and related industries could result in operating difficulties, dilution to our shareholders and other consequences harmful to our business. Integration of new acquisitions can undermine an acquiring company’s business strengths by diluting resources and manpower and imposing operational losses. |

As part of our growth strategy, and if we attain adequate funding as well as stability and profitability in our core business, we may selectively pursue strategic acquisitions in our industry and related industries. We may not be able to consummate such acquisitions, or efficiently integrate new businesses into our existing business, which could adversely impact our growth. The “penny stock” status of our common stock does not allow our company readily access public capital markets for funding. If we do consummate acquisitions, integrating an acquired company, business or technology may result in unforeseen operating difficulties and expenditures, including:

| * | increased expenses due to transaction and integration costs; |

| * | potential liabilities of the acquired businesses; |

| * | potential adverse tax and accounting effects of the acquisitions; |

| * | diversion of capital and other resources from our existing business; |

| * | diversion of our management’s attention during the acquisition process and any transition periods; |

| * | loss of key employees and key customers of the acquired businesses following the acquisition or inability of existing management to manage newly acquired businesses; and |

| * | inaccurate budgets and projected financial statements due to inaccurate valuation assessments of the acquired businesses. |

There can be no assurance that we can successfully achieve any or all of the above initiatives in the manner or time period that we expect. Furthermore, achieving these objectives will require investments which may result in short-term costs without generating any current revenues and therefore may be dilutive to our earnings. We cannot provide any assurance that we will realize, in full or in part, the anticipated benefits we expect our strategy will achieve. The failure to realize those benefits could have a material adverse effect on our business, financial condition and results of operations.

We may need additional and ongoing financing to fund our operations or to acquire or start new operations or business lines, which financing we may not be able to obtain on acceptable terms or at all, especially as a microcap, smaller company. Additional capital raising efforts in future periods will be dilutive to our then current stockholders or result in increased interest expense and debt load in future periods. We have been able to obtain credit lines in July 2022 of $1 million and in January 2023 of $1.5 million for operating costs, including possible expansion of business operations. Nonetheless, we may need to raise additional and ongoing capital to fund our plans to invest in current business development, sustain current operations or marketing initiatives and possible future acquisition of the operating assets. Due to the “penny stock” status of our Common Stock and lack of tangible assets required for traditional debt financing, we may be limited in our ability to obtain additional debt or obtain equity funding to meet operating costs or expansion of our operations in existing or new markets. Our future capital requirements depend on a number of factors, including our ability to manage any growth of our business and our ability to control our expenses while maximizing profits. Also, if we raise additional capital through the issuance of debt, this will result in increased interest expense. If we raise additional capital through the issuance of equity or convertible debt securities, the percentage ownership of our company held by existing public shareholders will be reduced and those shareholders will probably experience significant dilution due to the “penny stock” status of our Common Stock.

New securities issued by us may contain certain rights, preferences or privileges that are senior to those of our Common Stock or other securities. Such seniority may adversely impact the rights and any possible financial return for our holders of the VEII Common Stock. We cannot assure investors that we will be able to raise the working capital as needed in the future on terms acceptable to us, if at all. If we do not raise capital as needed, we will be unable to operate our business or fully implement our business development and acquisition expansion strategy.

| 17 |

We may not be able to adequately finance the significant costs associated with the development, licensing or purchase of new product lines and new services. While we have been able to secure a credit line for $1.5 million for operating costs in February 2023 and a credit line for $1 million in July 2022, any technology business is subject to a demand to have the newest product and services to match changes in technology and customer purchasing habits. This technological cycle will require us to develop, license or purchase new products and develop or license new technologies to match changes in the technologies used by or preferred by our customers. The cost of keeping pace on technologies, products and services required by our customers may exceed our ability to fund from cash from operations and credit lines the development, purchase or licensing of those technologies, products and services. We do not possess the internal research and development capabilities and resources of many of our competitors, especially the larger ones.

We could be required to expend substantial funds for and commit significant resources to the following:

| · | training our personnel on new products and services; |

| · | purchasing, licensing or developing new products for resell or new services; |

| · | marketing and promotional costs for new products and services; and |

our future operating results will depend to a significant extent on our ability to continue to provide new and competitive products and services that compare favorably on the basis of cost and performance with the design and manufacturing capabilities of competitive third-party technologies. We will need to sufficiently increase our net sales to offset these increased costs, the failure of which would negatively affect our operating results.

Operational and Legal Risks Associated with being a U.S. Public Company with Chinese-Based and Hong Kong-Based Operations

We operate primarily in Hong Kong SAR and China are subject to significant political and economic uncertainties if Chinese government significantly alters the laws governing Hong Kong.

The Chinese government may exercise significant oversight and discretion over the conduct of Company and Company’s operating subsidiaries in China as well as in Hong Kong (despite Hong Kong being a separate system from mainland China) and may intervene in or influence our operations and our status as a U.S. public holding company at any time. These Chinese governmental actions:

| 1) | could disallow our corporate structure as a U.S .public holding company in Hong Kong or our ownership of Chinese subsidiaries; |

| 2) | could result in a material change in our operations, including, without limitation, reincorporation of companies, transfers of operations or assets to other jurisdictions, cessations of operations, bankruptcy, insolvency, liquidation, changes in business lines, efforts to list or continue to trade our securities on non-U.S. securities exchanges and going private transactions – each of these transactions could render worthless or illiquid or nominal in value any investment in the Company; |

| 3) | could hinder our ability to continue to offer securities to investors outside of China and Hong Kong or list our securities on any U.S. national securities exchange or OTCQB; and |

| 4) | may cause the value of our securities to significantly decline or become illiquid investment or completely worthless. |

Significant changes in PRC laws and regulations, or their interpretation, or the imposition of confiscatory taxation, restrictions on currency conversion, imports and sources of supply, devaluations of currency or the nationalization or other expropriation of private enterprises could have a material adverse effect on our business, results of operations and financial condition. Under its current leadership, the Chinese government has generally been pursuing economic reform policies that encourage private economic activity and greater economic decentralization. There is no assurance, however, that the Chinese government will continue to pursue these policies, or that it will not significantly alter these policies from time to time without notice and in respect of Hong Kong SAR.

Chinese Government or Hong Kong Government may restrict our ability to transfer cash held in or from operations in China or Hong Kong. To the extent cash in the Company’s or its subsidiaries’ business is held in China or Hong Kong, or held by a Chinese or Hong Kong entity, those funds may not be available to fund operations of the Company or its subsidiaries or for other uses outside of China or Hong Kong due to interventions in or the imposition of restrictions and limitations on the ability of the Company or its subsidiaries by the Chinese government to transfer cash. There can be no assurance the Chinese government will not intervene in or impose restrictions on the ability of the Company or its subsidiaries to transfer cash outside of China or Hong Kong.