UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16 UNDER

THE SECURITIES EXCHANGE ACT OF 1934

For the month of September 2013

Commission File Number: 001-34477

AUTOCHINA INTERNATIONAL LIMITED

(Translation of registrant’s name into English)

27/F, Kai Yuan Center, No. 5, East Main Street Shijiazhuang, Hebei

People’s Republic of China

(Address of Principal Executive Offices)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

Form 20-F x Form 40-F ¨

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1): ¨

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7): ¨

Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes ¨ No x

If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): 82-_______________.

THIS REPORT ON FORM 6-K SHALL BE DEEMED TO BE INCORPORATED BY REFERENCE IN THE REGISTRATION STATEMENT ON FORM S-8 (FILE NO. 333-170786) OF AUTOCHINA INTERNATIONAL LIMITED AND TO BE A PART THEREOF FROM THE DATE ON WHICH THIS REPORT IS FURNISHED, TO THE EXTENT NOT SUPERSEDED BY DOCUMENTS OR REPORTS SUBSEQUENTLY FILED OR FURNISHED.

FORWARD-LOOKING STATEMENTS

This Report of Foreign Private Issuer on Form 6-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, and Section 21E of the Securities Exchange Act of 1934. These statements relate to future events or the future financial performance of AutoChina International Limited (the “Company”). The Company has attempted to identify forward-looking statements by terminology including “anticipates”, “believes”, “expects”, “can”, “continue”, “could”, “estimates”, “intends”, “may”, “plans”, “potential”, “predict”, “should” or “will” or the negative of these terms or other comparable terminology. These statements are only predictions, uncertainties and other factors may cause the Company’s actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements. The information in this Report on Form 6-K is not intended to project future performance of the Company. Although the Company believes that the expectations reflected in the forward-looking statements are reasonable, the Company does not guarantee future results, levels of activity, performance or achievements. The Company’s expectations are as of the date this Form 6-K is filed, and the Company does not intend to update any of the forward-looking statements after the date this Report on Form 6-K is filed to confirm these statements to actual results, unless required by law.

The forward-looking statements included in this Form 6-K are subject to risks, uncertainties and assumptions about our businesses and business environments. These statements reflect our current views with respect to future events and are not a guarantee of future performance. Actual results of our operations may differ materially from information contained in the forward-looking statements as a result of risk factors some of which include, among other things: continued compliance with government regulations; changing legislation or regulatory environments; requirements or changes affecting the businesses in which the Company is engaged; industry trends, including factors affecting supply and demand; labor and personnel relations; credit risks affecting the Company's revenue and profitability; changes in the commercial vehicle industry; the Company’s ability to effectively manage its growth, including implementing effective controls and procedures and attracting and retaining key management and personnel; changing interpretations of generally accepted accounting principles; general economic conditions; and other relevant risks detailed in the Company’s filings with the Securities and Exchange Commission.

This report is hereby incorporated by reference to the Post-Effective Amendment to the Registration Statement on Form S-8 (File No. 333-170786) of the Company.

Results of Operations and Financial Condition.

Following this page are the unaudited condensed consolidated financial statements as of June 30, 2013 and December 31, 2012 and the financial results for the three and six month periods ended June 30, 2013 and 2012 of the Company.

| 2 |

AUTOCHINA INTERNATIONAL LIMITED AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

(in thousands except share and per share data)

| June 30, | December 31, | |||||||

| 2013 | 2012 | |||||||

| (unaudited) | ||||||||

| ASSETS | ||||||||

| Current assets | ||||||||

| Cash and cash equivalents | $ | 65,356 | $ | 75,777 | ||||

| Restricted cash | 973 | 160 | ||||||

| Accounts receivable, net of provision for doubtful debts of $16,409 and $12,041 respectively | 34,509 | 32,956 | ||||||

| Inventories | 6,350 | 6,728 | ||||||

| Deposits for inventories | 265 | 20 | ||||||

| Prepaid expenses and other current assets | 11,291 | 4,512 | ||||||

| Current maturities of net investment in direct financing and sales-type leases, net of provision for doubtful debts of $249 and $296, respectively | 179,601 | 196,213 | ||||||

| Deferred income tax assets | 1,863 | — | ||||||

| Total current assets | 300,208 | 316,366 | ||||||

| Construction in progress | — | 76,669 | ||||||

| Property, equipment and leasehold improvements, net | 82,831 | 4,985 | ||||||

| Deferred income tax assets | 3,757 | 2,547 | ||||||

| Net investment in direct financing and sales-type leases, net of current maturities | 69,272 | 38,739 | ||||||

| Total assets | $ | 456,068 | $ | 439,306 | ||||

| LIABILITIES AND SHAREHOLDERS’ EQUITY | ||||||||

| Current liabilities | ||||||||

| Short-term borrowings (including short-term borrowings of the consolidated variable interest entities (“VIEs”) without recourse to AutoChina of $89,015 and $75,412 as of June 30, 2013 and December 31, 2012, respectively) | $ | 116,529 | $ | 102,458 | ||||

| Long-term payables, current portion (including long-term borrowings, current of the consolidated VIEs without recourse to AutoChina of nil and nil as of June 30, 2013 and December 31, 2012, respectively) | 644 | — | ||||||

| Accounts payable (including accounts payable of the consolidated VIEs without recourse to AutoChina of $1,097 and $68 as of June 30, 2013 and December 31, 2012, respectively) | 9,860 | 16,392 | ||||||

| Accounts payable, related parties (including accounts payable of the consolidated VIEs without recourse to AutoChina of $4,397 and $706 as of June 30, 2013 and December 31, 2012, respectively) | 6,057 | 2,228 | ||||||

| Other payables and accrued liabilities (including other payables and accrued liabilities of the consolidated VIEs without recourse to AutoChina of $8,122 and $4,857 as of June 30, 2013 and December 31, 2012, respectively) | 18,589 | 15,049 | ||||||

| Due to affiliates (including due to affiliates of the consolidated VIEs without recourse to AutoChina of $131 and $86 as of June 30, 2013 and December 31, 2012, respectively) | 53,732 | 65,595 | ||||||

| Customer deposits (including customer deposits of the consolidated VIEs without recourse to AutoChina of $537 and $161 as of June 30, 2013 and December 31, 2012, respectively) | 2,854 | 1,956 | ||||||

| Income tax payable (including income tax payable of the consolidated VIEs without recourse to AutoChina of $4,495 and $1,931 as of June 30, 2013 and December 31, 2012, respectively) | 7,011 | 2,551 | ||||||

| Deferred income tax liabilities (including deferred income tax liabilities of the consolidated VIEs without recourse to AutoChina of nil and nil as of June 30, 2013 and December 31, 2012, respectively) | — | 4,717 | ||||||

| Total current liabilities | 215,276 | 210,946 | ||||||

| Noncurrent liabilities | ||||||||

| Long-term payables (including long-term borrowings of the consolidated VIEs without recourse to AutoChina of nil and nil as of June 30, 2013 and December 31, 2012, respectively) | 707 | — | ||||||

| Total liabilities | 215,983 | 210,946 | ||||||

| 3 |

AUTOCHINA INTERNATIONAL LIMITED AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS - Continued

(in thousands except share and per share data)

| June 30, | December 31, | |||||||

| 2013 | 2012 | |||||||

| (unaudited) | ||||||||

| Commitment and Contingency | ||||||||

| Shareholders’ equity | ||||||||

| Preferred shares, $0.001 par value authorized - 1,000,000 shares; issued - none | — | — | ||||||

| Ordinary shares - $0.001 par value authorized - 100,000,000 shares; issued and outstanding – 23,538,919 shares at June 30, 2013 and December 31, 2012, respectively | 24 | 24 | ||||||

| Additional paid-in capital | 325,798 | 323,856 | ||||||

| Statutory reserves | 16,997 | 16,997 | ||||||

| Accumulated losses | (130,714 | ) | (135,487 | ) | ||||

| Accumulated other comprehensive income | 27,980 | 22,970 | ||||||

| Total shareholders’ equity | 240,085 | 228,360 | ||||||

| Total liabilities and shareholders’ equity | $ | 456,068 | $ | 439,306 | ||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

| 4 |

AUTOCHINA INTERNATIONAL LIMITED AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENT OF INCOME AND COMPREHENSIVE INCOME (Unaudited)

(in thousands except share and per share data)

| Three months ended June 30, | Six months ended June 30, | |||||||||||||||

| 2013 | 2012 | 2013 | 2012 | |||||||||||||

| As Adjusted – Note 2 | As Adjusted – Note 2 | |||||||||||||||

| Revenues | ||||||||||||||||

| Commercial vehicles | $ | 156,567 | $ | 81,293 | $ | 213,674 | $ | 161,736 | ||||||||

| Finance | 10,279 | 19,546 | 20,780 | 40,278 | ||||||||||||

| Insurance | 5,258 | 3,982 | 9,005 | 5,875 | ||||||||||||

| Total revenues | 172,104 | 104,821 | 243,459 | 207,889 | ||||||||||||

| Cost of sales | ||||||||||||||||

| Commercial vehicles | 2,966 | 1,827 | 4,457 | 4,574 | ||||||||||||

| Commercial vehicles, related parties | 150,239 | 77,182 | 204,956 | 152,979 | ||||||||||||

| Insurance | 871 | 470 | 1,678 | 470 | ||||||||||||

| Total cost of sales | 154,076 | 79,479 | 211,091 | 158,023 | ||||||||||||

| Gross profit | 18,028 | 25,342 | 32,368 | 49,866 | ||||||||||||

| Operating (income) expenses | ||||||||||||||||

| Selling and marketing | 2,618 | 2,727 | 4,821 | 4,851 | ||||||||||||

| General and administrative | 11,468 | 8,815 | 23,244 | 16,945 | ||||||||||||

| Interest expense | 1,789 | 2,976 | 3,449 | 6,771 | ||||||||||||

| Interest expense, related parties | 196 | 230 | 377 | 511 | ||||||||||||

| Other income, net | (4,227 | ) | (322 | ) | (6,640 | ) | (890 | ) | ||||||||

| Total operating expenses | 11,844 | 14,426 | 25,251 | 28,188 | ||||||||||||

| Income from operations | 6,184 | 10,916 | 7,117 | 21,677 | ||||||||||||

| Other income | ||||||||||||||||

| Interest income | 135 | 117 | 227 | 152 | ||||||||||||

| Other income | 135 | 117 | 227 | 152 | ||||||||||||

| Income before income taxes | 6,319 | 11,033 | 7,344 | 21,829 | ||||||||||||

| Income tax provision | 1,959 | 2,635 | 2,571 | 5,403 | ||||||||||||

| Net income | 4,360 | 8,398 | 4,773 | 16,426 | ||||||||||||

| Foreign currency translation adjustment | 4,182 | (1,552 | ) | 5,010 | (1,360 | ) | ||||||||||

| Comprehensive income | $ | 8,542 | $ | 6,846 | $ | 9,783 | $ | 15,067 | ||||||||

| 5 |

AUTOCHINA INTERNATIONAL LIMITED AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENT OF INCOME AND COMPREHENSIVE INCOME (Unaudited) - Continued

(in thousands except share and per share data)

| Three months ended June 30, | Six months ended June 30, | |||||||||||||||

| 2013 | 2012 | 2013 | 2012 | |||||||||||||

| As Adjusted – Note 2 | As Adjusted – Note 2 | |||||||||||||||

| Earnings per share | ||||||||||||||||

| Basic | $ | 0.19 | $ | 0.36 | $ | 0.20 | $ | 0.70 | ||||||||

| Diluted | $ | 0.18 | $ | 0.36 | $ | 0.20 | $ | 0.70 | ||||||||

| Dividend declared per share | $ | — | $ | — | $ | — | $ | 0.25 | ||||||||

| Weighted average shares outstanding | ||||||||||||||||

| Basic | 23,538,919 | 23,538,919 | 23,538,919 | 23,538,919 | ||||||||||||

| Diluted | 23,687,491 | 23,561,344 | 23,777,275 | 23,613,692 | ||||||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

| 6 |

AUTOCHINA INTERNATIONAL LIMITED AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (Unaudited)

(in thousands)

| Six Months Ended June 30, | ||||||||

| 2013 | 2012 | |||||||

| As Adjusted – note 2 | ||||||||

| Net cash provided by (used in) operating activities | $ | (14,977 | ) | $ | 136,433 | |||

| Cash flow from investing activities: | ||||||||

| Capital expenditure on construction in progress | — | (74,111 | ) | |||||

| Purchase of property, equipment and leasehold improvements | (1,095 | ) | (1,689 | ) | ||||

| Repayment (borrowing) of due from an affiliate | — | 7,903 | ||||||

| Net cash used in investing activities | (1,095 | ) | (67,897 | ) | ||||

| Cash flow from financing activities: | ||||||||

| Proceeds from borrowings | 57,363 | 29,185 | ||||||

| Repayments of borrowings | (43,877 | ) | (102,315 | ) | ||||

| Proceeds from affiliates for debt | 7,651 | 113,419 | ||||||

| Repayment to affiliates | (19,843 | ) | (73,480 | ) | ||||

| Increase in accounts payable, related parties | 204,956 | 152,979 | ||||||

| Repayment to accounts payable, related parties | (201,207 | ) | (136,116 | ) | ||||

| Dividend paid | — | (5,885 | ) | |||||

| Capital distribution | — | (29,358 | ) | |||||

| Net cash provided by used in financing activities | 5,043 | (51, 571) | ||||||

| Net cash provided by (used in) operating, investing and financing activities | (11,029 | ) | 16,965 | |||||

| Effect of foreign currency translation on cash and cash equivalents | 608 | (213 | ) | |||||

| Net increase (decrease) in cash and cash equivalents | (10,421 | ) | 16,752 | |||||

| Cash and cash equivalents, beginning of the period | 75,777 | 43,048 | ||||||

| Cash and cash equivalents, end of the period | $ | 65,356 | $ | 59,800 | ||||

| Supplemental disclosure of cash flow information: | ||||||||

| Interest paid | $ | 3,589 | $ | 10,894 | ||||

| Income taxes paid | $ | 5,855 | $ | 4,930 | ||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

| 7 |

AUTOCHINA INTERNATIONAL LIMITED AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

Six Months Ended June 30, 2013 and 2012

(in thousands except share and per share data)

NOTE 1 – BACKGROUND

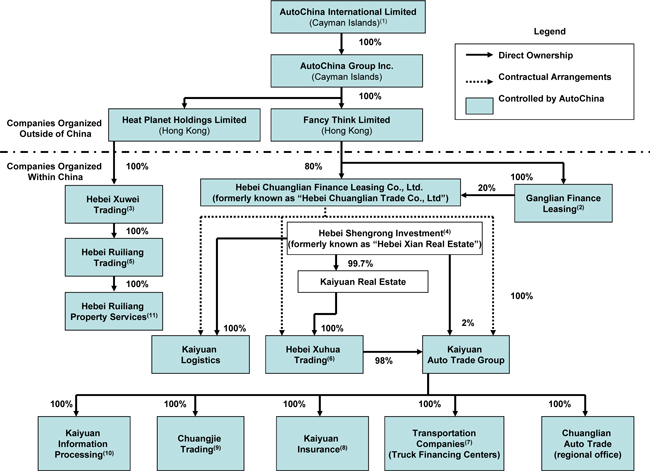

AutoChina International Limited (the “Company” or “AutoChina”) is a holding company whose only business operations are conducted through its wholly owned subsidiary, AutoChina Group Inc. (“ACG”). ACG’s operations primarily consist of the commercial vehicle sales, servicing, leasing and support business, which provides financing to customers to purchase commercial vehicles and related services. In April 2013, the Company commenced office leasing business in China.

The Company owns a store branch network in different regions of China to provide commercial vehicle sales and services which include leasing services, general support services, licensing and permit services, insurance services and registration services, to its lessee. As of June 3, 2013, the Company had 535 stores in 26 provinces or provincial-level regions.

The Company launched its own insurance agency business in December 2011 and has signed agreements with various major insurance companies in China to sell insurance. AutoChina’s 535 store locations are each licensed to sell insurance from these carrier partners.

On August 30, 2012, the Company’s independent directors approved, and the Company entered into, an equity transfer agreement through its wholly owned subsidiary, ACG, to purchase 100% of the equity of Heat Planet Holdings Limited (“Heat Planet”) and its subsidiaries, whose primary asset consists of 23 floors, or over 60,000 square meters, of newly constructed office space in the Kai Yuan Center building (the “Real Estate Asset”). Heat Planet was controlled by the Company’s Chairman and Chief Executive Officer, Mr. Yong Hui Li. The total transaction value of approximately RMB1 billion ($159.3 million) was negotiated and approved by the Company’s Audit Committee and equals the appraisal value that was determined by a third party appraisal of the Real Estate Asset. Located at 5 East Main Street in Shijiazhuang, where the Company is currently based, the 245-meter tall Kai Yuan Center is the tallest building in Shijiazhuang and Hebei Province and will also be occupied by a Hilton Worldwide-operated, five-star hotel. The acquisition closed on September 11, 2012, and on October 12, 2012, the Company entered into a written consent with Heat Planet and its seller to modify the required timeframe to provide audited financial statements of Heat Planet to be delivered to the Company. The required audited financial statements of Heat Planet were delivered to the Company on December 26, 2012.The building was completed in April 2013, and AutoChina moved its headquarters to the new Kai Yuan Center, which serves as the control center for each of the Company’s 535 commercial vehicle financial centers located throughout China. The Company does not anticipate that it will occupy the entire office space purchased, and has commenced leasing out the unoccupied space, the proceeds from which will be reported as rental income.

Heat Planet’s equity was purchased for approximately $56.4 million. In connection with the acquisition, the Company assumed approximately $102.9 million in debt, resulting in a total transaction value of approximately $159.3 million. The $56.4 million purchase price is payable within six months of occupation of the Real Estate Asset, and any unpaid amounts after such six months will begin to accrue interest at the one-year rate announced by the People’s Bank of China (6.00% as of June 30, 2013).

In January 2013, the Company agreed to amend the contractual arrangements (the “Enterprise Agreements”) with its variable interest entities (“VIEs”), Kaiyuan Auto Trade Co., Ltd. (“Kaiyuan Auto Trade”) and Hebei Shijie Kaiyuan Logistics Co., Ltd. (“Kaiyuan Logistics”) and their registered shareholder, Hebei Kaiyuan Real Estate Development Co., Ltd. (“Hebei Kaiyuan”). Under the amendment to the Enterprise Agreements, Hebei Kaiyuan transferred its entire equity interest held in Kaiyuan Auto Trade (2%) and Kaiyuan Logistics (100%) to its parent company, Hebei Shengrong Investment Co., Ltd. (“Hebei Shengrong Investment”). Thereafter, Hebei Shengrong Investment became the registered shareholder of these two VIEs. Except for authorizing such transfer, the rights and obligations of the Company and the VIEs in the Enterprise Agreements remain unchanged. The amendment of the Enterprise Agreements does not have any financial impact to the Company’s financial positions and operating results.

In March 2013, the Company performed a group restructuring to transfer the entire equity interest of its subsidiary, Hebei Chuangjie Trading Co., Ltd. (“Chuangjie Trading”) from Ganglian Finance Leasing Co., Ltd. (“Ganglian Finance Leasing”) to Kaiyuan Auto Trade. The change resulted in Chuangjie Trading becoming a VIE of the Company. In addition, Fancy Think Limited transferred a 10% interest in Hebei Chuanglian Finance Leasing Co., Ltd. to Ganglian Finance Leasing. Accordingly, Fancy Think Limited and Ganglian Finance Leasing hold 80% and 20% interest of Chuanglian, respectively. The change in group structure does not have any financial impact to the Company’s financial position or operating results.

In March 2013, Ganglian Finance Leasing entered into a mortgage financing arrangement with China CITIC Bank, Shijiazhuang, Hebei Province Branch (“CITIC Bank”), whereby CITIC Bank agreed to provide up to 50% of the mortgage financing to Ganglian Finance Leasing’s lessees of commercial vehicles. Ganglian Finance Leasing agreed to provide a full guarantee to CITIC Bank for such mortgage financing and will provide a pledge of the ownership of the commercial vehicle to CITIC Bank to secure its guarantees.

In May 2013 Kaiyuan Auto Trade Co., Ltd. (“Kaiyuan Auto Trade”) changed its name to Kaiyuan Auto Trade Group Co., Ltd. (“Kaiyuan Auto Trade Group”). In June 2013 we established a new wholly-owned subsidiary called Hebei Ruiliang Property Services.

| 8 |

The following financial statement amounts and balances of the VIEs were included in the accompanying condensed consolidated financial statements as of June 30, 2013 and December 31, 2012 and for the six months ended June 30, 2013 and 2012:

| June 30, | December 31, | |||||||

| 2013 | 2012 | |||||||

| (unaudited) | ||||||||

| Total assets | $ | 297,377 | $ | 237,875 | ||||

| Total liabilities | 107,794 | 83,221 | ||||||

| Six months ended June 30, | ||||||||

| 2013 | 2012 | |||||||

| (unaudited) | (unaudited) | |||||||

| Revenues | $ | 16,501 | $ | 8,546 | ||||

| Net (loss) income | (6,647 | ) | 706 | |||||

NOTE 2 –ADJUSTMENT OF PREVIOUSLY ISSUED CONSOLIDATED FINANCIAL STATEMENTS

On September 11, 2012, the Company acquired 100% of the equity of Heat Planet and its subsidiaries from Alliance Rich Management Limited (“Alliance Rich”) through its wholly-owned subsidiary, ACG, for total consideration of approximately $159.3 million (see Note 1). On the same date, Mr. Li owned 65.9% and 100% equity of the Company and Alliance Rich, respectively. As both the Company and the acquired companies are under the common control of Mr. Li immediately before and after the acquisition, this transaction was accounted for as a merger under common control, using merger accounting as if the merger had been consummated at the beginning of the earliest period presented, and no gain or loss is recognized. All the assets and liabilities of Heat Planet and its subsidiaries are recorded at carrying value. The cash consideration in excess of carrying value of net assets of Heat Planet’s subsidiary was deemed a capital distribution to Mr. Li and a deduction to additional paid in capital amounting to $85,442 was recorded upon consummation of acquisition.

The Company has adjusted its financial statements for the six months ended June 30, 2012 to account for operating results and cash flows of Heat Planet and its subsidiaries to reflect the merger under common control.

Selected consolidated statement of income information for the six months ended June 30, 2012:

| Six months ended June 30, 2012 (as previously reported) | Effect of Adjustment | Six months ended June 30, 2012 (As Adjusted) | ||||||||||

| (unaudited) | (unaudited) | (unaudited) | ||||||||||

| General and administrative | $ | 16,896 | $ | 50 | $ | 16,946 | ||||||

| Income from operations | 21,727 | (50 | ) | 21,677 | ||||||||

| Interest income | 149 | 3 | 152 | |||||||||

| Income before income taxes | 21,876 | (47 | ) | 21,829 | ||||||||

| Net income | $ | 16,473 | $ | (47 | ) | $ | 16,426 | |||||

Selected consolidated statement of income information for the three months ended June 30, 2012:

| Three months ended June 30, 2012 (as previously reported) | Effect of Adjustment | Three months ended June 30, 2012 (As Adjusted) | ||||||||||

| (unaudited) | (unaudited) | (unaudited) | ||||||||||

| General and administrative | $ | 8,776 | $ | 39 | $ | 8,815 | ||||||

| Income from operations | 10,955 | (39 | ) | 10,916 | ||||||||

| Interest income | 117 | 0 | 117 | |||||||||

| Income before income taxes | 11,072 | (39 | ) | 11,033 | ||||||||

| Net income | $ | 8,437 | $ | (39 | ) | $ | 8,398 | |||||

| 9 |

Selected consolidated statement of cash flow information for the six months ended June 30, 2012:

| Six months ended June 30, 2012 (as previously reported) | Effect of Adjustment | Six months ended June 30, 2012 (As Adjusted) | ||||||||||

| (unaudited) | (unaudited) | (unaudited) | ||||||||||

| Net cash provided by operating activities | $ | 111,877 | $ | 24,556 | $ | 136,433 | ||||||

| Net cash (used in) investing activities | (1,689 | ) | (66,208 | ) | (67,897 | ) | ||||||

| Net cash (used in) provided by financing activities | (93,305 | ) | 41,734 | (51,571 | ) | |||||||

| Effect of foreign currency translation on cash | (185 | ) | (28 | ) | (213 | ) | ||||||

| Net increase in cash and cash equivalents | 16,698 | 54 | 16,752 | |||||||||

| Cash and equivalents, beginning of period | 43,019 | 29 | 43,048 | |||||||||

| Cash and equivalents, end of period | $ | 59,717 | $ | 83 | $ | 59,800 | ||||||

NOTE 3 – BASIS OF PRESENTATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Unaudited Interim Financial Information

The accompanying unaudited condensed consolidated financial statements have been prepared by the Company pursuant to the rules and regulations of the Securities and Exchange Commission (the “SEC”) and generally accepted accounting principles in the United States (“U.S. GAAP”) for interim financial reporting. The information furnished herein reflects all adjustments (consisting of normal recurring accruals and adjustments) which are, in the opinion of management, necessary to fairly state the operating results for the respective periods. Certain information and footnote disclosures normally present in annual consolidated financial statements prepared in accordance with accounting principles generally accepted in the United States of America have been omitted pursuant to such rules and regulations. These condensed consolidated financial statements should be read in conjunction with the financial statements and footnotes thereto, included in the Company’s 2012 Annual Report filed with the SEC on April 30, 2013. The interim results of operations are not necessarily indicative of the results to be expected for the full fiscal year or any future periods.

Principles of Consolidation

The condensed consolidated financial statements include the financial statements of the Company, its subsidiaries and VIEs. All significant inter-company balances and transactions have been eliminated in consolidation.

Fair Value of Financial Instruments

Financial instruments consist primarily of cash and cash equivalents, restricted cash, accounts receivable, accounts payable, due to affiliates and short-term borrowings. The carrying amounts of the financial instruments at June 30, 2013 and December 31, 2012 approximated their fair values because of the short maturity of these instruments or existence of variable interest rates, which reflect current market rates. When available, the Company measures the fair value of financial instruments based on quoted market prices in active markets, valuation techniques that use observable market-based inputs or unobservable inputs that are corroborated by market data. Pricing information that the Company obtains from third parties is internally validated for reasonableness prior to use in the condensed consolidated financial statements. When observable market prices are not readily available, the Company generally estimates fair value using valuation techniques that rely on alternate market data or inputs that are generally less readily observable from objective sources and are estimated based on pertinent information available at the time of the applicable reporting periods. In certain cases, fair values are not subject to precise quantification or verification and may fluctuate as economic and market factors vary and the Company’s evaluation of those factors changes. Although the Company uses its best judgment in estimating the fair value of these financial instruments, there are inherent limitations in any estimation technique. In these cases, a minor change in an assumption could result in a significant change in its estimate of fair value, thereby increasing or decreasing the amounts of the Company’s consolidated assets, liabilities, shareholders’ equity and net income or loss.

A financial instrument’s categorization within the fair value hierarchy is based upon the lowest level of input that is significant to the fair value measurement. Three levels of inputs are used to measure fair value:

Level 1 applies to assets or liabilities for which there are quoted prices in active markets for identical assets or liabilities.

Level 2 applies to assets or liabilities for which there are inputs other than quoted prices included within Level 1 that are observable for the asset or liability such as quoted prices for similar assets or liabilities in active markets; quoted prices for identical assets or liabilities in markets with insufficient volume or infrequent transactions (less active markets); or model-derived valuations in which significant inputs are observable or can be derived principally from, or corroborated by, observable market data.

Level 3 applies to assets or liabilities for which there are unobservable inputs to the valuation methodology that are significant to the measurement of the fair value of the assets or liabilities.

Guarantee

The Company recognizes the financial guarantees in accordance with ASC 460, “Guarantees”.

| 10 |

Revenue Recognition

The Company recognizes its current new commercial vehicle lease financing arrangement, including leases under the mortgage financing arrangement with China CITIC Bank, as a sales-type lease. For new commercial vehicles financed by the Company, the Company recognizes revenue when the following conditions are met: (a) when the lease contract is signed, (b) when the customer has taken possession of the vehicle, and (c) if the collectability of owed amounts are reasonably assured. The Company recognizes revenue using the fair value of the commercial vehicles by reference to the retail market price of the vehicles. The Company also records the sale of the GPS tracking unit sold to the lessee upon the transfer of the title and delivery of the product. These sales revenues are recorded as “Commercial Vehicles”.

In addition, the Company recognizes its second-hand vehicle lease financing arrangement as a direct financing lease because it does not give rise to dealer’s profit or loss to the Company. Under the second-hand vehicle lease financing program, the Company holds the title of the used vehicle and then transfers title to the customer at the end of the lease term. The excess of aggregate lease rentals over the acquisition cost of leased second-hand vehicle constitutes unearned lease income to be taken into income over the lease term by using the effective interest method.

A membership fee is charged to all lessees for the privilege of utilizing the Company’s store branch network for certain services, which include general support services, licensing and permit services, insurance services and registration services. The membership fee is charged and collected by the Company when a direct financing and sales-type lease is signed. The Company records the amount as a deduction of minimum lease payment receivable. Revenue from our membership fee is deferred and recognized ratably over the term of the direct financing and sales-type lease. The difference between the gross investment in the lease (and the fair value of the commercial vehicles) is recorded as unearned income and amortized based on the effective interest rate method over the lease term. Management servicing fees are recognized when services are rendered. The Company also receives commissions from insurance institutions for referring its customers to buy auto insurance. Insurance commission and agency income is recorded when the insurance contract is signed and the insurance premium is paid to the insurance company. With respect to the value added services (tires, fuel, insurance and second-hand vehicles financing services) that the Company offers, the Company provides one to three months of revolving credit facilities to eligible customers. Revenue from our tires, fuel and insurance services that is charged and collected at the beginning of the financing period is deferred and recognized ratably based on the effective interest rate method over the term of the financing period.

The membership fee, interest from direct financing and sales-type lease, management servicing fee, and revenues from tires, fuel and insurance financing services are recorded as “Finance”. The insurance commission and agency fee is recorded as “Insurance”.

Penalty income generated from the lessees for late payment is recognized when the payment is overdue and the collectability is reasonably assured. This income is recorded as “Other income”.

Office rental income related to the office leases is recognized on an accrual basis when due from office tenants as required by the accounting guidance applicable to leases, which provides guidance on classification and recognition. In accordance with the Company's standard lease terms, rental payments are generally due on a monthly basis. Any cash concessions given at the inception of the lease are amortized over the approximate life of the lease, which is generally one year.

Segment Reporting

Operating segments are defined as components of an enterprise about which separate financial information is available that is evaluated regularly by the chief executive officer, in deciding how to allocate resources and assessing performance. All of the Company’s sales are generated in the PRC and substantially all of the Company’s assets are located in the PRC. The Company’s operations consist of two reporting and operating segments, the commercial vehicle sales, servicing, leasing and support business, and office leasing business.

Earnings Per Share

The Company computes earnings per share (“EPS”) in accordance with generally accepted accounting principles. Companies with complex capital structures are to present basic and diluted EPS. Basic EPS is measured as the income available to ordinary shareholders divided by the weighted average ordinary shares outstanding for the period. For basic EPS, the weighted average number of shares outstanding for the period includes contingently issuable shares (i.e., shares issuable for little or no cash consideration upon the satisfaction of the conditions of a contingent stock agreement) as of the date that all necessary conditions have been met. Diluted EPS is similar to basic EPS but presents the dilutive effect on a per share basis of potential ordinary shares (e.g., convertible securities, options and warrants) as if they had been converted at the beginning of the periods presented, or issuance date, if later. Potential ordinary shares that have an anti-dilutive effect (i.e., those that increase income per share or decrease loss per share) are excluded from the calculation of diluted EPS.

| 11 |

Basic and diluted earnings per share for each of the periods presented are calculated as follows:

| Three months ended June 30, | Six months ended June 30, | |||||||||||||||

| 2013 | 2012 | 2013 | 2012 | |||||||||||||

| (unaudited) | (unaudited) | (unaudited) | (unaudited) | |||||||||||||

| Net income | $ | 4,360 | $ | 8,398 | $ | 4,773 | $ | 16,426 | ||||||||

| Weighted average number of common shares outstanding – Basic | 23,538,919 | 23,538,919 | 23,538,919 | 23,538,919 | ||||||||||||

| Stock options | 148,572 | 22,425 | 238,356 | 74,773 | ||||||||||||

| Weighted average number of common shares outstanding – Diluted | 23,687,491 | 23,561,344 | 23,777,275 | 23,613,692 | ||||||||||||

| Earnings per share | ||||||||||||||||

| Basic | $ | 0.19 | $ | 0.36 | $ | 0.20 | $ | 0.70 | ||||||||

| Diluted | $ | 0.18 | $ | 0.36 | $ | 0.20 | $ | 0.70 | ||||||||

Recently Issued Accounting Pronouncements

Management does not believe that any recently issued, but not yet effective, accounting standards or pronouncements, if currently adopted, would have a material effect on the Company’s condensed consolidated financial statements.

NOTE 4 – ACCOUNTS RECEIVABLE

Summaries of accounts receivable are as follows:

| June 30, | December 31, | |||||||

| 2013 | 2012 | |||||||

| (unaudited) | ||||||||

| Net investment in direct financing and sales-type lease | $ | 47,538 | $ | 41,427 | ||||

| Receivable from value-added services | 3,380 | 3,570 | ||||||

| Less: Allowance for doubtful accounts | (16,409 | ) | (12,041 | ) | ||||

| $ | 34,509 | $ | 32,956 | |||||

Net investment in direct financing and sales-type lease included into the accounts receivable represents the net investment in direct financing and sales-type lease which is overdue and delinquent.

NOTE 5 –PREPAID EXPENSES AND OTHER CURRENT ASSETS

Summaries of prepaid expenses and other current assets are as follows:

| June 30, | December 31, | |||||||

| 2013 | 2012 | |||||||

| (unaudited) | ||||||||

| Temporary advances to employees | $ | 289 | $ | 197 | ||||

| Prepaid interest expenses | 437 | 51 | ||||||

| Prepaid rent | 1,302 | 1,632 | ||||||

| Prepaid other taxes | 24 | 81 | ||||||

| Prepaid fuel charges | 42 | 46 | ||||||

| Prepaid insurance | — | 1,365 | ||||||

| Other current assets | 9,197 | 1,140 | ||||||

| Total | $ | 11,291 | $ | 4,512 | ||||

Prepaid insurance mainly includes the insurance premium of directors and officers liability insurance of the Company and the amount prepaid by the Company on behalf of the customers for its insurance agency business. Other current assets mainly include short-term advances made to third parties, such as to petrol companies and to customers for insurance claims and as of June 30, 2013 includes $6.5 million advanced to an unrelated third party named Hebei Five Parties Real Estate Development Company, which was subsequently repaid in August 2013.

| 12 |

NOTE 6 – NET INVESTMENT IN DIRECT FINANCING AND SALES-TYPE LEASES

The following lists the components of the net investment in direct financing and sales-type leases:

| June 30, | December 31, | |||||||

| 2013 | 2012 | |||||||

| (unaudited) | ||||||||

| Minimum lease payments receivable | $ | 273,501 | $ | 261,652 | ||||

| Less: Allowance for doubtful accounts | (249 | ) | (296 | ) | ||||

| Net minimum lease payments receivable | 273,252 | 261,356 | ||||||

| Less: unearned interest income | (24,379 | ) | (26,404 | ) | ||||

| Net investment in direct financing and sales-type leases | 248,873 | 234,952 | ||||||

| Less: Current maturities of net investment in direct financing and sales-type leases | (179,601 | ) | (196,213 | ) | ||||

| Net investment in direct financing and sales-type leases, net of current maturities | $ | 69,272 | $ | 38,739 | ||||

Net investment in direct financing and sales-type leases arises from the sale of commercial vehicles, for which the Company enters into monthly installment arrangements with its customers for approximately 2 years. The legal titles of the commercial vehicles are transferred to the customer when all the outstanding lease payments are fully settled. There is no unguaranteed residual value at the end of the lease upon the transfer of the lease. As of June 30, 2013 and December 31, 2012, the aggregate effective interest rate on direct financing and sales-type leases is approximately 16.86% and 18.96% per annum, respectively.

At June 30, 2013, future minimum lease payments are as follows:

| Years Ending December 31, | ||||||||||||||||

| 2013 | 2014 | 2015 | Total | |||||||||||||

| Net minimum lease payments receivable | $ | 122,886 | $ | 125,468 | $ | 24,898 | $ | 273,252 | ||||||||

| Less: unearned interest income | (13,911 | ) | (9,759 | ) | (709 | ) | (24,379 | ) | ||||||||

| Net investment in direct financing and sales-type leases | $ | 108,975 | $ | 115,709 | $ | 24,189 | $ | 248,873 | ||||||||

NOTE 7 – PROPERTY, EQUIPMENT AND LEASEHOLD IMPROVEMENTS, NET

Summaries of property, equipment and leasehold improvements are as follows:

| June 30, | December 31, | |||||||

| 2013 | 2012 | |||||||

| (unaudited) | ||||||||

| Buildings and leasehold improvements | $ | 73,976 | $ | 1,512 | ||||

| Furniture and fixtures | 6,539 | 6,189 | ||||||

| Machinery and equipment | 6,155 | — | ||||||

| Company automobiles | 1,867 | 1,730 | ||||||

| Total | 88,537 | 9,431 | ||||||

| Less: accumulated depreciation and amortization | (5,706 | ) | (4,446 | ) | ||||

| Property, equipment and leasehold improvements, net | $ | 82,831 | $ | 4,985 | ||||

Depreciation and amortization expense for the operations was approximately $869, $496, $1,342 and $919 for the three months and six months ended June 30, 2013 and 2012, respectively.

| 13 |

NOTE 8 – OTHER PAYABLES AND ACCRUED LIABILITIES

Other payables and accrued liabilities consist of the following:

| June 30, | December 31, | |||||||

| 2013 | 2012 | |||||||

| (unaudited) | ||||||||

| Accrued expenses | $ | 1,644 | $ | 2,540 | ||||

| Business and other tax payables | 6,674 | 6,418 | ||||||

| Salary payable | 1,924 | 1,524 | ||||||

| Temporary receipt of insurance premium | 236 | 176 | ||||||

| Temporary receipt of insurance claims | 881 | 755 | ||||||

| Deposits received | 5,699 | 2,128 | ||||||

| Interest payable | 157 | 207 | ||||||

| Other current liabilities | 1,374 | 1,301 | ||||||

| Total | $ | 18,589 | $ | 15,049 | ||||

Deposits received represented security deposits received from staff and customer deposits. Temporary receipt of insurance premium represents the premium collected from customers but not yet paid to the insurance company. Temporary receipt of insurance claims represents the insurance claims received but not yet released to the relevant customers. Other current liabilities mainly include the unpaid expenses reimbursement due to staff, withholding taxes collected from customers for the value-added services.

NOTE 9 – LONG-TERM PAYABLES

Other Long-term payables consists of the following:

| June 30, | December 31, | |||||||

| 2013 | 2012 | |||||||

| (unaudited) | ||||||||

| Total long-term payables | $ | 1,463 | $ | — | ||||

| Less: Unrealized interest expense | (112 | ) | — | |||||

| Net long-term payables | $ | 1,351 | $ | — | ||||

| Long-term payables, current | (644 | ) | — | |||||

| Long-term payables, non-current | $ | 707 | $ | — | ||||

Under the mortgage financing arrangement with CITIC Bank, the Company’s customers obtain mortgage financing from CITIC while the Company provides a guarantee. The Company enters into a lease contract directly with the customer and also enters into a contractual obligation to repay the mortgage financing on behalf of the customer. The CITIC mortgage financing has a 24-month term and as a result the Company recognizes a long-term liability for amounts borrowed under the CITIC mortgage financing arrangement.

The loans bore interest at rates in the range of 8.19% to 8.82% as of June 30, 2013, are denominated in RMB and have terms maturing within two years.

At June 30, 3013, future amounts due under long-term payables are as follows:

| Years Ending December 31, | ||||||||||||||||

| 2013 | 2014 | 2015 | Total | |||||||||||||

| Long-term payables | $ | 355 | $ | 742 | $ | 366 | $ | 1,463 | ||||||||

| Less: Unrealized interest expense | (46 | ) | (58 | ) | (8 | ) | (112 | ) | ||||||||

| Total long-term payables | $ | 309 | $ | 684 | $ | 357 | $ | 1,351 | ||||||||

NOTE 10 – THIRD PARTY BORROWINGS

Short-term borrowings

A summary of the Company’s short-term borrowings is as follows:

| Weighted-average interest rate | ||||||||||||||||||

| June 30, | December 31, | June 30, | December 31, | |||||||||||||||

| 2013 | 2012 | Maturities | 2013 | 2012 | ||||||||||||||

| (unaudited) | ||||||||||||||||||

| Short-term bank loans | 6.24 | % | 7.03 | % | July 2013 to January 2014 | $ | 116,529 | $ | 102,458 | |||||||||

Short-term bank loans represent loans from local banks that were used for working capital and capital expenditures purposes. The loans bore interest at rates in the range of 4.8% to 7.26% as of June 30, 2013, are denominated in RMB and have terms maturing within one year. The company has repaid the loans that were due in July and August 2013, in addition to one loan due on September 3, 2013.

NOTE 11 – INCOME TAXES

Cayman Islands: Under the current tax laws of the Cayman Islands, the Company and its subsidiaries are not subject to tax on their income or capital gains.

Hong Kong: The Company’s subsidiary in Hong Kong did not have assessable profits that were derived from Hong Kong during the six months ended June 30, 2013 and during 2012. Therefore, no Hong Kong profit tax has been provided for in the periods presented.

China: Effective January 1, 2008, the National People’s Congress of China enacted a new PRC Enterprise Income Tax Law, under which foreign invested enterprises and domestic companies are generally subject to enterprise income tax at a uniform rate of 25%.

| 14 |

Summaries of the income tax provision in the condensed consolidated statements of income are as follows:

| Three months ended June 30, | Six months ended June 30, | |||||||||||||||

| 2013 | 2012 | 2013 | 2012 | |||||||||||||

| Current | $ | 5,623 | $ | 3,620 | $ | 10,361 | $ | 5,977 | ||||||||

| Deferred | (3,664 | ) | (985 | ) | (7,790 | ) | (574 | ) | ||||||||

| Total | $ | 1,959 | $ | 2,635 | $ | 2,571 | $ | 5,403 | ||||||||

The tax effects of temporary differences representing deferred income tax assets (liabilities) result principally from the following:

| June 30, | December 31, | |||||||

| 2013 | 2012 | |||||||

| (unaudited) | ||||||||

| Current | ||||||||

| Deferred income tax assets: | ||||||||

| Provision for doubtful accounts | $ | 4,177 | $ | 3,096 | ||||

| Accrued liabilities | 254 | 410 | ||||||

| Tax loss carry forward | 725 | 520 | ||||||

| Other temporary differences | 852 | 582 | ||||||

| Net deferred income tax assets – current | 6,008 | 4,608 | ||||||

| Deferred income tax liabilities - current | ||||||||

| Unearned income | (4,145 | ) | (9,325 | ) | ||||

| Net deferred income tax assets (liabilities) – current | $ | 1,863 | $ | (4,717 | ) | |||

| Non-current | ||||||||

| Deferred income tax assets: | ||||||||

| Accrued liabilities | 1,776 | 1,738 | ||||||

| Tax loss carry forward | 2,174 | 1,560 | ||||||

| Deferred income tax assets – non-current | 3,950 | 3,298 | ||||||

| Deferred income tax liabilities – non-current: | ||||||||

| Unearned income | (193 | ) | (751 | ) | ||||

| Net deferred income tax assets – non-current | $ | 3,757 | $ | 2,547 | ||||

As of June 30, 2013, deferred income tax assets derived from accrued liabilities, unearned income, tax loss carried forward, provision for doubtful accounts and other temporary differences arose from the same tax jurisdictions in China with the deferred income tax liabilities. Therefore, the respective deferred income tax assets and liabilities were net off for presentation.

At June 30, 2013, the Company had $11,600 of tax loss carry forwards that expire through December 31, 2016.

| 15 |

The difference between the effective income tax rate and the expected statutory rate was as follows:

| Three months ended June 30, | Six months ended June 30, | |||||||||||||||

| 2013 | 2012 | 2013 | 2012 | |||||||||||||

| (unaudited) | (unaudited) | (unaudited) | (unaudited) | |||||||||||||

| Statutory rate | 25.0 | % | 25.0 | % | 25.0 | % | 25.0 | % | ||||||||

| Non-deductible expenses | 4.8 | % | 2.8 | % | 8.7 | % | 3.3 | % | ||||||||

| Non-taxable income | (1.4 | )% | (0.8 | )% | (2.4 | )% | (0.8 | )% | ||||||||

| Effect of rate differences in various transportation centers | 2.5 | % | (3.2 | )% | 3.7 | % | (2.8 | )% | ||||||||

| Effective tax rate | 31.0 | % | 23.8 | % | 35.0 | % | 24.7 | % | ||||||||

The guidance on accounting for uncertainties in income taxes prescribes a more likely than not threshold for financial statement recognition and measurement of a tax position taken or expected to be taken in a tax return. Guidance was also provided on recognition of income tax assets and liabilities, classification of current and deferred income tax assets and liabilities, accounting for interest and penalties associated with tax positions, accounting for income taxes in interim periods, and income tax disclosures. Non-deductible expenses are mainly related to the share based payment. Significant judgment is required in evaluating the Group’s uncertain tax positions and determining its provision for income taxes. The Company did not have any significant interest and penalties associated with uncertain tax positions for the three months and six months ended June 30, 2013 and 2012. As of June 30, 2013 and December 31, 2012, the Company did not have any significant unrecognized uncertain tax positions.

NOTE 12 – COMMITMENTS AND CONTINGENCIES

Lease Commitments

The Company leases certain facilities under long-term, non-cancelable leases and month-to-month leases. These leases are accounted for as operating leases. Rent expense amounted to $771, $1,578, $722, and $1,368 for the three months and six months ended June 30, 2013 and 2012, respectively.

Future minimum payments under long-term, non-cancelable leases as of June 30, 2013, are as follows:

| Year Ending December 31, | Future Minimum Payments | |||

| 2013 (six months) | $ | 50 | ||

| 2014 | 985 | |||

| 2015 | 265 | |||

| 2016 | 44 | |||

| Total | $ | 1,344 | ||

Legal Proceedings

The staff of the SEC conducted a non-public investigation relating to the Company and, in this regard, the Company and its officers have received subpoenas for information. On January 6, 2012, the Company announced that it received a Wells Notice from the staff of the SEC, which the Company responded to. The Company cooperated with the SEC regarding this matter, including voluntarily providing information beyond that formally requested by the SEC staff, in an effort to assist in an expeditious conclusion of the staff’s investigation. On April 11, 2012, the SEC filed a lawsuit against the Company and 11 of its shareholders for stock manipulation, alleging that the Company deliberately manipulated trading in its shares to create the appearance of a liquid and active market. The Company continues to work closely with its legal counsel and advisors to defend the Company. The Company is unable at this time to predict the outcome of this lawsuit or whether the Company will incur any liability associated with the lawsuit, or to estimate the effect such outcome would have on the condensed consolidated financial statements.

In the opinion of management, there are no other material claims assessments or litigation pending against the Company.

NOTE 13 – SEGMENT REPORTING

The Company measures segment income as income from operations less depreciation and amortization. The reportable segments are components of the Company which offer different products or services and are separately managed, with separate financial information available that is separately evaluated regularly by the Company’s Chief Executive Officer in determining the performance of the business.

Upon consummation of the merger of Heat Planet and the Company, the Company operated two segments: commercial vehicle sales, servicing, leasing and support segment and office leasing segment. Prior to the acquisition of Hebei Ruiliang Trading in April 2012, the Company operated a single segment of commercial vehicle sales, servicing, leasing and support segment. During the reporting periods, the office leasing segment did not commence operation and did not generate any revenues or operating results. However, the value of the assets of the office leasing segment as of June 30, 2013 and December 31, 2012 are $78,939 and $76,893, respectively. The remaining values of assets as of June 30, 2013 and December 31, 2012 are $377,129 and $362,413, respectively, which are related to the commercial vehicle sales, servicing, leasing and support segment.

| 16 |

NOTE 14 – RELATED PARTY BALANCES AND TRANSACTIONS

Due to affiliates:

During the periods presented, the Company has borrowed from the Company’s Chairman and Chief Executive Officer, Mr. Yong Hui Li (“Mr. Li”), Honest Best and other companies affiliated with Mr. Li. Each of these loans was entered into to satisfy the Company’s short-term capital needs.

The amount due to Alliance Rich represented a portion of the consideration of the acquisition of Heat Planet. The amount is payable within six months of the later of the occupation of the Real Estate Asset, which occurred in April 2013, and delivery of the audited financial statements of Heat Planet for the five months ended May 31, 2012, which were delivered in December 2012. Therefore, any unpaid amounts after October 6, 2013 will begin to accrue interest at the one-year rate announced by the People’s Bank of China (6.00% as of June 30, 2013).

Prior to September 2011, the amount due to Hebei Kaiyuan was non-interest bearing, unsecured and due on demand by the lender. In September 2011, Hebei Kaiyuan began charging interest at 8.00% per annum, and continues to be unsecured and due on demand by the lender.

The amount due to Hebei Shengrong Kaiyuan Auto Parts Co., Ltd. (“Kaiyuan Shengrong”) bears the average interest rate of 6.93% per annum, which is adjustable in connection with the basis rate established by the People’s Bank of China, is unsecured and will commence maturity in July 2013.

The amount due to AutoChina Inc., Smart Success Investment Limited (“Smart Success”) and Alliance Rich were non-interest bearing, unsecured and due on demand by the lenders.

The outstanding amounts due to related parties as of June 30, 2013 and December 31, 2012 were as follows:

| June 30, | December 31, | |||||||||

| Notes | 2013 | 2012 | ||||||||

| (unaudited) | ||||||||||

| Mr. Li | (1) | $ | 144 | $ | 144 | |||||

| Alliance Rich | (2) | 39,961 | 56,170 | |||||||

| Hebei Kaiyuan | (2) | 5,084 | 1,162 | |||||||

| Kaiyuan Shengrong | (2) | 8,534 | 8,110 | |||||||

| Smart Success | (2) | 9 | 9 | |||||||

| Total | $ | 53,732 | $ | 65,595 | ||||||

Notes:

| (1) | The Chairman and Chief Executive Officer of AutoChina. | |

| (2) | Entity controlled by Mr. Li. |

Accounts payable, related party:

During the periods presented, the Company purchased commercial vehicles from Ruituo, a company which is controlled by Mr. Li’s brother. The amount due to Ruituo was non-interest bearing until October 2011. In addition, the payable balance is unsecured and due on demand by Ruituo. In October 2011, Ruituo began charging interest at 8.00% per annum to the Company for the payables.

The outstanding amount due to related party as of June 30, 2013 and December 31, 2012 was as follows:

| June 30, | December 31, | |||||||||

| Note | 2013 | 2012 | ||||||||

| (unaudited) | ||||||||||

| Ruituo | (1) | $ | 6,057 | $ | 2,228 | |||||

Note:

(1) Entity controlled by Mr. Li’s brother.

| 17 |

Related Party Transactions

During the periods presented, the details of the related party transactions were as follows:

| Six months ended June 30, | ||||||||||

| Notes | 2013 | 2012 | ||||||||

| (unaudited) | As Adjusted – note 2 (unaudited) | |||||||||

| Capital nature: | ||||||||||

| Hebei Kaiyuan | (1) (a) | $ | 21,040 | $ | 65,037 | |||||

| Hebei Kaiyuan | (1) (d) | 5,004 | 71,049 | |||||||

| Kaiyuan Shengrong | (1) (b) | 10,520 | 3,173 | |||||||

| Kaiyuan Shengrong | (1) (c) | 10,520 | 3,173 | |||||||

| Ruihua Real Estate | (1) (a) | 24,277 | — | |||||||

| Ruituo | (2) (a) | 24,277 | — | |||||||

| Beijing Wantong Longxin Auto Trading Co., Ltd. | (3) (d) | — | 41,369 | |||||||

| Trading nature: | ||||||||||

| Beijing Wantong Longxin Auto Trading Co., Ltd. | (3) (g) | 2,642 | — | |||||||

| Hebei Kaiyuan | (1) (f) | $ | 43 | $ | 43 | |||||

| Kaiyuan Shengrong | (1) (f) | 282 | 131 | |||||||

| Ruituo | (2) (e) | 204,956 | 152,979 | |||||||

| Ruituo | (2) (f) | 52 | 279 | |||||||

| Honest Best | (4) (f) | $ | — | $ | 58 | |||||

Notes:

| (1) | Entity controlled by Mr. Li. | |

| (2) | Entity controlled by Mr. Li’s brother. | |

| (3) | Entity in which Mr. Li’s brother holds a 40% equity interest. | |

| (4) | Parent company of AutoChina and entity controlled by Mr. Li. |

Nature of transaction:

| (a) | Bank loan guarantee provided by the affiliates to the Company. | |

| (b) | Bank loan guarantee provided by the Company to the affiliate. | |

| (c) | Receivables of the Company pledged to guarantee the bank loans borne by the affiliate. | |

| (d) | Loan provided to the Company during the period. | |

| (e) | Sale of automobiles to the Company, including VAT, during the period. | |

| (f) | Interest expenses incurred by the Company during the period. | |

| (g) | Deposits for inventories made by the Company to affiliates for the purchase of commercial vehicles and amounts returned during the year. | |

Since the year ended December 31, 2010, the Company started purchasing commercial vehicles from an affiliate of Mr. Li, Ruituo, at a markup of approximately 0.3%. The balance due on such purchase is interest-free, unsecured and due on demand and was initially interest-free. In October 2011, Ruituo began charging interest at 8.00% per annum to the Company for the payables.

During the six months ended June 30, 2013 and 2012, the Company purchased commercial vehicles from Ruituo amounting to $204,956 and $152,979, respectively. The Company incurred interest expense of $52 and $279 for the purchase from Ruituo throughout the six months ended June 30, 2013 and 2012, respectively.

The Company occupied office space in Shijiazhuang, China provided by Hebei Kaiyuan, an affiliate of Mr. Li. Hebei Kaiyuan agreed to provide the office space at free of charge and no rental costs were incurred by the Company during the six months ended June 30, 2013 and 2012. In April 2013 the Company moved to and began occupying its new wholly-owned office space in the Kai Yuan Center.

NOTE 15 – CREDIT QUALITY OF FINANCING RECEIVABLES AND ALLOWANCE FOR CREDIT LOSSES

The Company applies a systematic methodology to determine the allowance for credit losses for account receivables and net investments in direct financing and sales-type leases. Based upon a credit loss and risk factor analysis, since the Company only leases commercial vehicles to its customers, it considers its lessee customers as its only portfolio segment.

The Company further evaluated the portfolio by the class of the account receivables and net investments in direct financing and sales-type leases, which is defined as a level of information (below a portfolio segment) in which the receivables have the same initial measurement attribute and a similar method for assessing and monitoring credit risk. The Company’s account receivables and net investments in direct financing and sales-type leases consist of the receivables from the net investment in direct financing and sales-type lease and the receivables from value-added services. The Company only offers the optional value-added services to existing customers who have a history of making on-time payments with the Company. The Company controls legal title to the commercial vehicles leased to the lessee customers and it is allowed to repossess the commercial vehicles if the lessee customer defaults on its monthly installment payments (of the net investment in direct financing and sales-type lease) or the payment of value-added services. Therefore, both of these receivables are secured by the commercial vehicles leased to the lessee customers and the Company uses the same credit control to evaluate the risk of credit loss.

| 18 |

Impaired net investment in direct financing and sales-type lease and receivable from value-added services

Net investment in direct financing and sales-type leases and receivables from value-added services is considered impaired, based on current information and events, if it is probable that we will be unable to collect all amounts due according to the contractual terms of the lease. The net investment in direct financing and sales-type leases and receivables from value-added services will be reviewed for impairment. Included in these amounts are leases that are in default, non-performing or in bankruptcy. Based on our non-performing direct financing and sales-type leases experience from those leases that were either matured or in the stage that were close to maturities, we also assess and make provision for performing loans. Recognition of income is suspended and a lease is placed on non-accrual status when management determines that collection of future income is not probable. Accrual is resumed, and previously suspended income is recognized, when the lease becomes contractually current and/or collection doubts are removed. Cash receipts on impaired leases are recorded against the receivable and then to any unrecognized income.

Allowance for credit loss activity

In estimating the allowance for credit loss, the Company reviews the net investment in direct financing and sales-type lease and receivable from value-added services that are non-performing or in bankruptcy. The allowance for credit loss as of June 30, 2013 and December 31, 2012 were as follows:

| June 30, | December 31, | |||||||

| 2013 | 2012 | |||||||

| (unaudited) | ||||||||

| Balance at the beginning of the period | $ | 12,337 | $ | 5,544 | ||||

| Provision during the period | 7,853 | 14,550 | ||||||

| Bad debts written off | (3,532 | ) | (7,757 | ) | ||||

| Balance at the end of the period | $ | 16,658 | $ | 12,337 | ||||

Credit quality of finance receivables

The credit quality of net investment in sales-type lease and receivable from value-added services is reviewed on a quarterly basis. Credit quality indicators include performing and non-performing. Non-performing is defined as receivables past due and/or on nonaccrual status or in bankruptcy. The receivables not meeting the criteria listed above are considered performing. Non-performing receivables have the highest probability for credit loss. The allowance for credit loss attributable to non-performing receivables is based on the most probable source of repayment, which is normally the residual value of commercial vehicles. In determining residual value of the commercial vehicles, the Company refers to the second-hand market values of the commercial vehicles as a reference.

The carrying amount of the performing and non-performing finance receivables as of June 30, 2013 and December 31, 2012 was as follows:

| June 30, 2013 | Performing | Non- performing | Total carrying amount | |||||||||

| Net investment in direct financing and sales-type leases | $ | 248,872 | $ | — | $ | 248,872 | ||||||

| Accounts receivable | 4,050 | 30,459 | 34,509 | |||||||||

| $ | 252,922 | $ | 30,459 | $ | 283,381 | |||||||

| December 31, 2012 | Performing | Non- performing | Total carrying amount | |||||||||

| Net investment in direct financing and sales-type leases | $ | 234,952 | $ | — | $ | 234,952 | ||||||

| Accounts receivable | 3,025 | 29,931 | 32,956 | |||||||||

| $ | 237,977 | $ | 29,931 | $ | 267,908 | |||||||

The carrying amount of the impaired finance receivables as of June 30, 2013 and December 31, 2012 was as follows:

| June 30, 2013 | Gross amount | Allowance for credit losses | Total carrying amount | |||||||||

| Net investment in direct financing and sales-type leases | $ | 862 | $ | 249 | $ | 613 | ||||||

| Accounts receivable | 38,369 | 16,409 | 21,960 | |||||||||

| $ | 39,231 | $ | 16,658 | $ | 22,573 | |||||||

| December 31, 2012 | Gross amount | Allowance for credit losses | Total carrying amount | |||||||||

| Net investment in direct financing and sales-type leases | $ | 5,084 | $ | 296 | $ | 4,788 | ||||||

| Accounts receivable | 29,716 | 12,041 | 17,675 | |||||||||

| $ | 34,800 | $ | 12,337 | $ | 22,463 | |||||||

The analysis of the age of the carrying amount of the overdue receivables as of June 30, 2013 and December 31, 2012 was as follows:

| June 30, | December 31, | |||||||

| 2013 | 2012 | |||||||

| Less than 90 days | $ | 16,223 | $ | 19,103 | ||||

| Over 90 days | 30,645 | 22,869 | ||||||

| 46,868 | 41,972 | |||||||

| Less: allowance for credit losses | (16,409 | ) | (12,041 | ) | ||||

| Total | $ | 30,459 | $ | 29,931 | ||||

For the three and six months ended June 30, 2013 and 2012, the related amount of interest income recognized for impaired finance receivables was $870, $1,903, $1,059 and $2,033, respectively.

| 19 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

OVERVIEW

AutoChina International Limited (“AutoChina,” the “Company,” “our,” or “we”) is a holding company whose only business operations are conducted through its wholly owned subsidiary, AutoChina Group Inc. (“ACG”). ACG’s operations consist of the commercial vehicle sales, servicing, leasing and support business, which provides financing to customers to purchase commercial vehicles and related services.

We were incorporated in the Cayman Islands on October 16, 2007 under the name “Spring Creek Acquisition Corp.” as a blank check company formed for the purpose of acquiring, through a stock exchange, asset acquisition or other similar business combination, or controlling, through contractual arrangements, an operating business, that had its principal operations in greater China.

On April 9, 2009, we acquired all of the outstanding securities of ACG, an exempt company incorporated in the Cayman Islands, from Honest Best Int’l Ltd., resulting in ACG becoming our wholly owned subsidiary. Promptly after our acquisition of ACG, we changed our name to “AutoChina International Limited.”

The Company owns a store branch network in different regions of China to provide commercial vehicle sales and services which include leasing services, general support services, licensing and permit services, insurance services and registration services, to its lessees. As of June 30, 2013, the Company had 535 stores in 26 provinces or provincial-level regions.

The Company launched its own insurance agency business in December 2011 and has signed agreements with various major insurance companies in China to sell insurance. AutoChina’s 535 store locations are each licensed to sell insurance from these carrier partners.

On September 11, 2012, the Company acquired Heat Planet Holdings Limited (“Heat Planet”) and its subsidiaries, whose primary asset consists of 23 floors, or over 60,000 square meters, of newly constructed office space in the Kai Yuan Center building (the “Real Estate Asset”). Located at 5 East Main Street in Shijiazhuang, where the Company is currently based, the 245-meter tall Kai Yuan Center, whose topmost floors are occupied by a Hilton Worldwide-operated, five-star hotel, is the tallest building in Shijiazhuang and Hebei Province.. The building was completed in April 2013, and AutoChina moved its headquarters to the new Kai Yuan Center, which serves as the control center for each of the Company’s 535 commercial vehicle financial centers located throughout China. The Company does not occupy the entire office space purchased, and has commenced leasing out the unoccupied space, the proceeds from which will be reported as rental income.

Commercial Vehicle Financing Structure

From late September 2009 to November 2011, Hebei Chuangjie Trading Co., Ltd. (“Chuangjie Trading”), our VIE, engaged CITIC Trust Co., Ltd., which we refer to as the Trustee, a division of the CITIC Group, to act as trustee for a trust fund set up for the sole benefit of Chuangjie Trading, or the Trust Fund. The Trustee was responsible for the management of the funds invested in the Trust Fund, and the Trust Fund was used to purchase commercial vehicles from Kaiyuan Auto Trade Co., Ltd. (“Kaiyuan Auto Trade”) (our existing VIE). Pursuant to the Trust Fund documents, each use of the Trust Fund (e.g. to purchase a commercial vehicle) required a written order to the Trustee from Chuangjie Trading. This structure was implemented through a non-exclusive 3-year contractual relationship that was automatically renewable and unilaterally amendable and cancellable by CITIC Trust. Under this structure, we utilized CITIC Trust’s business license for vehicle leasing. This structure also allowed us to promote our leasing business by using the nationally recognized name of CITIC, and enabled us to start a lease securitization program with CITIC, which provided an additional source of financing.

Under the structure in which CITIC Trust acted as an intermediary, commercial vehicle purchase orders were issued (upon completion of credit checks) by a local center to Chuangjie Trading, which then instructed the Trustee to place the orders for the vehicles with Kaiyuan Auto Trade. Upon the issuance of a commercial vehicle purchase order, the Trustee, Kaiyuan Auto Trade and the relevant local center entered into a Sale and Management Agreement, and the Trustee, relevant local center and customer lessee entered into a Lease and Management Agreement governing each commercial vehicle purchase. Under the Sale and Management Agreements and Lease and Management Agreements, the parties agreed that: (1) the Trustee would deliver the funds for the purchase of the commercial vehicle and instructed Kaiyuan Auto Trade to have the vehicle delivered directly to the lessee; (2) the local center would hold title to the commercial vehicle for the benefit of the Trustee for the term of the lease and would provide services to the lessee including maintaining the vehicle legal records (registration, tax invoices, etc.), assisting the end user in performing annual inspections, renewing the vehicle’s license, purchasing insurance, and making insurance claims; (3) the lessee would be responsible for the costs associated with the lease of the truck and with the maintenance and administrative services contracted out by the local center; and (4) upon the completion of the lease and payment in full by the lessee of all fees, the local center would transfer title to the vehicle to the lessee upon the lessee’s request. Under the Lease and Management Agreement, the Trust Fund was entitled to future receivables under a lease, while Chuangjie Trading was entitled to the economic benefits of the Trust Fund as the trust beneficiary.

| 20 |

In September 2010, we established a new wholly foreign owned enterprise in China, Ganglian Finance Leasing Co., Ltd. (“Ganglian Finance Leasing”), which performs the leasing business of commercial vehicles. In December 2010, the Company increased the paid-in capital of Ganglian Finance Leasing through its VIE, Kaiyuan Auto Trade, and converted Ganglian Finance Leasing from a wholly foreign-owned enterprise to a Chinese-foreign joint venture. Thereafter, In December 2010, our subsidiary, Hebei Chuanglian Trade Co. Ltd., changed its name to Hebei Chuanglian Finance Leasing Co., Ltd. (“Hebei Chuanglian Finance Leasing”) and commenced leasing commercial vehicles.

Since December 2010, our subsidiaries, Ganglian Finance Leasing and Hebei Chuanglian Finance Leasing, as lessors, have been leasing commercial vehicles directly to our customers and not as part of the structure in which CITIC Trust acted as an intermediary. Under this new business model, the lessor purchases the commercial vehicles from Kaiyuan Auto Trade and/or Hebei Xuhua Trading, then leases the commercial vehicles to the customer lessees directly. The lessor, the relevant local center and customer lessee will enter into a Lease and Management Agreement governing each commercial vehicle purchase. Under the Lease and Management Agreement, the parties agree that: (1) the local center will hold title to the commercial vehicle for the benefit of the lessor for the term of the lease and will provide services to the lessee, including maintaining the vehicle legal records (registration, tax invoices, etc.), assisting the end user in performing annual inspections, renewing the vehicle’s license, purchasing insurance, and making insurance claims; (2) the lessee will be responsible for the costs associated with the lease of the truck and with the maintenance and administrative services contracted out by the local center; and (3) upon the completion of the lease and payment in full by the lessee of all fees, the local center will transfer title to the vehicle to the lessee upon the lessee’s request. Since November 2011, the Company ceased to engage CITIC Trust as an intermediary for its new leases. However, CITIC Trust continues to serve as an intermediary for existing leases until these leases are fully settled and/or expired. The last of the leases entered into pursuant to this financing structure will expire in March 2014. Thereafter, the Company will operate its entire leasing business directly through its subsidiaries, Hebei Chuanglian Finance Leasing and Ganglian Finance Leasing.

In March 2013 we began leasing commercial vehicles under the newly established mortgage financing arrangement with CITIC bank. Under this agreement, CITIC Bank provides up to 50% of the mortgage financing to Ganglian Finance Leasing’s lessees of commercial vehicles and Ganglian Finance Leasing agrees to provide a full guarantee to CITIC Bank for such mortgage financing and also provides a pledge of the ownership of the commercial vehicle to CITIC Bank to secure its guarantees.

In June 2011, our subsidiary, Fancy Think Limited, acquired the remaining equity interest of Ganglian Finance Leasing from our VIE, Kaiyuan Auto Trade, and converted Ganglian Finance Leasing back to a wholly foreign-owned enterprise. In addition, our VIE, Kaiyuan Auto Trade transferred 100% of the equity interest in Chuangjie Trading, the beneficiary of the Trust Fund, to Ganglian Finance Leasing. After the June 2011 restructuring Ganglian Finance Leasing, Hebei Chuanglian Finance Leasing and Chuangjie Trading were all directly owned by AutoChina, and were no longer part of a VIE holding structure. In March 2013, Ganglian Finance Leasing transferred its entire equity interest in Chuangjie Trading back to Kaiyuan Auto Trade. The change resulted in Chuangjie Trading once again becoming a VIE of the Company. In addition, Fancy Think Limited transferred a 10% interest of Hebei Chuanglian Finance Leasing to Ganglian Finance Leasing. Accordingly, Fancy Think Limited and Ganglian Finance Leasing hold an 80% and 20% interest, respectively, in Hebei Chuanglian Finance Leasing.

In May 2013 Kaiyuan Auto Trade Co., Ltd. (“Kaiyuan Auto Trade”) changed its name to Kaiyuan Auto Trade Group Co., Ltd. (“Kaiyuan Auto Trade Group”). In June 2013 we established a new wholly-owned subsidiary called Hebei Ruiliang Property Services.

Tires and Fuel Services

Commencing in January 2010, we began offering our customers financing to purchase tires and diesel fuel. Under the tire purchase program, approved customers pay for new tire purchases over a 3-month term. Under the fuel purchase program, the Company offers approved customers a 1-month revolving credit facility to buy diesel fuel from selected fueling stations that have partnered with AutoChina. AutoChina charges customers a fee for both services and also receives commission fees on customer purchases from the associated vendors.

Insurance Service

During the term of the lease, customers are required to purchase insurance covering the commercial vehicle on an annual pre-paid basis. We receive commission on customer purchases from the associated insurance companies. Commencing in March 2010, we began offering our customers financing for their annual insurance premium. Beginning with the second year of a lease, approved customers may pay for their annual insurance premium over the course of 90 days. We charge customers a fee for this service.

Second-Hand Commercial Vehicle Financing Service

Commencing September 2010, we began offering our customers second-hand vehicle financing services, pursuant to which we provide financing for approved customers to purchase a second-hand commercial vehicle. The resulting lease is structured similarly to those that we provide to customers purchasing new commercial vehicles, with each customer having full access to AutoChina’s value-added services, such as diesel, tire, and fuel financing. We expanded this service to offer a sale-leaseback program, which allows both former and new AutoChina customers to place vehicles they own outright into the Company’s network to accommodate their financing needs.

We charge a service fee to the customer and require monthly repayment over a term of 12 to 18 months. We recognized the second-hand vehicle leasing arrangements as a direct financing lease.

Lease Securitization Program