As filed with the Securities and Exchange Commission on September 23, 2020.

No. 333-146827

No. 811-22135

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

_____________________________

FORM

|

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 |

☐ |

|

Pre-Effective Amendment No. |

☐ |

|

Post-Effective Amendment No. 452 |

☒ |

|

and/or | |

|

REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 |

☐ |

|

Amendment No. 453 |

☒ |

(Exact Name of Registrant as Specified in Charter)

109 North Hale Street

Wheaton,

Illinois 60187

(Address of Principal Executive Office)

Registrant’s Telephone Number, including Area Code: (800) 208-5212

Corporation Service Company

2711 Centerville Road, Suite 400

Wilmington,

New Castle County, Delaware 19808

(Name and Address of Agent for Service)

Copy to:

|

Morrison C. Warren, Esq. |

|

Chapman and Cutler LLP |

|

111 West Monroe Street |

|

Chicago, Illinois 60603 |

It is proposed that this filing will become effective (check appropriate box):

☐ Immediately upon filing pursuant to paragraph (b) of Rule 485.

☒ On September 29, 2020 pursuant to paragraph (b) of Rule 485.

☐ 60 days after filing pursuant to paragraph (a)(1) of Rule 485.

☐ On (date) pursuant to paragraph (a) of Rule 485.

☐ 75 days after filing pursuant to paragraph (a)(2) of Rule 485.

☐ On (date) pursuant to paragraph (a) of Rule 485.

If appropriate, check the following box:

☒ This post-effective amendment designates a new effective date for a previously filed post-effective amendment.

Contents of Post-Effective Amendment No. 452

This Registration Statement comprises the following papers and contents:

The Facing Sheet

Part A - Prospectus for Innovator Triple Stacker ETF – October (formerly Innovator U.S. Equity Triple Stacker ETF – October)

Part B - Statement of Additional Information for Innovator Triple Stacker ETF – October (formerly Innovator U.S. Equity Triple Stacker ETF – October)

Part C - Other Information

Signatures

The information in this Prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This Prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer of sale is not permitted.

Subject to Completion

Dated September 23, 2020

Prospectus

Innovator Triple Stacker ETF – October

(Cboe BZX—TSOC)

October 1, 2020

Innovator Triple Stacker ETF –

October (the “Fund”)

is a series of Innovator ETFs Trust (the “Trust”) and is an actively managed

ETF.

• The Fund will invest substantially all of its assets in a portfolio of FLexible EXchange® Options (“FLEX Options”) that reference the SPDR® S&P 500® ETF Trust (the “S&P 500 ETF”), the Invesco QQQ TrustSM, Series 1 (the “NASDAQ-100 ETF”) and iShares Russell 2000 ETF (the “Russell 2000 ETF,” and together with the S&P 500 ETF and NASDAQ-100 ETF, the “Underlying ETFs”). FLEX Options are customizable exchange-traded option contracts guaranteed for settlement by the Options Clearing Corporation. The Fund uses FLEX Options to employ a “defined outcome strategy.” Defined outcome strategies seek to produce pre-determined investment outcomes based upon the performance of an underlying security or index. The pre-determined outcomes sought by the Fund discussed below (the “Outcomes”) are based upon the performance of each Underlying ETF’s share price over successive one-year periods (each, an “Outcome Period”), each of which is expected to begin on the first trading day of October and conclude on the last trading day of the following September. The initial Outcome Period begins on October 1, 2020 and will end on September 30, 2021. The Fund will not terminate after the conclusion of an Outcome Period. After the conclusion of an Outcome Period, another approximately one-year Outcome Period will begin. There is no guarantee that the Outcomes for an Outcome Period will be realized.

|

• |

The Fund’s strategy has been specifically designed to produce the Outcomes over the duration of the Outcome Period. The Outcomes may only be realized by investors that are holding shares of the Fund (“Shares”) at the outset of an Outcome Period and continue to hold them until that Outcome Period concludes. An investor that purchases Shares after an Outcome Period has begun or sells Shares prior to the Outcome Period’s conclusion may experience investment returns very different from those that the Fund seeks to provide. |

|

• |

The Fund has exposure to the S&P 500 ETF, NASDAQ-100 ETF and Russell 2000 ETF. The Fund is not a “leveraged” ETF, which typically seeks to provide a multiple return on a single underlying index. Instead, the Fund’s returns will be based upon the price performance of the S&P 500 ETF’s share price (or its “price return”) over the duration of the Outcome Period, subject to a cap that is detailed below (the “S&P 500 ETF Cap”). In addition, to the extent that the NASDAQ-100 ETF’s or Russell 2000 ETF’s share price increases in value over the duration of the Outcome Period, the Fund’s strategy is designed such that the Fund will experience an increase in value that approximately matches the increase experienced by the NASDAQ-100 ETF and Russell 2000 ETF, as applicable, each subject to a cap that is detailed below (respectively, the “NASDAQ-100 ETF Cap” and “Russell 2000 ETF Cap”, and together with the S&P 500 ETF Cap, the “Underlying ETF Caps”). Therefore, the Fund’s overall performance for an Outcome Period will be the returns provided by its exposure to the S&P 500 ETF, plus the gains (if any) experienced by the NASDAQ-100 ETF and Russell 2000 ETF. There is no guarantee that the Fund will successfully provide the Outcomes. |

|

• |

If the S&P 500 ETF’s share price increases in value over the duration of the Outcome Period, the Fund seeks to provide Fund shareholders that hold Fund Shares for the entire Outcome Period with an increase in value that approximately matches the increase experienced by the S&P 500 ETF, subject to the S&P 500 ETF Cap discussed in greater detail below. If the S&P 500 ETF’s share price decreases in value over the duration of the Outcome Period, the Fund seeks to provide Fund shareholders that hold Fund Shares for the entire Outcome Period with a decrease in value that approximately matches the decrease experienced by the S&P 500 ETF. |

• In addition, at the outset of the Outcome Period, the Fund will also purchase an “at-the-money” call option on both the NASDAQ-100 ETF and Russell 2000 ETF. If either (or both) the NASDAQ-100 ETF’s or Russell 2000 ETF’s share price increases in value over the duration of the Outcome Period, the Fund will exercise the applicable option and will experience an increase in value that approximately matches the increase experienced by the NASDAQ-100 ETF or Russell 2000 ETF, as applicable, over the duration of the Outcome Period. This increase in value will be cumulative with the returns otherwise provided by the Fund’s exposure to the S&P 500 ETF. Any increase in value in the NASDAQ-100 ETF’s or Russell 2000 ETF’s share price will also be subject to the respective NASDAQ-100 ETF Cap and Russell 2000 ETF Cap. If the NASDAQ-100 ETF’s or Russell 2000 ETF’s share price does not increase in value over the duration of the Outcome Period, the Fund will not exercise the applicable option. If neither the NASDAQ-100 ETF’s or Russell 2000 ETF’s share price increase in value over the duration of the Outcome Period, the Fund’s returns for the entirety of the Outcome Period will solely be dictated by the performance of the S&P 500 ETF. The Fund’s net asset value, the per Share value of the Fund’s assets (“NAV”), does not have exposure to any decreases in value experienced by the NASDAQ-100 ETF or Russell 2000 ETF when measured from the beginning to the end of an Outcome Period. However, an investor that purchases Fund Shares during an Outcome Period after the NASDAQ-100 ETF or Russell 2000 ETF has increased in value may be negatively affected by future decreases during the remainder of the Outcome Period. In the event an Outcome Period has begun, and the NASDAQ-100 ETF’s or Russell 2000 ETF’s share price has increased in value, such an increase will be reflected in the value of the Fund’s purchased call option on the NASDAQ-100 ETF and Russell 2000 ETF, as applicable. Accordingly, in the event that the NASDAQ-100 ETF’s or Russell 2000 ETF’s share price were to subsequently decrease in value after a previous increase in its respective value, that decrease would also be reflected in the value of that option, and therefore the Fund’s NAV.

(continued on next page)

(continued from previous page)

|

• |

There is no guarantee that the Outcomes for an Outcome Period will be realized. Additionally, the Outcomes may only be realized by investors that are holding Fund Shares at the outset of an Outcome Period and continue to hold them until that Outcome Period concludes. An investor that purchases Shares after an Outcome Period has begun or sells Shares prior to the Outcome Period’s conclusion may experience investment returns very different from those that the Fund seeks to provide. |

|

• |

The gain or loss experienced by an Underlying ETF is determined by the difference in its share price on the first day of the Outcome Period (when the Fund enters into the FLEX Options) and its share price on the last day of the Outcome Period (when the FLEX Options expire). Fund shareholders will bear all S&P 500 ETF losses on a one-to-one basis over the duration of an Outcome Period. |

|

• |

The extent to which the Fund will participate in gains experienced by the S&P 500 ETF, NASDAQ-100 ETF and Russell 2000 ETF is subject to the S&P 500 ETF Cap, NASDAQ-100 ETF Cap and Russell 2000 ETF Cap, respectively, that each represents the maximum percentage return the Fund can achieve from its FLEX Options that reference the S&P 500 ETF, NASDAQ-100 ETF and Russell 2000 ETF, respectively, for the duration of the Outcome Period. Therefore, even though the Fund’s returns are based upon the performance of each Underlying ETF’s share price, if an Underlying ETF experiences returns for the Outcome Period in excess of its Underlying ETF Cap, the Fund will not experience those excess gains. The sum of the S&P 500 ETF Cap, NASDAQ-100 ETF Cap and Russell 2000 ETF Cap represents the maximum percentage return the Fund itself can experience for the Outcome Period (the “Cumulative Fund Cap”). If the Outcome Period has begun and the Fund has increased in value to a level near to an Underlying ETF Cap, an investor purchasing Fund Shares at that price has little or no ability to achieve gains relating to the Underlying ETF but remains vulnerable to downside risks. There is no guarantee that the Fund will successfully achieve its investment objective. The Underlying ETF Caps and Cumulative Fund Cap may rise or fall from one Outcome Period to the next. |

|

• |

The Outcomes, including each Underlying ETF Cap, are provided prior to taking into account annual Fund management fees equal to 0.79% of the Fund’s daily net assets, transaction fees and any extraordinary expenses incurred by the Fund and will have the effect of reducing each Underlying ETF Cap amount for Fund shareholders. For the purpose of this prospectus, “extraordinary expenses” are non-recurring expenses that may be incurred by the Fund outside of the ordinary course of its business, including, without limitation, costs incurred in connection with any claim, litigation, arbitration, mediation, government investigation or similar proceedings, indemnification expenses and expenses in connection with holding and/or soliciting proxies for a meeting of Fund shareholders. |

|

• |

The Underlying ETF Caps and Cumulative Fund Cap will be determined at the outset of the Outcome Period based upon prevailing market conditions. For the current Outcome Period, the Underlying ETF Caps and Cumulative Fund Cap are set forth below, prior to taking into account any fees or expenses charged to shareholders (based upon the 20 trading days prior to the date of this prospectus). |

• The S&P 500 ETF Cap is expected to be between 6.07% and 10.24%.

• The NASDAQ-100 ETF Cap is expected to be between 6.07% and 10.24%.

• The Russell 2000 ETF Cap is expected to be between 6.07% and 10.24%.

• The Cumulative Fund Cap is expected to be between 18.21% and 30.72%.

When the Fund’s annual Fund management fee of 0.79% of the Fund’s average daily net assets is taken into account, the Underlying ETF Caps and Cumulative Fund Cap are revised downwards accordingly as set forth below (based upon the 20 trading days prior to the date of this prospectus) and will be further reduced by any shareholder transaction fees and any extraordinary expenses incurred by the Fund.

(continued on next page)

(continued from previous page)

• The S&P 500 ETF Cap is expected to be between 5.28% and 9.45%.

• The NASDAQ-100 ETF Cap is expected to be between 5.28% and 9.45%.

• The Russell 2000 ETF Cap is expected to be between 5.28% and 9.45%.

• The Cumulative Fund Cap is expected to be between 15.84% and 28.35%.

The Underlying ETF Caps and Cumulative Fund Cap are based upon prevailing market conditions at the beginning of an Outcome Period and will therefore rise or fall from one Outcome Period to the next.

|

• |

The Outcomes are based on the Fund’s NAV, on the first day of the Outcome Period. The Fund’s assets will be principally composed of FLEX Options, the value of which is derived from the performance of the applicable Underlying ETF’s share price. However, because a component of an option’s value is the number of days remaining until its expiration, the Fund’s NAV will not directly correlate on a day-to-day basis with the returns experienced by the Underlying ETFs. |

• The Fund’s investment sub-adviser generally anticipates that the Fund’s NAV will move in the same direction as the combined performance of the Underlying ETFs. For example, during an Outcome Period, the Fund’s NAV is expected to increase if each Underlying ETF’s share price increases or one or more of the Underlying ETFs’ share price increase offsets any decrease in the other Underlying ETFs. Similarly, during an Outcome Period, the Fund’s NAV is expected to decrease if each Underlying ETF’s share price decreases or one or more of the Underlying ETFs’ share price decrease offsets any increase in the other Underlying ETFs. However, the Fund’s NAV will not directly correlate on a day-to-day basis with the returns experienced by the Underlying ETFs because a component of an Underlying ETF’s value is the number of days remaining until the expiration of the FLEX Options during the Outcome Period. The Fund’s strategy is designed to produce the Outcomes upon the expiration of the FLEX Options on the last day of the Outcome Period. It should not be expected that the Outcomes will be provided at any point prior to that time and there is no guarantee that the Outcomes will be achieved on the last day of the Outcome Period.

|

• |

The Fund’s website, www.innovatoretfs.com/tsoc, provides important Fund information (including Outcome Period start and end dates and information relating to the Underlying ETF Caps and Cumulative Fund Cap), as well information relating to the potential outcomes of an investment in the Fund on a daily basis. |

If you are contemplating purchasing Shares, please visit the website. Investors considering purchasing Shares after the Outcome Period has begun or selling Shares prior to the end of the Outcome Period should visit the website to fully understand potential investment outcomes.

|

• |

As stated above and explained in greater detail within the prospectus, if the Fund has experienced certain levels of gains from the S&P 500 ETF, NASDAQ-100 ETF or Russell 2000 ETF, or losses from the S&P 500 ETF since the beginning of the Outcome Period, there may be little to no ability to achieve gains for the remainder of the Outcome Period. The website contains important information that will assist you in determining whether to buy shares. |

• Although the Fund’s shares are listed for trading on a national securities exchange, there can be no assurance that an active trading market for the shares will develop or be maintained.

Although the Fund seeks to achieve its investment objective, there is no guarantee that it will do so. The returns that the Fund seeks to provide do not include the costs associated with purchasing shares of the Funds and certain expenses incurred by the Fund. The Fund has characteristics unlike many other traditional investment products and may not be suitable for all investors. The table on the following page provides considerations for determining whether an investment in the Fund is appropriate for you.

Investor Suitability Considerations

|

You should only consider this investment if: |

You should not consider this investment if: |

|

• you fully understand the risks inherent in an investment in the Fund; • you desire to invest in a product with a return that depends upon the performance of each Underlying ETF’s share price over the Outcome Period; • you are willing to hold Shares for the duration of the Outcome Period in order to achieve the outcomes that the Fund seeks to provide; • you are willing to forgo some or all of the investment return derived from the Underlying ETFs’ dividend distributions; • you fully understand that investments made when the Fund is at or near an Underlying ETF Cap may have limited to no upside relating to that Underlying ETF; • you are willing to forgo any gains in excess of the Underlying ETF Caps and Cumulative Fund Cap; • you understand that the Fund’s investments do not provide for dividends to the Fund; • you are willing to accept the risk of losing your entire investment; and • you have visited the Fund’s website and understand the investment outcomes available to you based upon the time of your purchase. |

• you do not fully understand the risks inherent in an investment in the Fund; • you do not desire to invest in a product with a return that depends upon the performance of each Underlying ETF’s share price over the Outcome Period; • you are unwilling to hold Shares for the duration of the Outcome Period in order to achieve the outcomes that the Fund seeks to provide; • you are unwilling to forgo some or all of the investment return derived from the Underlying ETFs’ dividend distributions; • you do not fully understand that investments made when the Fund is at or near to an Underlying ETF Cap may have limited to no upside relating to that Underlying ETF; • you are unwilling to forgo any gains in excess of the Underlying ETF Caps and Cumulative Fund Cap; • you do not fully understand that the Fund’s investments do not provide for dividends to the Fund; • you are unwilling to accept the risk of losing your entire investment; and • you have not visited the Fund’s website and do not understand the investment outcomes available to you based upon the timing of your purchase. |

For more information regarding whether an investment

in the Fund is right for you,

please see “Investor Suitability” in the prospectus.

|

Table of Contents

| |

|

|

|

|

Summary Information |

2 |

|

Additional Information About the Fund’s Principal Investment Strategies |

16 |

|

Fund Investments |

18 |

|

Additional Risks of Investing in the Fund |

19 |

|

Investor Suitability |

25 |

|

Management of the Fund |

26 |

|

How to Buy and Sell Shares |

28 |

|

Dividends, Distributions and Taxes |

29 |

|

Distributor |

34 |

|

Net Asset Value |

34 |

|

Fund Service Providers |

36 |

|

Premium/Discount Information |

36 |

|

Investments by Other Investment Companies |

36 |

|

|

Investment Objective

The Fund seeks to provide investors with returns that match those of the SPDR S&P 500 ETF Trust, up to the upside cap of ___% (prior to taking into account management fees and other fees) and ___% (after taking into account management fees and other fees) over the period from October 1, 2020 to September 30, 2021. The Fund also seeks to provide investors with any positive returns of the Invesco QQQ TrustSM, Series 1 and iShares Russell 2000 ETF, up to the upside cap of ___% and ___%, respectively, (prior to taking into account management fees and other fees) and ___% and ___%, respectively, (after taking into account management fees and other fees) over the period from October 1, 2020 to September 30, 2021.

Fees and Expenses of the Fund

This table describes the fees and expenses that you may pay if you buy, hold, and sell shares of the Fund (“Shares”). You may pay other fees, such as brokerage commissions and other fees to financial intermediaries, which are not reflected in the table and example below.

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment)

|

Management Fees |

|

% | ||

|

Distribution and Service (12b-1) Fees |

% | |||

|

Other Expenses(1) |

% | |||

|

Total Annual Fund Operating Expenses |

|

% | ||

|

(1) |

|

Example

This example is intended to help you compare the cost of investing in the Fund with the cost of investing in other funds.

This example assumes that you invest $10,000 in the Fund for the time periods indicated and then sell all of your Shares at the end of those periods. The example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses remain at current levels. This example does not include the brokerage commissions that investors may pay to buy and sell Shares.

|

|

1 Year |

3 Years |

| Although your actual costs may be higher or lower, your costs, based on these assumptions, would be: |

$ |

$ |

Portfolio Turnover

The Fund pays transaction costs, such as commissions, when it purchases and sells securities (or “turns over” its portfolio). A higher portfolio turnover will cause the Fund to incur additional transaction costs and may result in higher taxes when Shares are held in a taxable account. These costs, which are not reflected in Total Annual Fund Operating Expenses or in the example, may affect the Fund’s performance. Because the Fund has not yet commenced investment operations, no portfolio turnover information is available at this time.

Principal Investment Strategies

General Strategy Description The Fund will invest substantially all of its assets in a portfolio of FLexible EXchange® Options (“FLEX Options”) that reference the SPDR® S&P 500® ETF Trust (“S&P 500 ETF”), Invesco QQQ TrustSM, Series 1 (the “NASDAQ-100 ETF”) and the iShares Russell 2000 ETF (the “Russell 2000 ETF,” and together with the S&P 500 ETF and NASDAQ-100 ETF, the “Underlying ETFs”). Each Underlying ETF is an exchange-traded fund registered under the Investment Company Act of 1940 (the “1940 Act”). The S&P 500 ETF seeks to track the investment results of the S&P 500 Index, a large-cap, market-weighted, U.S. equities index that tracks the performance of 500 leading companies in leading industries. The NASDAQ-100 ETF seeks to track the investment results of the NASDAQ-100 Index, a modified market capitalization-weighted index composed of the 100 largest (by market capitalization) domestic and international non-financial companies listed on the NASDAQ Stock Market, LLC. The Russell 2000 ETF seeks to track the investment results of the Russell 2000 Index, an index composed of small-capitalization U.S. equities.

Additional information about the Underlying ETFs is set forth in the section entitled “Additional Information Regarding the Fund’s Principal Investment Strategies.” Due to the unique mechanics of the Fund’s strategy, the return an investor can expect to receive from an investment in the Fund has characteristics that are distinct from many other investment vehicles. It is important that an investor understand these characteristics before making an investment in the Fund.

In general, an option contract is an agreement between a buyer and seller that gives the purchaser of the option the right to buy or sell a particular asset at a specified future date at an agreed upon price. FLEX Options are exchange-traded options contracts with uniquely customizable terms. Although guaranteed for settlement by the Options Clearing Corporation (the “OCC”), FLEX Options are still subject to counterparty risk with the OCC and may be less liquid than more traditional exchange-traded options. Each of the FLEX Options purchased and sold throughout the Outcome Period will have the same terms (i.e., strike price and expiration) as the corresponding FLEX Options purchased and sold at the outset of the Outcome Period. A detailed explanation regarding the terms of the FLEX Options and the mechanics of the Fund’s strategy can be found below and in the section entitled “Additional Information About the Fund’s Principal Investment Strategies.”

The pre-determined outcomes sought by the Fund, which includes the upside return caps discussed below (the “Outcomes”), are based upon the performance of each Underlying ETF’s share price over successive approximately one-year periods (each, an “Outcome Period”). The start and end dates of an Outcome Period correspond to the date on which the Fund entered into the FLEX Options comprising its portfolio and the date on which those FLEX Options expire. Upon the conclusion of the Outcome Period, the Fund will receive the cash value of all the FLEX Options it held for the prior Outcome Period. It will then invest in a new series of FLEX Options with an expiration date in approximately one year, and a new Outcome Period will begin. The initial Outcome Period begins on October 1, 2020 and will conclude on September 30, 2021. Each subsequent Outcome Period is expected to begin on the first trading day of October and conclude on the last trading day of September. The Outcomes may only be realized by investors who continuously hold Shares from the commencement of the Outcome Period until its conclusion. Investors who purchase Shares after the Outcome Period has begun, or sell Shares prior to the Outcome Period’s conclusion, may experience investment returns very different from those that the Fund seeks to provide.

The Outcomes. The Fund seeks to provide returns based upon the price performance of the S&P 500 ETF, up to a cap on upside returns, over the duration of the Outcome Period (the “S&P 500 ETF Returns”). The Fund also seeks to supplement the S&P 500 ETF Returns with any gains experienced by the NASDAQ-100 ETF, up to a cap on upside returns, over the duration of the Outcome Period (the “NASDAQ-100 ETF Returns”) and any gains experienced by the Russell 2000 ETF, up to a cap on upside returns, over the duration of the Outcome Period (the “Russell 2000 ETF Returns”). The Fund seeks to experience performance over the duration of the Outcome Period equal to the sum of the S&P 500 ETF Returns, the NASDAQ-100 ETF Returns and the Russell 2000 ETF Returns. There is no guarantee that the Fund will successfully provide the Outcomes.

S&P 500 ETF Returns. If the S&P 500 ETF’s share price increases in value over the duration of the Outcome Period, the Fund seeks to experience an increase in value that approximately matches the increase experienced by the S&P 500 ETF, subject to an upside return cap discussed in greater detail below. If the S&P 500 ETF’s share price decreases in value over the duration of the Outcome Period, the Fund seeks to experience a decrease in value that approximately matches the decrease experienced by the S&P 500 ETF. The Fund will participate in all S&P 500 ETF losses on a one-to-one basis.

NASDAQ-100 ETF Returns. If the NASDAQ-100 ETF’s share price increases in value over the duration of the Outcome Period, the Fund seeks to experience an increase in value that approximately matches the increase experienced by the NASDAQ-100 ETF, subject to an upside return cap discussed in greater detail below. The Fund’s NAV will not participate in any decreases in value experienced by the NASDAQ-100 ETF when measured from the beginning to the end of the Outcome Period.

Russell 2000 ETF Returns. If the Russell 2000 ETF’s share price increases in value over the duration of the Outcome Period, the Fund seeks to experience an increase in value that approximately matches the increase experienced by the Russell 2000 ETF, subject to an upside return cap discussed in greater detail below. The Fund’s NAV will not participate in any decreases in value experienced by the Russell 2000 ETF when measured from the beginning to the end of the Outcome Period.

If both the NASDAQ-100 ETF’s and Russell 2000 ETF’s share price decreases in value over the course of an entire Outcome Period, the Fund’s overall performance will be approximately the S&P 500 ETF Return for the Outcome Period. For an investor that purchases Fund Shares during an Outcome Period after either the NASDAQ-100 ETF or Russell 2000 ETF has increased in value, in the event that the NASDAQ-100 ETF’s or Russell 2000 ETF’s share price were to subsequently decrease in value after an increase in its respective value, that decrease would also be reflected in the Fund’s NAV.

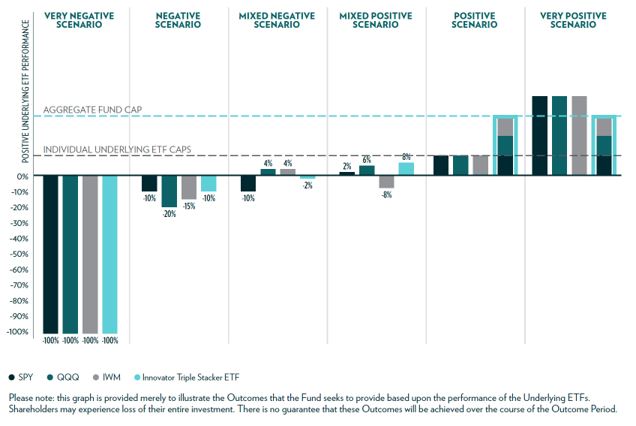

The hypothetical graphical illustration provided below is designed to illustrate the Outcomes based upon the hypothetical performances of the Underlying ETFs for a shareholder that holds Fund Shares for the entirety of the Outcome Period. Additional hypothetical graphical representations of the Outcomes are provided in “Additional Information Regarding the Fund’s Principal Investment Strategies.” There is no guarantee that the Fund will be successful in its attempt to provide the Outcomes for an Outcome Period. The returns that the Fund seeks to provide do not include the costs associated with purchasing shares of the Fund and certain expenses incurred by the Fund.

[Insert chart and accompanying disclosure]

The Outcome Period. The Outcomes sought by the Fund are based upon the Fund’s NAV on the first day of the Outcome Period. The Outcome Period begins on the day the FLEX Options are entered into and ends on the day they expire. Each FLEX Option’s value is ultimately derived from the performance of the applicable Underlying ETF over the duration of the Outcome Period. Because the terms of the FLEX Options don’t change, the Outcomes relate to the Fund’s NAV on the first day of the Outcome Period. A shareholder that purchases Shares after the commencement of the Outcome Period will likely have purchased Shares at a different NAV than the NAV on the first day of the Outcome Period (the NAV upon which the Outcomes are based) and may experience investment outcomes very different from those sought by the Fund. A shareholder that sells Shares prior to the end of the Outcome Period may also experience investment outcomes very different from those sought by the Fund. To achieve the Outcomes sought by the Fund for the Outcome Period, an investor must be holding Shares on the day that the Fund enters into the FLEX Options and on the day those FLEX Options expire. There is no guarantee that the Fund will be successful in its attempt to provide the Outcomes.

The Fund’s assets will be principally composed of FLEX Options, the value of which is derived from the performance of the underlying reference asset, the applicable Underlying ETF’s share price. However, because a component of an option’s value is the number of days remaining until its expiration, during the Outcome Period, the Fund’s NAV will not directly correlate on a day-to-day basis with the returns experienced by the Underlying ETF. While the Fund’s investment sub-advisor generally anticipates that the Fund’s NAV will move in the same direction as the Underlying ETF’s share price. For example, during an Outcome Period, the Fund’s NAV is expected to increase if each Underlying ETF’s share price increases or one or more of the Underlying ETFs’ share price increase offsets any decrease in the other Underlying ETFs. Similarly, during an Outcome Period, the Fund’s NAV is expected to decrease if each Underlying ETF’s share price decreases or one or more of the Underlying ETFs’ share price decrease offsets any increase in the other Underlying ETFs. However, the Fund’s NAV will not directly correlate on a day-to-day basis with the returns experienced by the Underlying ETFs because a component of an Underlying ETF’s value is the number of days remaining until the expiration of the FLEX Options during the Outcome Period. The Fund’s strategy is designed to produce the Outcomes upon the expiration of the FLEX Options on the last day of the Outcome Period and it should not be expected that the Outcomes will be provided at any point prior to that time.

While the Fund will not participate in any NASDAQ-100 ETF or Russell 2000 ETF losses when measured from the beginning to the end of an Outcome Period as whole, a decrease in the value of the NASDAQ-100 ETF’s or Russell 2000 ETF’s share price may cause a decrease in the Fund’s NAV while an Outcome Period is on-going. In the event an Outcome Period has begun, and the NASDAQ-100 ETF’s or Russell 2000 ETF’s share price has increased in value, such an increase will be reflected in the value of the Fund’s purchased call option on the NASDAQ-100 ETF or Russell 2000 ETF, as applicable. Accordingly, in the event that the NASDAQ-100 ETF’s or Russell 2000 ETF’s share price were to subsequently decrease in value, that decrease would also be reflected in the value of that option, and therefore the Fund’s NAV. An investor that purchases Fund Shares after the NASDAQ-100 ETF or Russell 2000 ETF has increased in value may be negatively affected by future decreases.

Upside Return Caps. The extent to which the Fund will participate in gains experienced by the S&P 500 ETF, NASDAQ-100 ETF and Russell 2000 ETF is subject to an upside return cap (the “S&P 500 ETF Cap,” “NASDAQ-100 ETF Cap” and “Russell 2000 ETF Cap,” respectively, and together, the “Underlying ETF Caps”) that each represents the maximum percentage return the Fund can achieve from its FLEX Options that reference the S&P 500 ETF, NASDAQ-100 ETF and Russell 2000 ETF, respectively, for the duration of the Outcome Period. Therefore, even though the Fund’s returns are based upon the performance of each Underlying ETF’s share price, if an Underlying ETF experiences returns for the Outcome Period in excess of its Underlying ETF Cap, the Fund will not experience those excess gains. The sum of the S&P 500 ETF Cap, NASDAQ-100 ETF Cap and Russell 2000 ETF Cap represents the maximum percentage return the Fund itself can experience for the Outcome Period (the “Cumulative Fund Cap”). The Underlying ETF Caps and Cumulative Fund Cap should be considered before investing in the Fund. If an investor is considering purchasing Shares during the Outcome Period, and the Fund has already increased in value to a level near to the Cumulative Fund Cap, an investor purchasing Shares at that price has limited to no gains available for the remainder of the Outcome Period but remains vulnerable to significant downside risks. The Underlying ETF Caps and Cumulative Fund Cap may rise or fall from one Outcome Period to the next.

The Underlying ETF Caps and Cumulative Fund Cap will be determined on the first day of the Outcome Period based upon prevailing market conditions. For the current Outcome Period, the Underlying ETF Caps and Cumulative Fund Cap are set forth below, prior to taking into account any fees or expenses charged to shareholders (based upon the 20 trading days prior to the date of this prospectus).

• The S&P 500 ETF Cap is expected to be between 6.07% and 10.24%.

• The NASDAQ-100 ETF Cap is expected to be between 6.07% and 10.24%.

• The Russell 2000 ETF Cap is expected to be between 6.07% and 10.24%.

• The Cumulative Fund Cap is expected to be between 18.21% and 30.72%.

When the Fund’s annual Fund management fee of 0.79% of the Fund’s average daily net assets is taken into account, the Underlying ETF Caps and Cumulative Fund Cap are revised downwards accordingly as set forth below (based upon the 20 trading days prior to the date of this prospectus) and will be further reduced by any shareholder transaction fees and any extraordinary expenses incurred by the Fund.

• The S&P 500 ETF Cap is expected to be between 5.28% and 9.45%.

• The NASDAQ-100 ETF Cap is expected to be between 5.28% and 9.45%.

• The Russell 2000 ETF Cap is expected to be between 5.28% and 9.45%.

• The Cumulative Fund Cap is expected to be between 15.84% and 28.35%.

The occurrence of the Underlying ETF Caps (and therefore, the Cumulative Fund Cap, which is the sum of the Underlying ETF Caps) is a result of the design of the Fund’s principal investment strategy and the properties of the FLEX Options that comprise its portfolio. In order to provide participation in the return of the S&P 500 ETF, the Fund, at the outset of the Outcome Period, purchases a call option on the S&P 500 ETF with a strike price putting the option already deeply “in-the-money.” As a purchaser of a call option, the Fund is obligated to pay a premium to the seller. However, because the Fund’s principal investment strategy is designed so that all premiums that the Fund must pay in connection with its FLEX Options positions must be offset by premiums it receives in connection with its FLEX Options positions, the Fund will sell a call option entitling the Fund to receive a premium equal to the premium it must pay in connection with its purchased call option. The strike price of this FLEX Option relative to the S&P 500 ETF’s share price determines the S&P 500 ETF Cap.

At the outset of the Outcome Period, the Fund also purchases a call option on the NASDAQ-100 ETF and Russell 2000 ETF with a strike price approximately equal to the NASDAQ-100 ETF’s or Russell 2000 ETF’s share price, as applicable, at the outset of the Outcome Period. If the NASDAQ-100 ETF’s or Russell 2000 ETF’s share price increases in value over the duration of the Outcome Period, the Fund will exercise the option and realize a gain approximately equal to the difference in the value of the NASDAQ-100 ETF’s or Russell 2000 ETF’s share price, as applicable, at the outset of the Outcome Period and the value of its share price at the conclusion of the Outcome Period. If the NASDAQ-100 ETF’s or Russell 2000 ETF’s share price decreases in value, the Fund will not exercise the applicable option and it will expire worthless. This is the mechanism by which the Fund participates in any gains experienced by the NASDAQ-100 ETF and Russell 2000 ETF, but will not participate in losses experienced by the NASDAQ-100 ETF or Russell 2000 ETF, when measured from the beginning to the end of the Outcome Period. However, as a purchaser of a call option, the Fund is obligated to pay a premium to the seller. Because the Fund’s principal investment strategy is designed so that all premiums that the Fund must pay in connection with its FLEX Options positions must be offset by premiums it receives in connection with its FLEX Options positions, the Fund will sell a call option entitling the Fund to receive a premium equal to the premium it must pay in connection with its purchased call option. The strike price of this FLEX Option relative to the NASDAQ-100 ETF’s or Russell 2000 ETF’s share price, as applicable, determines the applicable Underlying ETF Cap.

Fund Rebalance. The Fund is a continuous investment vehicle. It does not terminate and distribute its assets at the conclusion of each Outcome Period. On the termination date of an Outcome Period, the Sub-Adviser will invest in a new set of FLEX Options and another Outcome Period will commence.

Approximately one week prior to the end of each Outcome Period, the Fund will file a prospectus supplement, which will alert existing shareholders that an Outcome Period is approaching its conclusion and disclose the anticipated ranges for the Fund’s Underlying ETF Caps and Cumulative Fund Cap for the next Outcome Period. Following the close of business on the last day of the Outcome Period, the Fund will file a prospectus supplement that discloses the Fund’s final Underlying ETF Caps and Cumulative Fund Cap (both gross and net of the unitary management fee) for the next Outcome Period. This information will be available on the Fund’s website, www.innovatoretfs.com/tsoc, which also provides information relating to the Outcomes, including the Fund’s position relative to the Underlying ETF Caps and Cumulative Fund Cap, of an investment in the Fund on a daily basis.

The Fund is classified as “non-diversified” under the Investment Company Act of 1940, as amended (the “1940 Act”).

Principal Risks

Capped Upside Return Risk. The Fund’s strategy seeks to provide returns that are subject to the Underlying ETF Caps and Cumulative Fund Cap. In the event that an Underlying ETF experiences gains in excess of its applicable Underlying ETF Cap over the duration of the Outcome Period, the Fund will not participate in those excess gains. Because the Fund’s strategy provides capped exposure to three Underlying ETFs, the Underlying ETF Caps (and thus the Cumulative Fund Cap) may be lower than if the Fund provided capped exposure to only a single reference asset. The Fund’s strategy seeks to provide the Outcomes if Shares are bought on the day on which the Fund enters into the FLEX Options and held until those FLEX Options expire at the end of the Outcome Period. In the event an investor purchases Shares after the date on which the FLEX Options were entered into and the Fund has risen in value to a level near to an Underlying ETF Cap, there may be little or no ability for that investor to experience an investment gain on their Shares relating to that Underlying ETF.

FLEX Options Risk. The Fund will utilize FLEX Options issued and guaranteed for settlement by the OCC. The Fund bears the risk that the OCC will be unable or unwilling to perform its obligations under the FLEX Options contracts. In the unlikely event that the OCC becomes insolvent or is otherwise unable to meet its settlement obligations, the Fund could suffer significant losses. Additionally, FLEX Options may be less liquid than certain other securities such as standardized options. In less liquid market for the FLEX Options, the Fund may have difficulty closing out certain FLEX Options positions at desired times and prices. The Fund may experience substantial downside from specific FLEX Option positions and certain FLEX Option positions may expire worthless.

FLEX Options Performance Risk. The Fund’s overall performance will be based upon the price returns of multiple Underlying ETFs, subject to each Underlying ETF Cap. During an Outcome Period, in the event each Underlying ETF’s share price increases, or one or more Underlying ETFs’ share price increase offsets any decrease in the other Underlying ETFs, the Fund’s NAV is expected to increase. Similarly, during an Outcome Period, if each Underlying ETF’s share price decreases, or one or more Underlying ETF’s share price decrease offsets any increase in the other Underlying ETFs, the Fund’s NAV is expected to decrease. The value of the underlying FLEX Options will be affected by, among others, changes in an Underlying ETF’s share price, changes in interest rates, changes in the actual and implied volatility of an Underlying ETF, and the remaining time to until the FLEX Options expire. The value of the FLEX Options will likely not increase or decrease at the same rate as an Underlying ETF’s share price on a day-to-day basis (although they generally move in the same direction). As such, the Fund’s NAV will likely not increase or decrease at the same rate as the Underlying ETFs’ cumulative returns on a day-to-day basis. However, as a FLEX Option approaches its expiration date, its value typically increasingly moves with the value of an Underlying ETF.

Clearing Member Default Risk. Transactions in some types of derivatives, including FLEX Options, are required to be centrally cleared. In a transaction involving such derivatives (“cleared derivatives”), the Fund’s counterparty is a clearing house, such as the OCC, rather than a bank or broker. Since the Fund is not a member of clearing houses and only members of a clearing house (“clearing members”) can participate directly in the clearing house, the Fund will hold cleared derivatives through accounts at clearing members. In cleared derivatives positions, the Fund will make payments (including margin payments) to and receive payments from a clearing house through their accounts at clearing members. Customer funds held at a clearing organization in connection with any options contracts are held in a commingled omnibus account and are not identified to the name of the clearing member’s individual customers. As a result, assets deposited by the Fund with any clearing member as margin for FLEX Options may, in certain circumstances, be used to satisfy losses of other clients of the Fund’s clearing member. In addition, although clearing members guarantee performance of their clients’ obligations to the clearing house, there is a risk that the assets of the Fund might not be fully protected in the event of the clearing member’s bankruptcy, as the Fund would be limited to recovering only a pro rata share of all available funds segregated on behalf of the clearing member’s customers for the relevant account class.

Outcome Period Risk. The Fund’s investment strategy is designed to deliver the Outcomes if Shares are bought on the day on which the Fund enters into the FLEX Options and held until those FLEX Options expire at the end of the Outcome Period. In the event an investor purchases Shares after the date on which the FLEX Options were entered into or sells Shares prior to the expiration of the FLEX Options, the returns realized by the investor will not match those that the Fund seeks to achieve.

Correlation Risk. The FLEX Options held by the Fund will be exercisable at the strike price only on their expiration date. Prior to the expiration date, the value of the FLEX Options will be determined based upon market quotations or using other recognized pricing methods. The value of the FLEX Options prior to the expiration date may vary because of related factors other than the value of the Underlying ETFs. Factors that may influence the value of the FLEX Options include interest rate changes and implied volatility levels of an Underlying ETF, among others.

Investment Objective Risk. Certain circumstances under which the Fund might not achieve its objective include, but are not limited, to (i) if the Fund disposes of FLEX Options, (ii) if the Fund is unable to maintain the proportional relationship based on the number of FLEX Options in the Fund’s portfolio, (iii) significant accrual of Fund expenses in connection with effecting the Fund’s principal investment strategy or (iv) adverse tax law changes affecting the treatment of FLEX Options.

Upside Participation Risk. There can be no guarantee that the Fund will be successful in its strategy to provide shareholders with a total return that matches the increase in value experienced by the Underlying ETFs over the duration of the Outcome Period, subject to the Underlying ETF Caps. In the event an investor purchases Shares after the FLEX Options were entered into or does not stay invested in the Fund for the entirety of the Outcome Period, the returns realized by the investor may not match those that the Fund seeks to achieve.

Management Risk. The Fund is subject to management risk because it is an actively managed portfolio. The Sub-Adviser will apply investment techniques and risk analyses in making investment decisions for the Fund, but there can be no guarantee that the Fund will meet its investment objective.

Cap Change Risk. The Underlying ETF Caps and Cumulative Fund Cap are established at the beginning of each Outcome Period and are dependent on prevailing market conditions. As such, an Underlying ETF Cap (and thus the Cumulative Fund Cap) may rise or fall from one Outcome Period to the next and is unlikely to remain the same for consecutive Outcome Periods.

Market Risk. The Fund could lose money over short periods due to short-term market movements and over longer periods during more prolonged market downturns. Assets may decline in value due to factors affecting financial markets generally or particular asset classes or industries represented in the markets. The value of a FLEX Options or other asset may also decline due to general market conditions, economic trends or events that are not specifically related to the issuer of the security or other asset, or due to factors that affect a particular issuer or issuers, country, group of countries, region, market, industry, group of industries, sector or asset class. During a general market downturn, multiple asset classes may be negatively affected. Changes in market conditions and interest rates will not have the same impact on all types of securities.

Non-Diversification Risk.

Liquidity Risk. In the event that trading in the underlying FLEX Options is limited or absent, the value of the Fund’s FLEX Options may decrease. There is no guarantee that a liquid secondary trading market will exist for the FLEX Options. The trading in FLEX Options may be less deep and liquid than the market for certain other securities. FLEX Options may be less liquid than certain non-customized options. In a less liquid market for the FLEX Options, terminating the FLEX Options may require the payment of a premium or acceptance of a discounted price and may take longer to complete. In a less liquid market for the FLEX Options, the liquidation of a large number of options may more significantly impact the price. A less liquid trading market may adversely impact the value of the FLEX Options and the value of your investment.

Valuation Risk. During periods of reduced market liquidity or in the absence of readily available market quotations for the holdings of the Fund, the ability of the Fund to value the FLEX Options becomes more difficult and the judgment of the Fund’s investment adviser (employing the fair value procedures adopted by the Board of Trustees of the Trust may play a greater role in the valuation of the Fund’s holdings due to reduced availability of reliable objective pricing data. Consequently, while such determinations may be made in good faith, it may nevertheless be more difficult for the Fund to accurately assign a daily value.

Operational Risk. The Fund is exposed to operational risks arising from a number of factors, including, but not limited to, human error in the calculation of the Underlying ETF Caps and Cumulative Fund Cap, processing and communication errors, errors of the Fund’s service providers, counterparties or other third-parties, failed or inadequate processes and technology or systems failures. The Fund and its investment adviser and Sub-adviser seek to reduce these operational risks through controls and procedures. However, these measures do not address every possible risk and may be inadequate to address these risks.

Market Maker Risk. If the Fund has lower average daily trading volumes, it may rely on a small number of third-party market makers to provide a market for the purchase and sale of Shares. Any trading halt or other problem relating to the trading activity of these market makers could result in a dramatic change in the spread between the Fund’s NAV and the price at which the Shares are trading on the Exchange, which could result in a decrease in value of the Shares. In addition, decisions by market makers or authorized participants to reduce their role or step away from these activities in times of market stress could inhibit the effectiveness of the arbitrage process in maintaining the relationship between the underlying values of the Fund’s portfolio securities and the Fund’s market price. This reduced effectiveness could result in Shares trading at a discount to NAV and also in greater than normal intra-day bid-ask spreads for Shares.

Trading Issues Risk. Although the Shares are listed for trading on the Exchange, there can be no assurance that an active trading market for such Shares will develop or be maintained. Trading in Shares on the Exchange may be halted due to market conditions or for reasons that, in the view of the Exchange, make trading in Shares inadvisable. In addition, trading in Shares on the Exchange is subject to trading halts caused by extraordinary market volatility pursuant to the Exchange “circuit breaker” rules. Market makers are under no obligation to make a market in the Shares, and authorized participants are not obligated to submit purchase or redemption orders for Creation Units. There can be no assurance that the requirements of the Exchange necessary to maintain the listing of the Fund will continue to be met or will remain unchanged. Initially, due to the small asset size of the Fund, it may have difficulty maintaining its listings on the Exchange.

Active Markets Risk. Although the Shares are listed for trading on the Exchange, there can be no assurance that an active trading market for the Shares will develop or be maintained. Shares trade on the Exchange at market prices that may be below, at or above the Fund’s NAV. Securities, including the Shares, are subject to market fluctuations and liquidity constraints that may be caused by such factors as economic, political, or regulatory developments, changes in interest rates, and/or perceived trends in securities prices. Shares of the Fund could decline in value or underperform other investments.

Authorized Participation Concentration Risk. Only an authorized participant may engage in creation or redemption transactions directly with the Fund. The Fund has a limited number of institutions that may act as authorized participants on an agency basis (i.e., on behalf of other market participants). To the extent that authorized participants exit the business or are unable to proceed with creation and/or redemption orders with respect to the Fund and no other authorized participant is able to step forward to create or redeem “Creation Units” (as defined in “Purchase and Sale of Shares,”) Shares may be more likely to trade at a premium or discount to NAV and possibly face trading halts and/or delisting.

Counterparty Risk. Counterparty risk is the risk an issuer, guarantor or counterparty of a security in the Fund is unable or unwilling to meet its obligation on the security. The OCC acts as guarantor and central counterparty with respect to the FLEX Options. As a result, the ability of the Fund to meet its objective depends on the OCC being able to meet its obligations. In the unlikely event that the OCC becomes insolvent or is otherwise unable to meet its settlement obligations, the Fund could suffer significant losses.

Fluctuation of Net Asset Value Risk. The Fund’s Shares trade on the Exchange at their market price rather than their NAV. The market price may be at, above or below the Fund’s NAV. Differences in market price and NAV may be due, in large part, to the fact that supply and demand forces at work in the secondary trading market for Shares will be closely related to, but not identical to, the same forces influencing the prices of the holdings of the Fund trading individually or in the aggregate at any point in time. These differences can be especially pronounced during times of market volatility or stress. During these periods, the demand for Shares may decrease considerably and cause the market price of Shares to deviate significantly from the Fund’s NAV.

Cash Transactions Risk. The Fund intends to effectuate creations and redemptions for cash, rather than in-kind securities. As a result, an investment in the Fund may be less tax-efficient than an investment in an exchange-traded fund (“ETF”) that effects its creations and redemption for in-kind securities. Because the Fund will effect redemptions for cash, it may be required to sell portfolio securities in order to obtain the cash needed to distribute redemption proceeds. A sale of Shares may result in capital gains or losses and may also result in higher brokerage costs. Consequently, an investment in the Fund may be less tax-efficient than investments in other ETFs. Moreover, cash transactions may have to be carried out over several days if the securities market is relatively illiquid and may involve considerable brokerage fees and taxes. These brokerage fees and taxes, which will be higher than if the Fund sold and redeemed its shares principally in-kind, will be passed on to purchasers and redeemers of Shares in the form of creation and redemption transaction fees. In addition, these factors may result in wider spreads between the bid and the offered prices of Shares than for other ETFs.

Cyber Security Risk. As the use of Internet technology has become more prevalent in the course of business, the investment industry has become more susceptible to potential operational risks through breaches in cyber security. A breach in cyber security refers to both intentional and unintentional events that may cause the Fund to lose proprietary information, suffer data corruption or lose operational capacity. Such events could cause the Fund to incur regulatory penalties, reputational damage, additional compliance costs associated with corrective measures and/or financial loss. Cyber security breaches may involve unauthorized access to the Fund’s digital information systems through “hacking” or malicious software coding, but may also result from outside attacks such as denial-of-service attacks through efforts to make network services unavailable to intended users. In addition, cyber security breaches of the Fund’s third-party service providers, such as its administrator, transfer agent, custodian, or issuers in which the Fund invests, can also subject the Fund to many of the same risks associated with direct cyber security breaches. The Fund has established risk management systems designed to reduce the risks associated with cyber security. However, there is no guarantee that such efforts will succeed, especially because the Fund does not directly control the cyber security systems of issuers or third-party service providers.

Tax Risk. The Fund intends to elect and to qualify each year to be treated as a regulated investment company (“RIC”) under Subchapter M of the Code. However, the federal income tax treatment of certain aspects of the proposed operations of the Fund are not entirely clear. This includes the tax aspects of the Fund’s options strategy, its hedging strategy, the possible application of the “straddle” rules, and various loss limitation provisions of the Code. If, in any year, the Fund fails to qualify as a RIC under the applicable tax laws, the Fund would be taxed as an ordinary corporation. Certain options on an ETF may not qualify as “Section 1256 contracts” under Section 1256 of the Code, and disposition of such options will likely result in short-term or long-term capital gains or losses depending on the holding period. The Fund intends to treat any income it may derive from the FLEX Options as “qualifying income” under the provisions of the Code applicable to RICs. In addition, based upon language in the legislative history, the Fund intends to treat the issuer of the FLEX Options as the referenced asset, which, assuming the referenced asset qualifies as a RIC, would allow the Fund to qualify for special rules in the RIC diversification requirements. If the income is not qualifying income or the issuer of the FLEX Options is not appropriately the referenced asset, the Fund could lose its own status as a RIC. In the event that a shareholder purchases Shares of the Fund shortly before a distribution by the Fund, the entire distribution may be taxable to the shareholder even though a portion of the distribution effectively represents a return of the purchase price.

The Shares will change in value, and you could lose money by investing in the Fund. The Fund may not achieve its investment objective.

Performance

Management

Investment Adviser

Innovator Capital Management, LLC (“Innovator” or the “Adviser”)

Investment Sub-Adviser

Milliman Financial Risk Management LLC (“Milliman” or the “Sub-Adviser”)

Portfolio Managers

The following persons serve as portfolio managers of the Fund.

|

• |

Robert T. Cummings, Principal and Director of Global Trading at Milliman |

|

• |

Daniel S. Hare, Senior Trader and Risk Manager at Milliman |

Each of the portfolio managers is primarily and jointly responsible for the day-to-day management of the Fund and has served in such capacity since the Fund’s inception in 2020.

Purchase and Sale of Shares

The Fund issues and redeems Shares at NAV only with authorized participants (“APs”) that have entered into agreements with the Fund’s distributor and only in Creation Units (large blocks of 25,000 Shares) or multiples thereof (“Creation Unit Aggregations”), in exchange for cash. Except when aggregated in Creation Units, the Shares are not redeemable securities of the Fund.

Individual Shares may only be bought and sold in the secondary market (i.e., on a national securities exchange) through a broker or dealer at a market price. Because the Shares trade at market prices rather than NAV, Shares may trade at a price greater than NAV (at a premium), at NAV, or less than NAV (at a discount). An investor may incur costs attributable to the difference between the highest price a buyer is willing to pay to purchase Shares (bid) and the lowest price a seller is willing to accept for Shares (ask) when buying or selling shares in the secondary market (the “bid-ask spread”).

Recent information, including information on the Fund’s NAV, market price, premiums and discounts, and bid-ask spreads, is available online at www.innovatoretfs.com.

Tax Information

The Fund’s distributions will generally be taxable as ordinary income, returns of capital or capital gains. A sale of Shares may result in capital gain or loss.

Payments to Broker-Dealers and Other Financial Intermediaries

If you purchase Shares through a broker-dealer or other financial intermediary (such as a bank), Innovator and Foreside Fund Services, LLC, the Fund’s distributor, may pay the intermediary for the sale of Shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

Additional Information About the Fund’s Principal Investment Strategies

The Fund seeks to provide returns based upon the price performance of the S&P 500 ETF over the duration of the Outcome Period, subject to the S&P 500 ETF Cap described below. These returns will be supplemented by any gains experienced by the NASDAQ-100 ETF and Russell 2000 ETF, up to the NASDAQ-100 ETF Cap and Russell 2000 Cap on upside returns described below, over the duration of the Outcome Period. There is no guarantee that the Fund will successfully provide the Outcomes. The extent to which the Fund will participate in gains experienced by the Underlying ETFs will be subject to the Underlying ETF Caps. The Underlying ETF Caps and Cumulative Fund Cap are provided prior to taking into account annual Fund management fees equal to 0.79% of the Fund’s daily net assets, transaction fees and any extraordinary expenses incurred by the Fund. Such expenses will reduce the Underlying ETF Caps and Cumulative Fund Cap. There is no guarantee that the Fund will be successful in its attempt to provide the Outcomes.

The S&P 500 ETF is a registered investment company that seeks to provide investment results that, before expenses, correspond generally to the price and yield performance of the S&P 500 Index. The S&P 500 Index is a large-cap, market-weighted, U.S. equities index that tracks the price (excluding dividends) of the 500 leading companies in leading industries. The S&P 500 Price Index is rebalanced quarterly in March, June, September and December.

The NASDAQ-100 ETF is a registered investment company that seeks to provide investment results that, before expenses, correspond generally to the price and yield performance of the NASDAQ-100 Index. The NASDAQ-100 Index includes 100 of the largest domestic and international non-financial companies listed on the NASDAQ Stock Market based on market capitalization. The NASDAQ-100 Index reflects companies across major industry groups including computer hardware and software, telecommunications, retail/wholesale trade and biotechnologies. It does not contain securities of financial companies including investment companies. Except under extraordinary circumstances that may prompt an interim evaluation, the NASDAQ-100 Index composition is reviewed on an annual basis.

The Russell 2000 ETF is a registered investment company that seeks to provide investment results that, before expenses, correspond generally to the price and yield performance of the Russell 2000 Index. The Russell 2000 Index The Russell 2000 Index is a float-adjusted capitalization-weighted index of equity securities issued by the approximately 2,000 smallest issuers in the Russell 3000 Index. The Russell 2000 Index measures the performance of the small-capitalization sector of the U.S. equity market, as defined by FTSE Russell. The Russell 2000 Index is a subset of the Russell 3000 Index, which measures the performance of the broad U.S. equity market, as defined by FTSE Russell. The Russell 2000 Index is reconstituted on an annual basis

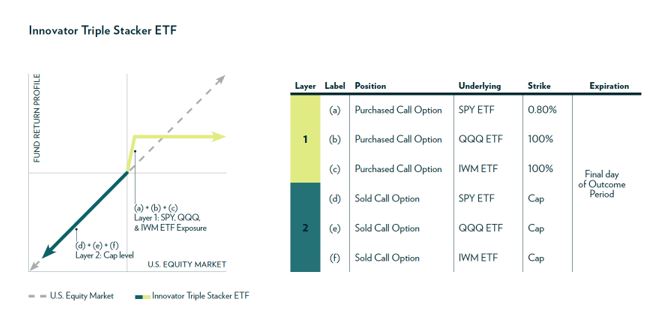

In general, an option contract is an agreement between a buyer and seller that gives the purchaser of the option the right to buy or sell a particular asset at a specified future date at an agreed upon price (commonly known as the “strike price”). FLEX Options are exchange-traded options contracts with uniquely customizable terms. Each FLEX Option that the Fund enters into references the applicable Underlying ETF and expires on the last day of the Outcome Period. The FLEX Options, however, have varying strike prices. The layering of these FLEX Options with varying strike prices provides the mechanism for producing the Fund’s desired outcome. The Fund has two main layers of FLEX Options as set forth below.

|

● |

Position (a) provides participation in the increases or decreases in the value of the S&P 500 ETF’s share price. At its expiration, this deeply in-the-money call option will realize a value approximately equal to that of the S&P 500 ETF’s share price. |

|

● |

Position (b) provides upside exposure to the increase in value (if any) of the NASDAQ-100 ETF’s share price. |

|

● |

Position (c) provides upside exposure to the increase in value (if any) of the Russell 2000 ETF’s share price. |

|

● |

The strike price of position (d) produces the S&P 500 ETF Cap. |

|

● |

The strike price of position (e) produces the NASDAQ-100 ETF Cap. |

|

● |

The strike price of position (f) produces the Russell 2000 ETF Cap. |

As described on the cover of this prospectus, in “Principal Investment Strategies” and in “Principal Risks,” there are risks associated with an investment in the Fund and there is no guarantee the Fund achieve the Outcomes it seeks to provide. The Fund’s unique characteristics (i.e., the imperative of holding Shares for the entire Outcome Period and the Underlying ETF Caps and Cumulative Fund Cap) distinguish it from other investment products and may make it an unsuitable some investors. To help decide whether an investment in the Fund is appropriate based upon individual circumstances, please see the section of this prospectus entitled “Investor Suitability.”

The Fund’s investment objective may be changed by the Board of Trustees of the Trust (the “Board”) without shareholder approval. Additionally, the Fund may liquidate and terminate at any time without shareholder approval.

Fund Investments

Principal Investments

FLEX Options

FLEX Options are customized option contracts that trade on an exchange but provide investors with the ability to customize key contract terms like strike price, style and expiration date while achieving price discovery in competitive, transparent auctions markets and avoiding the counterparty exposure of over-the-counter options positions. Like traditional exchange-traded options, FLEX Options are guaranteed for settlement by the OCC, a market clearinghouse that guarantees performance by counterparties to certain derivatives contracts.

The FLEX Options in which the Fund will invest are all European style options (options that are exercisable only on the expiration date).

The Fund will purchase and sell call and put FLEX Options. In general, put options give the holder (i.e., the buyer) the right to sell an asset (or deliver the cash value of the index, in case of an index put option) and the seller (i.e., the writer) of the put has the obligation to buy the asset (or receive cash value of the index, in case of an index put option) at a certain defined price. Call options give the holder (i.e., the buyer) the right to buy an asset (or receive cash value of the index, in case of an index call option) and the seller (i.e., the writer) the obligation to sell the asset (or deliver cash value of the index, in case of an index call option) at a certain defined price.

The Fund will use the market value of its derivatives holdings for the purpose of determining compliance with the 1940 Act and the rules promulgated thereunder. Since the FLEX Options held by the Fund are exchange-traded, these will be valued on a mark-to-market basis. In the event market prices are not available, the Fund will use fair value pricing.

Non-Principal Investments

Cash Equivalents and Short-Term Investments

The Fund may invest in securities with maturities of less than one year or cash equivalents, or it may hold cash. The percentage of the Fund invested in such holdings varies and depends on several factors, including market conditions.

Traditional Options Contracts

Options contracts on an index give one party the right to receive or deliver cash value of the particular index, and another party the obligation to receive or deliver the cash value of that index. Option contracts on an individual security such as an ETF give one party the right to buy or sell the particular security, and another party the obligation to sell or buy that same security. Many options are exchange-traded and are available to investors with set or defined contract terms.

Disclosure of Portfolio Holdings

A description of the Trust’s policies and procedures with respect to the disclosure of the Fund’s portfolio holdings is available in the Fund’s SAI, which is available at www.innovatoretfs.com.

Additional Risks of Investing in the Fund

Risk is inherent in all investing. Investing in the Fund involves risk, including the risk that you may lose all or part of your investment. There can be no assurance that the Fund will meet its stated objective. Before you invest, you should consider the following supplemental disclosure pertaining to the Principal Risks set forth above as well as additional Non-Principal Risks set forth below in this prospectus.

Principal Risks

Capped Upside Return Risk. The Fund’s strategy seeks to provide returns that are subject to the Underlying ETF Caps and Cumulative Fund Cap. In the event that an Underlying ETF experiences gains in excess of its applicable Underlying ETF Cap over the duration of the Outcome Period, the Fund will not participate in those excess gains. Because the Fund’s strategy provides capped exposure to three Underlying ETFs, the Underlying ETF Caps (and thus the Cumulative Fund Cap) may be lower than if the Fund provided capped exposure to only a single reference asset. The Fund’s strategy seeks to provide the Outcomes if Shares are bought on the day on which the Fund enters into the FLEX Options and held until those FLEX Options expire at the end of the Outcome Period. In the event an investor purchases Shares after the date on which the FLEX Options were entered into and the Fund has risen in value to a level near to an Underlying ETF Cap, there may be little or no ability for that investor to experience an investment gain on their Shares relating to that Underlying ETF.

FLEX Options Risk. The Fund will utilize FLEX Options issued and guaranteed for settlement by the OCC. The Fund bears the risk that the OCC will be unable or unwilling to perform its obligations under the FLEX Options contracts. In the unlikely event that the OCC becomes insolvent or is otherwise unable to meet its settlement obligations, the Fund could suffer significant losses. Additionally, FLEX Options may be less liquid than certain other securities such as standardized options. In less liquid market for the FLEX Options, the Fund may have difficulty closing out certain FLEX Options positions at desired times and prices. The Fund may experience substantial downside from specific FLEX Option positions and certain FLEX Option positions may expire worthless.

FLEX Options Performance Risk. The Fund’s overall performance will be based upon the price returns of multiple Underlying ETFs, subject to each Underlying ETF Cap. During an Outcome Period, in the event each Underlying ETF’s share price increases, or one or more Underlying ETFs’ share price increase offsets any decrease in the other Underlying ETFs, the Fund’s NAV is expected to increase. Similarly, during an Outcome Period, if each Underlying ETF’s share price decreases, or one or more Underlying ETF’s share price decrease offsets any increase in the other Underlying ETFs, the Fund’s NAV is expected to decrease. The value of the underlying FLEX Options will be affected by, among others, changes in an Underlying ETF’s share price, changes in interest rates, changes in the actual and implied volatility of an Underlying ETF, and the remaining time to until the FLEX Options expire. The value of the FLEX Options will likely not increase or decrease at the same rate as an Underlying ETF’s share price on a day-to-day basis (although they generally move in the same direction). As such, the Fund’s NAV will likely not increase or decrease at the same rate as the Underlying ETFs’ cumulative returns on a day-to-day basis. However, as a FLEX Option approaches its expiration date, its value typically increasingly moves with the value of an Underlying ETF.

Clearing Member Default Risk. Transactions in some types of derivatives, including FLEX Options, are required to be centrally cleared. In a transaction involving such derivatives (“cleared derivatives”), the Fund’s counterparty is a clearing house, such as the OCC, rather than a bank or broker. Since the Fund is not a member of clearing houses and only members of a clearing house (“clearing members”) can participate directly in the clearing house, the Fund will hold cleared derivatives through accounts at clearing members. In cleared derivatives positions, the Fund will make payments (including margin payments) to and receive payments from a clearing house through their accounts at clearing members. Customer funds held at a clearing organization in connection with any options contracts are held in a commingled omnibus account and are not identified to the name of the clearing member’s individual customers. As a result, assets deposited by the Fund with any clearing member as margin for FLEX Options may, in certain circumstances, be used to satisfy losses of other clients of the Fund’s clearing member. In addition, although clearing members guarantee performance of their clients’ obligations to the clearing house, there is a risk that the assets of the Fund might not be fully protected in the event of the clearing member’s bankruptcy, as the Fund would be limited to recovering only a pro rata share of all available funds segregated on behalf of the clearing member’s customers for the relevant account class.

Outcome Period Risk. The Fund’s investment strategy is designed to deliver the Outcomes if Shares are bought on the day on which the Fund enters into the FLEX Options and held until those FLEX Options expire at the end of the Outcome Period. In the event an investor purchases Shares after the date on which the FLEX Options were entered into or sells Shares prior to the expiration of the FLEX Options, the returns realized by the investor will not match those that the Fund seeks to achieve.

Correlation Risk. The FLEX Options held by the Fund will be exercisable at the strike price only on their expiration date. Prior to the expiration date, the value of the FLEX Options will be determined based upon market quotations or using other recognized pricing methods. The value of the FLEX Options prior to the expiration date may vary because of related factors other than the value of the Underlying ETFs. Factors that may influence the value of the FLEX Options include interest rate changes and implied volatility levels of an Underlying ETF, among others.

Investment Objective Risk. Certain circumstances under which the Fund might not achieve its objective include, but are not limited, to (i) if the Fund disposes of FLEX Options, (ii) if the Fund is unable to maintain the proportional relationship based on the number of FLEX Options in the Fund’s portfolio, (iii) significant accrual of Fund expenses in connection with effecting the Fund’s principal investment strategy or (iv) adverse tax law changes affecting the treatment of FLEX Options.