UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

Amendment No. 1

(Mark One)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from [ ] to [ ]

Commission file number

(Exact name of registrant as specified in its charter) |

| ||

(State or other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification No.) |

| ||

(Address of principal executive offices) |

| (Zip Code) |

Registrant’s telephone number, including area code: (

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class |

| Name of Each Exchange On Which Registered |

N/A |

| N/A |

Securities registered pursuant to Section 12(g) of the Act:

(Title of class) |

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 the Securities Act. |

Yes ☐ |

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act

|

Yes ☐ |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the last 90 days. |

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-K (§229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

|

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

|

Yes |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. |

Large accelerated filer | ☐ | Accelerated filer | ☐ |

|

|

|

|

☐ | Smaller reporting company | ||

(Do not check if smaller reporting company) |

|

| |

| Emerging growth company | ||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

|

Yes |

The aggregate market value of Common Stock held by non-affiliates of the Registrant on June 30, 2022, the last business day of the registrant’s most recently completed second fiscal quarter, was $

Indicate the number of shares outstanding of each of the registrant’s classes of common stock as of the latest practicable date.

| |

| |

DOCUMENTS INCORPORATED BY REFERENCE

None.

TABLE OF CONTENTS

| 2 |

| Table of Contents |

PART I

Item 1. Business

This annual report contains forward-looking statements. These statements relate to future events or our future financial performance. In some cases, you can identify forward-looking statements by terminology such as “may”, “should”, “expects”, “plans”, “anticipates”, “believes”, “estimates”, “predicts”, “potential” or “continue” or the negative of these terms or other comparable terminology. These statements are only predictions and involve known and unknown risks, uncertainties and other factors, including the risks in the section entitled “Risk Factors” that may cause our or our industry’s actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements.

Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Except as required by applicable law, including the securities laws of the United States, we do not intend to update any of the forward-looking statements to conform these statements to actual results.

Our financial statements are stated in United States Dollars (US$) and are prepared in accordance with United States Generally Accepted Accounting Principles.

In this annual report, unless otherwise specified, all dollar amounts are expressed in United States dollars and all references to “common shares” refer to the common shares in our capital stock.

As used in this current report and unless otherwise indicated, the terms “we”, “us” and “our” mean Lithium Corporation, unless otherwise indicated.

General Overview

We were incorporated under the laws of the State of Nevada on January 30, 2007 under the name “Utalk Communications Inc.”. At inception, we were a development stage corporation engaged in the business of developing and marketing a call-back service using a call-back platform. Because we were not successful in implementing our business plan, we considered various alternatives to ensure the viability and solvency of our company.

On August 31, 2009, we entered into a letter of intent with Nevada Lithium regarding a business combination which may be effected in one of several different ways, including an asset acquisition, merger of our company and Nevada Lithium, or a share exchange whereby we would purchase the shares of Nevada Lithium from its shareholders in exchange for restricted shares of our common stock.

Effective September 30, 2009, we effected a 1 old for 60 new forward stock split of our issued and outstanding common stock. As a result, our authorized capital increased from 50,000,000 shares of common stock with a par value of $0.001 to 3,000,000,000 shares of common stock with a par value of $0.001 and our issued and outstanding shares increased from 4,470,000 shares of common stock to 268,200,000 shares of common stock.

Also effective September 30, 2009, we changed our name from “Utalk Communications, Inc.” to “Lithium Corporation”, by way of a merger with our wholly owned subsidiary Lithium Corporation, which was formed solely for the change of name. The name change and forward stock split became effective with the Over-the-Counter Bulletin Board at the opening for trading on October 1, 2009 under the stock symbol “LTUM”. Our CUSIP number is 536804 107.

| 3 |

| Table of Contents |

On October 9, 2009, we entered into a share exchange agreement with Nevada Lithium and the shareholders of Nevada Lithium. The closing of the transactions contemplated in the share exchange agreement and the acquisition of all of the issued and outstanding common stock in the capital of Nevada Lithium occurred on October 19, 2009. In accordance with the closing of the share exchange agreement, we issued 12,350,000 shares of our common stock to the former shareholders of Nevada Lithium in exchange for the acquisition, by our company, of all of the 12,350,000 issued and outstanding shares of Nevada Lithium. Also, pursuant to the terms of the share exchange agreement, a director of our company cancelled 220,000,000 restricted shares of our common stock. Nevada Lithium’s corporate status was allowed to lapse and the company’s status with the Nevada Secretary of State has been revoked.

In June 2009 we optioned the Fish Lake Valley property in Esmeralda County Nevada, and ultimately earned a 100% interest in the property through a combination of exploration expenditures and share issuances. Lithium Corporation performed geophysical, geochemical and drilling work in the area into early 2016 at which time we entered into an agreement with the forerunner of American Lithium Corporation (TSX-V:Li) who could have earned an undivided 80% interest (with the residual 20% interest being purchasable post earn-in) in the property by incurring exploration expenses, making cash and share payments over a period of three years. American Lithium relinquished all interest in the property/option agreement in April 2019. In April 2021 the Company entered into a Letter of Intent with Altura Mining Limited whereby Altura (now Morella Corporation ASX:1MC, OTC-QB: ALTAF) may earn a 60% interest in the property by incurring exploration expenses, and making staged cash and share payments to Lithium Corporation over the next four years. Morella Corporation is the single largest shareholder in Lithium Corporation with over 8% of the Company’s common shares, having acquired an interest through a non-brokered private placement in our Company in 2012.

In 2010 the Company acquired the San Emidio property through the staking of claims on open Bureau of Land Management administered Federal land in Washoe County Nevada. The company conducted geochemical, geophysical and drilling work over the next several years, and eventually optioned them off to American Lithium Corporation in May 2016 for a combination of exploration work, cash and share payments over the following three years. American Lithium allowed the option to lapse in 2018. In September 2021 Surge Battery Metals (TSX-V: Nili) entered into an option to earn an 80% interest in the property by incurring exploration expenses and making staged cash and share payments over the following five years. Lithium Corporation received notification in August 2022 that Surge was relinquishing all interest in the property. The company conducted a CSAMT geophysical survey on the property in Fall 2022.

In June 2013, we purchased a claim in the Sugar Lake area of British Columbia for 250,000 shares of our common stock. Known as the BC Sugar Property this property has expanded and contracted over time as we allowed a number of the less prospective claims to lapse. In January, 2014, we agreed to buy back the shares issued pursuant to the June 2013 agreement for $2,500. After doing considerable work up until spring 2019 all but approximately 203 acres (82.33 Hectares) of claims were allowed to lapse, and the property sat dormant. The market for flake graphite is improving, and the Company’s holdings here are currently approximately 102 acres (41 hectares), and the company is currently contemplating a small work program here this year.

Effective April 23, 2014, we entered into an operating agreement with All American Resources, L.L.C and TY & Sons Investments Inc. with respect to Summa, LLC, a Nevada limited liability company incorporated on December 12, 2013, wherein we hold 25%, and are active “Managing Members”. Our company's initial capital contribution to Summa, LLC was $125,000, of which $100,000 was in cash and the balance in services. To date we have contributed an additional $31,700 in cash, and also over the years an indeterminate amount of casual geological expertise to Summa, LLC. In recognition, Summa transferred five urban lots in Tonopah of indeterminate value in 2020, and since Jan 2021 have issued checks to the company for $138,000. The Tonopah property was optioned in early 2020, and the Optionee has earned a 100% interest in the property. Summa still retains a 1% (LTUM’s share 0.25%) Net Smelter Royalty on the property, as well as other interests around the state of Nevada, including a property in Belmont Nevada that is currently under option to Nevada Silver Corporation.

| 4 |

| Table of Contents |

In April of 2016, our Company established a wholly owned subsidiary called Lithium Royalty Corp. The subsidiary was a Nevada Corporation and was the entity through which we had planned to build a portfolio of lithium mineral properties. Also that April Lithium Royalty Corp acquired through staking the North Big Smoky Prospect, a block of placer mineral claims in Nye County Nevada. On May 13, 2016 our wholly owned subsidiary sold 100% of the interest in the North Big Smoky property through a Property Acquisition Agreement with 1069934 Nevada Ltd. ("Purchaser") a private company. Consideration paid to Lithium Royalty Corp. consisted of mainly of 300,000 shares in the "Purchaser Parent", 1069934 B.C. Ltd. By agreement dated September 13, 2017 Lithium Corporation agreed to sell back the shares of 1069934 Nevada Ltd. to San Antone Minerals Corp. and compensation under the agreement was received on November 2, 2017. The North Big Smoky claims were abandoned by the Purchaser in 2017 and in 2021 the Company re-staked claims in the general area, and optioned the property to Morella Corp (a related company) who conducted geochemical and geophysical work on the claims in 2022, and an initial 2 hole drilling program in 2023.

Our Current Business

We are an exploration stage mining company engaged in the identification, acquisition, and exploration of metals and minerals with a focus on lithium mineralization on properties located in Nevada, and graphite and other energy metals properties in British Columbia.

Our current operational focus is to conduct generative exploration activities in Nevada, and on our titanium/REE and graphite properties, in British Columbia.

In April of 2016, our Company established a wholly owned subsidiary called Lithium Royalty Corp. The subsidiary was a Nevada Corporation and was the entity through which we had planned to build a portfolio of lithium mineral properties. Also that April Lithium Royalty Corp acquired through staking the North Big Smoky Prospect, a block of placer mineral claims in Nye County Nevada. On May 13, 2016 our wholly owned subsidiary sold 100% of the interest in the North Big Smoky Property through a Property Acquisition Agreement with 1069934 Nevada Ltd. ("Purchaser") a private company. Consideration paid to Lithium Royalty Corp. consisted of mainly of 300,000 shares in the "Purchaser Parent", 1069934 B.C. Ltd. By agreement dated September 13, 2017 Lithium Corporation agreed to sell back the shares of 1069934 Nevada Ltd. to San Antone Minerals Corp (successor corporation) and the North Big Smoky claims were allowed to lapse. In March of 2022 we staked a block of claims in North Big Smoky Valley covering approximately 3400 acres which roughly corresponds to the lands previously held by Lithium Corporation’s former subsidiary Lithium Royalty Corp. in 2016/2017. On May 13, 2022 we signed a Letter of Intent (LOI) with Morella Corporation (a related party) whereby Morella can earn a 60% interest in the property by paying $65,000 US (done) to the Company on the signing of the LOI, and issuing $100,000 worth of Morella shares at the time of signing the formal agreement, and issuing $100,000 worth of shares at each anniversary of the signing of the formal agreement over the next four years. Additionally, Morella must incur exploration expenditures of $100,000, $200,000, $300,000 and $400,000 in years one through four of the option agreement. Should they fulfill these obligations they will have earned an undivided 60% interest in the property and may purchase a further 20% interest within 1 year for $750,000 and purchase the remaining 20% interest within the following year for $750,000. Should Morella buy Lithium Corporation’s undivided working interest in the property, the Company will revert to a 2.5 % Net Smelter Royalty interest, ½ of which would be purchasable by Morella for $1,000,000. Since Optioning the property Morella has conducted Controlled Source Audio-Magnetotelluric geophysical and sediment geochemical surveys, staked more claims adjacent to the original option claim block as well as staking a non-contiguous area to the north and west of the earlier claims here. Most recently Morella has concluded a two-hole drilling program, testing for both lithium-in-brine and clay mineralization, where anomalous lithium-in-clay mineralization was discovered, but no lithium-in-brine mineralization was encountered.

On September 16th 2021 Lithium Corporation signed an agreement with Surge Battery Metals whereby Surge could have earned an 80% interest in the Company’s San Emidio lithium-in-brine prospect in Washoe County Nevada, by paying an initial $50,000 and issuing 200,000 shares of Surge (TSX-V:Nili). Surge had undertaken to make payments of $620,000 in cash and stock over 5 years while incurring expenditures on the property of $1,000,000 over that period. Upon fulfillment of the aforementioned commitments Surge would have been deemed to have earned their undivided 80% interest and could have formed a joint venture with the Company. The Company had optioned this property off before as effective May 3, 2016, our company entered in to an Exploration Earn-In Agreement with 1067323 B.C. Ltd. with respect to our San Emidio property. The terms of the formal agreement were; payment of $100,000, issuance of 300,000 common shares of 1067323 B.C. Ltd., or of the publicly traded company anticipated to result from a Going Public Transaction, and work performed on the property by the Optionee in the amount of $600,000 over the following three years to earn an 80% interest in the property. 1067323 then had a subsequent Earn-In option to purchase Lithium Corporation's remaining 20% working interest within three years of earning the 80% by paying our company a further $1,000,000, at which point our company would retain a 2.5% Net Smelter Royalty, half of which could have been purchased by 1067323 for an additional $1,000,000. 1067323 B.C. Ltd. merged with American Lithium Corp., and the first tranche of cash and shares were issued in June of 2016. The Company waived the work requirement for the first year and received extra shares of American Lithium Corp as consideration for the amendment to the Agreement. In June 2018, the Company received notification that the purchaser was relinquishing any right to earn an interest in the property and, as such, $202,901 was taken into income. During the year-ended December 31, 2019, the Company recorded a $217,668 allowance for the property which then had a net book value of $Nil. Surge Battery Metals completed some geochemical work on the prospect block and gave Lithium Corporation formal notice in Summer 2022 that they were relinquishing all interest in the property. In Fall 2022 the Company completed a Controlled Source Audio-Magnetotelluric (CSAMT) survey on the property and is currently considering next steps with respect to exploring and developing this property.

| 5 |

| Table of Contents |

On April 29, 2021 we signed a Letter Of Intent (LOI) with Altura Mining Limited (now Morella Corporation after a name change) an Australian Lithium explorer and developer and related party, whereby Morella can earn a 60% interest in the Fish Lake Valley lithium-in-brine property in Esmeralda County, Nevada by paying the Company $675,000, issuing the equivalent of $500,000 worth of Morella stock, and expending $2,000,000 of exploration work over the next four years. To date Morella is current with its obligations under the formal agreement ratified on October 12th 2021, having paid the initial $50,000 on signing the LOI, the $100,000 due on signing the formal agreement, and has issued 26,791,685 shares of Morella (1MC:ASX, Altaf:OTC-QB) common stock in consideration for this agreement. On February 16, 2016, Lithium Corp had issued a news release announcing that our company had entered into a letter of intent with 1032701 B.C. Ltd. with respect to our Fish Lake Valley property. On March 10, 2016 we issued a news release announcing the signing of the Fish Lake Valley Earn-In Agreement. The terms of the Earn-In Agreement allowed 1032701 to earn an 80% interest in Fish Lake Valley for payments over three years totaling $300,000 and issuance of 400,000 common shares of the publicly traded company anticipated to result from a Going Public Transaction, and work performed on the property over three years in the amount of $1,100,000. 1032701 then had a Subsequent Earn-In option to purchase Lithium Corporation's remaining 20% working interest within one year of earning the 80% by paying the Company a further $1,000,000, at that point the Company would retain a 2.5% Net Smelter Royalty, half of which could have been purchased by 1032701 for an additional $1,000,000. Menika Mining, a publicly traded company on the TSX Venture Exchange trading under the symbol MML announced on March 8, 2016 that it intended to acquire 1032701 B.C. Ltd and the right to acquire the Fish Lake Valley Property. Menika Mining completed the acquisition of 1032701 B.C. and fulfilled the initial obligations of the Fish Lake Valley Earn-In-Agreement in April of 2016. Meninka later changed their name to American Lithium. While the Purchaser did comply with all terms of the agreement with respect to cash and share payments the Company received formal notice of the relinquishment of the Purchasers right to earn an interest in the property on April 30th 2019. As this was the termination of the option agreement $443,308 was taken into income. During the year-ended December 31, 2019, the Company recorded a $159,859 allowance for the properties and at that time had a net book value of $Nil. On April 29, 2021 we signed a Letter Of Intent (LOI) with Altura Mining Limited (now Morella Corporation after a name change) an Australian Lithium explorer and developer, and related party whereby Morella can earn a 60% interest in the Fish Lake Valley lithium-in-brine property in Esmeralda County, Nevada by paying the Company $675,000, issuing the equivalent of $500,000 worth of Morella stock, and expending $2,000,000 of exploration work over the following four years. To date Morella is current with its obligations under the formal agreement ratified on October 12th 2021, having paid all initial and anniversary cash disbursements as per the agreement, and has issued a total of 55,560,526 shares of Morella (1MC:ASX, Altaf:OTC-QB) common stock relating to this agreement to date. In the last couple of years Morella has completed two phases of passive seismic and magnetotelluric (MT) surveys, and have received permits for drilling on both the south and northern blocks. Preparatory work for drilling was done during the summer of 2022, with surface casing being installed on the prospect to the south in late 2022, and drilling commenced in early October 2023, to the northeast of the playa, proximal to but away from the area of known mineralization. Only moderate mineralization was encountered in the 2023 drillhole in both clays and brines. Winter 2023-24 was very wet in western Nevada, so it will be several months before work can be contemplated on the playa at Fish Lake Valley, however initial planning has commenced for the 2024 program.

| 6 |

| Table of Contents |

On March 2, 2017 we issued a news release announcing that we had signed a letter of intent with Bormal Resources Inc. with respect to three tantalum-niobium (Ta-Nb) properties (Michael, Yeehaw, and Three Valley Gap) located in British Columbia, Canada. The Michael property in the Trail Creek Mining Division was originally staked to cover one of the most compelling tantalum in stream sediment anomalies as seen in the government RGS database in British Columbia. Bormal conducted a stream sediment sampling program in 2014, and determined that the tantalum-niobium in stream sediment anomaly here is bona fide, and in the order of 6 kilometers in length. In November of 2016 Lithium Corporation conducted a short soil geochemistry orientation program on the property as part of its due diligence, and determined that there are elevated levels of tantalum-niobium in soils here.

Also, in the general area of the Michael property, the Yeehaw property had been staked over a similar but lower amplitude tantalum/total rare earth elements (TREE’s) in stream sediment anomaly. Both properties are situated within the Eocene Coryell Batholith, and at the time it was thought that these anomalies may arise from either carbonatite or pegmatite type deposits. The Company conducted a helicopter borne bio-geochemical survey on these two properties in June 2017, which did return anomalous results. This was followed up by a geological and geochemical examination of the Yeehaw property in early July 2017, and additional work of a similar nature later in July, and again in early October 2017. These examinations uncovered a zone roughly 30 meters wide which included an interval that is mineralized with approximately 0.75% TREE’s. While markedly anomalous it is not exceedingly enriched in TREE’s. However this zone may not be the “main event” in the area but a harbinger of bigger and better things, and also it is enriched in titanium (Ti), which could possibly be in the form of Perovskite, a mineral of considerable interest for the next generation of photo-voltaic cells. Preliminary geological and geochemical work were performed on the Michael property in October of 2016, followed by a brief airborne biogeochemical survey in June of 2017, and additional ground geological and geochemical assessment work in early October, 2017. The third property – Three Valley Gap, is in the Revelstoke Mining Division and is situated in a locale where several Nb-Ta enriched carbonatites have been noted to occur. A brief field program by Bormal in 2015 located one of these carbonatites, and concurrent soil sampling determined that the soils here are enriched with Nb-Ta over the known carbonatite, and indicated that there are other geochemical anomalies locally that may indicate that more carbonatites exist here and are shallowly buried.

On February 23, 2018 we issued a news release announcing that we had dropped any interest in the Michael and Three Valley Gap properties, and had renegotiated the final share payment as required in the agreement from 750,000 to 400,000 shares. The final consideration shares were issued and the Yeehaw property has been transferred by Bormal. During 2017 the Company conducted initial stream, rock and magnetometer surveys on the property, and discovered a 30 meter wide lamprophyric dyke (Horseshoe Bend showing) that exhibits anomalous titanium/REE mineralization. The company staked an additional 5227 acre (2115.51 hectares) mineral claim and conducted a brief exploration program in Spring 2018 of geological mapping and rock and soil sampling on the property. This program discovered a slightly stronger zone of similar mineralization approximately 660 feet (200 meters) to the northwest of the Horseshoe Bend, and similar float mineralization another 0.75 miles (1.2 kms) further to the northwest. Additional work was performed on the property in 2019 and 2020 which extended the known strike of the Horseshoe Bend showing approximately 50 meters to the west, and mineralized float was found that possibly indicates it could continue to the east for another several hundred meters. The Company is currently in the planning stages for field season 2024.

At the BC Sugar property in the Okanagan Highlands to the east of Vernon British Columbia the Company revised its trenching permit in 2017 and conducted a program of 12 mechanized test pits in May 2018. This work was done in an area ranging from 1 to 1.5 kilometers to the east of the Weather Station Zone in a zone of numerous discrete conductors detected during the 2015 FDEM geophysical survey. Three of these pits intercepted weathered weak to moderately mineralized graphitic material with the best assay being 2.62% graphitic, carbon, and six test pits bottomed in non-mineralized bedrock. The remaining three did not reach bedrock or intercept graphitic material prior to reaching the maximum digging capability of the excavating equipment used. The Company has reduced its acreage holdings here to approximately 203 acres (82 hectares) and is currently considering further work this year.

Effective April 23, 2014, we entered into an operating agreement with All American Resources, L.L.C and TY & Sons Investments Inc. with respect to Summa, LLC, a Nevada limited liability company incorporated on December 12, 2013, wherein we hold a 25% membership. Summa was formed to acquire and administer the residual lands that originated in the 60’s and 70’s through Howard Hughes’s – Hughes Corporation, which went on a mining property buying spree at that time. Our company's capital contribution to Summa, LLC was $125,000, of which $100,000 was in cash and the balance in services. To date we have contributed an additional $31,700 in cash, and also over the years an indeterminate amount of casual geological and land expertise to Summa, LLC. In recognition, Summa transferred five urban lots in Tonopah of indeterminate value in 2020, and since Jan 2021 have issued checks to the company for $167,500. The Tonopah property was optioned in early 2020, and the Optionee has earned a 100% interest in the property. Summa still retains a 1% (LTUM’s share 0.25%) Net Smelter Royalty on the property. Recently Summa entered into an agreement with North American Silver Corporation (TSX-V:NSC) whereby NSC can earn a 100% interest with respect to Summa’s Belmont Nevada claims (not to be confused with the Belmont mine in Tonopah) by paying $200,000 in cash or at Optionor’s discretion shares over 5 years, and election must be made by the sixth agreement anniversary to purchase the lands (69.96 acres) at $10,000 per acre. Should NSC earn their interest Summa, LLC would retain a 1% Net Smelter Royalty – 50% of which may be subsequently purchased by the Optionor. Summa, LLC still retains a 100% interest (subject to a 2% NSR in favor of Summa Corp. (the successor entity to the Hughes Corporation) in a further five project areas in the state of Nevada, and Lithium Corporation remains committed to casually helping them move the projects along so that they may be optioned eventually.

| 7 |

| Table of Contents |

Competition

The mining industry is intensely competitive. We compete with numerous individuals and companies, including many major mining companies, which have substantially greater technical, financial and operational resources and staffs. Accordingly, there is a high degree of competition for access to funds. There are other competitors that have operations in the area and the presence of these competitors could adversely affect our ability to compete for financing and obtain the service providers, staff or equipment necessary for the exploration and exploitation of our properties.

Compliance with Government Regulation

Mining operations and exploration activities are subject to various national, state, provincial and local laws and regulations in United States and Canada, as well as other jurisdictions, which govern prospecting, development, mining, production, exports, taxes, labor standards, occupational health, waste disposal, protection of the environment, mine safety, hazardous substances and other matters.

We believe that we are and will continue to be in compliance in all material respects with applicable statutes and the regulations passed in the United States and Canada. There are no current orders or directions relating to our company with respect to the foregoing laws and regulations.

Research and Development

We have not incurred any research and development expenditures over the last two fiscal years.

Intellectual Property

We do not currently have any intellectual property, other than our domain name and website, www.lithiumcorporation.com.

Employees

We have no employees. Our officers and directors provide their services to our company as independent consultants.

Item 1A. Risk Factors

Our business operations are subject to a number of risks and uncertainties, including, but not limited to those set forth below:

| 8 |

| Table of Contents |

Risks Associated with Mining

All of our properties are in the exploration stage. There is no assurance that we can establish the existence of any mineral resource on any of our properties in commercially exploitable quantities. Until we can do so, we cannot earn any revenues from operations and if we do not do so we will lose all of the funds that we expend on exploration. If we do not discover any mineral resource in a commercially exploitable quantity, our business could fail.

Despite exploration work on our mineral properties, we have not established that any of them contain any mineral reserve, nor can there be any assurance that we will be able to do so. If we do not, our business could fail.

A mineral reserve is defined by the Securities and Exchange Commission in its Industry Guide 7 (which can be viewed over the Internet at http://www.sec.gov/about/forms/industryguides.pdf) as that part of a mineral deposit which could be economically and legally extracted or produced at the time of the reserve determination. The probability of an individual prospect ever having a “reserve” that meets the requirements of the Securities and Exchange Commission’s Industry Guide 7 is extremely remote; in all probability our mineral resource property does not contain any “reserve” and any funds that we spend on exploration will probably be lost.

Even if we do eventually discover a mineral reserve on one or more of our properties, there can be no assurance that we will be able to develop our properties into producing mines and extract those resources. Both mineral exploration and development involve a high degree of risk and few properties which are explored are ultimately developed into producing mines.

The commercial viability of an established mineral deposit will depend on a number of factors including, by way of example, the size, grade and other attributes of the mineral deposit, the proximity of the resource to infrastructure such as a smelter, roads and a point for shipping, government regulation and market prices. Most of these factors will be beyond our control, and any of them could increase costs and make extraction of any identified mineral resource unprofitable.

Mineral operations are subject to applicable law and government regulation. Even if we discover a mineral resource in a commercially exploitable quantity, these laws and regulations could restrict or prohibit the exploitation of that mineral resource. If we cannot exploit any mineral resource that we might discover on our properties, our business may fail.

Both mineral exploration and extraction require permits from various foreign, federal, state, provincial and local governmental authorities and are governed by laws and regulations, including those with respect to prospecting, mine development, mineral production, transport, export, taxation, labor standards, occupational health, waste disposal, toxic substances, land use, environmental protection, mine safety and other matters. There can be no assurance that we will be able to obtain or maintain any of the permits required for the continued exploration of our mineral properties or for the construction and operation of a mine on our properties at economically viable costs. If we cannot accomplish these objectives, our business could fail.

We believe that we are in compliance with all material laws and regulations that currently apply to our activities but there can be no assurance that we can continue to remain in compliance. Current laws and regulations could be amended and we might not be able to comply with them, as amended. Further, there can be no assurance that we will be able to obtain or maintain all permits necessary for our future operations, or that we will be able to obtain them on reasonable terms. To the extent such approvals are required and are not obtained, we may be delayed or prohibited from proceeding with planned exploration or development of our mineral properties.

| 9 |

| Table of Contents |

If we establish the existence of a mineral resource on any of our properties in a commercially exploitable quantity, we will require additional capital in order to develop the property into a producing mine. If we cannot raise this additional capital, we will not be able to exploit the resource, and our business could fail.

If we do discover mineral resources in commercially exploitable quantities on any of our properties, we will be required to expend substantial sums of money to establish the extent of the resource, develop processes to extract it and develop extraction and processing facilities and infrastructure. Although we may derive substantial benefits from the discovery of a major deposit, there can be no assurance that such a resource will be large enough to justify commercial operations, nor can there be any assurance that we will be able to raise the funds required for development on a timely basis. If we cannot raise the necessary capital or complete the necessary facilities and infrastructure, our business may fail.

Mineral exploration and development is subject to extraordinary operating risks. We do not currently insure against these risks. In the event of a cave-in or similar occurrence, our liability may exceed our resources, which would have an adverse impact on our company.

Mineral exploration, development and production involves many risks which even a combination of experience, knowledge and careful evaluation may not be able to overcome. Our operations will be subject to all the hazards and risks inherent in the exploration for mineral resources and, if we discover a mineral resource in commercially exploitable quantity, our operations could be subject to all of the hazards and risks inherent in the development and production of resources, including liability for pollution, cave-ins or similar hazards against which we cannot insure or against which we may elect not to insure. Any such event could result in work stoppages and damage to property, including damage to the environment. We do not currently maintain any insurance coverage against these operating hazards. The payment of any liabilities that arise from any such occurrence would have a material adverse impact on our company.

Mineral prices are subject to dramatic and unpredictable fluctuations.

We expect to derive revenues, if any, either from the sale of our mineral resource properties or from the extraction and sale of lithium and/or associated byproducts. The price of those commodities has fluctuated widely in recent years, and is affected by numerous factors beyond our control, including international, economic and political trends, expectations of inflation, currency exchange fluctuations, interest rates, global or regional consumptive patterns, speculative activities and increased production due to new extraction developments and improved extraction and production methods. The effect of these factors on the price of base and precious metals, and therefore the economic viability of any of our exploration properties and projects, cannot accurately be predicted.

The mining industry is highly competitive and there is no assurance that we will continue to be successful in acquiring mineral claims. If we cannot continue to acquire properties to explore for mineral resources, we may be required to reduce or cease operations.

The mineral exploration, development, and production industry is largely un-integrated. We compete with other exploration companies looking for mineral resource properties. While we compete with other exploration companies in the effort to locate and acquire mineral resource properties, we will not compete with them for the removal or sales of mineral products from our properties if we should eventually discover the presence of them in quantities sufficient to make production economically feasible. Readily available markets exist worldwide for the sale of mineral products. Therefore, we will likely be able to sell any mineral products that we identify and produce.

In identifying and acquiring mineral resource properties, we compete with many companies possessing greater financial resources and technical facilities. This competition could adversely affect our ability to acquire suitable prospects for exploration in the future. Accordingly, there can be no assurance that we will acquire any interest in additional mineral resource properties that might yield reserves or result in commercial mining operations.

| 10 |

| Table of Contents |

Risks Related to our Company

The fact that we have not earned any operating revenues since our incorporation raises substantial doubt about our ability to continue to explore our mineral properties as a going concern.

We have not generated any revenue from operations since our incorporation and we anticipate that we will continue to incur operating expenses without revenues unless and until we are able to identify a mineral resource in a commercially exploitable quantity on one or more of our mineral properties and we build and operate a mine. We had cash in the amount of $3,667,617 as of December 31, 2023. At December 31, 2023, we had working capital of $1,797,272. We incurred a net loss of $618,193 for the year ended December 31, 2023. We estimate our average monthly operating expenses to be approximately $74,000, including property costs, management services and administrative costs. Should the results of our planned exploration require us to increase our current operating budget, we may have to raise additional funds to meet our currently budgeted operating requirements for the next 12 months. As we cannot assure a lender that we will be able to successfully explore and develop our mineral properties, we will probably find it difficult to raise debt financing from traditional lending sources. We have traditionally raised our operating capital from sales of equity securities, but there can be no assurance that we will continue to be able to do so. If we cannot raise the money that we need to continue exploration of our mineral properties, we may be forced to delay, scale back, or eliminate our exploration activities. If any of these were to occur, there is a substantial risk that our business would fail.

Management has plans to seek additional capital through private placements of its capital stock. These conditions raise substantial doubt about our company’s ability to continue as a going concern. Although there are no assurances that management’s plans will be realized, management believes that our company will be able to continue operations in the future. The financial statements do not include any adjustments relating to the recoverability and classification of recorded assets, or the amounts of and classification of liabilities that might be necessary in the event our company cannot continue in existence.” We continue to experience net operating losses.

Risks Associated with Our Common Stock

Trading on the OCTQB may be volatile and sporadic, which could depress the market price of our common stock and make it difficult for our stockholders to resell their shares.

Our common stock is quoted on the OTCQB electronic quotation service operated by OTC Markets Group Inc. Trading in stock quoted on the OTCQB is often thin and characterized by wide fluctuations in trading prices, due to many factors that may have little to do with our operations or business prospects. This volatility could depress the market price of our common stock for reasons unrelated to operating performance. Moreover, the OTCQB is not a stock exchange, and trading of securities on the OTCQB is often more sporadic than the trading of securities listed on a quotation system like Nasdaq or a stock exchange like Amex. Accordingly, shareholders may have difficulty reselling any of the shares.

| 11 |

| Table of Contents |

Our stock is a penny stock. Trading of our stock may be restricted by the Securities and Exchange Commission’s penny stock regulations and FINRA’s sales practice requirements, which may limit a stockholder’s ability to buy and sell our stock.

Our stock is a penny stock. The Securities and Exchange Commission (“SEC”) has adopted Rule 15g-9 which generally defines “penny stock” to be any equity security that has a market price (as defined) less than $5.00 per share or an exercise price of less than $5.00 per share, subject to certain exceptions. Our securities are covered by the penny stock rules, which impose additional sales practice requirements on broker-dealers who sell to persons other than established customers and “accredited investors”. The term “accredited investor” refers generally to institutions with assets in excess of $5,000,000 or individuals with a net worth in excess of $1,000,000 or annual income exceeding $200,000 or $300,000 jointly with their spouse. The penny stock rules require a broker-dealer, prior to a transaction in a penny stock not otherwise exempt from the rules, to deliver a standardized risk disclosure document in a form prepared by the SEC which provides information about penny stocks and the nature and level of risks in the penny stock market. The broker-dealer also must provide the customer with current bid and offer quotations for the penny stock, the compensation of the broker-dealer and its salesperson in the transaction and monthly account statements showing the market value of each penny stock held in the customer’s account. The bid and offer quotations, and the broker-dealer and salesperson compensation information, must be given to the customer orally or in writing prior to effecting the transaction and must be given to the customer in writing before or with the customer’s confirmation. In addition, the penny stock rules require that prior to a transaction in a penny stock not otherwise exempt from these rules, the broker-dealer must make a special written determination that the penny stock is a suitable investment for the purchaser and receive the purchaser’s written agreement to the transaction. These disclosure requirements may have the effect of reducing the level of trading activity in the secondary market for the stock that is subject to these penny stock rules. Consequently, these penny stock rules may affect the ability of broker-dealers to trade our securities. We believe that the penny stock rules discourage investor interest in, and limit the marketability of, our common stock.

In addition to the “penny stock” rules promulgated by the SEC, FINRA has adopted rules that require that in recommending an investment to a customer, a broker-dealer must have reasonable grounds for believing that the investment is suitable for that customer. Prior to recommending speculative low priced securities to their non-institutional customers, broker-dealers must make reasonable efforts to obtain information about the customer’s financial status, tax status, investment objectives and other information. Under interpretations of these rules, FINRA believes that there is a high probability that speculative low-priced securities will not be suitable for at least some customers. FINRA’s requirements make it more difficult for broker-dealers to recommend that their customers buy our common stock, which may limit your ability to buy and sell our stock.

Other Risks

Trends, Risks and Uncertainties

We have sought to identify what we believe to be the most significant risks to our business, but we cannot predict whether, or to what extent, any of such risks may be realized nor can we guarantee that we have identified all possible risks that might arise. Investors should carefully consider all of such risk factors before making an investment decision with respect to our common stock.

Item 1B. Unresolved Staff Comments

As a “smaller reporting company”, we are not required to provide the information required by this Item.

| 12 |

| Table of Contents |

Item 1C. Cybersecurity

Risk Management and Strategy

The Company has processes for assessing, identifying, and managing material risks from cybersecurity threats. These processes are integrated into the Company’s overall risk management systems, as overseen by the Company’s board of directors, primarily through its audit committee.

Governance

Board of Directors

The audit committee of the Company’s board of directors, with the input of management, oversees the Company’s internal controls, including internal controls designed to assess, identify, and manage material risks from cybersecurity threats. The audit committee is informed of material risks, when applicable, from cybersecurity threats by the Company’s Chief Executive Officer. Updates on cybersecurity matters, including material risks and threats, are provided to the Company’s audit committee, and the audit committee provides updates to the Company’s board of directors at regular board meetings.

Management

Under the oversight of the audit committee of the Company’s board of directors, the Company’s Chief Executive Officer is primarily responsible for the assessment and management of material cybersecurity risks and establishing and maintaining adequate and effective internal controls covering cybersecurity matters.

The audit committee of the Company’s board of directors, with the assistance of the Company’s Chief Executive Officer, is responsible for overseeing the establishment and effectiveness of controls and other procedures, including controls and procedures related to the public disclosure of material cybersecurity matters.

As of the date of this report, other than the foregoing, the Company is not aware of any cybersecurity incidents that have materially affected or are reasonably likely to materially affect the Company, including its business strategy, results of operations, or financial condition and that are required to be reported in this report. For further discussion of the risks associated with cybersecurity incidents, see the cybersecurity risk factors in Item 1A. Risk Factors in this report.

Item 2. Properties

Our corporate head office is located at 1031 Railroad St., Ste 102B, Elko Nevada 89801, our monthly rent is $500 paid to a Rangefront Geological, a related party, which also includes storage space for field gear. We also rent office and storage space in Richland WA in support of our Yeehaw and BC Sugar prospects, which rent is also $500 per month. Additionally Lithium Corporation owns outright 2.3 acres (five lots) of undeveloped fee-title land in the town of Tonopah, NV.

Mineral Properties

Of our various property interests, we consider the Fish Lake Valley Property to be our material property interest.

Fish Lake Valley Property

Lithium Corp’s flagship property is the Fish Lake Valley Project and is a lithium brine prospect - similar to the salars of Chile & Peru, and more importantly Silver Peak Nevada, which is only approximately 25 miles to the east of Lithium Corp’s Fish Lake Valley project. The only lithium producing facility in North America is located at Silver Peak in Clayton Valley, Nevada. The facility was opened in 1967 and has been producing lithium carbonate from brines since. Lithium Corp’s Fish Lake Valley Project is in a similar geologic setting and geothermal regime as Clayton Valley.

Fish Lake Valley Project is a lithium brine exploration project in Esmerelda County, Nevada, USA. The project consists of Lithium Corp’s 100% owned 297 placer claims totaling 10,972 acres. Fish Lake Valley has not had mining production in the most recent three fiscal years although historically in the 1800’s the property was a boron brine producer with an indeterminate amount of boron salts having been produced. The earliest record of any modern exploration on the property was in the 1970’s when the USGS drilled several rotary holes on the periphery of the playa testing for lithium in brines and sediments. Lithium processing facilities do not currently exist in Fish Lake Valley.

Fish Lake Valley is a lithium/boron/potassium enriched playa (also known as a salar, or salt pan), which is located in northern Esmeralda County in west central Nevada, and the area of greatest interest is roughly centered at 417050E 4195350N (NAD 27 CONUS). After staking numerous new claims in 2016 we currently hold 143, nominally 80-acre Association Placer claims that cover approximately 11,360 acres (4,597 hectares). Lithium-enriched Tertiary-era Fish Lake formation rhyolitic tuffs or ash flow tuffs have accumulated in a valley or basinal environment. Over time interstitial formational waters in contact with these tuffs, have become enriched in lithium, boron and potassium which could possibly be economic, and amenable to extraction by evaporative methods.

| 13 |

| Table of Contents |

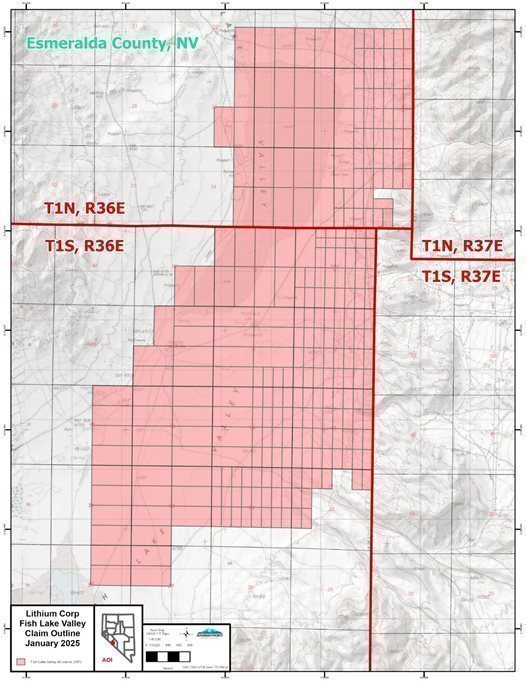

Map 1, Fish Lake Valley Project claim outline.

The property was originally held under mining lease purchase agreement dated June 1, 2009, between Nevada Lithium Corporation, and Nevada Alaska Mining Co. Inc., Robert Craig, Barbara Craig, and Elizabeth Dickman. Nevada Lithium issued to the vendors $350,000 worth of common stock of our company in eight regular disbursements. All disbursements were made of stock worth a total of $350,000, and claim ownership was transferred to our company.

The geological setting at Fish Lake Valley is highly analogous to the salars of Chile, Bolivia, and Peru, and more importantly Clayton Valley, where Albemarle has its Silver Peak lithium-brine operation. Access is excellent in Fish Lake Valley with all-weather gravel roads leading to the property from state highways 264, and 265, and maintained gravel roads ring the playa. Power is available approximately 10 miles from the property, and the village of Dyer is approximately 12 miles to the south, while the town of Tonopah, Nevada is approximately 50 miles to the east.

Our company completed a number of geochemical and geophysical studies on the property, and conducted a short drill program on the periphery of the playa in the fall of 2010. Near-surface brine sampling during the spring of 2011 outlined a boron/lithium/potassium anomaly on the northern portions of the northern playa, that is roughly 1.3 x 2 miles long, which has a smaller higher grade core where lithium mineralization ranges from 100 to 150 mg/L (average 122.5 mg/L), with boron ranging from 1,500 to 2,670 mg/L (average 2,219 mg/L), and potassium from 5,400 to 8,400 mg/L (average 7,030 mg/L). Wet conditions on the playa precluded drilling there in 2011, and for a good portion of 2012, however a window of opportunity presented itself in late fall 2012. In November/December 2012 we conducted a short direct push drill program on the northern end of the playa, wherein a total of 1,240.58 feet (378.09 meters) was drilled in 20 holes at 17 discrete sites, and an area of 3,356 feet (1,023 meters) by 2,776 feet (846 meters) was systematically explored by grid probing. The deepest hole was 81 feet (24.69 meters), and the shallowest hole that produced brine was 34 feet (10.36 meters). The average depth of the holes drilled during the program was 62 feet (18.90 meters). The program successfully demonstrated that lithium-boron-potassium-enriched brines exist to at least 62 feet (18.9 meters) depth in sandy or silty aquifers that vary from approximately three to ten feet (one to three meters) in thickness. Average lithium, boron and potassium contents of all samples are 47.05 mg/L, 992.7 mg/L, and 0.535% respectively, with lithium values ranging from 7.6 mg/L to 151.3 mg/L, boron ranging from 146 to 2,160.7 mg/L, and potassium ranging from 0.1 to 1.3%. The anomaly outlined by the program is 1,476 by 2,461 feet (450 meters by 750 meters), and is not fully delimited, as the area available for probing was restricted due to soft ground conditions to the east and to the south. A 50 mg/L lithium cutoff is used to define this anomaly and within this zone average lithium, boron and potassium contents are 90.97 mg/L, 1,532.92 mg/L, and 0.88% respectively. On September 3, 2013, we announced that drilling had commenced at Fish Lake Valley. Due to storms and wet conditions in the area that our company had hoped to concentrate on, the playa was not passable, and so the program concentrated on larger step-out drilling well off the playa. This 11 hole, 1,025 foot program did prove that mineralization does not extend much, if at all, past the margins of the playa, as none of the fluids encountered in this program were particularly briny, and returned values of less than 5 mg/L lithium. Results from the work done in the past by Lithium Corporation have been very positive, and our company believes that the playa at Fish Lake Valley may be conducive to the formation of a “Silver Peak” style lithium brine deposit.

Early in 2016 the company signed an Exploration Earn-In Agreement with 1032701 B.C. Ltd., a private British Columbia company with respect to our Fish Lake Valley lithium brine property, wherein 1032701 B.C. Ltd., may acquire an initial 80% undivided interest in the Fish Lake Valley property through the payment of an aggregate of US$300,000 in cash, completing a “Going Public Transaction” on or before May 6, 2016, and subject to the completion of the “Going Public Transaction, arranging for the issuance of a total of 400,000 common shares in the capital of the resulting issuer as follows: (i) within five business days following the effective date,

| 14 |

| Table of Contents |

| · | Pay $100,000 to our company and issue 200,000 common shares of the TSX-V listed public company. |

|

|

|

| · | On or before the first anniversary of the signing of the Definitive Agreement pay $100,000 to our company and issue 100,000 common shares of the Optionee/TSX-V listed public company. |

|

|

|

| · | On or before the second anniversary of the signing of the definitive agreement pay $100,000 to our company and issue 100,000 common shares of the Optionee/TSX-V listed public company. |

The Optionee needed to make qualified exploration or development expenditures on the property of $200,000 before the first anniversary, an additional $300,000 before the second anniversary, an additional $600,000 prior to the third anniversary, and make all payments and perform all other acts to maintain the Property in good standing before fully earning their 80% interest. Additionally, after the initial earn-in the Optionee had the right for up to 12 months to purchase our 20% interest in the property for $1,000,000, at which point our interest would have reverted to a 2 1/2% Net Smelter Royalty (NSR). The Optionee could then have elected at any time to purchase one half (1.25%) of our NSR for $1,000,000.

American Lithium Corp. subsequently acquired 100% of 1032701 BC, and a formal option agreement was entered into, effective March 31, 2016. An amendment to the agreement was entered into on the 14th of February 2018 whereby American Lithium issued 10,000 post consolidation “Agreement Year” shares to Lithium Corporation as mandated by the agreement, as well as a further 80,000 shares in consideration for Lithium Corporation agreeing to extend the work commitment date for Year 2 of the agreement to September 30, 2018. We had received all money, and common shares issuable in relation to the Fish Lake Valley option agreement, but the Purchaser issued formal notice of the relinquishment of the Purchasers right to earn the interest in the property on April 30th 2019. As this was the termination of the option agreement $443,308 was taken into income. During the year-ended December 31, 2019, the Company recorded a $159,859 allowance for the properties and has a net book value of $Nil.

On April 29, 2021 we signed a Letter Of Intent (LOI) with Altura Mining Limited (now Morella Corporation after a name change), an Australian Lithium explorer and developer and a related party, whereby Morella can earn a 60% interest in the Fish Lake Valley lithium-in-brine property in Esmeralda County, Nevada by paying the Company $675,000, issuing the equivalent of $500,000 worth of Morella stock, and expending $2,000,000 of exploration work over the next four years. To date Morella is current with its obligations under the formal agreement ratified on October 12th 2021, having paid the initial $50,000 on signing the LOI, the $100,000 due on signing the formal agreement, and all anniversary payments since, and has issued a total of 55,560,526 shares of Morella (1MC:ASX, Altaf:OTC-QB) common stock to date. Morella has completed Passive Seismic and Magneto-telluric surveys, have permitted 8 drill sites, installed surface casing on the first site on the southern block, while conducting ongoing tests for amenability to direct lithium extraction (DLE). Drilling commenced in early October 2023, to the northeast of the playa, proximal to but away from the area of known mineralization. Only moderate lithium mineralization was encountered in the 2023 drillhole in both clays and brines.

In addition to the cash and share payments under the Option Agreement, Morella is to perform and exploration and development work on the property in the value of:

Year 1: |

| $ | 200,000 |

|

Year 2: |

| $ | 400,000 |

|

Year 3: |

| $ | 600,000 |

|

Year 4: |

| $ | 800,000 |

|

Under the Option Agreement Morella is the operator of the Fish Lake Valley Project and is responsible for all exploration efforts. Fish Lake Valley Project is an early-stage exploration property and is currently permitted under a BLM Notice of Intent (NOI) level permit. This permit limits surface disturbance to 5 acres or less.

Fish Lake Valley does not currently have any Measured, Indicated, or Inferred Resources calculated, nor does Fish Lake Valley have any Proven or Probable Resources.

| 15 |

| Table of contents |

Table 1 to Paragraph (b) – Summary Mineral Resources at End of the Fiscal Year Ended December 31, 2023.

| Measured Mineral Resources | Indicated Mineral Resources | Measured + Indicated Mineral Resources | Inferred Mineral Resources | ||||

| Amount | Grade/Quality | Amount | Grade/Quality | Amount | Grade/Quality | Amount | Grade/Quality |

Lithium

| Nil

| N/A

| Nil

| N/A

| Nil

| N/A

| Nil

| N/A

|

Table 1 to Paragraph (b) – Summary Mineral Reserves at End of the Fiscal Year Ended December 31, 2023.

| Proven Mineral Reserves | Probable Mineral Reserves | Total Mineral Reserves |

| Proven Mineral Reserves | Probable Mineral Reserves |

| Amount | Grade/Quality | Amount |

| Amount | Grade/Quality |

Lithium

| Nil

| N/A

| Nil

| Lithium

| Nil

| N/A

|

Fish Lake Valley lithium-brine project, located in west Esmeralda County, Nevada. The project area was the scene of historical boron from brine production but is currently at an early stage of exploration. Drilling and other exploratory work has occurred on the property since 2009 When Lithium Corp acquired the property.

The Fish Lake Valley property is in Esmeralda County, west central Nevada, approximately 18 miles from the California border. It is roughly 37 miles to the west-southwest of Tonopah Nevada, 37 miles north-northeast of Bishop California, and 174 miles to the northwest of Las Vegas Nevada, the largest population center in the region. Using the Public Land Survey System, the center of the property is Township 1S, Range 36E, Section 11, Mount Diablo Meridian.

The infrastructure is excellent in the general area of the Fish Lake Valley prospect. Power is available along highway 264 which runs north to south some 8 miles to the west of the property. The capacity of the line is unknown however it does appear on government issued maps as being equal to or greater than 55 kilovolts to the south of the village of Dyer. There are defined geothermal resources around the prospect. Should lithium production be established in the valley it may present an opportunity to the company who originally defined these geothermal resources to continue to the development stage. Abundant fresh water is available in the valley to the south of the northern playa. Most supplies are available in Tonopah which is approximately 75 miles by road from the property. Also, sufficient manpower is available in the region, and some personnel exist locally with training specific to lithium brine processing due to the proximity of the property to Albemarle’s Silver Peak operation. The property does have patchy cell phone service from two different providers. Las Vegas’ Harry Reid International Airport is 249 miles by road to the southeast of the property, while Reno-Tahoe International Airport is 213 miles by road to the northwest, and Elko, NV (which is an important mining supply center) is approximately 334 miles by road from the property. The playa or claim block area should be large enough to accommodate a production facility like that found at Silver Peak, and there are several potential processing plant sites in the area.

Lithium Corporation owns 100% of the property totaling 297 placer claims and 10,972 acres. The original claims were staked by Nevada-Alaska Corp and Optioned to Lithium Corp in an Agreement in which Lithium Corp acquired 100% interest in the claims with no underlying royalties. 86 Association Placer claims were Optioned to Morella Corp and an additional 211 placer claims were staked by Morella and claimed in the name of Morella. Lithium Corp’s Option Agreement with Morella (formerly Altura Mining Limited) does state that any additional staking in the project area is to be included as part of the Option Agreement and reverts to Lithium Corp if the Option Agreement is terminated. The claims are named with a prefix of letters and a number; the prefixes are FL, FLN, FLW, LI, and FLV. The claims have all been staked and filed on BLM managed public land. In order to maintain the claims an annual fee must be paid to the BLM on a per claim basis.

| 16 |

| Table of contents |

(2)

Most of the the property’s present condition it’s natural state except for two drill pads constructed by Morella Corp. The drilling conducted by Morella was bonded with the State of Nevada and the pads will be deconstructed and the ground reclaimed to it’s natural state once Morella is through with the drill pads. The property is in exploration stage and is expected to need substantial further work and permitting to progress to delineation or development stage.

There is not any equipment currently on the property as drilling operations are not active now and no facilities have been built on the property.

Because exploration expenditures are expensed rather than accrued the current book value of Fish Lake Valley Project as reported on Lithium Corporation’s financial statements is zero. There are no processing plant or equipment on the property so no book value is assigned for processing plants or equipment.

The property was developed as a borate producer sometime in the late 1860’s, with the earliest record of production in 1873. Production by 1875 was in the order of 1.814 tonnes (2 tons) of concentrated borax daily. Operations ceased sometime prior to the 1900’s and there is no record of any further activity or exploration until the 1970’s, when interest in lithium brines was high due to the discovery and eventual development of the Silver Peak deposit in nearby Clayton Valley. During the 1970’s the USGS conducted some lithium focused exploration in the general area and drilled several holes on the periphery of the playa. During the 1980’s US Borax discovered the Cave Springs boron/lithium clay deposits which are a few kilometres to the east of the Fish Lake Valley playa. These deposits were called the Borate Hills and were being explored during 2011 by American Lithium in a joint venture with Japan Oil and Gas (JOGMEC). Recently the property has become known as the Rhyolite Ridge Lithium-Boron Project which is being developed by ASX-listed Ioneer Limited.

Since Lithium Corporation’s optioning of the property in 2009 the following work has been conducted on the property:

| · | Surficial sediment sampling – 49 grid sediment samples were collected, and a further 32 sediment samples from discrete points on the property in 2009 and early 2010. |

| · | Preliminary water sampling 2009-10 – 9 water samples collected. |

| · | Surficial sediment temperature and pH/ORP survey, March 2010. |

| · | SP gradient surveys on the northern playa March 2010, a total of 8.525-line km surveyed. Also, a 1 km line of long-wire SP surveying was completed on a line where a gradient survey was performed earlier. |

| · | Gravity survey of the southern playa in May 2010 – an area of approximately 6 km2 was investigated via high-definition gravity. Follow-up surveying was completed in October 2011 and a further 30 stations were read. The northern playa was too wet to access for survey work. |

| · | Near surface brine and sediment sampling program in March 2011 – 39 brine samples. |

| · | Gravity survey of the northern playa in August 2011. An abortive attempt was made to survey the northern playa where 22 stations were setup on the periphery. The northern playa was too wet to survey. |

| · | Direct push drilling program in October 2011, included 41 holes at 25 sites (1080.77 m) a total of 37 samples collected. |

| · | Direct push drilling program in November 2012, included 19 holes at 17 sites (362.97 m). |

| · | a total of 19 samples collected. |

| · | Confirmatory and expanded hand auger drill hole brine sampling by American Lithium Corporation in 2016. A total of 154 samples collected. |

| · | Geological and Geophysical collaboration between American Lithium Corporation and University of Texas at Dallas, August 2016. |

| · | Drilling of a deep sonic drill hole (L-16-13A) on the property to the east of the margin of the playa, south of the area of strongest lithium/boron/potassium mineralization in September 2016. |

| 17 |

| Table of contents |

Approximately $25 million dollars has been spent on geothermal exploration in the general area (personal communication J. Demonyaz) since the 1980’s, and two deep oil exploration holes were drilled immediately to the west-southwest of the claim area. Lithium Corporation’s property was acquired by staking by Nevada Alaska and others in mid-2009, and subsequently optioned to Lithium Corporation, who joint ventured it with American Lithium Corporation in 2016. The property was returned in 2019 and is now under option to Morella Corp (formerly Altura Mining Limited). Since optioning the property from Lithium Corp, Morella Corp has conducted a Passive Seismic Geophysical Survey, Direct Lithium Extraction (DLE) Process Development Work, a Magnetotelluric Geophysical survey, and a drill program.

There are no known encumbrances to the property. To our knowledge Morella Corp has not pursued additional permitting for future exploration. Once the next stage of exploration and budgeting has been determined permitting is expected to take no more than 15 days from the time the permit application is submitted to the BLM. Key permit conditions are generally bonding of planned disturbances. No violations or fines are expected or normally incurred at this stage of exploration as long as the operator executes the plan in the Notice of Intent that is submitted to the BLM.

San Emidio Property

The San Emidio property, located in Washoe County in northwestern Nevada, was acquired through the staking of claims in September 2011, and has expanded and contracted over time depending on the state of the lithium carbonate market. Currently the Company holds 35 - 80-acre, Association Placer claims here covering an area of approximately 2,800 acres (1133 hectares). The property is approximately 65 miles north-northeast of Reno, Nevada, and has excellent infrastructure.

We identified this prospect during 2009, and 2010 through surficial geochemical sampling, and geological interpretation. The early reconnaissance sampling determined that anomalous values for lithium occur in sediments over a good portion of the playa. Our company conducted near-surface brine sampling in the spring of 2011, and a high resolution gravity geophysical survey in summer/fall 2011. Our company then permitted a 7 hole drilling program with the Bureau of Land Management in late fall 2011, and a direct push drill program was commenced in early February 2012. Drilling here delineated a narrow elongated shallow brine reservoir which is greater than 2.5 miles length, somewhat distal to the basinal feature outlined by the earlier gravity survey. The anomaly aligns with the present day topographical low in the valley, which could be the result of extension along a north-easterly trending fault. Two values of over 20 milligrams/liter lithium were obtained from two shallow direct push probe holes located centrally in this brine anomaly.

| 18 |

| Table of contents |

We drilled this prospect in late October 2012, further testing the area of the property in the vicinity where prior exploration by our company discovered elevated lithium levels in subsurface brines. During the 2012 program a total of 856 feet (260.89 meters) was drilled at 8 discrete sites. The deepest hole was 160 feet (48.76 meters), and the shallowest hole that produced brine was 90 feet (27.43 meters). The average depth of the seven hole program was 107 feet (32.61 meters). The program better defined the lithium-in-brine anomaly that was discovered in early 2012. This anomaly is approximately 0.6 miles (370 meters) wide at its widest point by more than 2 miles (3 kilometers) long. The peak value seen within the anomaly is 23.7 mg/l lithium, which is 10 to 20 times background levels outside the anomaly. Our company believes that, much like Fish Lake Valley, the playa at San Emidio may be conducive to the formation of a “Silver Peak” style lithium brine deposit, and the recent drilling indicates that the anomaly occurs at or near the intersection of several faults that may have provided the structural setting necessary for the formation of a lithium-in-brine deposit at depth.

Our company entered into an exploration earn-in agreement on the property on May 3, 2016 with 1067323 B.C. Ltd., wherein the Optionee was to pay an initial $100,000 and issue 100,000 shares within 30 days of a “Going Public Transaction”. 1067323 subsequently merged with American Lithium Corp., who then assumed the duties of the Optionee, and fulfilled the initial obligations. The further terms of the agreement were that American Lithium was to issue 100,000 shares to Lithium Corporation on or before both the first & second anniversaries of the going public transaction. Additionally American Lithium was to conduct $100,000 exploration work in year 1, $200,000 in year 2, and $300,000 in year 3. On fulfillment of all its obligations American Lithium would have earned an 80% interest in the property. The Optionee also had the option to earn a further 20% interest in the property by paying $1,000,000 to the company within 36 months of the exercise of the initial earn-in. If American Lithium had exercised its right with respect to the subsequent earn-in then Lithium Corporation’s interest would have reverted to a 2.5% Net Smelter Revenue (NSR) interest. American Lithium then could have purchased one half of the NSR (1.25%) for $1,000,000 at any time thereafter.

In June 2018, the Company received notification that the purchaser was relinquishing any right to earn an interest in the property and, as such, $202,901 was taken into income. During the year-ended December 31, 2019, the Company recorded a $217,668 allowance for the property which then had a net book value of $Nil.

Lithium Corporation was granted a drilling permit in 2019 to drill three drill holes here, and had intended to drill in 2020, however the weak market for lithium carbonate precluded expending capital on this project, and so drilling was delayed until such time as the market picked up again.

On September 16th 2021 Lithium Corporation signed an agreement with Surge Battery Metals whereby Surge may earn an 80% interest in the Company’s San Emidio lithium-in-brine prospect in Washoe County Nevada, by paying an initial $50,000 and issuing 200,000 shares of Surge (TSX-V:Nili). Surge had undertaken to make payments of $620,000 in cash and stock over 5 years while incurring expenditures on the property of $1,000,000 over that period. Upon fulfillment of the aforementioned commitments Surge would have been deemed to have earned their undivided 80% interest and could have formed a joint venture with the Company. Surge Battery Metals completed some geochemical work on the prospect block and gave Lithium Corporation formal notice in Summer 2022 that they were relinquishing all interest in the property. In Fall 2022 the Company completed a Controlled Source Audio-Magnetotelluric (CSAMT) survey on the property and is currently actively searching for a Joint Venture Partner for this prospect.

BC Sugar Flake Graphite Property

On June 6, 2013, we entered into a mining claim sale agreement with Herb Hyder wherein Mr. Hyder agreed to sell to our company a 50.829 acre (20.57 hectare) claim located in the Cherryville area of British Columbia. As consideration for the purchase of the property, we issued 250,000 shares of our company’s common stock to Mr. Hyder. In addition to the acquired claim, our company staked or acquired another 13 claims at various times over the subsequent months, to bring the total area held under tenure to approximately 19,816 acres (8,020 hectares). Since that time the company has let all but what appears to be the most prospective claims lapse, and currently the company holds one title – the “Heavy Weather” claim that is 1422 acres (575.67 hectares) in size. The flake graphite mineralization of interest here is hosted predominately in graphitic quartz/biotite, and lesser graphitic calc-silicate gneisses. The rocks and mineralization in the general area of the BC Sugar prospect are similar to the host rocks in the area of the crystal graphite deposit 55 miles (90 kms) to the southeast that is being mined by Eagle Graphite.

| 19 |

| Table of contents |