As filed with the Securities and Exchange Commission on March 9, 2018

1933 Act File No. 333-222736

U.S. SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-14

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

Pre-Effective Amendment No. 1

Post-Effective Amendment No. o

(Check appropriate box or boxes)

ABERDEEN FUNDS

(Exact Name of Registrant as Specified in Charter)

1735 Market Street, 32nd Floor

Philadelphia, Pennsylvania 19103

(Address of Principal Executive Offices) (Zip Code)

(866) 667-9231

(Registrant’s Telephone Number, including Area Code)

Lucia Sitar, Esquire

c/o Aberdeen Asset Management Inc.

1735 Market Street, 32nd Floor

Philadelphia, Pennsylvania 19103

(Name and Address of Agent for Service of Process)

With Copies to:

Elliot Gluck, Esquire

Willkie Farr & Gallagher LLP

787 Seventh Avenue

New York, New York 10019

Approximate Date of Proposed Public Offering: As soon as practicable after this Registration Statement becomes effective under the Securities Act of 1933.

Title of Securities Being Registered: Shares of Beneficial Interest, no par value.

An indefinite amount of Registrant’s securities has been registered under the Securities Act of 1933 pursuant to Rule 24f-2 under the Investment Company Act of 1940. In reliance upon such Rule, no filing fee is being paid at this time.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to Section 8(a), may determine.

ALPINE EQUITY TRUST

Alpine Global Infrastructure Fund

Alpine International Real Estate Equity Fund

Alpine Realty Income & Growth Fund

ALPINE INCOME TRUST

Alpine High Yield Managed Duration Municipal Fund

Alpine Ultra Short Municipal Income Fund

ALPINE SERIES TRUST

Alpine Dynamic Dividend Fund

Alpine Rising Dividend Fund

c/o DST Asset Manager Solutions, Inc.

PO Box 8061

Boston, MA 02266

1-888-785-5578

IMPORTANT SHAREHOLDER INFORMATION

We are pleased to enclose a notice, combined proxy statement/prospectus (the "Proxy Statement/Prospectus"), and proxy card(s) for a Joint Special Meeting of Shareholders (the "Meeting") relating to Alpine Global Infrastructure Fund, Alpine International Real Estate Equity Fund and Alpine Realty Income & Growth Fund, each a series of Alpine Equity Trust, a Massachusetts business trust; Alpine High Yield Managed Duration Municipal Fund and Alpine Ultra Short Municipal Income Fund, each a series of Alpine Income Trust, a Delaware statutory trust; and Alpine Dynamic Dividend Fund and Alpine Rising Dividend Fund, each a series of Alpine Series Trust, a Delaware statutory trust (each, a "Target Fund" and collectively, the "Target Funds"). The Meeting is scheduled for April 26, 2018 at 11:00 a.m., Eastern Time, at 711 Westchester Avenue, White Plains, New York 10604. At the Meeting, shareholders of each Target Fund will be asked to approve a proposed Agreement and Plan of Reorganization (each, a "Plan of Reorganization" and collectively, the "Plans of Reorganization"), which contemplates the reorganization of the Target Fund into a corresponding newly-created series (each, an "Acquiring Fund", and collectively, the "Acquiring Funds") of Aberdeen Funds, a Delaware statutory trust, as listed in the table below (each, a "Reorganization", and collectively, the "Reorganizations").

| Target Fund |

Acquiring Fund |

||||||

| Alpine Dynamic Dividend Fund |

Aberdeen Dynamic Dividend Fund |

||||||

| Alpine Global Infrastructure Fund |

Aberdeen Global Infrastructure Fund |

||||||

|

Alpine High Yield Managed Duration Municipal Fund |

Aberdeen High Yield Managed Duration Municipal Fund |

||||||

| Alpine International Real Estate Equity Fund |

Aberdeen International Real Estate Equity Fund |

||||||

| Alpine Realty Income & Growth Fund |

Aberdeen Realty Income & Growth Fund |

||||||

| Alpine Rising Dividend Fund |

Aberdeen Income Builder Fund |

||||||

| Alpine Ultra Short Municipal Income Fund |

Aberdeen Ultra Short Municipal Income Fund |

||||||

If the Reorganizations are approved by the Target Funds' shareholders, and certain other conditions are fulfilled, each Target Fund will transfer all of its assets and liabilities to the corresponding Acquiring Fund in exchange for Class A or Institutional Class shares of the Acquiring Fund, which shares will be distributed to the shareholders of the corresponding class of the Target Fund in complete liquidation and dissolution of the Target Fund. Shareholders of the Institutional Class of a Target Fund would receive Institutional Class shares of the corresponding Acquiring Fund and Class A shareholders of a Target Fund would receive Class A shares of the corresponding Acquiring Fund. The Reorganization of one Target Fund is contingent on all of the conditions of the Asset Purchase Agreement being satisfied, including a condition requiring the approval by shareholders of the Reorganizations of the other Target Funds. Therefore, if any of the Reorganizations are not approved by shareholders, and the conditions of the Asset Purchase Agreement are not waived by mutual agreement of the parties, the Reorganizations will not occur and Alpine will continue to serve as investment adviser to the Target Funds.

The Acquiring Funds are newly-organized funds that will commence operations upon consummation of the Reorganizations. The Target Funds would then be dissolved. The Reorganizations are not expected to have any federal income tax consequences for the Target Funds or their shareholders. Each Reorganization is anticipated to provide continuity with a similar investment approach (except for Alpine Rising Dividend Fund, as detailed in the

Proxy Statement/Prospectus) centering on fundamental analysis, micro and macro research, long-term perspective, team-based ethos and shared insights. The attached Proxy Statement/Prospectus is designed to give you more information about the proposals.

After careful consideration, the Boards of Trustees of the Alpine Equity Trust, Alpine Income Trust and Alpine Series Trust each unanimously recommends that shareholders of their corresponding Target Funds vote "FOR" the proposed Plans of Reorganization. Shareholders of record of any of the Target Funds as of the close of business on February 21, 2018 may vote on the Plan(s) of Reorganization corresponding to their Target Fund(s) at the Meeting and any adjournment or postponement thereof.

|

Sincerely, |

|||

|

|

|||

| Samuel A. Lieber, President | |||

|

Alpine Equity Trust Alpine Income Trust Alpine Series Trust |

|||

2

ALPINE EQUITY TRUST

Alpine Global Infrastructure Fund

Alpine International Real Estate Equity Fund Alpine Realty

Income & Growth Fund

ALPINE INCOME TRUST

Alpine High Yield Managed Duration Municipal Fund

Alpine Ultra Short Municipal Income Fund

ALPINE SERIES TRUST

Alpine Dynamic Dividend Fund

Alpine Rising Dividend Fund

NOTICE OF JOINT SPECIAL MEETING OF SHAREHOLDERS

To be held on April 26, 2018

Dear Shareholder:

Notice is hereby given that a Joint Special Meeting of Shareholders (the "Meeting") relating to Alpine Global Infrastructure Fund, Alpine International Real Estate Equity Fund and Alpine Realty Income & Growth Fund, each, a series of Alpine Equity Trust, a Massachusetts business trust; Alpine High Yield Managed Duration Municipal Fund and Alpine Ultra Short Municipal Income Fund, each a series of Alpine Income Trust, a Delaware statutory trust; and Alpine Dynamic Dividend Fund and Alpine Rising Dividend Fund, each a series of Alpine Series Trust, a Delaware statutory trust (each a "Target Fund" and collectively, the "Target Funds"). The Meeting is scheduled for April 26, 2018 at 11:00 a.m., Eastern Time, at 711 Westchester Avenue, White Plains, New York 10604. At the Meeting, shareholders of each Target Fund will be asked to approve a proposed reorganization of the Target Fund into a corresponding newly-created series (each, an "Acquiring Fund", and collectively, the "Acquiring Funds") of Aberdeen Funds, a Delaware statutory trust, as described in the table below.

| Target Fund |

Acquiring Fund |

||||||

| Alpine Dynamic Dividend Fund |

Aberdeen Dynamic Dividend Fund |

||||||

| Alpine Global Infrastructure Fund |

Aberdeen Global Infrastructure Fund |

||||||

|

Alpine High Yield Managed Duration Municipal Fund |

Aberdeen High Yield Managed Duration Municipal Fund |

||||||

| Alpine International Real Estate Equity Fund |

Aberdeen International Real Estate Equity Fund |

||||||

| Alpine Realty Income & Growth Fund |

Aberdeen Realty Income & Growth Fund |

||||||

| Alpine Rising Dividend Fund |

Aberdeen Income Builder Fund |

||||||

| Alpine Ultra Short Municipal Income Fund |

Aberdeen Ultra Short Municipal Income Fund |

||||||

The Meeting is being called by each Target Fund, for the purpose of considering and voting on the following proposal (the "Proposal"):

• to approve an Agreement and Plan of Reorganization (the "Plan of Reorganization") which contemplates the reorganization of the Target Fund into the corresponding Acquiring Fund, which is a series of Aberdeen Funds, and provides that the Target Fund will transfer all of its assets and liabilities to the Acquiring Fund in exchange for shares of certain classes of the Acquiring Fund, which shares will be distributed to the shareholders of the corresponding class of the Target Fund in complete liquidation and dissolution of the Target Fund (the "Reorganization").

The Proposal is described in the attached combined proxy statement/prospectus (the "Proxy Statement/Prospectus").

The Boards of Trustees of the Alpine Equity Trust, Alpine Income Trust and Alpine Series Trust (collectively, the "Boards of Trustees") on behalf of the Target Funds unanimously recommend that you vote in favor of the Proposal.

The enclosed materials provide additional information about the Proposal. Shareholders of record of any of the Target Funds as of the close of business on February 21, 2018 may vote on the Plan(s) of Reorganization

corresponding to their Target Fund(s) at the Meeting and any adjournment or postponement thereof. Whether or not you plan to attend the Meeting in person, please vote your shares. The notice and related proxy materials will be mailed to shareholders on or about 14, 2018.

The Questions and Answers below are provided to assist you in understanding the Proposal.

Please read the accompanying Proxy Statement/Prospectus. Regardless of whether you plan to attend the Meeting, please complete, sign and return promptly the proxy card, so that a quorum will be present and a maximum number of shares may be voted.

Important Notice Regarding the Availability of Proxy Materials for the Joint Special Meeting of Shareholders to Be Held on April 26, 2018: This Notice, the Proxy Statement and the form of proxy card are available on the Internet at https://proxyonline.com/docs/Alpine2018.pdf. On this website, you will be able to access the Notice, the Proxy Statement/Prospectus, the form of proxy card and any amendments or supplements to the foregoing material that are required to be furnished to shareholders.

By Order of the Boards of Trustees,

|

|

|||

| Samuel A. Lieber, President | |||

|

March 12, 2018 |

|||

2

ALPINE EQUITY TRUST

ALPINE INCOME TRUST

ALPINE SERIES TRUST

IMPORTANT NEWS FOR SHAREHOLDERS

The enclosed combined proxy statement/prospectus (the "Proxy Statement/Prospectus") describes proposals to reorganize Alpine Global Infrastructure Fund, Alpine International Real Estate Equity Fund and Alpine Realty Income & Growth Fund (each a series of Alpine Equity Trust), Alpine High Yield Managed Duration Municipal Fund and Alpine Ultra Short Municipal Income Fund (each a series of Alpine Income Trust), and Alpine Dynamic Dividend Fund and Alpine Rising Dividend Fund (each a series of Alpine Series Trust) (each a "Target Fund" and collectively, the "Target Funds") into corresponding newly-created series (each, an "Acquiring Fund", and collectively, the "Acquiring Funds") of Aberdeen Funds (each, a "Reorganization", and collectively, the "Reorganizations"). While we encourage you to read the full text of the enclosed Proxy Statement/Prospectus, here is a brief overview of the proposed Reorganizations. Please refer to the more complete information about the Reorganizations contained elsewhere in the Proxy Statement/Prospectus.

COMMON QUESTIONS ABOUT THE PROPOSED REORGANIZATIONS

Q. Why is a shareholder meeting being held?

A. The Boards of Trustees of the Alpine Equity Trust, Alpine Income Trust and Alpine Series Trust (each, a "Board" and collectively, the "Boards") unanimously approved agreements and plans of reorganization (each, a "Plan of Reorganization", and collectively, the "Plans of Reorganization"), subject to Target Fund shareholder approval, under which each Target Fund would be reorganized into a corresponding newly-created series of Aberdeen Funds that would be managed by Aberdeen Asset Management Inc. ("AAMI"). If shareholders of each Target Fund approve the proposed Plans of Reorganization, and certain other conditions are fulfilled, you would become a shareholder of the respective Acquiring Fund. The Reorganization of one Target Fund is contingent on all of the conditions of the Asset Purchase Agreement being satisfied, including a condition requiring the approval by shareholders of the Reorganizations of the other Target Funds. Therefore, if any of the Reorganizations are not approved by shareholders, and the conditions of the Asset Purchase Agreement are not waived by mutual agreement of the parties, the Reorganizations will not occur and Alpine will continue to serve as investment adviser to the Target Funds.

On December 21, 2017, Alpine Woods Capital Investors, LLC ("Alpine") and Aberdeen Asset Managers Limited ("AAML") entered into a separate agreement (the "Asset Purchase Agreement") pursuant to which AAML will acquire certain assets related to Alpine's business of providing investment management services to the Target Funds and other registered investment companies (the "Business") upon receipt of the necessary approvals of the Plans of Reorganization and satisfaction or waiver of certain other conditions. More specifically, under the Asset Purchase Agreement, Alpine has agreed to transfer to AAML, for a cash payment at the closing of the Asset Transfer (as defined below) and subject to certain exceptions, (i) all right, title and interest of Alpine in and to the accounts, books, files and other records or documents to the extent used in or relating to the Business; (ii) the right to include in AAML's and in the Fund's performance information the investment performance of the Target Funds since the inception of each Target Fund and copies of information necessary to calculate such investment performance; (iii) all claims, causes of action, choses in action, rights of recovery and rights of set-off of any kind to the extent relating to items (i) and (ii) listed above against any person, including any liens, security interest, pledges or other rights to payment or to enforce payment in connection with products or services delivered by Alpine on or prior to the closing date; and (iv) all goodwill of the Business as a going concern together with the rights to represent to third parties that AAML is the successor to the Business. Such transfers hereinafter are referred to collectively as the "Asset Transfer." Samuel A. Lieber, a Trustee who is currently an "interested person" of the Target Funds as that term is defined in the 1940 Act (the "Interested Trustee") and the Trust's President, will benefit from the Asset Transfer as an indirect majority owner of Alpine. None of the Trustees, who are not "interested persons" of the Target Funds (the "Independent Trustees") as that term is defined in the 1940 Act), have any interest in the Asset Transfer and the Boards, including all of the Independent Trustees voting separately, unanimously approved the Plans of Reorganization.

Each Target Fund is not a party to the Asset Purchase Agreement; however, the completion of the Asset Transfer is subject to certain conditions, including shareholder approval by each Target Fund of the proposal described in the Proxy Statement/Prospectus. Therefore, if each Target Fund's shareholders do not approve its Plan of Reorganization at the Meeting or if the other conditions in the Asset Purchase Agreement are not satisfied and the parties to the Asset Purchase Agreement do not mutually agree to waive the shareholder approval condition and/or any other conditions that are not satisfied, then the Asset Transfer will not be completed and the Asset Purchase Agreement will terminate and the Reorganizations will not occur.

Q. How will the Reorganizations affect me?

A. If each Reorganization is approved by the respective Target Fund's shareholders, and certain other conditions are fulfilled, each shareholder will receive shares of the corresponding Acquiring Fund listed in the table below having an aggregate net asset value equal to the aggregate net asset value of the shares of the Target Fund held by that shareholder on the closing date of the Reorganization. Shareholders of the Institutional Class of a Target Fund would receive Institutional Class shares of the corresponding Acquiring Fund and Class A shareholders of a Target Fund would receive Class A shares of the corresponding Acquiring Fund.

| Target Fund |

Acquiring Fund |

||||||

| Alpine Dynamic Dividend Fund |

Aberdeen Dynamic Dividend Fund |

||||||

| Alpine Global Infrastructure Fund |

Aberdeen Global Infrastructure Fund |

||||||

|

Alpine High Yield Managed Duration Municipal Fund |

Aberdeen High Yield Managed Duration Municipal Fund |

||||||

| Alpine International Real Estate Equity Fund |

Aberdeen International Real Estate Equity Fund |

||||||

| Alpine Realty Income & Growth Fund |

Aberdeen Realty Income & Growth Fund |

||||||

| Alpine Rising Dividend Fund |

Aberdeen Income Builder Fund |

||||||

| Alpine Ultra Short Municipal Income Fund |

Aberdeen Ultra Short Municipal Income Fund |

||||||

The Acquiring Funds are newly-created funds that will commence operations upon consummation of the Reorganizations. The Target Funds would then be dissolved. The Reorganizations are not expected to have any federal income tax consequences for the Target Funds or their shareholders. The attached Proxy Statement/Prospectus is designed to give you more information about the proposals.

Q. Do the Acquiring Funds have different service providers from the Target Funds?

A. Each Acquiring Fund will offer the same shareholder services to those offered by Target Fund. AAMI serves as the adviser for all of the Acquiring Funds and Aberdeen Asset Managers Limited ("AAML"), which is an affiliate of AAMI, serves as the sub-adviser to certain of the Acquiring Funds and they anticipate providing advisory services that are substantially similar in nature and quality to the nature and quality of the advisory services that are currently provided to each Target Fund by Alpine. The following table outlines the service providers for each of the Target Funds and the comparable service providers for the Acquiring Funds.

|

Target Fund |

Acquiring Fund |

||||||||||

|

Adviser |

Alpine |

AAMI |

|||||||||

|

Subadviser |

None |

None (Aberdeen High Yield Managed Duration Municipal Fund, Aberdeen Income Builder Fund and Aberdeen Ultra Short Municipal Income Fund) Aberdeen Asset Managers Limited (Aberdeen Dynamic Dividend Fund, Aberdeen Global Infrastructure Fund, Aberdeen International Real Estate Equity Fund and Alpine Realty Income & Growth Fund) |

|||||||||

|

Administrator |

State Street Bank and Trust Company ("State Street") |

AAMI (State Street serves as subadministrator) |

|||||||||

|

Transfer Agent |

DST Asset Manager Solutions, Inc. |

DST Asset Manager Solutions, Inc. |

|||||||||

|

Custodian |

State Street |

State Street |

|||||||||

|

Distributor |

Quasar Distributors, LLC |

Aberdeen Fund Distributors LLC |

|||||||||

|

Auditor |

Ernst & Young LLP |

KPMG LLP |

|||||||||

2

Q. How do the fees of the Acquiring Funds compare to those of the Target Funds?

A. Although each Acquiring Fund is expected to have a gross expense ratio approximately 6 basis points higher than its corresponding Target Fund due to a higher administration fee, each Acquiring Fund is expected to have the same or a lower net expense ratio than its corresponding Target Fund. AAMI has proposed an expense limitation agreement whereby AAMI would agree to limit fund expenses (excluding interest, brokerage commissions, acquired fund fees and expenses and extraordinary expenses of a Fund) with respect to each Acquiring Fund until at least the end of the two year period following the date that the corresponding Target Fund completed its Reorganization into the Acquiring Fund. These limits are the same or lower than the expense limits currently in place for the Target Funds. Each Acquiring Fund will be authorized to reimburse AAMI for management fees limited and/or for expenses paid by AAMI pursuant to the expense limitation agreement, provided, however, that any reimbursements must be paid at a date not more than three years after the date when AAMI limited the fees or reimbursed the expenses and the reimbursements do not cause the Fund to exceed the lesser of the applicable expense limitation in the agreement at the time the fees were limited or expenses are paid or the applicable expense limitation in effect at the time the expenses are being recouped by AAMI.

As indicated above, it is anticipated that the Acquiring Funds will pay service providers roughly equivalent to or lower fees than fees paid to service providers by the Target Funds, with the exception of administration fees. Acquiring Funds would pay 0.08% of net assets for administration services compared to the Target Funds rate of 0.02% of net assets.

Each Acquiring Fund would apply the same total advisory fee rate as currently applied to the Target Fund, but for the sub-advised Acquiring Funds, a portion of the fee would be shared with the sub-adviser.

Under the Administrative Services Plan of the Acquiring Funds, each Acquiring Fund may pay a broker-dealer or other intermediary a maximum annual administrative services fee of 0.25% for Class A shares (or under an amendment to the Administrative Services Plan that is in effect until at least February 28, 2019, a maximum of 0.15% for contracts with fees that are calculated as percentage of Fund assets and a maximum of $16 per account for contracts with fees that are calculated on a dollar per account basis). The Target Funds do not have an administrative services plan, but the Target Funds have entered into agreements with certain financial intermediaries pursuant to which the Target Funds pay fees to these financial intermediaries for services such as networking, sub-transfer agency, administrative, recordkeeping and shareholder services, as described in more detail in "Comparison of Target Funds and Acquiring Funds—Sub-Transfer Agency Fees" in this Proxy Statement/Prospectus. It is not anticipated that any such differences in these such expenses will materially impact the Acquiring Funds' gross expense ratios. The expense limitation agreement proposed by AAMI would include within the cap administrative service fees, sub-transfer agency fees and other related intermediary fees, so any such differences would not result in any increase in net expense ratios for the Target Funds.

Class A shares of the Target Funds and Class A Shares of the Acquiring Funds have slightly different contingent deferred sales charges. Class A shares of the Aberdeen High Yield Managed Duration Municipal Fund and Aberdeen Ultra Short Municipal Income Fund have a contingent deferred sales load of 0.75%, while the remaining Acquiring Funds have a contingent deferred sales load of 1.00%. This contingent deferred sales charge is only applicable in the event that a Class A shareholder bought shares without paying a sales charge (and is not otherwise eligible to purchase Class A shares without a sales charge), redeems within 18 months of purchase and a finder's fee was paid. This compares to a contingent deferred sales charge of 1.00% for shares of the Target Funds if shares are redeemed within 12 months of purchase as part of an investment greater than $1,000,000 if no front-end sales charge was paid at the time of purchase and a concession was paid to the financial intermediary or dealer, except that there is a contingent deferred sales charge of 0.50% applicable to shares of the Alpine High Yield Managed Duration Municipal Fund if shares are redeemed within 12 months of purchase as part of an investment greater than $250,000 if no front-end sales charge was paid at the time of purchase and a concession was paid to the financial intermediary or dealer and there is no contingent deferred sales charge applicable to shares of the Alpine Ultra Short Municipal Income Fund. Following the Reorganizations, Target Fund shareholders will only be subject to a CDSC on any purchased Class A shares of the Acquiring Funds and will not be subject to a CDSC on shares of the Acquiring Funds received in the Reorganizations.

3

The Target Funds impose a redemption fee when shares are redeemed within less than 60 days of purchase. The Alpine High Yield Managed Duration Municipal Fund charges a redemption fee of 0.75%, the Alpine Ultra Short Municipal Income Fund charges a redemption fee of 0.25% and each other Target Fund charges a redemption fee of 1.00%. The Acquiring Funds do not charge such a fee. Conversely, the Acquiring Funds charge a small account fee of $5 quarterly fee (with an annual maximum of $20 per account) on accounts with balances below $1,000, while the Target Funds do not charge such a fee. This fee will be applicable to accounts of former Target Fund shareholders following the Reorganizations.

It is anticipated that the Target Funds could potentially benefit from being part of a larger fund complex due to economies of scale from the spreading of complex-wide costs over a larger asset base. There can be no assurance, however, that such savings will be realized.

Q. How does the Board recommend that I vote?

A. For the reasons summarized in this Proxy Statement/Prospectus, each Board recommends that shareholders vote FOR the proposal to approve the Plan of Reorganization of their Target Fund. If no instructions are indicated on your proxy, the representatives holding proxies will vote in accordance with the recommendations of your Target Fund's Board.

Q. Are there any significant differences between the investment objectives, principal investment strategies and related policies of the Target Funds and the Acquiring Funds?

A. The Target Funds and Acquiring Funds have the same investment objectives, principal strategies and related policies, with one exception. The Alpine Rising Dividend Fund would be reorganized into the Aberdeen Income Builder Fund, which has the same investment objective but different principal investment strategies, but otherwise has similar investment policies and the same fundamental investment restrictions. Although the Alpine Rising Dividend Fund and the Aberdeen Income Builder Fund have the same investment objective, the Alpine Rising Dividend Fund's investment objective is fundamental and cannot be changed without the approval of a majority of outstanding shares, while the Aberdeen Income Builder Fund's investment objective is non-fundamental and may be changed by the Board upon 60 days' prior notice to shareholders. The below chart provides the investment objective and a summary of the principal investment strategy of the Alpine Rising Dividend Fund Target Fund compared to the corresponding Acquiring Fund, the Aberdeen Income Builder Fund.

|

Fund |

Alpine Rising Dividend Fund (Target Fund) |

Aberdeen Income Builder Fund (Acquiring Fund) |

|||||||||

|

Investment Objective |

The Alpine Rising Dividend Fund seeks income. Long-term growth of capital is a secondary objective. |

The Aberdeen Income Builder Fund seeks income. Long term growth of capital is a secondary objective. |

|||||||||

|

Principal Investment Strategy |

Under normal circumstances, the Rising Dividend Fund invests at least 80% of its net assets in the equity securities of certain domestic and foreign companies that pay dividends. This includes companies that have announced a special dividend or announced that they will pay dividends within six months. The Fund seeks to provide dividend income without regard to whether the dividends qualify for the reduced U.S. federal income tax rates applicable to qualified dividends under the Internal Revenue Code of 1986, as amended (the "Code"). Under normal circumstances, the Fund expects to invest in the equity securities of U.S. issuers, as well as in non-U.S. issuers. |

Under normal circumstances, the Income Builder Fund invests at least 80% of its net assets in equity and fixed income securities of domestic and foreign issuers. Net assets include the amounts of any borrowings for investment purposes. The Fund uses a multi-cap, multi-sector, multi-style approach to invest in the securities of issuers of any capitalization level and in any sector or industry. In order to achieve its investment objectives, the Fund seeks investments in income-producing instruments and equity securities that have the potential to provide income and/or long term growth of capital. In order to generate income, the Fund may use a dividend capture strategy where it purchases shares prior to the record date for a dividend and sells them within a short time thereafter. The Fund invests in the fixed income and equity securities of U.S. and foreign issuers, including those in emerging markets. |

|||||||||

4

For other information concerning how the Acquiring Funds compare to the Target Funds, please see "How do the Investment Objectives, Investment Strategies and Investment Restrictions of the Target Funds and Acquiring Funds Compare" in the Proxy Statement/Prospectus.

Q. Will I have to pay any sales load, charge or other commission in connection with a Reorganization?

A. No. No sales load, contingent deferred sales charge, commission, redemption fee or other transactional fee will be charged by a Target Fund as a result of a Reorganization. You will receive shares of the corresponding Acquiring Fund having an aggregate net asset value equal to the aggregate net asset value of the shares of the Target Fund that you own as of the close of business on the day of the closing of the Reorganizations (the "Closing Date").

Q. What classes of shares will I receive?

A. You will receive shares of the same class of the Acquiring Fund as you hold in the Target Fund as of the Closing Date. No matter which class of shares you hold in a Target Fund, you will receive shares of the Acquiring Fund having an aggregate net asset value equal to the aggregate net asset value of the shares of the Target Fund that you own as of the close of business on the Closing Date.

Q. What if I redeem or exchange my shares before the closing of the Reorganization with respect to my Target Fund?

A. Redemptions or exchanges of Target Fund shares that occur before the closing of each Reorganization will be processed according to your Target Fund's policies and procedures in effect at the time of the redemption or exchange.

Q. Can I purchase additional shares in a Target Fund prior to a Reorganization?

A. Institutional Class and Class A shares of each Target Fund are currently available for purchase and incoming exchanges. However, if the shareholders of each Target Fund approve its Reorganization, and certain other conditions are fulfilled, each Target Fund will close to new purchases and exchanges approximately two business days prior to the Closing Date of the Reorganizations.

Q. Will I have to pay any taxes as a result of a Reorganization?

A. Each Reorganization is intended to qualify as a tax-free transaction for federal income tax purposes. Assuming each Reorganization qualifies for such treatment, you will not recognize a gain or loss for federal income tax purposes as a direct result of a Reorganization. As a condition to the closing of each Reorganization, each Target Fund and each Acquiring Fund will receive an opinion of Willkie Farr & Gallagher LLP to the effect that the Reorganization will qualify for such treatment. Opinions of counsel are not binding on the Internal Revenue Service or the courts. You should talk to your tax adviser about any state, local and other tax consequences of the Reorganization with respect to your Target Fund.

If shareholders of each Target Fund approve the Reorganizations, your Target Fund will distribute its realized capital gains to shareholders prior to the Closing Date. Fund shareholders who do not hold their shares in a tax-advantaged account will receive a taxable capital gain distribution as a result.

Q. Who will pay for each Reorganization?

A. Fund shareholders will not bear the costs of the Reorganizations. The costs solely and directly related to the Reorganizations will be paid by AAMI (or an affiliate) and Alpine, the investment advisers to the Acquiring Funds and Target Funds, respectively, including any proxy solicitation costs (the "Reorganization Costs"), on behalf of each Target Fund and each Acquiring Fund. Alpine, on behalf of the Target Funds, has retained AST Fund Solutions, LLC, a proxy solicitation firm, to assist in the solicitation of proxies and the cost for such solicitation services will be borne by AAMI and Alpine.

Q. How does the Board recommend that I vote?

A. Each Board, including all of the independent Board members, unanimously recommends that you vote FOR the Reorganization with respect to your Target Fund.

Q. What happens if the Reorganization of my Target Fund is not approved?

A. If the shareholders of your Target Fund do not approve the Reorganization with respect to your Target Fund, then you will remain a shareholder of the Target Fund and the Board may consider other alternatives. Each

5

Reorganization is contingent upon the satisfaction of closing conditions in the Asset Purchase Agreement, including the condition that the shareholders of each of the Target Funds approve the Reorganizations. Therefore, if shareholders of any of the Target Funds do not receive shareholder approval of their Reorganizations or if any other conditions of the Asset Purchase Agreement are not met and the parties to the Asset Purchase Agreement do not mutually agree to waive the unsatisfied condition(s), the Reorganizations will not occur and Alpine will continue to serve as investment adviser to the Target Funds.

Q. I am an investor who holds a small number of shares. Why should I vote?

A. Your vote makes a difference. If many shareholders like you fail to vote their proxies, a Target Fund may not receive enough votes to go forward with the Meeting, and additional costs will be incurred to solicit additional proxies. You should be aware that the principals of Alpine and their family members and Alpine's affiliates beneficially own and have voting authority of over 54% of the Alpine Rising Dividend Fund's outstanding voting securities and over 48% of the Alpine International Real Estate Equity Fund's outstanding voting securities (each as of December 31, 2017), and such shares are expected to be voted in favor of the Reorganization of those Funds, which will control the outcome of the vote. The principals of Alpine and their family members and Alpine's affiliates also beneficially own and have voting authority of over 9% of the Alpine Dynamic Dividend Fund's outstanding voting securities, over 9% of the Alpine High Yield Managed Duration Municipal Fund's outstanding voting securities, over 7% of the Alpine Ultra Short Municipal Income Fund's outstanding voting securities, over 9% of the Alpine Realty Income & Growth Fund's outstanding voting securities, and over 14% of the Alpine Global Infrastructure Fund's outstanding voting securities (each as of December 31, 2017), and such shares are expected to be voted in favor of the Reorganization of those Funds. Shares of a Target Fund held by institutions and charitable trusts overseen by the principals of Alpine, but for which they do not maintain a beneficial ownership interest, will be voted in proportion to the total votes received from shareholders who are not principals of Alpine, their family members or affiliates of Alpine. Proxies relating to shares of a Target Fund held by clients of Alpine's affiliates will be passed through to those clients so that those clients will vote with respect to the applicable Reorganization.

Q. When is the Reorganization of my Target Fund expected to happen?

A. If the shareholders of your Target Fund approve the Reorganization with respect to your Target Fund, and each of the other Reorganizations is also approved, and certain other conditions are fulfilled, at the Meeting on April 26, 2018, the Closing Date of the Reorganizations is expected to occur during the second quarter of 2018.

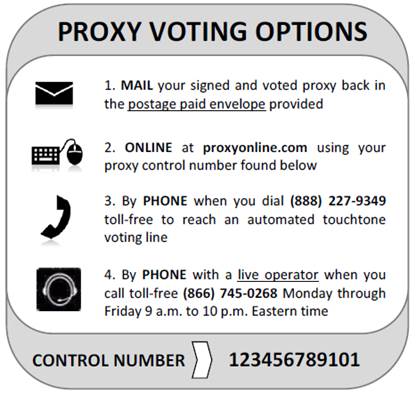

Q. How can I vote or authorize a proxy to vote?

A. In addition to voting in person at the Meeting or authorizing a proxy to vote by mail by returning the enclosed proxy card, you also may authorize a proxy to vote by either touch-tone telephone or online via the Internet, as follows:

| To authorize a proxy to vote by touch-tone telephone: |

To authorize a proxy to vote by Internet: |

||||||

|

Read the Proxy Statement/Prospectus and have your Proxy Card at hand. |

Read the Proxy Statement/Prospectus and have your Proxy Card at hand. |

||||||

|

Call the toll-free number that appears on your Proxy Card. |

Go to the website that appears on your Proxy Card. |

||||||

|

Enter the control number set out on the Proxy Card and follow the simple instructions. |

Enter the control number set out on the Proxy Card and follow the simple instructions. |

||||||

Q. Who gets to vote?

A. If you owned shares of a Target Fund at the close of business on February 21, 2018, you are entitled to vote those shares, even if you are no longer a shareholder of that Target Fund.

Q. What if I hold my shares in "street name"?

A. You should follow the voting directions provided by your bank, brokerage firm or other nominee. You may complete and mail a voting instruction form to your bank, brokerage firm or other nominee or, in most cases, submit voting instructions by telephone or over the Internet to your bank, brokerage firm or other nominee. If you provide specific voting instructions by mail, telephone or the Internet, your bank, brokerage firm or other nominee will vote your shares as you have directed. Please note that if you wish to vote in person at the Meeting, you must obtain a "legal" proxy from your bank, brokerage firm or other nominee.

6

Q. Whom do I call if I have questions?

A. If you need more information or have any questions about how to authorize a proxy to cast your vote, please call AST Fund Solutions, LLC, each Target Fund's proxy solicitor, at (866) 745-0268.

Your vote is important. Please authorize a proxy to vote promptly to avoid the additional expense of another solicitation.

TO AVOID UNNECESSARY EXPENSE OF FURTHER SOLICITATION, WE URGE YOU to indicate voting instructions on the enclosed proxy card(s), date and sign it and return it promptly in the envelope provided, no matter how large or small your holdings may be.

INSTRUCTIONS FOR SIGNING PROXY CARDS

The following general rules for signing proxy cards may be of assistance to you and avoid the time and expense to the Target Funds involved in validating your vote if you fail to sign your proxy card properly.

1. Individual Accounts: Sign your name exactly as it appears in the registration on the proxy card.

2. Joint Accounts: Either party may sign, but the name of the party signing should conform exactly to a name shown in the registration.

3. Other Accounts: The capacity of the individual signing the proxy card should be indicated unless it is reflected in the form of registration. For example:

| REGISTRATION |

VALID SIGNATURES |

||||||

| Corporate Accounts | |||||||

| (1) ABC Corp. |

ABC Corp. (by John Doe, Treasurer) |

||||||

| (2) ABC Corp. |

John Doe, Treasurer |

||||||

| (3) ABC Corp. | |||||||

| c/o John Doe, Treasurer |

John Doe |

||||||

| (4) ABC Corp. Profit Sharing Plan |

John Doe, Trustee |

||||||

7

COMBINED PROXY STATEMENT/PROSPECTUS

March 12, 2018

COMBINED PROXY STATEMENT FOR:

ALPINE EQUITY TRUST

Alpine Global Infrastructure Fund

Alpine International Real Estate Equity Fund

Alpine Realty Income & Growth Fund

ALPINE INCOME TRUST

Alpine High Yield Managed Duration Municipal Fund

Alpine Ultra Short Municipal Income Fund

ALPINE SERIES TRUST

Alpine Dynamic Dividend Fund

Alpine Rising Dividend Fund

(each, a "Target Fund" and collectively, the "Target Funds")

c/o DST Asset Manager Solutions, Inc.

PO Box 8061

Boston, MA 02266

1-888-785-5578

PROSPECTUS FOR:

ABERDEEN FUNDS

Aberdeen Dynamic Dividend Fund

Aberdeen Global Infrastructure Fund

Aberdeen High Yield Managed Duration Municipal Fund

Aberdeen International Real Estate Equity Fund

Aberdeen Realty Income & Growth Fund

Aberdeen Income Builder Fund

Aberdeen Ultra Short Municipal Income Fund

(collectively, the "Acquiring Funds")

c/o Aberdeen Asset Management Inc.

1735 Market Street, 32nd Floor

Philadelphia, PA 19103

(the Target Funds, together with the Acquiring Funds, the "Funds" and each, a "Fund")

COMBINED PROXY STATEMENT/PROSPECTUS

ABERDEEN FUNDS

Aberdeen Dynamic Dividend Fund

Aberdeen Global Infrastructure Fund

Aberdeen High Yield Managed Duration Municipal Fund

Aberdeen International Real Estate Equity Fund

Aberdeen Realty Income & Growth Fund

Aberdeen Income Builder Fund

Aberdeen Ultra Short Municipal Income Fund

(collectively, the "Acquiring Funds")

1735 Market Street, 32nd Floor Philadelphia,

Pennsylvania 19103 (866) 667-9231

Dated March 12, 2018

This combined proxy statement/prospectus (the "Proxy Statement/Prospectus") solicits proxies to be voted at a Joint Special Meeting of Shareholders (the "Meeting") of the Alpine Global Infrastructure Fund, Alpine International Real Estate Equity Fund and Alpine Realty Income & Growth Fund, each a series of Alpine Equity Trust, a Massachusetts business trust; Alpine High Yield Managed Duration Municipal Fund and Alpine Ultra Short Municipal Income Fund, each a series of Alpine Income Trust, a Delaware statutory trust; and Alpine Dynamic Dividend Fund and Alpine Rising Dividend Fund, each a series of Alpine Series Trust, a Delaware statutory trust (each, a "Target Fund" and collectively, the "Target Funds"). The Meeting has been called by the Boards of Trustees (collectively, the "Boards") of Alpine Equity Trust, Alpine Income Trust and Alpine Series Trust (collectively, the "Trusts") where shareholders of each Target Fund will be asked to vote on the following proposal (the "Proposal"):

| Proposal |

Shareholders Entitled to Vote |

||||||

|

To approve an Agreement and Plan of Reorganization (a "Plan of Reorganization") which contemplates the reorganization of the Target Fund into the corresponding Acquiring Fund, which is a series of Aberdeen Funds, and provides that the Target Fund will transfer all of its assets and liabilities to the Acquiring Fund in exchange for shares of certain classes of the Acquiring Fund, which shares will be distributed to the shareholders of the corresponding class of the Target Fund in complete liquidation and dissolution of the Target Fund (the "Reorganization"). |

Shareholders of the Target Funds as of the close of business on February 21, 2018 ("Record Date"). |

||||||

The Meeting is scheduled for April 26, 2018 at 11:00 a.m. Eastern Time, at 711 Westchester Avenue, White Plains, New York 10604. The Boards, on behalf of the Target Funds, are soliciting these proxies. This Proxy Statement/Prospectus will be mailed to shareholders on or about March 14, 2018. The Reorganization of one Target Fund is contingent on all of the conditions of the Asset Purchase Agreement being satisfied, including a condition requiring the approval by shareholders of the Reorganizations of the other Target Funds. Therefore, if any of the Reorganizations are not approved by shareholders, and the conditions of the Asset Purchase Agreement are not waived by mutual agreement of the parties, the Reorganizations will not occur and Alpine will continue to serve as investment adviser to the Target Funds.

Each Plan of Reorganization contemplates the Reorganization of each Target Fund and its share classes into the corresponding Acquiring Fund and its share classes as set out below:

|

Target Funds Alpine Dynamic Dividend Fund |

Acquiring Funds Aberdeen Dynamic Dividend Fund |

||||||

| Class A |

Class A |

||||||

| Institutional Class |

Institutional Class |

||||||

| Alpine Global Infrastructure Fund |

Aberdeen Global Infrastructure Fund |

||||||

| Class A |

Class A |

||||||

| Institutional Class |

Institutional Class |

||||||

|

Alpine High Yield Managed Duration Municipal Fund |

Aberdeen High Yield Managed Duration Municipal Fund |

||||||

| Class A |

Class A |

||||||

| Institutional Class |

Institutional Class |

||||||

| Alpine International Real Estate Equity Fund |

Aberdeen International Real Estate Equity Fund |

||||||

| Class A |

Class A |

||||||

| Institutional Class |

Institutional Class |

||||||

| Alpine Realty Income & Growth Fund |

Aberdeen Realty Income & Growth Fund |

||||||

| Class A |

Class A |

||||||

| Institutional Class |

Institutional Class |

||||||

| Alpine Rising Dividend Fund |

Aberdeen Income Builder Fund |

||||||

| Class A |

Class A |

||||||

| Institutional Class |

Institutional Class |

||||||

| Alpine Ultra Short Municipal Income Fund |

Aberdeen Ultra Short Municipal Income Fund |

||||||

| Class A |

Class A |

||||||

| Institutional Class |

Institutional Class |

||||||

The Target Funds and the Acquiring Funds are referred to collectively as the "Funds" and each as a "Fund" in this Proxy Statement/Prospectus.

This Proxy Statement/Prospectus gives you information about your investment in the Target Funds and the Acquiring Funds and other matters that you should know about before voting and investing. It is both the Target Funds' proxy statement for the Meeting and a prospectus for the Acquiring Funds. Please read this Proxy Statement/Prospectus carefully and retain it for future reference.

The following documents containing additional information about the Target Funds and the Acquiring Funds, each having been filed with the Securities and Exchange Commission (the "SEC"), are incorporated by reference into (legally considered to be part of) this Proxy Statement/Prospectus:

• the Statement of Additional Information dated March 12, 2018 (the "Statement of Additional Information") relating to this Proxy Statement/Prospectus;

• the Prospectus of the Alpine Equity Trust and Alpine Series Trust and the Prospectus of the Alpine Income Trust, each dated February 28, 2018 (collectively, the "Target Funds' Statutory Prospectuses");

• the Statement of Additional Information of the Alpine Equity Trust and Alpine Series Trust and the Statement of Additional Information of the Alpine Income Trust, each dated February 28, 2018 (collectively, the "Target Funds' Statements of Additional Information");

• the Aberdeen Funds Statement of Additional Information relating to the Acquiring Funds dated March 7, 2018 (the "Acquiring Funds' Statement of Additional Information" and collectively with the Target Funds' Statements of Additional Information, the "Funds' Statements of Additional Information"); and

• the Annual Report with respect to Alpine Equity Trust and the Annual Report with respect to Alpine Series Trust and Alpine Income Trust, each for the fiscal year ended October 31, 2017.

For more information regarding the Acquiring Funds, the Aberdeen Funds Prospectus relating to the Acquiring Funds dated March 7, 2018 (the "Acquiring Funds' Statutory Prospectus" and collectively with the Target Funds' Statutory Prospectuses, the "Funds' Statutory Prospectuses") is on file with the SEC.

The financial highlights for the Target Funds contained in the annual report to shareholders for the fiscal year ended October 31, 2017 are attached to this Proxy Statement/Prospectus as Exhibit E.

The Acquiring Funds' documents noted above are on file with the SEC. The Funds are subject to the informational requirements of the Securities Exchange Act of 1934, as amended, and the Investment Company Act of 1940, as amended (the "1940 Act") and in accordance therewith, file reports and other information,

ii

including proxy materials and charter documents, with the SEC. Copies of the foregoing and any more recent reports filed after the date hereof may be obtained without charge by calling or writing:

Aberdeen Funds

1735 Market Street, 32nd Floor

Philadelphia, Pennsylvania 19103 (866) 667-9231

The Target Funds' documents noted above are on file with the SEC. The Funds are subject to the informational requirements of the Securities Exchange Act of 1934, as amended, and the Investment Company Act of 1940, as amended (the "1940 Act") and in accordance therewith, file reports and other information, including proxy materials and charter documents, with the SEC. Copies of the foregoing and any more recent reports filed after the date hereof may be obtained without charge by calling or writing:

Alpine Funds

c/o DST Asset Manager Solutions, Inc.

PO Box 8061

Boston, MA 02266

1-888-785-5578

You also may view or obtain these documents from the SEC as follows:

|

In Person: |

At the SEC's Public Reference Room at 100 F Street, N.E. Washington, DC 20549 |

||||||

|

By Phone: |

(202) 551-8090 | ||||||

|

By Mail: |

Public Reference Room Office of Consumer Affairs and Information Services Securities and Exchange Commission 100 F Street, N.E. Washington, DC 20549 (duplicating fee required) |

||||||

|

By E-mail: |

publicinfo@sec.gov (duplicating fee required) |

||||||

|

By Internet: |

www.sec.gov |

||||||

The Boards know of no business other than that discussed above that will be presented for consideration at the Meeting. If any other matter is properly presented, it is the intention of the persons named in the enclosed proxy to vote in accordance with their best judgment.

No person has been authorized to give any information or make any representation not contained in this Proxy Statement/Prospectus and, if so given or made, such information or representation must not be relied upon as having been authorized. This Proxy Statement/Prospectus does not constitute an offer to sell or a solicitation of an offer to buy any securities in any jurisdiction in which, or to any person to whom, it is unlawful to make such offer or solicitation.

As with all mutual funds, the SEC has not approved or disapproved these securities or passed upon the adequacy of this Proxy Statement/Prospectus. Any representation to the contrary is a criminal offense.

Mutual fund shares are not deposits or obligations of, or guaranteed or endorsed by, any bank, and are not insured by the Federal Deposit Insurance Corporation, the Federal Reserve Board, or any other U.S. government agency. Mutual fund shares involve investment risks, including the possible loss of principal.

iii

COMBINED PROXY STATEMENT/PROSPECTUS

TABLE OF CONTENTS

|

Page |

|||||||

|

SUMMARY |

1 |

||||||

|

PROPOSAL: TO APPROVE AN AGREEMENT AND PLAN OF REORGANIZATION |

1 |

||||||

|

What is the purpose of the Proposal? |

1 |

||||||

|

What are the federal income tax consequences of the Reorganizations? |

2 |

||||||

|

How do the investment objectives, investment strategies and investment restrictions of the Target Funds and the Acquiring Funds compare? |

2 |

||||||

|

Differences between the Target Funds' and Acquiring Funds' Investment Restrictions |

10 |

||||||

|

What class of shares of the corresponding Acquiring Fund will I receive in the Reorganization? |

10 |

||||||

|

What are the fees and expenses of the Target Funds compared to the Acquiring Funds? |

10 |

||||||

|

How do the Funds' portfolio turnovers compare? |

20 |

||||||

|

How do the Funds' performances compare? |

20 |

||||||

|

Who are the Service Providers? |

30 |

||||||

|

How are Shares Priced? |

30 |

||||||

|

What are the Sales Load, Redemption Fees and Rule 12b-1 Arrangements for Target Funds and Acquiring Funds? |

33 |

||||||

|

Where can I find more financial information about the Funds? |

35 |

||||||

|

What are the principal risks associated with investments in the Funds? |

35 |

||||||

|

REASONS FOR THE REORGANIZATIONS |

41 |

||||||

|

How will the Reorganizations be carried out? |

42 |

||||||

|

Who will pay the expenses of the Reorganizations? |

44 |

||||||

|

What are the federal income tax consequences of the Reorganizations? |

44 |

||||||

|

What should I know about shares of the Acquiring Funds? |

45 |

||||||

|

What are the capitalizations of the Funds and what might the capitalizations be after the Reorganizations? |

45 |

||||||

|

COMPARISON OF TARGET FUNDS AND ACQUIRING FUNDS |

49 |

||||||

|

Who manages the Funds? |

49 |

||||||

|

What management fees do the Funds pay? |

56 |

||||||

|

Who are the other service providers? |

58 |

||||||

|

What are the Funds' Additional Investments, Investment Techniques and Risks? |

60 |

||||||

|

How do the Funds' Dividends and Distributions, Purchase, Redemption and Exchange Policies Differ? |

80 |

||||||

|

ADDITIONAL INFORMATION ABOUT THE ACQUIRING FUNDS |

93 |

||||||

|

VOTING INFORMATION |

98 |

||||||

|

Quorum; Adjournment |

98 |

||||||

|

Shareholder Approval |

98 |

||||||

|

Who can vote to approve the Proposal? |

99 |

||||||

|

How do I ensure my vote is accurately recorded? |

99 |

||||||

|

May I revoke my proxy? |

99 |

||||||

|

What other matters will be voted upon at the Meeting? |

100 |

||||||

|

How do I submit a shareholder proposal? |

100 |

||||||

|

PRINCIPAL HOLDERS OF SHARES |

101 |

||||||

|

SECTION 15(f) OF THE 1940 ACT |

101 |

||||||

|

MORE INFORMATION ABOUT THE FUNDS |

101 |

||||||

|

Additional Information |

101 |

||||||

|

Financial Statements |

102 |

||||||

|

Financial Highlights |

102 |

||||||

|

Broker-Defined Sales Charge Waiver Policies. |

102 |

||||||

|

EXHIBITS |

|||||||

|

Exhibit A—Agreement and Plan of Reorganization |

A-1 |

||||||

|

Exhibit B—Investment Restrictions |

B-1 |

||||||

|

Exhibit C—Outstanding Voting Securities as of February 21, 2018 |

C-1 |

||||||

|

Exhibit D—Principal Holders of Shares as of February 21, 2018 |

D-1 |

||||||

|

Exhibit E—Financial Highlights of the Target Funds |

E-1 |

||||||

iv

SUMMARY

The following is a summary of certain information contained elsewhere in this Proxy Statement/Prospectus and is qualified in its entirety by reference to the more complete information contained herein. You should read the entire Proxy Statement/Prospectus carefully, including the Form of Plan of Reorganization (attached as Exhibit A). For more information, please read the Prospectuses of the Target Funds and Acquiring Funds and the Statement of Additional Information relating to this Proxy Statement/Prospectus.

PROPOSAL: TO APPROVE AN AGREEMENT AND PLAN OF REORGANIZATION

Shareholders of each Target Fund are being asked to consider and approve a Plan of Reorganization. Each Plan of Reorganization provides that the Target Fund will transfer all of its assets and liabilities to the corresponding Acquiring Fund in exchange for shares of that Acquiring Fund, which shares will be distributed to the shareholders of the corresponding class of the Target Fund in complete liquidation and dissolution of the Target Fund.

If each Plan of Reorganization is approved by the shareholders of the Target Funds, and certain other conditions are fulfilled, each shareholder of a Target Fund will receive the corresponding class of the corresponding Acquiring Fund's shares having an aggregate net asset value equal to the aggregate net asset value of the shares of the Target Fund that the shareholder owns as of the close of business on a closing date agreed to by the parties to the Plan of Reorganization (referred to in this Proxy Statement/Prospectus as the "Closing Date"). The Reorganization of one Target Fund is contingent on all of the conditions of the Asset Purchase Agreement being satisfied, including a condition requiring the approval by shareholders of the Reorganizations of the other Target Funds. Therefore, if any of the Reorganizations are not approved by shareholders, and the conditions of the Asset Purchase Agreement are not waived by mutual agreement of the parties, the Reorganizations will not occur and Alpine will continue to serve as investment adviser to the Target Funds.

If approved and consummated, the Plan of Reorganization will have the effect of reorganizing the Target Fund with and into the Acquiring Fund. This means that you will cease to be a shareholder of the Target Fund and will become a shareholder of the Acquiring Fund. This exchange will occur on the Closing Date, which is currently expected to be in the second quarter of 2018.

What is the purpose of the Proposal?

The Target Funds are managed by Alpine Woods Capital Investors, LLC ("Alpine") while the Acquiring Funds are managed by Aberdeen Asset Management Inc. ("AAMI") and some are sub-advised by Aberdeen Asset Managers Limited ("AAML", and together with AAMI and affiliated advisory entities "Aberdeen"). On December 21, 2017, Alpine and Aberdeen entered into a separate agreement (the "Asset Purchase Agreement") pursuant to which Aberdeen will acquire certain assets related to Alpine's business of providing investment management services to the Target Funds and other registered investment companies (the "Business") if Aberdeen becomes the investment adviser to the Target Funds pursuant to their Reorganizations into the Acquiring Funds upon receipt of the necessary approvals and satisfaction or waiver of certain other conditions. More specifically, under the Asset Purchase Agreement, Alpine has agreed to transfer to Aberdeen, for a cash payment at the closing of the Asset Transfer (as defined below) and subject to certain exceptions, (i) all right, title and interest of Alpine in and to the accounts, books, files and other records or documents to the extent used in or relating to the Business; (ii) the right to include in Aberdeen's and in the Acquiring Funds' performance information the investment performance of the Target Funds since the inception of the Target Funds and copies of information necessary to calculate such investment performance; (iii) all claims, causes of action, choses in action, rights of recovery and rights of set-off of any kind to the extent relating to items (i) and (ii) listed above against any person, including any liens, security interest, pledges or other rights to payment or to enforce payment in connection with products or services delivered by Alpine on or prior to the closing date; and (iv) all goodwill of the Business as a going concern together with the rights to represent to third parties that Aberdeen is the successor to the Business. Such transfers hereinafter are referred to collectively as the "Asset Transfer." Samuel A. Lieber, a Trustee on each Board who is currently an "interested person" of the Target Funds as that term is defined in the 1940 Act (the "Interested Trustee") and the President of the Trusts, will benefit from the Asset Transfer as an indirect majority owner of Alpine. None of the Trustees of the Trusts, who are not "interested persons" of the Target Funds (the "Independent Trustees") as that term is defined in the 1940 Act), have any interest in the Reorganizations and the Boards of Trustees of the Trusts (each, a "Board" and collectively, the "Boards"), including all of the Independent Trustees voting separately, unanimously approved the respective Plans of Reorganization.

1

The Funds are not parties to the Asset Purchase Agreement; however, the completion of the Asset Transfer is subject to certain conditions, including shareholder approval of the Proposal described in this Proxy Statement/Prospectus by each Target Fund. Therefore, if shareholders do not approve the Plans of Reorganizations for each of the Target Funds or if the other conditions in the Asset Purchase Agreement are not satisfied, and the parties to the Asset Purchase Agreement do not mutually agree to waive the shareholder approval condition and/or any other conditions that are not satisfied, then the Asset Transfer will not be completed and the Asset Purchase Agreement will terminate and the Reorganizations will not occur.

Alpine and Aberdeen anticipate that the Reorganizations will be beneficial in a number of ways, including:

• As one of the largest listed global asset managers in Europe, Aberdeen has the scale and resources necessary to service future investor demands;

• Providing access to the significant breadth and depth of Aberdeen's global asset management organization;

• Continuity of investment policies and strategies with a similar investment approach centering on fundamental analysis, micro and macro research, long-term perspective, team-based ethos and shared insights; and

• Management by an investment adviser that also has years of experience managing U.S. registered open-end funds.

As further discussed below, Aberdeen has agreed that, for a minimum of two years subsequent to the consummation of the Asset Transfer, it will use commercially reasonable efforts to ensure that there is not imposed an "unfair burden," as defined in Section 15(f) of the 1940 Act, on the Funds.

Furthermore, during the three-year period after the closing of the Asset Transfer, Aberdeen will use commercially reasonable efforts to ensure that at least 75% of the Board will be comprised of persons who are not "interested persons" of either Aberdeen or Alpine.

For the reasons set out below under "Reasons for the Reorganization," the Boards have concluded that the Reorganizations of each Target Fund into the Acquiring Fund is advisable for each respective Target Fund and its shareholders.

What are the federal income tax consequences of the Reorganizations?

It is expected that shareholders of the Target Funds will not recognize any gain or loss for federal income tax purposes as a result of the exchange of their shares in the Target Funds for shares of the corresponding Acquiring Funds pursuant to the Plans of Reorganization (although there can be no assurance that the Internal Revenue Service ("IRS") will deem the exchanges to be tax-free). You should, however, consult your tax adviser regarding the effect, if any, of the Reorganization of your Target Fund(s) in light of your individual circumstances. You should also consult your tax adviser about other state and local tax consequences of the Reorganization, if any, because the information about tax consequences in this document relates to the federal income tax consequences of the Reorganizations only. For further information about the federal income tax consequences of the Reorganization, see "Information About the Reorganization—What are the federal income tax consequences of the Reorganization?"

As a condition to the closing of the Reorganizations, the Target Funds and the Acquiring Funds will receive an opinion from legal counsel to the Funds, Willkie Farr & Gallagher LLP, (based on certain facts, assumptions and representations) to the effect that, on the basis of the existing provisions of the Internal Revenue Code of 1986, as amended (the "Code"), current administrative rules and court decisions, the transactions contemplated by the Plans of Reorganization constitute a tax-free reorganization within the meaning of Section 368(a) of the Code. Despite this opinion, there can be no assurances that the IRS will deem the exchanges to be tax-free.

How do the investment objectives, investment strategies and investment restrictions of the Target Funds and the Acquiring Funds compare?

Name and Investment Objectives

Each of the Acquiring Fund names begins with Aberdeen while each of the Target Fund names begin with Alpine. Otherwise the remainder of each Acquiring Fund's name is the same as its Target Fund's name, with the exception of the Alpine Rising Dividend Fund (a Target Fund), which corresponds to the Aberdeen Income Builder Fund (an Acquiring Fund). When discussing the like-named Target Fund with its corresponding Acquiring Fund within this Proxy Statement/Prospectus, the Target Fund and corresponding Acquiring Fund might be referred to collectively using "Alpine/Aberdeen" and the remainder common naming. For example, the Alpine International

2

Real Estate Equity Fund (Target Fund) and the Aberdeen International Real Estate Equity Fund (Acquiring Fund) may be referred to collectively as the "Alpine/Aberdeen International Real Estate Equity Funds".

Additionally, each of the Acquiring Funds has the same investment objective as its corresponding Target Fund. The below table shows the investment objective that applies to each Target Fund and its corresponding Acquiring Fund.

| Target/Acquiring Fund |

Investment Objective |

||||||

|

Alpine Rising Dividend Fund and Aberdeen Income Builder Fund |

Seeks income. Long term growth of capital is a secondary objective. |

||||||

|

Alpine/Aberdeen Dynamic Dividend Funds |

Seeks high current dividend income that qualifies for the reduced U.S. federal income tax rates created by the "Jobs and Growth Tax Relief Reconciliation Act of 2003," while also focusing on total return for long-term growth of capital. |

||||||

|

Alpine/Aberdeen Global Infrastructure Funds |

Seeks capital appreciation. Current income is a secondary objective. |

||||||

|

Alpine/Aberdeen High Yield Managed Duration Municipal Funds |

Seeks a high level of current income exempt from federal income tax. |

||||||

|

Alpine/Aberdeen International Real Estate Equity Funds |

Seeks long-term capital growth. Current income is a secondary objective. |

||||||

|

Alpine/Aberdeen Realty Income & Growth Funds |

Seeks a high level of current income. Capital appreciation is a secondary objective. |

||||||

|

Alpine/Aberdeen Ultra Short Municipal Income Funds |

Seeks high after-tax current income consistent with preservation of capital. |

||||||

Comparison. The investment objectives of the Target Funds and Acquiring Funds are identical. Although the Alpine Rising Dividend Fund and the Aberdeen Income Builder Fund have the same investment objective, the Alpine Rising Dividend Fund's investment objective is fundamental and cannot be changed without the approval of a majority of outstanding shares, while the Aberdeen Income Builder Fund's investment objective is non-fundamental and may be changed by the respective Board without shareholder approval. The investment objective(s) of the Alpine/Aberdeen Ultra Short Municipal Income Funds and Alpine/Aberdeen High Yield Managed Duration Municipal Funds (each a "Municipal Fund" and together, the "Municipal Funds") are fundamental and may not be changed without the approval of a majority of the outstanding voting securities of that Fund. The investment objective for the remaining Funds is non-fundamental, which means it may be changed by the respective Board without shareholder approval.

Investment Strategies

The investment strategies of the Target Funds and the Acquiring Funds are the same, with the exception of those that apply to the Alpine Rising Dividend Fund (Target Fund) (the "Rising Dividend Target Fund") and the Aberdeen Income Builder Fund (Acquiring Fund) ("Income Builder Acquiring Fund"). The investment strategies of each of the Target Funds and the Acquiring Funds are non-fundamental, except for the 80% policies of the Municipal Funds, which are fundamental and may not be changed without the approval of a majority of the outstanding voting securities of those Funds. The investment strategies of the Rising Dividend Target Fund and Income Builder Acquiring Fund are compared below.

Both of the Rising Dividend Target Fund and Income Builder Acquiring Fund have strategies to use a dividend capture strategy to seek dividend income where the Funds purchase shares prior to the record date for a dividend and sell them within a short time thereafter. Additionally, both Funds use a multi-cap, multi-sector, multi-style approach to invest in the securities of issuers of any capitalization level and in any sector or industry in the United States or foreign countries, including up to 25% in emerging markets countries.

A significant difference between the investment strategies of the Rising Dividend Target Fund and Income Builder Acquiring Fund is that the Rising Dividend Target Fund invests primarily in equity securities while the Income Builder Acquiring Fund invests in both equity and fixed-income securities. Further, the Rising Dividend Target Fund focuses entirely on a dividend capture strategy to obtain income while the Income Builder Acquiring Fund seeks income both through dividend capture and through its investments in fixed-income securities. Due to an increased focus on dividend capture, which involves the Rising Dividend Target Fund

3

purchasing shares prior to the record date for a dividend and selling them within a short time thereafter, the expected portfolio turnover and associated transaction costs are higher for the Rising Dividend Target Fund than it is for the Income Builder Acquiring Fund. Additionally, as a principal investment strategy, the Rising Dividend Target Fund may invest a portion of its assets in shares of secondary offerings and initial public offerings ("IPOs"), however, the Fund is subject to Alpine's discretionary policy relating to IPO investment that is based on percentage of beneficial ownership of the Fund by Alpine or principals of Alpine, which, as of February 28, 2018, the date of its most recent prospectus, does not permit investments in IPOs. The Income Builder Acquiring Fund may invest in IPOs, but it is not a principal investment strategy.

The following illustrates the similarities and differences between the investment strategies of the Alpine Rising Dividend Fund (Target Fund) and the Aberdeen Income Builder Fund (Acquiring Fund):

|

Alpine Rising Dividend Fund (Target Fund) |

Aberdeen Income Builder Fund (Acquiring Fund) |

||||||

|

Under normal circumstances, the Rising Dividend Fund invests at least 80% of its net assets in the equity securities of certain domestic and foreign companies that pay dividends. This includes companies that have announced a special dividend or announced that they will pay dividends within six months. The Fund seeks to provide dividend income without regard to whether the dividends qualify for the reduced U.S. federal income tax rates applicable to qualified dividends under the Internal Revenue Code of 1986, as amended (the "Code"). Under normal circumstances, the Fund expects to invest in the equity securities of U.S. issuers, as well as in non-U.S. issuers. The Fund combines three research driven investment strategies—dividend, growth and value—to generate sustainable distributed dividend income and to identify issuers globally with the history of or potential for increasing dividends and capital appreciation. The Fund seeks to invest in issuers with a history of or potential for increasing and/or accelerating dividends, dividends that increase over time and where the amount of such increases grows over time. In selecting issuers, Alpine analyzes each company's dividend history, free cash flow and dividend payout ratios to assess that company's potential to provide dividends as well the sustainability of dividend growth. The Fund uses a multi-cap, multi-sector, multi-style approach to invest in the securities of issuers of any capitalization level and in any sector or industry. In order to generate dividend income, the Fund may use a dividend capture strategy where it purchases share prior to the record date for a dividend and sells them within a short time thereafter. This strategy may result in higher turnover and associated transactions costs for the Fund and may generate taxable short-term gains or losses. There is the potential for market loss on the shares that are purchased to capture a dividend, although Aberdeen Standard Investments seeks to use this strategy to generate additional income with limited adverse impact on the Fund's total return. |

Under normal circumstances, the Income Builder Fund invests at least 80% of its net assets in equity and fixed income securities of domestic and foreign issuers. Net assets include the amounts of any borrowings for investment purposes. The Fund uses a multi-cap, multi-sector, multi-style approach to invest in the securities of issuers of any capitalization level and in any sector or industry. In order to achieve its investment objectives, the Fund seeks investments in income-producing instruments and equity securities that have the potential to provide income and/or long term growth of capital. In order to generate income, the Fund may use a dividend capture strategy where it purchases shares prior to the record date for a dividend and sells them within a short time thereafter. The Fund invests in the fixed income and equity securities of U.S. and foreign issuers, including those in emerging markets. The Fund is not restricted with respect to how much it may invest in the issuers of any single country or the amount it may invest in non-U.S. issuers, provided the Fund limits its investments in countries that are considered emerging markets to no more than 25% of its net assets at the time of investment. An "emerging market" country is any country that is considered to be an emerging or developing country by the International Bank for Reconstruction and Development. Emerging market countries generally include every nation in the world except the United States, Canada, Japan, Australia, New Zealand and most countries located in Western Europe. AAMI defines "Western Europe" as Austria, Belgium, Denmark, Finland, France, Germany, Iceland, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland and the United Kingdom. Allocation of the Fund's assets among countries is dependent on the economic outlook of those countries and the dividends available in their markets. AAMI screens the U.S. and foreign issuers in which it considers investing using the same criteria, including accelerating dividends, sufficiently liquid trading in an established market, and also its judgment that the issuer may have good prospects for earnings growth or may be undervalued. The equity securities in which the Fund invests may include common stocks, preferred stocks and securities convertible into or exchangeable for common stocks, such as convertible debt, options on securities and warrants. The Fund may invest in securities of any market capitalization. |

||||||

4

|

Alpine Rising Dividend Fund (Target Fund) |

Aberdeen Income Builder Fund (Acquiring Fund) |

||||||

|