Table of Contents

As filed with the Securities and Exchange Commission on February 28, 2014

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2013

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

OR

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

Commission file number 001-34841

NXP Semiconductors N.V.

(Exact name of Registrant as specified in its charter)

The Netherlands

(Jurisdiction of incorporation or organization)

High Tech Campus 60, Eindhoven 5656 AG, the Netherlands

(Address of principal executive offices)

Jean Schreurs, SVP and Senior Corporate Counsel, High Tech Campus 60, 5656 AG, Eindhoven, the Netherlands

Telephone: +31 40 2728686 / E-mail: jean.schreurs@nxp.com

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Title of each class |

Name of each exchange on which registered | |

| Common shares—par value euro (EUR) 0.20 per share | The NASDAQ Global Select Market |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

Common shares—par value EUR 0.20 per share

(Title of class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the Annual Report.

| Class |

Outstanding at December 31, 2013 | |

| Ordinary shares, par value EUR 0.20 per share | 251,751,500 shares |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. x Yes ¨ No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ¨ Yes x No

Note—Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). x Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one)

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP x |

International Financial Reporting Standards as issued by the International Accounting Standards Board ¨ | Other ¨ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ¨ Item 18 ¨

If this is an Annual Report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ¨ Yes x No

Table of Contents

Table of Contents

Table of Contents

Introduction

This Annual Report contains forward-looking statements that contain risks and uncertainties. Our actual results may differ significantly from future results as a result of factors such as those set forth in Part I. Item 3D. Risk Factors and Part I, Item 5G. Safe Harbor.

The financial information included in this Annual Report is based on United States Generally Accepted Accounting Principles (U.S. GAAP), unless otherwise indicated.

In presenting and discussing our financial position, operating results and cash flows, management uses certain non-U.S. GAAP financial measures. These non-U.S. GAAP financial measures should not be viewed in isolation or as alternatives to the equivalent U.S. GAAP measures and should be used in conjunction with the most directly comparable U.S. GAAP measures. A discussion of non-U.S. GAAP measures included in this Annual Report and a reconciliation of such measures to the most directly comparable U.S. GAAP measures are set forth under “Use of Certain Non-U.S. GAAP Financial Measures” contained in this report under Part I, Item 5A. Operating Results.

Unless otherwise required, all references herein to “we”, “our”, “us”, “NXP” and the “Company” are to NXP Semiconductors N.V. and its consolidated subsidiaries.

A glossary of abbreviations and technical terms used in this Annual Report is set forth on page 96.

1

Table of Contents

PART I

| Item 1. | Identity of Directors, Senior Management and Advisers |

Not applicable.

| Item 2. | Offer Statistics and Expected Timetable |

Not applicable.

| Item 3. | Key Information |

The following table presents a summary of our selected historical consolidated financial data. We prepare our financial statements in accordance with U.S. GAAP.

The results of operations for prior years are not necessarily indicative of the results to be expected for any future period.

2

Table of Contents

The selected historical consolidated financial data should be read in conjunction with the discussion under Part I, Item 5A. Operating Results and the Consolidated Financial Statements and the accompanying Notes included elsewhere in this Annual Report.

| As of and for the years ended December 31, | ||||||||||||||||||||

| ($ in millions unless otherwise stated) | 2013 | 2012 | 2011 | 2010 | 2009(1) | |||||||||||||||

| Consolidated Statements of Operations: |

||||||||||||||||||||

| Revenue |

4,815 | 4,358 | 4,194 | 4,402 | 3,519 | |||||||||||||||

| Operating income (loss) |

651 | 412 | 357 | 273 | (931 | ) | ||||||||||||||

| Financial income (expense)-net |

(274 | ) | (437 | ) | (257 | ) | (628 | ) | 682 | |||||||||||

| Income (loss) from continuing operations attributable to stockholders |

348 | (116 | ) | (44 | ) | (515 | ) | (199 | ) | |||||||||||

| Income (loss) from discontinued operations attributable to stockholders |

— | 1 | 434 | 59 | 32 | |||||||||||||||

| Net income (loss) attributable to stockholders |

348 | (115 | ) | 390 | (456 | ) | (167 | ) | ||||||||||||

| Per share data(2)(3): |

||||||||||||||||||||

| Basic earnings per common share attributable to stockholders in $ |

||||||||||||||||||||

| - Income (loss) from continuing operations |

1.40 | (0.46 | ) | (0.17 | ) | (2.25 | ) | (0.93 | ) | |||||||||||

| - Income (loss) from discontinued operations |

— | — | 1.74 | 0.26 | 0.15 | |||||||||||||||

| - Net income (loss) |

1.40 | (0.46 | ) | 1.57 | (1.99 | ) | (0.78 | ) | ||||||||||||

| Diluted earnings per common share attributable to stockholders in $ |

||||||||||||||||||||

| - Income (loss) from continuing operations |

1.36 | (0.46 | ) | (0.17 | ) | (2.25 | ) | (0.93 | ) | |||||||||||

| - Income (loss) from discontinued operations |

— | — | 1.74 | 0.26 | 0.15 | |||||||||||||||

| - Net income (loss) |

1.36 | (0.46 | ) | 1.57 | (1.99 | ) | (0.78 | ) | ||||||||||||

| Weighted average number of shares of common stock outstanding during the year (in thousands) |

||||||||||||||||||||

| - Basic |

248,526 | 248,064 | 248,812 | 229,280 | 215,252 | |||||||||||||||

| - Diluted |

255,050 | 248,064 | (4) | 248,812 | (4) | 229,280 | (4) | 215,252 | (4) | |||||||||||

| Consolidated balance sheet data: |

||||||||||||||||||||

| Cash and cash equivalents |

670 | 617 | 743 | 898 | 1,026 | |||||||||||||||

| Total assets |

6,449 | 6,439 | 6,612 | 7,637 | 8,579 | |||||||||||||||

| Net assets |

1,546 | 1,284 | 1,357 | 1,219 | 1,041 | |||||||||||||||

| Working capital(5) |

939 | 765 | 969 | 811 | 870 | |||||||||||||||

| Total debt(6) |

3,321 | 3,492 | 3,799 | 4,551 | 5,283 | |||||||||||||||

| Total stockholders’ equity |

1,301 | 1,049 | 1,145 | 986 | 843 | |||||||||||||||

| Common stock |

51 | 51 | 51 | 51 | 42 | |||||||||||||||

| Other operating data: |

||||||||||||||||||||

| Capital expenditures |

(215 | ) | (251 | ) | (221 | ) | (258 | ) | (92 | ) | ||||||||||

| Depreciation and amortization(7) |

514 | 533 | 591 | 684 | 887 | |||||||||||||||

| Consolidated statements of cash flows data: |

||||||||||||||||||||

| Net cash provided by (used for): |

||||||||||||||||||||

| Operating activities |

891 | 722 | 175 | 361 | (701 | ) | ||||||||||||||

| Investing activities |

(240 | ) | (243 | ) | (202 | ) | (269 | ) | 63 | |||||||||||

| Financing activities |

(598 | ) | (574 | ) | (926 | ) | (157 | ) | (109 | ) | ||||||||||

| Net cash provided by (used for) continuing operations |

53 | (95 | ) | (953 | ) | (65 | ) | (747 | ) | |||||||||||

| Net cash provided by (used for) discontinued operations |

— | (45 | ) | 809 | (5 | ) | — | |||||||||||||

| (1) | The financial data for 2009 have been restated to reflect the effect of the sale of the Sound Solutions business in 2011 as discontinued operations. |

3

Table of Contents

| (2) | On August 2, 2010, we amended our articles of association in order to effect a 1-for-20 reverse stock split, decreasing the number of shares of common stock outstanding from approximately 4.3 billion to approximately 215 million and increasing the par value of the shares of common stock from €0.01 to €0.20. In all periods presented, basic and diluted weighted average shares outstanding and earnings per share have been calculated to reflect the 1-for-20 reverse stock split. |

| (3) | The Company has not paid any dividends during the periods presented. |

| (4) | Due to our net losses from continuing operations attributable to stockholders in the periods from 2009 to 2012, all potentially dilutive securities have been excluded from the calculation of diluted earnings per common share because their effect would be anti-dilutive. |

| (5) | Working capital is calculated as current assets less current liabilities (excluding short-term debt). |

| (6) | As adjusted for our cash and cash equivalents our net debt was calculated as follows: |

| ($ in millions) | 2013 | 2012 | 2011 | 2010 | 2009 | |||||||||||||||

| Long-term debt |

3,281 | 3,185 | 3,747 | 4,128 | 4,673 | |||||||||||||||

| Short-term debt |

40 | 307 | 52 | 423 | 610 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total debt |

3,321 | 3,492 | 3,799 | 4,551 | 5,283 | |||||||||||||||

| Less: cash and cash equivalents |

(670 | ) | (617 | ) | (743 | ) | (898 | ) | (1,026 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net debt |

2,651 | 2,875 | 3,056 | 3,653 | 4,257 | |||||||||||||||

Net debt is a non-GAAP financial measure. See “Use of Certain Non-GAAP Financial Measures” under Part I, 5A. Operating Results.

| (7) | Depreciation and amortization includes the cumulative net effect of purchase price adjustments related to a number of acquisitions and divestments, including the purchase by a consortium of private equity investors of an 80.1% interest in our business, described elsewhere in this Annual Report as our “Formation.” The cumulative net effects of purchase price adjustments in depreciation and amortization aggregated to $246 million in 2013, $273 million in 2012, $301 million in 2011, $302 million in 2010 and $371 million in 2009. In 2013, depreciation and amortization included $9 million (2012: $2 million; 2011: $5 million) related to disposals that occurred in connection with our restructuring activities and $3 million (2012: $2 million; 2011: $1 million) relating to other incidental items. For a detailed list of the acquisitions and a discussion of the effect of acquisition accounting, see the “Effect of Acquisition Accounting” section in Part I, Item 5 A. Operating Results. Depreciation and amortization also includes impairments to goodwill and other intangibles, as well as write-offs in connection with acquired in-process research and development, if any. |

As used in this Annual Report, “euro”, or “€” means the single unified currency of the European Monetary Union. “U.S. dollar”, “USD”, “U.S. $” or “$” means the lawful currency of the United States of America. As used in this Annual Report, the term “noon buying rate” refers to the exchange rate for euro, expressed in U.S. dollars per euro, as announced by the Federal Reserve Bank of New York for customs purposes as the rate in the city of New York for cable transfers in foreign currencies.

The table below shows the average noon buying rates for U.S. dollars per euro for the five years ended December 31, 2013. The averages set forth in the table below have been computed using the noon buying rate on the last business day of each month during the periods indicated.

| Year ended December 31, | ||||||||||||||||||||

| 2013 | 2012 | 2011 | 2010 | 2009 | ||||||||||||||||

| Average $ per € |

1.3281 | 1.2859 | 1.3931 | 1.3261 | 1.3935 | |||||||||||||||

4

Table of Contents

The following table shows the high and low noon buying rates for U.S. dollars per euro for each of the six months in the six-month period ended February 21, 2014:

| Month | High | Low | ||||||

| ($ per €) | ||||||||

| 2013 |

||||||||

| August |

1.3426 | 1.3196 | ||||||

| September |

1.3537 | 1.3120 | ||||||

| October |

1.3810 | 1.3490 | ||||||

| November |

1.3606 | 1.3357 | ||||||

| December |

1.3816 | 1.3552 | ||||||

| 2014 |

||||||||

| January |

1.3682 | 1.3500 | ||||||

On February 21, 2014, the noon buying rate was $1.3722 per €1.00.

Fluctuations in the value of the euro relative to the U.S. dollar have had a significant effect on the translation into U.S. dollar of our euro denominated assets, liabilities, revenue and expenses, and may continue to do so in the future. For further information on the impact of fluctuations in exchange rates on our operations, see the “Fluctuations in Foreign Rates May Have An Adverse Effect On Our Financial Results” section in Part I, Item 3D. Risk Factors and the “Foreign Currency Risks” section in Part I, Item 11. Quantitative and Qualitative Disclosures About Market Risk.

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

The following section provides an overview of the risks to which our business is exposed. You should carefully consider the risk factors described below and all other information contained in this Annual Report, including the Consolidated Financial Statements and related Notes. The occurrence of the risks described below could have a material adverse impact on our business, financial condition or results of operations. Various statements in this Annual Report, including the following risk factors, contain forward-looking statements. Please also refer to Part I, Item 5G. Safe Harbor, contained elsewhere in this Annual Report.

The semiconductor industry is highly cyclical.

Historically, the relationship between supply and demand in the semiconductor industry has caused a high degree of cyclicality in the semiconductor market. Semiconductor supply is partly driven by manufacturing capacity, which in the past has demonstrated alternating periods of substantial capacity additions and periods in which no or limited capacity was added. As a general matter, semiconductor companies are more likely to add capacity in periods when current or expected future demand is strong and margins are, or are expected to be, high. Investments in new capacity can result in overcapacity, which can lead to a reduction in prices and margins. In response, companies typically limit further capacity additions, eventually causing the market to be relatively undersupplied. In addition, demand for semiconductors varies, which can exacerbate the effect of supply fluctuations. As a result of this cyclicality, the semiconductor industry has in the past experienced significant downturns, such as in 1997/1998, 2001/2002 and in 2008/2009, often in connection with, or in anticipation of, maturing life cycles of semiconductor companies’ products and declines in general economic conditions. These

5

Table of Contents

downturns have been characterized by diminishing demand for end-user products, high inventory levels, under-utilization of manufacturing capacity and accelerated erosion of average selling prices. The foregoing risks have historically had, and may continue to have, a material adverse effect on our business, financial condition and results of operations.

Significantly increased volatility and instability and unfavorable economic conditions may adversely affect our business.

In 2008 and 2009, Europe, the United States and international markets experienced increased volatility and instability. Since the second half of 2011, this volatility and instability has resumed periodically because of the sovereign debt crisis in Europe and the debt-ceiling crisis in the United States and the related financial restructuring efforts, continued hostilities in the Middle East and tensions in North Africa and other world events. These, or other events, could further adversely affect the economies of the European Union, the United States and those of other countries and may exacerbate the cyclicality of our business. Among other factors, we face risks attendant to declines in general economic conditions, changes in demand for end-user products and changes in interest rates.

Despite indications of recovery and aggressive measures taken by governments and central banks, there is a significant risk that the global economy could fall into recession again. If economic conditions remain uncertain or deteriorate, our business, financial condition and results of operations could be materially adversely affected.

As a consequence of the significantly increased volatility and instability, it is difficult for us, our customers and suppliers to forecast demand trends. We may be unable to accurately predict the extent or duration of cycles or their effect on our financial condition or result of operations and can give no assurance as to the timing, extent or duration of the current or future business cycles. A recurrent decline in demand or the failure of demand to return to prior levels could place pressure on our results of operations. The timing and extent of any changes to currently prevailing market conditions is uncertain and supply and demand may be unbalanced at any time.

The semiconductor industry is highly competitive. If we fail to introduce new technologies and products in a timely manner, this could adversely affect our business.

The semiconductor industry is highly competitive and characterized by constant and rapid technological change, short product lifecycles, significant price erosion and evolving standards. Accordingly, the success of our business depends to a significant extent on our ability to develop new technologies and products that are ultimately successful in the market. The costs related to the research and development necessary to develop new technologies and products are significant and any reduction of our research and development budget could harm our competitiveness. Meeting evolving industry requirements and introducing new products to the market in a timely manner and at prices that are acceptable to our customers are significant factors in determining our competitiveness and success. Commitments to develop new products must be made well in advance of any resulting sales, and technologies and standards may change during development, potentially rendering our products outdated or uncompetitive before their introduction. If we are unable to successfully develop new products, our revenue may decline substantially. Moreover, some of our competitors are well-established entities, are larger than us and have greater resources than we do. If these competitors increase the resources they devote to developing and marketing their products, we may not be able to compete effectively. Any consolidation among our competitors could enhance their product offerings and financial resources, further strengthening their competitive position. In addition, some of our competitors operate in narrow business areas relative to us, allowing them to concentrate their research and development efforts directly on products and services for those areas, which may give them a competitive advantage. As a result of these competitive pressures, we may face declining sales volumes or lower prevailing prices for our products, and we may not be able to reduce our total costs in line with this declining revenue. If any of these risks materialize, they could have a material adverse effect on our business, financial condition and results of operations.

6

Table of Contents

In many of the market segments in which we compete, we depend on winning selection processes, and failure to be selected could adversely affect our business in those market segments.

One of our business strategies is to participate in and win competitive bid selection processes to develop products for use in our customers’ equipment and products. These selection processes can be lengthy and require us to incur significant design and development expenditures, with no guarantee of winning a contract or generating revenue. Failure to win new design projects and delays in developing new products with anticipated technological advances or in commencing volume shipments of these products may have an adverse effect on our business. This risk is particularly pronounced in markets where there are only a few potential customers and in the automotive market, where, due to the longer design cycles involved, failure to win a design-in could prevent access to a customer for several years. Our failure to win a sufficient number of these bids could result in reduced revenue and hurt our competitive position in future selection processes because we may not be perceived as being a technology or industry leader, each of which could have a material adverse effect on our business, financial condition and results of operations.

The demand for our products depends to a significant degree on the demand for our customers’ end products.

The vast majority of our revenue is derived from sales to manufacturers in the automotive, identification, wireless infrastructure, lighting, industrial, mobile, consumer and computing markets. Demand in these markets fluctuates significantly, driven by consumer spending, consumer preferences, the development of new technologies and prevailing economic conditions. In addition, the specific products in which our semiconductors are incorporated may not be successful, or may experience price erosion or other competitive factors that affect the price manufacturers are willing to pay us. Such customers have in the past, and may in the future, vary order levels significantly from period to period, request postponements to scheduled delivery dates, modify their orders or reduce lead times. This is particularly common during periods of low demand. This can make managing our business difficult, as it limits the predictability of future revenue. It can also affect the accuracy of our financial forecasts. Furthermore, developing industry trends, including customers’ use of outsourcing and new and revised supply chain models, may affect our revenue, costs and working capital requirements. Additionally, a significant portion of our products is made to order.

If customers do not purchase products made specifically for them, we may not be able to resell such products to other customers or may not be able to require the customers who have ordered these products to pay a cancellation fee. The foregoing risks could have a material adverse effect on our business, financial condition and results of operations.

The semiconductor industry is characterized by significant price erosion, especially after a product has been on the market for a significant period of time.

One of the results of the rapid innovation in the semiconductor industry is that pricing pressure, especially on products containing older technology, can be intense. Product life cycles are relatively short, and as a result, products tend to be replaced by more technologically advanced substitutes on a regular basis.

In turn, demand for older technology falls, causing the price at which such products can be sold to drop, in some cases precipitously. In order to continue profitably supplying these products, we must reduce our production costs in line with the lower revenue we can expect to generate per unit. Usually, this must be accomplished through improvements in process technology and production efficiencies. If we cannot advance our process technologies or improve our efficiencies to a degree sufficient to maintain required margins, we will no longer be able to make a profit from the sale of these products. Moreover, we may not be able to cease production of such products, either due to contractual obligations or for customer relationship reasons, and as a result may be required to bear a loss on such products. We cannot guarantee that competition in our core product markets will not lead to price erosion, lower revenue or lower margins in the future. Should reductions in our manufacturing costs fail to keep pace with reductions in market prices for the products we sell, this could have a material adverse effect on our business, financial condition and results of operations.

7

Table of Contents

Our substantial amount of debt could adversely affect our financial condition, which could adversely affect our results of operations.

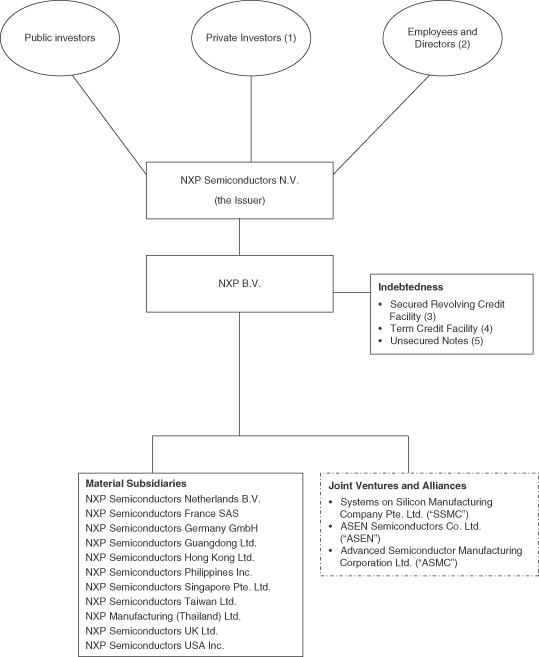

Our substantial indebtedness could have a material adverse effect on our business by: limiting our ability to borrow money for working capital, restructurings, capital expenditures, research and development, investments, acquisitions or other purposes, if needed, and increasing the cost of any of these borrowings; reducing the portion of our funds available for operations and future business opportunities; limiting our flexibility in responding to changing business and economic conditions, including increased competition and demand for new services; placing us at a disadvantage when compared to those of our competitors that have less debt, by making us more vulnerable to a downturn in our business, industry or the economy in general than our competitors who have less debt and making it more difficult for us to satisfy our payment obligations under our senior secured revolving credit facility that we entered into on April 27, 2012 (the “Secured Revolving Credit Facility”) under the secured term credit agreement that we entered into on March 4, 2011 (the “ 2017 Term Loan”) and the joinder and amendment to the secured term credit agreement that we entered into on December 10, 2012 (the “2020 Term Loan” and, together with the 2017 Term Loan, the “Term Loans”) or under the indentures (collectively, the “Indentures”) governing the terms of our U.S. dollar-denominated 5.75% senior notes due February 15, 2021 (the “2021 Unsecured Notes”), our U.S. dollar denominated 5.75% senior notes due March 15, 2023 (our “2023 Unsecured Notes”), our U.S. dollar-denominated 3.5% senior notes due September 15, 2016 (the “2016 Unsecured Notes”) and our U.S. dollar-denominated 3.75% senior notes due June 1, 2018 (our “2018 Unsecured Notes,”) and together with 2016 Unsecured Notes, the 2021 Unsecured Notes and the 2023 Unsecured Notes, the “Notes”). Despite our substantial indebtedness, we may still incur significantly more debt, which could further exacerbate the risks described above.

We may not be able to generate sufficient cash to service and repay all of our indebtedness and may be forced to take other actions to satisfy our obligations under our indebtedness, which may not be successful.

Our ability to make scheduled payments or to refinance our debt obligations depends on our financial and operating performance, which is subject to prevailing economic and competitive conditions. In the future, we may not be able to maintain a level of cash flows from operating activities sufficient to permit us to pay the principal, premium, if any, and interest on our indebtedness. We have seen substantial negative cash flows from operations in periods of adverse economic developments. Our business may not generate sufficient cash flow from operations and future borrowings under our Secured Revolving Credit Facility or from other sources may not be available to us, in an amount sufficient to enable us to repay our indebtedness, including the Secured Revolving Credit Facility, the Term Loans, or the Notes, or to fund our other liquidity needs, and working capital and capital expenditure requirements, and we may be forced to reduce or delay capital expenditures, sell assets or operations, seek additional capital or restructure or refinance our indebtedness.

If we cannot make scheduled payments on our debt, we will be in default and, as a result:

| • | holders of our debt securities could declare all outstanding principal and interest to be due and payable; |

| • | the lenders under our Secured Revolving Credit Facility could declare all outstanding principal and interest to be due and payable, terminate their commitments to lend us money and/or foreclose against the assets securing any outstanding borrowings; and |

| • | we could be forced into bankruptcy or liquidation. |

Goodwill and other identifiable intangible assets represent a significant portion of our total assets, and we may never realize the full value of our intangible assets.

Goodwill and other identifiable intangible assets are recorded at fair value on the date of acquisition. We review our goodwill and other intangible assets balance for impairment upon any indication of a potential impairment, and in the case of goodwill, at a minimum of once a year. Impairment may result from, among other things, deterioration in performance, adverse market conditions, adverse changes in applicable laws or regulations, including changes that restrict the activities of or affect the products and services we sell, challenges

8

Table of Contents

to the validity of certain registered intellectual property, reduced sales of certain products incorporating registered intellectual property and a variety of other factors. The amount of any quantified impairment must be expensed immediately as a charge to results of operations. Depending on future circumstances, it is possible that we may never realize the full value of our intangible assets. Any future determination of impairment of goodwill or other identifiable intangible assets could have a material adverse effect on our financial position, results of operations and stockholders’ equity.

As our business is global, we need to comply with laws and regulations in countries across the world and are exposed to international business risks that could adversely affect our business.

We operate globally, with manufacturing, assembly and testing facilities in several continents, and we market our products globally.

As a result, we are subject to environmental, labor and health and safety laws and regulations in each jurisdiction in which we operate. We are also required to obtain environmental permits and other authorizations or licenses from governmental authorities for certain of our operations and have to protect our intellectual property worldwide. In the jurisdictions where we operate, we need to comply with differing standards and varying practices of regulatory, tax, judicial and administrative bodies.

The SEC has adopted disclosure requirements under Section 1502 of the Dodd-Frank Wall Street Reform and Consumer Protection Act, regarding the source of certain conflict minerals for reporting companies for which such conflict minerals are necessary to the functionality or production of a product manufactured, or contracted to be manufactured which are mined from the Democratic Republic of Congo (“DRC”) and adjoining countries, including: Sudan, Uganda, Rwanda, Burundi, United Republic of Tanzania, Zambia, Angola and Central African Republic. These rules require reporting companies to file a Conflict Minerals Report as an exhibit to a Form SD report with the SEC. The Conflict Minerals Report is required to set out the due diligence efforts and procedures exercised on the source and chain of custody of such conflict minerals, in accordance with a nationally or internationally recognized due diligence framework, and a description of the company’s products containing such conflict minerals. Although we expect that we and our suppliers will be able to comply with the requirements of any rules promulgated by the SEC and file our first report by May 31, 2014, as required, we may not be able to gather all the information required. Furthermore, the implementation of these requirements could increase our legal compliance costs. It may also affect the sourcing and availability of minerals used in the manufacture of our products. As a result, there may only be a limited pool of certified suppliers who provide conflict free minerals, and we cannot assure you that we will be able to obtain products in sufficient quantities or at competitive prices. Also, since our supply chain is complex, we may face reputational challenges with our customers and other stakeholders if we are unable to sufficiently verify the origins of all minerals used in our products.

In addition, the business environment is also subject to many economic and political uncertainties, including the following international business risks:

| • | negative economic developments in economies around the world and the instability of governments, such as the sovereign debt crisis in certain European countries; |

| • | social and political instability in a number of countries around the world, including continued hostilities and civil unrest in the Middle East. Although we have no direct investments in North Africa and the Middle East, the ongoing changes may have, for instance via our customers, the energy prices and the financial markets, a negative effect on our business, financial condition and operations; |

| • | potential terrorist attacks; |

| • | epidemics and pandemics, which may adversely affect our workforce, as well as our local suppliers and customers in particular in Asia; |

| • | adverse changes in governmental policies, especially those affecting trade and investment; |

9

Table of Contents

| • | our customers or other groups of stakeholders might impose requirements that are more stringent than the laws in the countries in which we are active; |

| • | volatility in foreign currency exchange rates, in particular with respect to the U.S. dollar, and transfer restrictions, in particular in Greater China; and |

| • | threats that our operations or property could be subject to nationalization and expropriation. |

No assurance can be given that we have been or will be at all times in complete compliance with the laws and regulations to which we are subject or that we have obtained or will obtain the permits and other authorizations or licenses that we need. If we violate or fail to comply with laws, regulations, permits and other authorizations or licenses, we could be fined or otherwise sanctioned by regulators. In this case, or if any of the international business risks were to materialize or become worse, they could have a material adverse effect on our business, financial condition and results of operations.

In addition, changing laws, regulations and standards relating to corporate governance and public disclosure are creating uncertainty for public companies, further increasing legal and financial compliance costs. These laws, regulations and standards are subject to varying interpretations, in many cases due to their lack of specificity, and, as a result, their application in practice may evolve over time as new guidance is provided by regulatory and governing bodies. This could result in continuing uncertainty regarding compliance matters and higher costs necessitated by ongoing revisions to disclosure.

Interruptions in our information technology systems could adversely affect our business.

We rely on the efficient and uninterrupted operation of complex information technology applications, systems and networks to operate our business. Any significant interruption in our business applications, systems or networks, including but not limited to new system implementations, computer viruses, cyber attacks, security breaches, facility issues or energy blackouts could have a material adverse impact on our operations, sales and operating results. In recent years, the risks that we and other companies face from cyber attacks have increased significantly. Given the nature of some of our products these attacks may originate from well organized, highly skilled and highly funded organizations. Any such attack or system or network disruption could result in a loss of our intellectual property, the release of commercially sensitive information or partner, customer or employee personal data, disruption of the supply chain towards our customers, or the loss of production capabilities at one of our manufacturing sites. Therefore, any such severe incident could harm our competitive position, result in a loss of customer confidence, and cause us to incur significant costs to remedy the damages caused by the system or network disruptions, whether caused by cyber attacks, security breaches or otherwise. The protective measures that we are adopting to avoid system or network disruptions may, especially given the potential professionalism of the intruders, be insufficient to prevent or limit the damage from any future disruptions and any disruption could have a material adverse impact on our business, operations and financial results. Although we have experienced cyber attacks, to date we have not incurred any significant damage as a result. There can be no assurance that in the future we will be as successful in avoiding damages from cyber attacks.

In difficult market conditions, our high fixed costs combined with low revenue negatively affect our results of operations.

The semiconductor industry is characterized by high fixed costs and, notwithstanding our significant utilization of third-party manufacturing capacity, most of our production requirements are met by our own manufacturing facilities. In less favorable industry environments, like we faced in the second half in 2011, we are generally faced with a decline in the utilization rates of our manufacturing facilities due to decreases in demand for our products. During such periods, our fabrication plants operate at lower loading level, while the fixed costs associated with the full capacity continue to be incurred, resulting in lower gross profit.

10

Table of Contents

The semiconductor industry is capital intensive and if we are unable to invest the necessary capital to operate and grow our business, we may not remain competitive.

To remain competitive, we must constantly improve our facilities and process technologies and carry out extensive research and development, each of which requires investment of significant amounts of capital. This risk is magnified by the substantial indebtedness we currently have, since we are required to use a portion of our cash flow to service that debt. If we are unable to generate sufficient cash flow or raise sufficient capital to meet both our debt service and capital investment requirements, or if we are unable to raise required capital on favorable terms when needed, this could have a material adverse effect on our business, financial condition and results of operations.

We are bound by the restrictions contained in the Secured Revolving Credit Facility, the Term Loans and the Indentures, which may restrict our ability to pursue our business strategies.

Restrictive covenants in our Secured Revolving Credit Facility, the Term Loans and the Indentures limit our ability, among other things, to:

| • | incur additional indebtedness or issue preferred stock; |

| • | pay dividends or make distributions in respect of our capital stock or make certain other restricted payments or investments; |

| • | repurchase or redeem capital stock; |

| • | sell assets, including capital stock of restricted subsidiaries; |

| • | agree to limitations on the ability of our restricted subsidiaries to make distributions; |

| • | enter into transactions with our affiliates; |

| • | incur liens; |

| • | guarantee indebtedness; and |

| • | engage in consolidations, mergers or sales of substantially all of our assets. |

These restrictions could restrict our ability to pursue our business strategies. We are currently in compliance with all of our restrictive covenants.

Our failure to comply with the covenants contained in our Secured Revolving Credit Facility, the Term Loans or the Indentures or our other debt agreements, including as a result of events beyond our control, could result in an event of default which could materially and adversely affect our operating results and our financial condition.

Our Secured Revolving Credit Facility, the Term Loans and the Indentures require us to comply with various covenants. Even though we are currently in compliance with all of our covenants, if there were an event of default under any of our debt instruments that was not cured or waived, the holders of the defaulted debt could terminate commitments to lend and cause all amounts outstanding with respect to the debt to be declared due and payable immediately, which in turn could result in cross defaults under our other debt instruments. Our assets and cash flow may not be sufficient to fully repay borrowings under all of our outstanding debt instruments if some or all of these instruments are accelerated upon an event of default.

If, when required, we are unable to repay, refinance or restructure our indebtedness under, or amend the covenants contained in, our Secured Revolving Credit Facility or if a default otherwise occurs, the lenders under our Secured Revolving Credit Facility could elect to terminate their commitments thereunder, cease making further loans and issuing or renewing letters of credit, declare all outstanding borrowings and other amounts, together with accrued interest and other fees, to be immediately due and payable, institute enforcement

11

Table of Contents

proceedings against those assets that secure the extensions of credit under our Secured Revolving Credit Facility and thereby prevent us from making payments on our debt. Any such actions could force us into bankruptcy or liquidation.

We rely to a significant extent on proprietary intellectual property. We may not be able to protect this intellectual property against improper use by our competitors or others.

We depend significantly on patents and other intellectual property rights to protect our products and proprietary design and fabrication processes against misappropriation by others. We may in the future have difficulty obtaining patents and other intellectual property rights, and the patents we receive may be insufficient to provide us with meaningful protection or commercial advantage. We may not be able to obtain patent protection or secure other intellectual property rights in all the countries in which we operate, and under the laws of such countries, patents and other intellectual property rights may be or become unavailable or limited in scope. The protection offered by intellectual property rights may be inadequate or weakened for reasons or circumstances that are out of our control. Further, our trade secrets may be vulnerable to disclosure or misappropriation by employees, contractors and other persons. In particular, intellectual property rights are difficult to enforce in the People’s Republic of China (PRC) and certain other countries, since the application and enforcement of the laws governing such rights may not have reached the same level as compared to other jurisdictions where we operate, such as the United States, Germany and the Netherlands. Consequently, operating in some of these countries may subject us to an increased risk that unauthorized parties may attempt to copy or otherwise use our intellectual property or the intellectual property of our suppliers or other parties with whom we engage. There is no assurance that we will be able to protect our intellectual property rights or have adequate legal recourse in the event that we seek legal or judicial enforcement of our intellectual property rights under the laws of such countries. Any inability on our part to adequately protect our intellectual property may have a material adverse effect on our business, financial condition and results of operations.

The intellectual property that was transferred or licensed to us from Philips may not be sufficient to protect our position in the industry.

In connection with our separation from Philips in 2006, Philips transferred approximately 5,300 patent families to us subject to certain limitations, including (1) any prior commitments to and undertakings with third parties entered into prior to the separation and (2) certain licenses retained by Philips. The licenses retained by Philips give Philips the right to sublicense to third parties in certain circumstances, which may divert revenue opportunities from us. Approximately 800 of the patent families transferred from Philips were transferred to ST-NXP Wireless (and subsequently to ST-Ericsson, its successor) in connection with the contribution of our wireless operations to ST-NXP Wireless in 2008. Approximately 400 of the patent families transferred from Philips were transferred to Trident Microsystems, Inc. (“Trident”) in connection with the divestment of our television systems and set-top box business lines to Trident in 2010. Further, a number of other patent families have been transferred in the context of other transactions. In addition, the sale of our Sound Solutions business to Knowles Electronics in 2011 has led to the transfer of certain patent families to them.

Philips granted us a non-exclusive license to: (1) all patents Philips holds but has not assigned to us, to the extent that they are entitled to the benefit of a filing date prior to the separation and for which Philips is free to grant licenses without the consent of or accounting to any third party and (2) certain know-how that is available to us, where such patents and know-how relate to: (i) our current products and technologies, as well as successor products and technologies, (ii) technology that was developed for us prior to the separation and (iii) technology developed pursuant to contract research co-funded by us. Philips has also granted us a non-exclusive royalty-free and irrevocable license under: (1) certain patents for use in giant magneto-resistive devices outside the field of healthcare and bio applications, and (2) certain patents relevant to polymer electronics resulting from contract research work co-funded by us in the field of radio frequency identification tags. Such licenses are subject to certain prior commitments and undertakings. However, Philips retained ownership of certain intellectual property related to our business, as well as certain rights with respect to intellectual property transferred to us in connection with the separation. There can be no guarantee that the patents transferred to us will be sufficient to

12

Table of Contents

assert offensively against our competitors, to be used as leverage to negotiate future cross-licenses or to give us freedom to operate and innovate in the industry. The strength and value of our intellectual property may be diluted if Philips licenses or otherwise transfers such intellectual property or such rights to third parties, especially if those third parties compete with us. The foregoing risks could have a material adverse effect on our business, financial condition and results of operations.

We may become party to intellectual property claims or litigation that could cause us to incur substantial costs, pay substantial damages or prohibit us from selling our products.

We have from time to time received, and may in the future receive, communications alleging possible infringement of patents and other intellectual property rights of others. Further, we may become involved in costly litigation brought against us regarding patents, copyrights, trademarks, trade secrets or other intellectual property rights. If any such claims are asserted against us, we may seek to obtain a license under the third party’s intellectual property rights. We cannot assure you that we will be able to obtain any or all of the necessary licenses on satisfactory terms, if at all. In the event that we cannot obtain or take the view that we don’t need a license, these parties may file lawsuits against us seeking damages (and potentially treble damages in the United States) or an injunction against the sale of our products that incorporate allegedly infringed intellectual property or against the operation of our business as presently conducted. Such lawsuits, if successful, could result in an increase in the costs of selling certain of our products, our having to partially or completely redesign our products or stop the sale of some of our products and could cause damage to our reputation. Any litigation could require significant financial and management resources regardless of the merits or outcome, and we cannot assure you that we would prevail in any litigation or that our intellectual property rights can be successfully asserted in the future or will not be invalidated, circumvented or challenged. The award of damages, including material royalty payments, or the entry of an injunction against the manufacture and sale of some or all of our products, could affect our ability to compete or have a material adverse effect on our business, financial condition and results of operations.

We rely on strategic partnerships, joint ventures and alliances for manufacturing and research and development. However, we often do not control these partnerships and joint ventures, and actions taken by any of our partners or the termination of these partnerships or joint ventures could adversely affect our business.

As part of our strategy, we have entered into a number of long-term strategic partnerships with other leading industry participants. For example, we have entered into a joint venture with Taiwan Semiconductor Manufacturing Company Limited (“TSMC”) called Systems on Silicon Manufacturing Company Pte. Ltd. (“SSMC”). We established Advanced Semiconductor Manufacturing Corporation Limited (“ASMC”) together with a number of Chinese partners, and together with Advanced Semiconductor Engineering Inc. (“ASE”), we established the assembly and test joint venture ASEN Semiconductors Co. Ltd. (“ASEN”).

If any of our strategic partners in industry groups or in any of the other alliances we engage with were to encounter financial difficulties or change their business strategies, they may no longer be able or willing to participate in these groups or alliances, which could have a material adverse effect on our business, financial condition and results of operations. We do not control some of these strategic partnerships, joint ventures and alliances in which we participate. We may also have certain obligations, including some limited funding obligations or take or pay obligations, with regard to some of our strategic partnerships, joint ventures and alliances. For example, we have made certain commitments to SSMC, in which we have a 61.2% ownership share, whereby we are obligated to make cash payments to SSMC should we fail to utilize, and TSMC does not utilize, an agreed upon percentage of the total available capacity at SSMC’s fabrication facilities if overall SSMC utilization levels drop below a fixed proportion of the total available capacity.

13

Table of Contents

We have made and may continue to make acquisitions and engage in other transactions to complement or expand our existing businesses. However, we may not be successful in acquiring suitable targets at acceptable prices and integrating them into our operations, and any acquisitions we make may lead to a diversion of management resources.

Our future success may depend on acquiring businesses and technologies, making investments or forming joint ventures that complement, enhance or expand our current portfolio or otherwise offer us growth opportunities. If we are unable to identify suitable targets, our growth prospects may suffer, and we may not be able to realize sufficient scale advantages to compete effectively in all markets. In addition, in pursuing acquisitions, we may face competition from other companies in the semiconductor industry. Our ability to acquire targets may also be limited by applicable antitrust laws and other regulations in the United States, the European Union and other jurisdictions in which we do business. To the extent that we are successful in making acquisitions, we may have to expend substantial amounts of cash, incur debt, assume loss-making divisions and incur other types of expenses. We may also face challenges in successfully integrating acquired companies into our existing organization. Each of these risks could have a material adverse effect on our business, financial condition and results of operations.

We may from time to time desire to exit certain product lines or businesses, or to restructure our operations, but may not be successful in doing so.

From time to time, we may decide to divest certain product lines and businesses or restructure our operations, including through the contribution of assets to joint ventures. We have, in recent years, exited several of our product lines and businesses, and we have closed several of our manufacturing and research facilities. We may continue to do so in the future. However, our ability to successfully exit product lines and businesses, or to close or consolidate operations, depends on a number of factors, many of which are outside of our control. For example, if we are seeking a buyer for a particular business line, none may be available, or we may not be successful in negotiating satisfactory terms with prospective buyers. In addition, we may face internal obstacles to our efforts. In particular, several of our operations and facilities are subject to collective bargaining agreements and social plans or require us to consult with our employee representatives, such as work councils which may prevent or complicate our efforts to sell or restructure our businesses. In some cases, particularly with respect to our European operations, there may be laws or other legal impediments affecting our ability to carry out such sales or restructuring.

If we are unable to exit a product line or business in a timely manner, or to restructure our operations in a manner we deem to be advantageous, this could have a material adverse effect on our business, financial condition and results of operations. Even if a divestment is successful, we may face indemnity and other liability claims by the acquirer or other parties.

We may from time to time restructure parts of our processes. Any such restructuring may impact customer satisfaction and the costs of implementation may be difficult to predict.

Between 2008 and 2011, we executed our redesign program (the “Redesign Program”) and in 2013 we executed a restructuring initiative designed to improve operational efficiency and to competitively position the company for sustainable growth (the “OPEX Reduction Program”). We plan to continue to restructure and make changes to parts of the processes in our organization. Furthermore, if the global economy remains as volatile or unstable or if the global economy reenters into a deeper and longer lasting recession, our revenues could decline, and we may be forced to take additional cost savings steps that could result in additional charges and materially affect our business. The costs of implementing any restructurings, changes or cost savings steps may differ from our estimates and any negative impacts on our revenues or otherwise of such restructurings, changes or steps, such as situations in which customer satisfaction is negatively impacted, may be larger than originally estimated.

14

Table of Contents

If we fail to extend or renegotiate our collective bargaining agreements and social plans with our labor unions as they expire from time to time, if regular or statutory consultation processes with employee representatives such as works councils fail or are delayed, or if our unionized employees were to engage in a strike or other work stoppage, our business and operating results could be materially harmed.

We are a party to collective bargaining agreements and social plans with our labor unions. We are also required to consult with our employee representatives, such as works councils, on items such as restructurings, acquisitions and divestitures. Although we believe that our relations with our employees, employee representatives and unions are satisfactory, no assurance can be given that we will be able to successfully extend or renegotiate these agreements as they expire from time to time or to conclude the consultation processes in a timely and favorable way. The impact of future negotiations and consultation processes with employee representatives could have a material impact on our financial results. Also, if we fail to extend or renegotiate our labor agreements and social plans, if significant disputes with our unions arise, or if our unionized workers engage in a strike or other work stoppage, we could incur higher ongoing labor costs or experience a significant disruption of operations, which could have a material adverse effect on our business.

Our working capital needs are difficult to predict.

Our working capital needs are difficult to predict and may fluctuate. The comparatively long period between the time at which we commence development of a product and the time at which it may be delivered to a customer leads to high inventory and work-in-progress levels. The volatility of our customers’ own businesses and the time required to manufacture products also makes it difficult to manage inventory levels and requires us to stockpile products across many different specifications.

Our business may be adversely affected by costs relating to product defects, and we could be faced with product liability and warranty claims.

We make highly complex electronic components and, accordingly, there is a risk that defects may occur in any of our products. Such defects can give rise to significant costs, including expenses relating to recalling products, replacing defective items, writing down defective inventory and loss of potential sales. In addition, the occurrence of such defects may give rise to product liability and warranty claims, including liability for damages caused by such defects. If we release defective products into the market, our reputation could suffer and we may lose sales opportunities and incur liability for damages. Moreover, since the cost of replacing defective semiconductor devices is often much higher than the value of the devices themselves, we may at times face damage claims from customers in excess of the amounts they pay us for our products, including consequential damages. We also face exposure to potential liability resulting from the fact that our customers typically integrate the semiconductors we sell into numerous consumer products, which are then sold into the marketplace. We are exposed to product liability claims if our semiconductors or the consumer products based on them malfunction and result in personal injury or death. We may be named in product liability claims even if there is no evidence that our products caused the damage in question, and such claims could result in significant costs and expenses relating to attorneys’ fees and damages. In addition, our customers may recall their products if they prove to be defective or make compensatory payments in accordance with industry or business practice or in order to maintain good customer relationships. If such a recall or payment is caused by a defect in one of our products, our customers may seek to recover all or a portion of their losses from us. If any of these risks materialize, our reputation would be harmed and there could be a material adverse effect on our business, financial condition and results of operations.

Our business has suffered, and could in the future suffer, from manufacturing problems.

We manufacture, in our own factories as well as subcontracted, our products using processes that are highly complex, require advanced and costly equipment and must continuously be modified to improve yields and performance. Difficulties in the production process can reduce yields or interrupt production, and, as a result of such problems, we may on occasion not be able to deliver products or do so in a timely or cost-effective or

15

Table of Contents

competitive manner. As the complexity of both our products and our fabrication processes has become more advanced, manufacturing tolerances have been reduced and requirements for precision have become more demanding. As is common in the semiconductor industry, we have in the past experienced manufacturing difficulties that have given rise to delays in delivery and quality control problems. There can be no assurance that any such occurrence in the future would not materially harm our results of operations. Further, we may suffer disruptions in our manufacturing operations, either due to production difficulties such as those described above or as a result of external factors beyond our control. We may, in the future, experience manufacturing difficulties or permanent or temporary loss of manufacturing capacity due to the preceding or other risks. Any such event could have a material adverse effect on our business, financial condition and results of operations.

We rely on the timely supply of equipment and materials and could suffer if suppliers fail to meet their delivery obligations or raise prices. Certain equipment and materials needed in our manufacturing operations are only available from a limited number of suppliers.

Our manufacturing operations depend on deliveries of equipment and materials in a timely manner and, in some cases, on a just-in-time basis. From time to time, suppliers may extend lead times, limit the amounts supplied to us or increase prices due to capacity constraints or other factors. Supply disruptions may also occur due to shortages in critical materials, such as silicon wafers or specialized chemicals. Because the equipment that we purchase is complex, it is frequently difficult or impossible for us to substitute one piece of equipment for another or replace one type of material with another. A failure by our suppliers to deliver our requirements could result in disruptions to our manufacturing operations. Our business, financial condition and results of operations could be harmed if we are unable to obtain adequate supplies of quality equipment or materials in a timely manner or if there are significant increases in the costs of equipment or materials.

Failure of our outside foundry suppliers to perform could adversely affect our ability to exploit growth opportunities.

We currently use outside suppliers or foundries for a portion of our manufacturing capacity. Outsourcing our production presents a number of risks. If our outside suppliers are unable to satisfy our demand, or experience manufacturing difficulties, delays or reduced yields, our results of operations and ability to satisfy customer demand could suffer. In addition, purchasing rather than manufacturing these products may adversely affect our gross profit margin if the purchase costs of these products are higher than our own manufacturing costs would have been. Our internal manufacturing costs include depreciation and other fixed costs, while costs for products outsourced are based on market conditions. Prices for foundry products also vary depending on capacity utilization rates at our suppliers, quantities demanded, product technology and geometry. Furthermore, these outsourcing costs can vary materially from quarter to quarter and, in cases of industry shortages, they can increase significantly, negatively affecting our gross profit.

Loss of our key management and other personnel, or an inability to attract such management and other personnel, could affect our business.

We depend on our key management to run our business and on our senior engineers to develop new products and technologies. Our success will depend on the continued service of these individuals. Although we have several share based compensation plans in place, we cannot be sure that these plans will help us in our ability to retain key personnel, especially considering the fact that the stock options under some of our plans become exercisable upon a change of control (in particular, when a third party, or third parties acting in concert, other than the Private Equity Consortium, obtains, whether directly or indirectly, control of us). The loss of any of our key personnel, whether due to departures, death, ill health or otherwise, could have a material adverse effect on our business. The market for qualified employees, including skilled engineers and other individuals with the required technical expertise to succeed in our business, is highly competitive and the loss of qualified employees or an inability to attract, retain and motivate the additional highly skilled employees required for the operation and expansion of our business could hinder our ability to successfully conduct research activities or develop marketable products. The foregoing risks could have a material adverse effect on our business.

16

Table of Contents

Disruptions in our relationships with any one of our key customers could adversely affect our business.

A substantial portion of our revenue is derived from our top customers, including our distributors. We cannot guarantee that we will be able to generate similar levels of revenue from our largest customers in the future. If one or more of these customers substantially reduce their purchases from us, this could have a material adverse effect on our business, financial condition and results of operations.

We receive subsidies and grants in certain countries, and a reduction in the amount of governmental funding available to us or demands for repayment could increase our costs and affect our results of operations.

As is the case with other large semiconductor companies, we receive subsidies and grants from governments in some countries. These programs are subject to periodic review by the relevant governments, and if any of these programs are curtailed or discontinued, this could have a material adverse effect on our business, financial condition and results of operations. As the availability of government funding is outside our control, we cannot guarantee that we will continue to benefit from government support or that sufficient alternative funding will be available if we lose such support. Moreover, if we terminate any activities or operations, including strategic alliances or joint ventures, we may face adverse actions from the local governmental agencies providing such subsidies to us. In particular, such government agencies could seek to recover such subsidies from us and they could cancel or reduce other subsidies we receive from them. This could have a material adverse effect on our business, financial condition and results of operations.

Legal proceedings covering a range of matters are pending in various jurisdictions. Due to the uncertainty inherent in litigation, it is difficult to predict the final outcome. An adverse outcome might affect our results of operations.

We and certain of our businesses are involved as plaintiffs or defendants in legal proceedings in various matters. Although the ultimate disposition of asserted claims and proceedings cannot be predicted with certainty, our financial position and results of operations could be affected by an adverse outcome.

Fluctuations in foreign exchange rates may have an adverse effect on our financial results.

A higher proportion of our revenue is in U.S. dollar or U.S. dollar-related currencies, compared to our costs and expenses resulting in a structural currency mismatch. Accordingly, our results of operations may be affected by changes in foreign exchange rates, particularly between the euro and the U.S. dollar. In addition, we have euro denominated assets and liabilities and, since our reporting currency is the U.S. dollar, the impact of currency translation adjustments to such assets and liabilities may have a negative effect on our stockholders’ equity. In addition, the U.S. dollar-denominated debt issued by our subsidiary, NXP B.V., with functional currency euro may generate adverse currency results in our financial income and expenses. Part of this effect is mitigated due to the application of net investment hedge accounting, since May 2011, pursuant to which the currency results on (part of) the U.S. dollar denominated debt is reported as part of other comprehensive income within equity instead of financial income and expense in the income statement. Absent the application of net investment hedge accounting, we would have recorded an additional benefit of $68 million, before tax, within financial income and expense in the 2013 statement of operations. We continue to hold or convert a part of our cash in euros as a hedge for euro expenses and euro interest payments. We are exposed to fluctuations in exchange rates when we convert U.S. dollars to euro. The ongoing economic weakness in the European Union may intensify these currency exchange risks.

We are exposed to a variety of financial risks, including currency risk, interest rate risk, liquidity risk, commodity price risk, credit risk and other non-insured risks, which may have an adverse effect on our financial results.

We are a global company and, as a direct consequence, movements in the financial markets may impact our financial results. We are exposed to a variety of financial risks, including currency fluctuations, interest rate risk,

17

Table of Contents

liquidity risk, commodity price risk and credit risk and other non-insured risks. We enter into diverse financial transactions with several counterparties to mitigate our currency risk. We only use derivative instruments for hedging purposes. The rating of our debt by major rating agencies may further improve or deteriorate, which could affect our additional borrowing capacity and financing costs.

We are also a purchaser of certain base metals, precious metals and energy used in the manufacturing process of our products, the prices of which can be volatile. Credit risk represents the loss that would be recognized at the reporting date if counterparties failed to perform upon their agreed payment obligations. Credit risk is present within our trade receivables. Such exposure is reduced through ongoing credit evaluations of the financial conditions of our customers and by adjusting payment terms and credit limits when appropriate. We invest available cash and cash equivalents with various financial institutions and are in that respect exposed to credit risk with these counterparties. We actively manage concentration risk on a daily basis adhering to a treasury management policy. We seek to limit the financial institutions with which we enter into financial transactions, such as depositing cash, to those with a strong credit rating wherever possible. If we are unable to successfully manage these risks, they could have a material adverse effect on our business, financial condition and results of operations.

The impact of a negative performance of financial markets and demographic trends on our defined benefit pension liabilities and costs cannot be predicted and may be severe.

We sponsor defined benefit pension plans in a number of countries and a significant number of our employees are covered by our defined benefit pension plans. As of December 31, 2013, we had recognized a net accrued benefit liability of $236 million, representing the unfunded benefit obligations of our defined pension plans. The funding status and the liabilities and costs of maintaining these defined benefit pension plans may be impacted by financial market developments. For example, the accounting for such plans requires determining discount rates, expected rates of compensation and expected returns on plan assets, and any changes in these variables can have a significant impact on the projected benefit obligations and net periodic pension costs. Negative performance of the financial markets could also have a material impact on funding requirements and net periodic pension costs. Our defined benefit pension plans may also be subject to demographic trends. Accordingly, our costs to meet pension liabilities going forward may be significantly higher than they are today, which could have a material adverse impact on our financial condition.

Changes in the tax deductibility of interest may adversely affect our financial position and our ability to service the obligations under our indebtedness.

Effective January 1, 2013 certain new limitations apply to the tax deductibility of interest expense in the Netherlands. A Dutch company that is considered to be financed with excessive debt, may not be entitled to deduct interest expense on such excessive debt. Existing debt is not grandfathered under these rules. The measurement of whether there is excessive debt is based on arithmetic tests based on the amount of equity of the company in relation to the acquisition cost of and capital invested in Netherlands and foreign subsidiaries of the Netherlands consolidated group. When the equity of the company is below a certain minimum threshold, the company may be considered to have excessive debt. Certain safe harbor rules apply when new operational businesses are acquired by the company. Despite this was not the case in 2013 and is not expected for 2014, the application of this limitation on tax deductibility of interest expense may adversely affect our financial position and our ability to service the obligations under our indebtedness.

We are exposed to a number of different tax uncertainties, which could have an impact on tax results.

We are required to pay taxes in multiple jurisdictions. We determine the taxation we are required to pay based on our interpretation of the applicable tax laws and regulations in the jurisdictions in which we operate. We may be subject to unfavorable changes in the respective tax laws and regulations to which we are subject. Tax controls, audits, change in controls and changes in tax laws or regulations or the interpretation given to them may expose us to negative tax consequences, including interest payments and potentially penalties. We have

18

Table of Contents

issued transfer-pricing directives in the areas of goods, services and financing, which are in accordance with the Guidelines of the Organization of Economic Co-operation and Development (OECD). As transfer pricing has a cross border effect, the focus of local tax authorities on implemented transfer pricing procedures in a country may have an impact on results in another country.

Transfer pricing uncertainties can also result from disputes with local tax authorities about transfer pricing of internal deliveries of goods and services or related to financing, acquisitions and divestments, the use of tax credits and permanent establishments, and tax losses carried forward. These uncertainties may have a significant impact on local tax results. We also have various tax assets resulting from acquisitions. Tax assets can also result from the generation of tax losses in certain legal entities. Tax authorities may challenge these tax assets. In addition, the value of the tax assets resulting from tax losses carried forward depends on having sufficient taxable profits in the future.

There may from time to time exist deficiencies in our internal control systems that could adversely affect the accuracy and reliability of our periodic reporting.