Advisory Agreement was approved by the Board of Trustees (including all the independent trustees) on March 23, 2023, effective April 1, 2023 until March 31, 2024. The Board of Trustees has provided investment guidance for the Advisor to follow and must approve each investment recommended by the Advisor. Currently, the Advisor has nine members on the Board, seven of whom are independent.

Although the Trust has executive officers, it does not have any paid employees. The President, Chief Executive Officer, Chief Investment Officer, Chief Financial Officer and Treasurer, and General Counsel and Secretary of the Trust, are also officers, employees, or governors of our Advisor. Among others, such executive officers oversee the Advisor’s day-to-day operations with respect to the Trust. However, when doing so, such executive officers are acting on behalf of the Advisor in performing the Advisor’s obligations under the Advisory Agreement. Generally, the only services performed by the Trust’s executive officers are those required by law or regulation, such as executing documents as required by North Dakota law and providing certifications required by the federal securities laws.

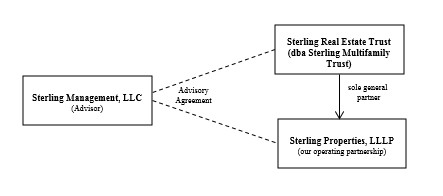

Organizational Structure

On January 1, 2021, the advisor was acquired by Trustmark Enterprises, Inc. in an equity transfer.

The following chart shows the relationship structure with the advisor:

| (1) | As of December 31, 2023, the Advisor was owned 100% by Trustmark Enterprises, Inc. Trustmark was owned in part by the Trust’s Chief Executive Officer and Trustee Kenneth P. Regan (30.00%), by Trustee James S. Wieland (25.00%), by President and Chief Investment Officer Joel S. Thomsen (18.50%), by General Counsel and Secretary Michael P. Carlson (1.00%) and by Chief Financial Officer and Treasurer Damon K. Gleave (1.00%). Messrs. Regan, Thomsen, Carlson, and Gleave serve as officers of the Advisor. Messrs. Regan, Wieland, Thomsen, Carlson, and Gleave serve on the Advisor’s Board of Governors. |

| (2) | Sterling Management, LLC serves as Advisor to both the Trust and the operating partnership. The Advisor does not own any of our shares. Messrs. Regan and Wieland beneficially own approximately 1.43% and 2.81%, respectively, of our shares as of December 31, 2023. |

| (3) | The Trust controls the operating partnership as the general partner and owns approximately 37.72% of the operating partnership as of December 31, 2023. Messrs. Regan and Wieland beneficially owned and had voting power over approximately 16.54% and 5.16%, respectively, of the Operating Partnership as of December 31, 2023. |

CORE INVESTMENT OBJECTIVES AND STRATEGY

Investment Objectives

The Trust’s primary investment objectives are to:

| ● | Acquire quality real estate properties or interests in real estate properties that can provide stable cash flow for distribution to our shareholders, preservation of capital and realization of long-term capital appreciation upon the sale of such properties; |

| ● | Offer an investment option in which the value of the common shares is correlated to real estate as an asset class rather than traditional asset classes such as stocks and bonds; and |

5