| Electronic Articles of Incorporation For |

P06000148652 FILED November 30, 2006 Sec. Of State clewis |

HOMEOWNERS CHOICE, INC.

The undersigned incorporator, for the purpose of forming a Florida profit corporation, hereby adopts the following Articles of Incorporation:

Article I

The name of the corporation is:

HOMEOWNERS CHOICE, INC.

Article II

The principal place of business address:

145 NW CENTRAL PARK PLAZA

SUITE 110

PORT ST. LUCIE, FL. US 34986

The mailing address of the corporation is:

145 NW CENTRAL PARK PLAZA

SUITE 110

PORT ST. LUCIE, FL. US 34986

Article III

The purpose for which this corporation is organized is:

ANY AND ALL LAWFUL BUSINESS.

Article IV

The number of shares the corporation is authorized to issue is:

1,000,000

Article V

The name and Florida street address of the registered agent is:

F&L CORP.

ONE INDEPENDENT DRIVE

SUITE 1300

JACKSONVILLE, FL. 32202

| I certify that I am familiar with and accept the responsibilities of registered agent.

Registered Agent Signature: MARTIN A. TRABER, V.P. |

P06000148652 FILED November 30, 2006 Sec. Of State clewis |

Article VI

The name and address of the incorporator is:

ROBERT H. MACE, JR., C/O FOLEY & LARDNER LLP

100 NORTH TAMPA STREET

SUITE 2700

TAMPA, FLORIDA 33602

Incorporator Signature: ROBERT H. MACE, JR.

Article VII

The initial officer(s) and/or director(s) of the corporation is/are:

Title: D,P

FRANCIS X MCCAHILL III

145 NW CENTRAL PARK PLAZA, SUITE 110

PORT ST. LUCIE, FL. 34986 US

Title: D,VP

RONALD E CHAPMAN

145 NW CENTRAL PARK PLAZA, SUITE 110

PORT ST. LUCIE, FL. 34986 US

Title: CFO

RICHARD A ALLEN

145 NW CENTRAL PARK PLAZA, SUITE 110

PORT ST. LUCIE, FL. 34986 US

Title: D

PARESH PATEL

145 NW CENTRAL PARK PLAZA, SUITE 110

PORT ST. LUCIE, FL. 34986 US

Title: D

MARTIN A TRABER

100 NORTH TAMPA STREET, SUITE 2700

TAMPA, FL. 33602 US

Title: D

GREGORY POLITIS

145 NW CENTRAL PARK PLAZA, SUITE 110

PORT ST. LUCIE, FL. 34986 US

| To: FI Dept of State Subject: 000672.68223 |

From: Tracy Spear | Tuesday, May 08, 2007 9:43 AM Page: 2 of 2 |

| H07000126369 3 | ||

|

ARTICLES OF AMENDMENT

TO THE

ARTICLES OF INCORPORATION

OF

HOMEOWNERS CHOICE, INC.

Pursuant to the provisions of Section 607.1006 of the Florida Business Corporation Act (“FBCA”), Homeowners Choice, Inc., a Florida corporation (the “Corporation”) hereby adopts the following Articles of Amendment to its Articles of Incorporation:

1. The name of the Corporation is Homeowners Choice, Inc.

2. The Corporation was incorporated in the State of Florida on November 30, 2006, and assigned Document Number P06000148652.

3. Article IV of the Articles of Incorporation of the Corporation is hereby amended and restated to read in its entirety as follows:

“ARTICLE IV

The number of shares the Corporation is authorized to issue is 100,000,000 without par value consisting of 50,000,000 shares of Common Stock and 50,000,000 shares of Non-Voting Preferred Stock.”

4. The foregoing Amendment to the Articles of Incorporation was adopted and approved by the Board of Directors and by the Shareholders of the corporation, in accordance with section 607.1003 of the Florida Statutes, effective as of March 1, 2007.

5. The foregoing amendment to the Corporation’s Articles of Incorporation will become effective upon the filing of these Articles of Amendment to the Articles of Incorporation with the Florida Department of State.

WHEREUPON, this 3rd day of May, 2007, the Corporation has caused its President to execute these Articles of Amendment to Articles of Incorporation to be effective as of March 1, 2007.

|

|

| By: |

|

|||||

| Francis X. McCahill, III, President & CEO | ||||||

| H07000126369 3 | ||||||

| ||

| ARTICLES OF AMENDMENT TO THE ARTICLES OF INCORPORATION OF HOMEOWNERS CHOICE, INC. |

||

|

Pursuant to the provisions of Section 607.1006 of the Florida Business Corporation Act (“FBCA”), Homeowners Choice, Inc., a Florida corporation (the “Corporation”) hereby adopts the following Articles of Amendment to its Articles of Incorporation:

1. The name of the Corporation is Homeowners Choice, Inc.

2. The Corporation was incorporated in the State of Florida on November 30, 2006, and assigned Document Number P06000148652.

3. Article JV of the Articles of Incorporation of the Corporation is hereby amended and hereafter restated to read in its entirety as follows:

“ARTICLE IV

The number of shares the Corporation is authorized to issue is 150,000,000, without par value, consisting of 100,000,000 shares of Common Stock and 50,000,000 shares of Preferred Stock. The Board of Directors is expressly authorized, pursuant to Section 607.0602 of the Florida Business Corporation Act (“FBCA”), to provide for the classification and reclassification of any unissued shares of Preferred Stock and the issuance thereof in one or more classes or series without approval of the shareholders of the Corporation, all within the limitations set forth in Section 607.0601 of the FBCA.”

4. Article VII of the Articles of Incorporation of the Corporation is hereby amended and hereafter restated to read in its entirety as follows:

“ARTICLE VII

The Board of Directors shall be classified by or pursuant to these Articles of Incorporation or by the Bylaws of the Corporation. The directors shall be classified, with respect to the time for which they severally hold office, into three classes, Class A, Class B and Class C, each of which shall be as nearly equal number as possible, and shall be adjusted from time to time in the manner specified in the Bylaws to maintain such proportionality. Each initial director in Class A shall hold office for a term expiring at the 2009 annual meeting of the shareholders; each director in Class B shall hold office for a term expiring at the 2010 annual meeting of the shareholders; and each director in Class C shall hold office for a term expiring at the 2011 annual meeting of the shareholders. Notwithstanding the foregoing provisions of this Article VII, each director shall serve until such director’s successor is duly elected and qualified or until such director’s earlier death, resignation or removal. At each annual meeting of the shareholders, successors to the class of directors whose term expires at that meeting shall be elected to hold office for a term expiring at the annual meeting of the shareholders held in the third year following the year of election and until their successors shall have been duly elected and qualified or until such director’s earlier death, resignation or removal.” |

| 5. The Board of Directors of the Corporation duly adopted and approved resolutions on April 8, 2008 proposing and declaring advisable that the Articles of Incorporation be amended by deleting the existing ARTICLES “IV” and “VII” in their entirety and substituting therefore the aforesaid amendments.

6. The aforesaid proposed amendments were adopted and approved by a vote of the shareholders of the Corporation at the annual meeting on May 29, 2008. The number of votes cast for the amendments was sufficient. All shares of stock of the Corporation are shares of common stock and there was no group entitled to vote separately.

7. The aforesaid amendments to the Corporation’s Articles of Incorporation do not provide for an exchange, reclassification or cancellation of issued shares.

8. The aforesaid amendments to the Corporation’s Articles of Incorporation will be become effective upon the filing of these Articles of Amendment to the Articles of Incorporation with the Florida Department of State.

IN WITNESS WHEREOF, Homeowners Choice, Inc. has caused these Articles of Amendment of the Articles of Incorporation to be executed by its President on this 29th of May, 2008.

|

| HOMEOWNERS CHOICE, INC. | ||||||

| By: |

|

|||||

| Paresh Patel, Chairman of the Board | ||||||

(((H08000152607 3)))

| ARTICLES OF AMENDMENT TO THE ARTICLES OF INCORPORATION OF HOMEOWNERS CHOICE, INC.

Pursuant to the provisions of Section 607-1006 of the Florida Business Corporation Act (“FBCA”), Homeowners Choice, Inc., a Florida corporation (the “Corporation”), hereby adopts the following Articles of Amendment to its Articles of Incorporation:

1. The name of the Corporation is Homeowners Choice, Inc.

2. The Corporation was incorporated in the State of Florida on November 30, 2006, and assigned Document Number P06000148652.

3. Article IV of the Articles of Incorporation of the Corporation is hereby amended and hereafter restated to read in its entirety as follows:

ARTICLE IV

Section 4.01 Reverse Stock Split. Effective 5:00 P.M. June 16, 2008 (the “Effective Time”), each two and one-half shares of Common Stock of the Corporation (“Old Common Stock”) issued and outstanding immediately prior to the Effective Time shall be automatically combined, reclassified and exchanged into one share of Common Stock of the Corporation (“New Common Stock”).

No fractional shares of New Common Stock will result from or be issued in connection with the foregoing combination, reclassification and exchange of shares of Old Common Stock.

|

| |

| Each stock certificate that, immediately prior to the Effective Time, represented shares of Old Common Stock shall, from and after the Effective Time, automatically and without the necessity of presenting the certificate for exchange, represent that number of shares of New Common Stock into which the shares of Old Common Stock represented by such certificate have been combined, exchanged and reclassified; provided, however, that each holder of record of certificate that represented shares of Old Common Stock shall receive, upon surrender of such certificate, a new certificate representing the number of shares of New Common Stock into which the shares of Old Common Stock represented by such certificate have been combined, exchanged and reclassified.

At the Effective Time, the number of authorized shares will be correspondingly reduced as reflected in Section 4.02 below.

Section 4.02 Authorized Shares. The number of shares the Corporation is authorised to issue is 60,000,000, without par value, consisting of 40,000,000 shares of Common Stock and 20,000,000 shares of Preferred Stock. The Board of Directors is expressly authorized, pursuant to Section 607.0602 of |

| Carolyn T. Long, Esquire Florida Bar # 0050032 Foley & Lardner 100 N. Tampa Street, Suite 2700 Tampa, Florida 33602 Phone 813-229-2300 |

(((H08000152607 3))) |

(((H08000152607 3)))

| the Florida Business Corporation Act (“FBCA”), to provide for the classification and reclassification of any unissued shares of Preferred Stock and the issuance thereof in one or more classes or series without approval of the shareholders of the Corporation, all within the limitations set forth in Section 607.0601 of the FBCA.

* * * * * * * * *

4. The Board of Directors of the Corporation duly adopted and approved a resolution proposing that the shareholders approve the aforesaid amendment and declaring advisable the aforesaid amendment on May 7, 2008.

5. The aforesaid amendment was adapted and approved by a vote of the shareholders of the Corporation at the annual meeting on May 29, 2008. The number of votes cast for the amendments was sufficient. All issued shares of stock of the Corporation are shares of common stock and there was no group entitled to vote separately.

6. The provisions for implementing the combination, exchange and reclassification of issued shares of the Corporation are contained in this Articles of Amendment to the Articles of Incorporation of the Corporation.

7. This amendment does not adversely affect the rights or preferences of the holders of the outstanding shares of any class or series of the Corporation and does not result in the percentage of authorized shares that remain unissued after the combination exceeding the percentage of authorized shares that were unissued before the combination.

8. The aforesaid amendment to the Corporation’s Articles of Incorporation will be become affective upon filing on June 16, 2008.

IN WITNESS WHEHEOF, Homeowners Choice, Inc. has caused these Articles of Amendment of the Articles of Incorporation to be executed by its Chairman on this 16th of June, 2008. |

| HOMEOWNERS CHOICE, INC. | ||||||

| By: |

|

|||||

| Paresh Patel, Chairman of the Board | ||||||

(((H08000152607 3)))

| H11000059959 3 | ||

|

ARTICLES OF AMENDMENT TO THE ARTICLES OF INCORPORATION OF

HOMEOWNERS CHOICE, INC.

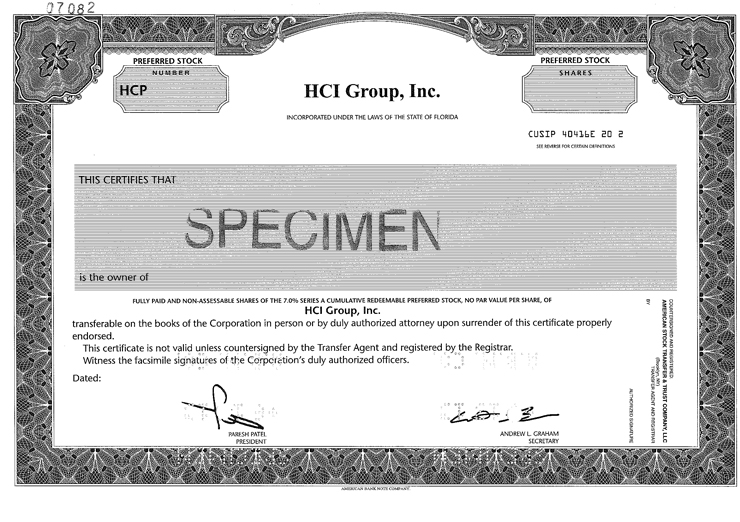

DESIGNATION OF RIGHTS, PREFERENCES, AND LIMITATIONS OF SERIES A CUMULATIVE REDEEMABLE PREFERRED STOCK

FIRST: This Corporation is named Homeowners Choice, Inc, (the “Corporation”). The Articles of Incorporation of the Corporation were originally filed with the Secretary of State of the State of Florida and became effective on November 30, 2006. Articles of Amendment to the Articles of Incorporation were filed and became effective on May 8, 2007, June 3, 2008, and June 16, 2008.

SECOND: Pursuant to the authority of the Board of Directors of the Corporation set forth in the Corporation’s Articles of Incorporation, as amended, and Section 607.0602 of the Florida Business Corporation Act, the Board of Directors of the Corporation, by resolutions duly adopted as of January 26, 2011, has amended the Corporation’s Articles of Incorporation to (i) designate a series of preferred stock of the Corporation as “Series A Cumulative Redeemable Preferred Stock,” consisting of 1,500,000 shares of the Corporation’s authorized but unissued preferred stock, (ii) authorize the issuance of a maximum of 1,500,000 shares of Series A Cumulative Redeemable Preferred Stock, and (iii) set the rights, preferences, limitations, and other terms and conditions of the Series A Cumulative Redeemable Preferred Stock. Approval of the shareholders of the Corporation was not required.

THIRD: Article IV of the Articles of Incorporation of the Corporation is hereby amended to add the following Section 4.03:

“Section 4.03 Series A Cumulative Redeemable Preferred Stock.

1. Designation and Amount. A total of 1,500,000 shares of preferred stock, no par value per share, of the Corporation shall be designated “Series A Cumulative Redeemable Preferred Stock.”

2. Rank. All shares of Series A Cumulative Redeemable Preferred Stock (the “Series A Preferred”) will, with respect to dividend rights and rights upon liquidation, dissolution or winding up of the Corporation, rank (a) prior or senior to the Common Stock issued by the Corporation; (b) prior or senior to all classes or series of preferred stock issued by the Corporation, the terms of which specifically provide that such shares rank junior to the Series A Preferred with respect to dividend rights or rights upon liquidation, dissolution or winding up of the Corporation; (c) on a parity with all classes or series of shares of preferred stock issued by the Corporation, the terms of which specifically provide that such shares rank on a parity with the Series A Preferred with respect to dividend rights or rights upon liquidation, dissolution or winding up of the Corporation (the “Parity Shares”); and (d) junior to all existing and future indebtedness of the Corporation. |

|

| H11000059959 3 |

| H11000059959 3 |

| 3. Maturity. The Series A Preferred has no stated maturity and will not be subject to any sinking fund or mandatory redemption.

4. Dividends.

(a) Holders of the Series A Preferred shall be entitled to receive, when and as authorized by the Board of Directors of the Corporation, or a duly authorized committee thereof, and declared by the Corporation out of funds of the Corporation legally available for payment, preferential cumulative cash dividends at the rate of 7.00% per annum of the Liquidation Preference (as defined below) per share (equivalent to a fixed annual amount of $0.70 per share). Such dividends shall be cumulative from the date of original issue and shall accrue on the last day of each month (each a “Dividend Accrual Date”) for the period ending on such Dividend Accrual Date, commencing on the date of issue. The first dividend will accrue on May 31, 2011 with respect to the period beginning on the dare of issue and ending on May 31, 2011. Any dividend accruing on the Series A Preferred for any partial dividend period will be computed on the basis of twelve 30-day months and a 360-day year. Dividends will be payable in arrears to holders of record as they appear on the share transfer records of the Corporation at the close of business on the applicable record date, which shall be the date designated by the Board of Directors of the Corporation as the record date for the payment of dividends (each, a “Dividend Record Date”). When so designating the Dividend Record Date, the Board of Directors shall establish the date of payment for such accrued dividends (each, a “Dividend Payment Date”), which date shall be no more than 30 nor less than 10 days after such Dividend Record Date.

(b) No dividends on the Series A Preferred shall be authorized by the Board of Directors of the Corporation or declared or paid or set apart for payment by the Corporation at such time as the terms and provisions of any agreement of the Corporation, including any agreement relating to its indebtedness, prohibits such declaration, payment or setting apart for payment or provides that such declaration, payment or setting apart for payment would constitute a breach thereof or a default thereunder, or if such declaration, payment or setting apart for payment shall be restricted or prohibited by law.

(c) Notwithstanding the foregoing, dividends on the Series A Preferred will accrue whether or not the Corporation has earnings, whether or not there are funds legally available for the payment of such dividends, whether or not such dividends are declared and whether or not such dividends are prohibited by agreement. Accrued but unpaid dividends on the Series A Preferred will accumulate and earn additional dividends at 7.00%, compounded monthly. Except as set forth in the next sentence, the Board of Directors of the Corporation shall not declare, pay or set apart for payment any dividends on any other class or series of preferred stock ranking, as to dividends, on a parity with or junior to the Series A Preferred (other than a dividend payable in capital stock of the Corporation ranking junior to the Series A Preferred as to dividends and upon liquidation) if, after the tenth (10th) day after the respective Dividend Accrual Date, the Corporation has not paid in full the cumulative dividends on the Series A Preferred due thereon; following payment of such cumulative dividends, however, the Board of |

| H11000059959 3 |

2

| H11000059959 3 |

| Directors of the Corporation may then declare, pay or set apart for payment any dividends on any other class or series of preferred stock ranking, as to dividends, on a parity with or junior to the Series A Preferred. When dividends are not paid in full (or a sum sufficient for such full payment is not so set apart) upon the Series A Preferred and the shares of any other class or series of preferred stock ranking on a parity as to dividends with the Series A Preferred, all dividends declared upon the Series A Preferred and any other class or series of preferred stock ranking on a parity as to dividends with the Series A Preferred shall be declared pro rata so that the amount of dividends declared per share of the Series A Preferred and such other class or series of preferred stock, shall in all cases bear to each other the same ratio that accrued dividends per share on the Series A Preferred and such other class or series of preferred stock (which shall not include any accrual in respect of unpaid dividends for prior dividend periods if such preferred stock does not have a cumulative dividend) bear to each other.

(d) Unless full cumulative dividends on the Series A Preferred have been or contemporaneously are declared and paid or declared and a sum sufficient for the payment thereof is set apart for payment for all past dividend periods and the then current dividend period, neither the Common Stock, nor any other class or series of capital stock of the Corporation ranking junior to or on a parity with the Series A Preferred as to dividends or upon liquidation may be redeemed, purchased or otherwise acquired for any consideration (or any moneys be paid to or made available for a sinking fund for the redemption of any such shares) by the Corporation (except by conversion into or exchange for any other class or series of capital stock of the Corporation ranking junior to the Series A Preferred as to dividends). Holders of the Series A Preferred shall not be entitled to any dividend, whether payable in cash, property or stock, in excess of full cumulative dividends on the Series A Preferred as provided above. Any dividend payment made on the Series A Preferred shall first be credited against the earliest accrued but unpaid dividend due with respect to such shares which remains payable,

5. Liquidation Preference.

(a) Upon any voluntary or involuntary liquidation, dissolution or winding up of the affairs of the Corporation, the holders of the Series A Preferred are entitled to be paid out of the assets of the Corporation legally available for distribution to its shareholders a liquidation preference of $10.00 per share (the “Liquidation Preference”) in cash or property at Us fair market value as determined by the Board of Directors of the Corporation, plus an amount equal to any accrued and unpaid dividends to the date of payment, but without interest, before any distribution of assets is made to holders of the Corporation’s Common Stock or any other class or series of capital stock of the Corporation that ranks junior to the Series A Preferred as to liquidation rights. The Corporation will promptly provide to the holders of the Series A Preferred written notice of any event triggering the right to receive such Liquidation Preference. After payment of the full amount of the Liquidation Preference, plus any accrued and unpaid dividends to which they are entitled, the holders of the Series A Preferred will have no right or claim to any of the remaining assets of the Corporation. The consolidation or merger of the Corporation with or into any other corporation, trust or entity or of any other corporation, trust or entity with or into the Corporation, the sale, lease or conveyance of all |

| H11000059959 3 |

3

| H11000059959 3 |

| or substantially all of the property or business of the Corporation or a statutory share exchange, shall not be deemed to constitute a liquidation, dissolution or winding up of the Corporation, unless a liquidation, dissolution or winding up of the Corporation is effected in connection with, or as a step in a series of transactions by which, a consolidation or merger of the Corporation is effected. In determining whether a distribution (other than upon voluntary or involuntary liquidation) by dividend, redemption or other acquisition of shares of capital stock of the Corporation or otherwise is permitted under Florida law, no effect shall be given to amounts that would be needed, if the Corporation were to be dissolved at the time of the distribution, to satisfy the preferential rights upon distribution to holders of shares of capital stock of the Corporation whose preferential rights upon distribution are superior to those receiving the distribution.

(b) If upon any liquidation, dissolution or winding up of the Corporation, the assets of the Corporation, or proceeds thereof, distributable among the holders of the Series A Preferred shall be insufficient to pay in full the above described preferential amount and liquidating payments on any other class or series of Parity Shares, then such assets, or the proceeds thereof, shall be distributed among the holders of the Series A Preferred and any such other Parity Shares ratably in the same proportion as the respective amounts that would be payable on such Series A Preferred and any such other Parity Shares if all amounts payable thereon were paid in full.

(c) Upon any liquidation, dissolution or winding up of the Corporation, after payment shall have been made in full to the holders of the Series A Preferred and any Parity Shares, the holders of Common Stock shall be entitled to receive any and all assets remaining to be paid or distributed, and the holders of the Series A Preferred and any Parity Shares shall not be entitled to share therein.

6. Redemption.

(a) The Corporation may, at its option, upon not less than 30 nor more than 60 days’ written notice, redeem the Series A Preferred, in whole or in pan, at any lime or from time to time, for cash at a redemption price equal to (i) 104% of the Liquidation Preference per share on or after March 31, 2014, (ii) 102% of the Liquidation Preference per share on or after March 31, 2015, (iii) the Liquidation Preference per share on or after March 31, 2016, and (iv) provided that the Corporation has previously canceled the conversion rights of the holders of the Series A Preferred pursuant to a Conversion Cancellation Notice (as defined in subsection 8(b)) that was issued in accordance with the terms of subsection 8(b), the Liquidation Preference per share on or after a Conversion Cancellation Event (as defined in subsection 8(b)), plus, in each case, all accrued and unpaid dividends thereon to the date fixed for redemption (the “Redemption Date”), without Interest.

(b) No Series A Preferred may be redeemed except with assets legally available for the payment of the redemption price. Holders of Series A Preferred to be redeemed shall surrender such Series A Preferred at the place designated in such notice and shall be entitled to the redemption price and any accrued and unpaid dividends payable upon such redemption following such surrender. If notice of redemption of any |

| H11000059959 3 |

4

| H11000059959 3 |

| of the Series A Preferred has been given and if the funds necessary for such redemption have been set aside, separate and apart from other funds, by the Corporation in trust for the pro rata benefit of the holders of any Series A Preferred so called for redemption, then from and after the Redemption Date dividends will cease to accrue on such Series A Preferred, such Series A Preferred shall no longer be deemed outstanding and all rights of the holders of such shares will terminate, except the right to receive the redemption price, If less than all of the outstanding Series A Preferred is to be redeemed, the Series A Preferred to be redeemed shall be selected pro rata (as nearly as may be practicable without creating fractional shares) or by any other equitable method determined by the Corporation.

(c) Unless full cumulative dividends on all Series A Preferred shall have been or contemporaneously are declared and paid or declared and a sum sufficient for the payment thereof set apart for payment for all past dividend periods and the then current dividend period, no Series A Preferred shall be redeemed unless all outstanding Series A Preferred is simultaneously redeemed and the Corporation shall not purchase or otherwise acquire, directly or indirectly, any Series A Preferred (except by exchange for any other class or series of capital stock of the Corporation ranking junior to the Series A Preferred as to dividends and upon liquidation); provided, however, that the foregoing shall not prevent the purchase or acquisition of Series A Preferred pursuant to a purchase or exchange offer made on the same terms to holders of all outstanding Series A Preferred. So long as no dividends are in arrears, the Corporation shall be entitled at any time and from time to time to repurchase any Series A Preferred in open-market transactions duly authorized by the Board of Directors of the Corporation and effected in compliance with applicable laws.

(d) Notice of redemption of the Series A Preferred shall be mailed by the Corporation by first class mail, postage prepaid, not less than 30 nor more than 60 days prior to the Redemption Date, addressed to each holder of record of the Series A Preferred to be redeemed at such holder’s address as the same appears on the share transfer records of the Corporation. No failure to give such notice or any defect therein or in the mailing thereof shall affect the validity of the proceedings for the redemption of any Series A Preferred except as to the holder to whom notice was defective or not given. Each notice shall state; (0 the Redemption Date; (ii) the redemption price; (iii) the number of shares of Series A Preferred to be redeemed; and (iv) the place or places where the Series A Preferred is to be surrendered for payment of the redemption price.

(e) Immediately prior to any redemption of Series A Preferred, the Corporation shall pay, in cash, any accumulated and unpaid dividends through the Redemption Date, unless a Redemption Date falls after a Dividend Record Date and prior to the corresponding Dividend Payment Date, in which case each holder of Series A Preferred at the close of business on such Dividend Record Date shall be entitled to the dividend payable on such shares on the corresponding Dividend Payment Date notwithstanding the redemption of such shares before such Dividend Payment Date. |

| H11000059959 3 |

5

| H11000059959 3 |

|

(f) The Series A Preferred has no stated maturity and will not be subject to any sinking fund or mandatory redemption provisions.

(g) Subject to applicable law and the limitation on purchases when dividends on the Series A Preferred are in arrears, the Corporation may, at any time and from time to time, purchase any Series A Preferred in the open market, by tender or by private agreement.

(h) All Series A Preferred redeemed, purchased or otherwise acquired by the Corporation in any manner whatsoever shall be retired and reclassified as authorized but unissued preferred stock, without designation as to class or series, and may thereafter be reissued as any class or series of preferred stock in accordance with the applicable provisions of these Articles of Incorporation.

7. Voting Rights.

(a) Holders of the Series A Preferred will not have any voting rights, except as set Forth below.

(b) Whenever dividends on any Series A Preferred shall have not been declared and fully paid for more than six (6) consecutive months (a “Preferred Dividend Default”), the number of directors then constituting the Board of Directors of the Corporation shall increase by two (if not already increased by reason of a similar arrearage with respect to any Parity Preferred (as hereinafter defined)). The holders of such Series A Preferred (voting separately as a class with all other classes or series of preferred stock ranking on a parity with the Series A Preferred as to dividends or upon liquidation and upon which like voting rights have been conferred and are exercisable (“Parity Preferred”)) will be entitled to vote separately as a class, in order to fill the vacancies thereby created, for the election of a total of two additional directors of the Corporation (the “Preferred Stock Directors”) at a special meeting called by the holders of record of at least 20% of the Series A Preferred or the holders of record of at least 20% of any series of Parity Preferred so in arrears (unless such request is received less than 90 days before the date fixed for the next annual or special meeting of the shareholders) or at the next annual meeting of shareholders, and at each subsequent annual meeting at which a Preferred Stock Director is to be elected until up to twelve months after all dividends accumulated on such Series A Preferred and Parity Preferred for the past dividend periods and the dividend for the then current dividend period shall have been fully paid or declared and a sum sufficient for the payment thereof set aside for payment. At least one of the Preferred Stock Directors shall meet the “independence” standards mandated by The Nasdaq Stock Market LLC (the “Nasdaq”), or such other exchange or inter-dealer market upon which the Series A Preferred is traded. For so long as the directors of the Corporation are divided into classes, each such vacancy shall be apportioned among the classes of directors to prevent stacking in any one class and to ensure that the number of directors in each of the classes of directors are as equal as possible. Within twelve months after all accumulated dividends and the dividend for the then current dividend period on the Series A Preferred shall have been paid in full or declared and set aside for payment in full the holders thereof shall be divested of the |

| H11000059959 3 |

6

| H11000059959 3 |

| foregoing voting rights (subject to revesting in the event of each and every Preferred Dividend Default) and, if all accumulated dividends and the dividend for the then current dividend period have been paid in full or set aside for payment in full on the Series A Preferred and all series of Parity Preferred upon which like voting rights have been conferred and are exercisable, the term of office of each Preferred Stock Director so elected shall terminate within twelve months thereafter and the number of directors then constituting the Board of Directors of the Corporation shall decrease accordingly, Any Preferred Stock Director may be removed at any time with or without cause by, and shall not be removed otherwise than by, the vote of the holders of record of a majority of the outstanding Series A Preferred when they have the voting rights described above (voting separately as a class with all series of Parity Preferred upon which like voting rights have been conferred and are exercisable). So long as a Preferred Dividend Default shall continue, any vacancy in the office of a Preferred Stock Director may be filled by written consent of the Preferred Stock Director remaining in office, or if none remains in office, by a vote of the holders of record of a majority of the outstanding shares of the Series A Preferred when they have the voting rights described above (voting separately as a class with all series of Parity Preferred upon which like voting rights have been conferred and are exercisable). The Preferred Stock Directors shall each be entitled to one vote per director on any matter.

(c) So long as any shares of the Series A Preferred remain outstanding, the Corporation will not, without the affirmative vote or consent of the holders of the Series A Preferred entitled to cast at least two-thirds of the votes entitled to be cast by the holders of the Series A Preferred, given in person or by proxy, either in writing or at a meeting (voting separately as a class):

(i) amend, alter or repeal the provisions of the Corporation’s Articles of Incorporation, whether by merger, consolidation or otherwise (an “Event”), so as to materially and adversely affect any right, preference, privilege or voting power of the Series A Preferred or the holders thereof; or

(ii) authorize, create or issue, or increase the authorized or issued amount of, any class or series of capital stock or rights to subscribe to or acquire any class or series of capital stock or any class or series of capital stock convertible into any class or series of capital stock, in each case ranking senior to the Series A Preferred with respect to payment of dividends or the distribution of assets upon liquidation, dissolution or winding up, or reclassify any shares of capital stock into any such shares;

provided, however, that with respect to the occurrence of any Event set forth above, so long as the Series A Preferred (or any equivalent class or series of stock or shares issued by the surviving corporation, trust or other entity in any merger or consolidation to which the Corporation became a party) remains outstanding with the terms thereof materially unchanged, the occurrence of any such Event shall not be deemed to materially and adversely affect such rights, preferences, privileges or voting power of holders of the Series A Preferred; and provided, further, that (i) any increase in the amount of the authorized preferred stock or the creation or issuance of any other class or series of preferred stock, (ii) any increase in the amount of the authorized shares |

| H11000059959 3 |

7

| H11000059959 3 |

| of such series, in each case ranking on a parity with or junior to the Series A Preferred with respect to payment of dividends or the distribution of assets upon liquidation, dissolution or winding up or (iii) any merger or consolidation in which the Corporation is not the surviving entity if, as a result of the merger or consolidation, the holders of Series A Preferred receive cash in the amount of the Liquidation Preference in exchange for each of their shares of Series A Preferred, shall not be deemed to materially and adversely affect such rights, preferences, privileges or voting powers.

(d) With respect to the exercise of the above described voting rights, each share of the Series A Preferred shall have one vote per share, except that when any other class or series of capital stock shall have the right to vote with the Series A Preferred as a single class, then the Series A Preferred and such other class or series of capital stock shall each have one vote per $10.00 of liquidation preference.

(e) The foregoing voting provisions will not apply if, at or prior to the time when the act with respect to which such vote would otherwise be required shall be effected, ail outstanding shares of the Series A Preferred shall have been redeemed or called for redemption upon proper notice and sufficient funds shall have been deposited in trust to effect such redemption.

(f) Except as expressly stated herein, the Series A Preferred shall not have any relative, participating, optional or other special voting rights and powers, and the consent of the holders thereof shall not be required for the taking of any corporate action, including but not limited to, (i) any merger or consolidation involving the Corporation or a sale of all or substantially all of the assets of the Corporation, irrespective of the effect that such merger, consolidation or sale may have upon the rights, preferences or voting power of the holders of the Series A Preferred, or (ii) any authorization, creation or issuance, or increase in the authorized or issued amount of, any class or series of Parity Preferred or rights to subscribe to or acquire any class or series of Parity Preferred or any class or series of capital stock convertible into any class or series of Parity Preferred, or reclassification of any shares of capital stock into any such shares.

8. Conversion.

(a) Subject to and upon compliance with the provisions of this subsection 8, a holder of the Series A Preferred shall have the right, at the holder’s option, at any time to convert such shares, in whole or in part, into the number of authorized but previously unissued shares of Common Stock obtained by dividing the aggregate Liquidation Preference of such shares by $10.00, the conversion price per share of Common Stock at which the Series A Preferred is convertible into shares of Common Stock, as such price may be adjusted pursuant to paragraph (g) of this subsection 8 (the “Conversion Price”) (as in effect at the time and on the date provided for paragraph (c) of this subsection 8) by delivering such shares to be converted, such delivery to be made in the manner provided in paragraph (c) of this subsection 8; provided, however, that the right to convert shares called for redemption pursuant to subsection 6 of this Section 4.03 shall terminate at the close of business on the Business Day prior to the Redemption Date, unless the Corporation shall default in making payment of any amounts payable upon such |

| H11000059959 3 |

8

| H11000059959 3 |

| redemption under subsection 6 of this Section 4.03, “Business Day” shall mean any day other than a Saturday, Sunday or other day on which commercial banks in the City of New York are authorized or required to close. (b) The conversion rights of the holders of the Series A Preferred are subject to cancellation by the Corporation on or after March 31, 2014 if, (i) for at least 20 Trading Days (as defined below) within any period of 30 consecutive Trading Days, the Current Market Price (as defined below) of the Common Stock of the Corporation exceeds the Conversion Price by more than 20% and (ii) the Common Stock is then traded on the New York Stock Exchange, the NASDAQ Global Select Market, the NASDAQ Global Market, the NASDAQ Capital Market, or the NYSE Amex (a “Conversion Cancellation Event”). Within 90 days of the occurrence of a Conversion Cancellation Event, the Corporation may, at its option, provide notice to the respective holders of record of the Series A Preferred at their respective addresses as they appear on the share transfer records of the Corporation, via first class mail, specifying a date upon which each such holder’s conversion rights will be deemed cancelled (a “Conversion Cancellation Notice”). The cancellation date specified in the Conversion Cancellation Notice will be more than 30 days, but less than 60 days, after the Conversion Cancellation Notice is mailed. The right to convert the shares of the Series A Preferred for which any Conversion Cancellation Notice has been issued will terminate at the close of business on the Business Day prior to the cancellation date specified in the Conversion Cancellation Notice. “Trading Day” shall mean any day on which the securities in question are traded on the Nasdaq Global Select Market, or if such securities are not listed or admitted for trading on the Nasdaq Global Select Market, on the principal national securities exchange on which such securities are listed or admitted, or if not listed or admitted for trading on any national securities exchange, in the applicable securities market in which the securities are traded. “Current Market Price” of the Common Stock of the Corporation for any day shall mean the last reported sales price on such day or, if no sale takes place on such day, the average of the reported closing bid and asked prices on such day, in either case as reported on the Nasdaq Global Select Market or, if such security is not listed or admitted for trading on the Nasdaq Global Select Market, on the principal national securities exchange on which such security is listed or admitted for trading or, if not listed or admitted for trading on any national securities exchange, the average of the closing bid and asked prices on such day in the over-the-counter market as reported by Nasdaq or, if bid and asked prices for such security on such day shall not have been reported through Nasdaq, the average of the bid and asked prices on such day as furnished by any Nasdaq member firm regularly making a market in such security and selected for such purpose by the Board of Directors of the Corporation or, if such security is not so listed or quoted, as determined in good faith at the sole discretion of the Board of Directors of the Corporation, which determination shall be final, conclusive and binding.

(c) In order to exercise the conversion right, the holder of the Series A Preferred to be converted shall deliver the certificate evidencing such shares, duly endorsed or assigned to the Corporation or in blank, to the office of the transfer agent of the Corporation, accompanied by written notice to the Corporation that the holder thereof elects to convert such shares of Series A Preferred. Unless the shares issuable on |

| H11000059959 3 |

9

| H11000059959 3 |

| conversion are to be issued in the same name as the name in which such shares of Series A Preferred are registered, each share surrendered for conversion shall be accompanied by instruments of transfer, in form satisfactory to the Corporation, duly executed by the holder or such holder’s duly authorized agent and an amount sufficient to pay any transfer or similar tax (or evidence reasonably satisfactory to the Corporation demonstrating that such taxes have been paid).

(d) Holders of Series A Preferred exercising their conversion rights will not be entitled to, nor will the Conversion Price be adjusted for, any accumulated and unpaid dividends, whether or not in arrears, or for dividends on the Common Stock issued upon conversion. Holders of Series A Preferred at the close of business on a Dividend Record Date will be entitled to receive the dividend payable on such shares on the corresponding Dividend Payment Date notwithstanding the conversion of such shares following such Dividend Record Date and prior to such Dividend Payment Date. However, Series A Preferred surrendered for conversion during the period between the close of business on any Dividend Record Date and ending with the opening of business on the corresponding Dividend Payment Dale (except shares converted after the issuance of a notice of redemption with respect to a Redemption Date during such period or coinciding with such Dividend Payment Date, which will be entitled to such dividend on the Dividend Payment Date) must be accompanied by payment of an amount equal to the dividend payable on such shares on such Dividend Payment Date. A holder of Series A Preferred on a Dividend Record Date who (OR whose transferee) tenders any such shares for conversion into Common Stock on such Dividend Payment Date will receive the dividend payable by the Corporation on such Series A Preferred on such date, and the converting holder need not include payment of the amount of such dividend upon surrender of Series A Preferred for conversion.

(e) As promptly as practicable after the surrender of certificates for Series A Preferred as aforesaid, the Corporation shall issue and shall deliver at such office to such holder, or on his written order, a certificate or certificates for the number of full shares of Common Stock issuable upon the conversion of such shares in accordance with the provisions of this subsection 8, and any fractional interest in respect of a share of Common Stock arising upon such conversion shall be settled as provided in paragraph (0 of this subsection 8. Each conversion shall be deemed to have been effected immediately prior to the close of business on the date on which the certificates for Series A Preferred shall have been surrendered and such notice (and if applicable, payment of an amount equal to the dividend payable on such shares as described above) received by the Corporation as aforesaid, and the person or persons in whose name or names any certificate or certificates for Common Stock shall be issuable upon such conversion shall be deemed to have become the holder or holders of record of the shares represented thereby at such time on such date, and such conversion shall be at the Conversion Price in effect at such time and on such date, unless the share transfer books of the Corporation shall be closed on that date, in which event such person or persons shall be deemed to have become such holder or holders of record at the opening of business on the next succeeding day on which such share transfer books are open, but such conversion shall be at the Conversion Price in effect on the date on which such certificates for Series A Preferred have been surrendered and such notice received by the Corporation. |

| H11000059959 3 |

10

| H11000059959 3 |

| (f) No fractional shares or scrip representing fractions of Common Stock shall be issued upon conversion of the Series A Preferred. Instead of any fractional interest in a share of Common Stock that would otherwise be deliverable upon the conversion of a share of Series A Preferred, the Corporation shall pay to the holder of such share an amount in cash based upon the Current Market Price of Common Stock on the Trading Day immediately preceding the date of conversion. If more than one share of Series A Preferred shall be surrendered for conversion at one time by the same holder, the number of full shares of Common Stock issuable upon conversion thereof shall be computed on the basis of the aggregate number of shares of Series A Preferred so surrendered.

(g) If the Corporation shall (i) make a payment of dividends or distributions to holders of any class or series of capital stock of the Corporation in Common Stock, (ii) subdivide its outstanding Common Stock into a greater number of shares, (iii) combine its outstanding Common Stock into a smaller number of shares or (iv) issue any shares of capital stock by reclassification of its Common Stock, the Conversion Price shall be adjusted so that the holder of any Series A Preferred thereafter surrendered for conversion shall be entitled to receive the number of shares of Common Stock that such holder would have owned or have been entitled to receive after the happening of any of the events described above had such shares been converted immediately prior to the record date in the case of a dividend or distribution or the effective date in the case of a subdivision, combination or reclassification. An adjustment made pursuant to this paragraph (g) shall become effective immediately after the opening of business on the day next following the record date (except as provided in paragraph (i) of this subsection 8) in the case of a distribution and shall become effective immediately after the opening of business on the day next following the effective date in the case of a subdivision, combination or reclassification. Such adjustment(s) shall be made successively whenever any of the events listed above shall occur.

(h) Whenever the Conversion Price is adjusted as set forth in paragraph (g) of this subsection 8, the Corporation shall promptly file with the transfer agent of the Corporation an officer’s certificate setting forth the Conversion Price after such adjustment. Promptly after delivery of such certificate, the Corporation shall prepare a notice of such adjustment of the Conversion Price, setting forth the adjusted Conversion Price and the effective date on which such adjustment becomes effective and shall mail such notice of such adjustment of the Conversion Price to the holder of each share of Series A Preferred at such holder’s last address as shown on the share records of the Corporation.

(i) In any case in which paragraph (g) of subsection 8 provides that an adjustment shall become effective on the date next following the record date for an event, the Corporation may defer until the occurrence of such event (I) issuing to the holder of any Series A Preferred converted after such record date and before the occurrence of such event the additional Common Stock issuable upon such conversion by reason of the adjustment required by such event over and above the Common Stock issuable upon such conversion before giving effect to such adjustment and (II) fractionalizing any Series A Preferred and/or paying to such holder any amount of cash in lieu of any fraction pursuant to paragraph (f) of this subsection 8. |

| H11000059959 3 |

11

| H11000059959 3 |

| (j) The Corporation covenants that it will at all times reserve and keep available, free from preemptive rights, out of the aggregate of its authorized but unissued Common Stock, for the purpose of effecting conversion of the Series A Preferred, the full number of shares of Common Stock deliverable upon the conversion of all outstanding Series A Preferred not theretofore converted. For purposes of this paragraph (j), the number of shares of Common Stock that shall be deliverable upon the conversion of all outstanding Series A Preferred shall be computed as if at the time of computation all such outstanding shares were held by a single holder.

The Corporation covenants that any Common Stock issued upon conversion of the Series A Preferred shall be validly issued, fully paid and nonassessable. Before taking any action that would cause an adjustment reducing the Conversion Price below the then par value of the Common Stock deliverable upon conversion of the Series A Preferred, the Corporation will take any action that, in the opinion of its counsel, may be necessary in order that the Corporation may validly and legally issue fully paid and nonassessable Common Stock at such adjusted Conversion Price.

(k) The Corporation will pay any and all documentary stamp or similar issue or transfer taxes payable in respect of the issue or delivery of Common Stock or other securities or property on conversion of the Series A Preferred pursuant hereto; provided, however, that the Corporation shall not be required to pay any tax that may be payable in respect of any transfer involved in the issue or delivery of Common Stock or other securities or property in a name other than that of the holder of the Series A Preferred to be converted, and no such issue or delivery shall be made unless and until the person requesting such issue or delivery has paid to the Corporation the amount of any such tax or has established, to the reasonable satisfaction of the Corporation, that such tax has been paid.

(1) In addition to the foregoing adjustments, the Corporation shall be entitled to make such reductions in the Conversion Price, in addition to those required herein, as it in its discretion considers to be advisable in order that any share distributions, subdivisions of shares, reclassification or combination of shares, distribution of rights, options, warrants to purchase shares or securities, or a distribution of other assets (other than cash distributions) will not be taxable or, if that is not possible, to diminish any income taxes that are otherwise payable because of such event

9. Articles of Incorporation and Bylaws.

(a) The rights of all holders of the Series A Preferred and the terms of the Series A Preferred are subject to the provisions of the Articles of Incorporation, as amended, and the Bylaws of the Corporation.

(b) Except as may otherwise be required by law, the Series A Preferred shall not have any voting powers, preferences or relative, participating, optional or other special rights, other than those specifically set forth in the Corporation’s Articles of Incorporation (as such may be amended from time to time). The Series A Preferred shall have no preemptive or subscription rights. |

| H11000059959 3 |

12

| H11000059959 3 |

|

(c) The headings of the various subdivisions hereof are for convenience of reference only and shall not affect the interpretation of any of the provisions hereof.

(d) If any voting powers, preferences or relative, participating, optional and other special rights of the Series A Preferred or qualifications, limitations or restrictions thereof set forth in the Corporation’s Articles of Incorporation (as such may be amended from time to time) is invalid, unlawful or incapable of being enforced by reason of any rule of law or public policy, all other voting powers, preferences and relative, participating, optional and other special rights of Series A Preferred and qualifications, limitations and restrictions thereof set forth in the Corporation’s Articles of Incorporation (as so amended) which can be given effect without the invalid, unlawful or unenforceable voting powers, preferences or relative, participating, optional or other special rights of Series A Preferred or qualifications, limitations and restrictions thereof shall be given such effect. None of the voting powers, preferences or relative participating, optional or other special rights of the Series A Preferred or qualifications, limitations or restrictions thereof herein set forth shall be deemed dependent upon any other such voting powers, preferences or relative, participating, optional or other special right of Series A Preferred or qualifications, limitations or restrictions thereof unless so expressed herein. |

| H11000059959 3 |

13

| H11000059959 3 |

|

IN WITNESS WHEREOF, the undersigned has executed these Articles of Amendment as of March 7, 2011. |

|

||||||

| Andrew L. Graham, | ||||||

| Secretary | ||||||

| H11000059959 3 |

14

| ARTICLES OF AMENDMENT OF HOMEOWNERS CHOICE, INC.

1. Article I of the Articles of Incorporation of HOMEOWNERS CHOICE, INC. is amended in its entirety to read as follows:

“ARTICLE I NAME

The name of the corporation is HCI GROUP, INC.”

* * * * * * *

2. The foregoing amendment was adopted May 22, 2013.

3. The number of votes cast for the amendment by the shareholders was sufficient for approval.

IN WITNESS WHEREOF, the undersigned has executed these Articles of Amendment this 22nd day of May 2013. |

|

|

||||||

| Paresh Patel | ||||||

| As Chairman of the Board and | ||||||

| Chief Executive Officer | ||||||

90%

90%