UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

x | ANNUAL REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2018 | |

or | |

o | TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from________to | |

Commission file number 001-34963

LPL Financial Holdings Inc.

(Exact name of registrant as specified in its charter)

Delaware | 20-3717839 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

75 State Street, Boston, MA 02109

(Address of principal executive offices; including zip code)

800-877-7210

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered |

Common Stock — $0.001 par value per share | Nasdaq Global Select Market |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer x | Accelerated filer o | Non-accelerated filer o | Smaller reporting company o |

Emerging growth company o | |||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

As of June 30, 2018, the aggregate market value of the voting stock held by non-affiliates of the registrant was $5.8 billion. For purposes of this information, the outstanding shares of Common Stock owned by directors and executive officers of the registrant were deemed to be shares of the voting stock held by affiliates.

The number of shares of common stock, par value $0.001 per share, outstanding as of February 19, 2019 was 84,450,439.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive Proxy Statement to be delivered to stockholders in connection with the Annual Meeting of Stockholders are incorporated by reference into Part III.

TABLE OF CONTENTS

Page | ||

i

WHERE YOU CAN FIND MORE INFORMATION

We file annual, quarterly, and current reports, proxy statements, and other information required by the Securities Exchange Act of 1934, as amended (“Exchange Act”), with the Securities and Exchange Commission ("SEC"). Our SEC filings are available to the public from the SEC’s internet site at SEC.gov.

On our internet site, LPL.com, we post the following filings as soon as reasonably practicable after they are electronically filed with or furnished to the SEC: our annual reports on Form 10-K, our proxy statements, our quarterly reports on Form 10-Q, our current reports on Form 8-K, and any amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act. Hard copies of all such filings are available free of charge by request via email (investor.relations@lpl.com), telephone (617) 897-4574, or mail (LPL Financial Investor Relations at 75 State Street, 22nd Floor, Boston, MA 02109). The information contained or incorporated on our website is not a part of this Annual Report on Form 10-K.

When we use the terms “LPLFH,” "LPL," “we,” “us,” “our,” and the “Company,” we mean LPL Financial Holdings Inc., a Delaware corporation, and its consolidated subsidiaries, taken as a whole, unless the context otherwise indicates.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

Statements in Item 7 - “Management's Discussion and Analysis of Financial Condition and Results of Operations” and other sections of this Annual Report on Form 10-K regarding the Company's future financial and operating results, outlook, growth, plans, business strategies, liquidity, future indebtedness, future share repurchases, and future dividends, including statements regarding future resolution of regulatory matters, legal proceedings and related costs, future revenue and expenses, and projected savings and anticipated improvements to the Company's operating model, services, and technologies as a result of its initiatives, programs and/or acquisitions, as well as any other statements that are not related to present facts or current conditions or that are not purely historical, constitute forward-looking statements. These forward-looking statements are based on the Company's historical performance and its plans, estimates, and expectations as of February 26, 2019. The words “anticipates,” “believes,” “expects,” “may,” “plans,” “predicts,” “will,” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words. Forward-looking statements are not guarantees that the future results, plans, intentions, or expectations expressed or implied by the Company will be achieved. Matters subject to forward-looking statements involve known and unknown risks and uncertainties, including economic, legislative, regulatory, competitive, and other factors, which may cause actual financial or operating results, levels of activity, or the timing of events, to be materially different than those expressed or implied by forward-looking statements. Important factors that could cause or contribute to such differences include: changes in general economic and financial market conditions, including retail investor sentiment; changes in interest rates and fees payable by banks participating in the Company's cash sweep programs, including the Company's success in negotiating agreements with current or additional counterparties; the Company's success and strategy in managing cash sweep program fees; fluctuations in the levels of brokerage and advisory assets, including net new assets, and the related impact on revenue; effects of competition in the financial services industry; the success of the Company in attracting and retaining financial advisors and institutions, and their ability to market effectively financial products and services; whether retail investors served by newly-recruited advisors choose to move their respective assets to new accounts at the Company; changes in growth and profitability of the Company’s fee-based business, including the Company's centrally managed advisory platform; the effect of current, pending, and future legislation, regulation, and regulatory actions, including disciplinary actions imposed by federal and state regulators and self-regulatory organizations; the cost of settling and remediating issues related to regulatory matters or legal proceedings, including actual costs of reimbursing customers for losses in excess of our reserves; changes made to the Company's services and pricing, including in response to current, pending, and future legislation, regulation, and regulatory actions, and the effect that such changes may have on the Company's gross profit streams and costs; execution of the Company's capital management plans, including its compliance with the terms of its credit agreement and the indenture governing its senior notes; the price, the availability of shares, and trading volumes of the Company's common stock, which will affect the timing and size of future share repurchases by the Company; execution of the Company's plans and its success in realizing the synergies, expense savings, service improvements or efficiencies expected to result from its initiatives and programs, including its acquisitions of AdvisoryWorld and the broker-dealer network of National Planning Holdings, Inc. and its expense plans and technology initiatives; the performance of third-party service providers to which business processes are transitioned; the Company's ability to control operating risks, information technology systems risks, cybersecurity risks, and sourcing risks; and the other factors set forth in Part I, “Item 1A. Risk Factors.” Except as required by law, the Company specifically disclaims any obligation to update any forward-

ii

looking statements as a result of developments occurring after the date of this Annual Report on Form 10-K, even if its estimates change, and you should not rely on statements contained herein as representing the Company's views as of any date subsequent to the date of this Annual Report on Form 10-K.

iii

PART I

Item 1. Business

General Corporate Overview

We are a leader in the retail financial advice market and the nation's largest independent broker-dealer. We serve independent financial advisors and financial institutions, providing them with the technology, research, clearing and compliance services, and practice management programs they need to create and grow their practices. We enable them to provide objective financial guidance to millions of American families seeking wealth management, retirement planning, financial planning and asset management solutions.

We believe that objective financial guidance is a fundamental need for everyone. We enable our advisors to focus on what they do best—create the personal, long-term relationships that are the foundation for turning life’s aspirations into financial realities. We do that through a singular focus on providing our advisors with the front-, middle-, and back-office support they need to serve the large and growing market for independent investment advice. We believe that we are the only company that offers advisors the unique combination of an integrated technology platform, comprehensive self-clearing services, and open architecture access to a wide range of non-proprietary products, all delivered in an environment unencumbered by conflicts from product manufacturing, underwriting, and market-making.

We believe investors achieve better outcomes when working with a financial advisor. We strive to make it easy for advisors to do what is best for their clients, while protecting advisors and investors and promoting independence and choice through access to a wide range of diligently evaluated non-proprietary products.

We began operations through LPL Financial LLC, our broker-dealer subsidiary (“LPL Financial”), in 1989. LPL Financial Holdings Inc., which is the parent company of our collective businesses, was incorporated in Delaware in 2005. LPL Financial is a clearing broker-dealer and an investment advisor that primarily transacts business as an agent for our advisors on behalf of their clients by providing access to a broad array of financial products and services. Through our subsidiary The Private Trust Company, N.A. (“PTC”), we offer trust administration, investment management oversight, and Individual Retirement Account (“IRA”) custodial services for estates and families. Through our subsidiary AdvisoryWorld, we offer technology products, including proposal generation, investment analytics and portfolio modeling, to both our advisors and external clients in the wealth management industry. Fortigent Holdings Company, Inc. and its subsidiaries (“Fortigent”) provide solutions and consulting services to registered investment advisors, banks, and trust companies serving high-net-worth clients. Our subsidiary, LPL Insurance Associates, Inc. (“LPLIA”), operates as a brokerage general agency that offers life and disability insurance sales and services.

Our Business

Our Advisor Relationships

Our business is dedicated exclusively to our advisors; we are not a market-maker nor do we offer investment banking or underwriting services. We offer no proprietary products of our own. Because we do not offer proprietary products, we enable the independent financial advisors, banks, and credit unions that we support to offer their clients lower-conflict advice.

We work alongside advisors to navigate complex market and regulatory environments and strive to empower them to create the best outcomes for investors. In addition, we make meaningful investments in technology and services to support the growth, productivity, and efficiency of advisors across a broad spectrum of business models as their practices evolve. Our advisors are a community of diverse, entrepreneurial financial services professionals. They build long-term relationships with their clients in communities across the United States by guiding them through the complexities of investment decisions, retirement solutions, financial planning, and wealth management. Our advisors support approximately 5.4 million client accounts. Our services are designed to support the evolution of our advisors’ businesses over time and to adapt as our advisors' needs change.

We believe we offer a compelling economic value proposition to independent advisors, which is a key factor in our ability to attract and retain advisors and their practices. The independent channels pay advisors a greater share of brokerage commissions and advisory fees than the captive channels — generally 80-90% compared to 30-50%. Through our scale and operating efficiencies, we are able to offer our advisors what we believe to be the highest average payout ratios among the five largest United States broker-dealers, ranked by number of advisors.

1

Furthermore, we believe that our technology and service platforms enable our advisors to operate their practices with a greater focus on serving investors while generating revenue opportunities and at a lower cost than other independent advisors. As a result, we believe that our advisors who own practices earn more pre-tax profit than practice owners affiliated with other independent brokerage firms. Finally, as business owners, our independent financial advisors, unlike captive advisors, also have the opportunity to build equity in their own businesses.

Our advisors average over 15 years of industry experience, which generally allows us to focus on supporting and enhancing our advisors’ businesses without needing to provide basic training or subsidizing advisors who are new to the industry. Our flexible business platform allows our advisors to choose the most appropriate business model to support their clients, whether they conduct brokerage business, offer brokerage and fee-based services on our corporate registered investment advisor (“RIA”) platform, or provide fee-based services through their own RIA practices.

The majority of our advisors are entrepreneurial independent contractors who are primarily located in rural and suburban areas and, as such, are viewed as local providers of independent advice. Many of our advisors operate under their own business name, and we may assist these advisors with their own branding, marketing and promotion, and regulatory review.

Advisors licensed with LPL Financial as registered representatives and as investment advisory representatives are able to conduct both commission-based business on our brokerage platform and fee-based business on our corporate RIA platform. In order to be licensed with LPL Financial, advisors must be approved through our assessment process, which includes a review of each advisor’s education, experience, and compliance history, among other factors. Approved advisors become registered with LPL Financial and enter into a representative agreement that establishes the duties and responsibilities of each party. Pursuant to the representative agreement, each advisor makes a series of representations, including that the advisor will disclose to all clients and prospective clients that the advisor is acting as LPL Financial's registered representative or investment advisory representative, that all orders for securities will be placed through LPL Financial, that the advisor will sell only products that LPL Financial has approved, and that the advisor will comply with LPL Financial policies and procedures as well as securities rules and regulations. These advisors also agree not to engage in any outside business activity without prior approval from us and not to act in competition with us.

LPL Financial also supports over 420 independent RIA firms that conduct their business through separate entities ("Hybrid RIAs") with over 5,000 advisors who conduct their advisory business through these separate entities, rather than through LPL Financial. Hybrid RIAs operate pursuant to the Investment Advisers Act of 1940, as amended (the "Advisers Act") or their respective states' investment advisory licensing rules. These Hybrid RIAs engage us for technology, clearing, and custody services, as well as access to our investment platforms. Advisors associated with Hybrid RIAs retain 100% of their advisory fees. In return, we charge separate fees for custody, trading, administrative, and support services. In addition, most financial advisors associated with Hybrid RIAs carry their brokerage license with LPL Financial and access our fully-integrated brokerage platform under standard terms, although some financial advisors associated with Hybrid RIAs do not carry a brokerage license with us.

We believe we are the market leader in providing support to over 2,500 financial advisors at approximately 800 banks and credit unions nationwide. The core capabilities of these institutions may not include investment and financial planning services, or they may find the technology, infrastructure, and regulatory requirements of supporting such services to be cost-prohibitive. For these institutions, we provide their financial advisors with the infrastructure and services they need to be successful, allowing the institutions to focus more attention and capital on their core businesses.

We also provide support to approximately 3,600 additional financial advisors who are affiliated and licensed with insurance companies. These arrangements allow us to provide outsourced customized clearing, advisory platforms, and technology solutions that enable the financial advisors at these insurance companies to offer a breadth of services to their client base in an efficient manner.

Our Value Proposition

The core of our business is dedicated to meeting the evolving needs of our advisors and providing the platform and tools to grow and enhance the profitability of their businesses. We are dedicated to continuously improving the processes, systems, and resources we leverage to meet these needs.

We support our advisors by providing front-, middle-, and back-office solutions through our distinct value proposition: integrated technology solutions, comprehensive clearing and compliance services, consultative practice

2

management programs and training, and independent research. The comprehensive and increasingly automated nature of our offering enables our advisors to focus on their clients while successfully and efficiently managing the complexities of running their own practice.

Integrated Technology Solutions

We provide our technology and service to advisors through an integrated technology platform that is server-based and web-accessible. Our technology offerings are designed to permit our advisors to effectively manage all critical aspects of their businesses in an efficient manner while remaining responsive to their clients’ needs. We continue to automate time-consuming processes, such as account opening and management, document imaging, transaction execution, and account rebalancing, in an effort to improve our advisors' efficiency and accuracy.

Comprehensive Clearing and Compliance Services

We provide custody and clearing services for the majority of our advisors’ transactions, and seek to offer a simplified and streamlined advisor experience and expedited processing capabilities. Our self-clearing platform enables us to control client data, more efficiently process and report trades, facilitate platform development, reduce costs, and ultimately enhance the service experience for our advisors and their clients. Our self-clearing platform also enables us to serve a wide range of advisors, including those associated with Hybrid RIAs.

We continue to make substantial investments in our compliance function to provide our advisors with a strong framework through which to understand and operate within regulatory guidelines, as well as guidelines that we establish. Protecting the best interests of investors and our affiliated advisors is of utmost importance to us. As the financial industry and regulatory environment evolve and become more complex, we remain devoted to serving our advisors ethically and well. We have made a long-term commitment to enhancing our risk management and compliance structure, as well as our technology-based compliance and risk management tools, in order to further enhance the overall effectiveness and scalability of our control environment.

Our team of risk and compliance employees assists our advisors through:

• | training and advising advisors on new products, new regulatory guidelines, compliance and risk management tools, security policies and procedures, and best practices; |

• | advising on sales practice activities and facilitating the supervision of activities by branch managers; |

• | conducting technology-enabled surveillance of trading activities and sales practices; |

• | for advisors on our corporate RIA platform, monitoring of registered investment advisory activities; and |

• | inspecting branch offices and advising on how to strengthen compliance procedures. |

Practice Management Programs and Training

Our practice management programs are designed to help financial advisors in independent practices and financial institutions, as well as all levels of financial institution leadership, enhance and grow their businesses. Our experience gives us the ability to benchmark the best practices of successful advisors and develop customized recommendations to meet the specific needs of an advisor’s business and market, and our scale allows us to dedicate a team of experienced professionals to this effort. Our practice management and training services include:

• | personalized business consulting that helps eligible advisors and program leadership enhance the value and operational efficiency of their businesses; |

• | advisory and brokerage consulting and financial planning to support advisors in growing their businesses through our broad range of products and fee-based offerings, as well as wealth management services, to assist advisors serving high-net-worth clients with comprehensive estate, tax, philanthropic, and financial planning processes; |

• | marketing strategies, including campaign templates, to enable advisors to build awareness of their services and capitalize on opportunities in their local markets; |

• | succession planning and an advisor loan program for advisors looking to either sell their own or buy another practice; |

• | transition services to help advisors establish independent practices and migrate client accounts to us; and |

• | in-person and virtual training and educational programs on topics including technology, use of advisory platforms, and business development. |

3

Independent Research

We provide our advisors with integrated access to comprehensive research on a broad range of investments and market analysis on macro-economic events, capital markets assumptions, and strategic and tactical asset allocation. Our research team provides advice that is designed to empower our advisors to provide their clients with thoughtful advice in a timely manner, including the creation of discretionary portfolios for which we serve as a portfolio manager, available through our turnkey advisory asset management platforms. Our research team actively works with our product risk management group to review the financial products offered through our platform. This includes third-party asset manager search, selection, and monitoring services for both traditional and alternative strategies across all investment access points (exchange-traded funds, mutual funds, separately managed accounts, unified managed accounts, and other products and services). We believe our lack of proprietary products or investment banking services better enables us to provide research that is unbiased and objective.

Our Product and Solution Access

We do not manufacture any financial products. Instead, we provide our advisors with open architecture access to a broad range of commission, fee-based, cash, and money market products and services. Our product risk management group conducts a review on substantially all of our product offerings.

The sales and administration of these products are facilitated through our technology solutions that allow our advisors to access client accounts, product information, asset allocation models, investment recommendations, and economic insight as well as to perform trade execution.

Commission-Based Products

Commission-based products are those for which we and our advisors receive an upfront commission and, for certain products, a trailing commission, or a mark-up or mark-down. Our brokerage offerings include variable and fixed annuities, mutual funds, equities, alternative investments such as non-traded real estate investment trusts and business development companies, retirement and 529 education savings plans, fixed income, and insurance. As of December 31, 2018, the total brokerage assets in our commission-based products were $346.0 billion. We regularly review the structure and fees of our commission-based products in the context of retail investor preferences and the changing regulatory environment.

Fee-Based Advisory Platforms and Support

LPL Financial has various fee-based advisory platforms that provide centrally managed or customized solutions from which advisors can choose to meet the investment needs of their clients, including wrap-fee programs, mutual fund asset allocation programs, an advisor-enhanced digital advice program, advisory programs offered by third-party investment advisor firms, financial planning services, and retirement plan consulting services. The fee structure of our platforms enables our advisors to provide their clients with higher levels of service, while establishing a recurring revenue stream for the advisor and for us. Our fee-based platforms provide access to mutual funds, exchange-traded funds, stocks, bonds, certain option strategies, unit investment trusts, and institutional money managers and no-load multi-manager variable annuities. As of December 31, 2018, the total advisory assets under custody in these platforms, through both our corporate RIA platform and Hybrid RIAs, were $282.0 billion.

Cash Sweep Programs

We assist our advisors in managing their clients’ cash balances through three primary cash sweep programs: a money market sweep vehicle involving money market fund providers and two insured sweep vehicles involving banks. As of December 31, 2018, the total assets in our cash sweep programs, which are held within brokerage and advisory accounts, were approximately $34.9 billion. The balance in insured cash account vehicles was $24.8 billion, deposit cash account vehicles was $5.1 billion and money market vehicles was $4.9 billion.

Other Services

We provide a number of tools and services that enable advisors to maintain and grow their practices. Through our subsidiary PTC, we provide custodial services to trusts for estates and families. Under our unique model, an advisor may provide a trust with investment management services, while administrative services for the trust are provided by PTC. We also offer retirement solutions for commission- and fee-based services that allow advisors to provide brokerage services, consultation, and advice to retirement plan sponsors using LPL Financial. Finally, we offer proposal generation, investment analytics and portfolio modeling capabilities to both our advisors and external clients in the wealth management industry through our subsidiary AdvisoryWorld.

4

Our Financial Model

Our overall financial performance is a function of the following dynamics of our business:

• | Our revenues stem from diverse sources, including advisor-generated commission and advisory fees, as well as other asset-based fees from product manufacturers, omnibus, networking services, cash sweep balances, and transaction and other fees for other ancillary services that we provide. Revenues are not concentrated by advisor, product, or geography. For the year ended December 31, 2018, no single relationship with our independent advisor practices, banks, credit unions, or insurance companies accounted for more than 7% of our net revenues, and no single advisor accounted for more than 2% of our net revenues. |

• | The largest variable component of our cost base, advisor payout percentages, is directly linked to revenues generated by our advisors. |

• | A portion of our revenues, such as software licensing and account and client fees, are not correlated with the equity financial markets. |

• | Our operating model is scalable and is capable of delivering expanding profit margins over time. |

• | We have been able to operate with low capital expenditures and limited capital requirements, and as a result have been able to invest in our business as well as return value to shareholders. |

Our Competitive Strengths

Market Leadership Position and Significant Scale

We are the established leader in the independent advisor market, which is our core business focus. We use our scale and position as an industry leader to champion the independent business model and the rights of our advisors.

Our scale enables us to benefit from the following dynamics:

• | Continual Reinvestment — We actively reinvest in our comprehensive technology platform and practice management support, which further improves the productivity of our advisors. |

• | Economies of Scale — As one of the largest distributors of financial products in the United States, we have been able to obtain attractive economics from product manufacturers. |

• | Payout Ratios to Advisors — Among the largest United States broker-dealers by number of advisors, we believe that we offer the highest average payout ratios to our advisors. |

The combination of our ability to reinvest in our business and maintain highly competitive payout ratios has enabled us to attract and retain advisors. This, in turn, has driven our growth and led to a continuous cycle of reinvestment that reinforces our established scale advantage.

Comprehensive Solutions

Our differentiator is the combination of our capabilities across research, technology, risk management, and practice management. LPL makes meaningful investments to support the growth, productivity, and efficiency of advisors across a broad spectrum of models as their practices evolve. Our focus is working alongside advisors to navigate complex environments in order to create the best outcomes for their clients.

We believe we offer a compelling value proposition to independent financial advisors and financial institutions. This value proposition is built upon the delivery of our services through our scale, independence, and integrated technology, the sum of which we believe is not replicated in the industry. As a result we believe that we do not have any direct competitors that offer our business model at the scale at which we offer it. For example, because we do not have any proprietary manufactured financial products, we do not view firms that manufacture asset management products and other financial products as direct competitors.

We provide comprehensive solutions to financial institutions, such as regional banks, credit unions, and insurers that seek to provide a broad array of services for their clients. We believe many institutions find the technology, infrastructure, and regulatory requirements associated with delivering financial advice to be cost-prohibitive. The solutions we provide enable financial advisors at these institutions to deliver their services on a cost-effective basis.

5

Flexibility of Our Business Model

Our business model allows our advisors the freedom to choose how they conduct their business, subject to certain regulatory parameters, which has helped us attract and retain advisors from multiple channels, including wire houses, regional broker-dealers, and other independent broker-dealers. Our platform can accommodate a variety of independent advisor business models, including independent financial advisors and Hybrid RIAs. The flexibility of our business model enables our advisors to transition among the independent advisor business models and product mix as their business evolves and preferences change within the market or their client base. Our business model provides advisors with a multitude of customizable service and technology offerings that allow them to increase their efficiency, focus on their clients, and grow their practice.

Our Sources of Growth

We believe we can increase our revenue and profitability by benefiting from favorable industry trends and by executing strategies to accelerate our growth beyond that of the broader markets in which we operate.

Favorable Industry Trends

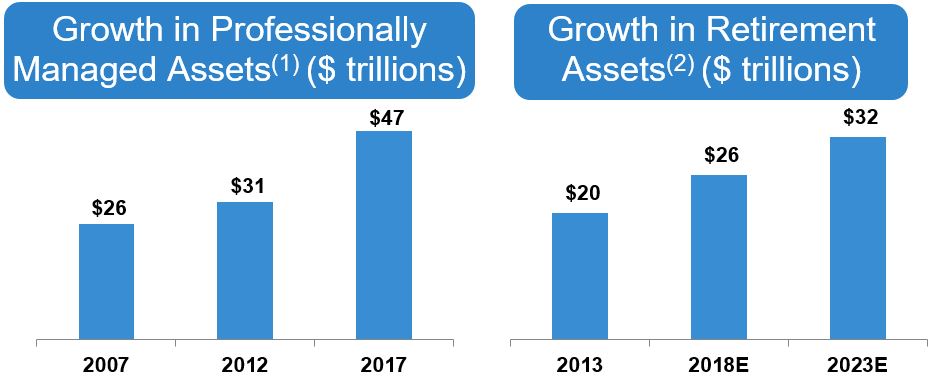

Growth in Investable Assets

Over the past five years assets serviced in the market segments in the United States that we address grew 9.9% per year, while retirement assets are expected to grow 4.7% per year over the next five years (in part due to the retirement of the baby boomer generation and the resulting assets that are projected to flow out of retirement plans and into IRAs). In addition, IRA assets are projected to grow from $9.8 trillion as of 2018 to $12.6 trillion by 2022.

____________________

(1) | The Cerulli Report: The State of U.S. Retail and Institutional Asset Management 2018. |

(2) | The Cerulli Report: U.S. Retirement Markets 2018. |

Increasing Demand for Independent Financial Advice

Retail investors, particularly in the mass-affluent market, are increasingly seeking financial advice from independent sources. We are highly focused on helping independent advisors meet the needs of the mass-affluent market, which constitutes a significant and underserved portion of investable assets.

Advisor Migration to Independent Channels

Independent channels continue to gain market share from captive channels. We believe that we are not just a beneficiary of this secular shift, but an active catalyst in the movement to independence. There is an increased shift towards advisors seeking complete independence by forming an RIA firm and registering directly with the SEC or state securities regulators. This shift has led to significant growth in the number of advisors associated with Hybrid RIAs and independent RIA firms.

6

Macroeconomic Trends

Our business has benefited from recent interest rate increases, and we expect that it will benefit from growth in advisory and brokerage assets as well as any additional increase in interest rates.

Executing Our Growth Strategies

Increasing Productivity of Existing Advisor Base

We believe the productivity of our advisors has the potential to increase over time as we continue to develop solutions designed to enable them to add new clients, manage more of their clients’ investable assets, and expand their existing practices with additional advisors. We expect to facilitate these productivity improvements by helping our advisors better manage their practices in an increasingly complex external environment, which we believe has the potential to result in the assets per advisor growing over time.

Attracting New Advisors to Our Platform

We intend to grow the number of advisors who are served by our platform — either those who are independent or who are aligned with financial institutions. Cerulli Associates estimates there are 311,927 financial advisors in the United States, of which we have a 5.2% market share, and we believe we are uniquely positioned to attract seasoned advisors of any practice size and from any of the channels listed below.

Channel | Advisors | % of Market | ||

Independent Broker-Dealer(1) | 60,564 | 19.4% | ||

Insurance Broker-Dealer | 75,863 | 24.3% | ||

Wire House | 46,402 | 14.9% | ||

National and Regional Broker-Dealer | 40,896 | 13.1% | ||

Independent RIA(1) | 36,852 | 11.8% | ||

Retail Bank Broker-Dealer | 23,373 | 7.5% | ||

Hybrid RIAs(1) | 27,977 | 9.0% | ||

Total | 311,927 | 100.0% | ||

____________________

(1) | The 27,977 advisors classified as "Hybrid RIAs" are advisors who are both licensed through independent broker-dealers and registered as investment advisors. The Hybrid RIAs are excluded from the Independent Broker-Dealer and Independent RIA categories in the table above. |

Competition

We compete with a variety of financial firms to attract and retain experienced and productive advisors:

•Within the independent broker-dealer channel, the industry is highly fragmented and comprised primarily of regional firms that rely on third-party custodians and technology providers to support their operations. Some of the competitors in this space include:

◦Commonwealth Financial Network

◦Cetera Financial Group

◦Cambridge

•The captive wire house channel tends to consist of large nationwide firms with multiple lines of business that have a focus on the highly competitive high-net-worth investor market. Competitors in this channel include:

◦Morgan Stanley

◦Bank of America Merrill Lynch

◦UBS Financial Services Inc.

◦Wells Fargo Advisors, LLC

•Competition for advisors also includes regional firms, such as Edward D. Jones & Co., L.P., Ameriprise Financial Services Inc. and Raymond James Financial Services, Inc.

•Independent RIA firms, which are registered with the SEC or through their respective states' investment advisory regulator and not through a broker-dealer, may choose from a number of third-party firms to provide custodial services. Our significant competitors in this space include:

7

◦Charles Schwab & Co.

◦Fidelity Brokerage Services LLC

◦TD Ameritrade

Those competitors that do not offer a complete clearing solution for advisors are frequently supported by third-party clearing and custody oriented firms. Pershing LLC, a subsidiary of Bank of New York Mellon; National Financial Services LLC, a subsidiary of Fidelity Investments; and J.P. Morgan Clearing Corp., a subsidiary of J.P. Morgan Chase & Co., offer custodial services and technology solutions to independent firms and RIAs that are not self-clearing. These clearing firms and their affiliates and other providers also offer an array of service, technology and reporting tools. Albridge Solutions, a subsidiary of Bank of New York Mellon, Advent Software, Inc., Envestnet, Inc., and Morningstar, Inc., provide an array of research, analytics, and reporting solutions.

Our advisors compete for clients with financial advisors of brokerage firms, banks, insurance companies, asset management, and investment advisory firms. In addition, they also compete with a number of firms offering direct-to-investor online financial services and discount brokerage services, such as Charles Schwab & Co, E*TRADE, and Fidelity Brokerage Services LLC.

Employees

As of December 31, 2018, we had 4,229 full-time employees. None of our employees are subject to collective bargaining agreements governing their employment with us. We build deep expertise by attracting talented employees from a variety of fields and developing that talent into future leaders of our business and our industry. Our continued growth is dependent, in part, on our ability to be an employer of choice and an organization that recruits and retains talented employees who best fit our culture and business needs. We offer ongoing learning opportunities and programs that empower employees to grow in their professional development and careers. We provide comprehensive compensation and benefits packages, as well as financial education tools to assist our employees as they plan for their future.

Regulation

The financial services industry is subject to extensive regulation by United States federal, state, and international government agencies as well as various self-regulatory organizations. We take an active leadership role in the development of the rules and regulations that govern our industry. We have been investing in our compliance functions to monitor our adherence to the numerous legal and regulatory requirements applicable to our business. Compliance with all applicable laws and regulations, only some of which are described below, involves a significant investment in time and resources. Any new laws or regulations applicable to our business, any changes to existing laws or regulations, or any changes to the interpretations or enforcement of those laws or regulations, may affect our operations and/or financial condition.

Broker-Dealer Regulation

LPL Financial is a broker-dealer registered with the SEC, a member of the Financial Industry Regulatory Authority ("FINRA") and various other self-regulatory organizations, and a participant in various clearing organizations including the Depository Trust Company, the National Securities Clearing Corporation, and the Options Clearing Corporation. LPL Financial is registered as a broker-dealer in each of the 50 states, the District of Columbia, Puerto Rico, and the U.S. Virgin Islands. The rules of the Municipal Securities Rulemaking Board, which are enforced by the SEC and FINRA, apply to the municipal securities activities of LPL Financial.

Broker-dealers are subject to rules and regulations covering all aspects of the securities business, including sales and trading practices, public offerings, publication of research reports, use and safekeeping of clients’ funds and securities, capital adequacy, recordkeeping and reporting, the conduct of directors, officers, and employees, qualification and licensing of supervisory and sales personnel, marketing practices, supervisory and organizational procedures intended to ensure compliance with securities laws and to prevent improper trading on material nonpublic information, limitations on extensions of credit in securities transactions, clearance and settlement procedures, and rules designed to promote high standards of commercial honor and just and equitable principles of trade. Broker-dealers are also subject to state securities laws and regulated by state securities administrators in those jurisdictions where they do business. Applicable laws, rules and regulations may be subject to varying interpretations and change from time to time.

Regulators make periodic examinations and inquiries of us, and review annual, monthly, and other reports on our operations, track record, and financial condition. Regulatory actions brought against us alleging violations of applicable laws, rules and regulations could result in censures, penalties and fines, settlements, disgorgement of

8

profits, restitution to customers, remediation, or the issuance of cease-and-desist orders. Such actions could also result in the restriction, suspension, or expulsion from the securities industry of us or our financial advisors, officers or employees. We also may incur substantial expenses, damage to our reputation, or similar adverse consequences in connection with any such actions by the SEC, FINRA, the U.S. Department of Labor ("DOL") or state securities regulators, regardless of the outcome.

LPL Financial's margin lending is regulated by the Federal Reserve Board’s restrictions on lending in connection with client purchases and short sales of securities, and FINRA rules also require LPL Financial to impose maintenance requirements based on the value of securities contained in margin accounts. In many cases, our margin policies are more stringent than these rules.

Significant new rules and regulations continue to arise as a result of the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”), which was enacted in July 2010. Provisions of the Dodd-Frank Act that have not been implemented, but may affect our business in the future include, but are not limited to, the potential implementation of a more stringent fiduciary standard for broker-dealers and the potential establishment of a new self-regulatory organization (“SRO”) for investment advisors. Compliance with these provisions could require us to review our product and service offerings for potential changes and would likely result in increased compliance costs. Moreover, to the extent the Dodd-Frank Act affects the operations, financial condition, liquidity, and capital requirements of financial institutions with which we do business, those institutions may seek to pass on increased costs, reduce their capacity to transact, or otherwise present inefficiencies in their interactions with us. The ultimate impact that the Dodd-Frank Act or other new rules or regulations will have on us, the financial industry, and the economy cannot be known until all applicable regulations called for under the Dodd-Frank Act have been finalized and implemented.

Investment Advisor Regulation

As investment advisors registered with the SEC, our subsidiaries LPL Financial and Fortigent, LLC are subject to the requirements of the Advisers Act, and the regulations promulgated thereunder, including examination by the SEC’s staff. Such requirements relate to, among other things, fiduciary duties to clients, performance fees, maintaining an effective compliance program, solicitation arrangements, conflicts of interest, advertising, limitations on agency cross and principal transactions between the advisor and advisory clients, recordkeeping and reporting requirements, disclosure requirements, and general anti-fraud provisions.

The SEC is authorized to institute proceedings and impose sanctions for violations of the Advisers Act and associated regulations. Investment advisors also are subject to certain state securities laws and regulations. Failure to comply with the Advisers Act or other federal and state securities laws and regulations could result in investigations, censures, penalties and fines, settlements, disgorgement of profits, restitution to customers, remediation, the issuance of cease-and-desist orders or the termination of an investment advisor’s registration. We also may incur substantial expenses, damage to our reputation, or similar adverse consequences in connection with such actions, regardless of the outcome.

Retirement Plan Services Regulation

Certain subsidiaries, including LPL Financial, PTC, and LPLIA, are subject to the Employee Retirement Income Security Act of 1974, as amended ("ERISA") and Section 4975 of the Internal Revenue Code of 1986, as amended (the "Code"), and to regulations promulgated under ERISA or the Code, insofar as the subsidiaries provide services with respect to plan clients, or otherwise deal with plan clients that are subject to ERISA or the Code. ERISA imposes certain duties on persons who are "fiduciaries" (as defined in Section 3(21) of ERISA) and prohibits certain transactions involving plans subject to ERISA and fiduciaries or other service providers to such plans. Non-compliance with or breaches of these provisions may expose an ERISA fiduciary or other service provider to liability under ERISA, which may include monetary and criminal penalties as well as equitable remedies for the affected plan. Section 4975 of the Code prohibits certain transactions involving "plans" (as defined in Section 4975(e)(1), which include, for example, IRAs and certain Keogh plans) and service providers, including fiduciaries (as defined in Section 4975(e)(3)), to such plans. Section 4975 imposes excise taxes for violations of these prohibitions.

These regulations were significantly broadened and became more onerous under the DOL rule on conflicts of interest (Definition of the Term "Fiduciary", Conflicts of Interest Rule-Retirement Investment Advice (“DOL Rule”)), which became applicable in June 2017. The DOL Rule was retroactively invalidated in June 2018, however, as a result of a mandate issued by the U.S. Court of Appeals for the Fifth Circuit. Although the DOL Rule no longer applies, we expect the DOL will remain engaged in its regulation of accounts subject to ERISA and the Code, including continued focus on enforcement with respect to ERISA plans and the possibility of future rulemaking. The

9

DOL’s actions could result in legal, compliance, information technology, and other costs and could lead to a greater risk of client lawsuits and enforcement activity by the DOL. The effect of DOL regulation on our retirement plan business cannot now be anticipated or planned for, but may have further impacts on our products and services, and results of operations.

Commodities and Futures Regulation

LPL Financial is registered as an introducing broker with the Commodity Futures Trading Commission (“CFTC”) and is a member of the National Futures Association (“NFA”). LPL Financial introduces commodities and futures products to ADM Investor Services, Inc. (“ADM”), and all commodities accounts and related client positions are held by ADM. LPL Financial is regulated by the CFTC and the NFA. Violations of the rules of the CFTC and the NFA could result in remedial actions including fines, registration terminations, or revocations of exchange memberships.

Trust Regulation

Through our subsidiary, PTC, we offer trust, investment management oversight, and custodial services for estates and families. PTC is chartered as a non-depository national banking association. As a limited purpose national bank, PTC is regulated and regularly examined by the Office of the Comptroller of the Currency (“OCC”). PTC files reports with the OCC within 30 days after the conclusion of each calendar quarter. Because the powers of PTC are limited to providing fiduciary services and investment advice, it does not have the power or authority to accept deposits or make loans. For this reason, trust assets under PTC’s management are not insured by the FDIC.

Because of its limited purpose, PTC is not a “bank” as defined under the Bank Holding Company Act of 1956. Consequently, neither its immediate parent, PTC Holdings, Inc., nor its ultimate parent, LPLFH, is regulated by the Board of Governors of the Federal Reserve System as a bank holding company. However, PTC is subject to regulation by the OCC and to various laws and regulations enforced by the OCC, such as capital adequacy, change of control restrictions and regulations governing fiduciary duties, conflicts of interest, self-dealing, and anti-money laundering. For example, the Change in Bank Control Act of 1978, as implemented by OCC supervisory policy, imposes restrictions on parties who wish to acquire a controlling interest in a limited purpose national bank such as PTC or the holding company of a limited purpose national bank such as LPLFH. In general, an acquisition of 10% or more of our common stock, or another acquisition of “control” as defined in OCC regulations, may require OCC approval. These laws and regulations are designed to serve specific bank regulatory and supervisory purposes and are not meant for the protection of PTC, PTC Holdings, Inc., LPLFH, or their stockholders.

Regulatory Capital Requirements

The SEC, FINRA, the CFTC, and the NFA have stringent rules and regulations with respect to the maintenance of specific levels of net capital by regulated entities. Generally, a broker-dealer’s net capital is calculated as net worth plus qualified subordinated debt less deductions for certain types of assets. The net capital rule under the Exchange Act requires a broker-dealer to maintain a minimum net capital, and applies certain discounts to the value of its assets based on the liquidity of such assets. LPL Financial is also subject to the NFA's financial requirements and is required to maintain net capital that is in excess of or equal to the greatest of the NFA's minimum financial requirements. Under these requirements, LPL Financial is currently required to maintain minimum net capital that is in excess of or equal to the minimum net capital calculated and required pursuant to the SEC's Net Capital Rule.

The SEC, FINRA, the CFTC, and the NFA impose rules that require notification when net capital falls below certain predefined criteria. These broker-dealer capital rules also dictate the ratio of debt to equity in regulatory capital composition and constrain the ability of a broker-dealer to expand its business under certain circumstances. If a broker-dealer fails to maintain the required net capital, then certain notice requirements to the regulators are required and the broker-dealer may be subject to suspension or revocation of registration by the applicable regulatory agency, and suspension or expulsion by these regulators ultimately could lead to the broker-dealer’s liquidation. Additionally, the net capital rule and certain FINRA rules impose requirements that may have the effect of prohibiting a broker-dealer from distributing or withdrawing capital, and require prior notice to the SEC and FINRA for certain capital withdrawals. LPL Financial, which is subject to net capital rules, has been and currently is in compliance with those rules and has net capital in excess of the minimum requirements.

Anti-Money Laundering and Sanctions Compliance

The USA PATRIOT Act of 2001 (the “PATRIOT Act”), which amended the Bank Secrecy Act, contains anti-money laundering and financial transparency laws and mandates the implementation of various regulations

10

applicable to broker-dealers, futures commission merchants, and other financial services companies. Financial institutions subject to these requirements generally must have an anti-money laundering program in place, which includes monitoring for and reporting suspicious activity, implementing specialized employee training programs, designating an anti-money laundering compliance officer, and annually conducting an independent test of the effectiveness of its program. In addition, sanctions administered by the United States Office of Foreign Asset Control prohibit United States persons from doing business with blocked persons and entities or certain sanctioned countries. We have established policies, procedures, and systems designed to comply with these regulations but

we work continuously to improve and strengthen our regulatory compliance mechanisms.

Security and Privacy

Regulatory activity in the areas of privacy and data protection continues to grow worldwide and is generally being driven by the growth of technology and related concerns about the rapid and widespread dissemination and use of information. To the extent they are applicable to us, we must comply with federal and state information-related laws and regulations in the United States, including the Gramm-Leach-Bliley Act of 1999, SEC Regulation S-P, the Fair Credit Reporting Act of 1970, as amended, and Regulation S-ID, as well as the California Consumer Protection Act and further potential federal and state requirements.

Financial Information about Geographic Areas

Our revenues for the periods presented were derived from our operations in the United States.

Trademarks

Access Overlay®, BranchNet®, CLIENTWORKS®, Fortigent®, LPL®, LPL Career Match®, LPL Financial (& Design)®, Manager Access Network®, Manager Access Select®, OMP®, and SPONSORWORKS® are our registered trademarks, and ADVISORYWORLD, CLIENTWORKS CONNECTED and THE PRIVATE TRUST COMPANY, N.A. (& Design) are among our service marks.

11

Item 1A. Risk Factors

Risks Related to Our Business and Industry

We depend on our ability to attract and retain experienced and productive advisors.

We derive a large portion of our revenues from commissions and fees generated by our advisors. Our ability to attract and retain experienced and productive advisors has contributed significantly to our growth and success, and our strategic plan is premised upon continued growth in the number of our advisors and the assets they serve. If we fail to attract new advisors or to retain and motivate our current advisors, replace our advisors who retire, or assist our retiring advisors with transitioning their practices to existing advisors, or if advisor migration away from wire houses and to independent channels decreases or slows, our business may suffer.

The market for experienced and productive advisors is highly competitive, and we devote significant resources to attracting and retaining the most qualified advisors. In attracting and retaining advisors, we compete directly with a variety of financial institutions such as wire houses, regional broker-dealers, banks, insurance companies, and other independent broker-dealers. If we are not successful in retaining highly qualified advisors, we may not be able to recover the expense involved in attracting and training these individuals. There can be no assurance that we will be successful in our efforts to attract and retain the advisors needed to achieve our growth objectives.

In 2017, certain wire houses announced their withdrawal as signatories to an industry broker recruiting protocol, compliance with which protects financial advisors who move from one brokerage firm to another from risk of legal action from their prior brokerage firm. As firms withdraw from the protocol, we could become engaged in more litigation related to our recruiting of advisors from firms which are not signatories to the protocol. In addition, financial advisors from such firms may be more reluctant to consider joining us and, if they do, they may be less successful in transitioning their clients’ assets to our platforms than financial advisors who join us from firms that are signatories to the protocol. As a result, developments with regard to the protocol could negatively impact our recruiting results or could lead to increased litigation.

Our financial condition and results of operations may be adversely affected by market fluctuations and other economic factors.

Significant downturns and volatility in equity and other financial markets have had and could continue to have an adverse effect on our financial condition and results of operations.

General economic and market factors can affect our commission and fee revenue. For example, a decrease in market levels or market volatility can:

• | reduce new investments by both new and existing clients in financial products that are linked to the equity markets, such as variable life insurance, variable annuities, mutual funds, and managed accounts; |

• | reduce trading activity, thereby affecting our brokerage commissions and our transaction revenue; |

• | reduce the value of advisory and brokerage assets, thereby reducing advisory fee revenue, trailing commissions and asset-based fee income; and |

• | motivate clients to withdraw funds from their accounts, reducing advisory and brokerage assets, advisory fee revenue, and asset-based fee income. |

Other more specific trends may also affect our financial condition and results of operations, including, for example: changes in the mix of products preferred by investors may result in increases or decreases in our fee revenues associated with such products, depending on whether investors gravitate towards or away from such products. The timing of such trends, if any, and their potential impact on our financial condition and results of operations are beyond our control.

In addition, because certain of our expenses are fixed, our ability to reduce them in response to market factors over short periods of time is limited, which could negatively impact our profitability.

Significant interest rate changes could affect our profitability and financial condition.

Our revenues are exposed to interest rate risk primarily from changes in fees payable to us from banks participating in our cash sweep programs, which are generally based on prevailing interest rates. Our revenue from our cash sweep programs has declined in the past as a result of a low interest rate environment, and our revenue may decline in the future due to decreases in interest rates, decreases in cash sweep balances or mix shifts among the current or future cash sweep and money market vehicles that we offer. Although the Federal Reserve has

12

incrementally raised the federal funds rate in recent years, there can be no assurance that it will continue to do so, and a reversal of this trend would adversely affect our results. Our revenue from our cash sweep programs also depends on our success in negotiating favorable terms in current and future agreements with banks and money market fund providers participating in our programs, as well as our success in offering competitive products, program fees and interest rates payable to clients. The expiration of contracts with favorable pricing terms, less favorable terms in future contracts with participants in our cash sweep programs or changes in the cash sweep or money market vehicles that we offer, could result in declines in our revenue. A sustained low interest rate environment may also have a negative impact upon our ability to negotiate contracts with new banks or renegotiate existing contracts on comparable terms with banks participating in our cash sweep programs. If interest rates do not rise in accordance with management and market expectations, or if balances or yields in our cash sweep programs decrease, future revenues from our cash sweep programs may be lower than expected.

Any damage to our reputation could harm our business and lead to a loss of revenues and net income.

We have spent many years developing our reputation for integrity and client service, which is built upon our support for our advisors through: enabling technology, comprehensive clearing and compliance services, practice management programs and training, and independent research. Our ability to attract and retain advisors and employees is highly dependent upon external perceptions of our level of service, business practices, and financial condition. Damage to our reputation could cause significant harm to our business and prospects and may arise from numerous sources, including:

• | litigation or regulatory actions; |

• | failing to deliver acceptable standards of service and quality; |

• | compliance failures; and |

• | unethical behavior and the misconduct of employees, advisors, or counterparties. |

Negative perceptions or publicity regarding these matters could damage our reputation among existing and potential advisors and employees, and could lead advisors to terminate their agreements with us, which they generally have the right to do unilaterally upon short notice. Adverse developments with respect to our industry may also, by association, negatively impact our reputation or result in greater regulatory or legislative scrutiny or litigation against us. These occurrences could lead to loss of revenue and net income.

Our business is subject to risks related to litigation, arbitration claims, and regulatory actions.

From time to time, we have been subjected to and are currently subject to legal and regulatory proceedings arising out of our business operations, including lawsuits, arbitration claims, governmental subpoenas, and regulatory, governmental and SRO inquiries, investigations, and enforcement proceedings, as well as other actions and claims. Many of our legal claims are initiated by clients of our advisors and involve the purchase or sale of investment securities, but other claims and proceedings may be, and have been, initiated by state-level and federal regulatory authorities and SROs, including the SEC, FINRA, and state securities regulators.

The outcomes of any such legal or regulatory proceedings, including inquiries, investigations and enforcement proceedings by the SEC, FINRA, DOL and state securities regulators, are difficult to predict. A negative outcome in such a matter could result in substantial legal liability, censures, penalties and fines, disgorgement of profits, restitution to customers, remediation, the issuance of cease-and-desist orders, or injunctive or other equitable relief against us. Further, such negative outcomes individually or in the aggregate may cause us significant reputational harm and could have a material adverse effect on our ability to recruit or retain financial advisors, or our results of operations, cash flows, or financial condition.

We may face liabilities for deficiencies or failures in our compliance systems and programs, as well as actual or alleged breaches of legal duties to our advisors' clients, including in respect of issues related to the suitability of the financial products we make available in our open architecture product platform or the investment advice of our advisors based on their clients' investment objectives (including, for example, alternative investments or exchange-traded funds) and certain fiduciary obligations for advice and recommendations made to our advisory clients.

Moreover, new and developing state and federal regulatory requirements with respect to standards of care and other obligations, as discussed under "Risks Related to Our Regulatory Environment" below, may introduce new grounds for legal claims or enforcement actions against us in the future, including, in particular with respect to our brokerage services. We may also become subject to claims, allegations and legal proceedings that we infringe or misappropriate intellectual property or other proprietary rights of others. In addition, we may be subject to legal proceedings related to employment matters, including wage and hour, discrimination or harassment claims.

13

There are risks inherent in the independent broker-dealer business model.

Compared to wire houses and other employee model broker-dealers, we generally offer advisors wider choice in operating their businesses with regard to product offerings, outside business activities, office technology and supervisory model. Our approach may make it more challenging for us to comply with our supervisory and regulatory compliance obligations, particularly in light of our limited on-site supervision and the complexity of certain advisor business models.

Misconduct and errors by our employees and our advisors could be difficult for us to detect and could result in violations of law by us, regulatory sanctions, or serious reputational or financial harm. Although we have designed policies and procedures to comply with applicable laws, rules, regulations and interpretations, we cannot always prevent misconduct and errors by our employees and our advisors, and the precautions we take to prevent and detect these activities may not be effective in all cases. Prevention and detection among our advisors, who are typically not our direct employees and some of whom tend to be located in small, decentralized offices, present additional challenges, particularly in the case of complex products or supervision of outside business activities. In addition, although we provide our advisors with requirements and recommendations for their office technology, we cannot fully control or monitor the extent of their implementation of our requirements and recommendations. Accordingly, we cannot assure that our advisors’ technology meets our standards, including with regard to information security and cybersecurity. We also cannot assure that misconduct or errors by our employees or advisors will not lead to a material adverse effect on our business, or that our errors and omissions insurance will be sufficient to cover such misconduct or errors.

Our insurance coverage may be inadequate or expensive.

We are subject to claims in the ordinary course of business. These claims may involve substantial amounts of money and involve significant defense costs. It is not always possible to prevent or detect activities giving rise to claims, and the precautions we take may not be effective in all cases.

We maintain voluntary and required insurance coverage, including, among others, general liability, property, director and officer, excess-SIPC, business interruption, cyber and data breach, errors and omissions, and fidelity bond insurance. We have self-insurance for certain potential liabilities through a wholly-owned captive insurance subsidiary. While we endeavor to self-insure and purchase coverage that is appropriate to our assessment of our risk, we are unable to predict with certainty the frequency, nature, or magnitude of claims for direct or consequential damages. Assessing the probability of a loss occurring and the timing and amount of any loss related to a regulatory matter or a legal proceeding is inherently difficult, and there are particular uncertainties and complexities involved when assessing the adequacy of loss reserves for potential liabilities that are self-insured by our captive insurance subsidiary. In addition, certain types of potential claims for damages cannot be insured. Our business may be negatively affected if in the future some or all of our insurance proves to be inadequate or unavailable to cover our liabilities related to legal or regulatory matters. Such negative consequences could include additional expense and financial loss, which could be significant in amount. In addition, insurance claims may harm our reputation or divert management resources away from operating our business.

Our risk management policies and procedures may not be fully effective in mitigating our risk exposure in all market environments or against all types of risks.

We have adopted policies and procedures to identify, monitor and manage our operational risk. These policies and procedures, however, may not be effective and may not be adapted quickly enough to respond effectively to changed circumstances. Some of our compliance and risk evaluation functions depend upon information provided by others and public information regarding markets, clients, or other matters that are otherwise accessible by us. In some cases, however, that information may not be available, accurate, complete, or up-to-date. Also, because our advisors work in decentralized offices, additional risk management challenges may exist, including with regard to advisor office technology and information security practices. In addition, our existing policies and procedures and staffing levels may be insufficient to support a significant increase in our advisor population; such an increase may require us to increase our costs in order to maintain our compliance and risk management obligations or put a strain on our existing policies and procedures as we evolve to support a larger advisor population. If our policies and procedures are not effective or if we are not successful in capturing risks to which we are or may be exposed, we may suffer harm to our reputation or be subject to litigation or regulatory actions that could have a material adverse effect on our business and financial condition.

14

The securities settlement process exposes us to risks that may expose our advisors and us to adverse movements in price.

LPL Financial provides clearing services and trade processing for our advisors and their clients and certain financial institutions. Broker-dealers that clear their own trades are subject to substantially more regulatory requirements than brokers that outsource these functions to third-party providers. Errors in performing clearing functions, including clerical, technological, and other errors related to the handling of funds and securities held by us on behalf of our advisors' clients, could lead to censures, fines, or other sanctions imposed by applicable regulatory authorities as well as losses and liability in related lawsuits and proceedings brought by our advisors’ clients and others. Any unsettled securities transactions or wrongly executed transactions may expose our advisors and us to losses resulting from adverse movements in the prices of such securities.

Lack of liquidity or access to capital could impair our business and financial condition.

Liquidity, or ready access to funds, is essential to our business. We expend significant resources investing in our business, particularly with respect to our technology and service platforms. In addition, we must maintain certain levels of required capital. As a result, reduced levels of liquidity could have a significant negative effect on us. Some potential conditions that could negatively affect our liquidity include:

• | illiquid or volatile markets; |

• | diminished access to debt or capital markets; |

• | unforeseen cash or capital requirements; |

• | regulatory penalties or fines, settlements, customer restitution or other remediation costs; or |

• | adverse legal settlements or judgments. |

The capital and credit markets continue to experience varying degrees of volatility and disruption. In some cases, the markets have exerted downward pressure on availability of liquidity and credit capacity for businesses similar to ours. Without sufficient liquidity, we could be required to limit or curtail our operations or growth plans, and our business would suffer.

We may sometimes be required to fund timing differences arising from the delayed receipt of client funds associated with the settlement of client transactions in securities markets. These timing differences are funded either with internally generated cash flow or, if needed, with funds drawn under our revolving credit facility, or uncommitted lines of credit at our broker-dealer subsidiary LPL Financial. We may also need access to capital in connection with the growth of our business, through acquisitions or otherwise.

In the event current resources are insufficient to satisfy our needs, we may need to rely on financing sources such as bank debt. The availability of additional financing will depend on a variety of factors such as:

• | market conditions; |

• | the general availability of credit; |

• | the volume of trading activities; |

• | the overall availability of credit to the financial services industry; |

• | our credit ratings and credit capacity; and |

• | the possibility that our lenders could develop a negative perception of our long- or short-term financial prospects as a result of industry- or company-specific considerations. Similarly, our access to funds may be impaired if regulatory authorities or rating organizations take negative actions against us. |

Disruptions, uncertainty or volatility in the capital and credit markets may also limit our access to capital required to operate our business. Such market conditions may limit our ability to satisfy statutory capital requirements, generate commission, fee and other market-related revenue to meet liquidity needs and access the capital necessary to grow our business. As such, we may be forced to delay raising capital, issue different types of capital than we would otherwise, less effectively deploy such capital, or bear an unattractive cost of capital, which could decrease our profitability and significantly reduce our financial flexibility.

A loss of our marketing relationships with manufacturers of financial products could harm our relationship with our advisors and, in turn, their clients.

We operate on an open architecture product platform offering no proprietary financial products. To help our advisors meet their clients’ needs with suitable investment options, we have relationships with many of the industry-leading providers of financial and insurance products. We have sponsorship agreements with some manufacturers of fixed and variable annuities and mutual funds that, subject to the survival of certain terms and conditions, may be

15

terminated by the manufacturer upon notice. If we lose our relationships with one or more of these manufacturers, our ability to serve our advisors and, in turn, their clients, and our business, may be materially adversely affected. As an example, certain variable annuity product sponsors have ceased offering and issuing new variable annuity contracts. If this trend continues, we could experience a loss in the revenue currently generated from the sale of such products. In addition, certain features of such contracts have been eliminated by variable annuity product sponsors. If this trend continues, the attractiveness of these products would be reduced, potentially reducing the revenue we currently generate from the sale of such products.

Our business could be materially adversely affected as a result of the risks associated with acquisitions and investments.