Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended January 29, 2012

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 001-33608

lululemon athletica inc.

(Exact name of registrant as specified in its charter)

| Delaware | 20-3842867 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification Number) | |

| 1818 Cornwall Avenue Vancouver, British Columbia |

V6J 1C7 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (604) 732-6124

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of Each Exchange on Which Registered | |

| Common Stock, par value $0.005 per share | Nasdaq Global Select Market |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 of Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | þ | Accelerated filer | ¨ | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in rule 12b-2 of the Act). Yes ¨ No þ

The aggregate market value of the voting stock held by non-affiliates of the registrant on July 29, 2011 was approximately $5,950,828,701. Such aggregate market value was computed by reference to the closing price of the common stock as reported on the Nasdaq Global Select Market on July 29, 2011. For purposes of determining this amount only, the registrant has defined affiliates as including the executive officers and directors of the registrant on July 29, 2011.

Common Stock:

At March 19, 2012 there were 111,054,699 shares of the registrant’s common stock, par value $0.005 per share, outstanding.

Exchangeable and Special Voting Shares:

At March 19, 2012, there were outstanding 32,501,680 exchangeable shares of Lulu Canadian Holding, Inc., a wholly-owned subsidiary of the registrant. Exchangeable shares are exchangeable for an equal number of shares of the registrant’s common stock.

In addition, at March 19, 2012, the registrant had outstanding 32,501,680 shares of special voting stock, through which the holders of exchangeable shares of Lulu Canadian Holding, Inc. may exercise their voting rights with respect to the registrant. The special voting stock and the registrant’s common stock generally vote together as a single class on all matters on which the common stock is entitled to vote.

DOCUMENTS INCORPORATED BY REFERENCE

| DOCUMENT |

PARTS INTO WHICH INCORPORATED | |

| Portions of Proxy Statement for the 2012 Annual Meeting of Stockholders |

Part III |

Table of Contents

| Page | ||||||

| Item 1. |

1 | |||||

| Item 1A. |

10 | |||||

| Item 2. |

18 | |||||

| Item 3. |

19 | |||||

| Item 5. |

MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

20 | ||||

| Item 6. |

23 | |||||

| Item 7. |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

25 | ||||

| Item 7A. |

45 | |||||

| Item 8. |

47 | |||||

| Item 9A. |

75 | |||||

| Item 10. |

76 | |||||

| Item 11. |

76 | |||||

| Item 12. |

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS |

76 | ||||

| Item 13. |

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE |

77 | ||||

| Item 14. |

77 | |||||

| Item 15. |

78 | |||||

Table of Contents

Special Note Regarding Forward-Looking Statements

This Annual Report on Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended and Section 21E of the Securities Exchange Act of 1934, as amended. We use words such as “anticipates,” “believes,” “estimates,” “may,” “intends,” “expects” and similar expressions to identify forward-looking statements. Discussions containing forward-looking statements may be found in the material set forth under “Business,” “Management’s Discussion and Analysis of Financial Condition and Results of Operation” and in other sections of the report. All forward-looking statements are inherently uncertain as they are based on our expectations and assumptions concerning future events. Any or all of our forward-looking statements in this report may turn out to be inaccurate. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. They may be affected by inaccurate assumptions we might make or by known or unknown risks and uncertainties, including the risks, uncertainties and assumptions described in the section entitled Item 1A and elsewhere in this report. In light of these risks, uncertainties and assumptions, the forward-looking events and circumstances discussed in this report may not occur as contemplated, and our actual results could differ materially from those anticipated or implied by the forward-looking statements. All forward-looking statements in this report are made as of the date hereof, based on information available to us as of the date hereof, and we assume no obligation to update any forward-looking statement.

| ITEM 1. | BUSINESS |

Overview

lululemon athletica inc. is a designer and retailer of technical athletic apparel operating primarily in North America and Australia. Our yoga-inspired apparel is marketed under the lululemon athletica brand name. We believe consumers associate our brand with innovative, technical apparel products. Our products are designed to offer performance, fit and comfort while incorporating both function and style. Our heritage of combining performance and style distinctly positions us to address the needs of female athletes as well as a growing core of consumers who desire everyday casual wear that is consistent with their active lifestyles. We also continue to broaden our product range to increasingly appeal to male athletes and athletic female youth. We offer a comprehensive line of apparel and accessories including fitness pants, shorts, tops and jackets designed for athletic pursuits such as yoga, running and general fitness. As of January 29, 2012, our branded apparel was principally sold through 174 stores that are located in Canada, the United States, Australia and New Zealand. We believe our vertical retail strategy allows us to interact more directly with, and gain feedback from, our customers, whom we call guests, while providing us with greater control of our brand.

We have developed a distinctive community-based strategy that we believe enhances our brand and reinforces our guest loyalty. The key elements of our strategy are to:

| • | design and develop innovative athletic apparel that combines performance with style and incorporates real-time guest feedback; |

| • | locate our stores in street locations, lifestyle centers and malls that position each lululemon athletica store as an integral part of its community; |

| • | create an inviting and educational store environment that encourages product trial and repeat visits; and |

| • | market on a grassroots level in each community, including through social media and influential fitness practitioners who embrace and create excitement around our brand. |

We were founded in 1998 by Dennis “Chip” Wilson in Vancouver, British Columbia. Noting the increasing number of women participating in sports, and specifically yoga, Mr. Wilson developed lululemon athletica to address a void in the women’s athletic apparel market. The founding principles established by Mr. Wilson drive

1

Table of Contents

our distinctive corporate culture with a mission of providing people with the components to live a longer, healthier and more fun life. Consistent with this mission, we promote a set of core values in our business, which include developing the highest quality products, operating with integrity, leading a healthy balanced life, and training our employees in self responsibility and goal setting. These core values attract passionate and motivated employees who are driven to succeed and share our vision of “elevating the world from mediocrity to greatness.” We believe the energy and passion of our employees allow us to successfully execute on our business strategy, enhance brand loyalty and create a distinctive connection with our guests.

We believe our culture and community-based business approach provides us with competitive advantages that are responsible for our strong financial performance. Our net revenue has increased from $40.7 million in fiscal 2004 to $1,000.8 million in fiscal 2011, representing a 58% compound annual growth rate. Our net revenue increased from $711.7 million in fiscal 2010 to $1,000.8 million in fiscal 2011, representing a 41% increase. During fiscal 2011, our comparable store sales growth was 22% and we reported income from operations of $287.0 million. During fiscal 2010, our comparable store sales growth was 37% and we reported income from operations of $180.4 million. In fiscal 2011, our corporate-owned stores opened at least one year, averaged sales of approximately $2,004 per square foot, compared to sales per square foot of approximately $1,726 for fiscal 2010. We believe this is among the best in the apparel retail sector.

Our Market

Our primary target customer is a sophisticated and educated woman who understands the importance of an active, healthy lifestyle. She is increasingly tasked with the dual responsibilities of career and family and is constantly challenged to balance her work, life and health. We believe she pursues exercise to achieve physical fitness and inner peace.

As women have continued to embrace a variety of fitness and athletic activities, including yoga, we believe other athletic apparel companies are not effectively addressing their unique style, fit and performance needs. We believe we have been able to help address this void in the marketplace by incorporating style along with comfort and functionality into our products through our vertical retail strategy. Although we were founded to address the unique needs of women, we are also successfully designing products for men and athletic female youth who also appreciate the technical rigor and premium quality of our products. We also believe longer-term growth in athletic participation will be reinforced as the aging Baby Boomer generation focuses more on longevity. In addition, we believe consumer purchase decisions are driven by both an actual need for functional products and a desire to create a particular lifestyle perception. As such, we believe the credibility and authenticity of our brand expands our potential market beyond just athletes to those who desire to lead an active, healthy, and balanced life.

Our Competitive Strengths

We believe the following strengths differentiate us from our competitors and are important to our success:

| • | Premium Active Brand. lululemon athletica stands for leading a healthy, balanced and fun life. We believe customers associate the lululemon athletica brand with high quality premium athletic apparel that incorporates technically advanced materials, innovative functional features and style. We believe our focus on women differentiates us and positions lululemon athletica to address a void in the growing market for women’s athletic apparel. While our brand has its roots in yoga, our products are increasingly being designed and used for other athletic and casual lifestyle pursuits, such as running and general fitness. We work with local athletes and fitness practitioners to enhance our brand awareness and broaden our product appeal. |

| • | Distinctive Retail Experience. We locate our stores in street locations, lifestyle centers and malls that position lululemon athletica stores to be an integral part of their communities. We coach our store sales associates, whom we refer to as “educators,” to develop a personal connection with each guest. Our |

2

Table of Contents

| educators receive approximately 30 hours of in-house training within the first three months of the start of their employment and are well prepared to explain the technical and innovative design aspects of each product. |

| • | Innovative Design Process. We offer high-quality premium apparel that is designed for performance, comfort, functionality and style. We attribute our ability to develop superior products to a number of factors, including: |

| • | our feedback-based design process through which our design and product development team proactively and frequently seeks input from our guests and local fitness practitioners; |

| • | close collaboration with our third-party suppliers to formulate innovative and technically-advanced fabrics and features for our products; and |

| • | although we typically bring products from design to market in eight to 10 months, our vertical retail strategy enables us to bring select products to market in as little as two months, thereby allowing us to respond quickly to customer feedback, changing market conditions and apparel trends. |

| • | Community-Based Marketing Approach. We differentiate lululemon athletica through an innovative, community-based approach to building brand awareness and customer loyalty. We use a multi-faceted grassroots marketing strategy that includes social media, and creating in-store community boards. We believe this grassroots approach allows us to successfully increase brand awareness and broaden our appeal while reinforcing our premium brand image. |

| • | Deep Rooted Culture Centered on Training and Personal Growth. We believe our core values and distinctive corporate culture allow us to attract passionate and motivated employees who are driven to succeed and share our vision. We provide our employees with a supportive, goal-oriented environment and encourage them to reach their full professional, health and personal potential. We offer programs such as personal development workshops and goal coaching to assist our employees in realizing their long-term objectives. We believe our relationship with our employees is exceptional and a key contributor to our success. |

| • | Experienced Management Team with Proven Ability to Execute. Our Chief Executive Officer, Ms. Day, whose experience includes 20 years at Starbucks Corporation, most recently serving as President of Asia Pacific Group of Starbucks International from 2004 to 2007, joined us in January 2008. Ms. Day has assembled a management team with a complementary mix of retail, design, operations, product sourcing, marketing and information technology experience from leading apparel and retail companies such as Abercrombie & Fitch Co., The Gap, Inc., Nike, Inc. and Speedo International Limited. We believe our management team is well positioned to execute the long-term growth strategy for our business. |

Growth Strategy

Key elements of our growth strategy are to:

| • | Grow our Store Base in North America. As of January 29, 2012, our products were sold through 155 corporate-owned stores in North America, including 47 in Canada and 108 in the United States. We expect that most of our near-term store growth will occur in the United States. We plan to add new stores to strengthen existing markets and selectively enter new markets in the United States and Canada. We opened 33 stores in the United States and Canada in fiscal 2011, including our remaining four franchised stores that were reacquired, and we plan to open up to 30 stores in the United States and two ivivva athletica branded stores in Canada in fiscal 2012. |

| • | Develop our Direct to Consumer Sales Channel. We launched our retail website in the first quarter of fiscal 2009. The addition of e-commerce to our direct to consumer sales channel expanded our |

3

Table of Contents

| customer base and supplemented our growing store base over the past three years. We plan to continue developing our e-commerce website to provide a distinctive online shopping experience and extend our reach. |

| • | Increase our Brand Awareness. We will continue to increase brand awareness and customer loyalty through our grassroots marketing efforts, social media and planned store expansion. We believe that increased brand awareness will result in increased comparable store sales and store productivity over time. |

| • | Introduce New Product Technologies. We remain focused on developing and offering products that incorporate technology-enhanced fabrics and performance features that differentiate us in the market. Collaborating with leading fabric manufacturers, we have jointly developed and trademarked names for innovative fabrics such as Luon and Silverescent, and natural stretch fabrics using organic elements such as cotton and seaweed. Among our ongoing efforts, we are developing fabrics to provide advanced features such as UV protection and inherent reflectivity. In addition, we will continue to develop differentiated manufacturing techniques that provide greater support, protection, and comfort. |

| • | Broaden the Appeal of our Products. We will selectively seek opportunities to expand the appeal of our brand to improve store productivity and increase our overall addressable market. To enhance our product appeal, we intend to: |

| • | Expand our Product Categories. We continue to expand our product offerings in complementary existing and new categories such as bags, underwear and outerwear; |

| • | Increase the Range of Athletic Activities our Products Target. Our guests purchase our products mainly for activities such as yoga, running and general fitness. We will continue to expand our product categories and educate our guests on the versatility of our products; |

| • | Expand Beyond North America. As of January 29, 2012, we operated 18 corporate-owned stores and four showrooms in Australia, one corporate-owned store and two showrooms in New Zealand, and one corporate-owned showroom in Hong Kong. We plan to open approximately five lululemon stores in fiscal 2012 in Australia and New Zealand. Over time, we intend to expand on our own or pursue additional joint venture opportunities in other Asian and European markets; |

| • | Grow our Men’s Business. We believe the premium quality and technical rigor of our products will continue to appeal to men and that there is an opportunity to expand our men’s business as a proportion of our total sales; and |

| • | Develop our Youth Brand. We launched our youth focused brand, ivivva athletica, in the fourth quarter of fiscal 2009. We believe the premium quality and technical rigor of our dance-inspired products designed for female youth serve an open market and provide us with an opportunity for future growth. |

Our Stores

As of January 29, 2012, our retail footprint included 47 stores in Canada, 108 stores in the United States, 18 stores in Australia and one in New Zealand. While most of our stores are branded lululemon athletica, five of our corporate-owned stores are branded ivivva athletica and specialize in dance-inspired apparel for female youth. We no longer operate any franchised stores as we reacquired our four remaining franchises during fiscal 2011. Our retail stores are located primarily on street locations, in lifestyle centers and in malls.

4

Table of Contents

The following store list shows the number of corporate-owned stores operated in each Canadian province, U.S. state, and internationally:

| January 29, 2012 | January 30, 2011 | |||||||

| Canada |

||||||||

| Alberta |

11 | 9 | ||||||

| British Columbia |

12 | 11 | ||||||

| Manitoba |

1 | 1 | ||||||

| Nova Scotia |

1 | 1 | ||||||

| Ontario |

17 | 17 | ||||||

| Québec |

4 | 4 | ||||||

| Saskatchewan |

1 | 1 | ||||||

|

|

|

|

|

|||||

| Total Canada |

47 | 44 | ||||||

|

|

|

|

|

|||||

| United States |

||||||||

| Alabama |

1 | 1 | ||||||

| Arizona |

3 | 2 | ||||||

| California |

23 | 19 | ||||||

| Colorado |

3 | — | ||||||

| Connecticut |

3 | 2 | ||||||

| District of Columbia |

2 | 2 | ||||||

| Florida |

7 | 4 | ||||||

| Georgia |

1 | 1 | ||||||

| Hawaii |

1 | 1 | ||||||

| Illinois |

8 | 8 | ||||||

| Indiana |

1 | — | ||||||

| Kansas |

1 | — | ||||||

| Maryland |

2 | 2 | ||||||

| Massachusetts |

5 | 5 | ||||||

| Michigan |

1 | 1 | ||||||

| Minnesota |

3 | 2 | ||||||

| Missouri |

1 | 1 | ||||||

| Nevada |

1 | 1 | ||||||

| New Jersey |

5 | 3 | ||||||

| New York |

8 | 7 | ||||||

| North Carolina |

2 | — | ||||||

| Ohio |

3 | 1 | ||||||

| Oregon |

2 | 2 | ||||||

| Pennsylvania |

4 | 2 | ||||||

| Tennessee |

1 | 1 | ||||||

| Texas |

10 | 6 | ||||||

| Virginia |

3 | 2 | ||||||

| Washington |

3 | 3 | ||||||

|

|

|

|

|

|||||

| Total United States |

108 | 78 | ||||||

|

|

|

|

|

|||||

| Australia |

||||||||

| New South Wales |

6 | 5 | ||||||

| Queensland |

2 | — | ||||||

| South Australia |

1 | — | ||||||

| Victoria |

6 | 5 | ||||||

| Western Australia |

3 | 1 | ||||||

|

|

|

|

|

|||||

| Total Australia |

18 | 11 | ||||||

|

|

|

|

|

|||||

| New Zealand |

1 | — | ||||||

|

|

|

|

|

|||||

| Total |

174 | 133 | ||||||

|

|

|

|

|

|||||

5

Table of Contents

Store Economics

We believe that our innovative retail concept and guest experience contribute to the success of our stores. During fiscal 2011 our corporate-owned stores open at least one year, which average approximately 2,662 square feet, averaged sales of approximately $2,004 per square foot.

Management performs an ongoing evaluation of our portfolio of corporate-owned store locations. In fiscal 2011 we did not close any of our corporate-owned stores. As we continue our evaluation we may in future periods close corporate-owned store locations.

Store Expansion

From February 1, 2002 (when we had one store, in Vancouver) to January 29, 2012, we opened or acquired 173 net corporate-owned stores in North America and Australia. We opened our first corporate-owned store in the United States in 2003 and in Australia in 2010. We opened 41 corporate-owned stores in the North America and Australia in fiscal 2011, including our remaining four franchised stores that were reacquired. Over the next few years, our new store growth will be primarily focused on corporate-owned stores in the United States, an attractive market with a population of over nine times that of Canada. Beyond North America, we intend to expand our global presence as part of our long-term business strategy. We believe that partnering with companies and individuals with significant experience and proven success in the target country is to our advantage.

Direct to Consumer

In fiscal 2009 we launched our e-commerce website which makes up our direct to consumer channel. Direct to consumer is an increasingly substantial part of our business, representing approximately 11% of our net revenue in fiscal 2011, compared to 8% of our net revenue in fiscal 2010. We believe that a direct to consumer channel is convenient for our core customer and enhances the image of our brand. Our direct to consumer channel makes our product accessible in more markets than our corporate-owned store channel alone. We use this channel to build brand awareness, especially in new markets, including those outside of North America.

Wholesale Channel

We also sell lululemon athletica products through premium yoga studios, health clubs and fitness centers. This channel represented 2% of our net revenue in both fiscal 2011 and fiscal 2010. We believe these premium wholesale locations offer an alternative distribution channel that is convenient for our core consumer and enhances the image of our brand. We do not intend wholesale to be a significant contributor to overall sales. Instead, we use the channel to build brand awareness, especially in new markets.

Franchise Stores

As of January 29, 2012, we no longer have franchised stores. We reacquired our four remaining franchised stores in the United States during fiscal 2011, thereby decreasing the net revenue earned through our franchise channel. This channel represented 1% of our net revenue in fiscal 2010 and an immaterial amount in fiscal 2011.

Our Products

We offer a comprehensive line of performance apparel and accessories for women, men and female youth. Our apparel assortment, including items such as fitness pants, shorts, tops and jackets, is designed for healthy lifestyle activities such as yoga, running and general fitness. Although we benefit from the growing number of people that participate in yoga, we believe the percentage of our products sold for other activities will continue to increase as we broaden our product range to address other activities. Our fitness-related accessories include an array of items such as bags, socks, underwear, yoga mats, instructional yoga DVDs and water bottles.

Our design team continues to develop fabrics that we believe will help advance our product line and differentiate us from the competition.

6

Table of Contents

Our Culture and Values

Since our inception, we have developed a distinctive corporate culture with a mission to provide people with components to live a longer, healthier and more fun life. We promote a set of core values in our business, which include developing the highest quality products, operating with integrity, leading a healthy balanced life and instilling in our employees a sense of self responsibility and personal achievement. These core values allow us to attract passionate and motivated employees who are driven to succeed and share our vision of “elevating the world from mediocrity to greatness.”

Community-Based Marketing

We differentiate our business through an innovative, community-based approach to building brand awareness and customer loyalty. We pursue a multi-faceted strategy which leverages our local ambassadors, social media, in-store community boards and a variety of grassroots initiatives.

Product Design and Development

Our product design efforts are led by a team of designers based in Vancouver, British Columbia partnering with international designers. Our team is comprised of dedicated athletes and users of our products who embody our design philosophy and dedication to premium quality. Our design team identifies trends based on market intelligence and research, proactively seeks the input of our guests and our ambassadors and broadly seeks inspiration consistent with our goals of style, function and technical superiority.

To ensure that we continue to provide our guests with functional fabrics, our design team works closely with our suppliers to incorporate innovative fabrics that bring particular specifications to our products. We partner with a leading independent inspection, verification, testing and certification company, which conducts a battery of tests before each season on our fabrics, testing for a variety of performance characteristics including pilling, shrinkage, abrasion resistance and colorfastness. We collaborate with leading fabric suppliers to develop fabrics that we ultimately trademark for brand recognition whenever possible.

Sourcing and Manufacturing

We do not own or operate any manufacturing facilities, nor do we contract directly with third-party vendors for fabrics and finished goods. The fabric used in our products is sourced by our manufacturers from a limited number of pre-approved suppliers. We work with a group of approximately 45 manufacturers, five of which produced approximately 67% of our products in fiscal 2011. During fiscal 2011, no single manufacturer produced more than 36% of our product offering. During fiscal 2011, approximately 49% of our products were produced in China, approximately 41% in South/South East Asia, approximately 3% in Canada and the remainder in the United States, Peru, Israel, Egypt and other countries. Our North American manufacturers provide us with the speed to market necessary to respond quickly to changing trends and increased demand. While we plan to support future growth through manufacturers outside of North America, our intent is also to maintain production in Canada and the United States whenever practicable. We have developed long-standing relationships with a number of our vendors and take great care to ensure that they share our commitment to quality and ethics. We do not, however, have any long-term agreements requiring us to use any manufacturer, and no manufacturer is required to produce our products in the long-term. We require that all of our manufacturers adhere to a code of conduct regarding quality of manufacturing, working conditions and other social concerns. We currently also work with a leading inspection and verification firm to closely monitor each supplier’s compliance with applicable law and our workplace code of conduct. We believe that the services of additional, or other, producers of our fabrics could be obtained with little or no additional expense to us and/or delay in the timeliness of our production process.

7

Table of Contents

Distribution Facilities

We centrally distribute finished products in from distribution facilities in Vancouver, British Columbia, Sumner, Washington, and Melbourne, Victoria. We operate the distribution facilities in Vancouver, Sumner and Melbourne which are leased and are approximately 120,000, 167,000 and 54,000 square feet, respectively. We believe these modern facilities enhance the efficiency of our operations. We believe our distribution infrastructure will be sufficient to accommodate our expected store growth and expanded product offerings over the next several years. Merchandise is typically shipped to our stores through third-party delivery services multiple times per week, providing them with a steady flow of new inventory.

Competition

Competition in the athletic apparel industry is principally on the basis of brand image and recognition as well as product quality, innovation, style, distribution and price. We believe that we successfully compete on the basis of our premium brand image, our focus on women and our technical product innovation. In addition, we believe our vertical retail distribution strategy differentiates us from our competitors and allows us to more effectively control our brand image.

The market for athletic apparel is highly competitive. It includes increasing competition from established companies who are expanding their production and marketing of performance products, as well as from frequent new entrants to the market. We are in direct competition with wholesalers and direct sellers of athletic apparel, such as Nike, Inc., adidas AG, which includes the adidas and Reebok brands, and Under Armour, Inc. We also compete with retailers specifically focused on women’s athletic apparel including The Gap, Inc. (including the Athleta brand), Lucy Activewear Inc., and bebe stores, inc. (including the BEBE SPORT collection).

Our Employees

As of January 29, 2012, we had 5,807 employees, of which 2,511 were employed in Canada, 2,869 were employed in the United States, and 427 were employed internationally. Of the 2,511 Canadian employees, 1,790 were employed in our retail locations, 71 were employed in distribution, 132 were employed in design, merchandise and production, and the remaining 518 performed selling, general and administrative and other functions. Of the 2,869 employees in the United States, 2,739 were employed in our retail locations, 63 were employed in distribution and 67 performed selling, general and administration functions. Of the 427 international employees, 343 were employed in our international retail locations, 23 were employed in distribution, and 61 performed merchandise, production, and administrative functions. None of our employees is currently covered by a collective bargaining agreement. We have had no labor-related work stoppages and we believe our relations with our employees are excellent.

Intellectual Property

We believe we own the material trademarks used in connection with the marketing, distribution and sale of all of our products in Canada, the United States and in the other countries in which our products are currently or intended to be either sold or manufactured. Our major trademarks include lululemon athletica & design, the logo design (WAVE design) and lululemon as a word mark. In addition to the registrations in Canada and the United States, lululemon’s design and word mark are registered in over 66 other jurisdictions which cover over 114 countries. We own trademark registrations for names of several of our fabrics including Luon, Silverescent, VitaSea, Soyla, Boolux and Luxtreme. In addition to trademarks, we own 16 industrial design registrations in Canada protecting our distinctive apparel and accessory designs, as well as a number of corresponding design patent applications in the United States and design registrations in Europe.

Securities and Exchange Commission Filings

Our website address is www.lululemon.com. We provide free access to various reports that we file with, or furnish to, the United States Securities and Exchange Commission, or the SEC, through our website, as soon as

8

Table of Contents

reasonably practicable after they have been filed or furnished. These reports include, but are not limited to, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and any amendments to those reports. Our SEC reports can also be accessed through the SEC’s website at www.sec.gov. Also available on our website are printable versions of our Code of Business Conduct and Ethics and charters of the Audit, Compensation, and Nominating and Governance Committees of our Board of Directors. Information on our website does not constitute part of this annual report on Form 10-K or any other report we file or furnish with the SEC.

9

Table of Contents

| ITEM 1A. | RISK FACTORS |

In addition to the other information contained in this Form 10-K, the following risk factors should be considered carefully in evaluating our business. Our business, financial condition or results of operations could be materially adversely affected by any of these risks. Please note that additional risks not presently known to us or that we currently deem immaterial could also impair our business and operations.

Our success depends on our ability to maintain the value and reputation of our brand.

Our success depends on the value and reputation of the lululemon athletica brand. The lululemon athletica name is integral to our business as well as to the implementation of our strategies for expanding our business. Maintaining, promoting and positioning our brand will depend largely on the success of our marketing and merchandising efforts and our ability to provide a consistent, high quality guest experience. We rely on social media, as one of our marketing strategies, to have a positive impact on both our brand value and reputation. Our brand could be adversely affected if we fail to achieve these objectives or if our public image or reputation were to be tarnished by negative publicity. Negative publicity regarding the production methods of any of our suppliers or manufacturers could adversely affect our reputation and sales and force us to locate alternative suppliers or manufacturing sources. Additionally, while we devote considerable efforts and resources to protecting our intellectual property, if these efforts are not successful the value of our brand may be harmed, which could have a material adverse effect on our financial condition.

An economic downturn or economic uncertainty in our key markets may adversely affect consumer discretionary spending and demand for our products.

Many of our products may be considered discretionary items for consumers. Factors affecting the level of consumer spending for such discretionary items include general economic conditions, particularly those in Canada and the United States, and other factors such as consumer confidence in future economic conditions, fears of recession, the availability of consumer credit, levels of unemployment, tax rates and the cost of consumer credit. As global economic conditions continue to be volatile or economic uncertainty remains, trends in consumer discretionary spending also remain unpredictable and subject to reductions due to credit constraints and uncertainties about the future. The current volatility in the United States economy in particular has resulted in an overall slowing in growth in the retail sector because of decreased consumer spending, which may remain depressed for the foreseeable future. These unfavorable economic conditions may lead consumers to delay or reduce purchase of our products. Consumer demand for our products may not reach our sales targets, or may decline, when there is an economic downturn or economic uncertainty in our key markets, particularly in North America. Our sensitivity to economic cycles and any related fluctuation in consumer demand may have a material adverse effect on our financial condition.

Our sales and profitability may decline as a result of increasing product costs and decreasing selling prices.

Our business is subject to significant pressure on pricing and costs caused by many factors, including intense competition, constrained sourcing capacity and related inflationary pressure, pressure from consumers to reduce the prices we charge for our products and changes in consumer demand. These factors may cause us to experience increased costs, reduce our sales prices to consumers or experience reduced sales in response to increased prices, any of which could cause our operating margin to decline if we are unable to offset these factors with reductions in operating costs and could have a material adverse affect on our financial conditions, operating results and cash flows.

If we are unable to anticipate consumer preferences and successfully develop and introduce new, innovative and updated products, we may not be able to maintain or increase our sales and profitability.

Our success depends on our ability to identify and originate product trends as well as to anticipate and react to changing consumer demands in a timely manner. All of our products are subject to changing consumer

10

Table of Contents

preferences that cannot be predicted with certainty. If we are unable to introduce new products or novel technologies in a timely manner or our new products or technologies are not accepted by our customers, our competitors may introduce similar products in a more timely fashion, which could hurt our goal to be viewed as a leader in technical athletic apparel innovation. Our new products may not receive consumer acceptance as consumer preferences could shift rapidly to different types of athletic apparel or away from these types of products altogether, and our future success depends in part on our ability to anticipate and respond to these changes. Failure to anticipate and respond in a timely manner to changing consumer preferences could lead to, among other things, lower sales and excess inventory levels. Even if we are successful in anticipating consumer preferences, our ability to adequately react to and address those preferences will in part depend upon our continued ability to develop and introduce innovative, high-quality products. Our failure to effectively introduce new products that are accepted by consumers could result in a decrease in net revenue and excess inventory levels, which could have a material adverse effect on our financial condition.

Our results of operations could be materially harmed if we are unable to accurately forecast customer demand for our products.

To ensure adequate inventory supply, we must forecast inventory needs and place orders with our manufacturers based on our estimates of future demand for particular products. Our ability to accurately forecast demand for our products could be affected by many factors, including an increase or decrease in customer demand for our products or for products of our competitors, our failure to accurately forecast customer acceptance of new products, product introductions by competitors, unanticipated changes in general market conditions, and weakening of economic conditions or consumer confidence in future economic conditions. If we fail to accurately forecast customer demand we may experience excess inventory levels or a shortage of products available for sale in our stores or for delivery to guests.

Inventory levels in excess of customer demand may result in inventory write-downs or write-offs and the sale of excess inventory at discounted prices, which would cause our gross margin to suffer and could impair the strength and exclusivity of our brand. Conversely, if we underestimate customer demand for our products, our manufacturers may not be able to deliver products to meet our requirements, and this could result in damage to our reputation and customer relationships.

If we continue to grow at a rapid pace, we may not be able to effectively manage our growth and the increased complexity of our business and as a result our brand image and financial performance may suffer.

We have expanded our operations rapidly since our inception in 1998 and our net revenue has increased from $40.7 million in fiscal 2004 to $1,000.8 million in fiscal 2011. If our operations continue to grow at a rapid pace, we may experience difficulties in obtaining sufficient raw materials and manufacturing capacity to produce our products, as well as delays in production and shipments, as our products are subject to risks associated with overseas sourcing and manufacturing. We could be required to continue to expand our sales and marketing, product development and distribution functions, to upgrade our management information systems and other processes and technology, and to obtain more space for our expanding workforce. This expansion could increase the strain on our resources, and we could experience serious operating difficulties, including difficulties in hiring, training and managing an increasing number of employees. These difficulties could result in the erosion of our brand image which could have a material adverse effect on our financial condition.

The fluctuating cost of raw materials could increase our cost of goods sold and cause our results of operations and financial condition to suffer.

The fabrics used by our suppliers and manufacturers include synthetic fabrics whose raw materials include petroleum-based products. Our products also include natural fibers, including cotton. Our costs for raw materials are affected by, among other things, weather, consumer demand, speculation on the commodities market, the

11

Table of Contents

relative valuations and fluctuations of the currencies of producer versus consumer countries and other factors that are generally unpredictable and beyond our control. Increases in the cost of raw materials, including petroleum or the prices we pay for our cotton yarn and cotton-based textiles, could have a material adverse effect on our cost of goods sold, results of operations, financial condition and cash flows.

We rely on third-party suppliers to provide fabrics for and to produce our products, and we have limited control over them and may not be able to obtain quality products on a timely basis or in sufficient quantity.

We do not manufacture our products or the raw materials for them and rely instead on third-party suppliers. Many of the specialty fabrics used in our products are technically advanced textile products developed and manufactured by third parties and may be available, in the short-term, from only one or a very limited number of sources. For example, Luon fabric, which is included in many of our products, is supplied to the mills we use by a single manufacturer in Taiwan, and the fibers used in manufacturing Luon fabric are supplied to our Taiwanese manufacturer by a single company. In fiscal 2011, approximately 67% of our products were produced by our top five manufacturing suppliers. We have no long term contracts with our suppliers or manufacturing sources, and we compete with other companies for fabrics, raw materials, production and import quota capacity.

We may experience a significant disruption in the supply of fabrics or raw materials from current sources or, in the event of a disruption, we may be unable to locate alternative materials suppliers of comparable quality at an acceptable price, or at all. In addition, if we experience significant increased demand, or if we need to replace an existing supplier manufacturer, we may be unable to locate additional supplies of fabrics or raw materials or additional manufacturing capacity on terms that are acceptable to us, or at all, or we may be unable to locate any supplier or manufacturer with sufficient capacity to meet our requirements or to fill our orders in a timely manner. Identifying a suitable supplier is an involved process that requires us to become satisfied with their quality control, responsiveness and service, financial stability and labor and other ethical practices. Even if we are able to expand existing or find new manufacturing or fabric sources, we may encounter delays in production and added costs as a result of the time it takes to train our suppliers and manufacturers in our methods, products and quality control standards. Delays related to supplier changes could also arise due to an increase in shipping times if new suppliers are located farther away from our markets or from other participants in our supply chain. Any delays, interruption or increased costs in the supply of fabric or manufacture of our products could have an adverse effect on our ability to meet customer demand for our products and our results in lower net revenue and income from operations both in the short and long term. We have occasionally received, and may in the future continue to receive, shipments of products that fail to comply with our technical specifications or that fail to conform to our quality control standards. In that event, unless we are able to obtain replacement products in a timely manner, we risk the loss of net revenue resulting from the inability to sell those products and related increased administrative and shipping costs. Additionally, if defects in the manufacture of our products are not discovered until after such products are purchased by our guests, our guests could lose confidence in the technical attributes of our products and our results of operations could suffer and our business could be harmed.

We operate in a highly competitive market and the size and resources of some of our competitors may allow them to compete more effectively than we can, resulting in a loss of our market share and a decrease in our net revenue and profitability.

The market for technical athletic apparel is highly competitive. Competition may result in pricing pressures, reduced profit margins or lost market share or a failure to grow our market share, any of which could substantially harm our business and results of operations. We compete directly against wholesalers and direct retailers of athletic apparel, including large, diversified apparel companies with substantial market share and established companies expanding their production and marketing of technical athletic apparel, as well as against retailers specifically focused on women’s athletic apparel. We also face competition from wholesalers and direct retailers of traditional commodity athletic apparel, such as cotton T-shirts and sweatshirts. Many of our competitors are large apparel and sporting goods companies with strong worldwide brand recognition, such as Nike, Inc., adidas AG, which includes the adidas and Reebok brands, and The Gap, Inc, which includes the

12

Table of Contents

Athleta brand. Because of the fragmented nature of the industry, we also compete with other apparel sellers, including those specializing in yoga apparel. Many of our competitors have significant competitive advantages, including longer operating histories, larger and broader customer bases, more established relationships with a broader set of suppliers, greater brand recognition and greater financial, research and development, store development, marketing, distribution and other resources than we do. In addition, our technical athletic apparel is sold at a price premium to traditional athletic apparel.

Our competitors may be able to achieve and maintain brand awareness and market share more quickly and effectively than we can. In contrast to our “grassroots” marketing approach, many of our competitors promote their brands through traditional forms of advertising, such as print media and television commercials, and through celebrity endorsements, and have substantial resources to devote to such efforts. Our competitors may also create and maintain brand awareness using traditional forms of advertising more quickly than we can. Our competitors may also be able to increase sales in their new and existing markets faster than we do by emphasizing different distribution channels than we do, such as catalog sales or an extensive franchise network, as opposed to distribution through retail stores, wholesale or internet, and many of our competitors have substantial resources to devote toward increasing sales in such ways.

In addition, because we own no patents or exclusive intellectual property rights in the technology, fabrics or processes underlying our products, our current and future competitors are able to manufacture and sell products with performance characteristics, fabrication techniques and styling similar to our products.

Any material disruption of our information systems could disrupt our business and reduce our sales.

We are increasingly dependent on information systems to operate our e-commerce website, process transactions, respond to guest inquiries, manage inventory, purchase, sell and ship goods on a timely basis and maintain cost-efficient operations. Any material disruption or slowdown of our systems, including a disruption or slowdown caused by our failure to successfully upgrade our systems, system failures, viruses, computer “hackers” or other causes, could cause information, including data related to customer orders, to be lost or delayed which could—especially if the disruption or slowdown occurred during the holiday season—result in delays in the delivery of merchandise to our stores and customers or lost sales, which could reduce demand for our merchandise and cause our sales to decline. If changes in technology cause our information systems to become obsolete, or if our information systems are inadequate to handle our growth, we could lose customers.

If we encounter problems with our distribution system, our ability to deliver our products to the market and to meet guest expectations could be harmed.

We rely on our distribution facilities for substantially all of our product distribution. Our distribution facilities include computer controlled and automated equipment, which means their operations are complicated and may be subject to a number of risks related to security or computer viruses, the proper operation of software and hardware, electronic or power interruptions or other system failures. In addition, because substantially all of our products are distributed from three locations, our operations could also be interrupted by labor difficulties, extreme or severe weather conditions or by floods, fires or other natural disasters near our distribution centers. For example, severe weather conditions in Sumner, Washington in 2011, including snow and freezing rain, resulted in disruption in our distribution facilities and the local transportation system. If we encounter problems with our distribution system, our ability to meet guest expectations, manage inventory, complete sales and achieve objectives for operating efficiencies could be harmed.

We are subject to risks associated with leasing retail space subject to long-term and non-cancelable leases.

We do not own any of our store facilities, but instead lease all of our corporate-owned stores under operating leases and our inability to secure appropriate real estate or lease terms could impact our ability to grow. Our leases generally have initial terms of between five and ten years, and generally can be extended only in five-

13

Table of Contents

year increments if at all. We generally cannot cancel these leases at our option. If an existing or new store is not profitable, and we decide to close it, as we have done in the past and may do in the future, we may nonetheless be committed to perform our obligations under the applicable lease including, among other things, paying the base rent for the balance of the lease term. Similarly, we may be committed to perform our obligations under the applicable leases even if current locations of our stores become unattractive as demographic patterns change. In addition, as each of our leases expire, we may fail to negotiate renewals, either on commercially acceptable terms or at all, which could require us to close stores in desirable locations.

Increasing labor costs and other factors associated with the production of our products in China could increase the costs to produce our products.

During fiscal 2011, approximately 49% of our products were produced in China and increases in the costs of labor and other costs of doing business in China could significantly increase our costs to produce our products and could have a negative impact on our operations, revenue and earnings. Factors that could negatively affect our business include a potential significant revaluation of the Chinese Yuan, which may result in an increase in the cost of producing products in China, labor shortage and increases in labor costs in China, and difficulties in moving products manufactured in China out of Asia and through the ports on the western coast of North America, whether due to port congestion, labor disputes, product regulations and/or inspections or other factors, and natural disasters or health pandemics impacting China. Also, the imposition of trade sanctions or other regulations against products imported by us from, or the loss of “normal trade relations” status with, China, could significantly increase our cost of products imported into North America, Australia or New Zealand and harm our business.

We may not be able to successfully open new store locations in a timely manner, if at all, which could harm our results of operations.

Our growth will largely depend on our ability to successfully open and operate new stores. Our approach to identifying locations for our stores typically favors street locations, lifestyle centers and malls where we can be a part of the community. As a result, our stores are typically located near retailers or fitness facilities that we believe are consistent with our guests’ lifestyle choices. Sales at these stores are derived, in part, from the volume of foot traffic in these locations. Our ability to successfully open and operate new stores depends on many factors, including, among others, our ability to:

| • | identify suitable store locations, the availability of which is outside of our control; |

| • | negotiate acceptable lease terms, including desired tenant improvement allowances; |

| • | hire, train and retain store personnel and field management; |

| • | assimilate new store personnel and field management into our corporate culture; |

| • | source sufficient inventory levels; and |

| • | successfully integrate new stores into our existing operations and information technology systems. |

Successful new store openings may also be affected by our ability to initiate our grassroots marketing efforts in advance of opening our first store in a new market. We typically rely on our grassroots marketing efforts to build awareness of our brand and demand for our products. Our grassroots marketing efforts are often lengthy and must be tailored to each new market based on our emerging understanding of the market. Accordingly, there can be no assurance that we will be able to successfully implement our grassroots marketing efforts in a particular market in a timely manner, if at all. Additionally, we may be unsuccessful in identifying new markets where our technical athletic apparel and other products and brand image will be accepted or the performance of our stores will be considered successful.

14

Table of Contents

Our failure to comply with trade and other regulations could lead to investigations or actions by government regulators and negative publicity.

The labeling, distribution, importation, marketing and sale of our products are subject to extensive regulation by various federal agencies, including the Federal Trade Commission, Consumer Product Safety Commission and state attorneys general in the United States, the Competition Bureau and Health Canada in Canada, as well as by various other federal, state, provincial, local and international regulatory authorities in the countries in which our products are distributed or sold. If we fail to comply with any of these regulations, we could become subject to enforcement actions or the imposition of significant penalties or claims, which could harm our results of operations or our ability to conduct our business. In addition, the adoption of new regulations or changes in the interpretation of existing regulations may result in significant compliance costs or discontinuation of product sales and could impair the marketing of our products, resulting in significant loss of net sales.

Our fabrics and manufacturing technology are not patented and can be imitated by our competitors.

The intellectual property rights in the technology, fabrics and processes used to manufacture our products are owned or controlled by our suppliers and are generally not unique to us. Our ability to obtain intellectual property protection for our products is therefore limited and we currently own no patents or exclusive intellectual property rights in the technology, fabrics or processes underlying our products. As a result, our current and future competitors are able to manufacture and sell products with performance characteristics, fabrics and styling similar to our products. Because many of our competitors have significantly greater financial, distribution, marketing and other resources than we do, they may be able to manufacture and sell products based on our fabrics and manufacturing technology at lower prices than we can. If our competitors do sell similar products to ours at lower prices, our net revenue and profitability could suffer.

Our failure or inability to protect our intellectual property rights could diminish the value of our brand and weaken our competitive position.

We currently rely on a combination of copyright, trademark, trade dress and unfair competition laws, as well as confidentiality procedures and licensing arrangements, to establish and protect our intellectual property rights. We cannot assure you that the steps taken by us to protect our intellectual property rights will be adequate to prevent infringement of such rights by others, including imitation of our products and misappropriation of our brand. In addition, intellectual property protection may be unavailable or limited in some foreign countries where laws or law enforcement practices may not protect our intellectual property rights as fully as in the United States or Canada, and it may be more difficult for us to successfully challenge the use of our intellectual property rights by other parties in these countries. If we fail to protect and maintain our intellectual property rights, the value of our brand could be diminished and our competitive position may suffer.

Our future success is substantially dependent on the continued service of our senior management.

Our future success is substantially dependent on the continued service of our senior management and other key employees. The loss of the services of our senior management or other key employees could make it more difficult to successfully operate our business and achieve our business goals.

We also may be unable to retain existing management, technical, sales and client support personnel that are critical to our success, which could result in harm to our customer and employee relationships, loss of key information, expertise or know-how and unanticipated recruitment and training costs.

We do not maintain a key person life insurance policy on Ms. Day or any of the other members of our senior management team. As a result, we would have no way to cover the financial loss if we were to lose the services of members of our senior management team.

15

Table of Contents

Our business is affected by seasonality.

Our business is affected by the general seasonal trends common to the retail apparel industry. Our annual net sales are weighted more heavily toward our fourth fiscal quarter, reflecting our historical strength in sales during the holiday season, while our operating expenses are more equally distributed throughout the year. As a result, a substantial portion of our operating profits are generated in the fourth quarter of our fiscal year. For example, we generated approximately 37%, 36% and 39% of our full year gross profit during the fourth quarters of fiscal 2011, fiscal 2010 and fiscal 2009, respectively. This seasonality may adversely affect our business and cause our results of operations to fluctuate, and, as a result, we believe that comparisons of our operating results between different quarters within a single fiscal year are not necessarily meaningful and that results of operations in any period should not be considered indicative of the results to be expected for any future period.

Because a significant portion of our sales are generated in Canada, fluctuations in foreign currency exchange rates have negatively affected our results of operations and may continue to do so in the future.

The reporting currency for our consolidated financial statements is the U.S. dollar. In the future, we expect to continue to derive a significant portion of our net revenue and incur a significant portion of our operating costs in Canada, and changes in exchange rates between the Canadian dollar and the U.S. dollar may have a significant, and potentially adverse, effect on our results of operations. Additionally, a portion of our net revenue is generated in each of Australia. Our primary risk of loss regarding foreign currency exchange rate risk is caused by fluctuations in the exchange rates between the U.S. dollar, Canadian dollar and Australian dollar. Because we recognize net revenue from sales in Canada in Canadian dollars, if the Canadian dollar weakens against the U.S. dollar it would have a negative impact on our Canadian operating results upon translation of those results into U.S. dollars for the purposes of consolidation. The exchange rate of the Canadian dollar against the U.S. dollar has increased over fiscal 2011 and our results of operations have benefited from the strength in the Canadian dollar. If the Canadian dollar were to weaken relative to the U.S. dollar, our net revenue would decline and our income from operations and net income could be adversely affected. A 10% depreciation in the relative value of the Canadian dollar compared to the U.S. dollar would have resulted in lost income from operations of approximately $15.4 million in fiscal 2011 and approximately $11.3 million in fiscal 2010. Similarly, a 10% depreciation in the relative value of the Australian dollar compared to the U.S. dollar would have resulted in lost income from operations of approximately $0.4 million in fiscal 2011 and $0.1 million in fiscal 2010. We have not historically engaged in hedging transactions and do not currently contemplate engaging in hedging transactions to mitigate foreign exchange risks. As we continue to recognize gains and losses in foreign currency transactions, depending upon changes in future currency rates, such gains or losses could have a significant, and potentially adverse, effect on our results of operations.

The operations of many of our suppliers are subject to additional risks that are beyond our control and that could harm our business, financial condition and results of operations.

Almost all of our suppliers are located outside the United States. During fiscal 2011, approximately 3% of our products were produced in Canada, approximately 49% in China, approximately 41% in South and South East Asia and the remainder in the United States, Peru, Israel, Egypt and other countries. As a result of our international suppliers, we are subject to risks associated with doing business abroad, including:

| • | political unrest, terrorism, labor disputes and economic instability resulting in the disruption of trade from foreign countries in which our products are manufactured; |

| • | the imposition of new laws and regulations, including those relating to labor conditions, quality and safety standards, imports, duties, taxes and other charges on imports, as well as trade restrictions and restrictions on currency exchange or the transfer of funds; |

| • | reduced protection for intellectual property rights, including trademark protection, in some countries, particularly China; |

| • | disruptions or delays in shipments; and |

16

Table of Contents

| • | changes in local economic conditions in countries where our manufacturers, suppliers or guests are located. |

These and other factors beyond our control could interrupt our suppliers’ production in offshore facilities, influence the ability of our suppliers to export our products cost-effectively or at all and inhibit our suppliers’ ability to procure certain materials, any of which could harm our business, financial condition and results of operations.

Our ability to source our merchandise profitably or at all could be hurt if new trade restrictions are imposed or existing trade restrictions become more burdensome.

The United States and the countries in which our products are produced or sold internationally have imposed and may impose additional quotas, duties, tariffs, or other restrictions or regulations, or may adversely adjust prevailing quota, duty or tariff levels. For example, under the provisions of the World Trade Organization, or the WTO, Agreement on Textiles and Clothing, effective as of January 1, 2005, the United States and other WTO member countries eliminated quotas on textiles and apparel-related products from WTO member countries. In 2005, China’s exports into the United States surged as a result of the eliminated quotas. In response to the perceived disruption of the market, the United States imposed new quotas, which remained in place through the end of 2008, on certain categories of natural-fiber products that we import from China. These quotas were lifted on January 1, 2009, but we have expanded our relationships with suppliers outside of China, which among other things has resulted in increased costs and shipping times for some products. Countries impose, modify and remove tariffs and other trade restrictions in response to a diverse array of factors, including global and national economic and political conditions, which make it impossible for us to predict future developments regarding tariffs and other trade restrictions. Trade restrictions, including tariffs, quotas, embargoes, safeguards and customs restrictions, could increase the cost or reduce the supply of products available to us or may require us to modify our supply chain organization or other current business practices, any of which could harm our business, financial condition and results of operations.

Our trademarks and other proprietary rights could potentially conflict with the rights of others and we may be prevented from selling some of our products.

Our success depends in large part on our brand image. We believe that our trademarks and other proprietary rights have significant value and are important to identifying and differentiating our products from those of our competitors and creating and sustaining demand for our products. We have obtained and applied for some United States and foreign trademark registrations, and will continue to evaluate the registration of additional trademarks as appropriate. However, we cannot guarantee that any of our pending trademark applications will be approved by the applicable governmental authorities. Moreover, even if the applications are approved, third parties may seek to oppose or otherwise challenge these registrations. Additionally, we cannot assure you that obstacles will not arise as we expand our product line and the geographic scope of our sales and marketing. Third parties may assert intellectual property claims against us, particularly as we expand our business and the number of products we offer. Our defense of any claim, regardless of its merit, could be expensive and time consuming and could divert management resources. Successful infringement claims against us could result in significant monetary liability or prevent us from selling some of our products. In addition, resolution of claims may require us to redesign our products, license rights from third parties or cease using those rights altogether. Any of these events could harm our business and cause our results of operations, liquidity and financial condition to suffer.

Our limited operating experience and limited brand recognition in new international markets may limit our expansion strategy and cause our business and growth to suffer.

Our future growth depends, to an extent, on our international expansion efforts. We have limited experience with regulatory environments and market practices internationally, and we may not be able to penetrate or successfully operate in any new market. In connection with our initial expansion efforts in Japan, we encountered

17

Table of Contents

obstacles we did not face in North America, including cultural and linguistic differences, differences in regulatory environments, labor practices and market practices, difficulties in keeping abreast of market, business and technical developments and foreign guests’ tastes and preferences. We may also encounter difficulty expanding into new international markets because of limited brand recognition leading to delayed acceptance of our technical athletic apparel by guests in these new international markets. Our failure to develop new international markets or disappointing growth outside of existing markets will harm our business and results of operations.

Our founder controls a significant percentage of our stock and is able to exercise significant influence over our affairs.

Our founder, Dennis Wilson, beneficially owns approximately 30% of our common stock. As a result, Mr. Wilson is able to influence or control matters requiring approval by our stockholders, including the election of directors and the approval of mergers, acquisitions or other extraordinary transactions. This concentration of ownership may have various effects including, but not limited to, delaying, preventing or deterring a change of control of our company.

Anti-takeover provisions of Delaware law and our certificate of incorporation and bylaws could delay and discourage takeover attempts that stockholders may consider to be favorable.

Certain provisions of our certificate of incorporation and bylaws and applicable provisions of the Delaware General Corporation Law may make it more difficult or impossible for a third-party to acquire control of us or effect a change in our board of directors and management. These provisions include:

| • | the classification of our board of directors into three classes, with one class elected each year; |

| • | prohibiting cumulative voting in the election of directors; |

| • | the ability of our board of directors to issue preferred stock without stockholder approval; |

| • | the ability to remove a director only for cause and only with the vote of the holders of at least 66 2/3% of our voting stock; |

| • | a special meeting of stockholders may only be called by our chairman or Chief Executive Officer, or upon a resolution adopted by an affirmative vote of a majority of the board of directors, and not by our stockholders; |

| • | prohibiting stockholder action by written consent; and |

| • | our stockholders must comply with advance notice procedures in order to nominate candidates for election to our board of directors or to place stockholder proposals on the agenda for consideration at any meeting of our stockholders. |

In addition, we are governed by Section 203 of the Delaware General Corporation Law which, subject to some specified exceptions, prohibits “business combinations” between a Delaware corporation and an “interested stockholder,” which is generally defined as a stockholder who becomes a beneficial owner of 15% or more of a Delaware corporation’s voting stock, for a three-year period following the date that the stockholder became an interested stockholder. Section 203 could have the effect of delaying, deferring or preventing a change in control that our stockholders might consider to be in their best interests.

| ITEM 2. | PROPERTIES |

Our principal executive and administrative offices are located at 1818 Cornwall Avenue, Vancouver, British Columbia, Canada, V6J 1C7. We expect that our current administrative offices are sufficient for our expansion plans for the foreseeable future. In March 2011, we purchased the building that currently houses our administrative offices. We currently operate three distribution centers located in Vancouver, British Columbia, Sumner, Washington, and Melbourne, Victoria which together are capable of accommodating our expansion plans through the foreseeable future.

18

Table of Contents

The general location, use, approximate size and lease renewal date of our properties at January 29, 2012, are set forth below:

| Location |

Use | Approximate Square Feet |

Lease Renewal Date | |||||

| Sumner, WA |

Distribution Center | 167,000 | April 2020 | |||||

| Vancouver, BC |

Distribution Center | 120,000 | November 2017 | |||||

| Vancouver, BC |

Executive and Administrative Offices | 78,000 | n/a | |||||

| Melbourne, VIC |

Distribution Center | 54,000 | September 2016 | |||||

| Melbourne, VIC |

Executive and Administrative Offices | 19,000 | September 2013 | |||||

As of January 29, 2012, we leased approximately 494,000 gross square feet relating to our 174 corporate-owned stores. Our leases generally have initial terms of between five and 10 years, and generally can be extended only in five-year increments, if at all. All of our leases require a fixed annual rent, and most require the payment of additional rent if store sales exceed a negotiated amount. Generally, our leases are “net” leases, which require us to pay all of the cost of insurance, taxes, maintenance and utilities. We generally cannot cancel these leases at our option.

| ITEM 3. | LEGAL PROCEEDINGS |

We are a party to various legal proceedings arising in the ordinary course of our business, but we are not currently a party to any legal proceeding that management believes would have a material adverse effect on our consolidated financial position or results of operations.

19

Table of Contents

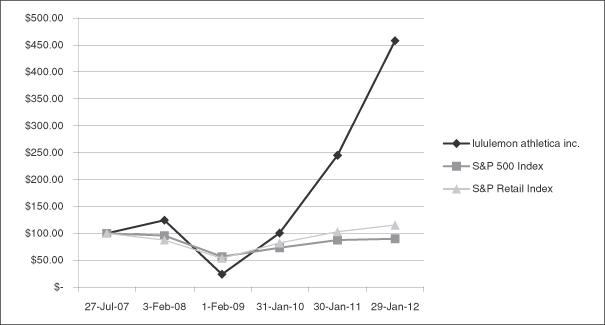

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Market Information and Dividends