U.S. SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

þ Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

for the fiscal year ended December 30, 2018

or

¨ Transition Report Under Section 13 or 15(d) of the Securities Exchange Act of 1934

Commission File No. 000-53577

DIVERSIFIED RESTAURANT HOLDINGS, INC.

(Exact name of registrant as specified in its charter)

Nevada | 03-0606420 | |

(State or other jurisdiction of incorporation | (I.R.S. Employer Identification No.) | |

or organization) | ||

27680 Franklin Rd., Southfield, MI 48034

(833) 374-7282

(Address, including zip code and telephone number, including area code, of Registrant’s principal executive offices)

Securities registered pursuant to Section 12(b) of the Exchange Act:

None

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, $.0001 par value per share

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer☐ | Accelerated filer ☐ | Non-accelerated filer þ | Smaller reporting company þ |

Emerging growth company ☐ | |||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No þ

The aggregate market value of the Registrant’s voting common stock held by non-affiliates was $17.1 million based on the per share closing price of the Company's common stock as reported on the NASDAQ stock market on June 29, 2018.

The number of shares outstanding of the registrant's common stock as of March 29, 2019 was 33,182,875 shares.

DOCUMENTS INCORPORATED BY REFERENCE:

None.

TABLE OF CONTENTS

Page | |

3

PART I

When used in this Form 10-K, the “Company” and “DRH” refers to Diversified Restaurant Holdings, Inc. and, depending on the context, could also be used to refer generally to the Company and its subsidiaries, which are described below.

Cautionary Statement Regarding Forward-Looking Information

Some of the statements in the sections entitled “Business,” and “Risk Factors,” and statements made elsewhere in this Form 10-K may constitute forward-looking statements. These statements reflect the current views of our senior management team with respect to future events, including our financial performance, business, and industry in general. Statements that include the words “expect,” “intend,” “plan,” “believe,” “project,” “forecast,” “estimate,” “may,” “should,” “anticipate” and similar statements of a future or forward-looking nature identify forward-looking statements for purposes of the federal securities laws or otherwise.

Forward-looking statements address matters that involve risks and uncertainties. Accordingly, there are or will be important factors that could cause our actual results to differ materially from those indicated in these statements. We believe that these factors include, but are not limited to, the following:

● | the success of our existing and new restaurants; |

● | our ability to obtain debt or other financing on favorable terms, or at all; |

● | our ability to identify appropriate sites and to finance the development and expansion of our operations; |

● | changes in economic conditions; |

● | damage to our reputation or lack of acceptance of our brand in existing or new markets; |

● | economic and other trends and developments, including adverse weather conditions, in the local or regional areas in which our restaurants are located; |

● | the impact of negative economic factors, including the availability of credit, on our landlords and surrounding tenants; |

● | changes in food availability and costs; |

● | labor shortages and increases in our compensation costs, including, as a result, changes in government regulation; |

● | increased competition in the restaurant industry and the segments in which we compete; |

● | the impact of legislation and regulations regarding nutritional information, new information or attitudes regarding diet and health, or adverse opinions about the health of consuming our menu offerings; |

● | the impact of federal, state, and local beer, liquor, and food service regulations; |

● | the success of our and our franchisor's marketing programs; |

● | the impact of new restaurant openings, including the effect on our existing restaurants of opening new restaurants in the same markets; |

● | the loss of key members of our management team; |

● | inability or failure to effectively manage our growth, including without limitation, our need for liquidity and human capital; |

● | the impact of litigation; |

● | the adequacy of our insurance coverage and fluctuating insurance requirements and costs; |

● | the impact of our indebtedness on our ability to invest in the ongoing needs of our business; |

4

● | the impact of a potential asset impairment charge in the future; |

● | the impact of any security breaches of confidential guest information in connection with our electronic processing of credit/debit card transactions; |

● | our ability to protect our intellectual property; |

● | the impact of any failure of our information technology system or any breach of our network security; |

● | the impact of any materially adverse changes in our federal, state, and local taxes; |

● | the impact of any food-borne illness outbreak; |

● | our ability to maintain our relationship with our franchisor on economically favorable terms; |

● | the impact of future sales of our common stock in the public market, the exercise of stock options, and any additional capital raised by us through the sale of our common stock; |

● | the effect of changes in accounting principles applicable to us; and |

● | the impact on the Company's future results as a result of its guarantees of certain leases of Bagger Dave's Burger Tavern, Inc. |

The foregoing factors should not be construed as exhaustive and should be read together with the other cautionary statements included in this Form 10-K. If one or more of these or other risks or uncertainties materialize, or if our underlying assumptions prove to be incorrect, actual results may differ materially from what we anticipate. Any forward-looking statements you read in this Form 10-K reflect our views as of the date of this Form 10-K with respect to future events and are subject to these and other risks, uncertainties, and assumptions relating to our operations, results of operations, growth strategy, and liquidity. You should carefully consider all of the factors identified in this Form 10-K that could cause actual results to differ. Investors are cautioned that all forward-looking statements involve risk and uncertainties and speak only as of the date on which they were made, and we do not undertake any obligation to update any forward-looking statement.

5

ITEM 1. BUSINESS

Business Overview

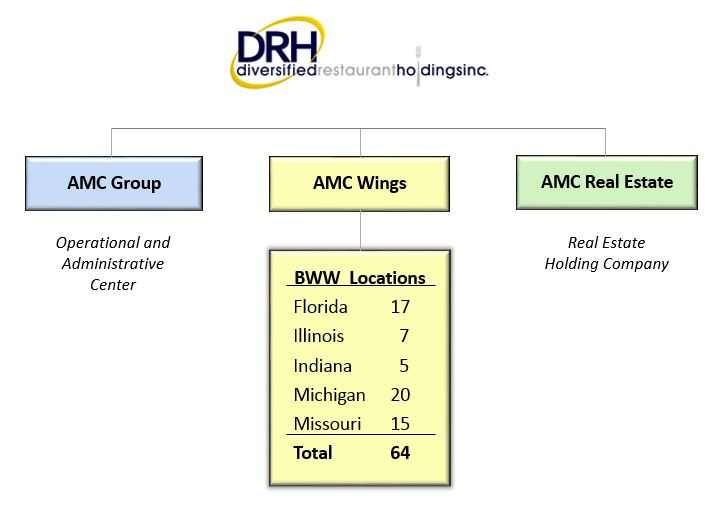

DRH is a restaurant company operating a single concept, Buffalo Wild Wings® (“BWW”). As one of the largest franchisees of BWW, we provide a unique guest experience in a casual and inviting environment. We were incorporated in 2006 and are headquartered in the Detroit metropolitan area. As of December 30, 2018, we owned 64 restaurants in Florida, Illinois, Indiana, Michigan and Missouri, including the nation’s largest BWW, based on square footage, in downtown Detroit, Michigan.

In 2008, DRH became publicly-owned by completing a self-underwritten initial public offering for $735,000 and 140,000 shares. We subsequently completed underwritten, follow-on offerings on April 23, 2013 of 6.9 million shares with net proceeds of $31.9 million and on July 24, 2018 of 5.3 million shares with net proceeds of $4.6 million.

DRH and its wholly-owned subsidiaries AMC Group, Inc. (“AMC”), AMC Wings, Inc. ("WINGS”), and AMC Real Estate, Inc. (“REAL ESTATE”and collectively, the "Company") own and operate BWW restaurants.

DRH is continually recognized as a leading franchisee in the BWW system. In 2018, our restaurants claimed 8 out of 15 Grand Prix awards, recognizing the top 15 operators in the franchise system. In 2017 and 2016, three and four of the Company's restaurants, respectively, were recognized as Blazin' 25 restaurants, which rewarded the top performing 25 franchise restaurants in the system. In both 2015 and 2014 we were recognized as Franchisee of the Year. Additionally, in 2016 our Chief Operating Officer was awarded the Franchise Advisory Council Excellence Award and in 2014 he received the Founders' Award.

6

The following organizational chart outlines the current corporate structure of DRH. A brief description of the entities follows the organizational chart. DRH is incorporated in Nevada.

AMC was formed on March 28, 2007, and serves as our operational and administrative center. AMC renders management, operational support, and advertising services to WINGS, REAL ESTATE and their subsidiaries. Services rendered by AMC include marketing, restaurant operations, restaurant management consultation, hiring and training of management and staff, and other management services required in the ordinary course of restaurant operations.

WINGS was formed on March 12, 2007, and serves as a holding company for our restaurants. We are economically dependent on retaining our franchise rights with BWW. The franchise agreements have specific initial term expiration dates ranging from December 2020 through June 2037. The franchise agreements are renewable at the option of the franchisor and are generally renewable if the franchisee has complied with the terms of the franchise agreement. When factoring in any applicable renewals, the franchise agreements have specific expiration dates ranging from December 2025 through June 2052. We believe we are in substantial compliance with the terms of these agreements.

REAL ESTATE was formed on March 18, 2013 and serves as the holding company for any real estate properties owned by DRH. Currently, DRH does not own any real estate.

Our headquarters are located at 27680 Franklin Road, Southfield, Michigan 48034. Our telephone number is (833) 374-7282. We can also be found on the Internet at www.diversifiedrestaurantholdings.com.

As of December 30, 2018, we had 2,549 employees of which 1,372 were full-time employees.

7

Background

Bagger Dave’s Spin-Off

On December 25, 2016, DRH completed a tax-free spin-off (the “Spin-Off”) of its Bagger Dave's business. Specifically, DRH contributed its 100.0% owned entity, AMC Burgers, LLC and certain real estate entities into Bagger Dave's Burger Tavern, Inc., a newly created Nevada corporation ("Bagger Dave's" or "Bagger"), which was then spun-off into a stand-alone, publicly-traded company on the over-the-counter exchange. In connection with the Spin-Off, DRH contributed to Bagger certain assets, liabilities, and employees related to its Bagger Dave's businesses. Intercompany balances due to/from DRH, which included amounts from sales, were contributed to equity. Additionally, DRH contributed $2 million in cash to Bagger to provide working capital for Bagger’s operations and remains a guarantor for certain of Bagger's lease obligations.

In conjunction with the Spin-Off, DRH entered into a transition services agreement (the "TSA") with Bagger Dave's pursuant to which DRH provided certain information technology and human resources support, limited accounting support, and other minor administrative functions at no charge. The TSA was intended to assist the discontinued component in efficiently and seamlessly transitioning to stand on its own. Certain provisions of the TSA terminated in December 2017 and the First Amendment to TSA (the "Amended TSA") was entered into effective January 1, 2018. Under the Amended TSA, DRH provides limited ongoing administrative support to Bagger in certain areas, including information technology, human resources and real estate, in exchange for a fee based on a rate-per-hour of service.

Restaurant Concept

With 64 BWW restaurants (20 in Michigan, 17 in Florida, 15 in Missouri, seven in Illinois and five in Indiana), including the nation’s largest BWW, based on square footage, in downtown Detroit, Michigan, DRH is one of the largest BWW franchisees. As of December 30, 2018, BWW reported over 1,270 restaurants worldwide that were either directly owned or franchised. The restaurants feature a variety of boldly-flavored, crave-able menu items, including Buffalo, New York-style chicken wings. BWW restaurants create a welcoming neighborhood atmosphere that includes an extensive multi-media system, a full bar and an open layout, which appeals to sports fans and families alike. The social environment created and the connections made with team members, guests and the local community help to differentiate BWW restaurants. Guests have the option of watching sporting events or other popular programs on various projector screens and televisions, competing in Buzztime ® Trivia or playing video games. The open layout of the restaurants offers dining and bar areas that provide distinct seating choices for sports fans and families. BWW restaurants offer flexibility and allow guests to customize their experience to meet their time demands, service preferences or the experience they are seeking for a workday lunch, a dine-in dinner, a take-out meal, an afternoon or evening enjoying a sporting event, or a late-night craving.

BWW restaurants have widespread appeal and have won dozens of “Best Wings” and “Best Sports Bar” awards across the country. The made-to-order menu items are enhanced by the bold flavor profile of 16 signature sauces and 5 signature seasonings, ranging from Sweet BBQ™ to Blazin’®. Restaurants offer 20 to 40 domestic and imported beers on tap, including craft brews, and a wide selection of bottled beers, wines, and liquor. The award-winning food and memorable experience drive guest visits and loyalty. For fiscal year 2018, our average BWW restaurant derived 83% of its revenue from food, including non-alcoholic beverages, and 17% of its revenue from alcohol sales, primarily draft beer.

Growth Strategy

We are focused on driving sales growth in all of our locations through the execution of local, traffic-driving marketing and advertising strategies, continued support of the community through sponsorship programs and local charities, and delivery of quality food, drinks and service, all in a clean and modern environment. One of our guiding principles is that a happy team member translates to a happy guest. A happy guest drives repeat sales and word-of-mouth referrals, which are two key factors that directly support our local marketing strategy.

We also strive to improve our margins through a number of initiatives, including enhanced methods to manage cost of sales and hourly labor with use of technology and improved application of standards, and working with our service vendors to leverage our scale and obtain higher value at more competitive prices.

We currently own 64 BWW restaurants in five states. We may open a limited number of new BWW locations in our core markets over the long term. However, as capital resources become available, our growth strategy is more likely to consist of disciplined, strategic acquisitions of existing BWW or other franchised restaurants from other operators or franchisors.

8

Since 2012 we have acquired 29 restaurants in several transactions and have developed a strong process to identify, evaluate and integrate acquisitions. We have been regularly recognized as one of the best operators in the BWW system, and we believe that we can apply our strong operating disciplines and management culture to acquired locations to achieve financial improvements and growth over the long term. On February 22, 2019 we entered into an Asset Purchase Agreement to acquire 9 BWW restaurants in the Chicago, Illinois market for a cash purchase price of approximately $22.5 million, subject to customary closing conditions. Upon completion of the transaction, since 2012, we will have acquired a total of 38 restaurants and will own and operate a total of 73 BWW restaurants. The transaction remains subject to the franchisor waiving its right of first refusal and franchisor consent, among other things. The transaction also remains contingent upon the Company's completion of satisfactory financing.

Restaurant Operations

We believe retaining talented and passionate restaurant managers and providing our team members with the tools, skills and motivation to deliver our goal of the ultimate social experience, represent two key elements to our success. In order to retain our unique culture, we devote substantial resources to identifying, selecting, and training our restaurant-level team members. We typically have six in-restaurant trainers at each location who provide both front- and back-of-house training on site. We also have a seven-week training program for our restaurant managers, which consists of an average of four weeks of restaurant training and three weeks of cultural training. During this training, managers observe and have the opportunity to participate in our established restaurants’ operations and guest interactions. We believe our focus on guest-centric training is a core strength of our Company and reinforces our mission to delight our guests.

Management and Staffing

The core values that define our culture are to be guest driven, team focused, community connected and dedicated to excellence. Our restaurants are generally staffed with one managing partner and up to five additional managers, depending on the sales volume of the restaurant. The managing partner is responsible for day-to-day operations and for maintaining the standards of quality and performance that define our corporate culture. We use regional directors to oversee our managing partners and supervise the operation of our restaurants, including the continuing development of each restaurant’s management team. Through regular visits to the restaurants and constant communication with the management team, the regional directors ensure adherence to all aspects of our concept, strategy and standards of quality.

Training, Development, and Recruiting

We believe that successful restaurant operations, guest satisfaction, quality, and cleanliness begin with the team member - a key component of our strategy. Our training program, the Hospitality Excellence Academy ("HEA"), is a well-organized, thorough, hands-on training program designed to foster our culture of excellence by cultivating the leaders of tomorrow. We are also in the process of implementing a new learning management system which is expected to represent another step forward by introducing a fully digital platform.

We offer an incentive program that we believe is very competitive in the restaurant industry. In addition to competitive base salaries and benefits, management is incentivized with a performance-based bonus program. Our benefit offerings include group health, dental, and vision insurance, a company-sponsored Safe Harbor 401(k) plan with a non-discretionary company match, a tuition reimbursement program, a referral bonus program and opportunities for career advancement. We emphasize growth from within the organization, giving our team members the opportunity to develop and advance. We believe this philosophy helps build a strong, loyal management team with high team member retention rates, giving us an advantage over our competitors.

Restaurants

Our restaurants range in size from 5,300 to 13,500 square feet, with an average of about 6,400 square feet. We anticipate that future restaurants will range in size from 4,800 to 5,500 square feet with an average cash investment per restaurant ranging from approximately $1.7 million to $2.6 million for a leased site. From time to time, our restaurants may be smaller or larger or cost more or less than our targeted range, depending on the particular circumstances of the selected site. Also, from time to time, we may elect to purchase either the building or the land and the building for certain restaurants, which would require additional capital.

We have a continuous capital improvement plan for our restaurants and generally plan major renovations every seven to ten years. For a more detailed discussion of our capital improvement plans, see the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and specifically, the subsection entitled “Liquidity and Capital Resources; Acquisition and Expansion Plans.”

9

Quality Control and Purchasing

We strive to maintain high quality standards, protecting our food supply at all times. Purchasing for our restaurants is primarily through channels established by BWW corporate operations. We do, however, negotiate directly with many of these channels regarding price and delivery terms. When we purchase directly, we seek to obtain the highest quality ingredients, products, and supplies from reliable sources at competitive prices. To maximize our purchasing efficiencies, our corporate staff negotiates, when available, fixed-price contracts (usually for a one-year period) or, where appropriate, contracts based on commodity indexes.

Marketing and Advertising

We are required to pay an advertising fee to BWW equal to 3.00% - 3.15% of total net sales (the "National Ad Fund fee"), which supports national advertising designed to build brand awareness and drive traffic to our restaurants. Some examples include television commercials on major networks, particularly during certain regional and national key games for the NFL, NHL, MLB, NBA, NCAA football, NCAA basketball and the March Madness NCAA basketball tournament. In addition, we invest 0.25% - 0.5% of certain regional net sales in cooperatives of BWW restaurants for two metropolitan areas. We currently have co-ops for the Detroit, MI and Chicago, IL markets where we engage in coordinated local restaurant marketing efforts with other BWW restaurants.

In addition to the National Ad Fund fee, in fiscal year 2018, we spent approximately 1% of total net sales on local marketing efforts (including co-ops), before rebates. This includes charitable donations and local community sponsorships, which help develop local public relations and are a major component of our marketing efforts. We support programs that build traffic at the grass-roots level. We also participate in numerous local restaurant marketing events throughout the communities we serve.

Information Systems and Technology

Enhancing the security of our financial data and other personal information remains a high priority for us. We continue to innovate and modernize our technology infrastructure to provide improved efficiency, control and security. Our ability to accept credit cards as payment in our restaurants and for online orders depends on us remaining compliant with standards set by the Payment Card Industry Security Standards Council (“PCI”). The PCI standards include compliance guidelines and standards with regard to our security surrounding the physical and electronic storage, processing and transmission of individual cardholder data. We maintain security measures that are designed to protect and prevent unauthorized access to such information. We continue to assess new payment standards and have implemented EMV chip enabled devices to ensure the most secure interface available for in-restaurant transactions. We have also implemented a CCV-code requirement for online purchases.

We also believe that technology can provide a competitive advantage and enable our strategy for growth through efficient restaurant operations, information analysis and ease and speed of guest service. We have a standard point-of-sale system in our restaurants that is integrated to our corporate office through a web-based, above-store business intelligence reporting and analysis tool. Our systems are designed to improve operating efficiencies, enable rapid analysis of marketing and financial information and improve administrative productivity. We also integrated the online ordering function and leverage third-party vendors which allow guests to select the music played throughout the restaurant using their mobile devices. In-restaurant tablets have also been introduced to enhance the guest experience through arcade games, some of which are free and some of which are available for purchase. In 2018 we implemented a new operations execution technology platform to enforce compliance and streamline performance across our restaurants. Additionally, in 2017 we completed the roll-out of the BWW loyalty program, Blazin' Rewards®, which is a mobile-based loyalty program.

We are constantly assessing new technologies to improve operations, back-office processes and overall guest experience. This includes the implementation of mobile payment options, advanced programming of kitchen display units, tablet-based wait-listing applications, integration with delivery service providers, and server tablet ordering functionality.

Competition

The restaurant industry is highly competitive. We believe we compete primarily with local and regional sports bars and national casual dining and quick-casual establishments. Competition is expected to remain intense with respect to price, service, location, concept and type and quality of food. There is also competition for real estate sites, qualified management personnel and hourly restaurant staff. Many of our competitors have been in existence longer than we have and may be better established in markets where we are currently located or may, in the future, be located. Accordingly, we strive to continually improve our restaurants, maintain high quality standards and treat our guests in a manner that encourages them to return. We believe our pricing communicates value to guests in a comfortable, welcoming, full service atmosphere.

10

Trademarks, Service Marks, and Trade Secrets

The BWW registered service mark is owned by Buffalo Wild Wings, International, Inc.

Government Regulations

The restaurant industry is subject to numerous federal, state, and local governmental regulations, including those relating to the preparation and sale of food and alcoholic beverages, sanitation, public health, nutrition labeling requirements, fire codes, zoning, and building requirements and to periodic review by state and municipal authorities for areas in which the restaurants are located. Each restaurant requires appropriate licenses from regulatory authorities allowing it to sell beer, wine and liquor and each restaurant requires food service licenses from local health authorities. The majority of our licenses to sell alcoholic beverages must be renewed annually and may be suspended or revoked at any time for cause, including violation by us or our team members of any law or regulation pertaining to alcoholic beverage control, such as those regulating the minimum age of team members or patrons who may serve or be served alcoholic beverages, the serving of alcoholic beverages to visibly intoxicated patrons, advertising, wholesale purchasing and inventory control. In order to reduce this risk, restaurant team members are trained in standardized operating procedures designed to assure compliance with all applicable codes and regulations. We have not encountered any material problems relating to alcoholic beverage licenses or permits to date.

We are also subject to laws governing our relationship with team members. Our failure to comply with federal, state and local employment laws and regulations may subject us to losses and harm our brand. The laws and regulations govern such matters as: workers’ compensation insurance; wage and hour requirements; unemployment and other taxes; working and safety conditions; overtime; and citizenship and immigration status. Significant additional government-imposed regulations under the Fair Labor Standards Act and similar laws related to minimum wages, overtime, rest breaks, paid leaves of absence, and mandated health benefits may also impact the performance of our operations. In addition, team member claims based on, among other things, discrimination, harassment, wrongful termination, wages, hour requirements and payments to team members who receive gratuities, may divert financial and management resources and adversely affect operations. The losses that may be incurred as a result of any violation of such governmental regulations by the Company are difficult to quantify. To our knowledge, we are in compliance in all material respects with all applicable federal, state and local laws affecting our business.

The federal Patient Protection and Affordable Care Act (the "ACA") applies to our business. Under the ACA, we are required to provide full-time employees with medical insurance that meets minimum value and affordability standards. We are also required to provide covered employees and the Internal Revenue Service with specific reportable benefit information. The Company’s medical plans have been offered to all full-time employees and meet the minimum value and affordability requirements of the ACA, and the Company has complied with the informational reporting requirements of the ACA.

Compliance with these laws and regulations may lead to increased costs and operational complexity and may increase our exposure to governmental investigations or litigation. We may also be subject, in certain states, to “dram shop” statutes, which generally allow a person injured by an intoxicated person to recover damages from an establishment that wrongfully served alcoholic beverages to the intoxicated person. We carry liquor liability coverage as part of our existing comprehensive general liability insurance which we believe is consistent with coverage carried by other companies in the restaurant industry of similar size and scope of operations. Even though we carry liquor liability insurance, a judgment against us under a “dram shop” statute in excess of our liability coverage could have a material adverse effect on our business, financial condition and results of operations.

11

ITEM 1A. RISK FACTORS

Risks Related to Our Business and Industry

Our Independent Auditors Have Expressed Substantial Doubt About Our Ability to Continue as a Going Concern.

In the audit opinion for our consolidated financial statements as of and for the year ended December 30, 2018, BDO USA, LLP, our independent auditors, included an explanatory emphasis of matter paragraph expressing substantial doubt about the Company’s ability to continue as a going concern. As further discussed in Note 1 and Note 7 to our consolidated financial statements, the Company has approximately $102.4 million of debt outstanding under its $155.0 million senior secured credit facility with a syndicate of lenders led by Citizens (the “Credit Facility”) with a maturity date of June 29, 2020. The Credit Facility contains various customary financial covenants generally based on the earnings of the Company relative to its debt. The financial covenants consist of a quarterly minimum required debt service coverage ratio (the "DSCR") and a maximum permitted lease adjusted leverage ratio (the "LALR").

As of December 30, 2018 the Company was in compliance with its loan covenants. However, beginning in the third quarter of 2019, the Company is currently forecasting that it may not be in compliance with these financial covenants.

While the Company has successfully negotiated financial covenant amendments in the past and would seek to do so again should it be in default or near a default, there can be no assurance that it will be successful in obtaining a satisfactory amendment.

As a result of this uncertainty coupled with the June 2020 maturity of the Credit Facility, the Company has been in discussions with its current lenders and other sources of capital regarding a possible refinancing and/or replacement of the Credit Facility. The Company is also exploring various other alternatives, including, among other things, possible equity financing. There can be no assurance, however, that any such efforts will be successful.

Until such time as the Company has executed an agreement to amend, refinance or replace the Credit Facility, the Company cannot conclude that it is probable that it will do so, and accordingly, this raises substantial doubt about the Company’s ability to continue as a going concern.

However, our financial statements have been prepared assuming the Company will continue to operate as a going concern, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. Our financial statements do not include adjustments that might result from the outcome of this uncertainty, including any adjustments to reflect the possible future effects of the recoverability and classification of recorded asset amounts or amounts and classifications of liabilities that might be necessary should the Company be unable to continue as a going concern.

Our Financial Results Depend Significantly Upon the Success of Our Existing and New Restaurants

Our ability to maintain and grow our revenue and profits will depend on our ability to successfully drive sales volumes and efficiently manage costs in our existing and new restaurants. Currently, we have 64 BWW restaurants. The results achieved by our current restaurants may not be indicative of longer-term performance or the potential market acceptance of our restaurant concept in other locations.

12

The success of our restaurants depends principally upon generating and maintaining guest traffic, loyalty and achieving positive margins. Significant factors that might adversely affect guest traffic, loyalty and profit margins include:

● | economic conditions, including housing market downturns, rising unemployment rates, lower disposable income, adverse credit conditions, rising fuel prices and decreasing consumer confidence and other events or factors that adversely affect consumer spending in the markets we serve; |

● | competition in the restaurant industry, particularly in the casual and fast-casual dining segments; |

● | changes in consumer preferences; |

● | our guests’ failure to accept menu price increases that we may make to offset increases in certain operating costs; |

● | our reputation and consumer perception of our concepts’ offerings in terms of quality, price, value, ambiance and service; and |

● | our guests’ personal experiences from dining in our restaurants. |

Our restaurants are also susceptible to increases in certain key operating expenses that are either wholly or partially beyond our control, including:

● | food and other raw materials costs, many of which we cannot predict or effectively hedge against; |

● | compensation costs, including wage, workers’ compensation, health care and other benefits expenses; |

● | rent expenses and construction, remodeling, maintenance and other costs under leases for our new and existing restaurants; |

● | compliance costs as a result of changes in regulatory or industry standards; |

● | energy, water and other utility costs; |

● | costs for insurance (including health, liability and workers’ compensation); |

● | information technology and other logistical costs; and |

● | expenses due to litigation against us. |

Competition in the Restaurant Industry May Affect Our Ability to Compete Effectively

The restaurant industry is intensely competitive. We believe we compete primarily with regional and local sports bars, casual dining concepts, and fast-casual establishments. Many of our direct and indirect competitors are well-established national, regional or local chains with a greater market presence than us. Further, some competitors have substantially greater financial, marketing and other resources than us. In addition, independent owners of local or regional establishments may enter the wing-based restaurant business without significant barriers to entry and such establishments may provide price competition for our restaurants. Competition in the casual dining, fast-casual and quick-service segments of the restaurant industry is expected to remain intense with respect to price, service, location, concept and the type and quality of food. We also face intense competition for real estate sites, qualified management personnel and hourly restaurant staff.

Our Ability to Raise Capital in the Future May Be Limited, Which Could Adversely Impact Our Business

Changes in our restaurant operations, lower than anticipated restaurant sales, increased food or compensation costs, increased property expenses, acceleration of our expansion plans or other events, including those described in this Annual Report, may cause us to seek additional debt or equity financing on an accelerated basis. Financing may not be available to us on acceptable terms, and our failure to raise capital when needed could negatively impact our ability to service our debt, our restaurant growth plans as well as our financial condition and the results of our operations. Additional equity financing, if available, may be dilutive to the holders of our common stock. Debt financing may involve significant cash payment obligations, covenants and financial ratios that may restrict our ability to operate and grow our business, if available at all.

13

There Can Be No Assurances That, in the Future, We Will Be in Compliance With All Covenants of Our Current or Future Debt Agreements or That Our Lenders Will Waive Any Violations of Such Covenants

Non-compliance with our debt covenants could have a material adverse effect on our business, results of operations, and financial condition. Non-compliance may result in us being in default under our debt agreements, which could cause a substantial financial burden by requiring us to repay our debt earlier than otherwise anticipated.

Actions by Our Franchisor Could Negatively Affect Our Business and Operating Results

We are economically dependent on retaining our franchise rights with BWW. Our restaurant operations depend, in part, on decisions made by our franchisor, including changes of distributors, food menu items and prices, policies and procedures, and advertising programs. Business decisions made by BWW could adversely impact our business, financial condition or results of operations.

Poor Operating Results at Any of Our Restaurants Could Cause us to Cease Operations Regardless of Ongoing Lease and Franchise Agreement Obligations

Factors such as intense competition, difficult labor market conditions and low levels of guest traffic could cause us to cease operations at any of our BWW restaurants. From time to time, we have elected to close underperforming restaurants, and may elect to do so in the future regardless of ongoing lease or franchise agreement terms. In the past we have experienced, and may in the future experience, reduced sales as a result of restaurant closures and could have ongoing liabilities beyond the date of the closure.

Our Success Depends Substantially on the Value of the BWW Brand and Unfavorable Publicity Could Harm Our Business

Multi-unit restaurant businesses such as ours can be adversely affected by publicity resulting from complaints, litigation or general publicity regarding poor food quality, food-borne illness, personal injury, food tampering, adverse health effects of consumption of various food products or high-calorie foods (including obesity) or other concerns. Negative publicity of the BWW brand from traditional media or online social network postings may also result from actual or alleged incidents or events taking place in our restaurants or any BWW restaurant not owned by us.

There has been a marked increase in the use of social media platforms, including weblogs (blogs), social media websites, and other forms of Internet-based communications which allow individuals access to a broad audience of consumers and other interested persons. Consumers value readily available information concerning goods and services that they have or plan to purchase, and may act on such information without further investigation or authentication. The availability of information on social media platforms is virtually immediate, as is its impact. Many social media platforms immediately publish the content their subscribers and participants post, often without filters or checks on accuracy of the content posted. The opportunity for dissemination of any sort of information or media, including inaccurate and prospectively harmful materials, is practically limitless and the technology through which such opportunities are afforded is ubiquitous. Information concerning our Company may be posted on such platforms at any time. Information posted may be adverse to our interests or may be inaccurate, each of which may harm our performance, prospects or business. The harm may be immediate without affording us an opportunity for redress or correction. Such platforms also could be used for dissemination of trade secret information, compromising valuable company assets. In summary, the dissemination of information online could harm our business, prospects, financial condition and results of operations, regardless of the information’s accuracy.

Regardless of whether any public allegations or complaints are valid, unfavorable publicity relating to any BWW restaurant, whether owned by us or not, could adversely affect public perception of the entire brand. Adverse publicity and its effect on overall consumer perceptions of food safety, or our failure to respond effectively to adverse publicity, could have a material adverse effect on our business, financial condition or results of operations. We must protect and grow the value of our brand to continue to be successful in the future. Any incident that erodes consumer trust in or affinity for our brand could significantly reduce the value. If consumers perceive or experience a reduction in food quality, service and ambiance or in any way believe we failed to deliver a consistently positive experience, the value of our brand could suffer.

We May Not Be Able to Attract and Retain Qualified Team Members to Operate and Manage Our Restaurants

The success of our restaurants depends on our ability to attract, motivate, develop and retain a sufficient number of qualified restaurant team members, including managers and hourly team members. The inability to recruit, develop and retain these individuals may delay the planned openings of new restaurants or result in high team member turnover in existing restaurants, thus increasing the cost to efficiently operate our restaurants. This could inhibit our expansion strategy and business performance and negatively impact our operating results.

14

Fluctuations in the Cost of Food Could Impact Operating Results

Our primary food products are fresh bone-in chicken wings, frozen boneless chicken and potatoes. Our food, beverage and packaging costs could be significantly affected by increases in the cost of fresh chicken wings, which can result from a number of factors, including but not limited to, seasonality, cost of corn and grain, animal disease, drought and other weather phenomena, increase in demand domestically and internationally, and other factors that may affect availability. Additionally, if there is a significant rise in the price of chicken wings, and we are unable to successfully adjust menu prices or menu mix or otherwise make operational adjustments to account for the higher wing prices, our operating results could be adversely affected. We also depend on our franchisor, BWW, as it relates to chicken wings, to negotiate prices and deliver product to us at a competitive cost. BWW currently sources, negotiates and secures fresh bone-in chicken wings for its franchisees.

Shortages or Interruptions in the Availability and Delivery of Food and Other Supplies May Increase Costs or Reduce Revenue

Possible shortages or interruptions in the supply of food items and other supplies to our restaurants caused by inclement weather, terrorist attacks, natural disasters such as floods, drought, and hurricanes, pandemics, the inability of our vendors to obtain credit in a tightened credit market, food safety warnings or advisories, or the prospect of such pronouncements or other conditions beyond our control, could adversely affect the availability, quality and cost of items we buy and the operations of our restaurants. Our inability to effectively manage supply chain risk could increase our costs and limit the availability of products critical to our restaurant operations.

We May Face Guaranty Obligations or Other Potential Liabilities in Connection With the Spin-Off of Bagger Dave's

Following the Bagger Dave's Spin-Off, we continue to provide lease guaranties and certain transition services to Bagger. We remain as a guarantor on 10 lease agreements as of December 30, 2018, 3 of which now relate to an unaffiliated party which has taken over the Bagger Dave's lease. In the event Bagger Dave's or the unaffiliated party were unable to meet their lease obligations, we could be required to make the lease payments or suffer other financial liability. The maximum exposure from lease guarantees is approximately $7.3 million. These or other liabilities and costs that may be incurred in connection with the Spin-Off, may exceed our estimates and could have an adverse impact on our business, financial condition and results of operations.

Board Overlap with Bagger Dave's May Give Rise to Conflicts of Interest

Our Executive Chairman currently serves on Bagger Dave's board of directors. Our Executive Chairman is also the Chairman of the Board, Chief Executive Officer and President of Bagger Dave's. We have certain business dealings with Bagger Dave's, including a sublease, a transition services agreement and lease guarantees. We may also have business dealings that extend beyond separation matters. In certain locations, our restaurants are located adjacent to or near a Bagger Dave's restaurant and may compete for guests. While we have procedures in place to consider related party transactions through independent committee members of our board, the overlap in directors with Bagger Dave's may give rise to conflicts of interest.

Increases in Our Compensation Costs, Including as a Result of Changes in Government Regulation, Could Slow Our Growth or Harm Our Business

We are subject to a wide range of compensation costs. Because our compensation costs are, as a percentage of revenue, higher than other industries, we may be significantly harmed by compensation cost increases. Unfavorable fluctuations in market conditions, availability of insurance, or changes in state and/or federal regulations could significantly increase our insurance premiums. In addition, we are subject to the risk of employment-related litigation at both the state and federal levels, including claims styled as class action lawsuits, which are costlier to defend. Also, some employment-related claims in the area of wage and hour disputes are not insurable risks.

Significant increases in health care costs may also continue to occur, and we can provide no assurance that we will be able to effectively contain those costs.

In addition, many of our restaurant personnel are hourly team members subject to various minimum wage requirements or changes to existing tip credit laws. Mandated increases in minimum wage levels and changes to the tip credit laws, which dictate the amounts an employer is permitted to assume a team member receives in tips when calculating the team member’s hourly wage for minimum wage compliance purposes, have recently been and continue to be proposed and implemented at both federal and state government levels. Continued minimum wage increases or changes to allowable tip credits may further increase our compensation costs or effective tax rate.

15

Various states in which we operate are considering or have already adopted new immigration laws, and the U.S. Congress and Department of Homeland Security from time to time consider or implement changes to federal immigration laws, regulations, or enforcement programs as well. Some of these changes may increase our obligations for compliance and oversight, which could subject us to additional costs and make our hiring process cumbersome or reduce the availability of potential team members. Although we require all team members to provide us with government-specified documentation evidencing their employment eligibility, some of our team members may, without our knowledge, be unauthorized team members. Unauthorized team members are subject to deportation and may subject us to fines or penalties, and if any of our team members are found to be unauthorized, we could experience adverse publicity that negatively impacts our brand and may make it more difficult to hire and keep qualified team members. Termination of a significant number of team members that, unbeknownst to us, were unauthorized team members may disrupt our operations, cause temporary increases in our compensation costs as we train new team members and result in additional adverse publicity. Our financial performance could be materially harmed as a result of any of these factors.

Changes in Public Health Concerns and Legislation and Regulations Requiring the Provision of Nutritional Information May Impact Our Performance

Government regulation and consumer eating habits may impact our business as a result of changes in attitudes regarding diet and health or new information regarding the health effects of consuming our menu offerings. These changes have resulted in, and may continue to result in, the enactment of laws and regulations that impact the ingredients and nutritional content of our menu offerings, or laws and regulations requiring us to disclose the nutritional content of our food offerings. For example, a number of states, counties and cities have enacted menu labeling laws requiring multi-unit restaurant operators to disclose certain nutritional information available to guests or have enacted legislation restricting the use of certain types of ingredients in restaurants. The ACA included nation-wide menu labeling and nutrition disclosure requirements as well, and our restaurants are now covered by these national requirements. The effect of such labeling requirements on consumer choices, if any, is unclear at this time. We cannot make any assurances regarding our ability to effectively respond to changes in consumer health perceptions and to adapt our menu offerings to trends in eating habits. The imposition of menu-labeling laws could have an adverse effect on our business, financial condition and results of operations, as well as the restaurant industry in general.

Multiple jurisdictions in which we operate could adopt recently enacted new requirements that require us to adopt and implement a Hazard Analysis and Critical Control Points (“HACCP”) system for managing food safety and quality. HACCP refers to a management system in which food safety is addressed through the analysis and control of potential hazards from production, procurement and handling, to manufacturing, distribution and consumption of the finished product. We expect to incur certain costs to comply with these regulations, and these costs may be more than we anticipate. Failure to comply with these laws or regulations could materially adversely affect our business, financial condition and results of operations.

Further, growing movements to change laws relating to alcohol may result in a decline in alcohol consumption at our restaurants or increase the number of "dram shop" claims made against us, either of which may negatively impact operations or result in the loss of liquor licenses.

A Regional or Global Health Pandemic Could Severely Affect Our Business

A health pandemic is a disease outbreak that spreads rapidly and widely by infection and affects many individuals in an area or population at the same time. If a regional or global health pandemic were to occur, depending upon its duration and severity, our business could be severely affected. We have positioned our brand as a place where people can gather together. Customers might avoid public gathering places in the event of a health pandemic, and local, regional or national governments might limit or ban public gatherings to halt or delay the spread of disease. A regional or global health pandemic might also adversely impact our business by disrupting or delaying production and delivery of materials and products in our supply chain and by causing staffing shortages in our restaurants. The impact of a health pandemic on us might be disproportionately greater than on other companies that depend less on the gathering of people together for the sale or use of their products and services.

16

Changes in Consumer Preferences or Discretionary Consumer Spending Could Harm Our Performance

Our success depends, in part, upon the continued popularity of our chicken wings, other food and beverage items and the appeal of our restaurant concept. We also depend on trends toward consumers eating away from home. Shifts in these consumer preferences could negatively affect our future profitability. Such shifts could be based on health concerns related to the cholesterol, carbohydrate, fat, calorie or salt content of certain food items, including items featured on our menu. Negative publicity over the health aspects of such food items may adversely affect consumer demand for our menu items and could result in a decrease in guest traffic to our restaurants, which could materially harm our business. In addition, our success depends, to a significant extent, on numerous factors affecting discretionary consumer spending, general economic conditions, disposable consumer income, and consumer confidence. A decline in consumer spending or in economic conditions could reduce guest traffic or impose practical limits on pricing, either of which could harm our business, financial condition and results of operations.

Our Operating Results May Fluctuate Due to the Timing of Special Events

Our operating results depend, in part, on special events, such as the Super Bowl® and other sporting events viewed by our guests in our restaurants, including those sponsored by the National Football League, Major League Baseball, National Basketball Association, National Hockey League and National Collegiate Athletic Association. Interruptions in the viewing of these professional sporting league events due to strikes or lockouts may impact our business, financial condition and results of operations. Additionally, our results are subject to fluctuations based on the dates of sporting events, their availability for viewing through broadcast, satellite, Internet and cable networks, and the level of participation in these events by teams that are relevant to the markets in which we operate. Historically, sales in most of our restaurants have been higher during fall and winter months based on the relative popularity and extent of national, regional and local sporting and other events in the geographic regions in which we currently operate.

We May Not Be Successful When Entering New Markets

When expanding the BWW concept or potentially acquiring other franchise concepts, we may enter new markets in which we may have limited or no operating experience. There can be no assurance that we will be able to achieve success and/or profitability in our new markets or in our new restaurants. The success of these new restaurants will be affected by the different competitive conditions, consumer taste, and discretionary spending patterns within the new markets, as well as by our ability to generate market awareness of the BWW brand, or other brands. New restaurants typically require several months of operation before achieving normal levels of profitability. When we enter highly competitive new markets or territories in which we have not yet established a market presence, the realization of our revenue targets and desired profit margins may be more susceptible to volatility and/or more prolonged than anticipated.

Higher-Than-Anticipated Costs Associated With the Opening of New Restaurants or With the Closing, Relocating, or Remodeling of Existing Restaurants May Adversely Affect Our Business, Financial Condition or Results of Operations

Our revenue and expenses may be significantly impacted by the location, number and timing of the opening of new restaurants and the closing, relocating and remodeling of existing restaurants. We incur substantial pre-opening expenses each time we open a new restaurant and will incur other expenses if we close, relocate or remodel existing restaurants. These expenses are generally higher when we open restaurants in new markets, but the costs of opening, closing, relocating or remodeling any of our restaurants may be higher than anticipated. An increase in such expenses could have an adverse effect on our results of operations.

17

Future Acquisitions May Have Unanticipated Consequences That Could Harm Our Business and Our Financial Condition

We may seek to selectively acquire existing BWW or other restaurant concepts as a franchisee, for example, our recent entrance into an Asset Purchase Agreement to acquire 9 BWW restaurants in the Chicago, Illinois market. To do so, we would need to identify suitable acquisition candidates, negotiate acceptable acquisition terms and obtain appropriate financing as needed. Any acquisitions we pursue, whether successfully completed or not, may involve risks, including:

● | material adverse effects on our operating results, particularly in the fiscal quarters immediately following the acquisition as the acquired restaurants are integrated into our operations; |

● | customary closing and indemnification risks associated with any acquisition; |

● | funds used pursuing acquisitions we are ultimately unable to consummate because the transaction is subject to a right of first refusal in favor of our franchisor, BWW; and |

● | diversion of management’s attention from other business concerns. |

Future acquisitions of existing restaurants, which may be accomplished through a cash purchase transaction, the issuance of our equity securities, or a combination of both, could result in potentially dilutive issuances of our equity securities, the incurrence of debt and contingent liabilities and impairment charges related to intangible assets, any of which could harm our business, financial condition and results of operations.

Our Inability to Renew Existing Leases or Enter Into New Leases For New or Relocated Restaurants on Favorable Terms May Adversely Affect Our Results of Operations

As of December 30, 2018, all of our restaurants are located on leased premises and are subject to varying lease-specific arrangements. For example, some of the leases require base rent that is subject to increase based on market factors, and other leases include base rent with specified periodic increases. Some leases are subject to renewals, which could involve substantial increases. Additionally, a few leases require contingent rent based on a percentage of gross sales. When our leases expire, we will evaluate the desirability of renewing such leases. While we currently expect to pursue all renewal options, no guarantee can be given that such leases will be renewed or, if renewed, that rents will not increase substantially. The success of our restaurants depends in large part on their leased locations. As demographic and economic patterns change, current leased locations may or may not continue to be attractive or profitable. Possible declines in trade areas where our restaurants are located or adverse economic conditions in surrounding areas could result in reduced revenue in those locations. In addition, desirable lease locations for new restaurant openings or for the relocation of existing restaurants may not be available at an acceptable cost when we identify a particular opportunity for a new restaurant or relocation.

Economic Conditions Could Have a Material Adverse Impact on Our Landlords in Retail Centers in Which We Are Located

Our landlords may be unable to obtain financing or remain in good standing under their existing financing arrangements, resulting in failures to pay required construction contributions or satisfy other lease covenants to us. If our landlords fail to satisfy required co-tenancies, such failures may result in us terminating leases or delaying openings in these locations. Also, decreases in total tenant occupancy in retail centers in which we are located may affect guest traffic at our restaurants. All of these factors could have a material adverse impact on our business, financial condition or results of operations.

A Decline in Visitors to Any of the Business Districts Near the Locations of Our Restaurants Could Negatively Affect Our Restaurant Sales

Some of our restaurants are located near high-activity areas such as retail centers, big-box shopping centers and entertainment centers. We depend on high visitor rates at these businesses to attract guests to our restaurants. If visitors to these centers decline due to economic conditions, closure of big-box retailers, road construction, changes in consumer preferences or shopping patterns, changes in discretionary consumer spending or otherwise, our restaurant sales in these areas could decline significantly and adversely affect our business, financial condition or results of operations.

18

Because Many of Our Restaurants are Concentrated in Local or Regional Areas, We are Susceptible to Economic and Other Trends and Developments, Including Adverse Weather Conditions, in These Areas

Our financial performance is highly dependent on restaurants located in Florida, Illinois, Indiana, Michigan, and Missouri. As a result, adverse economic conditions in any of these areas could have a material adverse effect on our overall results of operations. In addition, other regional occurrences such as local strikes, terrorist attacks, increases in energy prices, adverse weather conditions, hurricanes, droughts or other natural or man-made disasters have occurred. In particular, adverse weather conditions can impact guest traffic at our restaurants, cause the temporary underutilization of certain seating areas, and, in more severe cases, cause temporary restaurant closures, sometimes for prolonged periods. As of December 30, 2018, approximately 73.4% of our total restaurants are located in Illinois, Indiana, Michigan and Missouri, which are particularly susceptible to snowfall, and approximately 26.6% of our total restaurants are located in Florida, which is particularly susceptible to hurricanes.

Legal Actions Could Have an Adverse Effect on Us

We have faced in the past and could face in the future legal action from government agencies, team members, guests, or other parties. Many state and federal laws govern our industry, and if we fail to comply with these laws, we could be liable for damages or penalties. Further, we may face litigation from guests alleging that we were responsible for an illness or injury they suffered at or after a visit to our restaurants, or alleging that we are not complying with regulations governing our food quality or operations. We may also face employment-related litigation, including claims of age discrimination, sexual harassment, gender discrimination, immigration violations, or other local, state, and federal labor law violations. In light of the potential cost and uncertainty involved in litigation, we may settle matters even when we believe we have a meritorious defense. Litigation and its related costs may have a material adverse effect on our business, financial condition or results of operations.

We May Not Be Able to Obtain and Maintain Licenses and Permits Necessary to Operate Our Restaurants

The restaurant industry is subject to various federal, state and local government licensure and permitting requirements, including those relating to the sale of food and alcoholic beverages. The failure to obtain and maintain these licenses, permits and approvals, including food and liquor licenses, could adversely affect our operating results. Difficulties or failure to obtain any required licenses, permits or other government approvals could delay or result in our decision to cancel the opening of new restaurants. Local authorities may revoke, suspend or deny renewal of our food and liquor licenses if they determine that our conduct violates applicable regulations.

The Sale of Alcoholic Beverages at Our Restaurants Subjects Us to Additional Regulations and Potential Liability

For fiscal year 2018, approximately 17% of our consolidated restaurant sales were attributable to the sale of alcoholic beverages. We are required to comply with the alcohol licensing requirements of the federal government, states and municipalities where our restaurants are located. Alcoholic beverage control regulations require applications to state authorities and, in certain locations, county and municipal authorities for a license and permit to sell alcoholic beverages on the premises and to provide service for extended hours and on Sundays. Typically, the licenses are renewed annually and may be revoked or suspended for cause at any time. Alcoholic beverage control regulations relate to numerous aspects of the daily operations of our restaurants, including minimum age of guests and team members, hours of operation, advertising, wholesale purchasing, inventory control and handling, storage and dispensing of alcoholic beverages. If we fail to comply with federal, state or local regulations, our licenses may be revoked and we may be forced to terminate the sale of alcoholic beverages at one or more of our restaurants.

In certain states, we are subject to “dram shop” statutes, which generally allow a person injured by an intoxicated person the right to recover damages from an establishment that wrongfully served alcoholic beverages to the intoxicated person. Some dram shop litigation against restaurant companies has resulted in significant judgments, including punitive damages.

We Are Dependent on Information Technology and Any Material Failure or Breach in Security of That Technology Could Impair Our Ability to Efficiently Operate Our Business

We rely on information systems across our operations, including, for example, point-of-sale processing in our restaurants, management of our supply chain, collection of cash, payment of obligations, and various other processes and procedures. Our ability to efficiently manage our business depends significantly on the reliability and capacity of these systems. The failure of these systems to operate effectively, problems with maintenance, upgrading or transitioning to replacement systems, or a breach in security of these systems could cause delays in guest service and reduce efficiency in our operations. There have been a number of recent occurrences of cyber security breaches across many retail industries, and such a breach of our systems could represent a material risk to our operations. Significant capital investments might be required to remediate any problems.

19

An Impairment in the Carrying Value of Our Fixed Assets, Intangible Assets or Goodwill Could Adversely Affect Our Financial Condition and Consolidated Results of Operations

Goodwill represents the excess of cost over the fair value of identified net assets of businesses acquired. We review goodwill for impairment annually, or whenever circumstances change in a way which could indicate that impairment may have occurred. Goodwill is tested at the reporting unit level. We identify potential goodwill impairments by comparing the fair value of the reporting unit to its carrying amount, which includes goodwill and other intangible assets. If the carrying amount of the reporting unit exceeds the fair value, an impairment exists. The amount of the impairment is the amount by which the carrying amount exceeds the fair value. A significant amount of judgment is involved in determining if an indication of impairment exists. Factors may include, among others: a significant decline in our expected future cash flows; a sustained, significant decline in our stock price and market capitalization; a significant adverse change in legal factors or in the business climate; unanticipated competition; the testing for recoverability of a significant asset group within a reporting unit; and slower growth rates. Any adverse change in these factors would have a significant impact on the recoverability of these assets and negatively affect our financial condition and consolidated results of operations. We are required to record a non-cash impairment charge if the testing performed indicates that goodwill has been impaired.

We evaluate the useful lives of our fixed assets and intangible assets to determine if they are definite- or indefinite-lived. Reaching a determination on useful life requires significant judgments and assumptions regarding the lease term, future effects of obsolescence, demand, competition, other economic factors (such as the stability of the industry, legislative action that results in an uncertain or changing regulatory environment, and expected changes in distribution channels), the level of required maintenance expenditures and the expected lives of other related groups of assets. We cannot accurately predict the amount and timing of any impairment of assets. Should the value of fixed assets or intangible assets become impaired, there could be an adverse effect on our financial condition and consolidated results of operations.

We May Incur Costs Resulting From Security Risks We Face in Connection With Our Electronic Processing and Transmission of Confidential Guest Information

We accept electronic payment cards from our guests in our restaurants. For the fiscal year ended December 30, 2018, approximately 73% of our sales were attributable to credit/debit card transactions, and credit/debit card usage could continue to increase. A number of restaurant operators and retailers have experienced actual or potential security breaches in which credit/debit card information may have been stolen. While we carry cyber risk insurance and have taken reasonable steps to prevent the occurrence of security breaches in this respect, we may in the future become subject to claims for purportedly fraudulent transactions arising out of the actual or alleged theft of credit/debit card information, and we may also be subject to lawsuits or other proceedings in the future relating to these types of incidents. Proceedings related to theft of credit/debit card information may be brought by payment card providers, banks, and credit unions that issue cards, cardholders (either individually or as part of a class action lawsuit), and federal and state regulators. Any such proceedings could distract our management team members from running our business and cause us to incur significant unplanned losses and expenses.

We also receive and maintain certain personal information about our guests and team members. The use of this information by us is regulated at the federal and state levels. If our security and information systems are compromised or our team members fail to comply with these laws and regulations and this information is obtained by unauthorized persons or used inappropriately, it could adversely affect our reputation, as well as the results of operations, and could result in litigation against us or the imposition of penalties. In addition, our ability to accept credit/debit cards as payment in our restaurants and online depends on us maintaining our compliance status with standards set by the PCI Security Standards Council. These standards, set by a consortium of the major credit card companies, require certain levels of system security and procedures to protect our guests’ credit/debit card information as well as other personal information. Privacy and information security laws and regulations change over time, and compliance with those changes may result in cost increases due to necessary system and process changes.

Failure to Establish and Maintain Our Internal Control Over Financial Reporting Could Harm Our Business and Financial Results

Our management team members are responsible for establishing and maintaining effective internal control over financial reporting. Internal control over financial reporting is a process to provide reasonable assurance regarding the reliability of financial reporting for external purposes in accordance with accounting principles generally accepted in the United States. Because of its inherent limitations, internal control over financial reporting is not intended to provide absolute assurance that we would prevent or detect a misstatement of our financial statements or fraud. Any failure to maintain an effective system of internal control over financial reporting could limit our ability to report our financial results accurately and timely or to detect and prevent fraud. The occurrence of material weaknesses in internal control over financial reporting could cause a loss of investor confidence and decline in the market price of our stock.

20

Our Inability or Failure to Effectively Manage Our Marketing Through Social Media Could Materially Adversely Impact Our Business

As part of our marketing efforts, we rely on BWW managed search engine marketing and social media platforms such as Facebook® and Twitter® to attract and retain guests. BWW is also initiating a multi-year effort to implement new technology platforms that should allow us to digitally engage with our guests and team members and strengthen our marketing and analytics capabilities. These initiatives may not be successful, resulting in expenses incurred without the benefit of higher revenues or increased employee engagement. In addition, a variety of risks are associated with the use of social media, including the improper disclosure of proprietary information, negative comments about our company, exposure of personally identifiable information, fraud, or out-of-date information. The inappropriate use of social media platforms by our guests or team members could increase our costs, lead to litigation or result in negative publicity that could damage our reputation.

There is Volatility in Our Stock Price

The market for our stock has, from time to time, experienced extreme price and volume fluctuations. Factors such as announcements of variations in our quarterly financial results and fluctuations in same-store sales could cause the market price of our stock to fluctuate significantly. In addition, the stock market in general, and the market prices for restaurant companies in particular, have experienced volatility that often has been unrelated to the operating performance of such companies. These broad market and industry fluctuations may adversely affect the price of our stock, regardless of our operating performance.

The market price of our stock can be influenced by shareholders’ expectations about the ability of our business to grow and to achieve certain profitability targets. If our financial performance in a particular quarter does not meet the expectations of our shareholders, it may adversely affect their views concerning our growth potential and future financial performance. In addition, if the securities analysts who regularly follow our stock lower their ratings of our stock, the market price of our stock is likely to drop significantly.

If the Spin-Off Does Not Qualify as a Tax-free Transaction, the Company and its Shareholders Could be Subject to Additional Tax Liabilities

The Company, with the assistance of an opinion obtained from our tax advisors, structured the Spin-Off of Bagger Dave's as a 100% tax-free transaction under the applicable provisions of the U.S. Internal Revenue Code. This opinion is based on assumptions and other representations regarding factual matters made by the Company and Bagger Dave's. In the event these assumptions and representations were found to be inaccurate or incomplete, the tax-free status conclusion reached by our advisors could be in jeopardy. There is a risk that the IRS, upon examination of the facts and circumstances surrounding the transaction, could conclude that the Spin-Off is a taxable event. As a result, the Company and its shareholders could possibly incur additional tax liabilities, including penalties and interest.

21

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES