Exhibit 10.1

Freddie Mac Loan Number: 504183354

Property Name: Greenfield Assisted Living of Stafford

SENIORS HOUSING LOAN AND SECURITY AGREEMENT

(CME)

(Revised 9-1-2011)

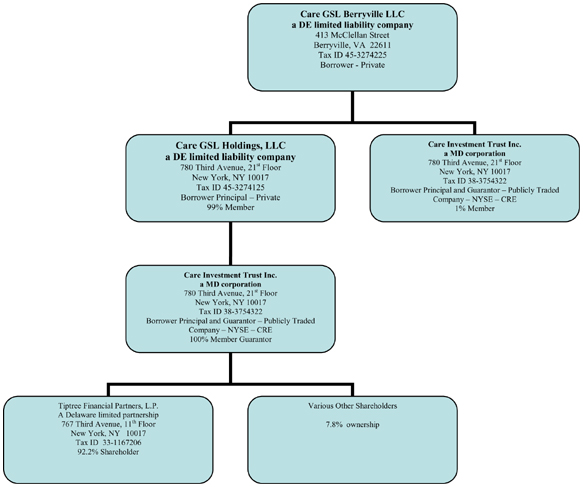

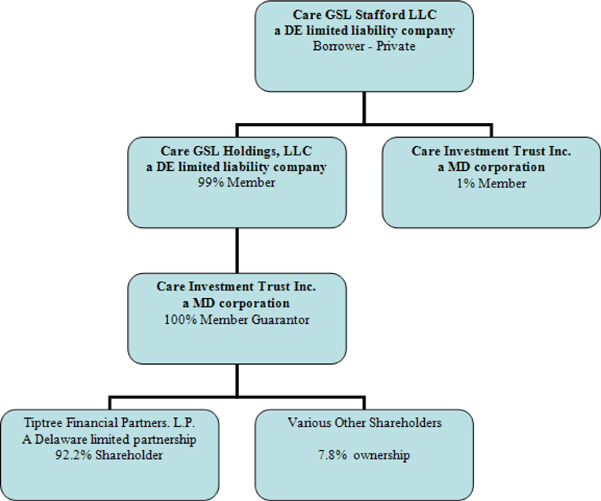

| Borrower: | CARE GSL STAFFORD LLC, a Delaware limited liability company | |

| Lender: | KEYCORP REAL ESTATE CAPITAL MARKETS, INC., an Ohio corporation | |

| Date: | April 24, 2012 | |

Reserve Fund Information

(See Article IV)

| Imposition Reserves | Deferred Insurance | Collect Taxes | Deferred water/sewer | |||

| (fill in “Collect” or “Deferred” | ||||||

| as appropriate for each item) | N/A Ground Rents | Deferred assessments/other charges | ||||

| Repair Reserve | Repairs required? | x Yes | ¨ No | |||

| If Yes, is a Reserve required? | ¨ Yes | x No | ||||

| If Yes to Repairs, but No Reserve, is a Letter of Credit required? | ¨ Yes | x No | ||||

| Replacement Reserve | x Yes If Yes: | x Funded | ¨ Deferred | |||

| ¨ No | ||||||

| Rental Achievement Reserve | ¨ Yes If Yes: | ¨ Cash | ¨ Letter of Credit | |||

| x No | ||||||

| External Rate Cap Reserve | ¨ Yes x No | |||

| Other Reserve(s) | ¨ Yes x No | |||

| If Yes, specify: | ||||||

TABLE OF CONTENTS

| Page | ||||

| ARTICLE I DEFINITIONS; CONSTRUCTION |

1 | |||

| 1.01 Defined Terms |

1 | |||

| 1.02 Construction |

1 | |||

| ARTICLE II LOAN |

2 | |||

| 2.01 Loan Terms |

2 | |||

| 2.02 Prepayment Premium |

2 | |||

| 2.03 Exculpation |

2 | |||

| 2.04 Application of Payments |

2 | |||

| 2.05 Usury Savings |

2 | |||

| 2.06 Adjustable Rate Mortgage – Third Party Cap Agreement |

2 | |||

| ARTICLE III LOAN SECURITY AND GUARANTY |

3 | |||

| 3.01 Security Instrument |

3 | |||

| 3.02 Reserve Funds |

3 | |||

| 3.03 Uniform Commercial Code Security Agreement |

4 | |||

| 3.04 Cap Collateral |

4 | |||

| 3.04 Guaranty |

4 | |||

| 3.06 Collateral Assignment of Licenses, Certificates and Permits |

4 | |||

| ARTICLE IV RESERVE FUNDS AND REQUIREMENTS |

4 | |||

| 4.01 Reserves Generally |

4 | |||

| 4.02 Reserves for Taxes, Insurance and Other Charges |

5 | |||

| 4.03 Repairs; Repair Reserve Fund |

6 | |||

| 4.04 Replacement Reserve Fund |

7 | |||

| 4.05 Rental Achievement Provisions |

7 | |||

| 4.06 Reserved |

7 | |||

| 4.07 External Cap Agreement Reserve Fund Guaranty |

7 | |||

| ARTICLE V REPRESENTATIONS AND WARRANTIES |

7 | |||

| 5.01 Review of Documents |

7 | |||

| 5.02 Condition of Mortgaged Property |

7 | |||

| 5.03 No Condemnation |

7 | |||

| 5.04 Actions; Suits; Proceedings |

7 | |||

| 5.05 Environmental |

8 | |||

| 5.06 Commencement of Work; No Labor or Materialmen’s Claims |

9 | |||

| 5.07 Compliance with Applicable Laws and Regulations |

9 | |||

| 5.08 Access; Utilities; Tax Parcels |

10 | |||

| 5.09 Licenses and Permits |

10 | |||

| 5.10 No Other Interests |

11 | |||

| 5.11 Term of Leases |

11 | |||

| 5.12 No Prior Assignment; Prepayment of Rents |

11 | |||

| Seniors Housing Loan and Security Agreement (CME) | Page i |

| 5.13 Illegal Activity |

12 | |||

| 5.14 Taxes Paid |

12 | |||

| 5.15 Title Exceptions |

12 | |||

| 5.16 No Change in Facts or Circumstances |

12 | |||

| 5.17 Financial Statements |

12 | |||

| 5.18 ERISA – Borrower Status |

13 | |||

| 5.19 No Fraudulent Transfer or Preference |

13 | |||

| 5.20 No Insolvency or Judgment |

13 | |||

| 5.21 Working Capital |

13 | |||

| 5.22 Cap Collateral |

14 | |||

| 5.23 Ground Lease |

14 | |||

| 5.24 Purpose of Loan |

14 | |||

| 5.25 Intended Use |

14 | |||

| 5.25 Furniture, Fixtures, Equipment and Motor Vehicles |

15 | |||

| 5.26 Participant in Federal Programs |

15 | |||

| 5.27 Certificate of Need |

15 | |||

| 5.28 Contracts |

16 | |||

| 5.29 Material Contracts |

16 | |||

| 5.30 No Financing Statements |

17 | |||

| 5.31 Compliance with Medicare and Medicaid Requirements |

17 | |||

| 5.32 Third-Party Payer Programs and Private Commercial Insurance Managed Care and Employee Assistance Programs |

17 | |||

| 5.33 No Transfer or Pledge of Licenses |

17 | |||

| 5.34 No Pledge of Receivables |

17 | |||

| 5.35 Patient and Resident Care Agreements |

18 | |||

| 5.36 Patient and Resident Records |

18 | |||

| 5.37 No Facility Deficiencies, Enforcement Actions or Violations |

18 | |||

| 5.38 Survival |

18 | |||

| ARTICLE VI BORROWER COVENANTS |

18 | |||

| 6.01 Compliance with Laws |

18 | |||

| 6.02 Compliance with Organizational Documents |

18 | |||

| 6.03 Use of Mortgaged Property |

19 | |||

| 6.04 Non-Residential Leases |

20 | |||

| 6.05 Prepayment of Rents |

21 | |||

| 6.06 Inspection |

21 | |||

| 6.07 Books and Records; Financial Reporting |

22 | |||

| 6.08 Taxes; Operating Expenses; Ground Rents |

25 | |||

| 6.09 Preservation, Management and Maintenance of Mortgaged Property |

26 | |||

| 6.10 Property and Liability Insurance |

28 | |||

| 6.11 Condemnation |

36 | |||

| 6.12 Environmental Hazards |

38 | |||

| 6.13 Single Purpose Entity Requirements |

41 | |||

| 6.14 Repairs and Capital Replacements |

46 | |||

| 6.15 Residential Leases Affecting the Mortgaged Property |

47 | |||

| 6.16 Litigation; Government Proceedings |

47 | |||

| Seniors Housing Loan and Security Agreement (CME) | Page ii |

| 6.17 Further Assurances and Estoppel Certificates; Lender’s Expenses |

47 | |||

| 6.18 Cap Collateral |

48 | |||

| 6.19 Ground Lease |

48 | |||

| 6.20 ERISA Requirements |

48 | |||

| 6.21 Operation of the Facility |

49 | |||

| 6.22 Facility Reporting |

50 | |||

| 6.23 Covenants Regarding Material Contracts |

51 | |||

| 6.24 Pledge of Receivables |

51 | |||

| 6.25 Property Manager and Operator of the Facility |

51 | |||

| 6.26 Residential Leases and Agreements |

52 | |||

| 6.27 Performance Under Leases |

52 | |||

| 6.28 Governmental Payer Programs |

52 | |||

| ARTICLE VII TRANSFERS OF THE MORTGAGED PROPERTY OR INTERESTS IN BORROWER |

53 | |||

| 7.01 Permitted Transfers |

53 | |||

| 7.02 Prohibited Transfers |

54 | |||

| 7.03 Conditionally Permitted Transfers |

55 | |||

| 7.04 Preapproved Intrafamily Transfers |

57 | |||

| 7.05 Lender’s Consent to Prohibited Transfers |

57 | |||

| ARTICLE VIII SUBROGATION |

57 | |||

| ARTICLE IX EVENTS OF DEFAULT AND REMEDIES |

58 | |||

| 9.01 Events of Default |

58 | |||

| 9.02 Protection of Lender’s Security; Security Instrument Secures Future Advances |

61 | |||

| 9.03 Remedies |

62 | |||

| 9.04 Forbearance |

63 | |||

| 9.05 Waiver of Marshalling |

64 | |||

| ARTICLE X RELEASE; INDEMNITY |

64 | |||

| 10.01 Release |

64 | |||

| 10.02 Indemnity |

64 | |||

| ARTICLE XI SENIORS HOUSING OPERATOR |

70 | |||

| ARTICLE XII MISCELLANEOUS PROVISIONS |

70 | |||

| 12.01 Waiver of Statute of Limitations, Offsets and Counterclaims |

70 | |||

| 12.02 Governing Law; Consent to Jurisdiction and Venue |

70 | |||

| 12.03 Notice |

70 | |||

| 12.04 Successors and Assigns Bound |

71 | |||

| 12.05 Joint and Several Liability |

71 | |||

| 12.06 Relationship of Parties; No Third Party Beneficiary |

71 | |||

| 12.07 Severability; Amendments |

72 | |||

| 12.08 Disclosure of Information |

72 | |||

| 12.09 Determinations by Lender |

72 | |||

| Seniors Housing Loan and Security Agreement (CME) | Page iii |

| 12.10 Sale of Note; Change in Servicer; Loan Servicing |

73 | |||

| 12.11 Supplemental Financing |

73 | |||

| 12.12 Defeasance |

77 | |||

| 12.13 Lender’s Rights to Sell or Securitize |

81 | |||

| 12.14 Cooperation with Rating Agencies and Investors |

81 | |||

| 12.15 Time is of the Essence |

82 | |||

| ARTICLE XIII DEFINITIONS |

82 | |||

| ARTICLE XIV INCORPORATION OF ATTACHED RIDERS |

99 | |||

| ARTICLE XV INCORPORATION OF ATTACHED EXHIBITS |

100 | |||

| A. ARTICLE XI IS DELETED AND REPLACED WITH THE FOLLOWING: |

1 | |||

| Seniors Housing Loan and Security Agreement (CME) | Page iv |

SENIORS HOUSING LOAN AND SECURITY AGREEMENT

THIS SENIORS HOUSING LOAN AND SECURITY AGREEMENT (“Loan Agreement”) is dated as of the 24th day of April, 2012 and is made by and between CARE GSL STAFFORD LLC, a Delaware limited liability company (“Borrower”), and KEYCORP REAL ESTATE CAPITAL MARKETS, INC., an Ohio corporation (together with its successors and assigns, “Lender”).

RECITAL

Lender has agreed to make and Borrower has agreed to accept a loan in the original principal amount of Six Million Four Hundred Twenty-Four Thousand and No/100 Dollars ($6,424,000.00) (“Loan”). Lender is willing to make the Loan to Borrower upon the terms and subject to the conditions set forth in this Loan Agreement.

AGREEMENT

NOW, THEREFORE, in consideration of these promises, the mutual covenants contained in this Loan Agreement and other good and valuable consideration, the receipt and sufficiency of which are acknowledged, the parties agree as follows:

ARTICLE I DEFINITIONS; CONSTRUCTION.

| 1.01 | Defined Terms. Each defined term in this Loan Agreement will have the meaning ascribed to that term in Article XIII unless otherwise defined in this Loan Agreement. |

| 1.02 | Construction. The captions and headings of the Articles and Sections of this Loan Agreement are for convenience only and will be disregarded in construing this Loan Agreement. Any reference in this Loan Agreement to an “Exhibit,” an “Article” or a “Section” will, unless otherwise explicitly provided, be construed as referring, respectively, to an Exhibit attached to this Loan Agreement or to an Article or Section of this Loan Agreement. All Exhibits and Riders attached to or referred to in this Loan Agreement are incorporated by reference in this Loan Agreement. Any reference in this Loan Agreement to a statute or regulation will be construed as referring to that statute or regulation as amended from time to time. Use of the singular in this Loan Agreement includes the plural and use of the plural includes the singular. As used in this Loan Agreement, the term “including” means “including, but not limited to” and the term “includes” means “includes without limitation.” The use of one gender includes the other gender, as the context may require. Unless the context requires otherwise, (a) any definition of or reference to any agreement, instrument or other document in this Loan Agreement will be construed as referring to such agreement, instrument or other document as from time to time amended, supplemented or otherwise modified (subject to any restrictions on such amendments, supplements or modifications set forth in this Loan Agreement), and (b) any reference in this Loan Agreement to any Person will be construed to include such Person’s successors and assigns. |

| Seniors Housing Loan and Security Agreement (CME) | Page 1 |

ARTICLE II LOAN.

| 2.01 | Loan Terms. The Loan will be evidenced by the Note and will bear interest and be paid in accordance with the payment terms set forth in the Note. |

| 2.02 | Prepayment Premium . Borrower will be required to pay a prepayment premium in connection with certain prepayments of the Indebtedness, including a payment made after Lender’s exercise of any right of acceleration of the Indebtedness, as provided in the Note. |

| 2.03 | Exculpation. Borrower’s personal liability for payment of the Indebtedness and for performance of the other obligations to be performed by it under this Loan Agreement is limited in the manner, and to the extent, provided in the Note. |

| 2.04 | Application of Payments. If at any time Lender receives, from Borrower or otherwise, any amount applicable to the Indebtedness which is less than all amounts due and payable at such time, then Lender may apply that payment to amounts then due and payable in any manner and in any order determined by Lender (unless otherwise required by applicable law), in Lender’s sole and absolute discretion. Neither Lender’s acceptance of an amount that is less than all amounts then due and payable, nor Lender’s application of such payment in the manner authorized, will constitute or be deemed to constitute either a waiver of the unpaid amounts or an accord and satisfaction. Notwithstanding the application of any such amount to the Indebtedness, Borrower’s obligations under this Loan Agreement, the Note and all other Loan Documents will remain unchanged. |

| 2.05 | Usury Savings. If any applicable law limiting the amount of interest or other charges permitted to be collected from Borrower is interpreted so that any charge provided for in any Loan Document, whether considered separately or together with other charges levied in connection with any other Loan Document, violates that law, and Borrower is entitled to the benefit of that law, that charge is hereby reduced to the extent necessary to eliminate that violation. The amounts, if any, previously paid to Lender in excess of the permitted amounts will be applied by Lender to reduce the principal amount of the Indebtedness. For the purpose of determining whether any applicable law limiting the amount of interest or other charges permitted to be collected from Borrower has been violated, all Indebtedness which constitutes interest, as well as all other charges levied in connection with the Indebtedness which constitute interest, will be deemed to be allocated and spread ratably over the stated term of the Note. Unless otherwise required by applicable law, such allocation and spreading will be effected in such a manner that the rate of interest so computed is uniform throughout the stated term of the Note. |

| 2.06 | Adjustable Rate Mortgage – Third Party Cap Agreement. If (a) the Note does not provide for interest to accrue at an adjustable or variable interest rate, and (b) a third party Cap Agreement is not required, then this Section 2.06 and Section 3.04 will be of no force or effect. |

| Seniors Housing Loan and Security Agreement (CME) | Page 2 |

| (a) | So long as there is no Event of Default, Lender or Loan Servicer will remit to Borrower each Cap Payment received by Lender or Loan Servicer with respect to any month for which Borrower has paid in full the monthly installment of principal and interest or interest only, as applicable, due under the Note. Alternatively, at Lender’s option, so long as there is no Event of Default, Lender may apply a Cap Payment received by Lender or Loan Servicer with respect to any month to the applicable monthly payment of accrued interest due under the Note if Borrower has paid in full the remaining portion of such monthly payment of principal and interest or interest only, as applicable. |

| (b) | Neither the existence of a Cap Agreement nor anything in this Loan Agreement will relieve Borrower of its primary obligation to timely pay in full all amounts due under the Note and otherwise due on account of the Indebtedness. |

ARTICLE III LOAN SECURITY AND GUARANTY.

| 3.01 | Security Instrument. Borrower will execute the Security Instrument dated of even date with this Loan Agreement. The Security Instrument will be recorded in the applicable land records in the Property Jurisdiction. |

| 3.02 | Reserve Funds. |

| (a) | Security Interest. To secure Borrower’s obligations under this Loan Agreement and to further secure Borrower’s obligations under the Note and the other Loan Documents, Borrower conveys, pledges, transfers and grants to Lender a security interest pursuant to the Uniform Commercial Code of the Property Jurisdiction or any other applicable law in and to all money in the Reserve Funds, as the same may increase or decrease from time to time, all interest and dividends thereon and all proceeds thereof. |

| (b) | Supplemental Loan. If this Loan Agreement is entered into in connection with a Supplemental Loan and if the same Person is or becomes both Senior Lender and Supplemental Lender, then: |

| (i) | Borrower assigns and grants to Supplemental Lender a security interest in the Reserve Funds established in connection with the Senior Indebtedness as additional security for all of Borrower’s obligations under the Supplemental Note. |

| (ii) | In addition, Borrower assigns and grants to Senior Lender a security interest in the Reserve Funds established in connection with the Supplemental Indebtedness as additional security for all of Borrower’s obligations under the Senior Note. |

| Seniors Housing Loan and Security Agreement (CME) | Page 3 |

| (iii) | It is the intention of Borrower that all amounts deposited by Borrower in connection with either the Senior Loan Documents, the Supplemental Loan Documents, or both, constitute collateral for the Supplemental Indebtedness secured by the Supplemental Instrument and the Senior Indebtedness secured by the Senior Instrument, with the application of such amounts to such Senior Indebtedness or Supplemental Indebtedness to be at the discretion of Senior Lender and Supplemental Lender. |

| 3.03 | Uniform Commercial Code Security Agreement. This Loan Agreement is also a security agreement under the Uniform Commercial Code for any of the Mortgaged Property which, under applicable law, may be subjected to a security interest under the Uniform Commercial Code, for the purpose of securing Borrower’s obligations under this Loan Agreement and to further secure Borrower’s obligations under the Note, Security Instrument and other Loan Documents, whether such Mortgaged Property is owned now or acquired in the future, and all products and cash and non-cash proceeds thereof (collectively, “UCC Collateral”), and by this Loan Agreement, Borrower grants to Lender a security interest in the UCC Collateral. |

| 3.04 | Cap Collateral. Reserved. |

| 3.05 | Guaranty. Borrower will cause each Guarantor (if any) to execute a Guaranty of all or a portion of Borrower’s obligations under the Loan Documents effective as of the date of this Loan Agreement. |

| 3.06 | Collateral Assignment of Licenses, Certificates and Permits. Reserved. |

ARTICLE IV RESERVE FUNDS AND REQUIREMENTS.

| 4.01 | Reserves Generally. |

| (a) | Establishment of Reserve Funds; Investment of Deposits. Unless otherwise provided in Section 4.04, each Reserve Fund will be established on the date of this Loan Agreement and all Reserve Funds will be deposited in an Eligible Account at an Eligible Institution or invested in “permitted investments” as then defined and required by the Rating Agencies. Lender will not be obligated to open additional accounts or deposit Reserve Funds in additional institutions when the amount of any Reserve Fund exceeds the maximum amount of the federal deposit insurance or guaranty. Borrower acknowledges and agrees that it will not have the right to direct Lender as to any specific investment of monies in any Reserve Fund. Lender will not be responsible for any losses resulting from investment of monies in any Reserve Fund or for obtaining any specific level or percentage of earnings on such investment. |

| (b) | Interest on Reserve Funds; Trust Funds. Unless applicable law requires, Lender will not be required to pay Borrower any interest, earnings or profits on the Reserve Funds. Any amounts deposited with Lender under this Article IV will not be trust funds, nor will they operate to reduce the Indebtedness, unless applied by Lender for that purpose pursuant to the terms of this Loan Agreement. |

| Seniors Housing Loan and Security Agreement (CME) | Page 4 |

| (c) | Use of Reserve Funds. Each Reserve Fund will, except as otherwise provided in this Loan Agreement, be used for the sole purpose of paying, or reimbursing Borrower for payment of, the item(s) for which the applicable Reserve Fund was established. Borrower acknowledges and agrees that, except as specified in this Loan Agreement, monies in one Reserve Fund will not be used to pay, or reimburse Borrower for, matters for which another Reserve Fund has been established. |

| (d) | Termination of Reserve Funds. Upon the payment in full of the Indebtedness, Lender will pay to Borrower all funds remaining in any Reserve Funds. |

| 4.02 | Reserves for Taxes, Insurance and Other Charges. |

| (a) | Deposits to Imposition Reserve Deposits. Borrower will deposit with Lender on the day monthly installments of principal or interest, or both, are due under the Note (or on another day designated in writing by Lender), until the Indebtedness is paid in full, an additional amount sufficient to accumulate with Lender the entire sum required to pay, when due, the items marked “Collect” below. Except as provided in Section 4.02(e), Lender will not require Borrower to make Imposition Reserve Deposits with respect to the items marked “Deferred” below. |

| [Deferred] | Hazard Insurance premiums or premiums for other Insurance required by Lender under Section 6.10 | |

| [Collect ] | Taxes and payments in lieu of taxes | |

| [Deferred] | water and sewer charges that could become a Lien on the Mortgaged Property | |

| [ N/A ] | Ground Rents | |

| [Deferred] | assessments or other charges that could become a Lien on the Mortgaged Property | |

The amounts deposited pursuant to this Section 4.02(a) are collectively referred to in this Loan Agreement as the “Imposition Reserve Deposits.” The obligations of Borrower for which the Imposition Reserve Deposits are required are collectively referred to in this Loan Agreement as “Impositions.” The amount of the Imposition Reserve Deposits must be sufficient to enable Lender to pay each Imposition before the last date upon which such payment may be made without any penalty or interest charge being added. Lender will maintain records indicating how much of the monthly Imposition Reserve Deposits and how much of the aggregate Imposition Reserve Deposits held by Lender are held for the purpose of paying Taxes, Insurance premiums, Ground Rent (if applicable) and each other Imposition.

| Seniors Housing Loan and Security Agreement (CME) | Page 5 |

| (b) | Disbursement of Imposition Reserve Deposits. Lender will apply the Imposition Reserve Deposits to pay Impositions so long as no Event of Default has occurred and is continuing. Lender will pay all Impositions from the Imposition Reserve Deposits held by Lender upon Lender’s receipt of a bill or invoice for an Imposition. If Borrower holds a ground lessee interest in the Mortgaged Property and Imposition Reserve Deposits are collected for Ground Rent, then Lender will pay the monthly or other periodic installments of Ground Rent from the Imposition Reserve Deposits, whether or not Lender receives a bill or invoice for such installments. Lender will have no obligation to pay any Imposition to the extent it exceeds the amount of the Imposition Reserve Deposits then held by Lender. Lender may pay an Imposition according to any bill, statement or estimate from the appropriate public office, Ground Lessor (if applicable) or insurance company without inquiring into the accuracy of the bill, statement or estimate or into the validity of the Imposition. |

| (c) | Excess or Deficiency of Imposition Reserve Deposits. If at any time the amount of the Imposition Reserve Deposits held by Lender for payment of a specific Imposition exceeds the amount reasonably deemed necessary by Lender, the excess will be credited against future installments of Imposition Reserve Deposits. If at any time the amount of the Imposition Reserve Deposits held by Lender for payment of a specific Imposition is less than the amount reasonably estimated by Lender to be necessary, Borrower will pay to Lender the amount of the deficiency within 15 days after Notice from Lender. |

| (d) | Delivery of Invoices. Borrower will promptly deliver to Lender a copy of all notices of, and invoices for, Impositions. |

| (e) | Deferral of Collection of Any Imposition Reserve Deposits; Delivery of Receipts. If Lender does not collect an Imposition Reserve Deposit with respect to an Imposition either marked “Deferred” in Section 4.02(a) or pursuant to a separate written deferral by Lender, then on or before the date each such Imposition is due, or on the date this Loan Agreement requires each such Imposition to be paid, Borrower will provide Lender with proof of payment of each such Imposition. Upon Notice to Borrower, Lender may revoke its deferral and require Borrower to deposit with Lender any or all of the Imposition Reserve Deposits listed in Section 4.02(a), regardless of whether any such item is marked “Deferred” (i) if Borrower does not timely pay any of the Impositions, (ii) if Borrower fails to provide timely proof to Lender of such payment, or (iii) at any time during the existence of an Event of Default. |

| 4.03 | Repairs; Repair Reserve Fund. Reserved. |

| Seniors Housing Loan and Security Agreement (CME) | Page 6 |

| 4.04 | Replacement Reserve Fund. See Rider. |

| 4.05 | Rental Achievement Provisions. Reserved. |

| 4.06 | Reserved. |

| 4.07 | External Cap Agreement Reserve Fund. Reserved. |

ARTICLE V REPRESENTATIONS AND WARRANTIES.

Borrower represents and warrants to Lender as follows as of the date of this Loan Agreement:

| 5.01 | Review of Documents. Borrower has reviewed (a) the Note, (b) the Security Instrument, (c) the Commitment Letter, and (d) all other Loan Documents. |

| 5.02 | Condition of Mortgaged Property. Except as Borrower may have disclosed to Lender in writing in connection with the issuance of the Commitment Letter, the Mortgaged Property has not been damaged by fire, water, wind or other cause of loss, or any previous damage to the Mortgaged Property has been fully restored. |

| 5.03 | No Condemnation. No part of the Mortgaged Property has been taken in Condemnation or other like proceeding, and, to the best of Borrower’s knowledge after due inquiry and investigation, no such proceeding is pending or threatened for the partial or total Condemnation or other taking of the Mortgaged Property. |

| 5.04 | Actions; Suits; Proceedings. |

| (a) | There are no judicial, administrative, mediation or arbitration actions, suits or proceedings pending or, to the best of Borrower’s knowledge, threatened in writing against or affecting Borrower (and, if Borrower is a limited partnership, any of its general partners or if Borrower is a limited liability company, any member of Borrower) or the Mortgaged Property which, if adversely determined, would have a Material Adverse Effect. |

| (b) | Without limiting the generality of subsection (a) above, neither Borrower, any operator of the Facility, nor the Facility are subject to any proceeding, suit or investigation by any Governmental Authority and neither Borrower nor any operator of the Facility has received any notice from any Governmental Authority which may, directly or indirectly, or with the passage of time, result in the imposition of a fine, or interim or final sanction, or would (i) have a Material |

| Seniors Housing Loan and Security Agreement (CME) | Page 7 |

Adverse Effect, (ii) result in the appointment of a receiver or trustee, (iii) affect Borrower’s or any operator of the Facility’s ability to accept and retain residents, (iv) result in the Downgrade, revocation, transfer, surrender or suspension, or non-renewal or reissuance or other impairment of any License, or (v) affect Borrower’s or operator’s continued participation in Medicare, Medicaid, TRICARE, or any similar governmental payor program, as applicable, or any successor programs thereto, at current rate certifications.

| 5.05 | Environmental. Except as previously disclosed by Borrower to Lender in writing (which written disclosure may be in certain environmental assessments and other written reports accepted by Lender in connection with the funding of the Indebtedness and dated prior to the date of this Loan Agreement), each of the following is true: |

| (a) | Borrower has not at any time engaged in, caused or permitted any Prohibited Activities or Conditions on the Mortgaged Property. |

| (b) | To the best of Borrower’s knowledge after due inquiry and investigation, no Prohibited Activities or Conditions exist or have existed on the Mortgaged Property. |

| (c) | The Mortgaged Property does not now contain any underground storage tanks, and, to the best of Borrower’s knowledge after due inquiry and investigation, the Mortgaged Property has not contained any underground storage tanks in the past. If there is an underground storage tank located on the Mortgaged Property that has been previously disclosed by Borrower to Lender in writing, that tank complies with all requirements of Hazardous Materials Laws. |

| (d) | To the best of Borrower’s knowledge after due inquiry and investigation, Borrower has complied with all Hazardous Materials Laws, including all requirements for notification regarding releases of Hazardous Materials. Without limiting the generality of the foregoing, all Environmental Permits required for the operation of the Mortgaged Property in accordance with Hazardous Materials Laws now in effect have been obtained and all such Environmental Permits are in full force and effect. |

| (e) | To the best of Borrower’s knowledge after due inquiry and investigation, no event has occurred with respect to the Mortgaged Property that constitutes, or with the passage of time or the giving of notice, or both, would constitute, noncompliance with the terms of any Environmental Permit. |

| (f) | There are no actions, suits, claims or proceedings pending or, to the best of Borrower’s knowledge after due inquiry and investigation, threatened in writing, that involve the Mortgaged Property and allege, arise out of, or relate to any Prohibited Activity or Condition. |

| (g) | Borrower has received no actual or constructive notice of any written complaint, order, notice of violation or other communication from any Governmental |

| Seniors Housing Loan and Security Agreement (CME) | Page 8 |

Authority with regard to air emissions, water discharges, noise emissions or Hazardous Materials, or any other environmental, health or safety matters affecting the Mortgaged Property or any property that is adjacent to the Mortgaged Property.

| 5.06 | Commencement of Work; No Labor or Materialmen’s Claims. Except as set forth on Exhibit E, prior to the recordation of the Security Instrument, no work of any kind has been or will be commenced or performed upon the Mortgaged Property, and no materials or equipment have been or will be delivered to or upon the Mortgaged Property, for which the contractor, subcontractor or vendor continues to have any rights including the existence of or right to assert or file a mechanic’s or materialman’s Lien. If any such work of any kind has been commenced or performed upon the Mortgaged Property, or if any such materials or equipment have been ordered or delivered to or upon the Mortgaged Property, then prior to the execution of the Security Instrument, Borrower has satisfied each of the following conditions: |

| (a) | Borrower has fully disclosed in writing to the title insurance company issuing the mortgagee title insurance policy insuring the Lien of the Security Instrument that work has been commenced or performed on the Mortgaged Property, or materials or equipment have been ordered or delivered to or upon the Mortgaged Property. |

| (b) | Borrower has obtained and delivered to Lender and the title company issuing the mortgagee title insurance policy insuring the Lien of the Security Instrument Lien waivers from all contractors, subcontractors, suppliers or any other applicable party, pertaining to all work commenced or performed on the Mortgaged Property, or materials or equipment ordered or delivered to or upon the Mortgaged Property. |

Borrower represents and warrants that all parties furnishing labor and materials for which a Lien or claim of Lien may be filed against the Mortgaged Property have been paid in full and, except for such Liens or claims insured against by the policy of title insurance to be issued in connection with the Loan, there are no mechanics’, laborers’ or materialmen’s Liens or claims outstanding for work, labor or materials affecting the Mortgaged Property, whether prior to, equal with or subordinate to the Lien of the Security Instrument.

| 5.07 | Compliance with Applicable Laws and Regulations. |

| (a) | To the best of Borrower’s knowledge after due inquiry and investigation, (i) all Improvements and the use of the Mortgaged Property comply with all applicable statutes, rules and regulations, including all applicable statutes, rules and regulations pertaining to requirements for equal opportunity, anti-discrimination, fair housing, environmental protection, zoning and land use (“legal, non-conforming” status with respect to uses or structures will be considered to comply with zoning and land use requirements for the purposes of this representation), (ii) the Improvements comply with applicable health, fire, and building codes, and (iii) there is no evidence of any illegal activities relating to controlled substances on the Mortgaged Property. |

| Seniors Housing Loan and Security Agreement (CME) | Page 9 |

| (b) | Without limiting the generality of subsection (a) above, Borrower, any operator of the Facility, and the Facility (and its operation) and all residential care agreements and residential Leases are in compliance with the applicable provisions of all laws, regulations, ordinances, orders or standards of any Governmental Authority having jurisdiction over the operation of the Facility (including any governmental payor program requirements and disclosure of ownership and related information requirements), including without limitation: (i) Healthcare Laws, Privacy Laws, fire and safety codes and building codes (and no waivers of such requirements exist at the Facility); (ii) laws, rules, regulations and published interpretations thereof regulating the preparation and serving of food; (iii) laws, rules, regulations and published interpretations thereof regulating the handling and disposal of medical or biological waste; (iv) the applicable provisions of all laws, rules, regulations and published interpretations thereof to which Borrower or the Facility is subject by virtue of its Intended Use; and (v) all criteria established to classify the Facility as housing for older persons under the Fair Housing Amendments Act of 1988. |

| (c) | Borrower has received no notice of, and is not aware of, any violation of applicable antitrust laws or securities laws relating to the Facility, the Borrower, or any operator of the Facility. |

| 5.08 | Access; Utilities; Tax Parcels. The Mortgaged Property (a) has ingress and egress via a publicly dedicated right of way or via an irrevocable easement permitting ingress and egress, (b) is served by public utilities and services generally available in the surrounding community or otherwise appropriate for the use in which the Mortgaged Property is currently being utilized, and (c) constitutes one or more separate tax parcels. |

| 5.09 | Licenses and Permits. |

| (a) | Borrower, any commercial tenant of the Mortgaged Property and/or any operator of the Mortgaged Property (i) is in possession of all material licenses, permits and authorizations required for use of the Mortgaged Property, which are valid and in full force and effect as of the date of this Loan Agreement, and (ii) will remain in material compliance with all material licenses, permits and other legal requirements necessary and required to conduct its business. |

| (b) | Without limiting the generality of subsection (a) above, Borrower has obtained or has caused any operator of the Facility to obtain all Licenses necessary to use, occupy or operate the Facility for its Intended Use (such Licenses being in its own name or in the name of an operator of the Facility, if any, and in any event in the names of the Persons required by the applicable Governmental Authorities), and all such Licenses are in full force and effect. Borrower has provided Lender with |

| Seniors Housing Loan and Security Agreement (CME) | Page 10 |

complete and accurate copies of all Licenses. The Intended Use of the Facility is in conformity with all certificates of occupancy and Licenses and any other restrictions or covenants affecting the Facility. The Facility has all equipment, staff and supplies necessary to use and operate the Facility for its Intended Use.

| (c) | Each License, and the name of the Person in whose name each License is issued, if other than Borrower, is identified on Exhibit J, and a copy of each License is attached as Exhibit J. |

| (d) | As of the Closing Date, the Licenses attached as Exhibit J are true and complete copies, the Licenses are current, and Borrower has not received any notice of pending violations or investigations that have not been brought to Lender’s attention in writing. |

| (e) | Other than the Licenses attached as Exhibit J, as of the Closing Date, no other Licenses are required to operate the Facility as it is currently being operated and for its Intended Use. |

| (f) | Neither the execution and delivery of the Note, this Loan Agreement, the Security Instrument nor any other Loan Document, Borrower’s performance under the Loan Documents, nor the recordation of the Security Instrument, nor the exercise of any remedies by Lender pursuant to the Loan Documents, at law or in equity, will adversely affect the Licenses. |

| 5.10 | No Other Interests. No Person has (a) any possessory interest in the Mortgaged Property or right to occupy the Mortgaged Property except under and pursuant to the provisions of existing Leases by and between tenants and Borrower (a form of residential lease having been previously provided to Lender together with the material terms of any and all Non-Residential Leases at the Mortgaged Property), or (b) an option to purchase the Mortgaged Property or an interest in the Mortgaged Property, except as has been disclosed to and approved in writing by Lender. |

| 5.11 | Term of Leases. All Leases for residential dwelling units with respect to the Mortgaged Property are on forms acceptable to Lender, are for initial terms of at least 6 months and not more than 2 years (unless otherwise approved in writing by Lender), and do not include options to purchase. |

| 5.12 | No Prior Assignment; Prepayment of Rents. Borrower has (a) not executed any prior assignment of Rents (other than an assignment of Rents securing any prior indebtedness that is being assigned to Lender, or paid off and discharged with the proceeds of the Loan evidenced by the Note or, if this Loan Agreement is entered into in connection with a Supplemental Loan, other than an assignment of Rents securing any Senior Indebtedness), and (b) not performed any acts and has not executed, and will not execute, any instrument which would prevent Lender from exercising its rights under any Loan Document. At the time of execution of this Loan Agreement, unless otherwise approved by Lender in writing, there has been no prepayment of any Rents for more than 2 months prior to the due dates of such Rents. |

| Seniors Housing Loan and Security Agreement (CME) | Page 11 |

| 5.13 | Illegal Activity. No portion of the Mortgaged Property has been or will be purchased with the proceeds of any illegal activity and Borrower will not permit any portion of the Mortgaged Property to be used for any illegal activity. |

| 5.14 | Taxes Paid. Borrower has filed all federal, state, county and municipal tax returns required to have been filed by Borrower, and has paid all Taxes which have become due pursuant to such returns or to any notice of assessment received by Borrower, and Borrower has no knowledge of any basis for additional assessment with respect to such taxes. To the best of Borrower’s knowledge after due inquiry and investigation, there are not presently pending any special assessments against the Mortgaged Property or any part of the Mortgaged Property. |

| 5.15 | Title Exceptions. To the best of Borrower’s knowledge after due inquiry and investigation, none of the items shown in the schedule of exceptions to coverage in the title policy issued to and accepted by Lender contemporaneously with the execution of this Loan Agreement and insuring Lender’s interest in the Mortgaged Property will have a Material Adverse Effect on the (a) ability of Borrower to pay the Loan in full, (b) ability of Borrower to use all or any part of the Mortgaged Property in the manner in which the Mortgaged Property is being used on the Closing Date, except as set forth in Section 6.03, (c) operation of the Mortgaged Property, or (d) value of the Mortgaged Property. |

| 5.16 | No Change in Facts or Circumstances. |

| (a) | All information in the application for the Loan submitted to Lender, including all financial statements for the Mortgaged Property, Borrower and any Borrower Principal, and all Rent Schedules, reports, certificates, and any other documents submitted in connection with the application (collectively, “Loan Application”) is complete and accurate in all material respects as of the date such information was submitted to Lender. |

| (b) | There has been no Material Adverse Change since the Loan Application was submitted to Lender in any fact or circumstance that would make any information submitted as part of the Loan Application incomplete or inaccurate. |

| (c) | The organizational structure of Borrower is as set forth in Exhibit H. |

| 5.17 | Financial Statements. The financial statements of Borrower and each Borrower Principal furnished to Lender as part of the Loan Application reflect in each case a positive net worth as of the date of the applicable financial statement. |

| Seniors Housing Loan and Security Agreement (CME) | Page 12 |

| 5.18 | ERISA – Borrower Status. Borrower is not one of the following: |

| (a) | An “investment company,” or a company under the Control of an “investment company,” as such terms are defined in the Investment Company Act of 1940, as amended. |

| (b) | An “employee benefit plan,” as defined in Section 3(3) of ERISA, which is subject to Title I of ERISA and the assets of Borrower do not constitute “plan assets” of one or more such plans within the meaning of 29 C.F.R. Section 2510.3-101. |

| 5.19 | No Fraudulent Transfer or Preference. No Borrower or Borrower Principal (a) has made, or is making in connection with and as security for the Loan, a transfer of an interest in property of the Borrower or Borrower Principal to or for the benefit of Lender or otherwise as security for any of the obligations under the Loan Documents which is or could constitute a voidable preference under federal bankruptcy, state insolvency or similar applicable creditors’ rights laws or (b) has made, or is making in connection with the Loan, a transfer (including any transfer to or for the benefit of an insider under an employment contract) of an interest of Borrower or any Borrower Principal in property, or (c) has incurred, or is incurring in connection with the Loan, any obligation (including any obligation to or for the benefit of an insider under an employment contract) within 2 years of the date of this Loan Agreement which is or could constitute a fraudulent transfer under federal bankruptcy, state insolvency, or similar applicable creditors’ rights laws. |

| 5.20 | No Insolvency or Judgment. |

| (a) | No Pending Proceedings or Judgments. No Borrower or Borrower Principal is (i) the subject of or a party to (other than as a creditor) any completed or pending bankruptcy, reorganization or insolvency proceeding; or (ii) the subject of any judgment unsatisfied of record or docketed in any court located in the United States. |

| (b) | Insolvency. Borrower is not presently insolvent, and the Loan will not render Borrower insolvent. As used in this Section, the term “insolvent” means that the total of all of a Person’s liabilities (whether secured or unsecured, contingent or fixed, or liquidated or unliquidated) is in excess of the value of all of the assets of the Person that are available to satisfy claims of creditors. |

| 5.21 | Working Capital. After the Loan is made, Borrower intends to have sufficient working capital, including cash flow from the Mortgaged Property or other sources, not only to adequately maintain the Mortgaged Property, but also to pay all of Borrower’s outstanding debts as they come due (other than any balloon payment due upon the maturity of the Loan). Lender acknowledges that no members or partners of Borrower or any Borrower Principal will be obligated to contribute equity to Borrower for purposes of providing working capital to maintain the Mortgaged Property or to pay Borrower’s outstanding debts except as may otherwise be required under their organizational documents. |

| Seniors Housing Loan and Security Agreement (CME) | Page 13 |

| 5.22 | Cap Collateral. Reserved. |

| 5.23 | Ground Lease. Reserved. |

| 5.24 | Purpose of Loan. The purpose of the Loan is as indicated by the checked box(es) below: |

| x | Refinance Loan: The Loan is a refinancing of existing indebtedness and, except to the extent specifically required by Lender, there is to be no change in the ownership of either the Mortgaged Property or Borrower Principals. The intended use of any cash received by Borrower from Lender, to the extent applicable, in connection with the refinancing has been fully disclosed to Lender. |

| ¨ | Acquisition Loan: All of the consideration given or received or to be given or received in connection with the acquisition of the Mortgaged Property has been fully disclosed to Lender. The Mortgaged Property was or will be purchased from (“Property Seller”). No Borrower or Borrower Principal has or had, directly or indirectly (through a family member or otherwise), any interest in the Property Seller and the acquisition of the Mortgaged Property is an arm’s-length transaction. To the best of Borrower’s knowledge after due inquiry and investigation, the purchase price of the Mortgaged Property represents the fair market value of the Mortgaged Property and Property Seller is not or will not be insolvent subsequent to the sale of the Mortgaged Property. |

| x | Cross-Collateralized/Cross-Defaulted Loan Pool: The Loan is part of a cross-collateralized/cross-defaulted pool of loans described as follows: |

| x | being simultaneously made to Borrower and/or Borrower’s Affiliates |

| ¨ | made previously by Borrower and/or Borrower’s Affiliates |

The intended use of any cash received by Borrower from Lender, to the extent applicable, in connection with the Loan and the other loans comprising the cross-collateralized/cross-defaulted loan pool has been fully disclosed to Lender.

| 5.25 | Intended Use. The residential units in the Facility are allocated as follows (“Intended Use”): |

| 1. | Independent Living Units | 0 | % | |||

| 0 | units | |||||

| 2. | Assisted Living Residences | 50 | % | |||

| 22 | units | |||||

| 28 | beds | |||||

| Seniors Housing Loan and Security Agreement (CME) | Page 14 |

| 3. | Assisted Living Residences devoted to Alzheimer’s care, dementia care and/or memory care | 50 | % | |||

| 22 | units | |||||

| 34 | beds | |||||

| 4. | Skilled Nursing Beds | 0 | % | |||

| 0 | units | |||||

| 0 | beds | |||||

| 5. | Continuing Care Retirement Community with the following percentages of use: | N/A | % | |||

| a. Seniors Apartments | N/A | units | ||||

| b. Independent Living Units | N/A | % | ||||

| N/A | units | |||||

| c. Assisted Living Residences | N/A | % | ||||

| N/A | units | |||||

| N/A | beds | |||||

| d. Skilled Nursing Beds | N/A | % | ||||

| N/A | units | |||||

| N/A | beds | |||||

| 5.26 | Furniture, Fixtures, Equipment and Motor Vehicles. As of the Closing Date, all FF&E and motor vehicles located on or used in connection with the Mortgaged Property, and the name of the Person that owns and/or leases each item, if other than Borrower, is listed on Exhibit K, and such list is true and complete. |

| 5.27 | Participant in Federal Programs. Neither Borrower nor any operator of the Facility is a participant in any federal program under which any Governmental Authority may have the right to recover funds by reason of the advance of federal funds. |

| 5.28 | Certificate of Need. Under applicable laws and regulations as in effect on the date of this Loan Agreement, if any existing management agreement or operating lease is terminated or Lender acquires the Facility through foreclosure or otherwise, none of Borrower, Lender, any subsequent operator or management agent, or any subsequent purchaser (through foreclosure or otherwise) must obtain a certificate of need from any Governmental Authority (other than giving of any notice required under the applicable state law or regulation) prior to applying for any License, so long as neither the type of service nor any unit complement is changed. |

| Seniors Housing Loan and Security Agreement (CME) | Page 15 |

| 5.29 | Contracts. |

| (a) | Exhibit L lists all Contracts in effect as of the date of this Loan Agreement, the names of the parties to such Contracts and the dates of such Contracts. |

| (b) | With regard to each Contract listed in Exhibit L, (i) the Contract is in full force and effect in accordance with its terms, and (ii) there is no default by any party under the Contract. |

| (c) | Borrower has delivered to Lender a copy of each Contract, together with all amendments, modifications, supplements and renewals thereto in effect as of the date of this Loan Agreement. |

| (d) | Except as set forth on Exhibit L, each Contract listed in Exhibit L provides that it is terminable by Borrower or any operator of the Facility upon not more than 30 days notice without the necessity of establishing cause and without payment of a penalty or termination fee by Borrower or any operator of the Facility or their respective successors or assigns, except only Third Party Provider Agreements. |

| 5.30 | Material Contracts. |

| (a) | Exhibit M lists all Material Contracts in effect as of the date of this Loan Agreement. |

| (b) | With regard to each Material Contract listed in Exhibit M, (i) the Material Contract is assignable by Borrower, or if Borrower is not a party thereto, by an operator of the Facility, without the consent of the other party thereto (or Borrower and any operator of the Facility, as applicable, has obtained express written consent to the assignment from the other party thereto), except only Third Party Provider Agreements; (ii) no previous assignment of Borrower’s or any operator of the Facility’s interest in the Material Contract has been made except such assignments that have been properly terminated prior to or concurrently with the execution and delivery of this Loan Agreement; (iii) the Material Contract is in full force and effect in accordance with its terms; and (iv) there is no default by any party under the Material Contract. |

| (c) | Borrower has delivered to Lender a copy of each Material Contract, together with all amendments, modifications, supplements and renewals thereto in effect as of the date of this Loan Agreement. |

| (d) | Each Material Contract listed in Exhibit M provides that it is terminable upon not more than 30 days notice without the necessity of establishing cause and without payment of a penalty or termination fee by Borrower or any operator of the Facility or their respective successors or assigns, except only Third Party Provider Agreements. |

| Seniors Housing Loan and Security Agreement (CME) | Page 16 |

| 5.31 | No Financing Statements. Except for termination statements and continuation statements, during the 45-day period prior to the date of this Loan Agreement, there have been no UCC financing statements filed with respect to any of the UCC Collateral listing as debtor Borrower, any operator of the Facility, or the Facility’s common name. |

| 5.32 | Compliance with Medicare and Medicaid Requirements. The Facility is in compliance with all requirements for participation in Medicare and Medicaid, including without limitation, the Medicare and Medicaid Patient and Program Protection Act of 1987. The Facility is in conformance in all material respects with all insurance, reimbursement and cost reporting requirements and has a current provider agreement that is in full force and effect under Medicare and Medicaid, as applicable. As of the date of this Loan Agreement, neither Borrower nor any operator of the Facility has received any notice from any Governmental Authority of any overbilling of Medicare, Medicaid, TRICARE (or any so-called “waiver program” associated therewith) or any other Governmental Authority payor for similar goods or services with respect to the Facility and there are no current or pending Medicare, Medicaid, TRICARE or similar governmental payor program recoupment efforts at the Facility, and there are no current, pending or outstanding audits or appeals with respect thereto (or which remain open to audit with respect thereto). |

| 5.33 | Third-Party Payor Programs and Private Commercial Insurance Managed Care and Employee Assistance Programs. There is no threatened or pending revocation, suspension, termination, probation, restriction, limitation or nonrenewal affecting Borrower or operator of the Facility, of any participation or provider agreement with any third-party payor, including Medicare, Medicaid, TRICARE, and any private commercial insurance managed care and employee assistance program to which Borrower or operator of the Facility is subject. All Medicare, Medicaid, TRICARE and private insurance cost reports and financial reports submitted by Borrower or operator of the Facility are and will be materially accurate and complete and have not been and will not be misleading in any material respects. No cost reports for the Facility remain “open” or unsettled. |

| 5.34 | No Transfer or Pledge of Licenses. The Licenses, including, without limitation, the certificate of need, may not be, and have not been, transferred to any location other than the Facility, have not been pledged as collateral security for any other loan or indebtedness, and are held free from restrictions or known conflicts that would materially impair the use or operation of the Facility for its Intended Use, and are not provisional, probationary, or restricted in any way. |

| 5.35 | No Pledge of Receivables. Neither Borrower nor the operator of the Facility has pledged its receivables as collateral security for any other loan or indebtedness. |

| Seniors Housing Loan and Security Agreement (CME) | Page 17 |

| 5.36 | Patient and Resident Care Agreements. There are no patient or resident care agreements with patients or residents or with any other persons that deviate in any material adverse respect from the standard form customarily used at the Facility. |

| 5.37 | Patient and Resident Records. All patient or resident records at the Facility, including patient or resident trust fund accounts, are true and correct in all material respects. |

| 5.38 | No Facility Deficiencies, Enforcement Actions or Violations. |

| (a) | The Facility has not received a statement of charges or deficiencies and no penalty enforcement actions have been undertaken against the Facility, the operator of the Facility or Borrower or against any officer, director or stockholder thereof, by any Governmental Agency during the last three calendar years, and there have been no violations over the past three years that have threatened the Facility’s or the operator of the Facility’s or Borrower’s certification for participation in any third-party payor programs. |

| (b) | [RESERVED] |

| 5.39 | Survival. The representations and warranties set forth in this Loan Agreement will survive until the Indebtedness is paid in full; however, the representations and warranties set forth in Section 5.05 will survive beyond repayment of the entire Indebtedness, to the extent provided in Section 10.02(b). |

ARTICLE VI BORROWER COVENANTS.

| 6.01 | Compliance with Laws. Borrower will comply with all laws, ordinances, rules, regulations and requirements of any Governmental Authority having jurisdiction over the Mortgaged Property and all recorded covenants and agreements relating to or affecting the Mortgaged Property, including all laws, ordinances, regulations, requirements and covenants pertaining to health and safety, construction of improvements on the Mortgaged Property, Repairs, Capital Replacements, fair housing, disability accommodation, zoning and land use, applicable building codes, special use permits and environmental regulations, Leases and the maintenance and disposition of tenant security deposits. Borrower will take appropriate measures to prevent, and will not engage in or knowingly permit, any illegal activities at the Mortgaged Property, including those that could endanger tenants or visitors, result in damage to the Mortgaged Property, result in forfeiture of the Mortgaged Property, or otherwise materially impair the Lien created by the Security Instrument or Lender’s interest in the Mortgaged Property. Borrower will at all times maintain records sufficient to demonstrate compliance with the provisions of this Section 6.01. |

| 6.02 | Compliance with Organizational Documents. Borrower will at all times comply with all laws, regulations and requirements of any Governmental Authority relating to Borrower’s |

| Seniors Housing Loan and Security Agreement (CME) | Page 18 |

formation, continued existence and good standing in its state of formation and, if different, in the Property Jurisdiction. Borrower will at all times comply with its organizational documents, including its partnership agreement (if Borrower is a partnership), its by-laws (if Borrower is a corporation or housing cooperative corporation or association) or its operating agreement (if Borrower is a limited liability company or tenancy-in-common). If Borrower is a housing cooperative corporation or association, Borrower will at all times maintain its status as a “cooperative housing corporation” as such term is defined in Section 216(b) of the Internal Revenue Code of 1986, as amended, or any successor statute thereto.

| 6.03 | Use of Mortgaged Property. |

| (a) | Unless required by applicable law, without the prior written consent of Lender, Borrower will not, and will not permit any operator of the Facility to, take any of the following actions: |

| (i) | Allow changes in the use for which all or any part of the Mortgaged Property is being used at the time this Loan Agreement is executed. |

| (ii) | Convert any individual dwelling units or common areas to commercial use. |

| (iii) | Initiate a change in the zoning classification of the Mortgaged Property or acquiesce to a change in the zoning classification of the Mortgaged Property. |

| (iv) | Establish any condominium or cooperative regime with respect to the Mortgaged Property beyond any which may be in existence on the date of this Loan Agreement. |

| (v) | Combine all or any part of the Mortgaged Property with all or any part of a tax parcel which is not part of the Mortgaged Property. |

| (vi) | Subdivide or otherwise split any tax parcel constituting all or any part of the Mortgaged Property. |

| (vii) | Add to or change any location at which any of the Mortgaged Property is stored, held or located unless Borrower (A) gives Notice to Lender within 30 days after the occurrence of such addition or change, (B) executes and delivers to Lender any modifications of or supplements to this Loan Agreement that Lender may require, and (C) authorizes the filing of any financing statement which may be filed in connection with this Loan Agreement, as Lender may require. |

| (b) | Notwithstanding anything contained in this Section to the contrary, if Borrower is a housing cooperative corporation or association, Lender acknowledges and consents to Borrower’s use of the Mortgaged Property as a housing cooperative. |

| Seniors Housing Loan and Security Agreement (CME) | Page 19 |

| (c) | Without the prior written consent of Lender, which may be granted or withheld in Lender’s discretion, Borrower will not, and will not permit any operator of the Facility to, provide or contract for skilled nursing care, assisted living care, Alzheimer’s care, memory care or dementia care for any of the residents other than that level of care which both (i) is consistent with the Intended Use and (ii) is permissible for Borrower or the operator of the Facility to provide at the Facility under (A) applicable Healthcare Laws, and (B) applicable Licenses. |

| 6.04 | Non-Residential Leases. |

| (a) | Prohibited New Non-Residential Leases or Modified Non-Residential Leases. Borrower will not enter into any New Non-Residential Lease, enter into any Modified Non-Residential Lease or terminate any Non-Residential Lease (including any Non-Residential Lease in existence on the date of this Loan Agreement) without the prior written consent of Lender. |

| (b) | Reserved. |

| (c) | Executed Copies of Non-Residential Leases. Borrower will, without request by Lender, deliver a fully executed copy of each Non-Residential Lease to Lender promptly after such Non-Residential Lease is signed. |

| (d) | Subordination and Attornment Requirements. All Non-Residential Leases will specifically include the following provisions: |

| (i) | The Lease is subordinate to the Lien of the Security Instrument, with such subordination to be self-executing. |

| (ii) | The tenant will attorn to Lender and any purchaser at a foreclosure sale, such attornment to be self-executing and effective upon acquisition of title to the Mortgaged Property by any purchaser at a foreclosure sale or by Lender in any manner. |

| (iii) | The tenant agrees to execute such further evidences of attornment as Lender or any purchaser at a foreclosure sale may from time to time request. |

| (iv) | The tenant will, upon receipt of a written request from Lender following the occurrence of and during the continuance of an Event of Default, pay all Rents payable under the Lease to Lender. |

| (v) | If Lender or a purchaser at a foreclosure sale so elects, the Lease shall not be terminated by foreclosure or any other transfer of the Mortgaged Property. |

| (vi) | After a foreclosure sale of the Mortgaged Property, Lender or any other purchaser at such foreclosure sale may, at Lender’s or such purchaser’s option, accept or terminate such Lease without payment of any fee or penalty. |

| Seniors Housing Loan and Security Agreement (CME) | Page 20 |

| 6.05 | Prepayment of Rents. Borrower will not receive or accept Rent under any Lease (whether a residential Lease or a Non-Residential Lease) for more than 2 months in advance. |

| 6.06 | Inspection. |

| (a) | Right of Entry. Borrower will permit Lender, its agents, representatives and designees and any interested Governmental Authority to make or cause to be made entries upon and inspections of the Mortgaged Property to inspect, among other things (i) Repairs, (ii) Capital Replacements, in process and upon completion, and (iii) Improvements (including environmental inspections and tests performed by professional inspection engineers) during normal business hours, or at any other reasonable time, upon reasonable Notice to Borrower if the inspection is to include occupied residential units (which Notice need not be in writing). During normal business hours, or at any other reasonable time, Borrower will also permit Lender to examine all books and records and contracts and bills pertaining to the foregoing. Notice to Borrower will not be required in the case of an emergency, as determined in Lender’s Discretion, or when an Event of Default has occurred and is continuing. |

| (b) | Inspection of Mold. If Lender determines that Mold has or may have developed as a result of a water intrusion event or leak, Lender, at Lender’s Discretion, may require that a professional inspector inspect the Mortgaged Property to confirm whether Mold has developed and, if so, thereafter as frequently as Lender determines is necessary until any issue with Mold and its cause(s) are resolved to Lender’s satisfaction. Such inspection will be limited to a visual and olfactory inspection of the area that has experienced the Mold, water intrusion event or leak. Borrower will be responsible for the cost of each such professional inspection and any remediation deemed to be necessary as a result of the professional inspection. After any issue with Mold is remedied to Lender’s satisfaction, Lender will not require a professional inspection any more frequently than once every 3 years unless Lender otherwise becomes aware of Mold as a result of a subsequent water intrusion event or leak. |

| (c) | Certification in Lieu of Inspection. If Lender or Loan Servicer determines not to conduct an annual inspection of the Mortgaged Property, and in lieu thereof Lender requests a certification, Borrower will provide to Lender a factually correct certification each year that the annual inspection is waived to the following effect: |

Borrower has not received any written complaint, notice, letter or other written communication from any tenant, Property Manager, operator of the Facility or governmental authority regarding mold, fungus, microbial contamination or pathogenic organisms (“Mold”) or any activity,

| Seniors Housing Loan and Security Agreement (CME) | Page 21 |

condition, event or omission that causes or facilitates the growth of Mold on or in any part of the Mortgaged Property or, if Borrower has received any such written complaint, notice, letter or other written communication, that Borrower has investigated and determined that no Mold activity, condition or event exists or alternatively has fully and properly remediated such activity, condition, event or omission in compliance with the Moisture Management Plan for the Mortgaged Property.

If Borrower is unwilling or unable to provide such certification, Lender may require a professional inspection of the Mortgaged Property at Borrower’s expense.

| 6.07 | Books and Records; Financial Reporting. |

| (a) | Delivery of Books and Records. Borrower will keep and maintain at all times at the Mortgaged Property or the Property Manager’s or operator of the Facility’s office, and upon Lender’s request will make available at the Mortgaged Property (or, at Borrower’s option, at the Property Manager’s or operator of the Facility’s office), complete and accurate books of account and records (including copies of supporting bills and invoices) adequate to reflect correctly the operation of the Mortgaged Property, in accordance with GAAP consistently applied (or such other method which is reasonably acceptable to Lender), and copies of all written contracts, Leases, and other instruments which affect the Mortgaged Property. The books, records, contracts, Leases and other instruments will be subject to examination and inspection by Lender at any reasonable time. |

| (b) | Delivery of Statement of Income and Expenses; Rent Schedule and Other Statements. Borrower will furnish to Lender each of the following: |

| (i) | Within 25 days after the end of each calendar quarter prior to Securitization and within 35 days after each calendar quarter after Securitization, each of the following: |

| (A) | A Rent Schedule dated no earlier than the date that is 5 days prior to the end of such quarter. |

| (B) | A statement of income and expenses for Borrower’s operation of the Mortgaged Property that is either of the following: |

| (1) | For the 12 month period ending on the last day of such quarter. |

| (2) | If at the end of such quarter Borrower or any Affiliate of Borrower has owned the Mortgaged Property for less than 12 months, for the period commencing with the acquisition of the Mortgaged Property by Borrower or its Affiliate, and ending on the last day of such quarter. |

| Seniors Housing Loan and Security Agreement (CME) | Page 22 |

| (C) | A statement of changes in financial position of Borrower relating to the Mortgaged Property for that fiscal quarter and, when requested by Lender, a balance sheet showing all assets and liabilities of Borrower relating to the Mortgaged Property as of the end of that fiscal quarter. |

| (ii) | Within 90 days after the end of each fiscal year of Borrower, each of the following: |

| (A) | An annual statement of income and expenses for Borrower’s operation of the Mortgaged Property for that fiscal year. |

| (B) | A statement of changes in financial position of Borrower relating to the Mortgaged Property for that fiscal year. |

| (C) | A balance sheet showing all assets and liabilities of Borrower relating to the Mortgaged Property as of the end of that fiscal year and a profit and loss statement for Borrower. |

| (D) | An accounting of all security deposits held pursuant to all Leases, including the name of the institution (if any) and the names and identification numbers of the accounts (if any) in which such security deposits are held and the name of the person to contact at such financial institution, along with any authority or release necessary for Lender to access information regarding such accounts. |

| (iii) | Within 30 days after the date of filing, copies of all tax returns filed by Borrower. |

| (c) | Delivery of Borrower Financial Statements Upon Request. Borrower will furnish to Lender each of the following: |

| (i) | Upon Lender’s request, in Lender’s sole and absolute discretion prior to a Securitization, and thereafter upon Lender’s request in Lender’s Discretion, a monthly Rent Schedule and a monthly statement of income and expenses for Borrower’s operation of the Mortgaged Property, in each case within 25 days after the end of each month. |

| (ii) | Upon Lender’s request in Lender’s sole and absolute discretion prior to a Securitization, and thereafter upon Lender’s request in Lender’s Discretion, a statement that identifies all owners of any interest in Borrower and any Designated Entity for Transfers and the interest held by each (unless Borrower or any Designated Entity for Transfers is a publicly-traded entity in which case such statement of ownership will not be required), and if Borrower or a Designated Entity for Transfers is a corporation then all officers and directors of Borrower and the Designated Entity for Transfers, and if Borrower or a Designated Entity for Transfers is a limited liability company then all Managers who are not members, in each case within 10 days after such request. |

| Seniors Housing Loan and Security Agreement (CME) | Page 23 |

| (iii) | Upon Lender’s request in Lender’s Discretion, such other financial information or property management information (including information on tenants under Leases to the extent such information is available to Borrower, copies of bank account statements from financial institutions where funds owned or controlled by Borrower are maintained, and an accounting of security deposits) as may be required by Lender from time to time, in each case within 30 days after such request. |

| (iv) | Upon Lender’s request in Lender’s Discretion, a monthly property management report for the Mortgaged Property, showing the number of inquiries made and rental applications received from tenants or prospective tenants and deposits received from tenants and any other information requested by Lender within 30 days after such request. However, Lender will not require the foregoing more frequently than quarterly except when there has been an Event of Default and such Event of Default is continuing, in which case Lender may require Borrower to furnish the foregoing more frequently. |

| (d) | Form of Statements; Audited Financials. A natural person having authority to bind Borrower (or the SPE Equity Owner or Guarantor, as applicable) will certify each of the statements, schedules and reports required by Sections 6.07(b), 6.07(c) and 6.07(f) to be complete and accurate. Each of the statements, schedules and reports required by Sections 6.07(b), 6.07(c)(i) and (iii) and 6.07(f) will be in such form and contain such detail as Lender may reasonably require. Lender also may require that any of the statements, schedules or reports listed in Sections 6.07(b), 6.07(c) and 6.07(f) be audited at Borrower’s expense by independent certified public accountants acceptable to Lender, at any time when an Event of Default has occurred and is continuing or at any time that Lender, in its reasonable judgment, determines that audited financial statements are required for an accurate assessment of the financial condition of Borrower or of the Mortgaged Property. |

| (e) | Failure to Timely Provide Financial Statements. If Borrower fails to provide in a timely manner the statements, schedules and reports required by Sections 6.07(b), 6.07(c) and 6.07(f), Lender will give Notice to Borrower specifying the statements, schedules and reports required by Sections 6.07(b), 6.07(c) and 6.07(f) that Borrower has failed to provide. If Borrower has not provided the required statements, schedules and reports within 10 Business Days following such Notice, then (i) Borrower will pay a late fee of $500 for each late statement, schedule or report, plus an additional $500 per month that any such statement, schedule or report continues to be late, and (ii) Lender will have the right to have Borrower’s books and records audited, at Borrower’s expense, by independent certified public accountants selected by Lender in order to obtain such statements, schedules and reports, and all related costs and expenses of Lender will become |

| Seniors Housing Loan and Security Agreement (CME) | Page 24 |

immediately due and payable and will become an additional part of the Indebtedness as provided in Section 9.02. Notice to Borrower of Lender’s exercise of its rights to require an audit will not be required in the case of an emergency, as determined in Lender’s Discretion, or when an Event of Default has occurred and is continuing.

| (f) | Delivery of Guarantor and SPE Equity Owner Financial Statements Upon Request. Borrower will cause each Guarantor and, at Lender’s request in Lender’s Discretion, any SPE Equity Owner, to provide to Lender (i) within 90 days after the close of such party’s fiscal year, such party’s balance sheet and profit and loss statement (or if such party is a natural person, within 90 days after the close of each calendar year, such party’s personal financial statements) in form reasonably satisfactory to Lender and certified by such party to be accurate and complete; and (ii) such additional financial information (including copies of state and federal tax returns with respect to any SPE Equity Owner but Lender will only require copies of such tax returns with respect to each Guarantor if an Event of Default has occurred and is continuing) as Lender may reasonably require from time to time and in such detail as reasonably required by Lender. |

| (g) | Reporting Upon Event of Default. If an Event of Default has occurred and is continuing, Borrower will deliver to Lender upon written demand all books and records relating to the Mortgaged Property or its operation. |

| (h) | Credit Reports. Borrower authorizes Lender to obtain a credit report on Borrower at any time. |

| 6.08 | Taxes; Operating Expenses; Ground Rents. |

| (a) | Payment of Taxes and Ground Rent. Subject to the provisions of Sections 6.08(c) and (d), Borrower will pay or cause to be paid (i) all Taxes when due and before the addition of any interest, fine, penalty or cost for nonpayment, and (ii) if Borrower’s interest in the Mortgaged Property is as a Ground Lessee, then the monthly or other periodic installments of Ground Rent before the last date upon which each such installment may be made without penalty or interest charges being added. |

| (b) | Payment of Operating Expenses. Subject to the provisions of Section 6.08(c), Borrower will (i) pay the expenses of operating, managing, maintaining and repairing the Mortgaged Property (including utilities, Repairs and Capital Replacements) before the last date upon which each such payment may be made without any penalty or interest charge being added, and (ii) pay Insurance premiums at least 30 days prior to the expiration date of each policy of Insurance, unless applicable law specifies some lesser period. |

| (c) | Payment of Impositions and Reserve Funds. If Lender is collecting Imposition Reserve Deposits pursuant to Article IV, then so long as no Event of Default |

| Seniors Housing Loan and Security Agreement (CME) | Page 25 |