UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

| ANNUAL REPORT PURSUANT TO SECTION 13 or 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

OR

| | TRANSITION REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number

BLUEKNIGHT ENERGY PARTNERS, L.P.

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) |

|

|

|

| (Address of principal executive offices, zip code)

Registrant’s telephone number, including area code: ( | |

(Former name, former address and former fiscal year, if changed since last report)

Securities Registered Pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbols | Name of each exchange on which registered |

| | | |

| | | |

Securities Registered Pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ☐ | |

| Non-accelerated filer ☐ | Smaller reporting company |

|

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

As of June 30, 2021, the aggregate market value of the registrant’s common units held by non-affiliates of the registrant was approximately $

As of March 1, 2022, there were

|

|

|

Page |

|

|

||

| Business. |

||

| Risk Factors. |

||

| Unresolved Staff Comments. |

21 | |

| Properties. |

||

| Legal Proceedings. |

||

| Mine Safety Disclosures. |

||

|

|

|

|

|

|

||

| Market for Registrant’s Common Equity, Related Unitholder Matters and Issuer Purchases of Equity Securities. |

||

| Reserved. |

||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations. |

||

| Quantitative and Qualitative Disclosures About Market Risk. |

||

| Financial Statements and Supplementary Data. |

||

| Changes in and Disagreements with Accountants on Accounting and Financial Disclosure. |

||

| Controls and Procedures. |

||

|

|

|

|

|

|

||

| Directors, Executive Officers and Corporate Governance. |

||

| Executive Compensation. |

||

| Security Ownership of Certain Beneficial Owners and Management and Related Unitholder Matters. |

||

| Certain Relationships and Related Transactions, and Director Independence. |

41 | |

| Principal Accountant Fees and Services. |

42 | |

|

|

|

|

|

|

||

| Exhibits, Financial Statement Schedules. |

||

| Form 10-K Summary. |

||

DEFINITIONS

We use the following terms in this report:

Finished asphalt products: As used herein, the term refers to: (i) liquid asphalt cement sold directly to end users, and to (ii) asphalt emulsions, asphalt cutbacks, polymer modified asphalt cement, and related asphalt products processed using liquid asphalt cement. The term is also used to refer to various residual fuel oil products directly sold to end users.

Liquid asphalt: A dark brown-to-black cementitious material that is primarily produced by petroleum distillation. When crude oil is separated in distillation towers at a refinery, the heaviest hydrocarbons with the highest boiling points settle at the bottom. These tar-like fractions, called residuum, require relatively little additional processing to become products such as liquid asphalt cement or residual fuel oil. Liquid asphalt cement is primarily used in the road construction and maintenance industry. Residual fuel oil is primarily used as a burner fuel in numerous industrial and commercial business applications. As used herein, the term refers to both liquid asphalt cement and residual fuel oils.

Preferred Units: Series A Preferred Units representing limited partnership interests in our partnership.

Terminalling: The receipt of products for storage into storage tanks and other appurtenant equipment where the products may be commingled with other products of similar quality or where the products may be manufactured and changed; the storage of the products; and the delivery of the products as directed by a distributor into a truck or other transportation vessels.

Throughput: The volume of product transported or passing through a plant, terminal or other facility.

As used in this annual report, unless we indicate otherwise: (1) “Blueknight,” “our,” “we,” “us” and similar terms refer to Blueknight Energy Partners, L.P., together with its subsidiaries, (2) our “General Partner” refers to Blueknight Energy Partners G.P., L.L.C., and (3) “Ergon” refers to Ergon, Inc., its affiliates and subsidiaries (other than our General Partner and us).

Forward-Looking Statements

This report contains “forward-looking statements” within the meaning of the federal securities laws. Statements included in this annual report that are not historical facts (including any statements regarding plans and objectives of management for future operations or economic performance, or assumptions or forecasts related thereto) are forward-looking statements. These statements can be identified by the use of forward-looking terminology including “may,” “will,” “should,” “believe,” “expect,” “intend,” “anticipate,” “estimate,” “continue,” or other similar words. These statements discuss future expectations, contain projections of results of operations or of financial condition, or state other “forward-looking” information. We and our representatives may from time to time make other oral or written statements that are also forward-looking statements.

Such forward-looking statements are subject to various risks and uncertainties that could cause actual results to differ materially from those anticipated as of the date of this report. Although we believe that the expectations or assumptions reflected in these forward-looking statements are based on reasonable assumptions, no assurance can be given that these expectations will prove to be correct. Important factors that could cause our actual results to differ materially from the expectations reflected in these forward-looking statements include, among other things, those set forth in “Item 1A-Risk Factors,” included in this annual report, and those set forth from time to time in our filings with the Securities and Exchange Commission (“SEC”), which are available through the Investors - SEC Filings page at www.bkep.com and through the SEC’s Electronic Data Gathering and Retrieval System (“EDGAR”) at www.sec.gov.

All forward-looking statements included in this report are based on information available to us on the date of this report. We undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise. All subsequent written and oral forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements contained throughout this report.

Overview

Blueknight is a publicly traded master limited partnership with operations in 26 states. We have the largest independent asphalt facility footprint in the nation, and through that we provide integrated terminalling services for companies engaged in the production, distribution, and handling of liquid asphalt that are providing the basic materials for the infrastructure and construction needed to maintain and expand the U.S. economy. We manage our operations through a single segment, asphalt terminalling services.

We previously provided integrated terminalling, gathering, and transportation services for companies engaged in the production, distribution, and marketing of crude oil in three different operating segments: (i) crude oil terminalling services, (ii) crude oil pipeline services, and (iii) crude oil trucking services. On December 21, 2020, we announced we had entered into multiple definitive agreements to sell these segments, and these segments are presented as discontinued operations. The transaction related to the crude oil pipeline services segment closed on February 1, 2021, and the transactions relating to the crude oil trucking services segment closed on December 15, 2020, and February 2, 2021. The transaction related to the crude oil terminalling services segment closed on March 1, 2021.

Our Operations

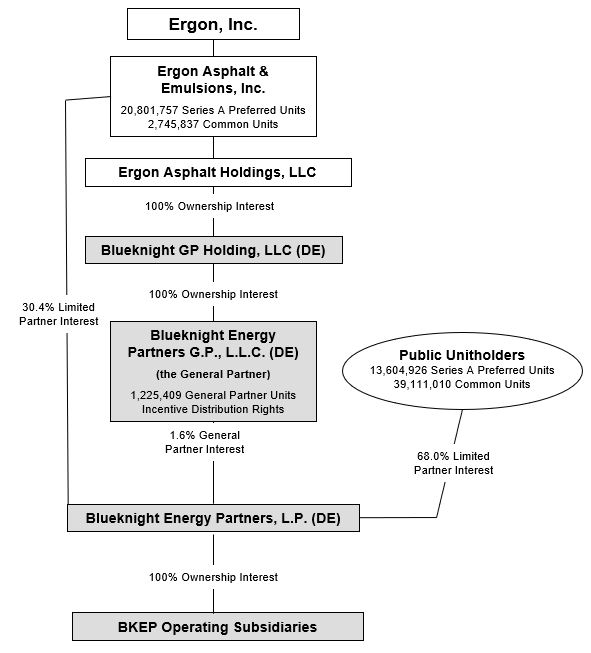

We were formed as a Delaware limited partnership in 2007. Our operating assets are owned by, and our operations are conducted through, our subsidiaries. Our General Partner has sole responsibility for conducting our business and for managing our operations. Ergon owns 100% of the outstanding membership interest of Blueknight GP Holding, L.L.C., which owns 100% of the membership interest of our General Partner.

Our General Partner has no business or operations other than managing our business. In addition, outside of its investment in us, our General Partner owns no assets or property. Our partnership agreement imposes no additional material liabilities upon our General Partner or obligations to contribute to us other than those liabilities and obligations imposed on general partners under the Delaware Revised Uniform Limited Partnership Act.

The following diagram depicts our organizational structure, including our relationship with our affiliates and subsidiaries, as of March 1, 2022:

Our Strengths and Strategies

Business strategy. Our strategy is to be a downstream terminalling solutions provider focused on infrastructure and transportation end-markets. During the first quarter of 2021, we completed the transformational divestitures of our three crude oil business segments. Through these divestitures, we have improved our balance sheet and achieved financial flexibility to pursue accretive growth investments. We have refocused expansion activities on core competencies and inherent competitive advantages in specialty terminalling markets. We plan to redeploy capital and maximize risk-adjusted returns in both organic and non-organic growth projects.

Strategically placed assets. We own 54 asphalt terminalling facilities in 26 states, consisting of approximately 9.0 million barrels of liquid asphalt storage, which we believe are well positioned to provide services in the market areas they serve throughout the continental United States. In addition, we have a focus on leveraging this existing site footprint to increase utilization for other complementary specialty products.

Growth opportunities. We evaluate growth opportunities from multiple angles, including growth through third-party acquisitions and optimizing our existing asset base.

Experienced management team. Our General Partner has an experienced and knowledgeable management team with extensive experience as a service provider in the product handling and construction materials industries. We expect to directly benefit from this management team’s strengths, including significant relationships throughout these industries with customers of our terminalling services.

Our relationship with Ergon. Ergon owns our General Partner and therefore controls our operations. Ergon is a privately held company formed in 1954 and is based in Jackson, Mississippi, with over 3,000 employees globally. Ergon and its subsidiaries are engaged in a wide range of operations that are categorized into six primary business segments: Refining & Marketing, Specialty Chemicals, Asphalt & Emulsions, Midstream & Logistics, Oil & Gas, and Construction & Real Estate. This relationship may provide us with additional capital sources for future growth as well as increased opportunities to provide terminalling services. While this relationship may benefit us, it may also be a source of potential conflicts. Ergon is not restricted from competing with us and may acquire, construct or dispose of additional assets in the future without any obligation to offer us the opportunity to purchase or construct those assets.

Asphalt Industry Overview

Liquid asphalt is one of the oldest engineering materials. Liquid asphalt’s adhesive and waterproofing properties have been used for building structures, waterproofing ships, and numerous other applications.

Production of liquid asphalt begins with the refining of crude oil. When crude oil is separated in distillation towers at a refinery, the heaviest hydrocarbons with the highest boiling points settle at the bottom. These tar-like fractions, called residuum, require relatively little additional processing to become products such as liquid asphalt. Liquid asphalt production typically represents only a small portion of the total product production in the crude oil refining process. The liquid asphalt produced by petroleum distillation can be sold by the refinery either directly into the wholesale or retail liquid asphalt markets.

In its normal state, liquid asphalt cement is too viscous to be used at ambient temperatures. For paving and roofing applications, asphalt cement is heated for handling and transporting to markets. Asphalt cement is generally used as straight-run asphalt cement (asphalt straight from refineries), polymer modified asphalt (PMA) or emulsified in a water base with emulsifying chemicals by a colloid mill (asphalt emulsions) and handled and transported at lower temperatures.

Hot mix asphalt is produced by mixing asphalt cement and heated with aggregate (stone, sand and/or gravel). The hot mix asphalt is loaded into trucks for transport to the paving site, where it is placed on the road surface by paving machines and compacted by rollers. Hot mix asphalt is used for roofing applications, new construction, reconstruction, and for thin maintenance overlay on existing roads.

Polymer modified asphalt is produced by mixing asphalt cement and heated with various qualities of polymers and chemicals to produce a higher quality of finished material that provides greater durability and elasticity for various markets. Polymer modified asphalt can also be included in asphalt emulsions. The polymer modified asphalt is loaded into trucks for transport to the paving site, or the hot mix facility, where it is then placed on the road surface by paving machines and compacted by rollers. Polymer modified asphalt is used for roofing applications, new construction, reconstruction, and for thin maintenance overlay on existing roads.

Asphalt emulsions are used for a variety of applications, including spraying as a tack coat between an old pavement and a new hot mix asphalt overlay, cold mix pothole patching material, and preventive maintenance surface applications such as chip seals. Asphalt emulsions are also used for fog seal, slurry seal, scrub seal, sand seal and microsurfacing maintenance treatments, warm mix emulsion/aggregate mixtures, base stabilization, and in-place recycling.

The asphalt industry in the United States is characterized by a high degree of seasonality. Much of this seasonality is due to the impact that weather conditions have on road construction schedules, particularly in cold weather states. Refineries produce liquid asphalt year-round, but the peak asphalt demand season is during the warm weather months when most of the road construction activity in the United States takes place. Liquid asphalt marketers and finished asphalt product producers with access to storage capacity possess the inherent advantage of being able to purchase supply from refineries on a year-round basis and then sell finished asphalt products in the peak summer demand season.

Asphalt Terminalling Services

We provide asphalt terminalling services to marketers and distributors of liquid asphalt and asphalt-related products. We do not take title to the product. With approximately 9.0 million barrels of liquid asphalt cement storage capacity, we are able to provide our customers the ability to effectively manage their liquid asphalt inventories while allowing significant flexibility in their processing and marketing activities. As of March 1, 2022, we have 54 terminals located in 26 states and, as such, are well-positioned to provide asphalt terminalling services in the market areas we serve throughout the continental United States.

We serve the asphalt industry by providing our customers access to their market areas through a combination of leasing our liquid asphalt facilities and providing terminalling services at certain facilities. We generate revenues by charging a fee for the lease of a facility or for services provided as asphalt products are terminalled at our facilities.

As of March 1, 2022, we have leases and terminalling agreements relating to all of our asphalt facilities, including 28 under contract with Ergon. Our agreements have, based on a weighted average of remaining fixed revenue, approximately 5.3 years remaining under their terms. Based on tank capacity, approximately 13% of capacity, all with third parties, expire in late 2022 if not renewed with the current customer or a new customer, and the remaining capacity expires at varying times thereafter, through 2035. We may not be able to extend, renegotiate or replace these contracts when they expire, and the terms of any renegotiated contracts may not be as favorable as the contracts they replace.

At leased facilities, our customers conduct the operations at the asphalt facility, including the storage and processing of asphalt products, and we collect a monthly rental fee relating to the lease of such facility. Generally, under the terms of those leases, (i) title to the asphalt, raw materials or finished asphalt products received, unloaded, stored, or otherwise handled at such asphalt facility is in the name of the lessee; (ii) the lessee is responsible for complying with environmental, health, safety, transportation and security laws; (iii) the lessee is required to obtain and maintain necessary permits, licenses, plans, approvals, or other such authorizations and is required to provide insurance for such asphalt facility; and (iv) most routine maintenance and repairs of such asphalt facility are the responsibility of the lessee.

We do not take title to or have marketing responsibility for the liquid asphalt product at terminals we operate. As a result, our asphalt operations have minimal direct exposure to changes in commodity prices, but the volumes of liquid asphalt we terminal are indirectly affected by commodity prices.

The following table provides an overview of our asphalt facilities as of March 1, 2022:

| Total Tankage |

||||

| Location |

Number of Facilities |

(in thousands of bbls)(1) |

||

| Alabama |

1 |

205 |

||

| Arizona |

1 |

66 |

||

| Arkansas |

1 |

21 |

||

| California |

1 |

66 |

||

| Colorado |

5 |

736 |

||

| Georgia |

2 |

192 |

||

| Idaho |

1 |

285 |

||

| Illinois |

2 |

232 |

||

| Indiana |

1 |

156 |

||

| Kansas |

5 |

662 |

||

| Missouri |

3 |

662 |

||

| Mississippi |

1 |

202 |

||

| Montana |

1 |

123 |

||

| Nebraska |

1 |

292 |

||

| New Jersey |

1 |

459 |

||

| Nevada |

1 |

280 |

||

| North Carolina |

1 |

243 |

||

| Ohio |

1 |

38 |

||

| Oklahoma |

7 |

1,420 |

||

| Pennsylvania |

1 |

59 |

||

| Tennessee |

4 |

770 |

||

| Texas |

4 |

248 |

||

| Utah |

2 |

300 |

||

| Virginia |

2 |

635 |

||

| Washington |

3 |

468 |

||

| Wyoming |

1 |

220 |

||

| Total |

54 |

9,040 |

| (1) |

Total tankage refers to the approximate total capacity of all tanks. |

Our asphalt assets range in age from one year to over 50 years, and we expect that our storage tanks and related assets will have an average remaining life in excess of 20 years.

Significant Customers. For the year ended December 31, 2021, Ergon accounted for at least 40% but not more than 45% of our total asphalt terminalling services revenue. Two third-party customers each accounted for at least 10% but not more than 15% of asphalt terminalling services revenue in 2021. The loss of any of those customers could have a material adverse effect on our business, cash flows and results of operations. No other customer accounted for more than 10% of our revenue during 2021. As of March 1, 2022, we have terminalling agreements or operating leases with Ergon for 28 of our asphalt facilities. For more information regarding the Ergon agreements, please see Note 12 to our consolidated financial statements.

Competition

We compete with regional and local terminalling companies of widely varying sizes, financial resources, and experience. Participants range in size from major companies to small family-owned businesses. We are subject to competition from other terminalling operations that may be able to supply our customers with the same or comparable services on a more competitive basis. Our ability to compete could be harmed by factors we cannot control, including the perception that another company can provide better service or a decision by our competitors to acquire or construct asphalt terminalling assets and provide terminalling services in geographic areas, or to customers, served by our assets and services. Competition we are subject to is mitigated by our long-term contracts, the fact that we do not market products, and high barriers to entry from new construction. If we are unable to compete effectively with services offered by other asphalt terminalling companies, our financial results and ability to make distributions to our unitholders may be adversely affected. Additionally, we also compete with regional and local companies for asset acquisitions and expansion opportunities. Some of these competitors are substantially larger than us and have greater financial resources and lower costs of capital than we do.

Environmental, Health and Safety Risk

Federal, state and local laws and regulations related to zoning, land use, air emissions (including greenhouse gases), water discharges, waste management and disposal, noise, odor and dust control, and other environmental, health and safety and security matters govern our operations. Some of our operations require permits or other government-issued authorizations, which may impose additional operating standards, and are subject to modification renewal and revocation. We commit resources to achieve and maintain compliance with all applicable laws and regulations, however the risk of liabilities, particularly environmental liabilities, is inherent in the operation of our businesses. These potential liabilities could result in material costs, including for fines or personal injury or damages claims, which could have an adverse impact on our operations and profitability.

Future events, including changes in existing laws or regulations or enforcement policies, or further investigation or evaluation of the potential health hazards of the products handled or business activities may result in additional or unanticipated compliance and other costs. We could be required to invest in preventive or remedial action, like control equipment, which could be substantial, or which could result in restrictions on our operations or delays in obtaining required permits or other approvals.

Our operations are subject to manufacturing, operating, and handling risks associated with the products we produce and the products we use in our operations, including the related storage of finished products, hazardous substances, and wastes. We are exposed to potential hazards including storage tank leaks, explosions, discharges or releases of hazardous substances, health hazard exposure, documentation and reporting failures and the operation of mobile equipment and manufacturing machinery. These risks can subject us to potential liabilities relating to personal injury or death, or property damage, and may result in civil or criminal penalties, which could have an adverse impact on our productivity or profitability. We may be called upon to investigate and remediate environmental contamination relating to our prior or current operations, as well as operations we have acquired from others, or we may be named as a defendant in litigation brought by governmental agencies or private parties.

Operational Hazards and Insurance

Terminals and similar facilities may experience damage as a result of an accident or natural disaster. These hazards can cause personal injury and loss of life, severe damage to and destruction of property and equipment, pollution or environmental damage, and suspension of operations. We maintain insurance of various types and varying levels of coverage which we consider adequate under the circumstances to cover our operations and properties, including coverage for pollution-related events. However, such insurance does not cover every potential risk associated with operating terminals and other facilities. In 2020, we experienced increased costs as insurers are increasing premiums to ameliorate recent losses. Through the utilization of deductibles and retentions, where appropriate and efficient, we self-insure the “working layer” of loss activity to create a more efficient and cost-effective program. The working layer consists of high-frequency/low-severity losses that are best retained and managed in-house. We continue to monitor our retentions as they relate to the overall cost and scope of our insurance program.

Employees

As of December 31, 2021, we had approximately 130 full-time employees. None of these employees are represented by labor unions or covered by any collective bargaining agreement.

Financial Information about Segments

We operate our asphalt terminalling facilities under a single operating segment.

Available Information

We provide public access to our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to these reports filed with the SEC under the Securities and Exchange Act of 1934. These documents may be accessed free of charge on our website, www.bkep.com, as soon as is reasonably practicable after their filing with the SEC. Information contained on our website is not incorporated by reference in this report or any of our other filings. The SEC also maintains a website which contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC. The SEC’s website is www.sec.gov.

Limited partner interests are inherently different from the capital stock of a corporation, although many of the business risks to which we are subject are similar to those that would be faced by a corporation engaged in a similar business. You should carefully consider the following risk factors together with all of the other information included in this report. If any of the following risks were actually to occur, our business, financial condition, results of operations and cash flows could be materially adversely affected. In that case, we might not be able to pay distributions on our units, the trading price of our units could decline and our unitholders could lose all or part of their investment.

Risks Related to our Business

We may not have sufficient cash from operations following the establishment of cash reserves and payment of fees and expenses, including cost reimbursements to our General Partner, to enable us to make cash distributions to holders of our units at our current distribution rate.

In order to make cash distributions on our Preferred Units at the preference distribution rate of $0.17875 per unit per quarter, or $0.715 per unit per year, and on our common units at the current quarterly distribution of $0.0425 per unit per quarter, or $0.17 per unit per year, we will require available cash of approximately $8.1 million per quarter, or $32.4 million per year. We may not have sufficient available cash from operating surplus each quarter to enable us to make cash distributions on our Preferred Units at the preference rate or on our common units at the current quarterly distribution rate. The amount of cash we can distribute on our units principally depends upon the amount of cash we generate from our operations, which will fluctuate from quarter to quarter based on, among other things, the risks described herein.

In addition, the actual amount of cash we will have available for distribution will depend on other factors, including:

| • |

the level of capital expenditures we make; |

| • |

the cost of acquisitions; |

| • |

our debt service requirements and other liabilities; |

| • |

fluctuations in our working capital needs; |

| • |

our ability to borrow funds and access capital markets; |

| • |

restrictions contained in our credit facility or other debt agreements; and |

| • |

the amount of cash reserves established by our General Partner. |

We depend on certain key customers for a portion of our revenues and are exposed to credit risks of these customers. The loss of or material nonpayment or nonperformance by any of these key customers could adversely affect our financial condition, results of operations and cash flows.

We rely on certain key customers for a portion of our revenues. For example, Ergon Asphalt and Emulsion, Inc., a wholly-owned subsidiary of Ergon, Inc., represented at least 40% but not more than 45% of our total revenue in 2021. Ergon is a private company and we have limited information regarding its financial condition. Ergon comprised 11% of total accounts receivable at December 31, 2021.

In addition to Ergon, we have two other key customers that each accounted for at least 10% but not more than 15% of total revenue in 2021. Four third-party customers each accounted for between 10% and 25% of accounts receivable at December 31, 2021.

We may be unable to negotiate extensions or replacements of contracts with key customers on favorable terms. In addition, some of these key customers may experience financial problems which could have a significant effect on their creditworthiness. Severe financial problems encountered by our customers could limit our ability to collect amounts owed to us or to enforce performance of obligations under contractual arrangements. Additionally, many of our customers finance their activities through cash flows from operations, the incurrence of debt or the issuance of equity. The reduction of cash flows resulting from a reduction in borrowing bases under credit facilities, the lack of availability of debt or equity financing, or any combination of such factors may result in a significant reduction of our customers’ liquidity and limit their ability to make payments or perform on their obligations to us. Furthermore, some of our customers may be highly leveraged and subject to their own operating and regulatory risks, which increases the risk that they may default on their obligations to us. The loss of all or even a portion of the contracted fees of these key customers, as a result of competition, creditworthiness or otherwise, could have a material adverse effect on our business, cash flows, ability to make distributions to our unitholders, unit price, results of operations and ability to conduct our business.

The amount of cash we have available for distribution to holders of our units depends primarily on our cash flows and not solely on earnings reflected in our financial statements. Consequently, even if we are profitable and are otherwise able to pay distributions, we may not be able to make cash distributions to holders of our units.

Our unitholders should be aware that the amount of cash we have available for distribution depends primarily upon our cash flows and not solely on earnings reflected in our financial statements, which will be affected by non-cash items. As a result, we may make cash distributions, if permitted by our credit agreement, during periods when we record losses for financial accounting purposes and may not make cash distributions during periods when we record net earnings for financial accounting purposes.

Our debt levels under our credit agreement may limit our ability to make distributions and our flexibility in obtaining additional financing and in pursuing other business opportunities.

As of December 31, 2021, we had $98.0 million in outstanding indebtedness, excluding approximately $0.6 million in outstanding letters of credit, under our $300.0 million credit agreement. Our level of debt under the credit agreement could have important consequences for us, including the following:

| • |

Our ability to obtain additional financing, if necessary, for working capital, capital expenditures, acquisitions or other purposes may be impaired or such financing may not be available on favorable terms. |

| • |

We will need a substantial portion of our cash flows to make principal and interest payments on our debt, reducing the funds that would otherwise be available for operations, future business opportunities and distributions to unitholders. |

| • |

We could be more vulnerable to competitive pressures or a downturn in our business or the economy generally. |

| • |

Our flexibility in responding to changing business and economic conditions may be limited. |

Our ability to service our debt will depend upon, among other things, our future financial and operating performance, which will be affected by prevailing economic conditions and financial, business, regulatory and other factors. Our ability to service debt under our credit agreement also will depend on market interest rates, since the interest rates applicable to our borrowings will fluctuate with the eurodollar rate or the prime rate. If our operating results are not sufficient to service our current or future indebtedness, we may be forced to take actions such as reducing distributions, reducing or delaying our business activities, acquisitions, investments or capital expenditures, selling assets, restructuring or refinancing our debt, or seeking additional equity capital. We may not be able to effect any of these actions on satisfactory terms, or at all.

Restrictions in our credit agreement could materially adversely affect our business, financial condition, results of operations, ability to make cash distributions to unitholders and value of our units.

We are dependent upon the earnings and cash flows generated by our operations to meet our debt service obligations and to make cash distributions to our unitholders. The operating and financial restrictions and covenants in our credit agreement and any future financing agreements could restrict our ability to finance future operations or capital needs or to expand or pursue our business activities, which may, in turn, limit our ability to make cash distributions to our unitholders. For example, our credit agreement restricts our ability to, among other things:

| • |

incur or guarantee certain additional debt; |

| • |

make certain cash distributions on or redeem or repurchase certain units; |

| • |

make certain investments and acquisitions; |

| • |

make certain capital expenditures; |

| • |

incur certain liens or permit them to exist; |

| • |

enter into certain types of transactions with affiliates; |

| • |

merge or consolidate with another company or otherwise engage in a change of control transaction; and |

| • |

transfer, sell or otherwise dispose of certain assets. |

Our credit agreement also contains covenants requiring us to maintain certain financial ratios and meet certain financial tests. Our ability to meet those financial ratios and financial tests can be affected by events beyond our control, and we cannot guarantee that we will meet those ratios and tests.

The provisions of our credit agreement may affect our ability to obtain future financing and pursue attractive business opportunities, as well as affect our flexibility in planning for, and reacting to, changes in business conditions. In addition, a failure to comply with the provisions of our credit agreement could result in a default or an event of default that could enable our lenders to declare the outstanding principal of that debt, together with accrued and unpaid interest, to be immediately due and payable. If we were unable to repay the accelerated amounts, the lenders under our credit agreement could proceed against the collateral granted to them to secure such debt. If the payment of our debt is accelerated, our assets may be insufficient to repay such debt in full, and our unitholders could experience a partial or total loss of their investment. The credit agreement also has cross default provisions that apply to any other indebtedness we may have, and the indentures have cross default provisions that apply to certain other indebtedness.

We may not be able to raise sufficient capital to grow our business.

As of March 1, 2022, we have aggregate unused credit availability under our credit agreement of approximately $189.4 million, plus cash on hand of approximately $1.1 million. Our ability to borrow funds under our credit facility may be limited by the financial covenants in our credit agreement. Our ability to access the public capital markets on terms acceptable to us or at all may be limited due to, among other things, general economic conditions, rising interest rates, capital market volatility, the uncertainty of our future cash flows, adverse business developments and other contingencies. In addition, we may have difficulty obtaining a credit rating or any credit rating that we do obtain may be lower than it otherwise would be due to these uncertainties. The lack of a credit rating or a low credit rating may also adversely impact our ability to access capital markets on terms acceptable to us or at all, and may increase significantly the costs of financing our growth potential. The credit agreement includes procedures for additional financial institutions to become revolving lenders, or for any existing lender to increase its revolving commitment thereunder, subject to an aggregate maximum of $450.0 million for all revolving loan commitments under the credit agreement.

If we fail to raise additional capital or an event of default occurs under our credit agreement, we may be forced to sell assets or take other action that could have a material adverse effect on our business, unit price and results of operations. In addition, if we are unable to access the capital markets for acquisitions or expansion projects on terms acceptable to us or at all, or if the financing cost related to any such acquisitions or expansion projects increases, it may have a material adverse effect on our business, cash flows, ability to make distributions to our unitholders, unit price, results of operations and ability to conduct our business.

If we borrow funds to make any permitted quarterly distributions, our ability to pursue acquisitions and other business opportunities may be limited and our operations may be materially and adversely affected.

Available cash for the purpose of making distributions to unitholders includes working capital borrowings. If we borrow funds to pay one or more quarterly distributions, such amounts will incur interest and must be repaid in accordance with the terms of our credit agreement. In addition, any amounts borrowed for permitted distributions to our unitholders will reduce the funds available to us for other purposes under our credit agreement, including amounts available for use in connection with acquisitions and other business opportunities. If we are unable to pursue our growth strategy due to our limited ability to borrow funds, our operations may be materially and adversely affected.

Our revenues from third-party customers are generated under contracts that must be renegotiated periodically and that allow the customer to reduce or suspend performance in some circumstances, which could cause our revenues from those contracts to decline and reduce our ability to make distributions to our unitholders.

Some of our contract-based revenues from customers are generated under contracts with terms which allow the customer to reduce or suspend performance under the contract in specified circumstances, such as the occurrence of a catastrophic event to our or the customer’s operations. The occurrence of an event which results in a material reduction or suspension of our customer’s performance could have a material adverse effect on our financial condition, results of operations and cash flows.

Our contracts with some of our customers have remaining terms of one year or less. As these contracts expire, they must be extended and renegotiated or replaced. We may not be able to extend and renegotiate or replace these contracts when they expire, and the terms of any renegotiated contracts may not be as favorable as the contracts they replace. In particular, our ability to extend or replace contracts could be harmed by numerous competitive factors, such as those described above under “Item 1. Business - Competition.” If we cannot successfully renew significant contracts or must renew them on less favorable terms, or if we incur substantial costs in modifying our terminals, our revenues from these arrangements could decline, which could have a material adverse effect on our financial condition, results of operations and cash flows.

Certain of our asphalt terminalling services contracts have short remaining terms, and certain leases relating to our asphalt operations may be terminated upon short notice.

As of March 1, 2022, we had leases or terminalling agreements with customers for all of our 54 asphalt facilities. Approximately 13% of our tank capacity, all with third parties, will expire by the end of 2022 if not renewed with the current customer or a new customer. We may not be able to renew or extend our existing contracts or enter into new leases or terminalling agreements when such contracts expire on terms acceptable to us or at all. In addition, certain key customers account for a significant portion of our asphalt terminalling services revenues, the loss of which could result in a significant decrease in revenues from our asphalt operations. A significant decrease in the revenues we receive from our asphalt operations could result in violations of covenants under our credit agreement and could have a material adverse effect on our business, cash flows, ability to make distributions to our unitholders, unit price, results of operations, and ability to conduct our business.

In addition, certain of our asphalt facilities are located on land that we lease from third parties. Some of these leases may be terminated by the lessor with as short as thirty days’ notice. We also have not yet received consent from certain of the lessors to sublease such facilities, which may result in a default under such lease or invalidate the subleases. If such leases were terminated, it could have a material adverse effect on our ability to provide asphalt terminalling services, which could have a material adverse effect on our business, cash flows, ability to make distributions to our unitholders, unit price, results of operations, and ability to conduct our business. In addition, in certain instances we have not entered into new leases with a lessor, although we continue to operate under expired leases and make payments to the lessor and are in the process of negotiating new leases. If it were determined that we did not have rights under these expired leases, it could have a material adverse effect on our ability to conduct our asphalt operations and on our financial condition, results of operations and cash flows.

We may not be fully insured against all risks incident to our business and could incur substantial liabilities as a result.

We may not be able to maintain or obtain insurance of the type and amount we desire at reasonable rates. As a result of changing market conditions, premiums and deductibles for certain of our insurance policies may increase substantially in the future. In some instances, certain insurance could become unavailable or available only for reduced amounts of coverage. If we were to incur a significant liability for which we were not fully insured, it could have a material adverse effect on our business, cash flows, ability to make distributions to our unitholders, unit price, results of operations, and ability to conduct our business.

A significant decrease in demand for liquid asphalt products in the areas served by our operations could reduce our ability to make distributions to our unitholders.

A sustained decrease in demand for liquid asphalt products in the areas served by our terminalling facilities could significantly reduce our revenues and, therefore, reduce our ability to make or increase distributions to our unitholders. Factors that could lead to a decrease in market demand for liquid asphalt products include: lower demand by consumers for refined products, including asphalt products, as a result of (i) recession or other adverse economic conditions; (ii) higher prices caused by an increase in the market price of crude oil; or (iii) higher taxes or other governmental or regulatory actions that increase, directly or indirectly, the cost of gasoline or other refined products.

A material decrease in the production of liquid asphalt could materially reduce our ability to make distributions to our unitholders.

The throughput at our asphalt facilities depends on the availability of attractively priced liquid asphalt produced from the various liquid asphalt producing refineries. Liquid asphalt production may decline for a number of reasons, including refiners processing more light, sweet crude oil or refiners installing coker units which further refine heavy residual fuel oil bottoms such as liquid asphalt. If our customers are unable to replace volumes lost due to a temporary or permanent material decrease in production from the suppliers of liquid asphalt, our throughput could decline, reducing our revenue and cash flows and adversely affecting our financial condition and results of operations.

If we are unable to make acquisitions on economically acceptable terms, our future growth may be limited.

Our ability to grow in the future will depend, in part, on our ability to make acquisitions that result in an increase in the cash generated per unit from operations. If we are unable to make accretive acquisitions because we are (i) unable to acquire projects when they are available; (ii) unable to identify attractive acquisition candidates or negotiate acceptable purchase contracts with them; (iii) unable to obtain financing for these acquisitions on economically acceptable terms; or (iv) outbid by competitors, then our future growth and ability to increase distributions may be limited. Furthermore, even if we do make acquisitions that we believe will be accretive, these acquisitions may nevertheless result in a decrease in the cash generated from operations per unit.

Any acquisition involves potential risks, including, among other things:

| • |

inaccurate assumptions about volumes, revenues and costs, including synergies; |

| • |

an inability to integrate successfully the businesses we acquire; |

| • |

an inability to hire, train or retain qualified personnel to manage and operate our business and assets; |

| • |

the assumption of unknown liabilities; |

| • |

limitations on rights to indemnity from the seller; |

| • |

mistaken assumptions about the overall costs of equity or debt; |

| • |

the diversion of management’s and employees’ attention from other business concerns; |

| • |

unforeseen difficulties operating in new product areas or new geographic areas; and |

| • |

customer or key employee losses at the acquired businesses. |

If we consummate any future acquisitions, our capitalization and results of operations may change significantly, and our unitholders likely will not have the opportunity to evaluate the economic, financial, and other relevant information that we will consider in determining the application of these funds and other resources.

If we acquire assets that are distinct and separate from our existing terminalling operations, it could subject us to additional business and operating risks.

We may acquire assets that have operations in new and distinct lines of business from our liquid asphalt operations. Integration of a new business is a complex, costly and time-consuming process. Failure to timely and successfully integrate acquired entities’ lines of business with our existing operations may have a material adverse effect on our business, financial condition, results of operations and cash flows. The difficulties of integrating a new business with our existing operations include, among other things:

| • |

operating distinct businesses which require different operating strategies and different managerial expertise; |

| • |

the necessity of coordinating organizations, systems and facilities in different locations; |

| • |

integrating personnel with diverse business backgrounds and organizational cultures; and |

| • |

consolidating corporate and administrative functions. |

In addition, the diversion of our attention and any delays or difficulties encountered in connection with the integration of a new business, such as unanticipated liabilities or costs, could harm our existing business, results of operations, financial condition, and prospects. Furthermore, new lines of business may subject us to additional business and operating risks. These new business and operating risks could have a material adverse effect on our financial condition, results of operations and cash flows.

Expanding our business by constructing new assets subjects us to risks that projects may not be completed on schedule and that the costs associated with projects may exceed our expectations and budgets, which could cause our cash available for distribution to our unitholders to be less than anticipated.

The construction of additions or modifications to our existing assets and the construction of new assets involves numerous regulatory, environmental, political, legal, and operational uncertainties and requires the expenditure of significant amounts of capital. If we undertake these types of projects, they may not be completed on schedule or at all or within the budgeted cost. Moreover, we may construct facilities to capture anticipated future growth in demand in a market in which such growth does not materialize.

Our expansion projects may not immediately produce operating cash flows.

Expansion projects require significant capital investments over time, and we will incur financing costs during the planning and construction phases of these projects; however, the operating cash flows we expect these projects to generate will not materialize, if at all, until sometime after the projects are completed and placed into service. As a result, to the extent we finance our projects with borrowings, our leverage may increase during the period prior to the generation of those operating cash flows and, to the extent we finance our projects with equity, our cash available for distribution on a common unit basis may decrease during the period prior to the generation of those operating cash flows. If we experience unanticipated or extended delays in generating operating cash flows from construction projects, or if such operating cash flows do not materialize as expected, we may need to reduce or reprioritize our capital budget in order to meet our capital requirements, and our liquidity and capital position could be adversely affected.

Our business involves many hazards and operational risks, including adverse weather conditions, which could cause us to incur substantial liabilities.

Our operations are subject to the many hazards inherent in the terminalling of liquid asphalt cement, including:

| • |

explosions, earthquakes, fires and accidents; |

| • |

extreme weather conditions, such as hurricanes, which are common in the Gulf Coast and East Coast regions, and tornadoes and flooding, which are common in the Midwest and other areas of the United States in which we operate; |

| • |

damage to our terminals and equipment; |

| • |

leaks or releases of liquid asphalt product into the environment; and |

| • |

acts of terrorism or vandalism. |

If any of these events were to occur, we could suffer substantial losses because of personal injury or loss of life, severe damage to and destruction of property and equipment and pollution or other environmental damage resulting in curtailment or suspension of our related operations. In addition, mechanical malfunctions, faulty measurement or other errors may result in significant costs or lost revenues.

We could be negatively impacted by the outbreak of coronavirus (COVID-19).

In light of the uncertain situation relating to the coronavirus (COVID-19), including resurgences and variants of the virus, this public health concern could pose a risk to our employees, our customers, our vendors and the communities in which we operate, which could negatively impact our business. While COVID-19 has not had a significant impact on our business thus far, the extent to which COVID-19 could impact our business will depend on future developments, which are uncertain and cannot be predicted at this time. We continue to monitor the situation, have actively implemented policies and practices to address the situation, and may adjust our current policies and practices as more information and guidance become available.

We do not own all of the land on which our facilities are located, which could disrupt our operations.

We do not own all of the land on which our asphalt facilities have been constructed, and we are therefore subject to the possibility of more onerous terms and/or increased costs to retain necessary land use if any material real property leases are invalid, lapse or terminate. We obtain the rights to construct and operate some of our asphalt facilities on land owned by third parties and governmental agencies for a specific period of time. Our loss of these rights through our inability to renew leases, could have a material adverse effect on our business, results of operations, financial condition, cash flows and ability to make cash distributions to our unitholders. In addition, we are in the process of obtaining consents from the lessors for certain leased property that was transferred to us as part of the acquisition of our asphalt assets. If any consent is denied, it could have a material adverse effect on our business, results of operations, financial condition, cash flows and our ability to make cash distributions to our unitholders.

Terrorist or cyber-attacks and threats, escalation of military activity in response to these attacks, or acts of war could have a material adverse effect on our business, financial condition or results of operations.

Terrorist attacks and threats, cyber-attacks, escalation of military activity, or acts of war may have significant effects on general economic conditions, fluctuations in consumer confidence and spending, and market liquidity, each of which could materially and adversely affect our business. Terrorist or cyber-attacks, rumors or threats of war, actual conflicts involving the United States or its allies, or military or trade disruptions may significantly affect our operations and those of our customers. Strategic targets, such as infrastructure-related and energy-related assets, may be at greater risk of future attacks than other targets in the United States. We do not maintain specialized insurance for possible exposures resulting from a cyber-attack on our assets that may shut down all or part of our business. Disruption or significant increases in commodity prices could result in government-imposed price controls. It is possible that any of these occurrences, or a combination of them, could have a material adverse effect on our business, financial condition, and results of operations.

The threat and impact of cyberattacks may adversely impact our operations and could result in information theft, data corruption, operational disruption, and/or financial loss.

We depend on digital technology, including information systems and related infrastructure as well as cloud applications and services, to store, transmit, process, and record sensitive information (including trade secrets, employee information and financial and operating data), communicate with our employees and business partners and for many other activities related to our business. Our business processes depend on the availability, capacity, reliability and security of our information technology infrastructure and our ability to expand and continually update this infrastructure in response to our changing needs and, therefore, it is critical to our business that our facilities and infrastructure remain secure. While we have implemented strategies to mitigate impacts from these types of events, we cannot guarantee that measures taken to defend against cybersecurity threats will be sufficient for this purpose. The ability of the information technology function to support our business in the event of a security breach or a disaster such as fire or flood and our ability to recover key systems and information from unexpected interruptions cannot be fully tested, and there is a risk that, if such an event occurs, we may not be able to address immediately the repercussions of the breach or disaster. In that event, key information and systems may be unavailable for a number of days or weeks, leading to our inability to conduct business or perform some business processes in a timely manner. Moreover, if any of these events were to materialize, they could lead to losses of sensitive information, critical infrastructure, personnel or capabilities essential to our operations and could have a material adverse effect on our reputation, financial condition or results of operations.

Our employees have been and will continue to be targeted by parties using fraudulent “spoof” and “phishing” emails to misappropriate information or to introduce viruses or other malware through “trojan horse” programs to our computers. These emails appear to be legitimate emails but direct recipients to fake websites operated by the sender of the email or request that the recipient send a password or other confidential information through email or download malware. “Spoof” and “phishing” activities are a serious risk that may damage our information technology infrastructure.

If we fail to maintain an effective system of internal controls, we may not be able to accurately report our financial results or prevent fraud. In addition, potential changes in accounting standards might cause us to revise our financial results and disclosure in the future.

Effective internal controls are necessary for us to provide timely and reliable financial reports and effectively prevent fraud. If we cannot provide timely and reliable financial reports or prevent fraud, our reputation and operating results would be harmed. We continue to enhance our internal controls and financial reporting capabilities. These enhancements require a significant commitment of resources, personnel and the development and maintenance of formalized internal reporting procedures to ensure the reliability of our financial reporting. Our efforts to update and maintain our internal controls may not be successful, and we may be unable to maintain adequate controls over our financial processes and reporting now or in the future, including future compliance with the obligations under Section 404 of the Sarbanes-Oxley Act of 2002. Any failure to maintain effective controls or difficulties encountered in the effective improvement of our internal controls could prevent us from timely and reliably reporting our financial results and may harm our operating results. Ineffective internal controls could also cause investors to lose confidence in our reported financial information. In addition, the Financial Accounting Standards Board or the SEC could enact new accounting standards that might affect how we are required to record revenues, expenses, assets and liabilities. Any significant change in accounting standards or disclosure requirements could have a material effect on our business, results of operations, financial condition and ability to comply with our debt obligations.

Risks Inherent in an Investment in Us

Ergon controls our General Partner, which has sole responsibility for conducting our business and managing our operations. Our General Partner has conflicts of interest with us and limited fiduciary duties, which may permit it to favor its own interests to the detriment of our unitholders.

Ergon owns and controls our General Partner. Some of our General Partner’s directors are directors and officers of Ergon. Therefore, conflicts of interest may arise between our General Partner, on the one hand, and us and our unitholders, on the other hand. In resolving those conflicts of interest, our General Partner may favor its own interests and the interests of its affiliates over the interests of our unitholders. Although the conflicts committee of the board of directors of our General Partner (the “Board”) may review such conflicts of interest, the Board is not required to submit such matters to the conflicts committee. These conflicts include, among others, the following situations:

| • |

Neither our partnership agreement nor any other agreement requires our General Partner or Ergon to pursue a business strategy that favors us. Such persons may make decisions in their best interest, which may be contrary to our interests. |

| • |

Our General Partner is allowed to consider the interests of parties other than us and our unitholders, such as Ergon and its affiliates, in resolving conflicts of interest. |

| • |

If we do not have sufficient available cash from operating surplus, our General Partner could cause us to use cash from non-operating sources, such as asset sales, issuances of securities and borrowings, to pay distributions, which means that we could make distributions that deteriorate our capital base and that our General Partner could receive distributions on its incentive distribution rights to which it would not otherwise be entitled if we did not have sufficient available cash from operating surplus to make such distributions. |

| • |

Ergon is a holder of our Preferred Units and may favor its own interests in actions relating to such units, including causing us to make distributions on such units even if no distributions are made on the common units. |

| • |

Ergon may compete with us, including with respect to future acquisition opportunities. |

| • |

Ergon may favor its own interests in proposing the terms of any acquisitions we make directly from them, and such terms may not be as favorable as those we could receive from an unrelated third party. |

| • |

Our General Partner has limited liability and reduced fiduciary duties and our unitholders have restricted remedies available for actions that, without the limitations, might constitute breaches of fiduciary duty. |

| • |

Our General Partner determines the amount and timing of asset purchases and sales, borrowings, issuance of additional partnership securities and reserves, each of which can affect the amount of cash that is distributed to unitholders. |

| • |

Our General Partner determines the amount and timing of any capital expenditures and whether a capital expenditure is a maintenance capital expenditure, which reduces operating surplus, or an expansion capital expenditure, which does not reduce operating surplus. This determination can affect the amount of cash that is distributed to our unitholders. |

| • |

Our General Partner may decide to receive a quantity of our Class B units in exchange for resetting the target distribution levels related to its incentive distribution rights without the approval of the conflicts committee of our General Partner or our unitholders. |

| • |

Our General Partner determines which costs incurred by it and its affiliates are reimbursable by us. |

| • |

Our partnership agreement does not restrict our General Partner from causing us to pay it or its affiliates for any services rendered to us or entering into additional contractual arrangements with any of these entities on our behalf. |

| • |

Our General Partner intends to limit its liability regarding our contractual and other obligations and, in some circumstances, is entitled to be indemnified by us. |

| • |

Our General Partner may exercise its limited right to call and purchase common units if it and its affiliates own more than 80% of the common units. |

| • |

Our General Partner controls the enforcement of obligations owed to us by our General Partner and its affiliates. |

| • |

Our General Partner decides whether to retain separate counsel, accountants or others to perform services for us. |

Our partnership agreement limits the fiduciary duties our General Partner owes to holders of our units and restricts the remedies available to holders of our units for actions taken by our General Partner that might otherwise constitute breaches of fiduciary duty.

Our partnership agreement contains provisions that reduce the fiduciary standards to which our General Partner would otherwise be held by state fiduciary duty laws. For example, our partnership agreement:

| • |

permits our General Partner to make a number of decisions in its individual capacity, as opposed to in its capacity as our General Partner. This entitles our General Partner to consider only the interests and factors that it desires, and it has no duty or obligation to give any consideration to any interest of, or factors affecting, us, our affiliates or any limited partner. Examples include the exercise of its right to receive a quantity of our Class B units in exchange for resetting the target distribution levels related to its incentive distribution rights, the exercise of its limited call right, the exercise of its rights to transfer or vote the units it owns, the exercise of its registration rights and its determination whether or not to consent to any merger or consolidation of the partnership or amendment to the partnership agreement; |

| • |

provides that our General Partner will not have any liability to us or our unitholders for decisions made in its capacity as a general partner so long as it acted in good faith, meaning it believed the decision was in the best interests of our partnership; |

| • |

generally provides that affiliated transactions and resolutions of conflicts of interest not approved by the conflicts committee of the Board acting in good faith and not involving a vote of unitholders must be on terms no less favorable to us than those generally being provided to or available from unrelated third parties or must be “fair and reasonable” to us, as determined by our General Partner in good faith. In determining whether a transaction or resolution is “fair and reasonable,” our General Partner may consider the totality of the relationships between the parties involved, including other transactions that may be particularly advantageous or beneficial to us; |

| • |

provides that our General Partner and its officers and directors will not be liable for monetary damages to us, our limited partners or assignees for any acts or omissions unless there has been a final and non-appealable judgment entered by a court of competent jurisdiction determining that our General Partner or its officers and directors acted in bad faith or engaged in fraud or willful misconduct or, in the case of a criminal matter, acted with knowledge that the conduct was criminal; and |

| • |

provides that in resolving conflicts of interest, it will be presumed that in making its decision, our General Partner acted in good faith, and in any proceeding brought by or on behalf of any limited partner or us, the person bringing or prosecuting such proceeding will have the burden of overcoming such presumption. |

By purchasing a common unit, a common unitholder will become bound by the provisions in the partnership agreement, including the provisions discussed above.

Ergon may compete with us, which could adversely affect our existing business and limit our ability to acquire additional assets or businesses.

Neither our partnership agreement nor any other agreement with Ergon prohibits Ergon from owning assets or engaging in businesses that compete directly or indirectly with us. In addition, Ergon may acquire, construct or dispose of assets in the future, without any obligation to offer us the opportunity to purchase or construct any of those assets. Ergon is a privately held company engaged in a wide range of operations. Ergon has significantly greater resources and experience than we have, which may make it more difficult for us to compete with Ergon with respect to commercial activities as well as for acquisition candidates. As a result, competition from Ergon could adversely impact our results of operations and cash available for distribution.

Cost reimbursements due to our General Partner and its affiliates for services provided, which are determined by our General Partner, may be substantial and will reduce our cash available for distribution to our unitholders.

Pursuant to our partnership agreement, our General Partner is entitled to receive reimbursement for the payment of expenses related to our operations and for the provision of various general and administrative services for our benefit. Payments for these services may be substantial and reduce the amount of cash available for distribution to unitholders. In addition, under Delaware partnership law, our General Partner has unlimited liability for our obligations, such as our debts and environmental liabilities, except for our contractual obligations that are expressly made without recourse to our General Partner. To the extent our General Partner incurs obligations on our behalf, we are obligated under our partnership agreement to reimburse or indemnify our General Partner. If we are unable or unwilling to reimburse or indemnify our General Partner, our General Partner may take actions to cause us to make payments of these obligations and liabilities. Any such payments would reduce the amount of cash otherwise available for distribution to our unitholders.

Holders of our Preferred Units and common units have limited voting rights and are not entitled to elect our General Partner or its directors.

Unlike the holders of common stock in a corporation, unitholders have only limited voting rights on matters affecting our business and, therefore, limited ability to influence management’s decisions regarding our business. Unitholders did not elect our General Partner or the Board and have no right to elect our General Partner or the Board on an annual or other continuing basis. The Board is chosen by Ergon. Furthermore, if the unitholders are dissatisfied with the performance of our General Partner, they have little ability to remove our General Partner. Amendments to our partnership agreement may be proposed only by or with the consent of our General Partner. As a result of these limitations, the price at which the common units will trade could be diminished because of the absence or reduction of a takeover premium in the trading price.

Control of our General Partner may be transferred to a third party without unitholder consent.

Our General Partner may transfer its general partner interest to a third party in a merger or in a sale of all or substantially all of its assets without the consent of the unitholders. Furthermore, our partnership agreement does not restrict the ability of Ergon, the owner of our General Partner, from transferring all or a portion of its ownership interest in our General Partner to a third party. The new owner of our General Partner would then be in a position to replace the Board and officers of our General Partner with its own choices and thereby influence the decisions made by the Board and officers.

We may issue additional units without approval of our unitholders, which would dilute our unitholders’ ownership interests.

Except in the case of the issuance of units that rank equal to or senior to the Preferred Units, our partnership agreement does not limit the number or price of additional limited partner interests we may issue at any time without the approval of our unitholders. In addition, because we are a limited partnership, we will not be subject to the shareholder approval requirements relating to the issuance of securities (other than in connection with the establishment or material amendment of a stock option or purchase plan or the making or material amendment of any other equity compensation arrangement) contained in Nasdaq Marketplace Rule 5635. The issuance by us of additional common units or other equity securities of equal or senior rank may have any or all of the following effects, among others:

| • |

Our unitholders’ proportionate ownership interest in us will decrease. |

| • |

The amount of cash available for distribution on each unit may decrease. |

| • |

The ratio of taxable income to distributions may increase. |

| • |

The relative voting strength of each previously outstanding unit may be diminished. |

| • |

The market price of the common units may decline. |

Our partnership agreement restricts the voting rights of unitholders, other than our General Partner and its affiliates, including Ergon, owning 20% or more of any class of our partnership securities.

Unitholders’ voting rights are further restricted by the partnership agreement, which provides that any units held by a person that owns 20% or more of any class of units then outstanding, other than our General Partner, its affiliates, their transferees and persons who acquired such units with the prior approval of the Board, cannot vote on any matter. Our partnership agreement also contains provisions limiting the ability of unitholders to call meetings or to acquire information about our operations, as well as other provisions.

Even if our public unitholders are dissatisfied with our General Partner, it will be difficult for them to remove our General Partner without its consent.

It will be difficult for our public unitholders to remove our General Partner without its consent because our General Partner and its affiliates own a substantial number of our units. The vote of the holders of at least 66 2/3% of all outstanding units voting together as a single class is required to remove the General Partner. As of March 1, 2022, Ergon owned approximately 30.9% of our aggregate outstanding Preferred Units and common units.

Affiliates of our General Partner may sell units in the public markets, which sales could have an adverse impact on the trading price of the units.