MULTI-TENANT

OFFICE/INDUSTRIAL LEASE (NNN)

CYPRESS DISTRIBUTION CENTER

Cypress, California

Cypress, California

LANDLORD:

KATELLA/HOLDER STREET, LLC,

a Delaware limited liability company

a Delaware limited liability company

TENANT:

IRHYTHM TECHNOLOGIES, INC.,

a Delaware corporation

a Delaware corporation

TABLE OF CONTENTS

Article 1 - LEASE SUMMARY AND PROPERTY SPECIFIC PROVISIONS | 1 | |||||||

| 9 | ||||||||

| Article 3 - PREMISES | 9 | |||||||

| 9 | ||||||||

| 10 | ||||||||

| 10 | ||||||||

| 11 | ||||||||

| 11 | ||||||||

| 12 | ||||||||

| 13 | ||||||||

| 13 | ||||||||

| 14 | ||||||||

| 14 | ||||||||

| 15 | ||||||||

| 16 | ||||||||

| 17 | ||||||||

| 18 | ||||||||

| 19 | ||||||||

| 19 | ||||||||

| 20 | ||||||||

| 21 | ||||||||

| 22 | ||||||||

| 22 | ||||||||

| 23 | ||||||||

| 24 | ||||||||

| 24 | ||||||||

| 24 | ||||||||

| Article 28 - RELOCATION OF PREMISES | 24 | |||||||

| Article 29 - MORTGAGEE PROTECTION | 24 | |||||||

| 25 | ||||||||

| 25 | ||||||||

Exhibits

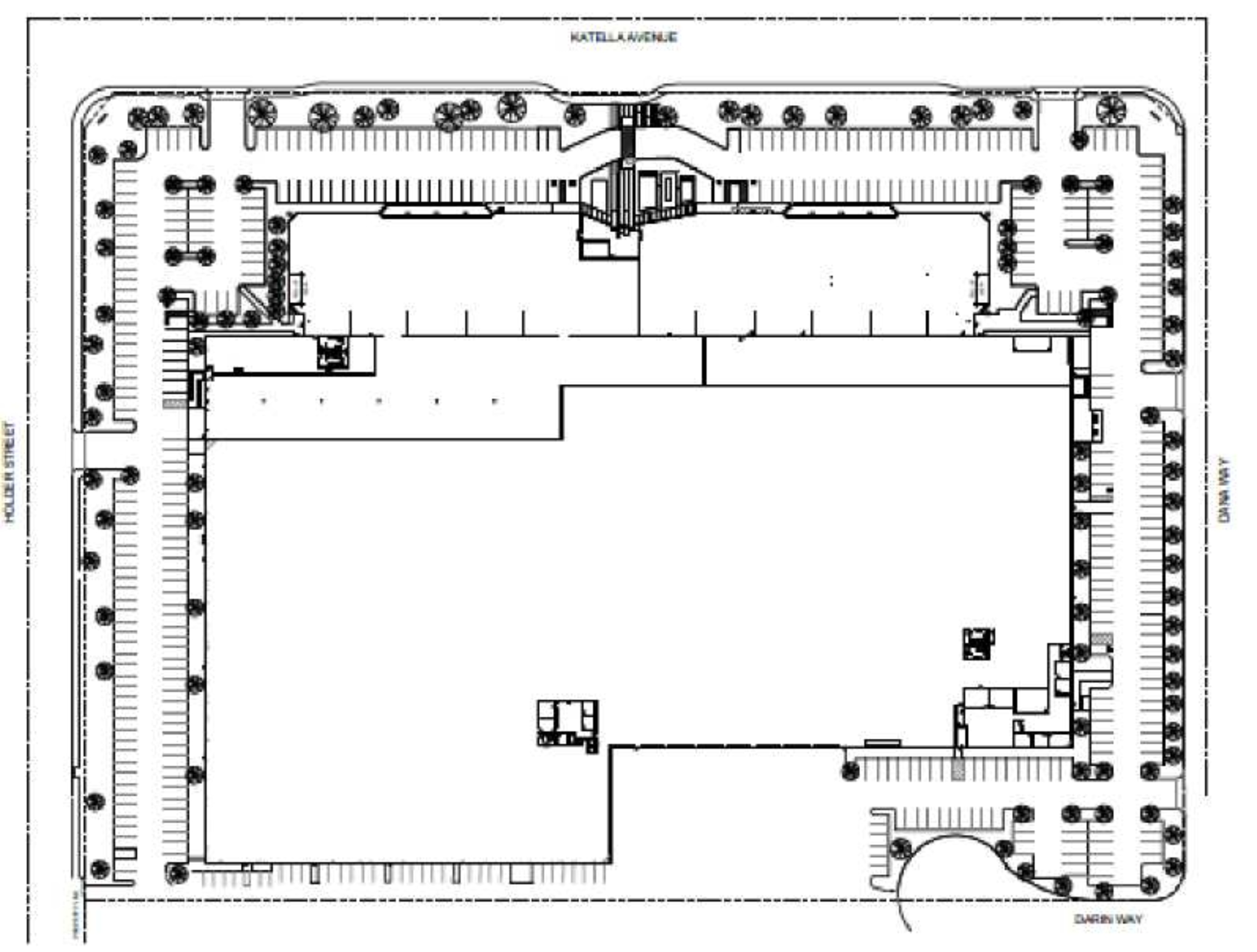

Exhibit A Premises Floor Plan

Exhibit B Site Plan

Exhibit C Work Letter

Exhibit D Notice of Lease Term Dates

Exhibit E Rules and Regulations

Exhibit F Estoppel Certificate

Exhibit G Environmental Questionnaire and Disclosure Statement

Riders

Rider No. 1 Extension Option

Rider No. 2 Fair Market Rental Rate

Rider No. 3 Expansion Option

Rider No. 4 Termination Option

Rider No. 5 Options in General

18th

This MULTI-TENANT OFFICE/INDUSTRIAL LEASE (NNN) (“Lease”), entered into as of this __ day of March, 2021 (the “Effective Date”) for reference purposes, is by and between KATELLA/HOLDER STREET, LLC, a Delaware limited liability company, hereinafter referred to as “Landlord”, and IRHYTHM TECHNOLOGIES, INC., a Delaware corporation, hereinafter referred to as “Tenant”.

ARTICLE 1 - LEASE SUMMARY AND PROPERTY SPECIFIC PROVISIONS

1.1 Landlord’s Address: KATELLA/HOLDER STREET, LLC

c/o LBA Realty LLC

3347 Michelson Drive, Suite 200

Irvine, California 92612

Attn: Asset Manager - Cypress Distribution Center

Telephone: (949) 833-0400

E-mail: leasingnotices@lbarealty.com

With a copy to: Katella/Holder Street, LLC

c/o LBA Realty

3347 Michelson Drive, Suite 210 Irvine, California 92612

Attn: Regional Operations Manager - Cypress Distribution Center

Telephone: (949) 833-0400

E-mail: leasingnotices@lbarealty.com

For payment of Rent: KATELLA/HOLDER STREET, LLC

P.O. Box 741151

Los Angeles, California 90074-1151

1.1 Tenant’s Address: Before the Commencement Date:

IRHYTHM TECHNOLOGIES, INC. 11085 Knott Ave, Suite B Cypress, CA 90630

Attn: Head of Workplace & Real Estate

After the Commencement Date:

The Premises

With a copy to: IRHYTHM TECHNOLOGIES, INC.

699 8th St # 600

San Francisco, CA 94103

Attn: Head of Workplace & Real Estate

Tenant Billing Address: IRHYTHM TECHNOLOGIES, INC.

699 8th St # 600 San Francisco, CA 94103 Attn: Finance

1.3.Building; Property: The building located at 6550 Katella Avenue, Cypress, California 90630 (the “Building”). The Building, together with all other buildings, improvements and facilities, now or subsequently located upon the land (the “Site”), including, without limitation, the two (2) buildings currently located within the Property, as shown on the Site Plan attached hereto as Exhibit B (as such area may be expanded or reduced from time to time) is referred to herein as the “Property”. The Property is commonly known as the Cypress Distribution Center. Landlord and Tenant stipulate and agree that the Property contains 546,219 rentable square feet in the aggregate and the Building contains 342,086 rentable square feet, for all purposes of this Lease.

1.4.Premises: Suite 200 of the Building, consisting of 34,573 rentable square feet of office space (the “Office Premises”) and 34,360 rentable square feet of warehouse space (the “Warehouse Premises”), as outlined on the Premises Floor Plan attached hereto as Exhibit A. The estimated rentable square footage of the Premises is 68,933, subject to adjustment pursuant to Section 3.2 of the Standard Lease Provisions. Tenant’s Percentage of the Building: 19.75%.

1.5.City: The City of Cypress, County of Orange, State of California.

1.6.Commencement Date: The later of: (i) six (6) months following the Turnover Date, (ii) August 1, 2021. Estimated Commencement Date: August 1, 2021.

1.7.Term: One hundred twenty-six (126) full calendar months, plus any partial month at the beginning of the Term, commencing on the Commencement Date and ending on the last day of the one hundred twenty-sixth (126th) full calendar month following the Commencement Date (“Expiration Date”).

1.8.Monthly Base Rent:

Office Premises:

Months or Period

01-12*

13-24

01-36

01-48

01-60

01-72

01-84

01-96

01-108

01-120

01-126

Monthly Base Rent

$57,045.45**

$58,756.81

$60,519.52

$62,335.10

$64,205.16

$66,131.31

$68,115.25

$70,158.71

$72,263.47

$74,431.37

$76,664.31

Warehouse Premises:

Months or Period

01-12*

13-24

01-36

01-48

01-60

01-72

01-84

01-96

01-108

01-120

01-126

Monthly Base Rent

$30,924.00**

$31,851.72

$32,807.27

$33,791.49

$34,805.23

$35,849.39

$36,924.87

$38,032.62

$39,173.60

$40,348.81

$41,559.27

*Including any partial month at the beginning of the Term.

**Notwithstanding the foregoing, provided Tenant is not in default under this Lease beyond any applicable notice and cure period, Landlord hereby agrees to abate Tenant’s obligation to pay Monthly Base Rent during the second (2nd) through the seventh (7th) full calendar months of the initial Term (such total amount of abated Monthly Base Rent being hereinafter referred to as the “Abated Amount”). During such abatement period, Tenant will still be responsible for the payment of all other monetary obligations under the Lease. Tenant acknowledges that any default by Tenant under this Lease will cause Landlord to incur costs not contemplated hereunder, the exact amount of such costs being extremely difficult and impracticable to ascertain, therefore, should Landlord terminate the Lease as after a Tenant default after having been given notice and opportunity to cure, then the total unamortized sum of such Abated Amount (amortized on a straight line basis over the initial Term of this Lease) so conditionally excused shall become immediately due and payable by Tenant to Landlord; provided, however, Tenant acknowledges and agrees that nothing in this subparagraph is intended to limit any other remedies available to Landlord at law or in equity under applicable law (including, without limitation, the remedies under Civil Code Section 1951.2 and/or 1951.4 and any successor statutes or similar laws), in the event Tenant defaults under this Lease beyond any applicable notice and cure period. Upon reasonable notice to Tenant at any time prior to application of the entire Abated Amount, Landlord shall have the right to purchase from Tenant any and all then remaining Abated Amount as it applies to one or more of the remaining abatement months by paying to Tenant an amount equal to the unused balance of the Abated Amount that Landlord elects to purchase back from Tenant (the “Abated Amount Purchase Price”). Upon Landlord’s payment to Tenant of the Abated Amount Purchase Price with respect to the applicable remaining abatement months, Tenant shall thereupon be required to pay Monthly Base Rent during such months in an amount equal to the Abated Amount that Tenant would have been entitled to receive but for Landlord’s payment to Tenant of the Abated Amount Purchase Price.

Accordingly, Tenant shall deliver the following amounts to Landlord upon its execution of this Lease (pursuant to Sections 4.2 and 5.1 of the Standard Provisions):

| (a) | Monthly Base Rent: | $87,969.45 for Month 1. | ||||||

| (b) | Tenant’s Percentage | |||||||

| of Operating Expenses (est.): | $16,514.49 for Month 1. | |||||||

| (c) | Security Deposit: | $354,670.74 (See Section 1.9 below) | ||||||

| Total due upon execution of this Lease: | $459,154.68. | |||||||

1.9.Security Deposit: $354,670.74, subject to reduction in accordance with the terms and conditions of Article 6.

1.10.Permitted Use: Warehousing, manufacturing, research and development, storage and general office use, subject to the provisions set forth in this Lease and as permitted by Law.

1.11.Parking: One hundred sixty-nine (169) unreserved parking spaces, subject to the terms of Article 11 of the Standard Lease Provisions.

1.12.Brokers: Cushman & Wakefield of California, Inc., representing Landlord and Tenant.

1.13.Interest Rate: The lesser of: (a) Eight percent (8%) or (b) the maximum rate permitted by law in the State where the Property is located.

1.14.Insurance Amounts:

a.Commercial General Liability Insurance: General liability of not less than One Million Dollars ($1,000,000.00) per occurrence and Two Million Dollars ($2,000,000.00) in the aggregate.

b.Commercial Automobile Liability Insurance: Limit of liability of not less than One Million Dollars ($1,000,000.00) per accident.

c.Worker’s Compensation and Employers Liability Insurance: With limits as mandated pursuant to the laws in the State in which the Property is located, or One Million Dollars ($1,000,000.00) per person, disease and accident, whichever is greater.

d.Umbrella Liability Insurance: Limits of not less than Three Million Dollars ($3,000,000.00) per occurrence.

e.If Tenant’s business includes professional services, Professional Liability (also known as errors and omissions insurance): Not less than the minimum limits required by law for Tenant’s profession, and in any event, not less than One Million Dollars ($1,000,000.00) per occurrence.

f.Loss of Income, Extra Expense and Business Interruption Insurance: In the amount of at least 12 months of Monthly Base Rent.

1.3.Tenant Improvements: Landlord, at Landlord’s sole cost and expense, promptly following the mutual execution of this Lease, using Building-standard methods, materials, finishes and specifications, shall complete certain sewer system work as further described in Schedule 2 attached to Exhibit C attached hereto (the “Landlord Improvements”). The Landlord Improvements shall be constructed in accordance with all applicable Laws, in a good and workmanlike manner, free of defects and using new Building standard materials and equipment of good quality. Tenant shall have the right to submit a written “punch list” to Landlord, setting forth any defective item of construction, and Landlord shall promptly cause such items to be corrected.

Landlord hereby grants to Tenant an allowance of: (i) up to $75.00 per rentable square foot of the Office Premises (i.e., up to $2,592,975.00, based on the Office Premises containing approximately 34,573 rentable square feet), plus (ii) up to $2.50 per rentable square foot of the Warehouse Premises (i.e., up to $85,900.00, based on the Warehouse Premises containing approximately 34,360 rentable square feet), plus (iii) $675,000.00 ($3,353,875.00 in the aggregate) (collectively, the “Allowance”), to be applied as provided in the Work Letter.

1.4.Tenant’s Percentage: 12.62%, which is the ratio that the rentable square footage of the Premises bears to the rentable square footage of the Property.

1.5.Common Areas; Definitions; Tenant’s Rights. During the Term, Tenant shall have the non-exclusive right to use, in common with other tenants in the Property, and subject to the Rules and Regulations referred to in Article 9 of the Standard Lease Provisions, those portions of the Property (the “Property Common Areas”) not leased or designated for lease to tenants that are provided for use in common by Landlord, Tenant and any other tenants of the Property (or by the sublessees, agents, employees, customers invitees, guests or licensees of any such party), whether or not those areas are open to the general public. The Property Common Areas shall include, without limitation, all other buildings on the Property exclusive of areas maintained and repaired by tenants, and all parking areas (subject to Article 11 of the Standard Lease Provisions), loading and unloading areas, trash areas, roadways, sidewalks, walkways, parkways, driveways and landscaped areas appurtenant to the Building, fixtures, systems, decor, facilities and landscaping contained, maintained or used in connection with those areas, and shall be deemed to include any city sidewalks adjacent to the Property and located on the Site, any pedestrian walkway system, park or other facilities located on the Site and open to the general public. The common areas of the Building shall be referred to herein as the “Building Common Areas” and shall include, without limitation, the following areas of the Building: the common entrances, lobbies, common restrooms, accessways, loading docks, ramps, drives and platforms and any passageways and serviceways thereto to the extent not exclusively serving another tenant or contained within another tenant’s premises, and the common pipes, conduits, wires and appurtenant equipment serving the Premises. The Building Common Areas and the Property Common Areas shall be referred to herein collectively as the “Common Areas.” If Tenant is leasing the entire Building, then all elements of the Building and the Building Common Areas shall constitute part of the Premises and all references to Common Areas contained in this Lease shall mean and refer to those elements of the Property outside of the Premises. Notwithstanding anything to the contrary herein, Landlord acknowledges that the Tenant Improvements identified in the plans issued for review by Hendy on January 13, 2021 (the “Hendy Plans”) will include certain modifications to the Building and parking areas required to accommodate both grade and dock high loading including, without limitation, the construction of a truck well serving the Premises (the “Truck Well”). In furtherance of the foregoing, the Common Areas shall exclude, and Tenant shall have the exclusive right to use and modify, the Truck Well identified in the Hendy Plans.

1.6.Operating Expenses.

a.Intentionally omitted.

b.Operating Expenses. In addition to the Monthly Base Rent, Tenant shall pay to Landlord Tenant’s Percentage of Operating Expenses, in the manner and at the times set forth in the following provisions of this Section 1.18. “Operating Expenses” shall consist of all costs and expenses of operation, maintenance and repair of the Common Areas of the Property as determined by standard accounting practices and calculated assuming the Property is at least ninety-five percent (95%) occupied. Operating Expenses include the following costs by way of illustration but not limitation: (i) any and all assessments imposed with respect to the Property pursuant to any covenants, conditions and restrictions affecting the Property; (ii) costs, levies or assessments resulting from statutes or regulations promulgated by any government authority in connection with the use or occupancy of the Property; (iii) all costs of utilities serving the Common Areas and any costs of utilities for the Premises which are not separately metered, (iv) all Taxes and Insurance Costs as defined in the Standard Lease Provisions, (v) waste disposal; (vi)

security, if any; (vii) costs incurred in the management of the Property, including, without limitation: (1) supplies, materials, equipment and tools, (2) wages, salaries, benefits, pension payments, fringe benefits, (and payroll taxes, insurance and similar governmental charges related thereto) of employees used in the operation and maintenance of the Property, (3) the rental of personal property used by Landlord’s personnel in the maintenance, repair and operation of the Property, (4) accounting fees, legal fees and real estate consultant’s fees, and (5) a management/administrative fee not to exceed four percent (4%) of gross rents for the Property; (viii) repair and maintenance of all portions of the Building and all buildings on the Property other than such portions as are maintained by Tenant or any other tenants, including the elevators (if any), restrooms (if any), structural and non-structural portions of the Building and all other buildings on the Property, and the plumbing, heating, ventilating, air-conditioning and electrical systems installed or furnished by Landlord and not maintained by Tenant pursuant to Section 8.2 of the Standard Provisions; (ix) maintenance, costs and upkeep of all parking and Common Areas; (x) amortization on a straight-line basis over the useful life together with interest at the rate of eight percent (8%) per annum on the unamortized balance of all costs of a capital nature (including, without limitation, capital improvements, capital replacements, capital repairs, capital equipment and capital tools): (1) reasonably intended to produce a reduction in operating charges or energy consumption; or (2) required after the date of this Lease under any Law that was not applicable to the Building at the time it was originally constructed; or (3) for repair or replacement of any equipment or improvements needed to operate and/or maintain the Property at the same quality levels as prior to the repair or replacement; (xi) costs and expenses of gardening and landscaping; (xii) maintenance of signs (other than signs of tenants of the Property); (xiii) personal property taxes levied on or attributable to personal property used in connection with the Property; and (xiv) costs and expenses of repairs, resurfacing, repairing, maintenance, painting, lighting and similar items. Landlord shall have the right, from time to time, to equitably allocate some or all of the Operating Expenses among different tenants and/or different buildings and/or different premises of the Property based upon differing levels of use, demand, risk or other distinctions among such parties, premises or Buildings (the “Cost Pools”). Such Cost Pools may include, for example, all office space tenants or industrial/R&D space tenants in the Property and may be modified to take into account the addition of any additional buildings within the Property. Accordingly, in the event of such allocations into Cost Pools, Tenant’s Percentage shall be appropriately adjusted to reflect such allocation. In addition, if Landlord does not furnish a particular service or work (the cost of which, if furnished by Landlord would be included in Operating Expenses) to a tenant (other than Tenant) that has undertaken to perform such service or work in lieu of receiving it from Landlord, then Operating Expenses shall be considered to be increased by an amount equal to the additional Operating Expenses that Landlord would reasonably have incurred had Landlord furnished such service or work to that tenant.

c.Exclusions from Operating Expenses. Notwithstanding anything to the contrary contained elsewhere in this Lease, the following items shall be excluded from Operating Expenses: (i) Costs of decorating, redecorating, or special cleaning or other services provided to certain tenants and not provided on a regular basis to all tenants of the Property; (ii) Any charge for depreciation of the Property or equipment and any interest or other financing charge; (iii) All costs relating to activities for the marketing, solicitation, negotiation and execution of leases of space in the Property, including without limitation, costs of tenant improvements; (iv) All costs for which Tenant or any other tenant in the Property is being charged other than pursuant to the operating expense clauses of leases for space in the Property; (v) The cost of correcting defects in the construction of the Building or any other building in the Property or in the building equipment, except that conditions (not occasioned by construction defects) resulting from ordinary wear and tear will not be deemed defects for the purpose of this category; (vi) the cost of repair made by Landlord because of the total or partial destruction of the Property or the condemnation of a portion of the Building or any other building in the Property; (vii) The cost of any items for which Landlord is reimbursed by insurance or otherwise compensated by parties other than tenants of the Building or any other building in the Property pursuant to clauses similar to this paragraph; (viii) Any operating expense representing an amount paid to a related corporation, entity, or person which is in excess of the amount which would be paid in the absence of such relationship; (ix) The cost of any work or service performed for or facilities furnished to any tenant of the Building or any other building in the Property to a greater extent or in a manner more favorable to such tenant than that performed for or furnished to Tenant; (x) The cost of alterations of space in the Building or any other building in the Property which is leased to other tenants; (xi) Ground rent or similar payments to a ground lessor; (xii) Legal fees and related expenses incurred by Landlord (together with any damages awarded against Landlord) due to the gross negligence or willful misconduct of Landlord; (xiii) Costs arising from the presence, removal, abatement, or remediation of any Hazardous Materials within, upon or beneath the Property except to the extent caused by the release or emissions of such Hazardous Materials by Tenant or any Tenant’s Parties; (xiv) Salaries and compensation of ownership and management personnel to the extent that such persons provide services to properties other than the Property and wages and/or benefits attributable to personnel above the level of the immediate supervisor of the Property manager; (xv) Costs of selling or financing the Property, the Building or any portions thereof; (xvi) capital costs other than as expressly provided in Section 1.18(b)(x); (xvii) costs, fines, penalties, or interest incurred due to a violation of Laws by Landlord; and (xviii) expense reserves.

d.Estimate Statement and Payment of Tenant’s Percentage of Operating Expenses. By

the first day of April (or as soon as practicable thereafter) of each calendar year during the Term, Landlord shall endeavor to deliver to Tenant a statement (“Estimate Statement”) estimating the Tenant’s Percentage of Operating Expenses for the current calendar year. If at any time during the Term, but not more often than quarterly, Landlord reasonably determines that the estimated amount of Tenant’s Percentage of Operating Expenses payable by Tenant for the current calendar year will be greater or less than the amount set forth in the then current Estimate Statement, Landlord may issue a revised Estimate Statement and Tenant agrees to pay Landlord, within thirty (30) days after receipt of the revised Estimate Statement, the difference between the amount owed by Tenant under such revised Estimate Statement and the amount owed by Tenant under the original Estimate Statement for the portion of the then current calendar year which has expired. Thereafter Tenant agrees to pay Tenant’s Percentage of Operating Expenses based on such revised Estimate Statement until Tenant receives the next calendar year’s Estimate Statement or a new revised Estimate Statement for the current calendar year. Tenant’s Percentage of Operating Expenses shown on the Estimate Statement (or revised Estimate Statement, as applicable) shall be divided into twelve (12) equal monthly installments, and Tenant shall pay to Landlord, concurrently with the regular monthly Rent payment next due following the receipt of the Estimate Statement (or revised Estimate Statement, as applicable), an amount equal to one (1) monthly installment of such Tenant’s Percentage of Operating Expenses multiplied by the number of months from January in the calendar year in which such statement is submitted to the month of such payment, both months inclusive (less any amounts previously paid by Tenant with respect to any previously delivered Estimate Statement or revised Estimate Statement for such calendar year). Subsequent installments shall be paid concurrently with the regular monthly Rent payments for the balance of the calendar year and shall continue until the next calendar year’s Estimate Statement (or current calendar year’s revised Estimate Statement) is received.

e.Actual Statement. By the first day of June (or as soon as practicable thereafter) of each subsequent calendar year during the Term, Landlord shall endeavor to deliver to Tenant a statement (“Actual Statement”) which states the Tenant’s Percentage of actual Operating Expenses payable by Tenant for the immediately preceding calendar year. If the Actual Statement reveals that the Tenant’s Percentage of actual Operating Expenses were more than the Tenant’s Percentage of estimated Operating Expenses paid by Tenant with respect to the preceding calendar year, Tenant agrees to pay Landlord the difference in a lump sum within thirty (30) days after receipt of the Actual Statement. Such obligation will be a continuing one which will survive

the expiration or earlier termination of this Lease. If the Actual Statement reveals that the Tenant’s Percentage of actual Operating Expenses were less than the Operating Expenses paid by Tenant with respect to the preceding calendar year, Landlord will credit any overpayment toward the next monthly installment(s) of Rent due from Tenant or, if no such installments remain (i.e., following the expiration or earlier termination of the Lease), refund such amounts to Tenant within thirty (30) days. Prior to the expiration or sooner termination of the Term and Landlord’s acceptance of Tenant’s surrender of the Premises, Landlord will have the right to estimate the Tenant’s Percentage of actual Operating Expenses for the then current calendar year and to collect from Tenant prior to Tenant’s surrender of the Premises, any excess of such Tenant’s Percentage of actual Operating Expenses over the Tenant’s Percentage of estimated Operating Expenses paid by Tenant in such calendar year, and Landlord shall reconcile the same with the actual Operating Expenses incurred by Landlord and charge or refund Tenant for any underpayment or overpayment in accordance with this Section; provided, however, in the event of an overpayment by Tenant, Landlord shall reimburse Tenant for such overpayment within thirty (30) days following Landlord’s delivery of the Actual Statement.

f.No Release. Any delay or failure by Landlord in delivering any Estimate Statement or Actual Statement pursuant to this Section 1.18 shall not constitute a waiver of its right to receive Tenant’s payment of Tenant’s Percentage of Operating Expenses, nor shall it relieve Tenant of its obligations to pay Operating Expenses pursuant to this Section 1.18, except that Tenant shall not be obligated to make any payments based on such Estimate or Actual Statement until thirty (30) days after receipt of such statement.

g.Review. Within one hundred twenty (120) days after receiving Landlord’s Actual Statement, Tenant may, upon advance written notice to Landlord and during reasonable business hours, cause a review of Landlord’s books and records with respect to the preceding calendar year only to determine the accuracy of Landlord’s Actual Statement. Landlord shall make all pertinent records available for review that are reasonably necessary for Tenant to conduct its review. If any records are maintained at a location other than the office of the Building, Tenant may either review the records at such other location or pay for the reasonable cost of copying and shipping the records. If Tenant retains an agent, at Tenant’s sole cost and expense, to review Landlord’s records, the agent shall be an independent accountant of national standing which is reasonably acceptable to Landlord, is not compensated on a contingency basis and is also subject to a confidentiality agreement. Within sixty (60) days after the records are made available to Tenant, Tenant shall have the right to give Landlord written notice (an “Objection Notice”) stating in reasonable detail any objection to the Actual Statement of Operating Expenses for that year. If Tenant provides Landlord with a timely Objection Notice, Landlord and Tenant shall work together in good faith to resolve any issues raised in Tenant’s Objection Notice. If Tenant fails to provide Landlord with a timely Objection Notice, Landlord’s Actual Statement shall be deemed final and binding, and Tenant shall have no further right to review or object to such statement. If Landlord and Tenant determine that Operating Expenses for the calendar year are less than reported, Landlord shall provide Tenant with a credit against the next installment of Rent in the amount of the overpayment by Tenant. Likewise, if Landlord and Tenant determine that Operating Expenses for the calendar year are greater than reported, Tenant shall pay Landlord the amount of any underpayment within thirty (30) days after such determination. The records obtained by Tenant shall be treated as confidential. In no event shall Tenant be permitted to review Landlord’s records or to dispute any statement of Operating Expenses unless Tenant has paid and continues to pay all Rent when due.

1.3.Utilities and Services.

a. Utilities and Services. As used in this Lease, “Premises Utilities Costs” shall mean all actual charges for utilities for the Premises of any kind, including but not limited to water, sewer and electricity, telecommunications and cable service, and the costs of heating, ventilating and air conditioning and other utilities as well as related fees, assessments and surcharges. Tenant shall contract directly for all utilities services for the Premises and shall pay all Premises Utilities Costs directly to the various utility service providers providing such utility services to the Premises. Should Landlord elect to supply any or all of such utilities, Tenant agrees to purchase and pay for the same as Additional Rent. Tenant shall reimburse Landlord within thirty (30) days after billing for fixture charges and/or water tariffs, if applicable, which are charged to Landlord by local utility companies. Landlord will notify Tenant of this charge as soon as it becomes known. This charge will increase or decrease with current charges being levied against Landlord, the Premises or the Building by the local utility company, and will be due as Additional Rent. In no event shall Landlord be liable for any interruption or failure in the supply of any such utility or other services to Tenant. In no event shall any Rent owed Landlord under this Lease be abated by reason of the failure to furnish, delay in furnishing, unavailability or diminution in quality or quantity of any such utility or other services or interference with Tenant’s business operations as a result of any such occurrence; nor shall any such occurrence constitute an actual or constructive eviction of Tenant or a breach of an implied warranty by Landlord.

b.Maintenance/Janitorial/Service Contracts. Tenant shall, at its sole cost and expense, maintain and repair, and enter into a regularly scheduled preventive maintenance/service contract with a maintenance contractor to service all hot water, heating and air conditioning systems and equipment (“HVAC”) within the Premises, or which serve the Premises exclusively, including, without limitation, any rooftop package HVAC units, distribution lines and internal venting systems. Such repair and maintenance shall include any and all services required to conform and maintain the HVAC units in compliance with current ASHRAE Standards. As used herein, "ASHRAE Standards" shall mean those standards established by the American Society of Heating, Refrigerating and Air Conditioning Engineers, Inc. (“ASHRAE”) and Air Conditioning Contractors of America (“ACCA”) Standard Practice for Inspection and Maintenance of Commercial Building HVAC Systems, ANSI/ASHRAE/ACCA Standard 180-2008, as the same may be amended from time to time. Tenant shall have complete control over the operation of the HVAC units within the Premises, or which exclusively serve the Premises, during the Term. All cleaning and janitorial services, including regular removal of trash and debris, for the Premises shall be performed and obtained, at Tenant’s sole cost and expense, exclusively by or through Tenant or Tenant’s janitorial contractors. The maintenance contractor and janitorial contractor for same must be approved in writing by Landlord in advance, such approval not to be unreasonably withheld, conditioned or delayed. All maintenance/service contracts shall include all services recommended by the equipment manufacturer within the operation/maintenance manual and all services required to conform and maintain the HVAC in compliance with current ASHRAE Standards and shall become effective (and a copy thereof delivered to Landlord) within thirty (30) days following the Commencement Date. If Tenant fails to procure and maintain any or all of such service contacts, then Landlord reserves the right, upon thirty (30) days’ prior written notice to Tenant and Tenant’s failure to cure prior to the expiration of such notice period, to procure and maintain any or all of such service contracts, and if Landlord so elects, Tenant shall reimburse Landlord, as Additional Rent, within thirty (30) days following written demand, for the cost therefor.

c.Tenant’s Obligations. Tenant shall cooperate fully at all times with Landlord and abide by current ASHRAE Standards all reasonable and non-discriminatory regulations and requirements which Landlord may prescribe for the proper functioning and protection of the Building’s services and systems. Tenant shall not connect any conduit, pipe, apparatus or other device to the Building’s water, waste or other supply lines or systems for any purpose. Neither Tenant nor its employees, agents, contractors, licensees or invitees shall at any time enter, adjust, tamper with, touch or otherwise in any manner affect the

mechanical installations or facilities of the Building. Tenant agrees to reasonably cooperate with Landlord to the extent required by Landlord to comply with California Public Resources Code Section 25402.10 including, without limitation, providing or consenting to any utility company releasing Tenant’s energy consumption information for the Premises to Landlord. Tenant hereby consents to the release of Tenant’s energy consumption information for the Premises to Landlord, and if requested, Tenant shall promptly sign any documentation requested by the utility company to evidence such consent.

1.20 Additional Hazardous Materials Requirements. In addition to Tenant’s obligations under Article 10 of the Standard Provisions, Tenant shall comply with the following provisions with respect to Hazardous Materials (as that term is defined in Article 10):

a. Environmental Questionnaire; Disclosure. Prior to the execution of this Lease, Tenant

shall complete, execute and deliver to Landlord an Environmental Questionnaire and Disclosure Statement (the “Environmental Questionnaire”) in the form of Exhibit G, and Tenant shall certify to Landlord all information contained in the Environmental Questionnaire as true and correct to the best of Tenant’s knowledge and belief. The completed Environmental Questionnaire shall be deemed incorporated into this Lease for all purposes, and Landlord shall be entitled to rely fully on the information contained therein. Within ten (10) business days following Landlord’s demand therefor (each such date of demand is hereinafter referred to as a “Disclosure Date”), until and including the last Disclosure Date occurring prior to the expiration or sooner termination of this Lease, Tenant shall disclose to Landlord in writing the names and amounts of all Hazardous Materials, or any combination thereof, that were stored, generated, used or disposed of on, under or about the Premises for the twelve (12) month period prior to each Disclosure Date, and that Tenant intends to store, generate, use or dispose of on, under or about the Premises during the next twelve (12) month period. At Landlord’s request, Tenant’s disclosure obligations under this Section 1.20 shall include a requirement that Tenant update, execute and deliver to Landlord the Environmental Questionnaire, as the same may be reasonably modified by Landlord from time to time; provided, however, Tenant shall not be required to update the Environmental Questionnaire more than once per year unless an environmental event of default has occurred or Tenant has materially changed its business. In addition to the foregoing, within ten (10) business days of Landlord’s request, Tenant shall promptly notify Landlord of, and shall promptly provide Landlord with true, correct, complete and legible copies of, all of the following environmental items relating to the Premises: reports filed pursuant to any self-reporting requirements; reports filed pursuant to any Environmental Laws or this Lease; all permit applications, permits, monitoring reports, workplace exposure and community exposure warnings or notices, and all other reports, disclosures, plans or documents (even those that may be characterized as confidential) relating to water discharges, air pollution, waste generation or disposal, underground storage tanks or Hazardous Materials; all orders, reports, notices, listings and correspondence (even those that may be considered confidential) of or concerning the release, investigation, compliance, clean up, remedial and corrective actions, and abatement of Hazardous Materials

whether or not required by Environmental Laws; and all complaints, pleadings and other legal documents filed against Tenant related to Tenant’s use, handling, storage or disposal of Hazardous Materials.

b.Inspection; Compliance. Subject to the provisions of Article 24, below, Landlord and Landlord Parties (as that term is defined in Article 10) shall have the right, but not the obligation, to inspect, investigate, sample and/or monitor the Premises, including any air, soil, water, groundwater or other sampling, and any other testing, digging, drilling or analyses, at any time to determine whether Tenant is complying with the terms of this Section 1.20 and Article 10, and in connection therewith, Tenant shall provide Landlord with access to all relevant facilities, records and personnel. If Tenant is not in compliance with any of the provisions of this Section

1.20.and Article 10, or in the event of a release of any Hazardous Materials on, under, from or about the Premises by Tenant or any Tenant’s Parties in violation of applicable Environmental Laws, Landlord and Landlord Parties shall have the right, but not the obligation, without limitation on any of Landlord’s other rights and remedies under this Lease, to immediately enter upon the Premises and to discharge Tenant’s obligations under this Section 1.20 and Article 10 at Tenant’s expense, including without limitation the taking of emergency or long term remedial action. Landlord and Landlord Parties shall endeavor to minimize interference with Tenant’s business but shall not be liable for any such interference. In addition, Landlord, at Tenant’s sole cost and expense, shall have the right, but not the obligation, to join and participate in any legal proceedings or actions initiated in connection with any claims or causes of action arising out of the storage, generation, use or disposal by Tenant or Tenant’s Parties of Hazardous Materials on, under, from or about the Premises in violation of applicable Environmental Laws. All sums reasonably disbursed, deposited or incurred by Landlord in connection herewith, including, but not limited to, all costs, expenses and actual attorneys’ fees, shall be due and payable by Tenant to Landlord, as an item of Additional Rent, on demand by Landlord, together with interest thereon at the Interest Rate from the date of such demand until paid by Tenant. Landlord agrees that if any testing proves that the Tenant or Tenant’s Parties have not violated applicable Environmental Laws or this Lease in connection with the presence of said Hazardous Materials, Tenant shall not be liable for any costs or expenses in connection with such inspection, testing and monitoring.

c.Tenant Obligations. If the presence of any Hazardous Materials on, under or about the Premises caused by Tenant or Tenant’s Parties results in (i) injury to any person, (ii) injury to or contamination of the Premises, or (iii) injury to or contamination of any real or personal property wherever situated, Tenant, at its sole cost and expense, shall promptly take all actions necessary to return the Premises to the condition required by applicable Environmental Laws. Without limiting any other rights or remedies of Landlord under this Lease, Tenant shall pay the cost of any cleanup work performed on, under or about the Premises as required by this Lease or any Environmental Laws in connection with the removal, disposal, neutralization or other treatment of such Hazardous Materials caused by Tenant or Tenant’s Parties. If Landlord has reason to believe that Tenant or Tenant’s Parties may have caused the release of any Hazardous Materials on, under, from or about the Premises in violation of applicable Environmental Laws, then Landlord may require Tenant, at Tenant’s sole cost and expense, to conduct monitoring activities on or about the Premises satisfactory to Landlord, in its sole and absolute judgment, concerning such release of Hazardous Materials on, under, from or about the Premises. Notwithstanding anything to the contrary contained in the foregoing, Tenant shall not, without Landlord’s prior written consent, take any remedial action in response to the presence of any Hazardous Materials on, under or about the Premises, or enter into any settlement agreement, consent decree or other compromise with any governmental agency with respect to any Hazardous Materials claims; provided, however, Landlord’s prior written consent shall not be necessary in the event that the presence of Hazardous Materials on, under or about the Premises (i) poses an immediate threat to the health, safety or welfare of any individual, or (ii) is of such a nature that an immediate remedial response is necessary and it is not possible to obtain Landlord’s consent before taking such action. Tenant’s failure to timely comply with this Section 1.20 shall constitute an event of default under this Lease.

d. Tenant’s Responsibility at Conclusion of Lease. Promptly upon the expiration or sooner termination of this Lease, Tenant shall represent to Landlord in writing that (i) Tenant has made a diligent effort to determine whether any Hazardous Materials are on, under or about the Premises in violation of applicable Environmental Laws, as a result of any acts or omissions of Tenant or Tenant’s Parties and (ii) no such Hazardous Materials exist on, under or about the Premises, other than as specifically identified to Landlord by Tenant in writing. If Tenant discloses the existence of Hazardous Materials on, under or

about the Premises or if Landlord at any time discovers that Tenant or Tenant’s Parties caused the release of any Hazardous Materials on, under, from or about the Premises in violation of applicable Environmental Laws, Tenant shall, at Landlord’s request, immediately prepare and submit to Landlord within thirty (30) days after such request a comprehensive plan, subject to Landlord’s approval, specifying the actions to be taken by Tenant to return the Premises to the condition required by applicable Environmental Laws. Upon Landlord’s approval of such clean-up plan, Tenant shall, at Tenant’s sole cost and expense, without limitation on any rights and remedies of Landlord under this Lease or at law or in equity, immediately implement such plan and proceed to clean up such Hazardous Materials in accordance with all Environmental Laws and as required by such plan and this Lease. Notwithstanding anything to the contrary herein, under no circumstance shall Tenant be liable for any losses, costs, claims, liabilities and damages (including attorneys’ and consultants’ fees) arising out of any Hazardous Material present at any time on or about the Property, or the soil, air, improvements, groundwater or surface water thereof, except to the extent due to the release or emission of such Hazardous Material by Tenant or Tenant’s Parties in violation of applicable Environmental Laws.

1.21 Landlord’s Additional Repair Obligations. Landlord, at Landlord's cost (subject to inclusion in Operating Expenses as provided in Section 1.18 of the Summary), shall repair, maintain and replace as necessary, the foundation and structural elements of the Building (including structural load bearing walls and roof structure), and utility meters, electrical lines, pipes and conduits serving the Building and the Premises; provided, however, to the extent such maintenance, repairs or replacements are required as a result of any act, neglect, fault or omission of Tenant or any of Tenant's Parties, Tenant shall pay to Landlord, as Additional Rent, the costs of such maintenance, repairs and replacements. In addition, and subject to Sections 17.1 and 17.2 of the Standard Lease Provisions, Landlord shall, as part of the Operating Expenses, repair, maintain and replace, as necessary (a) the basic heating, ventilating, air conditioning ("HVAC"), sprinkler and electrical systems within the Building core and standard conduits, connections and distribution systems thereof within the Premises (but not any above standard improvements installed in the Premises such as, for example, but not by way of limitation, custom lighting, special or supplementary HVAC or plumbing systems or distribution extensions, special or supplemental electrical panels or distribution systems, or kitchen or restroom facilities and appliances to the extent such facilities and appliances are intended for the exclusive use of Tenant), and (b) the Common Areas, if any; provided, however, to the extent such maintenance, repairs or replacements are required as a result of any act, neglect, fault or omission of Tenant or any of Tenant's Parties, Tenant shall pay to Landlord, as Additional Rent within ten (10) days after demand, the costs of such maintenance, repairs and replacements. Landlord shall not be liable to Tenant for failure to perform any such maintenance, repairs or replacements, unless Landlord shall fail to make such maintenance, repairs or replacements and such failure shall continue for an unreasonable time following written notice from Tenant to Landlord of the need therefor. Without limiting the foregoing, Tenant waives the right to make repairs at Landlord's expense under any applicable Laws now or hereafter in effect.

1.22 Tenant Termination Right. If Tenant is unable to obtain approval from the City of Cypress permitting Tenant to add a loading dock/truck well on or before April 25, 2021 (the “Outside Termination Date”), then Tenant shall have the one-time right to terminate the Lease by delivering written notice of such termination (the “Termination Notice”) to Landlord on or before April 30, 2021 (the “Termination Notice Delivery Date”); provided, that, if the City of Cypress is still reviewing Tenant’s application for approval as of the Outside Termination Date, Tenant shall have the right to extend the Outside Termination Date and the Termination Notice Delivery Date by an additional 14 days by providing notice to Landlord of the same. If Tenant timely delivers the Termination Notice to Landlord, then the Lease shall terminate, and Landlord shall promptly return any prepaid Rent and the Security Deposit to Tenant. If Tenant fails to timely deliver the Termination Notice to Landlord on or before April 20, 2021 (as may be extended), then the Lease shall not terminate and Tenant shall be deemed to have irrevocably waived its right to terminate the Lease under this Section 1.22.

[REST OF PAGE INTENTIONALLY BLANK]

STANDARD LEASE PROVISIONS

ARTICLE 2 - LEASE

ARTICLE 2 - LEASE

2.1 Lease Elements; Definitions; Exhibits. The Lease is comprised of the Lease Summary and Property Specific Provisions (the “Summary”), these Standard Lease Provisions (“Standard Provisions”) and all exhibits, and riders attached hereto (collectively, “Exhibits”), all of which are incorporated together as part of one and the same instrument. All references in any such documents and instruments to “Lease” means the Summary, these Standard Provisions and all Exhibits attached hereto. All terms used in this Lease shall have the meanings ascribed to such terms in the Summary, these Standard Provisions and any Exhibits. To the extent of any inconsistency between the terms and conditions of the Summary, these Standard Provisions, or any Exhibits attached hereto, the Summary and any Exhibits attached hereto shall control over these Standard Provisions.

ARTICLE 3 - PREMISES

3.1.Lease of Premises. Landlord hereby leases to Tenant, and Tenant hereby leases from Landlord, the Premises, upon and subject to, the terms, covenants and conditions of this Lease. Each party covenants and agrees, as a material part of the consideration for this Lease, to keep and perform their respective obligations under this Lease.

3.2.Landlord’s Reserved Rights. Provided the same do not unreasonably adversely affect Tenant’s use of the Premises or Tenant’s parking rights and do not materially increase the obligations or decrease the rights of Tenant under this Lease, Landlord reserves the right from time to time to do any of the following: (a) expand the Building and construct or alter other buildings or improvements on the Property; (b) make any changes, additions, improvements, maintenance, repairs or replacements in or to the Property, Common Areas and/or the Building (including the Premises if required to do so by any applicable Laws or to the extent necessary in conjunction with any improvements to the Property, Common Areas and/or the Building), and the fixtures and equipment thereof, including, without limitation: (i) maintenance, replacement and relocation of pipes, ducts, conduits, wires and meters and equipment above the ceiling surfaces, below the floor surfaces and within the walls of the Building and the Premises; and (ii) changes in the location, size, shape and number of driveways, entrances, stairways, elevators, loading and unloading areas, ingress, egress, direction of traffic, landscaped areas and walkways, easements, parking spaces and parking areas as long as Tenant’s parking ratio is not substantially and adversely impacted; (c) close temporarily any of the Property while engaged in making repairs, improvements or alterations to the Property; and (d) perform such other acts and make such other changes with respect to the Property, as Landlord may, in the exercise of reasonable good faith business judgment, deem to be appropriate. In no event shall Landlord reconfigure the Premises as a result of any changes to the Property, Common Areas and/or the Building or as a result of Landlord’s exercise of its rights under this Section 3.2. Landlord shall endeavor to minimize, as reasonably practicable, the interference with Tenant’s business as a result of any construction performed pursuant to this Section 3.2. All measurements of rentable area of the Premises in this Lease shall be deemed to be correct and shall not be subject to remeasurement.

ARTICLE 4 - TERM AND POSSESSION

4.1.Term; Notice of Lease Dates. The Term shall be for the period designated in the Summary commencing on the Commencement Date and ending on the Expiration Date, unless the Term is sooner terminated or extended as provided in this Lease. If the Commencement Date falls on any day other than the first day of a calendar month then the Term will be measured from the first day of the month following the month in which the Commencement Date occurs. Within ten (10) days after Landlord’s written request, Tenant shall execute a written confirmation of the Commencement Date and Expiration Date of the Term in the form of the Notice of Lease Term Dates attached hereto as Exhibit D. The Notice of Lease Term Dates shall be binding upon Tenant unless Tenant reasonably objects thereto in writing within such ten (10) day period. Landlord shall use commercially reasonable efforts to complete the Landlord Improvements promptly following the Effective Date, and Landlord shall cooperate with Tenant during the completion of the Landlord Improvements to timely permit Tenant to complete the Tenant Improvement.

4.2.Possession. Landlord shall deliver possession of the Premises to Tenant as provided in the Work Letter, or if no Work Letter is attached hereto, Landlord shall deliver possession of the Premises to Tenant in its then as-is condition, subject to the provisions of Section 4.3 below. Tenant agrees that if Landlord is unable to deliver possession of the Premises to Tenant on or prior to the date that this Lease is mutually executed and delivered, the Lease will not be void or voidable, nor will Landlord be liable to Tenant for any loss or damage therefrom. Notwithstanding the foregoing, Landlord will not be obligated to deliver possession of the Premises to Tenant until Landlord has received from Tenant all of the following: (i) a copy of this Lease fully executed by Tenant; (ii) the Security Deposit required hereunder and the first installment of Monthly Base Rent and Additional Rent, if any, due under this Lease; and (iii) copies of Tenant’s insurance certificates as required hereunder.

4.3.Condition of Premises. Tenant acknowledges that, except as otherwise expressly set forth in this Lease or the Work Letter, neither Landlord nor any agent of Landlord has made any representation or warranty with respect to the Premises, the Building or the Property or their condition, or with respect to the suitability thereof for the conduct of Tenant’s business, and Tenant shall accept the Premises in its then as-is condition on delivery by Landlord. Pursuant to Section 1938 of the California Civil Code, Landlord hereby advises Tenant that as of the date of this Lease neither the Premises, the Building nor the Property have undergone inspection by a Certified Access Specialist (CASp). Further, pursuant to Section 1938 of the California Civil Code, Landlord notifies Tenant of the following: “A Certified Access Specialist (CASp) can inspect the premises and determine whether the premises comply with all of the applicable construction-related accessibility standards under state law. Although California state law does not require a CASp inspection of the premises, the commercial property owner or lessor may not prohibit the lessee or tenant from obtaining a CASp inspection of the premises for the occupancy or potential occupancy of the lessee or tenant, if requested by the lessee or tenant. The parties shall mutually agree on the arrangements for the time and manner of any such CASp inspection, the payment of the costs and fees for the CASp inspection and the cost of making any repairs necessary to correct violations of construction-related accessibility standards within the premises.” Therefore and notwithstanding anything to the contrary contained in this Lease, Landlord and Tenant agree that (a) Tenant may, at its option and at its sole cost, cause a CASp to inspect the Premises and determine whether the Premises complies with all of the applicable construction-related accessibility standards under California law, (b) the parties shall mutually coordinate and reasonably approve of the timing of any such CASp inspection so that Landlord may, at its option, have a representative present during such inspection, and (c) Tenant shall be solely responsible for the cost of any repairs necessary to correct violations of construction-related accessibility standards within the Premises, any and all such alterations and repairs to be performed in accordance with Article 13 of this Lease, but only to the extent such alterations and repairs are disclosed by such CASp inspection and required by applicable Laws to be corrected; provided Tenant shall have no obligation to remove any repairs or alterations made pursuant to a CASp inspection under this Section 4.3.

4.4.Early Access. So long as Landlord has received from Tenant the first month’s Monthly Base Rent and Additional Rent, if any, due pursuant to Section 5.1 of this Lease, certificates satisfactory to Landlord evidencing the insurance required to be carried by Tenant under this Lease, and the Security Deposit, and so long as Tenant and its contractors and employees do not interfere with the completion of the Landlord Improvements, Landlord shall give Tenant and Tenant’s designated contractors access to the Premises upon mutual execution of this Lease (the “Early Access Period”) for purposes of installing Tenant’s furniture, fixtures, and equipment (“Tenant’s Work”) and constructing the Tenant Improvements. Tenant’s Work shall be performed by Tenant at Tenant’s sole cost and expense. Tenant’s access to the Premises during the Early Access Period shall be subject to all terms and conditions of this Lease, except that Tenant shall not be obligated to pay Rent during the Early Access Period until the Commencement Date. Landlord and Tenant agree to cooperate with the other party during the period of any such early access so as not to interfere with such party’s completion of the Landlord Improvements or the Tenant Improvements, as the case may be.

ARTICLE 5 - RENT

5.1.Monthly Base Rent. Tenant agrees to pay Landlord, the Monthly Base Rent as designated in the Summary. Monthly Base Rent and recurring monthly charges of Additional Rent (defined below) shall be paid by Tenant in advance on the first day of each and every calendar month (“Due Date”) during the Term, except that the first full month’s Monthly Base Rent and Additional Rent, if any, shall be paid upon Tenant’s execution and delivery of this Lease to Landlord. Monthly Base Rent for any partial month shall be prorated in the proportion that the number of days this Lease is in effect during such month bears to the actual number of days in such month.

5.2.Additional Rent. All amounts and charges payable by Tenant under this Lease in addition to Monthly Base Rent, if any, including, without limitation, payments for Operating Expenses, Taxes, Insurance Costs and Premises Utilities Costs to the extent payable by Tenant under this Lease shall be considered “Additional Rent”, and the word “Rent” in this Lease shall include Monthly Base Rent and all such Additional Rent unless the context specifically states or clearly implies that only Monthly Base Rent is referenced. Rent shall be paid to Landlord, without any prior notice or demand therefor and without any notice, deduction or offset, in lawful money of the United States of America.

5.3.Late Charges & Interest Rate. If Landlord does not receive Rent or any other payment due from Tenant within five (5) days after the Due Date, Tenant shall pay to Landlord a late charge equal to eight percent (8%) of such past due Rent or other payment. Tenant agrees that this late charge represents a fair and reasonable estimate of the cost Landlord will incur by reason of Tenant’s late payment. Accepting any late charge shall not constitute a waiver by Landlord of Tenant’s default with respect to any overdue amount nor prevent Landlord from exercising any other rights or remedies available to Landlord. If any installment of Monthly Base Rent or Additional Rent, or any other amount payable by Tenant hereunder is not received by Landlord by the Due Date, it shall bear interest at the Interest Rate set forth in the Summary from the Due Date until paid. All interest, and any late charges imposed pursuant to this Section 5.3, shall be considered Additional Rent due from Tenant to Landlord under the terms of this Lease. Notwithstanding the foregoing, Tenant will not be assessed the foregoing late charge and interest on the first two (2) late payments during the Term, if the applicable payment is made within five (5) days of Tenant’s receipt of notice of nonpayment from Landlord.

ARTICLE 6 - SECURITY DEPOSIT

Concurrently with Tenant’s execution and delivery of this Lease to Landlord, Tenant shall deposit with Landlord the Security Deposit, if any, designated in the Summary. The Security Deposit shall be held by Landlord as security for the full and faithful performance by Tenant of all of the terms, covenants and conditions of this Lease to be performed by Tenant during the Term. If Tenant defaults beyond the expiration of any applicable notice and cure periods with respect to any of its obligations under this Lease, Landlord may (but shall not be required to) use, apply or retain all or any part of the Security Deposit for the payment of any Monthly Base Rent, Additional Rent or any other sum in default, or for the payment of any other amount, loss or damage which Landlord may spend, incur or suffer by reason of Tenant’s default. If any portion of the Security Deposit is so used or applied, Tenant shall, within ten (10) days after demand therefor, deposit cash with Landlord in an amount sufficient to restore the Security Deposit to its original amount. Landlord shall not be required to keep the Security Deposit separate from its general funds, and Tenant shall not be entitled to interest on the Security Deposit. If Tenant shall not be in default beyond applicable notice and cure periods, the Security Deposit or any balance thereof shall be returned to Tenant within thirty (30) days following the expiration of the Term, provided that Landlord may retain the Security Deposit until such time as any amount due from Tenant in accordance with this Lease has been determined and paid in full. If Landlord sells its interest in the Building during the Term and if Landlord deposits with or credits to the purchaser the Security Deposit (or balance thereof), then, upon such sale, Landlord shall be discharged from any further liability with respect to the Security Deposit. Tenant hereby waives the provisions of Section 1950.7 of the California Civil Code to the extent such law (i) establishes the time frame by which a landlord must refund a security deposit under a lease, or (ii) provides that a landlord may claim from a security deposit only those sums reasonably necessary to remedy defaults in the payment of rent, to repair damage caused by a tenant, or to clean the subject premises.

Notwithstanding the foregoing, provided Tenant is not then in default beyond any applicable notice and cure periods and has not previously been in default beyond any applicable notice and cure periods under this Lease at any prior to the last day of the thirty-sixth (36th) full calendar month of the initial Term, on the first (1st) day of the thirty- seventh (37th) full calendar month of the initial Term (the “First Adjustment Date”), Landlord shall apply $118,223.58 of the Security Deposit against the Monthly Base Rent (for both the Office and Warehouse space) then payable by Tenant for the thirty-seventh (37th) full calendar month of the initial Term. Furthermore, provided Tenant is not then in default beyond any applicable notice and cure periods and has not previously been in default beyond any applicable notice and cure periods under this Lease at any prior to the last day of the forty-eighth (48th) full calendar month of the initial Term, on the first (1st) day of the forty-ninth (49th) full calendar month of the initial Term (the “Second Adjustment Date”), Landlord shall apply $118,223.58 of the Security Deposit against the Monthly Base Rent (for both the Office and Warehouse space) then payable by Tenant for the forty-ninth (49th) full calendar month of the initial Term. There shall be no reduction in the Security Deposit if Tenant is in default beyond any applicable notice and cure periods as of the applicable adjustment date set forth herein, or if Tenant has been in default beyond any applicable notice and cure periods under this Lease at any time prior to the First Adjustment Date of the Second Adjustment Date, as the case may be.

ARTICLE 7 - OPERATING EXPENSES/UTILITIES/SERVICES

7.1.Operating Expenses. Tenant shall pay for or contribute to the costs of operation, maintenance, repair and replacement of the Premises, Building and Property as provided in the Summary.

7.2.Utilities and Services. Utilities and services to the Premises and the Property are described in the Summary.

7.3.Taxes. As used in this Lease, the term “Taxes” means: All real property taxes and assessments, possessory interest taxes, sales taxes, personal property taxes, business or license taxes or fees, gross receipts taxes, license or use fees, excises, transit charges, and other impositions of any kind (including fees “in-lieu” or in substitution of any such tax or assessment) which are now or hereafter assessed, levied, charged or imposed by any public authority upon the Building, Site, Property and/or Premises or any portion thereof, its operations or the Rent derived therefrom (or any portion or component thereof, or the ownership, operation, or transfer thereof), and any and all costs and expenses (including, without limitation, reasonable attorneys’ fees) incurred in attempting to protest, reduce or minimize the same. Taxes shall not include inheritance or estate taxes imposed upon or assessed against the interest of Landlord, gift taxes, excess profit taxes, franchise taxes, or similar taxes on Landlord’s business or any other taxes computed upon the basis of the net income of Landlord. If it shall not be lawful for Tenant to reimburse Landlord for any such Taxes, the Monthly Base Rent payable to Landlord under this Lease shall be revised to net Landlord the same net rent after imposition of any such Taxes by Landlord as would have been payable to Landlord prior to the payment of any such Taxes. Tenant shall pay for or contribute to Taxes as part of Operating Expenses as provided in the Summary. Notwithstanding anything herein to the contrary, Tenant shall be liable for all taxes levied or assessed against personal property, furniture, fixtures, above-standard Tenant Improvements and alterations, additions or improvements placed by or for Tenant in the Premises. Furthermore, Tenant shall pay prior to delinquency any (i) rent tax or sales tax, service tax, transfer tax or value added tax, or any other applicable tax on the rent or services provided herein or otherwise respecting this Lease, (ii) taxes assessed upon or with respect to the possession, leasing, operation, management, maintenance, alteration, repair, use or occupancy by Tenant of the Premises or any portion of the Property; or (iii) taxes assessed upon this transaction or any document to which Tenant is a party creating or transferring an interest or an estate in the Premises.

7.4.Insurance Costs. As used in this Lease, “Insurance Costs” means the cost of insurance obtained by Landlord pursuant to Article 15 (including self-insured amounts and deductibles, if any, to the extent permitted under Article 15, below). Tenant shall pay for or contribute to Insurance Costs as part of Operating Expenses as provided in the Summary.

7.5.Interruption of Utilities. Landlord shall have no liability to Tenant for any interruption in utilities or services to be provided to the Premises when such failure is caused by all or any of the following: (a) accident, breakage or repairs; (b) strikes, lockouts or other labor disturbances or labor disputes of any such character;

(c)governmental regulation, moratorium or other governmental action; (d) inability, despite the exercise of reasonable diligence, to obtain electricity, water or fuel; (e) service interruptions or any other unavailability of utilities resulting from causes beyond Landlord’s control including without limitation, any electrical power “brown-out” or “black-out”; or (f) any other cause beyond Landlord’s reasonable control. In addition, in the event of any such interruption in utilities or services, Tenant shall not be entitled to any abatement or reduction of Rent (except as expressly provided in Articles 17 and 18 if such failure is a result of any casualty damage or taking described therein), no eviction of Tenant shall result, and Tenant shall not be relieved from the performance of any covenant or agreement in this Lease. In the event of any stoppage or interruption of services or utilities which are not obtained directly by Tenant, Landlord shall diligently attempt to resume such services or utilities as promptly as practicable. Tenant hereby waives the provisions of any applicable existing or future Law, ordinance or governmental regulation permitting the termination of this Lease due to an interruption, failure or inability to provide any services (including, without limitation, to the extent the Premises are located in California, the provisions of California Civil Code Section 1932(1)).

ARTICLE 8 - MAINTENANCE AND REPAIR

8.1.Landlord’s Repair Obligations. Except as otherwise stated in the Summary, Tenant waives the right to make repairs at Landlord’s expense under any applicable Laws (including, without limitation, to the extent the Premises are located in California, the provisions of California Civil Code Sections 1941 and 1942 and any successor statutes or laws of a similar nature). All other repair and maintenance of the Premises, Building and Property to be performed by Landlord, if any, shall be as provided in the Summary.

8.2.Tenant’s Repair Obligations. Except for Landlord’s obligations specifically set forth elsewhere in this Lease and in Section 8.1 above and in the Summary, Tenant shall at all times and at Tenant’s sole cost and expense, keep, maintain, clean, repair, preserve and replace, as necessary, the interior of the Premises and all parts thereof including, without limitation, all Tenant Improvements, Alterations, and all furniture, fixtures and equipment, including, without limitation, all computer, telephone and data cabling and equipment, Tenant’s signs, if any, door locks, closing devices, security devices, interior of windows, window sashes, casements and frames, floors and floor coverings, shelving, kitchen, restroom facilities and/or appliances of any kind located within the Premises, if any, custom lighting, and any additions and other property located within the Premises, so as to keep all of the foregoing elements of the Premises in good condition and repair, reasonable wear and tear and casualty damage excepted. Tenant shall replace, at its expense, any and all plate and other glass in and about the Premises which is damaged or broken from any cause whatsoever except due to the negligence or willful misconduct of Landlord, its agents or employees. Such maintenance and repairs shall be performed with due diligence, lien-free and in a first-class and workmanlike manner, by licensed contractor(s) that are selected by Tenant and approved by Landlord, which approval Landlord shall not unreasonably withhold or delay. All other repair and maintenance of the Premises, Building and Property to be performed by Tenant, if any, shall be as provided in the Summary. If Tenant refuses or neglects to repair and maintain the Premises properly as required hereunder to the reasonable satisfaction of Landlord, then at any time following ten (10) days from the date on which Landlord makes a written demand on Tenant to effect such repair and maintenance, Landlord may enter upon the Premises and make such repairs and/or maintenance, and upon completion thereof, Tenant agrees to pay to Landlord as Additional Rent, Landlord’s costs for making such repairs plus an amount not to exceed ten percent (10%) of such costs for overhead, within thirty (30) days after receipt from Landlord of a written itemized bill therefor. Any amounts not reimbursed by Tenant within such thirty (30) day period will bear interest at the Interest Rate until paid by Tenant.

ARTICLE 9 - USE

Tenant shall procure, at its sole cost and expense, any and all permits required by applicable Law for Tenant’s use and occupancy of the Premises. Tenant shall use the Premises solely for the Permitted Use specified in the Summary, and shall not use or permit the Premises to be used for any other use or purpose whatsoever without Landlord’s prior written approval. Tenant shall observe and comply with the Rules and Regulations attached hereto as Exhibit E, as the same may be modified by Landlord from time to time, and all reasonable non-discriminatory modifications thereof and additions thereto from time to time put into effect and furnished to Tenant by Landlord. Landlord shall endeavor to enforce the Rules and Regulations, but shall have no liability to

Tenant for the violation or non-performance by any other tenant or occupant of any such Rules and Regulations. Tenant shall not use or allow the Premises to be used for any improper, immoral, unlawful or reasonably objectionable purpose. Tenant shall not do or permit to be done anything that will obstruct or interfere with the rights of other tenants or occupants of the Building or the Property, if any, or injure or annoy them. Tenant shall not cause, maintain or permit any nuisance in, on or about the Premises, the Building or the Property, nor commit or suffer to be committed any waste in, on or about the Premises. Without limiting the foregoing, Tenant agrees that the Premises shall not be used for the use, growing, producing, processing, storing (short or long term), distributing, transporting, or selling of marijuana, cannabis, cannabis derivatives, or any cannabis containing substances (“Cannabis”), or any office uses related to the same, nor shall Tenant permit, allow or suffer, any of Tenant’s officers, employees, agents, servants, licensees, subtenants, concessionaires, contractors and invitees to bring onto the Premises, any Cannabis. Without limiting the foregoing, the prohibitions in this paragraph shall apply to all Cannabis, whether such Cannabis is legal for any purpose whatsoever under state or federal law or both. Notwithstanding anything to the contrary, any failure b y Tenant to comply with each of the terms, covenants, conditions and provisions of this paragraph relating to Cannabis shall automatically and without the requirement of any notice be a Default that is not subject to cure, and Tenant agrees that upon the occurrence of any such Default, Landlord may elect, in its sole discretion, to exercise all of its rights and remedies under this Lease, at law or in equity with respect to such Default. Furthermore Tenant is prohibited from engaging or permitting others to engage in any activity which would be a violation of any state and/or federal laws relating to the use, sale, possession, cultivation and/or distribution of any controlled substances (whether for commercial or personal purposes) regulated under any applicable law or other applicable law relating to the medicinal use and/or distribution of marijuana/Cannabis (“Prohibited Drug Law Activities”).

Tenant shall, at its sole cost and expense, observe and comply with all Laws and all requirements of any board of fire underwriters or similar body relating to (i) Tenant's particular use of the Premises, (ii) the Alterations or the Tenant Improvements in the Premises (as opposed to any pre-existing improvements in the Premises), or (iii) the Base Building, but, as to the Base Building, only to the extent such obligations are triggered by (x) Tenant's Alterations or the Tenant Improvements to the extent the same are non-general office improvements (i.e., any changes that would be required simply by “pulling a permit,” whether by Tenant, another tenant or Landlord for improvements to the Premises, would be a Landlord obligation pursuant to Section 9.3, below), or (z) Tenant’s particular use of the Premises for non-general office use. The "Base Building" shall include the structural portions of the Building, and the public restrooms, elevators, exit stairwells and the systems and equipment located in the internal core of the Building on the floor or floors on which the Premises is located.

Landlord shall comply with all applicable Laws relating to the Common Areas of the Property and Base Building, provided that compliance with such applicable Laws is not the responsibility of Tenant under this Lease (such as improvements to the Common Areas required in connection with Tenant’s particular use of the Premises for non-general office use and other requirements described in the immediately preceding paragraph), and provided further that Landlord's failure to comply therewith would prohibit Tenant from obtaining or maintaining a certificate of occupancy for the Premises, or would unreasonably and materially affect the safety of Tenant's employees or create a significant health hazard for Tenant's employees. Landlord shall be permitted to include in Operating Expenses any costs or expenses incurred by Landlord under this Section 9.3 to the extent not prohibited by the terms of Section 1.18 above.

ARTICLE 10 - HAZARDOUS MATERIALS