UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-22027

FundVantage Trust

(Exact name of registrant as specified in charter)

301 Bellevue Parkway

Wilmington, DE 19809

(Address of principal executive offices) (Zip code)

Joel L. Weiss

JW Fund Management LLC

1636 N. Cedar Crest Blvd.

Suite #161

Allentown, PA 18104

(Name and address of agent for service)

Registrant’s telephone number, including area code: 856-528-3500

Date of fiscal year end: April 30

Date of reporting period: April 30, 2023

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

| (a) | The Report to Shareholders is attached herewith. |

| Class A |

| Class C |

| Institutional Class |

| 1 | Data Source: S&P Capital IQPRO. December 31, 2019 and March 31, 2022 total deposits on balance sheets of SIVB and SBNY. |

| 2 | Data Source: Federal Financial Institutions Examination Council. Consolidated Reports of Condition and Income for SIVB and SBNY as of December 31, 2022. Deposit accounts of $250,000 or less as a percentage of total deposit liabilities of the bank. |

| 3 | Data Source: S&P Capital IQPRO. March 31, 2022 and December 31, 2022 total deposits on balance sheets of SIVB and SBNY. |

| 4 | The Russell 3000® Index measures the performance of the largest 3,000 U.S. companies representing approximately 96% of the investable U.S. equity market and is constructed to provide a comprehensive, unbiased, and stable barometer of the broad market. |

| 5 | Price/Projected Earnings (P/E) as of April 30, 2023, 2022 annual and year-to-date 2023 total return of Russell 3000® Index constituents. Constituents that were public for all of 2022 are divided equally into five buckets by annual total return as of December 31, 2022. For each bucket 2023 total return metrics and forward P/E are calculated as of April 30, 2023 on an index-weighted basis using weights at December 31, 2022. |

| 6 | Data Source: S&P Capital IQPRO. Loss-making companies are Russell 3000® Index constituents that were expected to be unprofitable over the next 12 months from January 1, 2022 and produced an index-weighted -51% total return for 2022. Constituents that were expected to be unprofitable over the next 12 months from January 1, 2023 produced an index-weighted 10.5% total return for year-to-date 2023 as of April 30, 2023. |

| 7 | Data Source: S&P Capital IQPRO. Annual returns calculated from quarterly price returns of the S&P 500® Index for January 1, 1929 through December 31, 1936 and quarterly total returns for January 1, 1937 through December 31, 2022. |

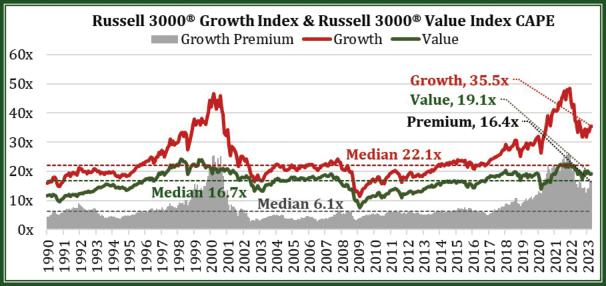

| 8 | Russell 3000® Growth Index modified CAPE premium over Russell 3000® Value Index modified CAPE at each month-end January 31, 1990 to April 30, 2013, plotted against the subsequent annualized 10-year total return difference between the Russell 3000® Growth Index and Russell 3000® Value Index for each month-end January 31, 2000 through April 30, 2023. Modified CAPE (Cyclically Adjusted Price-to-Earnings) is the ratio of index prices to trailing 10-year index-level earnings before taxes (EBT) on a time-weighted basis. Annual index level EBT is imputed by dividing the year-end index price by an aggregated price to EBT multiple of index constituents. A 16.4x valuation premium of growth over value indicates 5–7% per year historical underperformance of growth versus value over the following 10 years. |

| 9 | Russell 3000® Growth Index modified CAPE (red line), Russell 3000® Value Index modified CAPE (green line),

Russell 3000® Growth Index modified CAPE premium over Russell 3000® Value Index modified CAPE

(gray area) at each month-end from January 31, 1990 to April 30, 2023. |

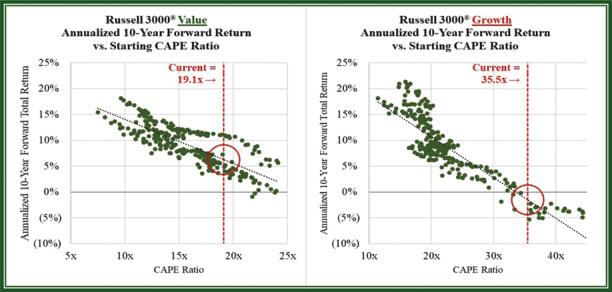

| 10 | (Left Chart) Russell 3000® Value Index modified CAPE at each month-end January 31, 1990 to April 30, 2013, plotted against the subsequent annualized 10-year total return of the Russell 3000® Value Index for each month-end January 31, 2000 through April 30, 2023. (Right Chart) Russell 3000® Growth Index modified CAPE at each month-end from January 31, 1990 to April 30, 2013, plotted against the subsequent annualized 10-year total return of the Russell 3000® Growth Index for each month-end January 31, 2000 through April 30, 2023. |

| 11 | Data Source: S&P Capital IQPRO. Monthly trend of S&P 500 Index Aggregate Bottom Up earnings per share estimates for 2023 from September 6, 2022 through May 3, 2023. |

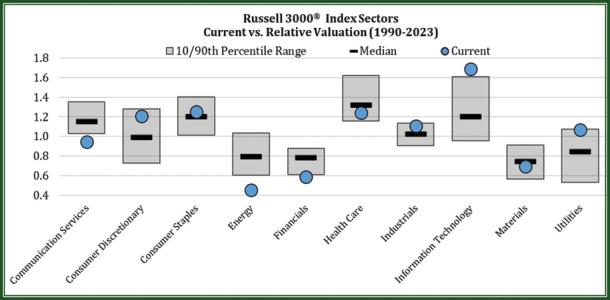

| 12 | Russell 3000® Index sector valuation relative to Russell 3000® Index valuation based on constituent price to prior three-year peak earnings for month-end periods from January 31, 1990 to April 30, 2023. Real Estate sector excluded. |

| 13 | Normalized earnings are EIC’s estimate of a company’s annual earnings per share when adjusting for temporary, unusual, or non-recurring items (e.g., margin pressure from supply chain bottlenecks, pandemic-related revenues, unusually high or low commodity prices, etc.). |

| 14 | Data Source: S&P Capital IQPRO. All credit-quality ratings discussed in this section represent Standard & Poor’s (S&P) opinion as to the quality of the securities they rate as of April 30, 2023, unless otherwise indicated. The ratings range from AAA (extremely strong capacity to meet its financial commitments) to D (in default). Ratings are relative and subjective and are not absolute standards of quality. |

| 15 | Buffett, Warren E., Chairman’s Letter, 28 February 2002. Berkshire Hathaway Inc. Annual Report 2001. https://www. berkshirehathaway.com/ 2001ar/2001letter.html. |

| 16 | Data Source: Morningstar Direct℠ as of April 30, 2023. Weighted average trailing twelve-month Price/Earnings Ratio, trailing twelve-month return on equity, and estimated five-year long-term earnings growth for The EIC Value Fund, as calculated by Morningstar. |

and S&P 500® Index

| Average Annual Total Returns for the Years Ended April 30, 2023 | |||||||

| 1 Year | 3 Years | 5 Years | 10 Years | ||||

| Class A (with sales charge) | -3.82% | 15.71% | 8.41% | 8.19% | |||

| Class A (without sales charge) | 1.80% | 17.90% | 9.64% | 8.80% | |||

| Russell 3000® Value Index | 0.67% | 14.46% | 7.48% | 8.98% | |||

| S&P 500® Index | 2.66% | 14.52% | 11.45% | 12.20% | |||

| Average Annual Total Returns for the Years Ended April 30, 2023 | |||||||

| 1 Year | 3 Years | 5 Years | 10 Years | ||||

| Class C (with CDSC charge) | 0.12% | 17.03% | 8.80% | 7.99% | |||

| Class C (without CDSC charge) | 1.07% | 17.03% | 8.80% | 7.99% | |||

| Russell 3000® Value Index | 0.67% | 14.46% | 7.48% | 8.98% | |||

| S&P 500® Index | 2.66% | 14.52% | 11.45% | 12.20% | |||

and S&P 500® Index

| Average Annual Total Returns for the Years Ended April 30, 2023 | |||||||

| 1 Year | 3 Years | 5 Years | 10 Years | ||||

| Institutional Class | 2.06% | 18.18% | 9.90% | 9.07% | |||

| Russell 3000® Value Index | 0.67% | 14.46% | 7.48% | 8.98% | |||

| S&P 500® Index | 2.66% | 14.52% | 11.45% | 12.20% | |||

| Beginning

Account Value November 1, 2022 |

Ending

Account Value April 30, 2023 |

Annualized

Expense Ratio |

Expenses

Paid During Period* | ||||

| EIC Value Fund | |||||||

| Class A | |||||||

| Actual | $1,000.00 | $1,046.70 | 1.20% | $6.09 | |||

| Hypothetical (5% return before expenses) | 1,000.00 | 1,018.84 | 1.20% | 6.01 | |||

| Class C | |||||||

| Actual | $1,000.00 | $1,043.20 | 1.95% | $9.88 | |||

| Hypothetical (5% return before expenses) | 1,000.00 | 1,015.12 | 1.95% | 9.74 | |||

| Institutional Class | |||||||

| Actual | $1,000.00 | $1,048.00 | 0.95% | $4.82 | |||

| Hypothetical (5% return before expenses) | 1,000.00 | 1,020.08 | 0.95% | 4.76 | |||

| * | Expenses are equal to the Fund’s annualized expense ratio for the six-month period ended April 30, 2023 of 1.20%, 1.95%, and 0.95% for Class A, Class C, and Institutional Class shares, respectively, multiplied by the average account value over the period, multiplied by the number of days in the most recent period (181), then divided by 365 to reflect the period. The Fund’s ending account values on the first line in each table are based on the actual six-month total returns for the Fund of 4.67%, 4.32%, and 4.80% for Class A, Class C, and Institutional Class shares, respectively. |

| %

of Net Assets |

Value | ||

| COMMON STOCKS: | |||

| Financial | 25.3% | $ 64,694,922 | |

| Consumer, Non-cyclical | 23.3 | 59,640,970 | |

| Communications | 13.8 | 35,354,532 | |

| Energy | 11.5 | 29,498,571 | |

| Industrial | 7.3 | 18,580,635 | |

| Basic Materials | 4.0 | 10,240,399 | |

| Utilities | 3.7 | 9,527,516 | |

| Consumer, Cyclical | 3.7 | 9,488,943 | |

| Technology | 2.0 | 5,221,676 | |

| Exchange Traded Funds | 1.0 | 2,544,168 | |

| Short-Term Investment | 2.7 | 6,778,453 | |

| Other Assets in Excess of Liabilities | 1.7 | 4,420,728 | |

| NET ASSETS | 100.0% | $255,991,513 |

| Assets | |

| Investments, at value (Cost $201,581,968) | $251,570,785 |

| Receivables: | |

| Investments sold | 3,734,108 |

| Capital shares sold | 437,056 |

| Dividends and interest | 694,248 |

| Prepaid expenses and other assets | 13,405 |

| Total Assets | 256,449,602 |

| Liabilities | |

| Payables: | |

| Capital shares redeemed | 165,774 |

| Investment adviser | 126,622 |

| Transfer agent fees | 47,967 |

| Administration and accounting fees | 36,286 |

| Audit fees | 33,755 |

| Shareholder reporting fees | 25,522 |

| Distribution fees (Class A and C Shares) | 8,429 |

| Shareholder servicing fees | 1,327 |

| Accrued expenses | 12,407 |

| Total Liabilities | 458,089 |

| Net Assets | $255,991,513 |

| Net Assets Consisted of: | |

| Capital stock, $0.01 par value | $ 165,809 |

| Paid-in capital | 204,769,945 |

| Total distributable earnings | 51,055,759 |

| Net Assets | $255,991,513 |

| Class A Shares: | |

| Net assets | $ 21,775,861 |

| Shares outstanding | 1,411,313 |

| Net asset value, redemption price per share | $ 15.43 |

| Maximum offering price per share (100/94.50 of $15.43) | $ 16.33 |

| Class C Shares: | |

| Net assets | $ 6,371,446 |

| Shares outstanding | 426,219 |

| Net asset value, offering and redemption price per share | $ 14.95 |

| Institutional Class Shares: | |

| Net assets | $227,844,206 |

| Shares outstanding | 14,743,320 |

| Net asset value, offering and redemption price per share | $ 15.45 |

| Investment income | |

| Dividends | $ 8,178,109 |

| Less: foreign taxes withheld | (221,637) |

| Total investment income | 7,956,472 |

| Expenses | |

| Advisory fees (Note 2) | 1,871,193 |

| Transfer agent fees (Note 2) | 171,097 |

| Administration and accounting fees (Note 2) | 141,265 |

| Registration and filing fees | 79,951 |

| Shareholder reporting fees | 63,261 |

| Distribution fees (Class C)(Note 2) | 56,765 |

| Trustees’ and officers’ fees(Note 2) | 51,139 |

| Distribution fees (Class A)(Note 2) | 50,174 |

| Custodian fees(Note 2) | 45,606 |

| Legal fees | 43,400 |

| Audit fees | 33,755 |

| Shareholder servicing fees (Class C) | 18,922 |

| Other expenses | 21,148 |

| Total expenses before waivers and reimbursements | 2,647,676 |

| Less: waivers and reimbursements(Note 2) | (151,677) |

| Net expenses after waivers and reimbursements | 2,495,999 |

| Net investment income | 5,460,473 |

| Net realized and unrealized gain/(loss) from investments: | |

| Net realized loss from investments | (4,190,123) |

| Net change in unrealized appreciation on investments | 3,506,318 |

| Net realized and unrealized loss on investments | (683,805) |

| Net increase in net assets resulting from operations | $ 4,776,668 |

| For

the Year Ended April 30, 2023 |

For

the Year Ended April 30, 2022 | ||

| Net increase/(decrease) in net assets from operations: | |||

| Net investment income | $ 5,460,473 | $ 3,226,519 | |

| Net realized gains/(losses) from investments | (4,190,123) | 23,688,598 | |

| Net change in unrealized appreciation/(depreciation) on investments | 3,506,318 | (13,539,396) | |

| Net increase in net assets resulting from operations | 4,776,668 | 13,375,721 | |

| Less dividends and distributions to shareholders from: | |||

| Total distributable earnings: | |||

| Class A | (1,180,466) | (1,699,293) | |

| Class C | (425,777) | (993,191) | |

| Institutional Class | (12,910,018) | (16,626,160) | |

| Net decrease in net assets from dividends and distributions to shareholders | (14,516,261) | (19,318,644) | |

| Increase in net assets derived from capital share transactions (Note 4) | 29,838,380 | 64,164,853 | |

| Total increase in net assets | 20,098,787 | 58,221,930 | |

| Net assets | |||

| Beginning of year | 235,892,726 | 177,670,796 | |

| End of year | $255,991,513 | $235,892,726 |

| Class A | |||||||||

| For

the Year Ended April 30, 2023 |

For

the Year Ended April 30, 2022 |

For

the Year Ended April 30, 2021 |

For

the Year Ended April 30, 2020 |

For

the Year Ended April 30, 2019 | |||||

| Per Share Operating Performance | |||||||||

| Net asset value, beginning of year | $ 16.08 | $ 16.48 | $ 11.75 | $13.98 | $ 14.33 | ||||

| Net investment income(1) | 0.31 | 0.24 | 0.20 | 0.23 | 0.21 | ||||

| Net realized and unrealized gain/(loss) on investments | (0.04) | 1.10 | 5.33 | (1.42) | 0.68 | ||||

| Total from investment operations | 0.27 | 1.34 | 5.53 | (1.19) | 0.89 | ||||

| Dividends and distributions to shareholders from: | |||||||||

| Net investment income | — | (0.23) | (0.23) | (0.21) | (0.16) | ||||

| Net realized capital gains | (0.92) | (1.51) | (0.57) | (0.83) | (1.08) | ||||

| Total dividends and distributions to shareholders | (0.92) | (1.74) | (0.80) | (1.04) | (1.24) | ||||

| Redemption fees | 0.00 (2) | 0.00 (2) | 0.00 (2) | 0.00 (2) | 0.00 (2) | ||||

| Net asset value, end of year | $ 15.43 | $ 16.08 | $ 16.48 | $11.75 | $ 13.98 | ||||

| Total investment return(3) | 1.80% | 8.39% | 48.52% | (9.54)% | 6.86% | ||||

| Ratios/Supplemental Data | |||||||||

| Net assets, end of year (in 000s) | $21,776 | $19,522 | $11,784 | $8,347 | $15,019 | ||||

| Ratio of expenses to average net assets | 1.20% | 1.20% | 1.18% | 1.15% | 1.18% | ||||

| Ratio of expenses to average net assets without waivers and/or reimbursements | 1.26% (4) | 1.25% (4) | 1.32% (4) | 1.24% (4) | 1.23% (4) | ||||

| Ratio of net investment income to average net assets | 1.99% | 1.44% | 1.45% | 1.67% | 1.47% | ||||

| Portfolio turnover rate | 39% | 33% | 41% | 36% | 42% | ||||

| (1) | The selected per share data was calculated using the average shares outstanding method for the year. |

| (2) | Amount is less than $0.005 per share. |

| (3) | Total investment return is calculated assuming a purchase of shares on the first day and a sale of shares on the last day of each period reported and includes reinvestment of dividends and distributions, if any. Total investment return does not reflect the impact of the maximum front-end sales load of 5.50% or any applicable sales charge. If reflected, the return would be lower. |

| (4) | During the period, certain fees were waived and/or reimbursed. If such fee waivers and/or reimbursements had not occurred, the ratios would have been as indicated (See Note 2). |

| Class C | |||||||||

| For

the Year Ended April 30, 2023 |

For

the Year Ended April 30, 2022 |

For

the Year Ended April 30, 2021 |

For

the Year Ended April 30, 2020 |

For

the Year Ended April 30, 2019 | |||||

| Per Share Operating Performance | |||||||||

| Net asset value, beginning of year | $15.72 | $16.10 | $ 11.52 | $ 13.73 | $ 14.12 | ||||

| Net investment income(1) | 0.19 | 0.11 | 0.09 | 0.12 | 0.10 | ||||

| Net realized and unrealized gain/(loss) on investments | (0.04) | 1.07 | 5.22 | (1.41) | 0.67 | ||||

| Total from investment operations | 0.15 | 1.18 | 5.31 | (1.29) | 0.77 | ||||

| Dividends and distributions to shareholders from: | |||||||||

| Net investment income | — | (0.05) | (0.16) | (0.09) | (0.08) | ||||

| Net realized capital gains | (0.92) | (1.51) | (0.57) | (0.83) | (1.08) | ||||

| Total dividends and distributions to shareholders | (0.92) | (1.56) | (0.73) | (0.92) | (1.16) | ||||

| Redemption fees | 0.00 (2) | 0.00 (2) | 0.00 (2) | 0.00 (2) | 0.00 (2) | ||||

| Net asset value, end of year | $14.95 | $15.72 | $ 16.10 | $ 11.52 | $ 13.73 | ||||

| Total investment return(3) | 1.07% | 7.56% | 47.46% | (10.30)% | 6.05% | ||||

| Ratios/Supplemental Data | |||||||||

| Net assets, end of year (in 000s) | $6,371 | $8,933 | $16,926 | $17,926 | $27,407 | ||||

| Ratio of expenses to average net assets | 1.95% | 1.95% | 1.93% | 1.90% | 1.93% | ||||

| Ratio of expenses to average net assets without waivers and/or reimbursements | 2.01% (4) | 2.00% (4) | 2.07% (4) | 1.99% (4) | 1.98% (4) | ||||

| Ratio of net investment income to average net assets | 1.24% | 0.69% | 0.70% | 0.92% | 0.71% | ||||

| Portfolio turnover rate | 39% | 33% | 41% | 36% | 42% | ||||

| (1) | The selected per share data was calculated using the average shares outstanding method for the year. |

| (2) | Amount is less than $0.005 per share. |

| (3) | Total investment return is calculated assuming a purchase of shares on the first day and a sale of shares on the last day of each period reported and includes reinvestment of dividends and distributions, if any. Total investment return does not reflect any applicable sales charge. |

| (4) | During the period, certain fees were waived and/or reimbursed. If such fee waivers and/or reimbursements had not occurred, the ratios would have been as indicated (See Note 2). |

| Institutional Class | |||||||||

| For

the Year Ended April 30, 2023 |

For

the Year Ended April 30, 2022 |

For

the Year Ended April 30, 2021 |

For

the Year Ended April 30, 2020 |

For

the Year Ended April 30, 2019 | |||||

| Per Share Operating Performance | |||||||||

| Net asset value, beginning of year | $ 16.06 | $ 16.46 | $ 11.73 | $ 13.97 | $ 14.37 | ||||

| Net investment income(1) | 0.35 | 0.28 | 0.23 | 0.26 | 0.24 | ||||

| Net realized and unrealized gain/(loss) on investments | (0.04) | 1.10 | 5.32 | (1.42) | 0.69 | ||||

| Total from investment operations | 0.31 | 1.38 | 5.55 | (1.16) | 0.93 | ||||

| Dividends and distributions to shareholders from: | |||||||||

| Net investment income | — | (0.27) | (0.25) | (0.25) | (0.25) | ||||

| Net realized capital gains | (0.92) | (1.51) | (0.57) | (0.83) | (1.08) | ||||

| Total dividends and distributions to shareholders | (0.92) | (1.78) | (0.82) | (1.08) | (1.33) | ||||

| Redemption fees | 0.00 (2) | 0.00 (2) | 0.00 (2) | 0.00 (2) | 0.00 (2) | ||||

| Net asset value, end of year | $ 15.45 | $ 16.06 | $ 16.46 | $ 11.73 | $ 13.97 | ||||

| Total investment return(3) | 2.06% | 8.64% | 48.85% | (9.36)% | 7.16% | ||||

| Ratios/Supplemental Data | |||||||||

| Net assets, end of year (in 000s) | $227,844 | $207,437 | $148,961 | $113,292 | $173,468 | ||||

| Ratio of expenses to average net assets | 0.95% | 0.95% | 0.93% | 0.90% | 0.93% | ||||

| Ratio of expenses to average net assets without waivers and/or reimbursements | 1.01% (4) | 1.00% (4) | 1.07% (4) | 0.99% (4) | 0.99% (4) | ||||

| Ratio of net investment income to average net assets | 2.24% | 1.69% | 1.70% | 1.91% | 1.72% | ||||

| Portfolio turnover rate | 39% | 33% | 41% | 36% | 42% | ||||

| (1) | The selected per share data was calculated using the average shares outstanding method for the year. |

| (2) | Amount is less than $0.005 per share. |

| (3) | Total investment return is calculated assuming a purchase of shares on the first day and a sale of shares on the last day of each period reported and includes reinvestment of dividends and distributions, if any. |

| (4) | During the period, certain fees were waived and/or reimbursed. If such fee waivers and/or reimbursements had not occurred, the ratios would have been as indicated (See Note 2). |

| Total

Value at 04/30/23 |

Level

1 Quoted Prices |

Level

2 Other Significant Observable Inputs |

Level

3 Significant Unobservable Inputs | ||||

| Assets | |||||||

| Common Stocks* | $ 242,248,164 | $ 242,248,164 | $ — | $ — | |||

| Exchange Traded Funds* | 2,544,168 | 2,544,168 | — | — | |||

| Short-Term Investments* | 6,778,453 | 6,778,453 | — | — | |||

| Total Assets | $ 251,570,785 | $ 251,570,785 | $ — | $ — |

| * | Please refer to Portfolio of Investments for further details on portfolio holdings. |

| Expiration | |||||||

| 04/30/2024 | 04/30/2025 | 04/30/2026 | Total | ||||

| $189,225 | $104,148 | $151,677 | $445,050 | ||||

| Purchases | Sales | ||

| Investment Securities | $113,095,838 | $91,022,099 |

| For

the Year Ended April 30, 2023 |

For

the Year Ended April 30, 2022 | ||||||

| Shares | Amount | Shares | Amount | ||||

| Class A | |||||||

| Sales | 326,841 | $ 5,075,997 | 552,866 | $ 9,249,204 | |||

| Reinvestments | 71,941 | 1,089,899 | 99,610 | 1,565,872 | |||

| Redemption Fees* | — | 411 | — | 444 | |||

| Redemptions | (201,732) | (3,117,450) | (153,445) | (2,582,919) | |||

| Net increase | 197,050 | $ 3,048,857 | 499,031 | $ 8,232,601 | |||

| For

the Year Ended April 30, 2023 |

For

the Year Ended April 30, 2022 | ||||||

| Shares | Amount | Shares | Amount | ||||

| Class C | |||||||

| Sales | 108,951 | $ 1,656,613 | 53,779 | $ 879,446 | |||

| Reinvestments | 27,557 | 405,649 | 62,070 | 956,505 | |||

| Redemption Fees* | — | 144 | — | 260 | |||

| Redemptions | (278,587) | (4,186,873) | (599,087) | (9,784,506) | |||

| Net decrease | (142,079) | $ (2,124,467) | (483,238) | $ (7,948,295) | |||

| Institutional Class | |||||||

| Sales | 4,735,378 | $ 73,679,118 | 4,706,008 | $ 78,828,319 | |||

| Reinvestments | 788,658 | 11,956,048 | 1,038,153 | 16,288,620 | |||

| Redemption Fees* | — | 4,516 | — | 4,766 | |||

| Redemptions | (3,695,740) | (56,725,692) | (1,880,784) | (31,241,158) | |||

| Net increase | 1,828,296 | $ 28,913,990 | 3,863,377 | $ 63,880,547 | |||

| Total net increase | 1,883,267 | $ 29,838,380 | 3,879,170 | $ 64,164,853 | |||

| * | There is a 2.00% redemption fee that may be charged on shares redeemed which have been held 30 days or less. The redemption fees are retained by the Fund for the benefit of the remaining shareholders and recorded as paid-in capital. |

| Capital

Loss Carryforward |

Undistributed

Ordinary Income |

Unrealized

Appreciation/ (Depreciation) | |||

| $(4,201,943) | $5,383,631 | $49,874,071 | |||

| Federal Tax Cost | $201,696,714 |

| Unrealized Appreciation | 52,825,799 |

| Unrealized Depreciation | (2,951,728) |

| Net Unrealized Appreciation | $ 49,874,071 |

Shareholders of EIC Value Fund

| Name

and Date of Birth |

Position(s)

Held with Trust |

Term

of Office and Length of Time Served |

Principal

Occupation(s) During Past Five Years |

Number

of Funds in Trust Complex Overseen by Trustee |

Other

Directorships Held by Trustee |

| INDEPENDENT TRUSTEES | |||||

| ROBERT

J. CHRISTIAN Date of Birth: 2/49 |

Trustee | Shall

serve until death, resignation or removal. Trustee since 2007. Chairman from 2007 until September 30, 2019. |

Retired

since February 2006; Executive Vice President of Wilmington Trust Company from February 1996 to February 2006; President of Rodney Square Management Corporation (“RSMC”) (investment advisory firm) from 1996 to 2005; Vice President of RSMC from 2005 to 2006. |

36 | Optimum

Fund Trust (registered investment company with 6 portfolios); Third Avenue Trust (registered investment company with 4 portfolios); Third Avenue Variable Series Trust (registered investment company with 1 portfolio). |

| IQBAL

MANSUR Date of Birth: 6/55 |

Trustee | Shall

serve until death, resignation or removal. Trustee since 2007. |

Retired

since September 2020; Professor of Finance, Widener University from 1998 to August 2020; Member of the Investment Committee of ChristianaCare Health System from January 2022 to present. |

36 | Third

Avenue Trust (registered investment company with 4 portfolios); Third Avenue Variable Series Trust (registered investment company with 1 portfolio). |

| Name

and Date of Birth |

Position(s)

Held with Trust |

Term

of Office and Length of Time Served |

Principal

Occupation(s) During Past Five Years |

Number

of Funds in Trust Complex Overseen by Trustee |

Other

Directorships Held by Trustee |

| NICHOLAS

M. MARSINI, JR. Date of Birth: 8/55 |

Trustee

and Chairman of the Board |

Shall

serve until death, resignation or removal. Trustee since 2016. Chairman since October 1, 2019. |

Retired

since March 2016. President of PNC Bank Delaware from June 2011 to March 2016; Executive Vice President of Finance of BNY Mellon from July 2010 to January 2011; Executive Vice President and Chief Financial Officer of PNC Global Investment Servicing from September 1997 to July 2010. |

36 | Brinker

Capital Destinations Trust (registered investment company with 10 portfolios); Third Avenue Trust (registered investment company with 4 portfolios); Third Avenue Variable Series Trust (registered investment company with 1 portfolio). |

| NANCY

B. WOLCOTT Date of Birth: 11/54 |

Trustee | Shall

serve until death, resignation or removal. Trustee since 2011. |

Retired since May 2014; EVP, Head of GFI Client Service Delivery, BNY Mellon from January 2012 to May 2014; EVP, Head of US Funds Services, BNY Mellon from July 2010 to January 2012; President of PNC Global Investment Servicing from 2008 to July 2010; Chief Operating Officer of PNC Global Investment Servicing from 2007 to 2008; Executive Vice President of PFPC Worldwide Inc. from 2006 to 2007. | 36 | Lincoln

Variable Trust Products Trust (registered investment company with 97 portfolios); Third Avenue Trust (registered investment company with 4 portfolios); Third Avenue Variable Series Trust (registered investment company with 1 portfolio). |

| Name

and Date of Birth |

Position(s)

Held with Trust |

Term

of Office and Length of Time Served |

Principal

Occupation(s) During Past Five Years |

Number

of Funds in Trust Complex Overseen by Trustee |

Other

Directorships Held by Trustee |

| STEPHEN

M. WYNNE Date of Birth: 1/55 |

Trustee | Shall

serve until death, resignation or removal. Trustee since 2009. |

Retired

since December 2010; Chief Executive Officer of US Funds Services, BNY Mellon Asset Servicing from July 2010 to December 2010; Chief Executive Officer of PNC Global Investment Servicing from March 2008 to July 2010; President, PNC Global Investment Servicing from 2003 to 2008. |

36 | Copeland

Trust (registered investment company with 3 portfolios); Third Avenue Trust (registered investment company with 4 portfolios); Third Avenue Variable Series Trust (registered investment company with 1 portfolio). |

| Name

and Date of Birth |

Position(s)

Held with Trust |

Term

of Office and Length of Time Served |

Principal

Occupation(s) During Past Five Years |

| EXECUTIVE OFFICERS | |||

| JOEL

L. WEISS Date of Birth: 1/63 |

President

and Chief Executive Officer |

Shall

serve until death, resignation or removal. Officer since 2007. |

President of JW Fund Management LLC since June 2016; Vice President and Managing Director of BNY Mellon Investment Servicing (US) Inc. and predecessor firms from 1993 to June 2016. |

| CHRISTINE

S. CATANZARO Date of Birth: 8/84 |

Treasurer and Chief Financial Officer | Shall

serve until death, resignation or removal. Officer since 2022. |

Financial Reporting Consultant from October 2020 to September 2022; Senior Manager, Ernst & Young LLP from March 2013 to October 2020. |

| T.

RICHARD KEYES Date of Birth: 1/57 |

Vice

President |

Shall

serve until death, resignation or removal. Officer since 2016. |

President of TRK Fund Consulting LLC since July 2016; Head of Tax — U.S. Fund Services of BNY Mellon Investment Servicing (US) Inc. and predecessor firms from February 2006 to July 2016. |

| GABRIELLA

MERCINCAVAGE Date of Birth: 6/68 |

Assistant Treasurer | Shall

serve until death, resignation or removal. Officer since 2019. |

Fund

Administration Consultant since January 2019; Fund Accounting and Tax Compliance Accountant to financial services companies from November 2003 to July 2018. |

| VINCENZO

A. SCARDUZIO Date of Birth: 4/72 |

Secretary | Shall

serve until death, resignation or removal. Officer since 2012. |

Director and Vice President Regulatory Administration of The Bank of New York Mellon and predecessor firms since 2001. |

| JOHN

CANNING Date of Birth: 11/70 |

Chief

Compliance Officer and Anti-Money Laundering Officer |

Shall

serve until death, resignation or removal. Officer since 2022. |

Director of Chenery Compliance Group, LLC from March 2021 to present; Senior Consultant of Foreside Financial Group from August 2020 to March 2021; Chief Compliance Officer & Chief Operating Officer of Schneider Capital Management LP from May 2019 to July 2020; Chief Operating Officer and Chief Compliance Officer of Context Capital Partners, LP from March 2016 to March 2018 and February 2019, respectively. |

301 Bellevue Parkway

Wilmington, DE 19809

500 Ross Street, 154-0520

Pittsburgh, PA 15262

Three Canal Plaza, Suite 100

Portland, ME 04101

240 Greenwich Street

New York, NY 10286

3000 Two Logan Square

18th and Arch Streets

| Pacific Capital Tax-Free Securities Fund |

| Pacific Capital Tax-Free Short Intermediate Securities Fund |

| Class Y |

| Average Annual Total Returns for the Years Ended April 30, 2023 | |||||||

| 1 Year | 3 Years | 5 Years | 10 Years | ||||

| Class Y | 2.49% | 0.36% | 1.88% | 1.84% | |||

| Bloomberg Hawaii Municipal Bond Index | 3.11% | 0.54% | 2.05% | 2.15% | |||

| Average Annual Total Returns for the Years Ended April 30, 2023 | |||||||

| 1 Year | 3 Years | 5 Years | 10 Years | ||||

| Class Y | 2.16% | 0.49% | 1.29% | 0.92% | |||

| Bloomberg Hawaii 3-Year Municipal Bond Index | 1.90% | -0.15% | 1.12% | 0.95% | |||

| Beginning

Account Value November 1, 2022 |

Ending

Account Value April 30, 2023 |

Annualized

Expense Ratio |

Expenses

Paid During Period* | ||||

| Pacific Capital Tax-Free Securities Fund | |||||||

| Class Y | |||||||

| Actual | $1,000.00 | $1,059.00 | 0.14% | $0.71 | |||

| Hypothetical (5% return before expenses) | 1,000.00 | 1,024.10 | 0.14% | 0.70 | |||

| Pacific Capital Tax-Free Short Intermediate Securities Fund | |||||||

| Class Y | |||||||

| Actual | $1,000.00 | $1,032.40 | 0.36% | $1.81 | |||

| Hypothetical (5% return before expenses) | 1,000.00 | 1,023.01 | 0.36% | 1.81 | |||

| * | Expenses are equal to an annualized expense ratio for the six-month period ended April 30, 2023 of 0.14% for the Pacific Capital Tax-Free Securities Fund and 0.36% for the Pacific Capital Tax-Free Short Intermediate Securities Fund, multiplied by average account value over the period, multiplied by the number of days in the most recent period (181), then divided by 365 to reflect the period. The Funds’ ending account values on the first line in each table are based on the actual six-month total returns of 5.90% for the Pacific Capital Tax-Free Securities Fund and 3.24% for the Pacific Capital Tax-Free Short Intermediate Securities Fund. |

| Credit Quality: | % of Total Investments |

| Pre-refunded/Escrowed to Maturity | 0.99% |

| Aaa | 8.28 |

| Aa | 77.37 |

| A | 8.02 |

| Baa | 4.94 |

| Cash | 0.40 |

| Total | 100.00% |

| (a) | Zero coupon bond. |

| (b) | Rate disclosed is the 7-day yield at April 30, 2023. |

| AGM | Assured Guaranty Municipal Corp. |

| AGM-CR | Assured Guaranty Municipal Corp. Custodial Receipts |

| AMT | Alternative Minimum Tax |

| CAB | Capital Appreciation Bond |

| COP | Certificate of Participation |

| ETM | Escrowed to Maturity |

| FGIC | Financial Guaranty Insurance Co. |

| GO | General Obligation |

| MWC | Make Whole Callable |

| NATL-RE | National Reinsurance Corp. |

| OID | Original Issue Discount |

| Credit Quality: | % of Total Investments |

| Pre-refunded/Escrowed to Maturity | 8.57% |

| Aaa | 9.96 |

| Aa | 61.19 |

| A | 10.71 |

| Baa | 8.67 |

| Cash | 0.90 |

| Total | 100.00% |

| Pacific

Capital Tax-Free Securities Fund |

Pacific

Capital Tax-Free Short Intermediate Securities Fund | ||

| Assets | |||

| Investments, at value* | $238,671,739 | $43,951,268 | |

| Receivables: | |||

| Capital shares sold | 116,189 | 45,209 | |

| Interest | 2,639,290 | 585,840 | |

| Prepaid expenses and other assets | 513 | 36 | |

| Total Assets | 241,427,731 | 44,582,353 | |

| Liabilities | |||

| Payables: | |||

| Distributions to shareholders | 513,800 | 68,432 | |

| Audit fees | 33,249 | 33,212 | |

| Administration and accounting fees | 23,202 | 14,208 | |

| Shareholder reporting fees | 16,543 | 11,593 | |

| Capital shares redeemed | 12,835 | 355 | |

| Transfer agent fees | 7,931 | 7,659 | |

| Custodian fees | 6,523 | 1,736 | |

| Accrued expenses | 6,926 | 6,011 | |

| Total Liabilities | 621,009 | 143,206 | |

| Net Assets | $240,806,722 | $44,439,147 | |

| Net Assets Consisted of: | |||

| Capital stock, $0.01 par value | $ 248,794 | $ 45,214 | |

| Paid-in capital | 249,305,445 | 45,190,816 | |

| Total distributable loss | (8,747,517) | (796,883) | |

| Net Assets | $240,806,722 | $44,439,147 | |

| Class Y Shares: | |||

| Net assets | $240,806,722 | $44,439,147 | |

| Shares outstanding | 24,879,353 | 4,521,362 | |

| Net asset value, offering and redemption price per share | $ 9.68 | $ 9.83 | |

| * Investments, at cost | $245,028,206 | $44,494,699 |

| Pacific

Capital Tax-Free Securities Fund |

Pacific

Capital Tax-Free Short Intermediate Securities Fund | ||

| Investment income | |||

| Interest | $6,484,796 | $ 910,910 | |

| Dividends | 146,313 | 31,317 | |

| Total investment income | 6,631,109 | 942,227 | |

| Expenses | |||

| Advisory fees (Note 2) | 490,755 | 94,359 | |

| Administration and accounting fees (Note 2) | 74,943 | 45,380 | |

| Trustees’ and officers’ fees(Note 2) | 69,175 | 13,158 | |

| Legal fees | 57,000 | 15,343 | |

| Audit fees | 33,626 | 33,606 | |

| Shareholder reporting fees | 29,852 | 22,325 | |

| Custodian fees(Note 2) | 26,604 | 8,752 | |

| Transfer agent fees (Note 2) | 24,168 | 23,148 | |

| Registration and filing fees | 4,935 | 4,775 | |

| Other expenses | 20,436 | 10,330 | |

| Total expenses before waivers | 831,494 | 271,176 | |

| Less: waivers(Note 2) | (490,755) | (94,359) | |

| Net expenses after waivers | 340,739 | 176,817 | |

| Net investment income | 6,290,370 | 765,410 | |

| Net realized and unrealized gain/(loss) from investments: | |||

| Net realized loss from investments | (339,602) | (121,751) | |

| Net change in unrealized appreciation/(depreciation) on investments | (311,185) | 364,544 | |

| Net realized and unrealized gain/(loss) on investments | (650,787) | 242,793 | |

| Net increase in net assets resulting from operations | $5,639,583 | $1,008,203 |

| Pacific Capital Tax-Free Securities Fund | |||

| For

the Year Ended April 30, 2023 |

For

the Year Ended April 30, 2022 | ||

| Net increase/(decrease) in net assets from operations: | |||

| Net investment income | $ 6,290,370 | $ 6,273,377 | |

| Net realized losses from investments | (339,602) | (899,722) | |

| Net change in unrealized depreciation on investments | (311,185) | (23,896,219) | |

| Net increase/(decrease) in net assets resulting from operations | 5,639,583 | (18,522,564) | |

| Less dividends and distributions to shareholders from: | |||

| Total distributable earnings: | |||

| Class Y | (6,290,370) | (6,273,383) | |

| Net decrease in net assets from dividends and distributions to shareholders | (6,290,370) | (6,273,383) | |

| Increase/(decrease) in net assets derived from capital share transactions (Note 4) | (17,896,541) | 8,502,189 | |

| Total decrease in net assets | (18,547,328) | (16,293,758) | |

| Net assets | |||

| Beginning of year | 259,354,050 | 275,647,808 | |

| End of year | $240,806,722 | $259,354,050 | |

| Pacific

Capital Tax-Free Short Intermediate Securities Fund | |||

| For

the Year Ended April 30, 2023 |

For

the Year Ended April 30, 2022 | ||

| Net increase/(decrease) in net assets from operations: | |||

| Net investment income | $ 765,410 | $ 577,276 | |

| Net realized losses from investments | (121,751) | (48,853) | |

| Net change in unrealized appreciation/(depreciation) on investments | 364,544 | (2,223,998) | |

| Net increase/(decrease) in net assets resulting from operations | 1,008,203 | (1,695,575) | |

| Less dividends and distributions to shareholders from: | |||

| Total distributable earnings: | |||

| Class Y | (765,405) | (636,658) | |

| Net decrease in net assets from dividends and distributions to shareholders | (765,405) | (636,658) | |

| Decrease in net assets derived from capital share transactions (Note 4) | (3,132,412) | (362,334) | |

| Total decrease in net assets | (2,889,614) | (2,694,567) | |

| Net assets | |||

| Beginning of year | 47,328,761 | 50,023,328 | |

| End of year | $44,439,147 | $47,328,761 | |

| Class Y shares | |||||||||

| For

the Year Ended April 30, 2023 |

For

the Year Ended April 30, 2022 |

For

the Year Ended April 30, 2021 |

For

the Year Ended April 30, 2020 |

For

the Year Ended April 30, 2019 | |||||

| Per Share Operating Performance | |||||||||

| Net asset value, beginning of year | $ 9.69 | $ 10.61 | $ 10.30 | $ 10.24 | $ 9.97 | ||||

| Net investment income | 0.25 | 0.24 | 0.26 | 0.26 | 0.25 | ||||

| Net realized and unrealized gain/(loss) on investments | (0.01) | (0.92) | 0.31 | 0.06 | 0.27 | ||||

| Total from investment operations | 0.24 | (0.68) | 0.57 | 0.32 | 0.52 | ||||

| Dividends and distributions to shareholders from: | |||||||||

| Net investment income | (0.25) | (0.24) | (0.26) | (0.26) | (0.25) | ||||

| Net asset value, end of year | $ 9.68 | $ 9.69 | $ 10.61 | $ 10.30 | $ 10.24 | ||||

| Total investment return(1) | 2.49% | (6.56)% | 5.54% | 3.14% | 5.30% | ||||

| Ratios/Supplemental Data | |||||||||

| Net assets, end of year (in 000s) | $240,807 | $259,354 | $275,648 | $265,993 | $281,615 | ||||

| Ratio of expenses to average net assets | 0.14% | 0.12% | 0.11% | 0.09% | 0.11% | ||||

| Ratio of expenses to average net assets without waivers(2) | 0.34% | 0.32% | 0.31% | 0.29% | 0.31% | ||||

| Ratio of net investment income to average net assets | 2.54% | 2.27% | 2.43% | 2.51% | 2.50% | ||||

| Portfolio turnover rate | 9% | 14% | 9% | 10% | 11% | ||||

| (1) | Total investment return is calculated assuming a purchase of shares on the first day and a sale of shares on the last day of each period reported and includes reinvestment of dividends and distributions, if any. |

| (2) | During the period, certain fees were waived. If such fee waivers had not occurred, the ratios would have been as indicated (See Note 2). |

| Class Y shares | |||||||||

| For

the Year Ended April 30, 2023 |

For

the Year Ended April 30, 2022 |

For

the Year Ended April 30, 2021 |

For

the Year Ended April 30, 2020 |

For

the Year Ended April 30, 2019 | |||||

| Per Share Operating Performance | |||||||||

| Net asset value, beginning of year | $ 9.78 | $ 10.28 | $ 10.12 | $ 10.09 | $ 9.95 | ||||

| Net investment income | 0.16 | 0.12 | 0.15 | 0.17 | 0.16 | ||||

| Net realized and unrealized gain/(loss) on investments | 0.05 | (0.49) | 0.16 | 0.03 | 0.14 | ||||

| Total from investment operations | 0.21 | (0.37) | 0.31 | 0.20 | 0.30 | ||||

| Dividends and distributions to shareholders from: | |||||||||

| Net investment income | (0.16) | (0.12) | (0.15) | (0.17) | (0.16) | ||||

| Net realized capital gains | — | (0.01) | — | — | — | ||||

| Total dividends and distributions to shareholders | (0.16) | (0.13) | (0.15) | (0.17) | (0.16) | ||||

| Net asset value, end of year | $ 9.83 | $ 9.78 | $ 10.28 | $ 10.12 | $ 10.09 | ||||

| Total investment return(1) | 2.16% | (3.61)% | 3.04% | 1.98% | 3.01% | ||||

| Ratios/Supplemental Data | |||||||||

| Net assets, end of year (in 000s) | $44,439 | $47,329 | $50,023 | $53,599 | $53,479 | ||||

| Ratio of expenses to average net assets | 0.37% | 0.38% | 0.28% | 0.24% | 0.34% | ||||

| Ratio of expenses to average net assets without waivers(2) | 0.57% | 0.58% | 0.48% | 0.44% | 0.54% | ||||

| Ratio of net investment income to average net assets | 1.61% | 1.18% | 1.43% | 1.66% | 1.57% | ||||

| Portfolio turnover rate | 31% | 27% | 22% | 30% | 34% | ||||

| (1) | Total investment return is calculated assuming a purchase of shares on the first day and a sale of shares on the last day of each period reported and includes reinvestment of dividends and distributions, if any. |

| (2) | During the period, certain fees were waived. If such fee waivers had not occurred, the ratios would have been as indicated (See Note 2). |

| Funds | Total

Value at 04/30/23 |

Level

1 Quoted Price |

Level

2 Other Significant Observable Inputs |

Level

3 Significant Unobservable Inputs | ||||

| Pacific Capital Tax-Free Securities Fund | ||||||||

| Assets | ||||||||

| Municipal Bonds | $ 237,636,629 | $ — | $ 237,636,629 | $ — | ||||

| Registered Investment Company | 1,035,110 | 1,035,110 | — | — | ||||

| Total Assets | $ 238,671,739 | $ 1,035,110 | $ 237,636,629 | $ — | ||||

| Pacific Capital Tax-Free Short Intermediate Securities Fund | ||||||||

| Assets | ||||||||

| Municipal Bonds | $ 40,549,286 | $ — | $ 40,549,286 | $ — | ||||

| Municipal Commercial Paper | 2,996,434 | — | 2,996,434 | — | ||||

| Registered Investment Company | 405,548 | 405,548 | — | — | ||||

| Total Assets | $ 43,951,268 | $ 405,548 | $ 43,545,720 | $ — | ||||

| Maximum

Annual Advisory Fee |

Net

Annual Fees Paid After Contractual Waivers | ||

| Pacific Capital Tax-Free Securities Fund | 0.20% | 0.00% | |

| Pacific Capital Tax-Free Short Intermediate Securities Fund | 0.20% | 0.00% |

| Purchases | Sales | ||

| Pacific Capital Tax-Free Securities Fund | $22,619,068 | $35,076,649 | |

| Pacific Capital Tax-Free Short Intermediate Securities Fund | 13,367,845 | 18,835,389 |

| For

the Year Ended April 30, 2023 |

For

the Year Ended April 30, 2022 | ||||||

| Shares | Amount | Shares | Amount | ||||

| Pacific Capital Tax-Free Securities Fund: | |||||||

| Class Y | |||||||

| Sales | 2,316,387 | $ 22,357,524 | 3,941,358 | $ 41,130,908 | |||

| Reinvestments | 3,654 | 35,117 | 3,401 | 35,378 | |||

| Redemptions | (4,195,090) | (40,289,182) | (3,169,894) | (32,664,097) | |||

| Net increase/(decrease) | (1,875,049) | $(17,896,541) | 774,865 | $ 8,502,189 | |||

| For

the Year Ended April 30, 2023 |

For

the Year Ended April 30, 2022 | ||||||

| Shares | Amount | Shares | Amount | ||||

| Pacific Capital Tax-Free Short Intermediate Securities Fund: | |||||||

| Class Y | |||||||

| Sales | 522,746 | $ 5,126,766 | 562,263 | $ 5,638,001 | |||

| Reinvestments | 502 | 4,919 | 391 | 3,961 | |||

| Redemptions | (840,637) | (8,264,097) | (591,817) | (6,004,296) | |||

| Net decrease | (317,389) | $ (3,132,412) | (29,163) | $ (362,334) | |||

| Ordinary

Income Distributions |

Total

Taxable Distributions |

Tax

Exempt Distributions |

Total

Distributions Paid* | ||||

| Pacific Capital Tax-Free Securities Fund | $145,429 | $145,429 | $6,141,549 | $6,286,978 | |||

| Pacific Capital Tax-Free Short Intermediate Securities Fund | 31,879 | 31,879 | 703,940 | 735,819 |

| * | Distributions will not tie to Statements of Changes in Net Assets because distributions are recognized when actually paid for tax purposes. |

| Ordinary

Income Distributions |

Long-Term

Capital Gain Distributions |

Total

Taxable Distributions |

Tax

Exempt Distributions |

Total

Distributions Paid* | |||||

| Pacific Capital Tax-Free Securities Fund | $331,448 | $ — | $331,448 | $5,953,539 | $6,284,987 | ||||

| Pacific Capital Tax-Free Short Intermediate Securities Fund | 32,313 | 2,063 | 34,376 | 613,565 | 647,941 |

| * | Distributions will not tie to Statements of Changes in Net Assets because distributions are recognized when actually paid for tax purposes. |

| Capital

Loss Carryforward |

Undistributed

Tax Exempt Income |

Distributions

Payable |

Unrealized

Appreciation/ (Depreciation) | ||||

| Pacific Capital Tax-Free Securities Fund | $(2,391,044) | $513,794 | $(513,800) | $(6,356,467) | |||

| Pacific Capital Tax-Free Short Intermediate Securities Fund | (214,611) | 29,591 | (68,432) | (543,431) |

| Federal

Tax Cost |

Unrealized

Appreciation |

Unrealized

(Depreciation) |

Net

Unrealized (Depreciation) | |||||

| Pacific Capital Tax-Free Securities Fund | $245,028,206 | $1,820,479 | $(8,176,946) | $(6,356,467) | ||||

| Pacific Capital Tax-Free Short Intermediate Securities Fund | 44,494,699 | 207,056 | (750,487) | (543,431) |

| Capital Loss Carryforward | |||

| Short-Term | Long-Term | ||

| Pacific Capital Tax-Free Securities Fund | $2,081,545 | $309,499 | |

| Pacific Capital Tax-Free Short Intermediate Securities Fund | 80,910 | 133,701 | |

| Ordinary

Income Distributions |

Total

Taxable Distributions |

Tax

Exempt Distributions |

Total

Distributions Paid* | ||||

| Pacific Capital Tax-Free Securities Fund | $145,429 | $145,429 | $6,141,549 | $6,286,978 | |||

| Pacific Capital Tax-Free Short Intermediate Securities Fund | 31,879 | 31,879 | 703,940 | 735,819 |

| * | Distributions will not tie to Statements of Changes in Net Assets because distributions are recognized when actually paid for tax purposes. |

| Name

and Date of Birth |

Position(s)

Held with Trust |

Term

of Office and Length of Time Served |

Principal

Occupation(s) During Past Five Years |

Number

of Funds in Trust Complex Overseen by Trustee |

Other

Directorships Held by Trustee |

| INDEPENDENT TRUSTEES | |||||

| ROBERT

J. CHRISTIAN Date of Birth: 2/49 |

Trustee | Shall

serve until death, resignation or removal. Trustee since 2007. Chairman from 2007 until September 30, 2019. |

Retired

since February 2006; Executive Vice President of Wilmington Trust Company from February 1996 to February 2006; President of Rodney Square Management Corporation (“RSMC”) (investment advisory firm) from 1996 to 2005; Vice President of RSMC from 2005 to 2006. |

36 | Optimum

Fund Trust (registered investment company with 6 portfolios); Third Avenue Trust (registered investment company with 4 portfolios); Third Avenue Variable Series Trust (registered investment company with 1 portfolio). |

| IQBAL

MANSUR Date of Birth: 6/55 |

Trustee | Shall

serve until death, resignation or removal. Trustee since 2007. |

Retired

since September 2020; Professor of Finance, Widener University from 1998 to August 2020; Member of the Investment Committee of ChristianaCare Health System from January 2022 to present. |

36 | Third

Avenue Trust (registered investment company with 4 portfolios); Third Avenue Variable Series Trust (registered investment company with 1 portfolio). |

| Name

and Date of Birth |

Position(s)

Held with Trust |

Term

of Office and Length of Time Served |

Principal

Occupation(s) During Past Five Years |

Number

of Funds in Trust Complex Overseen by Trustee |

Other

Directorships Held by Trustee |

| NICHOLAS

M. MARSINI, JR. Date of Birth: 8/55 |

Trustee

and Chairman of the Board |

Shall

serve until death, resignation or removal. Trustee since 2016. Chairman since October 1, 2019. |

Retired

since March 2016. President of PNC Bank Delaware from June 2011 to March 2016; Executive Vice President of Finance of BNY Mellon from July 2010 to January 2011; Executive Vice President and Chief Financial Officer of PNC Global Investment Servicing from September 1997 to July 2010. |

36 | Brinker

Capital Destinations Trust (registered investment company with 10 portfolios); Third Avenue Trust (registered investment company with 4 portfolios); Third Avenue Variable Series Trust (registered investment company with 1 portfolio). |

| NANCY

B. WOLCOTT Date of Birth: 11/54 |

Trustee | Shall

serve until death, resignation or removal. Trustee since 2011. |

Retired since May 2014; EVP, Head of GFI Client Service Delivery, BNY Mellon from January 2012 to May 2014; EVP, Head of US Funds Services, BNY Mellon from July 2010 to January 2012; President of PNC Global Investment Servicing from 2008 to July 2010; Chief Operating Officer of PNC Global Investment Servicing from 2007 to 2008; Executive Vice President of PFPC Worldwide Inc. from 2006 to 2007. | 36 | Lincoln

Variable Trust Products Trust (registered investment company with 97 portfolios); Third Avenue Trust (registered investment company with 4 portfolios); Third Avenue Variable Series Trust (registered investment company with 1 portfolio). |

| Name

and Date of Birth |

Position(s)

Held with Trust |

Term

of Office and Length of Time Served |

Principal

Occupation(s) During Past Five Years |

Number

of Funds in Trust Complex Overseen by Trustee |

Other

Directorships Held by Trustee |

| STEPHEN

M. WYNNE Date of Birth: 1/55 |

Trustee | Shall

serve until death, resignation or removal. Trustee since 2009. |

Retired

since December 2010; Chief Executive Officer of US Funds Services, BNY Mellon Asset Servicing from July 2010 to December 2010; Chief Executive Officer of PNC Global Investment Servicing from March 2008 to July 2010; President, PNC Global Investment Servicing from 2003 to 2008. |

36 | Copeland

Trust (registered investment company with 3 portfolios); Third Avenue Trust (registered investment company with 4 portfolios); Third Avenue Variable Series Trust (registered investment company with 1 portfolio). |

| Name

and Date of Birth |

Position(s)

Held with Trust |

Term

of Office and Length of Time Served |

Principal

Occupation(s) During Past Five Years |

| EXECUTIVE OFFICERS | |||

| JOEL

L. WEISS Date of Birth: 1/63 |

President

and Chief Executive Officer |

Shall

serve until death, resignation or removal. Officer since 2007. |

President of JW Fund Management LLC since June 2016; Vice President and Managing Director of BNY Mellon Investment Servicing (US) Inc. and predecessor firms from 1993 to June 2016. |

| CHRISTINE

S. CATANZARO Date of Birth: 8/84 |

Treasurer and Chief Financial Officer | Shall

serve until death, resignation or removal. Officer since 2022. |

Financial Reporting Consultant from October 2020 to September 2022; Senior Manager, Ernst & Young LLP from March 2013 to October 2020. |

| T.

RICHARD KEYES Date of Birth: 1/57 |

Vice

President |

Shall

serve until death, resignation or removal. Officer since 2016. |

President of TRK Fund Consulting LLC since July 2016; Head of Tax — U.S. Fund Services of BNY Mellon Investment Servicing (US) Inc. and predecessor firms from February 2006 to July 2016. |

| GABRIELLA

MERCINCAVAGE Date of Birth: 6/68 |

Assistant Treasurer | Shall

serve until death, resignation or removal. Officer since 2019. |

Fund

Administration Consultant since January 2019; Fund Accounting and Tax Compliance Accountant to financial services companies from November 2003 to July 2018. |

| VINCENZO

A. SCARDUZIO Date of Birth: 4/72 |

Secretary | Shall

serve until death, resignation or removal. Officer since 2012. |

Director and Vice President Regulatory Administration of The Bank of New York Mellon and predecessor firms since 2001. |

| JOHN

CANNING Date of Birth: 11/70 |

Chief

Compliance Officer and Anti-Money Laundering Officer |

Shall

serve until death, resignation or removal. Officer since 2022. |

Director of Chenery Compliance Group, LLC from March 2021 to present; Senior Consultant of Foreside Financial Group from August 2020 to March 2021; Chief Compliance Officer & Chief Operating Officer of Schneider Capital Management LP from May 2019 to July 2020; Chief Operating Officer and Chief Compliance Officer of Context Capital Partners, LP from March 2016 to March 2018 and February 2019, respectively. |

111 South King Street, 4th Floor,

Honolulu, HI 96813

301 Bellevue Parkway

Wilmington, DE 19809

500 Ross Street, 154-0520

Pittsburgh, PA 15262

Three Canal Plaza, Suite 100

Portland, ME 04101

240 Greenwich Street

New York, NY 10286

2001 Market Street

3000 Two Logan Square

18th and Arch Streets

| Polen Growth Fund |

| Polen Global Growth Fund |

| Polen International Growth Fund |

| Polen U.S. Small Company Growth Fund |

| Polen International Small Company Growth Fund |

| Polen

Emerging Markets Growth Fund (formerly, Polen Global Emerging Markets Growth Fund) |

| Polen U.S. SMID Company Growth Fund |

| Polen Global SMID Company Growth Fund |

| Polen Emerging Markets ex China Growth Fund |

| Polen Bank Loan Fund |

| Polen Upper Tier High Yield Fund |

| Institutional Class |

| Investor Class |

| Class Y |

| 1 | In March 2023, three small- to mid-size U.S. banks failed, triggering a sharp decline in global bank stock prices and a contagion effect around the worldwide. |

| The

Large Company Growth Team Polen Growth Fund: |

The

Small Company Growth Team Polen U.S. Small Company Growth Fund & Polen U.S. SMID Company Growth Fund: | ||

|

|

|

|

| Dan Davidowitz | Brandon Ladoff | Rayna Lesser Hannaway | Whitney Young Crawford |

| Polen Global Growth Fund: | Polen

International Small Company Growth Fund & Polen Global SMID Company Growth Fund: | ||

|

|

|

|

| Damon Ficklin | Jeff Mueller | Rob Forker | |

| Polen International Growth Fund: | |||

|

|

||

| Todd Morris | Daniel Fields | ||

| The

Emerging Markets Growth Team Polen Emerging Markets Growth Fund (formerly, Polen Global Emerging Markets Growth Fund) & Polen Emerging Markets ex China Growth Fund: |

|||

|

|

|

|

| Damian Bird | Dafydd Lewis | Rishikesh Patel | |

| High

Yield Team: Polen Bank Loan Fund |

Polen Upper Tier High Yield Fund | ||

|

|

|

|

| John Sherman | Ben Santonelli | Dave Breazzano | Roman Rjanikov |

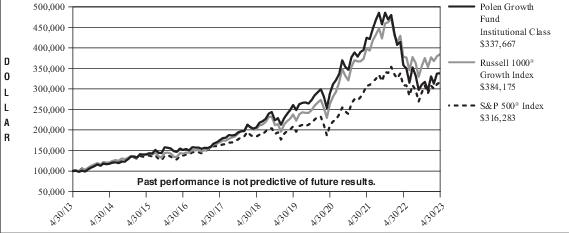

| Average Annual Total Returns for the Years Ended April 30, 2023 | |||||||

| 1 Year | 3 Years | 5 Years | 10 Years | ||||

| Institutional Class | -5.67% | 5.33% | 10.36% | 12.94% | |||

| S&P 500® Index | 2.64% | 14.50% | 11.42% | 12.18% | |||

| Russell 1000® Growth Index | 2.33% | 13.61% | 13.79% | 14.45% | |||

| Average Annual Total Returns for the Years Ended April 30, 2023 | |||||||

| 1 Year | 3 Years | 5 Years | 10 Years | ||||

| Investor Class | -5.92% | 5.06% | 10.08% | 12.65% | |||

| S&P 500® Index | 2.64% | 14.50% | 11.42% | 12.18% | |||

| Russell 1000® Growth Index | 2.33% | 13.61% | 13.79% | 14.45% | |||

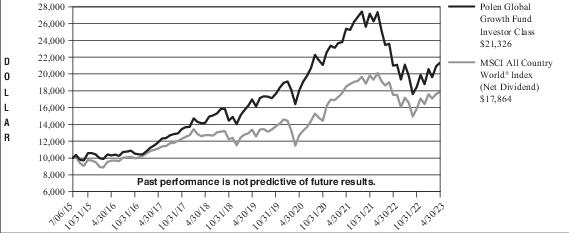

| Average Annual Total Returns for the Periods Ended April 30, 2023 | |||||||

| 1 Year | 3 Years | 5 Years | Since

Inception* | ||||

| Institutional Class | 1.80% | 6.01% | 8.76% | 10.20% | |||

| MSCI

All Country World® Index (“ACWI”) (Net Dividend) |

2.06% | 12.04% | 7.03% | 7.47% ** | |||

| * | The Polen Global Growth Fund (the “Fund” ) Institutional Class commenced operations on December 30, 2014. |

| ** | Benchmark performance is from the commencement date of the Fund Class only and is not the commencement date of the benchmark itself. |

| Average Annual Total Returns for the Periods Ended April 30, 2023 | |||||||

| 1 Year | 3 Years | 5 Years | Since

Inception* | ||||

| Investor Class | 1.59% | 5.76% | 8.51% | 10.17% | |||

| MSCI

All Country World® Index (“ACWI”) (Net Dividend) |

2.06% | 12.04% | 7.03% | 7.78% ** | |||

| * | The Polen Global Growth Fund (the “Fund”) Investor Class commenced operations on July 6, 2015. |

| ** | Benchmark performance is from the commencement date of the Fund Class only and is not the commencement date of the benchmark itself. |

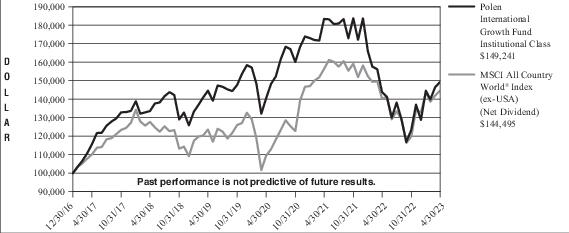

| Average Annual Total Returns for the Periods Ended April 30, 2023 | |||||||

| 1 Year | 3 Years | 5 Years | Since

Inception* | ||||

| Institutional Class | 3.78% | 2.06% | 2.24% | 6.53% | |||

| MSCI

All Country World® Index (“ACWI”) (ex-USA) (Net Dividend) |

3.05% | 9.74% | 2.50% | 5.98% ** | |||

| * | The Polen International Growth Fund (the "Fund") Institutional Class commenced operations on December 30, 2016. |

| ** | Benchmark performance is from the commencement date of the Fund Class only and is not the commencement date of the benchmark itself. |

| Average Annual Total Returns for the Periods Ended April 30, 2023 | |||||||

| 1 Year | 3 Years | 5 Years | Since

Inception* | ||||

| Investor Class | 3.55% | 1.80% | 1.99% | 4.98% | |||

| MSCI

All Country World® Index (“ACWI”) (ex-USA) (Net Dividend) |

3.05% | 9.74% | 2.50% | 5.17% ** | |||

| * | The Polen International Growth Fund (the “Fund”) Investor Class commenced operations on March 15, 2017. |

| ** | Benchmark performance is from the commencement date of the Fund Class only and is not the commencement date of the benchmark itself. |

| Average Annual Total Returns for the Periods Ended April 30, 2023 | |||||||

| 1 Year | 3 Years | 5 Years | Since

Inception* | ||||

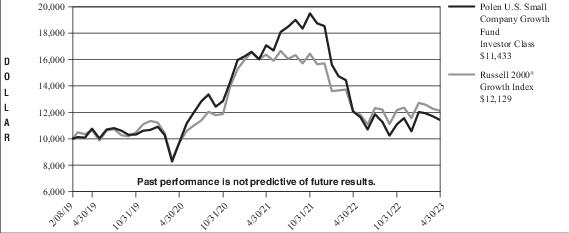

| Institutional Class | -5.04% | 5.91% | 5.52% | 5.41% | |||

| Russell 2000® Growth Index | 0.69% | 7.79% | 3.97% | 4.77% ** | |||

| * | The Polen U.S. Small Company Growth Fund (the “Fund”) Institutional Class commenced operations on November 1, 2017. |

| ** | Benchmark performance is from the commencement date of the Fund Class only and is not the commencement date of the benchmark itself. |

| Average Annual Total Returns for the Periods Ended April 30, 2023 | |||||

| 1 Year | 3 Years | Since

Inception* | |||

| Investor Class | -5.31% | 5.63% | 3.22% | ||

| Russell 2000® Growth Index | 0.69% | 7.79% | 4.87% ** | ||

| * | The Polen U.S. Small Company Growth Fund (the "Fund") Investor Class commenced operations on February 8, 2019. |

| ** | Benchmark performance is from the commencement date of the Fund Class only and is not the commencement date of the benchmark itself. |

| Average Annual Total Returns for the Periods Ended April 30, 2023 | |||

| 1 Year | Since

Inception* | ||

| Class Y | -4.96% | -17.55% | |

| Russell 2000® Growth Index | 0.69% | -13.36% ** | |

| * | The Polen U.S. Small Company Growth Fund (the “Fund”) Class Y commenced operations on June 1, 2021. |

| ** | Benchmark performance is from the commencement date of the Fund Class only and is not the commencement date of the benchmark itself. |

| Average Annual Total Returns for the Periods Ended April 30, 2023 | |||||

| 1 Year | 3 Years | Since

Inception* | |||

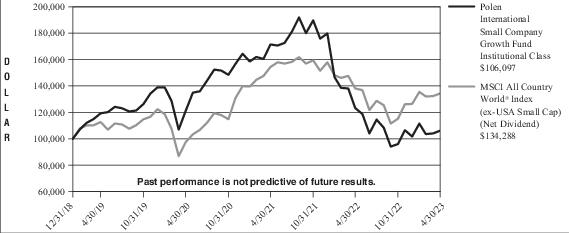

| Institutional Class | -13.94% | -4.30% | 1.38% | ||

| MSCI All Country World® Index (“ACWI”) (ex-USA Small Cap) (Net Dividend) | -2.78% | 11.27% | 5.75% ** | ||

| * | The Polen International Small Company Growth Fund (the “Fund” ) Institutional Class commenced operations on December 31, 2018. |

| ** | Benchmark performance is from the commencement date of the Fund Class only and is not the commencement date of the benchmark itself. |

| Average Annual Total Returns for the Periods Ended April 30, 2023 | |||||

| 1 Year | 3 Years | Since

Inception* | |||

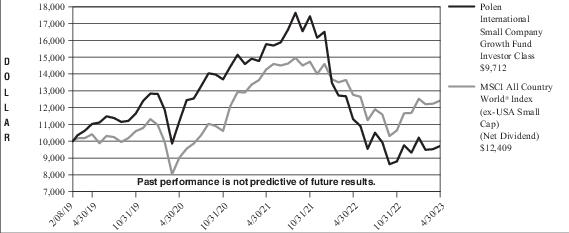

| Investor Class | -14.14% | -4.53% | -0.69% | ||

| MSCI All Country World® Index (“ACWI”) (ex-USA Small Cap) (Net Dividend) | -2.78% | 11.27% | 7.11% ** | ||

| * | The Polen International Small Company Growth Fund (the “Fund”) Investor Class commenced operations on February 8, 2019. |

| ** | Benchmark performance is from the commencement date of the Fund Class only and is not the commencement date of the benchmark itself. |

| Average Annual Total Returns for the Periods Ended April 30, 2023 | |||

| 1 Year | Since

Inception* | ||

| Institutional Class | 2.57% | -9.02% | |

| MSCI Emerging Markets Index (Net Dividend) | -6.15% | -2.85% ** | |

| * | The Polen Emerging Markets Growth Fund (the “Fund” ) Institutional Class commenced operations on October 16, 2020. |

| ** | Benchmark performance is from the commencement date of the Fund Class only and is not the commencement date of the benchmark itself. |

| Average Annual Total Returns for the Periods Ended April 30, 2023 | |||

| 1 Year | Since

Inception* | ||

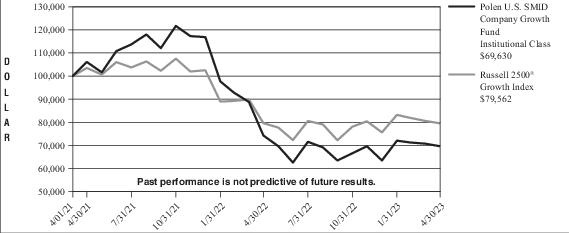

| Institutional Class | -6.25% | -15.96% | |

| Russell 2500® Growth Index | -0.09% | -10.44% ** | |

| * | The Polen U.S. SMID Company Growth Fund (the "Fund") Institutional Class commenced operations on April 1, 2021. |

| ** | Benchmark performance is from the commencement date of the Fund Class only and is not the commencement date of the benchmark itself. |

| Average Annual Total Returns for the Periods Ended April 30, 2023 | |||

| 1 Year | Since

Inception* | ||

| Institutional Class | -5.74% | -28.44% | |

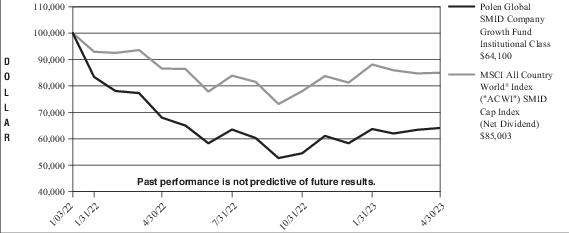

| MSCI All Country World® Index (“ACWI”) SMID Cap Index (Net Dividend) | -1.84% | -11.61% ** | |

| * | The Polen Global SMID Company Growth Fund (the "Fund") Institutional Class commenced operations on January 3, 2022. |

| ** | Benchmark performance is from the commencement date of the Fund Class only and is not the commencement date of the benchmark itself. |

| Total Returns for the Period Ended April 30, 2023 | |

| Since

Inception† | |

| Institutional Class | 3.50% * |

| MSCI Emerging Markets ex China Index (Net Dividend) | 2.29% ** |

| † | Not Annualized. |

| * | The Polen Emerging Markets ex China Growth Fund (the "Fund") Institutional Class commenced operations on March 1, 2023. |

| ** | Benchmark performance is from the commencement date of the Fund Class only and is not the commencement date of the benchmark itself. |

| Total Returns for the Period Ended April 30, 2023 | |

| Since

Inception†* | |

| Institutional Class | 7.12% |

| Morningstar LSTA US Leveraged Loan Index | 8.40% ** |

| † | Not Annualized. |

| * | The Polen Bank Loan Fund (the "Fund") Institutional Class commenced operations on June 30, 2022. |

| ** | Benchmark performance is from inception date of the Fund Class only and is not the inception date of the benchmark itself. |

| Total Returns for the Period Ended April 30, 2023 | |

| Since

Inception†* | |

| Institutional Class | 7.22% |

| ICE BofA BB/B U.S. Non-Financial High Yield Constrained Index | 8.14% ** |

| † | Not Annualized. |

| * | The Polen Upper Tier High Yield Fund (the "Fund") Institutional Class commenced operations on June 30, 2022. |

| ** | Benchmark performance is from the commencement date of the Fund Class only and is not the commencement date of the benchmark itself. |

| Beginning

Account Value November 1, 2022 |

Ending

Account Value April 30, 2023 |

Annualized

Expense Ratio |

Expenses

Paid During Period | ||||

| Polen Growth Fund | |||||||

| Institutional Class1 | |||||||

| Actual | $1,000.00 | $1,088.00 | 0.96% | $4.97 | |||

| Hypothetical (5% return before expenses) | 1,000.00 | 1,020.03 | 0.96% | 4.81 | |||

| Investor Class1 | |||||||

| Actual | $1,000.00 | $1,086.50 | 1.21% | $6.26 | |||

| Hypothetical (5% return before expenses) | 1,000.00 | 1,018.79 | 1.21% | 6.06 | |||

| Polen Global Growth Fund | |||||||

| Institutional Class2 | |||||||

| Actual | $1,000.00 | $1,156.80 | 0.99% | $5.29 | |||

| Hypothetical (5% return before expenses) | 1,000.00 | 1,019.89 | 0.99% | 4.96 | |||

| Investor Class2 | |||||||

| Actual | $1,000.00 | $1,155.40 | 1.24% | $6.63 | |||

| Hypothetical (5% return before expenses) | 1,000.00 | 1,018.65 | 1.24% | 6.21 | |||

| Beginning

Account Value November 1, 2022 |

Ending

Account Value April 30, 2023 |

Annualized

Expense Ratio |

Expenses

Paid During Period | ||||

| Polen International Growth Fund | |||||||

| Institutional Class3 | |||||||

| Actual | $1,000.00 | $1,210.00 | 1.05% | $5.75 | |||

| Hypothetical (5% return before expenses) | 1,000.00 | 1,019.59 | 1.05% | 5.26 | |||

| Investor Class3 | |||||||

| Actual | $1,000.00 | $1,208.60 | 1.30% | $7.12 | |||

| Hypothetical (5% return before expenses) | 1,000.00 | 1,018.35 | 1.30% | 6.51 | |||

| Polen U.S. Small Company Growth Fund | |||||||

| Institutional Class4 | |||||||

| Actual | $1,000.00 | $1,031.40 | 1.10% | $5.54 | |||

| Hypothetical (5% return before expenses) | 1,000.00 | 1,019.34 | 1.10% | 5.51 | |||

| Investor Class4 | |||||||

| Actual | $1,000.00 | $1,030.10 | 1.35% | $6.80 | |||

| Hypothetical (5% return before expenses) | 1,000.00 | 1,018.10 | 1.35% | 6.76 | |||

| Class Y4 | |||||||

| Actual | $1,000.00 | $1,032.20 | 1.00% | $5.04 | |||

| Hypothetical (5% return before expenses) | 1,000.00 | 1,019.84 | 1.00% | 5.01 | |||

| Polen International Small Company Growth Fund | |||||||

| Institutional Class5 | |||||||

| Actual | $1,000.00 | $1,104.90 | 1.25% | $6.52 | |||

| Hypothetical (5% return before expenses) | 1,000.00 | 1,018.60 | 1.25% | 6.26 | |||

| Investor Class5 | |||||||

| Actual | $1,000.00 | $1,103.70 | 1.50% | $7.82 | |||

| Hypothetical (5% return before expenses) | 1,000.00 | 1,017.36 | 1.50% | 7.50 | |||

| Polen Emerging Markets Growth Fund | |||||||

| Institutional Class6 | |||||||

| Actual | $1,000.00 | $1,281.30 | 1.25% | $7.07 | |||

| Hypothetical (5% return before expenses) | 1,000.00 | 1,018.60 | 1.25% | 6.26 | |||

| Polen U.S. SMID Company Growth Fund | |||||||

| Institutional Class7 | |||||||

| Actual | $1,000.00 | $1,045.50 | 1.05% | $5.33 | |||

| Hypothetical (5% return before expenses) | 1,000.00 | 1,019.59 | 1.05% | 5.26 | |||

| Polen Global SMID Company Growth Fund | |||||||

| Institutional Class8 | |||||||

| Actual | $1,000.00 | $1,176.20 | 1.25% | $6.74 | |||

| Hypothetical (5% return before expenses) | 1,000.00 | 1,018.60 | 1.25% | 6.26 | |||

| Polen Emerging Markets ex China Growth Fund | |||||||

| Institutional Class9 | |||||||

| Actual | $1,000.00 | $1,035.00 | 1.25% | $2.13 | |||

| Hypothetical (5% return before expenses) | 1,000.00 | 1,018.60 | 1.25% | 6.26 | |||

| Beginning

Account Value November 1, 2022 |

Ending

Account Value April 30, 2023 |

Annualized

Expense Ratio |

Expenses

Paid During Period | ||||

| Polen Bank Loan Fund | |||||||

| Institutional Class10 | |||||||

| Actual | $1,000.00 | $1,069.30 | 0.75% | $3.85 | |||

| Hypothetical (5% return before expenses) | 1,000.00 | 1,021.08 | 0.75% | 3.76 | |||

| Polen Upper Tier High Yield Fund | |||||||

| Institutional Class11 | |||||||

| Actual | $1,000.00 | $1,051.60 | 0.65% | $3.31 | |||

| Hypothetical (5% return before expenses) | 1,000.00 | 1,021.57 | 0.65% | 3.26 | |||

| 1 | Expenses are equal to an annualized expense ratio for the six-month period ended April 30, 2023 of 0.96% for Institutional Class and 1.21% for Investor Class, multiplied by the average account value over the period, multiplied by the number of days in the most recent period (181), then divided by 365 to reflect the period. The Fund’s ending account values on the first line of each table are based on the actual six-month total returns for the Fund of 8.80% and 8.65% for Institutional Class and Investor Class, respectively. |

| 2 | Expenses are equal to an annualized expense ratio for the six-month period ended April 30, 2023 of 0.99% for Institutional Class and 1.24% for Investor Class, multiplied by the average account value over the period, multiplied by the number of days in the most recent period (181), then divided by 365 to reflect the period. The Fund’s ending account values on the first line of each table are based on the actual six-month total returns for the Fund of 15.68% and 15.54% for Institutional Class and Investor Class, respectively. |

| 3 | Expenses are equal to an annualized expense ratio for the six-month period ended April 30, 2023 of 1.05% for Institutional Class and 1.30% for Investor Class, multiplied by the average account value over the period, multiplied by the number of days in the most recent period (181), then divided by 365 to reflect the period. The Fund’s ending account values on the first line of each table are based on the actual six-month total returns for the Fund of 21.00% and 20.86% for Institutional Class and Investor Class, respectively. |

| 4 | Expenses are equal to an annualized expense ratio for the six-month period ended April 30, 2023 of 1.10% for Institutional Class, 1.35% for Investor Class and 1.00% for Class Y, multiplied by the average account value over the period, multiplied by the number of days in the most recent period (181), then divided by 365 to reflect the period. The Fund’s ending account values on the first line of each table are based on the actual six-month total returns for the Fund of 3.14%, 3.01% and3.22% for Institutional Class, Investor Class and Class Y, respectively. |

| 5 | Expenses are equal to an annualized expense ratio for the six-month period ended April 30, 2023 of 1.25% for Institutional Class and 1.50% for the Investor Class, multiplied by the average account value over the period, multiplied by the number of days in the most recent period (181), then divided by 365 to reflect the period. The Fund’s ending account values on the first line of each table are based on the actual six-month total returns for the Fund of 10.49% and10.37% for Institutional Class and Investor Class, respectively. |

| 6 | Expenses are equal to an annualized expense ratio for the six-month period ended April 30, 2023 of 1.25% for Institutional Class, multiplied by the average account value over the period, multiplied by the number of days in the most recent period (181), then divided by 365 to reflect the period. The Institutional Class ending account values on the first line of the table is based on the actual six-month total return for the Fund of 28.13%. |

| 7 | Expenses are equal to an annualized expense ratio for the six-month period ended April 30, 2023 of 1.05% for Institutional Class, multiplied by the average account value over the period, multiplied by the number of days in the most recent period (181), then divided by 365 to reflect the period. The Institutional Class ending account values on the first line of the table is based on the actual six-month total return for the Fund of 4.55%. |

| 8 | Expenses are equal to an annualized expense ratio for the six-month period ended April 30, 2023 of 1.25% for Institutional Class, multiplied by the average account value over the period, multiplied by the number of days in the most recent period (181), then divided by 365 to reflect the period. The Institutional Class ending account values on the first line of the table is based on the actual six-month total return for the Fund of 17.62%. |

| 9 | Expenses are equal to an annualized expense ratio for the period beginning March 1, 2023, commencement of operations, to April 30, 2023 of 1.25% for Institutional Class, multiplied by the average account value over the period, multiplied by the number of days in the most recent period (61), then divided by 365 to reflect the period. The Institutional Class ending account values on the first line of the table is based on the actual total return for the Fund of 3.50%. For comparative purposes, the Hypothetical expenses are as if the Institutional Class had been in existence from May 1, 2022, and are equal to the Institutional Class annualized expense ratio, multiplied by the average account value over the period, multiplied by the number of days in the most recent six-month period (181), then divided by 365 to reflect the period. |

| 10 | Expenses are equal to an annualized expense ratio for the six-month period ended April 30, 2023 of 0.75% for Institutional Class, multiplied by the average account value over the period, multiplied by the number of days in the most recent period (181), then divided by 365 to reflect the period. The Institutional Class ending account values on the first line of the table is based on the actual six-month total return for the Fund of 6.93%. |

| 11 | Expenses are equal to an annualized expense ratio for the six-month period ended April 30, 2023 of 0.65% for Institutional Class, multiplied by the average account value over the period, multiplied by the number of days in the most recent period (181), then divided by 365 to reflect the period. The Institutional Class ending account values on the first line of the table is based on the actual six-month total return for the Fund of 5.16%. |

| %

of Net Assets |

Value | ||

| COMMON STOCKS: | |||

| Software Application | 16.7% | $1,172,080,569 | |

| Internet Retail | 14.2 | 1,000,795,791 | |

| Credit Services | 12.4 | 875,314,930 | |

| Software Infrastructure | 11.9 | 838,922,782 | |

| Entertainment | 6.6 | 460,799,374 | |

| Internet Content & Information | 6.5 | 456,061,157 | |

| Diagnostics & Research | 6.3 | 440,052,457 | |

| Information Technology Services | 6.2 | 439,306,374 | |

| Medical Devices | 5.3 | 374,298,067 | |

| Travel Services | 4.0 | 281,749,732 | |

| Healthcare Plans | 3.7 | 262,086,642 | |