Exhibit 99.1

Investor Presentation June 15, 2022 Peter A. Gray, Senior Executive Vice President & Chief Operating Officer Allan Muto, Executive Vice President & Chief Financial Officer

Forward Looking Statements and Safe Harbor Certain statements contained herein are “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Such forward-looking statements may be identified by reference to a future period or periods, or by the use of forward-looking terminology, such as “may,” “will,” “believe,” “expect,” “estimate,” “anticipate,” “continue,” or similar terms or variations on those terms, or the negative of those terms. Forward-looking statements are subject to numerous risks and uncertainties, including, but not limited to, those related to the economic environment, particularly in the market areas in which the Company operates, competitive products and pricing, fiscal and monetary policies of the U.S. Government, changes in government regulations affecting financial institutions, including compliance costs and capital requirements, changes in prevailing interest rates, acquisitions and the integration of acquired businesses, credit risk management, asset-liability management, the financial and securities markets and the availability of and costs associated with sources of liquidity, and the Risk Factors disclosed in our annual and quarterly reports. In addition, the COVID-19 pandemic continues to have an adverse impact on the Company, its customers, and the communities it serves. The adverse effect of the COVID-19 pandemic on the Company, its customers, and the communities where it operates will continue to adversely affect the Company’s business, results of operations, and financial condition for an indefinite period of time. The Company wishes to caution readers not to place undue reliance on any such forward-looking statements, which speak only as of the date made. The Company wishes to advise readers that the factors listed above could affect the Company’s financial performance and could cause the Company’s actual results for future periods to differ materially from any opinions or statements expressed with respect to future periods in any current statements. The Company does not undertake and specifically declines any obligation to publicly release the result of any revisions that may be made to any forward-looking statements to reflect events or circumstances after the date of such statements or to reflect the occurrence of anticipated or unanticipated events.

At-A-Glance ESSA Key Numbers* Assets. $ 1.87 billion Net Loans $ 1.34 billion Deposits. $1.62 billion Employees. 243 ATMs. 20 Branches. 21 * At March 31, 2022 Capital Strength ESSA has a strong common equity tier 1 capital ratio, a key measure of a bank’s strength and capital adequacy. ESSA capital ratios exceed regulatory minimums for well-capitalized. Common equity tier 1 13.27% 6.5% Total capital ratio 14. 52% 10.0% * Not Federally Insured | No Financial Institution Guarantee | May Lose Value Investment advisory products and services are made available through Ameriprise Financial Services, LLC., a registered investment adviser. Ameriprise Financial Services, LLC. Member FINRA and SIPC. At-A-Glance ESSA Bancorp, Inc. is the Pennsylvania-chartered holding company for ESSA Bank & Trust. The Bank operates 21 community offices throughout the Greater Pocono, Lehigh Valley, Scranton/Wilkes-Barre and suburban Philadelphia markets, in Pennsylvania. The Bank provides banking, insurance, investments and wealth management services to individuals and businesses in Eastern Pennsylvania. At March 31, 2022, ESSA Bancorp had consolidated assets of $1.87 billion, net loans of $1.34 billion, consolidated deposits of $1.62 billion and consolidated stockholders’ equity of $212.7 million. Our corporate headquarters are located at 200 Palmer Street, Stroudsburg, PA 18360. Key Consumer Banking Key Commercial Banking Products and Services Products and Services Checking Savings Money Market Accounts Commercial Real Estate Banking Certificates of Deposit Commercial and Industrial Banking IRAs Small Business Banking ATM Network Government Banking Online Banking Not-For-Profit Banking Online Account Opening Interest Rate Risk Management Mobile Banking Employee Benefits Debit Cards Bank @ Work Treasury Solutions Zelle Cash Management Lending Options Commercial Cards Merchant Services Mortgages Home Equity Wealth Management Credit Cards Investment Services* Personal Loans Asset Management & Trust 3

Mid-Year 2022 Highlights Six months ended 03/31/2022 unless otherwise noted • Net income of $9.2 million compared to $8.5 million for the comparable period in 2021; earnings per share of $0.94, ROE 8.86%, ROA 0.99%. • Compared to six months ended 03/31/2021 revenue, net of interest expense, increased $1.3 million. Net interest income (NII) of $27.8 million, up 7.1%; Net interest margin (NIM) increased to 3.15% from 2.89%. • Noninterest income of $4.3 million, compared to $6.7 million; decrease driven by lower gain on sale of loans and investments; decrease of $1.7 million due to interest rate changes. • Credit quality improved, non-performing assets at 0.44% compared to 0.88% at 09/30/2021. • Noninterest expense flat. • Balance Sheet relatively flat, 1.8% loan growth net of PPP and Indirect auto run-off, asset quality remains strong. ? Deposits $1.62 billion, core deposits increased $26.5 million or 1.9%. ? Loans of $1.36 billion, including commercial loan growth of $11.5 million or 1.7%, net of PPP forgiveness of $17.2 million. ? CET1 ratio of 13.27%. ? Paid common dividends of $2.3 million, $0.12 per share per quarter. ? AOCI positive of $4 million. • Other highlights. ? Libor transition continues to progress as planned. ? CECL implementation in process, fully implemented beginning October 1, 2023. ? Subsequent announcement (June 6, 2022) of three cent (25%) dividend increase and authorization to repurchase up to 500,000 shares.

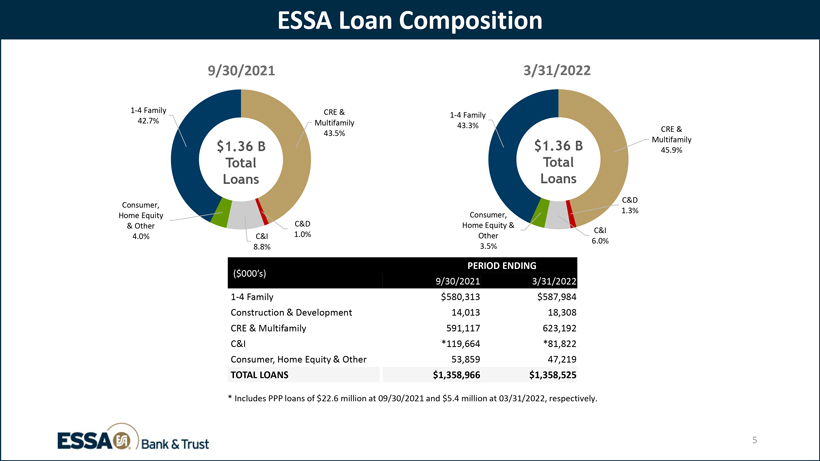

ESSA Loan Composition PERIOD ENDING 9/30/2021 3/31/2022 ($000’s) 1-4 Family $580,313 $587,984 Construction & Development 14,013 18,308 CRE & Multifamily 591,117 623,192 C&I *119,664 *81,822 Consumer, Home Equity & Other 53,859 47,219 TOTAL LOANS $1,358,966 $1,358,525 * Includes PPP loans of $22.6 million at 09/30/2021 and $5.4 million at 03/31/2022, respectively.

Lending Highlights • Loan quality improved, with reduced levels of NPAs and foreclosed real estate. • 5.2% growth in CRE. • Growth in commercial and residential real estate was offset by sales of $13.6 million of residential mortgages, $6.4 million reduction in indirect auto, and $17.2 million of PPP forgiveness. • Added banking professionals in commercial credit and relationship management during 2Q and 3Q 2022. • Loan pipelines remain relatively strong through May 31, 2022. • Gross commercial loan production of $151 million through March 31, 2022. • Gross residential mortgage loan production of $95.9 million through March 31, 2022.

ESSA Retail Deposit Composition DDA $257,747 $291,676 NOW 341,138 320,207 SAV 189,004 197,936 MMDA 428,272 417,801 TD 194,924 168,252 TOTAL $1,411,085 $1,395,872 • Excludes broker deposits of $225 million at 09/30/2021 and 03/31/2022, respectively. • Average cost of interest-bearing deposits was .40% at 09/30/2021 and . 12% at 03/31/2022. ($000’s) PERIOD ENDING 9/30/2021 3/31/2022

Deposit Highlights • Total deposits were $1.62 billion. • Core deposits comprised 89.6% of total deposits at March 31, 2022 • Non-interest bearing DDA increased 12.4% or $33.9 million from September 30, 2021. • Total costs of interest-bearing liabilities was .17% at March 31, 2022. • Retail FTE count at lowest level in three years. • Continued growth in digital adoption.

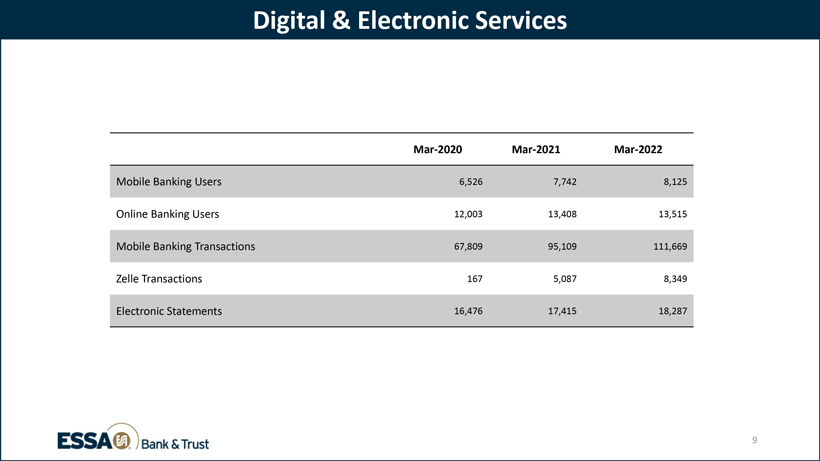

Digital & Electronic Services Mar-2020 Mar-2021 Mar-2022 Mobile Banking Users 6,526 7,742 8,125 Online Banking Users 12,003 13,408 13,515 Mobile Banking Transactions 67,809 95,109 111,669 Zelle Transactions 167 5,087 8,349 Electronic Statements 16,476 17,415 18,287

ESSA Bank & Trust ESSA Investment Services ESSA Asset Management & Trust ESSA Advisory Services