UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2015

or

[ ] TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _____________ to _____________

Commission file number: 000-52444

PLASTIC2OIL, INC.

(Exact name of registrant as specified in its charter)

| Nevada | 90-0822950 | |

| (State

or other jurisdiction of incorporation or organization) |

(IRS

Employer Identification No.) |

| 20

Iroquois Street Niagara Falls, NY 14303 |

| (Address of Principal Executive Offices) (Zip Code) |

Registrant’s telephone number: (716) 278-0015

Securities registered pursuant to Section 12(b) of the Act: None.

Securities registered pursuant to Section 12(g) of the Act: Common Stock, par value $0.001 per share.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such report(s)), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer [ ] | Accelerated filer [ ] | |

| Non-accelerated filer [ ] | Smaller reporting company [X] |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [X]

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the Registrant was approximately $10.3 million as of June 30, 2015 based upon the closing price of $0.09 per share on June 30, 2015.

As of April 14, 2016, there were 124,756,158 shares of the Registrant’s common stock, $0.001 par value, outstanding.

Documents Incorporated by Reference

None

PLASTIC2OIL, INC.

Table of Contents

| 2 |

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This annual report on Form 10-K (“Report”) contains “forward looking statements” within the meaning of applicable securities laws. Such statements include, but are not limited to, statements with respect to management’s beliefs, plans, strategies, objectives, goals and expectations, including expectations about the future financial or operating performance of our Company and its projects, capital expenditures, capital needs, government regulation of the industry, environmental risks, limitations of insurance coverage, and the timing and possible outcome of regulatory matters, including the granting of patents and permits. Words such as “expect”, “anticipate”, “intend”, “attempt”, “may”, “will”, “plan”, “believe”, “seek”, “estimate”, and variations of such words and similar expressions are intended to identify such forward looking statements. These statements are not guarantees of future performance and involve assumptions, risks and uncertainties that are difficult to predict.

These statements are based on and were developed using a number of factors and assumptions including, but not limited to: stability in the U.S. and other foreign economies; stability in the availability and pricing of raw materials, energy and supplies; stability in the competitive environment; the continued ability of our Company to access cost effective capital when needed; and no unexpected or unforeseen events occurring that would materially alter the Company’s current plans. All of these assumptions have been derived from information currently available to the Company including information obtained by our Company from third party sources. Although management believes that these assumptions are reasonable, these assumptions may prove to be incorrect in whole or in part. As a result of these and other factors, actual results may differ materially from those expressed, implied or forecasted in such forward looking information, which reflect our Company’s expectations only as of the date hereof.

Factors that could cause actual results or outcomes to differ materially from the results expressed, implied or forecasted by the forward-looking statements include risks associated with general business, economic, competitive, political and social uncertainties; risks associated with changes in project parameters as plans continue to be refined; risks associated with failure of plant, equipment or processes to operate as anticipated; risks associated with accidents or labor disputes; risks associated in delays in obtaining governmental approvals or financing, or in the completion of development or construction activities; risks associated with financial leverage and the availability of capital; risks associated with the price of commodities and the inability of our Company to control commodity prices; risks associated with the regulatory environment within which our Company operates; risks associated with litigation including the availability of insurance; and risks posed by competition. These and other factors that could cause actual results or outcomes to differ materially from the results expressed, implied or forecasted by the forward looking statements are discussed in more detail in the section entitled “Risk Factors” Part I, Item 1A of this Report and in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Part II, Item 7 of this Report.

Some of the forward-looking statements may be considered to be financial outlooks for purposes of applicable securities legislation including, but not limited to, statements concerning capital expenditures. These financial outlooks are presented to allow the Company to benchmark the results of our Company’s Plastic2Oil business. These financial outlooks may not be appropriate for other purposes and readers should not assume they will be achieved.

Our Company does not intend to, and the Company disclaims any obligation to, update any forward-looking statements (including any financial outlooks), whether written or oral, or whether as a result of new information, future events or otherwise, except as required by law.

Unless otherwise noted, references in this Report to “P2O” the “Company,” “we,” “our” or “us” means Plastic2Oil, Inc., a Nevada corporation.

| 3 |

GLOSSARY OF TECHNICAL TERMS

In this filing, the technical terms, phrases, and abbreviations set forth below have the following meanings:

“ASTM” means American Society for Testing and Materials, the entity responsible for the development and delivery of international voluntary consensus standards.

“distillate” means a product derived from petroleum-based hydrocarbons.

“Fuel Oil” means various ranges of Number 1 to 6 fuels distilled from crude oil, or in P2O’s case, distilled from plastic;

“Fuel Oil No. 2” means a distillate heating oil similar to diesel fuel with the same cetane number, or measurement of combustibility quality, as diesel fuel. This is generally obtained in the crude oil distillation process from the lighter cuts of crude oil. In our process, it is the second fuel made in the conversion from plastic to oil;

“Fuel Oil No. 6” means a high viscosity residual oil that requires preheating to 104 – 127 degree Celsius. It is generally the material remaining after the more valuable cuts of crude oil have been boiled off. In our process, it is the first fuel made in the conversion from plastic to oil;

“hydrocarbon” means an organic compound consisting entirely of hydrogen and carbon;

“MACT” means Maximum Achievable Control Technology, which are various degrees of emissions reductions that the EPA determines to be achievable;

“Naphtha” means a flammable liquid mixture of hydrocarbons covering the lightest and most volatile fraction of the liquid hydrocarbons in petroleum with a boiling range of 60 to 200 degrees Celsius. In our process, it is the last liquid fuel made in the conversion from plastic to oil;

“NESHAP” means the National Emissions Standards for Hazardous Pollutants which are emissions standards set by the EPA for an air pollutant that may cause an increase in fatalities or in serious irreversible and incapacitating illnesses; and

“Stack Test” means a procedure for sampling a gas stream from a single sampling location at a facility, used to determine a pollutant emission rate, concentration or parameter while the facility equipment is operating at conditions that result in the measurement of the highest emission values approved by regulatory authorities;

“tipping fees” means the charge levied on a given quantity of waste received at a landfill, recycling center or waste transfer facility.

| 4 |

Overview

We manufacture processors which produce fuel products mainly from unsorted, unwashed waste plastics for distribution across a number of markets. We continue to execute on our business strategy with the goal of becoming a leading manufacturer of processors and other related equipment that transform waste plastic into ultra-clean, ultra-low sulphur fuel.

Our P2O business is a commercial manufacturing and production business. We plan to grow mainly from sale of processors, secondarily from the sale of fuel products. We provide environmentally-friendly solutions through our processors and technologies. Our primary offering is our Plastic2Oil®, or P2O®, solution, which is our proprietary process that converts waste plastic into fuel through a series of chemical reactions (our “P2O business”). We collect mainly mixed plastics from commercial and industrial enterprises that generate large amounts of waste plastic for use in our process. Generally, this waste plastic would otherwise be sent to landfills and its disposal potentially can be quite costly for companies. We use this waste plastic as feedstock to produce Fuel Oil No. 2, Naphtha, and Fuel Oil No. 6 for various uses by our customers. We own and operate our P2O processors and have the capability to produce and store the fuels at, and ship from, our facilities in Niagara Falls, NY. We sell the fuels we produce to customers through two main distribution channels, fuel wholesalers and directly to commercial and industrial end-users.

At April 14, 2015, we had three fully-permitted operational P2O processors, one dedicated to research & development and two dedicated to fuel production. All three processors are located at our Niagara Falls, NY facility, and our fourth and fifth processors were in process of assembly for sale. For the reasons described in Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, the three operational P2O processors have been idle since late December 2013.

For financial reporting purposes, we operate in two business segments, (i) our P2O solution, which manufactures and sells processors as well as sells the fuel produced through our processors (ii) data storage and recovery (the “Data Business”). As part of our P2O business segment, we began to offer for sale built-to-order P2O processors for use at a customer’s site. Previously, we operated a chemical processing and cleaning business, known as Pak-It and a retail and wholesale distribution business known as Javaco, Inc. As of December 31, 2012, we had exited both of these businesses and their results in all periods presented are classified as discontinued operations. As of this filing date of the report, our processors were idle and not producing fuel products. Our P2O business has been operating in a limited commercial capacity since December 2010 and we anticipate that this line of business will account for a majority of our revenues in 2016 and periods thereafter. Historically, however, our revenues have been partially derived from our other lines of business and products, Javaco and Pak-It, which are classified in this Annual Report as discontinued operations. In the year ended December 31, 2015, we had total sales of approximately $16,728, of which $0 were derived from our P2O business and $16,728 were derived from our Data Business. In the year ended December 31, 2014, we had total sales of $59,017 from our P2O business and $12,906 from our Data Business.

We conduct our P2O business at our facilities located in Niagara Falls, New York. Our corporate address is 20 Iroquois Street, Niagara Falls, NY 14303.

| 5 |

Organizational History

We were incorporated on April 20, 2006 under the laws of the State of Nevada under the name 310 Holdings Inc. (“310”). On April 24, 2009, the Company’s founder, former CEO and Chief of Technology, John Bordynuik, purchased 63% of the issued and outstanding shares of 310 and became our chairman and chief executive officer. On June 25, 2009, we purchased certain assets from John Bordynuik, Inc., a corporation founded by Mr. Bordynuik. The assets acquired included tape drives, computer hardware, servers and a mobile data recovery container to read and transfer data from magnetic tapes. From inception until August 2009, we were a shell company within the meaning of the rules of the Securities and Exchange Commission. On August 24, 2009, we acquired all of the outstanding shares of Javaco, Inc., a wholly owned subsidiary of Domark International, Inc. On September 30, 2009, we acquired 100% of the issued and outstanding equity interests of Pak-It, LLC. We formed JBI (Canada) Inc. on February 9, 2010 for purposes of distributing Pak-It products in Canada. We formed Plastic2Oil of NY, #1, LLC on May 4, 2010, for the development and commercialization of our Plastic2Oil business in Niagara Falls, NY.

On October 5, 2009, we changed our corporate name to JBI, Inc.

On August 24, 2009, the Company acquired Javaco, Inc. (“Javaco”), a distributor of electronic components, including home theater and audio video products. On July 9, 2012, we announced the closure of our Javaco operations and sold substantially all of its assets to an unrelated third party. In July 2012, the Company closed Javaco and sold substantially all its inventory and fixed assets. The operations of Javaco have been classified as discontinued operations for all periods presented (See Note 15).

In September 2009, the Company acquired Pak-It, LLC (“Pak-It”). Pak-It operated a bulk chemical processing, mixing, and packaging facility. It also developed and patented a delivery system that packages condensed cleaners in small water-soluble packages. During 2011, the Company initiated a plan to sell certain operating assets of Pak-It and subsequently sold Pak-It in February 2012, with an effective date of January 1, 2012. On February 10, 2012, we sold substantially all the assets of Pak-It. The operations of Pak-It have been classified as discontinued operations for all periods presented (See Note 16).

In December 2010, the Company entered into a twenty year lease for a recycling facility in Thorold, Ontario. During the period ended December 31, 2013, the Company determined that it would no longer operate the facility and shut down all operations. The assets and operations related to the recycling facility have been reclassified as discontinued operations for all periods presented (See Note 15). The property was vacated on November 10, 2015 and the lease was terminated on January 15, 2016 effective October 31, 2015.

On July 31, 2014, we changed our corporate name to Plastic2Oil, Inc. On January 6, 2015, we changed the names of our two Canadian subsidiaries from JBI (Canada) Inc. to Plastic2Oil (Canada), Inc., and from JBI RE ONE, Inc. to Plastic2Oil RE ONE, Inc.

Our common stock is quoted on the OTCQB Market under the symbol “PTOI”.

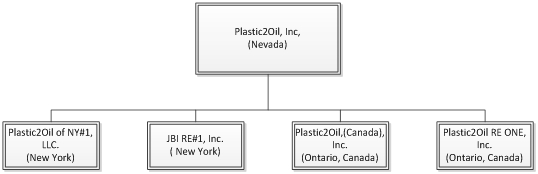

Organizational Chart

The following chart outlines our corporate structure, as of March 30, 2016, and identifies the jurisdiction of organization of each of our material subsidiaries. Each material subsidiary is wholly-owned by the company.

| 6 |

| Plastic2Oil, Inc. | - | Operates our Data Recovery and Migration business and Parent company with corporate office in Niagara Falls, NY. |

| Plastic2Oil of NY #1, LLC | - | Operates our P2O business in Niagara Falls, NY. |

| Plastic2Oil (Canada) Inc. | - | Conducts our P2O business in Canada, including management of our Ontario, Canada fuel blending site. |

| JBI RE#1, Inc. | Real Estate holding subsidiary operating out of the Niagara Fall, NY | |

| Plastic2Oil RE ONE, Inc. | Real Estate subsidiary operating out of Ontario, Canada |

Our Primary Business - Plastic2Oil

P2O Overview

Our business focus is to manufacture and sell processors that produce fuel products mainly from unsorted, unwashed waste plastics for distribution across a number of markets. We plan to grow mainly from sale of processors, secondarily from the sale of fuel products. We continue to execute on our business strategy with the goal of becoming a leading North American company that sells procesors to transform waste plastic into ultra-clean, ultra-low sulphur fuel. We have years of operating data and have solved numerous challenges that vexed the plastics-to-oil industry. Since inception we have produced approximately 670,000 gallons of fuel. Our P2O processors have evolved into a modular solution with the completion of our third P2O processor in 2013. We use third party contract manufacturers to supply us with many of the key modular components of our processors, including the kilns, distillation towers and other key components that require specialized machining and fabrication. As of the filing date of this report, our processors were idle and not producing fuel products. Processors are being used only for customer visits and for maintenance activities.

Our proprietary P2O process converts waste plastic into fuel through a series of chemical reactions. We developed this process in 2009 and began very limited commercial production in 2010 following our receipt of a consent order from the New York State Department of Environmental Conservation (“NYSDEC”) allowing us to commercially operate our first large-scale P2O processor at our Niagara Falls, New York facility. Currently, we have three fully-permitted P2O processors, which are capable of producing Naphtha, Fuel Oil No. 2 and Fuel Oil No. 6, all of which are fuels produced to the specifications published by ASTM. One fully-permitted P2O processor is dedicated to research and development activities. We have components for two additional processors at an outside vendor, which are included in the balance sheet as deposits. Our P2O process is capable of producing two by-products, an off-gas similar to natural gas and a petcoke carbon residue. In instances when wwe produce and sell fuel products, we primarily use our off-gas product in our operations to fuel the burners in our P2O processors. Historically, we have sold our fuel products through two main distribution channels comprised of fuel wholesalers and directly to commercial and industrial end-users.

| 7 |

We shut down our fuel production late in the fourth quarter of 2013 due to severe cold weather that caused damage to condensers and other components of our processors and we have not resumed fuel production due to the repair costs as well as our shift in strategy toward manufacturing processors for sale, as opposed to producing and selling fuel products. Management estimates that the repair of the processors will require the expenditure of between $175,000 and $200,000. An additional $300,000 of startup working capital will be required to resume operations mainly for hiring operational personnel and incremental overhead expenses. At March 30, 2016, we lacked the working capital or access to bank credit to make these repairs. We are reviewing our financing options, including the sale of shares of our common stock or other securities, in order to allow us to obtain sufficient funds to make the required repairs and resume pilot operation of our processors to support processor sales. These processors were idle for all of 2015.Management currently anticipates that the processors will remain idle at least until the third quarter of 2016 other than pilot,or demo ,runs to support processor sales. During the idle period, we significantly reduced our headcount by furloughing our operations personnel but retained a small team to perform general repairs and maintenance on the processors. Once the processors are fully operational, we expect a small increase in our headcount in order to resume fuel production.

Our P2O process accepts mainly unsorted, unwashed waste plastics. We believe our P2O process offers a cost-effective solution for businesses that currently have to pay to dispose of these types of waste. Although many sources of plastic waste are available, we have focused our feedstock sources on primarily post-commercial and industrial waste plastic. Generally, we believe that this waste stream is more costly for companies to dispose of, making it more readily available in large quantities and cheaper for us to acquire than other potential types of feedstock.

Currently, we understand that there are several plastic-to-oil processes operational globally. These other processes employ a wide range of technologies and yield varying purities of fuel output. We believe that our process has many advantages over many other commercially available processes in that our P2O solution requires a comparatively less initial capital investment and yields high-quality, ultra-low sulphur fuel, with no need for further refinement. Additionally, our process uses comparatively little energy and physical space, which, in our view, makes it well suited for high-volume production and expansion to multiple sites.

P2O Process and Operations

Our patent-pendingP2O conversion process involves the cracking of the plastic hydrocarbon chains at ambient pressure and comparatively low temperature using a catalyst. There are various processes in existence for converting plastic and other hydrocarbon materials into products for use in the production of fuels, chemicals and recycled items. These processes include: pyrolysis (conversion using dry materials at high pressure and temperature in the absence of oxygen), catalytic conversion (conversion using a catalyst for stimulating a chemical reaction), depolymerization (conversion using superheated water and high pressure and temperature) and gasification (conversion at high temperature using oxygen or steam).

We have developed our Plastic2Oil processors with the ability to be continuously running, energy-efficient and environmentally-friendly while converting waste plastics into end-user ready, and ultra-clean, ultra-low sulfur fuels. The processors are periodically shut-down for maintenance and residue removal. The fuels produced can be used directly by our customers without further refining or processing. Over a three year period, we have scaled our processing operations from a one gallon processor to three processors, each permitted to feed up to 4,000 pounds of feedstock per hour. In prior years, some of the milestones that we have reached include:

| ● | Manufacturing and operating multiple processors at our Niagara Falls, NY site; | |

| ● | From inception, the processors were designed with safety and green emissions as top priorities; | |

| ● | Standardization and modularization of the components of our processors; | |

| ● | Ability to continuously feed waste plastic 24 hours a day; | |

| ● | Approximately 86% of waste plastic by weight is converted to liquid fuel conversion; | |

| ● | Approximately 8% of waste plastic by weight is converted to gas and is used to fuel the process; | |

| ● | Operating at atmospheric pressure, not susceptible to pinhole leaks and other problems with pressure and vacuum-based systems; |

| 8 |

| ● | No requirement for incinerators, thermal oxidizers or scrubbers and no stack monitoring is necessary; | |

| ● | Three stack tests (two on the initial processor and one on the second processor) conducted by Conestoga-Rovers & Associates (“CRA”), prove emissions are extremely low; | |

| ● | Process validation by SAIC Energy, Environment & Infrastructure, LLC and IsleChem, LLC; and | |

| ● | Permitted to operate three processors commercially in New York by the NYSDEC. |

Processor Input

Waste Plastics: We are able to feed mainly mixed unwashed waste plastics into the Plastic2Oil processors. Waste plastic is widely available and we are focused on maximizing the types and densities of the plastic we procure for optimal processor performance.

Heat Transfer Fluid: We are also able to include hydrocarbon based transfer fluid as feed into the Platic2Oil processors.

Processor Output

We are currently permitted to feed two tons, or 4,000 pounds, of waste plastic per hour into each processor by a continuous conveyor belt where it is heated by a burner that mainly burns off-gases produced from the P2O process. Plastic hydrocarbons are cracked into various shorter hydrocarbon chains and exit in a gaseous state. Any residue, metals and or non-usable substances remain in the reactor and are periodically removed. Through our proprietary process, Fuel Oil No. 6, Fuel Oil No. 2, and Naphtha are condensed from the reactor through the remainder of the process. The fuel output is then transferred to storage tanks automatically by the system. Our process is mainly operated by an automated computer system that controls the conveyor feed rate, system temperatures, off-gas systems and the pumping out of newly created fuel to storage tanks. The plastic to liquid fuel conversion is approximately 86% by weight. Therefore, 20 tons of plastic can be processed into approximately 4,100 gallons of fuel. At March 30, 2016, we had three processors at our Niagara Falls, NY facility. One processor was dedicated to research and development and all three processors remained idle due to maintenance and repair issues.

Fuel Produced: The fuel produced in our processors is ultra-low sulfur fuel and is ready for end-users without the need for further refinement.

Off-gas: Approximately 8-10% of waste plastics fed into the processors are converted to a mixture of hydrogen, methane, ethane, butane and propane gas, which we call “off-gas”. Once our processors are in a state to begin the P2O process, they use their own off-gas to fuel the burners in the process.

Residue: There is approximately 2-4% residue from our process, which is petroleum coke or carbon black (which we call “petcoke”) that needs to be removed on a periodic basis.

Feedstock

Our P2O process primarily uses post-commercial and industrial waste plastic that might otherwise be sent to a landfill by the commercial and industrial producers of such waste plastic. We believe that this can be costly for these producers due to the large volumes of plastic waste that they generate. As such, our business model is premised on the processor’s ability to accept numerous types of waste plastics from such sources at a relatively low cost. We believe that our processor ability to accept mainly mixed, unwashed waste plastics is a significant advantage of our P2O process compared to similar operations in our industry.

Fuel Products

Our P2O process makes both light and heavy fuel products which are Naphtha, Fuel Oil No. 2 and Fuel Oil No. 6, as defined by ASTM. Our process also generates two main by-products, a reusable off-gas similar to natural gas and a carbon residue known as petcoke.

| 9 |

Naphtha is a very light fuel product that is used as a cutting component for both high and regular grade gasoline. Fuel Oil No. 2 is a mid-range fuel commonly known as diesel and has numerous transportation, manufacturing and industrial uses. Fuel Oil No. 6 is a heavy fuel generally used in industrial boilers and ships. Our process produces high quality, ultra-low sulphur fuels, without the need for further refinement which enables fuel sales directly from the processors to the end-user.

The reusable off-gas that is produced by the P2O process is used to fuel the burner that heats the entire processor.

P2O Facilities

We currently have one main facility (located in Niagara Falls, NY) that we use in our P2O business, as well as a second facility, our fuel blending site (located in Thorold, Canada), for use in the future. These are briefly described below. Additional information on our properties can be found in Item 2 of this report.

Niagara Falls, NY facility: Our Niagara Falls, NY facility currently has two buildings, a 10,000 square foot building that currently houses one commercial-scale P2O processor and one P2O processor devoted to research and development activities, and a 7,200 square foot building housing the third commercial-scale P2O processor. Our Niagara Falls operations are situated on eight acres that can accommodate expansion of our operations. This facility also serves as the center of our research and development operations and our administrative offices.

Blending Site: We own a 250,000 gallon fuel-blending facility in Thorold, Ontario, Canada, which, when in use, would allow us to blend and self-certify certain fuels that are produced from our process to meet government specifications.

Sales and Distribution

Our P2O business is a commercial manufacturing and production business. We plan to grow mainly from sale of processors first, and fuel seller second.

We sell our fuel products through two main channels: fuel brokers and direct to end-users. We have no long-term contracts for fuel sales; rather, we sell our fuel through the issuance of routine purchase orders.

During the years ended December 31, 2015 and 2014, 100%, and 89% of total net revenues were generated from a single, and two customers, respectively. As of December 31, 2015 and 2014, one and two customers, respectively, accounted for 100% of accounts receivable.

Suppliers

The principal goods that we require for our P2O business are the waste plastic that we use as feedstock for production of our fuels. We collect waste plastics from commercial and industrial businesses that generate large amounts of this waste stream. As of April 14, 2016, we had approximately 327,000 pounds of waste plastic and approximately 10,000 gallons of heat transfer fluid available in inventory as feedstock, to support the resumption of operations upon the repairs, as mentioned above.

We also rely on third party manufacturers for the manufacture of many components of our processors including kilns and distillation towers.

During the years ended December 31, 2015 and 2014, five and four suppliers, respectively, accounted for 30.9% and 38.0% of accounts payable, respectively.

Licenses, Permits and Testing

We maintain the following permits and licenses in connection with the operation of our P2O business.

| 10 |

| License/Permit | Issuing Authority | Registration Number | Issue date | |||

| Air Permit | NYSDEC | 9-2911-00348/00002 | 06/30/2015(Annual) | |||

| Solid Waste Permit | NYSDEC | 9-2911-00348/00003 | 06/30/2015(Annual) | |||

| Bulk Fuel Blending License | Ontario Technical Standards & Safety Authority | 000184322 | 10/12/2015(Annual) | |||

| Waste Disposal Site | Ontario Ministry of the Environment | A121029 | Perpetual (subject to annual reviews) |

In 2010, our P2O process and processors were tested by IsleChem, LLC, an independent chemical firm providing contract research and development, manufacturing and scale-up services, using two small prototypes of our P2O processor. The IsleChem test results indicated that our process is both repeatable and scalable. Following this testing, we assembled a large-scale P2O processor capable of processing at least 20 metric tons of plastic per day. In September 2010, we had a Stack Test performed by Conestoga-Rovers & Associates (“CRA”), an independent engineering and consulting firm, which concluded that, with a feed rate of 2,000 pounds of plastic per hour, our processor’s emissions were below the maximum emissions levels allowed by the NYSDEC simple air permit, which is needed to commercially operate the P2O processor at that location. We used the CRA test results to apply for the required operating permits and in June 2011 we received an Air State Facility Permit (“Air Permit”) and Solid Waste Management Permit (“Solid Waste Permit”) for up to three processors at the Niagara Falls, NY facility. In December 2011, we had a second stack test performed by CRA for an increased rate of 4,000 pounds per hour. In January 2012, we received a final emissions report from CRA confirming that emissions were considerably decreased with an increased feed rate. In December 2012, we had a stack test performed on the second processor.

The emissions tests conducted by CRA on our processors are summarized in the following table:

| Emissions | Units1 | Original Stack Test (2010) – Processor #1 | Final Stack Test (Dec. 2011) – Processor #1 | Stack Test (Dec. 2012) – Processor #2 | ||||||||||||

| CO – Carbon Monoxide | ppm | 3.16 | 3.1 | 3.7 | ||||||||||||

| SO 2 - Sulphur Dioxide | ppm | 0.23 | 0.02 | 0.39 | ||||||||||||

| NOx – Oxides of Nitrogen | ppm | 86.4 | 15.1 | 21.3 | ||||||||||||

| TNMHC – Total Non-Methane Hydrocarbons | ppm | 0.25 | 3.92 | 0.62 | ||||||||||||

| PM – Particulate Matter | Lbs./hr. | 0.016 | 0.002 | 0.012 | ||||||||||||

| Hexane | Lbs./hr. | Not tested | 0.00001 | 0.0013 | ||||||||||||

1 “ppm” means parts per million

Industry Background

Alternative fuels are generally considered to be any substances that can be used as fuel, other than conventional fossil fuels such as naturally occurring oil, gas and coal. There have been many approaches taken to producing alternative fuels, including conversion of corn oil, vegetable oil and non-food-based materials. These approaches have demonstrated varying degrees of commercial potential. Some of the challenges that alternative fuel producers have faced include high feedstock supply costs, lower perceived value of fuel product, higher capital costs and dependence on government regulations for economic viabilities. We believe our company is distinguishable from other producers of alternative or renewable fuels because our P2O solution represents a process and product that is commercially viable and designed to provide immediate benefit for industries, communities and government organizations with waste plastic recycling challenges. Our business model is premised on the need for a more efficient and cost-effective. alternative to disposing of waste plastic in jurisdictions where the cost of transporting and landfilling large amounts of plastic is quite costly.

| 11 |

Competition

Our P2O business has elements of both a recycling business and a fuel refiner/ production business, which makes it difficult to identify and make direct comparisons to competitors. Both the recycling and energy sectors are characterized by rapid technological change. Our future success will depend on our ability to achieve and maintain a competitive position with respect to technological advances in both of these sectors. We believe that our business currently faces competition in the plastics-to-energy market, including competition from PK Clean, Vadxx Energy, Green Envirotec Holdings LLC, Agilyx and RES polyflow, each of which has developed alternative methods for obtaining and generating fuel from plastics. See “Risk Factors—Risks Related to Our Business”. Because P2O solution end products include a variety of fuels, we also face competition from the broader petroleum industry.

Business Model

We believe that our business model provides a unique proposition for both the “supply side” and the “end-user” side of the waste-to-fuel value chain. Our P2O technology is positioned to link these two sides by offering economic incentives in both directions. We believe P2O offers value to suppliers of waste plastic by saving transport and landfill tipping fees, and value to fuel end-users by providing ultra-low sulphur green fuel. Given these incentives, we believe that our business will be sought after by those industries that can benefit from the added value that we provide, thus allowing the potential for our company’s growth through sale of processors.

Business Strategy

Our long-term strategy is to become the leading plastic-to-oil processor manufacturer. Our processor buyer are private and municipalities in the recycling industry who can operate on a commercial scale. Our fuels consumers are fuel distributors. Our processors are to demonstrate our technology and processor capabilities, for process improvement, for research and development activities and to test potential customer feedstock. The key elements of our strategy to achieve this goal are as follows:

Marketing Strategy

We target post-commercial and industrial waste plastic partners. We believe this allows us to identify sources of large plastic waste streams, such as industrial sites and material recovery facilities and recycling centers. We also seek to partner with businesses and municipalities that collect waste plastics. Our vision is to help redirect these waste plastic streams, preventing them from entering landfills.

Manufacturing and Procurement Strategy

Our P2O business model allows us to simultaneously pursue sales to multiple commercial opportunities (partners) across the waste plastic and fuel markets. Our P2O processors have evolved to be modular solutions with the completion of processor #3 in 2013. We use third party contract manufacturers for the manufacture of many of the key modular components of our processors, including the kilns, distillation towers as well as other key components that require specialized machining and fabrication. We will license our P2O technology, including construction operation and maintenance of processors for operation at our partners’ sites. Our strategy is to have our partners construct clusters of P2O processors at sources of large plastic waste streams, such as industrial sites, material recovery facilities and recycling centers.

Feedstock Procurement Strategy

Our feedstock strategy is as follows:

| ● | Get the Right Material to Maximize Throughput. Although the P2O processor can process many different types of plastic and create consistent fuels, we will focus on the types of plastic that will maximize the machine’s productivity. This is typically high density material. | |

| ● | Contract for Long-Term Consistent Feedstock Supply. By contracting with our suppliers, we are able to gain commitments for consistent flows of feedstock. This also allows us to more accurately forecast our feedstock supply and fuel outputs. An additional benefit of contracting with suppliers is that we are able to rely on this material flow as it relates to our continued growth planning. | |

| ● | Cost to the Processor. We look at all feedstock opportunities considering the “cost to the processor”. This means we consider including the cost is the price we pay to the supplier, the cost of transportation or our costs to pre-process the feedstock material, the critical thing is the total cost incurred for “ready to process” material. |

| 12 |

Competitive Strengths

We believe that our competitive strengths are as follows:

Our processors convert unwashed waste plastics into “in specification fuels” ready for use by the end-user customer. Our process does not generate any waste water. The fuel is Halide-free and there is no further need for refinement. The process does not produce any hazardous waste.

In addition to producing fuel, our P2O solution simultaneously addresses the problem of disposing of waste plastic. We offer an alternative to disposing of waste plastic in a landfill. Our processors can accept mainly mixed, unwashed plastic feedstock. In the United States and Canada, a substantial amount of plastic is currently considered waste and is disposed of in landfills, resulting in tipping fees levied by the landfill or other waste disposal facility fees. We believe that the current low landfill diversion rates for waste plastic in the United States and Canada, together with the costs of transporting and disposing of plastic in bulk, present a significant opportunity to provide an alternative to conventional recycling and waste disposal.

The P2O process provides a highly efficient means of converting plastic into fuel. Our proprietary P2O process and catalyst provide a highly efficient means of converting plastic into fuel. Our business model depends on us being able to provide both a cost-competitive means of disposing of waste plastic and an efficient and non-energy intensive means of producing fuel. Our process requires comparatively minimal electricity to operate, and the energy balance of the process is positive, meaning that more energy can be produced than is consumed by the process.

Low capital costs and small footprint. We have designed the processors with a modular design with standardized components, making construction of our processors relatively simple and cost effective. We have designed our processors to take up approximately 3,000 square feet of space, giving the processors a relatively small footprint. We believe that this design facilitates the construction and operation of multiple processors on a single site. We estimate that the costs of constructing our processors on industrial partner sites will be substantially less than the cost of constructing waste-to-fuel facilities offered by our competitors.

Lower emissions

In the United States, businesses and other producers of emissions are subject to various regulatory requirements, including the National Emission Standards for Hazardous Air Pollutants, or “NESHAP.” These emission standards may be established according to Maximum Achievable Control Technology requirements set by the EPA, often referred to as “MACT standards”. MACT standards apply to a number of sources of emissions, including operators of boilers, process heaters and certain solid waste incinerators. Because our P2O fuel products have ultra-low sulphur content, we believe that our P2O fuel can assist industrial partners with meeting MACT requirements through reduced hazardous emissions.

Our processors produce fuels that have very low sulphur content, which allows the end-user to potentially lower the emissions generated by its operations while using our fuels. These lower emissions potentially could save the end-user from expensive environmental compliance costs, stemming from such initiatives as the NESHAP regulations and more specifically the MACT standards for each pollution source.

Validation of repeatability and scalability of P2O processors.

Our P2O business has been validated for repeatability and scalability by extensive testing by our customers and multiple independent tests by outside consultants and third party laboratories.

| 13 |

Other Businesses

Data Recovery & Migration

In June 2009, we purchased certain assets from John Bordynuik, Inc., a corporation founded by John Bordynuik, our former Chief Executive Officer and former Chief of Technology and who now serves as a consultant to the company.. The assets acquired from John Bordynuik, Inc. included tape drives, computer hardware, servers and a mobile data recovery lab to read and transfer data from magnetic tapes and these assets are used in our Data Recovery & Migration business.

Magnetic tapes were previously a primary media for data storage. Because of its cost effectiveness, magnetic tape was widely used by government, scientific, educational and commercial organizations for decades. Over time, these tapes can become vulnerable to deterioration when exposed to natural elements, which can render the tapes difficult to read or unreadable using the original tape-reading equipment. Our Data Business involves reading old magnetic tapes, interpreting and restoring the data where necessary and transferring the recovered data to storage formats used in current systems. The recovered data is verified for accuracy and returned to customers in the media storage format of their choice. Our process gives customers the ability to conveniently catalogue and safely archive difficult-to-retrieve data on readily accessible, contemporary storage media. Users of these services generally include businesses or organizations that have historically stored information on magnetic tape, such as government agencies, oil and gas companies and academic institutions.

The process for data recovery was developed and is very highly dependent on the services of Mr. Bordynuik. The Data Business’s reliance on Mr. Bordynuik was a key driver to achieving revenue in 2015 and 2014. In light of our business strategy focus on our P2O business, we anticipate that revenues and profits generated from our Data Business operations will represent a decreasing share, if any, of our total revenues and profits in future reporting periods. Due to these factors, all related to the assets of the Data Business was recorded as impaired in 2012.

Pak-It

From September 2009 until February 2012, through Pak-It, we were engaged in the manufacture of cleaning chemicals. As previously reported, we sold substantially all of the assets of this business in February 2012 because management felt that Pak-It’s business was no longer aligned with our strategic focus on our P2O business. For all years reported, the results of operations of Pak-It have been recorded as discontinued operation, as recorded in Footnote 17 of our Consolidated Financial Statements.

Javaco

From August 2009 until July 2012, through Javaco, we were a retailer and wholesale distributor of equipment, hardware and tools for the safety, maintenance and construction industries. As previously reported, in July 2012, we closed Javaco and liquidated substantially all of the fixed assets and inventory because management felt that Javaco’s business was no longer aligned with our strategic focus on our P2O business. For all years reported, the results of operations of Javaco have been recorded as discontinued operations, as recorded in Footnote 17 of our Consolidated Financial Statements.

Intellectual Property

To ensure the protection of our proprietary technology, we have applied for patent protection for both the P2O process and P2O processor. As of March 30, 2016, no patents have been issued. (The application was published on January 1, 2015 under Publication No. US2015/0001061 and is available on the USPTO website at http://patft.uspto.gov/). Management anticipates filing additional patent applications for various aspects of our P2O process in the near future. A lack of patent protection could have a material adverse effect on our ability to gain a competitive advantage for our process and processors, since it is possible that our competitors may be able to duplicate the P2O process for their own purposes. We also rely on our trade secrets to provide protection from portions of our process and proprietary catalyst. See “Risk Factors—Risks Related to Our Business”.

We also hold a U.S. patent relating to our Data Business for the recovery of tape information.

| 14 |

Research and Development

Given our strategic focus on developing our P2O business, we anticipate that our research and development activities related to our P2O processors and the construction, operation and systems management of those processors will decrease. Specifically, we will seek to increase the operational capabilities and performance of our P2O processors as opportunities arise. Research and development expenditures were $1,653, and $20,999 in 2015 and 2014, respectively.

Employees

As of April 14,, 2016, we employed four persons on a full-time basis, of which one is were executive management, two were in finance and administration, one were in operations. None of our employees are subject to a collective bargaining agreement and we believe that our labor relations are good.

Environmental and Other Regulatory Matters

As we further develop and commercialize our P2O business, we will be subject to extensive and frequently developing federal, state, provincial and local laws and regulations, including, but not limited to those relating to emissions requirements, fuel production, fuel transportation, fuel storage, waste management, waste storage, composition of fuels and permitting. Compliance with current and future regulations could increase our operational costs. Management believes that the company is currently in substantial compliance with applicable environmental regulations and permitting.

Our operations require various governmental permits and approvals. We believe that we have obtained, or are in the process of obtaining, all necessary permits and approvals for the operations of our P2O business; however, any of these permits or approvals may be subject to denial, revocation or modification under various circumstances. Failure to obtain or comply with the conditions of permits and approvals or to have the necessary approvals in place may adversely affect our operations and may subject us to penalties.

Company Information

We are a reporting company and file annual, quarterly and current reports, proxy statements and other information with the SEC. You may read and copy these reports, proxy statements and other information at the SEC’s Public Reference Room at 100 F Street N.E., Washington, D.C. 20549. Please call the SEC at 1-800-SEC-0330 or e-mail the SEC at publicinfo@sec.gov for more information on the operation of the public reference room. Our SEC filings are also available at the SEC’s website at http://www.sec.gov. Our Internet address is http://www.plastic2oil.com. There we make available, free of charge, our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and any amendments to those reports, as soon as reasonably practicable after we electronically file such material with, or furnish such material to, the SEC.

The following risk factors should be considered in evaluating our businesses and future prospects. These risk factors represent what we believe to be the known material risk factors with respect to our business and our company. Our businesses, operating results, cash flows and financial condition are subject to these risks and uncertainties, any of which could cause actual results to vary materially from recent results or from anticipated future results.

| 15 |

Risks Related to our Business

We are an early stage company with a history of net losses, and we may not achieve or maintain profitability.

We have incurred net losses since our inception, including losses of $4,266,070, and $6,801,519 in 2015 and 2014, respectively. We expect to incur losses and potentially have negative cash flow from operating activities for the near future. We have divested of our significant non-core businesses, which historically had generated revenues for the Company and have transitioned our focus solely on the development of our P2O business. To date, our revenues from our P2O business have been limited and we expect to invest significant additional capital in the further development and expansion of our P2O business and for marketing and general and administrative expenses associated with our planned growth and management of operations as a public company. As a result, even if our revenues increase substantially, we expect that our expenses could exceed revenues for the foreseeable future. It is not certain when we will achieve profitability. If we fail to achieve profitability, or if the time required to achieve profitability is longer than we anticipate, we may not be able to continue our business. Even if we do achieve profitability, we may not be able to sustain or increase profitability on a quarterly or annual basis. We may experience significant fluctuations in our revenues, significantly driven in part by the long negotiation periods, market price of fuel and we may incur losses from period to period. The impact of the foregoing may cause our operating results to be below the expectations of investors and securities analysts, which may result in a decrease in the market value of our securities.

We have a limited operating history and are focused on our P2O business, which may make it difficult to evaluate our current business and predict our future performance.

After divesting certain non-core business lines, we are solely focused on our P2O business and our limited operating history may make it difficult to evaluate our current business and predict future performance as we continue to expand and grow, as well as modify the current processors to become more efficient. Additionally, with the shutdown of our regional recycling center in 2013 and the divestitures of Pak-It and Javaco in 2012, our historical results are not indicative of future revenues. Any assessment of our current business and predictions about our future success or viability may not be as accurate as otherwise possible if we had a longer operating history. We have encountered, and may continue to encounter risks and difficulties frequently experienced by growing companies in rapidly changing industries. If we do not address these risks successfully, our business could be harmed.

Our process and processors may fail to produce fuel at the volumes we expect.

A key component of our business strategy is to market our processors that produce a viable high quality fuel to wholesalers and industrial end users. Even with a reliable supply of sufficient volumes of waste plastic, our and ours customer processors may fail to perform due to mechanical failure or unscheduled maintenance resulting in potentially significant downtime. Our processors do not have a long operating history, and accordingly the equipment and systems in any given processor may not operate as planned or for as long as expected based on preliminary testing and trials.

We may be required to replace parts more often than expected due to excessive wear and tear or malfunction due to their use during the evolution of our process. Replacement of parts or components of the processor could result in additional unplanned downtime, resulting in lower fuel volume productions.

Different feedstock may result in different fuel yields including potentially higher production of off-gas or petcoke residue, which would proportionately reduce the amount of salable fuels produced. The presence of contaminants in our feedstock could reduce the purity of the fuel that we produce and require further investment in more costly separation processes or equipment. Additionally, contaminants that are present in the feedstock could result in damage to the processor which would cause unplanned downtime and lower than expected fuel volumes.

Unexpected problems with either the processor or our feedstock supplies may force us to cease or delay production and the time and costs involved with such delays may be significant. Any or all of these risks could prevent us from achieving the production volumes and yields, and producing fuel at the costs, necessary to achieve profitability from our business. Failure to achieve expected production volumes and yields, or achieving them only after significant additional expenditures, could substantially harm our financial condition and operating results.

| 16 |

We need substantial additional capital in the future in order to develop our business.

Our future capital requirements will be substantial, particularly as we continue to develop our P2O business. We believe that our current cash and cash equivalents will not allow us to expand commercial operations at the Niagara Falls, NY Facility. Because the costs of developing the P2O business on a commercial scale are highly contingent on our approach to commercialization, and are subject to many variables, including site-specific development costs and the number of processors to be placed at a given location, we cannot reliably reasonably estimate the amount of capital required to expand the P2O business beyond the Niagara Falls, NY facility; thus processor manufacturer first, and fuel seller second. If we are successful in achieving our plans to enter into other P2O industrial partnerships, we may require significant additional funding to execute such partnerships and may not be able to rely on funding through our own earnings. Funding would be required for constructing P2O processors, site specific build-outs and developing other aspects of our business with our industrial partners.

To date, we have funded our operations primarily through private offerings of equity securities. If future financings involve the issuance of equity securities, our existing stockholders could suffer dilution. If we were able to raise debt financing to expand our operations, we may be subject to restrictive covenants that could limit our ability to conduct our business. Our plans and expectations may change as a result of factors currently unknown to us, and we may need additional funds sooner than planned. We may also choose to seek additional capital sooner than required due to favorable market conditions or strategic considerations.

Our future capital requirements will depend on many factors, including:

| ● | the financial success of our P2O business and sale of processors; |

| ● | the timing of, and costs involved in, entering into agreements with suitable industrial partners, and the timing and terms of those agreements; |

| ● | the cost of constructing P2O processors and the amount of other capital expenditures related to site development; |

| ● | our ability to negotiate distribution or further sale agreements for the processors we manufacture, and the timing and terms of those agreements; and |

| ● | the timing of, and costs involved in obtaining, the necessary government or regulatory approvals and permits by our customers. |

Additional funds may not be available when we need them, on terms that are acceptable to us, or at all. If funds are necessary or required and are not available to us on a timely basis, we may delay, limit, reduce or terminate:

| ● | our research and development activities; |

| ● | our plans to expand our business through industrial partnerships; |

| ● | our activities in negotiating agreements necessary in connection with the commercial scale operation of the P2O business; and |

| ● | the development of the P2O business, generally. |

If we fail to raise sufficient funds and continue to incur losses, our ability to fund our operations, construct processors, enter into agreements with suitable industrial partners, take advantage of other strategic opportunities and otherwise develop our business could be significantly limited. We may not be able to raise sufficient additional funds on terms that are favorable or acceptable to us, if at all. If adequate funds are required for operations and are not available, we may not be able to successfully execute our business plan or continue our business.

Our future success is dependent on being able to attract and retain qualified management and personnel.

We will require additional expertise in specific areas applicable to our P2O business and will require the addition of new personnel, and the development of additional expertise by existing personnel. The inability to attract talented personnel with appropriate skills or to develop the necessary expertise could impair our ability to develop and grow our business.

| 17 |

The loss of any key members of our management team or the failure to attract or retain qualified management and personnel who possess the requisite expertise for the conduct of our business could prevent us from further developing our businesses according to our current strategy. We may be unable to attract or retain qualified personnel in the future due to the intense competition for qualified personnel amongst technology-based businesses, or due to the unavailability of personnel with the qualifications or experience necessary for our business. Competition for business, financial, technical and other personnel from numerous companies and academic and other research institutions may limit our ability to attract and retain such personnel on acceptable terms. If we are unable to attract and retain the necessary personnel to accomplish our business objectives, we may experience staffing constraints that will adversely affect our ability to meet the demands of our industrial partners and customers in a timely fashion or to support continued development of our P2O business.

Competitors and potential competitors who have greater resources and experience than we do may develop processors and technologies that make ours obsolete or may use their greater resources to gain market share at our expense.

Our P2O business has elements of both a recycling business and a fuel refiner/ production business, which makes it difficult to identify and make direct comparisons to competitors. Both the recycling and energy sectors are characterized by rapid technological change. Our future success will depend on our ability to achieve and maintain a competitive position with respect to technological advances in both of these sectors. We believe that our business currently faces competition in the plastics-to-energy market, including competition from PK Clean, Vadxx Energy, Green Envirotec Holdings LLC, Agilyx and RES polyflow, each of which has developed alternative methods for obtaining and generating fuel from plastics. See “Risk Factors—Risks Related to Our Business”. Because P2O solution end products include a variety of fuels, we also face competition from the broader petroleum industry.

Our P2O business faces competition in acquiring feedstock, mainly because there are other technologies and processes that are being developed and/or commercialized to offer recycling solutions for plastic. Additionally, there is significant competition from businesses in the energy sector that sell fuel, including both traditional producers and alternative fuel producers. Companies in the fuel sales industry may be able to exert economies of scale in the fuels market to limit the success of our fuel sales business. We believe that our business is more appealing in both the recycling sector and the fuel sector due to its green aspect. Technological developments by any form of competition could result in our processors and technologies becoming obsolete.

In addition, various governments have recently announced a number of spending programs focused on the development of clean technologies, including alternatives to petroleum-based fuels and the reduction of carbon emissions. Such spending programs could lead to increased funding for our competitors or a rapid increase in the number of competitors within these markets.

Our limited resources relative to many of our competitors may cause us to fail to anticipate or respond adequately to new developments and other competitive pressures. This failure could reduce our competiveness and market share, adversely affect our results of operations and financial position and prevent us from obtaining or maintaining profitability.

The effectiveness of our business model may be limited by the availability or potential cost of plastic feedstock sources.

Our P2O business model depends on sale of processors. However, our customers may delay procurement due to the availability of waste plastic obtained at relatively low cost to be used as a feedstock to produce our fuel products. If the availability of feedstock decreases, or if our customers are required to pay substantially more than is reasonable to become profitable for feedstock, this could reduce their fuel production and/or potentially reduce their profit margins if they are forced to use alternative, more costly measures to procure feedstock. It is possible that an adequate supply of feedstock may not be available for the customer processors to meet daily processing capacity. This could have a materially adverse effect on our customer’s financial condition and operating results.

| 18 |

Our P2O financial results will also be dependent on the operating costs of our processors, including costs for feedstock and the prices at which we are able to sell our end products. Volatility in both the pricing of feedstock as well as the market price for fuels could have an impact on this relationship. General economic, market, and regulatory factors may influence the availability and potential cost of waste plastic. These factors include the availability and abundance of waste plastic, government policies and subsidies with respect to waste management and international trade and global supply and demand. The significance and relative impact of these factors on the availability of plastic is difficult to predict.

We will, for the very near future, depend on one production facility for revenues related to our business. Therefore, any operational disruption could result in a reduction of our fuel production volumes.

A significant portion of our anticipated revenue for fiscal 2016 will be derived from processor sales, as well as from the sale of fuel that we produce at our Niagara Falls, NY Facility. We will incur additional expenses to increase production at that facility and any failure to produce fuel at anticipated volumes and costs would adversely affect our revenues, free cash flow and potential ability to build other planned production facilities. Such failure would adversely affect our business, financial condition and results of operations.

Unforeseen manufacturing issues or processor downtime could have significant adverse impact on our business.

Our business and strategic growth plans rely on assumptions of processor uptime reaching certain levels in which ample fuel can be produced to meet the needs of our customers and provide us with adequate operating cash flow to cover our cost of operating. Unforeseen manufacturing issues with the processors or unscheduled downtime due to mechanical failure, low quality feedstock, severe weather conditions or unexpected issues with the processors could have a material adverse impact on our fuel production and operating results. In addition, manufacturing and/ or fabrication delays with respect to additional processors could cause our revenues and fuel production to be lower than anticipated.

We may have difficulties gaining market acceptance and successfully marketing our processors or fuel to our customers.

A key component of our business strategy is to market our processors and fuel as a viable high quality fuel to wholesalers and industrial end-users. If we fail to successfully market our processors or fuel or the targeted customers do not accept it, our business, financial condition and results of operations will be materially adversely affected.

To gain market acceptance and successfully market our processors and fuel, we must effectively demonstrate the advantages of using P2O fuel over other fuels, including conventional fossil fuels, biofuels and other alternative fuels and blended fuels. We must show that P2O fuel is a direct replacement for fossil fuels. We must also overcome marketing and lobbying efforts by producers of other fuels, many of whom have greater resources than we do. If the markets for our processors and fuel do not develop as we currently anticipate, or if we are unable to penetrate these markets successfully, our revenue and revenue growth rate could be materially and adversely affected.

Pre-existing contractual commitments and skepticism of new production methods for fuels may hinder market acceptance of our processors and fuel.

Adverse public opinions concerning the alternative fuel industry in general could harm our business.

The plastic-to-fuel industry is new, and general public acceptance of this method of recycling and fuel generation is uncertain. Public acceptance of P2O fuel as a reliable, high-quality alternative to traditionally refined petroleum fuels may be limited or slower than anticipated due to several factors, including:

| ● | public perception issues associated with the fact that P2O fuel is produced from waste plastics; |

| ● | public perception that the use of P2O fuel will require excessive burner, boiler or engine modifications; |

| ● | actual or perceived problems with P2O fuel quality or performance; and |

| ● | to the extent that P2O fuel is used in transportation applications, concern that using P2O fuel will void engine warranties. |

| 19 |

Such public perceptions or concerns, whether substantiated or not, may adversely affect the demand for our fuels, which in turn could decrease our sales, harm our business and adversely affect our financial condition.

A decline in the price of petroleum products may reduce demand for our P2O fuels and may otherwise adversely affect our business.

We anticipate that our fuels will be marketed as alternatives to their corresponding conventional petroleum product counterparts, such as heating oil, diesel fuel and naphtha. If the prices of these products fall, we may be unable to produce products that are cost-effective alternatives to conventional petroleum products. Declining oil prices, or the perception of a future decline in oil prices, may adversely affect the prices we can obtain from our potential customers or prevent potential customers from entering into agreements with us to buy our products. During sustained periods of lower oil prices, we may be unable to sell some of our fuel products, which could materially and adversely affect our operating results.

In addition, recent discoveries and drilling of shale gas deposits has caused a general decrease in natural gas prices which could cause commercial and industrial fuel users to switch from using petroleum-based products to natural gas to power their equipment, machinery and operations. In such case, demand for our fuel products may decline. Any decline in demand for petroleum-based products could materially and adversely affect our results from operation.

Our operations are subject to various regulations, and failure to obtain necessary renewed permits, licenses or other approvals, or failure to comply with such regulations, could harm our business, results of operations and financial condition.

We are, and may become subject to, various federal, state, provincial, local and foreign laws, regulations and approval requirements in the United States, Canada and other jurisdictions, including those relating to the discharge of materials or pollutants into the air, water and ground, the generation, storage, handling, use, transportation and disposal of waste materials, and the health and safety of our employees.

The Company currently possesses an Air Permit and Solid Waste Permit for up to three processors at the Niagara Falls, NY facility. Failure to maintain these permits on terms and conditions acceptable to and achievable by us, or at all, could affect the commercial viability of the Niagara Falls, NY facility, which could have a material adverse effect on our business, financial condition and results of operations.

As we implement our growth strategy, our planned P2O business will require additional permits, licenses or other approvals from various governmental authorities. Our ability to obtain, amend, comply with, sustain or renew such permits, licenses or other approvals on acceptable, commercially viable terms may change, as could the regulations and policies of applicable governmental authorities. Our inability to obtain, amend, comply with, sustain or renew such permits, licenses or other approvals may have a material adverse effect on our business, financial condition and results of operations.

Any fuels developed using our P2O process will be required to meet applicable government regulations and standards. Any failure to meet these standards and/or future regulations and standards could prevent or delay the commercialization or sale of any fuels developed using our P2O process or subject us to fines and other penalties.

All phases of designing, constructing and operating fuel production facilities present environmental risks and hazards. Among other things, environmental legislation provides for restrictions and prohibitions on spills and discharges, as well as emissions of various substances produced in association with fuel operations. Legislation also requires that sites be operated, maintained, abandoned and reclaimed in such a way that would satisfy applicable regulatory authorities. Compliance with such legislation can require significant expenditures and a breach may result in the imposition of fines and penalties, some of which may be material. Environmental legislation is evolving in a manner that may result in stricter standards and enforcement, larger fines, penalties and liability, as well as potentially increased capital expenditures and operating costs. The discharge of pollutants into the air, soil or water may give rise to liabilities to governments and third parties, and may require us to incur costs to remedy such discharge.

| 20 |

There is no assurance that our operations will comply with environmental or occupational, safety and health regulations in any applicable jurisdiction. Failure to comply with applicable laws, regulations and approval requirements could subject us to civil and criminal penalties, require us to forfeit property rights, and may affect the value of our assets or our ability to conduct our business. We may also be required to take corrective actions, including, but not limited to, installing additional equipment, which could require us to make substantial capital expenditures. These penalties could have a material adverse effect on our business, financial condition and results of operations.

We may be unable to produce our fuel products in accordance with governmental specifications.

Even if we produce P2O fuel at our targeted volumes and yields, we may be unable to produce fuel that meets future governmental regulations. If we fail to meet these specific regulations customers may not purchase our fuel or, to the extent we have an agreement in place for the supply of fuel, the customer may seek an alternate supply of fuel or terminate the agreement completely. A failure to successfully meet these specifications could decrease demand for our fuel, leading to reduced sales and operating results.

Our dependence on contract manufacturers for processor components exposes our business to supply risks.

We have limited internal capacity to manufacture our processor components. As a result, we are heavily dependent upon the performance and capacity of third party manufacturers for the manufacturing of many of the key components of our processors, including kilns and distillation towers as well as certain other key components that require specialized machining and fabrication.

We are working to establish long-term supply contracts with contract manufacturers. However, we cannot guarantee that we will be able to enter into long-term supply contracts on commercially reasonable terms, or at all, or to acquire, develop or contract for internal manufacturing capabilities. Any resources we expend on acquiring or building internal manufacturing capabilities could be at the expense of other potentially more profitable opportunities.

We currently have only patent-pending protection for our P2O process and processor.

We have sought patent protection of our intellectual property by filing for international patents via the Patent Cooperation Treaty, however, as yet, none have been granted. We also rely on trade secrets to provide protection for our proprietary catalyst. We currently have patent pending status for our P2O process and processor. However, a lack of patent protection could have a material adverse effect on our ability to gain a competitive advantage for our P2O processors, since it is possible that our competitors may be able to duplicate our P2O process for their own purposes. This may have a material adverse effect on our results of operations, including on our ability to enter into industrial partnership arrangements or other agreements relating to our P2O processors.

We rely in part on trade secrets to protect some of our intellectual property, and our failure to obtain or maintain trade secret protection could adversely affect our competitive position.