UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

(Mark One)

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2015

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ________________ to ___________________

OR

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

Date of event requiring this shell company report _______________

Commission file number: 001-33176

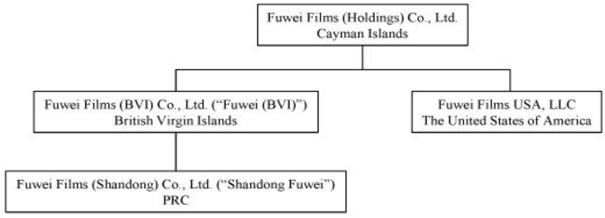

Fuwei Films (Holdings) Co., Ltd.

(Exact name of Registrant as specified in its charter)

____________________________________________________________

(Translation of Registrant’s name into English)

Cayman Islands

(Jurisdiction of incorporation or organization)

No. 387 Dongming Road

Weifang Shandong

People’s Republic of China, Postal Code: 261061

(Address of principal executive offices)

Yong Jiang

Tel: +86 133 615 59266

fuweiir@fuweifilms.com

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Title of each class | Name of each exchange on which registered |

| Ordinary Shares | NASDAQ Capital Market |

Securities registered or to be registered pursuant to Section 12(g) of the Act. None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act. None

As of December 31, 2015, there were 13,062,500 ordinary shares outstanding.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

¨ Yes x No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

¨ Yes x No

Note - Checking the box will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

x Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ¨ Accelerated filer ¨ Non-accelerated filer x

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

|

U.S. GAAP |

x |

International Financial Reporting Standards as issued by the International Accounting Standards Board |

¨ |

Other |

o |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow:

¨ Item 17 ¨ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

¨ Yes x No

TABLE OF CONTENTS

2

| Item 16 | [Reserved] | 72 |

| Item 16A | Audit Committee Financial Expert | 72 |

| Item 16B | Code of Ethics | 72 |

| Item 16C | Principal Accountant Fees and Services | 72 |

| Item 16D | Exemptions from the Listing Standards for Audit Committee | 72 |

| Item 16E | Purchase of Equity Securities by the Issuer and Affiliated Purchaser | 72 |

| Item 16F | Changes in Registrant’s Certifying Accountants | 72 |

| Item 16G | Significant Differences in Corporate Governance Practices | 73 |

| Item 16H | Mine Safety Disclosure | 73 |

| PART III | ||

| Item 17 | Financial Statements | 73 |

| Item 18 | Financial Statements | 73 |

| Item 19 | Exhibits | 74 |

3

SPECIAL NOTE ON FORWARD-LOOKING STATEMENTS

This Annual Report contains many statements that are “forward-looking” and uses forward-looking terminology such as “anticipate,” “believe,” “expect,” “estimate,” “future,” “intend,” “may,” “ought to,” “plan,” “should,” “will,” negatives of such terms or other similar statements. You should not place undue reliance on any forward-looking statement due to its inherent risk and uncertainties, both general and specific. Although we believe the assumptions on which the forward-looking statements are based are reasonable and within the bounds of our knowledge of our business and operations as of the date of this annual report, any or all of those assumptions could prove to be inaccurate. As a result, the forward-looking statements based on those assumptions could also be incorrect. The forward-looking statements in this Annual Report include, without limitation, statements relating to:

| ● | our goals and strategies; |

| ● | our future business development, results of operations and financial condition; |

| ● | our ability to protect our intellectual property rights; |

| ● | expected growth of and changes in the PRC BOPET film industry and in the demand for BOPET film products; |

| ● | projected revenues, profits, earnings and other estimated financial information; |

| ● | our ability to maintain and strengthen our position as a leading provider of BOPET film products in China; |

| ● | our ability to maintain strong relationships with our customers and suppliers; |

| ● | our planned use of proceeds; |

| ● | effect of competition in China and demand for and price of our products and services; and |

| ● | PRC governmental policies regarding our industry. |

The forward-looking statements included in this Annual Report are subject to risks, uncertainties and assumptions about our businesses and business environments. These statements reflect our current views with respect to future events and are not a guarantee of our future performance. Actual results of our operations may differ materially from information contained in the forward-looking statements as a result of risk factors some of which are described under “Risk Factors” and elsewhere in this Annual Report. Risks, uncertainties and assumptions include, among other things:

| ● | competition in the BOPET film industry; |

| ● | growth of, and risks inherent in, the BOPET film industry in China; |

| ● | unpredictable impact on the company’s revenue by price movements of crude oil in recent years; |

| ● | uncertainty in our export due to trade protectionism around the world; |

| ● | uncertainty as to future profitability and our ability to obtain adequate financing for our planned capital expenditure requirements; |

| ● | uncertainty in our ability to develop and manufacture high value-added products for the new production line (thick film) to win in the competition; |

| ● | uncertainty as to our ability to continuously develop new BOPET film products and keep up with changes in BOPET film technology; |

| ● | risks associated with possible defects and errors in our products; |

| ● | uncertainty as to our ability to protect and enforce our intellectual property rights; |

| ● | uncertainty as to our ability to attract and retain qualified executives and personnel; |

| ● | uncertainty as to our ability to attract and retain experienced financial reporting staff familiar with U.S. GAAP; |

| ● | uncertainty in acquiring raw materials on time and on acceptable terms; |

| ● | adverse effect on our business caused by adjustment of economic structure regulations of the Chinese government; |

| ● | adverse effect on our business caused by the uncertainty in economic recovery of major developed countries; and |

| ● | adverse effect on our business caused by extreme climate changes. |

These risks, uncertainties and assumptions are not exhaustive. Other sections of this Annual Report include additional factors which could adversely impact our business and financial performance. The forward-looking statements contained in this Annual Report speak only as of the date of this annual report or, if obtained from third-party studies or reports, the date of the corresponding study or report, and are expressly qualified in their entirety by the cautionary statements in this Annual Report. Since we operate in an emerging and evolving environment and new risk factors and uncertainties emerge from time to time, you should not rely upon forward-looking statements as predictions of future events. Except as otherwise required by the securities laws of the United States, we undertake no obligation to update or revise any forward-looking statements to reflect events or circumstances after the date of this Annual Report or to reflect the occurrence of unanticipated events.

4

This annual report on Form 20-F includes our audited consolidated financial statements as of December 31, 2015 and 2014 and for the years ended December 31, 2015, 2014 and 2013.

Our ordinary shares are listed on the Nasdaq Capital Market, or NASDAQ, under the symbol “FFHL”.

Except as otherwise required and for purposes of this Annual Report only:

| · | “Fuwei”, “Company”, “us”, “our” or “we” refer to Fuwei Films (Holdings) Co., Ltd. The term “you” refers to holders of our ordinary shares. |

| · | “China” or “PRC” and the “Chinese government” refer to the People’s Republic of China and its government. |

| · | All references to “Renminbi,” or “RMB” are to the legal currency of China, all references to “U.S. dollars,” “dollars,” “$” or “US$” are to the legal currency of the United States and all references to “Hong Kong dollars” or “HK$” are to the legal currency of Hong Kong. Any discrepancies in any table between totals and sums of the amounts listed are due to rounding. |

| · | “BOPET” refers to the Biaxially Oriented Polyester Film. |

We publish our financial statements in Chinese Yuan (“Renminbi” or “RMB”). In this annual report on Form 20-F, references to “U.S. dollars” or “$” are to the currency of the United States and references to “RMB” are to the currency of China.

Solely for your convenience, certain RMB amounts in this annual report have been translated into U.S. dollars. The rate of translation is based on the noon buying rate for Chinese Yuan in New York City as certified for custom purposes by the Federal Reserve Bank of New York on the various dates specified where the translations are set forth in this annual report. References to the “noon buying rate” in this annual report refer to this rate. These translations should not be taken as assurances that the RMB amounts actually represent these U.S. dollar amounts or that they were or could have been converted in U.S. dollars at the rate indicated or at any other rate. The noon buying rate was US $1.00 = RMB6.4778 on December 31, 2015.

The following table sets forth various information concerning exchange rates between the Renminbi and the U.S. dollar for the periods indicated. These rates are provided solely for your convenience and are not necessarily the exchange rates that we used in this Annual Report or will use in the preparation of our other periodic reports or any other information to be provided to you. The source of these rates is the Federal Reserve Bank of New York.

| Average | High | Low | Period-end | |||||||||||||

| 2010(1) | 6.7788 | 6.8336 | 6.5820 | 6.6118 | ||||||||||||

| 2011(1) | 6.4630 | 6.6364 | 6.2939 | 6.2939 | ||||||||||||

| 2012(1) | 6.3088 | 6.3879 | 6.2221 | 6.2301 | ||||||||||||

| 2013(1) | 6.1478 | 6.2438 | 6.0537 | 6.0537 | ||||||||||||

| 2014(1) | 6.1620 | 6.2591 | 6.0402 | 6.2046 | ||||||||||||

| 2015(1) | 6.2827 | 6.4896 | 6.1870 | 6.4778 | ||||||||||||

| November 2015(2) | 6.3640 | 6.3945 | 6.3180 | 6.3883 | ||||||||||||

| December 2015(2) | 6.4491 | 6.4896 | 6.3883 | 6.4778 | ||||||||||||

| January 2016(2) | 6.5726 | 6.5932 | 6.5219 | 6.5752 | ||||||||||||

| February 2016(2) | 6.5501 | 6.5795 | 6.5154 | 6.5525 | ||||||||||||

| March 2016(2) | 6.5027 | 6.5500 | 6.4480 | 6.4480 | ||||||||||||

| April 2016(2) (3) | 6.4776 | 6.4776 | 6.4776 | 6.4776 | ||||||||||||

| (1) | Annual averages are calculated by averaging the rates on the last business day of each month during the relevant period. |

| (2) | Monthly average is calculated by averaging the daily rates during the relevant period. |

| (3) | As of April 1, 2016, the exchange rate was 6.4776. |

Item 1. Identity of Directors, Senior Management and Advisers

Not applicable.

5

Item 2. Offer Statistics and Expected Timetable

Not applicable.

The following selected financial data should be read in conjunction with Item 5 - the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the Financial Statements and Notes thereto included elsewhere in this Annual Report.

The following selected historical statement of income data for the years ended December 31, 2015, 2014 and 2013 and the selected historical balance sheet data as of December 31, 2015 and 2014 have been derived from the Company’s audited consolidated financial statements included in this Annual Report beginning on page F-1. The following selected historical statement of income data for the years ended December 31, 2012 and 2011, and the selected historical balance sheet data as of December 31, 2013, 2012 and 2011 have been derived from the Company’s audited financial statements not included in this Annual Report. The audited financial statements are prepared and presented in accordance with United States generally accepted accounting principles, or U.S. GAAP.

Certain factors that affect the comparability of the information set forth in the following table are described in the “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and the Financial Statements and related notes thereto included elsewhere in this Annual Report.

| For the year ended December 31, | ||||||||||||||||||||||||

| 2015 | 2014 | 2013 | 2012 | 2011 | ||||||||||||||||||||

| (in thousands, except per share data) | RMB | US$ | RMB | RMB | RMB | RMB | ||||||||||||||||||

| Statement of Operations Data: | ||||||||||||||||||||||||

| Revenues | 248,862 | 38,418 | 284,464 | 304,950 | 372,866 | 537,645 | ||||||||||||||||||

| Gross (loss) profit | (4 | ) | (- | ) | (17,153 | ) | (15,425 | ) | (3,107 | ) | 85,472 | |||||||||||||

| Operating (loss) income | (61,186 | ) | (9,445 | ) | (60,692 | ) | (64,394 | ) | (63,984 | ) | 30,736 | |||||||||||||

| Interest expense | (8,333 | ) | (1,286 | ) | (12,486 | ) | (10,094 | ) | - | (10,227 | ) | |||||||||||||

| (Loss) Income before income taxes | (62,068 | ) | (9,581 | ) | (72,084 | ) | (68,959 | ) | (62,164 | ) | 24,993 | |||||||||||||

| Net (loss) income attributable to the Company | (69,065 | ) | (10,662 | ) | (71,327 | ) | (58,971 | ) | (54,427 | ) | 21,081 | |||||||||||||

| (Loss) Earnings per share | ||||||||||||||||||||||||

| Basic | (5.29 | ) | (0.82 | ) | (5.46 | ) | (4.51 | ) | (4.17 | ) | 1.61 | |||||||||||||

| Diluted | (5.29 | ) | (0.82 | ) | (5.46 | ) | (4.51 | ) | (4.17 | ) | 1.61 | |||||||||||||

| Weighted average number ordinary shares, Basic and diluted | ||||||||||||||||||||||||

| Basic | 13,062,500 | 13,062,500 | 13,062,500 | 13,062,500 | 13,062,500 | 13,062,500 | ||||||||||||||||||

| Diluted | 13,062,500 | 13,062,500 | 13,062,500 | 13,062,500 | 13,062,500 | 13,062,500 | ||||||||||||||||||

6

| Year Ended | ||||||||||||||||||||||||

| December 31, | ||||||||||||||||||||||||

| 2015 | 2014 | 2013 | 2012 | 2011 | ||||||||||||||||||||

| (in thousands) | RMB | US$ | RMB | RMB | RMB | RMB | ||||||||||||||||||

| Balance Sheet Data: | ||||||||||||||||||||||||

| Cash and cash equivalents | 14,355 | 2,216 | 9,020 | 11,578 | 5,006 | 44,172 | ||||||||||||||||||

| Accounts and bills receivable, net | 10,046 | 1,551 | 9,867 | 8,373 | 21,587 | 52,457 | ||||||||||||||||||

| Inventories | 29,574 | 4,565 | 24,034 | 38,454 | 34,291 | 41,774 | ||||||||||||||||||

| Total current assets | 124,602 | 19,235 | 120,084 | 134,613 | 123,915 | 281,904 | ||||||||||||||||||

| Property, plant and equipment, net | 431,021 | 66,538 | 482,534 | 524,777 | 233,335 | 277,119 | ||||||||||||||||||

| Total assets | 603,771 | 93,206 | 672,945 | 732,047 | 747,550 | 790,174 | ||||||||||||||||||

| Short-term bank loans | - | - | - | 105,000 | 110,000 | 168,501 | ||||||||||||||||||

| Total current liabilities | 276,201 | 42,638 | 272,057 | 250,200 | 201,922 | 205,492 | ||||||||||||||||||

| Total shareholders’ equity | 319,698 | 49,353 | 388,913 | 460,307 | 519,234 | 573,669 | ||||||||||||||||||

Shandong Fuwei was entitled to preferential tax treatment at an EIT rate of 15% for the years ended December 31, 2011, 2012 and 2013 due to its status as a High-and-New Tech Enterprise since December 2009. In 2014, Shandong Fuwei failed to be designated as such and it became subject to a standard enterprise income tax at a rate of 25% in 2014 and 2015. Net income and basic and diluted earnings per share would be reduced by the following amounts, if Shandong Fuwei was not entitled to a reduced EIT rate for the years 2013, 2012 and 2011:

| Year Ended December 31, | ||||||||||||||||

| (In thousands, except per share | 2013 | 2012 | 2011 | |||||||||||||

| data) | RMB | US$ | RMB | RMB | ||||||||||||

| Net income | - | - | - | (2,499 | ) | |||||||||||

| Earnings per share | ||||||||||||||||

| - basic | - | - | - | (0.19 | ) | |||||||||||

| - diluted | - | - | - | (0.19 | ) | |||||||||||

The 2015 RMB amounts included in the above selected financial data have been translated into U.S. dollars at the rate of US $1.00 = RMB6.4778, which was the noon buying rate for U.S. dollars in effect on December 31, 2015 in the City of New York for cable transfer in RMB per U.S. dollar as certified for custom purposes by the Federal Reserve Bank. No representation is made that the RMB amounts could have been, or could be, converted into U.S. dollars at that rate or at any other certain rate on December 31, 2015, or on any other date.

Exchange Rate Information

On July 21, 2005 the Chinese government changed its policy of pegging the value of the Renminbi to the U.S. dollar. This revaluation of the Renminbi was based on a conversion of Renminbi into United States dollars at an exchange rate of US$1.00=RMB8.11. Under the new policy, the Renminbi will be permitted to fluctuate within a band against a basket of certain foreign currencies. On December 31, 2015, this change in policy resulted in an approximately 20.1% appreciation in the value of the Renminbi against the U.S. dollar compared to 2005. The Company generates its revenue in the PRC in Renminbi and its overseas sales and U.S. dollars cash deposits are subject to foreign currency translations which will impact net income (loss).

B. Capitalization and indebtedness.

Not applicable.

C. Reasons for the offer and use of proceeds.

Not applicable.

The following matters and other additional risks not presently known to us or that we deem immaterial, may have a material adverse effect on our business, financial condition, liquidity, results of operations or prospects or otherwise. Reference to a cautionary statement in the context of a forward-looking statement or statements shall be deemed to be a statement that any one or more of the following factors may cause actual results to differ materially from those in such forward-looking statement or statements.

7

| (a) | Risks Associated with Our Business |

Our business may be adversely affected by the exchange rate fluctuation of RMB against the U.S. dollar and trade protection measures in place by several countries against exports of BOPET films from China.

Our business operation may be adversely affected due to appreciation of RMB against the U.S. dollar, and more stringent trade protection measures in place such as antidumping investigations conducted by several countries against exports of BOPET films originated from China.

A sharp fluctuation in the demand for raw materials may have a negative impact on our operations if we are unable to pass on all increases in cost of raw materials to our customers on a timely basis.

The total cost of raw materials made up approximately 66.4%, 67.8% and 71.4% of our production cost in 2015, 2014 and 2013, respectively. The main raw materials used in our production of BOPET film are polyethylene terephthalate (or PET) resin and additives, which respectively made up approximately 82.2% and 17.8% of our total cost of raw materials in the past three years on average.

The prices of PET resin and additives are, to a certain extent, affected by the price movement of crude oil. Currently the PET resin is mainly used as a raw material in China’s textile industry. Therefore, the market prices of PET resin will fluctuate due to changes in supply and demand conditions in that industry. Any sudden shortage of supply or significant increase in demand of PET resin and additives may result in higher market prices and thereby increase our cost of sales.

In 2016, it is expected that there will be a continued capacity expansion within China. The further growing oversupply plus price fluctuations of raw materials may continuously have an adverse impact on the results of our operations. Currently, we have no hedging transactions in place with respect to PET resin or any other petroleum product.

Rising Competition caused by soaring capacity of BOPET films may materially affect our operations and financial conditions.

We operate in a highly competitive and rapidly evolving field, and new developments are expected to continue at a rapid pace. Competitors may succeed by expanding their capacity or succeed in developing products that are more efficient, easier to use or less expensive than those which have been or are being developed by us or that would render our technology and products obsolete and non-competitive. Any of these actions by our competitors could adversely affect our sales.

In addition, several companies are developing similar and substitute products to address the same packaging field that we are targeting. These competitors may have greater financial and technical resources, productivity, marketing capabilities and facilities, cost-efficiency and human resources, or they may have a better quality of products, service, and shorter lead time. The competition from these competitors may adversely affect our business.

An increase in competition could result in slow increase in demand, selling price reductions or loss of our market share, which could have an adverse material impact on our operations and financial condition, or result in substantial losses to the Company.

The existing manufacturers and new entrants have been expanding their production capacity of the BOPET films since the second half of 2010, which have resulted in substantial increase in production of BOPET films from 2011 to 2015. As a result, the market supply in 2016 will continuously increase more than demand. This will have an adverse impact on our sales and operation. In the event that we are unable to compete successfully or retain effective control over the pricing of our products, our profit margins might decrease.

In addition, China has gradually lowered import tariffs after its entry into the World Trade Organization in December 2001. Aiming at the huge market for high value-added films in China, manufacturers from developed countries, including Japan and South Korea started investing in China and some of these facilities had been put into production. This may lead to increased competition from foreign companies in our industry, some of which are significantly larger and financially stronger than us. If we fail to compete effectively with these companies in the future, our current business and future growth potential would be adversely affected.

We may be subject to inventory risks that would negatively impact our operating results.

The possible price decline of our inventory may adversely affect the Company’s operation. The fluctuation of the market prices of our raw material inventory and end product inventory will also adversely affect the value of our inventory.

A significant portion of our revenue is derived from the flexible packaging industry in the PRC; our revenue might be adversely impacted if the flexible packaging industry is adversely affected.

A significant portion of our revenue is currently derived from the production and sale of BOPET films. Our BOPET films are mainly used in the flexible packaging industry for consumer products such as tobacco packaging, alcoholic beverages, food, cosmetics and so on. The demand for our BOPET films is therefore affected by the demand for flexible packaging.

8

Since the second half of 2011, the sales and prices of our products has been declining significantly as a result of increased supply over demand in China and declined demand from overseas markets. If such situation continues in the future, such as the continued slowdown of the market demand or the increase of the demand continues to be less than that of the supply, it could continue to have an adverse impact on our financial condition and operation of our business.

We rely on key managerial and technical personnel and failure to attract or retain such personnel may compromise our ability to perform our strategies and then to develop new products and to effectively carry on our research and development and other efforts.

Our success to date has been largely attributable to the contributions of key management and experienced personnel, with whom we have entered into service agreements. The loss of their services might impede the achievements of our strategies and development objectives and might damage the close business relationship we currently enjoy with some of our major customers. Our continued success is dependent, to a large extent, on our ability to attract or retain the services of these key personnel. Our future success will also depend on our continued ability to attract and retain highly motivated and qualified personnel. The rapid growth of the economy in China has caused intense competition to attract and retain qualified personnel. Considering the deficiency in the legal environment in China, we cannot assure you that we will be able to retain our key personnel or that we will be able to attract, train or retain qualified personnel in the future.

If our R & D team cannot effectively develop new products, or promote the market process, or we are unable to afford to continue to maintain this team or are not able to hire eligible and talented personnel, our ability to conduct research and development, and our operation results and market competitiveness may be adversely affected.

Marketability of any of our new products is uncertain and low acceptance levels of any of our new products will adversely affect our revenue and profitability.

The development of our products is based on complex technology, and requires significant time and expertise in order to meet industry standards and customers’ specifications. Although we have developed some products that meet customers’ requirements in the past, there is no assurance that any of our research and development efforts will necessarily lead to any new or enhanced products or generate expected market share to justify commercialization. We must continually improve our current products and develop competitive new products to address the requirements of our customers. If our new products are unable to gain market acceptance, we would not be able to generate future revenue from our investment in research and development. In such event, we would be unable to increase our market share and achieve and sustain profitability. Our failure to further refine our technology and develop and introduce new products attractive to the market could cause our products to become uncompetitive or obsolete, which could reduce our market share and cause our sales to decline.

It is difficult to anticipate whether and when our new production line can develop and manufacture high value-added films; this may have an adverse impact on us and we may not be able to reduce our losses.

The total investment in our new production line was approximately US$51 million. We have commenced the R & D of the high value-added products (such as films for TFT-LCD screens) to be manufactured by this line, however, we are uncertain as to whether the products can be developed as scheduled or recognized by customers.

The new production line has been approved to produce common thick films ranging from thickness of 38μm to 250μm, however, it is difficult to anticipate when the new production line can develop high-value-added films.

In addition, the sales prices of our commodity thick films are far less than our costs due to more supply than demand in such a tough market. As a result, the new production line may not be profitable in the short term and may be faced with more losses.

The circumstances under which we acquired ownership of our main productive assets may jeopardize our ability to continue as an operating business.

On September 24, 2004, the People’s Court of Weifang declared Shandong Neo-Luck bankrupt due to its financial difficulties. Shandong Neo-Luck pledged its main assets for the operation of the DMT production line to Weifang Commercial Bank before its bankruptcy.

The pledged DMT production line was auctioned on October 22, 2004 by the Shandong Neo-Luck Clearance Committee. DMT subsequently sought monetary damages from Shandong Neo-Luck for approximately US $1.25 million plus interest relating to a claim of partial non-payment for the DMT production line by way of application of the ICC arbitration and the hearing was held in Geneva in November 2007. Fuwei Shandong joined these discussions later as an interested party and in order to support a resolution of the pending dispute and to achieve resolution of certain outstanding service and spare part issues. All parties entered into a Settlement Agreement in March 2008 and the arbitration was withdrawn by the ICC. Under the Service Agreement entered into in connection with the Settlement Agreement, Shandong Fuwei would pay an amount of US$180,000 in two installments with respect to service and spare parts. The Company made its first payment in April 2008. As of December 31, 2015, Shandong Fuwei had paid US$135,000 and still has US$45,000 left unpaid.

9

Under the Settlement Agreement, the Neoluck Group was obligated to pay an amount equal to US$900,000 in RMB by delivery of a bank draft to DMT. In April 2008, the Neoluck Group had not performed its obligation under the Settlement Agreement, and, the Neoluck Group and DMT entered into a Supplemental Agreement pursuant to which the Neoluck Group would pay the amount owed to DMT in two installments. The Neoluck Group paid the first installment equal to US$ 450,000 in April 2008. As agreed between Neoluck Group and DMT, the remaining US$450,000 was to be paid in installments by the end of December 2008. As of December 31, 2015, Neoluck Group had paid US$ 320,000 and still had US$130,000 outstanding to DMT.

Substantially all of our operating assets were acquired through two auction proceedings under relevant PRC law. We acquired the Brückner production line in 2003 as a result of a foreclosure proceeding enforcing an effective court judgment and the DMT production in 2004 as a result of a commercial auction from a consigner who obtained such assets through a bankruptcy proceeding. In the opinion of our PRC counsel, Concord & Partners, these proceedings are both valid under Chinese auction and bankruptcy law based on certain factual assumptions. Our PRC counsel’s opinion solely relates to the legal procedure of the auctions and is based upon certain factual assumptions, our written representations and written reports of the auction company and other related parties. There can be no assurance that relevant authorities or creditors of the predecessor owner of these assets will not challenge the effectiveness of these asset transfers based upon the facts and circumstances of these transfers, despite the existence of independent appraisals, and other facts and circumstances of the auctions that cannot be verified by our PRC counsel. Taking into consideration the facts known by our PRC counsel related to the auction of the Brückner production line and the significant difference in the price paid for the DMT production line at the two bankruptcy auctions involved in our purchase of that asset and, assuming the representations and reports received by our PRC counsel are true and correct in all material respects, our PRC counsel is of the opinion that the auctions of the Brückner and DMT production lines were valid under PRC law and the possibility of the creditors of Shandong Neo-Luck successfully exercising recourse or claiming repayment with respect to our assets purchased in the bankruptcy proceeding should be remote. However, should any such challenge be brought in China (or elsewhere) and prevail, we may incur substantial liabilities and be required to pay substantial damages as a result of acquiring these assets and this could materially affect our ability to continue our operation.

We have, in the past, experienced and may, from time to time, experience negative working capital. We also face risks associated with debt financing (including exposure to variation in interest rates).

As of December 31, 2015, we had a long-term loan of RMB6.65 million (US$1.026 million). We have pledged part of our property, plant and lease prepayments as security for indebtedness of a credit line amounting to RMB45.0 million (US$6.95 million) granted by SPD bank. In the event that we default on all expired indebtedness, our lenders could foreclose on our assets. In the event that our assets are foreclosed upon, we will not be able to continue to operate our business.

Our obligations under our existing loans have been mainly met through the cash flow from our operations and our financing activities. We are subject to risks normally associated with debt financing, including the risk of significant increases in interest rates and the risk that our cash flow will be insufficient to meet required payment of principal and interest. We may also underestimate our capital requirements and other expenditures or overestimate our future cash flows. In such event, we may consider additional bank loans, issuing bonds, or other forms of financing to satisfy our capital requirements. If any of the aforesaid events occur and we are unable for any reason to raise additional capital, debt or other financing to meet our working capital requirements, our business, operating results, liquidity and financial position will be adversely affected. In addition, if we do not obtain financing or have negative working capital, there is a possibility that we may not be able to perform our contracts with our suppliers as a result of our inability to pay them back. The foregoing factors may have an adverse effect on our operation.

We may lose our competitive advantage and our operations may suffer if we fail to prevent the loss or misappropriation of, or disputes over, our intellectual property.

As of December 31, 2015, we have received 19 patents from the PRC authorities. All these patents are related to our products and production processes. We may not be able to successfully obtain the approvals of the PRC authorities for the pending patent applications. In addition to the patents, proprietary techniques including processes, ingredients and technologies are important to our business as they enable us to maintain our competitive advantage over our competitors. Furthermore, third parties may assert claims to our proprietary processes, ingredients and technologies.

Our ability to compete in our markets and to achieve future revenue growth will depend, in significant measure, on our ability to protect our proprietary technology and operate without infringing upon the intellectual property rights of others. The legal regime in China for the protection of intellectual property rights is still at its early stage of development. Intellectual property protection became a national effort in China in 1979 when China adopted its first statute on the protection of trademarks. Since then, China has adopted its Patent Law, Trademark Law and Copyright Law and promulgated related regulations, such as the Regulation on Computer Software Protection, Regulation on the Protection of Layout Designs of Integrated Circuits and Regulation on Internet Domain Names. China has also acceded to various international treaties and conventions in this area, such as the Paris Convention for the Protection of Industrial Property, Patent Cooperation Treaty, Madrid Agreement and its Protocol Concerning the International Registration of Marks. In addition, when China became a party to the World Trade Organization in 2001, China amended many of its laws and regulations to comply with the Agreement on Trade-Related Aspects of Intellectual Property Rights. Despite many laws and regulations promulgated and other efforts made by China over the years with a view to tightening up its regulation and protection of intellectual property rights, the enforcement of such laws and regulations in China has not achieved the level in developed countries. Both the administrative agencies and the court system in China are not well-equipped to deal with violations or handle the nuances and complexities between compliant technological innovation and non-compliant infringement.

10

We rely on trade secrets and registered patents and trademarks to protect our intellectual property. We have also entered into confidentiality agreements with our management and employees relating to our confidential proprietary information. However, the protection of our intellectual properties may be compromised as a result of:

| ● | departure of any of our management member(s) or employee(s) in possession of our confidential proprietary information; |

| ● | breach by such resigned management member(s) or employee(s) of his or her confidentiality and non-disclosure undertaking to us; |

| ● | expiration of the protection period of our registered patents or trademarks; |

| ● | infringement by others of our proprietary technology and intellectual property rights; or |

| ● | refusal by relevant regulatory authorities to approve our patent or trademark applications. |

Any of these events or occurrences may reduce or eliminate any competitive advantage we have developed, causing us to lose sales or otherwise harm our business. There is no assurance that the measures that we have put into place to protect our intellectual property rights will be sufficient. As the number of patents, trademarks, copyrights and other intellectual property rights in our industry increases, and as the coverage of these rights and the functionality of the products in the market further overlaps, we believe that business entities in our industry may face more frequent infringement claims. Litigation to enforce our intellectual property rights could result in substantial costs and may not be successful. If we are not able to successfully defend our intellectual property rights, we might lose the rights to technology that we need to conduct and develop our business. This may seriously harm our business, operating results and financial condition, and enable our competitors to use our intellectual property to compete against us.

Furthermore, if third parties claim that our products infringe their patents or other intellectual property rights, we might be required to devote substantial resources to defend against such claims. If we fail to defend against such infringement claims, we may be required to pay damages, modify our products or suspend the production and sale of such products. We cannot guarantee that we will be able to modify our products on commercially reasonable terms.

We may incur capital expenditures in the future in connection with our growth plans and therefore may require additional financing.

To expand our business, we will need to increase our products mix and capacity, which will require substantial capital expenditures especially enough working capital for the continued operation of our new production line. Such expenditures are likely to be incurred in advance of any increase in sales. We cannot assure you that our revenue will increase after such capital expenditures are incurred. Any failure to increase our revenue after incurring capital expenditures to expand production capacity will reduce our profitability.

In addition, we may need to obtain additional debt or equity financing to fund our capital expenditures. Additional equity financing may result in dilution to existing shareholders’ return. Additional debt financing may be required which, if obtained, may:

| ● | limit our ability to pay dividends or require us to seek consents for the payment of dividends; |

| ● | increase our vulnerability to general adverse economic and industry conditions; |

| ● | limit our ability to pursue our growth plan; |

| ● | require us to dedicate a substantial portion of our cash flow from operations to payment for our debt, thereby reducing availability of our cash flow to fund capital expenditures, working capital and other general corporate purposes; |

| ● | limit our flexibility in planning for, or reacting to, changes in our business and our industry; and/or |

| ● | not assure that we will be able to obtain the additional financing on terms that are acceptable to us, if at all. |

A disruption in the supply of utilities, or fire or other calamity at our manufacturing plant would disrupt production of our products and adversely affect our sales.

Our BOPET films are manufactured solely at our production facilities located in Weifang City in the PRC. Any disruption in the supply of utilities, in particular, electricity, water or gas supply or any outbreak of fire, flood or other calamity resulting in significant damage at our facilities would severely affect our production of BOPET film and, as a result, we could incur substantial loss of equipment and properties.

While we maintain insurance policies covering losses in respect of damage to our properties, machinery and inventories of raw materials and products, we cannot assure you that our insurance would be sufficient to cover all of our potential losses.

11

We have limited experience in operating outside mainland China, and failure to achieve our overseas expansion strategy may have an adverse effect on our business growth in the future.

Our future growth depends, to a considerable extent, on our ability to develop both the domestic and overseas markets. We are currently exploring new business opportunities outside mainland China for our BOPET film products. Our primary overseas customers are from Europe, Asia and North America. However, we have limited experience in operating outside mainland China, and limited experience with foreign regulatory environments and market practices. As a result, we cannot guarantee that we will be able to penetrate any overseas market. Failure in the development of overseas market may have an adverse effect on our business growth in the future.

We have encountered anti-dumping investigations in South Korea and the United States, and our overseas expansion strategy in our future business growth may be adversely affected.

Since 2007, the manufacturers in China, India and other countries have encountered anti-dumping investigations conducted by South Korea and the United States.

The Korean Trading Committee (KTC) announced the final results for anti-dumping investigations for enterprises in China and India on August 27, 2008. We finally received the anti-dumping duties (ADD) rate of 5.67% which is much lower than the average rate of 23.60% for other enterprises in China. On June 22, 2011, Ministry of Strategy and Finance, Republic of Korea, initiated a sunset review concerning the continued imposition of an anti-dumping duty on imports of the BOPET Films originating from China and India. The rate for Shandong Fuwei, the subsidiary of Fuwei Films was set at 11.72%, higher than one of its counterparts at 5.87%. Punitive duties of 25.32% will be imposed on the PET films manufactured by six Chinese firms. The rate for the remaining Chinese manufacturers was set at 23.61%. The anti-dumping duties imposed on the Company’s exported biaxially oriented polyethylene-terephthalate (BOPET) films to South Korea will be extended for three more years beginning on May 25, 2012.

On January 15, 2015, the Ministry of Strategy and Finance, Republic of Korea, initiated a sunset review concerning the continued imposition of an anti-dumping duty on imports of Polyethylene Terephthalate originating from China and India. Eight Chinese exporters, including Fuwei Films, are required to participate in this review. On January 13, 2016, the Ministry of Strategy and Finance announced that the rate for Shandong Fuwei, the subsidiary of Fuwei Films, was set at 12.92% and it will be extended for three more years beginning on January 13, 2016.

The US Department of Commerce conducted the anti-dumping investigation in October 2007 covering exporters in China, Brazil, Thailand and the United Arab Emirates. 41 exporters in China were under investigation. In October 2008, the anti-dumping judgments were announced. Although we received the lowest ADD rate of 3.49% among five exporters that received a duty, our export to the United States, to a certain extent, was still adversely affected by paying the ADD.

On January 23, 2010, the US Department of Commerce (“USDOC”) began a first round annual review of Chinese BOPET exporters. Fuwei received the lowest anti-dumping duty (ADD) rate of 30.91% in this administrative review conducted by the USDOC, while the ADD rate of other four Chinese companies reviewed by the USDOC is more than 36.93%. In accordance with relevant laws and regulations in the US, the ADD rate of final results will retroactively apply to those US companies which imported Chinese-exported BOPET films, including Fuwei Films USA, LLC, during the period of first review, so these US importers are obligated to pay a supplementary antidumping duty at this ADD rate. In March 2011, we submitted comments to the USDOC regarding perceived ministerial errors made in calculating the ADD applicable to us. As a result of a Court challenge brought by Fuwei, in January 2013, the USDOC found that Fuwei did not dump goods in the United States market for the period from November 6, 2008 to October 31, 2009. The USDOC, after recalculating the rate, found that the level of dumping was “de minimis.” A rate which is de minimis is treated by the USDOC as a finding of zero. The final results of the second round annual review were announced in March 2012, according to which, an ADD rate of 8.48% was imposed on Fuwei Films which is slightly higher than the lowest antidumping duty rate of 8.42% of all the Chinese exporters being reviewed.

On December 30, 2011, USDOC commenced its third routine annual review of BOPET films originated from China. In order to gain an opportunity to continue exporting to the United States, Fuwei Films, although not a mandatory respondent, will actively respond to the review to the extent permitted by law and will continue to seek the low rate which should properly apply to its exports to the United States. In June 2013, the final results of the third round annual review were issued and an ADD rate of 12.80% was imposed on Fuwei Films. The preliminary results of the fourth round annual review were announced in December 2013, according to which, an ADD rate of 31.77% was imposed on Fuwei Films. In June 2014, the final results of the fourth round annual review were announced and Fuwei Films was imposed on an ADD rate of 31.24%. There was no export to the United States for the year of 2014. The preliminary results of the fifth round annual review were announced in December 2014, which determined that Fuwei Films did not have any reviewable transactions during the fifth round annual review and no rate was assigned to it. On December 23, 2014, the USDOC initiated the sixth round annual review. In February 2015, Fuwei Films filed a No Shipment Certification with USDOC as the Company had no export to U.S. during the sixth round annual review.

In addition, if other countries or regions, such as the European Union, take trade protection measures against China's BOPET film or downstream industries, our business may be adversely affected.

12

Changes in Applicable PRC Taxes may be adversely affect the Company.

On October 18, 2010, the State Council issued a notice that the city maintenance and construction tax as well as educational surcharges shall be extended from Chinese companies to foreign-funded enterprises and citizens. Beginning December 1, 2010, Interim Regulations on City Maintenance and Construction Tax of the People’s Republic of China and Decision of the State Council on Amending the Interim Provisions on the Collection of Educational Surcharges shall be applicable to foreign-funded enterprises, foreign enterprises and foreign citizens, which mean they will no longer be exempt from such taxes. In accordance with the regulations, since December 1, 2010, our subsidiary - Shandong Fuwei - became a taxpayer of city maintenance and construction tax as well as educational surcharges which shall be based on value-added tax, the consumption tax and business tax which currently stands at 12%. In July 2011, according to the new rules promulgated by the local government in China, Shandong Fuwei shall contribute to a fund for local water conservation projects since July 1, 2011 which is based on the actual value-added tax, consumption tax and business tax with a rate of 1%. In August 2014, the local government promulgated a new regulation that adjusted the standard of urban land use tax, according to which the tax amount for Shandong Fuwei increased from RMB8 per square meter to RMB14 per square meter. The new policy incurs additional tax expense. If the Chinese government changes its tax policies or adds new types of taxes in the future, our business may be adversely affected.

China’s actions to save energy and reduce emissions may adversely affect our business, by subjecting us to significant new costs and restrictions on our operations.

Recently the Chinese government has tightened its control over energy saving and emission reduction. The Chinese government intends to reduce energy consumption for gross domestic products and water consumption for industrial added value. Certain of our manufacturing plants that use significant amounts of energy, including electricity and gas, are likely to be affected by this plan. Therefore, our operation might be influenced by the energy saving and emission reduction measures of the Chinese government. Regulations for restricting greenhouse gas emission may increase the prices of the electricity we purchase, increase costs for our use of natural gas, potentially restrict access to or the use of natural gas, require us to purchase allowances to offset our emissions or result in an overall increase in our costs of raw materials, any of which could increase costs and negatively affect our business operations or financial results.

The current labor law changes in the PRC may have an adverse impact on our business and profitability.

The Company is of the view that the amended Labor Law of the People’s Republic of China (the “PRC”), which took effect on January 1, 2008 and contains certain heightened requirements with respect to employment law, does not constitute a material risk to the Company. The amended Labor Law contains new provisions which protect the interests of the employees, including provisions which stipulate that an employer shall enter into labor contracts with its employees and pay social welfare insurance which may increase our human resources costs. In addition, the amended Labor Law also states that upon expiry of the labor contract, under some circumstances, an employer shall compensate an employee of the employer who does not renew the labor contract, which may increase our operating expenses. However, to the best of the Company’s knowledge, Shandong Fuwei constantly abides by the Labor Law of PRC, as amended, and therefore we does not believe the labor law provisions and any changes will have any material impact on its business or profitability. However, the Labor Law changes in the PRC in the future may have an adverse impact on our business and profitability.

Our primary source of funds for dividends and other distributions from our operating subsidiary in China is subject to various legal and contractual restrictions and uncertainties, and our ability to pay dividends or make other distributions to our shareholders are negatively affected by those restrictions and uncertainties.

We are a holding company established in the Cayman Islands and conduct our core business operations through our principal operating subsidiary, Shandong Fuwei, in China. As a result, our profits available for distribution to our shareholders are dependent on the profits available for distribution from Shandong Fuwei. If Shandong Fuwei incurs debt on its own behalf, the debt instruments may restrict its ability to pay dividends or make other distributions, which in turn would limit our ability to pay dividends of our ordinary shares. Under the current PRC laws, because we are incorporated in the Cayman Islands, our PRC subsidiary, Shandong Fuwei, is regarded as a wholly foreign-owned enterprise in China. For dividends paid by foreign invested enterprises, the PRC laws permit payment of dividends only out of net income as determined in accordance with PRC accounting standards and regulations. Determination of net income under PRC accounting standards and regulations may differ from determination under U.S. GAAP in significant respects, such as the use of different principles for recognition of revenues and expenses. In addition, distribution of additional equity interests by our PRC subsidiary, Shandong Fuwei, to us (which is credited as fully paid through capitalizing its undistributed profits) requires additional approval of the PRC government. Under the PRC laws, Shandong Fuwei, a wholly foreign-owned enterprise, is required to set aside a portion of its net income each year to fund designated statutory reserve funds. These reserves are not distributable as cash dividends. As a result, our primary internal source of funds of dividend payments from Shandong Fuwei is subject to these and other legal and contractual restrictions and uncertainties, which in turn may limit or impair our ability to pay dividends to our shareholders. Moreover, any allotment of funds from us to Shandong Fuwei, either as a shareholder loan or as an increase in registered capital, is subject to registration with or approval by PRC governmental authorities. These limitations on the flow of funds between us and Shandong Fuwei could restrict our ability to act in response to changing market conditions.

13

Investor confidence and the market price of our shares may be adversely impacted if we are unable to issue an unqualified opinion on the adequacy of our internal controls over our financial reporting beginning as of December 31, 2015, as required by Section 404 of the U.S. Sarbanes-Oxley Act of 2002.

As a public company, we are required by section 404 of the Sarbanes-Oxley Act 2002 to include a report by management on our internal controls over financial reporting that contains our management’s assessment of the effectiveness of our internal controls in our annual report on Form 20-F. Based on our evaluation, our principal executive officer and principal financial officer previously concluded as of December 31, 2010, our internal controls over financial reporting were effective as of such date. However, in connection with the review of our Annual Report on Form 20-F by the Securities and Exchange Commission and subsequent reconsideration of the conclusion regarding effectiveness originally expressed therein, our principal executive officer and principal financial officer have now revised their conclusions and believe that as of the Evaluation Date, our internal controls over financial reporting were ineffective as of December 31, 2010 and that such internal controls exhibited a “material weakness,” or a deficiency, or combination of deficiencies, in internal control over financial reporting such that there is a reasonable possibility that a material misstatement of our annual or interim financial statements will not be prevented or detected on a timely basis. The material weaknesses identified resulted from inadequate technical accounting staff with knowledge of and experience with US generally accepted accounting principles, pursuant to which we prepare our consolidated financial statements, to support stand-alone external financial reporting under public company or SEC requirements. The report of management contained in this Annual Report on Form 20-F also reflects the determination of the reviewing officers that as of December 31, 2011, 2012, 2013, 2014 and 2015, we continued to have a material weakness in our internal controls over financial reporting.

We are in the process of developing and implementing a remedial plan to address the deficiencies in the areas of personnel with knowledge of and experience with US generally accepted accounting principles, including recruiting a full-time reporting employee with U.S. GAAP experience and conducting training in U.S. GAAP principles for all the financial reporting staff of the Company. However, additional measures may be necessary, and the measures we expect to take to improve our internal controls may not be sufficient to address the issues identified, to ensure that our internal controls are effective or to ensure that such material weakness or other material weaknesses would not result in a material misstatement of our annual or interim financial statements. In addition, other material weaknesses or significant deficiencies may be identified in the future. If we are unable to correct deficiencies in internal controls in a timely manner, our ability to record, process, summarize and report financial information accurately and within the time periods specified in the rules and forms of the SEC will be adversely affected. This failure could negatively affect the market price and trading liquidity of our common stock, cause investors to lose confidence in our reported financial information, subject us to civil and criminal investigations and penalties, and generally materially and adversely impact our business and financial condition.

| (b) | Risks Relating to Business Operations in China |

Changes in China’s political and economic policies and conditions could cause a substantial decline in the demand for our products and services.

Currently, we derive substantially most of our revenues from mainland China. We anticipate that mainland China will continue to be our primary production and sales base in the near future. In addition, currently, substantially all of our assets are located in China and most of our services are performed in China. In 2015, 2014 and 2013, sales to our customers in the PRC accounted for approximately 78.0%, 84.9% and 86.3%, respectively, of our total revenue. Accordingly, any significant slowdown in the PRC economy or decline in demand for our products from our customers in the PRC will have an adverse effect on our business, financial condition and results of our operations. Furthermore, any unfavorable changes in the social and political conditions of the PRC may also adversely affect our business and operations.

Since the adoption of the “open door policy” in 1978 and the “socialist market economy” in 1992, the PRC government has been reforming and is expected to continue to reform its economic and political systems. Any changes in the political and economic policy of the PRC government may lead to changes in the laws and regulations or the interpretation of the same, as well as changes in the foreign exchange regulations, taxation and import and export restrictions, which may in turn adversely affect our financial performance. While the current policy of the PRC government seems to be one of imposing economic reform policies to encourage foreign investments and greater economic decentralization, there is no assurance that such a policy will continue to prevail in the future. We cannot make any assurances that our operations would not be adversely affected should there be any policy changes.

The financial policies, such as bank reserve ratio and deposit and loan interest rates, are subject to adjustment in accordance with the economic development. These policy changes may adversely affect our business.

A Chinese entity has substantial influence over our company and its interest may not be aligned with the interests of other holders of our ordinary shares.

Hongkong Ruishang International Trade Co., Ltd. (“Hongkong Ruishang”), beneficially owns approximately 52.90% of our outstanding share capital. Hongkong Ruishang has substantial influence over our business, including decisions regarding mergers, consolidations and the sale of all or substantially all of our assets, election of directors and other significant corporate actions. This concentration of ownership may discourage, delay or prevent a change in control of our company, which could deprive our shareholders of an opportunity to receive a premium for their shares as part of a sale of our company and might reduce the price of our ordinary shares. Alternatively, our controlling shareholder may cause a merger, consolidation or change of control transaction even if it is opposed by other shareholders.

14

In addition, Mr. Xiusheng Wang, who is the chairman of the board of directors of Hongkong Ruishang is also the Chairman of the board of directors of Shandong SNTON Group Co., Ltd. (the “SNTON Group”) which has a wholly owned subsidiary, Shandong SNTON Optical Materials Technology Co., Ltd. (“SNTON Optical”), a company in the BOPET industry. Furthermore, Mr. Benjie Dong, who was appointed as our Chief Financial Officer effective April 1, 2016 to fill the vacancy caused by resignation of Mr. Xiuyong Zhang, is also the director and vice president of SNTON Group. Majority of our products, customers and market orientation may be the same as SNTON Optical and as a result, the marketing strategy may conflict with the interests of other holders of our ordinary shares.

The discontinuation of any preferential tax treatments or other incentives currently available to us in the PRC could materially and adversely affect our business, financial condition and results of operations.

Our subsidiary, Shandong Fuwei, was converted into a wholly foreign owned enterprise in January 2005 and could enjoy certain special or preferential tax treatments regarding enterprise income tax in accordance with the “Income Tax Law of the PRC for Enterprises with Foreign Investment and Foreign Enterprises” at that time. Accordingly, at that time, it was entitled to tax concessions whereby the profit for the first two financial years beginning with the first profit-making year (after setting off tax losses carried forward from prior years) was exempt from income tax in the PRC and the profit for each of the subsequent three financial years was taxed at 50% of the prevailing tax rates set by the relevant tax authorities. Shandong Fuwei was designated as a High-and-New Tech Enterprise in December 2008 and was recertified in October 2011 and enjoys a favorable enterprise income tax rate of 15%. If there are any future changes in PRC tax laws, rules and regulations or Shandong Fuwei will not be designated as a High-and-New Tech Enterprise, Shandong Fuwei will no longer enjoy the preferential tax treatment. In December 2014, Shandong Fuwei failed to be designated as a High-and-New Tech Enterprise. As a result, Shandong Fuwei is now subject to a 25% standard enterprise income tax rate since from 2014.

On March 16, 2007, the National People’s Congress of the PRC passed the Enterprise Income Tax Law of the People’s Republic of China, which took effect on January 1, 2008. In accordance with the law, a unified enterprise income tax rate of 25% and unified tax deduction standards were applied equally to both domestic-invested enterprises and foreign-invested enterprises. Enterprises established prior to March 16, 2007 eligible for preferential tax treatment in accordance with the currently prevailing tax laws and administrative regulations would, under the regulations of the State Council, gradually become subject to the new tax rate over a five-year transition period starting from the date of effectiveness of the law. We expect details of the transitional arrangement for the five-year period from January 1, 2008 to December 31, 2012 applicable to enterprises established prior to March 16, 2007, such as Shandong Fuwei, to be set out in more detailed implementing rules to be adopted in the future. In addition, certain qualifying “High Technology Enterprises” may still benefit from a preferential tax rate of 15% under the new tax law if they meet the definition of “Government Advocated High Technology Enterprise” to be set forth in the more detailed implementing rules when they become adopted. Shandong Fuwei was designated as a High-and-New Tech Enterprise in December 2008 and will retain its status as a high-tech enterprise for three years commencing from 2011 enjoying a favorable corporate tax rate during the term from January 1, 2011 to December 31, 2013 pursuant to the income law Enterprise Income Tax Law.

In accordance with a notice issued by the PRC government in October, 2010, since December 1, 2010, Shandong Fuwei, our subsidiary, will become a taxpayer of city maintenance and construction tax as well as educational surcharges which shall be based on value-added tax, the consumption tax and business tax which currently stand at 12%. In July 2011, according to the new rules promulgated by the local government in China, Shandong Fuwei shall contribute to a fund for local water conservation projects since July 1, 2011 which is based on the actual value-added tax, consumption tax and business tax with a rate of 1%. The policy changes may have an adverse impact on our net profit.

We are subject to environmental laws and regulations in the PRC.

We are subject to environmental laws and regulations in the PRC. Any failure by us to comply fully with such laws and regulations will result in us being subject to penalties and fines or being required to pay damages. Any change in the regulations may require us to acquire equipment or incur additional capital expenditure or costs in order to comply with such regulations. Our profits will be adversely affected if we are unable to pass on such additional costs to our customers.

In recent years, there have been many newly-built residential buildings in close proximity to our factory. In March 2014 and November 2015, due to the noise caused by our production, Shandong Fuwei was fined RMB10,000 and RMB20,000, respectively, and was required to rectify and reform within a definite time. The complaints from nearby residents about the noise caused by our production may require us to take measures to lower noise, which will lead to additional cost to us. In the event that we are forced to suspend our production to take improvement measures, our operations and earnings may be adversely affected.

15

Changes in foreign exchange regulations in China may affect our ability to pay dividends in foreign currencies.

We currently receive most of our operating revenues in Renminbi. Currently, Renminbi is not a freely convertible currency and the restrictions on currency exchanges in China may limit our ability to use revenues generated in Renminbi to fund our business activities outside China or to make dividends or other payments in U.S. dollars. The PRC government strictly regulates conversion of Renminbi into foreign currencies. Over the years, the PRC government has significantly reduced its control over routine foreign exchange transactions under current accounts, including trade- and service-related foreign exchange transactions, foreign debt service and payment of dividends. In accordance with the existing foreign exchange regulations in China, our PRC subsidiary, Shandong Fuwei, is able to pay dividends in foreign currencies, without prior approval from the PRC State Administration of Foreign Exchange, or SAFE, by complying with certain procedural requirements. The PRC government may, however, at its discretion, restrict access in the future to foreign currencies for current account transactions and prohibit us from converting our Renminbi-denominated earnings into foreign currencies. If this occurs, our PRC subsidiary may not be able to pay us dividends in foreign currency without prior approval from SAFE. In addition, conversion of Renminbi for most capital account items, including direct investments, is still subject to government approval in China and companies are required to open and maintain separate foreign exchange accounts for capital account items. This restriction may limit our ability to invest earnings of Shandong Fuwei.

Fluctuation in the value of Renminbi could adversely affect our overseas sales and import of raw materials and the value of, and dividends payable on, our shares in foreign currency terms.

The value of Renminbi is subject to various factors and depends to a large extent on China’s domestic and international economic, financial and political developments, as well as the currency’s supply and demand in the local market. From 1994, the conversion of Renminbi into foreign currencies, including the U.S. dollar, was based on exchange rates set and published daily by the People’s Bank of China, the PRC central bank, based on the previous day’s interbank foreign exchange market rates in China and exchange rates on the world financial markets. The official exchange rate for the conversion of Renminbi into U.S. dollars remained stable until Renminbi was revalued in July 2005 and allowed to fluctuate by reference to a basket of foreign currencies, including the U.S. dollar. Under the new policy, Renminbi is permitted to fluctuate within a band against a basket of foreign currencies. This change in policy resulted initially in an approximately 2.0% appreciation in the value of Renminbi against the U.S. dollar. The Chinese government may adopt a substantially more liberalized currency policy, which could result in a further and more significant fluctuation in the value of Renminbi against the U.S. dollar. Since our income and profits are denominated in Renminbi, fluctuation in the value of Renminbi could adversely affect our overseas sales and import of raw materials and further negatively affect our revenue and net income. Any appreciation of Renminbi would increase the value of, and any dividends payable on, our shares in foreign currency terms. Conversely, any depreciation of Renminbi would decrease the value of, and any dividends payable on, our shares in foreign currency terms.

The uncertain legal environment in China could limit the legal protections available to you.

The PRC legal system is a civil law system based on written statutes. Unlike the common law system, the civil law system is a system in which decided legal cases have little precedential value. In the late 1970s, the PRC government began to promulgate a comprehensive system of laws and regulations to provide general guidance on economic and business practices in China and to regulate foreign investment. Our PRC subsidiary, Shandong Fuwei, is a wholly foreign-owned enterprise and is subject to laws and regulations applicable to foreign investment in China in general and laws and regulations applicable to wholly foreign-owned enterprises in particular. China has made significant progress in the promulgation of laws and regulations dealing with economic matters such as corporate organization and governance, foreign investment, commerce, taxation and trade. However, the promulgation of new laws, changes of existing laws and abrogation of local regulations by national laws may have a negative impact on our business and prospects. In addition, as these laws, regulations and legal requirements are relatively recent and because of the limited volume of published cases and their non-binding nature, the interpretation and enforcement of these laws, regulations and legal requirements involve significant uncertainties. These uncertainties could limit the legal protections available to foreign investors, including you. For example, it is not clear if a PRC court would enforce in China a foreign court decision brought by you against us in shareholders’ derivative actions. Moreover, the enforceability of contracts in China, especially with the government, is relatively uncertain. If counterparties repudiated our contracts or defaulted on their obligations, we may not have adequate remedies. Such uncertainties or inability to enforce our contracts could materially and adversely affect our revenues and earnings.

Outbreak of viruses such as SARS, H1N1 or other epidemics could materially and adversely affect our overall operations and results of operations.

From March to July 2003, mainland China, Hong Kong, Taiwan and some other areas in Asia experienced an outbreak of a new and contagious form of atypical pneumonia known as severe acute respiratory syndrome, or SARS. A recurrent outbreak, or an outbreak of a similarly contagious disease, such as the H1N1 avian flu, could potentially disrupt our operations to the extent that any one of our employees is suspected of having the infection or that any of our facilities is identified as a possible source of spreading the virus or disease. We may be required to quarantine employees who are suspected of having an infection. We may also be required to disinfect our facilities and therefore suffer a suspension of production of indefinite duration. Any quarantine or suspension of production at any of our facilities will adversely affect our overall operations. In addition, any such outbreak will likely restrict the level of economic activities in the affected areas, which could lead to a substantial decrease in our revenues accompanied by an increase in our costs.

16

Regulations relating to offshore investment activities by PRC residents may limit our ability to acquire PRC companies and adversely affect our business and prospects.

The Chinese State Administration of Foreign Exchange (“SAFE”) has promulgated several regulations, including the Notice on Relevant Issues Concerning Foreign Exchange Administration for Domestic Residents’ Financing and Roundtrip Investment through Offshore Special Purpose Vehicles, or Circular 75, effective on November 1, 2005 and its implementation rules. These regulations require PRC residents and PRC corporate entities to register with local branches of SAFE in connection with their direct or indirect offshore investment activities. These regulations are applicable to our shareholders who are PRC corporate entities and may be applicable to any offshore acquisitions that we make in the future. Under these foreign exchange regulations, PRC residents who make, or have prior to the implementation of these foreign exchange regulations made, direct or indirect investments in offshore special purpose vehicles, or SPVs, will be required to register such investments with SAFE or its local branches. In addition, any PRC corporate entities who is a direct or indirect shareholder of an SPV, is required to update its filed registration with the local branch of SAFE with respect to that SPV, to reflect any material change.

Circular of the State Administration of Foreign Exchange on Printing and Distributing on the Operating Rules for the Administration of Foreign Exchange with Respect to the Financing and Round-tripping Investment of Domestic Residents via Overseas Special Purpose Companies (“Circular 19”) was promulgated by SAFE on May 20, 2011 and came into effect on July 1, 2011. Circular 19 further clarifies the administration principles of Circular 75 and the relevant issues in its application and simplifies operating procedures. To a certain extent, Circular 19 will benefit the offshore investment and round-tripping investment.

Provisions on the Merger and Acquisition of Domestic Enterprises by Foreign Investors (Revised in 2009) (“Circular 6”) was promulgated by Ministry of Commerce and came into effect on June 22, 2009. According to Circular 6, where a domestic company sets up a company with special purpose abroad, it shall apply to the Ministry of Commerce for going through the examination and approval formalities. When merging or acquiring related domestic companies in the name of the companies in foreign countries legally established or controlled by them, the domestic companies, enterprises or natural persons shall report to the Ministry of Commerce for approval.

Item 4. Information on the Company

Overview

We were formed as a Cayman Islands corporation in August 2004 under the name “Neo-Luck Plastic Holdings Co., Ltd.” and changed our name to “Fuwei Films (Holdings) Co., Ltd.” in April 2005. Our corporate headquarters, principal place of business, production and ancillary facilities occupy an area of approximately 74,251 square meters at No. 387 Dongming Road, Weifang Shandong 261061, People’s Republic of China. Our agent for service in the United States is CT Corporation System located at 111 Eighth Avenue, NY, NY 10011.