Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

(Mark One)

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(B) OR 12(G) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended May 31, 2011.

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

For the transition period from to

Commission file number: 001-32993

NEW ORIENTAL EDUCATION & TECHNOLOGY GROUP INC.

(Exact name of Registrant as specified in its charter)

N/A

(Translation of Registrant’s name into English)

Cayman Islands

(Jurisdiction of incorporation or organization)

No. 6 Hai Dian Zhong Street

Haidian District, Beijing 100080

The People’s Republic of China

(Address of principal executive offices)

Louis T. Hsieh, President and Chief Financial Officer

Tel: +(86 10) 6260-5566

E-mail: louishsieh@xdf.cn

Fax: +(86 10) 6260-5511

No. 6 Hai Dian Zhong Street

Haidian District, Beijing 100080

The People’s Republic of China

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of Exchange on Which Registered | |

| American depositary shares, each representing one common share* |

New York Stock Exchange | |

| Common shares, par value US$0.01 per share | New York Stock Exchange** | |

| * | Effective August 18, 2011, the ratio of ADSs to our common shares was changed from one ADS representing four common shares to one ADS representing one common share. |

| ** | Not for trading, but only in connection with the listing on New York Stock Exchange of the American depositary shares. |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

Indicate the number of outstanding shares of each of the Issuer’s classes of capital or common stock as of the close of the period covered by the annual report. 158,379,387 common shares, par value US$0.01 per share, as of May 31, 2011.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP x | International Financial Reporting Standards as issued by the International Accounting Standards Board ¨ | Other ¨ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ¨ Item 18 ¨

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ¨ No ¨

Table of Contents

| 1 | ||||||

| 2 | ||||||

| ITEM 1. |

2 | |||||

| ITEM 2. |

2 | |||||

| ITEM 3. |

2 | |||||

| ITEM 4. |

26 | |||||

| Item 4A. |

44 | |||||

| ITEM 5. |

44 | |||||

| ITEM 6. |

64 | |||||

| ITEM 7. |

70 | |||||

| ITEM 8. |

72 | |||||

| ITEM 9. |

73 | |||||

| ITEM 10. |

74 | |||||

| ITEM 11. |

80 | |||||

| ITEM 12. |

81 | |||||

| 82 | ||||||

| ITEM 13. |

82 | |||||

| ITEM 14. |

MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS |

82 | ||||

| ITEM 15. |

82 | |||||

| ITEM 16A. |

83 | |||||

| ITEM 16B. |

84 | |||||

| ITEM 16C. |

84 | |||||

| ITEM 16D. |

84 | |||||

| ITEM 16E. |

PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS |

84 | ||||

| ITEM 16F. |

84 | |||||

| ITEM 16G. |

84 | |||||

| 85 | ||||||

| ITEM 17. |

85 | |||||

| ITEM 18. |

85 | |||||

| ITEM 19. |

85 | |||||

Table of Contents

Unless otherwise indicated and except where the context otherwise requires, references in this annual report on Form 20-F to:

| • | “we,” “us,” “our company” or “our” refers to New Oriental Education & Technology Group Inc., its predecessor entities and subsidiaries and, in the context of describing our operations and consolidated financial data, also include New Oriental China; |

| • | “China” or “PRC” refers to the People’s Republic of China, and for the purpose of this annual report, excludes Taiwan, Hong Kong and Macau; |

| • | “New Oriental China” refers to our consolidated affiliated entity in the PRC, Beijing New Oriental Education & Technology (Group) Co., Ltd., and its subsidiaries; |

| • | “student enrollments” refers to the cumulative total number of courses enrolled in and paid for by our students, including multiple courses enrolled in and paid for by the same student but excluding courses offered at our primary and secondary schools; |

| • | “shares” or “common shares” refers to our common shares, par value US$0.01 per share; |

| • | “ADSs” refers to our American depositary shares. Prior to August 18, 2011, each of our ADSs represented four common shares. On August 18, 2011, we effected a change in the ratio of our ADSs to common shares from one ADS representing four common shares to one ADS representing one common share. Except as otherwise noted, this change in our ADS to common share ratio has been retroactively reflected in all net income per ADS data included in this annual report on Form 20-F; and |

| • | “RMB” or “Renminbi” refers to the legal currency of China and “$,” “dollars,” “US$” or “U.S. dollars” refers to the legal currency of the United States. |

We refer to our teaching facilities in this annual report as either “schools” or “learning centers,” based primarily on a facility’s functions. Generally, our schools consist of classrooms and administrative facilities with student and administrative services, while our learning centers consist primarily of classroom facilities.

Glossary of Major Admissions and Assessment Tests

| ACT | American College Test (US) | |

| BEC | Business English Certificate (US) | |

| CET 4 | College English Test Level 4 (PRC) | |

| CET 6 | College English Test Level 6 (PRC) | |

| GMAT | Graduate Management Admission Test (US) | |

| GRE | Graduate Record Examination (US) | |

| IELTS | International English Language Testing System (Commonwealth countries) | |

| LSAT | Law School Admission Test (US) | |

| PETS | Public English Test System (PRC) | |

| SAT | SAT College Entrance Test (US) | |

| TOEFL | Test of English as a Foreign Language (US) | |

| TOEIC | Test of English for International Communication (US) | |

| TSE | Test of Spoken English (US) | |

1

Table of Contents

FORWARD-LOOKING STATEMENTS

This annual report contains forward-looking statements that involve risks and uncertainties. All statements other than statements of historical facts are forward-looking statements. These forward-looking statements are made under the “safe harbor” provisions of the U.S. Private Securities Litigation Reform Act of 1995. These statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from those expressed or implied by the forward-looking statements.

You can identify these forward-looking statements by words or phrases such as “may,” “will,” “expect,” “is expected to,” “anticipate,” “aim,” “estimate,” “intend,” “plan,” “believe,” “is/are likely to” or other similar expressions. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. These forward-looking statements include, but are not limited to:

| • | our anticipated growth strategies; |

| • | our future business development, results of operations and financial condition; |

| • | expected changes in our revenues and certain cost and expense items; |

| • | our ability to increase student enrollments and course fees and expand program, service and product offerings; |

| • | competition in the language training, test preparation, primary and secondary education, educational content, software and other technology development and online education markets; |

| • | risks associated with our offering of new educational programs, services and products and the expansion of our geographic reach; |

| • | the expected increase in expenditures on education in China; and |

| • | PRC laws, regulations and policies relating to private education and providers of private educational services. |

You should read thoroughly this annual report and the documents that we refer to herein with the understanding that our actual future results may be materially different from and/or worse than what we expect. We qualify all of our forward-looking statements by these cautionary statements. Other sections of this annual report include additional factors which could adversely impact our business and financial performance. Moreover, we operate in an evolving environment. New risk factors emerge from time to time and it is not possible for our management to predict all risk factors, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements.

You should not rely upon forward-looking statements as predictions of future events. The forward-looking statements made in this annual report relate only to events or information as of the date on which the statements are made in this annual report. We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by applicable law.

| ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

Not applicable.

| ITEM 2. | OFFER STATISTICS AND EXPECTED TIMETABLE |

Not applicable.

| ITEM 3. | KEY INFORMATION |

| A. | Selected Financial Data |

2

Table of Contents

Our Selected Consolidated Financial Data

The following selected consolidated condensed financial data as of May 31, 2007, 2008, 2009, 2010 and 2011 and for the years ended May 31, 2007, 2008, 2009, 2010 and 2011 have been derived from our audited consolidated financial statements. The selected consolidated condensed financial data should be read in conjunction with, and are qualified in their entirety by reference to, our audited consolidated financial statements and related notes and “Item 5. Operating and Financial Review and Prospects” included elsewhere in this annual report. Our audited consolidated financial statements are prepared and presented in accordance with generally accepted accounting principles in the United States, or U.S. GAAP. Effective December 1, 2007, we changed our reporting currency from RMB to the U.S. dollar in order to improve research analysts’ and investors’ ability to compare our financial results with other publicly-traded companies and to simplify our earnings release presentation. In order to allow for comparison to the financial results for the years ended May 31, 2008, 2009, 2010 and 2011, the financial data for the year ended, and as of, May 31 2007 has been restated to reflect U.S. dollars as the reporting currency according to the policy described in “Note 2—Significant Accounting Policies—Foreign currency translation” in the notes accompanying our financial statements which are included at the end of this annual report.

| For the Years Ended May 31, | ||||||||||||||||||||

| (in thousands of US$, except share, per share and per ADS data) |

2007 | 2008 | 2009 | 2010 | 2011 | |||||||||||||||

| Consolidated Statement of Operations Data: |

||||||||||||||||||||

| Net revenues: |

||||||||||||||||||||

| Educational programs and services |

123,543 | 183,917 | 266,389 | 352,857 | 508,439 | |||||||||||||||

| Books and others |

9,060 | 17,086 | 26,178 | 33,450 | 49,433 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total net revenues |

132,603 | 201,003 | 292,567 | 386,307 | 557,872 | |||||||||||||||

| Operating costs and expenses(1): |

||||||||||||||||||||

| Cost of revenues |

(53,744 | ) | (77,219 | ) | (112,011 | ) | (147,261 | ) | (222,625 | ) | ||||||||||

| Selling and marketing |

(16,549 | ) | (25,617 | ) | (38,947 | ) | (58,396 | ) | (82,797 | ) | ||||||||||

| General and administrative |

(36,218 | ) | (52,832 | ) | (80,689 | ) | (103,336 | ) | (155,412 | ) | ||||||||||

| Loss on disposal of subsidiaries |

— | — | — | — | (1,537 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total operating costs and expenses |

(106,511 | ) | (155,668 | ) | (231,647 | ) | (308,993 | ) | (462,371 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Operating income |

26,092 | 45,335 | 60,920 | 77,314 | 95,501 | |||||||||||||||

| Other income (expense): |

||||||||||||||||||||

| Interest income |

4,730 | 8,035 | 6,599 | 6,474 | 13,017 | |||||||||||||||

| Interest expense |

(416 | ) | — | — | — | — | ||||||||||||||

| Miscellaneous income (expense), net |

(105 | ) | (886 | ) | 590 | (252 | ) | 1,257 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income before provisions for income taxes and noncontrolling interest |

30,301 | 52,484 | 68,109 | 83,536 | 109,775 | |||||||||||||||

| Provision for income taxes: |

||||||||||||||||||||

| Current |

(2,231 | ) | (3,839 | ) | (8,399 | ) | (7,845 | ) | (9,390 | ) | ||||||||||

| Deferred |

401 | 195 | 1,143 | 1,871 | 1,154 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Provision for income taxes |

(1,830 | ) | (3,644 | ) | (7,256 | ) | (5,974 | ) | (8,236 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income |

28,471 | 48,840 | 60,853 | 77,562 | 101,539 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Add: Net loss attributable to noncontrolling interest(2) |

128 | 173 | 163 | 227 | 235 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income attributable to New Oriental Education & Technology Group Inc. |

28,599 | 49,013 | 61,016 | 77,789 | 101,774 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income per share and net income per ADS attributable to New Oriental Education & Technology Group Inc. – basic(3) |

0.21 | 0.33 | 0.41 | 0.52 | 0.66 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income per share and net income per ADS attributable to New Oriental Education & Technology Group Inc. – diluted(3) |

0.20 | 0.31 | 0.40 | 0.50 | 0.65 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Shares used in calculating basic net income per share |

134,218,191 | 149,992,200 | 149,090,088 | 150,952,249 | 153,253,065 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Shares used in calculating diluted net income per share |

142,093,794 | 156,449,101 | 153,528,383 | 154,831,633 | 156,071,833 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (1) | Share-based compensation expenses are included in our operating costs and expenses as follows: |

3

Table of Contents

| For the Years Ended May 31, | ||||||||||||||||||||

| (in thousands of US$) |

2007 | 2008 | 2009 | 2010 | 2011 | |||||||||||||||

| Cost of revenues |

277 | 707 | 316 | 657 | 900 | |||||||||||||||

| Selling and marketing |

109 | 226 | 225 | 117 | — | |||||||||||||||

| General and administrative |

4,261 | 7,809 | 16,209 | 15,409 | 14,145 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total |

4,647 | 8,742 | 16,750 | 16,183 | 15,045 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (2) | Amounts in relation to noncontrolling interests, formerly named minority interest, for the years ended May 31, 2007, 2008 and 2009 are reclassified in accordance with authoritative guidance regarding the noncontrolling interests, which we adopted on June 1, 2009. |

| (3) | Each ADS represents one common share. Effective August 18, 2011, the ratio of ADSs to our common shares was changed from one ADS representing four common shares to one ADS representing one common share. |

The following table presents a summary of our consolidated balance sheet data as of May 31, 2007, 2008, 2009, 2010 and 2011:

| As of May 31, | ||||||||||||||||||||

| (in thousands of US$) |

2007 | 2008 | 2009 | 2010 | 2011 | |||||||||||||||

| Condensed Consolidated Balance Sheet Data: |

||||||||||||||||||||

| Cash and cash equivalents |

204,396 | 208,440 | 254,772 | 281,104 | 317,260 | |||||||||||||||

| Total assets |

316,090 | 396,743 | 469,402 | 596,420 | 863,370 | |||||||||||||||

| Total current liabilities |

68,872 | 97,886 | 117,761 | 168,705 | 288,000 | |||||||||||||||

| Total liabilities |

68,872 | 97,886 | 117,918 | 168,842 | 289,147 | |||||||||||||||

| Total shareholders’ equity |

246,980 | 298,680 | 351,246 | 427,567 | 574,223 | |||||||||||||||

| Noncontrolling interest |

238 | 177 | 238 | 11 | — | |||||||||||||||

| Total equity |

247,218 | 298,857 | 351,484 | 427,578 | 574,223 | |||||||||||||||

Exchange Rate Information

Our business is primarily conducted in China and substantially all of our revenues are denominated in RMB. This annual report contains translations of RMB amounts into U.S. dollars at specific rates solely for the convenience of the reader. Unless otherwise noted, including in “Note 2—Significant Accounting Policies—Foreign currency translation” in the notes accompanying our financial statements, all translations from RMB to U.S. dollars and from U.S. dollars to RMB in this annual report were made at a rate of RMB6.4786 to US$1.00, the noon buying rate in The City of New York for cable transfers of RMB as certified for customs purposes by the Federal Reserve Bank of New York, or the noon buying rate, on May 31, 2011. We make no representation that any RMB or U.S. dollar amounts could have been, or could be, converted into U.S. dollars or RMB, as the case may be, at any particular rate, the rates stated below, or at all. The PRC government imposes control over its foreign currency reserves in part through direct regulation of the conversion of RMB into foreign exchange and through restrictions on foreign trade. On October 7, 2011, the noon buying rate was RMB6.3745 to US$1.00.

The following table sets forth information concerning exchange rates between the RMB and the U.S. dollar for the periods indicated. Fiscal year refers to our fiscal year ended on May 31. These rates are provided solely for your convenience and are not necessarily the exchange rates that we used in this annual report or will use in the preparation of our periodic reports or any other information to be provided to you.

4

Table of Contents

| Noon Buying Rate | ||||||||||||||||

| Period |

Period End | Average(1) | High | Low | ||||||||||||

| (RMB Per US$ 1.00) | ||||||||||||||||

| Fiscal Year 2007 |

7.6516 | 7.8473 | 7.6463 | 8.0225 | ||||||||||||

| Fiscal Year 2008 |

6.9400 | 7.3368 | 6.9377 | 7.6680 | ||||||||||||

| Fiscal Year 2009 |

6.8278 | 6.8298 | 6.7800 | 6.9633 | ||||||||||||

| Fiscal Year 2010 |

6.8305 | 6.8276 | 6.8229 | 6.8371 | ||||||||||||

| Fiscal Year 2011 |

6.4786 | 6.6556 | 6.4786 | 6.8323 | ||||||||||||

| 2011 |

||||||||||||||||

| April |

6.4900 | 6.5267 | 6.4900 | 6.5477 | ||||||||||||

| May |

6.4786 | 6.4957 | 6.4786 | 6.5073 | ||||||||||||

| June |

6.4635 | 6.4746 | 6.4628 | 6.4830 | ||||||||||||

| July |

6.4360 | 6.4575 | 6.4360 | 6.4720 | ||||||||||||

| August |

6.3778 | 6.4036 | 6.3778 | 6.4401 | ||||||||||||

| September |

6.3780 | 6.3885 | 6.3780 | 6.3975 | ||||||||||||

| October (through October 7, 2011) |

6.3745 | 6.3752 | 6.3745 | 6.3780 | ||||||||||||

Source: Federal Reserve Statistical Release

| (1) | Annual averages are calculated from the average of daily rates. Monthly averages are calculated using the average of the daily rates during the relevant period. |

| B. | Capitalization and Indebtedness |

Not applicable.

| C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

| D. | Risk Factors |

Risks Related to Our Business

If we are not able to continue to attract students to enroll in our courses without a significant decrease in course fees, our revenues may decline and we may not be able to maintain profitability.

The success of our business depends primarily on the number of student enrollments in our courses and the amount of course fees that our students are willing to pay. Therefore, our ability to continue to attract students to enroll in our courses without a significant decrease in course fees is critical to the continued success and growth of our business. This in turn will depend on several factors, including our ability to develop new programs and enhance existing programs to respond to changes in market trends and student demands, expand our geographic reach, manage our growth while maintaining the consistency of our teaching quality, effectively market our programs to a broader base of prospective students, develop and license additional high-quality educational content and respond to competitive pressures. If we are unable to continue to attract students to enroll in our courses without a significant decrease in course fees, our revenue may decline and we may not be able to maintain profitability.

We depend on our dedicated and capable faculty, and if we are not able to continue to hire, train and retain qualified teachers, we may not be able to maintain consistent teaching quality throughout our school network and our brand, business and operating results may be materially and adversely affected.

Our teachers are critical to maintaining the quality of our programs, services and products and maintaining our brand and reputation, as they interact with our students on a daily basis. We must continue to attract qualified teachers who have a strong command of the subject areas to be taught and meet our qualification. We also seek to hire teachers who are capable of delivering innovative and inspirational instruction. There are a limited number of teachers in China with the necessary experience and language proficiency to teach our courses and we must provide competitive compensation packages to attract and retain qualified teachers. In addition, criteria such as commitment and dedication are difficult to ascertain during the recruitment process, in particular as we continue to expand and add teachers to meet rising student enrollments. We must also provide continuous training to our teachers so that they can stay up to date with changes in student demands, admissions and assessment tests, admissions standards and other key trends necessary to effectively teach their respective courses. We may not be able to hire, train and retain enough qualified teachers to keep pace with our anticipated growth while maintaining consistent teaching quality across many different schools, learning centers and programs in different geographic locations. Shortages of qualified teachers or decreases in the quality of our instruction, whether actual or perceived, in one or more of our markets may have a material and adverse effect on our business.

5

Table of Contents

Our business depends on our “New Oriental” brand, and if we are not able to maintain and enhance our brand, our business and operating results may be harmed.

We believe that market awareness of our “New Oriental” brand has contributed significantly to the success of our business. We also believe that maintaining and enhancing the “New Oriental” brand is critical to maintaining our competitive advantage. We offer a diverse set of programs, services and products to primary and middle school students, college students and other adults throughout many provinces and cities in China. As we continue to grow in size, expand our program, service and product offerings and extend our geographic reach, maintaining quality and consistency may be more difficult to achieve.

In recent years, we have invested significantly in brand promotion initiatives. We cannot assure you that these or our other marketing efforts will be successful in promoting our brand to remain competitive. If we are unable to further enhance our brand recognition and increase awareness of our programs, services and products, or if we incur excessive marketing and promotion expenses, our business and results of operations may be materially and adversely affected. In addition, any negative publicity relating to our company or our programs and services, regardless of its veracity, could harm our brand image and in turn adversely affect our business and operating results.

We face risks related to health epidemics and other outbreaks, which could result in reduced attendance or temporary closure of our schools, learning centers and bookstores.

Our business could be materially and adversely affected by the outbreak of avian influenza, severe acute respiratory syndrome, or SARS, or other epidemics. In April 2009, a new strain of influenza A virus subtype H1N1, commonly referred to as “swine flu,” was first discovered in North America and quickly spread to other parts of the world, including China. In early June 2009, the World Health Organization declared the outbreak to be a pandemic, while noting that most of the illnesses were of moderate severity. The PRC Ministry of Health subsequently reported several hundred deaths caused by the influenza A (H1N1). The influenza A (H1N1) outbreak adversely affected our business and results of operations in the first and second fiscal quarters of 2010 as we experienced slower-than-usual student enrollment growth and large numbers of cancellations and deferments in enrollments from registered students. In addition, we had to cancel classes whenever an enrolled student was diagnosed with influenza A (H1N1), as required by applicable health regulations. Any future outbreak of avian influenza, SARS, the influenza A (H1N1) or other adverse public health developments in China may have a material and adverse effect on our business operations. These occurrences could cause cancellations or deferments of student enrollments and require the temporary closure of our schools, learning centers and bookstores, thus severely disrupting our business operations and adversely affecting our results of operations.

Failure to effectively and efficiently manage the expansion of our school network may materially and adversely affect our ability to capitalize on new business opportunities.

We have increased the number of our schools in China from three in 2001 to 54 by the end of May 2011, and we increased the number of our learning centers in China from 23 in 2001 to 433 by the end of May 2011. We plan to continue to expand our operations in different geographic locations in China. Our expansion has resulted, and will continue to result, in substantial demands on our management, faculty and operational, technological and other resources. Our planned expansion will also place significant demands on us to maintain the consistency of our teaching quality and our culture to ensure that our brand does not suffer as a result of any decreases, whether actual or perceived, in our teaching quality. To manage and support our growth, we must continue to improve our existing operational, administrative and technological systems and our financial and management controls, and recruit, train and retain additional qualified teachers, management personnel and other administrative and sales and marketing personnel, particularly as we expand into new markets. We cannot assure you that we will be able to effectively and efficiently manage the growth of our operations, recruit and retain qualified teachers and management personnel and integrate new schools and learning centers into our operations. Any failure to effectively and efficiently manage our expansion may materially and adversely affect our ability to capitalize on new business opportunities, which in turn may have a material adverse impact on our financial condition and results of operations.

If we fail to successfully execute our growth strategies, we may not be able to continue to attract students to enroll in our courses without a significant decrease in course fees, and our business and prospects may be materially and adversely affected.

6

Table of Contents

Our growth strategies include expanding our program, service and product offerings and our network of schools, learning centers and bookstores, updating and expanding the content of our programs, services and products in a cost-effective and timely manner, as well as maintaining and continuing to establish strategic relationships with complementary businesses. The expansion of our programs, services and products in terms of types of offerings and geographic locations may not succeed due to competition, failure to effectively market our new programs, services and products and maintain their quality and consistency, or other factors. In addition, we may be unable to identify new cities with sufficient growth potential to expand our network, and we may fail to attract students and increase student enrollments or recruit, train and retain qualified teachers for our new schools and learning centers. Some cities in China have undergone development and expansion for several decades while others are still at an early stage of urbanization and development. In more developed cities, it may be difficult to increase the number of schools and learning centers because we and/or our competitors already have extensive operations in these cities. In recently developed and developing cities, demand for our programs, services and products may not increase as rapidly as we expect. Furthermore, we may be unable to develop or license additional content on commercially reasonable terms and in a timely manner, or at all, to keep pace with changes in market demands. If we fail to successfully execute our growth strategies, we may not be able to continue to attract students to enroll in our courses without a significant decrease in course fees, and our business and prospects may be materially and adversely affected.

We may not be able to achieve the benefits we expect from recent and future acquisitions, and recent and future acquisitions may have an adverse effect on our ability to manage our business.

As part of our business strategy, we have pursued and intend to continue to pursue selective strategic acquisitions of businesses that complement our existing businesses. Acquisitions expose us to potential risks, including risks associated with the diversion of resources from our existing businesses, difficulties in successfully integrating the acquired businesses, failure to achieve expected growth by the acquired businesses and an inability to generate sufficient revenue to offset the costs and expenses of acquisitions. If the revenue and cost synergies that we expect to achieve from our acquisitions do not materialize, we may have to recognize impairment charges. For example, in June 2008 we acquired a 60% equity stake in Beijing Haidian Mingshitang Exam Training Education School, or Mingshitang School, a Beijing-based private school that specializes in tutoring students seeking to retake the Chinese college entrance examination, and in September 2008 we acquired Changchun Tongwen Gaokao Training Education School, or Tongwen Gaokao School, which provides services similar to those of Mingshitang School. In the fiscal year ended May 31, 2010, we recognized a goodwill impairment loss of US$76,000 arising from the acquisitions of Mingshitang School and Tongwen Gaokao School. We disposed Mingshitang School in April 2011 and recorded a loss of US$1.2 million on the disposal. As another example, in September 2010, we completed the acquisition of a 100% equity interest in Newave Education, a K-12 English language school in Shanghai. Due to breach of contract by the seller of Newave Education, we submitted a request for arbitration to the China International Economic and Trade Arbitration Commission for full refund of the purchase consideration which we had paid. The case was accepted in August 2011.

If any one or more of the aforementioned risks associated with acquisitions materialize, our acquisitions may not be beneficial to us and may have a material adverse effect on our business, financial condition and results of operations.

Third parties have in the past brought intellectual property infringement claims against us based on the content of the books and other teaching or marketing materials that we or our teachers authored and/or distributed and may bring similar claims against us in the future.

7

Table of Contents

We may be subject to claims by educational institutions and organizations, content providers and publishers, competitors and others on the ground of intellectual property rights infringement, defamation, negligence or other legal theories based on the content of the materials that we or our teachers author and/or distribute as course materials. These types of claims have been brought, sometimes successfully, against print publications and educational institutions in the past, including ourselves. For example, in January 2001, the Graduate Management Admission Council, or GMAC, and Educational Testing Service, or ETS, filed three separate lawsuits against us in the Beijing No. 1 Intermediate People’s Court, alleging that we had violated the copyrights and trademarks relating to the GMAT test owned by GMAC and relating to the GRE and TOEFL tests owned by ETS by duplicating, selling and distributing their test materials without their authorization. In September 2003, the trial court found that we had violated GMAC’s and ETS’s respective copyrights and trademarks in connection with those admissions tests. The trial court’s judgment was partially affirmed in a final judgment issued by the Beijing Higher People’s Court in December 2004. The Beijing Higher People’s Court held that we had not misused the trademarks of GMAC or ETS. However, it also found that the TOEFL and GRE tests were the original works of ETS and the GMAT test was the original work of GMAC, all of which are protected under the PRC Copyright Law. The Beijing Higher People’s Court held that our duplication, sale and distribution of the test materials relating to these tests without ETS’s and GMAC’s prior permission were not a “reasonable use” of the test materials under the PRC Copyright Law, and that we, therefore, had infringed upon ETS’s and GMAC’s respective copyrights. We were ordered to pay damages in an aggregate of approximately RMB6.5 million cease all infringing activities and destroy all copyright-infringing materials in our possession, all of which we have done. Since the Beijing Higher People’s Court issued the final judgment in 2004, we have endeavored to comply with the court order and applicable PRC laws and regulations relating to intellectual property, and we have adopted policies and procedures to prohibit our employees and contractors from engaging in any copyright, trademark or trade name infringing activities. However, we cannot assure you that every teacher or other personnel will strictly comply with these policies at our schools, learning centers or other locations or media through which we provide our programs, services and products.

We have also been involved in other claims and legal proceedings against us relating to infringement of third parties’ copyrights in materials distributed by us and the unauthorized use of a third party’s name in connection with the marketing and promotion of one of our programs, and may be subject to further claims in the future, particularly in light of the uncertainties in the interpretation and application of PRC intellectual property laws and regulations. Furthermore, if printed publications or other materials that we or our teachers author and/or distribute contain materials that government authorities find objectionable, these publications may have to be recalled, which could result in increased expenses, loss in revenues and adverse publicity. Any claims against us, with or without merit, could be time-consuming and costly to defend or litigate, divert our management’s attention and resources or result in the loss of goodwill associated with our brand. If a lawsuit against us is successful, we may be required to pay substantial damages and/or enter into royalty or license agreements that may not be based upon commercially reasonable terms, or we may be unable to enter into such agreements at all. We may also lose, or be limited in, the rights to offer some of our programs, services and products or be required to make changes to our course materials or websites. As a result, the scope of our course materials could be reduced, which could adversely affect the effectiveness of our teaching, limit our ability to attract new students, harm our reputation and have a material adverse effect on our results of operations and financial position.

We may lose our competitive advantage and our reputation, brand and operations may suffer if we fail to prevent the loss or misappropriation of, or disputes over, our intellectual property rights.

We consider our trademarks and trade name invaluable to our ability to continue to develop and enhance our brand recognition. We have spent over a decade building our “New Oriental” brand by emphasizing quality and consistency and building trust among students and parents. From time to time, our trademarks and trade name have been used by third parties for or as part of other branded programs, services and products unrelated to us. We have sent cease and desist letters to such third parties in the past and will continue to do so in the future. However, preventing trademark and trade name infringement, particularly in China, is difficult, costly and time-consuming and continued unauthorized use of our trademarks and trade name by unrelated third parties may damage our reputation and brand. In addition, we have spent significant time and expense developing or licensing and localizing the content of certain educational materials, such as books, software, CD-ROMs, magazines and other periodicals, to enrich our product offerings and meet students’ needs. The measures we take to protect our trademarks, copyrights and other intellectual property rights, which presently are based upon a combination of trademark, copyright and trade secret laws, may not be adequate to prevent unauthorized use by third parties. Furthermore, the application of laws governing intellectual property rights in China and abroad is uncertain and evolving, and could involve substantial risks to us. If we are unable to adequately protect our trademarks, copyrights and other intellectual property rights, we may lose these rights, our brand name may be harmed, and our business may suffer materially.

8

Table of Contents

We face significant competition in each major program we offer and each geographic market in which we operate, and if we fail to compete effectively, we may lose our market share and our profitability may be adversely affected.

The private education sector in China is rapidly evolving, highly fragmented and competitive, and we expect competition in this sector to persist and intensify. We face competition in each major program we offer and each geographic market in which we operate. For example, we face nationwide competition for our IELTS preparation courses from Global IELTS School, which offers IELTS preparation courses in many cities in China. We face regional competition for our English for children program from several competitors that focus on children’s English training in specific regions, including English First. We face competition for our “Elite English” program primarily from Wall Street Institute and EF English First, both of which offer English training courses for adults in many cities in China. Wall Street Institute began providing high-end English training courses to adults in major cities several years before we entered this market and enjoys a first-mover advantage. We also face competition from companies that focus on providing international and/or PRC test preparation courses in specific geographic markets in China.

Our student enrollments may decrease due to intense competition. Some of our competitors may have more resources than we do. These competitors may be able to devote greater resources than we can to the development, promotion and sale of their programs, services and products and respond more quickly than we can to changes in student needs, testing materials, admissions standards or new technologies. In addition, we face competition from many different smaller sized organizations that focus on some of our targeted markets, and they may be able to respond more promptly to changes in student preferences in these markets. In addition, the increasing use of the Internet and advances in Internet- and computer-related technologies, such as web video conferencing and online testing simulators, are eliminating geographic and cost-entry barriers to providing private educational services. As a result, many of our international competitors that offer online test preparation and language training courses, such as The Princeton Review, Inc. and Kaplan, Inc. may be able to more effectively penetrate the China market. Many of these international competitors have strong education brands, and students and parents in China may be attracted to the offerings of international competitors based in the country that the student wishes to study in or in which the selected language is widely spoken. Moreover, many smaller companies are able to use the Internet to quickly and cost-effectively offer their programs, services and products to a large number of students with less capital expenditure than previously required. We may have to reduce course fees or increase spending in response to competition in order to retain or attract students or pursue new market opportunities. As a result, our revenues and profitability may decrease. We cannot assure you that we will be able to compete successfully against current or future competitors. If we are unable to maintain our competitive position or otherwise respond to competitive pressures effectively, we may lose our market share and our profitability may be adversely affected.

Failure to adequately and promptly respond to changes in testing materials, admissions standards and technologies could cause our programs, services and products to be less attractive to students.

Admissions and assessment tests undergo continuous change, in terms of the focus of the subjects and questions tested, the format of the tests and the manner in which the tests are administered. For example, certain admissions and assessment tests in the United States now include an essay component, which required us to hire and train teachers to be able to analyze written essays that tend to be more subjective in nature and require a higher level of English proficiency. In addition, some admissions and assessment tests that were previously offered in paper format only are now offered in a computer-based testing format. These changes require us to continually update and enhance our test preparation materials and our teaching methods. Further, we understand the Chinese Ministry of Education has been discussing reforms of the curriculum of primary and secondary schools. Therefore, school curriculum will likely undergo changes, and our tutoring programs and materials will need to be adapted for such changes. Any inability to track and respond to these changes in a timely and cost-effective manner would make our programs, services and products less attractive to students, which may materially and adversely affect our reputation and ability to continue to attract students without a significant decrease in course fees.

If colleges, universities and other higher education institutions reduce their reliance on admissions and assessment tests, we may experience a decrease in demand for our test preparation courses and our business may be materially and adversely affected.

9

Table of Contents

We provide preparation courses for both overseas and domestic admissions and assessment tests. In the fiscal year ended May 31, 2011, we derived a significant portion of our revenues from test preparation courses. The success of our test preparation courses depends on the continued use of admissions and assessment tests as a requirement for admission or graduation. However, the use of admissions tests in China may decline or fall out of favor with educational institutions and government authorities. For example, in early 2005, the PRC Ministry of Education started reforming the CET 4 and the CET 6 exams. The reform, among other things, limited these exams only to college students starting from 2007 and has effectively limited the pool of potential students for our CET 4 and CET 6 exam preparation courses to college students only. More recently, educational institutions and government authorities in China have initiated discussions and conducted early experiments in China on school admissions. Generally, these discussions and experiments exhibit a trend of basing admissions decisions less on entrance exam scores and more on a combination of other factors, such as past academic record, extracurricular activities and comprehensive aptitude evaluations. There have been certain changes in some geographic areas in the way the high school entrance exam is administered. In 2009, 76 universities and colleges were allowed to recruit up to 5% of their students through independently administered tests according to a notice promulgated by the MOE, although students admitted in this manner still need to meet certain thresholds in the national college entrance exam. It has been reported that the number of such universities and colleges will further increase. If the use of admissions tests in China declines or falls out of favor with educational institutions and government authorities and if we fail to respond to these changes, the demand for certain of our services may decline, and our business may be materially and adversely affected.

In the United States, there has been a continuing debate regarding the usefulness of admissions and assessment tests to assess qualifications of applicants and many people have criticized the use of admissions and assessment tests as unfairly discriminating against certain test takers. If a large number of educational institutions abandon the use of existing admissions and assessment tests as a requirement for admission, without replacing them with other admissions and assessment tests, we may experience a decrease in demand for our test preparation courses and our business may be seriously harmed.

We have experienced and may continue to experience a decrease in our margins.

Many factors may cause our gross and net margins to decline. For example, there is a recent trend that the short-term language training and test preparation markets are moving towards smaller class sizes, especially for students between the ages of five and 12. This may have resulted from discretionary income increases for families in China, which cause students to be more willing and able to pay higher course fees for the more individualized attention that smaller classes can offer. In our fiscal year ended May 31, 2011, the average class size for our short-term language training and test preparation courses was approximately 15 students per class, which decreased from approximately 21 students per class in the previous fiscal year. Although our smaller-sized classes are highly profitable, they are marginally less profitable on average than our large classes. Our net margin for our fiscal year ended May 31, 2011 was 18.2%, down from 20.1% in the previous fiscal year. This decrease was partly due to the increase in demand for our smaller-sized classes. In addition, our new investments and acquisitions may also cause our margins to decline before we successfully integrate the acquired businesses into our operations and realize the full benefits of these investments and acquisitions. There is a risk that our margins could continue to decline in the future due to increasing demand for our smaller-sized classes and/or other factors.

New programs, services and products that we develop may compete with our current offerings.

We are constantly developing new programs, services and products to meet changes in student demands and respond to changes in testing materials, admissions standards, market needs and trends and technological changes. While some of the programs, services and products that we develop will expand our current offerings and increase student enrollments, others may compete with or make irrelevant our existing offerings without increasing our total student enrollments. For example, our online courses may take away students from our existing classroom-based courses, and our new schools and learning centers may take away students from our existing schools and learning centers. If we are unable to expand our program, service and product offerings while increasing our total student enrollments and profitability, our business and growth may be adversely affected.

10

Table of Contents

Our business is subject to fluctuations caused by seasonality or other factors beyond our control, which may cause our operating results to fluctuate from quarter to quarter. This may result in volatility and adversely affect the price of our ADSs.

We have experienced, and expect to continue to experience, seasonal fluctuations in our revenues and results of operations, primarily due to seasonal changes in student enrollments. Historically, our courses tend to have the largest student enrollments in our first fiscal quarter, which runs from June 1 to August 31 of each year, primarily because many students enroll in our courses during the summer vacation to enhance their foreign language skills and/or prepare for admissions and assessment tests in subsequent school terms. In addition, we have generally experienced larger student enrollments in our third fiscal quarter, which runs from December 1 to February 28 of each year, primarily because many students enroll in our language training and other courses during the winter school holidays. Our expenses, however, vary significantly and do not necessarily correspond with changes in our student enrollments and revenues. We make investments in marketing and promotion, teacher recruitment and training, and product development throughout the year. In addition, other factors beyond our control, such as special events that take place during a quarter when our student enrollment would normally be high, may have a negative impact on our student enrollments. For example, the Beijing Olympic Games held in August 2008 negatively impacted our business in the fiscal quarter ended August 31, 2008 due to transportation and security logistics arrangements in Beijing and some distractions from classes as the nation enjoyed the Olympic Games. We expect quarterly fluctuations in our revenues and results of operations to continue. These fluctuations could result in volatility and adversely affect the price of our ADSs. As our revenues grow, these seasonal fluctuations may become more pronounced.

Our historical financial and operating results are not indicative of our future performance; and our financial and operating results are difficult to forecast.

Our financial and operating results may not meet the expectations of public market analysts or investors, which could cause the price of our ADSs to decline. In addition to the fluctuations described above, our revenues, expenses and operating results may vary from quarter to quarter and from year to year in response to a variety of other factors beyond our control, including:

| • | general economic conditions; |

| • | regulations or actions pertaining to the provision of private educational services in China; |

| • | changes in consumers’ spending patterns; and |

| • | non-recurring charges incurred in connection with acquisitions or other extraordinary transactions or unexpected circumstances. |

Due to these and other factors, we believe that quarter-to-quarter comparisons of our operating results may not be indicative of our future performance, and therefore you should not rely on them to predict the future performance of our ADSs. In addition, our past results may not be indicative of future performance because of new businesses developed or acquired by us.

Our business is difficult to evaluate because we have limited experience generating net income from some of our newer services.

Historically, our core businesses have been English language training for adults and test preparation courses for college and graduate students. We started professional certification preparation programs in 2007, which include preparation for the PRC bar exam, certified public accountant exam, and the civil service exam. Also in 2007, we established our pre-school business with the opening of our first kindergarten in Beijing. In 2008, we launched our “New Oriental U-Can (Non-English)” training program, which targets middle and high school students in China from ages 13 to 18 who are preparing for the college entrance examination in China, known as the “gaokao.” The gaokao is required for admission to bachelor degree programs and most associate degree programs at colleges and universities in China. Some of these operations have not generated significant or any profit to date, and we have less experience responding quickly to changes, competing successfully and maintaining and expanding our brand in these areas without jeopardizing our brand in other areas. Consequently, there is limited operating history on which you can base your evaluation of the business and prospects of these relatively more recent operations.

11

Table of Contents

Our success depends on the continuing efforts of our senior management team and other key personnel, and our business may be harmed if we lose their services.

Our future success depends heavily upon the continuing services of the members of our senior management team, in particular, our founder, chairman and chief executive officer, Michael Minhong Yu, who has been our leader since our inception in 1993. If one or more of our senior executives or other key personnel are unable or unwilling to continue in their present positions, we may not be able to replace them easily or at all, and our business may be disrupted and our financial condition and results of operations may be materially and adversely affected. Competition for experienced management personnel in the private education sector is intense, the pool of qualified candidates is very limited, and we may not be able to retain the services of our senior executives or key personnel, or attract and retain high-quality senior executives or key personnel in the future. In addition, if any member of our senior management team or any of our other key personnel joins a competitor or forms a competing company, we may lose teachers, students, key professionals and staff members. Each of our executive officers and key employees has entered into a confidentiality and non-competition agreement with us. However, if any disputes arise between any of our senior executives or key personnel and us, it may be difficult to enforce these agreements against these individuals because of the uncertainties of China’s legal systems.

We generate a majority of our revenues from four cities in China. Any event negatively affecting the private education industry in these cities could have a material adverse effect on our overall business and results of operations.

We derived approximately 50% of our total net revenues for the fiscal year ended May 31, 2011 from our operations in Beijing, Shanghai, Wuhan and Guangzhou, and we expect these four cities to continue to constitute important sources of our revenues. If any of these cities experiences an event negatively affecting its private education industry, such as a serious economic downturn, a natural disaster or an outbreak of contagious disease, or if any of these cities adopts regulations relating to private education that place additional restrictions or burdens on us, our overall business and results of operations may be materially and adversely affected.

If we are not able to continually enhance our online programs, services and products and adapt them to rapid technological changes and student needs, we may lose market share and our business could be adversely affected.

The market for Internet-based educational programs, services and products is characterized by rapid technological changes and innovation, unpredictable product life cycles and user preferences. We have limited experience with generating revenues from online programs, services and products, and their results are largely uncertain. The increasing adoption of computer-based testing formats for admissions testing may lead more students to seek online test preparation courses. We must quickly modify our programs, services and products to adapt to changing student needs and preferences, technological advances and evolving Internet practices. Ongoing enhancement of our online offerings and related technology may entail significant expense and technical risk. We may fail to use new technologies effectively or adapt our online products or services and related technology on a timely and cost-effective basis. If our improvements to our online offerings and the related technology are delayed, result in systems interruptions or are not aligned with market expectations or preferences, we may lose market share and our business could be adversely affected.

Failure to maintain effective internal control over financial reporting could have a material and adverse effect on the trading price of our ADSs.

We are subject to the reporting obligations under the U.S. securities laws. Although our management concluded, and our independent registered public accounting firm reported, that we maintained effective internal control over financial reporting as of May 31, 2011, we cannot assure you that we will maintain effective internal control over financial reporting on an ongoing basis. If we fail to maintain effective internal control over financial reporting, we will not be able to conclude and our independent registered public accounting firm will not be able to report that we have effective internal control over financial reporting in accordance with the Sarbanes-Oxley Act of 2002 in our future annual report on Form 20-F covering the fiscal year in which this failure occurs. Effective internal control over financial reporting is necessary for us to produce reliable financial reports. Any failure to maintain effective internal control over financial reporting could result in the loss of investor confidence in the reliability of our financial statements, which in turn could have a material and adverse effect on the trading price of our ADSs. Furthermore, we may need to incur additional costs and use additional management and other resources as our business and operations further expand or in an effort to remediate any significant control deficiencies that may be identified in the future.

We do not have any liability or business disruption insurance, and a liability claim against us due to injuries suffered by our students or other people at our facilities could adversely affect our reputation and our financial results.

We could be held liable for accidents that occur at our schools, learning centers and other facilities, including indoor facilities where we organize certain summer camp activities and temporary housing facilities that we lease for our students from time to time. In the event of on-site food poisoning, personal injuries, fires or other accidents suffered by students or other people, we could face claims alleging that we were negligent, provided inadequate supervision or were otherwise liable for the injuries. We currently do not have any liability insurance or business disruption insurance. A successful liability claim against us due to injuries suffered by our students or other people at our facilities could adversely affect our reputation and our financial results. Even if unsuccessful, such a claim could cause unfavorable publicity, require substantial cost to defend and divert the time and attention of our management.

12

Table of Contents

Capacity constraints or system disruptions to our computer systems or websites could damage our reputation, limit our ability to retain students and increase student enrollments and require us to expend significant resources.

The performance and reliability of our online program infrastructure is critical to our reputation and ability to retain students and increase student enrollments. Any system error or failure, or a sudden and significant increase in traffic, could result in the difficulty of accessing our websites by our students or unavailability of our online programs. We cannot assure you that we will be able to timely expand our online program infrastructure to meet demand for such programs. Our computer systems and operations could be vulnerable to interruption or malfunction due to events beyond our control, including natural disasters and telecommunications failures. Our computer networks may also be vulnerable to unauthorized access, hacking, computer viruses and other security problems. A user who circumvents security measures could misappropriate proprietary information or cause interruptions or malfunctions in operations. Any interruption to our computer systems or operations could have a material adverse effect on our ability to retain students and increase student enrollments. Furthermore, we may be required to expend significant resources to protect against the threat of security breaches or to alleviate problems caused by these breaches.

Terrorist attacks, geopolitical uncertainty and international conflicts involving the U.S. and elsewhere may discourage more students from studying in the United States and elsewhere outside of China, which could cause declines in the student enrollments for our courses.

Terrorist attacks, geopolitical uncertainty and international conflicts involving the U.S. and elsewhere, such as those that took place on September 11, 2001, could have an adverse effect on our overseas test preparation courses and English language training courses. Such attacks may discourage students from studying in the United States and elsewhere outside of China and may also make it more difficult for Chinese students to obtain visas to study abroad. These factors could cause declines in the student enrollments for our test preparation and English language training courses and could have an adverse effect on our overall business and results of operations.

Risks Related to Our Corporate Structure

If the PRC government finds that the agreements that establish the structure for operating our China business do not comply with applicable PRC laws and regulations, we could be subject to severe penalties.

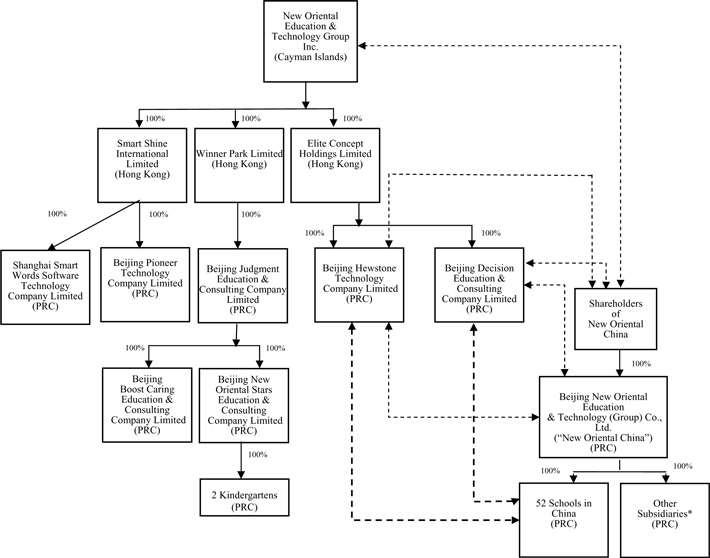

PRC laws and regulations currently require any foreign entity that invests in the education business in China to be an educational institution with relevant experience in providing educational services outside China. Our Cayman Islands holding company is not an educational institution and does not provide educational services. In addition, foreign ownership of primary and middle schools for students in grades one to nine is prohibited in the PRC. Accordingly, our wholly owned subsidiaries in China, which are considered foreign invested enterprises, are currently ineligible to apply for the required education licenses and permits in China. We conduct our education business in China through contractual arrangements with New Oriental China and its subsidiaries and shareholders. New Oriental China is our consolidated affiliated entity directly owned by our founders and/or their respective affiliates. New Oriental China’s subsidiaries hold the requisite licenses and permits necessary to conduct our education business and operate our schools, learning centers and bookstores in China. We have been and are expected to continue to be dependent on New Oriental China and its subsidiaries to operate our education business until we qualify for direct ownership of educational businesses in China. We have entered into contractual arrangements with New Oriental China and its subsidiaries, pursuant to which we, through our wholly owned subsidiaries in China, provide exclusive teaching support, new enrollment system support and other services to New Oriental China and its subsidiaries in exchange for payments from them. In addition, we have entered into agreements with New Oriental China and each of the shareholders of New Oriental China, which provide us with a substantial ability to control New Oriental China and its existing and future subsidiaries.

If we, any of our wholly owned subsidiaries, New Oriental China or any of its existing and future subsidiaries are found to be in violation of any existing or future PRC laws or regulations or fail to obtain or maintain any of the required permits or approvals, the relevant PRC regulatory authorities, including the Ministry of Education, which regulates the education industry, would have broad discretion in dealing with such violations, including:

| • | revoking the business and operating licenses of our PRC subsidiaries and affiliated entities; |

| • | discontinuing or restricting the operations of any related-party transactions among our PRC subsidiaries and affiliated entities; |

| • | imposing fines or other requirements with which we or our PRC subsidiaries and affiliated entities may not be able to comply; |

| • | requiring us or our PRC subsidiaries and affiliated entities to restructure the relevant ownership structure or operations; or |

13

Table of Contents

| • | restricting or prohibiting our use of the proceeds of our additional public offering to finance our business and operations in China. |

The imposition of any of these penalties could result in a material and adverse effect on our ability to conduct our business.

We rely on contractual arrangements with New Oriental China and its subsidiaries and shareholders for our China operations, which may not be as effective in providing operational control as direct ownership.

We have relied and expect to continue to rely on contractual arrangements with New Oriental China and its subsidiaries and shareholders to operate our education business. For a description of these contractual arrangements, see “Item 7. Major Shareholders and Related Party Transactions—B. Related Party Transactions—Contractual Arrangements with New Oriental China and Its Subsidiary and Shareholders.” These contractual arrangements may not be as effective in providing us with control over New Oriental China and its subsidiaries as direct ownership. If we had direct ownership of New Oriental China and its subsidiaries, we would be able to exercise our rights as a shareholder to effect changes in the board of directors of New Oriental China and its subsidiaries, which in turn could effect changes, subject to any applicable fiduciary obligations, at the management level. However, under the current contractual arrangements, as a legal matter, if New Oriental China or any of its subsidiaries and shareholders fails to perform its or his respective obligations under these contractual arrangements, we may have to incur substantial costs and spend other resources to enforce such arrangements, and rely on legal remedies under PRC law, including seeking specific performance or injunctive relief and claiming damages, which may not be effective. For example, if the shareholders of New Oriental China were to refuse to transfer their equity interest in New Oriental China to us or our designee when we exercise the call option pursuant to these contractual arrangements, or if they were otherwise to act in bad faith toward us, then we may have to take legal action to compel them to fulfill their contractual obligations. In addition, we may not be able to renew these contracts with New Oriental China and/or its subsidiaries and shareholders if the beneficial owners of New Oriental China do not act in the best interests of our company when conflicts of interest arise between their dual roles as beneficial owners and directors of both New Oriental China and our company.

Many of these contractual arrangements are governed by PRC law and provide for the resolution of disputes through arbitration in the PRC. Accordingly, these contracts would be interpreted in accordance with PRC law and any disputes would be resolved in accordance with PRC legal procedures. The legal environment in the PRC is not as developed as in some other jurisdictions, such as the United States. As a result, uncertainties in the PRC legal system could limit our ability to enforce these contractual arrangements. In the event we are unable to enforce these contractual arrangements, we may not be able to exert effective control over our affiliated entities, and our ability to conduct our business may be negatively affected.

The beneficial owners of New Oriental China may have potential conflicts of interest with us, which may materially and adversely affect our business and financial condition.

The beneficial owners of New Oriental China are also the founders and beneficial owners of our company. Some of them are directors of both New Oriental China and our company. Conflicts of interests between their dual roles as beneficial owners and directors of both New Oriental China and our company may arise. We cannot assure you that when conflicts of interest arise, any or all of these individuals will act in the best interests of our company or that conflicts of interests will be resolved in our favor. In addition, these individuals may breach or cause New Oriental China and its subsidiaries to breach or refuse to renew the existing contractual arrangements that allow us to effectively control New Oriental China and its subsidiaries and receive economic benefits from them. Currently, we do not have existing arrangements to address potential conflicts of interest between these individuals and our company. We rely on these individuals to abide by the laws of the Cayman Islands and China. These laws provide that directors owe a fiduciary duty to the company, which requires them to act in good faith and in the best interests of the company and not to use their positions for personal gain. If we cannot resolve any conflicts of interest or disputes between us and the beneficial owners of New Oriental China, we would have to rely on legal proceedings, which could result in disruption of our business, and the outcome of any such legal proceedings would be uncertain.

New Oriental China and its subsidiaries may be subject to significant limitations on their ability to operate private schools or make payments to related parties or otherwise be materially and adversely affected by changes in PRC laws and regulations.

14

Table of Contents

The principal regulations governing private education in China are The Law for Promoting Private Education (2003) and The Implementation Rules for the Law for Promoting Private Education (2004). Under these regulations, a private school may elect to be a school that does not require reasonable returns or a school that requires reasonable returns. At the end of each fiscal year, every private school is required to allocate a certain amount to its development fund for the construction or maintenance of the school or procurement or upgrade of educational equipment. In the case of a private school that requires reasonable returns, this amount shall be no less than 25% of annual net income of the school, while in the case of a private school that does not require reasonable returns, this amount shall be equivalent to no less than 25% of the annual increase in the net assets of the school, if any. A private school that requires reasonable returns must publicly disclose such election and additional information required under the regulations. A private school shall consider factors such as the school’s tuition, ratio of the funds used for education-related activities to the course fees collected, admission standards and educational quality when determining the percentage of the school’s net income that would be distributed to the investors as reasonable returns. However, none of the current PRC laws and regulations provides a formula or guidelines for determining “reasonable returns.” In addition, none of the current PRC laws and regulations sets forth different requirements or restrictions on a private school’s ability to operate its education business based on such school’s status as a school that requires reasonable returns or a school that does not require reasonable returns.

In some cities, our schools are registered as schools that require reasonable returns, while in other cities, our schools are registered as schools that do not require reasonable returns. The current PRC laws and regulations governing private education may be amended or replaced by new laws and regulations that (i) impose significant limitations on the ability of our schools to operate their business, charge course fees or make payments to related parties for services received, (ii) specify the formula for calculating “reasonable returns,” (iii) change the preferential tax treatment policies applicable to private schools, or (iv) restrict a private school’s ability to make payments to related parties for services. We cannot predict the timing and effects of any such amendments or new laws and regulations. Changes in PRC laws and regulations governing private education or otherwise affecting New Oriental China’s and its subsidiaries’ operations could materially and adversely affect our business prospects and results of operations. For example, if the PRC government imposes additional limitations on private schools’ ability to operate their business or restricts private schools from making payments to related parties for services, our ability to receive service fees from our affiliated schools may be limited or we may have to reorganize our group structure.