| RiverNorth/DoubleLine Strategic Income Fund | ||||||||||||||||||||||||||||

| SUMMARY SECTION | ||||||||||||||||||||||||||||

| Investment Objective | ||||||||||||||||||||||||||||

| The Fund’s investment objective is current income and overall total return. | ||||||||||||||||||||||||||||

| Fees And Expenses Of The Fund | ||||||||||||||||||||||||||||

| This table describes the fees and expenses that you may pay if you buy and hold shares of the Fund. | ||||||||||||||||||||||||||||

| Shareholder Fees (fees paid directly from your investment) | ||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||

| Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment) | ||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||

| Example | ||||||||||||||||||||||||||||

| This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year, and that the Fund’s operating expenses remain the same, except the first year which is covered by an expense cap and fee limitation agreement. Although your actual costs may be higher or lower, based on these assumptions, your costs would be: |

||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||

| Portfolio Turnover | ||||||||||||||||||||||||||||

| The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual operating expenses or in the Example affect the Fund’s performance. For the fiscal year ended September 30, 2012, the Fund’s portfolio turnover rate was 74% of the average value of its portfolio. | ||||||||||||||||||||||||||||

| Principal Investment Strategies | ||||||||||||||||||||||||||||

| The Fund’s adviser, after consultation with the sub-adviser, allocates the Fund’s assets among three principal strategies: Tactical Closed-end Fund Income strategy, Core Fixed Income strategy, and Opportunistic Income strategy. The amount allocated to each of the principal strategies may change depending on the adviser’s assessment of market risk, security valuations, market volatility, and the prospects for earning income and total return. The adviser determines which portion of the Fund’s assets are allocated to each strategy based on market conditions, although there is no set minimum for any strategy. Therefore, the amount allocated to any individual strategy may be between 0% and 100%. However, the adviser anticipates it will, under normal circumstances, allocate some portion of the Fund’s assets to each of the three strategies at any given time. The adviser manages the Tactical Closed-end Fund Income strategy. The sub-adviser manages the Core Fixed Income and Opportunistic Income strategies. The adviser’s and sub-adviser’s security selection process is described below. The adviser or sub-adviser may liquidate positions in order to implement a change in the adviser’s overall asset allocation or to generate cash to invest in more attractive opportunities. This may result in a larger portion of any net gains in the Fund being realized as short-term capital gains. In addition, the adviser, or sub-adviser may sell a security if there is a negative change in the fundamental or qualitative characteristics of the issuer or when its price approaches, meets or exceeds the target price established by the adviser or sub-adviser, as applicable. Tactical Closed-end Fund Income Strategy In implementing the Fund’s Tactical Closed-end Fund Income strategy, the adviser allocates that portion of the Fund’s investments among closed-end investment companies and exchange traded funds (“ETFs” and collectively, “Underlying Funds”) that invest primarily in income producing securities. The adviser considers a number of factors when selecting Underlying Funds, including fundamental and technical analysis to assess the relative risk and reward potential throughout the financial markets. The adviser may also allocate the Fund’s assets among cash and short term investments. The term “tactical” is used to indicate that the portion of the Fund’s assets allocated to this strategy will invest in closed-end funds to take advantage of pricing discrepancies in the closed-end fund market. In selecting closed-end funds, in particular, the adviser will opportunistically utilize a combination of short-term and longer-term trading strategies to seek to derive value from discount and premium spreads associated with closed-end funds. The adviser performs both a quantitative and qualitative analysis of closed-end funds prior to any closed-end fund being added to the Fund’s portfolio. This analysis and the adviser’s screening models and computer trading programs help determine when to buy and sell the closed-end funds in the Fund’s portfolio. If the Fund invests in affiliated closed-end funds, the Fund will only do so in accordance with the provisions of the Investment Company Act of 1940. The adviser may also be required to waive certain fees in the event the Fund invests in affiliated closed-end funds. The Underlying Funds in which the adviser invests generally focus on a broad range of fixed income strategies or sectors. The Underlying Funds may also invest in convertible securities, preferred securities, high yield securities, dividend strategies, covered call option strategies, real estate, energy, utility and other income-oriented strategies. Fixed income securities include exchange-traded notes (“ETNs”), which are debt securities whose returns are linked to a particular index. Fixed income securities may also include structured notes, which are debt securities whose returns are linked to the performance of a single equity security, a basket of equity securities, or an equity index. The Fund may invest in Underlying Funds that invest in securities rated below B- by Moody’s Investor Services, Inc., (commonly referred to as “junk bonds”) or that are in default. Junk bonds provide greater income and opportunity for gain, but entail greater risk of loss of principal. The issuer of a fixed income security may not be able to make interest and principal payments when due. With regard to junk bond issuers, the issuer’s capacity to pay interest and repay principal in accordance with the terms of the obligation may be more at risk. The adviser may invest the Tactical Closed-end Fund income assets, without limitation, in interest rate, index, total return and currency swap agreements. A swap is an agreement between two parties (known as counterparties) where one stream of payments is exchanged for another based on a specified principal amount. Swaps are typically used to gain, limit or manage exposure to fluctuations in interest rates, currency exchange rates or potential defaults by credit issuers. The adviser may use the Fund’s own net asset value or the return of closed-end funds as the underlying asset in a total return swap. The adviser utilizes a total return swap using the Fund’s return as the underlying asset in order for the Fund’s cash positions allocated to the swap to share in similar investment returns as the Fund itself while maintaining a sufficient cash position to meet liquidity needs in the Fund, including liquidity to invest in new investment opportunities. Core Fixed Income Strategy In implementing the Fund’s Core Fixed Income strategy, the sub-adviser allocates that portion of the Fund’s investments to a variety of fixed income instruments. These include securities issued or guaranteed by the United States Government, its agencies, instrumentalities or sponsored corporations; corporate obligations; agency mortgage-backed securities; non-agency mortgage-backed securities; commercial mortgage-backed securities; asset-backed securities; global developed credit (such as corporate obligations and foreign hybrid securities); foreign fixed income securities issued by corporations and governments; emerging market fixed income securities issued by corporations and governments; bank loans and assignments bearing fixed or variable interest rates of any maturity. There is no limit to the percentage of the strategy’s assets that may be allocated to any of the above-listed securities. The term “core” is used to indicate that the portion of the Fund’s assets allocated to this strategy will be the Fund’s principal fixed income holdings under normal circumstances. The Fund may invest in junk bonds, bank loans and assignments and credit default swaps of companies in the high yield universe. The sub-adviser allocates the high yield portfolio holdings broadly by industry and issuer in an attempt to reduce the impact of negative events for an industry or issuer. The sub-adviser defines junk bonds as fixed income instruments that are at the time of investment unrated or rated BB+ or lower by S&P or Ba1 or lower by Moody’s or the equivalent by any other nationally recognized statistical rating organization (“NRSRO”), or if unrated, of comparable quality in the opinion of the sub-adviser. High yield portfolio holdings are allocated broadly by industry and issuer in an attempt to reduce the impact of negative events for an industry or issuer. The sub-adviser may invest a portion of the assets allocated to the Core Fixed Income strategy in inverse floaters and interest-only and principal-only securities and a portion in fixed income instruments (including hybrid securities) issued or guaranteed by companies, financial institutions and government entities in emerging markets countries. The sub-adviser uses a controlled risk approach which includes consideration of:

Opportunistic Income Strategy In implementing the Fund’s Opportunistic Income strategy, the sub-adviser allocates this portion of the Fund’s investments to fixed income instruments and other investments including asset-backed securities; corporate bonds, including high-yield junk bonds; municipal bonds; and Real Estate Investment Trust (“REITs”). The strategy’s investments may include substantial investments in mortgage-backed securities, including non-agency residential mortgage-backed securities (“RMBS”). These RMBS investments have undergone extreme volatility over the past several years, driven primarily by high default rates and the securities being downgraded to “junk” status. However, the sub-adviser utilizes a unique investment process that first examines the macroeconomic status of the mortgage-backed sector. This analysis includes reviewing information regarding interest rates, yield curves and spreads, credit analysis of the issuers and a general analysis of the markets generally. From this detailed analysis, along with assessment of other economic data including market trends, unemployment data and pending legislation, the sub-adviser identifies subsectors within the mortgage sector which offer the highest potential for return. The sub-adviser then applies a qualitative analysis of potential investments looking at factors such as duration, level of delinquencies and default history. Finally, the sub-adviser performs a quantitative analysis of the potential investment, essentially performing a stress test of the potential investment’s underlying portfolio of mortgages. Only when a potential investment has passed the sub-adviser’s careful screening will it be added to the strategy’s portfolio. The sub-adviser may also utilize derivative instruments, including futures contracts, options and swaps as a substitute for taking positions in fixed income instruments, to hedge certain positions held in the strategy or to reduce exposure to other risks. The sub-adviser places no limits on the duration of the strategy’s investment portfolio. The term “opportunistic” is used to indicate that the portion of the Fund’s allocated to this strategy will be invested when certain market conditions exist that offer potentially attractive risk adjusted returns. |

||||||||||||||||||||||||||||

| Principal Risks | ||||||||||||||||||||||||||||

| All mutual funds carry a certain amount of risk. The Fund’s returns will vary and you could lose money on your investment in the Fund. An investment in the Fund is not a deposit of a bank and is not insured or guaranteed by the FDIC or any other government agency. Below is a summary of the principal risks of investing in the Fund. Asset-Backed Securities Investment Risk. The Fund may run the risk that the impairment of the value of the assets (whether tangible or intangible) underlying a security in which the Fund invests such as non-payment of loans, will result in a reduction in the value of the security. Borrowing Risk. The Fund may borrow amounts up to one-third of the value of total assets, but it will not borrow more than 5% of the value of its total assets except to satisfy redemption requests or for other temporary purposes. Such borrowings would result in increased expense to the Fund and, while they are outstanding, would magnify increases or decreases in the value of Fund shares. The Fund will not purchase additional portfolio securities while outstanding borrowings exceed 5% of the value of its total assets. Convertible Security Risk. The market value of convertible securities and other debt securities tends to fall when prevailing interest rates rise. The value of convertible securities also tends to change whenever the market value of the underlying common or preferred stock fluctuates. Defaulted Securities Risk. Defaulted securities carry with them the risk of the uncertainty of repayment and obligations of the distressed issuers. Derivatives Risk. To the extent the Fund invests in derivative securities, there is the risk that an insolvency of the counterparty to a derivative instrument could cause the Fund to lose all or substantially all of its investment in the derivative instrument, as well as the benefits derived therefrom. Emerging Markets Risk. Countries with emerging markets may have relatively unstable governments, social and legal systems that do not protect shareholders, economies based on only a few industries, and inefficient securities markets. Exchange-Traded Note Risk. The Fund may invest in ETNs, which are notes representing unsecured debt of the issuer. ETNs are typically linked to the performance of an index plus a specified rate of interest that could be earned on cash collateral. The value of an ETN may be influenced by time to maturity, level of supply and demand for the ETN, volatility and lack of liquidity in underlying markets, changes in the applicable interest rates, changes in the issuer’s credit rating and economic, legal, political or geographic events that affect the referenced index. There may be restrictions on the Fund’s right to redeem its investment in an ETN, and there may be limited availability of a secondary market. Fixed Income Risk. The Fund may invest directly or indirectly through Underlying Funds that invest in fixed income securities, including high yield junk bonds. Fixed income securities increase or decrease in value based on changes in interest rates. If interest rates increase, the value of the Fund’s fixed income securities generally declines. On the other hand, if interest rates fall, the value of the fixed income securities generally increases. Junk bonds provide greater income and opportunity for gain, but entail greater risk of loss of principal. The issuer of a fixed income security may not be able to make interest and principal payments when due. With regard to junk bond issuers, the issuer’s capacity to pay interest and repay principal in accordance with the terms of the obligation may be more at risk. Foreign Investing Risk. Investments in foreign securities may be affected by currency controls and exchange rates, different accounting, auditing, financial reporting, and legal standards and practices; expropriation; changes in tax policy; greater market volatility; differing securities market structures; higher transaction costs; and various administrative difficulties, such as delays in clearing and settling portfolio transactions or in receiving payment of dividends. These risks may be heightened in connection with investments in emerging or developing countries. Liquidity Risk. If the Fund invests in illiquid assets, or if asset become illiquid there may be no willing buyer of the securities and the Fund may have to sell those securities at a lower price or may not be able to sell the securities at all each of which would have a negative effect on performance. Management Risk. The adviser’s and sub-adviser’s judgments about the attractiveness, value and potential appreciation of a particular asset class or individual security in which the Fund invests may prove to be incorrect and there is no guarantee that the adviser’s or sub-adviser’s judgments will produce the desired results. Market Risk. Overall stock market risks may also affect the value of the Fund. Factors such as domestic economic growth and market conditions, interest rate levels, and political events affect the securities markets. Mortgage-Backed Securities Risk. Mortgage-backed securities have several risks, including:

Rating Agency Risk. Ratings agencies such as S&P, Moody’s or other NRSRO provide ratings on debt securities based on their analyses of information they deem relevant. Ratings are essentially opinions or judgments of the credit quality of an issuer and may prove to be inaccurate. In addition, there may be a delay between events or circumstances adversely affecting the ability of an issuer to pay interest and or repay principal and a NRSRO’s decision to downgrade a security. REIT Risk. The value of equity REITs may be affected by changes in the value of the underlying property owned by the REITs, while the value of mortgage REITs may be affected by the quality of any credit extended. Investment in REITs involves risks similar to those associated with investing in small capitalization companies, and REITs (especially mortgage REITs) are subject to interest rate risks. Because REITs incur expenses like management fees, investments in REITs also add an additional layer of expenses. Security Risk. The value of the Fund may decrease in response to the activities and financial prospects of individual securities in the Fund’s portfolio. Structured Notes Risk. Structured notes are subject to a number of fixed income risks including general market risk, interest rate risk, and the risk that the issuer on the note may fail to make interest and/or principal payments when due, or may default on its obligations entirely. In addition, as a result of the imbedded derivative features, structured notes generally are subject to more risk than investing in a simple note or bond issued by the same issuer. Swap Risk. The Fund may invest in interest rate, index, total return, currency and credit default swap agreements. The degree to which the Fund may invest in these instruments is not limited. All of these agreements are considered derivatives. Swaps could result in losses if interest or foreign currency exchange rates or credit quality changes are not correctly anticipated by the adviser. Total return swaps could result in losses if the reference index, security, or investments do not perform as anticipated. Credit default swaps can increase Fund exposure to credit risk and could result in losses if the adviser does not correctly evaluate the creditworthiness of the company or government on which the credit default swap is based. The use of swaps may not always be successful; using them could lower Fund total return, their prices can be highly volatile, and the potential loss from the use of swaps can exceed a Fund’s initial investment in such instruments. Also, the other party to a swap agreement could default on its obligations or refuse to cash out a Fund’s investment at a reasonable price, which could turn an expected gain into a loss. Underlying Fund Risk. The Fund will incur higher and duplicative expenses when it invests in Underlying Funds. There is also the risk that the Fund may suffer losses due to the investment practices of the Underlying Funds (such as the use of derivatives). The ETFs in which the Fund invests may not be able to replicate exactly the performance of the indices they track, due to transactions costs and other expenses of the ETFs. The shares of closed-end funds frequently trade at a discount to their net asset value. There can be no assurance that the market discount on shares of any closed-end fund purchased by the Fund will ever decrease, and it is possible that the discount may increase. |

||||||||||||||||||||||||||||

| Performance | ||||||||||||||||||||||||||||

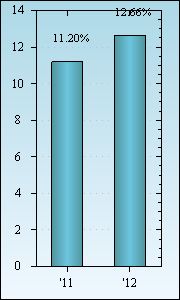

| The bar chart below shows how the Fund’s investment results have varied from year to year. The table below shows how the Fund’s average annual total returns compare over time to those of a broad-based securities market index. This information provides some indication of the risks of investing in the Fund. Past performance of the Fund (before and after taxes) is no guarantee of how it will perform in the future. Performance for the Fund is updated monthly and may be obtained online at www.RiverNorthFunds.com or by calling 1.888.848-7569. | ||||||||||||||||||||||||||||

| Calendar Year Total Returns through December 31, 2012 – Class I | ||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||

Highest/Lowest quarterly results during this time period were – Class I Shares:

|

||||||||||||||||||||||||||||

| Average Annual Total Returns (as of December 31, 2012) | ||||||||||||||||||||||||||||

|

||||||||||||||||||||||||||||

| After-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or IRAs. The Barclays Capital U.S. Aggregate Bond Index (“Barclays Index”) measures the performance of investment-grade fixed-rate debt obligations of U.S. and foreign corporations that are taxable, dollar-denominated, non-convertible, publicly traded, and with maturities of at least 1 year. The Barclay Index assumes reinvestment of all distributions. |

||||||||||||||||||||||||||||