NORTH AMERICAN ENERGY PARTNERS INC.

ANNUAL INFORMATION FORM

June 6, 2012

NOA

Table of Contents

| A. Explanatory Notes | 1 | |||||

| Industry Data and Forecasts |

1 | |||||

| Caution Regarding Forward-Looking Information |

1 | |||||

| Non-GAAP Financial Measures |

1 | |||||

| B. Corporate Structure | 2 | |||||

| North American Energy Partners Inc. |

2 | |||||

| Subsidiaries |

3 | |||||

| C. Business Overview | 4 | |||||

| Business Overview |

4 | |||||

| History and Development of the Business |

4 | |||||

| Competitive Strengths |

5 | |||||

| Operations Overview |

6 | |||||

| Our Strategy |

6 | |||||

| D. Projects, Competition and Major Suppliers | 7 | |||||

| Active Projects |

7 | |||||

| Recently Completed Projects |

8 | |||||

| Competition |

9 | |||||

| Major Suppliers |

9 | |||||

| E. Resources and Key Trends | 10 | |||||

| Fleet and Equipment |

10 | |||||

| Credit Facilities |

12 | |||||

| Variability of Results |

12 | |||||

| F. Legal and Labour Matters | 12 | |||||

| Laws and Regulations and Environmental Matters |

12 | |||||

| Legal Proceedings and Regulatory Actions |

13 | |||||

| Employees and Labour Relations |

13 | |||||

| G. Description of Securities, Rights Plans and Agreements | 13 | |||||

| Capital Structure |

13 | |||||

| Shareholder Rights Plan |

14 | |||||

| Registration Rights Agreement |

14 | |||||

| 9.125% Series 1 Debentures |

15 | |||||

| H. Material Contracts | 16 | |||||

| I. Directors and Officers | 16 | |||||

| Director and Officer Information |

16 | |||||

| Interest of Management and Others in Material Transactions |

20 | |||||

| J. The Board and Board Committees | 20 | |||||

| Audit Committee |

20 | |||||

| Compensation Committee |

20 | |||||

| Governance Committee |

21 | |||||

| Health, Safety, Environment and Business Risk Committee |

21 | |||||

| K. Forward-Looking Information, Assumptions and Risk Factors | 21 | |||||

| Forward-Looking Information |

21 | |||||

| Assumptions |

22 | |||||

| Business Risk Factors |

22 | |||||

| Risks Factors Related to Our Common Shares |

28 | |||||

| Risk Factors Relating to Debt Securities |

30 | |||||

| Quantitative and Qualitative Disclosures about Market Risk |

31 | |||||

| L. General Matters | 31 | |||||

| Additional Information |

31 | |||||

| Transfer Agent and Registrar |

32 | |||||

| Experts |

32 | |||||

| Glossary of Terms |

32 | |||||

| EXHIBIT A | 33 | |||||

| Audit Committee Charter |

33 | |||||

NOA

Annual Information Form

June 6, 2012

A. Explanatory Notes

The information in this Annual Information Form (AIF) is stated as at June 6, 2012, unless otherwise indicated. For an explanation of the capitalized terms and expressions and certain defined terms, please refer to the “Glossary of Terms” at the end of this AIF. All references in this AIF to “we”, “us”, “NAEPI” or the “Company”, unless the context otherwise requires, mean North American Energy Partners Inc. and its Subsidiaries (as defined below). Except where otherwise specifically indicated, all dollar amounts are expressed in Canadian dollars. For additional information and details, readers are referred to the audited consolidated financial statements for the year ended March 31, 2012 and notes there to, as well as the accompanying annual Management’s Discussion and Analysis (“annual MD&A”) which are available on the Canadian Securities Administrators’ SEDAR System at www.sedar.com, the Securities and Exchange Commission’s website at www.sec.gov and our company website at www.nacg.ca.

Industry Data and Forecasts

This AIF includes industry data and forecasts that we have obtained from publicly available information, various industry publications, other published industry sources and our internal data and estimates. For example, information regarding actual and anticipated production as well as reserves and current and scheduled projects in the Canadian oil sands was obtained from the Energy Resources Conservation Board (“ERCB”) and the Canadian Energy Research Institute. Information regarding historical capital expenditures in the oil sands was obtained from the Canadian Association of Petroleum Producers (“CAPP”).

Industry publications and other published industry sources generally indicate that the information contained therein was obtained from sources believed to be reliable, but do not guarantee the accuracy and completeness of such information. Although we believe that these publications and reports are reliable, we have not independently verified the data. Our internal data, estimates and forecasts are based upon information obtained from our customers, trade and business organizations and other contacts in the markets in which we operate and our management's understanding of industry conditions. Although we believe that such information is reliable, we have not had such information verified by any independent sources. References to barrels of oil related to the oil sands in this document are quoted directly from source documents and refer to both barrels of bitumen and barrels of bitumen that have been upgraded into synthetic crude oil, which is considered synthetic because its original hydrocarbon mark has been altered in the upgrading process. We understand that there is generally some shrinkage of bitumen volumes through the upgrading process. The shrinkage is approximately 11% according to the Canadian National Energy Board. We have not made any estimates or calculations with regard to these volumes and have quoted these volumes as they appeared in the related source documents.

Caution Regarding Forward-Looking Information

Our AIF is intended to enable readers to gain an understanding of our current results and financial position. To do so, we provide material information and analysis about the Company and our business at a point in time in the context of our historical and possible future development. Accordingly, certain sections of this report contain forward-looking information that is based on current plans and expectations. This forward-looking information is affected by risks, assumptions and uncertainties that could have a material impact on future prospects. Please refer to “Forward-Looking Information, Assumptions and Risk Factors” for a discussion of the risks, assumptions and uncertainties related to such information. Readers are cautioned that actual events and results may vary from those anticipated.

Non-GAAP Financial Measures

The body of generally accepted accounting principles applicable to us is commonly referred to as “GAAP”. A non-GAAP financial measure is generally defined by the Securities and Exchange Commission (SEC) and by the Canadian securities regulatory authorities as one that purports to measure historical or future financial performance, financial position or cash flows, but excludes or includes amounts that would not be so adjusted in the most comparable GAAP measures. In our AIF, we use non-GAAP financial measures such as “net income before interest expense, income taxes, depreciation and amortization” (EBITDA) and “Consolidated EBITDA” (as defined in our fourth amended and restated credit agreement, our “credit agreement”).

Consolidated EBITDA is defined as EBITDA, excluding the effects of unrealized foreign exchange gain or loss, realized and unrealized gain or loss on derivative financial instruments, non-cash stock-based compensation expense, gain or loss on disposal of plant and equipment, the impairment of goodwill, the amendment related to the $42.5 million revenue writedown on the Canadian Natural1 overburden removal contract (described in the “Explanatory Notes - Significant Business Event” section of our annual MD&A, which section is expressly incorporated by reference into this AIF) and certain other non-cash items included in the calculation of net income.

| 1 | Canadian Natural Resources Limited (Canadian Natural), owner and operator of the Horizon Oil Sands mine site. |

| 2012 Annual Information Form | 1 |

We believe that EBITDA is a meaningful measure of the performance of our business because it excludes items, such as interest, income taxes, depreciation and amortization that are not directly related to the operating performance of our business. Management reviews EBITDA to determine whether plant and equipment are being allocated efficiently. In addition, our credit facility requires us to maintain a minimum interest coverage ratio and a maximum senior leverage ratio, both of which are calculated using Consolidated EBITDA. Non-compliance with these financial covenants could result in a requirement to immediately repay all amounts outstanding under our credit facility.

As EBITDA and Consolidated EBITDA are non-GAAP financial measures, our computations of EBITDA and Consolidated EBITDA may vary from others in our industry. EBITDA and Consolidated EBITDA should not be considered as alternatives to operating income or net income as measures of operating performance or cash flows as measures of liquidity. EBITDA and Consolidated EBITDA have important limitations as analytical tools and should not be considered in isolation or as substitutes for analysis of our results as reported under US GAAP. For example, EBITDA and Consolidated EBITDA do not:

| • | reflect our cash expenditures or requirements for capital expenditures or capital commitments; |

| • | reflect changes in our cash requirements for our working capital needs; |

| • | reflect the interest expense or the cash requirements necessary to service interest or principal payments on our debt; |

| • | include tax payments that represent a reduction in cash available to us; or |

| • | reflect any cash requirements for assets being depreciated and amortized that may have to be replaced in the future. |

Consolidated EBITDA excludes certain unrealized losses, which may ultimately result in a liability that may need to be paid and in the case of certain excluded realized losses, represents an actual use of cash during the period.

Where relevant, particularly for earnings-based measures, we provide tables in this document that reconcile non-GAAP measures used to amounts reported on the face of the consolidated financial statements.

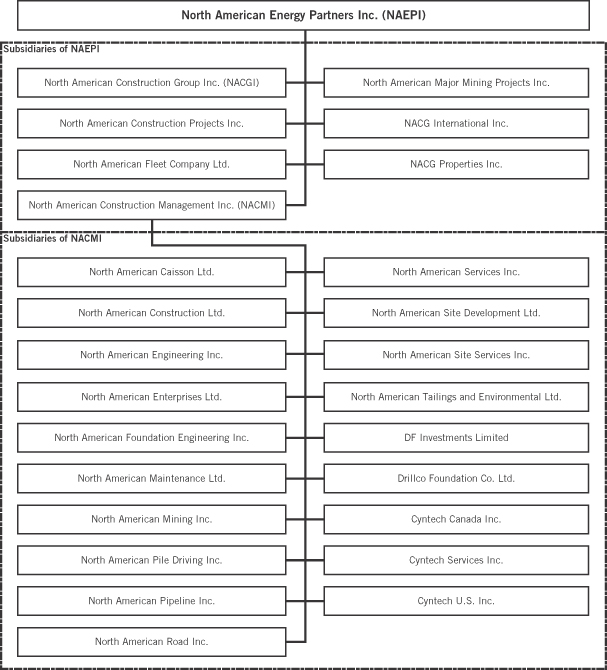

B. Corporate Structure

North American Energy Partners Inc.

The Company was amalgamated under the Canada Business Corporations Act on November 28, 2006, and was the entity continuing from the amalgamation of NACG Holdings Inc. with its wholly-owned subsidiaries, NACG Preferred Corp. and North American Energy Partners Inc. The amalgamated entity continued under the name North American Energy Partners Inc. (“NAEPI”).

| 2 | 2012 Annual Information Form |

NOA

Subsidiaries

NAEPI includes its wholly-owned subsidiaries North American Construction Group Inc. (“NACGI”), North American Construction Projects Inc., North American Fleet Company Ltd., NACG International Inc., North American Major Mining Projects Inc., NACG Properties Inc., North American Construction Management Inc. (“NACMI”) along with the wholly-owned operating subsidiaries of NACMI. The chart below depicts our current corporate structure with respect to each of our direct subsidiaries and indirect subsidiaries (collectively the “Subsidiaries”):

NAEPI and the Subsidiaries are all corporations subsisting under the Business Corporations Act (Alberta), except NACGI, NACG International Inc., North American Construction Ltd. and North American Foundation Engineering Inc., which are corporations subsisting under the Canada Business Corporations Act, Drillco Foundation Co. Ltd. and DF Investments Limited, which are corporations subsisting under the Business Corporations Act (Ontario) and Cyntech U.S. Inc., which is a corporation subsisting under the Texas Business Organizations Code.

| 2012 Annual Information Form | 3 |

C. Business Overview

Business Overview

We provide a wide range of heavy construction and mining, piling and pipeline installation services to customers in the Canadian oil sands, industrial construction, commercial and public construction and pipeline construction markets. Our primary market is the Canadian oil sands, where we support our customers’ mining operations and capital projects. While we provide services through all stages of an oil sands project’s lifecycle, our core focus is on providing recurring services, such as contract mining, during the operational phase. For the year ended March 31, 2012, recurring services represented 87% of our oil sands business. Our principal oil sands customers include all four producers that are currently mining bitumen in Alberta: Syncrude2, Suncor3, Shell4, and Canadian Natural. We focus on building long-term relationships with our customers and have provided services to each of them since inception of their respective projects. In the case of Syncrude and Suncor, these relationships span over 30 years.

We believe that we operate the largest fleet of equipment of any contract resource services provider in the oil sands. Our total fleet (owned, leased and rented) includes approximately 900 pieces of diversified heavy construction equipment supported by over 750 pieces of ancillary equipment. While our expertise covers mining, heavy construction, tailings management and mine reclamation services, underground services installation (fire lines, sewer, water, etc.) for industrial projects and piling and pipeline installation in many different locations, we have a specific capability operating in the harsh climate and difficult terrain of northern Canada, particularly in the Canadian oil sands.

We believe that our excellent safety record, coupled with our significant oil sands knowledge, experience, long-term customer relationships, equipment capacity, scale of operations and broad service offering, differentiate us from our competition. As such, our capabilities enable us to support our customers’ recurring services needs with respect to their new oil sands mining developments and expansions.¿

While our mining services are primarily focused on the oil sands, we believe that we have demonstrated our ability to successfully apply our oil sands knowledge and technology and put it to work in other resource development projects. We believe we are positioned to respond to the needs of a wide range of other resource developers and we remain committed to expanding our operations outside of the Canadian oil sands.

History and Development of the Business

We completed an Initial Public Offering (“IPO”) of our common shares and a related reorganization in November 2006 in order to reduce the leverage on our balance sheet and provide additional financial capacity as we pursued our growth strategy. The common shares began trading on the New York Stock Exchange on November 22, 2006 and became fully tradable on the Toronto Stock Exchange on November 28, 2006. Through the IPO, we raised a total of $152.6 million in net proceeds. These funds were primarily used to restructure our balance sheet, reduce outstanding debt and buy out a number of equipment operating leases.

The following is a summary of the significant events that have influenced our business over the past three years:

| • | In the oil sands, the economic downturn during fiscal 2009 contributed to a temporary reduction in demand for project development services supporting new construction. The economy began to stabilize in the second half of fiscal 2010 and by the end of fiscal 2011, commodity prices had largely recovered. Oil sands producers began announcing plans to restart construction on previously postponed expansions and greenfield projects, signalling a return to growth in the oil sands. In fiscal 2012, the announcements started translating into contracts, strengthening our project backlog with awards at new and existing oil sands mines and various steam assisted, gravity drainage (“SAGD”) developments. In the Heavy Construction and Mining segment, we were awarded construction contracts with major oil sands customers including: |

| • | contracts for the shear key and MSE wall for the Muskeg River Mine Relocation Project; |

| • | the initial earthworks contract for the Joslyn North Mine Project; |

| • | the initial site development contract for the BlackGold SAGD Project; |

| • | the initial site development contract for the Kirby SAGD Project; and |

| • | the initial site development contract for the MacKay River SAGD Project. |

| 2 | Syncrude Canada Ltd. (Syncrude) – operator of the oil sands mining and extraction operations for the Syncrude Project, a joint venture amongst Canadian Oil Sands Limited (37%), Imperial Oil Resources (25%), Suncor Energy Oil and Gas Partnership (12%), Sinopec Oil Sands Partnership (9%), Nexen Oil Sands Partnership (7%), Murphy Oil Company Ltd. (5%) and Mocal Energy Limited (5%). |

| 3 | Suncor Energy Inc. (Suncor). |

| 4 | Shell Canada Energy (Shell), a division of Shell Canada Limited, which is the operator of the oil sands mining and extraction operations on behalf of Athabasca Oil Sands Project (AOSP), a joint venture amongst Shell Canada Limited (60%), Chevron Canada Limited (20%) and Marathon Oil Corporation (20%). |

| ¿ | This paragraph contains forward-looking information. Please refer to “Forward-Looking Information, Assumptions and Risk Factors” for a discussion of the risks and uncertainties related to such information. |

| 4 | 2012 Annual Information Form |

NOA

| • | Demand for recurring services in the oil sands remained steady throughout the downturn, reflecting the inherent stability of operational oil sands mines. In the Heavy Construction and Mining segment, we were awarded multi-year agreements with major oil sands customers including: |

| • | a three-year master services agreement with Shell; |

| • | a three-year muskeg removal contract with Shell; |

| • | a four-year master services agreement with Syncrude; and |

| • | a five-year master services agreement with Suncor. |

| • | In addition to these master services contracts, we recently reached an agreement with Canadian Natural on amendments to our 10-year overburden removal and tailings dyke construction services contract with Canadian Natural (“the Canadian Natural contract”). The amending agreement included a $34.1 million settlement of past claims under the original contract. The general terms of the original contract related to work scope remained in place, however, these services will now be performed under a revised payment structure that carries less risk to us than the unit-rate structure it replaces. The new payment structure carries a base margin and provides for the opportunity to enhance margins, by meeting mutually agreed upon performance targets. |

| • | We also identified a service opportunity related to new regulations governing tailings pond management (Directive 74) and moved quickly to develop and market a capability that supports our clients’ requirements. While this industry development is still in its early stages, we have already been involved in the construction of several pilot plants and some of the initial commercial developments. |

| • | In the industrial sector outside of the oil sands, we have seen activity strengthening over the last three years. This has benefitted both our Piling segment and our Heavy Construction and Mining segment. In Saskatchewan, refinery and mine development projects have continued to generate opportunities for piling and light industrial services. Strong demand for industrial services in Western Canada has also created opportunities for us to expand our light industrial services to above-ground construction. As an example, we are currently erecting 7,000 tons of structural steel for the Mt. Milligan Copper/Gold Project in British Columbia. |

| • | In the commercial construction sector, activity levels began to recover in fiscal 2011 and continued to build momentum in fiscal 2012. This is reflected in the revenue and margin growth achieved by our Piling segment over the past three years. In addition to benefitting from improving market conditions, we have continued to position ourselves for the future by expanding our geographic reach and service offering with the acquisition of two piling companies. In fiscal 2010, we completed the acquisition of DF Investments Inc. and its subsidiary, Drillco Foundation Co. Ltd. This transaction established our presence in the large Ontario construction market. We followed up with the acquisition of Cyntech Corporation5 in fiscal 2011. Cyntech provided us with screw piling capabilities, a patented pipeline anchoring system and maintenance capabilities for above-ground storage tanks, while also bringing us international business opportunities. |

| • | In the pipeline sector, the recession led to a scaling back of plans for new pipeline construction and expansion projects. While companies in the late planning stages of specific projects opted to move forward, competition for these projects became intense and was characterized by a high number of bidders willing to assume more risk at lower margins. During fiscal 2010 and fiscal 2011, we secured a number of unit-price contracts, but were unable to achieve reasonable margins or risk levels on this work. We ultimately posted losses, or at best, break-even performance on our pipeline work during this period. While the contracting environment has begun to improve, we have altered our strategy to consider only cost-reimbursable contracts going forward. We are also pursuing stable maintenance pipeline work and are currently providing integrity services to Enbridge under a multi-year master services agreement with a cost-reimbursable structure. |

| • | On a company-wide basis, we have undertaken several strategic initiatives over the past three years to help us respond to changing market conditions and prepare for the future. Our initiatives include strengthening our financial position with a debt refinancing, capital spending reductions, organizational restructuring, cost-reduction initiatives and focused cash management. |

Competitive Strengths

We believe our competitive strengths are as follows:

Leading market position

We believe we are the largest provider of contract mining services in the Canadian oil sands area and we believe we are the largest piling foundations installer in Western Canada. We have operated in Western Canada for over 50 years and have participated in every significant oil sands mining project since operators first began developing this resource over 30 years ago. This has given us extensive experience operating in the challenging working conditions created by the harsh climate and difficult terrain of the oil sands and Northern Canada. We have amassed what we believe is the largest fleet of any contract services provider in the oil sands. We believe the combination of our significant size, extensive experience and broad service offerings makes us one of only a few companies capable of taking on long-term, large-scale mining and heavy construction projects in the oil sands.

| 5 | We acquired the assets of Cyntech Corporation, a private Alberta-based company and Cyntech Anchor System LLC, its US based subsidiary (collectively “Cyntech Corporation”), as at November 1, 2010. To facilitate the acquisition of Cyntech Corporation’s assets, we established two Canadian subsidiaries: Cyntech Canada Inc.; and Cyntech Services Inc.; and one US subsidiary, Cyntech U.S. Inc. (collectively “Cyntech”). |

| 2012 Annual Information Form | 5 |

Large, well-maintained equipment fleet

As of March 31, 2012, we had a heavy equipment fleet of approximately 900 owned, leased and rented units, made up of shovels, excavators, trucks and dozers as well as loaders, graders, scrapers, cranes, pipe layers and drill rigs. Over the past three years we have invested over $318.3 million in our fleet including upgrades, new equipment purchases and equipment leases. As a result, we believe we have an unmatched, modern fleet of equipment to service our clients’ needs. Our fleet includes some of the largest shovels in the world, which are designed for use in some of the largest earthmoving and mining applications globally. Being the only contractor in the oil sands to operate shovels of this size and one of only two contractors to operate trucks larger than 240 tons capacity gives us a competitive advantage with respect to both skill base and equipment availability. The size and diversity of our fleet provides us with the potential to respond on short notice and provide customized fleet solutions for each specific job.

A well-maintained fleet is critical in the harsh climatic and environmental conditions we encounter. We operate three significant maintenance and repair centers on our customers’ oil sands sites. These facilities are capable of accommodating the largest pieces of equipment in our fleet. In addition, we have a major repair facility located at our administrative offices near Edmonton, Alberta. This facility can perform the same major maintenance and repair activities as our facilities in the oil sands and provides back-up maintenance and repair requirements for oil sands equipment. We believe our combination of onsite and offsite service capabilities increases our efficiency. This, in turn, reduces costs and increases our equipment utilization, thereby enhancing our competitive edge and profitability.

Broad service offering across a project’s lifecycle

We are considered to be a “first-in, last-out” service provider in the oil sands because we provide services through the entire lifecycle of an oil sands project. Our work typically begins with the initial consulting services provided during the planning phase, including review of constructability, engineering and budgeting. This leads into the construction phase during which we provide a fuller range of services, including clearing, muskeg removal, site preparation, mine infrastructure construction, piling, pipeline and underground utility installation. As the mine moves into production, we support the preparation of the mine by providing ongoing site maintenance and upgrading, equipment and labour supply, overburden removal and land reclamation. Given the long-term nature of oil sands projects, we believe that our broad service offering has enabled us to establish ongoing relationships with our customers through a continuous supply of services as we transition from one stage of the project to the next.

Long-term customer relationships

We have established strong, long-term relationships with major oil sands producers and conventional oil and gas producers. Our largest oil sands customers by revenue are Syncrude, Suncor, Shell Canada and Canadian Natural. We have worked with each of these customers since they began operations in the oil sands. In the case of Syncrude and Suncor, our relationships date back over 30 years. The longevity of our customer relationships reflects our ability to deliver a strong safety and performance record, a well-maintained, highly capable fleet with specific equipment dedicated to individual customers and a staff of well-trained, experienced supervisors, operators and mechanics. In addition, our practice of maintaining offices and maintenance facilities directly on most of our oil sands customers’ sites enhances the relationship. Our proximity and close working relationships typically result in advance notice of projects, enabling us to anticipate our customers’ needs and align our resources accordingly.

Operational flexibility

The combination of our onsite fleets and relationships with multiple oil sands operators makes it possible for us to easily and cost-efficiently transfer equipment and other resources among projects. This keeps us highly responsive to customer needs and is an essential element in securing recurring services, where business lead times are short and the work is usually conducted outside of long-term contracts. This serves as a barrier to potential new competitors who may be unwilling to take on the risk of mobilizing a fleet for a single project or without the benefit of secure contracts. The fact that we work on every major site in the oil sands contributes to our flexibility, enhances the stability of our business model and enables us to continue bidding profitably on new contracts. This has helped us through the recent economic downturn.

Operations Overview

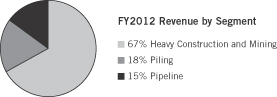

Our business is organized into three operating segments: (i) Heavy Construction and Mining, (ii) Piling and (iii) Pipeline. For a discussion of our operations overview, see the “Operations Overview” section of our annual MD&A, which section is expressly incorporated by reference into this AIF.

Our Strategy

Our strategy is to be an integrated service provider for the developers and operators of resource-based industries in a broad and often challenging range of environments. More specifically, our strategy is to:

| • | Enhance safety culture: We are committed to elevating the standard of excellence in health, safety and environmental protection with continuous improvement along with greater accountability and compliance. |

| • | Increase our recurring revenue base: It is our intention to expand our recurring services business to provide a larger base of stable revenue. |

| • | Leverage our long-term relationships with customers: We intend to continue building our relationships with existing oil sands customers to win an increased share of their heavy construction and mining, piling and pipeline services outsourced in connection with their projects. |

| 6 | 2012 Annual Information Form |

NOA

| • | Leverage and expand our complementary services: Our service segments, Heavy Construction and Mining, Pipeline and Piling are complementary to one another and allow us to compete for many different kinds of business opportunities. We intend to build on our “first-in” position to cross-sell our many services, while also pursuing selective acquisition opportunities that expand our complementary service offerings, increase our recurring revenues and / or reduce the overall capital intensity of the business. |

| • | Enhance operating efficiencies to improve revenues and margins: We seek to increase the availability and utilization of our equipment through enhanced maintenance and fleet management, providing the opportunity for increased revenue and margins. |

| • | Increase operational flexibility: We intend to structure our business in a way that enables us to adjust to changing market conditions while maintaining our profitability. |

| • | Increase our presence outside the oil sands: We intend to extend our services to other resource industries across Canada. Canada has significant natural resources and we believe that we have the equipment and the expertise to assist with extracting those resources. |

D. Projects, Competition and Major Suppliers

Active Projects

Canadian Natural: Overburden Removal Project

Canadian Natural completed construction of its Horizon Oil Sands Project and achieved first oil production in early 2009. This oil sands mining project has a targeted production capacity of 110,000 BPD from Phase 1. Canadian Natural has plans to ultimately increase total production capacity to 500,000 barrels per day (“BPD”) through future expansions. Phases 2 and 3 of the mine expansion plan are currently in the planning stages.

We have been working at the Horizon mine since 2005 under a 10-year contract with Canadian Natural to remove approximately 400 million bank cubic meters (“BCM”) of overburden and use 300 million BCM of that material to build a tailings dyke at the site. This work was suspended for approximately seven months in 2011 following a fire at the main processing plant that temporarily shut down mine operations. Our overburden removal operations resumed on January 2, 2012. This contract was amended in March 2012. The 10-year contract was amended in March 2012 and is worth approximately $1.3 billion with approximately $417.8 million in backlog revenue allotted over the remaining life of the contract. For further description of the Canadian Natural contract and amendment, see “Explanatory Notes – Significant Business Event” in our annual MD&A, which section is expressly incorporated by reference into this AIF.

We also perform time-and-materials work for Canadian Natural for its mine operations and projects groups.

The Canadian Natural overburden removal contract expires June 30, 2015.

Shell: Muskeg River and Jackpine Mines

Shell’s operations at the Athabasca Oil Sands Project include the Muskeg River Mine, which has a target production capacity of 155,000 BPD and the Jackpine Mine, which has a target production capacity of 100,000 BPD. Future planned mining expansions, while not imminent, are expected to potentially increase total production capacity to 500,000 BPD.¿

We signed a three-year earthmoving and mine support master services agreement with Shell which expires March 31, 2013. The agreement covers the provision of recurring services including construction, earthmoving and mine support and replaced an expiring two-year master services agreement. Work under the agreement covers general master services work and includes three years of defined scope and volumes for pre-strip and base-of-feed cleanup mining at the Muskeg River Mine. This type of work is typically performed under a time-and-materials arrangement and is not reflected in our reported backlog.

We signed an additional three-year master services agreement to provide muskeg removal services at Shell’s Jackpine Mine. This is a time-and-materials contract, which expires October 31, 2013 and is in addition to the agreement mentioned above.

Suncor: Steepbank, Millennium and Other Mines

Suncor’s current mining operation includes the Steepbank and Millennium mines, which have a combined production capacity in excess of 300,000 BPD. An additional 120,000 BPD of production capacity is anticipated from the planned development of the Voyageur South mine. Following their merger with Petro-Canada and a strategic alliance with Total, Suncor’s minable assets have expanded to include a 40.8% interest in the Fort Hills oil sands project and a 36.8% interest in the Total-operated Joslyn North Mine Project.

We are currently in the first year of a five-year master services agreement to provide reclamation, civil construction and mine services at Suncor’s Steepbank and Millennium oil sands mine operations with volumes and rates to be renegotiated after two and a half years to reflect changing market conditions. The Suncor overburden master services agreement expires December 31, 2015 and the Suncor civil works master services agreement expires May 31, 2015.

| ¿ | This paragraph contains forward-looking information. Please refer to “Forward-Looking Information, Assumptions and Risk Factors” for a discussion of the risks and uncertainties related to such information. |

| 2012 Annual Information Form | 7 |

Syncrude: Base Mine and Aurora Mine

Syncrude’s current mining operations include Base Mine (Mildred Lake) and Aurora Mine, which have a current combined production capacity of approximately 350,000 BPD. Further planned expansions include the development of a new mine (Aurora South), which is expected to potentially increase total production capacity to 600,000 BPD by 2020.¿

In November 2010, Imperial Oil Ltd. awarded us a new four-year master services agreement, which enables us to execute various types of projects for this customer. Construction work authorizations are issued for each piece of work under both time-and-materials and unit-price arrangements and are generally not reflected in our reported backlog.

Syncrude: Mildred Lake Mine Relocation

We are currently undertaking construction of a shear key foundation as part of the first phase of a mine relocation project at Syncrude’s Base Mine. We were recently awarded the second phase of this relocation project, which includes construction of a mechanically stabilized earth (MSE) wall. We expect to transition to this second phase as work on the shear key foundation nears completion this summer.¿

Total E&P Canada6: Joslyn North Mine Project

The Joslyn North Mine Project is in the initial construction phase and is not expected to commence production until 2018.¿

We are currently completing the initial earthworks at the Joslyn North Mine Project, including clearing the site and establishing access (roads, drainage etc.) in preparation for the planned future construction of the mine and extraction facility. This contract was awarded in November 2011 and is expected to be completed in July 2013.¿

Thompson Creek7: Mt Milligan Copper/Gold Project

We are currently completing facilities construction work at the Mt. Milligan Copper/Gold Project in northern British Columbia. The contract covers the erection of more than 7,000 tons of structural steel, as well as the installation of cladding, insulated roofing panels, cranes and lighting for new mill concentrator facilities at the mine. The work is an expansion of NAEPI’s industrial capabilities into above-ground construction and will be carried out by a combination of NAEPI personnel and specialized subcontractors. This contract was awarded in November 2011 and is targeted to be completed by October 2012.¿

PetroChina8 Dover: (Mackay River Central)

In November 2011, we were awarded two separate contracts for the MacKay River SAGD project, located 60 kms northwest of Ft. McMurray, AB. The contract with MacKay Operating Corp9 covers the plant site grading and gravel work, as well as construction of the water well road and well pads. Construction began in February 2012 and is scheduled to be completed in Fall 2012.¿

Enbridge10: Integrity Dig Program

We are currently providing pipeline testing and maintenance services for Enbridge under a two-year contract. This work is currently being performed on a time-and-materials basis in Manitoba and could possibly extend into Saskatchewan.¿

Recently Completed Projects

Syncrude: Reclamation

Between January 2012 and March 2012, we completed a winter reclamation project moving 2.6 million BCM of reclamation material at Syncrude’s Base Mine.

Suncor: Reclamation

Between December 2011 and March 2012, we completed a winter reclamation project, moving 3.4 million BCM of material in Suncor’s Millennium Mine.

Shell: Reclamation

Between November 2011 and February 2012, we completed a winter reclamation project, moving 2.5 million BCM of material in Shell’s Jackpine Mine and Muskeg River Mine.

Consumer’s Co-operative Refinery Limited: Tank Farm Project

In July 2009, we were awarded the Consumer’s Co-operative Refinery Limited11 heavy oil upgrader revamp and expansion project in Regina, Saskatchewan. Work continues on this site as we complete tank farm earthworks construction, associated piping and pipelines and other heavy civil works as required by the client under an open services agreement. Our Piling team is also installing piling foundations inside the operating facility and outside of the plant limits in the new expansion areas.

| ¿ | This paragraph contains forward-looking information. Please refer to “Forward-Looking Information, Assumptions and Risk Factors” for a discussion of the risks and uncertainties related to such information. |

| 6 | Total E&P Canada Ltd. (Total), a wholly owned subsidiary of Total SA. |

| 7 | Thompson Creek Metals Company Inc., owner of the Mt. Milligan Copper / Gold project in Central British Columbia. |

| 8 | PetroChina Dover SAGD project (PetroChina Dover) is owned by PetroChina International Investment Ltd. The project is operated by Dover Operating Corp, a joint venture between Cretaceous Oilsands Holdings Ltd, a wholly owned subsidiary of PetroChina (60%) and Alberta Oil Sands Corp. (AOSC) (40%). |

| 9 | Mackay Operating Corp is a private company categorized under Oil and Gas Exploration and Development and located in Calgary, AB, Canada. |

| 10 | Enbridge (Enbridge Inc.) is a publicly traded energy transportation and distribution company. |

| 11 | Consumers Co-operative Refinery Limited (CCRL) is a wholly owned subsidiary of Federation Co-operatives Limited. |

| 8 | 2012 Annual Information Form |

NOA

TransCanada Pipelines12: Gordondale, Karr North & Nosehill Creek Project

During fiscal 2012, we completed the installation of 44 kilometers of 42-inch pipeline in Northern Alberta for TransCanada.

TransCanada Pipelines: Cutbank Area Expansion Projects

During fiscal 2012, we completed the installation of ten kilometers of 24-inch pipeline and an additional 16 kilometres of NPS 20-inch pipeline for TransCanada.

Spectra Energy13: South Maxhamish Loop Project

During fiscal 2012, we completed the installation of 44 kilometers of 36-inch pipeline in British Columbia.

Competition

We operate businesses in highly competitive service and geographic markets in Canada, the United States and internationally. We compete with other major contractors, as well as many mid-size and smaller companies, across a range of industry segments. In addition, an increase in the number of international companies entering into the Canadian marketplace has also made the market more competitive. The majority of our new business is secured through formal bidding processes in which we are required to compete against other suppliers. Factors that impact success on competitive bids include price, safety, reliability, scale of operations, equipment and labour availability and quality of service.

We have seen a change in our competitive environment and customer behavior in the oil sands over the past three years. Several competitors were acquired over the past three years following the economic downturn in 2009. In addition, following the economic downturn, oil sands operators shifted their focus from controlling schedules to controlling costs which has resulted in some of our customers delaying planned mine development to re-engineer mine plans and insourcing mine services activity that would previously have been exclusively outsourced. These cost saving measures by our customers have resulted in a noticeable reduction in tendered mine support services and an increase in competition on oil sands project bids during the year ended March 31, 2012.

Our principal competitors in the Heavy Construction and Mining segment include Klemke Mining Corporation, Aecon Group Inc., Graham Construction Ltd, Ledcor Construction Limited (“Ledcor”), Peter Kiewit and Sons Co. Ltd., Tercon Contractors Ltd., Sureway Construction Ltd. and Thompson Bros. (Constr.) Ltd. In underground utilities installation and mechanical / structural construction (parts of our Heavy Construction and Mining segment), Voice Construction Ltd., Ledcor and IGL Canada, KBR Inc., JV Driver Projects Inc. and PCL Constructors Inc. are our major competitors.

In the private sector, the main competition to our deep foundation piling operations in Western Canada comes from Pacer Industries Inc., Ledcor, Agra Foundations Limited, Bauer Foundations Canada, Graham Construction, Beck Drilling & Environmental Services Ltd, Double Star Drilling and Midwest Caissons Inc. In Eastern Canada our main competitors include Deep Foundations, Anchor Shoring & Caissons Ltd., Birmingham Foundation Solutions and RUMBLE Foundations (Ontario) Ltd. In the public sector, we compete against national firms, as well as local competitors within individual geographic markets. Most of our public sector customers are local governments that are focused on serving only their respective regions. Competition in the public sector continues to increase and we typically choose to compete on projects only where we can utilize our equipment and operating strengths to secure profitable business.

With the acquisition of Cyntech in November 2010, we now compete in the anchor system manufacturing and installation market with from Almita Piling Inc., Hydraulic Power Systems, Inc. and Roterra Screw Piling Ltd., while competition in our tank maintenance and fabrication services comes from Horton CBI Ltd., Matrix Oil Corporation, TIW Canada Ltd. and G.L.M. Industries.

The primary competitors in the pipeline installation business include Ledcor, O.J. Pipelines Canada, Michels Canada (Michels), Louisbeurg Pipelines Inc., Bannister Pipeline Construction Co., Surerus Pipeline Inc. and Robert B. Somerville Co. Limited, while competitors in the pipeline maintenance and integrity business include Ledcor, Michels Canada, Willbros Group, Inc., and Summit Pipeline Services.

Major Suppliers

We have long-term relationships with the following equipment suppliers: Finning International Inc. (over 45 years), Wajax Income Fund (over 20 years), Brandt Tractor Ltd. (over 30 years) and SMS Equipment (over five years). Finning is a major Caterpillar heavy equipment dealer for Canada and Caterpillar equipment makes up the bulk of our fleet. Wajax is a major Hitachi equipment supplier to us for both mining and construction equipment. We purchase or rent John Deere equipment, including excavators, loaders and small bulldozers, from Brandt Tractor. SMS Equipment is a major Komatsu equipment supplier for our large mining trucks. In addition to the supply of new equipment, each of these companies is a major supplier for equipment rentals, parts and service labour. We are also actively working with these suppliers to identify cost savings opportunities, including opportunities to reduce our rental fleet and focus on parts management.

| 12 | TransCanada Pipelines Limited (TransCanada). |

| 13 | Spectra Energy Partners, LP (Spectra Energy). |

| 2012 Annual Information Form | 9 |

Tire contracts with Bridgestone and Goodyear plus allocation from Michelin have allowed us to maintain tire inventories to keep our fleet fully operational. Tire availability has tightened with global shortages occurring in larger sizes and the reselling of tires at prices far greater than new price has resumed in the mining industry. We have increased inventory and with our contracts and allocations as such we do not anticipate a tire shortfall.¿

E. Resources And Key Trends

Fleet and Equipment

We operate and maintain a heavy equipment fleet, including crawlers, graders, loaders, mining trucks, compactors, scrapers and excavators. We also maintain a fleet of ancillary vehicles including various service and maintenance vehicles. Overall, the equipment is in good condition, subject to normal wear and tear. Our credit facility is secured by liens on substantially all of our equipment. We lease some of this equipment under lease terms that include purchase options.

We acquire our equipment in three ways: capital expenditures, capital leases and operating leases (for a discussion on our equipment additions see the “Summary of Consolidated Equipment Additions”, section of our annual MD&A) The following table sets forth our owned and leased heavy equipment fleet (does not include rental equipment) as at March 31, 2012:

| Category | Capacity Range | Horsepower Range |

Number Owned |

Number Leased |

||||||||||||||||

| Heavy Construction and Mining: |

||||||||||||||||||||

| Articulating trucks |

30 to 40 tons | 305 - 406 | 20 | 10 | ||||||||||||||||

| Mining trucks |

40 to 330 tons | 476 - 2,700 | 108 | 65 | ||||||||||||||||

| Shovels |

35 - 80 cubic yards | 2,600 - 3,760 | 3 | 2 | ||||||||||||||||

| Excavators |

1 to 29 cubic yards | 90 - 1,944 | 82 | 27 | ||||||||||||||||

| Dozers |

20,741 lbs to 230,100 lbs | 96 - 850 | 75 | 44 | ||||||||||||||||

| Graders |

14 to 24 feet | 150 - 500 | 19 | 9 | ||||||||||||||||

| Loaders |

1.5 to 16 cubic yards | 110 - 690 | 91 | 3 | ||||||||||||||||

| Packers |

14,175 to 68,796 lbs | 216 - 315 | 7 | – | ||||||||||||||||

| Articulating Water Trucks |

8,000 gallon | 406 | 3 | – | ||||||||||||||||

| Scraper Water Wagons |

10,000 gallon | 462 | 2 | – | ||||||||||||||||

| Float Trucks |

250 tons | 703 | 4 | – | ||||||||||||||||

| Heavy Oil Recovery Barge |

30,000 US gal per hour | 125 | 9 | – | ||||||||||||||||

| Tractors |

43,000 lbs | 460 | 3 | – | ||||||||||||||||

| Pipeline: |

||||||||||||||||||||

| Trenchers |

60,000 lbs | 165 | 2 | – | ||||||||||||||||

| Pipe layers |

20,000 to 202,000 lbs | 78 - 265 | 36 | – | ||||||||||||||||

| Piling: |

||||||||||||||||||||

| Drill rigs |

Up to 267 feet (drill depth) | 210 - 1,500 | 55 | 8 | ||||||||||||||||

| Cranes |

25 to 150 tons | 200 - 263 | 24 | – | ||||||||||||||||

| Total |

543 | 168 | ||||||||||||||||||

For the fiscal years ended March 31, 2012, 2011 and 2010 we incurred expenses of $220.7 million, $234.9 million and $209.4 million, respectively, to maintain our equipment.

Many of our heavy equipment units are among the largest pieces of equipment in the world and are designed for use in some of the largest earthmoving and mining applications globally. Our large, diverse fleet gives us flexibility in scheduling jobs and we believe that this allows us to be responsive to our customers’ needs. A well-maintained fleet is critical in the harsh climate and environmental conditions in which we operate. We operate three significant maintenance and repair centers on the sites of the major oil sands projects, which are capable of accommodating the largest pieces of equipment in our fleet. These factors help us to be more efficient, thereby reducing costs to our customers to further improve our competitive position, while concurrently increasing our equipment utilization and thereby improving our profitability.

| ¿ | This paragraph contains forward-looking information. Please refer to “Forward-Looking Information, Assumptions and Risk Factors” for a discussion of the risks and uncertainties related to such information. |

| 10 | 2012 Annual Information Form |

NOA

Facilities

We own and lease a number of buildings and properties for use in our business, the locations of which were chosen for their geographic proximity to our major customers. Our corporate offices are located in Calgary, Alberta. Our primary administrative functions are carried out from offices in Edmonton, Alberta and Acheson, Alberta, where we also have a major equipment maintenance facility. Additional project management and equipment maintenance functions are carried out from leased and owned regional facilities in Calgary and Fort McMurray, Alberta; New Westminster, British Columbia; Regina and Martensville, Saskatchewan; and Milton, Ontario. The operations of our U.S. subsidiary, Cyntech U.S. Inc., are carried out in Plantersville, Texas. We also occupy, without charge, some customer-provided lands. The following table describes our primary facilities:

| Location | Function | Owned or Leased | Lease Expiration Date | |||||||||

| Acheson, Alberta |

Administrative office and major equipment repair facility | Leased | 11/30/2012 | |||||||||

| Calgary, Alberta (Corporate Office) |

Corporate head office | Leased | 1/31/2022 | |||||||||

| Calgary, Alberta (Piling Office) |

Regional office for piling operations and major equipment repair facility | Leased | 9/30/2020 | |||||||||

| Calgary, Alberta (Cyntech Office) |

Regional office for piling operations and manufacturing facility | Leased | 10/31/2013 | |||||||||

| Edmonton, Alberta (Mayfield) |

Administrative and operations support office | Leased | 3/31/2017 | |||||||||

| Edmonton, Alberta (Stone) |

Administrative office and regional office for piling operations | Leased | 2/28/2013 | |||||||||

| Fort McMurray, Alberta (Timberlea) |

Regional office for mining operations | Leased | 2/28/2022 | |||||||||

| Fort McMurray, Alberta (Canadian Natural site) |

Site office and maintenance facility | Building and land provided | Term of Canadian Natural contract (6/30/2015) | |||||||||

| Fort McMurray, Alberta (Shell Canada Muskeg River Mine site) |

Site office and maintenance facility | Building leased, land provided | Term of Shell MSA contract (10/31/2013) | |||||||||

| Fort McMurray, Alberta (Syncrude Ruth Lake site) |

Regional office and maintenance facility for all operations | Building owned, land provided | 8/31/2021 | |||||||||

| New Westminster, BC |

Regional office and equipment repair facility for piling operations | Leased | 12/31/2014 | |||||||||

| New Westminster, BC (Water Rights) |

Water rights adjacent to piling office premises | Leased | 3/31/2015 | |||||||||

| Martensville, Saskatchewan |

Regional office and equipment repair facility for piling operations | Leased | 4/30/2013 | |||||||||

| Regina, Saskatchewan |

Regional office and equipment repair facility for piling operations | Leased | 3/14/2013 | |||||||||

| Milton, Ontario (Drillco) |

Regional office and equipment repair facility for piling operations | Owned | N/A | |||||||||

| Plantersville, Texas (Cyntech US) |

Regional office for piling operations and manufacturing facility | Leased | 10/31/2013 | |||||||||

| 2012 Annual Information Form | 11 |

Credit Facilities

For a description of our credit facilities, see the “Credit Facilities” section of our annual MD&A, which section is expressly incorporated by reference into this AIF.

Variability of Results

A number of factors have the potential to contribute to variations in our quarterly financial results between periods, including:

| • | the timing and size of capital projects undertaken by our customers on large oil sands projects; |

| • | seasonal weather and ground conditions; |

| • | the timing of equipment maintenance and repairs; |

| • | claims and change-orders; and |

| • | the accounting for unrealized non-cash gains and losses related to foreign exchange and derivative financial instruments. |

For a description of our variability of results, see the “Summary of Quarterly Results” section of our annual MD&A, which section is expressly incorporated by reference into this AIF.

F. Legal And Labour Matters

Laws and Regulations and Environmental Matters

Many aspects of our operations are subject to various federal, provincial and local laws and regulations, including, among others:

| • | permit and licensing requirements applicable to contractors in their respective trades; |

| • | building and similar codes and zoning ordinances; |

| • | laws and regulations relating to consumer protection; and |

| • | laws and regulations relating to worker safety and protection of human health. |

We believe that we have all material required permits and licenses to conduct our operations and are in substantial compliance with applicable regulatory requirements relating to our operations. Our failure to comply with the applicable regulations could result in substantial fines or revocation of our operating permits.

Our operations are subject to numerous federal, provincial and municipal environmental laws and regulations, including those governing the release of substances, the remediation of contaminated soil and groundwater, vehicle emissions and air and water emissions. Federal, provincial and municipal authorities, such as Alberta Environment, Saskatchewan Environment, the British Columbia Ministry of Environment, Ontario Ministry of the Environment and other governmental agencies, administer these laws and regulations. The requirements of these laws and regulations are becoming increasingly complex and stringent and meeting these requirements can be expensive.

The nature of our operations and our ownership or operation of property exposes us to the risk of claims with respect to environmental matters and there can be no assurance that material costs or liabilities will not be incurred in relation to such claims. For example, some laws can impose strict joint and several liability on past and present owners or operators of facilities at, from or to which a release of hazardous substances has occurred, on parties who generated hazardous substances that were released at such facilities and on parties who arranged for the transportation of hazardous substances to such facilities. If we were found to be a responsible party under these statutes, we could be held liable for all investigative and remedial costs associated with addressing such contamination, even though the releases were caused by a prior owner or operator or third party. We are not currently named as a responsible party for any environmental liabilities on any of the properties on which we currently perform or have performed services. However, our leases typically include covenants that obligate us to comply with all applicable environmental regulations and to remediate any environmental damage caused by us to the leased premises. In addition, claims alleging personal injury or property damage may be brought against us if we cause the release of, or any exposure to, harmful substances.

Our construction contracts require us to comply with environmental and safety standards set by our customers. These requirements cover such areas as safety training for new hires, equipment use on site, visitor access on site and procedures for dealing with hazardous substances.

Capital expenditures relating to environmental matters during the fiscal years ended March 31, 2010, 2011 and 2012 were not material. We do not currently anticipate any material adverse effect on our business or financial position because of future compliance with applicable environmental laws and regulations. Future events, however, such as changes in existing laws and regulations or their interpretation, more vigorous enforcement policies of regulatory agencies or stricter or different interpretations of existing laws and regulations may require us to make additional expenditures which may or may not be material.

| 12 | 2012 Annual Information Form |

NOA

Legal Proceedings and Regulatory Actions

From time to time, we are a party to litigation and legal proceedings that we consider to be a part of the ordinary course of business. While no assurance can be given, we believe that, taking into account reserves and insurance coverage, none of the litigation or legal proceedings in which we are currently involved or know to be contemplated could reasonably be or could likely be considered important to a reasonable investor in making an investment decision, expected to have a material adverse effect on our business, financial condition or results of operations. We may, however, become involved in material legal proceedings in the future that could have such a material adverse effect.¿

Employees and Labour Relations

As of March 31, 2012, we had 743 salaried employees and approximately 2,270 hourly employees. Our hourly workforce fluctuates according to the seasonality of our business and the staging and timing of projects by our customers. The hourly workforce typically ranges in size from 1,000 employees to approximately 3,500 employees depending on the time of year and duration of awarded projects. We also utilize the services of subcontractors in our construction business. Subcontractors perform an estimated 8% to 10% of the construction work we undertake. As of March 31, 2012, approximately 2,050 employees are members of various unions and work under collective bargaining agreements.

The majority of our work is carried out by employees governed by our mining overburden collective bargaining agreement with the International Union of Operating Engineers (IUOE) Local 955, the primary term of which expires on March 31, 2015. Other collective agreements in operation include the provincial Industrial, Commercial and Institutional (ICI) agreements in Alberta and Ontario with both the Operating Engineers and Labourers Unions, Piling sector collective agreements in Saskatchewan with the Operating Engineers, Pipeline sector agreements in both British Columbia and Alberta with the Christian Labour Association of Canada (CLAC) as well as an all-sector agreement with CLAC in Ontario. We are subject to other industry and specialty collective agreements under which we complete work and the primary terms of all of these agreements are currently in effect. The provincial collective agreement between the IUOE Local 955 and the Alberta Roadbuilders and Heavy Construction Association (ARBHCA) expires February 28, 2013.

We believe that our relationships with all our employees, both union and non-union, are strong. We have not experienced a strike or lockout.

G. Description of Securities, Rights Plans and Agreements

Some of the statements contained herein are summaries of the material provisions of our articles of amalgamation relating to dividends, distribution of assets upon dissolution, liquidation or windingup. A copy of our articles of amalgamation can be found on www.sedar.com.

Capital Structure

We are authorized under our articles of amalgamation to issue an unlimited number of Voting Common Shares and an unlimited number of Non-Voting Common Shares. As at March 31, 2012, there were 36,251,006 voting Common Shares outstanding. We had no Non-Voting Common Shares outstanding as at March 31, 2012.

Voting Common Shares

Each voting common share has an equal and ratable right to receive dividends to be paid from our assets legally available therefore when, as and if declared by our board of directors.

In the event of our dissolution, liquidation or winding up, the holders of common shares are entitled to share equally and ratably in the assets available for distribution after payments are made to our creditors. Holders of common shares have no pre-emptive rights or other rights to subscribe for our securities. Each common share entitles the holder thereof to one vote in the election of directors and all other matters submitted to a vote of shareholders, and holders of common shares have no rights to cumulate their votes in the election of directors.

Non-Voting Common Shares

Except as prescribed by Canadian law and except in limited circumstances, the non-voting common shares have no voting rights but are otherwise identical to the voting common shares in all respects. The non-voting common shares are convertible into voting common shares on a share-for-share basis at the option of the holder if it transfers, sells or otherwise disposes of the converted voting common shares: (i) in a public offering of our voting common shares; (ii) to a third party that, prior to such sale, controls us; (iii) to a third party that, after such sale, is a beneficial owner of not more than 2% of our outstanding voting shares; (iv) in a transaction that complies with Rule 144 under the Securities Act of 1933, as amended; or (v) in a transaction approved in advance by regulatory bodies.

Options

Other than the exercise of options under the stock option plan, there have been no issuances of shares.

Dividends

We have not declared or paid any dividends on our common shares since our inception, and we do not anticipate declaring or paying any dividends on our common shares for the foreseeable future. We currently intend to retain any future earnings to finance future growth. Any future determination to pay dividends will be at the discretion of our board of directors and will depend on our financial condition, results of operations, capital requirements and other factors the board of directors considers relevant. In addition, our ability to declare and pay dividends is restricted by our governing statute, as well as the terms of our credit agreement and the indenture that governs our Series 1 Debentures (as defined herein).¿

| ¿ | This paragraph contains forward-looking information. Please refer to “Forward-Looking Information, Assumptions and Risk Factors” for a discussion of the risks and uncertainties related to such information. |

| 2012 Annual Information Form | 13 |

Trading Price and Volume

The following tables summarize the highest trading price, lowest trading price and volume for our common shares on the Toronto Stock Exchange (“TSX”) (in Canadian dollars) and on the New York Stock Exchange (“NYSE”) (in US dollars) on a monthly basis from April 1, 2011 to May 31, 2012:

| Toronto Stock Exchange | ||||||||||||||||

| Date | High ($) | Low ($) | Volume | |||||||||||||

| May 2012 |

4.00 | 2.31 | 435,648 | |||||||||||||

| April 2012 |

5.03 | 3.85 | 143,510 | |||||||||||||

| March 2012 |

6.19 | 4.38 | 305,460 | |||||||||||||

| February 2012 |

6.42 | 5.05 | 492,558 | |||||||||||||

| January 2012 |

6.99 | 6.27 | 306,744 | |||||||||||||

| December 2011 |

7.18 | 5.30 | 257,455 | |||||||||||||

| November 2011 |

8.10 | 6.28 | 112,988 | |||||||||||||

| October 2011 |

7.21 | 5.00 | 112,801 | |||||||||||||

| September 2011 |

6.49 | 5.25 | 389,323 | |||||||||||||

| August 2011 |

6.32 | 4.74 | 460,128 | |||||||||||||

| July 2011 |

7.49 | 5.75 | 308,685 | |||||||||||||

| June 2011 |

9.30 | 6.80 | 614,777 | |||||||||||||

| May 2011 |

11.06 | 6.89 | 752,857 | |||||||||||||

| April 2011 |

12.05 | 9.89 | 231,050 | |||||||||||||

| New York Stock Exchange | ||||||||||||||||

| Date | High ($) | Low ($) | Volume | |||||||||||||

| May 2012 |

4.06 | 2.23 | 2,314,440 | |||||||||||||

| April 2012 |

4.98 | 3.86 | 1,755,320 | |||||||||||||

| March 2012 |

6.03 | 4.40 | 2,632,786 | |||||||||||||

| February 2012 |

6.47 | 5.06 | 2,362,775 | |||||||||||||

| January 2012 |

6.92 | 6.24 | 1,576,720 | |||||||||||||

| December 2011 |

7.05 | 5.10 | 2,412,652 | |||||||||||||

| November 2011 |

8.03 | 6.09 | 1,980,394 | |||||||||||||

| October 2011 |

7.27 | 4.70 | 1,920,929 | |||||||||||||

| September 2011 |

6.36 | 5.09 | 4,372,029 | |||||||||||||

| August 2011 |

6.55 | 4.75 | 7,610,196 | |||||||||||||

| July 2011 |

7.82 | 5.95 | 6,072,520 | |||||||||||||

| June 2011 |

9.50 | 6.87 | 10,932,599 | |||||||||||||

| May 2011 |

11.64 | 7.15 | 12,381,080 | |||||||||||||

| April 2011 |

12.51 | 10.25 | 5,536,502 | |||||||||||||

Shareholder Rights Plan

On October 7, 2011, our Board of Directors adopted a Shareholder Rights Plan Agreement, dated October 7, 2011 (the “Rights Plan”) designed to encourage the fair and equal treatment of shareholders in connection with any takeover bid for our outstanding Common Shares. The Rights Plan was included as an exhibit to our Form 8-A, filed with the Securities and Exchange Commission on October 7, 2011. The Rights Plan terminated in accordance with its terms on April 7, 2012.

Registration Rights Agreement

We are party to a registration rights agreement with certain shareholders, including affiliates of each of the significant shareholders, Paribas North America, Inc. and Mr. William Oehmig, one of our directors. The shareholders party to the agreement and their permitted transferees are entitled, subject to certain limitations, to include their common shares in a registration of common shares we initiate under the Securities Act of 1933 (“Securities Act 1933”), as amended. In addition, after the 120th day following our IPO, any one or more shareholders party to the agreement has the right to require us to effect the registration of all or any part of such shareholders’ common shares under the Securities Act 1933, referred to as a “demand registration,” so long as the amount of common shares to be registered has an aggregate fair market value of at least US$5.0 million and, at such time, the SEC has ordered or declared effective fewer than four demand registrations initiated by us pursuant to the registration rights agreement. If the aggregate number of common shares that the shareholders party to the agreement request us to include in any registration, together, in the case of a registration we initiate, with the common shares to be included in such registration, exceeds the number which, in the opinion of the managing underwriter, can be sold in such offering without materially affecting the offering price of such shares, the number of shares of each shareholder to be included in such registration will be reduced pro rata based on the aggregate number of shares for which registration was requested. The shareholders party to the agreement have the right to require, after four demand registrations, one registration in which their common shares will not be subject to pro rata reduction with others entitled to registration rights.

| 14 | 2012 Annual Information Form |

NOA

We may opt to delay the filing of a registration statement required pursuant to any demand registration for:

| • | up to 120 days following a request for a demand registration if: |

| • | we have decided to file a registration statement for an underwritten public offering of our common shares, from which we expect to receive net proceeds of at least US$20.0 million; or |

| • | we have initiated discussions with underwriters in preparation for a public offering of our common shares from which we expect to receive net proceeds of at least US$20.0 million and the demand registration, in the underwriters’ opinion, would have a material adverse effect on the offering; or |

| • | up to 90 days following a request for a demand registration if we are in possession of material information that we reasonably deem advisable not to disclose in a registration statement. |

Our right to delay the filing of a registration statement if we possess information that we deem advisable not to disclose does not obviate any disclosure obligations which we may have under The Securities Exchange Act of 1934 or other applicable laws; it merely permits us to avoid filing a registration statement if our management believes that such a filing would require the disclosure of information which otherwise is not required to be disclosed and the disclosure of which our management believes is premature or otherwise inadvisable.

The registration rights agreement contains customary provisions whereby we and the shareholders party to the agreement covenant to indemnify and contribute to each other with regard to losses caused by the misstatement of any information or the omission of any information required to be provided in a registration statement filed under the Securities Act 1933. The registration rights agreement requires us to pay the expenses associated with any registration other than sales discounts, commissions, transfer taxes and amounts to be borne by underwriters or as otherwise required by law.

9.125% Series 1 Debentures

On April 7, 2010, we closed a private placement of 9.125% Series 1 Debentures (as defined below) due 2017 (the “Series 1 Debentures”) for gross proceeds of $225.0 million and net proceeds after commissions and related expenses of $218.1 million as part of a debt restructuring plan. Financing fees of $6.9 million were incurred in connection with the Series 1 Debentures and were recorded as deferred financing costs. A more detailed discussion on the debt restructuring can be found in the “Long-term debt restructuring” section of our annual MD&A.

The Series 1 Debentures are unsecured senior obligations and rank equally with all other existing and future unsecured senior debt and senior to any subordinated debt that may be issued by us or any of our subsidiaries. The Series 1 Debentures are effectively subordinated to all secured debt to the extent of the value of the collateral.

At any time prior to April 7, 2013, we may redeem up to 35% of the aggregate principal amount of the Series 1 Debentures, with the net cash proceeds of one or more of our public equity offerings (as defined in the trust indenture that governs the Series 1 Debentures) at a redemption price equal to 109.125% of the principal amount plus accrued and unpaid interest to the date of redemption, so long as:

| i. | at least 65% of the original aggregate amount of the Series 1 Debentures remains outstanding after each redemption; and |

| ii. | any redemption is made within 90 days of the equity offering. |

At any time prior to April 7, 2013, we may on one or more occasions redeem the Series 1 Debentures, in whole or in part, at a redemption price which is equal to the greater of:

| i. | the Canada Yield Price (as defined in the trust indenture that governs the Series 1 Debenture); and |

| ii. | 100% of the aggregate principal amount of Debentures redeemed, plus, in each case, accrued and unpaid interest to the redemption date (subject to the right of holders of record on the relevant record date to receive interest due on the relevant interest payment date). |

The Series 1 Debentures are redeemable at our option, in whole or in part, at any time on or after: April 7, 2013 at 104.563% of the principal amount; April 7, 2014 at 103.042% of the principal amount; April 7, 2015 at 101.520% of the principal amount; April 7, 2016 and thereafter at 100% of the principal amount; plus, in each case, interest accrued to the redemption date.

If a change of control, as defined in the trust indenture, occurs we will be required to offer to purchase all or a portion of each holder’s Series 1 Debentures at a purchase price in cash equal to 101% of the principal amount of the debentures offered for repurchase plus accrued interest to the date of purchase.

The Series 1 Debentures are also subject to covenants limiting our ability and the ability of most or all of its subsidiaries: to incur additional debt; pay dividends or distributions on our common shares or repurchase our common shares; make various investments; create liens on our assets to secure debt; enter into transactions with affiliates; consolidate, merge or transfer all or substantially all of our property and assets and the property and assets of our subsidiaries on a consolidated basis; transfer and sell assets; and enter into sale and leaseback transactions. These covenants are subject to exceptions and qualifications that are detailed in the indenture governing the Series 1 Debentures.

| 2012 Annual Information Form | 15 |

We are also required to meet a financial covenant with respect to our Series 1 Debentures that restricts the amount of additional debt that we and our subsidiaries can incur. Specifically, on a pro forma basis taking such additional debt into account, on a consolidated basis our “Consolidated Fixed Charge Coverage Ratio” must be greater than 2.0 to 1.0. The “Consolidated Fixed Charge Coverage Ratio” is approximately the same calculation as the “Interest Coverage” covenant found in our Credit Facility.

The Series 1 Debentures were rated B- by Standard & Poor’s and Caa1 by Moody’s (see “Debt Ratings”).

Debt Ratings

For a discussion of our debt ratings, see the “Debt Ratings” section of our annual MD&A, which section is expressly incorporated by reference in this AIF.

H. Material Contracts

We are party to the following material contracts, which are contracts other than those entered into in the ordinary course of our business, as the same have been amended from time to time:

| • | Indemnity Agreement between NACG Holdings Inc., NACG Preferred Corp., North American Energy Partners Inc., North American Construction Group Inc. and their respective officers and directors Please refer to the most recently filed management information circular for details; |

| • | Indenture, dated as of April 7, 2010, among North American Energy Partners Inc., the guarantors named therein and CIBC Mellon Trust Company, as Trustee, and Supplemental Indenture dated as of April 7, 2010, among North American Energy Partners Inc., the guarantors named therein and CIBC Mellon Trust Company, as Trustee. Please refer to “Description of Certain Indebtedness – 9.125% Series 1 Debentures” for details; |

| • | Registration Rights Agreement, dated as of November 26, 2003, among NACG Holdings Inc. and the shareholders party thereto. Please refer to “Interest of Management and Others in Material Transactions – Registration Rights Agreement” for details; |

| • | Amended and Restated 2004 Share Option Plan. Please refer to the most recently filed management information circular for details; |

| • | Directors Deferred Share Unit plan, dated January 1, 2008. Please refer to the most recently filed management information circular for details; |

| • | Restricted Share Unit plan dated April 1, 2008. Please refer to the most recently filed management information circular for details; |

| • | Overburden Removal and Mining Services Contract, dated November 17, 2004, between Canadian Natural Resources Ltd. and Noramac Ventures Inc., with the latter’s interest having been assigned to North American Construction Group Inc. by an Assignment Agreement dated February 27, 2006, all as amended by an Amending Agreement dated March 19, 2012. Please see “Projects – Active Projects – Canadian Natural: Overburden Removal Project; |