UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F/A

(Amendment No.2)

(Mark One)

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2016

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report ________________

For the transition period from to

Commission file number: 001-33429

Acorn International, Inc.

(Exact name of Registrant as

specified in its charter)

Not applicable

(Translation of Registrant’s name

into

English)

Cayman Islands

(Jurisdiction of incorporation

or

organization)

19/F, 20th Building, 487 Tianlin Road, Shanghai 200233

(Address of principal executive

offices)

Geoffrey Weiji Gao, geoffrey.gao@chinadrtv.com, 86-21-5151 8888

19/F, 20th Building, 487 Tianlin Road, Shanghai

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Title of each class | Name of each exchange on which registered | |

| American Depositary Shares, each representing twenty ordinary shares, par value $0.01 per share |

New York Stock Exchange |

Securities registered or to be registered pursuant to Section 12(g) of the Act.

None

(Title of Class)

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: 75,406,875.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ¨ Yes x No

If this report is an annual or transaction report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. ¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). x Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer," accelerated filer,” and "emerging growth company" in Rule 12b-2 of the Exchange Act:

Large accelerated filer ¨ Accelerated filer ¨ Non-accelerated filer x Emerging growth company ¨

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ¨

†The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

US GAAP x

International Financial Reporting Standards as issued by the International Accounting Standards

Board ¨ Other

¨

If “Other” has been checked in response to the previous question indicate by check mark which financial statement item the registrant has elected to follow. ¨ Item 17 ¨ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ¨ Yes x No

ACORN INTERNATIONAL, INC.

TABLE OF CONTENTS

| 2 |

We filed our Annual Report on Form 20-F for the year ended December 31, 2016 (our “Annual Report”) with the Commission on May 15, 2017. On July 11, 2017 we amended our Annual Report (“Amendment No. 1”) solely to reflect that the financial statements for the years ended 2014 and 2015 (our “2014 and 2015 Financial Statements”) appearing in that amended report were unaudited and to remove the audit report of Deloitte Touche Tomatshu Certified Public Accountants LLP (“Deloitte”) dated May 16, 2016. The reason for Amendment No. 1 was that, although our 2014 and 2015 Financial Statements were audited by Deloitte as of the date of their audit report, as of the time of Amendment No. 1’s filing, Deloitte had not yet conducted certain subsequent events procedures or granted permission to reprint our 2014 and 2015 Financial Statements and its audit report in our Annual Report and, until that work was completed, the staff of the Commission viewed those financial statements as unaudited.

We are now filing a further amendment to our Annual Report (“Amendment No. 2”) to reflect that Deloitte has completed the relevant subsequent events procedures and granted permission to reprint our 2014 and 2015 Financial Statements and its audit report in our Annual Report and, accordingly, our 2014 and 2015 Financial Statements are considered by the staff of the Commission as audited. There have been no material changes to our 2014 and 2015 Financial Statements between their original publication and their inclusion in this Amendment No. 2.

Except where the context otherwise requires and for purposes of this annual report only, references to:

| • | “ordinary shares” are to our ordinary shares, par value $0.01 per share; |

| • | “ADSs” are to our American depositary shares, each of which represents twenty ordinary shares; |

| • | “ADRs” are to American depositary receipts, which, if issued, evidence our ADSs; |

| • | “$”, “US$”, “USD” and “U.S. dollars” are to the legal currency of the United States; |

| • | “China” and the “PRC” are to the People’s Republic of China, excluding Taiwan and the special administrative regions of Hong Kong and Macau; |

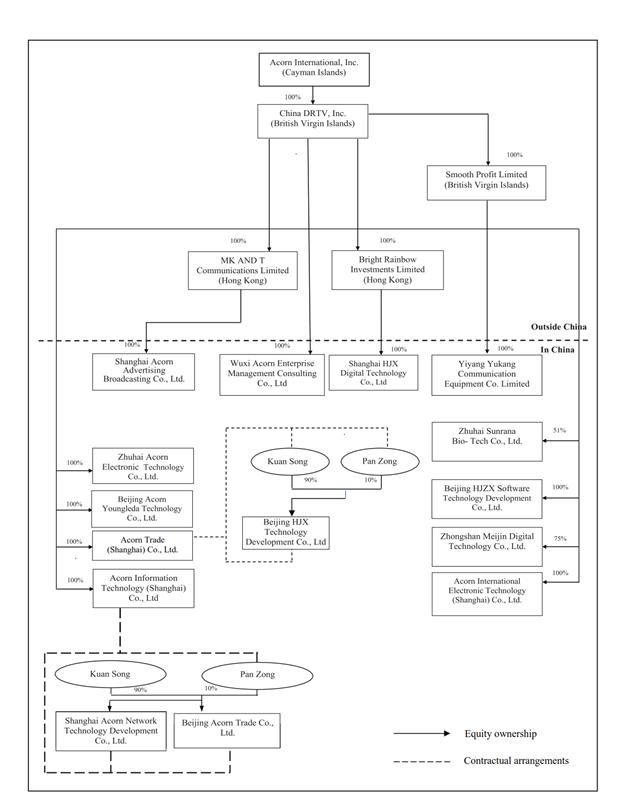

| • | “variable interest entities,” or “VIEs,” refer to Shanghai Acorn Network Technology Development Co., Ltd., Beijing Acorn Trade Co., Ltd. and Beijing HJX Technology Development Co., Ltd., the domestic PRC companies in which we do not have equity interests but whose financial results have been consolidated into our consolidated financial statements in accordance with U.S. GAAP due to our having effective control over, and our being the primary beneficiary of, the three companies; |

| • | “consolidated affiliated entities” refer to our variable interest entities and their direct and indirect subsidiaries; |

| • | “RMB” and “Renminbi” are to the legal currency of China; and |

| • | “we”, “us”, “our”, “our company” and “our Group” refer to Acorn International, Inc., its predecessor entities, subsidiaries and consolidated affiliated entities, as the context may require. |

This annual report on Form 20-F includes our audited consolidated statements of operations data for the years ended December 31, 2014, 2015 and 2016, and audited consolidated balance sheet data as of December 31, 2015 and 2016.

We completed the initial public offering of our ADSs in May 2007. Our ADSs are listed on the New York Stock Exchange under the symbol “ATV”.

FORWARD-LOOKING STATEMENTS

This annual report on Form 20-F contains forward-looking statements that involve risks and uncertainties. All statements other than statements of historical facts are forward-looking statements based on our current expectations, assumptions, estimates and projections about us and our industry. These statements involve known and unknown risks, uncertainties and other factors, including those listed under “Risk Factors,” which may cause our actual results, performance or achievements to be materially different from those expressed or implied by the forward- looking statements. These statements are made under the “safe harbor” provisions of the U.S. Private Securities Litigations Reform Act of 1995. In some cases, these forward-looking statements can be identified by words or phrases such as “aim”, “anticipate”, “believe”, “continue”, “estimate”, “expect”, “intend”, “is/are likely to”, “may”, “plan”, “potential”, “will” or other similar expressions. The forward-looking statements included in this annual report relate to, among others:

| • | anticipated operating results for 2017; |

| • | our ability to reduce our operating losses, generate cash flows and fund our operations; |

| • | our goals and strategies, and our success in developing our business model; |

| 3 |

| • | expected trends in our e-commerce channels, our direct sales platform and our distribution network, and in our margins and certain cost or expense items as a percentage of our net revenues; |

| • | our future business development, financial condition and results of operations; |

| • | our ability to introduce successful new products and attract new customers; |

| • | our ability to maintain and build our brand and revenue for our direct sales products, particularly following our decisions to terminate the purchase of TV airtime for TV direct sales; |

| • | our ability to manage our featured product lines; |

| • | competition from companies in a number of industries, including internet companies that provide direct sales marketing in China for consumer products; |

| • | our ability to effectively control our cost of sales and efficiently access media channels; |

| • | PRC governmental policies and regulations relating to our businesses; |

| • | general economic and business condition in China and elsewhere; and |

| • | assumptions underlying or related to any of the foregoing. |

| 4 |

The forward-looking statements made in this annual report relate only to events or information as of the date on which the statements are made in this annual report. We would like to caution you not to place undue reliance on forward-looking statements and you should read these statements in conjunction with the risk factors disclosed in “Item 3.D. Key Information — Risk Factors.” Those risks are not exhaustive. We operate in an emerging and evolving environment. New risk factors and uncertainties emerge from time to time and it is not possible for our management to predict all risk factors and uncertainties, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. You should read thoroughly this annual report and the documents that we refer to with the understanding that our actual future results may be materially different from what we expect. All forward-looking statements included herein attributable to us or other parties or any person acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. Except as required by law, we undertake no obligation to update any forward-looking statements to reflect events or circumstances after the date on which the statements are made or to reflect the occurrence of unanticipated events.

| 5 |

| ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

Not applicable.

| ITEM 2. | OFFER STATISTICS AND EXPECTED TIMETABLE |

Not applicable.

| ITEM 3. | KEY INFORMATION |

| A. | Selected Financial Data |

The following selected consolidated statements of operations data for the three years ended December 31, 2014, 2015 and 2016, and the selected consolidated balance sheet data as of December 31, 2015 and 2016, have been derived from our audited consolidated financial statements for the years ended December 31, 2014, 2015 and 2016, and are included elsewhere in this annual report. Our selected consolidated statements of operations data for the years ended December 31, 2012 and 2013, and our consolidated balance sheet data as of December 31, 2012, 2013 and 2014, have been derived from our audited consolidated financial statements that are not included in this annual report. Our selected consolidated financial statements are prepared and presented in accordance with accounting principles generally accepted in the United States, or U.S. GAAP. Our historical results for any period are not necessarily indicative of results to be expected for any future period. The selected consolidated financial data should be read in conjunction with those consolidated financial statements and related notes and Item 5, “Operating and Financial Review and Prospects” in this annual report.

| 6 |

| For the years ended December 31, | ||||||||||||||||||||

| 2012 | 2013 | 2014 | 2015 | 2016 | ||||||||||||||||

| (in thousands, except share and per share data) | ||||||||||||||||||||

| Condensed Consolidated Statements of Operations Data | ||||||||||||||||||||

| Revenues: | ||||||||||||||||||||

| Direct sales, net | $ | 193,615 | $ | 136,416 | $ | 45,233 | $ | 19,406 | $ | 13,833 | ||||||||||

| Distribution sales, net | 48,959 | 48,295 | 49,522 | 28,140 | 10,695 | |||||||||||||||

| Total revenues, net | 242,574 | 184,711 | 94,755 | 47,546 | 24,528 | |||||||||||||||

| Cost of revenues: | ||||||||||||||||||||

| Direct sales | 96,472 | 57,445 | 24,353 | 13,388 | 2,728 | |||||||||||||||

| Distribution sales | 35,475 | 35,046 | 32,570 | 21,499 | 9,244 | |||||||||||||||

| Total cost of revenues | 131,947 | 92,491 | 56,923 | 34,887 | 11,972 | |||||||||||||||

| Gross profit | 110,627 | 92,220 | 37,832 | 12,659 | 12,556 | |||||||||||||||

| Operating (expenses) income: | ||||||||||||||||||||

| Advertising expenses | (58,338 | ) | (51,731 | ) | (16,233 | ) | (2,204 | ) | (24 | ) | ||||||||||

| Other selling and marketing expenses | ||||||||||||||||||||

| (50,346 | ) | (54,874 | ) | (40,177 | ) | (25,185 | ) | (12,970 | ) | |||||||||||

| General and administrative expenses(1) | ||||||||||||||||||||

| (27,071 | ) | (30,681 | ) | (28,417 | ) | (27,839 | ) | (16,437 | ) | |||||||||||

| Other operating income, net | 3,277 | 2,615 | 2,121 | 1,712 | 7,607 | |||||||||||||||

| Total operating expenses | (132,478 | ) | (134,671 | ) | (82,706 | ) | (53,516 | ) | (21,824 | ) | ||||||||||

| Loss from operations | (21,851 | ) | (42,451 | ) | (44,874 | ) | (40,857 | ) | (9,268 | ) | ||||||||||

| Other income , net | 5,755 | 3,394 | 1,954 | 1,017 | 18,138 | |||||||||||||||

| Income tax expense | (1,822 | ) | (646 | ) | (1,171 | ) | (183 | ) | (4,593 | ) | ||||||||||

| Equity in losses of affiliates | — | (206 | ) | (235 | ) | (227 | ) | (868 | ) | |||||||||||

| Net income (loss)(2)(3) | (17,918 | ) | (39,908 | ) | (44,326 | ) | (40,250 | ) | 3,409 | |||||||||||

| Net income (loss) attributable to non-controlling interests | 8 | (12 | ) | 3 | (91 | ) | (29 | ) | ||||||||||||

| Net income (loss) attributable to Acorn International, Inc. shareholders | (17,926 | ) | (39,896 | ) | (44,329 | ) | (40,159 | ) | 3,438 | |||||||||||

| Income (loss) per ordinary share: | ||||||||||||||||||||

| Basic and Diluted | $ | (0.20 | ) | $ | (0.47 | ) | $ | (0.54 | ) | $ | (0.51 | ) | $ | 0.05 | ||||||

| Weighted average number of shares used in calculating income (loss) per ordinary share | ||||||||||||||||||||

| Basic | 89,965,979 | 84,115,169 | 82,690,613 | 79,226,404 | 75,600,700 | |||||||||||||||

| Diluted | 89,965,979 | 84,115,169 | 82,690,613 | 79,226,404 | 75,600,700 | |||||||||||||||

| 7 |

| As of December 31, | ||||||||||||||||||||

| 2012 | 2013 | 2014 | 2015 | 2016 | ||||||||||||||||

| (in thousands) | ||||||||||||||||||||

| Condensed Consolidated Balance Sheet Data | ||||||||||||||||||||

| Cash and cash equivalents | $ | 90,975 | $ | 82,552 | $ | 34,686 | $ | 12,147 | $ | 25,506 | ||||||||||

| Prepaid advertising expenses | 8,563 | 3,215 | 6,162 | 475 | 11 | |||||||||||||||

| Total assets | 207,397 | 175,354 | 125,732 | 240,719 | 133,320 | |||||||||||||||

| Deferred revenue | 904 | 787 | 667 | 548 | 381 | |||||||||||||||

| Total liabilities | 27,596 | 39,082 | 34,060 | 62,006 | 33,810 | |||||||||||||||

| Ordinary shares | 946 | 949 | 952 | 890 | 918 | |||||||||||||||

| Additional paid-in capital | 161,057 | 161,500 | 161,925 | 161,308 | 161,938 | |||||||||||||||

| Retained earnings | (1,966 | ) | (41,862 | ) | (86,191 | ) | (126,349 | ) | (122,911 | ) | ||||||||||

| Accumulated other comprehensive income | 30,721 | 35,285 | 34,585 | 162,580 | 80,865 | |||||||||||||||

| Treasury stock | (11,464 | ) | (20,109 | ) | (20,109 | ) | (20,109 | ) | (21,640 | ) | ||||||||||

| Non-controlling interests | 507 | 509 | 510 | 392 | 340 | |||||||||||||||

| Total equity | 179,801 | 136,272 | 91,672 | 178,713 | 99,510 | |||||||||||||||

| Total liabilities and equity | $ | 207,397 | $ | 175,354 | $ | 125,732 | $ | 240,719 | $ | 133,320 | ||||||||||

Note: Accumulated other comprehensive income in 2016 primarily reflects our unrealized gain on available-for-sales securities. See Notes 8 and 9 to our audited financial statements included elsewhere in this annual report.

| For the years ended December 31, | ||||||||||||

| 2014 | 2015 | 2016 | ||||||||||

| (in thousands, except percentages) | ||||||||||||

| Selected Operating Data | ||||||||||||

| Number of inbound calls generated through direct sales platforms | 1,204 | 92 | — | |||||||||

| Conversion rate for inbound calls to product purchase orders | 13.0 | % | 11.5 | % | — | % | ||||||

| Total TV direct sales program minutes | 131 | 3 | — | |||||||||

Note: Beginning in 2014, we reduced our TV advertising purchases for infomercials and in the first quarter of 2015 we discontinued our TV direct sales operations.

| (1) | Includes share-based compensation of: |

| For the years ended December 31, | ||||||||||||||||||||

| 2012 | 2013 | 2014 | 2015 | 2016 | ||||||||||||||||

| (in thousands) | ||||||||||||||||||||

| General and administrative expenses | $ | (424 | ) | $ | (446 | ) | $ | (428 | ) | $ | (71 | ) | $ | (658 | ) | |||||

| (2) | Includes: |

| For the years ended December 31, | ||||||||||||||||||||

| 2012 | 2013 | 2014 | 2015 | 2016 | ||||||||||||||||

| (in thousands) | ||||||||||||||||||||

| Share-based compensation | $ | (424 | ) | $ | (446 | ) | $ | (428 | ) | $ | (71 | ) | $ | (658 | ) | |||||

| (3) | Net income (loss) for the periods presented reflect effective tax rates, which may not be representative of our long- term expected effective tax rates in light of the tax holidays and exemptions enjoyed by certain of our PRC subsidiaries and our consolidated affiliated entities. See Item 5.A, “Operating and Financial Review and Prospects—Operating Results—Taxation”. |

Exchange Rate Information

We have published our financial statements in U.S. dollars. Our business is primarily conducted in China and substantially all of our revenues are denominated in Renminbi. Periodic reports will be made to shareholders and will be expressed in U.S. dollars using the then current exchange rates. The conversion of Renminbi into U.S. dollars in this annual report is based on the official base exchange rate published by the People’s Bank of China. Monetary assets and liabilities denominated in Renminbi are translated into U.S. dollars at the rates of exchange as of the balance sheet date; equity accounts are translated at historical exchange rates and revenues, expenses, gains and losses are translated using the average rate for the year as published by the People’s Bank of China. Unless otherwise noted, all translations from Renminbi to U.S. dollars in this annual report were made at $1.00 to RMB6.937, which was the prevailing rate on December 31, 2016. The prevailing rate on May 11, 2017 was $1.00 to RMB6.9051. We make no representation that any Renminbi or U.S. dollar amounts could have been, or could be, converted into U.S. dollars or Renminbi, as the case may be, at any particular rate, the rates stated below, or at all. The PRC government imposes controls over its foreign currency reserves in part through direct regulation of the conversion of Renminbi into foreign exchange and through restrictions on foreign trade.

| 8 |

The following table sets forth various information concerning exchange rates between the Renminbi and the U.S. dollar for the periods indicated. These rates are provided solely for your convenience and are not necessarily the exchange rates that we used in this annual report or will use in the preparation of our periodic reports or any other information to be provided to you.

| Period | Noon Buying Rate | |||||||||||||||

| Period End | Average(1) | Low | High | |||||||||||||

| (RMB per U.S. Dollar) | ||||||||||||||||

| 2012 | 6.2855 | 6.3085 | 6.3495 | 6.2670 | ||||||||||||

| 2013 | 6.0969 | 6.1896 | 6.2898 | 6.0969 | ||||||||||||

| 2014 | 6.1190 | 6.1428 | 6.1710 | 6.0930 | ||||||||||||

| 2015 | 6.4936 | 6.2284 | 6.4936 | 6.1079 | ||||||||||||

| 2016 | 6.9370 | 6.6529 | 6.4564 | 6.9508 | ||||||||||||

| October | 6.7641 | 6.7303 | 6.6513 | 6.6908 | ||||||||||||

| November | 6.8865 | 6.8402 | 6.7491 | 6.9168 | ||||||||||||

| December | 6.9370 | 6.9198 | 6.8575 | 6.9508 | ||||||||||||

| 2017 | ||||||||||||||||

| January | 6.8588 | 6.8907 | 6.8331 | 6.9526 | ||||||||||||

| February | 6.8750 | 6.8694 | 6.8458 | 6.8898 | ||||||||||||

| March | 6.8993 | 6.8940 | 6.8701 | 6.9125 | ||||||||||||

| April | 6.8931 | 6.8844 | 6.6851 | 6.9042 | ||||||||||||

| May (through May 11, 2016) | 6.9051 | 6.8974 | 6.8884 | 6.9066 | ||||||||||||

| (1) | Annual average for any given year is calculated by using the average of the exchange rates on the end of each month during such year. Monthly average for any given month is calculated by using the average of the daily rates during such month. |

| B. | Capitalization and Indebtedness |

Not applicable.

| C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

| D. | Risk Factors |

Risks Relating to Our Business and Industry

If various measures to reduce operating expenses or generate additional cash flows are unsuccessful, we may continue to experience significant net losses and negative cash flows. Moreover, we believe we must achieve operating profitability in order to position the business for long term sustainable success.

We had a net loss of approximately $39.9 million, $44.3 million and $40.2 million in 2013, 2014 and 2015, respectively. While we had net income of approximately $3.4 million in 2016, our operating loss was around $9.3 million and we achieved profitability only due to other income of approximately $17.7 million, which resulted primarily from sales of approximately 8 million shares in Yimeng Software Technology Co., Ltd. In our 2014 annual report filed with the U.S. SEC in May 2015, we indicated that there was substantial doubt as to our ability to continue as a going concern. In response, we began implementing, a series of initiatives, some of which are ongoing, designed to liquidate our non-core assets, stabilize our core businesses, reduce our expenses and losses, and generate additional cash flow. Our liquidity position improved in 2015 and 2016, in part due to these measures, allowing us to realize our assets and satisfy our liabilities in the normal course of business. Nonetheless, a number of these measures continued during this time. Among other related actions:

| · | in 2015 and 2016, we sold a number of non-core properties in Shanghai and Beijing for a total consideration of approximately $14.5 million; |

| · | we are negotiating for a potential transfer of our land use rights to a piece of land in the Qingpu district of Shanghai and selling a warehouse and factory constructed by us which is located on that land; |

| · | in the first quarter of 2015, we discontinued our TV direct sales channel and related TV adverting time purchases in response to various increasingly restrictive PRC regulations on TV advertising time (in 2014 we had already began reducing our TV advertising expenditures in response to increasing PRC regulation and TV advertising pricing); |

| · | we consolidated our four call center facilities into one call center in Wuxi, China with significant related headcount reductions; |

| · | in 2016 and the first four months of 2017, we have sold approximately 12.6 million shares in Yimeng Software Technology Co., Ltd. for aggregate consideration of RMB190.7 million, or $27.5 million; and |

| · | we have subleased excess warehouse space to third parties, resulting in a decrease in associated costs and an increase in other operating income in 2015 and 2016. |

Our ability to achieve and maintain profitability and positive cash flow from operating activities depends on various factors, including our ability to grow revenue and control our costs and expenses, the effectiveness of our selling and marketing activities, consumer acceptance of our products and the growth and maintenance of our customer base. We may fail to achieve or sustain profitability or positive cash flow from operating activities. See “Operating and Financial Review and Prospects—A. Operating Results—Overview” and “—B. Liquidity and Capital Resources.”

| 9 |

We do not believe our 2015 and 2016 results of operations are comparable to our historical operating results or are necessarily a reliable indicator of our future operating results, making it difficult for you to evaluate our business or future prospects; our 2017 total net revenues may be lower than 2016 total net revenues.

Our 2015 and 2016 operating results were impacted by, among other factors, our decision to deemphasize our TV direct sales channel beginning in 2014 and then to discontinue those operations in the first quarter of 2015; the decline in sales of our electronic learning products in the face of intense competition, which was partially offset by increased sales of our Babaka branded posture correction products; our cash generation and cost cutting efforts and related charges and expenses; the streamlining of our business model; and the legal dispute between two groups of our shareholders relating to the management and direction of our company and the related diversion of our management’s attention from our business and litigation-related prohibitions on our pursuing transactions outside our ordinary course of business. Our 2017 results may be impacted by these events and our ongoing efforts to evolve our business model.

Historically, a significant portion of our revenues were generated through TV direct sales and one of our largest expenses was our purchase of TV advertising time (which typically was 90% dedicated to TV infomercial time). Consistent with deemphasizing in 2014, and then discontinuing in the first quarter of 2015, our TV direct sales channel, TV direct sales revenues decreased from $5.7 million in 2014 to $0.3 million in 2015 and further to nil in 2016 (or approximately 6.0%, 0.7% and nil of our total gross revenues in those periods). We also believe that product sales through our distribution channel are also adversely impacted by decreased advertising expenditures.

More recently, sales of our electronic learning products had decreased significantly from $44,137,557 in 2014 to $24,637,772 in 2015, representing 46.5% and 51.7%, respectively, of our total gross revenues in those years. However, due to intense competition and other factors, sales of our electronic learning products declined to $8,071,401 in 2016, representing only 32.8% of our total gross revenues in that year. While these declines were partially offset in 2016 by increased sales of our Babaka branded posture correction products, we cannot assure you this trend will continue.

Our 2016 operating results include various charges and expenses in connection with efforts to generate cash and cut costs, including approximately $1.5 million of severance costs in connection with our headcount reductions.

In addition, as a result of the shareholder dispute that is more generally described in “Item 8A Financial Information—Consolidated financial statements and other financial information—Legal Proceedings”, we incurred substantial direct costs associated with ongoing legal proceedings in the Cayman Islands, including fees and expenses of various professionals to advise us on this matter, including legal advisors, as well as substantial indirect costs to us resulting from the dispute, including potentially (in some cases), but not limited to derivative law suits in China separate from but related to the dispute, inappropriate severance payments, excess payment to third-party vendors and suppliers, distraction of management and staff from the core business to focus, and lost opportunities. We estimate that the total direct costs associated with the legal proceedings related to the shareholder dispute were approximately $0.4 million for 2015. Although the shareholder dispute was generally resolved in May 2015, on December 1, 2016, we filed a related action in the Grand Court of the Cayman Islands against Mr. Andrew Yan and two other directors for damages resulting from breach of fiduciary duties and related misconduct and mismanagement, and initially will face further expenses in relation to this action, although we have asked the Court to award costs. Furthermore, we may experience ongoing related disputes or expenses.

As more fully described below under “Historical disputes regarding control of our strategic direction and control of our board of directors could adversely impact our business, operating results and prospects” and in “Item 7 Major Shareholders and Related Party Transactions—Related Party Transactions— Transitional Services and Separation Agreement”, we entered into settlement arrangements with Mr. Yang and Mr. Roche and exchanged certain liability releases. Other than those arrangements, we have not entered into any agreements settling any claims or provided or received any releases from any of the directors or shareholders involved in the dispute with respect to the matters leading up to or resulting from the dispute. We may be subject to indemnification claims or legal proceedings with respect to these matters which may result in corresponding fees and expenses (including attorney’s fees) which would negatively impact our future financial results.

The overall impact of these events on our future operating results depends on, among other things, our success in reshaping our business model, our ability to promote our products through our other existing platforms and distribution networks, and our ability to establish new direct sales platforms or distribution networks.

Our evolving business model and the evolution of China’s direct sales industry makes it difficult to evaluate our business and future prospects.

Our business model has varied throughout our operating history in response to changes in the direct sales industry and the regulatory environment in China. In response to regulatory changes our direct sales model now consists of primarily outbound marketing and Internet sales. Also, as the direct sales industry has evolved we have begun to focus on sourcing other branded products to complement our own proprietary-branded product lines, including Ozing electronic learning products and Youngleda health products for distribution through our direct sales channel and our distribution channel.

The evolution of our business model makes it difficult for you to evaluate our business and future prospects. Our longer term goal is to become one of the leading direct marketing and branding companies in China that markets and distributes our proprietary, self-owned brands and products as well as well-established and promising new third-party brands and products. To achieve this goal, we need to continue to grow our business across platforms and product lines. Our ability to successfully implement our strategy is subject to various risks and uncertainties, including:

| 10 |

| • | our relatively short history in the Internet business; |

| • |

dramatic changes in success levels of our different brands from year to year, e.g., from Ozing electronic learning products last year to BABAKA branded posture correction products this year; |

| • | our ability to maintain awareness of our brands, generate sales and develop customer loyalty through our direct sales platform, particularly following our termination of TV direct sales in early 2015; |

| • | our ability to anticipate and adapt to new media platforms and technological developments; |

| • | changes in government regulations, industry consolidation and other significant competitive and market dynamics; |

| • | our ability to upgrade our technology or infrastructure to keep pace with our current and future direct sales platforms; and |

| • | the potential need in the future for additional capital to finance our expansion of these business operations, which may not be available on reasonable terms or at all; and |

| • | the need to recruit additional skilled employees, including technicians and managers at different levels. |

There can be no assurance that we will be able to effectively manage these risks or execute our business strategies, which could have a material adverse effect on our growth, results of operations and business prospects.

Our operating results fluctuate from period to period, making them difficult to predict.

Our operating results are highly dependent upon, and will fluctuate based on, the following product-related factors:

| • | the mix of products selected by us for marketing through our direct sales platforms and our nationwide distribution network and their average selling prices; |

| • |

Declining impact of historical large TV marketing spend on our primary products as time passes and we are no longer marketing on TV;

| |

| • | Positive and negative publicity about our products and our company generally; |

| • | new product introductions by us or our competitors and our ability to identify new products; |

| • | the availability of competing products and possible reductions in the sales price of our products over time in response to competitive offerings or in anticipation of our introduction of new or upgraded offerings; |

| • | seasonality with respect to certain of our products, such as our electronic learning products, for which sales are typically higher around our first and third fiscal quarters corresponding with the end and beginning of school semesters in China, respectively; |

| • | the market of certain featured products becoming saturated over time; |

| • | discounts offered to our distributors as part of incentive plans to stimulate sales; |

| • | the success of our distributors in promoting and selling our products locally; |

| • | the potential negative impact distributor sales may have on our own direct sales efforts; and |

| 11 |

| • | depletion of our pool of quality names or data for outbound marketing. |

In addition, factors not directly relating to our products which could cause our operating results to fluctuate in a particular period or in comparison to a prior period include:

| • | new laws, regulations or rules promulgated by the PRC government governing the consumer products marketing and branding industries; |

| • | natural disasters, such as the severe snow storms or earthquake experienced by China in 2008; |

| • | the amount and timing of operating expenses incurred by us, including our media procurement expenses, inventory-related losses, bad debt expense, product returns and options grants to our employees; |

| • | gains and losses related to our sale of non-core assets and our investments in marketable and other securities; and |

| • | the level of advertising and other promotional efforts by us and our competitors in a particular period. |

Due to these and other factors, our operating results will vary from period to period, will be difficult to predict for any given period, may be adversely affected from period to period and may not be indicative of our future performance. If our operating results for any period fall below our expectations or the expectations of investors or any market analyst that may issue reports or analyses regarding our ADSs, the price of our ADSs is likely to decrease.

Changes in the quoted prices for Shanghai Yimeng Software Technology Co., Ltd., or Yimeng, on the China National Equities Exchange and Quotations, or NEEQ, will cause the carrying value of our Yimeng shares to vary impacting our comprehensive net income; and our ability to sell our Yimeng shares at desired prices or in desired volumes will be impacted by related developments in the NEEQ market and the market for Yimeng shares.

In July 2015, Yimeng listed on the NEEQ and at December 31, 2016 our 8.5% ownership stake in Yimeng was valued at $74.7 million. During 2017, we continued to sell Yimeng shares on the NEEQ. Through April 30, 2017, we reduced our ownership stake in Yimeng to 7.5% and at such date our remaining ownership stake (consisting of approximately 32.7 million Yimeng shares) was valued at $66.8 million. Our management will consider additional sales of Yimeng shares as it deems appropriate.

The NEEQ is a new over-the-counter (OTC) market in China listing companies not otherwise eligible for listing on China’s other markets including the Shanghai and Shenzhen Main Boards. Both the NEEQ and Yimeng’s shares on the NEEQ have experienced significant volatility and limited liquidity. On March 28, 2017, Yimeng announced that it is temporarily halting the trading of its stock on NEEQ in anticipation of a potential material event and is expected to resume trading no later than June 28, 2017. We may be unable to sell our Yimeng shares at prices equal to the then-quoted price and or in desired volumes. Sales of Yimeng shares by us or others could also impact the price of Yimeng shares due to the limited trading volume. Actions by Yimeng may also restrict our ability to sell Yimeng shares. For example, Yimeng has publicly announced that it is engaged in a counseling period for listing on China’s Shanghai Mainboard. As a result, with the permission of the Mainboard, Yimeng may de-list its shares on the NEEQ which could result in there being no potential public market for Yimeng shares for an extended period of time (possibly for as long as four years or longer).

If we are deemed an “investment company” under the U.S. Investment Company Act of 1940, it would adversely affect the price of our ADSs and ordinary shares and could have a material adverse effect on our business.

As of the date of this annual report, our assets include a 7.5% interest in Yimeng. This may be deemed to be “investment securities” within the meaning of the Investment Company Act of 1940, as amended. Our investment in Yimeng and other factors may cause us to be deemed to be an “investment company” under the Investment Company Act. As a foreign private issuer, we would not be eligible to register under the Investment Company Act, so if we are deemed to be an investment company within the meaning of the Investment Company Act, we would either have to obtain exemptive relief from the SEC or dispose of investments in order to fall outside the definition of an investment company. Additionally, we may have to forego potential future acquisitions of interests in companies that may be deemed to be investment securities within the meaning of the Investment Company Act. Failure to avoid being deemed an investment company under the Investment Company Act coupled with our inability as a foreign private issuer to register under the Investment Company Act could make us unable to comply with our reporting obligations as a public company in the United States and lead to our being delisted from the New York Stock Exchange, which would have a material adverse effect on the liquidity and value of our ADSs and ordinary shares.

Our best-selling featured product lines, such as our Babaka product line, have varied significantly but account for, and are expected to continue to account for, the substantial majority of our sales in the near term. Featured products sales may decline, these products may have limited product lifecycles, and we may fail to introduce new products to offset declines in sales of our featured products.

Over the three years ended in 2015, we became increasingly dependent on our electronic learning device product line which is one of our oldest product lines and accounted for 22.1%, 46.5% and 51.7% of our gross revenue in 2013, 2014 and 2015. However, due to intense competition and other factors, sales of our electronic learning products declined in 2016, representing only 32.8% of our total gross revenues last year. While these declines were partially offset in 2016 by increased sales of our Babaka branded posture correction product, we cannot assure you this trend will continue. In addition, our five best-selling featured product lines accounted for 89.7%, 94.4% and 95.7% of our gross revenues in 2014, 2015 and 2016, respectively. Our featured products may fail to maintain or achieve sufficient consumer market popularity and sales may decline due to, among other factors, the introduction of competing products, entry of new competitors, customer dissatisfaction with the value or quality offered by our products, negative publicity or market saturation. Consequently, our future sales success depends on our ability to successfully identify, develop, introduce and distribute in a timely and cost- effective manner new and upgraded products.

| 12 |

Our product sales for a given period will depend upon, among other things, a positive customer response to our direct sales efforts, as well as the efforts of our distributors, our effective management of product inventory, the stage of our products’ lifecycles during the period or our add-on services provided in connection with our products. Positive customer responses depend on many factors, including the appeal of the products and services being marketed, the effectiveness of our direct sales platforms and the viability of competing products. Our new products may not receive market acceptance. In addition, from time to time, we experience delays in the supply of our products to customers due to production delays or shortages or inadequate inventory management, and we lose potential product sales as a result. Furthermore, during a product’s lifecycle, problems may arise regarding regulatory, intellectual property, product liability or other issues which may affect the continued viability of the product for sale.

If we fail to identify and introduce additional successful products, including those to replace existing featured products suffering from declining sales or approaching the end of their product lifecycle, our gross revenues may not grow or may decline and our market share and value of our brand may be materially and adversely affected. In addition, any change in the provision of our add-on services, such as the internet interactive services provided for our featured electronic learning products could materially and adversely affect the perception and acceptance of our products, which could materially and adversely affect our business, financial condition and results of operations.

Our failure to quickly identify and adapt to changing industry conditions may have a material and adverse effect on our business, financial condition and results of operations.

The online and offline consumer marketing and sales industries are subject to changing consumer preferences and industry conditions. Consequently, we must stay abreast of emerging fashion, lifestyle, design, technological and other industry and consumer trends. This requires timely collection of market feedback, accurate assessments of market trends, deep understanding of industry dynamics and flexible manufacturing capabilities.

We must also maintain relationships with suppliers who can adapt to fast-changing consumer preferences. If one or more of our existing suppliers cannot meet these requirements effectively, we will need to find and source from new suppliers, which may be costly and time-consuming. We or our suppliers may overestimate customer demand, face increased overhead expenditures without a corresponding increase in sales and incur inventory write-downs, which will adversely affect our results of operations.

If we cannot offer appealing products on our websites or through our other direct sales platforms or distributors, our customers may purchase fewer products from us or stop purchasing products from us altogether. Our reputation may also be negatively impacted. If we do not anticipate, identify and respond effectively to consumer preferences or changes in consumer trends at an early stage, we may not be able to generate our desired level of sales. Failure to properly address these challenges may materially and adversely affect our business, financial condition and results of operations.

Our business depends significantly on the strength of our product brands and corporate reputation; our failure to develop, maintain and enhance our product brands and corporate reputation may materially and adversely affect the level of market recognition of, and trust in, our products.

In China’s fragmented, developing and increasingly competitive consumer market, product brands and corporate reputation have become critical to the success of our new products and the continued popularity of our existing products. Our brand promotion efforts, particularly our brand promotion activities, may be materially and adversely affected by our suspending purchases of TV airtime for TV direct sales programs, and our other promotion activities may prove to be expensive and may fail to either effectively promote our product brands or generate additional sales.

In addition, our product brands, corporate reputation and product sales could be harmed if, for example:

| • | our advertisements, or the advertisements of the owners of the third-party brands that we market or those of our distributors, are deemed to be misleading or inaccurate; |

| • | our products fail to meet customer expectations; |

| • | we provide poor or ineffective customer service; |

| • | our products contain defects or otherwise fail; |

| • | consumers confuse our products with inferior or counterfeit products; or |

| • | consumers find our outbound marketing intrusive or annoying. |

Furthermore, some of our customers reported that they have received phone calls from certain unidentified third parties impersonating our staff. These unidentified individuals called our customers to request that they (i) modify their order because the ordered product was out of stock or (ii) reject an ordered product upon delivery because it was damaged. In some cases, these unidentified individuals delivered counterfeit or inferior products to our customers. After our internal investigation and the investigation conducted by relevant PRC authorities, a group of impersonators were arrested by the police and were sentenced by the court in August 2011. Since 2011, we have identified other occurrences involving individuals impersonating our staff and calling our customers to achieve similar results, and in each case we identified such activities, have taken steps necessary to thwart and prosecute the impersonators. Although we continue to take steps reasonably aimed at preventing such events from recurring, including periodic internal investigations, there can be no assurance that we will be able to effectively prevent the recurrence of such events in the future, and in case such events recurs in the future, it could materially adversely affect our reputation among our customers and potential customers and our result of operations.

| 13 |

We rely on our nationwide distribution network for a substantial portion of our revenues. Failure to maintain good distributor relations could materially disrupt our distribution business and harm our net revenues.

Our distribution sales account for a substantial portion of our net revenues. In 2014, 2015 and 2016, 52.3%, 59.2%, and 43.6% respectively, of our net revenues were generated through our distributors across China. Our largest distributor accounted for approximately 4.5%, 14.2%, and 6.0% of our gross revenues in 2014, 2015 and 2016, respectively. We do not maintain long-term contracts with our distributors. Maintaining relationships with existing distributors and replacing any distributor may be difficult or time consuming. In addition, we are in the process of rationalizing and streamlining our distribution network to adapt to our evolving business model. If we cannot negotiate favorable terms regarding our distribution agreement with our existing distributors, they may discontinue their relationships with us and we may not be able to identity and attract new distributors or find suitable replacement of our existing distributors. Our failure to maintain good relationships with our distributors could materially disrupt our distribution business and harm our net revenues.

We may be unable to effectively manage our nationwide distribution network. Any failure by our distributors to operate in compliance with our distribution agreements and applicable law may result in liability to us, may interrupt the effective operation of our distribution network, may harm our brands and our corporate image and of which may result in decreased sales.

We have limited ability to manage the activities of our distributors, who operate independently from us. In addition, our distributors or the retail outlets to which they sell our products may violate our distribution agreements with them or the sales agreements between our distributors and the retail outlets. Such violations may include, among other things:

| • | failure to meet minimum sales targets for our products or minimum price levels for our products in accordance with relevant agreements; |

| • | failure to properly promote our products through local marketing media, including Internet and local print media, violation of our media content requirements, or failure to meet minimum required media spending levels; |

| • | selling products that compete with our products, including product imitations, or selling our products outside their designated territories, possibly in violation of the exclusive distribution rights of other distributors; |

| • | providing poor customer service of the after-sale repair or return; or |

| • | violating PRC law in the marketing and sale of our products, including PRC restrictions on advertising content or product claims. |

In particular, we have discovered that some of the retail outlets to which our distributors sell our products are selling imitation products that compete with our products, such as our Ozing electronic learning product. Although we continue to rigorously monitor this situation and require our distributors to abide by their contractual obligation to eliminate any such violation by the retail outlets, we may be unable to police or stop violations such as the selling of imitation products by retail outlets.

If we determine to fine, suspend or terminate our distributors for acting in violation of our distribution agreements, or if the distributors fail to address material violations committed by any of their retail outlets, our ability to effectively sell our products in any given territory could be negatively impacted. In addition, these and similar actions could negatively affect our brands and our corporate image, possibly resulting in loss of customers and a decline in sales.

We may not realize the anticipated benefits of our potential future joint ventures, acquisitions or investments or be able to integrate any acquired employees, businesses, products, which in turn may negatively affect their performance and respective contributions to our results of operations.

From time to time, we conduct acquisitions, make investments or enter into joint ventures or other investment structures with other entities as a means of developing new products, acquiring managerial expertise or further expanding our complementary distribution network infrastructure. In addition to the two joint ventures and other minority investments that we currently maintain, we may continue to enter into similar joint ventures or make other acquisitions or investments when proper opportunities occur. Risks related to our existing and future joint ventures, acquisitions and investments include, as applicable:

| • | our ability to enter into, exit or acquire additional interests in our joint ventures or other acquisitions or investments may be restricted by or subject to various approvals under PRC law or may not otherwise be possible, may result in a possible dilutive issuance of our securities or may require us to secure financing to fund those activities; |

| • | we may disagree with our joint venture partner(s) or other investors on how the venture or business investment should be managed and/or operated; |

| • | to the degree we wish to do so, we may be unable to integrate and retain acquired employees or management personnel; incorporate acquired products, or capabilities into our business; integrate and support pre-existing manufacturing or distribution arrangements; consolidate duplicate facilities and functions; or combine aspects of our accounting processes, order processing and support functions; and |

| 14 |

| • | the joint venture or investment could suffer losses and we could lose our total investment, which would have a negative effect on our operating results. |

Any of these events could distract our management’s attention and result in our not obtaining the anticipated benefits of our joint ventures, acquisitions or investments and, in turn, negatively affect the performance of such joint ventures, acquisitions and investments and their respective contributions to our results of operations.

Our business could be disrupted and our business prospects could be adversely affected if we were to lose the services of our co-founder, Mr. Robert W. Roche, our business could be further disrupted.

Mr. Roche has played an important role in the growth and development of our business since its inception. If Mr. Roche is unable or unwilling to continue in his present position, we may be unable to replace him easily or at all, our business could be severely disrupted, and our financial condition and results of operations could be materially and adversely affected. We do not maintain key-man life insurance on Mr. Roche.

If we are unable to attract, retain and motivate key personnel or hire qualified personnel, or if such personnel do not work well together, our growth prospects and profitability will be harmed.

Our business is supported and enhanced by a team of highly skilled employees who are critical to maintaining the quality and consistency of our business and reputation. It is important for us to attract qualified employees, especially marketing personnel, supply chain managers, call center operators and employees with high levels of experience in Internet-related sales.

During 2015, 2016 and continuing into 2017, we have effected a substantial reduction in our work force across all functions of our operations and restructured our senior management, which reductions are primarily driven by cost control efforts as well as restructuring and streamlining our business structure and operation. In addition, through voluntary attrition, certain key personnel have recently left, and we have yet to recruit replacements. The reductions and adjustments in our workforce and the loss of such key personnel could seriously harm the moral of existing employees and our ability to attract prospective employees in key areas of need or retain current key personnel in critical areas of operations, which could disrupt our business and operations and negatively affect our financial performance.

We must also provide continuous training to our employees so that they have up-to-date knowledge of various aspects of our operations and can meet our demand for high quality services. If we fail to do so, the quality of our services may deteriorate in one or more of the markets where we operate, which may cause a negative perception of our brand and adversely affect our business. Finally, disputes between us and our employees may arise from time to time and if we are not able to properly handle our relationship with our employees, our business, financial condition and results of operations may be adversely affected.

In fulfilling sales through our direct sales platforms, we face customer acceptance, delivery, payment and collection risks that could adversely impact our direct sales net revenues and overall operating results. We are dependent on China Express Mail Service Corporation, or EMS and local delivery companies, to make our product deliveries and from time to time we have been required to write off certain accounts receivable from them.

We rely on EMS, the largest national express mail service operated by the China Post Office, and certain local delivery companies such as Yuantong and Zhai-ji-song to deliver products sold through our direct sales platforms. EMS and local delivery companies made deliveries of products representing 11.3% and 36.4% of our sales in 2014, respectively, 16.4% and 24.4% of our sales in 2015, respectively, and 16.3% and 40.1% of our sales in 2016, respectively. Although we offer credit/debit card and other payment options for our customers, substantially all of the products that we sell through our direct sales platforms are delivered and paid for by customers on a cash-on-delivery, or COD, basis. We rely on EMS and local delivery companies to remit customer payment collections to us. Of the total attempted product deliveries by EMS and local delivery companies on a COD basis, approximately 68%, 54% and 45% were successful in 2014, 2015 and 2016, respectively. Reasons for delivery failure primarily include customer refusal to accept a product upon delivery or failure to successfully locate the delivery address. Although we continue to explore alternative payment methods and expand our credit card payment options, we expect to continue to be dependent on COD customer payments for the foreseeable future.

| 15 |

EMS typically requires two to three weeks to remit to us the COD payments received from our customers. Of our total accounts receivable balance as of December 31, 2014, 2015 and 2016, no single delivery company accounted for more than 10% of our total accounts receivables. In addition, from time to time, we have been required to write off certain EMS accounts receivable due to a difference between EMS’s collections according to our records and cash amounts actually received by EMS according to their records. The total amount of EMS-related accounts receivable written off in 2014 was approximately $0.2 million. While we did not record any write-off in connection with EMS-related accounts receivable in 2015 and 2016, we may be required to make such write-off in the future. We do not maintain a long-term contract with EMS or local delivery companies. Failure or inability to renew our contract with EMS or local delivery companies could disrupt our business and operations and negatively affect our financial performance.

We expect competition in China’s consumer market to intensify. If we do not compete successfully against new and existing competitors, we may lose our market share, and our profitability may be adversely affected.

Competition from current or future competitors could cause our products to lose market acceptance or require us to significantly reduce our prices or increase our promotional activities to maintain and attract customers. Many of our current or future competitors may have longer operating histories, better brand recognition and consumer trust, strong media management capabilities, better media and supplier relationships, a larger technical staff and sales force and/or greater financial, technical or marketing resources than we do. We face competition from the following companies operating in our value chain:

| • | numerous domestic and international sellers of consumer branded products that sell their products in China and which compete with our products, such as our Youngleda health products which compete with Oxygen-generating devices from Yuwell, Ding Xiang, De Li Kang and other brands, and our mobile phone products which compete with similar products sold by local and international mobile phone manufacturers; and |

| • | other Internet and e-commerce companies in China that offer consumer products online via an Internet platform, such as Tmall, JD.COM, Dang Dang Wang and Yihaodian. |

Interruption or failure of our telephone system and management information systems could impair our ability to effectively sell and deliver our products or result in a loss or corruption of data, which could damage our reputation and negatively impact our results of operations.

In 2015, we consolidated our four call centers into our call center located in Wuxi, China. In 2014, 2015 and 2016, approximately 47.9%, 29.7% and 14.5% of our total net revenues, respectively, were generated through our direct sales platforms with orders processed by our call centers. In 2014 and through early 2015, our call center relies heavily on our telephone and management information systems, or MIS, to receive customer calls at our call center, process customer purchases, arrange product delivery and assess the effectiveness of advertising placements and consumer acceptance of our products, among other things. We may experience difficulties or call center interruptions due to our consolidation activities. As our business evolves and our MIS requirements change, we may need to modify, upgrade and replace our systems. We work closely with third-party vendors and our related party vendors to provide telephone service tailored to our specific needs. We are and will continue to be substantially reliant on these third-party vendors for the provision of maintenance, modifications, upgrades and replacements to our systems. If these third-party vendors can no longer provide these services, it may be difficult, time consuming and costly to replace them. Any such modification, upgrading or replacement of our systems may be costly and could create disturbances or interruptions to our operations. Similarly, undetected errors or inadequacies in our telephone and MIS may be difficult or expensive to timely correct and could result in substantial service interruptions.

From time to time, our computer systems may experience short periods of power outage resulted from unexpected damage of the facilities where our computers system locate, natural disasters or other reasons. Any telephone or MIS failure (including as a result of natural disaster or power outage), particularly during peak or critical periods, could inhibit our ability to receive calls and complete orders or evaluate the effectiveness of our promotions or consumer acceptance of our products or otherwise operate our business. These events could, in turn, impair our ability to effectively sell and deliver our products or result in the loss or corruption of customer, supplier and distributor data, which could damage our reputation and negatively impact our results of operations.

| 16 |

The provision of our add-on services via third party service providers may be beyond our control and negatively impact our customer experience, and we may not be able to continue to provide such services if we are deemed to be providing online education service, which could substantially harm our business, financial condition and results of operations and expose us to liabilities.

In order to provide internet interactive services to users of our electronic learning products or mobile apps, we maintain a large team of service providers with an aim to respond to inquiries from our customers on their inquiries on a real time basis. However, we may not be able to properly control or monitor the quality of these third party service providers engaged by us. If our third party service providers fail to provide quality services that meet the expectation of our customers or fail to continuously provide their services, it could damage our reputation and adversely affect our customer’s experience. Moreover, if our provision of such add-on services were to be deemed by relevant PRC government authorities to be providing online education services, we may not be able to continue to product such services as we would need to obtain relevant licenses and permits from relevant PRC government authorities. If any such circumstances happen, it could substantially harm our business, financial condition and results of operations and expose us to liabilities.

Failure to protect personal and confidential information of our customers could damage our reputation and substantially harm our business, financial condition and results of operations and expose us to liability.

We collect and store personally identifiable information of our customers in our database through which we sell and market our products. We may not be able to prevent our employees or other third parties, such as hackers, criminal organizations, our external service providers and business partners, from stealing or leaking information provided by our customers to us. In addition, significant capital and other resources may be required to protect against security breaches or to alleviate problems caused by such breaches. The methods used by hackers and others engaged in online criminal activities are increasingly sophisticated and constantly evolving. Even if we are successful in adapting to and preventing new security breaches, any perception by the public that the privacy of customer information are becoming increasingly unsafe or vulnerable to attack could inhibit the growth of online business generally, which in turn may reduce our customers’ confidence and materially and adversely affect our business and prospects. Moreover, we are required to comply with laws and regulations in connection with protection of electronic personal information of our customers in China and we may be obligated to comply with the privacy and data security laws of foreign countries where our customers reside. With the promulgation of the PRC Cyber Security Law in November 7, 2016 and effective from June 1, 2017, we will face more stringent requirements to protect the personal information we collect from being divulged or tampered with. Failure to comply with such requirements will result in more severe administrative penalties. Our exposure to the PRC and foreign countries’ privacy and data security laws impacts our ability to collect and use personal data, increases our legal compliance costs and may expose us to liability. As such laws proliferate, there may be uncertainty regarding their application or interpretation, which consequently increases our exposure to potential compliance costs and liability. Even if a claim of noncompliance against us does not ultimately result in liability, investigating or responding to a claim may present significant costs and demands on our management.

We could be liable for breaches of security of our service and third-party payment systems, which may have a material and adverse effect on our reputation and business.

In recent years, we have generated an increasingly significant proportion of our net revenues from payments collected through third-party online payment systems, which are primarily generated from our Internet sales. In such transactions, confidential information, such as customers’ debit and credit card numbers and expiration dates, personal information and billing addresses, is transmitted over public networks and security of such information is essential for maintaining customer confidence. While we have not experienced any breach of our security to date, current security measures may prove to be inadequate. In addition, we expect that an increasing number of our sales will be conducted over the Internet as a result of our expanding customer base and the growing use of online payment systems. We also expect that associated online criminal activities will likely increase accordingly. We strive to be prepared to increase our security measures and efforts in order to maintain customer confidence in the reliability of our online payment systems. However, we may not be able to prevent future breaches of our security, which may have a material and adverse effect on our reputation and business.

We may not be able to prevent others from unauthorized use of our intellectual property, which could harm our product brand, reputation and competitive position. In addition, we may have to enforce our intellectual property rights through litigation. Such litigation may result in substantial costs and diversion of resources and management attention.

We rely on a combination of patent, copyright, trademark and unfair competition laws, as well as nondisclosure agreements and other methods to protect our intellectual property rights. In particular, we rely on the trademark law in China to protect our product brands. We currently maintain 624 trademark registrations in China which expire between 2017 and 2025. We are in the process of extending the trademarks which are expected to expire in the near future. Separately, we are in the process of applying for registration or transfer of approximately 182 trademarks among our group companies in China. The legal regime in China for the protection of intellectual property rights is still at a relatively early stage of development. Despite many laws and regulations promulgated and other efforts made by China over the years to enhance its regulation and protection of intellectual property rights, private parties may not enjoy intellectual property rights in China to the same extent as they would in many western countries, including the United States, and enforcement of such laws and regulations in China has not achieved the levels reached in those countries. Although the PRC State Council approved the State Outlines on the Protection of Intellectual Property on April 9, 2008 in an effort to protect intellectual property, we shall keep on making endeavors to prevent the misappropriation of our intellectual property.

We may be unable to enforce our proprietary rights in connection with these trademarks before such registrations or transfers are approved by the relevant authorities and it is possible that such registrations or transfers may not be approved at all. In addition, manufacturers or suppliers in China may imitate our products, copy our various brands and infringe our intellectual property rights. We have discovered unauthorized products on e-commerce platforms and in the marketplace that are counterfeit reproductions of our products sold by the retailers within our nationwide distribution network and by third parties in retail stores and on websites. The counterfeit products that we found include our Babaka posture correction products, our Yierjian fitness products, Vibrashape fitness products, cosmetic products and our health products.

| 17 |

It is difficult and expensive to police and enforce against infringement of intellectual property rights in China. Imitation or counterfeiting of our products or other infringement of our intellectual property rights, including our trademarks, could diminish the value of our various brands, harm our reputation and competitive position or otherwise adversely affect our net revenues. We may have to enforce our intellectual property rights through litigation. Such litigation may result in substantial costs and diversion of resources and management attention.

We have in the past been and in the future may again be, subject to intellectual property rights infringement claims by third parties, which could be time-consuming and costly to defend or litigate, divert our attention and resources, or require us to enter into licensing agreements. These licenses may not be available on commercially reasonable terms, or at all.

We have in the past been and in the future may again be, the subject of claims for infringement, invalidity, or indemnification relating to other parties’ proprietary rights. The defense of intellectual property suits, including copyright infringement suits, and related legal and administrative proceedings can be costly and time consuming and may significantly divert the efforts and resources of our technical and management personnel. Furthermore, an adverse determination in any such litigation or proceeding to which we may become a party could cause us to pay damages, seek licenses from third parties, pay ongoing royalties, redesign our products or become subject to injunctions, each of which could prevent us from pursuing some or all of our businesses and result in our customers or potential customers deferring or limiting their purchase or use of our products, which could materially and adversely affect our financial condition and results of operations.

We may from time to time be involved in legal or other disputes, or become a party to legal, administrative or other proceedings which, if adversely decided, could lead to significant liabilities and materially adversely affect us.

We may from time to time be involved in disputes with various parties involved in our daily operations, including but not limited to our suppliers, customers and distributors. These disputes may lead to legal, administrative or other proceedings to which we are a party, and defense of which may increase our expenses and divert management attention and resources. For example, in September 2015, Beijing Mai-La-Ke Technology Center, or the Mai-La-Ke, the previous holder of the trademark of our Oxygen-generating devices, filed a suitcase in the Haidian People’s Court in Beijing against Beijing Acorn Trade Co., Ltd and Beijing Acorn Younglide Science and Technology Co., Ltd., alleging that the two defendants should provide relevant data of selling our Oxygen-generating devices from November 2000 to November 2005 in order for them to claim for 50% of the net profit for the period based on a previous agreement with the two defendants. In July 25, 2016, the Haidian People’s Court in Beijing issued the first-instance judgment in which all claims raised by Mai-La-Ke were rejected. As of the date of this annual report, Mai-La-Ke has not appealed.

We were also the subject of the legal dispute between our shareholders as described immediately below.

Any adverse outcome in any legal, administrative or other similar proceedings that we are a party could lead to significant liabilities and could have a material adverse effect on our business, results of operations and financial condition.

Historical and ongoing disputes regarding control of our strategic direction and control of our board of directors could adversely impact our business, operating results and prospects.

From mid-2014 through mid-2015, we and our board of directors were involved in a protracted dispute between various shareholders for the control of our strategic direction and our board of directors. The alignment of the various parties to this dispute generally fell across two lines, with Mr. Robert W. Roche, our co-founder and our executive chairman and chief executive officer, and shareholders that are allied with him, in one camp, and the other camp comprised of our other largest shareholders, Mr. Don Dongjie Yang, our other co-founder and our former executive chairman and chief executive officer, and SB Asia Investment Fund II L.P.

As described in greater detail in Item 8.A, “Financial Information—Consolidated statements and other financial information— Legal Proceedings,” this dispute involved, among other things (i) the improper removal of Mr. Roche by our then-board of directors, comprising Mr. Robert W. Roche, Mr. Don Dongjie Yang, Mr. Andrew Y. Yan, Mr. Gordon Xiaogang Wang, Mr. Jing Wang and Mr. William Liang, from his role as executive chairman in August 2014 and, as a result, his preclusion from involvement in our day-to-day operations and management, (ii) various efforts by Mr. Roche (which were rejected by our then-board of directors) to call an extraordinary general meeting of shareholders, or EGM, for the purpose of removing certain of our directors, (iii) Mr. Roche, through a shareholder of our company controlled by him, filing a petition in the Cayman Islands in September 2014, seeking a winding up of the company (or, in the alternative, other remedies), (iv) a cross-petition brought by shareholders of our company controlled or aligned with Mr. Yang also seeking a winding up of the company (or, in the alternative, other remedies) based on, among other things, allegations that Mr. Roche engaged in conduct and/or threatened to engage in conduct harmful to the company, and (v) four new directors being elected in December 2014 at our annual general meeting over Mr. Roche’s objection.