Table of Contents

| |

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| |

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered | ||

The | ||||

The |

| |

☒ |

Accelerated filer |

☐ | |||

| Non-accelerated filer |

☐ |

Emerging growth company |

| |||

| † |

The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

| |

International Financial Reporting Standards as issued by the International Accounting Standards Board ☐ |

Other | ☐ |

Table of Contents

HOLLYSYS AUTOMATION TECHNOLOGIES LTD.

ANNUAL REPORT ON FORM 20-F

FOR THE FISCAL YEAR ENDED JUNE 30, 2023

TABLE OF CONTENTS

| Page | ||||||

| PART I | ||||||

| ITEM 1. |

5 | |||||

| ITEM 2. |

5 | |||||

| ITEM 3. |

5 | |||||

| ITEM 4. |

40 | |||||

| ITEM 4A. |

68 | |||||

| ITEM 5. |

69 | |||||

| ITEM 6. |

84 | |||||

| ITEM 7. |

94 | |||||

| ITEM 8. |

95 | |||||

| ITEM 9. |

96 | |||||

| ITEM 10. |

96 | |||||

| ITEM 11. |

109 | |||||

| ITEM 12. |

110 | |||||

| PART II | ||||||

| ITEM 13. |

111 | |||||

| ITEM 14. |

MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITIES HOLDERS AND USE OF PROCEEDS |

111 | ||||

| ITEM 15. |

111 | |||||

| ITEM 16A. |

112 | |||||

| ITEM 16B. |

113 | |||||

| ITEM 16C. |

113 | |||||

| ITEM 16D. |

113 | |||||

| ITEM 16E. |

PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS |

114 | ||||

| ITEM 16F. |

114 | |||||

| ITEM 16G. |

115 | |||||

| ITEM 16H. |

115 | |||||

| ITEM 16I. |

DISCLOSURE REGARDING FOREIGN JURISDICTIONS THAT PREVENT INSPECTIONS |

115 | ||||

| ITEM 16J. |

115 | |||||

| PART III | ||||||

| ITEM 17. |

116 | |||||

| ITEM 18. |

116 | |||||

| ITEM 19. |

116 | |||||

i

Table of Contents

USE OF CERTAIN DEFINED TERMS

Except as otherwise indicated by the context, references in this annual report to:

| • |

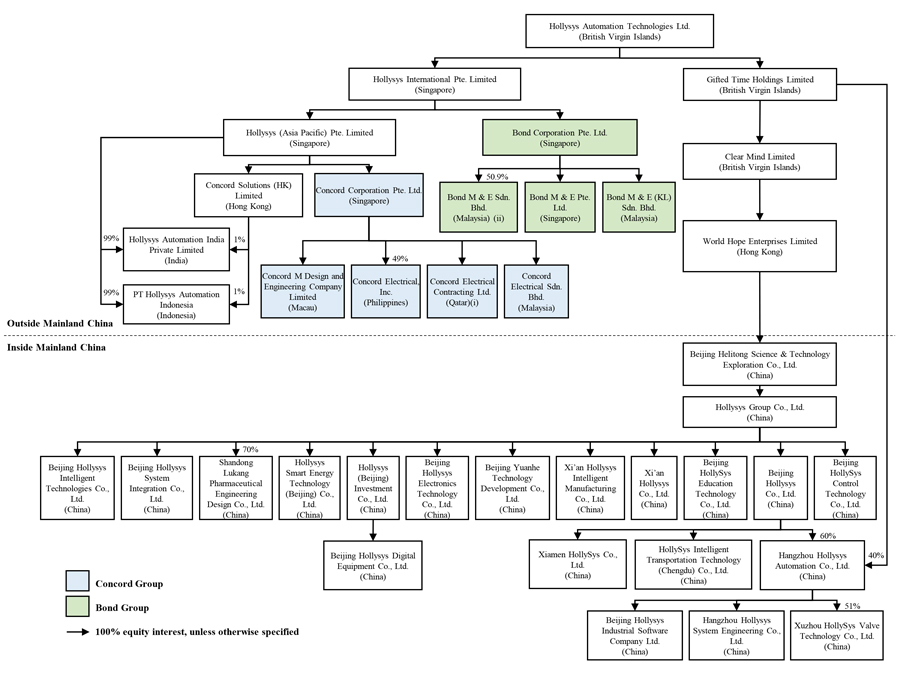

“Hollysys,” “we,” “us,” or “our,” and “the Company,” refer to the combined business of Hollysys Automation Technologies Ltd., a BVI company, and its consolidated subsidiaries, HI, HAP, HAIP, PTHAI, Bond Group, Concord Group, CSHK, GTH, Clear Mind, World Hope, Helitong, Hollysys Group, Hangzhou Hollysys, Hangzhou System, Hollysys Industrial Software, Beijing Hollysys, Hollysys Electronics, Xi’an Hollysys, Hollysys Investment, HollySys Smart Energy, Shandong Lukang, Xuzhou HollySys, Hollysys Intelligent, HollySys System Integration, HollySys Control, HollySys Education, Xiamen HollySys, and Chengdu HollySys Transportation; |

| • |

“HI” refers to Hollysys International Pte. Limited, a Singapore company; |

| • |

“HAP” refers to Hollysys (Asia Pacific) Pte. Limited, a Singapore company; |

| • |

“HAIP” refers to Hollysys Automation India Private Limited, an India Company; |

| • |

“Bond Group” refers to a group of our subsidiaries, including Bond Corporation Pte. Ltd. (“BCPL”), a Singapore company, Bond M&E Pte. Ltd. (“BMSG”), a Singapore Company, Bond M&E Sdn. Bhd. (“BMJB”), a Malaysia company, and Bond M&E (KL) Sdn. Bhd. (“BMKL”), a Malaysia company; |

| • |

“Concord Group” refers to a group of our subsidiaries, including Concord Corporation Pte. Ltd. (“CCPL”), a Singapore company, and CCPL’s subsidiaries, Concord Electrical Sdn. Bhd. (“CESB”), a Malaysia company, Concord Electrical Contracting Ltd. (“CECL”), a Qatar company, Concord M Design and Engineering Company Limited. (“CMDE”), a Macau company, and Concord Electrical, Inc. (“CEI”), a Philippines company; |

| • |

“CSHK” refers to Concord Solutions (HK) Limited, a Hong Kong company; |

| • |

“PTHAI” refers to PT Hollysys Automation Indonesia, an Indonesian company; |

| • |

“GTH” refers to Gifted Time Holdings Limited, a BVI company; |

| • |

“Clear Mind” refers to Clear Mind Limited, a BVI company; |

| • |

“World Hope” refers to World Hope Enterprises Limited, a Hong Kong company; |

| • |

“Helitong” refers to Beijing Helitong Science & Technology Exploration Co., Ltd., a PRC company; |

| • |

“Hollysys Group” refers to Hollysys Group Co., Ltd., formerly known as Beijing Hollysys Science & Technology Co., Ltd, a PRC company; |

| • |

“Hangzhou Hollysys” refers to Hangzhou Hollysys Automation Co., Ltd., a PRC company; |

| • |

“Hangzhou System” refers to Hangzhou Hollysys System Engineering Co., Ltd., a PRC company; |

| • |

“Hollysys Industrial Software” refers to Beijing Hollysys Industrial Software Company Ltd., a PRC company; |

| • |

“Beijing Hollysys” refers to Beijing Hollysys Co., Ltd., a PRC company; |

| • |

“Hollysys Electronics” refers to Beijing Hollysys Electronics Technology Co., Ltd., a PRC company; |

1

Table of Contents

| • |

“Xi’an Hollysys” refers to Xi’an Hollysys Co., Ltd., a PRC company; |

| • |

“Hollysys Investment” refers to Hollysys (Beijing) Investment Co., Ltd., a PRC company; |

| • |

“HollySys Smart Energy” refers to HollySys Smart Energy Technology (Beijing) Co., Ltd., a PRC company; |

| • |

“Shandong Lukang” refers to Shandong Lukang Pharmaceutical Engineering Design Co., Ltd., a PRC company; |

| • |

“Xuzhou HollySys” refers to Xuzhou HollySys Valve Technology Co., Ltd., a PRC company; |

| • |

“Hollysys Intelligent” refers to Beijing Hollysys Intelligent Technologies Co., Ltd., a PRC company; |

| • |

“HollySys System Integration” refers to Beijing HollySys System Integration Co., Ltd., a PRC company; |

| • |

“HollySys Control” refers to Beijing HollySys Control Technology Co., Ltd., a PRC company; |

| • |

“HollySys Education” refers to Beijing HollySys Education Technology Co., Ltd, a PRC company; |

| • |

“Xiamen HollySys” refers to Xiamen HollySys Co., Ltd., a PRC company; |

| • |

“Chengdu HollySys Transportation” refers to HollySys Intelligent Transportation Technology (Chengdu) Co., Ltd., a PRC company; |

| • |

“RMB” and “CNY” refer to Renminbi, the legal currency of China; “SGD” and “S$” refer to the Singapore dollar, the legal currency of Singapore; “US dollar,” “$” and “US$” refer to the legal currency of the United States; “MYR” refers to the Malaysian Ringgit, the legal currency of Malaysia; “AED” refers to the United Arab Emirates Dirham, the legal currency of the United Arab Emirates; “HKD” refers to the Hong Kong dollar, the legal currency of Hong Kong; “MOP” refers to the Macau Pataca, the legal currency of Macau; “INR” refers to the Indian Rupee, the legal currency of India; “QAR” refers to the Qatar Riyal, the legal currency of Qatar; “IDR” refers to Indonesia Rupiah, the legal currency of Indonesia, and “PHP” refers to Philippine Peso, the legal currency of the Philippines; |

| • |

“BVI” refers to the British Virgin Islands; |

| • |

“China,” “PRC” and “mainland China” refer to the People’s Republic of China, and only in the context of describing PRC rules, laws, regulations, regulatory authority, and any PRC entities or citizens under such rules, laws and regulations and other legal or tax matters in this annual report, excludes Taiwan, Hong Kong and Macau; |

| • |

“Hong Kong” and “Hong Kong SAR” refer to the Hong Kong Special Administrative Region of China; |

| • |

“Macau” refers to the Macau Special Administrative Region of China; |

| • |

“Exchange Act” refers to the Securities Exchange Act of 1934, as amended; and |

| • |

“Securities Act” refers to the Securities Act of 1933, as amended. |

In addition, we have listed below certain technical terms we use to describe our business and industry:

| • |

APC: Advanced Process Control |

| • |

ART: Autonomous rail Rapid Transit |

| • |

ATO: Automatic Train Operation system |

| • |

ATP: Automation Train Protection |

| • |

BTM: Balise Transmission Module |

| • |

CBI: Computer Based Interlocking |

| • |

CNC: Computer Numerical Control |

| • |

CTCS: China Train Control Standard |

| • |

CTCS-2: Chinese Train Control System Level 2 |

| • |

CTCS-3: Chinese Train Control System Level 3 |

| • |

DCS: Distributed Control System |

| • |

DEH: Digital Electro-Hydraulic |

| • |

GW: Gigawatt |

| • |

HAMS: HolliAS Asset Management System |

2

Table of Contents

| • |

IIoT: Industrial Internet of Things |

| • |

LEU: Line-Side Electronic Unit |

| • |

MES: Manufacturing Execution System |

| • |

PaaS: Platform as a Service |

| • |

PLC: Programmable Logic Controller |

| • |

RBC: Radio Block Center |

| • |

SaaS: Software as a Service |

| • |

SCADA: Supervisory Control and Data Acquisition |

| • |

SIL: Safety Integrity Level |

| • |

SIS: Safety Instrumentation System |

| • |

SMT: Surface Mounting Technology |

| • |

STS: Simulation Training System |

| • |

TCC: Train Control Center |

| • |

TSRS: Temporary Speed Restriction Server |

3

Table of Contents

FORWARD-LOOKING INFORMATION

This annual report contains forward-looking statements and information relating to us that are based on the current beliefs, expectations, assumptions, estimates and projections of our management regarding our company and industry. These forward-looking statements are made under the “safe harbor” provision under Section 21E of the Securities Exchange Act of 1934, as amended, and as defined in the Private Securities Litigation Reform Act of 1995. When used in this annual report, the words “may,” “will,” “anticipate,” “believe,” “estimate,” “expect,” “intend,” “plan” and similar expressions, as they relate to us or our management, are intended to identify forward-looking statements. These statements reflect management’s current view of us concerning future events and are subject to certain risks, uncertainties and assumptions, including our potential inability to achieve similar growth in future periods as we did historically, a decrease in the availability of our raw materials, the emergence of additional competing technologies, changes in domestic and foreign laws, regulations and taxes, changes in economic conditions, uncertainties related to China’s legal system and economic, political and social events in China, the volatility of the securities markets and other risks and uncertainties which are generally set forth under the heading “Item 3. Key information—D. Risk Factors” and elsewhere in this annual report. Should any of these risks or uncertainties materialize, or should the underlying assumptions about our business and the commercial markets in which we operate prove incorrect, actual results may vary materially from those described as anticipated, estimated or expected in this annual report.

All forward-looking statements included herein attributable to us or other parties or any person acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. Except to the extent required by applicable laws and regulations, we undertake no obligations to update these forward-looking statements to reflect events or circumstances after the date of this annual report or to reflect the occurrence of unanticipated events.

4

Table of Contents

PART I

| ITEM 1. |

IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

Not applicable.

| ITEM 2. |

OFFER STATISTICS AND EXPECTED TIMETABLE |

Not applicable.

| ITEM 3. |

KEY INFORMATION |

Implications of Being a Holding Company

Our investors hold securities of Hollysys Automation Technologies Ltd., which is not an operating company but a BVI holding company that conducts operations in China mainly through its Chinese operating subsidiaries and in Southeast Asia and the Middle East mainly through Concord Group and Bond Group. Investors in our company should note that they are purchasing equity securities of a BVI holding company rather than equity securities issued by our operating subsidiaries. Under our current corporate structure, as a BVI holding company, Hollysys Automation Technologies Ltd. may rely on dividend payments from Helitong, which is a wholly foreign-owned enterprise incorporated in China, to fund any cash and financing requirements. Under applicable PRC laws and regulations, our PRC subsidiaries are permitted to pay dividends to us only out of their accumulated profits, if any, determined in accordance with PRC accounting standards and regulations. In addition, our PRC subsidiaries are required to allocate at least 10% of their accumulated profits each year, if any, to fund statutory reserves of up to 50% of the registered capital of the enterprise. Allocations from these statutory surplus reserves may only be used for specific purposes and are not distributable to us in the form of loans, advances, or cash dividends. As a result, our Chinese subsidiaries are restricted in their ability to transfer a portion of its net assets to us in the form of dividends, loans or advances. As an offshore holding company, we will be permitted under PRC laws and regulations to provide funding from the proceeds of our offshore fund-raising activities to our subsidiaries in China only through loans or capital contributions, subject to the satisfaction of the applicable government registration and approval requirements. Before providing loans to our PRC subsidiaries, we will be required to make filings about details of the loans with the State Administration of Foreign Exchange of the PRC (the “SAFE”) in accordance with relevant PRC laws and regulations. Our PRC subsidiaries that receive the loans are only allowed to use the loans for the purposes set forth in these laws and regulations. Under regulations of the SAFE, Renminbi is not convertible into foreign currencies for capital account items, such as loans, repatriation of investments and investments outside of China, unless the prior approval of the SAFE is obtained and prior registration with the SAFE is made. Investors in our securities should note that, to the extent cash in the business is in the PRC or a PRC entity, the funds may not be available to fund operations or for other use outside of the PRC due to interventions in or the imposition of restrictions and limitations on the ability of Hollysys or its subsidiaries by the PRC government to transfer cash. For the description of how cash is transferred through our organization, see “Item 5. Operating and Financial Review and Prospects—B. Liquidity and Capital Resources—Holding Company Structure.” For related risks, see “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China.”

Risks Associated with Operations in China

Our activities are primarily conducted in the PRC through our Chinese operating subsidiaries. We do not have any variable interest entity in China. Our Chinese operating subsidiaries are required to, and have obtained, from PRC authorities all permits or approvals required to engage in our business in China, including the business licenses from local authorities for their operations. We believe that currently we are not required to obtain permissions from the China Securities Regulatory Commission (the “CSRC”), the Cyberspace Administration of China (the “CAC”) or other entity in China for our operations in China, while we cannot assure you that we will not be required to obtain the approval of the CSRC, the CAC or of potentially other regulatory authorities to maintain the listing status of our ordinary shares on the NASDAQ or to conduct offerings of securities in the future. In addition, we face risks and uncertainties as to whether and how PRC regulatory developments, such as those relating to data and cyberspace security and anti-monopoly concerns, would apply to us. The PRC government has also recently indicated an intent to exert more oversight and control over securities offerings and other capital markets activities that are conducted overseas and foreign investment in China-based companies. See “Item 4. Information of the Company—B. Business Overview—Recent Regulatory Development.”

5

Table of Contents

Given the uncertainties of interpretation and implementation of relevant laws and regulations and the enforcement practice by relevant government authorities, we may be required to obtain additional licenses, permits, filings, or approvals for the business operations in the future. If we are found to be in violation of any existing or future PRC laws or regulations, or fail to obtain or maintain any of the required permits or approvals, the relevant PRC regulatory authorities would have broad discretion to take action in dealing with such violations or failures. Furthermore, it is highly uncertain how existing or new laws or regulations or detailed implementations and interpretations will be modified or promulgated with respect to the approvals we need for our operations. If we inadvertently conclude that certain approvals are not required, or applicable laws, regulations, or interpretations change, we may be required to obtain approval in the future. We may not be able to obtain required approvals in a timely and cost-effective manner, or at all, which may adversely affect our operations, financial condition and reputation. In addition, the PRC government may intervene in or influence our operations at any time, or may exert more control over our future overseas offerings or foreign investments in us, which could result in a material change in our operations, significantly limit or completely hinder our ability to continue to offer or continue to offer securities to investments, and could cause the value of our securities to significantly decline or become worthless. See “Item 3. Key Information—D. Risk Factors—Risks Related to Doing Business in China” for more details.

6

Table of Contents

| A. |

[Reserved] |

| B. |

Capitalization and Indebtedness |

Not applicable.

| C. |

Reasons for the Offer and Use of Proceeds |

Not applicable.

| D. |

Risk Factors |

Summary of Risk Factors

An investment in our securities involves a high degree of risk. You should carefully consider the risks described below, together with all of the other information included in this annual report, before making an investment decision. If any of the following risks actually occurs, our business, prospects, financial condition or results of operations could suffer. In that case, the trading price of our securities could decline, and you may lose all or part of your investment. Below please find a summary of the principal risks we face, organized under relevant headings. All the legal and operational risks associated with being based in and having operations in China also apply to our operations in Hong Kong and Macau.

Risks Related to Our Business

Risks and uncertainties related to our business include, but are not limited to, the following:

| • |

We commit substantial resources to new product and service development and acquisition opportunities in order to stay competitive and grow our business, and we may fail to offset the increased cost of such investment with a sufficient increase in net sales or margins. |

| • |

Our businesses and financial performance may be affected by changes in the PRC government policies promoting infrastructural development, such as high-speed rail and urban mass transit. Any decrease in public expenditures on, or any change in the public procurement policies or industry standards relating to, such industries may affect our business. |

| • |

Our capital and human resources committed to product and service offerings may not always achieve anticipated results and we may not be able to develop new product and service offerings that meet market demand or successfully introduce new products and services in a timely manner. |

| • |

Loss of major customers or changes in their orders may have an adverse impact on our business. |

| • |

We do not have long-term purchase commitments from our customers, and we are exposed to potential volatility in our turnover. |

| • |

An increase in our contract backlog may reflect our inability to perform our contracts on a timely basis instead of our ability to expand our business. |

| • |

We may face risks associated with our international operations and expansion, which could result in significant additional costs for our business operations. |

| • |

If we fail to accurately estimate the overall risks or costs under the contracts with our customers, or the time needed to complete the relevant projects under such contracts, we may experience cost overruns, schedule delays, lower profitability or even losses under such contracts when we perform such contracts. |

7

Table of Contents

| • |

Our products may contain design or manufacturing defects that could result in product liability claims and cause us to suffer losses, and such defects could adversely affect demand for our products and services. |

| • |

Since we use a variety of raw materials and components in our production, shortages or price fluctuations of raw materials and the inability of key suppliers to meet our quantity or quality requirements could increase the cost of our products, undermine our product quality and adversely impact our business. |

Risks Related to Doing Business in China

While we do not have any variable interest entity in China, we face risks and uncertainties as to whether and how the recent PRC regulatory developments, such as those relating to data and cyberspace security and anti-monopoly concerns, would apply to us. Risks and uncertainties related to doing business in China include, but are not limited to, the following:

| • |

Changes in the economic and political policies of the PRC government could have a material and adverse effect on our business, financial condition and results of operations and may result in our inability to sustain our growth and expansion strategies. For details, see page 24 of this annual report. |

| • |

Uncertainties with respect to the PRC legal system, including uncertainties regarding the enforcement of laws, and sudden or unexpected changes in policies, laws and regulations in China, could adversely affect us. For details, see page 25 of this annual report. |

| • |

The PRC government may intervene in or influence our operations at any time, or may exert more control over our future overseas offerings or foreign investments in us, which could result in a material change in our operations, significantly limit or completely hinder our ability to offer or continue to offer securities to investors, and could cause the value of our securities to significantly decline or become worthless. For details, see page 25 of this annual report. |

| • |

PRC regulations regarding acquisitions impose significant regulatory approval and review requirements, which could make it more difficult for us to pursue growth through acquisitions. For details, see page 26 of this annual report. |

| • |

The permission and approval from the CSRC or other PRC government authorities may be required in connection with an offshore offering under PRC law, and, if required, we cannot predict whether or for how long we will be able to obtain such permission or approval. For details, see page 27 of this annual report. |

| • |

Trading in our securities will be prohibited under the HFCAA if the PCAOB determines that it is unable to inspect or investigate completely registered public accounting firms headquartered in mainland China and Hong Kong, including our auditor as an independent registered public accounting firm, and as a result, U.S. national securities exchanges, such as the NASDAQ, may determine to delist our securities. For details, see page 27 of this annual report. |

Risks Related to Our Shares

Risks and uncertainties related to our shares include, but are not limited to, the following:

| • |

The market price of our ordinary shares is volatile, leading to the possibility of its value being depressed at a time when you want to sell your holdings. |

| • |

Share prices of companies with business operations primarily in China have fluctuated widely in recent years, and the trading prices of our ordinary shares are likely to be volatile, which could result in substantial losses to investors. |

8

Table of Contents

Risks Related to Our Business

We commit substantial resources to new product and service development and acquisition opportunities in order to stay competitive and grow our business, and we may fail to offset the increased cost of such investment with a sufficient increase in net sales or margins.

The success of our business depends in great measure on our ability to keep pace with, or even lead, changes that occur in our industry and expand our product and service offerings. Traditionally, the automation and control systems business was relatively stable and slow moving. Successive generations of products offered only marginal improvements in terms of functionality and reliability. However, the emergence of computers, computer networks and electronic components as key elements of the systems that we design and build has accelerated the pace of change in our industry. Where there was formerly as much as a decade or more between successive generations of automation systems, the time between generations is now as little as two to three years. Technological advances and the introduction of new products, new designs and new manufacturing techniques by our competitors could adversely affect our business unless we are able to respond with similar advances. To remain competitive, we must continue to incur significant costs in product development, equipment and facilities and to make capital investments and seek complementary acquisitions. These costs may increase, resulting in greater fixed costs and operating expenses than we have incurred to date. As a result, we could be required to expend substantial funds for and commit significant resources to the following:

| • |

research and development activities on existing and potential products and services; |

| • |

additional engineering and other technical personnel; |

| • |

advanced design, production and test equipment; |

| • |

manufacturing services that meet changing customer needs; |

| • |

technological changes in manufacturing processes; |

| • |

expansion of manufacturing capacity; and |

| • |

acquiring technology through licensing and acquisitions. |

Our future operating results will depend to a significant extent on our ability to continue providing new product and service solutions that compare favorably on the basis of time to market, cost and performance, with competing third-party suppliers and technologies. However, we may develop new products and services that do not gain market acceptance, which would result in the failure to recover the significant costs for design and manufacturing of new products and services, thus adversely affecting operating results.

Our businesses and financial performance may be affected by changes in the PRC government policies promoting infrastructural development, such as high-speed rail and urban mass transit. Any decrease in the public expenditures on, or any change in the public procurement policies or industry standards relating to, such industries may affect our business.

Our business includes providing high-speed rail signaling systems that ensure operational safety of passenger trains. The development of the PRC high-speed rail signaling system industry is dependent upon state planning and investment in high-speed rail transportation projects. The nature, scale and timetable of these projects may be affected by a number of factors, including the overall state investment in high-speed rail transportation projects and approval of such new projects. By the end of 2022, the total length of China’s high-speed railway was over 42,000 kilometers. We cannot predict whether the total annual investment in and the market size of the PRC high-speed railway industry will continue to grow in the future. If the total annual investment or the market size declines, our business and financial position may be adversely affected.

9

Table of Contents

We have also provided our supervisory control and data acquisition (“SCADA”) system to a number of China’s subway lines over the past years. Although the PRC government has historically been supportive of the development of the urban mass transit industry, its industrial policy may change from time to time and it may adopt new policies or measures to further regulate the urban mass transit industry due to changes in macroeconomic trends or certain unexpected events.

The spending patterns and priorities of Chinese policymakers cannot be predicted with certainty. We cannot assure you that the generally favorable policies will remain in force in the future. If the PRC government reduces its public investment in, or changes any industrial standards relating to the high-speed railway industry, railway or urban mass transit industry in the PRC, if any of our major customers changes its procurement or bidding policy, or if our rail transportation projects face challenges, there could have a material adverse effect on our business, financial position and results of operations.

Our capital and human resources committed to product and service offerings may not always achieve anticipated results and we may not be able to develop new product and service offerings that meet market demand or successfully introduce new products and services in a timely manner.

We are a technology-driven company. To maintain our leading position in the industry and meet the requirement of safety and efficiency, we have to continuously improve existing technology, product and service offerings, and design and develop new technology, product and service offerings that closely follow technology development trends and customer needs. However, we cannot guarantee that our capital and human resources activities will always keep pace with market demand and technological advances or yield the anticipated results. The products and services, which we have spent substantial capital and human resources to develop, may not be able to deliver expected commercial returns when they are developed due to changing technology trends and market demands. If we encounter delays in technology development, fail to meet changing market demands, underestimate or fail to follow technological trends, or if our competitors respond more quickly than we do, our business or operating results may be materially and adversely affected. Failure to develop and introduce new product and service solutions in the areas of industrial automation, rail transportation and mechanical and electrical solutions on a timely basis or at all could adversely affect our competitiveness and profitability.

Loss of major customers or changes in their orders may have an adverse impact on our business.

We have developed significant customer relationships with several local urban mass transit providers and railway authorities in respect of the high-speed train system in China and other geographies. We expect to continue to rely on our current major customers for a portion of our revenue in the future. Moreover, due to the nature of our business, the contract value of a single contract tends to be large. As such, our cash flows may become dependent on those customers’ payment practices and overall public funding policies, including the lengthening of collection times under contracts that have been performed. If our major customers significantly reduce, modify, postpone or cancel their purchase orders with us, we may not be able to get substitute orders with similar terms from other customers in a timely manner or at all. If we are not able to enter into contracts with our major customers on terms favorable to us or at all, our business and financial position may be adversely affected.

We do not have long-term purchase commitments from our customers, and we are exposed to potential volatility in our turnover.

Our business with our customers has been, and we expect it will continue to be, conducted on the basis of actual purchase orders received from time to time. Our customers are not obligated in any way to continue to place orders with us at the same or increased levels or at all. In addition, our customers may change or delay or terminate orders for products and services without notice for reasons unrelated to us, including lack of market acceptance for the products that our system was designed to control.

10

Table of Contents

We cannot assure you that our customers will continue to place purchase orders with us at the same volume or same margin, as compared to prior periods, or at all. We may not be able to locate alternative customers to replace purchase orders or sales. As a result, our business, financial condition and results of operations may vary from period to period and may fluctuate significantly in the future.

An increase in our contract backlog may reflect our inability to perform our contracts on a timely basis instead of our ability to expand our business.

Our backlog indicates our ability to sell our products and services and increase our revenue, which represents the amount of unrealized revenue to be earned from the contracts that we have won. Backlog is not a standard financial measure that has been defined by generally accepted accounting principles, and may not be indicative of future operating results. The amount of our aggregate backlog is based on the assumption that our relevant contracts will be performed in full in accordance with their terms. The termination or modification of any one or more major contracts may have a substantial and immediate effect on our backlog. We cannot guarantee that the amount estimated in our backlog will be realized in full, in a timely manner, or at all, or that, even if it is realized, such backlog will result in profits as expected. As a result, you should not rely on our backlog information presented in this annual report as an indicator of our future earnings.

We may face risks associated with our international operations and expansion, which could result in significant additional costs for our business operations.

A core component of our growth strategy is international expansion. As we continue to expand our international operations, we will be increasingly susceptible to the risks associated with overseas expansion. We have a limited operating history outside of the PRC and management of our international operations requires significant resources and management attention. Entering into new markets presents challenges, including, among others, the challenges of supporting a rapidly growing business in new environments with diverse cultures, languages, customs, legal systems, alternative dispute systems and economic, political and regulatory systems. We expect to incur significant costs associated with expanding our overseas operations, including hiring personnel internationally. The risks and challenges associated with overseas expansion include:

| • |

uncertain political and economic climates; |

| • |

lack of familiarity and burdens of complying with foreign laws, accounting and legal standards, regulatory requirements, tariffs and other barriers; |

| • |

unexpected changes in regulatory requirements, taxes, trade laws, tariffs, export quotas, custom duties or other trade restrictions; |

| • |

lack of experience in connection with the localization of our applications, including translation into foreign languages and adaptation for local practices, and associated expenses and regulatory requirements; |

| • |

difficulties in adapting to differing technology standards; |

| • |

longer sales cycles and accounts receivable payment cycles and difficulties in collecting accounts receivable; |

| • |

difficulties in managing, growing, and staffing international operations, including varying legal and cultural expectations for employee relationships, increased travel, infrastructure and legal compliance costs associated with international operations; |

| • |

challenges to our corporate culture resulting from a dispersed workforce and intricacies of foreign employees joining labor unions, employee representative bodies, or engaging in collective bargaining agreements, and challenges related to work stoppages or slowdowns; |

| • |

fluctuations in exchange rates that may increase the volatility of our foreign-based revenue and expenses; |

| • |

potentially adverse tax consequences, including the complexities of foreign value-added tax, goods and services tax and other transactional taxes; |

| • |

reduced or varied protection for intellectual property rights in some countries; |

| • |

difficulties in managing and adapting to differing cultures and customs; |

| • |

difficulties in implementing and maintaining the financial systems and processes needed to enable compliance across multiple product and service offerings and jurisdictions; |

11

Table of Contents

| • |

data privacy laws which require that customer data be stored and processed in a designated territory subject to laws different from those of the PRC; |

| • |

new and different sources of competition as well as laws and business practices favoring local competitors and local employees; |

| • |

compliance with anti-bribery laws, including compliance with the Foreign Corrupt Practices Act (the “FCPA”); |

| • |

increased financial accounting and reporting burdens and complexities; and |

| • |

restrictions on the transfer of funds across borders or repatriation of earnings. |

In addition, in our international business expansion to Southeast Asia, South Asia and the Middle East, we may not be able to find adequate and qualified local engineers to bid and complete sizable rail transportation orders and industrial automation projects, and because of visa requirements, we may have difficulties relocating adequate engineers from China to various foreign countries and have them stay there long enough to finish the projects, which could have an adverse impact on our international business expansion. With operations in Singapore, Malaysia, Indonesia, India and the Middle East, we are subject to numerous, and sometimes conflicting, legal requirements on matters as diverse as import/export controls, trade restrictions, tariffs, taxation, sanctions, government affairs, anti-corruption, whistle blowing, internal and disclosure control obligations, data protection and privacy and labor relations and regulatory requirements that are specific to our clients’ industries. Non-compliance with these regulations in the conduct of our business could result in fines, penalties, criminal sanctions against us or our officers, disgorgement of profits, prohibitions on doing business and adverse impact on our reputation. Gaps in compliance with these regulations in connection with the performance of our obligations to our clients could also result in exposure to monetary damages, fines and/or criminal prosecution, unfavorable publicity, restrictions on our ability to process information and allegations by our clients that we have not performed our contractual obligations. Many countries also seek to regulate the actions that companies take outside of their respective jurisdictions, subjecting us to multiple and sometimes competing legal frameworks in addition to our home country rules. Due to the varying degree of development of the legal systems of the countries in which we operate and plan to operate, local laws might be insufficient to defend us and preserve our rights. We could also be subjected to risks to our reputation and regulatory action on account of any unethical acts by any of our employees, partners or other related individuals. As a result of these factors, international expansion may be more difficult, take longer and not generate the results we anticipate, which could negatively impact our growth and business.

If we fail to accurately estimate the overall risks or costs under the contracts with our customers, or the time needed to complete the relevant projects under such contracts, we may experience cost overruns, schedule delays, lower profitability or even losses under such contracts when we perform such contracts.

We derive the majority of our total consolidated revenues from the integrated solutions contracts that we have won through a competitive bidding process. The purpose of an integrated solutions contract is to furnish an automation system that provides the customer with a total solution for the automation or process control requirement being addressed. These contracts require us to complete projects at a fixed price, and therefore expose us to the risk of cost overruns. Cost overruns, whether due to efficiency, estimates or other reasons, could result in lower profit or losses. Other variations and risks inherent in the performance of fixed-price contracts such as delays caused by technical issues, and any inability to obtain the requisite permits and approvals, may cause our actual risk exposure and costs to differ from our original estimates.

In addition, we may be unable to deliver products or complete projects in accordance with the schedules set forth under the integrated solutions contracts. Our projects and our manufacturing and sales of products could be delayed for a number of reasons, including those relating to market conditions, policies, laws and regulations of the PRC and other relevant jurisdictions, availability of funding, transportation, disputes with business partners and subcontractors, technology and raw materials suppliers, employees, local governments, natural disasters, epidemics (such as Covid-19), power and other energy supplies, and availability of technical or human resources.

12

Table of Contents

We cannot guarantee that we will not encounter cost overruns or delays in our current and future delivery of products and the completion of projects. If such cost overruns or delays were to occur, our costs could exceed our budget, and our profits on the relevant contracts may be adversely affected.

Our products may contain design or manufacturing defects that could result in product liability claims and cause us to suffer losses, and such defects could adversely affect demand for our products and services.

Our products are very complex, integrated systems, often with elements designed specifically for the particular situation of a customer. These products may have dormant design or manufacturing issues or defects that are not detected until they are put into actual use. Also, we manufacture spare parts for maintenance and replacement purposes after the completion of integrated solutions contracts. While there have been no significant issues or defects identified as of the date of this annual report, any issues or defects in the design, manufacture and spare parts we provide may result in returns, claims, delayed shipments to customers or reduced or cancelled customer orders and other forms of damages asserted against us. A product issue or defect or negative publicity concerning defective products or services of ours could adversely affect our results of operations, reputation, customer satisfaction and market share.

Moreover, we are active in the conventional and nuclear power generation and railway control systems sectors. Each of these sectors poses a substantially higher risk of liability in the event of a system failure than is present in the industrial process controls markets in which we have traditionally competed. In certain jurisdictions that impose strict liability on product defects, we could be held liable for injuries or accidents involving our products even if the defects are not caused by us. We may be held liable for any damages or losses incurred in connection with or arising from defective products manufactured or designed by us, and if the damages or losses are severe, we may also be subject to administrative penalties imposed by the government. If our products or services are proven to be defective and have caused personal injury, property damage or other losses to rail passengers, we may be held responsible under liability claims under the laws of the PRC or other jurisdictions in which our products or services are sold, used or provided. We may need to devote substantial funds and other financial and administrative resources to rectifying or preventing potential product liability incidents, which could adversely affect our working capital, cash flow and results of operation.

In line with the industry practice, we generally do not carry large amounts of product liability insurance for our products, and we may not be able to obtain adequate insurance coverage in the future or may experience difficulties in obtaining the insurance coverage we need, which could negatively affect our business, financial condition and results of operations. The typical industrial practice is for the customers to obtain insurance to protect against their own operational risks. Any claims against us, regardless of their merits, could materially and adversely affect our financial condition. If we recall any of our products or are punished by governmental authorities, our business activities, financial condition and results of operations, as well as reputation, could be adversely affected.

Since we use a variety of raw materials and components in our production, shortages or price fluctuations of raw materials and the inability of key suppliers to meet our quantity or quality requirements could increase the cost of our products, undermine our product quality and adversely impact our business.

Our major requirements for raw materials include bare printed circuit boards, electronic components, chips, cabinets and cables. Although we believe the sources of supply for these raw materials and components are generally adequate, any shortages or price increases could lead to higher costs of sales in the future. Our inability to pass on all or any raw material price increases to our customers or suppliers or offset the price fluctuations through commodity hedges could adversely affect our business, financial condition and results of operations.

Moreover, we procure our major raw materials, bare printed circuit boards, from suppliers based on our requirements and design considerations. Our suppliers may not be able to scale production or adjust the delivery of products during times of volatile demand. In addition, we cannot guarantee that our suppliers have developed adequate and effective quality control systems. Our vendors’ inability to meet our volume requirements or quality standards may materially and adversely affect our brand and reputation, as well as our business, financial condition and results of operations.

13

Table of Contents

We may experience material disruptions to our productions and business operations.

We primarily manufacture the hardware of our products in Beijing and Hangzhou facilities and on certain occasions outsource the production to third-party manufacturers. These facilities may be affected by natural or man-made disasters and other external events, including but not limited to fire, natural disasters, diseases and epidemics (such as Covid-19), weather, manufacturing problems, strikes, transportation interruption, government regulation, supply chain disruption or terrorism. Any such disruptions or facility downtime could prevent us from meeting customer demand for our product and require us to make unexpected capital expenditures. In such circumstances, we may not be able to find alternatives on terms acceptable to us, or at all. Any of these disruptions may force us to cease operations, shift production to other third-party manufacturers or cease certain parts of our business operations, which could incur substantial costs or take a significant time to re-start production or operations, each of which may adversely impact our business and results of operations.

Security breaches or disruptions of our information technology systems could adversely affect our business.

We rely on information technology networks and systems, including the Internet, to process, transmit and store electronic information, and to manage or support a variety of business processes and activities. Additionally, we collect and store certain data, including proprietary business information, and may have access to confidential or personal information in certain of our businesses, which is subject to privacy and security laws and regulations, and customer-imposed controls. These information technology networks and systems may be susceptible to damage, disruptions or shutdowns due to failures during the process of upgrading or replacing software, databases or components; power outages; telecommunications or system failures; terrorist attacks; natural disasters; employee error or malfeasance; server or cloud provider breaches; and computer viruses or cyberattacks. Cybersecurity threats and incidents can range from uncoordinated individual attempts to gain unauthorized access to information technology networks and systems to more sophisticated and targeted measures, known as advanced persistent threats, directed at us, our products, customers and/or third-party service providers. Despite the implementation of cybersecurity measures (including access controls, data encryption, vulnerability assessments, continuous monitoring, and maintenance of backup and protective systems), our information technology networks and systems may still be vulnerable to cybersecurity threats and other electronic security breaches. It is possible for such vulnerabilities to remain undetected for an extended period, up to and including several years. In addition, it is possible a security breach could result in theft of trade secrets or other intellectual property or disclosure of confidential customer, supplier or employee information. We cannot guarantee that we will be able to prevent security breaches or other damage to our information technology systems, nor can we guarantee that our internal control and compliance programs will be able to adequately address all or any of such breaches. Disruptions caused by any such breaches or damage could have an adverse effect on our operations, as well as expose us to litigation, liability or penalties under privacy laws, increased cybersecurity protection costs, reputational damage and product failure.

Our failure to comply with cybersecurity and data protection laws and regulations could lead to government enforcement actions and significant penalties against us, and adversely impact our operating results.

The regulatory framework for the collection, use, safeguarding, sharing, transfer and other processing of personal information and important data worldwide is rapidly evolving and is likely to remain uncertain for the foreseeable future. For example, regulatory authorities in China have implemented and are considering a number of legislative and regulatory proposals concerning cybersecurity and data protection.

The PRC Cyber Security Law, which took effect in June 2017, created China’s first national-level data protection regime for “network operators,” which may include all organizations in China that provide services over the internet or another information network. Specifically, the Cyber Security Law provides that China adopts a multi-level protection scheme, under which network operators are required to perform obligations of security protection to ensure that the network is free from interference, disruption or unauthorized access, and to prevent network data from being disclosed, stolen or tampered.

14

Table of Contents

In addition, the PRC Data Security Law was promulgated by the Standing Committee of the National People’s Congress on June 10, 2021 and took effect on September 1, 2021. The Data Security Law establishes a tiered system for data protection in terms of their importance, data categorized as “important data,” which will be determined by governmental authorities in the form of catalogs, are required to be treated with a higher level of protection. Specifically, the Data Security Law provides that operators processing “important data” are required to appoint a “data security officer” and a “management department” to take charge of data security. In addition, such an operator is required to evaluate the risk of its data activities periodically and file assessment reports with relevant regulatory authorities.

Numerous regulations, guidelines and other measures have been or are expected to be adopted under the umbrella of, or in addition to, the Cyber Security Law and Data Security Law. For example, Regulations on the Security Protection of Critical Information Infrastructure (the “CII Protection Regulations”) was promulgated by the State Council of the PRC on July 30, 2021 and became effective on September 1, 2021. According to the CII Protection Regulations, critical information infrastructure (the “CII”) refers to any important network facilities or information systems of the important industry or field such as public communication and information service, energy, transportation, water conservancy, finance, public services, e-government affairs and national defense science, which may endanger national security, people’s livelihood and public interest in the case of damage, function loss or data leakage. Regulators supervising specific industries are required to formulate detailed guidance to recognize the CII in the respective sectors, and a critical information infrastructure operator, or a CIIO, must take the responsibility to protect the CII’s security by performing certain prescribed obligations. For example, CIIOs are required to conduct network security test and risk assessment, report the assessment results to relevant regulatory authorities, and timely rectify the issues identified at least once a year.

Additionally, in November 2021, the CAC issued the Cyber Data Security Administration Regulations (Draft for Comments), which, among other things, stipulates that a data processor that processes “important data” or listed overseas must conduct an annual data security review by itself or by engaging a data security service provider and submit the annual data security review report for a given year to the relevant municipal counterpart of the CAC before January 31 of the following year. As of the date of this annual report, such administration regulations have not been adopted. In January 2022, the CAC and several other administrations jointly promulgated the amended Cybersecurity Review Measures (the “Cybersecurity Review Measures”), which became effective on February 15, 2022, and superseded and replaced the current cybersecurity review measures that became effective in June 2020. Pursuant to the Cybersecurity Review Measures, a CIIO that purchases network products and services, or conducts data process activities, which affect or may affect national security will be subject to the cybersecurity review. The Cybersecurity Review Measures also expands the cybersecurity review to “internet platform operators” in possession of personal information of over one million users if such operators intend to list their securities in a foreign country. See “—Risks Related to Doing Business in China—The permission and approval from the CSRC or other PRC government authorities may be required in connection with an offshore offering under PRC law, and, if required, we cannot predict whether or for how long we will be able to obtain such permission or approval.” Alternatively, relevant governmental authorities in the PRC may initiate a cybersecurity review if they determine an operator’s network products or services or data processing activities affect or may affect national security.

Furthermore, the Opinions on Strictly Cracking Down on Illegal Securities Activities requires (i) speeding up the revision of the provisions on strengthening the confidentiality and archives management relating to overseas issuance and listing of securities and (ii) improving the laws and regulations relating to data security, cross-border data flow, and management of confidential information. The Personal Information Protection Law, which was promulgated by the Standing Committee of the National People’s Congress on August 20, 2021 and took effect on November 1, 2021, integrates the various rules with respect to personal information rights and privacy protection and applies to the processing of personal information within mainland China as well as certain personal information processing activities outside mainland China, including those for the provision of products and services to natural persons within China or for the analysis and assessment of acts of natural persons within China. We may have access to confidential or personal information in certain of our businesses. Although we endeavor to comply with our privacy policies and other documentation regarding the protection of personal information, we may at times fail to do so or may be perceived to have failed to do so. Moreover, despite our efforts, we may not be successful in achieving compliance if our employees or contractors fail to comply with these policies and documentation.

15

Table of Contents

Since the Cyber Security Law, Data Security Law and relevant regulations are relatively new, uncertainties still exist in relation to their interpretation and implementation. Any change in laws and regulations relating to privacy, data protection and information security and any enhanced and scrutinized governmental enforcement action of such laws and regulations could greatly increase our cost in providing our products and services, limit their use or adoption or require certain changes to be made to our operations. We cannot assure you that we will be compliant with the laws and regulations described above in all respects, and we may be ordered to rectify and terminate any actions that are deemed illegal by the government authorities and become subject to fines and other government sanctions, which may materially and adversely affect our business, financial condition, and results of operations.

Specifically, given the uncertainties surrounding the interpretation and implementation of the Cyber Security Law, Data Security Law and relevant regulations, we cannot rule out the possibility that we, or certain of our customers or suppliers may be deemed as a CIIO, or an operator processing “important data.” First, if we are deemed as a CIIO, our purchase of network products or services, if deemed to be affecting or may affect national security, will need to be subject to cybersecurity review, before we can enter into agreements with relevant customers or suppliers, and before the conclusion of such procedure, these customers will not be allowed to use our products or services, and we are not allowed to purchase products or services from our suppliers. There can be no assurance that we would be able to complete the applicable cybersecurity review procedures in a timely manner, or at all, if we are required to follow such procedures. Any failure or delay in the completion of the cybersecurity review procedures may prevent us from using certain network products and services, and may result in fines of up to ten times the purchase price of such network products and services being imposed upon us, if we are deemed a CIIO using network products or services without having completed the required cybersecurity review procedures. If the reviewing authority is of the view that the use of such network products or services by us, or by certain of our customers or suppliers, involves risk of disruption, is vulnerable to external attacks, or may negatively affect, compromise, or weaken the protection of national security, we may not be able to provide such products or services to relevant customers, or purchase products or services from relevant suppliers. This could have a material adverse effect on our results of operations and business prospects. Second, the notion of “important data” is not clearly defined by the Cyber Security Law or the Data Security Law. In order to comply with the statutory requirements, we will need to determine whether we possess important data, monitor the important data catalogs that are expected to be published by local governments and departments, perform risk assessments and ensure we are complying with reporting obligations to applicable regulators. We may also be required to disclose to regulators business-sensitive or network security-sensitive details regarding our processing of important data, and may need to pass the government security review or obtain government approval in order to share important data with offshore recipients, which can include foreign licensors, or share data stored in China with judicial and law enforcement authorities outside of China. If judicial and law enforcement authorities outside China require us to provide data stored in China, and we are not able to pass any required government security review or obtain any required government approval to do so, we may not be able to meet the foreign authorities’ requirements. The potential conflicts in legal obligations could have an adverse impact on our operations in and outside of China.

Our goodwill is subject to impairment review and any goodwill impairment may negatively affect our reported results.

Goodwill represents the excess of the purchase price over the estimated fair value of net tangible and identifiable intangible assets acquired. Our outstanding goodwill as of June 30, 2023 was related to the acquisition of Hollysys Industrial Software in July 2017, Shandong Lukang in August 2019 and Hollysys Intelligent in August 2021. Based on our quantitative assessment for Hollysys Intelligent and qualitative assessment for Hollysys Industrial Software and Shandong Lukang, the goodwill was not impaired as of June 30, 2023.

However, there are uncertainties surrounding the amount and timing of future expected cash flows for Hollysys Industrial Software, Shandong Lukang and Hollysys Intelligent. In the future, if actual future cash flows being less than forecasted or delays in the timing of when those cash flows are expected to be realized, goodwill impairment might be triggered. Further, the timing of when actual future cash flows are received could differ from our estimates, which are based on historical trends and do not factor in unexpected delays in project commencement or execution.

In addition, we might make acquisitions and execute other forms of business combination, which would record goodwill, from to time in the future.

16

Table of Contents

We may experience delays or defaults in payment of accounts receivables or in release of retention by our customers, which may adversely affect our cash flow and working capital, financial condition and results of operations.

In line with the industry practice, we typically have a long receivable collection cycle. We have in the past faced, and may face in the future, the risk that customers may delay their settlement with us or delay or fail to pay us as scheduled such as due to financial distress of our customers. Furthermore, defaults in payments to us on projects for which we have already incurred significant costs and expenses can materially and adversely affect our results of operations and reduce our financial resources that would otherwise be available to fund other projects. We cannot assure you that payments from customers will be made in a timely manner or at all, or that delays or defaults in payments will not adversely affect our financial condition and results of operations.

Our operations require certain permits, licenses, approvals and certificates, the revocation, cancellation or non-renewal of which could significantly hinder our business and operations, and we are subject to periodic inspections, examinations, inquiries and audits by regulatory authorities.

We are required to obtain and maintain valid permits, licenses, certificates and approvals from various governmental authorities or institutions under relevant laws and regulations for our businesses of design and integration, equipment manufacturing and system implementation services. We must comply with the restrictions and conditions imposed by various levels of governmental agencies to maintain our permits, licenses, approvals and certificates. If we fail to comply with any of the regulations or meet any of the conditions required for the maintenance of our permits, licenses, approvals and certificates, our permits, licenses, approvals and certificates could be temporarily suspended or even revoked, or the renewal thereof, upon expiry of their original terms, may be delayed or rejected, which could materially and adversely impact our business, financial condition and results of operations.

We are subject to periodic inspections, examinations, inquiries and audits by regulatory authorities and may be subject to suspension or revocation of the relevant permits, licenses, approvals or certificates, or fines or other penalties due to any non-compliance identified as a result of such inspections, examinations, inquiries and audits. We cannot assure you that we will be able to maintain or renew our existing permits, licenses, approvals and certificates or obtain future permits, licenses, approvals and certificates required for our continued operation on a timely basis or at all. In the event that we fail to comply with applicable laws and regulations or fail to maintain, renew or obtain the necessary permits, licenses, approvals or certificates, our qualification to conduct various businesses may be adversely impacted.

As we expand our business outside of mainland China, we will encounter the increasing need for international certifications and compliance with the regulation of different governments, which if not obtained and complied with may adversely impact our business.

We are expanding our business outside of mainland China, including seeking business opportunities in Hong Kong, Singapore, Malaysia, India, Indonesia, and the Middle East. For our marketing both in mainland China and in other jurisdictions, we seek international certifications and have obtained certificates such as the European Safety Standard Certification Level 4 and the Safety Integrity Level 3 (SIL 3) Certification. As we operate in jurisdictions outside of mainland China, we will have to comply with local laws, some of which relate to various safety and quality requirements for the kinds of products we provide. The failure to have any necessary or beneficial certifications and the failure to comply with local laws will have an adverse impact on our marketing and business, and may result in additional costs and expenses.

We are exposed to risks associated with public project contracts.

Due to the nature of our industry, we are exposed to risks associated with public project contracts. For example, many of our contracts are for large and high-profile high-speed railway or urban mass transit infrastructure projects, which can result in increased political and public scrutiny of our work. Certain of our customers are affiliated with government authorities. Such customers may delay making payments for our projects, and it may take a considerably longer period of time to resolve disputes with these customers than resolving disputes with customers in private sectors.

Moreover, such government-affiliated customers may require us to undertake additional obligations, change the type of our services, equipment used or other terms of service, or purchase specific equipment, or modify other contractual terms from time to time for the social benefit or other administrative purposes, resulting in additional costs incurred by us, which may not be reimbursed by such customers in full. If any early termination by any government-affiliated customers occurs or if any government-affiliated customers fail to renew their contracts with us in the future, our backlog may be reduced and our investment plan may be hindered, which may have a material adverse effect on our business and financial performance.

17

Table of Contents

Many of our competitors have substantially greater resources than we do, allowing them to compete on an advantageous basis, and any increased competition from foreign and PRC domestic competitors within the industries where we operate could negatively impact our market share in the industry.

We operate in a very competitive environment. Our principal offering is a comprehensive suite of automation systems for a wide spectrum of industrial market clientele, ranging from power, chemical, petrochemical, to nuclear, metallurgy, building materials, food-beverage, pharmaceutical and other industries. Many of our competitors are better established and more experienced than we are, have longer operating history than we do, have substantially greater financial resources, operate in more international markets, and are substantially more diversified than we are. As a result, they are in a stronger position to compete effectively with us.

Multi-national companies including Honeywell (US), ABB (Sweden), Siemens (Germany), Emerson (US), Yokogawa (Japan) and Hitachi (Japan) account for the majority of the global automation market share. In domestic market, except the multi-national companies, our main local competitor is Supon. These large competitors are also in a better position than we are to weather any extended weaknesses in the market for automation and control systems.

Additionally, if major competitors increase their investments in China or our targeted overseas markets or collaborate with our existing competitors, we may face even more intense competition. We may not be able to compete successfully with existing industry leaders in new business areas into which we intend to expand. This may in turn affect our business, operating results and financial condition. Other emerging companies or companies in related industries may also increase their participation in relevant markets, which would add to the competitive pressure that we face.

Our business operations are largely dependent on our senior management and our ability to attract and retain engineering talents.

The stability of our business operations and the continuing growth of our business depend on the continuing services of our senior management and engineering talents. In the industries in which we operate, industry experience, management expertise and strategic direction are crucial. If we lose the services of our senior management and engineering staff, we may not be able to recruit a suitable or qualified replacement and may incur further costs and expenses to recruit and/or train new employees. In particular, any sudden loss of a member of our senior management or engineering staff may disrupt our strategic direction and leadership. As we continue to expand our business, we will need to continue to attract and retain experienced management personnel with extensive experience in the industries in which we operate.

We believe that competition for experienced personnel in the areas of industrial automation, rail transportation and mechanical and electrical solutions is intense. Competition for such qualified personnel could lead to higher emoluments and other compensations in order to attract and retain such personnel and an increase in our operating costs. If we are not able to retain the members of our senior management or engineering staff required to achieve our business objectives, this may materially and adversely affect our business operations and prospects.

Our control systems are used in infrastructure projects such as subway systems, railways and nuclear plants; to the extent that our systems do not perform as designed, we could be found responsible for the damage resulting from that failure.

We face potential responsibility for the failure of our control systems in performing the various functions for which they are designed and the damages resulting from any such problem. To the extent that we contract to provide control systems in larger scale projects, the level of damages for which we may be held responsible is likely to increase. To the extent that any of our installed control systems do not perform as designed for their intended purposes, and we are held responsible for the consequences of those performance failures and resulting damages, there may be an adverse impact on our business, reputation, revenues and profits. We believe that our control systems have so far performed as designed, and there are no claims asserted against us based on any significant, non-performance event. Notwithstanding our record, no assurance can be given that no claims will be sought in the future based on the design and performance of our control systems.

18

Table of Contents

Industry and economic conditions may adversely affect the markets and operating conditions of our customers, which in turn can affect demand for our products and services and our results of operations.

We operate in a cyclical industry that is sensitive to general economic conditions in the PRC and abroad. Rapid growth in the PRC economy and urban population could lead to an increased demand for high-speed railway, urban transportation and power plants, which could in turn foster demand for control system products and services in high-speed rail transportation, urban mass transit and power sectors. Changes in market supply and demand could also have a substantial effect on our product prices, business, revenue and financial condition. Macroeconomic conditions (such as the government’s announcement of economic stimulus policies to encourage the construction of public infrastructure or the termination of such policies), supply and demand imbalances and other factors beyond our control, including import and export policies, value-added tax and export taxes could have a major impact on our market share, and the demand for and prices of our products. Increased demand for rail transportation and increased operating margins may result in a larger amount of new investments in the relevant industries and increased production in the overall industry, which may cause supply to exceed the demand and lead to a period of lower prices. This cycle of rising and falling demand may repeat itself. Any of these cyclical factors may adversely impact our business, financial condition, results of operations and prospects.

We are striving to expand our sales into the international markets. Our overseas business extends to Southeast Asia and the Middle East. Any economic downturn may result in reduced funding for public infrastructures including railway or urban mass transit infrastructures and a decreased demand for our transportation control system products and services in the international market. Moreover, any economic downturn may negatively impact the ability of our international customers to obtain financing, which may lead to their unwillingness to purchase our products. Therefore, the general demand for our products and their selling price could decline. Any adverse changes in the global market and economic conditions and any slowdown or recession of the global economy could have a material adverse effect on our business, financial condition, results of operations and prospects. See “—Our business, financial condition, and results of operations may be materially and adversely affected by any economic slowdown in China as well as globally, or tensions in international trade and rising political tensions, particularly between the U.S. and China.”

We may not be able to sufficiently protect our intellectual property.

Our business primarily relies on a combination of copyright, patent, trademark and other intellectual property laws, nondisclosure agreements and other protective measures to protect our proprietary rights. As of June 30, 2023, we held 458 software copyrights, 502 authorized patents, 343 patent applications and 63 registered trademarks.

Our competitors may independently develop proprietary technology similar to ours, introduce counterfeits of our products, misappropriate our proprietary information or processes, infringe on our patents, brand name and trademarks, or produce similar products that do not infringe on our patents or successfully challenge our patents. Our efforts to defend our patents, trademarks and other intellectual property rights against competitors or other violating entities may be unsuccessful. We may be unable to identify any unauthorized use of our patents, trademarks and other intellectual property rights and may not be afforded adequate remedies for any breach. In particular, in the event that our registered patents and our applications do not adequately describe, enable or otherwise provide coverage of our technologies, samples and products, we would not be able to exclude others from developing or commercializing these technologies, samples and products.

19

Table of Contents