UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-Q

(Mark One)

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the quarterly period ended September 30, 2023

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission File Number: 001-35518

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||||||||

| (Address of principal executive offices) | (Zip Code) | ||||||||||

(301 ) 838-2500

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

☒ Yes No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | |||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes ☒ No

Securities registered pursuant to Section 12(b) of the Exchange Act:

| Title of each class | Outstanding at November 1, 2023 | Trading Symbol | Name of each exchange on which registered | |||||||||||||||||

1

SUPERNUS PHARMACEUTICALS, INC.

FORM 10-Q — QUARTERLY REPORT

FOR THE QUARTERLY PERIOD ENDED September 30, 2023

| Page No. | |||||

2

PART I — FINANCIAL INFORMATION

Supernus Pharmaceuticals, Inc.

Condensed Consolidated Balance Sheets

(in thousands, except share data)

| September 30, | December 31, | ||||||||||

| 2023 | 2022 | ||||||||||

| (unaudited) | |||||||||||

| Assets | |||||||||||

| Current assets | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Marketable securities | |||||||||||

| Accounts receivable, net | |||||||||||

| Inventories, net | |||||||||||

| Prepaid expenses and other current assets | |||||||||||

| Total current assets | |||||||||||

| Long-term marketable securities | |||||||||||

| Property and equipment, net | |||||||||||

| Intangible assets, net | |||||||||||

| Goodwill | |||||||||||

| Other assets | |||||||||||

| Total assets | $ | $ | |||||||||

| Liabilities and stockholders’ equity | |||||||||||

| Current liabilities | |||||||||||

| Accounts payable and accrued liabilities | $ | $ | |||||||||

| Accrued product returns and rebates | |||||||||||

| Convertible notes, net | |||||||||||

| Contingent consideration, current portion | |||||||||||

| Other current liabilities | |||||||||||

| Total current liabilities | |||||||||||

| Contingent consideration, long-term | |||||||||||

| Operating lease liabilities, long-term | |||||||||||

| Deferred income tax liabilities, net | |||||||||||

| Other liabilities | |||||||||||

| Total liabilities | |||||||||||

| Stockholders’ equity | |||||||||||

Common stock, $ | |||||||||||

| Additional paid-in capital | |||||||||||

| Accumulated other comprehensive loss, net of tax | ( | ( | |||||||||

| Retained earnings | |||||||||||

| Total stockholders’ equity | |||||||||||

| Total liabilities and stockholders’ equity | $ | $ | |||||||||

See accompanying notes.

3

Supernus Pharmaceuticals, Inc.

Condensed Consolidated Statements of Earnings (Loss)

(in thousands, except share and per share data)

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| (unaudited) | (unaudited) | ||||||||||||||||||||||

| Revenues | |||||||||||||||||||||||

| Net product sales | $ | $ | $ | $ | |||||||||||||||||||

| Royalty revenues | |||||||||||||||||||||||

| Total revenues | |||||||||||||||||||||||

| Costs and expenses | |||||||||||||||||||||||

| Cost of goods sold | |||||||||||||||||||||||

| Research and development | |||||||||||||||||||||||

| Selling, general and administrative | |||||||||||||||||||||||

| Amortization of intangible assets | |||||||||||||||||||||||

| Contingent consideration expense (gain) | ( | ( | |||||||||||||||||||||

| Total costs and expenses | |||||||||||||||||||||||

| Operating earnings (loss) | ( | ( | |||||||||||||||||||||

| Other income (expense) | |||||||||||||||||||||||

| Interest expense | ( | ( | ( | ||||||||||||||||||||

| Interest and other income, net | |||||||||||||||||||||||

| Total other income (expense) | |||||||||||||||||||||||

| Earnings (loss) before income taxes | ( | ||||||||||||||||||||||

| Income tax expense (benefit) | ( | ( | |||||||||||||||||||||

| Net earnings (loss) | $ | ( | $ | $ | $ | ||||||||||||||||||

| Earnings (loss) per share | |||||||||||||||||||||||

| Basic | $ | ( | $ | $ | $ | ||||||||||||||||||

| Diluted | $ | ( | $ | $ | $ | ||||||||||||||||||

| Weighted average shares outstanding | |||||||||||||||||||||||

| Basic | |||||||||||||||||||||||

| Diluted | |||||||||||||||||||||||

See accompanying notes.

4

Supernus Pharmaceuticals, Inc.

Condensed Consolidated Statements of Comprehensive Earnings (Loss)

(in thousands)

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| (unaudited) | (unaudited) | ||||||||||||||||||||||

| Net earnings (loss) | $ | ( | $ | $ | $ | ||||||||||||||||||

| Other comprehensive gain (loss) | |||||||||||||||||||||||

| Unrealized gain (loss) on marketable securities, net of tax | ( | ( | |||||||||||||||||||||

| Other comprehensive gain (loss) | ( | ( | |||||||||||||||||||||

| Comprehensive earnings (loss) | $ | ( | $ | ( | $ | $ | |||||||||||||||||

See accompanying notes.

5

Supernus Pharmaceuticals, Inc.

Condensed Consolidated Statements of Changes in Stockholders’ Equity

Nine Months Ended September 30, 2023 and 2022

(unaudited, in thousands, except share data)

| j | Common Stock | Additional Paid-in Capital | Accumulated Other Comprehensive Earnings (Loss) | Retained Earnings | Total Stockholders’ Equity | ||||||||||||||||||||||||||||||

| Shares | Amount | ||||||||||||||||||||||||||||||||||

| Balance, December 31, 2022 | $ | $ | $ | ( | $ | $ | |||||||||||||||||||||||||||||

| Share-based compensation | — | — | — | — | |||||||||||||||||||||||||||||||

| Issuance of common stock under the equity award plans, net of shares withheld for employee taxes | — | — | — | ||||||||||||||||||||||||||||||||

| Net earnings | — | — | — | — | |||||||||||||||||||||||||||||||

| Unrealized gain on marketable securities, net of tax | — | — | — | — | |||||||||||||||||||||||||||||||

| Balance, March 31, 2023 | $ | $ | $ | ( | $ | $ | |||||||||||||||||||||||||||||

| Share-based compensation | — | — | — | — | |||||||||||||||||||||||||||||||

| Issuance of common stock under the equity award plans, net of shares withheld for employee taxes | — | — | |||||||||||||||||||||||||||||||||

| Net loss | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||

| Unrealized gain on marketable securities, net of tax | — | — | — | — | |||||||||||||||||||||||||||||||

| Balance, June 30, 2023 | $ | $ | $ | ( | $ | $ | |||||||||||||||||||||||||||||

| Share-based compensation | — | — | — | — | |||||||||||||||||||||||||||||||

| Issuance of common stock under the equity award plans, net of shares withheld for employee taxes | — | ( | — | — | ( | ||||||||||||||||||||||||||||||

| Net loss | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||

| Unrealized loss on marketable securities, net of tax | — | — | — | — | |||||||||||||||||||||||||||||||

| Balance, September 30, 2023 | $ | $ | $ | ( | $ | $ | |||||||||||||||||||||||||||||

6

Supernus Pharmaceuticals, Inc.

Condensed Consolidated Statements of Changes in Stockholders’ Equity

Nine Months Ended September 30, 2023 and 2022

(unaudited, in thousands, except share data)

| Common Stock | Additional Paid-in Capital | Accumulated Other Comprehensive Earnings (Loss) | Retained Earnings | Total Stockholders’ Equity | |||||||||||||||||||||||||||||||

| Shares | Amount | ||||||||||||||||||||||||||||||||||

| Balance, December 31, 2021 | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||

| — | — | ( | — | ( | |||||||||||||||||||||||||||||||

| Balance, January 1, 2022 | |||||||||||||||||||||||||||||||||||

| Share-based compensation | — | — | — | — | |||||||||||||||||||||||||||||||

| Issuance of common stock in connection with the Company’s equity award plans | — | — | — | ||||||||||||||||||||||||||||||||

| Net earnings | — | — | — | — | |||||||||||||||||||||||||||||||

| Unrealized loss on marketable securities, net of tax | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| Balance, March 31, 2022 | $ | $ | $ | ( | $ | $ | |||||||||||||||||||||||||||||

| Share-based compensation | — | — | — | — | |||||||||||||||||||||||||||||||

| Issuance of common stock in connection with the Company’s equity award plans | — | — | — | ||||||||||||||||||||||||||||||||

| Net earnings | — | — | — | — | |||||||||||||||||||||||||||||||

| Unrealized loss on marketable securities, net of tax | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| Balance, June 30, 2022 | $ | $ | $ | ( | $ | $ | |||||||||||||||||||||||||||||

| Share-based compensation | — | — | — | — | |||||||||||||||||||||||||||||||

| Issuance of common stock in connection with the Company’s equity award plans | — | — | |||||||||||||||||||||||||||||||||

| Net earnings | — | — | — | — | |||||||||||||||||||||||||||||||

| Unrealized loss on marketable securities, net of tax | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||

| Balance, September 30, 2022 | $ | $ | $ | ( | $ | $ | |||||||||||||||||||||||||||||

See accompanying notes.

7

Supernus Pharmaceuticals, Inc.

Condensed Consolidated Statements of Cash Flows

(in thousands)

| Nine Months Ended September 30, | |||||||||||

| 2023 | 2022 | ||||||||||

| (unaudited) | |||||||||||

| Cash flows from operating activities | |||||||||||

| Net earnings | $ | $ | |||||||||

| Adjustments to reconcile net earnings (loss) to net cash provided by operating activities: | |||||||||||

| Depreciation and amortization | |||||||||||

| Other income from Navitor (see Note 4) | ( | ||||||||||

| Amortization of deferred financing costs and debt discount | |||||||||||

| Realized gains from sales of marketable securities | ( | ||||||||||

| Amortization of premium/discount on marketable securities | ( | ||||||||||

| Change in fair value of contingent consideration | ( | ||||||||||

| Other noncash adjustments, net | |||||||||||

| Share-based compensation expense | |||||||||||

| Deferred income tax benefit | ( | ( | |||||||||

| Changes in operating assets and liabilities: | |||||||||||

| Accounts receivable | ( | ||||||||||

| Inventories | ( | ||||||||||

| Prepaid expenses and other assets | ( | ||||||||||

| Accrued product returns and rebates | |||||||||||

| Accounts payable and other liabilities | ( | ( | |||||||||

| Contingent consideration | ( | ||||||||||

| Net cash provided by operating activities | |||||||||||

| Cash flows from investing activities | |||||||||||

| Purchases of marketable securities | ( | ||||||||||

| Sales and maturities of marketable securities | |||||||||||

| Purchases of property and equipment | ( | ( | |||||||||

| Net cash provided by (used in) investing activities | ( | ||||||||||

| Cash flows from financing activities | |||||||||||

| Proceeds from Line of Credit | |||||||||||

| Payments on Line of Credit | ( | ||||||||||

| Payment on convertible notes | ( | ||||||||||

| Payment of contingent consideration | ( | ||||||||||

| Proceeds from issuance of common stock | |||||||||||

| Net cash used in financing activities | ( | ( | |||||||||

| Net change in cash and cash equivalents | ( | ||||||||||

| Cash and cash equivalents at beginning of year | |||||||||||

| Cash and cash equivalents at end of period | $ | $ | |||||||||

| Supplemental cash flow information | |||||||||||

| Cash paid for interest on debt | $ | $ | |||||||||

| Cash paid for income taxes | |||||||||||

| Cash paid for operating leases | |||||||||||

| Noncash investing and financing activities | |||||||||||

| Lease assets obtained for new operating leases | $ | $ | |||||||||

| Deferred legal fees and fixed assets included in accounts payable and accrued expenses | |||||||||||

| Property and equipment additions from utilization of tenant improvement allowance | |||||||||||

See accompanying notes.

8

Supernus Pharmaceuticals, Inc.

Notes to Condensed Consolidated Financial Statements (unaudited)

1. Business Organization

Supernus Pharmaceuticals, Inc. (the "Company", see Note 2, Consolidation) is a biopharmaceutical company focused on developing and commercializing products for the treatment of central nervous system (CNS) diseases. The Company's diverse neuroscience portfolio includes approved treatments for epilepsy, migraine, attention-deficit hyperactivity disorder (ADHD), hypomobility in Parkinson’s Disease (PD), cervical dystonia, chronic sialorrhea, dyskinesia in PD patients receiving levodopa-based therapy, and drug-induced extrapyramidal reactions in adult patients. The Company is developing a broad range of novel CNS product candidates including new potential treatments for hypomobility in PD, epilepsy, depression, and other CNS disorders.

The Company has eight commercial products that it markets: Qelbree®, GOCOVRI®, Trokendi XR®, Oxtellar XR®, APOKYN®, XADAGO®, Osmolex ER®, and MYOBLOC®. In addition, SPN-830 (apomorphine infusion device) is a late-stage drug/device combination product candidate for the continuous treatment of motor fluctuations ("off" episodes) in PD patients that are not adequately controlled with oral levodopa and one or more adjunct PD medications.

2. Summary of Significant Accounting Policies

Basis of Presentation

The Company’s unaudited condensed consolidated financial statements have been prepared in accordance with the requirements of the U.S. Securities and Exchange Commission (SEC) for interim financial information. As permitted under Generally Accepted Accounting Principles in the United States (U.S. GAAP), certain notes and other information have been omitted from the interim unaudited condensed consolidated financial statements presented in this Quarterly Report on Form 10-Q. Therefore, these unaudited condensed consolidated financial statements should be read in conjunction with the Company’s most recent Annual Report on Form 10-K, for the year ended December 31, 2022, filed with the SEC.

In management’s opinion, the unaudited condensed consolidated financial statements include all normal and recurring adjustments necessary for a fair presentation of the Company’s financial position, results of operations, and cash flows. The results of operations for any interim period are not necessarily indicative of the Company’s future quarterly or annual results.

The Company, which is primarily located in the U.S., operates in one operating segment.

Consolidation

The Company's unaudited condensed consolidated financial statements include the accounts of Supernus Pharmaceuticals, Inc. and its wholly owned subsidiaries. These are collectively referred to herein as "Supernus" or "the Company." Supernus Pharmaceuticals, Inc. and each of its subsidiaries are distinct legal entities. All significant intercompany transactions and balances have been eliminated in consolidation.

The unaudited condensed consolidated financial statements reflect the consolidation of entities in which the Company has a controlling financial interest. In determining whether there is a controlling financial interest, the Company considers if it has a majority of the voting interests of the entity, or if the entity is a variable interest entity (VIE) and if the Company is the primary beneficiary. In determining the primary beneficiary of a VIE, the Company evaluates whether it has both: the power to direct the activities of the VIE that most significantly impact the VIE's economic performance; and the obligation to absorb losses of, or the right to receive benefits from the VIE that could potentially be significant to that VIE. The Company's judgment with respect to its level of influence or control of an entity involves the consideration of various factors, including the form of an ownership interest; representation in the entity's governance; the size of the investment; estimates of future cash flows; the ability to participate in policymaking decisions; and the rights of the other investors to participate in the decision making process, including the right to liquidate the entity, if applicable. If the Company is not the primary beneficiary of the VIE, and an ownership interest is maintained in the entity, the interest is accounted for under the equity or cost methods of accounting, as appropriate.

The Company continuously assesses whether it is the primary beneficiary of a VIE as changes to existing relationships or future transactions may affect its conclusions.

9

Use of Estimates

The Company bases its estimates on: historical experience; forecasts; information received from its service providers; information from other sources, including public and proprietary sources; and other assumptions that the Company believes are reasonable under the circumstances. Actual results could differ materially from the Company’s estimates. The Company periodically evaluates the methodologies employed in making its estimates.

Advertising Expense

Advertising expense includes the cost of promotional materials and activities, such as printed materials and digital marketing, marketing programs and speaker programs. The costs of the Company's advertising efforts are expensed as incurred.

The Company incurred approximately $25.1 million and $76.9 million in advertising expense for the three and nine months ended September 30, 2023, respectively, and approximately $52.0 million and $112.8 million for the three and nine months ended September 30, 2022. These expenses are recorded as a component of Selling, general and administrative expenses in the unaudited condensed consolidated statements of earnings (loss).

Restricted Cash

On March 30, 2023, the Company transferred funds totaling $403.8 million, which was reported as restricted cash in the first quarter of 2023, to the Trustee (Wilmington Trust) related to the repayment of the 2023 Notes. On April 1, 2023, the Company paid the total principal amount due of $402.5 million under the 2023 Notes and the remaining outstanding interest due of $1.3 million with the restricted cash. Refer to Note 8, Debt.

Line of Credit

Line of credit includes borrowings under the uncommitted demand secured line of credit. On February 8, 2023, the Company entered into a credit line agreement (the “Credit Line”) with UBS Bank USA (“UBS”). The Credit Line provides for a revolving line of credit of up to $150 million, which can be drawn at any time. Refer to Note 8, Debt.

Recently Issued Accounting Pronouncements

Accounting Pronouncements Adopted

Accounting Standards Update (ASU) 2020-06, Debt - Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging - Contracts in Entity's Own Equity (Subtopic 815-40): Accounting for Convertible Instruments and Contracts in an Entity's Own Equity - The new standard, issued in August 2020, simplifies the accounting for certain financial instruments with characteristics of liabilities and equity, including convertible debt instruments with cash conversion and beneficial conversion features. ASU 2020-06 eliminates requirements to separately account for liability and equity components of such convertible debt instruments and eliminates the ability to use the treasury stock method for calculating diluted earnings per share for convertible instruments whose principal amount may be settled in whole or in part with equity. Instead, ASU 2020-06 requires (i) the entire amount of the security to be presented as a liability on the balance sheet and (ii) application of the “if-converted” method for calculating diluted earnings per share. This new standard also removes certain settlement conditions required for equity contracts to qualify for the derivative scope exception.

10

3. Disaggregated Revenues

The following table summarizes the disaggregation of revenues by product or source, (dollars in thousands):

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| (unaudited) | (unaudited) | ||||||||||||||||||||||

| Net product sales | |||||||||||||||||||||||

| Qelbree | $ | $ | $ | $ | |||||||||||||||||||

| GOCOVRI | |||||||||||||||||||||||

| Oxtellar XR | |||||||||||||||||||||||

| Trokendi XR | |||||||||||||||||||||||

| APOKYN | |||||||||||||||||||||||

Other(1) | |||||||||||||||||||||||

| Total net product sales | $ | $ | $ | $ | |||||||||||||||||||

| Royalty revenues | |||||||||||||||||||||||

| Total revenues | $ | $ | $ | $ | |||||||||||||||||||

___________________________________________

(1) Includes net product sales of MYOBLOC, XADAGO and Osmolex ER.

The decrease in Trokendi XR net product sales for the three and nine months ended September 30, 2023, compared to the same period in 2022 was primarily attributable to the loss of exclusivity with generic entrants in January 2023.

The following table shows the percentage of net product sales to total net product sales:

| Percentage of Net Product Sales | |||||||||||||||||||||||

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| Qelbree | |||||||||||||||||||||||

| GOCOVRI | |||||||||||||||||||||||

| Oxtellar XR | |||||||||||||||||||||||

| Trokendi XR | |||||||||||||||||||||||

| APOKYN | |||||||||||||||||||||||

Other(1) | |||||||||||||||||||||||

| Total | |||||||||||||||||||||||

(1) Includes net product sales of MYOBLOC, XADAGO and Osmolex ER.

Each of our three major customers, AmerisourceBergen Drug Corporation, Cardinal Health, Inc. and McKesson Corporation, individually accounted for more than 20 70

11

4. Investments

Marketable Securities

| September 30, 2023 | December 31, 2022 | ||||||||||

| (unaudited) | |||||||||||

| Corporate and municipal debt securities | |||||||||||

| Amortized cost | $ | $ | |||||||||

| Gross unrealized gains | |||||||||||

| Gross unrealized losses | ( | ( | |||||||||

| Total fair value | $ | $ | |||||||||

| September 30, 2023 | |||||

| (unaudited) | |||||

| Less than 1 year | $ | ||||

| 1 year to 2 years | |||||

| Total | $ | ||||

As of September 30, 2023, there was no impairment due to credit loss on any available-for-sale marketable securities.

Investment in Navitor

Development Agreement

In April 2020, the Company entered into a development agreement (the Development Agreement) with Navitor Pharmaceuticals, Inc. (Navitor Inc.). The Company can terminate the Development Agreement upon 30 days' notice. Under the terms of the Development Agreement, the Company and Navitor Inc. will jointly conduct a Phase II clinical program for NV-5138 (SPN-820) for treatment-resistant depression. The Company will bear all of the Phase I and Phase II development costs incurred by either party, up to a maximum of $50 million. In addition, the Company will incur certain other research and development support costs. There are certain additional payment amounts which could be incurred by the Company. These costs are contingent upon Navitor Inc. achieving defined development milestones. The Company has an option to acquire or license NV-5138 (SPN-820), for which additional payments would be required.

Equity investment

In addition to entering into the Development Agreement in April 2020, the Company acquired Series D Preferred Shares of Navitor Inc. for $15 million, representing an approximately 13 % ownership position in Navitor Inc.

In March 2021, Navitor Inc. underwent a legal restructuring. In the restructuring, Navitor Inc. became a wholly owned subsidiary of a newly formed limited liability company, Navitor Pharmaceuticals LLC (Navitor LLC), and the outstanding shares of stock in Navitor Inc. were exchanged for units of membership in Navitor LLC having equivalent rights and preferences (Navitor Restructuring). As part of the Navitor Restructuring, the Series D Preferred Shares previously held by the Company were exchanged for Series D Preferred Shares in Navitor LLC. In addition, certain assets that did not relate to NV-5138 (SPN-820) were transferred from Navitor Inc. to a newly formed entity that became a separate, wholly owned subsidiary of Navitor LLC.

The Company had determined that Navitor LLC is a VIE. The Company does not consolidate this VIE because the Company lacks the power to direct the activities that most significantly impact Navitor’s economic performance.

Prior to the Navitor Restructuring, the investment was accounted for under the practical expedient allowed for equity securities without readily determinable fair value, which is cost minus impairment plus any changes in observable price changes from an orderly transaction of similar investments in Navitor Inc. Following the legal restructuring and exchange of the preferred shares for member equity units of Navitor LLC, the investment was accounted for under the equity method of accounting due to the Company's ability to exert significant influence over but not control the financial and operating decisions of Navitor LLC. As

12

a result of the change from a cost method investment to an equity method investment, the Company was required to measure its investment initially in accordance with the guidance in ASC 805. The majority of the assets and liabilities recorded in Navitor LLC's financial statements represent working capital items and cash that are being used for research and development purposes and are significantly lower than the Company's investment in Navitor LLC, which created a significant basis difference for the Company's investment in the underlying net assets. The Company determined that substantially all of the fair value of the investment was attributable to a single in-process research and development (IPR&D) asset. As a result, Navitor LLC was not considered a business as defined in ASC 805. In the first quarter of 2021, the $15 million investment, which was previously recorded in Other assets in the unaudited condensed consolidated balance sheets, was expensed and recorded in Research and development expense.

The Company records its share of the results of Navitor LLC, a private company, on a quarter lag as the financial information of Navitor LLC is not available on a sufficiently timely basis for the Company to apply the equity method of accounting. In December 2021, Navitor LLC sold one of its subsidiaries and distributed cash to its members in accordance with each member's share of the proceeds from the sale. The Company received $12.9 million in December 2021 from Navitor LLC in connection with this sale. As the Company's policy is to record its share of the results in its equity method investment on a quarter lag as previously indicated, the Company recorded the cash amount received in Other current liabilities in the consolidated balance sheets as of December 31, 2021. In the first quarter of 2022, the Company determined its estimated share of Navitor LLC's year-end 2021 earnings and recorded a gain of $12.9 million in Interest and other income, net in the unaudited condensed consolidated statement of earnings (loss).

The maximum exposure to losses related to Navitor LLC is a maximum of approximately $50 million in expense for Phase I and Phase II development of NV-5138 (SPN-820), and the cost of other development and formulation activities provided by the Company.

Subsequent to the Development Agreement entered into in 2020, no additional equity investment has been made or financing has been provided to Navitor LLC.

5. Fair Value of Financial Measurements

The fair value of an asset or liability represents the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between unrelated market participants.

The Company reports the fair value of assets and liabilities using a three level measurement hierarchy that prioritizes the inputs used to measure fair value. Fair value hierarchy consists of the following three levels:

•Level 1—Valuations based on unadjusted quoted prices in active markets that are accessible at measurement date for identical assets.

•Level 2—Valuations based on quoted prices for similar assets or liabilities in active markets, quoted prices for identical or similar assets or liabilities in markets that are not active and model-based valuations in which all significant inputs are observable in the market, either directly or indirectly (e.g., interest rates; yield curves).

•Level 3—Valuations using significant inputs that are unobservable in the market and inputs that reflect the Company’s own assumptions. These are based on the best information available, including the Company’s own data.

The fair value of the restricted marketable securities is recorded in Other assets on the unaudited condensed consolidated balance sheets. There have been no transfers of assets or liabilities into or out of Level 3 of the fair value hierarchy.

13

Financial Assets and Liabilities Recorded at Fair Value

The Company’s financial assets that are required to be measured at fair value on a recurring basis are as follows (dollars in thousands):

| Fair Value Measurements as of September 30, 2023 (unaudited) | |||||||||||||||||||||||

| Total Fair Value as of September 30, 2023 (unaudited) | Level 1 | Level 2 | Level 3 | ||||||||||||||||||||

| Assets: | |||||||||||||||||||||||

| Cash and cash equivalents | |||||||||||||||||||||||

| Cash | $ | $ | $ | $ | |||||||||||||||||||

| Money market securities and funds | |||||||||||||||||||||||

| Marketable securities | |||||||||||||||||||||||

| Corporate and municipal debt securities | |||||||||||||||||||||||

| Long-term marketable securities | |||||||||||||||||||||||

| Corporate and municipal debt securities | |||||||||||||||||||||||

| Other assets | |||||||||||||||||||||||

| Marketable securities - restricted (SERP) | |||||||||||||||||||||||

| Total assets at fair value | $ | $ | $ | $ | |||||||||||||||||||

| Liabilities: | |||||||||||||||||||||||

| Contingent consideration | $ | $ | $ | $ | |||||||||||||||||||

| Total liabilities at fair value | $ | $ | $ | $ | |||||||||||||||||||

| Fair Value Measurements as of December 31, 2022 | |||||||||||||||||||||||

| Total Fair Value as of December 31, 2022 | Level 1 | Level 2 | Level 3 | ||||||||||||||||||||

| Assets: | |||||||||||||||||||||||

| Cash and cash equivalents | |||||||||||||||||||||||

| Cash | $ | $ | $ | $ | |||||||||||||||||||

| Money market securities and funds | |||||||||||||||||||||||

| Marketable securities | |||||||||||||||||||||||

| Corporate and municipal debt securities | |||||||||||||||||||||||

| Long-term marketable securities | |||||||||||||||||||||||

| Corporate and municipal debt securities | |||||||||||||||||||||||

| Other assets | |||||||||||||||||||||||

| Marketable securities - restricted (SERP) | |||||||||||||||||||||||

| Total assets at fair value | $ | $ | $ | $ | |||||||||||||||||||

| Liabilities: | |||||||||||||||||||||||

| Contingent consideration | $ | $ | $ | $ | |||||||||||||||||||

| Total liabilities at fair value | $ | $ | $ | $ | |||||||||||||||||||

Other Financial Instruments

The carrying amounts of other financial instruments, including accounts receivable, accounts payable, and accrued expenses approximate fair value due to their short-term maturities.

14

Financial Liabilities Recorded at Carrying Value

On April 1, 2023, the Company paid the total principal amount due of $402.5 million under the 2023 Notes and the outstanding interest due of $1.3 million.

As of December 31, 2022, the carrying value and fair value of the 2023 Notes which were not carried at fair value was as follows (dollars in thousands):

| December 31, 2022 | |||||||||||

| Carrying Value | Fair Value (Level 2) | ||||||||||

| Convertible notes, net | $ | $ | |||||||||

6. Contingent Consideration

The following table provides the current and long-term portions related to the contingent consideration for the USWM Acquisition and Adamas Acquisition (dollars in thousands):

| September 30, 2023 | December 31, 2022 | ||||||||||

| Reported under the following captions in the condensed consolidated balance sheets: | (unaudited) | ||||||||||

| Contingent consideration, current portion | $ | $ | |||||||||

| Contingent consideration, long-term | |||||||||||

| Total | $ | $ | |||||||||

The Company's contingent consideration liabilities are related to the USWM Acquisition in 2020 and the Adamas Acquisition in 2021 (each acquisition as defined below). The contingent consideration liabilities are measured at fair value using either a Monte Carlo simulation or the income approach. The Company classifies its contingent consideration liabilities as Level 3 fair value measurements based on the significant unobservable inputs used to estimate fair value. These reflect the inputs and assumptions the Company believes would be made by market participants. Changes in any of those inputs together or in isolation may result in significantly lower or higher fair value measurement. The change in fair value is reported on the condensed consolidated statement of earnings (loss) in Contingent consideration (gain) expense.

USWM Contingent Consideration

On June 9, 2020 (the USWM Closing Date), the Company completed its acquisition of all the outstanding equity of USWM Enterprises, LLC (USWM Enterprises) (USWM Acquisition). The USWM Acquisition included potential additional contingent consideration payments for regulatory and development milestones and sales-based milestones. As of September 30, 2023, the potential contingent consideration payments are up to $85 million, which is comprised of the potential $55 million in regulatory and development milestones and $30 million in sales-based milestones.

•Regulatory and development milestones:

The potential $55 million in regulatory and development milestones is comprised of (1) $25 million related to the FDA's approval of the SPN-830 NDA and (2) $30 million related to the subsequent commercial product launch.

•Sales-based milestones:

The potential $30 million sales-based milestone relates to the achievement of certain net product sales of the acquired USWM products in 2023. As of September 30, 2023, the Company assessed that this remaining $30 million sales-based milestone will not be achieved based on net sales projections.

The key assumptions considered in estimating the fair value include the estimated probability and timing of milestone achievement, such as the probability and timing of obtaining regulatory approval, discount rate, and the estimated amount and timing of projected revenues from the acquired USWM products.

15

Adamas Contingent Consideration

On November 24, 2021 (the Adamas Closing Date), the Company completed its acquisition of all the outstanding equity of Adamas (Adamas Acquisition). The Adamas Acquisition included payment of two non-tradable contingent value rights (CVRs) each of which represents the contractual right to receive a contingent payment upon the achievement of the applicable aggregate worldwide net product sales of GOCOVRI.

Each CVR represents the contractual right to receive a contingent payment of $0.50 per share in cash, less any applicable withholding taxes and without interest, upon the achievement of the applicable milestone (each such amount, a Milestone Payment) in accordance with the terms of a Contingent Value Rights Agreement entered into between the Company and American Stock Transfer & Trust Company, LLC, as rights agent, as further defined in the CVR agreement. One Milestone Payment is payable (subject to certain terms and conditions) upon the first occurrence of the achievement of aggregate worldwide net sales of GOCOVRI in excess of $150 million during any consecutive 12-month period ending on or before December 31, 2024 (Milestone 2024). Another Milestone Payment is payable (subject to certain terms and conditions) upon the first occurrence of the achievement of aggregate worldwide net sales of GOCOVRI in excess of $225 million during any consecutive 12-month period ending on or before December 31, 2025 (Milestone 2025 and, together with Milestone 2024, the Milestones). Each Milestone may only be achieved once. The possible outcomes for the contingent consideration range from $0 to $50.9 million on an undiscounted basis.

The key assumptions considered in estimating the fair value of the Adamas sales-based milestones include the estimated revenue projections, volatility, estimated discount rates and risk-free interest rate.

Change in the Fair Value of Contingent Consideration

The following tables provide a reconciliation of the beginning and ending balances related to the contingent consideration for the USWM Acquisition and Adamas Acquisition (dollars in thousands):

| USWM Acquisition | Adamas Acquisition | Total | |||||||||||||||

| Balance at December 31, 2022 | $ | $ | $ | ||||||||||||||

| Change in fair value recognized in earnings | ( | ( | |||||||||||||||

| Balance at March 31, 2023 (unaudited) | |||||||||||||||||

| Change in fair value recognized in earnings | |||||||||||||||||

| Balance at June 30, 2023 (unaudited) | |||||||||||||||||

| Change in fair value recognized in earnings | ( | ( | |||||||||||||||

| Balance at September 30, 2023 (unaudited) | $ | $ | $ | ||||||||||||||

| USWM Acquisition | Adamas Acquisition | Total | |||||||||||||||

| Balance at December 31, 2021 | $ | $ | $ | ||||||||||||||

| Milestone payments | ( | ( | |||||||||||||||

| Change in fair value recognized in earnings | ( | ||||||||||||||||

| Balance at March 31, 2022 (unaudited) | |||||||||||||||||

| Change in fair value recognized in earnings | |||||||||||||||||

| Balance at June 30, 2022 (unaudited) | |||||||||||||||||

| Change in fair value recognized in earnings | |||||||||||||||||

| Balance at September 30, 2022 (unaudited) | $ | $ | $ | ||||||||||||||

The Company recorded a $0.7 million expense and a $0.4 million gain due to the change in the fair value of the contingent consideration liabilities for the USWM milestones for the three and nine months ended September 30, 2023 primarily driven by the passage of time in both periods, as well as the change in timing of milestone achievement and estimated discount rate in the first quarter of 2023. The Company recorded a $0.4 million expense and a $2.4 million expense due to the change in the fair value of the contingent consideration liabilities for the USWM milestones for the three and nine months ended September 30, 2022 primarily driven by the passage of time and the accretion to the payout amount related to the milestone achieved in the first quarter of 2022.

16

The Company recorded a $1.1 million gain and a $0.9 million gain due to the change in fair value of the contingent consideration liabilities for the Adamas CVRs for the three and nine months ended September 30, 2023 primarily driven by the passage of time. The Company recorded a $0.1 million expense and a $0.5 million gain due to the change in fair value of the contingent consideration liabilities for the Adamas CVRs for the three and nine months ended September 30, 2022 primarily driven by the passage of time.

The Company paid $25 million in the first quarter of 2022 of which $22.9 million represents the acquisition date fair value of the contingent consideration liability and was reported under cash flows from financing activities. The remaining $2.1 million represents the excess of the acquisition date fair value and was reported under cash flows from operating activities. The amount paid was for the milestone that was due upon the FDA acceptance of the SPN-830 NDA for review, which was achieved in the first quarter of 2022.

7. Intangible Assets, Net

| September 30, 2023 | December 31, 2022 | ||||||||||||||||||||||||||||||||||||||||

| (unaudited) | |||||||||||||||||||||||||||||||||||||||||

| Remaining Weighted Average Life (Years) | Carrying Amount, Gross | Accumulated Amortization | Carrying Amount, Net | Carrying Amount, Gross | Accumulated Amortization | Carrying Amount, Net | |||||||||||||||||||||||||||||||||||

| Acquired in-process research and development | $ | $ | — | $ | $ | $ | — | $ | |||||||||||||||||||||||||||||||||

| Intangible assets subject to amortization: | |||||||||||||||||||||||||||||||||||||||||

| Acquired developed technology and product rights | ( | ( | |||||||||||||||||||||||||||||||||||||||

| Capitalized patent defense costs | ( | ( | |||||||||||||||||||||||||||||||||||||||

| Total intangible assets | $ | $ | ( | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||||||||

Amortization expense for intangible assets was approximately $21.2 million and $61.3 million, for the three and nine months ended September 30, 2023 and approximately $20.6 million and $61.9 million for the three and nine months ended September 30, 2022, respectively.

8. Debt

Convertible Senior Notes Due 2023

The 0.625 % Convertible Senior Notes Due 2023 (2023 Notes), which were issued in March 2018, bore interest at an annual rate of 0.625 %, payable semi-annually in arrears on April 1 and October 1 of each year. The 2023 Notes matured on April 1, 2023. On March 30, 2023, the Company transferred funds totaling $403.8 million to the Trustee (Wilmington Trust) related to the repayment of the 2023 Notes which was reported as restricted cash in the first quarter of 2023. On April 1, 2023, the Company paid the total principal amount due of $402.5 million under the 2023 Notes and the remaining outstanding interest due of $1.3 million with the restricted cash.

Contemporaneous with the issuance of the 2023 Notes, the Company also entered into separate privately negotiated convertible note hedge transactions (collectively, the Convertible Note Hedge Transactions) with each of the call spread counterparties. The Company issued 402,500 convertible note hedge options. As of March 31, 2023, the Convertible Note Hedges have expired.

Concurrently with entering into the Convertible Note Hedge Transactions, the Company also entered into separate privately negotiated warrant transactions (collectively, the Warrant Transactions) with each of the call spread counterparties. The

17

Company issued a total of 6,783,939 warrants. The warrants entitle the holder to one share per warrant. The strike price of the Warrant Transactions will initially be $80.91 per share of the Company’s common stock, and is subject to adjustment.

The Warrant Transactions were intended to partially offset the cost to the Company of the purchased Convertible Note Hedge Transactions; however, the Warrant Transactions could have a dilutive effect with respect to the Company’s common stock, to the extent that the market price per share of the Company’s common stock, as measured under the terms of the Warrant Transactions, exceeds the strike price of the warrants. The warrants expire in tranches, if unexercised, on or before November 22, 2023.

| December 31, 2022 | |||||

| 2023 Notes | $ | ||||

| Unamortized debt discount and deferred financing costs | ( | ||||

| Total carrying value | $ | ||||

Uncommitted Demand Secured Line of Credit

On February 8, 2023, the Company entered into a credit line agreement with UBS. The Credit Line provides for a revolving line of credit of up to $150 million, which can be drawn at any time. Any fixed rate borrowing will bear interest at a fixed interest rate, equal to the sum of (i) the UBS Fixed Funding Rate (as defined in the Credit Line) plus (ii) the applicable Percentage Spread established in the Credit Line. Any variable rate borrowing will bear interest at a variable interest rate, equal to the sum of (i) the UBS Variable Rate (as defined in the Credit Line) plus (ii) the applicable Percentage Spread established in the Credit Line.

The Credit Line is secured by a first priority lien and security interest in certain of the Company’s assets, including each account of the Company at UBS Financial Services Inc. (the “Collateral Account”), and other such collateral (collectively, the "Collateral"), as further defined in the Credit Line. The Company may be required to post additional collateral if the value of the Collateral declines below the required collateral maintenance requirements.

Upon certain customary events of default, all amounts due under the Credit Line will become immediately due and payable without demand, and UBS has the right, in its discretion, to liquidate, transfer, withdraw or sell all or any part of the Collateral and apply the proceeds to repay any borrowings pursuant to the Credit Line.

The Company has the right to repay any variable rate advance under the Credit Line at any time, in whole or in part, without penalty. The Company may repay any fixed rate advance in whole, but may not repay any fixed rate advance in part. In its discretion and without cause, UBS has the right at any time to demand full or partial payment of amounts borrowed pursuant to the Credit Line and terminate the Credit Line.

On March 30, 2023, the Company borrowed $93.0 million under the Credit Line, which bore a variable interest rate. The funds from this borrowing were used to repay outstanding indebtedness under the 2023 Notes as discussed above under the Convertible Senior Notes Due 2023. As of June 30, 2023, the Company repaid the total principal balance of $93.0 million under the Credit Line and the interest incurred on the Credit Line of $0.7 million. As of September 30, 2023, there was no outstanding debt under the Credit Line.

9. Share-Based Payments

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| (unaudited) | (unaudited) | ||||||||||||||||||||||

| Research and development | $ | $ | $ | $ | |||||||||||||||||||

| Selling, general and administrative | |||||||||||||||||||||||

| Total | $ | $ | $ | $ | |||||||||||||||||||

18

Stock Option and Stock Appreciation Rights

| Number of Options | Weighted Average Exercise Price | Weighted Average Remaining Contractual Term (in years) | |||||||||||||||

| Outstanding, December 31, 2022 | $ | ||||||||||||||||

| Granted | $ | ||||||||||||||||

| Exercised | ( | $ | |||||||||||||||

| Forfeited | ( | $ | |||||||||||||||

| Outstanding, September 30, 2023 (unaudited) | $ | ||||||||||||||||

| As of September 30, 2023 (unaudited): | |||||||||||||||||

| Vested and expected to vest | $ | ||||||||||||||||

| Exercisable | $ | ||||||||||||||||

| As of December 31, 2022: | |||||||||||||||||

| Vested and expected to vest | $ | ||||||||||||||||

| Exercisable | $ | ||||||||||||||||

Restricted Stock Units

The following table summarizes restricted stock unit (RSU) activities:

| Number of RSUs | Weighted Average Grant Date Fair Value per Share | ||||||||||

| Nonvested, December 31, 2022 | $ | ||||||||||

| Granted | $ | ||||||||||

| Vested | ( | $ | |||||||||

| Forfeited | ( | $ | |||||||||

| Nonvested, September 30, 2023 (unaudited) | $ | ||||||||||

Performance Share Units

The following table summarizes performance share unit (PSU) activities:

| Performance-Based Units | Market-Based Units | Total PSUs | |||||||||||||||||||||||||||||||||

| Number of PSUs | Weighted Average Grant Date Fair Value per Share | Number of PSUs | Weighted Average Grant Date Fair Value per Share | Number of PSUs | Weighted Average Grant Date Fair Value per Share | ||||||||||||||||||||||||||||||

| Nonvested, December 31, 2022 | $ | $ | $ | ||||||||||||||||||||||||||||||||

| Granted | $ | $ | $ | ||||||||||||||||||||||||||||||||

| Vested | ( | $ | $ | ( | $ | ||||||||||||||||||||||||||||||

| Forfeited | ( | $ | $ | ( | $ | ||||||||||||||||||||||||||||||

| Nonvested, September 30, 2023 (unaudited) | $ | $ | $ | ||||||||||||||||||||||||||||||||

19

10. Earnings (Loss) per Share

Basic earnings (loss) per share is calculated using the weighted average number of common shares outstanding. Diluted earnings (loss) per share is calculated using the weighted average number of common shares outstanding, including the dilutive effect of the Company’s stock option grants, SARs, RSUs, employee stock purchase plan (ESPP) awards as determined per the treasury method, and the 2023 Notes, as determined per the if-converted method.

Effect of Convertible Notes and Related Convertible Note Hedges and Warrants

In connection with the issuance of the 2023 Notes, the Company entered into Convertible Note Hedge and Warrant Transactions as described further in Note 8, Debt. The expected collective impact of the Convertible Note Hedge and Warrant Transactions is to reduce the potential dilution that would occur if the price of the Company's common stock was between the conversion price of $59.33 per share and the strike price of the warrants of $80.91 per share.

Diluted earnings (loss) per share related to the 2023 Notes is calculated using the if-converted method. The number of dilutive shares is based on the initial conversion rate associated with the 2023 Notes. The Convertible Note Hedge and Warrant Transactions are excluded in the calculation of diluted earnings (loss) per share because inclusion would be anti-dilutive. Specifically, the denominator of the diluted earnings (loss) per share calculation excludes the additional shares related to the warrants because the average price of the Company's common stock was less than the strike price of the warrants of $80.91 per share. The Convertible Note Hedge Transactions are not considered in calculating diluted earnings (loss) per share as their impact would be anti-dilutive.

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| (unaudited) | (unaudited) | ||||||||||||||||||||||

| 2023 Notes | |||||||||||||||||||||||

| Stock options, RSUs, PSUs | |||||||||||||||||||||||

The following table sets forth the computation of basic and diluted earnings (loss) per share for the three and nine months ended September 30, 2023 and 2022 under the if-converted method (dollars in thousands, except share and per share amounts):

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| (unaudited) | (unaudited) | ||||||||||||||||||||||

| Numerator: | |||||||||||||||||||||||

| Net earnings (loss) | $ | ( | $ | $ | $ | ||||||||||||||||||

| After-tax interest expense for 2023 Notes | |||||||||||||||||||||||

Numerator for dilutive earnings (loss) per share | $ | ( | $ | $ | $ | ||||||||||||||||||

| Denominator: | |||||||||||||||||||||||

| Weighted average shares outstanding, basic | |||||||||||||||||||||||

| Effect of dilutive securities: | |||||||||||||||||||||||

| Stock options, RSUs and SARs | |||||||||||||||||||||||

| Convertible notes | |||||||||||||||||||||||

| Weighted average shares outstanding, diluted | |||||||||||||||||||||||

| Earnings (loss) per share, basic | $ | ( | $ | $ | $ | ||||||||||||||||||

| Earnings (loss) per share, diluted | $ | ( | $ | $ | $ | ||||||||||||||||||

20

11. Income Tax Expense (Benefit)

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| (unaudited) | (unaudited) | ||||||||||||||||||||||

| Income tax expense (benefit) | $ | $ | ( | $ | $ | ( | |||||||||||||||||

| Effective tax rate | % | % | % | ( | % | ||||||||||||||||||

Income tax expense was $25.9 million for the three months ended September 30, 2023, as compared to income tax benefit of $2.2 million for the same period in the prior year. The change was primarily due to the larger pretax income in the third quarter of 2023. Income tax expense was $1.6 million for the nine months ended September 30, 2023, as compared to income tax benefit of $9.6 million for the same period in the prior year. The change was primarily due to certain tax benefits recognized with certain reorganization activities that occurred during the first quarter of 2022.

The change in the effective tax rates for both the three months ended September 30, 2023 and nine months ended September 30, 2023, as compared to the same periods in prior year, were primarily due to lower pretax earnings forecasted for 2023. ASC 740, Income Taxes (ASC 740), requires an estimate of the annual effective income tax rate for the full year and apply it to pretax income (loss) for each interim period, taking into account year-to-date amounts and projected results for the full year. The annual forecasted earnings represent the Company's best estimate as of September 30, 2023 and is subject to changes, which could have a material impact on the effective tax rate in subsequent periods.

12. Leases

Operating lease assets and lease liabilities as reported on the unaudited condensed consolidated balance sheets are as follows (dollars in thousands):

| Balance Sheet Classification | September 30, 2023 | December 31, 2022 | |||||||||||||||

| (unaudited) | |||||||||||||||||

| Assets | |||||||||||||||||

| Operating lease assets | $ | $ | |||||||||||||||

| Total lease assets | $ | $ | |||||||||||||||

| Liabilities | |||||||||||||||||

| Operating lease liabilities, current portion | $ | $ | |||||||||||||||

| Operating lease liabilities, long-term | |||||||||||||||||

| Total lease liabilities | $ | $ | |||||||||||||||

13. Composition of Other Balance Sheet Items

Accounts Receivables, Net

As of September 30, 2023 and December 31, 2022, the Company has reduced accounts receivable by approximately $10.8 million and $13.0 million, respectively. Prompt pay discount and contractual service fees, which were originally recorded as a reduction to revenues, represents estimated amounts not expected to be paid by our customers. The Company's customers are primarily pharmaceutical wholesalers and distributors and specialty pharmacies.

21

Inventories

| September 30, 2023 | December 31, 2022 | ||||||||||

| (unaudited) | |||||||||||

| Raw materials | $ | $ | |||||||||

| Work in process | |||||||||||

| Finished goods | |||||||||||

| Total | $ | $ | |||||||||

Property and Equipment

| September 30, 2023 | December 31, 2022 | ||||||||||

| (unaudited) | |||||||||||

| Lab equipment and furniture | $ | $ | |||||||||

| Leasehold improvements | |||||||||||

| Software | |||||||||||

| Computer equipment | |||||||||||

| Construction-in-progress | |||||||||||

| Less accumulated depreciation and amortization | ( | ( | |||||||||

| Property and equipment, net | $ | $ | |||||||||

Depreciation and amortization expense on property and equipment was approximately $0.6 million and $1.9 million for the three and nine months ended September 30, 2023, and approximately $0.8 million and $2.2 million for the three and nine months ended September 30, 2022, respectively.

Accounts Payable and Accrued Liabilities

| September 30, 2023 | December 31, 2022 | ||||||||||

| (unaudited) | |||||||||||

| Accounts payable | $ | $ | |||||||||

| Accrued compensation, benefits, & related accruals | |||||||||||

| Accrued sales & marketing | |||||||||||

| Accrued R&D expenses | |||||||||||

| Accrued manufacturing expenses | |||||||||||

Accrued royalties (1) | |||||||||||

Operating lease liabilities, current portion (2) | |||||||||||

| Other accrued expenses | |||||||||||

| Total | $ | $ | |||||||||

_______________________________

(1) Refer to Note 15, Commitments and Contingencies.

(2) Refer to Note 12, Leases.

Accrued Product Returns and Rebates

| September 30, 2023 | December 31, 2022 | ||||||||||

| (unaudited) | |||||||||||

| Accrued product rebates | $ | $ | |||||||||

| Accrued product returns | |||||||||||

| Total | $ | $ | |||||||||

22

14. Interest Expense

The following details the composition of interest expense (dollars in thousands):

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| (unaudited) | (unaudited) | ||||||||||||||||||||||

| Interest expense | $ | $ | ( | $ | ( | $ | ( | ||||||||||||||||

| Noncash interest expense on nonrecourse liability related to sale of future royalties | ( | ( | ( | ||||||||||||||||||||

| Noncash interest expense on debt | ( | ( | ( | ||||||||||||||||||||

| Total | $ | $ | ( | $ | ( | $ | ( | ||||||||||||||||

Noncash interest expense on debt is related to amortization of deferred financing costs on the 2023 Notes. The Company fully amortized the deferred financing costs on the 2023 Notes in the first quarter of 2023.

15. Commitments and Contingencies

Product Licenses

The Company has obtained exclusive licenses from third parties for proprietary rights to support the product candidates in the Company's CNS portfolio. Under these license agreements, the Company may be required to pay certain amounts upon the achievement of defined milestones. If these products are ultimately commercialized, the Company is also obligated to pay royalties to third parties, computed as a percentage of net product sales, for each respective product under a license agreement.

Through the USWM Acquisition, the Company acquired licensing agreements with other pharmaceutical companies for APOKYN, XADAGO, and MYOBLOC. The Company is obligated to pay royalties to third parties, computed as a percentage of net product sales, for each of the products under the respective license agreements. The royalty expense incurred for these acquired products is recognized as Cost of goods sold in the unaudited condensed consolidated statements of earnings (loss).

Royalty Agreement

In the third quarter of 2014, the Company received $30 million pursuant to a Royalty Interest Acquisition Agreement related to the purchase by HC Royalty of certain of the Company's rights under the Company's agreement with United Therapeutics related to the commercialization of Orenitram (treprostinil) Extended-Release Tablets. Full ownership of the royalty rights have reverted back to the Company as the cumulative payment threshold has been reached as of June 30, 2023 (see Note 3, Disaggregated Revenues).

As of December 31, 2022, the nonrecourse liability related to the sale of future royalties was $6.0 million and was included in Other current liabilities as reported on the condensed consolidated balance sheet.

USWM Enterprise Commitments Assumed

As part of the USWM Acquisition, the Company assumed the remaining commitments of USWM Enterprises and its subsidiaries, which are discussed below.

The Company assumed the annual minimum purchase requirement of MYOBLOC, amounting to an estimated €3.9 million annually, under the contract manufacturing agreement with Merz for manufacture and supply.

MDD US Operations, LLC (formerly US WorldMeds, LLC) and its subsidiary, Solstice Neurosciences, LLC (US) (collectively, the MDD Subsidiaries) entered into a Corporate Integrity Agreement (CIA) with the Office of Inspector General of the U.S. Department of Health and Human Services which was effective in April 2019. Under the CIA, the MDD Subsidiaries agreed to and paid $17.5 million to resolve U.S. Department of Justice allegations that it violated the False Claims Act and committed to the establishment and ongoing maintenance of an effective compliance program. The fine was paid by the MDD Subsidiaries prior to closing of the USWM Acquisition. As part of the USWM Acquisition, the Company assumed the obligations of the CIA and could become liable for payment of certain stipulated monetary penalties in the event of any CIA violations. In addition, the Company will continue to maintain a broad array of processes, policies and procedures necessary to comply with the

23

CIA through March 2024.

Data Breach-related Contingency

On November 24, 2021, the Company announced that we were the target of a ransomware attack. The attack had no significant impact on our business and did not cause any long-term disruption to our operations. Based on its internal investigation, the Company believes the criminal ransomware groups ("criminal groups") copied certain data from our systems, encrypted certain data on the Company's systems, and then deployed malware designed to impede access to our systems. Thereafter the criminal groups contacted the Company and threatened to publish certain data copied from the Company's systems. Upon detection of the ransomware attack, the Company notified government authorities, engaged third-party cybersecurity experts through our outside counsel, and commenced its recovery process. The Company maintains redundant off-site data backups, which were verified to have not been compromised by the ransomware attack and were utilized to restore the data encrypted by the criminal groups. In the fourth quarter of 2021, the Company had successfully recovered the impacted files and took additional steps designed to further protect its networks and files.

Furthermore, while the Company has not been the subject of any legal proceedings involving the attack, the likelihood that the Company could be the subject of claims from persons alleging they suffered damages from the incident, or actions by governmental authorities is possible, but the amount of such fines, penalties or costs, if any, cannot be estimated at this time. The Company continues to monitor the situation.

Claims and Litigation

From time to time, the Company may be involved in various claims, litigation and legal proceedings. These matters may involve patent litigation, product liability and other product-related litigation, commercial and other matters, and government investigations, among others. On a quarterly basis, the Company reviews the status of each significant matter and assesses its potential financial exposure. If the potential loss from any claim, asserted or unasserted, or legal proceeding is considered probable and the amount can be reasonably estimated, the Company will accrue a liability for the estimated loss. Because of uncertainties related to claims, legal proceedings and litigation, accruals will be based on the Company's best estimates based on available information. The Company does not believe that any of these matters will have a material adverse effect on our financial position. The Company may reassess the potential liability related to these matters and may revise these estimates. The process of resolving matters through litigation or other means is inherently uncertain and it is possible that an unfavorable resolution of these matters will adversely affect the Company, its results of operations, financial condition and cash flows.

NAMENDA XR/Namzaric Qui Tam Litigation

On April 1, 2019, Adamas was served with a complaint filed in the United States District Court for the Northern District of California (the District Court) (Case No. 3:18-cv-03018-JCS) against it and several Allergan entities alleging violations of federal and state false claims acts (FCA) in connection with the commercialization of NAMENDA XR and Namzaric by Allergan. The lawsuit is a qui tam complaint brought by an individual, asserting rights of the federal government and various state governments. The lawsuit was originally filed in May 2018 under seal, and Adamas became aware of the lawsuit when it was served. The complaint alleges that patents held by Allergan and Adamas covering NAMENDA XR and Namzaric were procured through fraud on the United States Patent and Trademark Office and that these patents were asserted against potential generic manufacturers of NAMENDA XR and Namzaric to prevent the generic manufacturers from entering the market, thereby wrongfully excluding generic competition resulting in artificially high price being charged to government payors. Adamas' patents in question were licensed exclusively to Forest Laboratories Holdings Limited. The complaint includes a claim for damages of "potentially more than $2.5 billion dollars," treble damages and statutory penalties. To date the federal and state governments have declined to intervene in this action. This case is currently stayed pending Adamas's and Allergan's interlocutory appeal of the District Court's December 11, 2020 order denying Adamas's and Allergan's motion to dismiss the complaint. The appeal was heard by the United States Court of Appeals for the Ninth Circuit (Case No. 21-80005). Argument was held on January 10, 2022. On August 25, 2022, the Ninth Circuit sided with the defendants by reversing the District Court’s public disclosure bar rulings and remanding the case back to the District Court to decide certain issues in the first instance. On October 11, 2022, the plaintiff filed a petition for rehearing with the Ninth Circuit which was denied on November 3, 2022. On December 23, 2022, the defendants filed renewed motions to dismiss directed to the remaining unresolved issue. On March 20, 2023, the District Court entered an order and final judgment dismissing with prejudice Silbersher’s Federal False Claims Act claim while declining to exercise supplemental jurisdiction over the state false claims act claims which were dismissed without prejudice. On April 19, 2023, the plaintiff appealed the District Court's dismissal of the Federal False Claims Act claim.

24

APOKYN Litigation

On October 3, 2022, Sage Chemical, Inc. and TruPharma, LLC filed a lawsuit in the United States District Court for the District of Delaware (Case No.22-cv-1302) alleging that Supernus Pharmaceuticals, Inc., Britannia Pharmaceuticals Limited, and US WorldMeds Partners, LLC violated state and federal antitrust law in connection with APOKYN. On January 10, 2023, the Company filed motions to dismiss all claims. On January 25, 2023, Defendants filed a motion to stay discovery and stay the deadline to submit a proposed scheduling order pending resolutions of Defendants’ motions to dismiss. On March 7, 2023, the Court denied the Company's motion to stay and ordered that the parties commence discovery. On April 10, 2023, the Court issued a scheduling order that provides for a Pretrial Conference on March 7, 2025 and a jury trial beginning on March 24, 2025. Pretrial discovery is ongoing as the date of this letter. The Company intends to defend itself vigorously. However, the Company can offer no assurances that it will be successful in a litigation.

Apotex Settlement and License Agreements

The Company entered into a settlement and license agreements dated June 21, 2023 with Apotex Inc. to settle ongoing patent litigation regarding Apotex ANDA filings seeking approval to market a generic version of the Company's 150mg, 300mg, and 600mg strength Oxtellar XR (extended-release oxcarbazepine) tablets in September 2024, or sooner under certain conditions.

25

16. Subsequent Events

26

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Management’s Discussion and Analysis of Financial Condition and Results of Operations is intended to help the reader understand the results of operations and the financial condition of Supernus Pharmaceuticals, Inc. The interim condensed consolidated financial statements included in this report and this Management’s Discussion and Analysis of Financial Condition and Results of Operations should be read in conjunction with our audited consolidated financial statements and notes thereto for the year ended December 31, 2022 and the related Management’s Discussion and Analysis of Financial Condition and Results of Operations, both of which are contained in our Annual Report on Form 10-K, filed with the Securities and Exchange Commission on March 9, 2023.

In addition to historical information, this Quarterly Report on Form 10-Q contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, which are intended to be covered by the safe harbors created thereby. These forward-looking statements may include declarations regarding the Company’s belief or current expectations of management, such as statements including the words “budgeted,” “anticipate,” “project,” “forecast,” “estimate,” “expect,” “may,” “believe,” “potential,” and similar statements or expressions, which are intended to be among the statements that are forward-looking statements, as such statements reflect the reality of risk and uncertainty that is inherent in our business. Actual results may differ materially from those expressed or implied by such forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements, which are made as of the date this report was filed with the Securities and Exchange Commission. Our actual results and the timing of events could differ materially from those discussed in our forward-looking statements because of many factors, including those set forth under the “Risk Factors” section of our Annual Report on Form 10-K and elsewhere in this report as well as in other reports and documents we file with the Securities and Exchange Commission from time to time. Except as required by law, we undertake no obligation to update any forward-looking statements to reflect events or circumstances occurring after the date of this Quarterly Report on Form 10-Q.

Unless the content requires otherwise, the words "Supernus," "we," "our" and "the Company" refer to Supernus Pharmaceuticals, Inc. and/or one or more of its subsidiaries, as the case may be. These terms are used solely for the convenience of the reader. Supernus Pharmaceuticals, Inc. and each of its subsidiaries are distinct legal entities. For example, MDD US Operations, LLC, a wholly-owned indirect subsidiary of Supernus Pharmaceuticals, Inc., is the exclusive licensee and distributor of APOKYN in the United States and its territories. Adamas Operations, LLC, a wholly-owned indirect subsidiary of Supernus Pharmaceuticals, Inc., wholly owns the patents and patent applications related to GOCOVRI and Osmolex ER and has a license agreement with Supernus Pharmaceuticals, Inc., granting Supernus Pharmaceuticals, Inc. rights to market and sell GOCOVRI and Osmolex ER.

Solely for convenience, in this Quarterly Report on Form 10-Q, the trade names are referred to without the TM symbols and the trademark registrations are referred to without the circled R, but such references should not be construed as any indicator that the Company will not assert, to the fullest extent under applicable law, our rights thereto.

27

Overview

We are a biopharmaceutical company focused on developing and commercializing products for the treatment of central nervous system (CNS) diseases. Our diverse neuroscience portfolio includes approved treatments for epilepsy, migraine, attention-deficit hyperactivity disorder (ADHD), hypomobility in Parkinson’s Disease (PD), cervical dystonia, chronic sialorrhea, dyskinesia in PD patients receiving levodopa-based therapy, and drug-induced extrapyramidal reactions in adult patients. We are developing a broad range of novel CNS product candidates including new potential treatments for hypomobility in PD, epilepsy, depression, and other CNS disorders.

Commercial Products

•Qelbree® (viloxazine extended-release capsules) is a novel non-stimulant product indicated for the treatment of ADHD in adults and pediatric patients 6 years and older. The United States Food and Drug Administration (FDA) approved Qelbree for the treatment of ADHD in pediatric patients 6 to 17 years of age in April 2021, and in adult patients in April 2022. The Company launched Qelbree for pediatric patients in May 2021 and for adult patients in May 2022 in the United States (U.S.).

•GOCOVRI® (amantadine) extended-release capsules is the first and only FDA approved medicine indicated for the treatment of dyskinesia in patients with PD receiving levodopa-based therapy, with or without concomitant dopaminergic medications, and as an adjunctive treatment to levodopa/carbidopa with PD experiencing "off" episodes.

•Trokendi XR® (topiramate) is the first once-daily extended-release topiramate product indicated for the treatment of epilepsy in patients 6 years of age and older in the U.S. market. It is also indicated for the prophylaxis of migraine headache in adults and adolescents 12 years and older.

•Oxtellar XR® (oxcarbazepine) is indicated as therapy for the treatment of partial onset seizures in patients 6 years of age and older. It is also the first once-daily extended-release oxcarbazepine product indicated for the treatment of epilepsy in the U.S. market.

•APOKYN® (apomorphine hydrochloride injection) is a product indicated for the acute, intermittent treatment of hypomobility, "off" episodes ("end-of-dose wearing off" and unpredictable "on/off" episodes) in patients with advanced PD.

•XADAGO® (safinamide) is a once-daily product indicated as adjunctive treatment to levodopa/carbidopa in patients with PD experiencing "off" episodes.

•Osmolex ER® (amantadine) extended-release tablets is for the treatment of PD and drug-induced extrapyramidal reactions in adult patients.

•MYOBLOC® (rimabotulinumtoxinB injection) is a product indicated for the treatment of cervical dystonia and chronic sialorrhea in adults. It is the only botulinum toxin type B available on the market.

28

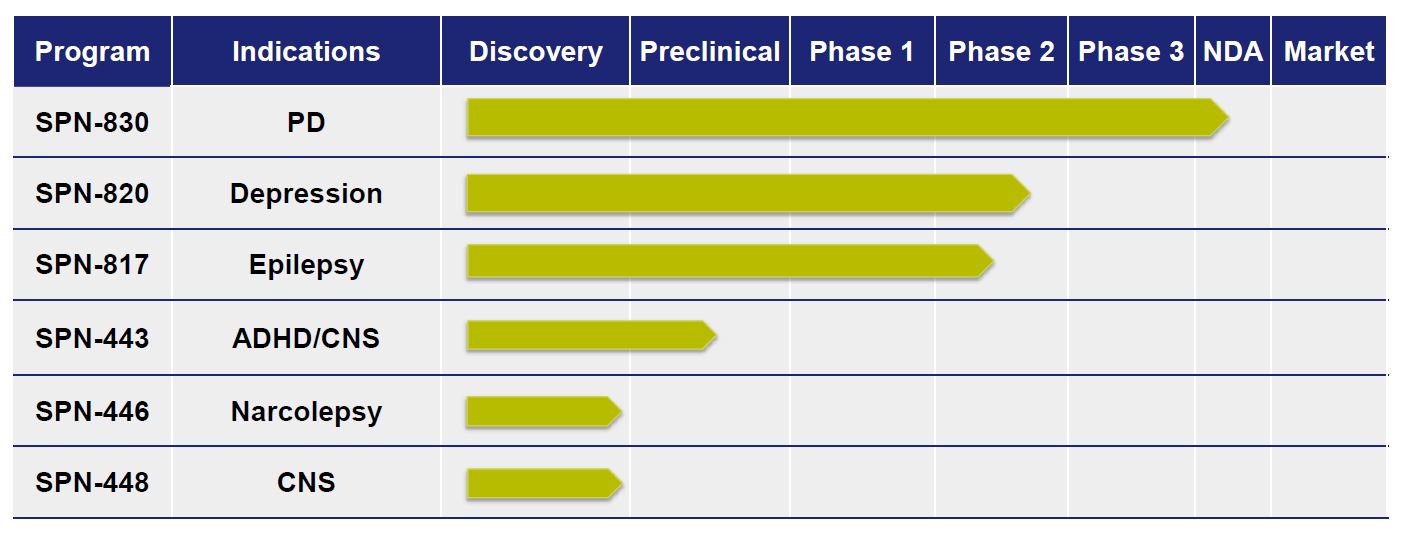

Research and Development

We are committed to the development of innovative product candidates in neurology and psychiatry, including the following:

SPN-830 (apomorphine infusion device) for treatment of PD

SPN-830 is a late-stage drug/device combination product candidate for the continuous treatment of motor fluctuations ("off" episodes) in PD patients that are not adequately controlled with oral levodopa and one or more adjunct PD medications. If approved, it would be the only continuous infusion of apomorphine available in the U.S. and an important step for PD patients that would have otherwise been candidates for potentially invasive surgical procedures, such as deep brain stimulation. Continuous slow infusion may also limit some of the side effects of a bolus injection of apomorphine.