UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form | ||

(Mark One)

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the quarterly period ended March 31, 2021

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission File Number: 001-33784

| (Exact name of registrant as specified in its charter) | ||||||||

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

(Address of principal executive offices) | (Zip Code) | |||||||

Registrant’s telephone number, including area code: (405 ) 429-5500

Former name, former address and former fiscal year, if changed since last report: Not applicable

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||||||||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||||||||||

☑ | Smaller reporting company | |||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No þ

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13, or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ☑ No o

The number of shares outstanding of the registrant’s common stock, par value $0.001 per share, as of the close of business on May 6, 2021, was 36,506,907 .

References in this report to the “Company,” “SandRidge,” “we,” “our,” and “us” mean SandRidge Energy, Inc., including its consolidated subsidiaries and its proportionately consolidated share of SandRidge Mississippian Trust I and SandRidge Mississippian Trust II, (collectively, the “Royalty Trusts”).

DISCLOSURES REGARDING FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q (“Quarterly Report”) of the Company includes “forward-looking statements” as defined by the SEC. These forward-looking statements may include projections and estimates concerning our capital expenditures, liquidity, capital resources and debt profile, the timing and success of specific projects, the impact of the COVID-19 pandemic, the potential impact of international negotiations on the supply and demand of oil and gas, outcomes and effects of litigation, claims and disputes, elements of our business strategy, compliance with governmental regulation of the oil and natural gas industry, including environmental regulations, acquisitions and divestitures and the potential effects on our financial condition and other statements concerning our operations, financial performance and financial condition.

Forward-looking statements are generally accompanied by words such as “estimate,” “assume,” “target,” “project,” “predict,” “believe,” “expect,” “anticipate,” “potential,” “could,” “may,” “foresee,” “plan,” “goal,” “should,” “intend” or other words that convey the uncertainty of future events or outcomes. These forward-looking statements are based on certain assumptions and analyses based on our experience and perception of historical trends, current conditions and expected future developments as well as other factors we believe are appropriate under the circumstances. Such statements are not guarantees of future performance and actual results or developments may differ materially from those projected. The Company disclaims any obligation to update or revise these forward-looking statements unless required by law, and it cautions readers not to rely on them unduly. While we consider these expectations and assumptions to be reasonable, they are inherently subject to significant business, economic, competitive, regulatory and other risks, contingencies and uncertainties relating to, among other matters, the risks and uncertainties discussed in “Risk Factors” in Item 1A of the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2020 (the “2020 Form 10-K”) and in Item 1A of this Quarterly Report.

SANDRIDGE ENERGY, INC. AND SUBSIDIARIES

FORM 10-Q

Quarter Ended March 31, 2021

INDEX

ITEM 1. | ||||||||

ITEM 2. | ||||||||

ITEM 3. | ||||||||

ITEM 4. | ||||||||

ITEM 1. | ||||||||

ITEM 1A. | ||||||||

ITEM 2. | ||||||||

ITEM 3. | ||||||||

| ITEM 4. | ||||||||

| ITEM 5. | ||||||||

ITEM 6. | ||||||||

PART I. Financial Information

ITEM 1. Financial Statements

SANDRIDGE ENERGY, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS (Unaudited)

(In thousands)

| March 31, 2021 | December 31, 2020 | ||||||||||

ASSETS | |||||||||||

| Current assets | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Restricted cash - other | |||||||||||

| Accounts receivable, net | |||||||||||

| Prepaid expenses | |||||||||||

| Other current assets | |||||||||||

| Total current assets | |||||||||||

| Oil and natural gas properties, using full cost method of accounting | |||||||||||

| Proved | |||||||||||

| Unproved | |||||||||||

| Less: accumulated depreciation, depletion and impairment | ( | ( | |||||||||

| Other property, plant and equipment, net | |||||||||||

| Other assets | |||||||||||

| Total assets | $ | $ | |||||||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | |||||||||||

| Current liabilities | |||||||||||

| Accounts payable and accrued expenses | $ | $ | |||||||||

| Asset retirement obligation | |||||||||||

| Other current liabilities | |||||||||||

| Total current liabilities | |||||||||||

| Long-term debt | |||||||||||

| Asset retirement obligation | |||||||||||

| Other long-term obligations | |||||||||||

| Total liabilities | |||||||||||

Commitments and contingencies (Note 9) | |||||||||||

| Stockholders’ Equity | |||||||||||

Common stock, $ | |||||||||||

| Warrants | |||||||||||

| Additional paid-in capital | |||||||||||

| Accumulated deficit | ( | ( | |||||||||

| Total stockholders’ equity | |||||||||||

| Total liabilities and stockholders’ equity | $ | $ | |||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

4

SANDRIDGE ENERGY, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (Unaudited)

(In thousands, except per share data)

| Three Months Ended March 31, | |||||||||||

| 2021 | 2020 | ||||||||||

| Revenues | |||||||||||

| Oil, natural gas and NGL | $ | $ | |||||||||

| Other | |||||||||||

| Total revenues | |||||||||||

| Expenses | |||||||||||

| Lease operating expenses | |||||||||||

| Production, ad valorem, and other taxes | |||||||||||

| Depreciation and depletion — oil and natural gas | |||||||||||

| Depreciation and amortization — other | |||||||||||

| Impairment | |||||||||||

| General and administrative | |||||||||||

| Restructuring expenses | |||||||||||

| Employee termination benefits | |||||||||||

| (Gain) loss on derivative contracts | ( | ||||||||||

| (Gain) loss on sale of assets | ( | ||||||||||

| Other operating (income) expense, net | ( | ||||||||||

| Total expenses | ( | ||||||||||

| Income (loss) from operations | ( | ||||||||||

| Other income (expense) | |||||||||||

| Interest expense, net | ( | ( | |||||||||

| Other income (expense), net | |||||||||||

| Total other income (expense) | ( | ( | |||||||||

| Income (loss) before income taxes | ( | ||||||||||

| Income tax expense (benefit) | ( | ||||||||||

| Net income (loss) | $ | $ | ( | ||||||||

| Net income (loss) per share | |||||||||||

| Basic | $ | $ | ( | ||||||||

| Diluted | $ | $ | ( | ||||||||

| Weighted average number of common shares outstanding | |||||||||||

| Basic | |||||||||||

| Diluted | |||||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

5

SANDRIDGE ENERGY, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENT OF CHANGES IN STOCKHOLDERS’ EQUITY (Unaudited)

(In thousands)

Common Stock | Warrants | Additional Paid-In Capital | Accumulated Deficit | Total | ||||||||||||||||||||||||||||||||||||||||

Shares | Amount | Shares | Amount | |||||||||||||||||||||||||||||||||||||||||

| Three Months Ended March 31, 2021 | ||||||||||||||||||||||||||||||||||||||||||||

Balance at December 31, 2020 | $ | $ | $ | $ | ( | $ | ||||||||||||||||||||||||||||||||||||||

| Issuance of stock awards, net of cancellations | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||

| Issuance of common stock for general unsecured claims | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||

| Issuance of warrants for general unsecured claims | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||

| Cash paid for tax obligations on vested stock awards | — | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||||||||||

Net Income | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||

| Balance at March 31, 2021 | $ | $ | $ | $ | ( | $ | ||||||||||||||||||||||||||||||||||||||

Common Stock | Warrants | Additional Paid-In Capital | Accumulated Deficit | Total | ||||||||||||||||||||||||||||||||||||||||

Shares | Amount | Shares | Amount | |||||||||||||||||||||||||||||||||||||||||

| Three Months Ended March 31, 2020 | ||||||||||||||||||||||||||||||||||||||||||||

| Balance at December 31, 2019 | $ | $ | $ | $ | ( | $ | ||||||||||||||||||||||||||||||||||||||

| Common stock issued for general unsecured claims | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||

| Stock-based compensation | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||

| Issuance of warrants for general unsecured claims | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||

| Cash paid for tax obligations on vested stock awards | — | — | — | — | ( | — | ( | |||||||||||||||||||||||||||||||||||||

Net loss | — | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||||||

Balance at March 31, 2020 | $ | $ | $ | $ | ( | $ | ||||||||||||||||||||||||||||||||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

6

SANDRIDGE ENERGY, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (Unaudited)

(In thousands)

| Three Months Ended March 31, | |||||||||||

| 2021 | 2020 | ||||||||||

| CASH FLOWS FROM OPERATING ACTIVITIES | |||||||||||

| Net income (loss) | $ | $ | ( | ||||||||

| Adjustments to reconcile net loss to net cash provided by operating activities | |||||||||||

| Provision for doubtful accounts | |||||||||||

| Depreciation, depletion, and amortization | |||||||||||

| Impairment | |||||||||||

| Debt issuance costs amortization | |||||||||||

| (Gain) loss on derivative contracts | ( | ||||||||||

| Cash received on settlement of derivative contracts | |||||||||||

| Gain on sale of assets | ( | ||||||||||

| Stock-based compensation | |||||||||||

| Other | |||||||||||

| Changes in operating assets and liabilities | ( | ||||||||||

| Net cash provided by (used in) operating activities | |||||||||||

| CASH FLOWS FROM INVESTING ACTIVITIES | |||||||||||

| Capital expenditures for property, plant and equipment | ( | ( | |||||||||

| Purchase of other property and equipment | ( | ||||||||||

| Proceeds from sale of assets | |||||||||||

| Net cash provided by (used in) investing activities | ( | ||||||||||

| CASH FLOWS FROM FINANCING ACTIVITIES | |||||||||||

| Proceeds from borrowings | |||||||||||

| Repayments of borrowings | ( | ||||||||||

| Reduction of financing lease liability | ( | ( | |||||||||

| Debt issuance costs | ( | ||||||||||

| Cash paid for tax obligations on vested stock awards | ( | ( | |||||||||

| Net cash provided by (used in) financing activities | ( | ( | |||||||||

| NET INCREASE (DECREASE) IN CASH, CASH EQUIVALENTS and RESTRICTED CASH | |||||||||||

| CASH, CASH EQUIVALENTS and RESTRICTED CASH, beginning of year | |||||||||||

| CASH, CASH EQUIVALENTS and RESTRICTED CASH, end of period | $ | $ | |||||||||

| Supplemental Disclosure of Cash Flow Information | |||||||||||

| Cash paid for interest, net of amounts capitalized | $ | ( | $ | ( | |||||||

| Cash received for income taxes | $ | $ | |||||||||

| Supplemental Disclosure of Noncash Investing and Financing Activities | |||||||||||

| Purchase of PP&E in accounts payable | $ | $ | |||||||||

| Right-of-use assets obtained in exchange for financing lease obligations | $ | $ | |||||||||

| Carrying value of properties exchanged | $ | $ | |||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

7

SANDRIDGE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited)

1. Basis of Presentation

Use of Estimates. The preparation of the unaudited condensed consolidated financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period.

The more significant areas requiring the use of assumptions, judgments and estimates include: oil, natural gas and natural gas liquids (“NGL”) reserves; impairment tests of long-lived assets; the carrying value of unproved oil and natural gas properties; depreciation, depletion and amortization; asset retirement obligations; determinations of significant alterations to the full cost pool and related estimates of fair value used to allocate the full cost pool net book value to divested properties, as necessary; valuation allowances for deferred tax assets; income taxes; valuation of derivative instruments; contingencies; and accrued revenue and related receivables. Although management believes the estimates used in the areas noted above are reasonable, actual results could differ significantly from those estimates.

Going Concern Consideration. The accompanying condensed consolidated financial statements are prepared in accordance with generally accepted accounting principles applicable to a going concern, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business.

8

SANDRIDGE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - CONTINUED

(Unaudited)

2. Fair Value Measurements

The Company measures and reports certain assets and liabilities on a fair value basis and has classified and disclosed its fair value measurements using the levels of the fair value hierarchy noted below. The carrying values of cash, restricted cash, accounts receivable, prepaid expenses, certain other current and non-current assets, accounts payable and accrued expenses, and other current liabilities and other long-term obligations included in the unaudited condensed consolidated balance sheets approximated fair value at March 31, 2021 and December 31, 2020. Additionally, the carrying amount of debt associated with borrowings outstanding under the credit facility dated November 30, 2020 ("New Credit Facility") approximates fair value as borrowings bear interest at variable rates. As a result, these financial assets and liabilities are not discussed below.

| Level 1 | Unadjusted quoted prices in active markets that are accessible at the measurement date for identical, unrestricted assets or liabilities. | ||||

| Level 2 | Quoted prices in markets that are not active, or inputs which are observable, either directly or indirectly, for substantially the full term of the asset or liability. | ||||

| Level 3 | Measurement based on prices or valuation models that require inputs that are both significant to the fair value measurement and less observable from objective sources (i.e., supported by little or no market activity). | ||||

Assets and liabilities that are measured at fair value are classified based on the lowest level of input that is significant to the fair value measurement. The Company’s assessment of the significance of a particular input to the fair value measurement requires judgment, which may affect the valuation of the fair value of assets and liabilities and their placement within the fair value hierarchy levels. The determination of the fair values, stated below, considers the market for the Company’s financial assets and liabilities, the associated credit risk and other factors. The Company considers active markets as those in which transactions for the assets or liabilities occur in sufficient frequency and volume to provide pricing information on an ongoing basis.

Level 2 Fair Value Measurements

Commodity Derivative Contracts. As applicable, the fair values of the Company’s oil and natural gas fixed price swaps are based upon inputs that are either readily available in the public market, such as oil and natural gas futures prices, volatility factors and discount rates, or can be corroborated from active markets. Fair value is determined through the use of a discounted cash flow model or option pricing model using the applicable inputs discussed above. The Company applies a weighted average credit default risk rating factor for its counterparties or gives effect to its credit default risk rating, as applicable, in determining the fair value of these derivative contracts. Credit default risk ratings are based on current published credit default swap rates.

Fair Value - Recurring Measurement Basis

There were no

Transfers. The Company did not have any transfers between Level 1, Level 2 or Level 3 fair value measurements during the three-month periods ended March 31, 2021 and 2020.

3. Derivatives

Commodity Derivatives

The Company is exposed to commodity price risk, which impacts the predictability of its cash flows from the sale of oil and natural gas. On occasion, the Company has attempted to manage this risk on a portion of its forecasted oil or natural gas production sales through the use of commodity derivative contracts. There were no

9

SANDRIDGE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - CONTINUED

(Unaudited)

The following table summarizes derivative activity for the three-month periods ended March 31, 2021, and 2020 (in thousands):

| Three Months Ended March 31, | |||||||||||

| 2021 | 2020 | ||||||||||

| (Gain) loss on commodity derivative contracts | $ | $ | ( | ||||||||

| Cash received on settlements | $ | $ | ( | ||||||||

Master Netting Agreements and the Right of Offset. As applicable, The Company historically had master netting agreements with all of its commodity derivative counterparties and has presented its derivative assets and liabilities with the same counterparty on a net basis in the unaudited condensed consolidated balance sheets. As a result of the netting provisions, the Company's maximum amount of loss under commodity derivative transactions due to credit risk is limited to the net amounts due from its counterparties. There were no

Because we did not designate any of our derivative contracts as hedges for accounting purposes, changes in the fair value of our derivative contracts were recognized as gains and losses in current period earnings. As a result, and as applicable, our current period earnings could have been significantly affected by changes in the fair value of our commodity derivative contracts. Changes in fair value were principally measured based on a comparison of future prices to the contract price at the end of the period.

4. Property, Plant and Equipment

| March 31, 2021 | December 31, 2020 | ||||||||||

Oil and natural gas properties | |||||||||||

Proved | $ | $ | |||||||||

Unproved | |||||||||||

Total oil and natural gas properties | |||||||||||

Less accumulated depreciation, depletion and impairment | ( | ( | |||||||||

Net oil and natural gas properties | |||||||||||

| Land | |||||||||||

| Electrical infrastructure | |||||||||||

| Other non-oil and natural gas equipment | |||||||||||

| Buildings and structures | |||||||||||

| Financing leases | |||||||||||

| Total | |||||||||||

Less accumulated depreciation and amortization | ( | ( | |||||||||

Other property, plant and equipment, net | |||||||||||

Total property, plant and equipment, net | $ | $ | |||||||||

See Note 5 for discussion of impairment of property, plant and equipment.

5. Impairment

10

SANDRIDGE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - CONTINUED

(Unaudited)

by comparing the carrying values of the assets to their estimated fair values. The full cost pool ceiling limitation and estimated fair values of midstream and other assets were determined in accordance with the policies discussed in Note 1 as applicable.

In the three-month period ended March 31, 2021, we did not record a full cost ceiling limitation impairment charge. The Company recorded a full cost ceiling limitation impairment of $8.0 million for the three-month period ended March 31, 2020, which resulted from various factors including a decrease in the trailing twelve-month weighted average natural gas price in the first quarter of 2020.

6. Acquisitions and Divestitures

North Park Basin Sale

On February 5, 2021, the Company sold all of its oil and natural gas properties and related assets of the North Park Basin ("NPB"), in Colorado, for a purchase price of $47 million. The sale closed for net proceeds of $39.7 million in cash, which amounts to the purchase price of $47 million net of effective date to close date adjustments. Consequently, the Company allocated a portion of the full cost pool net book value, using the income approach, to the divested oil and gas properties and recognized a reduction of full cost pool assets of $22.0 million and a reduction of $4.6 million to its non-full cost pool assets. As the sale significantly altered the relationship between capitalized costs and proved reserves, the Company recognized a $19.7 million gain related to the assets sold. The gain represents net proceeds of $39.7 million coupled with the release of revenues in suspense of $0.5 million and the relief of asset retirement obligations of $6.1 million offset by the reduction of $26.6 million in oil and gas properties related to NPB.

For the three-months ended March 31, 2021, NPB represented $3.2 million, or 9.4 % of the Company's $33.6 million total consolidated Revenues, NPB represented $0.9 million, or 11.6 % of the Company's $8.0 million consolidated Lease operating expense, it represented $0.2 million, or 11.4 % of the Company's $2.2 million consolidated Production, ad valorem and other taxes and NPB represented 0.1 MMBoe, or 4.1 % of the Company's consolidated total production volumes of 1.6 MMBoe.

For the three-months ended March 31, 2020, NPB represented $12.8 million, or 31.6 % of the Company's $40.3 million total consolidated Revenues, NPB represented $3.5 million or 22.7 % of the Company's $15.6 million consolidated Lease operating expense, it represented $0.8 million, or 24.1 % of the Company's $3.2 million consolidated Production, ad valorem and other taxes and NPB represented 0.3 MMBoe, or 12.8 % of the Company's consolidated total production volumes of 2.6 MMBoe.

7. Accounts Payable and Accrued Expenses

| March 31, 2021 | December 31, 2020 | ||||||||||

| Accounts payable and other accrued expenses | $ | $ | |||||||||

| Production payable | |||||||||||

| Payroll and benefits | |||||||||||

| Taxes payable | |||||||||||

| Drilling advances | |||||||||||

| Accrued interest | |||||||||||

| Total accounts payable and accrued expenses | $ | $ | |||||||||

11

SANDRIDGE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - CONTINUED

(Unaudited)

8. Long-Term Debt

Credit Facility.

Credit Facility. On November 30, 2020 the Company entered into a $30.0 million credit facility with a related party and affiliate of Icahn Enterprises and Icahn Agency Services LLC, as administrative agent. As of March 31, 2021 and December 31, 2020, the Company had a $20.0 million term loan outstanding under the New Credit Facility. The New Credit Facility consists of a $10.0 million revolving loan facility and a $20 million term loan facility. There are no scheduled borrowing base redeterminations under the New Credit Facility. At March 31, 2021, the Company had $10.0 million available to be drawn under the revolving loan facility. The New Credit Facility matures on November 30, 2023.

The outstanding borrowings under the New Credit Facility bear interest at a rate tied to a utilization ratio of (a) LIBOR plus an applicable margin that varies from 200 to 300 basis points or (b) the base rate plus an applicable margin that varies from 100 basis points to 200 basis points. During the three-months ended March 31, 2021, the weighted average interest rate paid for borrowings outstanding under the New Credit Facility was approximately 2.6 %.

The Company has the right to prepay loans under the New Credit Facility at any time without a prepayment penalty, other than customary “breakage” costs with respect to LIBOR loans.

The New Credit Facility is secured by (i) first-priority mortgages on at least 95 % of the PV-9 pricing of the of all proved reserves included in the most recently delivered reserve report of the Company, (ii) a first-priority perfected pledge of substantially all of the capital stock owned by each credit party and (iii) a first-priority security interest in the cash, cash equivalents, deposit, securities and other similar accounts, and a first-priority perfected security interest in substantially all other tangible and intangible assets of the credit parties (including but not limited to as-extracted collateral, accounts receivable, inventory, equipment, general intangibles, investment property, intellectual property, real property and the proceeds of the foregoing).

The New Credit Facility includes events of default and certain customary affirmative and negative covenants. The Company is required maintain certain financial covenants, commencing with the first full quarter ending after the effective date thereof to, maintain (i) a maximum consolidated total net leverage ratio, measured as of the end of any fiscal quarter, of no greater than 3.50 to 1.00 and (ii) a minimum consolidated interest coverage ratio, measured as of the end of any fiscal quarter, of no less than 2.25 to 1.00. As of March 31, 2021, the Company was in compliance with all applicable covenants and had a consolidated total net leverage ratio of (0.18 ) and consolidated interest coverage ratio of 42.86 .

9. Commitments and Contingencies

Legal Proceedings. As previously disclosed, on May 16, 2016, the Company and certain of its direct and indirect subsidiaries (collectively, the “Debtors”) filed voluntary petitions for reorganization under Chapter 11 of the United States Bankruptcy Code in the United States Bankruptcy Court for the Southern District of Texas (the “Bankruptcy Court”). The Bankruptcy Court confirmed the joint plan of organization (the “Plan”) of the Debtors on September 9, 2016, and the Debtors subsequently emerged from bankruptcy on October 4, 2016.

Pursuant to the Plan, claims against the Company were discharged without recovery in each of the following consolidated cases (the “Cases”):

• In re SandRidge Energy, Inc. Securities Litigation, Case No. 5:12-cv-01341-LRW, USDC, Western District of Oklahoma; and

• Ivan Nibur, Lawrence Ross, Jase Luna, Matthew Willenbucher, and the Duane & Virginia Lanier Trust v. SandRidge

Mississippian Trust I, et al., Case No. 5:15-cv-00634-SLP, USDC, Western District of Oklahoma

12

SANDRIDGE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - CONTINUED

(Unaudited)

The lead plaintiffs in both In re SandRidge Energy, Inc. Securities Litigation and Lanier Trust assert claims on behalf of themselves and (i) in In re SandRidge Energy, Inc. Securities Litigation, a class of all purchasers of SandRidge common stock from February 24, 2011 and November 8, 2012 under Sections 10(b) and 20(a) of the Securities Exchange Act of 1934, and Rule 10b-5 promulgated thereunder, and (ii) in Lanier Trust, a putative class of purchasers of SandRidge Mississippian Trust I and SandRidge Mississippian Trust II common units between April 7, 2011 and November 8, 2012 under Sections 11, 12(a)(2), and 15 of the Securities Act of 1933 and Sections 10(b) and 20(a) of the Securities Exchange Act of 1934, and Rule 10b-5 promulgated thereunder, both based on allegations that defendants, which include certain former officers of the Company and the SandRidge Mississippian Trust I, made misrepresentations or omissions concerning various topics including the performance of wells operated by the Company in the Mississippian region.

Discovery in each of the Cases closed on June 19, 2019. Following a hearing on class certification in each of the Cases on September 6, 2019, the court granted class certification in In re SandRidge Energy, Inc. Securities Litigation on September 30, 2019. The motion for class certification in Lanier Trust remains pending. On April 2, 2020, the individual defendants and SandRidge Mississippian Trust I filed motions for summary judgment seeking the dismissal of all claims asserted against them in the Lanier Trust matter. On the same date, the individual defendants filed motions for summary judgment seeking the dismissal of all claims asserted against them In re SandRidge Energy, Inc. Securities Litigation. The motions remain pending.

In each of the Cases, lead plaintiffs seek to recover unspecified damages, interest, costs and expenses incurred in the litigation on behalf of themselves and class members. Although the claims against the Company in each Case have been discharged pursuant to the Plan, the Company remains a nominal defendant. The Company may also be contractually obligated to indemnify two former officers who are defendants and the SandRidge Mississippian Trust I against losses, claims, damages, liabilities and expenses, including reasonable costs of investigation and attorney’s fees and expenses, which it is required to advance, arising out of the Cases, although the Company disputes any such obligations. Such indemnification is not covered by insurance with respect to the Trust. As of October 2020, we have exhausted all remaining insurance coverage for the costs of indemnification and expect no further reimbursements.

In light of the status of the Cases, and the facts, circumstances and legal theories relating thereto, the Company is not able to determine the likelihood of an outcome in either case or provide an estimate of any reasonably possible loss or range of possible loss related thereto. However, considering the exhaustion of insurance coverage available to the Company, such losses, if incurred, could be material. The Company has not established any liabilities relating to the Cases and believes that the plaintiffs’ claims are without merit. The Company intends to continue to vigorously defend against the Cases in its capacity as a nominal defendant.

In addition to the matters described above, the Company is involved in various lawsuits, claims and proceedings, which are being handled and defended by the Company in the ordinary course of business.

13

SANDRIDGE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - CONTINUED

(Unaudited)

10. Income Taxes

For each interim reporting period, the Company estimates the effective tax rate expected for the full fiscal year and uses that estimated rate in providing for income taxes on a current year-to-date basis.

Deferred income taxes are provided to reflect the future tax consequences of temporary differences between the tax basis of assets and liabilities and their reported amounts in the financial statements. The Company’s deferred tax assets have been reduced by a valuation allowance due to a determination that it is more likely than not that some or all of the deferred assets will not be realized based on the weight of all available evidence. The Company continues to closely monitor and weigh all available evidence, including both positive and negative, in making its determination whether to maintain a valuation allowance. As a result of the significant weight placed on the Company's cumulative negative earnings position, the Company continued to maintain a full valuation allowance against its net deferred tax asset at March 31, 2021 and December 31, 2020. As a result, the Company had no federal or state income tax expense or benefit for the three-month period ended March 31, 2021and recorded an insignificant income tax benefit for the year ended December 21, 2020. The benefit is related to previously sequestered alternative minimum tax (AMT) refund amounts released to the Company during 2020. The Company has no remaining AMT credits to be refunded.

Internal Revenue Code (“IRC”) Section 382 addresses company ownership changes and specifically limits the utilization of certain deductions and other tax attributes on an annual basis following an ownership change. As a result of the Chapter 11 reorganization and related transactions, the Company experienced an ownership change within the meaning of IRC Section 382 during 2016 that subjected certain of the Company’s tax attributes, including net operating losses ("NOLs"), to an IRC Section 382 limitation. This limitation has not resulted in cash taxes for any period subsequent to the ownership change. Since the 2016 ownership change, the Company has generated additional NOLs and other tax attributes that are not currently subject to an IRC Section 382 limitation. The Company's ability to use NOLs and other tax attributes to reduce taxable income and income taxes could be materially impacted by a future IRC 382 ownership change. Future transactions involving the Company's stock, including those outside of the Company's control, could cause an IRC 382 ownership change resulting in a limitation on tax attributes currently not limited and a more restrictive limitation on tax attributes currently subject to the previous IRC 382 limitation.

As of March 31, 2021, the Company had approximately $1.7 billion of federal NOL carryforwards, net of NOLs expected to expire unused due to the 2016 IRC Section 382 limitation. Of the $1.7 billion of federal NOL carryforwards, $0.8 billion expire during the years 2025 through 2037, while $0.9 billion do not have an expiration date. Additionally, the Company had federal tax credits in excess of $33.5 million which begin expiring in 2029.

The Company did not have unrecognized tax benefits at March 31, 2021 and December 31, 2020.

The Company’s only taxing jurisdiction is the United States (federal and state). The Company’s tax years 2017 to present remain open for federal examination. Additionally, tax years 2005 through 2017 remain subject to examination for the purpose of determining the amount of federal NOL and other carryforwards. The number of years open for state tax audits varies, depending on the state, but are generally from to five years .

In July 2020, the U.S. Treasury Department released final and proposed regulations on IRC Section 163(j) which limits business interest expense deductions. These regulations apply to tax years beginning January 1, 2021. However, taxpayers may choose to apply these regulations to tax years beginning after December 31, 2017. The Company adopted the final regulations for the year ended December 31, 2020. This does not result in any material impact to the provision.

11. Equity

Common Stock, Performance Share Units, and Stock Options. At March 31, 2021, the Company had approximately 250.0 million shares of common stock authorized, 36.1 0.001 per share, issued and outstanding. Further, at March 31, 2021, the Company had approximately 0.1 million shares of unvested restricted stock awards, 1.5 million shares of unvested restricted stock units, 0.1 million stock options outstanding, and 0.2 million of unvested performance share units.

Warrants. The Company has issued approximately 4.9 million Series A warrants and 2.1 million Series B warrants that are exercisable until October 4, 2022 for one 41.34 and $42.03 per share,

14

SANDRIDGE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - CONTINUED

(Unaudited)

respectively, subject to adjustments pursuant to the terms of the warrants, to certain holders of general unsecured claims as defined in the Plan. The warrants contain customary anti-dilution adjustments in the event of any stock split, reverse stock split, reclassification, stock dividend or other distributions.

The Tax Benefits Preservation Plan. On July 1, 2020, the Board declared a dividend distribution of one right (a “Right”) for each outstanding share of Company common stock, par value $0.001 per share to stockholders of record at the close of business on July 13, 2020. Each Right entitles its holder, under certain circumstances, to purchase from the Company one one-thousandth of a share of Series A Junior Participating Preferred Stock of the Company, par value $0.001 per share, at an exercise price of $5.00 per Right, subject to adjustment. The description and terms of the Rights are set forth in the tax benefits preservation plan, dated as of July 1, 2020, between the Company and American Stock Transfer & Trust Company, LLC, as rights agent (and any successor rights agent, the “Rights Agent”).

The Company adopted the Tax Benefits Preservation Plan, as amended on March 16, 2021, in order to protect shareholder value against a possible limitation on the Company’s ability to use its tax net operating losses (the “NOLs”) and certain other tax benefits to reduce potential future U.S. federal income tax obligations. The NOLs are a valuable to the Company, which may inure to the benefit of the Company and its stockholders. However, if the Company experiences an “ownership change,” as defined in Section 382 of the Internal Revenue Code of 1986, as amended (the “Code”), its ability to fully utilize the NOLs and certain other tax benefits will be substantially limited and the timing of the usage of the NOLs and such other benefits could be substantially delayed, which could significantly impair the value of those assets. Generally, an “ownership change” occurs if the percentage of the Company’s stock owned by one or more of its “five-percent shareholders” (as such term is defined in Section 382 of the Code) increases by more than 50 percentage points over the lowest percentage of stock owned by such stockholder or stockholders at any time over a three-year period. The Tax Benefits Preservation Plan is intended to prevent against such an “ownership change” by deterring any person or group from acquiring beneficial ownership of 4.9 % or more of the Company’s securities.

Subject to certain exceptions, the Rights become exercisable and trade separately from Common Stock only upon the “Distribution Time,” which occurs upon the earlier of:

•the close of business on the tenth (10th) day after the “Stock Acquisition Date,” which is (a) the first date of public announcement that a person or group of affiliated or associated persons (with certain exceptions, an “Acquiring Person”) has acquired, or obtained the right or obligation to acquire, beneficial ownership of 4.9 % or more of the outstanding shares of Common Stock (with certain exceptions) or (b) such other date, as determined by the Board, on which a person or group has become an Acquiring Person, or

•the close of business on the tenth (10th) business day (or later date as may be determined by the Board prior to such time as any person or group becomes an Acquiring Person) following the commencement of a tender offer or exchange offer which, if consummated, would result in a person or group becoming an Acquiring Person.

Any existing stockholder or group that beneficially owns 4.9 % or more of Common Stock has been grandfathered at its current ownership level, but the Rights will not be exercisable if, at any time after the announcement of the Tax Benefits Preservation Plan, such stockholder or group increases its ownership of Common Stock by one share of Common Stock. Certain synthetic interests in securities created by derivative positions, whether or not such interests are considered to be ownership of the underlying Common Stock or are reportable for purposes of Regulation 13D of the Securities Exchange Act of 1934, as amended, are treated as beneficial ownership of the number of shares of Common Stock equivalent to the economic exposure created by the derivative position, to the extent actual shares of Common Stock are directly or indirectly held by counterparties to the derivatives contracts.

Until the earlier of the Distribution Time and the Expiration Time, the surrender for transfer of any shares of Common Stock will also constitute the transfer of the Rights associated with those shares. As soon as practicable after the Distribution Time, separate rights certificates will be mailed to holders of record of Common Stock as of the close of business on the Distribution Time. From and after the Distribution Time, the separate rights certificates alone will represent the Rights. Except as otherwise provided in the Tax Benefits Preservation Plan, only shares of Common Stock issued prior to the Distribution Time will be issued with Rights. The Rights are not exercisable until the Distribution Time.

The Tax Benefits Preservation Plan will expire on the earliest of: (i) the close of business on the day following the certification of the voting results of the Company’s 2021 annual meeting of stockholders or any prior special meeting of

15

SANDRIDGE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - CONTINUED

(Unaudited)

stockholders, if at such stockholder meeting a proposal to approve this Agreement has not been passed by the affirmative vote of the holders of at least majority of the shares of Common Stock entitled to vote at the 2021 annual meeting of stockholders or any other meeting of the stockholders of the Company duly held prior to such meeting, (ii) the time at which the Rights are redeemed pursuant to the Tax Benefits Preservation Plan, (iii) the time at which the Rights are exchanged pursuant to the Tax Benefits Preservation Plan, (iv) the closing of any merger or other acquisition transaction involving the Company pursuant to an agreement of the type described in Section 13(f) of the Tax Benefits Preservation Plan, at which time, the Rights are terminated, (v) the time at which the Board determines that the NOLs are utilized in all material respects or that an ownership change under Section 382 would not adversely impact in any material respect the time period in which the Company could use the NOLs, or materially impair the amount of the NOLs that could be used by the Company in any particular time period, for applicable tax purposes and (vi) the Close of Business on July 1, 2023 (the earliest of (i), (ii), (iii), (iv), (v), and (vi) being herein referred to as the “Expiration Time”).

In the event that any person or group (other than certain exempt persons) becomes an Acquiring Person (a “Flip-in Event”), each holder of a Right (other than any Acquiring Person and certain related parties, whose Rights automatically become null and void) will have the right to receive, upon exercise, shares of Common Stock having a value equal to two times the exercise price of the Right.

In the event that, at any time following the Stock Acquisition Date, any of the following occurs (each, a “Flip-over Event”):

•the Company consolidates with, or merges with and into, any other entity, and the Company is not the continuing or surviving entity

•any entity engages in a share exchange with or consolidates with, or merges with or into, the Company, and the Company is the continuing or surviving entity and, in connection with such share exchange, consolidation or merger, all or part of the outstanding shares of Common Stock are changed into or exchanged for stock or other securities of any other entity or cash or any other property; or

•the Company sells or otherwise transfers, in one transaction or a series of related transactions, fifty percent (50%) or more of the Company’s assets, cash flow or earning power, each holder of a Right (except Rights which previously have been voided as described above) will have the right to receive, upon exercise, common stock of the acquiring company having a value equal to two times the exercise price of the Right.

12. Revenues

The following table disaggregates the Company’s revenue by source for the three-month periods ended March 31, 2021 and 2020:

| Three Months Ended March 31, | |||||||||||

| 2021 | 2020 | ||||||||||

(In thousands) | |||||||||||

Oil | $ | $ | |||||||||

NGL | |||||||||||

Natural gas | |||||||||||

Other | |||||||||||

Total revenues | $ | $ | |||||||||

16

SANDRIDGE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - CONTINUED

(Unaudited)

Revenues Receivable. The Company records an asset in accounts receivable, net on its consolidated balance sheet for revenues receivable from contracts with customers at the end of each period. Pricing for revenues receivable is estimated using current month crude oil, natural gas and NGL prices, net of deductions. Revenues receivable are typically collected the month after the Company delivers the related production to its customers. As of March 31, 2021, and December 31, 2020, the Company had revenues receivable of $14.2 million and $12.8 million, respectively, and did no

13. Employee Termination Benefits

Certain employees received termination benefits including cash severance and accelerated share-based compensation upon separation of service from the Company as a result of the sale of North Park assets and other employee terminations during the three-month period ended March 31, 2021 and as a result of a reduction in workforce during the three-month period ended March 31, 2020. The following tables presents a summary of employee termination benefits for the three-month periods ended March 31, 2021 and 2020 (in thousands):

Cash | Share-Based Compensation (1) | Number of Shares | Total Employee Termination Benefits | |||||||||||||||||||||||

| Three Months Ended March 31, 2021 | ||||||||||||||||||||||||||

| Executive Employee Termination Benefits | $ | $ | $ | |||||||||||||||||||||||

| Other Employee Termination Benefits | ||||||||||||||||||||||||||

| $ | $ | $ | ||||||||||||||||||||||||

| Three Months Ended March 31, 2020 | ||||||||||||||||||||||||||

| Executive Employee Termination Benefits | $ | $ | $ | |||||||||||||||||||||||

| Other Employee Termination Benefits | ||||||||||||||||||||||||||

| $ | $ | $ | ||||||||||||||||||||||||

____________________

(1) Share-based compensation recognized in connection with the accelerated vesting of restricted stock awards due to the sale of the North Park assets for the three-month period ended March 31, 2021 and as a result of the reduction in workforce for the three-month period ended March 31, 2020. The remaining unrecognized compensation expense associated with these awards at the date of termination was recorded as employee termination benefits. The unrecognized compensation expense was calculated using the grant date fair value for restricted stock awards. One share of the Company’s common stock was issued per restricted stock award.

17

SANDRIDGE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS - CONTINUED

(Unaudited)

14. Earnings (Loss) per Share

The following table summarizes the calculation of weighted average common shares outstanding used in the computation of diluted earnings (loss) per share:

Earnings (Loss) | Weighted Average Shares | Earnings (Loss) Per Share | |||||||||||||||

(In thousands, except per share amounts) | |||||||||||||||||

| Three Months Ended March 31, 2021 | |||||||||||||||||

Basic earnings per share | $ | (1) | $ | ||||||||||||||

| Effect of dilutive securities | |||||||||||||||||

| Restricted stock units | |||||||||||||||||

| Restricted stock awards | |||||||||||||||||

| Performance share units (2) | |||||||||||||||||

| Warrants | |||||||||||||||||

| Stock options | |||||||||||||||||

Diluted earnings per share (3) | $ | $ | |||||||||||||||

| Three Months Ended March 31, 2020 | |||||||||||||||||

| Basic loss per share | $ | ( | $ | ( | |||||||||||||

| Effect of dilutive securities | |||||||||||||||||

| Restricted stock awards | |||||||||||||||||

| Performance share units | |||||||||||||||||

| Warrants | |||||||||||||||||

| Diluted loss per share (4) | $ | ( | $ | ( | |||||||||||||

____________________

(1)Includes 0.2 million of performance share units that are no longer contingently issuable.

(2)The performance share unit awards are contingently issuable and are considered in the calculation of diluted earnings per share. The Company assesses the number of awards that would be issuable, if any, under the terms of the agreement if the end of the reporting period were the end of the contingency period.

(3)The incremental shares of potentially dilutive restricted stock units, restricted stock awards and stock options were included for the three-month periods ended March 31, 2021 as their effect was dilutive under the treasury stock method.

(4)No

15. Subsequent Events

18

ITEM 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Introduction

The following discussion and analysis is intended to help the reader understand our business, financial condition, results of operations, liquidity and capital resources. This discussion and analysis should be read in conjunction with the accompanying unaudited condensed consolidated financial statements and the accompanying notes included in this Quarterly Report, as well as our audited consolidated financial statements and the accompanying notes included in the 2020 Form 10-K. Our discussion and analysis includes the following subjects:

•Overview;

•Consolidated Results of Operations;

•Liquidity and Capital Resources; and

•Critical Accounting Policies and Estimates

The financial information with respect to the three-month periods ended March 31, 2021, and 2020, discussed below, is unaudited. In the opinion of management, this information contains all adjustments, which consist only of normal recurring adjustments unless otherwise disclosed, necessary to state fairly the accompanying unaudited condensed consolidated financial statements. The results of operations for the interim periods are not necessarily indicative of the results of operations for the full fiscal year.

Overview

We are an independent oil and natural gas company with a principal focus on acquisition, development and production activities in the U.S. Mid-Continent. Prior to February 5, 2021, we held assets in the North Park Basin of Colorado, which have been sold in their entirety.

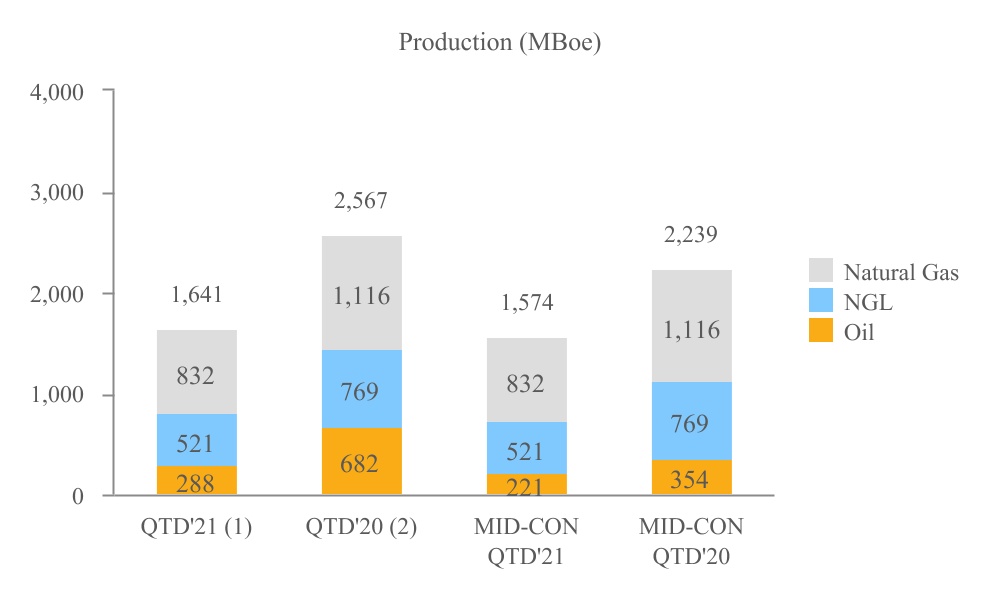

The charts below shows production by product for the three-month periods ended March 31, 2021 and 2020:

(1)For the year three-months ended March 31, 2021, Mid-Continent production was 832 MBoe of natural gas, 521 MBoe of NGLs and 221 MBoe of oil totaling 1,574 MBoe. North Park Basin had 67 MBoe of oil production.

(2)For the year three-months ended March 31, 2020, Mid-Continent production was 1,116 MBoe of natural gas, 769 MBoe of NGLs and 354 MBoe of oil totaling 2,239 MBoe. North Park Basin had 328 MBoe of oil production.

Total production for the three-month periods ended March 31, 2021 was comprised of approximately 17.6% oil, 50.7% natural gas and 31.7% NGLs compared to 26.6% oil, 43.4% natural gas and 30.0% NGLs in 2020.

19

Mid-continent production for the three-months ended March 31, 2021 was comprised of approximately 14.0% oil, 52.9% natural gas and 33.1% NGLs compared to 15.8% oil, 49.9% natural gas and 34.3% NGLs in 2020. The decline in Mid-Continent production was primarily due to pro-active well shut-ins in response to a drop in commodity prices in the second quarter of 2020, as well as regular production declines.

Recent Events

•On April 22, 2021, we announced the acquisition of all the overriding royalty interest assets of SandRidge Mississippian Trust I (the “Trust”). The gross purchase price is $4.9 million (net $3.6 million, given our 26.9% ownership of the Trust).

•On March 3, 2021, we named Mr. Grayson Pranin, formerly its Vice President for Reserves and Engineering, as Senior Vice President and Chief Operating Officer. We also named Mr. Salah Gamoudi, our Chief Financial Officer and Chief Accounting Officer, as a Senior Vice President. We also named Mr. Dean Parrish, formerly our Director of Operations, as our Vice President of Operations.

•On February 5, 2021, we sold all of our oil and natural gas properties and related assets of the North Park Basin ("NPB") in Colorado for a purchase price of $47 million in cash.

Outlook

We will focus on maximizing free cash flow in 2021 through a combination of cost control measures and the continued exercise of financial discipline and prudent capital allocation, which includes limiting our capital projects to projects we believe will provide high rates of return in the current commodity price environment. As a result, our planned capital expenditures for 2021 will be similar to our 2020 levels. Given this expected level of capital expenditures, our oil, natural gas and NGL production will likely decline in 2021. We will consider expanding our capital program after assessing all factors, including commodity prices. We will also continue our pursuit of acquisitions and business combinations which provide high margin properties with attractive returns at current commodity prices.

The COVID-19 pandemic reduced global economic activity and negatively impacted energy demand during the previous twelve months. Demand for oil and natural gas is slowly returning to pre-pandemic levels as COVID-19 vaccination rates and economic activity have increased. Additionally, we have implemented several additional initiatives to maximize free cash flow, reduce our debt level, maximize our liquidity position and, ultimately realize greater shareholder value. These initiatives included personnel and non-personnel cost reductions, along with the sale of the Company's headquarters during 2020. Prior to February 5, 2021, we held assets in the North Park Basin, which have been sold in their entirety.

Consolidated Results of Operations

The majority of our consolidated revenues and cash flow are generated from the production and sale of oil, natural gas and NGLs. Our revenues, profitability and future growth depend substantially on prevailing prices received for our production, the quantity of oil, natural gas and NGLs we produce, and our ability to find and economically develop and produce our reserves. Prices for oil, natural gas and NGLs fluctuate widely and are difficult to predict. To provide information on the general trend in pricing, the average New York Mercantile Exchange "NYMEX" prices for oil and natural gas are shown in the table below:

| Three month periods ended | ||||||||||||||||||||||||||

| March 31, 2021 | December 31, 2020 | September 30, 2020 | June 30, 2020 | |||||||||||||||||||||||

| NYMEX Oil (per Bbl) | $ | 58.09 | $ | 42.58 | $ | 40.92 | $ | 28.00 | ||||||||||||||||||

| NYMEX Natural gas (per MMBtu) | $ | 2.72 | $ | 2.76 | $ | 2.12 | $ | 1.75 | ||||||||||||||||||

In order to reduce our exposure to price fluctuations, we have historically entered into commodity derivative contracts for a portion of our anticipated future oil and natural gas production as discussed in “Item 3. Quantitative and Qualitative Disclosures About Market Risk.” As of March 31, 2021, we had no open commodity derivative contracts and there was no commodity derivative activity during the quarter ended March 31, 2021.

20

Revenues

Consolidated revenues for the three-month periods ended March 31, 2021, and 2020 are presented in the table below (in thousands):

| Three Months Ended March 31, | |||||||||||

| 2021 | 2020 | ||||||||||

| Oil | $ | 15,548 | $ | 28,654 | |||||||

| NGL | 8,856 | 5,934 | |||||||||

| Natural gas | 9,219 | 5,551 | |||||||||

| Other | — | 190 | |||||||||

| Total revenues (1) | $ | 33,623 | $ | 40,329 | |||||||

(1)Mid-Continent represented $30.4 million, or 90.6% and $27.5 million, or 68.4% of total consolidated revenues for the three-months ended March 31, 2021 and 2020, respectively. NPB represented $3.2 million, or 9.4% and $12.8 million, or 31.6% of total consolidated revenues for the three-months ended March 31, 2021 and 2020, respectively.

Oil, Natural Gas and NGL Production and Pricing

The Company's production and pricing information for the three-month periods ended March 31, 2021, and 2020 is shown in the table below:

| Three Months Ended March 31, | |||||||||||

| 2021 | 2020 | ||||||||||

Production data | |||||||||||

| Oil (MBbls) | 288 | 682 | |||||||||

NGL (MBbls) | 521 | 769 | |||||||||

| Natural gas (MMcf) | 4,993 | 6,695 | |||||||||

| Total volumes (MBoe) | 1,641 | 2,567 | |||||||||

| Average daily total volumes (MBoe/d) | 18.2 | 28.2 | |||||||||

| Average prices—as reported (1) | |||||||||||

| Oil (per Bbl) | $ | 53.99 | $ | 42.01 | |||||||

NGL (per Bbl) | $ | 17.00 | $ | 7.72 | |||||||

| Natural gas (per Mcf) | $ | 1.85 | $ | 0.83 | |||||||

| Total (per Boe) | $ | 20.49 | $ | 15.64 | |||||||

Average prices—including impact of derivative contract settlements | |||||||||||

Oil (per Bbl) | $ | 53.99 | $ | 48.01 | |||||||

| NGL (per Bbl) | $ | 17.00 | $ | 7.72 | |||||||

Natural gas (per Mcf) | $ | 1.85 | $ | 0.83 | |||||||

| Total (per Boe) | $ | 20.49 | $ | 17.23 | |||||||

__________________

(1)Prices represent actual average sales prices for the periods presented and do not include effects of derivatives.

21

The table below presents production by area of operation for the three-month periods ended March 31, 2021, and 2020:

| Three Months Ended March 31, | ||||||||||||||||||||||||||

| 2021 | 2020 | |||||||||||||||||||||||||

| Production (MBoe) | % of Total | Production (MBoe) | % of Total | |||||||||||||||||||||||

| Mid-Continent | 1,574 | 95.9 | % | 2,239 | 87.2 | % | ||||||||||||||||||||

| North Park Basin | 67 | 4.1 | % | 328 | 12.8 | % | ||||||||||||||||||||

| Total | 1,641 | 100.0 | % | 2,567 | 100.0 | % | ||||||||||||||||||||

Variances in oil, natural gas and NGL revenues attributable to changes in the average prices received for our production and total production volumes sold for the three-month periods ended March 31, 2021, and 2020 are shown in the table below (in thousands):

| Three Months Ended March 31, 2021 | |||||

| 2020 oil, natural gas and NGL revenues | $ | 40,139 | |||

| Change due to production volumes | $ | (18,972) | |||

| Change due to average prices | $ | 12,456 | |||

| 2021 oil, natural gas and NGL revenues | $ | 33,623 | |||

Revenues from oil, natural gas and NGL sales decreased $6.5 million or 16.2%for the three months ended March 31, 2021 as compared to the three months ended March 31, 2020. Revenue has declined primarily due to the divestiture of the North Park Basin properties and natural production declines in our existing producing wells in the Mid-Continent partially offset by increased realized commodity prices. Mid-Continent represented $30.4 million, or 90.6% and $27.5 million, or 68.4% of total consolidated revenues for the three-months ended March 31, 2021 and 2020, respectively. NPB represented $3.2 million, or 9.4% and $12.8 million, or 31.6% of total consolidated revenues for the three-months ended March 31, 2021 and 2020, respectively. See "Item 1A—Risk Factors" included in the Company's 2020 Form 10-K for additional discussion of the potential impact these events may have on our future revenues.

Operating Expenses

Operating expenses for the three-month periods ended March 31, 2021, and 2020 consisted of the following (in thousands):

| Three Months Ended March 31, | |||||||||||

| 2021 | 2020 | ||||||||||

| Lease operating expenses | $ | 7,954 | $ | 15,642 | |||||||

| Production, ad valorem, and other taxes | 2,176 | 3,199 | |||||||||

| Depreciation and depletion—oil and natural gas | 2,505 | 24,855 | |||||||||

| Depreciation and amortization—other | 1,494 | 2,634 | |||||||||

| Total operating expenses | $ | 14,129 | $ | 46,330 | |||||||

| Lease operating expenses ($/Boe) | $ | 4.85 | $ | 6.09 | |||||||

| Production, ad valorem, and other taxes ($/Boe) | $ | 1.33 | $ | 1.25 | |||||||

| Depreciation and depletion—oil and natural gas ($/Boe) | $ | 1.53 | $ | 9.68 | |||||||

| Production, ad valorem, and other taxes (% of oil, natural gas, and NGL revenue) | 6.5 | % | 8.0 | % | |||||||

Lease operating expenses decreased by $7.7 million or $1.24/Boe for the three months ended March 31, 2021, as compared to the three months ended March 31, 2020. These decreases primarily resulted from field personnel reductions in force, the sale of NPB and the shut-in of wells that had become uneconomic due to natural production declines. NPB represented $0.9 million, or 11.6% and $3.5 million, or 22.7% of consolidated Lease operating expense for the three months ended March 31, 2021 and 2020, respectively.

22

Production, ad valorem, and other taxes have continued to decrease primarily due to declining production and revenues as discussed above. Further, they have decreased as a percentage of oil, natural gas, and NGL revenue for the three months ended March 31, 2021 as compared to the same period in 2020, primarily due to decreases in ad valorem taxes as a result of credits and deductions earned on production taxes. NPB represented $0.2 million, or 11.4% and $0.8 million, or 24.1% of consolidated Production, ad valorem and other taxes for the three months ended March 31, 2021 and 2020, respectively.

The average depreciation and depletion rate for our oil and natural gas properties for the three months ended March 31, 2021 decreased by $8.15/Boe from the three months ended March 31, 2020. This decrease is primarily due to the sale of the North Park Basin properties and full cost ceiling test impairments recorded during 2020, which lowered the net cost basis of oil and gas properties significantly.

Impairment

We did not record a full cost ceiling limitation impairment during the three months ended March 31, 2021. We recorded a full cost ceiling limitation impairment of $8.0 million during the three months ended March 31, 2020, which resulted from various factors including a decrease in the trailing twelve-month weighted average natural gas price in the first quarter of 2020.

Calculation of the full cost ceiling test is based on, among other factors, trailing twelve-month (“SEC prices”) as adjusted for price differentials and other contractual arrangements. The SEC prices utilized in the calculation of proved reserves included in the full cost ceiling test at March 31, 2021 were $40.01 per barrel of oil and $2.16 per Mcf of natural gas, before price differential adjustments.

Based on the SEC prices over the eleven months ended May 1, 2021, as well as one month of NYMEX strip pricing for June of 2021 as of May 7, 2021 we anticipate the SEC prices utilized in the June 30, 2021 full cost ceiling test may be $49.54 per barrel of oil and $2.44 per Mcf of natural gas, (the "estimated second quarter prices"). Applying these estimated second quarter prices, and holding all other inputs constant to those used in the calculation of our March 31, 2021 ceiling test, we expect that no full cost ceiling limitation impairment is indicated for the second quarter of 2021.

Any actual full cost ceiling limitation impairment recognized in future quarters may fluctuate significantly from projected amounts based on the outcome of numerous other factors such as additional declines in the actual trailing twelve-month SEC prices, lower NGL pricing, changes in estimated future development costs and operating expenses, and other adjustments to our levels of proved reserves. Any such ceiling test impairments in 2021 could be material to our net earnings.

Full cost pool impairments have no impact to our cash flow or liquidity.

Other Operating Expenses

Other operating expenses for the three-month periods ended March 31, 2021, and 2020 consisted of the following (in thousands):

| Three Months Ended March 31, | |||||||||||

| 2021 | 2020 | ||||||||||

| General and administrative | $ | 2,090 | $ | 5,483 | |||||||

| Restructuring expenses | 2,054 | — | |||||||||

| Employee termination benefits | 49 | 3,254 | |||||||||

| (Gain) loss on derivative contracts | — | (10,226) | |||||||||

| (Gain) loss on sale of assets | (19,713) | — | |||||||||

| Other operating (income) expense | (48) | 277 | |||||||||

| Total non-operating expenses | $ | (15,568) | $ | (1,212) | |||||||

General and administrative expenses decreased by $3.4 million for the three months ended March 31, 2021, compared to the same period in 2020. These decreases resulted primarily from a reduction in compensation related costs after completing reductions in force during 2020, significant reductions in information technology and software costs and overhead related to the Company's previously held corporate headquarters building. Part of the decrease is also due to reductions in professional costs such as legal expenses, audit fees and consulting services. General and administrative expenses for the first three months of 2021 were impacted by a refund of a $0.4 million legal retainer related to prior periods.

23

Restructuring expenses represent fees and costs associated with the 2016 bankruptcy and exit from North Park Basin in Colorado. Restructuring expenses included payments of $1.3 million to settle general unsecured claims related to our 2016 bankruptcy during the quarter ended March 31, 2021.

Employee termination benefits for the three-month periods ended March 31, 2021 and 2020 include cash and share-based severance costs incurred for the reduction in force, sale of NPB and other employee terminations in the relevant periods. See “Note 12 - Employee Termination Benefits” in the accompanying unaudited condensed consolidated financial statements for additional discussion of these expenses.

The following table summarizes derivative activity for the three-month periods ended March 31, 2021, and 2020 (in thousands):

| Three Months Ended March 31, | |||||||||||

| 2021 | 2020 | ||||||||||

| (Gain) loss on commodity derivative contracts | $ | — | $ | (10,226) | |||||||

| Cash (received) paid on settlements | $ | — | $ | (4,087) | |||||||

There were no open commodity derivative contracts during the three months ended March 31, 2021. As applicable, our derivative contracts were not designated as accounting hedges and, as a result, changes in their fair values were recorded each quarter as a component of operating expenses. Internally, management has historically viewed the settlement of commodity derivative contracts at contractual maturity as adjustments to the price received for oil and natural gas production to determine “effective prices.” In general, cash is received on settlement of contracts due to lower oil and natural gas prices at the time of settlement compared to the contract price for our commodity derivative contracts, and cash is paid on settlement of contracts due to higher oil and natural gas prices at the time of settlement compared to the contract price for our commodity derivative contracts. See further discussion of derivative contracts in “Item 3. Quantitative and Qualitative Disclosures about Market Risk” included in Part I of this Quarterly Report.

Other Income (Expense)

The Company’s other income (expense) for the three-month periods ended March 31, 2021, and 2020 are presented in the table below (in thousands):

| Three Months Ended March 31, | |||||||||||

| 2021 | 2020 | ||||||||||

Other income (expense) | |||||||||||

Interest expense, net | $ | (47) | $ | (637) | |||||||

Other income (expense), net | 28 | 76 | |||||||||

Total other expense | $ | (19) | $ | (561) | |||||||

Interest expense incurred during the three-month period ended March 31, 2021 is primarily comprised of interest paid on the New Credit Facility. Interest expense incurred during the three-month period ended March 31, 2020 is primarily comprised of interest and fees paid on the prior credit facility that was terminated on November 30, 2020. Interest expense is net of amounts capitalized.

Liquidity and Capital Resources

As of March 31, 2021, we had cash and cash equivalents, excluding restricted cash, of $73.9 million. Additionally, we had a $20.0 million term loan outstanding and $10.0 million available under our $30.0 million New Credit Facility, which matures on November 30, 2023. See "Note—8 Long-Term Debt" to the accompanying condensed consolidated financial statements in Item 1 of this report. As of May 7, 2021, we had approximately $81.2 million of cash on hand, excluding restricted cash, $20.0 million outstanding under its term loan facility and no balance outstanding under the $10.0 million revolving loan facility. For the next twelve months, we expect to have ample liquidity with amounts available to be drawn on our New Credit Facility, cash on hand, and cash from operations.

24

Working Capital and Sources and Uses of Cash

Our principal sources of liquidity for the next year include cash flows from operations, cash on hand and amounts available under our New Credit Facility, as discussed in “Note 8—Long-Term Debt” to the accompanying unaudited condensed consolidated financial statements and “Item 1A. Risk Factors” included in Part I of the Company's Form 10-K Report, we expect market volatility factors to have a material, adverse impact on future revenue growth and overall profitability for the foreseeable future.

Our working capital increased to $39.8 million at March 31, 2021, compared to a deficit of $18.1 million at December 31, 2020, the positive impact on working capital resulted primarily from an increase in cash and cash equivalents at March 31, 2021 as a result of proceeds from the sale of NPB and cash from operations. In addition, accounts payable and accrued liabilities decreased due to our continuous cost reduction efforts, the sale of NPB and the timing of payments.

Cash Flows

Our cash flows from operations are substantially dependent on current and future prices for oil and natural gas, which historically have been, and may continue to be, volatile. Cash flows from operations are also affected by timing of cash receipts and disbursements and changes in other working capital assets and liabilities.

Our cash flows for the three-month periods ended March 31, 2021, and 2020 are presented in the following table and discussed below (in thousands):

| Three Months Ended March 31, | |||||||||||

| 2021 | 2020 | ||||||||||

| Cash flows provided by (used in ) operating activities | $ | 14,331 | $ | 18,103 | |||||||

| Cash flows provided by (used in) investing activities | 34,085 | (4,463) | |||||||||

| Cash flows provided by (used in) financing activities | (167) | (11,867) | |||||||||

| Net increase (decrease) in cash and cash equivalents | $ | 48,249 | $ | 1,773 | |||||||

Cash Flows from Operating Activities

The $3.8 million decrease in operating cash flows for the three-month period ended March 31, 2021 compared to the same period in 2020, is primarily due to the declines in revenues, partially offset by reduction in accounts payable and accrued expenses and reductions in expenses due to our cost reduction efforts.

See “—Condensed Consolidated Results of Operations” for further analysis of the changes in revenues and operating expenses, and see “Note 13—Employee Termination Benefits” to the accompanying unaudited condensed consolidated financial statements included in Item 1 of this report for additional detail on cash paid for employee termination benefits.

Cash Flows from Investing Activities

Our cash flows provided in investing activities during the three-month period ended March 31, 2021 primarily reflects $37.2 million of net cash proceeds from the sale of assets offset by capital expenditures of $3.1 million. See "Note 6—Acquisitions and Divestitures" to the accompanying unaudited condensed consolidated financial statements included in Item 1 of this report for additional information.

During the three-month period ended March 31, 2020, cash flows used in investing activities primarily reflects cash payments made for capital expenditures accrued at December 31, 2019.

25

Capital expenditures for the three-month periods ended March 31, 2021, and 2020 are summarized below (in thousands):

| Three Months Ended March 31, | |||||||||||

| 2021 | 2020 | ||||||||||

| Capital Expenditures | |||||||||||

| Drilling, completion and capital workovers | $ | 2,037 | $ | 1,425 | |||||||

| Leasehold and geophysical | 111 | 503 | |||||||||

| Capital expenditures, excluding acquisitions (on an accrual basis) | 2,148 | 1,928 | |||||||||

| Acquisitions | 59 | — | |||||||||

| Capital expenditures, including acquisitions | 2,207 | 1,928 | |||||||||

| Change in capital accruals (1) | 946 | 3,524 | |||||||||

| Total cash paid for capital expenditures | $ | 3,153 | $ | 5,452 | |||||||

__________________

1.Reflects cash paid or adjustments to accruals during the period presented for expenditures related to prior period capital expenditures program.

Cash Flows from Financing Activities

Cash used in financing activities for the three-month period ended March 31, 2021 consisted primarily of finance lease payments and cash paid for tax obligations on vested awards.

Indebtedness

See “Note 8—Long-Term Debt” to the accompanying unaudited condensed consolidated financial statements for additional discussion of the Company's debt at March 31, 2021 and December 31, 2020.

Contractual Obligations and Off-Balance Sheet Arrangements

At March 31, 2021, our contractual obligations included asset retirement obligations, long-term debt obligations and short-term leases and other individually insignificant obligations. Additionally, we have certain financial instruments representing potential commitments that were incurred in the normal course of business to support our operations, including surety bonds. The underlying liabilities insured by these instruments are reflected in our balance sheets, where applicable. Therefore, no additional liability is reflected for the surety bonds or other instruments.

There were no other significant changes in total contractual obligations and off-balance sheet arrangements from those reported in the 2020 Form 10-K.

Critical Accounting Policies and Estimates

For a description of our critical accounting policies and estimates, refer to Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations included in the 2020 Form 10-K. For a discussion of recent accounting pronouncements, newly adopted and recent accounting pronouncements not yet adopted, see “Note 1 - Basis of Presentation” to the accompanying unaudited condensed consolidated financial statements included in Item 1 of this Quarterly Report. We did not have any material changes in critical accounting policies, estimates, judgments and assumptions during the first three months of 2021.

26