UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| [X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2018

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 000-55785

Sun Pacific Holding Corp

(Exact name of registrant as specified in its charter)

| New Jersey | 90-1119774 | |

| (State or other jurisdiction of | (I.R.S. Employer | |

| incorporation or organization) | Identification No.) |

215 Gordon’s Corner Road, Suite 1a

Manalapan NJ 07726

(Address of principal executive offices)

Registrant’s telephone number, including area code: (732) 845-0906

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Exchange Act:

Common Stock, $.0001 par value per share

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act [ ] Yes [X] No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. [ ] Yes [X] No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. [X] Yes [ ] No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). [ ] Yes [X] No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non- accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer”, “non-accelerated filer”, “smaller reporting company” and “emerging growth” in Rule 12b-2 of the Exchange Act.

| Large Accelerated filer [ ] | Accelerated filer [ ] |

| Non-accelerated filer [ ] | Smaller reporting company [X] |

| (do not check if smaller reporting company) | Emerging growth company [X] |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (Section 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s Knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [X] Yes [ ] No

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). [ ] Yes [X] No

As of December 31, 2018, the last business day of the Registrant’s most recently completed fiscal year, the market value of our common stock held by non-affiliates was $346,433, which is based on the closing price of such common equity, as of the last practical business day of the registrant’s most recently completed fiscal year of $0.0106.

The number of shares of the Registrant’s common stock, $0.0001 par value per share, outstanding as of April 3, 2019 was 119,816,697.

TABLE OF CONTENTS

GENERAL INFORMATION

| 2 |

FORWARD-LOOKING STATEMENTS

Certain statements discussed in Item 1 (Business),, Item 3 (Legal Proceedings), Item 7 (Management’s Discussion and Analysis of Financial Condition and Results of Operations and elsewhere in this Annual Report on Form 10-K as well as in other materials and oral statements that the Company releases from time to time to the public constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements concerning management’s expectations, strategic objectives, business prospects, anticipated economic performance and financial condition and other similar matters involve significant known and unknown risks, uncertainties and other important factors that could cause the actual results, performance or achievements of results to differ materially from any future results, performance or achievements discussed or implied by such forward-looking statements. Such risks, uncertainties and other important factors are discussed and Item 7 Management’s Discussion and Analysis of Financial Condition and Results of Operations. In addition, these statements constitute the Company’s cautionary statements under the Private Securities Litigation Reform Act of 1995. It should be understood that it is not possible to predict or identify all such factors. Consequently, the following should not be considered to be a complete discussion of all potential risks or uncertainties. The words “anticipate,” “estimate,” “expect,” “project,” “intend,” “believe,” “plan,” “target,” “forecast” and similar expressions are intended to identify forward-looking statements. Forward-looking statements speak only as of the date of the document in which they are made. The Company disclaims any obligation or undertaking to provide any updates or revisions to any forward-looking statement to reflect any change in the Company’s expectations or any change in events, conditions or circumstances on which the forward-looking statement is based. It is advisable, however, to consult any further disclosures the Company makes on related subjects in its Quarterly Reports on Form 10-Q and Current Reports on Form 8-K filed with the Securities and Exchange Commission.

Emerging Growth Company Status

We are an “emerging growth company,” as defined in the Jumpstart Our Business Startups Act enacted in April 2012, and, for as long as we continue to be an “emerging growth company,” we may choose to take advantage of exemptions from various reporting requirements applicable to other public companies including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements, and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved. We will remain an “emerging growth company” until the earliest of (i) the last day of the fiscal year in which we have total annual gross revenues of $1 billion or more; (ii) the last day of the fiscal year following the fifth anniversary of the date of an initial public offering of our equity securities; (iii) the date on which we have issued more than $1 billion in non-convertible debt during the prior three year period; and (iv) the date on which we are deemed to be a “large accelerated filer.” Pursuant to (ii) above, we will cease to be an emerging growth company effective October 1, 2019.

| 3 |

Company Overview

Utilizing managements history and contacts in general contracting, coupled with our subject matter expertise and intellectual property (“IP”) knowledge of solar panels and other environmentally friendly technologies, Sun Pacific Holding (“the Company”) is focused on building a “Next Generation” green energy company. The Company offers competitively priced “Next Generation” solar panel and lighting products by working closely with design, engineering, integration and installation firms in order to deliver turnkey solar and other energy efficient solutions. We provide solar bus stops, solar trashcans and “street kiosks” that utilize advertising offerings that provide State and local municipalities with costs efficient solutions. We provide general, electrical, and plumbing contracting services to a range of both public and commercials customers in support of our goals of expanding our green energy market reach. In conjunction with these general contracting services and as part of our effort to expand our green energy marketplace, we have recently started the process to develop and build out a Waste to Energy plant in the State of Rhode Island. A facility that we believe may have the ability to handle medical waste in the Northeast Corridor of the United States of America.

Currently, the Company has six (6) subsidiary holdings. Sun Pacific Power Corp which was the initial company that specialized in solar, electrical and general construction, Bella Electric, LLC that in conjunction with the Company operates our electrical contracting work. Bella Electric, LLC is a Pennsylvania limited liability company. The Company also formed Sun Pacific Security Corp., a New Jersey corporation. Currently the Company has not begun operations in the security sector but is reviewing plans to provide residential and commercial security solutions, including installation and monitoring. The Company also formed National Mechanical Group Corp, a New Jersey corporation focused on plumbing operations in the New Jersey and Pennsylvania areas. The Company also formed Street Smart Outdoor Corp, a Wyoming corporation that acts as a holding company for the Company’s state specific operations in unique advertising through solar bus stops, solar trashcans and “street kiosks.” MedRecycler, LLC, is a wholly owned subsidiary duly formed in the state of Nevada. MedRecycler, LLC was created in 2018 to act as a holding company for potential waste to energy projects. MedRecycler, LLC, currently owns 51% of MedRecycler RI, Inc. a Rhode Island Corporation. MedRecycler RI, Inc. was created for the Medical Waste to Energy facility that the Company is attempting to finance and operate in West Warrick, Rhode Island.

As of today, our principal source of revenues is derived from Street Smart Outdoor Corp. operations in the outdoor advertising business with contracts in place in Rhode Island and Tallahassee, Florida, along with some other minor contracting work. We are currently in negotiations with a nationally known outdoor advertising firm to manage and expand our operations, either through a joint venture, partnership, and or a management arrangement as a result of the company’s insufficient working capital and as an option to allow for the expansion of our technologies and or contracts by working with other parties that can bring management expertise and or other resources that may allow us to further optimize our growth strategies.

Sun Pacific Power Corp. continues to make bids for construction projects throughout the Northeast region. However, as of today, we have limited operations in Sun Pacific Power Corp.

Bella Electric, LLC and Sun Pacific Security Corp. have generally ceased operations, but we maintain the subsidiaries in case we find opportunities to relaunch our operations.

| 4 |

MedRecycler, LLC, a wholly owned subsidiary of Sun Pacific Holding Company currently holds fifty one percent (51%) of MedRecycler-RI, Inc., a corporation formed in the state of Rhode Island for the development of waste to energy projects in the state of Rhode Island. Currently, MedRecycler-RI, Inc. has entered into an Indenture of Trust in the amount of $6,025,000.00 as bridge financing for a project in West Warwick, Rhode Island (the “Rhode Island Project”). The original plan was for a facility in Johnston, Rhode Island, but through our negotiations, determined that the West Warwick location was more suitable. The Indenture of Trust has been secured by all equity holdings in MedRecycler-RI, Inc., all personal holdings of equity in the Company held by Nick Campanella, our CEO and member of the Board of Directors. Mr. Campanella has further pledged personal property located in Manapalan in excess of $1,000,000. Payment for the Indenture of Trust is further guaranteed by the Company and Street Smart Outdoor Corp. Currently, MedRecycler-RI, Inc. has entered into a lease agreement in West Warwick, Rhode Island, has taken preliminary steps to order the equipment and is beginning to engage specialists and staff for building out the Rhode Island Project. In order to secure actual operations of the Rhode Island Project, we estimate that MedRecycler-RI, Inc. must still secure a minimum of $14,500,000 in long term financing. MedRecycler-RI, Inc. is currently negotiating with the state of Rhode Island and potential bond financiers to secure the long financing for the Rhode Island Project. Although we anticipate, assuming the long-term financing is secured, the Rhode Island Project may be fully operation as early as the fourth quarter of 2019. Initially, all operational earnings will be earmarked for interest, principal repayment, and the fulfillment of other covenants of the long term financing, As we have not secured long term financing, we can make no statement regarding the long term success of the Rhode Island Project, though, even in a best case scenario, the Rhode Island Project may not be cash flow positive until fully operational and proceeds fulfill covenants under the terms of the yet to be finalized debt financing. Through MeRecycler, LLC, the Company owns fifty-one percent (51%) of MedRecycler-RI, Inc., which was pledged by the Company to Mr. Campanella pursuant to a forbearance agreement related to debts owed to Mr. Campanella. The remaining forty nine percent (49%) of MedRecycler-RI, Inc. is held by Nicholas Campanella, personally, Marmac Corporate Advisors, LLC, and Eilers Law Group, P.A., holding thirty nine percent (39%), eight percent (8%), two percent (2%), respectfully. Mr. Campanella received his ownership as consideration for his personal pledges securing the Indenture of Trust, Marmac Corporate Advisors, LLC and Eilers Law Group, P.A. received their respective ownership as consideration for efforts and services performed. One hundred percent (100%) of the ownership of MedRecycler-RI, Inc. has been pledged to bridge financing, including any pledge rights held by Mr. Campanella in MedRecycler, LLC.

Currently, the Company has been and is insolvent. Over its history and to augment the Company’s strategy, it has sought out partnerships and other arrangements with professionals and companies at the operating subsidiary level to counter its insolvent state. It will continue to look for opportunities that will allow it to partner with others in the form of debt and or equity and other contributions at the subsidiary level, and where possible attempt to keep control of at least fifty one percent (51%) of those subsidiaries. While it will also look for the means to correct its insolvent state at the holding company level, given its current negative economic condition, many parties continue to prefer to work with the Company at an operational subsidiary level. The Company is currently exploring other equity and or debt opportunities to correct its overall insolvent state. Although we continue operations through our subsidiary holdings, revenues generated do not produce cash flows sufficient to meet our basic capital requirements. In order to meet our reporting requirements alone, we will have to seek additional capital through debt or equity financing and/or request deferred payment or other in-kind payments for services. Street Smart Outdoor is undercapitalized making expansion of our advertising products highly unlikely. Neither the Company nor Street Smart Outdoor have secured additional financing to support operations. We are attempting to partner or otherwise develop a capital strategy to allow us to grow the outdoor advertising business that includes financing outdoor structures with other parties, in which we arrange financing arrangements, and we continue to look for other professional organizations that we can partner with in expanding our contracts. Our Rhode Island Project currently represents a liability of over $6,000,000 and has yet to commence. It will require additional financing, we estimate, of not less than $8,500,000 to complete the build out of phase one for the facility and $14,500,000 if you include consolidating the current $6,000,000 short term indenture. We have plans upon the successful launch of our phase one to double the capacity of the facility, which will require additional financing. MedRecycler-RI, Inc. has yet to secure any additional financing. Failure to be successful with Rhode Island Project could lead to bankruptcy of the Company.

Strategic Vision

Our objective is to grow our business profitably as a premier green energy-based provider of both product and services to the public and private sectors. We are working to deploy our strategy in building upon our general and other contracting expertise in conjunction with our intellectual property and subject matter expertise in green energy that may allow us to grow a group of profitable business lines in solar, waste to energy, efficient lighting, and other unique energy related areas.

Recent advances in a multitude of different yet converging technologies have significantly improved the ability to integrate energy efficient products and solutions into infrastructure related projects. These technological advances decrease the requirements needed to jointly operate a multitude of differing assets, devices, and tools that create new ways to integrate evolving new technologies. This technological change and convergence in energy efficient devices, integrated communications among devices, and societal needs to more effectively and environmentally friendly handle the removal of waste, we believe presents a significant opportunity for us in providing and supporting simple to complex integrated solutions.

| 5 |

Our challenges continue to be reaching critical mass in our solar shelter business, expanding into other green energy related projects, completion of the Rhode Island Project and securing operational capital. Except for the bridge financing for the Rhode Island Project, we do not have any existing financing arrangements in place. While the Company has never been adequately funded from inception, the Company has attempted to use debt, equity, and other opportunistic in-kind compensation to further the Company’s strategic vision.

Competition

Our competitive market is made up of a variety of small to large company’s depending upon the area that we are competing within. In the Contracting marketplace they range from a large number of small to large organizations, while in the solar and advertising shelter marketplace it is made up of a smaller amount of direct competitors including JC DeCaoux, Lamar, Clear Chanel, Signal Outdoor, and various others. While the Contractor marketplace we believe is not subject to rapid technological change driven in part by periodic introductions of new technologies we believe the Shelter marketplace and the new areas in Waste to Energy and other green energy marketplace may be subject to more technological change. Given this we believe that the major competitive factors in our marketplace are distinctive technical competencies, governmental certifications and approvals to operate within this space, successful past contract performance, price of services, reputation for quality, and key management personnel with domain expertise.

Marketing and Sales

We currently engage in a limited amount of marketing activities related to request for proposals for projects related to government contracts and or other contracting activities with commercial and private entities. We are developing a variety of new marketing activities designed to broaden our market awareness of our products, services and solutions, that may include e-mail and direct mail campaigns, co-marketing strategies designed to leverage developing strategic relationships, website marketing, topical webcasts, public relations campaigns, speaking engagements and forums and industry analyst visibility initiatives. We plan to participate in and sponsor conferences that cater to our target market and demonstrate and promote our products, services and solutions at trade shows targeted to green energy companies and executives. We also plan to publish white papers relating to green energy projects and develop customer reference programs, such as customer case studies, in an effort to promote better awareness of industry issues and demonstrate that our solutions can address many of the benefits of our solutions.

Our marketing strategy is to build our brand and increase market awareness of our products, services, and solutions in our target markets and to generate qualified sales leads that will allow us to successfully build strong relationships with key decision makers. We plan to use partnerships and other business arrangements to augment our marketing and sales reach in both our outdoor advertising, construction, and waste to energy business.

Clients

We derive a significant amount of our revenues from contracts funded by state governments and large organizations that we provide contracting services for which we act in capacity as the prime contractor, or as a subcontractor. Our client base is located predominantly in the North East region of the U.S. Historically, we have derived, and may continue to derive in the future, a significant percentage of our total revenues from a relatively small number of contracts. Due to the nature of our business and the relative size of certain contracts, which are entered into in the ordinary course of business, the loss of any single significant customer would have a material adverse effect on our results of operations. In future periods, we will continue to focus on diversifying our revenue by increasing the number of our customer contracts and seeking out partnerships that will allow us to increase our customer reach beyond our limited reach.

Intellectual Property

Our intellectual property rights are important to our business. We believe we will come to rely on a combination of patent, copyright, trademark, service mark, trade secret and other rights in the United States and other jurisdictions, as well as confidentiality procedures and contractual provisions to protect our proprietary technology, processes and other intellectual property. We will protect our intellectual property rights in a number of ways including entering into confidentiality and other written agreements with our employees, customers, consultants and partners in an attempt to control access to and distribution of our documentation and other proprietary technology and other information. Despite our efforts to protect our proprietary rights, third parties may, in an unauthorized manner, attempt to use, copy or otherwise obtain and market or distribute our intellectual property rights or technology.

| 6 |

U.S. patent filings are intended to provide the holder with a right to exclude others from making, using, selling or importing in the United States the inventions covered by the claims of granted patents. Our patents, including our pending patents, if granted, may be contested, circumvented or invalidated. Moreover, the rights that may be granted in those issued and pending patents may not provide us with proprietary protection or competitive advantages, and we may not be able to prevent third parties from infringing those patents. Therefore, the exact benefits of our issued patents and, if issued, our pending patents and the other steps that we have taken to protect our intellectual property cannot be predicted with certainty.

Currently, our intellectual property consists of the application for a patent filed by Sun Pacific Power Corp., our wholly owned subsidiary, for a frame-less encapsulated photo-voltaic solar panel construction and method and apparatus for making the same, filed on March 14, 2018.

MedRecycler, LLC has filed for trademark protection for its name and logo. The application is currently pending.

Seasonality

Our business is not seasonal. However, our revenues and operating results may vary significantly from quarter-to-quarter, due to revenues earned on contracts, the commencement and completion of contracts during any particular quarter; as well as the schedule of government agencies awarding contracts, the term of each contract that we have been awarded and general economic conditions. Because a portion of our expenses, such as personnel and facilities costs, are fixed in the short term, successful contract performance and variation in the volume of activity as well as in the number of contracts commenced or completed during any quarter may cause significant variations in operating results from quarter to quarter.

Employees

As of December 31, 2018, we had approximately 10 full-time employees. We periodically engage additional consultants and employ temporary or full-time employees as needed. Potential employees possessing the unique qualifications required are readily available for both part-time and full-time employment. The primary method of soliciting personnel is through recruiting resources directly utilizing all known sources including electronic databases, public forums, and personal networks of friends and former co-workers.

We believe that our future success will depend in part on our continued ability to offer market competitive compensation packages to attract and retain highly skilled, highly motivated and disciplined managerial, technical, sales and support personnel. We generally do not have employment contracts with our employees, but we do selectively maintain employment agreements with key employees. In addition, confidentiality and non-disclosure agreements are in place with many of our customer, employees and consultants and such agreements are included our policies and procedures. None of our employees are subject to a collective bargaining agreement. We believe that our relations with our employees are good.

Corporate Information

The Company was incorporated under the laws of the State of New Jersey on July 28, 2009, as Sun Pacific Power Corporation and together with its subsidiaries, are referred to as the “Company”. On August 24, 2017, the Company entered into an Acquisition Agreement with EXOlifestyle, Inc. whereby the Company became a wholly owned subsidiary of EXOlifestyle, Inc. The acquisition was accounted for as a reverse merger, resulting in the Company being consider the accounting acquirer.

| 7 |

On October 3, 2017, pursuant to the written consent of the majority of the shareholders in lieu of a meeting, Sun Pacific Holding Corp., f/k/a EXOlifestyle, Inc. (the “Company”) filed a Certificate of Amendment with the state of Nevada to change the name of the Company from EXOlifestyle, Inc. to Sun Pacific Holding Corp.

Our principal executive offices are located at 215 Gordon’s Corner Road, Suite 1a, Manalapan NJ 07726. Our internet address www.sunpacificholding.com. Information on our website is not incorporated into this Form 10-K. We make available free of charge through our website our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 as soon as reasonably practicable after we electronically file such material with, or furnish it to, the United States Securities and Exchange Commission (the “SEC”). The SEC maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC at http://www.sec.gov.

Generally, as a smaller reporting company, we are permitted to omit risk factors. However, we believe the following Risk Factors are material to our business. These do not encompass all risks related to our operations.

You should carefully consider the risks described below together with all of the other information included in this annual report before making an investment decision with regard to our securities. The statements contained in or incorporated herein that are not historic facts are forward-looking statements that are subject to risks and uncertainties that could cause actual results to differ materially from those set forth in or implied by forward-looking statements. If any of the following risks actually occurs, our business, financial condition or results of operations could be harmed. In that case, you may lose all or part of your investment. In addition to the other information provided in this prospectus, you should carefully consider the following risk factors in evaluating our business before purchasing any of our common stock.

Risks Related to Our Financial Condition

Since our inception, we have been insolvent and have required debt and equity financing to maintain operations.

Since our inception, we have failed to create cashflows from revenues sufficient to cover basic costs. As a result, we have relied heavily on debt and equity financing. Equity financing, in particular, has created a dilutive effect on our common stock, which has hampered our ability to attract reasonable financing terms. For the foreseeable future, we will continue to rely upon debt and equity financing to maintain operation of the Company and its subsidiaries.

We have generated minimal revenues from operations, which makes it difficult for us to evaluate our future business prospects and make decisions based on those estimates of our future performance.

As of December 31, 2018, we had generated insufficient revenues. As a consequence, it is difficult, if not impossible, to forecast our future results based upon our historical data. Our projections are based upon our best estimates on future growth. Because of the related uncertainties, we may be hindered in our ability to anticipate and timely adapt to increases or decreases in sales, revenues, or expenses. If we make poor budgetary decisions as a result of unreliable data, we may never become profitable or incur losses, which may result in a decline in our stock price.

There is substantial doubt about our ability to continue as a going concern and if we are unable to generate significant revenue or secure additional financing, we may be unable to implement our business plan and grow our business.

We are an emerging growth company and are in the process of selling and developing our products. Consequently, we have not generated enough revenues as of the date of this prospectus. We have an accumulated deficit and have incurred operating losses since our inception and expect losses to continue during the remainder of fiscal 2019. Our independent registered public accounting firm has indicated in their report that these conditions raise substantial doubt about our ability to continue as a going concern for a period of 12 months from the issuance date of this report. The continuation of our business as a going concern is dependent upon the continued financial support from our stockholders.

| 8 |

There is uncertainty regarding our ability to grow our business to a greater extent than we can with our existing financial resources, also described above, without additional financing. We have no agreements, commitments, or understandings to secure additional financing at this time. Our long-term future growth and success is dependent upon our ability to continue selling our products and services, generate cash from operating activities and obtain additional financing. There is no assurance that we will be able to continue selling our products and services, generate sufficient cash from operations, sell additional shares of common stock or borrow additional funds. Our inability to obtain additional cash could have a material adverse effect on our ability to grow our business to a greater extent than we can with our existing financial resources, also described above.

Expenses required to operate as a public company will reduce funds available to implement our business plan and could negatively affect our stock price and adversely affect our results of operations, cash flow and financial condition.

Operating as a public company is more expensive than operating as a private company, including additional funds required to obtain outside assistance from legal, accounting, investor relations, or other professionals that could be costlier than planned. We may also be required to hire additional staff to comply with additional SEC reporting requirements. We anticipate that the cost of SEC reporting will be approximately $100,000 annually. Our failure to comply with reporting requirements and other provisions of securities laws could negatively affect our stock price and adversely affect our results of operations, cash flow and financial condition. If we fail to meet these requirements, we will be unable to secure a qualification for quotation of our securities on the OTCQB, or if we have secured a qualification, we may lose the qualification and our securities would no longer trade on the OTCQB. Further, if we fail to meet these obligations and consequently fail to satisfy our SEC reporting obligations, investors will then own stock in a company that does not provide the disclosure available in quarterly, annual reports and other required SEC reports that would be otherwise publicly available leading to increased difficulty in selling their stock due to our becoming a non-reporting issuer.

Our common stock trades below $0.01 and is substantially at risk of being delisted from the OTCQB Tier.

OTC Markets requires, amongst other things, that in order to qualify for OTCQB listings, an issuer have their common stock trade above $0.01 per share. If the bid price closes below $0.01 for 30 consecutive days, an issuer will be notified of their bid price deficiency and has a 90-day cure period, where by the stock’s closing bid price must be greater than $0.01 for 10 consecutive days. On February 5, 2019, we received notice of our bid price deficiency from OTC Markets, giving us until May 6, 2019 to cure the bid price deficiency. If we fail to cure, we will be dropped to the OTCPink tier. This could adversely affect the Company and our ability to raise funds through equity financing as OTCPink listings are generally deemed to have a greater risk. In addition, our shareholders face the risk that in order to cure the bid price deficiency, the Board of Directors may recommend a reverse stock split to the shareholders. As Nicholas Campanella has a majority of the voting rights, such recommendation would likely be affirmed which could result in the risk of greater dilution to the value of our shareholders.

Risks Related to Our Business

We rely on our Chief Executive Officer to operate our business. The loss of our Chief Executive Officer could have a material adverse effect on our business.

Our operations are highly dependent upon the efforts of our Chief Executive Officer, Nicholas Campanella. The success of our Company is heavily reliant upon the efforts and resources of Nicholas Campanella. The loss of our Chief Executive Officer would have a material adverse effect on our business, financial condition, and results of operations, particularly if we are unable to hire or relocate and integrate suitable replacements on a timely basis or at all. Further, in order to continue to grow our business, we will need to expand our senior management team. We may be unable to attract or retain these persons. This could hinder our ability to grow our business and could disrupt our operations or otherwise have a material adverse effect on our business.

| 9 |

We are unable to attract additional management personnel and members to our Board of Directors.

Due to our insolvency, we are unable to dedicate any amount of cashflows to executive salaries and/or directors’ and officers’ insurance, therefore we are unable to attract additional executive personnel or Board Members. Until we can secure, at a minimum directors’ and officers’ insurance, the executive duties shall remain with our Chief Executive Officer.

The current ownership has the effect of concentrating voting control with our Chief Executive Officer and his family; this limits our other stockholders’ and your ability to influence corporate matters.

Nicholas Campanella currently holds 12,000,000 shares of Series A Preferred Stock. Each share of Series A Preferred Stock is entitled to 125 votes per share. As a result, Nicholas Campanella has 1,500,000,000 voting rights. As a result of this concentration of voting power, Nicholas Campanella will have significant influence over the management and affairs of the Company and control over matters requiring stockholder approval, including the election of directors and significant corporate transactions, such as mergers or other sales of the Company or our assets, for the foreseeable future. This concentration of voting control will limit your ability to influence corporate matters and could adversely affect the market price of our Common Stock once a market is established.

Our director and officer, Nicholas Campanella will control and make corporate decisions that may differ from those that might be made by the other shareholders.

Due to the controlling amount of their share ownership in our Company, Nicholas Campanella will have a significant influence in determining the outcome of all corporate transactions, including the power to prevent or cause a change in control. His interests may differ from the interests of other stockholders and thus result in corporate decisions that are disadvantageous to other shareholders.

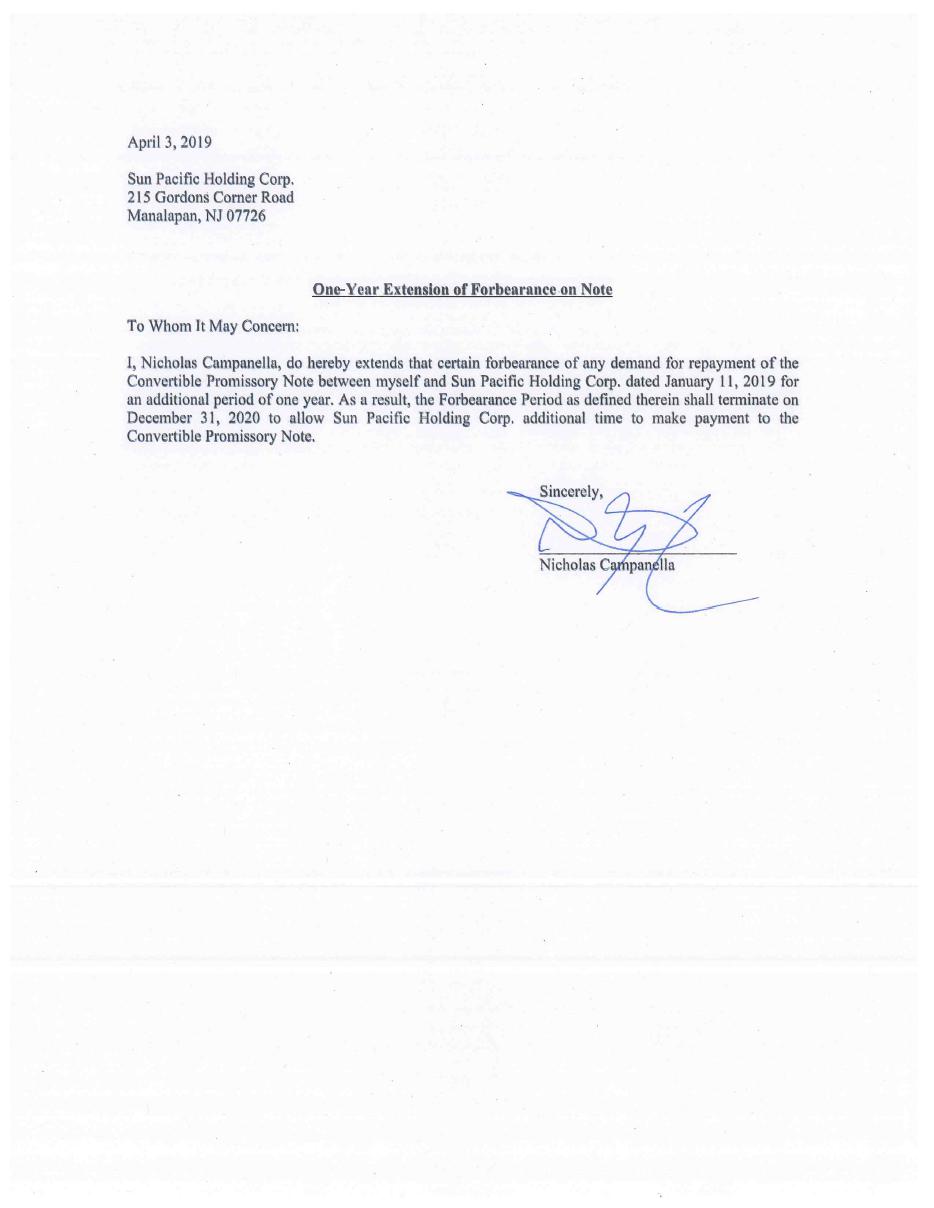

Our director and officer, Nicholas Campanella, holds substantial debt that is convertible into common stock, resulting in even greater control over the Company.

Nicholas Campanella holds convertible promissory notes in excess of $600,000, making Nicholas Campanella the largest creditor of the Company. The convertible promissory notes are convertible into common stock at rate of a 50% discount to market. Our current market cap is lower than $400,000. If Nicholas Campanella were to either convert his promissory notes or foreclose upon the limited assets of the Company, we would likely have to file for bankruptcy.

We currently lease 2,510 square feet at 215 Gordons Corner Road, Manalapan, NJ, 07726 under a five (5) year lease that commenced on March 15, 2017 for approximately $43,000 per annum with 2.5% annual scheduled rent increases. We believe we can obtain additional facilities required to accommodate projected needs without difficulty and at commercially reasonable prices, although no assurance can be given that we will be able to do so. Currently, our Gordons Corner Road office is headquarters for all our subsidiary operations. MedRecycler-RI, Inc. has entered into a lease for the Rhode Island Project at 1600 Division Road, West Warwick, RI, 02893. The lease is for ten (10) years, commencing on March 1, 2019 for approximately $192,668.00 per annum, increasing annual at a rate of five percent (5%). The space leased is approximately 48,000 square feet.

From time to time the Company is a party to various legal or administrative proceedings arising in the ordinary course of our business. While any litigation contains an element of uncertainty, we have no reason to believe that the outcome of such proceedings will have a material adverse effect on the financial condition or results of operations of the Company.

Currently, the Company is not involved in any pending or threatened material litigation or other material legal proceedings, nor have we been made aware of any pending or threatened regulatory audits.

| 10 |

There is no material bankruptcy, receivership, or similar proceeding with respect to the Company or any of its significant subsidiaries. However, given the Company’s insolvency, there is a high risk that the Company may be forced to file for bankruptcy if the Company is unable to meet its capital requirements in 2019.

The are no proceedings which any director, officer, or affiliate of the Company, any owner of record or beneficially of more than five percent (5%) of any class of voting securities of the Company, or any associate of any such director, officer, affiliate of the Company, or security holder is a party adverse to the Company or any of its subsidiaries or has any material interest adverse to the Company or any of its subsidiaries. However, several shareholders have threatened derivative suit against our Board of Directors. As of the date of this filing, no formal suit has been filed.

There are no administrative or judicial proceedings arising from any federal, state, or local provisions that have been enacted or adopted regulating the discharge of materials into the environment or primary for the purpose of protecting the environment.

In addition, no proceeding or action described in this Item 3 were terminated in the past 12 months.

| 11 |

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Market Information

The high and low per share closing sales prices of the Company’s stock on the OTC Markets (ticker symbol: SNPW) for each quarter for the years ended December 31, 2018 and 2017 were as follows:

| Quarter Ended | High | Low | ||||||

| March 31, 2017 | 0.98 | 0.32 | ||||||

| June 30, 2017 | 0.35 | 0.11 | ||||||

| September 31, 2017 | 0.38 | 0.05 | ||||||

| December 31, 2017 | 0.35 | 0.11 | ||||||

| March 31, 2018 | 0.138 | 0.12 | ||||||

| June 30, 2018 | 0.0635 | 0.0575 | ||||||

| September 31, 2018 | 0.0325 | 0.0275 | ||||||

| December 31, 2018 | 0.0145 | 0.0106 | ||||||

On February 5, 2019, the Company received notice of a bid price deficiency from OTCMarkets. We have until May 6, 2019 to cure the bid price deficiency or risk being downlisted to the OTCPink tier.

Holders of our Common Stock

As of March 28, 2019, there were approximately 569 stockholders of record of our common stock. This number does not include shares held by brokerage clearing houses, depositories or others in unregistered form. The stock transfer agent for our securities is VStock Transfer.

Dividend Policy

We have never paid dividends on our Common Stock and intend to continue this policy for the foreseeable future. We plan to retain earnings for use in growing our business base. Any future determination to pay dividends will be at the discretion of our Board of Directors and will be dependent on our results of operations, financial condition, contractual and legal restrictions and any other factors deemed by the management and the Board to be a priority requirement of the business.

Our Series C Preferred Stock holders were to be paid an annual dividend in the amount of $0.125 per year, for a total of $0.25, over an eighteen (18) month term, from the date of issuance (the “Commencement Date. Dividend payments shall be payable as follows: (i) dividend in the amount of $0.0625 per share of Series C Preferred Stock at the end of each of the third quarter and fourth quarter of the first twelve (12) months of the twenty-four (24) month period after the Commencement Date; and (ii) dividend in the amount of $0.03125 per share of Series C Preferred Stock at the end of each of the four quarters of the second twelve ( 12) months of the twenty-four (24) month period after the Commencement Date. The source of payment of the dividends will be derived from up to thirty-five percent (35%) of net revenues (‘‘Net Revenues”) from the Street Furniture Division of the Corporation following the seventh (7th) month after the Commencement Date. To the extent the amount derived from the Net Revenues of the Street Furniture Division is insufficient to pay dividends of Series C Preferred Stock, if a sufficient amount is available, the next quarterly payment date the funds will first pay dividends of Series C Preferred Stock past due. As of today’s date, no dividend payments have been made. 275,000 shares of Series C Preferred Stock were originally issued as Series B Preferred Stock of Sun Pacific Holding Corp. and all dividend payments have ceased, leaving only accrued payments due.

| 12 |

Securities Authorized for Issuance Under Equity Compensation Plans

The Company has not adopted an equity compensation plan.

Unregistered Sales of Equity Securities

Note that all issuances described below represent the number of shares issued at the time of issuance. On October 13, 2017, the Company implemented a reverse stock split at a rate of 1:50, rounding fractional shares up to the nearest whole share. Therefore, any issuance described below that occurred before October 13, 2017 represents pre-reverse stock split numbers.

On January 10, 2017, the Company issued to each of Randy Romano, the Company’s President, and Vaughan Dugan, the Company’s Chief Executive Officer, 5,000,000 shares of Series A Preferred Stock of the Company (the “Series A Stock”) in return for the payment to the Company from each of Randy Romano and Vaughan Dugan of $500.

On December 28, 2016, a holder of a convertible note payable of the Company with an outstanding principal balance of $7,773.60 converted $4,000.00 of the note into 2,601,626 shares of our common stock.

The Company issued the securities to the noteholder, Ms. McComb, Mr. Romano and Mr. Dugan in reliance upon exemptions from registration provided by the Securities Act of 1933, as amended.

On or about February 28, 2017, we issued 3,812,306 shares of common stock to one entity pursuant to the conversion of a certain convertible debenture at a conversion price of $0.0015375 per share of common stock

On or about April 7, 2017, we issued 4,247,381 shares of common stock to one entity pursuant to the conversion of a certain convertible promissory note at a conversion price of $0.0018 per share of common stock.

On or about May 5, 2017, we issued 5,000,000 shares of common stock to one entity pursuant to the conversion of a certain convertible debenture at a conversion price of $0.0025 per share of common stock.

On or about May 8, 2017, we issued 4,400,000 shares of common stock to one entity pursuant to the conversion of a certain convertible promissory note at a conversion price of $0.00165 per share of common stock.

On or about May 15, 2017, we issued 5,200,000 shares of common stock to one entity pursuant to the conversion of a certain convertible debenture at a conversion price of $0.00165 per share of common stock.

On or about May 25, 2017, we issued 6,083,000 shares of common stock to one entity pursuant to the conversion of a certain convertible debenture at a conversion price of $0.0014 per share of common stock.

On or about May 26, 2017, we issued 6,233,333 shares of common stock to one entity pursuant to the conversion of a certain convertible promissory note at a conversion price of $0.0015 per share of common stock.

On or about June 1, 2017 we issued 3,300,000 shares of common stock to one entity pursuant to the conversion of a certain convertible debenture dated June 27, 2015 at a conversion price of $0.00165 per share of common stock.

On or about June 1, 2017, we issued 6,083,000 shares of common stock to one entity pursuant to the conversion of a certain convertible debenture dated July 20, 2016 at a conversion price of $0.00135 per share of common stock.

On or about June 8, 2017, we issued 6,233,333 shares of common stock to one entity pursuant to the conversion of a certain convertible debenture dated June 27, 2015 at a conversion price of $0.0015 per share of common stock.

On or about June 12, 2017 we issued 7,425,000 shares of common stock to one entity pursuant to the conversion of a certain convertible debenture dated July 20, 2016 at a conversion price of $0.0011 per share of common stock.

On August 17, 2017, the Company agreed to issue to 1,000,000 shares of Series B Preferred stock, 200,000 shares of Series C Preferred stock and 284,215,420 shares of common stock to the respective shareholders of Sun Pacific Power Corp in exchange for services.

| 13 |

On August 24, 2017, in connection with the reverse merger, the Company issued 5,665,092 shares of common stock to the previous stockholders of the Company.

On October 2017, the Company sold 762,500 shares of common stock for gross proceeds of $152,500.

On August 24, 2017, in connection with the reverse merger, the Company assumed convertible notes with an aggregate principal balance of $833,787. The notes automatically converted into 17,052,925 shares of common stock on October 3, 2017 upon the effective date of the Company’s reverse split in accordance with the convertible note agreements.

On November 9, 2017, the Company issued 12,500 shares of common stock pursuant to subscriptions purchasing share at a rate equal to $0.20 per share

On December 5, 2017, the Company issued 1,575,000 shares of common stock pursuant to subscriptions purchasing share at a rate equal to $0.20 per share.

On December 19, 2017, the Company issued 258,651 shares of common stock pursuant to subscriptions purchasing shares at a rate equal to $0.20 per share. On the same date, 121,683 shares were issued to Nicholas Campanella for services.

On February 20, 2018, the Company issued 1,250,000 shares of common stock to Nicholas Campanella for services. On the same date, 100,000 shares of common stock were issued pursuant to 2 subscription agreements purchasing shares at a rate equal to $0.20 per share.

On May 5, 2018, the Company issued 668,324 shares of common stock for settlement of services previously provided.

On May 8, 2018, the Company issued 880,000 shares pursuant to subscription agreements purchasing shares of common stock at a rate of $0.20 per share.

On November 13, 2018, the Company issued 620,000 shares of common stock pursuant to conversions of certain convertible promissory notes at an average price of $0.013 per share.

On November 27, 2018, the Company issued 250,000 shares of common stock pursuant to conversion of a portion of a convertible note at a price of $0.012 per share.

On December 6, 2018, the Company issued 500,000 shares of common stock pursuant to a conversion of a portion of a convertible promissory note at a price of $0.005 per share.

On December 10, 2018, the Company issued 1,000,000 shares of common stock pursuant to a conversion of a portion of a convertible promissory note at a price of $0.0068 per share.

On December 26, 2018, the Company issued 1,300,000 shares of common stock pursuant to a conversion of a portion of a convertible promissory note at a price of $0.005 per share.

On December 31, 2018, the Company issued 500,000 shares of common stock pursuant to a conversion of a portion of a convertible promissory note at a price of $0.0044 per share.

In connection with the reverse merger, the Company issued 2,000,000 shares of Series B Preferred Stock. The Series B Preferred Stock automatically converted into 30,856,553 shares of common stock after giving effect to the reverse stock split that occurred on October 3, 2017.

The issuances of the above shares of common stock were exempt from the registration requirements of Section 5 of the Securities Act of 1933 (the “Act”) pursuant to Section 4(a)(2) thereto as isolated transactions not involving a public offering. Following the issuances and as of the date of this filing, the Registrant has a total of 114,378,697 shares of common stock issued and outstanding.

| 14 |

All the offers and sales of securities listed above were made to accredited investors. The issuance of the above securities is exempt from the registration requirements under Rule 4(2) of the Securities Act of 1933, as amended, and/or Rule 506 as promulgated under Regulation D.

Repurchases of Equity Securities

We repurchased no shares of our Common Stock during the year ended December 31, 2018.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The discussion and analysis of our financial condition and results of operations are based on our financial statements, which we have prepared in accordance with accounting principles generally accepted in the United States of America. This discussion should be read in conjunction with the other sections of this Form 10-K, including “Risk Factors,” and the Financial Statements. The various sections of this discussion contain a number of forward-looking statements, all of which are based on our current expectations and could be affected by the uncertainties and risk factors described throughout this Annual Report on Form 10-K. See “Forward-Looking Statements.” Our actual results may differ materially. The preparation of these financial statements requires us to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements, as well as the reported revenues and expenses during the reporting periods. On an ongoing basis, we evaluate estimates and judgments, including those described in greater detail below. We base our estimates on historical experience and on various other factors that we believe are reasonable under the circumstances, the results of which form the basis for making judgments about the carrying value of assets and liabilities that are not readily apparent from other sources. Actual results may differ from these estimates under different assumptions or conditions.

As used in this “Management’s Discussion and Analysis of Financial Condition and Results of Operation,” except where the context otherwise requires, the term “we,” “us,” “our,” or “the Company,” refers to the business of Sun Power Holdings Corp.

Organizational Overview

Utilizing managements history and contacts in general contracting, coupled with our subject matter expertise and intellectual property (“IP”) knowledge of solar panels and other environmentally friendly technologies, Sun Pacific Holding (“the Company”) is focused on building a “Next Generation” green energy company. Currently, the Company has six (6) subsidiary holdings with our principal executive offices located at 215 Gordon’s Corner Road, Suite 1a, Manalapan NJ 07726.

The Company was incorporated under the laws of the State of New Jersey on July 28, 2009, as Sun Pacific Power Corporation and together with its subsidiaries, are referred to as the “Company”. On August 24, 2017, the Company entered into an Acquisition Agreement with EXOlifestyle, Inc. whereby the Company became a wholly owned subsidiary of EXOlifestyle, Inc. The acquisition was accounted for as a reverse merger, resulting in the Company being consider the accounting acquirer.

On October 3, 2017, pursuant to the written consent of the majority of the shareholders in lieu of a meeting, Sun Pacific Holding Corp., f/k/a EXOlifestyle, Inc. (the “Company”) filed a Certificate of Amendment with the state of Nevada to change the name of the Company from EXOlifestyle, Inc. to Sun Pacific Holding Corp.

Going Concern

The Company has an accumulated deficit of $6,649,017 as of December 31, 2018. The Company’s continuation as a going concern is dependent on its ability to generate sufficient cash flows from operations to meet its obligations, which it has not been able to accomplish to date, and/or obtain additional financing from its stockholders and/or other third parties.

In order to further implement its business plan and satisfy its working capital requirements, the Company will need to raise additional capital. There is no guarantee that the Company will be able to raise additional equity or debt financing at acceptable terms, if at all.

| 15 |

There is no assurance that the Company will ever be profitable. These consolidated financial statements do not include any adjustments to reflect the possible future effects on the recoverability and classification of assets or the amounts and classifications of liabilities that may result should the Company be unable to continue as a going concern.

Critical Accounting Policies and Estimates

Our significant accounting policies are more fully described in the notes to our consolidated financial statements. Those material accounting estimates that we believe are the most critical to an investor’s understanding of our financial results and condition are discussed immediately below and are particularly important to the portrayal of our financial position and results of operations and require the application of significant judgment by our management to determine the appropriate assumptions to be used in the determination of certain estimates.

Use of estimates in the preparation of financial statements

Preparation of financial statements in conformity with accounting principles generally accepted in the United States requires management to make estimates and assumptions that affect reported amounts in the financial statements and accompanying notes. Actual results could differ from those estimates. Significant estimates include the allowance for doubtful accounts and impairment assessments related to long-lived assets.

Consolidation

The consolidated financial statements include the accounts of the Company and its wholly-owned subsidiaries. All significant intercompany balances and transactions have been eliminated.

Cash and cash equivalents

For purposes of the consolidated statements of cash flows, cash includes demand deposits and short-term liquid investments with original maturities of three months or less when purchased. As of December 31, 2018, the Federal Deposit Insurance Corporation (FDIC) provided insurance coverage of up to $250,000, per depositor, per institution. At December 31, 2018, none of the Company’s cash balances were in excess of federally insured limits.

Accounts Receivable

In the normal course of business, we decide to extend credit to certain customers without requiring collateral or other security interests. Management reviews its accounts receivable at each reporting period to provide for an allowance against accounts receivable for an amount that could become uncollectible. This review process may involve the identification of payment problems with specific customers. Periodically we estimate this allowance based on the aging of the accounts receivable, historical collection experience, and other relevant factors, such as changes in the economy and the imposition of regulatory requirements that can have an impact on the industry. These factors continuously change and can have an impact on collections and our estimation process. The Company’s allowance for doubtful accounts totaled $145,155 and $118,221 as of December 31, 2018 and 2017, respectively.

Contingencies

Certain conditions may exist as of the date financial statements are issued, which may result in a loss, but which will only be resolved when one or more future events occur or do not occur. We assess such contingent liabilities, and such assessment inherently involves an exercise of judgment. In assessing loss contingencies related to pending legal proceedings that are pending against us or unasserted claims that may result in such proceedings, we evaluate the perceived merits of any legal proceedings or unasserted claims as well as the perceived merits of the amount of relief sought or expected to be sought therein. If the assessment of a contingency indicates that it is probable that a liability has been incurred and the amount of the liability can be estimated, then the estimated liability would be accrued in our consolidated financial statements. If the assessment indicates that a potentially material loss contingency is not probable but is reasonably possible, or is probable but cannot be estimated, then the nature of the contingent liability, together with an estimate of the range of possible loss if determinable would be disclosed.

| 16 |

Fair value of financial instruments

The carrying amounts of the Company’s accounts payable, accrued expenses, and shareholder advances approximate fair value due to their short-term nature. The Company’s long-term debt approximates fair value based on prevailing market rates.

Property and equipment

Property and equipment are stated at cost. Additions and improvements that significantly add to the productive capacity or extend the life of an asset are capitalized. Maintenance and repairs are expensed as incurred. Depreciation is computed using the straight-line method over three to five years for vehicles and five to ten years for equipment. Leasehold improvements are amortized over the lesser of the estimated remaining useful life of the asset or the remaining lease term.

Income taxes

Under ASC Topic 740, “Income Taxes”, the Company is required to account for its income taxes through the establishment of a deferred tax asset or liability for the recognition of future deductible or taxable amounts and operating loss and tax credit carry forwards. Deferred tax expense or benefit is recognized as a result of timing differences between the recognition of assets and liabilities for book and tax purposes during the year.

Deferred tax assets and liabilities are measured using enacted tax rates expected to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled. Deferred tax assets are recognized for deductible temporary differences and operating losses, and tax credit carry forwards. A valuation allowance is established to reduce that deferred tax asset if it is “more likely than not” that the related tax benefits will not be realized.

Revenue recognition

100% of the Company’s revenue for the years ended December 31, 2018 and 2017, is recognized based on the Company’s satisfaction of distinct performance obligations identified in each agreement, generally at a point in time as defined by Topic 606, as amended.

In May 2014, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) No. 2014-09, Revenue from Contracts with Customers. This standard replaced most existing revenue recognition guidance and is codified in FASB ASC Topic 606. Effective January 1, 2018, the Company adopted ASU No. 2014-09 using the modified retrospective method. Under the new guidance, the Company recognizes revenue from contracts based on the Company’s satisfaction of distinct performance obligations identified in each agreement. The adoption of the guidance under ASU No. 2014-09 did not result in a material impact on the Company’s consolidated revenues, results of operations, or financial position. As part of the implementation of ASC 606 the Company must present disaggregation of revenues from contracts with customers into categories that depict how the nature, timing, and uncertainty of revenue and cash flows are affected by economic factors. Quantitative disclosures on the disaggregation of revenue are as follows:

| 2018 | 2017 | |||||||

| Outdoor Advertising Shelter Revenues | 276,591 | 85,157 | ||||||

| Contracting Service Revenues | 308,059 | 1,167,518 | ||||||

| 584,650 | 1,252,675 | |||||||

Earnings Per Share

Under ASC 260, “Earnings Per Share” (“EPS”), the Company provides for the calculation of basic and diluted earnings per share. Basic EPS includes no dilution and is computed by dividing income or loss available to common shareholders by the weighted average number of common shares outstanding for the period. Diluted EPS reflects the potential dilution of securities that could share in the earnings or losses of the entity. For the years ended December 31, 2018 and 2017, basic and diluted loss per share are the same as the calculation of diluted per share amounts would result in an anti-dilutive calculation. For the years ended December 31, 2018 and 2017, the following potential shares have been excluded from the calculation of diluted loss per share because their impact was anti-dilutive:

| 2018 | 2017 | |||||||

| Convertible Debt | 201,542,064 | 18,596,912 | ||||||

| Warrants | 8,324,757 | 1,020,000 | ||||||

| 209,866,791 | 19,616,912 | |||||||

Recent Accounting Pronouncements

ASU No. 2014-09, Revenue from Contracts with Customers (Topic 606) - This standard provides a single set of guidelines for revenue recognition to be used across all industries and requires additional disclosures, which we are currently evaluating. It is effective for annual and interim reporting periods beginning after December 15, 2017. The Company adopted this standard effective January 1, 2018, with no impact on its results of operations and financial condition.

| 17 |

ASU No. 2016-02, Leases (Topic 842) - This standard requires all leases that have a term of over 12 months to be recognized on the balance sheet with the liability for lease payments and the corresponding right-of-use asset initially measured at the present value of amounts expected to be paid over the term. Recognition of the costs of these leases on the income statement will be dependent upon their classification as either an operating or a financing lease. Costs of an operating lease will continue to be recognized as a single operating expense on a straight-line basis over the lease term. Costs for a financing lease will be disaggregated and recognized as both an operating expense (for the amortization of the right-of-use asset) and interest expense (for interest on the lease liability). This standard will be effective for our interim and annual periods beginning January 1, 2019 and must be applied on a modified retrospective basis to leases existing at, or entered into after, the beginning of the earliest comparative period presented in the financial statements. The Company is currently evaluating the potential impact of this standard on its financial position, but we do not expect a material impact on its results of operations and financial condition.

There were other new accounting pronouncements issued by the FASB. Each of these pronouncements, as applicable, has been or will be adopted by the Company. Management does not believe the adoption of any of these accounting pronouncements has had or will have a material impact on the Company’s financial statements.

There were other new accounting pronouncements issued by the FASB. Each of these pronouncements, as applicable, has been or will be adopted by the Company. Management does not believe the adoption of any of these accounting pronouncements has had or will have a material impact on the Company’s financial statements.

Results of Operations for the Year Ended December 31, 2018 as Compared to the Year Ended December 31, 2017

Revenues

During the year ended December 31, 2018, revenues decreased by $668,025, from $1,252,675 for the year ended December 31, 2017 to $584,650 in 2018, due to the migration away from General Contracting services towards the development of Green Energy Projects including the sale of Solar powered shelters and other energy related projects. The Company has entered into revenue sharing agreements with the City of Tallahassee and the State of Rhode Island Transportation Authority and the State of New Jersey and others to provide and manage approximately up to 1,700 Solar powered shelters and other related products for a period of up to Ten (10) years that may include providing WiFi Signal Boosters and Advertising in conjunction with the shelters and other related other outdoor related products. Depending upon the timing of installation and advertising revenue generated per shelter and or other advertising-based product, the Company’s Revenue may increase materially from this green energy offering.

In the first quarter of 2019, the Company, through its subsidiary, MedRecycler, Inc., has secured bridge financing of $6,025,000 to begin building out its waste to energy facility in West Warwick, Rhode Island. Depending upon the successful completion of raising the necessary capital and completing the facility timely, revenues may also increase materially from this additional green energy offering. However, any profits will be initially dedicated to servicing the debt load, paying principal, and building reserves under to be determined covenants for the project. These items along with other revenue generating opportunities under review by the Company may cause dramatic shifts in the Company’s comparative revenue profile of the products and services that the Company provides in the future.

Cost of Revenues

During the year ended December 31, 2018, cost of revenues decreased by $439,310, from $750,802 for the year ended December 31, 2017 to $311,492 in 2018, due to lesser revenues generated from General Contracting services in the Company’s migration to Green Energy Projects. Upon the successful launch and completion of the Company’s Waste to Energy facility and the increase in the Company’s Solar shelters the Company’s Cost of Revenues may increase on an absolute basis, in particular for the Waste to Energy facility.

| 18 |

Operating Expenses

During the year ended December 31, 2018, operating expenses increased by $127,785, from $1,432,783 for the year ended December 31, 2017 to $1,569,796 in 2018 due to an increase in professional fees and general and administrative costs. However, this was offset by reductions in wages and compensation, rent and insurance costs.

Other (Income) Expenses

During the year ended December 31, 2018, Other Expenses decreased by $815,030 from $1,283,456 for the year ended December 31, 2017 to $478,843 in 2018. Due primarily to a loss on settlement of accrued salaries in 2017, offset by increased interest expense in 2018, resulting from the amortization of debt discounts in 2018.

Net Loss

As a result of the above, Net Loss decreased $458,530 from $2,214,366 for the year ended December 31, 2017 to $1,755,837 in 2018.

Liquidity and Capital Resources

Net Working Capital

We have, since inception, financed operations and capital expenditures through the sale of stock and convertible notes and debt. Our immediate sources of liquidity include cash and cash equivalents, accounts receivable, and unbilled receivables.

At December 31, 2018, we had a net working capital deficit of approximately $2,866,303 compared to $1,933,619 at December 31, 2017. We relied on proceeds from the sale of common stock, convertible promissory notes and advances from related parties throughout fiscal 2018.

We must successfully execute our business plan to increase profitability in order to achieve positive cash flows to sustain adequate liquidity without requiring additional funds from external sources to meet minimum operating requirements. We may need to raise additional capital to fund our operations and there can be no assurance that additional capital will be available on acceptable terms or at all.

Generally, the Company has insufficient capital to maintain operations. Cashflows from operations of the Company and all its subsidiary holdings will not sustain the Company’s operations, let alone its filing requirements, unless there is substantial influx of cash flow through either debt and/or equity financing.

Cash Flows from Operating Activities

Cash provided by operating activities provides an indication of our ability to generate sufficient cash flow from our recurring business activities. Fixed costs such as labor, direct materials, and office rent represent a significant portion of the Company’s continuing operating costs.

For the year ended December 31, 2018, net cash used in operations was approximately $758,069 driven by current year operating loss, offset primarily by non-cash expenses for the loss on settlement of accrued officer compensation, accrued expenses, an increase in accounts payable, and loss on the conversion of debt.

For the year ended December 31, 2017, net cash used in operations was approximately $823,000 driven by current year operating loss, offset primarily by non-cash expenses for the loss on settlement of accrued officer compensation, and stock issued for services.

Cash Flows from Investing Activities

For the year ended December 31, 2018, no cash was provided by investing activities.

For the year ended December 31, 2017, cash provided by investing activities was approximately $2,500 from the sale of equipment.

| 19 |

Cash Flows from Financing Activities

Cash provided by (used in) financing activities provides an indication of our debt financing and proceeds from capital raise transactions.

For the year ended December 31, 2018, cash provided by financing activities was approximately $707,181 from the sale of common stock, sale of convertible notes, project financing obligations, and advances from officers, offset by repayments of vehicle loans.

For the year ended December 31, 2017, cash provided by financing activities was approximately $786,000 from the sale of common stock and advances from related parties, offset by repayments of vehicle loans.

At December 31, 2018, there were no material commitments for additional capital expenditures, but that could change with the addition of material contract awards, along with the potential commitments from the Company’s Medrecycler-RI, Inc. ongoing efforts to develop a Waste to Energy project in 2019.

In the short term, we must raise additional capital through debt or equity financing to support our business operations and grow our business. Over the long term, we must successfully execute our growth plans to increase profitable revenue and income streams to generate positive cash flows to sustain adequate liquidity without impairing growth initiatives or requiring the infusion of additional funds from external sources to meet minimum operating requirements. We may need to raise additional capital to fund our operations and there can be no assurance that additional capital will be available on acceptable terms or at all.

Off-Balance Sheet Arrangements

We have no off-balance sheet financing arrangements.

Contractual Obligations

Not required of smaller reporting companies.

Item 8. Financial Statements and Supplementary Data

Our consolidated financial statements and notes thereto and the report of our independent registered public accounting firm, are set forth on pages F-1 through F-15 of this report.

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure

None.

Item 9A. Controls and Procedures

As of the end of the period covered by this Annual Report, our Chief Executive Officer and Chief Financial Officer performed an evaluation of the effectiveness of our disclosure controls and procedures as defined in Rules 13a-15(e) and 15d-15(e) of the Exchange Act. Based on the evaluation and the identification of the material weaknesses in internal control over financial reporting described below, our Chief Executive Officer and Chief Financial Officer concluded that, as of December 31, 2018, the Company’s disclosure controls and procedures were not effective.

| 20 |

Management’s Report on Internal Control over Financial Reporting

Evaluation of Disclosure Controls and Procedures

Pursuant to Rules 13a-15(b) and 15-d-15(b) under the Securities Exchange Act of 1934, as amended (“Exchange Act”), the Company carried out an evaluation, with the participation of the Company’s management, including the Company’s Chief Executive Officer and Chief Financial Officer of the effectiveness of the Company’s disclosure controls and procedures as of the end of the period covered by this report. The term “disclosure controls and procedures”, as defined under Rules 13a-15(e) and 15d-15(e) under the Exchange Act, means controls and other procedures of a company that are designed to ensure that information required to be disclosed by a company in the reports that it files or submits under the Exchange Act is recorded, processed, summarized and reported, within the time periods specified in the SEC’s rules and forms. Disclosure controls and procedures include, without limitation, controls and procedures designed to ensure that information required to be disclosed by a company in the reports that it files or submits under the Exchange Act is accumulated and communicated to the company’s management, including its principal executive and principal financial officer, as appropriate to allow timely decisions regarding required disclosure. Based upon the evaluation of the disclosure controls and procedures at the end of the period covered by this report, the Company’s Chief Executive Officer and Chief Financial Officer concluded that the Company’s disclosure controls and procedures were not effective as a result of continuing weaknesses in its internal control over financial reporting principally due to the following:

| - | The Company has not established adequate financial reporting monitoring activities to mitigate the risk of management override, specifically because there are few employees and only one officers with management functions and therefore there is lack of segregation of duties. | |

| - | An outside consultant assists in the preparation of the annual and quarterly financial statements and partners with the Company to ensure compliance with US GAAP and SEC disclosure requirements. | |

| - | Outside counsel assists the Company in the external attorneys to review and editing of the annual and quarterly filings and to ensure compliance with SEC disclosure requirements. |

At such time as the Company raises additional working capital it plans to add staff, initiate training, add additional subject matter expertise in its finance area so that it may improve it processes, policies, procedures, and documentation of its internal control processes.

Changes in Internal Control over Financial Reporting

There have been no changes in our internal control over financial reporting that occurred during our last fiscal quarter that have materially affected, or are reasonably likely to materially affect, our internal control over financial reporting.

None.

| 21 |

Item 10. Directors, Executive Officers, and Corporate Governance;

The current Directors and Officers of the Company are as follows: