UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

For the quarterly period ended

OR

For the transition period from ______ to ______.

Commission File Number:

(Exact name of registrant as specified in its charter)

|

(State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) | |

|

|

||

| (Address of principal executive offices) | (Zip Code) |

(Registrant’s telephone number, including area code)

Securities registered under Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||

| N/A | N/A | N/A |

Securities registered under Section 12(g) of the Act:

Common Stock, $.0001 Par Value

(Title of class)

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days.

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to

Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer,” “smaller reporting company," and “emerging growth company” in Rule 12b-2 of the Exchange Act:

| Large accelerated filer ☐ | Accelerated filer ☐ |

| Smaller reporting company | |

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐

As of January 12, 2024, the registrant had shares of its Common Stock, $0.0001 par value, outstanding.

When used in this quarterly report, the terms “CNBX Pharmaceuticals Inc.,” “the Company,” “we,” “our,” and “us” refer to CNBX Pharmaceuticals Inc. and its wholly-owned subsidiary, G.R.I.N Ultra Ltd.

CNBX PHARMACEUTICALS INC.

FORM 10-Q

NOVEMBER 30, 2023

INDEX

| 2 |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain information set forth in this Quarterly Report on Form 10-Q, including in Item 2, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and elsewhere herein may address or relate to future events and expectations and as such constitutes “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Statements which are not historical reflect our current expectations and projections about our future results, performance, liquidity, financial condition, prospects and opportunities and are based upon information currently available to us and our management and their interpretation of what is believed to be significant factors affecting our business, including many assumptions regarding future events. Such forward-looking statements include statements regarding, among other things:

| · | the size and growth of the potential markets for our products and the ability to serve those markets; | |

| · | our expectations regarding our expenses and revenue, the sufficiency of our cash resources and needs for additional financing; | |

| · | the rate and degree of market acceptance of any of our products; | |

| · | our expectations regarding competition; | |

| · | our anticipated growth strategies; | |

| · | our ability to attract or retain key personnel; | |

| · | our ability to establish and maintain development partnerships; | |

| · | regulatory developments in the U.S. and foreign countries, especially those related to change in, and enforcement of, cannabis laws; | |

| · | our ability to obtain and maintain intellectual property protection for our products; and | |

| · | the anticipated trends and challenges in our business and the market in which we operate. |

Forward-looking statements, which involve assumptions and describe our future plans, strategies, and expectations, are generally identifiable by use of the words “may,” “should,” “would,” “could,” “scheduled,” “expect,” “anticipate,” “estimate,” “believe,” “intend,” “seek,” or “project” or the negative of these words or other variations on these words or comparable terminology. Actual results, performance, liquidity, financial condition and results of operations, prospects and opportunities could differ materially and perhaps substantially from those expressed in, or implied by, these forward-looking statements as a result of various risks, uncertainties and other factors. These statements may be found under the section of our Annual Report on Form 10-K for the year ended August 31, 2023 (filed on November 29, 2023) entitled “Risk Factors” as well as in our other public filings.

In light of these risks and uncertainties, and especially given the start-up nature of our business, there can be no assurance that the forward-looking statements contained herein will in fact occur. Readers should not place undue reliance on any forward-looking statements. Except as expressly required by the federal securities laws, we undertake no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events, changed circumstances or any other reason.

| 3 |

PART I – FINANCIAL INFORMATION

Item 1. Financial Statements

CNBX PHARMACEUTICALS INC.

Consolidated Balance Sheets

| November 30, | August 31, | |||||||

| 2023 | 2023 | |||||||

| Unaudited | Audited | |||||||

| ASSETS | ||||||||

| Current assets: | ||||||||

| Cash and cash equivalents | $ | $ | ||||||

| Prepaid expenses and other receivables | ||||||||

| Total current assets | ||||||||

| Equipment, net | ||||||||

| Total assets | $ | $ | ||||||

| LIABILITIES AND STOCKHOLDERS' EQUITY | ||||||||

| Current liabilities: | ||||||||

| Accounts payable and accrued liabilities | $ | $ | ||||||

| Convertible loan | ||||||||

| Due to a related party | ||||||||

| Total current liabilities | ||||||||

| Stockholders' equity (deficit): | ||||||||

| Preferred stock, $ par value, shares authorized, shares issued and outstanding | ||||||||

| Common stock, $ par value, shares authorized, and shares issued and outstanding at November 30, 2023 and outstanding at August 31, 2023 respectively | ||||||||

| Additional paid-in capital | ||||||||

| Accumulated deficit | ( | ) | ( | ) | ||||

| Total stockholders' equity (deficit) | ( | ) | ( | ) | ||||

| Total liabilities and stockholders' equity | $ | $ | ||||||

See accompanying notes to consolidated financial statements.

| 4 |

CNBX PHARMACEUTICALS INC.

Consolidated Statements of Operations and Comprehensive Loss

(Unaudited)

| For the Three Months Ended | ||||||||

| November 30, | November 30, | |||||||

| 2023 | 2022 | |||||||

| Unaudited | ||||||||

| Revenues | $ | $ | ||||||

| Operating expenses: | ||||||||

| Research and development expense | $ | $ | ||||||

| General and administrative expenses | ||||||||

| Total operating expenses | ||||||||

| Loss from operations | ( | ) | ( | ) | ||||

| Other (Loss) Income | ||||||||

| Financial (Loss) | ( | ) | ( | ) | ||||

| Net loss | ( | ) | ( | ) | ||||

| Loss from available for sale assets | ( | ) | ||||||

| Total comprehensive loss | $ | ( | ) | $ | ( | ) | ||

| Net loss per share - basic and diluted: | $ | ) | $ | ) | ||||

| Weighted average number of shares outstanding - Basic and Diluted | ||||||||

See accompanying notes to consolidated financial statements.

| 5 |

CNBX PHARMACEUTICALS INC.

Consolidated Statements of Stockholders' Equity (Deficit)

Unaudited

| Common Stock | Additional Paid In | Other Comprehensive | Accumulated | Total Stockholders’ Equity | ||||||||||||||||||||||||

| Shares | Amount | Capital | Warrants | Gain | Deficit | (Deficit) | ||||||||||||||||||||||

| Balance, August 31, 2023 | $ | $ | $ | $ | $ | ( | ) | $ | ( | ) | ||||||||||||||||||

| Share based payment | – | |||||||||||||||||||||||||||

| Exercise of a Convertible loan to shares of common stock. | ||||||||||||||||||||||||||||

| Net loss | – | ( | ) | ( | ) | |||||||||||||||||||||||

| Balance, November 30, 2023 | $ | $ | $ | $ | $ | ( | ) | $ | ( | ) | ||||||||||||||||||

| Common Stock | Additional Paid In | Other Comprehensive | Accumulated | Total Stockholders’ Equity | ||||||||||||||||||||||||

| Shares | Amount | Capital | Warrants | Gain | Deficit | (Deficit) | ||||||||||||||||||||||

| Balance, August 31, 2022 | $ | $ | $ | $ | ( | ) | $ | ( | ) | $ | ( | ) | ||||||||||||||||

| Share based payment | – | |||||||||||||||||||||||||||

| Other comprehensive loss | – | ( | ) | ( | ) | |||||||||||||||||||||||

| Net loss | – | ( | ) | ( | ) | |||||||||||||||||||||||

| Balance, November 30, 2022 | $ | $ | $ | $ | ( | ) | $ | ( | ) | $ | ( | ) | ||||||||||||||||

The accompanying notes are an integral part of the financial statements.

| 6 |

CNBX PHARMACEUTICALS INC.

Consolidated Statements of Cash Flows

(Unaudited)

| For the Three Months Ended | ||||||||

| November 30, | November 30, | |||||||

| 2023 | 2022 | |||||||

| Unaudited | ||||||||

| Cash flows from operating activities: | ||||||||

| Net Loss | $ | ( | ) | $ | ( | ) | ||

| Adjustments required to reconcile net loss to net cash used in operating activities: | ||||||||

| Depreciation | ||||||||

| Interest on loans | ||||||||

| Share based payment | ||||||||

| Changes in operating assets and liabilities: | ||||||||

| Decrease (increase) Accounts Receivable and prepaid expenses | ||||||||

| Increase (decrease) Accounts payable and accrued liabilities | ( | ) | ||||||

| Net cash used in operating activities | ( | ) | ( | ) | ||||

| Cash flows from investing activities: | ||||||||

| Acquisition of equipment | ( | ) | ||||||

| Net cash used in investing activities | ( | ) | ||||||

| Cash flows from financing activities: | ||||||||

| Proceeds from issuance of a Convertible loan | ||||||||

| Net cash provided by financing activities | ||||||||

| Net increase (Decrease) in cash | ( | ) | ( | ) | ||||

| Cash and cash equivalents at beginning of the Period | ||||||||

| Cash and cash equivalents at end of the Period | $ | $ | ||||||

See accompanying notes to consolidated financial statements.

| 7 |

CNBX PHARMACEUTICALS INC.

Notes to Consolidated Financial Statements

(unaudited)

Note 1 – Nature of Business, Presentation and Going Concern

Organization

CNBX Pharmaceuticals Inc. (the “Company”), was incorporated in the State of Nevada, on September 15, 2004, under the name of Thrust Energy Corp.

On September 30, 2010, we increased our authorized capital to 900 million shares of common stock (par value $0.0001) and 100 million shares of preferred stock (par value $0.0001) and effected a 20-for-1 reverse split of our issued and outstanding common stock. As a result of the reverse split, our issued and outstanding common stock was reduced from 13,604,000 shares to 680,200 shares and 5,000,000 preferred shares.

On April 25, 2014, the Company experienced a change in control. Cannabics, Inc. (“Cannabics”) acquired a majority of the issued and outstanding common stock of the Company in accordance with stock purchase agreements. On the closing date, April 25, 2014, pursuant to the terms of the Stock Purchase Agreement, Cannabics purchased 41,000,000 shares of the Company’s outstanding restricted common stock for $198,000, representing 51%.

On May 21, 2014, the Company changed its name, via merger in the state of Nevada, to CNBX Pharmaceuticals Inc. The Company’s principal offices are in Bethesda, Maryland. The Company changed its course of business to laboratory research and development.

On June 19, 2014, FINRA granted final approval of Change of Name & Ticker Symbol of the Corporation from American Mining Corporation to CNBX PHARMACEUTICALS INC., with the new Ticker Symbol of “CNBX”. Said approval was predicated upon CNBX Pharmaceuticals Inc.’s filing of Articles of Merger with American Mining Corporation with the Nevada Secretary of State on May 21, 2014. Under the laws of the State of Nevada, CNBX Pharmaceuticals Inc. was merged with and into the Registrant, with the Registrant being the surviving entity. The Merger was completed under Section 92A.180 of the Nevada Revised Statutes, Chapter 92A, as amended, and as such, does not require the approval of the stockholders of either the Registrant or CNBX Pharmaceuticals Inc.

On August 25, 2014, the Company organized G.R.I.N. Ultra Ltd. (“GRIN”), an Israeli corporation, as a wholly-owned subsidiary. GRIN will provide research and development activities for the Company’s products in Israel.

On July 24, 2017, the Company announced its establishment of a genetics laboratory to develop diagnostic tools based on human genome, tumor genetics and specific cannabinoids.

On August 20th, 2020, the Company announced the creation of a new division for its anti-tumor drug candidate RCC-33, for the treatment of colorectal cancer. This is the result of the Company’s focus on a clinical validation path, including in-vivo experiments, collaborations with key medical centers, and the preparation of a product dossier with which the company plans to schedule a Pre IND-Meeting with the US FDA.

On October 18th, 2022, the Company filed 2 new provisional patent applications on compositions and methods for treating cancer, including colorectal cancer and early intervention therapy for colorectal cancer patients.

| 8 |

Basis of Presentation

The accompanying unaudited financial statements have been prepared in accordance with accounting principles generally accepted in the United States (“U.S. GAAP”) for interim financial statement presentation and in accordance with Form 10-Q. Accordingly, they do not include all of the information and footnotes required in annual financial statements. In the opinion of management, the unaudited financial statements contain all adjustments (consisting only of normal recurring accruals) necessary to present fairly the financial position and results of operations and cash flows. The results of operations presented are not necessarily indicative of the results to be expected for any other interim period or for the entire year.

These unaudited financial statements should be read in conjunction with our August 31, 2022 annual financial statements included in our Form 10-K, filed with the U.S. Securities and Exchange Commission (“SEC”) on November 29th, 2022.

Principles of Consolidation

The consolidated financial statements include the accounts of the Company and GRIN. All significant inter-company balances and transactions have been eliminated in consolidation.

Going Concern

The accompanying unaudited financial statements

have been prepared on a going concern basis, which contemplates the realization of assets and the satisfaction of liabilities in the normal

course of business. The Company has incurred a net loss of $

The ability of the Company to continue as a going concern is dependent upon its abilities to generate revenues, to continue to raise investment capital, and develop and implement its business plan. No assurance can be given that the Company will be successful in these efforts.

Research and Development Costs

The Company accounts for research and development

costs in accordance with Accounting Standards Codification 730 “Research and Development” (“ASC 730”). ASC 730

requires that research and development costs be charged to expense when incurred. Research and development costs charged to expense were

$

Reclassifications

Certain amounts in the prior period financial statements have been reclassified to conform to the current period presentation. These reclassifications had no effect on reported losses, total assets, or stockholders’ equity as previously reported.

Note 2 – Related Party Transactions

During the three months ending November 30, 2023,

the Company paid $

In addition, During the three months ending

November 30, 2023 the Company accrued $

| 9 |

As of November 30, 2023, the Company had a balance

outstanding payable to two directors: Gabriel Yariv and Eyal Barad in the total of $

During the three months ending November 30, 2023, the Company recorded a non cash expense of $ as share-based expense, to the board chairman.

The Company had a balance outstanding at November

30, 2023 and at November 30, 2022 of $

Note 3 – Stockholders’ Equity (Deficit)

Authorized Shares

The Company is authorized to issue up to shares of common stock, par value $ per share. Each outstanding share of common stock entitles the holder to one vote per share on all matters submitted to a stockholder vote. All shares of common stock are non-assessable and non-cumulative, with no pre-emptive rights.

During the three months ending November

30, 2023, the Company issued shares of its common stock to an investors as a result of a convertible loan exercise in the sum

of $

Note 4 – Commitments and Contingencies

We lease the property of our laboratory in Rehovot, Israel, the monthly

lease is $

Note 5 – Private Placement of Notes and Warrant

On December 16, 2020, we entered into a Securities Purchase Agreement (“SPA”) with an institutional investor for a private placement of senior secured convertible notes totaling up to an aggregate of $2,750,000 to be issued in three tranches subject to the achievement of certain milestones. The convertible notes include a conversion right, at the Investor’s option, to convert the convertible notes into shares of our Common Stock at a conversion price equal to the lower of (i) $42 per share or (ii) eighty percent (80%) of the average of the two lowest daily volume-weighted average price for the Company’s Common Stock during the ten (10) consecutive trading days preceding the conversion date (the “notes”). The investor has the right to have the conversion price reduced if we issue Common Stock or convertible notes at a lower conversion price than $42 during the period that the notes are outstanding. The notes are due one year from issuance. The notes will be interest free, but in the event of a default, they will bear annual interest at a rate of 18.00%. The SPA and the notes contain events of default, including, among other things, failure to repay the notes by the maturity date, and bankruptcy and insolvency events, that would result in the imposition of the default interest rate.

On December 21, 2020, we closed the first tranche

and issued a note in the amount of $

| 10 |

On April 23, 2021, we entered into a senior secured

promissory note (the “Senior Secured Note”) for $

On February 15, 2022, we entered into a forbearance agreements with the institutional investor relating to that certain Senior Secured Note. Pursuant to the forbearance agreement, the investor, through March 7, 2022, agreed to forbear from exercising any rights and remedies against the Company related to the outstanding payments and to waive certain other defaults under the Senior Secured Note and related rights pursuant to the registration rights agreement entered into in December 2020 between the Company and the investor.

On November 28, 2022, we entered into a forbearance agreements with the institutional investor relating to that certain Senior Secured Note. Pursuant to the forbearance agreement, the investor, through December 12, 2022, agreed to forbear from exercising any rights and remedies against the Company related to the outstanding payments and to waive certain other defaults under the Senior Secured Note and related rights pursuant to the registration rights agreement entered into in December 2020 between the Company and the investor.

On March 16, 2022, we issued to the investor a

demand promissory note (the “Demand Note”) in the principal amount of $

We entered into a forbearance agreements with the institutional investor relating to that certain Senior Secured Note. Pursuant to the forbearance agreement, the investor, through January 31, 2023, agreed to forbear from exercising any rights and remedies against the Company related to the outstanding payments and to waive certain other defaults under the Senior Secured Note and related rights pursuant to the registration rights agreement.

On June 15, 2022, the Company entered into a

Securities Purchase Agreement providing for the issuance of the Convertible Promissory Note in the principal amount of $

In the period of January through March 2023,

the Company entered into a Securities Purchase Agreement providing for the issuance of the Convertible Promissory Note in the principal

amount of $

| 11 |

On June 12, 2023, the Company entered into a Securities

Purchase Agreement providing for the issuance of the Convertible Promissory Note in the principal amount of $

On October 13, 2023, the Company entered into

a Securities Purchase Agreement providing for the issuance of the Convertible Promissory Note in the principal amount of $

Interest expenses amounted to $

Note 6 – Subsequent events

On December, 2023 the company issued 2,800,000 shares as a result of a CLA conversion.

The Company has evaluated subsequent events through the date the financial statements were issued and filed with the SEC and has determined that there are no other such events that warrant disclosure or recognition in the financial statements.

| 12 |

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Our Business:

We are a pre-clinical-stage, platform technology biopharmaceutical company which has developed proprietary innovative medicines in areas of significant unmet medical needs in oncology, with a current focus on colorectal cancer ("CRC"). Our drug candidate under development for colon cancer is RCC-33, a first-in-class therapy being developed primarily in two settings: one to reduce tumor cell activity in colon cancer patients as a standalone in neoadjuvant treatment or "window of opportunity" at the time after colonoscopy, prior to cancer staging; and another for patients with refractory to therapy and adjuvant to surgery also at the time after colonoscopy. The Company hopes to start first in human Phase I/II clinical trials in 2025. Neoadjuvant treatment is the administration of a therapy before the surgical treatment to improve patient outcome, and our business strategy is to advance our programs through clinical studies including with partners, and to opportunistically add programs in areas of high unmet medical needs through acquisition, collaboration, or internal development.

CNBX Pharmaceuticals Inc. is a clinical stage pharmaceutical company primarily focused on the development of novel cannabinoid-based products and innovative technologies for the treatment of cancer.

The company has prepared to launch Phase I/II (a) clinical study in 2023 which has been delayed due to lack of funds,, for the evaluation of its lead drug candidates Cannabics SR for the treatment of patients with advanced cancer and cancer anorexia cachexia syndrome (CACS) and RCC-33 for the treatment of colorectal cancer. We continue our efforts to find the funds in order to continue our developments.

Our company’s core activities consist of:

| · | Drug Discovery: development of novel molecular formulations and drug candidates; | |

| · | Intellectual Property: filing of corresponding IP to protect our products; and | |

| · | Regulatory Affairs: initiation of the regulatory pathway for each drug candidate in our development pipeline |

Our current business model is to undertake an FDA regulatory pathway for each of the new drug candidates under IND (Investigational New Drug) classification and complete a successful Phase I/II(a) clinical study (toxicity and proof of concept in humans). In reaching this milestone, where an initial feasibility in humans was demonstrated, the company will have gained several commercial opportunities for capitalizing on each such product candidate, including entering into commercial agreements with larger pharma corporations. Accordingly, our company does not engage in any manufacturing, distribution, or sales of products, nor is it foreseeable to expect that we will in the near future.

2. Development pipeline:

2.1. Cannabics SR for Cancer Anorexia-Cachexia Syndrome

Overview

We are developing Cannabics SR as a product candidate for the treatment of CACS. Cannabics SR is a sustained-release oral capsule containing a standardized compound of cannabinoids that has demonstrated a clinically significant weight increase in CACS patients in a peer-reviewed pilot study conducted by Dr. Gil Bar-Sela of the Rambam Hospital Health Care Campus, Division of Oncology, in Haifa, Israel. Our patent-pending technology provides for a convenient, once or twice daily administration, with rapid onset and a steady state of therapeutic effect for a 6 to 8-hour duration.

| 13 |

Cancer Anorexia-Cachexia Syndrome

CACS is a common complication of cancer associated with high morbidity and mortality. It is a complex metabolic syndrome in which a persistently elevated basal metabolic rate is not compensated for by adequate calorie or protein intake, causing involuntary and progressive weight loss leading to increasing functional impairment in cancer patients, especially in advanced stages of the disease. Once established, CACS cannot presently be reversed using available pharmacological or nutritional support techniques.

Unlike starvation, body-weight loss in CACS patients arises mainly from loss of muscle mass, characterized by increased catabolism of skeletal muscle and decreased protein synthesis. This weight loss is associated with important clinical outcomes such as increased morbidity, diminished effectiveness of chemotherapy, muscle wasting, inflammation, fatigue, and reduced survival expectations. The impact of CACS on the patient is not, however, limited to the effect of weight loss. Quality of life, functional abilities, symptoms, psychological outcomes, and social aspects are all affected by CACS.

According to the National Cancer Institute, nearly one-third of cancer deaths can be attributed to the severe weight loss and “metabolic mutiny” associated with CACS, and more than 50% of patients with cancer die with cachexia being present. The overall prevalence of CACS is currently estimated to range from 40% at cancer diagnosis to 70-80% in advanced phases of the disease (Source: Critical Reviews in Oncology/Hematology, 2013;88(3):625-636), while the overall prevalence of weight loss in cancer patients may be as high as 86% in the last 1-2 weeks of life (Source: Journal of Pain and Symptom Management 2007;34:94–104).

The cause and subsequent development of CACS is still poorly understood, but several factors and biological pathways are known to be involved, including inflammation, decreased secretion of anabolic hormones, and altered metabolic response. While there have been important advances in the study of CACS over the past decade, including progress in understanding its mechanisms and the development of promising pharmacologic and supportive care interventions, there is presently no effective pharmacologic therapy for CACS.

Current treatments for CACS are generally based on nutritional support and CACS pathophysiology-modulating drugs, with the most common being the progestogens, megestrol and medroxyprogesterone, and corticosteroids. Progestogens appear to stimulate appetite and improvements in body weight by increasing adipose tissue, but have not been confirmed to augment lean body mass. Megestrol also carries an increased risk of mortality and thromboembolism. Nonetheless, megestrol is the only FDA approved treatment option for CACS and no drug to date has been shown to be superior to it in efficacy and tolerability. Corticosteroids are also considered effective in stimulating appetite and reducing fatigue but should only be used for short periods and in selected cases because of side effects from longer term use, such as insulin resistance, fluid retention, steroidal myopathy, skin fragility, adrenal insufficiency, and sleep and cognitive disorders. Other drugs are being investigated or are in development. Given the dearth of approved therapies, we believe that CACS remains a significant area of unmet medical need.

Cannabinoid Therapies for CACS

Cannabis has long been suggested as a well-tolerated, safe, and effective option to help patients cope with cancer related symptoms with fewer serious side effects than most prescription drugs currently used as anti-emetics, analgesics, and the like. As such, cannabinoids are finding application in palliative care for reducing nausea and vomiting, alleviating cancer pain, and stimulating appetite, as well as improving quality of life in cancer patients. Dronabinol (Marinol®) and nabilone (Cesamet®), two drugs based on synthetic cannabinoids, have each been approved by the FDA for the treatment of chemotherapy-related nausea in patients who do not respond to conventional antiemetic therapy. Another drug, nabiximols (Sativex®), a specific cannabis extract, is approved in Canada and the United Kingdom for symptomatic relief of pain in advanced cancer patients.

Despite interest in cannabinoid-based therapies as a treatment for CACS, their use has been limited by impediments beyond the legal status of cannabis. The most significant obstacle is the lack of clinical research demonstrating their efficacy. While there is evidence that cannabinoids improve appetite, body weight, body fat level, caloric intake, mood, and quality of life in cancer patients, the few studies on these effects have yielded mixed and inconclusive findings. In addition, some of these studies have suffered from methodological constraints that limit any ability to draw firm conclusions.

| 14 |

The therapeutic use of cannabinoids has also been inhibited by limitations associated with traditional administration routes that reduce their effectiveness. Smoking and ingestion of cannabis suffer from wide variability in potency due to a lack of standardized and reproducible formulations. The ingestion of unformulated cannabis has also been associated with poor absorption and low bioavailability versus other administration routes, requiring higher doses and a greater risk of negative side effects. Additionally, the lack of available information on cannabinoid strains has made it difficult for healthcare providers to establish dosing rates. In our experience, however, the principal concern of patients with respect to medical cannabis lies in the undesirable side effects, such as disorientation and dizziness, which result from significant variability in peak blood levels of active cannabinoids soon after administration. We further believe that these side effects, which are common among immediate release methods, are a significant factor in the failure of patients to adhere to recommended treatment regimens and are therefore a pervasive threat to their health and wellbeing.

Cannabics SR

Cannabics SR is an oral composition in the form of a hydroxypropylmethylcellulose (HPMC) capsule containing a patent-pending formulation of cannabinoid extracts suspended in a lipid emulsion. It provides a relatively rapid onset of action, typically within 30-40 minutes, followed by a gradual and sustained release of active cannabinoids, resulting in a steady state level of beneficial effects for up to 6 to 8 hours with each capsule. Cannabics SR provides a consistent, predictable concentration of cannabinoids with an absorption profile and bioavailability of active ingredients that we believe to be superior to other oral cannabinoid administrations. We believe that the multifactorial benefits of the active pharmaceutical ingredients in Cannabics SR address an unmet medical need for a safe and effective treatment of CACS, leading to improved patient adherence and better health outcomes.

Cannabics SR capsules contain only food grade materials without any artificial additives. The active ingredients of each capsule are standardized in composition, formulation, and dose, and are comprised of only pure, natural extracts of active cannabinoids from selected strains of medical cannabis. All excipients are recognized by the FDA as Generally Regarded as Safe.

In addition to the therapeutic potential of Cannabics SR as a treatment for CACS, we believe that our SR technology may be formulated to serve the unique needs of patients suffering from other indications for which a sustained release of a cannabinoid formulation may be beneficial.

Clinical Development

In 2016, we commenced a two-year pilot study to evaluate the influence of Cannabics SR capsules on CACS, and, in particular, on weight loss in advanced cancer patients. The study was led by Professor Gil Bar-Sela, the former Deputy Director of the Division of Oncology at Rambam Health Care Campus, Head of the Palliative and Supportive Oncology Unit, and Head of Service for Melanoma and Sarcoma Patients.

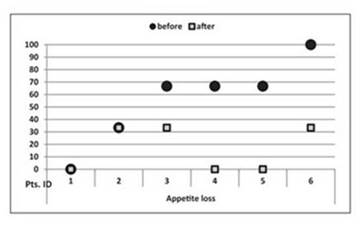

Patients were administered 2 × 10 mg of Cannabics SR per 24 hours for six months. During the study, after some patients reported several psychoactive side effects, the dosage of each capsule was reduced to 5 mg. Almost no side effects were reported with the 5 mg dosage. Participants were weighed at each physician visit. The primary objective of the study was a weight gain of ≥10% from baseline. Of 24 patients who agreed to participate in the study, 17 started the Cannabics SR treatment, but only 11 received the capsules for more than two weeks. Three of six patients who completed the study period met the primary end-point. The remaining three patients had stable weights. In quality-of-life questionnaires patients reported less appetite loss after the Cannabics SR treatment (p=0.05). According to patients’ self-reports, improvement in appetite and mood as well as a reduction in pain and fatigue was demonstrated.

Despite various limitations, the preliminary study demonstrated a weight increase of ≥10% in 3 out of 17 (17.6%) of patients with doses of 5 mg × 1 or 5 mg × 2 capsules daily, without significant side effects. The remaining patients had stable weights. Also, all patients who remained in the study for at least 4.5 months reported an increase in appetite, as did 83% of the patients who completed the study. For 50% of the patients who completed the study, there were reports of pain reduction and sleep improvement. Additional results showed a significant decrease of appetite loss complaints among 83% of the patients who completed the study. (See Bar-Sela, Gil et al. “The Effects of Dosage-Controlled Cannabis Capsules on Cancer-Related Cachexia and Anorexia Syndrome in Advanced Cancer Patients: Pilot Study.” Integrative Cancer Therapies vol. 18 (2019): 1534735419881498. doi:10.1177/1534735419881498.)

| 15 |

Figure 1: Appetite loss among the six patients who completed Cannabics SR treatment, as reported on European Organization of Research and Treatment of Cancer Quality of Life Questionnaire (EORTC QLC-C30)

Commercialization

The results of our planned pilot studies may permit us to commercialize Cannabics SR in Israel under license by the Israeli Ministry of Health. If we are granted such a permit, we intend to engage a GMP manufacturer in Israel to produce Cannabics SR capsules for national distribution.

On May 13, 2020, the Israeli Ministry of Economy signed a Free Export Order, authorizing the export of GMP certified medical cannabis products from Israel. We are currently evaluating our export opportunities and optimal commercialization path for Cannabics SR across all available international markets, particularly with regard to the European Union, Canada, and Australia.

Cancer and Cancer Anorexia Cachexia Syndrome (CACS) Market Analysis

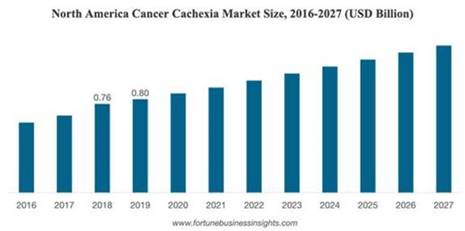

The dynamics of the cancer cachexia market are expected to shift in the coming years as a result of the positive outcomes of some of the rare candidates during the development stage by key players that are in the early stages of clinical development have the potential to create a significant positive shift. The emerging therapies are projected to be launched during the forecast period. In addition, the dearth of effective therapies for this condition presents a great opportunity for pharma companies to create novel drugs because there is less competition in the cancer cachexia market. Moreover, the rising awareness about the condition is also impacting the growth of the cancer cachexia market positively.

The Global Cancer Cachexia Market Size is projected to reach USD 2.93 billion by 2027, exhibiting a CAGR of 4.8% during the forecast period [2020-2027].

https://www.fortunebusinessinsights.com/cancer-cachexia-market-103262

| 16 |

North America region holds the largest market share of the global Cancer Anorexia-Cachexia Syndrome Drug North America is expected to hold a large market share in the global Cancer Anorexia-Cachexia Syndrome Drug Market due to the growing incidence of cancer cases. The International Agency for Research on Cancer (IARC) claims 13 million new cancer cases worldwide. The World Cancer Report provides that the incidence rate of new cancer cases is increased by 50% to 15 million in 2020. The existence of a highly developed healthcare system, the high degree of acceptance by medical practitioners of novel products, the total availability of advanced technological tools, FDA approval of new drugs and many companies are developing oncology products (https://www.datamintelligence.com/research-report/ cancer-anorexia-cachexia-syndrome-drug-market)

2.2 RCC-33: colorectal cancer treatment drug candidate:

Our anti-neoplastic flagship product under development, RCC-33, is an antitumor drug candidate for the treatment of colorectal cancer, which is the 3rd most diagnosed and 2nd most lethal of all cancers, with approximately 2M new cases being diagnosed annually worldwide and a current market estimated at $12B, and which is expected to reach $17B by 2027.

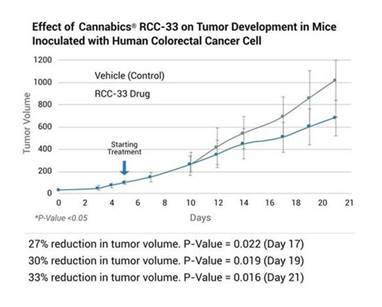

The RCC-33 proprietary formula consists of a specific synthetic cannabinoid molecular composition that has demonstrated the potential to reduce colorectal cancer tumor volume by over 30% in repeated in-vivo studies performed.

Overview

Cancer and Cannabinoids

Cancer is a general term used to describe a group of more than 100 related diseases characterized by uncontrolled growth and spread of abnormal cells, leading to the development of a mass commonly known as a tumor, followed by invasion of the surrounding tissues and subsequent spread, or metastasis, to other parts of the body. Despite enormous investment in research and the introduction of new treatments, cancer remains a critical area of unmet medical need. According to the World Health Organization, cancer is the second leading cause of mortality worldwide, responsible for an estimated nearly 10 million deaths in 2021. As of January 1, 2019, there were more than 16.9 million people with a history of cancer living in the United States, with 1.9 million new cases and 609,360 cancer deaths expected in 2022 (Source: American Cancer Society. Cancer Facts & Figures 2022).

Over the past decade, there has been growing interest in the therapeutic value of cannabinoid compounds in oncology. Cannabis has long been suggested as a well-tolerated, safe, and effective option to help patients cope with cancer related symptoms by reducing nausea and vomiting, alleviating cancer pain, stimulating appetite, and improving quality of life. Beyond their palliative benefits, however, cannabinoids have also been receiving increased attention for their anti-cancer potential, which we believe may one day revolutionize cancer therapy.

Cannabinoids are a diverse class of chemical compounds that occur naturally within cannabis plants and are pharmacologically similar to cannabinoids produced by the human body, known as endocannabinoids. Endocannabinoids form part of the human endocannabinoid system (ECS), a complex biological network that also includes cannabinoid receptors and enzymes involved in cannabinoid formation, transport, and degradation. The ECS is regarded as an important endogenous system implicated in regulation of the most vital biological processes to maintain homeostasis, assisting the body to remain stable and balanced despite external, or environmental, fluctuations (Source: Current Pharmaceutical Design, 2016;22(12):1756-1766).

Dysregulation of the ECS owing to variation in the expression and function of cannabinoid receptors or enzymes or the concentration of endocannabinoids has been associated with several diseases, including cancer (Source: International Journal of Molecular Sciences, 2020;21(3):747). Indeed, the mechanisms involved in the regulation of the ECS as well as the processes that it regulates include practically every pathway important in cancer biology. Expression of the ECS is altered in numerous types of tumors, compared to healthy tissue, and this aberrant expression has been related to cancer prognosis and disease outcome, depending on the origin of the cancer (Source: British Journal of Pharmacology, 2018;175(13):2566-2580). Recent studies suggest that endocannabinoids contribute to maintaining balance in cell proliferation and that targeting the ECS can affect cancer growth (Source: Canadian Urological Association Journal, 2017;11(3-4):E138-E142).

| 17 |

Cannabinoids can interact with the cannabinoid receptors in the ECS, sometimes with a higher affinity than endocannabinoids. As a consequence, all the processes regulated by endocannabinoids are susceptible to interference by cannabinoids. The ability to use cannabinoids to modulate the ECS encompasses several attractive pharmacotherapeutic targets for systemic anti-cancer treatment and has sparked considerable research examining cannabinoid action on cancer cells (Source: Pharmacological Reviews, 2006;58(3):389-462).

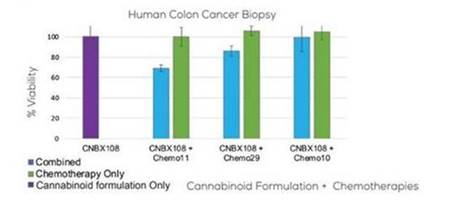

Cannabinoids have demonstrated selective anti-tumor properties in preclinical studies, exerting anti-proliferative, proapoptotic, anti-angiogenic, and anti-metastatic and anti-inflammatory effects depending on tumor type and specific setting (Source: Cancer Medicine, 2018:7(3):765-775). These effects appear to be more pronounced when cannabinoids are used together versus being administered separately, a mechanism known as the entourage effect. We believe, therefore, that cannabinoid combinations may hold promise for an improved anti-proliferative strategy for cancer management.

In addition to their potential role as anti-cancer agents, cannabinoids have been observed to act synergistically with some conventional antineoplastic drugs, such as chemotherapeutic agents, enhancing their effectiveness (Source: Cancer Medicine, 2018;7(3)765-775). This raises the potential for combinational therapies that may increase the range of chemotherapeutic options available to patients and enable targeting of tumor progression at different levels while also permitting dosages of cytotoxic drugs to be dramatically reduced without compromising efficacy.

Figure 2: Synergistic effects of cannabis extracts and chemotherapies on cancer biopsy after treatment with the same extract and three different chemotherapy combinations

As of the date of this filing, we are not aware of any cannabinoid-based therapies approved for the anti-cancer treatment.

Our lead product candidate is RCC-33, which we are developing as a treatment for CRC. RCC-33 is an oral capsule containing a proprietary formulation of cannabinoids that have demonstrated synergistic efficacy in reducing the viability of human colon cancer cell lines in preclinical studies.

Colorectal Cancer

CRC is one of the more common forms of cancer worldwide, representing a significant challenge to the global healthcare system. According to the World Health Organization, CRC is the third most diagnosed cancer in the world and the second-leading cause of cancer-related mortality. In the United States, there were approximately 1,369,005 people living with CRC in 2019(Source: National Cancer Institute. “Cancer Stat Facts: Colorectal Cancer”). In 2022, an estimated 151,030 cases of colon cancer and 44,850 cases of rectal cancer will be diagnosed in the US, and a total of 52,580 people will die from these cancers (Source: American Cancer Society. “Cancer Facts & Figures 2022”).

| 18 |

Most CRCs begin as a noncancerous growth called a polyp that develops on the inner lining of the colon or rectum. The most common kind of polyp is called an adenomatous polyp or adenoma. According to the American Cancer Society, an estimated one-third to one-half of all individuals will eventually develop one or more adenomas. Although all adenomas have the capacity to become cancerous, fewer than 10% are estimated to progress to invasive cancer. The likelihood that an adenoma will evolve into cancer increases as it becomes larger or when it acquires certain histopathological characteristics. Adenomas that become cancerous, called adenocarcinomas, comprise nearly 96% of all CRCs (Source: American Cancer Society. “Colorectal Cancer Facts & Figures 2020-2022”). Adenocarcinomas may grow into blood vessels or lymph vessels, increasing the chance of metastasis to other anatomical sites.

CRC usually develops slowly, over a period of 10 to 20 years. The complex sequence of events occurring during initiation, development and propagation of adenocarcinomas is likely the result of a lifelong accumulation of mutations caused by both genetic and environmental factors known as the adenoma to carcinoma sequence. While the specific cause of any particular case of CRC is often unknown, more than one-half of all cases and deaths are attributable to lifestyle and environmental factors, such as smoking, unhealthy diet, high alcohol consumption, physical inactivity, and excess body weight (Source: American Cancer Society. “Cancer Facts & Figures 2020”).

CRC does not usually cause symptoms until the disease is advanced, therefore early detection of adenomas by screening is vital. If not treated or removed, an adenoma can become a potentially life-threatening cancer.

Current Standard of Care

Treatment options for CRC patients depend on several factors, including the type and stage of cancer, possible side effects, and the patient’s preferences and overall health. Surgical removal of the tumor is the most common form of treatment, particularly in the early stages of malignancy. Patients with more advanced stages of CRC may be given adjuvant chemotherapy to kill any cancer cells remaining after surgery, though standard chemotherapy is associated with severe side effects and provides marginal benefit to the majority of patients. While radiation therapy is often used to treat rectal cancer, it is not generally recommended for colon cancer patients except in the later stages of the disease (Source: American Cancer Society. “Treating Colorectal Cancer”).

CRC is a heterogeneous disease with distinct clinical, molecular, and pathophysiological characteristics. As a result, the response to treatment is variable between patients, even when they are diagnosed at the same clinical stage. Such heterogeneity remains an obstacle to the optimization of treatment for each individual. Researchers are continuing to investigate new treatment options, such as immunotherapy and targeted therapy, that focus upon the genes, proteins, and other factors in a particular tumor (Source: American Cancer Society. “Advances in Colorectal Research”).

Immunotherapy uses the body’s own immune system to kill cancer cells. There are already several FDA-approved immunotherapy options for CRC, such as pembrolizumab (Keytruda®), nivolumab (Opdivo®), and ipilimumab (Yervoy®). Many immunotherapies that have shown promise in addressing other types of cancer are also being tested for CRC. While immunotherapy has had some encouraging results, significant limitations remain. Its efficacy is often unpredictable, and the treatment can lead to the body becoming resistant or result in off-target toxicities where the body’s immune system attacks healthy tissue. Immunotherapy may take longer than other protocols and it is substantially more expensive than classical treatments (Source: Pharmacy & Therapeutics, 2017;42(8):514-521).

Targeted therapy uses drugs to target specific molecules inside cancer cells or on their surface to slow the growth of cancer, destroy cancer cells, and relieve cancer symptoms. There are different types of targeted therapy drugs, each working differently depending on what molecule the drug is targeting. A treatment is chosen based on the types of molecules expressed on the patient’s tumor cells, which allows doctors to tailor cancer treatment for each person. Several targeted therapy drugs, such as bevacizumab (Avasin®) and cetuximab (Erbitux®), are already used to treat advanced CRC. Despite showing clinical promise, targeted therapy has challenges, such as tumor heterogeneity, off-target toxicity, and acquired resistance (Source: Medical Research Journal, 2019;4(2):99-105). The lack of biomarkers by which to identify patients having a high probability of response is also a particularly significant obstacle. As with immunotherapy, the cost of targeted therapy is substantially higher than classical treatments.

| 19 |

We believe that there is no “magic bullet” to cure cancer and that a personalized combination of cancer treatments may be the best course for long term survival benefits in each case. To that end, the development of more prevention strategies and novel agents will be essential.

Cannabinoids and Colorectal Cancer

One area of increasing interest in the treatment of CRC lies in the development and use of cannabinoid therapeutics. The ECS is regarded as an important regulatory system in the gastrointestinal tract, being involved in several important functions such as motility, secretion, sensation, inflammation, and carcinogenesis. Recent studies advocate that the ECS plays a critical role in the development of CRC and should therefore be considered as an appropriate target for CRC inhibition (Source: Frontiers in Pharmacology, 2016;7:361). The expression of ECS components in CRC has been found to be increased and associated with poorer prognosis and advanced stages of disease (Source: Cannabis and Cannabinoid Research, 2018, 3(1):272-281). For example, cannabinoid receptors have been found to be overexpressed in tumor cells of the colon and this up-regulation has been postulated to be an indicator of cancer outcome (Source: British Journal of Pharmacology, 2018; 175(13): 2566-2580).

Research on the effects of cannabinoid compounds on CRC has demonstrated an ability to reduce the viability of CRC cell lines in vitro (Source: Cancer Medicine, 2018;7(3):765-775), while there is also convincing scientific evidence that cannabinoids are able to prevent or reduce carcinogenesis in different animal models of colon cancer (Source: Expert Review of Gastroenterology & Hepatology, 11:10, 871-873).

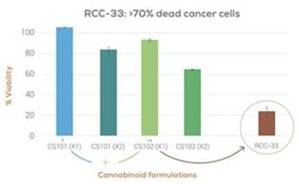

We believe that cannabinoids are a promising therapeutic agent for the treatment of CRC. We have conducted several in vitro unpublished studies using our bioinformatics platform to confirm that cannabinoids cause necrosis in colon cancer cells. While many cannabinoids demonstrate levels of toxicity on cancer cells, we have found that certain cannabinoid extracts and combinations show increased levels of toxicity relative to other isolated or combined cannabinoids. These findings have spurred the development of RCC-33, our product candidate for the treatment of CRC.

Figure 3: Synergistic effects of different cannabinoid combinations on viability of a colon cancer cell line.

RCC-33

We are developing RCC-33 as an oral capsule or solution containing high concentrations of the cannabinoids CBDV and CBGA in a novel formulation, which we believe may be effective in the treatment of adenocarcinomas of the colon. The cannabinoids in RCC-33 have demonstrated complex synergistic anti-tumor effects in combination, with no psychoactive effect. In our preclinical in vitro studies evaluating the influence of 15 different cannabinoids on human colon cancer cell lines (RKO, HCT116), alone and in combination, RCC-33 demonstrated clear efficacy in reducing the viability of colon cancer cells versus alternative cannabinoid combinations. Importantly, we could detect significant reduction effect on tumor development in mice inoculated with human colorectal cancer cells.

| 20 |

Development Plan

The company is currently preparing to launch Phase I/II (a) clinical study in 2025, for the evaluation of its lead drug candidates Cannabics SR for the treatment of patients with advanced cancer and cancer anorexia cachexia syndrome (CACS) and RCC-33 for the treatment of colorectal cancer. We plan to conduct further preclinical studies to establish the safety and efficacy before proceeding with first-in-human clinical testing.

Preclinical Studies

We plan to conduct non-clinical safety studies following Good Laboratory Practice (GLP) to evaluate the systemic and local toxicity of escalating doses of RCC-33 and establish dosing parameters. The results of these preclinical studies, which are expected in 2025, will guide our planned Phase I/II(a) clinical trial. The non-clinical requirements to support the development program will be verified with the FDA at a pre-IND meeting. Such studies may include repeated dose toxicity studies, male and female fertility studies, embryofetal development studies, animal abuse related studies, pharmacokinetics studies, drug-drug interaction studies, and others.

Clinical Trials

We plan to evaluate the safety, tolerability, and pharmacokinetic properties of Cannabis SR and RCC-33 in a Phase I/II(a) ascending dose clinical trial in CRC patients, commencing in the first quarter 2023. The clinical trial will examine the tolerability, pharmacokinetics, pharmacodynamics, and efficacy of multiple doses of RCC-33 in CRC patients. We are currently identifying potential contract research organizations and clinical trial centers to conduct the Phase I/II(a) human proof of concept study, which is estimated to cost $6,500,000. As of the date of this filing, however, the Company does not have sufficient funds to complete the Phase I/II(a) study.

Subject to the results from our Phase I trials, we plan to submit an IND to the FDA for RCC-33 with the clinical protocol for a Phase II double-blind placebo controlled clinical trial evaluating RCC-33 in patients with CRC at various dosing levels versus placebo. The outcomes from the planned Phase II human proof of concept trial will inform our decision regarding further steps in the clinical development of RCC-33.

| 21 |

Our Pipeline:

In addition to RCC-33, our colorectal cancer treatment drug candidate, the company has several other drug candidates under development, including PLP-33 for the local treatment of Lateral Spreading, or Sessile, colorectal polyps during colonoscopy, BRST-33 for the treatment of breast cancer, MLN-33 for the treatment of Melanoma and PRST-33 for the treatment of prostate cancer. These additional drug candidates are in the early stage of development and the company expects to complete the in-vivo research for each product by end of 2025

2.3 Product lines currently not actively developed:

The company has several product lines that are currently not being actively developed following company’s decision to focus its resources and attention exclusively on the development of its FDA route drug candidates, and SR Capsule described above. The product lines not actively developed include:

Cannabics CDx (evaluate) Drug Sensitivity Test

Cannabics CDx is an ex-vivo drug sensitivity test under development to provide healthcare providers with clinical decision support data from which they can identify, for a particular cancer patient undergoing cannabinoid therapy, which cannabinoids or cannabinoid combinations may have the most beneficial anti-cancer effects, and which cannabinoids may be contraindicated.

Company may revisit this decision at a later stage after launching the first in human clinical studies for the validation of its colorectal cancer treatment drug candidate RCC-33.

3. Market opportunity for cancer treatment drug candidates:

3.1. Neoadjuvant therapy:

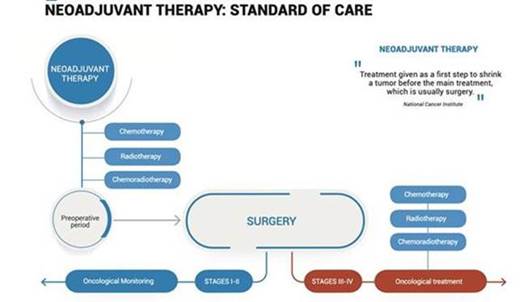

According to the National Cancer Institute, Neoadjuvant Therapy is a "treatment given as a first step to shrink a tumor before the main treatment, which is usually surgery”.

| 22 |

Limitations:

| · | Mild to severe side effects | |

| · | Suppressed immune system | |

| · | Potential resistance of tumor residues to postoperative chemotherapy * |

* “nCRT increases ITGH and may result in the expansion of resistant tumor cell populations in residual tumors”.

Frontiers in Oncology. 2019

The Effects of Neoadjuvant Chemoradiation in Locally Advanced Rectal Cancer—The Impact in Intratumoral Heterogeneity.

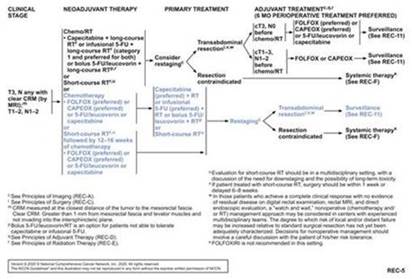

3.1.1 Neoadjuvant therapy in rectal cancer

Neoadjuvant chemoradiotherapy has become the standard treatment for locally advanced rectal cancer. Neoadjuvant chemoradiotherapy not only can reduce tumor size and recurrence, but also increase the tumor resection rate and anus retention rate with very slight side effect. Comparing with preoperative chemotherapy, preoperative chemoradiotherapy can further reduce the local recurrence rate and downstage. Middle and low rectal cancers can benefit more from neoadjuvant chemoradiotherapy than high rectal cancer.

| 23 |

3.1.2 Neoadjuvant therapy in breast cancer

In early breast cancer, surgery is the mainstay of curative treatment. Complementary local radiotherapy and systemic - adjuvant endocrine therapy or chemotherapy treatments are associated with the aim of reducing the risk of relapse according to the clinicopathological characteristics of the tumor. However, the possibility of administering these therapies prior to surgery in neoadjuvant setting offers several advantages:

| · | reduction in tumor size to improve respectability, | |

| · | increased rate of conservative surgery improving esthetic results, | |

| · | reduction in the extent of axillary surgery, | |

| · | early treatment of micrometastatic disease |

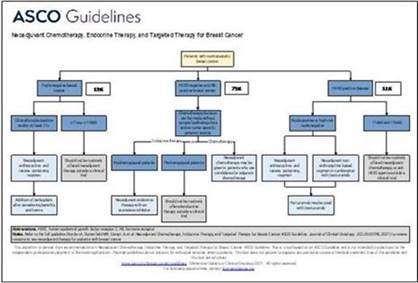

Fig5. Asco Guidelines for neoadjuvant therapy in breast cancer

According to ASCO guidelines most of the patients are eligible for neoadjuvant chemotherapy and are the end consumers of BRST-33, while the current treatment regimen negates severe side effects.

Side effects and risks of standard of care:

| · | nausea or vomiting | |

| · | hair loss | |

| · | nail or skin changes | |

| · | appetite loss | |

| · | weight changes | |

| · | diarrhea or constipation | |

| · | mouth sores | |

| · | fatigue |

| 24 |

3.2. Cannabinoid Neoadjuvant Therapy

For some time now, the FDA has promoted clinical studies on Cannabinoids as a growing range of stakeholders has expressed interest in development of drugs that contain cannabis and compounds found in cannabis. Recent legislative changes have also opened new opportunities for medical cannabis clinical research. As this body of research progresses and grows, the FDA is working to support drug development in this emerging scientific arena.

RCC-33 & BRST-33 – Potential safe drugs improving rectal and breast cancer neoadjuvant standard of care

RCC-33 & BRST-33 anticipated advantage over standard of care:

| · | Non-Suppressed immune system | |

| · | potential low toxicity which is even more important in neoadjuvant treatment since patients will suffer less side effects. Since the two drug candidates are based on two natural molecules (cannabinoids) found in the Cannabis plant, the safety of the molecules in the short and long run is potentially lower. Not like in a new drug entity in which toxicity could not be predicted. | |

| · | Overcoming Potential resistance of tumor residues to postoperative chemotherapy |

4. Outsourced GMP manufacturing and commercial operation:

4.1. Outsourced GMP manufacturing

Our current position is that all of our Chemistry Manufacturing and Controls (CMC) required for the approval process of our drug candidates is to be outsourced. The RCC-33 formulation, as well as all additional drug candidates in our pipeline, while inspired by natural molecules, could consist only of formulations made from chemically synthesized molecules, or APIs (Active Pharmaceutical Ingredients). Our Company is not engaged in the development of any botanical or botanically based product/s. Additionally, in view of our upcoming submission of a pre-IND meeting request with the FDA, the Company the company will need to enter into an agreement with a manufacturer and supplier of GMP (Good Manufacturing Practice) grade APIs suited for Clinical Stage Products. There are a couple of large and long-established US corporation with a long track record of working with the FDA. Accordingly, the manufacturer will also need to provide support to CNBX throughout an IND filing process, including providing all necessary and related information concerning CMC in the form of a comprehensive technical package to be presented to the FDA. APIs supplied under said agreement will be used by Company in Phase I/II (a) clinical studies that it is planning to launch in 2023.

4.2. Commercial Operations

We have not established a sales, marketing, or product distribution infrastructure. We plan to commercialize any drugs we develop through licensing arrangements and strategic partnerships with established companies in the pharmaceutical industry having strong marketing capabilities and distribution networks. We generally intend to advance our drug candidates through Phase I and Phase II clinical trials as appropriate in order to establish their clinical and commercial potential before negotiating the terms of any licensing or collaboration. We believe that this approach will achieve the fullest marketing and distribution potential of any drugs or other products that we may develop in the short term.

5. Core activities:

5.1. Drug Discovery

Conduct all screening and pre-clinical research at in-house state of the art laboratory facilities

| 26 |

Our Research and Development:

To address these problems and improve clinical outcomes, CNBX Pharmaceuticals focuses on the development of diagnostics that monitor cancer progression and cannabinoid-cancer sensitivity tests to tailor treatment of cancer with cannabinoid medicine. Utilizing novel High-Throughput Screening (HTS) methods to perform studies on cancer cell lines and on circulating tumor cells (CTC) derived from cannabis medicated patients.

We aim to treat a wide scope of cancers both as the main treatment and as a conjugate to conventional chemotherapy. We believe a significant need remains for novel drugs for patients who do not respond to existing therapies or for whom these therapies bear undesirable side effects. We recognize the potential therapeutic applications of the synergistic effects of these active compounds thus building the methodology and procedures that decipher specific ratios of active compounds in regard to their antitumor activity.

Our government licensed laboratory operates a unique, custom designed and built research and development laboratory which combines high throughput screening, (HTS) capabilities with the most advanced data tools allowing us to enable miniaturization and automation of a variety of biological assays. The automated system is comprised of:

| 1. | High Content Screening (HCS) Platform, which is an automated cellular imaging and analysis platform designed for quantitative microscopy. |

| 2. | Flow Cytometry, which enables multi-parametric single cell analysis. |

| 3. | Automated workstation, for liquid handling for dispensing accurate and reproducible volumes of liquids and compounds. |

| 4. | Multimode microplate reader, designed for fast measurements of numerous biological reactions/processes. |

The integration of these instruments is enabled via a robotic arm, which allows a continuous process which utilizes all instruments.

Readouts generated from these instruments provide us with insights to the effect of our cannabinoid library on parameters such as, proliferation inhibition, apoptosis induction, angiogenesis prevention and toxicity on cancerous cells.

These experiments will produce multiplexed data composed of images of cells, cell specific markers and the extent/signal of the biological response. The biological response will be measured using different concentration of cannabinoids and their combinations, thus determining the most effective cannabinoid treatment for a specific cancer type.

In vitro Studies – Drug Screening

We have a proprietary procedure of high throughput screening (HTS) and high content screening (HCS) for the detection of correlations between cannabinoid ratios, dosages and anti-tumor activity using a growing library of human cancer cell lines and creating an enlarged variety of Cannabis-based compounds. We examine the biological activity of these compounds on tumor cell lines of distinct tissue lineage and creating a highly valuable therapeutic data. We Screen for the most potent cannabinoid/natural extracts. Our goal in the invitro studies is to build a library of both shaulfied and natural cannabinoid extracts and to reveal their biological impact on a library of cancer cell lines. The HTS technology enables us to gain this data base in a faster manner and to reveal more mechanisms of action that are related to the genetics of the cancer. We are now in the process of merging our data with sophisticated data mining to help find meaningful insights of both treatment and outcome.

Our core technology is a continuously evolving bioinformatics platform that utilizes high-throughput screening technology, advanced data analytics, and proprietary methodologies to rapidly examine the physiologic effect of multiple cannabinoid compounds on tumor cells. This technology enables us to screen thousands of cannabinoid combinations, generating multiple datasets on the anti-tumor properties of different cannabinoid formulations and ratios. We conduct a broad range of preclinical research on cannabinoids through our bioinformatics platform, which informs the development of our product drug candidates.

| 27 |

|

|

We have developed a continuously evolving preclinical bioinformatics platform that enables us to evaluate and classify the physiological impact of multiple cannabinoid compounds on various cancer cells. Utilizing state-of-the-art high-throughput screening and flow cytometry, our platform is capable of testing thousands of compounds weekly, allowing us to rapidly and effectively examine their interactions with a growing library of human cancer cell lines and biopsies. Through the large body of data generated by our platform, we are accumulating in-depth knowledge of the various therapeutic effects of cannabinoids and patterns of cannabinoid ratios that demonstrate meaningful physiologic impact on cancer.

Our bioinformatics platform includes the following:

| Ø | high-throughput screening, high content screening, flow cytometry, machine learning, robotics, and proprietary methodologies; |

| Ø | a library of human cancer cell lines and thousands of different combinations and ratios of cannabinoid compounds in a costumed matrix; |

| Ø | a growing database of biological response data; |

| Ø | in-house extraction, processing methodologies, and analytical techniques that yield well-characterized and standardized extracts; |

| Ø | collaborations with regulated cannabis producers that may expand our cannabinoid compound library and provide us with access for future proprietary cultivars; |

| Ø | fully integrated in-house research and development; and |

| Ø | regulatory expertise. |

| 28 |

Once a series of potentially active cannabinoids is identified for a specific cancer type, we then test and confirm their activity through in vitro and ex-vivo evaluation studies to determine their potential activity. Through this process, we are able to assess their therapeutic potential. The results of our pre-clinical experiments provide starting points for our clinical development programs.

Results of Operations

For the Three Months Ended November 30, 2023 and 2022

Operating Expenses

For the three months ended November 30, 2023, our total operating expenses were $261,337 compared to $346,790 for the three months ended November 30, 2022, resulting in a decrease of $85,453. The decrease is attributable to a decrease of $134,983 in general administration expenses, mostly due to the Professional services expenses of $52,946, share based payment of $40,580 and salary expenses of $25,342 and an increase of $49,530 in research and development expenses.

We incurred a financial loss of $6,523 for the three months ended November 30, 2023, compared to financial income of $10,879 for the three months ended November 30, 2022. The decrease in financial expense was mainly attributable to interest expenses of a convertible loan of $7,000 and a decrees in currency exchange expenses.

Net loss

Net loss decreased by $179,146 to $178,523 for the three months ended November 30, 2023, compared to a net loss of $357,669 for the three months ended November 30, 2022.

Liquidity and Capital Resources

Overview

As of November 30, 2023, we had $81,647 in cash compared to $129,696 on November 30, 2022. We expect to incur a minimum of $1,000,000 in expenses during the next twelve months of operations. We estimate that these expenses will be comprised primarily of general expenses including overhead, legal and accounting fees, research and development expenses, and fees payable to outside medical centers for clinical studies.

Liquidity and Capital Resources during the Three Months Ended November 30, 2023 compared to the Three Months Ended November 30, 2022

We used cash in operations of $71,846 for the three months ended November 30, 2023, compared to cash used in operations of $95,915 for the three months ended November 30, 2022. The negative cash flow from operating activities for the three months ended November 30, 2023, is primarily attributable to the Company's net loss of $178,523, a decrease in accounts payables and accrued liabilities of $25,323 and a decrease of $4,533 in account receivables and prepaid expenses, depreciation of $39,461, interest on convertible loan of $11,451 and share-based payment of $34,975

We had no cash flow from investing activities during the three months ended November 30, 2023, compared to $513 cash flow from investing activities for the three months ended November 30, 2022.

We will have to raise funds to pay for our expenses. We may have to borrow money from shareholders, issue equity or enter into a strategic arrangement with a third party. There can be no assurance that additional capital will be available to us. We currently have no arrangements or understandings with any person to obtain funds through bank loans, lines of credit or any other sources. Since we have no such arrangements or plans currently in effect, our inability to raise funds for our operations will have a severe negative impact on our ability to remain a viable company.

| 29 |

Going Concern

Due to the uncertainty of our ability to meet our current operating and capital expenses, our independent auditors included an explanatory paragraph in their report on the audited financial statements for the year ended August 31, 2022, regarding concerns about our ability to continue as a going concern. Our financial statements contain additional note disclosures describing the circumstances that lead to this disclosure by our independent auditors.

Our unaudited financial statements have been prepared on a going concern basis, which assumes the realization of assets and settlement of liabilities in the normal course of business. Our ability to continue as a going concern is dependent upon our ability to generate profitable operations in the future and/or to obtain the necessary financing to meet our obligations and repay our liabilities arising from normal business operations when they become due. The outcome of these matters cannot be predicted with any certainty at this time and raise substantial doubt that we will be able to continue as a going concern. Our unaudited financial statements do not include any adjustments to the amount and classification of assets and liabilities that may be necessary should we be unable to continue as a going concern.

There is no assurance that our operations will be profitable. Our continued existence and plans for future growth depend on our ability to obtain the additional capital necessary to operate either through the generation of revenue or the issuance of additional debt or equity.

Off-Balance Sheet Arrangements

We currently have no off-balance sheet arrangements that have or are reasonably likely to have a current or future material effect on our financial condition, changes in financial condition, revenues or expenses, results of operations, liquidity, capital expenditures or capital resources.

Critical Accounting Policies

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires us to make a number of estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements. Such estimates and assumptions affect the reported amounts of revenues and expenses during the reporting period. We base our estimates on historical experiences and on various other assumptions that we believe to be reasonable under the circumstances. Actual results may differ materially from these estimates under different assumptions and conditions. We continue to monitor significant estimates made during the preparation of our financial statements. On an ongoing basis, we evaluate estimates and assumptions based upon historical experience and various other factors and circumstances. We believe our estimates and assumptions are reasonable in the circumstances; however, actual results may differ from these estimates under different future conditions.

See Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and Note 2, “Summary of Significant Accounting Policies” in our audited consolidated financial statements for the year ended August 31, 2022, included in our Annual Report on Form 10-K as filed on November 29, 2022, for a discussion of our critical accounting policies and estimates.

Item 3. Quantitative and Qualitative Disclosures About Market Risk.

The disclosure required under this item is not required to be reported by smaller reporting companies, as such term is defined by Item 503(e) of Regulation S-K.

| 30 |

Item 4. Controls and Procedures.

| (a) | Evaluation of Disclosure Controls and Procedures |

The Company maintains a set of disclosure controls and procedures (as defined in Rules 13a-15(e) and 15d-15(e) of the Exchange Act) designed to ensure that information required to be disclosed by the Company in reports that it files or submits under the Exchange Act, is recorded, processed, summarized and reported within the time periods specified in the SEC’s rules and forms and is accumulated and communicated to the Company’s management, including the Chief Executive Officer and Chief Financial Officer, as appropriate, to allow timely decisions regarding required disclosure. In accordance with Rule 13a-15(b) of the Exchange Act, as of the end of the period covered by this Quarterly Report on Form 10-Q, an evaluation was carried out under the supervision and with the participation of the Company’s management, including its Chief Executive Officer, Chief Financial Officer and the Audit Committee, of the effectiveness of its disclosure controls and procedures. The Audit Committee assessed, reviewed and determined that the Company’s disclosure controls and procedures were effective as to this quarterly filing. Based on that evaluation, The Board accepted and ratified the findings of the Audit Committee that the Company’s disclosure controls and procedures, as of November 30th, 2022, the end of the period covered by this Quarterly Report on Form 10-Q, were effective to provide reasonable assurance that information required to be disclosed by the Company in reports that it files or submits under the Exchange Act is recorded, processed, summarized and reported within the time periods specified in the SEC’s rules and forms and is accumulated and communicated to the Company’s management, including the Chief Executive Officer, Chief Financial Officer, and Audit Committee as appropriate to allow timely decisions regarding required disclosure.

| (c) | Limitations on the Effectiveness of Internal Controls |