Table of Contents

As filed with the Securities and Exchange Commission on February 3, 2017

Registration No. 333-215659

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 2

TO

FORM F-10

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Fortuna Silver Mines Inc.

(Exact name of Registrant as specified in its charter)

| British Columbia, Canada | 1040 | Not Applicable | ||

| (Province or other Jurisdiction of Incorporation or Organization) | (Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

200 Burrard Street, Suite 650

Vancouver, British Columbia

Canada V6C 3L6

(604) 484-4085

(Address and telephone number of Registrant’s principal executive offices)

C T Corporation System

111 Eighth Avenue

New York, New York 10011

(212) 894-8940

(Name, address and telephone number of agent for service in the United States)

Copies to:

| Riccardo A. Leofanti, Esq. Skadden, Arps, Slate, Meagher & Flom LLP 222 Bay Street, Suite 1750 P.O. Box 258 Toronto, Ontario, Canada M5K 1J5 (416) 777-4700 |

Susan Tomaine, Esq. Blake, Cassels & Graydon LLP 595 Burrard Street, Suite 2600 Vancouver, British Columbia, Canada V7X 1L3 (604) 631-3300 |

Christopher J. Cummings, Esq. Paul, Weiss, Rifkind, Wharton & Garrison LLP 77 King Street West, Suite 3100 Toronto, Ontario, Canada M5K 1J3 (416) 504-0522 |

Michael G. Urbani, Esq. Quentin Markin, Esq. Stikeman Elliot LLP 666 Burrard Street, Suite 1700 Vancouver, British Columbia, Canada V6C 2X8 (604) 631-1300 |

Approximate date of commencement of proposed sale of the securities to the public:

As soon as practicable after this Registration Statement becomes effective.

Province of British Columbia, Canada

(Principal jurisdiction regulating this offering)

It is proposed that this filing shall become effective (check appropriate box):

A. ☒ Upon filing with the Commission, pursuant to Rule 467(a) (if in connection with an offering being made contemporaneously in the United States and Canada).

B. ☐ At some future date (check the appropriate box below):

| 1. ☐ | pursuant to Rule 467(b) on ( ) at ( ). |

| 2. ☐ | pursuant to Rule 467(b) on ( ) at ( ) because the securities regulatory authority in the review jurisdiction has issued a receipt or notification of clearance on ( ). |

| 3. ☐ | pursuant to Rule 467(b) as soon as practicable after notification of the Commission by the Registrant or the Canadian securities regulatory authority of the review jurisdiction that a receipt or notification of clearance has been issued with respect hereto. |

| 4. ☐ | after the filing of the next amendment to this Form (if preliminary material is being filed). |

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to the home jurisdiction’s shelf prospectus offering procedures, check the following box. ☐

Table of Contents

PART I

INFORMATION REQUIRED TO BE DELIVERED TO OFFEREES OR PURCHASERS

Table of Contents

SHORT FORM PROSPECTUS

| New Issue | February 3, 2017 |

US$65,047,500

10,325,000 Common Shares

This short form prospectus qualifies the distribution (the “Offering”) of 10,325,000 common shares (the “Offered Shares”) in the capital of Fortuna Silver Mines Inc. (“Fortuna” or the “Company”) at a price of US$6.30 per Offered Share (the “Offering Price”). The Offered Shares will be sold pursuant to an underwriting agreement (the “Underwriting Agreement”) dated January 24, 2017 among the Company, Raymond James Ltd. (“RJL”), BMO Nesbitt Burns Inc., Scotia Capital Inc., CIBC World Markets Inc. and National Bank Financial Inc. (collectively, the “Underwriters”). The Offering Price was determined by negotiation between the Company and the Underwriters.

The common shares of Fortuna (the “Common Shares”) are listed on the Toronto Stock Exchange (the “TSX”) under the symbol “FVI” and on the New York Stock Exchange (the “NYSE”) under the symbol “FSM”. On February 2, 2017, the last trading day before the date hereof, the closing price of the Common Shares was C$8.21 on the TSX and US$6.28 on the NYSE. The TSX has conditionally approved the listing of the Offered Shares on the TSX, subject to Fortuna fulfilling all the listing requirements of the TSX on or before April 24, 2017. The NYSE has approved the listing of the Offered Shares.

Price: US$6.30 per Offered Share

| Price to the Public |

Underwriters’ Fee(1) |

Net Proceeds to the Company(2) |

||||||||||

| Per Offered Share |

US$ | 6.30 | US$ | 0.29925 | US$ | 6.00075 | ||||||

| Total(3) |

US$ | 65,047,500 | US$ | 3,089,756 | US$ | 61,957,744 | ||||||

| Notes: |

| (1) | Pursuant to the terms and conditions of the Underwriting Agreement, the Company has agreed to pay a cash commission to the Underwriters (the “Underwriters’ Fee”) equal to US$0.29925 per Offered Share. See “Plan of Distribution”. |

| (2) | After deducting the Underwriters’ Fee, but before deducting the other expenses of the Offering, estimated to be US$1,300,000, which will be paid from the proceeds of the Offering. |

| (3) | The Company has granted the Underwriters an option (the “Over-Allotment Option”), exercisable in whole or in part in the sole discretion of the Underwriters until 5:00pm (Vancouver time) on the date that is 30 days after the Closing Date (as defined below), to purchase up to an additional 1,548,750 Common Shares (the “Additional Shares”) of the Company on the same terms as set forth above, solely to cover over-allotments, if any, and for market stabilization purposes. If the Over-Allotment Option is exercised in full, the total number of Common Shares issued pursuant to the Offering will be 11,873,750, the total price to the public under the Offering will be US$74,804,625, the total Underwriters’ Fee will be US$3,553,220 and the aggregate net proceeds to the Company will be US$71,251,405, before deducting the other expenses of the Offering, estimated to be US$1,300,000. This short form prospectus also qualifies under applicable Canadian securities laws the grant of the Over-Allotment Option and the distribution of the Additional Shares to be issued upon the exercise of such Over-Allotment Option. A person who acquires Additional Shares issuable upon exercise of the Over-Allotment Option acquires such Additional Shares under this short form prospectus, regardless of whether the over-allotment position is ultimately filled through the exercise of the Over-Allotment Option or secondary market purchases. See “Plan of Distribution.” Unless the context otherwise requires, the term “Offered Shares” includes any Additional Shares issued upon the exercise of the Over-Allotment Option. |

Table of Contents

An investment in the Offered Shares involves a high degree of risk. It is important for a prospective purchaser to consider the risk factors described or referred to and incorporated by reference in this short form prospectus. See “Cautionary Note Regarding Forward-Looking Statements” and “Risk Factors ”.

Investors should rely only on the information contained or incorporated by reference in this short form prospectus. The Company and the Underwriters have not authorized anyone to provide investors with different information. The Underwriters are offering to sell, and seeking offers to buy, the Offered Shares only in jurisdictions where, and to persons to whom, offers and sales are lawfully permitted. Investors should not assume that the information contained or incorporated by reference in this short form prospectus is accurate as of any date other than the date on the front of this short form prospectus or the applicable document incorporated by reference herein. The Company’s business, operating results, financial condition and prospects may have changed since that date.

The Underwriters, as principals, conditionally offer the Offered Shares, subject to prior sale, if, as and when issued by the Company and accepted by the Underwriters in accordance with the conditions contained in the Underwriting Agreement referred to under “Plan of Distribution” and subject to approval of certain Canadian legal matters on behalf of the Company by Blake, Cassels & Graydon LLP, certain United States legal matters on behalf of the Company by Skadden, Arps, Slate, Meagher & Flom LLP, certain Canadian legal matters on behalf of the Underwriters by Stikeman Elliott LLP and certain United States legal matters on behalf of the Underwriters by Paul, Weiss, Rifkind, Wharton & Garrison LLP. In connection with the Offering and subject to applicable laws, the Underwriters may over-allot or effect transactions that are intended to stabilize or maintain the market price of the Offered Shares at levels other than that which might otherwise prevail in the open market. Such transactions, if commenced, may be discontinued at any time and must be brought to an end after a limited period. See “Plan of Distribution”. The Underwriters may offer the Offered Shares at prices lower than the Offering Price. Notwithstanding any reduction by the Underwriters of the Offering Price, the Company will still receive net proceeds of US$6.00075 per Offered Share pursuant to this Offering. See “Plan of Distribution”.

Subscriptions for Offered Shares will be received subject to rejection or allotment in whole or in part and the Underwriters reserve the right to close the subscription books at any time without notice. Closing is expected to take place on or about February 9, 2017, or such other date as may be agreed between the Company and the Underwriters, but in any event not later than 42 days following the date of a final receipt for the final short form prospectus (the “Closing Date”).

It is expected that the Company will arrange for an instant deposit of the Offered Shares to or for the account of the Underwriters with CDS Clearing and Depository Services Inc. (“CDS”) or its nominee on the Closing Date, against payment of the aggregate purchase price for the Offered Shares. A purchaser of Offered Shares will receive only a customer confirmation from the registered dealer, which is a CDS participant, and from or through which Offered Shares are purchased. See “Plan of Distribution”.

The following table sets out the number of Additional Shares that may be issued by the Company to the Underwriters under the Over-Allotment Option:

| Underwriters’ Position |

Maximum Size |

Percentage of Offering |

Exercise Period |

Exercise Price | ||||

| Over-Allotment Option |

1,548,750 Additional Shares | 15% | Up to 30 days after the Closing Date | US$6.30 per Additional Share |

Scotia Capital Inc. (“Scotia”) is an affiliate of the lender to Fortuna under the Credit Facility (defined herein). Consequently, we may be considered a “connected issuer” of Scotia under applicable securities laws in Canada in connection with the Offering. See “Plan of Distribution”.

The Company’s head office and registered office are located at 200 Burrard Street, Suite 650, Vancouver, British Columbia, V6C 3L6, Canada.

ii

Table of Contents

Jorge Ganoza Durant, Robert Gilmore, Mario Szotlender and Alfredo Sillau, directors of the Company and Luis Ganoza Durant, Chief Financial Officer of the Company, reside outside of Canada and have appointed the Company at its Vancouver head office address as their agent for services for process in Canada. Prospective purchasers are advised that it may not be possible for investors to enforce judgments obtained in Canada against any person or company that is incorporated, continued or otherwise organized under the laws of a foreign jurisdiction or resides outside of Canada, even if the party has appointed an agent for service of process.

The Offering is being made by a Canadian issuer that is permitted under a multi-jurisdictional disclosure system (the “MJDS”) adopted by Canada and the United States to prepare this short form prospectus in accordance with the disclosure requirements of Canada. Prospective investors should be aware that such requirements are different from those of the United States. Financial statements included or incorporated by reference herein have been prepared in accordance with International Financial Reporting Standards, as issued by the International Accounting Standards Board (“IFRS”), and thus may not be comparable to financial statements of United States companies.

Prospective investors should be aware that the acquisition of the Offered Shares may have tax consequences both in Canada and the United States, including the Canadian federal income tax consequences applicable to a foreign controlled Canadian corporation that acquires Offered Shares. Such consequences, for investors who are resident in, or citizens of, the United States, may not be described fully in this short form prospectus. Investors should read the tax discussion in this short form prospectus and consult their own tax advisors with respect to their own particular circumstances. See “Certain Canadian Federal Income Tax Considerations” and “Certain United States Federal Income Tax Considerations”.

The enforcement by investors of civil liabilities under the United States federal securities laws may be affected adversely by the fact that the Company is incorporated under the laws of the Province of British Columbia, Canada, that some or all of its officers, directors and experts named in this short form prospectus are residents of a country other than the United States, and that all or a substantial portion of the assets of the Company and the assets of those officers, directors and experts are located outside the United States.

Neither the United States Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of the Offered Shares nor passed upon the accuracy or adequacy of this short form prospectus. Any representation to the contrary is a criminal offence.

iii

Table of Contents

| 2 | ||||

| 2 | ||||

| 3 | ||||

| 6 | ||||

| 6 | ||||

| 6 | ||||

| 7 | ||||

| 8 | ||||

| 9 | ||||

| 13 | ||||

| 46 | ||||

| 59 | ||||

| 60 | ||||

| 61 | ||||

| 62 | ||||

| 62 | ||||

| 63 | ||||

| 66 | ||||

| 69 | ||||

| 73 | ||||

| 73 | ||||

| 73 | ||||

Unless otherwise indicated, all information in this short form prospectus assumes no exercise of the Over-Allotment Option.

In this short form prospectus and the documents incorporated by reference herein, unless the context otherwise requires, references to “we”, “us”, “our” or similar terms, as well as references to “Fortuna” or the “Company”, refer to Fortuna Silver Mines Inc. together with its subsidiaries.

1

Table of Contents

Unless otherwise indicated or the context otherwise requires, all dollar amounts and references to “C$” are to Canadian dollars and references to “US$” are to United States dollars.

The following table sets forth, for each of the periods indicated: (i) the high and low closing exchange rates during each period; (ii) the average noon exchange rate for each period; and (iii) the period end noon exchange rate, of Canadian dollars into United States dollars, as reported by the Bank of Canada:

| Year Ended December 31, |

Nine Months Ended September 30, |

|||||||||||||||

| 2015 (US$) |

2014 (US$) |

2016 (US$) |

2015 (US$) |

|||||||||||||

| High |

$ | 0.8527 | $ | 0.9422 | $ | 0.7972 | $ | 0.8527 | ||||||||

| Low |

$ | 0.7148 | $ | 0.8589 | $ | 0.6854 | $ | 0.7455 | ||||||||

| Average |

$ | 0.7833 | $ | 0.9058 | $ | 0.7574 | $ | 0.7945 | ||||||||

| Period End |

$ | 0.7225 | $ | 0.8620 | $ | 0.7624 | $ | 0.7466 | ||||||||

The noon exchange rate on February 2, 2017, as reported by the Bank of Canada, was C$1.00 equals US$0.7681.

The financial statements of the Company incorporated by reference herein are reported in United States dollars and have been prepared in accordance with IFRS.

CAUTIONARY NOTE FOR UNITED STATES INVESTORS

The Company is a Canadian “foreign private issuer” as defined in Rule 3b-4 under the United States Securities Exchange Act of 1934, as amended (the “Exchange Act”), which is permitted to prepare the technical information contained herein in accordance with the requirements of the securities laws in effect in Canada, which differ from the requirements of U.S. securities laws.

Canadian standards, including National Instrument 43-101 (“NI 43-101”), differ significantly from the requirements of the Exchange Act, and Mineral Reserve and Mineral Resource information contained or incorporated by reference in this short form prospectus may not be comparable to similar information disclosed by United States companies. In particular, and without limiting the generality of the foregoing, the term Mineral Resource does not equate to the term “reserve”. Under United States standards, mineralization may not be classified as a “reserve” unless the determination has been made that the mineralization could be economically and legally produced or extracted at the time the reserve determination is made. Among other things, all necessary permits would need to be in hand or issuance imminent in order to classify mineralized material as reserves under SEC standards. The SEC’s current disclosure standards normally do not permit the inclusion of information concerning Measured Mineral Resources, Indicated Mineral Resources or Inferred Mineral Resources or other descriptions of the amount of mineralization in mineral deposits that do not constitute “reserves” by United States standards in documents filed with the SEC. United States investors are cautioned not to assume that all or any part of Measured Mineral Resources or Indicated Mineral Resources will ever be converted into reserves. United States investors should also understand that Inferred Mineral Resources have an even greater amount of uncertainty as to their existence and as to their economic and legal feasibility. It cannot be assumed that all or any part of an Inferred Mineral Resource will ever be upgraded to a category having a higher degree of certainty. Under Canadian rules, estimates of Inferred Mineral Resources may not form the basis of Feasibility or Pre-Feasibility Studies except in rare cases. Investors are cautioned not to assume that all or any part of an Inferred Mineral Resource exists or is economically or legally mineable. Disclosure of “contained tonnes” in a Mineral Resource estimate is permitted disclosure under NI 43-101 provided that the grade or quality and the quantity of each category is stated; however, the SEC normally only permits issuers to report

2

Table of Contents

mineralization that does not constitute “reserves” by SEC standards as in place tonnage and grade without reference to unit measures. The requirements of NI 43-101 for identification of Mineral Reserves are also not the same as those of the SEC, and Mineral Reserves reported in compliance with NI 43-101 may not qualify as “reserves” under SEC standards. Accordingly, information contained in this short form prospectus and the documents incorporated by reference herein containing descriptions of mineral deposits may not be comparable to similar information made public by U.S. companies subject to the reporting and disclosure requirements under the U.S. federal securities laws and the rules and regulations thereunder. See “Technical Information – Summary of Mineral Reserve and Mineral Resource Estimates” for the definition of certain technical terms under applicable Canadian standards.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

Certain statements contained in this short form prospectus and any documents incorporated by reference into this short form prospectus constitute forward-looking statements within the meaning of the U.S. Private Securities Litigation Reform Act of 1995 and Section 21E of the Exchange Act and forward-looking information within the meaning of applicable Canadian securities legislation (collectively, “forward-looking statements”). All statements included or incorporated by reference herein, other than statements of historical fact, are forward-looking statements and are subject to a variety of known and unknown risks and uncertainties which could cause actual events or results to differ materially from those reflected in the forward-looking statements. The forward-looking statements included or incorporated by reference in this short form prospectus include, without limitation, statements relating to:

| • | Production guidance for 2017 at the San Jose Mine and the Caylloma Mine; |

| • | cash cost estimates and all-in sustaining cash cost estimates for 2017 at the Caylloma Mine and San Jose Mine; |

| • | Mineral Reserves and Mineral Resources, as they involve implied assessment, based on estimates and assumptions that the Mineral Reserves and Mineral Resources described exist in the quantities predicted or estimated and can be profitably produced in the future; |

| • | timing for delivery of materials and equipment for the Company’s properties; |

| • | the sufficiency of the Company’s cash position and its ability to raise equity capital or access debt facilities; |

| • | the Company’s planned processing and estimated capital investments for mine development and brownfields exploration at the San Jose Mine; |

| • | the Company’s planned processing and estimated capital investments for mine development, plant optimization and brownfields exploration at the Caylloma Mine; |

| • | the Company’s plans for development of the Lindero Project (as defined herein); |

| • | maturities of the Company’s financial liabilities, finance leases and other contractual commitments; |

| • | expiry dates of bank letters of guarantee; |

| • | estimated mine closure costs; |

| • | management’s expectation that any investigations, claims, and legal, labor and tax proceedings arising in the ordinary course of business will not have a material effect on the results of operations or financial condition of the Company; and |

| • | the Offering, including the expected closing date of the Offering, the estimated net proceeds from the Offering and our intended use of the net proceeds from the Offering. |

3

Table of Contents

Often, but not always, these forward-looking statements can be identified by the use of words such as “anticipates”, “believes”, “plans”, “estimates”, “expects”, “forecasts”, “scheduled”, “targets”, “possible”, “strategy”, “potential”, “intends”, “advance”, “goal”, “objective”, “projects”, “budget”, “calculates” or statements that events, “will”, “may”, “could” or “should” occur or be achieved and similar expressions, including negative variations.

Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Company to be materially different from any results, performance or achievements expressed or implied by the forward-looking statements. Such uncertainties and factors include, among others:

| • | operational risks associated with mining and mineral processing; |

| • | uncertainty relating to Mineral Resource and Mineral Reserve estimates; |

| • | uncertainty relating to capital and operating costs, production schedules and economic returns; |

| • | risks associated with the Company’s mineral exploration, project development and infrastructure; |

| • | risks associated with environmental matters, including the Company’s compliance with environmental laws and regulations and potential liability claims against the Company; |

| • | uncertainty relating to nature and climate conditions; |

| • | risks associated with changes in national and local government legislation, taxation, controls, regulations and political or economic developments in countries in which the Company does or may carry on business; |

| • | risks associated with political instability and changes to the regulations governing the Company’s business operations; |

| • | risks relating to the termination of the Company’s mining concessions in certain circumstances; |

| • | risks related to opposition of the Company’s exploration, development and operational activities; |

| • | risks related to the Company’s ability to obtain adequate financing for planned exploration and development activities; |

| • | risks associated with the Company’s substantial reliance on the Caylloma Mine and the San Jose Mine for revenues; |

| • | risks associated with property title matters; |

| • | risks related to the integration of businesses and assets acquired by the Company; |

| • | risks associated with the Company’s reliance on key personnel; |

| • | risks associated with the Company’s reliance on local counsel and advisors and its management and board of directors in foreign jurisdictions; |

| • | uncertainty relating to potential conflicts of interest involving the Company’s directors and officers; |

| • | risks associated with the adequacy of the Company’s insurance coverage; |

| • | risks related to the Company’s compliance with the Sarbanes-Oxley Act; |

| • | risks related to the foreign corrupt practices regulations and anti-bribery laws; |

| • | uncertainty related to potential legal proceedings involving the Company; |

| • | uncertainty relating to general economic conditions; |

| • | risks associated with competition in the mining industry; |

4

Table of Contents

| • | uncertainty relating to fluctuations in metal prices and the marketability of metals acquired by the Company; |

| • | risks associated with entering into commodity forward and option contracts for base metals production; |

| • | uncertainty relating to fluctuations in currency exchange rates and the Company’s operating expenses; |

| • | uncertainty relating to concentrate treatment charges and transportation costs; |

| • | uncertainty relating to the sufficiency of monies allotted by the Company for land reclamation; |

| • | risks related to the volatility of the trading price of the Company’s Common Shares; |

| • | risks related to shareholder dilution as a result of further equity financings; |

| • | risks related to future insufficient liquidity resulting from a decline in the price of the Company’s Common Shares; |

| • | uncertainty relating to the Company’s ability to pay dividends in the future; |

| • | uncertainty relating to the enforcement of U.S. judgments against the Company; and |

| • | risks related to the broad discretion of the Company over the use of the proceeds raised hereunder. |

This list is not exhaustive of the factors that may affect any of our forward-looking statements. Forward-looking statements are statements about the future and are inherently uncertain, and our actual achievements or other future events or conditions may differ materially from those reflected in the forward-looking statements due to a variety of risks, uncertainties and other factors, including, without limitation, those referred to in this short form prospectus under the heading “Risk Factors” and in the AIF (as defined below).

Forward-looking statements contained in this short form prospectus are based on the assumptions, beliefs, expectations and opinions of management, including but not limited to:

| • | all required third party contractual, regulatory and governmental approvals will be obtained for the exploration, development, construction and production of its properties; |

| • | there being no significant disruptions affecting operations, whether relating to labor, supply, power, damage to equipment or other matter; |

| • | permitting, construction, development and expansion proceeding on a basis consistent with the Company’s current expectations; |

| • | expected trends and specific assumptions regarding metal prices and currency exchange rates; |

| • | prices for and availability of fuel, electricity, parts and equipment and other key supplies remaining consistent with current levels; |

| • | production forecasts meeting expectations; and |

| • | the accuracy of the Company’s current Mineral Resource and Mineral Reserve estimates. |

Although the Company has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause actions, events or results not to be as anticipated, estimated or intended. These forward-looking statements are made as of the date of this short form prospectus. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers are cautioned not to place undue reliance on forward-looking statements. Except as required by law, the Company does not assume the obligation to revise or update these forward looking-statements after the date of this document or to revise them to reflect the occurrence of future unanticipated events.

5

Table of Contents

NOTICE REGARDING NON-IFRS MEASURES

This short form prospectus and the documents incorporated by reference herein include certain terms or performance measures that are not defined under IFRS, including but not limited to cash costs and all-in sustaining costs. The Company believes that, in addition to conventional measures prepared in accordance with IFRS, certain investors use this information to evaluate the Company’s performance. The data presented is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. These non-IFRS measures should be read in conjunction with the Company’s financial statements and management’s discussion and analysis incorporated by reference herein. See “Non-GAAP Financial Measures” in the Company’s management’s discussion and analysis for the three and nine months ended September 30, 2016 regarding the Company’s use of non-IFRS measures.

A registration statement on Form F-10 (the “Registration Statement”) has been filed by the Company with the SEC in respect of the Offering. The Registration Statement, of which this short form prospectus constitutes a part, contains additional information not included in this short form prospectus, certain items of which are contained in the exhibits to the Registration Statement, pursuant to the rules and regulations of the SEC.

In addition to the Company’s continuous disclosure obligations under the securities laws of the provinces of Canada, the Company is subject to the reporting requirements of the Exchange Act, and in accordance therewith the Company files with or furnishes to the SEC reports and other information. The reports and other information that the Company files with or furnishes to the SEC are prepared in accordance with the disclosure requirements of Canada, which differ in certain respects from those of the United States. As a foreign private issuer, the Company is exempt from the rules under the Exchange Act prescribing the furnishing and content of proxy statements, and the Company’s officers, directors and principal shareholders are exempt from the reporting and short-swing profit recovery provisions contained in Section 16 of the Exchange Act. In addition, the Company may not be required to publish financial statements as promptly as U.S. companies. Copies of any documents that the Company has filed with or furnished to the SEC may be read at the SEC’s public reference room at Room 1500, 100 F Street N.E., Washington, D.C., 20549. Copies of the same documents may also be obtained from the public reference room of the SEC by paying a fee. Please call the SEC at 1-800-SEC-0330 or access its website at www.sec.gov for further information about the public reference room.

DOCUMENTS FILED AS PART OF THE REGISTRATION STATEMENT

The following documents have been or will be filed or furnished with the SEC as part of the Registration Statement: (i) the documents listed under the heading “Documents Incorporated by Reference”; (ii) powers of attorney from certain of our directors and officers; (iii) consents of each of the following: Blake, Cassels & Graydon LLP, Stikeman Elliott LLP, Deloitte LLP, Davidson & Company LLP, Eric Chapman and Edwin Gutierrez; and (iv) the Underwriting Agreement.

6

Table of Contents

DOCUMENTS INCORPORATED BY REFERENCE

Information has been incorporated by reference in this short form prospectus from documents filed with securities commissions or similar authorities in Canada and with the SEC. Copies of the documents incorporated herein by reference may be obtained on request without charge from the Corporate Secretary of the Company at 200 Burrard Street, Suite 650, Vancouver, British Columbia, Canada V6C 3L6, and are also available electronically at www.sedar.com and on the SEC’s EDGAR system at www.sec.gov.

The following documents which have been filed by the Company with various securities commissions or similar authorities in Canada in which the Company is a reporting issuer and with the SEC are specifically incorporated by reference into, and form an integral part of, this short form prospectus:

| (a) | the Company’s annual information form dated March 24, 2016 for the year ended December 31, 2015 (except for the technical report entitled Fortuna Silver Mines Inc.: Caylloma Property, Caylloma District, Peru dated as of March 22, 2013, as amended April 15, 2013 and the technical report entitled Fortuna Silver Mines Inc.: San Jose Property, Oaxaca, Mexico dated as of November 22, 2013, each prepared by Eric Chapman and Thomas Kelly, incorporated by reference therein, and the information derived from such technical reports included therein) (the “AIF”); |

| (b) | the Company’s audited consolidated financial statements as at and for the years ended December 31, 2015 and 2014, together with the report of the independent registered public accounting firm thereon; |

| (c) | the Company’s management’s discussion and analysis for the year ended December 31, 2015; |

| (d) | the Company’s unaudited condensed consolidated interim financial statements for the three and nine months ended September 30, 2016 and 2015 (the “Q3 2016 Financial Statements”); |

| (e) | the Company’s management’s discussion and analysis for the three and nine months ended September 30, 2016 (the “Q3 2016 MD&A”); |

| (f) | the Company’s management information circular as at April 27, 2016, prepared in connection with the Company’s annual general meeting of shareholders held on June 16, 2016; |

| (g) | the Company’s material change report dated June 9, 2016 announcing the proposed acquisition of all of the issued and outstanding common shares of Goldrock Mines Corp. (“Goldrock”); |

| (h) | the Company’s material change report dated July 28, 2016 announcing the closing of the acquisition of all of the issued and outstanding common shares of Goldrock; |

| (i) | the Company’s business acquisition report dated November 2, 2016 prepared in connection with the acquisition of all of the issued and outstanding common shares of Goldrock; and |

| (j) | the Company’s material change report dated January 27, 2017 with respect to the announcement of the Offering. |

A reference herein to this short form prospectus also means any and all documents incorporated by reference in this short form prospectus. Any document of the type referred to above, including audited annual consolidated financial statements, unaudited interim consolidated financial statements and the related management’s discussion and analysis, material change reports (excluding confidential material change reports), any business acquisition reports, the content of any news release disclosing financial information for a period more recent than the period for which financial information is deemed incorporated by reference in this short form prospectus and certain other disclosure documents as set forth in Item 11.1 of Form 44-101F1 of National Instrument 44-101 of the Canadian Securities Administrators filed by the Company with the securities commissions or similar regulatory authorities in Canada after the date of this short form prospectus and prior to the termination of the Offering shall be deemed to be incorporated by reference in this short form prospectus.

In addition, to the extent that any document or information incorporated by reference into this short form prospectus is filed with, or furnished to, the SEC pursuant to the Exchange Act after the date of this short form prospectus, such document or information will be deemed to be incorporated by reference as an exhibit to the Registration Statement (in the case of a report on Form 6-K, if and to the extent expressly provided therein).

7

Table of Contents

Any statement contained in this short form prospectus or in a document incorporated or deemed to be incorporated by reference herein will be deemed to be modified or superseded for the purposes of this short form prospectus to the extent that a statement contained in this short form prospectus or in any other subsequently filed document which also is, or is deemed to be, incorporated by reference into this short form prospectus modifies or supersedes that statement. The modifying or superseding statement need not state that it has modified or superseded a prior statement or include any other information set forth in the document that it modifies or supersedes. The making of a modifying or superseding statement shall not be deemed an admission for any purposes that the modified or superseded statement when made, constituted a misrepresentation, an untrue statement of a material fact or an omission to state a material fact that is required to be stated or that is necessary to prevent a statement that is made from being false or misleading in the circumstances in which it was made. Any statement so modified or superseded shall not be deemed, except as so modified or superseded, to constitute part of this short form prospectus.

References to our website in any documents that are incorporated by reference into this short form prospectus do not incorporate by reference the information on such website into this short form prospectus, and we disclaim any such incorporation by reference.

Any “template version” of any “marketing materials” (as such terms are defined under applicable Canadian securities laws) that is used by the Underwriters in connection with the Offering does not form a part of this short form prospectus to the extent that the contents of the template version of the marketing materials have been modified or superseded by a statement contained in the final short form prospectus. Any template version of any marketing materials that has been, or will be, filed under the Company’s profile on SEDAR at www.sedar.com and on EDGAR at www.sec.gov before the termination of the distribution under the Offering (including any amendments to, or an amended version of, any template version of any marketing materials) is deemed to be incorporated by reference into the final short form prospectus.

8

Table of Contents

The Company was incorporated on September 4, 1990 pursuant to the Company Act (British Columbia) under the name Jopec Resources Ltd. and subsequently transitioned under the Business Corporations Act (British Columbia). On February 3, 1999, the Company changed its name to Fortuna Ventures Inc. On June 28, 2005, the Company changed its name to Fortuna Silver Mines Inc.

The management head office of the Company is located at Piso 5, Av. Jorge Chávez #154, Miraflores, Lima, Peru. The corporate office and registered office of the Company are located at 200 Burrard Street, Suite 650, Vancouver, BC V6C 3L6.

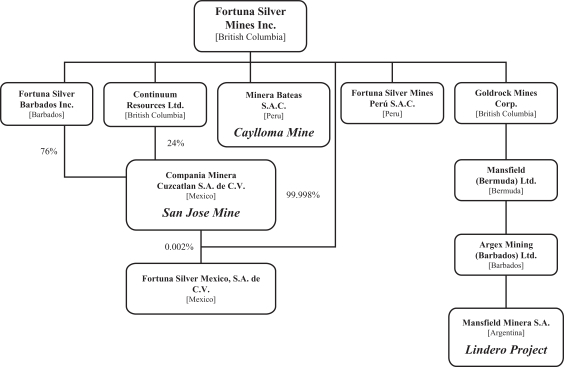

The Company carries on a significant portion of its business through a number of 100%-owned subsidiaries, held either directly or indirectly, as follows:

Fortuna is engaged in precious and base metals mining and related activities, including exploration, extraction, and processing. Fortuna operates the Caylloma zinc, lead and silver mine (the “Caylloma Mine”) in southern Peru and the San Jose silver and gold mine (the “San Jose Mine”) in southern Mexico. The Company is also developing its recently acquired Lindero gold project (the “Lindero Project”) in Argentina and is conducting an exploration program in Serbia.

Recent Developments

Production Data

Production data for 2016 for the San Jose Mine and the Caylloma Mine are summarized in the table below. The Company produced approximately 7.4 million ounces of silver and 46,600 ounces of gold or 10.2 million Ag Eq* ounces.

| (*) | Silver equivalent is calculated using a silver to gold ratio of 60 to 1 |

9

Table of Contents

Table 1: 2016 Consolidated Operating Results

| Q4 2016 | 2016 | |||||||||||||||||||||||

| Caylloma, Peru |

San Jose, Mexico |

Consolidated | Caylloma, Peru |

San Jose, Mexico |

Consolidated | |||||||||||||||||||

| Processed Ore |

||||||||||||||||||||||||

| Tonnes Milled |

135,121 | 273,036 | 514,828 | 905,467 | ||||||||||||||||||||

| Average tpd milled |

1,501 | 3,103 | 1,438 | 2,596 | ||||||||||||||||||||

| Silver |

||||||||||||||||||||||||

| Grade (g/t) |

82 | 225 | 90 | 228 | ||||||||||||||||||||

| Recovery (%) |

82.43 | 92.48 | 84.39 | 92.36 | ||||||||||||||||||||

| Production (oz) |

291,988 | 1,828,110 | 2,120,098 | 1,255,981 | 6,124,235 | 7,380,217 | ||||||||||||||||||

| Gold |

||||||||||||||||||||||||

| Grade (g/t) |

0.21 | 1.69 | 0.20 | 1.72 | ||||||||||||||||||||

| Recovery (%) |

17.03 | 92.24 | 16.41 | 92.07 | ||||||||||||||||||||

| Production (oz) |

152 | 13,660 | 13,812 | 533 | 46,018 | 46,551 | ||||||||||||||||||

| Lead |

||||||||||||||||||||||||

| Grade (%) |

2.60 | 3.06 | ||||||||||||||||||||||

| Recovery (%) |

94.17 | 94.10 | ||||||||||||||||||||||

| Production (lbs) |

7,290,060 | 7,290,060 | 32,673,479 | 32,673,479 | ||||||||||||||||||||

| Zinc |

||||||||||||||||||||||||

| Grade (%) |

4.06 | 4.25 | ||||||||||||||||||||||

| Recovery (%) |

91.05 | 89.50 | ||||||||||||||||||||||

| Production (lbs) |

11,006,018 | 11,006,018 | 43,204,154 | 43,204,154 | ||||||||||||||||||||

Note: Metallurgical recovery for silver at the Caylloma Mine is calculated based on silver content in lead concentrate

San Jose Mine

Silver and gold production for 2016 were 6,124,235 ounces and 46,018 ounces, or 4% and 10% percent above annual guidance, respectively. Annual average head grades for silver and gold were 228 g/t and 1.72 g/t, respectively.

Caylloma Mine

Silver production for 2016 was 1,255,981 ounces or 7% above annual guidance. Annual average head grades for silver, lead and zinc were 90 g/t, 3.06% and 4.25%, respectively.

The following table sets out consolidated production and cash cost guidance for 2017:

Table 2: 2017 Consolidated Production and Cash Cost Guidance

| Silver(1) (Moz) |

Gold(2) (koz) |

Lead(3) (Mlbs) |

Zinc (Mlbs) |

Cash Cost(4) ($/t) |

AISC(4)(5) ($/oz Ag) |

|||||||||||||||||||

| San Jose Mine, Mexico |

7.1 | 51.9 | NA | NA | 56.7 | 8.4 | ||||||||||||||||||

| Caylloma Mine, Peru |

1.0 | 0.5 | 30.0 | 41.0 | 75.5 | 10.8 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total |

8.1 | 52.4 | 30.0 | 41.0 | ||||||||||||||||||||

| (1) | Million troy ounces (“Moz”) |

| (2) | Thousand troy ounces (“koz”) |

| (3) | Million pounds (“Mlbs”) |

10

Table of Contents

| (4) | See “Note Regarding Non-IFRS Measures” |

| (5) | All-in sustaining cash cost (“AISC”) |

| • | 2017 silver equivalent production guidance of 11.2 million ounces |

| • | 2017 consolidated AISC of $9.8/oz Ag |

Notes:

| 1. | Silver equivalent production does not include lead or zinc and is calculated using a silver to gold ratio of 60 to 1 |

| 2. | AISC per ounce of silver is net of by-products gold, lead and zinc |

| 3. | Total figures may not add due to rounding |

2017 Outlook

The Company plans to process 1,050,000 tonnes of ore averaging 230 g/t Ag and 1.67 g/t Au at the San Jose Mine. Capital investment at the San Jose Mine is estimated to be $23.2 million in 2017.

The Company plans to process 535,000 tonnes of ore averaging 71 g/t Ag, 2.73% Pb and 3.86% Zn at the Caylloma Mine. Capital investment at the Caylloma Mine is estimated to be $14.1 million.

The information described under “2017 Production and Cash Cost Guidance” and “2017 Outlook” constitutes forward-looking statements. Such statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to be materially different from any results, performance or achievements expressed or implied by the forward-looking statements. Such risks and uncertainties include those listed under “Cautionary Statement Regarding Forward-Looking Information” and “Risk Factors” in this short form prospectus. Readers should not place undue reliance on such forward-looking statements.

Caylloma Mine

In March 2016, the Company increased production by optimizing the Caylloma Mine, improving mill throughput to 1,430 tonnes per day (“tpd”) from 1,300 tpd.

Pursuant to an agreement dated March 10, 2016, Minera Bateas S.A.C. (“Minera Bateas”), a wholly-owned subsidiary of the Company, has granted Compania de Minas Buenaventura S.A.A. (“Buenaventura”) the right to acquire an interest in six concessions near the Caylloma Mine that do not contain any known Mineral Resources or Mineral Reserves. To earn a 51% interest in the concessions, Buenaventura must spend US$4 million in the exploration of the concessions over four years. Fulfillment of this condition would entitle Buenaventura to 51% ownership of the concessions, while Minera Bateas would own 49%. Once the joint venture is formed, Buenaventura will have the option to invest an additional US$10 million over the next two years to increase its ownership to 70%, with Minera Bateas being reduced to 30% ownership. If any party’s ownership percentage is diluted below 10%, its ownership interest will be replaced by a 3% royalty.

San Jose Mine

In early July 2016, commissioning activities on the expansion of the San Jose Mine from 2,000 tpd to 3,000 tpd were completed, allowing for an annual production rate of 7 million to 8 million ounces of silver and 50,000 to 53,000 ounces of gold. The expansion was completed on schedule and under budget.

Acquisition of Goldrock and the Lindero Project

On July 28, 2016, the Company completed the acquisition of all of the issued and outstanding shares of Goldrock by way of plan of arrangement (the “Arrangement”). Goldrock is now a wholly-owned subsidiary of Fortuna.

11

Table of Contents

Pursuant to the Arrangement, Goldrock shareholders received 0.1331 of a Common Share for each common share of Goldrock held. Outstanding warrants to purchase Goldrock common shares are now exercisable for Common Shares based on the same exchange ratio.

As a result of the Arrangement, the Company acquired a 100% interest in the Lindero Project. The Lindero Project is a porphyry gold deposit located in northwestern Argentina 260 km due west of Salta City. Mineral tenements to the Lindero Project cover 3,500 hectares comprising 35 legally surveyed pertenecias, each 100 hectares in size. A 3% provincial royalty is payable on revenue after deduction of direct processing, commercial and general and administrative costs. There are no royalties payable to any other third party in respect of the Lindero Project.

Mineralization was initially discovered in September 1999. To date, exploration work at the Lindero Project has included geologic mapping, soil geochemistry, metallurgy testing, trenching and diamond drilling which has identified two known porphyry gold-copper deposits. Initially an independent resource estimate was calculated in 2003, followed by a Prefeasibility Study completed in 2010 and a Feasibility Study completed in 2013.

Goldrock commissioned the preparation of the Technical Report Update on the Lindero Heap Leach Project, Salta Province, Argentina, dated February 23, 2016 (the “Lindero Report”) in order to update the 2013 Feasibility Study. The Lindero Report was filed on SEDAR on March 2, 2016 by Goldrock. The Lindero Report indicated that the Lindero Project represents a robust twelve year open pit mining and heap leach project. The Lindero Project has all required surface rights and has been granted all environmental and other major permits necessary for development. See “Technical Information – Summary of Mineral Reserve and Mineral Resources Estimates” below.

The Company is currently conducting a detailed review of the Lindero Report and optimization of the Lindero Project, including tradeoff metallurgical tests and detailed engineering revisions.

Changes in Directors and Officers

In recent months, Michael Iverson and Thomas Kelly retired from the board of directors of the Company. On September 26, 2016, David Laing was appointed to the board of directors of the Company and to the Company’s audit committee. Alfredo Sillau was appointed to the board of directors on November 29, 2016. On December 21, 2016, Mr. Sillau was appointed to the audit committee in the place of Mr. Laing, and Mr. Laing was appointed to the Company’s compensation committee.

David Volkert was appointed as Vice-President, Exploration as of August 8, 2016 to replace Thomas Vehrs following Mr. Vehrs’ retirement in July 2016. Effective January 1, 2017, Eric Chapman, Corporate Head of Technical Services of Fortuna, was promoted to the new position of Vice President of Technical Services.

12

Table of Contents

Prior to the filing of this short form prospectus, the Company filed an amended technical report on the Caylloma Mine and an amended technical report on the San Jose Mine, both of which are summarized below.

For a complete description of the Caylloma Mine, see the amended report entitled Fortuna Silver Mines Inc.: Caylloma Property, Caylloma District, Peru, dated January 30, 2017 (the “Caylloma Technical Report”) and for further information on the San Jose Mine, see the amended report entitled Fortuna Silver Mines Inc.: San Jose Property, Oaxaca, Mexico, dated January 30, 2017 (the “San Jose Technical Report”), each prepared by Eric Chapman, P.Geo, and Edwin Gutierrez, SME Registered Member. The Caylloma Technical Report and the San Jose Technical Report (together, the “Technical Reports”) have each been filed with Canadian securities regulatory authorities on SEDAR (available at www.sedar.com) and with the SEC on EDGAR (available at www.sec.gov).

The information contained in this section of the prospectus regarding the Caylloma Mine and the San Jose Mine has been derived from the Technical Reports, is subject to certain assumptions, qualifications and procedures described in the Technical Reports and is qualified in its entirety by the full text of the Technical Reports. Reference should be made to the full text of the Technical Reports.

Summary of Mineral Reserve and Mineral Resource Estimates

Unless otherwise indicated, the Mineral Reserves and Mineral Resources for the Company’s mines and mineral projects set forth herein have been estimated in accordance with the Canadian Institute of Mining, Metallurgy and Petroleum definition standards on Mineral Resources and Mineral Reserves (the “CIM Standards”). The following definitions are summaries from the CIM Standards:

The term “Mineral Resource” means a concentration or occurrence of solid material of economic interest in or on the Earth’s crust in such form, grade or quality and quantity that there are reasonable prospects for eventual economic extraction. The location, quantity, grade or quality, continuity and other geological characteristics of a Mineral Resource are known, estimated or interpreted from specific geological evidence and knowledge, including sampling. Material of economic interest refers to diamonds, natural solid inorganic material, or natural solid fossilized organic material including base and precious metals, coal, and industrial minerals. Mineral Resources are sub-divided, in order of increasing geological confidence, into Inferred, Indicated and Measured categories.

The term “Inferred Mineral Resource” means that part of a Mineral Resource for which quantity and grade or quality are estimated on the basis of limited geological evidence and sampling. Geological evidence is sufficient to imply but not verify geological and grade or quality continuity. An Inferred Mineral Resource is based on limited information and sampling gathered through appropriate sampling techniques from locations such as outcrops, trenches, pits, workings and drill holes.

The term “Indicated Mineral Resource” means that part of a Mineral Resource for which quantity, grade or quality, densities, shape and physical characteristics are estimated with sufficient confidence to allow the application of Modifying Factors (as defined below) in sufficient detail to support mine planning and evaluation or the economic viability of the deposit. Geological evidence is derived from adequately detailed and reliable exploration, sampling and testing and is sufficient to assume geological and grade or quality continuity between points of observation.

The term “Measured Mineral Resource” means that part of a Mineral Resource for which quantity, grade or quality, densities, shape, and physical characteristics are estimated with confidence sufficient to allow the application of Modifying Factors to support detailed mine planning and final evaluation of the economic viability of the deposit. Geological evidence is derived from detailed and reliable exploration, sampling and testing and is sufficient to confirm geological and grade or quality continuity between points of observation.

13

Table of Contents

The term “Mineral Reserve” means the economically mineable part of a Measured and/or Indicated Mineral Resource. It includes diluting materials and allowances for losses, which may occur when the material is mined or extracted and is defined by studies at Pre-Feasibility or Feasibility levels as appropriate that include application of Modifying Factors. Such studies demonstrate that, at the time of reporting, extraction could reasonably be justified. Mineral Reserves are sub-divided in order of increasing confidence into Probable Mineral Reserves (as hereinafter defined) and Proven Mineral Reserves (as hereinafter defined). Mineral Reserves are inclusive of diluting material that will be mined in conjunction with the Mineral Reserves and delivered to the treatment plant or equivalent facility.

The term “Pre-Feasibility Study” means a comprehensive study of a range of options for the technical and economic viability of a mineral project that has advanced to a stage where a preferred mining method, in the case of underground mining, or the pit configuration, in the case of an open pit, is established and an effective method of mineral processing is determined. It includes a financial analysis based on reasonable assumptions on the Modifying Factors and the evaluation of any other recurrent factors which are sufficient for a Qualified Person, acting reasonably, to determine if all or part of the Mineral Resource may be converted to a Mineral Reserve at the time of reporting.

The term “Feasibility Study” means a comprehensive technical and economic study of the selected development option for a mineral project that includes appropriately detailed assessments of applicable Modifying Factors together with any other relevant operational factors and detailed financial analysis that are necessary to demonstrate, at the time of reporting, that extraction is reasonably justified (economically mineable). The results of the study may reasonably serve as the basis for a final decision by a proponent or financial institution to proceed with, or finance, the development of the project.

The term “Probable Mineral Reserve” means the economically mineable part of an Indicated, and in some circumstances, a Measured Mineral Resource. The confidence in the Modifying Factors applying to a Probable Mineral Reserve is lower than that applying to a Proven Mineral Reserve. Probable Mineral Reserve estimates must be demonstrated to be economic, at the time of reporting, by at least a Pre-Feasibility Study.

The term “Proven Mineral Reserve” means the economically mineable part of a Measured Mineral Resource. A Proven Mineral Reserve implies a high degree of confidence in the Modifying Factors. Proven Mineral Reserve estimates must be demonstrated to be economic, at the time of reporting, by at least a Pre-Feasibility Study.

The term “Modifying Factors” means considerations used to convert Mineral Resources to Mineral Reserves. These include, but are not restricted to, mining, processing, metallurgical, infrastructure, economic, marketing, legal, environmental, social and governmental factors.

United States investors are advised that the CIM Standards differ significantly from the requirements of the Exchange Act, and Mineral Reserve and Mineral Resource information may not be comparable to similar information disclosed by United States companies. See “Cautionary Note for United States Investors”.

Caylloma Mine

Mineral Resource and Mineral Reserve estimates for the Caylloma Mine are reported as of December 31, 2015 in the following tables:

Table 3: Caylloma Mineral Reserves as of December 31, 2015

| Category |

Tonnes (000) | Ag (g/t) | Au (g/t) | Pb (%) | Zn (%) | Contained Metal | ||||||||||||||||||||||

| Ag (Moz) | Au (koz) | |||||||||||||||||||||||||||

| Proven |

254 | 138 | 0.47 | 2.05 | 2.34 | 1.1 | 3.8 | |||||||||||||||||||||

| Probable |

1,724 | 119 | 0.28 | 2.95 | 3.73 | 6.6 | 15.4 | |||||||||||||||||||||

| Proven + Probable |

1,979 | 121 | 0.30 | 2.83 | 3.55 | 7.7 | 19.3 | |||||||||||||||||||||

14

Table of Contents

Notes:

| • | There are no known legal, political, environmental or other risks that could materially affect the potential development of the Mineral Reserves. |

| • | Mineral Reserves are estimated as of June 30, 2015 and reported as of December 31, 2015, taking into account production-related depletion for the period of July 1, 2015 through December 31, 2015. |

| • | Mineral Reserves are reported above a Net Smelter Return (“NSR”) breakeven cut-off value of US$82.73/t for Animas, US$82.53/t for Animas NE, US$97.07/t San Cristóbal and US$173.74/t for Bateas, Cimoide La Plata, La Plata, and Soledad. |

| • | Metal prices used in the NSR evaluation are US$19/oz for silver, US$1,140/oz for gold, US$2,150/t for lead and US$2,300/t for zinc. |

| • | Metallurgical recovery values used in the NSR evaluation are 84.5% for silver, 39.5% for gold, 92.6% for lead, and 89.9% for zinc with the exception of the Ramal Piso Carolina vein that uses metallurgical recovery rates of 84% for Ag and 75% for Au. |

| • | Operating costs were estimated based on actual operating costs incurred from July 2014 through June 2015. |

| • | Tonnes are rounded to the nearest thousand. |

| • | Totals may not add due to rounding. |

Table 4: Caylloma Mineral Resources as of December 31, 2015

| Category |

Tonnes (000) | Ag (g/t) | Au (g/t) | Pb (%) | Zn (%) | Contained Metal | ||||||||||||||||||||||

| Ag (Moz) | Ag (Moz) | |||||||||||||||||||||||||||

| Measured |

582 | 82 | 0.36 | 1.11 | 2.16 | 1.5 | 6.7 | |||||||||||||||||||||

| Indicated |

1,269 | 84 | 0.31 | 1.14 | 2.10 | 3.4 | 12.7 | |||||||||||||||||||||

| Measured + Indicated |

1,851 | 84 | 0.32 | 1.13 | 2.12 | 5.0 | 19.3 | |||||||||||||||||||||

| Inferred |

3,392 | 132 | 0.59 | 2.20 | 3.30 | 14.3 | 64.7 | |||||||||||||||||||||

Notes:

| • | Mineral Resources are exclusive of Mineral Reserves. |

| • | Mineral Resources which are not Mineral Reserves do not have demonstrated economic viability. |

| • | There are no known legal, political, environmental or other risks that could materially affect the potential development of the Mineral Resources. |

| • | Mineral Resources are estimated as of June 30, 2015 and reported as of December 31, 2015, taking into account production-related depletion for the period of July 1, 2015 through December 31, 2015. |

| • | Mineral Resources are reported based on a NSR cut-off grade of US$50/t for wide veins and US$100/t for narrow veins. |

| • | Metal prices used in the NSR evaluation are US$19/oz for silver, US$1,140/oz for gold, US$2,150/t for lead and US$2,300/t for zinc. |

| • | Metallurgical recovery values used in the NSR evaluation are 84.5% for silver, 39.5% for gold, 92.6% for lead, and 89.9% for zinc with the exception of the Ramal Piso Carolina vein that uses metallurgical recovery rates of 84% for Ag and 75% for Au. |

| • | Operating costs were estimated based on actual operating costs incurred from July 2014 through June 2015. |

15

Table of Contents

| • | Tonnes are rounded to the nearest thousand. |

| • | Totals may not add due to rounding. |

San Jose Mine

Mineral Resource and Mineral Reserve estimates for the San Jose Mine are reported as of December 31, 2015 in the following tables:

Table 5: San Jose Mineral Reserves as of December 31, 2015

| Classification |

Tonnes (000) | Ag (g/t) | Au (g/t) | Contained Metal | ||||||||||||||||

| Ag (Moz) | Au (koz) | |||||||||||||||||||

| Proven |

282 | 237 | 1.84 | 2.1 | 16.7 | |||||||||||||||

| Probable |

3,498 | 232 | 1.72 | 26.0 | 193.3 | |||||||||||||||

| Proven + Probable |

3,780 | 232 | 1.73 | 28.2 | 209.9 | |||||||||||||||

Notes:

| • | There are no known legal, political, environmental or other risks that could materially affect the estimate of the Mineral Reserves at the San Jose Mine. |

| • | Mineral Reserves are estimated as of June 30, 2015 and reported as of December 31, 2015, taking into account production related depletion for the period through December 31, 2015. |

| • | Mineral Reserves are estimated using break-even cut-off grades based on assumed metal prices of US$19.00/oz Ag and US$1,140.00/oz Au, estimated metallurgical recovery rates of 89% for Ag and 89% for Au and projected operating costs. |

| • | Mining, processing and administrative costs were estimated based on first half of 2015 actual costs. |

| • | Totals may not add due to rounding. |

Table 6: San Jose Mineral Resources as of December 31, 2015

| Classification |

Tonnes (000) | Ag (g/t) | Au (g/t) | Contained Metal | ||||||||||||||||

| Ag (Moz) | Au (koz) | |||||||||||||||||||

| Measured |

64 | 89 | 0.71 | 0.2 | 1.5 | |||||||||||||||

| Indicated |

780 | 84 | 0.72 | 2.1 | 18.1 | |||||||||||||||

| Measured + Indicated |

844 | 84 | 0.72 | 2.3 | 19.6 | |||||||||||||||

| Inferred |

6,561 | 261 | 1.61 | 55.0 | 339.9 | |||||||||||||||

Notes:

| • | Mineral Resources are exclusive of Mineral Reserves. |

| • | Mineral Resources which are not Mineral Reserves do not have demonstrated economic viability. |

| • | There are no known legal, political, environmental or other risks that could materially affect the potential development of the Mineral Resources. |

| • | Mineral Resources are estimated as of June 30, 2015 and reported as of December 31, 2015, taking into account production related depletion for the period through December 31, 2015. |

| • | Mineral Resources are estimated at a silver equivalent (“Ag Eq”) cut-off grade of 100 g/t, with Ag Eq in g/t = Ag (g/t) + Au (g/t) x ((US$1,140/US$19) x (89/89)). |

16

Table of Contents

| • | Mining, processing and administrative costs were estimated based on first half of 2015 actual costs. |

| • | Totals may not add due to rounding. |

Lindero Project

Mineral Resource and Mineral Reserve estimates for the Lindero Project are reported as of October 23, 2015 in the following tables:

Table 7: Lindero Mineral Reserves as of October 23, 2015

| Classification |

Tonnes (000) | Au (g/t) | Contained Metal | |||||||||

| Au (koz) | ||||||||||||

| Proven |

26,349 | 0.78 | 661 | |||||||||

| Probable |

56,184 | 0.57 | 1,022 | |||||||||

| Proven + Probable |

82,533 | 0.63 | 1,684 | |||||||||

Notes:

| • | There are no known legal, political, environmental, or other risks that could materially affect the potential development of the Mineral Reserves at the Lindero Project. |

| • | Mineral Reserves are reported as of October 23, 2015. |

| • | Mineral Reserves for the Lindero Project are reported based on open pit mining within designed pit shells based on variable gold cut-off grades and gold recoveries by metallurgical type. Met type 1 cut-off 0.25 g/t Au, recovery 67.9%; Met type 2 cut-off 0.23 g/t Au, recovery 73.6%; Met type 3 cut-off 0.24 g/t Au, recovery 69.3%; and Met type 4 cut-off 0.27 g/t Au, recovery 61.7%. |

| • | The cut-off grades and pit designs are considered appropriate for long term gold prices of US$1,200/oz |

| • | Totals may not add due to rounding. |

Table 8: Lindero Mineral Resources as of October 23, 2015

| Classification |

Tonnes (000) | Au (g/t) | Contained Metal | |||||||||

| Au (koz) | ||||||||||||

| Measured |

2,051 | 0.59 | 39 | |||||||||

| Indicated |

32,716 | 0.40 | 418 | |||||||||

| Measured + Indicated |

34,767 | 0.41 | 456 | |||||||||

| Inferred |

46,500 | 0.41 | 610 | |||||||||

Notes:

| • | Mineral Resources are exclusive of Mineral Reserves. |

| • | Mineral Resources which are not Mineral Reserves do not have demonstrated economic viability. |

| • | There are no known legal, political, environmental, or other risks that could materially affect the potential development of the Mineral Resources at the Lindero Project. |

| • | Mineral Resources are reported as of October 23, 2015. |

| • | Mineral Resources are reported above a 0.2 g/t Au cut-off grade with internal dilution appropriate for a 10 x 10 x 8 m selective mining unit and no external dilution. |

17

Table of Contents

| • | Mineral Resources are reported using a long-term gold price of US$1,350/oz, mining costs at US$1.80 per tonne of material, with total processing and process G&A costs of US$5.72 per tonne of ore and an average process recovery of 70%. The refinery costs net of pay factor were estimated to be US$10.21 per ounce gold. |

| • | Mineral Resources are reported within a conceptual pit shell using a slope angle (52°) consistent with geotechnical consultant recommendations. |

| • | Totals may not add due to rounding. |

Qualified Person

Eric Chapman, P. Geo., Vice President of Technical Services is a Qualified Person for Fortuna as defined by NI 43-101. Mr. Eric Chapman has reviewed and confirmed the technical information on the Lindero Project presented in the table above.

Summary of Capital and Operating Costs

Caylloma Mine

Minera Bateas capital and operating cost estimates for the Caylloma Mine (summarized in the following tables) are based on 2015 costs. The analysis includes forward estimates for sustaining capital. Inflation is not included in the cost projections and exchange rates were estimated at S/3.30 (Peruvian Soles) to US$1. Capital costs include all investments in mine development, equipment and infrastructure necessary to upgrade the mine facilities and sustain the continuity of the operation.

As disclosed in the Caylloma Technical Report, a total of US$9.39 million was budgeted for 2016 to sustain the operation. Capital costs are split into two areas, 1) mine development and 2) equipment and infrastructure, as set out in the following table:

Table 9: Caylloma Summary of Projected Major Capital Budget for 2016

| Capital Item |

Cost (US$ in millions) | |||

| Mine Development |

||||

| Development & Infrastructure |

6.39 | |||

| Total Mine Development |

6.39 | |||

| Equipment and Infrastructure |

||||

| Mine |

0.64 | |||

| Plant |

0.98 | |||

| Maintenance & Energy |

0.85 | |||

| IT |

0.04 | |||

| Logistics, Camp, Geology, Exploration, Planning |

0.11 | |||

| Laboratory |

0.17 | |||

| Environment |

0.47 | |||

| Total Equipment and Infrastructure |

3.00 | |||

|

|

|

|||

| Total Capital Expenditure |

9.39 | |||

|

|

|

|||

18

Table of Contents

As disclosed in the Caylloma Technical Report, projected operating costs for 2016 included the cash costs (US$67.47/t) and mine operating expenses (US$12.16/t) for the operation, as set out in the following table:

Table 10: Caylloma Summary of Projected Major Operating Costs for 2016

| Operating Item |

Cost US$/t | |||

| Cash Cost |

||||

| Mine (calculated using extracted ore) |

40.17 | |||

| Plant |

12.48 | |||

| General Services |

9.07 | |||

| Administration |

5.75 | |||

| Total Cash Cost |

67.47 | |||

| Mine Operating Expenses |

||||

| Distribution |

11.54 | |||

| Management Fees |

0.21 | |||

| Community Support Activities |

0.41 | |||

| Total Mine Operating Expenses |

12.16 | |||

|

|

|

|||

| Total Cash Cost and Mine Operating Expenses |

79.63 | |||

|

|

|

|||

San Jose Mine

Compania Minera Cuzcatlan S.A. de C.V. (“Minera Cuzcatlan”) capital and operating cost estimates for 2016 for the San Jose Mine were based on predictions of costs for 2016 and the long term. Capital costs include all investments in mine development, equipment and infrastructure necessary to upgrade the mine facilities and sustain the continuity of the operation. Projected capital costs for 2016, as set out in the San Jose Technical Report, are summarized in the table below.

As disclosed in the San Jose Technical Report, a total of US$37.40 million was estimated for 2016 in order to improve the mine facilities and sustain the operation. The capital costs beyond 2016 are expected to decrease significantly to ranges between US$5 million and US$10 million annually. The capital costs are split into three areas: 1) mine development, 2) equipment and infrastructure, and (3) principal projects, as set out in the following table:

Table 11: San Jose Summary of Projected Major Capital Costs for 2016

| Capital Item |

Cost (MUS$)* | |||

| Development |

5.30 | |||

| Mine Geology |

2.30 | |||

| Mine Development |

7.60 | |||

| Mine |

2.33 | |||

| Plant |

0.49 | |||

| Maintenance & Energy |

0.01 | |||

| Safety |

0.01 | |||

| Planning and Geology |

0.16 | |||

| Laboratory |

0.18 | |||

| Other Investment |

0.28 | |||

| Equipment and Infrastructure |

3.45 | |||

| Plant Expansion |

21.86 | |||

| Tailing Filtration Plant |

0.30 | |||

| Paste Fill Plant |

0.70 | |||

| Dry Tailing Deposit |

3.50 | |||

| Principal Projects |

26.36 | |||

|

|

|

|||

| Total Capital Expenditure |

37.40 | |||

|

|

|

|||

19

Table of Contents

| * | Numbers may not total due to rounding |

Operating costs include the site costs and other operating expenses for the operation. The site costs relate to activities that are performed on the property including mine, plant, general services and administrative service costs. The other operating expenses include costs associated with distribution, general and administrative services and community support activities. As disclosed in the San Jose Technical Report, projected operating costs for 2016 are set out in the following table:

Table 12: San Jose Summary of Projected Major Operating Costs for 2016

| Operating Item |

Cost US$/t | |||

| Mine |

31.14 | |||

| Plant |

14.38 | |||

| General Services |

4.85 | |||

| Administration Mine |

1.84 | |||

| Site Costs |

52.22 | |||

| Concentrate Transportation |

4.24 | |||

| Sales and Administration Expenses |

5.74 | |||

| Community Support Activities |

0.97 | |||

| Other Operating Expenses |

10.94 | |||

|

|

|

|||

| Total Site Cost & Operating Expenses |

63.16 | |||

|

|

|

|||

Based on a mineable Proven and Probable Mineral Reserve of 3.78 million tonnes, a project life of over four years is projected. The estimates of metal production, capital costs and operating costs are combined into the discounted cash flow evaluation. The economic evaluation is treated on a project basis using a silver price of US$19 per troy ounce and a gold price of US$1,140 per troy ounce. Income taxes have been accounted for in the cash flow analysis.

The start date for the economic analysis was January 1, 2016. The financial results are presented based on future metal production, operating expenses and capital expenditure to completion basis from this date. This represents the total project costs without the production and expenditures to that date. The economic analysis is based on an annual production plan for the life of mine (“LOM”) and associated operating and capital costs. The results of the cash flow evaluation are summarized in the following table:

Table 13: San Jose Economic Evaluation Summary

| Item |

Value | |

| Payable Silver |

24.0 Moz | |

| Payable Gold |

181.0 koz | |

| Undiscounted Free Cash Flow (After-tax) |

US$181 M | |

| Pre-tax Net Present Value at 5% |

US$291 M | |

| After-tax Net Present Value at 5% |

US$180 M | |

| Pre-tax Internal Rate of Return* |

N/A | |

| After-tax Internal Rate of Return* |

N/A |

| * | Internal Rate of Return cannot be estimated since all cash flows from the evaluation day onwards are positive |

It should be noted that the economic analysis is performed utilizing only Measured and Indicated Mineral Resources, which have been converted to Proven and Probable Mineral Reserves; however, Inferred Mineral Resources which are not included in the cash flow estimate, can potentially have a positive impact on the project economics and the LOM.

20

Table of Contents

Material Properties

Caylloma Mine

Property Description, Location and Access

The Caylloma Mine is an operating underground mine located in the Caylloma mining district, 14 kilometers northwest of the town of Caylloma at the Universal Transverse Mercator (“UTM”) grid location of 8192263E, 8321387N, (WGS84, UTM Zone 19S). The Caylloma Mine consists of mineral rights for 75 mining concessions covering a total of 35,022.24 hectares, of which six concessions, that contain no known Mineral Resources or Mineral Reserves, are subject to an earn-in agreement with Buenaventura. Sixty concessions are subject to a US$60 million lien in favour of Scotiabank Peru S.A.A. In addition to these mineral rights, the Huayllacho mill-site (processing plant) is a granted concession covering 91.12 hectares.

In Peru, a mining concession does not have an expiration date but an annual fee must be paid to maintain the concession in good standing. All of the Caylloma Mine concessions are in good standing. Pursuant to the General Mining Law approved by Supreme Decree N° 014-92-EM, Minera Bateas has six years from the date of grant of the mining concessions title to reach the minimum annual production (US$100 per hectare, per year). If Minera Bateas does not reach the minimum annual production within the six-year period, Minera Bateas is required to make a payment of US$6 per hectare, per year, in addition to the fees required to keep the mineral concessions in good standing in each additional year where the minimum annual production requirement is not met.

Minera Bateas hold surface rights to the Caylloma Mine via agreements with various landowners. Access to the Caylloma Mine is an approximate 5 hour drive from Arequipa, Peru over a combination of sealed and gravel roads covering a driving distance of 225 road kilometers.

The Caylloma Mine is subject to the following royalty rights:

| (a) | Pursuant to a royalty contract signed in May 2005, Minera Bateas granted to Compania Minera Arcata, S.A. (“CMA”), a wholly owned subsidiary of Hochschild Mining plc, a 2.0% NSR which will apply after not less than a total of 21 million ounces of silver have been recovered from the Huayllacho beneficio (mill site) concession right. In June 2016, CMA assigned its NSR royalty to Lemuria Royalties Corp. As of June 30, 2016, Minera Bateas has produced a total of 15.6 million troy ounces of silver; therefore, this royalty condition has not yet been met. |