As of June 13, 2018, the Partnership began offering three classes of limited partnership interests, Class A Redeemable Units, Class D Redeemable Units and Class Z Redeemable Units. All Redeemable Units issued prior to October 31, 2016 were deemed “Class A Redeemable Units.” Class Z Redeemable Units were first issued on January 1, 2017. The rights, liabilities, risks and fees associated with investment in the Class A Redeemable Units were not changed. Class D Redeemable Units were first issued July 1, 2018. The rights, liabilities, risks, and fees associated with investment in the Class A Redeemable Units and Class Z Redeemable Units were not changed. Class A Redeemable Units, Class D Redeemable Units and Class Z Redeemable Units will each be referred to as a “Class” and collectively referred to as the “Classes.” Class A Redeemable Units are and Class D Redeemable Units were available to taxable U.S. individuals and institutions, U.S. tax exempt individuals and institutions and non-U.S. investors. Class Z Redeemable Units are offered to limited partners who receive advisory services from Morgan Stanley Smith Barney LLC (doing business as Morgan Stanley Wealth Management) (“Morgan Stanley Wealth Management”) and may also be offered to certain employees of Morgan Stanley and/or its subsidiaries (and their family members). Class A Redeemable Units, Class D Redeemable Units and Class Z Redeemable Units are identical, except that Class A Redeemable Units and Class D Redeemable Units are subject to a monthly ongoing selling agent fee equal to 1/12 of 0.75% (a 0.75% annual rate) of the adjusted net assets of Class A Redeemable Units and Class D Redeemable Units, respectively, as of the end of each month, whereas Class Z Redeemable Units are not subject to a monthly ongoing selling agent fee. Effective January 1, 2021, the Partnership ceased offering Class D Redeemable Units.

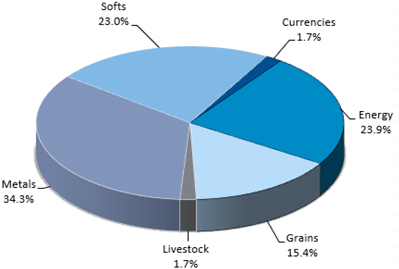

For the period January 1, 2024 through December 31, 2024, the approximate average market sector distribution for the Partnership was as follows:

At December 31, 2024, the Partnership owned approximately 41.3% of Drakewood Master. At December 31, 2023, the Partnership owned approximately 28.3% of NL Master and 35.5% of Drakewood Master. The performance of the Partnership is directly affected by the performance of the Funds.

The Partnership’s/Funds’ trading of futures, forward, swap and option contracts, if applicable, on commodities is done primarily on U.S. commodity exchanges and foreign commodity exchanges. The Partnership/Funds engage in such trading through commodity brokerage accounts maintained with MS&Co.

The General Partner and each limited partner of the Partnership share in the profits and losses of the Partnership in proportion to the amount of Partnership interest owned by each, except that no limited partner is liable for obligations of the Partnership in excess of its capital contribution and profits, if any, net of distributions or redemptions and losses, if any.

The Partnership will be liquidated upon the first of the following to occur: December 31, 2055; the net asset value per Redeemable Unit decreases to less than $400 as of the close of any business day; or under certain circumstances as set forth in the limited partnership agreement of the Partnership, as may be amended or restated from time to time (the “Limited Partnership Agreement.”) In addition, the General Partner may, in its sole discretion, cause the Partnership to dissolve if the Partnership’s aggregate net assets decline to less than $1,000,000.

4