|

|

TSX, NYSE - HBM 2021 No. 12 |

| 25 York Street, Suite 800 Toronto, Ontario Canada M5J 2V5 tel: 416 362-8181 fax: 416 362-7844 hudbay.com |

News Release |

Hudbay Announces First Quarter 2021 Results

Toronto, Ontario, May 11, 2021 - Hudbay Minerals Inc. ("Hudbay" or the "company") (TSX, NYSE:HBM) today released its first quarter 2021 financial results. All amounts are in U.S. dollars, unless otherwise noted.

First Quarter Operating and Financial Results

- Consolidated copper production in the first quarter was 24,553 tonnes at cash cost and sustaining cash costi per pound of copper produced, net of by-product credits, of $1.04 and $2.16, respectively. Consolidated gold production in the first quarter was 35,500 ounces, a record for Hudbay.

- Full year 2021 production and operating cost guidance reaffirmed; Pampacancha production commenced in April 2021, in line with guidance.

- First quarter Manitoba copper production significantly increased from 2020 levels primarily due to higher grades at 777 and higher recoveries at the Flin Flon concentrator; sales volumes were impacted by the availability of railcars during the quarter with 5,000 tonnes of copper concentrate inventory in excess of normal operating levels, valued at approximately $18 million.

- First quarter Peru sales impacted by a 10,000 tonne shipment of copper concentrate, valued at approximately $21 million, for which a payment was received but not recorded as revenue due to the timing of the shipment being delayed to early April. Peru's production in the first quarter was impacted by increased ore hardness as well as a semi-annual scheduled plant shutdown in January.

- First quarter net loss and loss per share were $60.1 million and $0.23, respectively. After adjusting for one-time financing charges mainly related to the redemption of the 2025 senior notes and a revaluation of the gold prepayment liability, first quarter adjusted net loss per sharei was $0.06. First quarter adjusted EBITDAi was $104.2 million.

- Operating cash flow before change in non-cash working capital increased to $90.7 million in the first quarter of 2021, from $86.1 million in the fourth quarter of 2020 due to higher realized metal prices, offset by lower sales volumes.

- Cash and cash equivalents decreased during the first quarter to $310.6 million, as at March 31, 2021, mainly as a result of $83.0 million of capital investments primarily for the New Britannia project and Pampacancha development activities, $50.8 million of interest payments and $31.0 million in net transaction and early redemption costs related to the refinancing of the company's 2025 notes, partially offset by cash generated from operations.

Executing on Growth Initiatives

• Announced three-year production guidance; consolidated copper and gold production are expected to increase by 36% and 125%ii, respectively, by 2023 from 2020 levels as the company brings the Pampacancha and New Britannia growth projects into production.

• Finalized the remaining land user agreement for Pampacancha in early April 2021. This provided Hudbay with full access to the site to complete pit development and commence first ore production in late April, in line with timelines assumed in the company's updated mine plan. Total 2021 growth capital guidance for Peru has increased to $25 million to include the final land user costs.

|

|

TSX, NYSE - HBM 2021 No. 12 |

• New Britannia project continues to track ahead of the original schedule and is nearing completion, with approximately 82% of the project completed at the end of April; first gold production continues to be expected early in the third quarter and the new copper flotation facility remains on track for commissioning and ramp-up in the fourth quarter of 2021.

• Announced a year-over-year increase to total mineral reserves of approximately 170,000 tonnes of contained copper and 360,000 ounces of contained gold, after adjusting for 2020 mining depletion.

• Announced an updated Constancia mine plan resulting in an increase in average annual copper production to approximately 102,000 tonnes over the next eight years at an average cash cost of $1.18 per pound of copper produced, net of by-product credits.

• Announced an updated Lalor and Snow Lake mine plan resulting in an increase in annual gold production to over 180,000 ounces during the first six years of New Britannia's operation at an average cash cost of $412 per ounce of gold produced, net of by-product credits.

• Announced a significant new discovery at the company's Copper World properties adjacent to Rosemont on wholly-owned private land. Four deposits have been identified to date with a combined strike length of over five kilometres consisting of high-grade copper sulphide and oxide mineralization at shallow depth. The follow-up 2021 exploration program has been expanded to further test the potential for additional mineralization, develop an initial inferred resource estimate and complete a preliminary economic assessment. As a result, Hudbay has increased its 2021 spending on Copper World by approximately $24 million.

• Announced a preliminary economic assessment ("PEA") for the Mason copper project with a 27-year mine life and average annual copper production of approximately 140,000 tonnes over the first ten years of full production. The PEA indicates an after-tax net present valueiii of $519 million and approximately 14% internal rate of return at $3.10 per pound copper, which increases to $773 million and approximately 15%, respectively, at $3.25 per pound copper.

• Issued $600.0 million of 4.5% senior notes due 2026 and redeemed all of the company's outstanding $600.0 million of 7.625% senior notes due 2025, thereby reducing its annual cash interest payments.

• On May 10, 2021, an amendment to the Constancia streaming agreement was signed with Wheaton Precious Metals ("Wheaton"). The amendment eliminates the requirement to deliver an additional 8,020 ounces of gold to Wheaton for not mining four million tonnes of ore from the Pampacancha deposit by June 30, 2021, while increasing the fixed gold recovery applied to Constancia ore processed during the reserve life of Pampacancha and introduces an additional potential future deposit of $4 million from Wheaton.

"Our operations remain on track to achieve full year production and unit cost guidance following a strong quarter of production at the Manitoba business unit and lower first quarter production in Peru as a result of planned mill maintenance," said Peter Kukielski, President and Chief Executive Officer. "We are very pleased to have commenced production at Pampacancha and we look forward to our first gold pour at the New Britannia mill, which remains on schedule for the third quarter. We expect to begin to see increased cash flows from these high-return investments in the second half of 2021. We also expect to significantly advance our longer-term copper growth opportunities this year, including the Rosemont, Copper World and Mason projects. We believe we will continue to leverage our exploration and development expertise to create significant value from our attractive organic growth pipeline at Hudbay."

|

|

TSX, NYSE - HBM 2021 No. 12 |

Summary of First Quarter Results

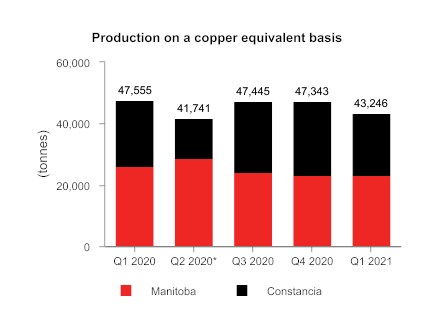

Consolidated copper production in the first quarter of 2021 was 24,553 tonnes, a 10% decrease from the fourth quarter of 2020, primarily as a result of lower mill throughput at Constancia due to a scheduled semi-annual mill maintenance shutdown, partially offset by higher copper grades at 777 and higher copper recoveries at the Flin Flon mill. Consolidated gold production increased by 10% compared to the fourth quarter of 2020 due to higher gold grades at 777, higher gold recoveries at the Flin Flon concentrator and higher gold grades at Constancia. Consolidated zinc production in the first quarter was 8% higher than the fourth quarter of 2020 due to higher zinc grades and throughput.

In the first quarter of 2021, consolidated cash cost per pound of copper produced, net of by-product creditsi, was $1.04, an increase compared to $0.43 in the fourth quarter due to lower copper production, higher operating costs and lower by-product credits. Incorporating cash sustaining capital, royalties, selling, administrative and regional costs, consolidated all-in sustaining cash cost per pound of copper produced, net of by-product creditsi, in the first quarter of 2021 was $2.37, which increased from $2.24 in the fourth quarter due to the same factors impacting cash costs, partially offset by lower cash sustaining capital.

Cash generated from operating activities in the first quarter of 2021 decreased to $51.8 million compared to $121.1 million in the fourth quarter of 2020, primarily as a result of changes in non-cash working capital and lower sales volumes. Operating cash flow before change in non-cash working capital was $90.7 million during the first quarter of 2021, reflecting a slight increase from $86.1 million in the fourth quarter. The increase in cash generated from operating activities is primarily the result of higher realized prices, offset by lower sales volumes during the quarter.

Net loss and loss per share in the first quarter of 2021 were $60.1 million and $0.23, respectively, compared to a net earnings and earnings per share of $7.4 million and $0.03, respectively, in the fourth quarter of 2020. First quarter earnings benefited from higher realized prices for all metals, which was offset by lower sales volumes of all metals due to the timing of sales in Peru and a buildup of copper concentrate in Manitoba caused by limited railcar availability. First quarter results included a $12.5 million non-cash gain on the revaluation of the gold prepayment liability but were negatively impacted by charges related to the refinancing of the 2025 senior notes, including a non-cash write off of $49.8 million connected with the exercise of the redemption option, a call premium payment of $22.9 million and a non-cash expense of unamortized transaction costs of $2.5 million in relation to the 2025 notes that were redeemed. A variable consideration adjustment to deferred gold and silver revenue resulted in a net increase to revenue of $1.6 million.

Adjusted net lossi and adjusted net loss per sharei in the first quarter of 2021 were $16.1 million and $0.06 per share after adjusting for the finance charges and the net mark-to-market loss on financial instruments, among other items. This compares to an adjusted net loss and adjusted net loss per share of $16.4 million and $0.06 per share in the fourth quarter of 2020. First quarter adjusted EBITDAi was $104.2 million, compared to $106.9 million in the fourth quarter of 2020.

First quarter Peru sales were impacted by a 10,000 tonne shipment of copper concentrate valued at approximately $21 million for which a payment was received but did not meet the revenue recognition criteria due to the delayed timing of the shipment into early April. First quarter Manitoba sales were impacted by a delay in accessing additional railcars after a strong copper production quarter resulting in approximately 5,000 tonnes of copper concentrate inventory in excess of normal operating levels, valued at approximately $18 million. Had both parcels of copper concentrate been sold during the first quarter, the company would have realized approximately $39 million of incremental revenue, assuming end of quarter commodity prices. The above quantities have been recognized as revenue in the second quarter of 2021. First quarter results were also negatively impacted by the realized copper price hedging of the company's provisionally priced copper sales.

|

|

TSX, NYSE - HBM 2021 No. 12 |

|

Financial Condition ($000s) |

|

Mar. 31, 2021 |

Dec. 31, 2020 |

Mar. 31, 2020 |

|

Cash and cash equivalents |

|

310,564 |

439,135 |

305,997 |

|

Total long-term debt |

|

1,180,798 |

1,135,675 |

988,074 |

|

Net debt1 |

|

870,234 |

696,540 |

682,077 |

|

Working capital |

|

236,281 |

306,888 |

193,045 |

|

Total assets |

|

4,549,196 |

4,666,645 |

4,366,226 |

|

Equity |

|

1,660,250 |

1,699,806 |

1,778,277 |

1 Net debt is a non-IFRS financial performance measure with no standardized definition under IFRS. For further information, please see the "Non-IFRS Financial Reporting Measures" section of this news release.

|

Consolidated Financial Performance |

|

Three Months Ended |

||

|

|

|

Mar. 31, 2021 |

Dec. 31, 2020 |

Mar. 31, 2020 |

|

Revenue |

$000s |

313,624 |

322,290 |

245,105 |

|

Cost of sales |

$000s |

261,112 |

287,923 |

267,096 |

|

Earnings (loss) before tax |

$000s |

(69,592) |

911 |

(81,452) |

|

Earnings (loss) |

$000s |

(60,102) |

7,406 |

(76,134) |

|

Basic and diluted earnings (loss) per share |

$/share |

(0.23) |

0.03 |

(0.29) |

|

Adjusted earnings (loss) per share1 |

$/share |

(0.06) |

(0.06) |

(0.15) |

|

Operating cash flow before change in non-cash working capital |

$ millions |

90.7 |

86.1 |

42.0 |

|

Adjusted EBITDA1 |

$ millions |

104.2 |

106.9 |

55.0 |

|

1 Adjusted loss per share and adjusted EBITDA are non-IFRS financial performance measures with no standardized definition under IFRS. For further information, please see the "Non-IFRS Financial Reporting Measures" section of this news release. |

||||

|

Consolidated Production and Cost Performance |

Three Months Ended |

|||

|

|

|

Mar. 31, 2021 |

Dec. 31, 2020 |

Mar. 31, 2020 |

|

Contained metal in concentrate produced1 |

|

|

|

|

|

Copper |

tonnes |

24,553 |

27,278 |

24,635 |

|

Gold |

ounces |

35,500 |

32,376 |

30,355 |

|

Silver |

ounces |

696,673 |

730,679 |

767,692 |

|

Zinc |

tonnes |

27,940 |

25,843 |

30,495 |

|

Molybdenum |

tonnes |

294 |

333 |

354 |

|

Payable metal in concentrate sold |

|

|

|

|

|

Copper |

tonnes |

20,929 |

22,963 |

24,072 |

|

Gold |

ounces |

25,383 |

35,179 |

26,574 |

|

Silver |

ounces |

509,760 |

762,384 |

575,922 |

|

Zinc2 |

tonnes |

28,343 |

28,431 |

26,792 |

|

Molybdenum |

tonnes |

284 |

457 |

431 |

|

Consolidated cash cost per pound of copper produced3 |

|

|

|

|

|

Cash cost |

$/lb |

1.04 |

0.43 |

0.98 |

|

Peru |

$/lb |

1.82 |

1.47 |

1.42 |

|

Manitoba |

$/lb |

(1.04) |

(3.48) |

(0.62) |

|

Sustaining cash cost |

$/lb |

2.16 |

1.97 |

2.05 |

|

Peru |

$/lb |

2.36 |

2.58 |

1.91 |

|

Manitoba |

$/lb |

1.62 |

(0.36) |

2.54 |

|

All-in sustaining cash cost |

$/lb |

2.37 |

2.24 |

2.17 |

1 Metal reported in concentrate is prior to deductions associated with smelter contract terms.

|

|

TSX, NYSE - HBM 2021 No. 12 |

2 Includes refined zinc metal sold.

3 Cash cost, sustaining cash cost and all-in sustaining cash cost per pound of copper produced, net of by-product credits, are non-IFRS financial performance measures with no standardized definition under IFRS. For further information, please see the "Non-IFRS Financial Reporting Measures" section of this news release.

Peru Operations Review

|

Peru Operations |

Three Months Ended |

|||

|

|

|

Mar. 31, 2021 |

Dec. 31, 2020 |

Mar. 31, 2020 |

|

Ore mined1 |

tonnes |

7,747,466 |

9,313,784 |

6,985,212 |

|

Copper |

% |

0.30 |

0.31 |

0.34 |

|

Gold |

g/tonne |

0.04 |

0.03 |

0.03 |

|

Silver |

g/tonne |

2.90 |

2.61 |

3.10 |

|

Molybdenum |

|

0.01 |

0.01 |

0.02 |

|

Ore milled |

tonnes |

6,362,752 |

7,741,714 |

6,719,466 |

|

Copper |

% |

0.33 |

0.33 |

0.34 |

|

Gold |

g/tonne |

0.04 |

0.03 |

0.03 |

|

Silver |

g/tonne |

2.84 |

2.74 |

3.13 |

|

Molybdenum |

|

0.01 |

0.02 |

0.02 |

|

Copper recovery |

% |

84.1 |

85.3 |

84.3 |

|

Gold recovery |

% |

52.0 |

52.7 |

50.2 |

|

Silver recovery |

% |

69.9 |

70.1 |

68.2 |

|

Molybdenum recovery |

|

33.4 |

28.4 |

35.0 |

|

Contained metal in concentrate |

|

|

|

|

|

Copper |

tonnes |

17,827 |

21,554 |

19,290 |

|

Gold |

ounces |

4,638 |

3,689 |

3,062 |

|

Silver |

ounces |

405,714 |

477,775 |

461,302 |

|

Molybdenum |

tonnes |

294 |

333 |

354 |

|

Payable metal sold |

|

|

|

|

|

Copper |

tonnes |

14,836 |

18,583 |

19,247 |

|

Gold |

ounces |

2,963 |

3,297 |

2,618 |

|

Silver |

ounces |

337,612 |

480,843 |

361,591 |

|

Molybdenum |

tonnes |

284 |

457 |

431 |

|

Combined unit operating cost2,3 |

$/tonne |

12.464 |

10.17 |

9.31 |

|

Cash cost3 |

$/lb |

1.82 |

1.47 |

1.42 |

|

Sustaining cash cost3 |

$/lb |

2.36 |

2.58 |

1.91 |

1 Reported tonnes and grade for ore mined are estimates based on mine plan assumptions and may not reconcile fully to ore milled.

2 Reflects combined mine, mill and general and administrative ("G&A") costs per tonne of ore milled. Reflects the deduction of expected capitalized stripping costs.

3 Combined unit cost, cash cost and sustaining cash cost are non-IFRS financial performance measures with no standardized definition under IFRS. For further information, please see the "Non-IFRS Financial Reporting Measures" section of this news release.

4 Includes approximately $4.6 million, or $0.72 per tonne, of COVID-related costs during the first quarter of 2021.

The Constancia team continues to effectively operate in an environment of strict COVID-19 measures and controls. This includes working collaboratively with the local health authorities to ensure the company's workforce and partners adhere to COVID-19 protocols while continuing to operate safely and efficiently. Full year production of all metals and unit operating costs at Constancia are on track to achieve the guidance ranges for 2021.

During the quarter, the Constancia operations produced 17,827 tonnes of copper, 4,638 ounces of gold, 405,714 ounces of silver and 294 tonnes of molybdenum. Production was lower than the fourth quarter of 2020 primarily as a result of lower throughput from a scheduled mill maintenance program in the first quarter.

|

|

TSX, NYSE - HBM 2021 No. 12 |

Ore mined during the first quarter of 2021 was lower than the fourth quarter of 2020 as mining levels were optimized for lower mill throughput while managing the level of contaminants and hardness in the ore sent to the mill. Ore milled during the first quarter of 2021 was lower compared to the fourth quarter of 2020 due to the deferral of a fourth quarter plant maintenance shutdown to January 2021 and increased ore hardness. Milled grades for copper were relatively consistent with fourth quarter levels while milled gold grades were higher as the company accessed high grade ore from the deeper banks of the pit. Recoveries of copper were lower than the previous quarter, but in line with the recently updated Constancia mine plan, and gold and silver recoveries remained consistent with the previous quarter.

Combined mine, mill and G&A unit operating costs in the first quarter of 2021 were $12.46 per tonne, and higher than the fourth quarter of 2020, primarily due to fewer tonnes of ore milled and increased operating costs related to the planned plant maintenance shutdown and enhanced COVID-19 protocols. Excluding COVID-related costs in Peru of $4.6 million, the unit operating costs in the first quarter were $11.74 per tonne. The company expects full year unit operating costs to decline and be in line with the 2021 guidance range.

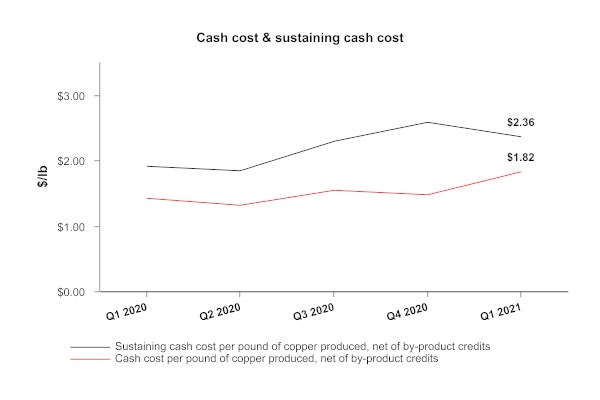

Peru's cash cost per pound of copper produced, net of by-product credits, in the first quarter of 2021 was $1.82, higher than the previous quarter primarily due to higher milling costs and lower copper production. Peru's sustaining cash cost per pound of copper produced, net of by-product credits, in the first quarter of 2021 improved to $2.36, compared to $2.58 in the prior quarter, due to lower cash sustaining capital spending in the first quarter, partially offset by the same factors affecting cash costs during the quarter.

|

|

TSX, NYSE - HBM 2021 No. 12 |

Manitoba Operations Review

|

Manitoba Operations |

Three Months Ended | |||

|

|

|

Mar. 31, 2021 |

Dec. 31, 2020 |

Mar. 31, 2020 |

|

Lalor ore mined |

tonnes |

421,602 |

468,101 |

421,518 |

|

Copper |

% |

0.57 |

0.80 |

0.70 |

|

Zinc |

% |

5.20 |

5.54 |

5.43 |

|

Gold |

g/tonne |

2.67 |

2.79 |

2.27 |

|

Silver |

g/tonne |

22.75 |

24.96 |

26.18 |

|

777 ore mined |

tonnes |

275,260 |

164,856 |

279,925 |

|

Copper |

% |

2.06 |

1.89 |

1.18 |

|

Zinc |

% |

4.00 |

2.98 |

4.11 |

|

Gold |

g/tonne |

2.39 |

1.85 |

1.82 |

|

Silver |

g/tonne |

29.32 |

21.64 |

23.86 |

|

Stall Concentrator: |

|

|

|

|

|

Ore milled |

tonnes |

361,344 |

372,624 |

369,787 |

|

Copper |

% |

0.60 |

0.79 |

0.70 |

|

Zinc |

% |

5.53 |

5.47 |

5.38 |

|

Gold |

g/tonne |

2.57 |

2.88 |

2.28 |

|

Silver |

g/tonne |

23.40 |

24.43 |

26.28 |

|

Copper recovery |

% |

85.7 |

87.1 |

86.5 |

|

Zinc recovery |

% |

91.1 |

90.9 |

91.4 |

|

Gold recovery |

% |

57.5 |

59.5 |

60.9 |

|

Silver recovery |

% |

56.2 |

60.3 |

61.1 |

|

Flin Flon Concentrator: |

|

|

|

|

|

Ore milled |

tonnes |

283,386 |

225,663 |

332,589 |

|

Copper |

% |

1.88 |

1.59 |

1.11 |

|

Zinc |

% |

4.20 |

3.87 |

4.36 |

|

Gold |

g/tonne |

2.34 |

1.99 |

1.88 |

|

Silver |

g/tonne |

28.01 |

22.65 |

24.33 |

|

Copper recovery |

% |

91.3 |

88.1 |

84.1 |

|

Zinc recovery |

% |

81.8 |

83.9 |

85.0 |

|

Gold recovery |

% |

64.0 |

56.6 |

53.5 |

|

Silver recovery |

% |

54.1 |

46.5 |

44.3 |

|

Total contained metal in concentrate |

|

|

|

|

|

Copper |

tonnes |

6,726 |

5,724 |

5,345 |

|

Zinc |

tonnes |

27,940 |

25,843 |

30,495 |

|

Gold |

ounces |

30,862 |

28,687 |

27,293 |

|

Silver |

ounces |

290,959 |

252,904 |

306,390 |

|

Total payable metal sold |

|

|

|

|

|

Copper |

tonnes |

6,093 |

4,380 |

4,852 |

|

Zinc1 |

tonnes |

28,343 |

28,431 |

26,792 |

|

Gold |

ounces |

22,420 |

31,882 |

23,956 |

|

Silver |

ounces |

172,148 |

281,541 |

214,331 |

|

Combined unit operating cost2,3 |

C$/tonne |

151 |

140 |

127 |

|

Cash cost3 |

$/lb |

(1.04) |

(3.48) |

(0.62) |

|

Sustaining cash cost3 |

$/lb |

1.62 |

(0.36) |

2.54 |

1 Includes refined zinc metal sold and payable zinc in concentrate sold.

|

|

TSX, NYSE - HBM 2021 No. 12 |

2 Reflects combined mine, mill and G&A costs per tonne of ore milled.

3 Combined unit cost, cash cost and sustaining cash cost are non-IFRS financial performance measures with no standardized definition under IFRS. For further information, please see the "Non-IFRS Financial Reporting Measures" section of this news release.

The Manitoba business unit had stable operating performance across the mines, mills and zinc plant during the first quarter while facing increasing COVID-19 related logistical challenges. Late in 2020, Hudbay added new controls at the Snow Lake camp by introducing point of care PCR testing. Similar testing is being introduced in Flin Flon during the second quarter. COVID-19 vaccinations are currently being rolled out throughout the Snow Lake and Flin Flon communities and workforce. Full year production of all metals and unit operating costs in Manitoba are on track to achieve the guidance ranges for 2021.

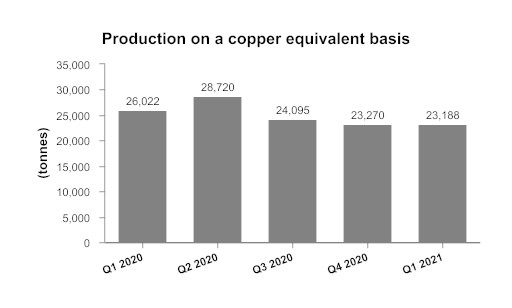

Production during the quarter included 27,940 tonnes of zinc, 6,726 tonnes of copper, 30,862 ounces of gold and 290,959 ounces of silver. Production results for all metals were higher than the previous quarter primarily due to higher throughput, head grades and recoveries.

Ore mined at the Manitoba operations during the first quarter of 2021 was higher than the fourth quarter of 2020 due to full production levels at the 777 mine following the shaft repairs that were completed in the fourth quarter. Copper and gold grades at 777 were higher than the fourth quarter as higher grade remnant stopes were mined as 777 nears the end of its mine life.

Development and underground construction activities continue in the lower part of the Lalor mine in order to ensure the company maintains consistent gold and copper-gold production for the start-up and ongoing operation of the New Britannia mill, scheduled for early in the third quarter of 2021. As at the end of the first quarter, approximately 26,000 tonnes of gold ore had been stockpiled as initial feed for the New Britannia mill, up from 12,000 tonnes at the end of the fourth quarter of 2020. The incremental mining activity associated with growing the gold ore stockpile has contributed to elevated combined mine, mill and G&A unit operating costs during the first quarter of 2021. The gold ore stockpile is expected to continue to grow during the second quarter of 2021.

At the Stall concentrator, ore processed during the first quarter of 2021 was only 3% lower than the fourth quarter of 2020, which was a record quarter for Stall, despite the continued stockpiling of Lalor gold ore ahead of the New Britannia mill. Stall recoveries during the first quarter of 2021 were consistent with the metallurgical model. In early April, production at the Stall mill was suspended for four days as a precaution due to COVID related absenteeism. Hudbay does not expect any material impact to second quarter financial results related to the Stall mill production suspension. Ore processed at the Flin Flon concentrator in the first quarter of 2021 increased compared to the previous quarter as a result of the 777 shaft repairs impacting the previous quarter, but were not as high as prior periods as less Lalor ore was processed in Flin Flon in order to grow the gold ore stockpile as initial feed for the New Britannia mill. Recoveries of copper, gold and silver at the Flin Flon concentrator during the first quarter of 2021 were higher than the previous quarter due to higher head grades from the mining out of higher grade remnant stopes at 777.

Combined mine, mill and G&A unit operating costs in the first quarter of 2021 increased by 8% compared to the fourth quarter of 2020, but remained within the annual guidance range. The increase was primarily due to lower capitalized development at both Lalor and 777, as well as higher mining activity at Lalor to grow the gold stockpile.

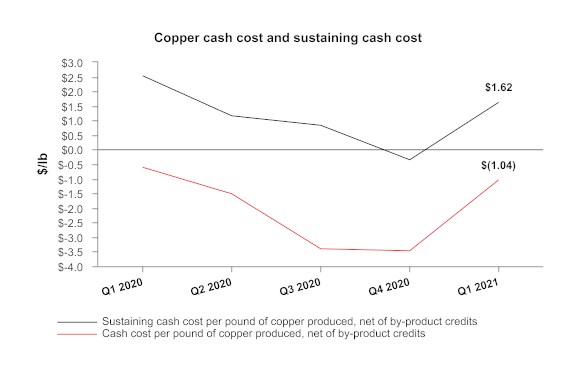

Manitoba's cash cost per pound of copper produced, net of by-product credits, for the first quarter of 2021 was negative $1.04, higher than the prior quarter primarily due to higher mining and general and administrative costs and lower by-product credits, offset by higher copper production. Manitoba's sustaining cash cost per pound of copper produced, net of by-product credits, in the first quarter of 2021 was $1.62, higher than the previous quarter due to the same factors affecting cash costs.

|

|

TSX, NYSE - HBM 2021 No. 12 |

COVID-19 Business Update

The COVID-19 pandemic continues to have a significant global impact as the one-year anniversary of the global outbreak is marked. Throughout this time, Hudbay has prioritized the health and safety of its people by adapting its processes and procedures based on the local situation and taking proactive measures to prevent or minimize the spread of COVID-19 within its workplaces.

As cases of COVID-19 remain elevated in Peru and continue to rise near the company's operations in Manitoba, Hudbay has experienced limited transmission at both of its operations. The company has responded to these events quickly and has worked collaboratively with local health authorities to contain outbreaks while strengthening preventative measures at the workplace with negligible production or financial impacts. Hudbay believes it is appropriately enhancing its preventative and monitoring activities as the challenges of the pandemic evolve, but the company remains at increased operational risk. The company continues to monitor the risks of the pandemic at each of its locations to ensure the safety of its workforce, their families, and the communities in which the company operates.

Increased Constancia Reserves and Updated Mine Plan

On March 29, 2021, Hudbay released an updated mine plan for the Constancia operations that reflects an increase in copper and gold production from 2022 to 2025 as the higher grades from the Pampacancha deposit enter the mine plan. The updated mine plan incorporates higher-grade reserves from the Constancia North pit extension, which contributed to an increase in reserves of 33 million tonnes at a grade of 0.48% copper and 0.115 grams per tonne gold and extends the higher grade profile to 2028. This resulted in an increase of approximately 11% in contained copper and 12% in contained gold over the prior year's reserves, after adjusting for mining depletion in 2020.

With the incorporation of Pampacancha and Constancia North, annual production at Constancia is expected to average approximately 102,000 tonnes of copper and 58,000 ounces of gold over the next eight years, an increase of 40% and 367%, respectively, from 2020 levels, which were partially impacted by an eight-week temporary mine interruption related to a government-declared state of emergency. Constancia's total copper and gold production increases by 12% and 9%, respectively, compared to the same period in the company's previous technical report. Constancia maintains its low-cost profile with average cash cost and sustaining cash cost of $1.18 and $1.71, respectively, per pound of copper produced, net of by-product credits, over the next eight years.

New Britannia Mill Refurbishment Update and Snow Lake Updated Mine Plan

The New Britannia project continues to track ahead of the original schedule and is nearing completion with approximately 82% of the project completed at the end of April. Commissioning of the gold plant is expected in mid-2021 with first gold production expected early in the third quarter. The new copper flotation facility is on track for commissioning and ramp-up in the fourth quarter of 2021. Operational readiness activities are progressing as planned with underground development of Lalor's gold-rich lenses well-advanced in preparation for the start-up of New Britannia. The company continues to see some COVID-related cost pressures on the project capital estimate at New Britannia.

On March 29, 2021, Hudbay announced that the company has advanced the third phase of its Snow Lake gold strategy focusing on expansion and further optimization of operations. Various mining and milling optimization opportunities have been incorporated into an updated mine plan, which contemplates an increase in annual gold production from Lalor and the Snow Lake operations from approximately 150,000 ounces to over 180,000 ounces during the first six years of New Britannia's operation at cash cost and sustaining cash cost, net of by-product credits, of $412 and $788 per ounce of gold, respectively. Mineral reserves increased year-over-year, which resulted in no change to Snow Lake's mine life (to 2037) as the company accelerated future reserves with a higher production rate at Lalor and Stall. This enhanced mine plan incorporates the results from several optimization initiatives, including:

|

|

TSX, NYSE - HBM 2021 No. 12 |

- Early gold production at New Britannia expected in the third quarter of 2021, ahead of the original schedule;

- Increasing the Lalor mining rate to 5,300 tonnes per day from 4,500 tonnes per day in the previous mine plan, which is expected to begin after the 777 mine closes in mid-2022;

- Adding the 1901 deposit to the mine plan to include 1.58 million tonnes of reserves at a grade of 7.9% zinc, with production expected to commence in 2026 at a rate of approximately 1,000 tonnes per day;

- Higher throughput at Stall to achieve a rate of 3,800 tonnes per day compared to 3,500 tonnes per day in the previous mine plan; and

- Starting in 2023, increased copper and precious metal recoveries at Stall, where capital upgrades of $19 million are expected to increase Stall's copper recoveries to between 91% and 95%, gold recoveries to between 64% and 70%, and silver recoveries to between 65% and 74%, a significant increase from the assumed recoveries in the previous mine plan of 84% copper, 53% gold and 53% silver.

These mine plan enhancements optimize the processing capacity of the Snow Lake operations in a manner that maximizes the net present value of the operations. As a result of these initiatives, the production of gold, copper and silver are expected to increase by 18%, 35% and 27%, respectively, from 2022 to 2027 compared to the previous mine plan.

Pampacancha First Production Achieved

In early April 2021, the company finalized the remaining land user agreement for Pampacancha and gained full access to the site to complete pit development activities. Blasting began in mid-April and first production from Pampacancha was achieved at the end of April, which is consistent with Hudbay's previous 2021 guidance and recently published mine plan.

As a result of the completion of the individual land user agreements, revised growth capital expenditure guidance for Peru has increased to approximately $25 million in 2021.

Growing Near-term Production Outlook

On March 29, 2021, Hudbay announced its updated three-year production outlook. Consolidated copper and gold production are expected to increase to 129,500 tonnes and 280,000ii ounces, respectively, in 2023, which represents an increase of 36% and 125%ii, respectively, from 2020 levels as Hudbay brings its Pampacancha and New Britannia projects into production. These growth projects more than offset the lost copper and gold production from 777 after its closure in mid-2022.

Rosemont Update

The appeal of the unprecedented Rosemont court decision with the U.S. Court of Appeals for the Ninth Circuit continues with a decision expected in the second half of 2021. In March 2021, the U.S. Army Corps of Engineers (the "Corps") granted an approved jurisdictional determination whereby the Corps determined there are no waters of the United States on the Rosemont property, and therefore, Rosemont does not require a Section 404 Water Permit.

Expanded Exploration Program at Copper World Discovery

On March 29, 2021, Hudbay announced the intersection of high-grade copper sulphide and oxide mineralization at shallow depth on its wholly-owned private land located within seven kilometres of the Rosemont copper project in Arizona. A 40,000-foot drill program was initiated in 2020 to confirm historical drilling in this past-producing copper region formerly known as Helvetia. After receiving encouraging initial results in February 2021, the company launched a larger 70,000-foot drill program and increased the number of drill rigs at site to further test the four deposits at Copper World and the potential for additional mineralization.

|

|

TSX, NYSE - HBM 2021 No. 12 |

Hudbay's 2020 drill program confirmed the discovery of the Broad Top Butte, Copper World, Peach and Elgin deposits, with a combined strike length of over five kilometres and opportunities to discover additional mineralization between the deposits. The program intersected significant volumes of high-grade copper sulphide and oxide mineralization starting, in most cases, near surface or at shallow depth. Drilling at Broad Top Butte included intersections of 440 feet of 1.38% copper and 246 feet of 0.70% copper starting at surface. Drilling at the Peach and Eglin deposits included intersections of 500 feet of 0.82% copper and 300 feet of 0.64% copper, both starting from surface. The mineralization at the Copper World deposits is located closer to surface than at Rosemont and remains open at depth.

Given the continued success from the Copper World exploration program, in April 2021, Hudbay increased the 2021 budget by approximately $24 million, which includes approximately $14 million for additional exploration expenditures and approximately $10 million of operational expenses related to further studies, none of which will be capitalized. The additional exploration activities are expected to include resource definition drilling and testing targets on Hudbay's private land. The additional studies relate to planned hydrogeological, geotechnical and other studies to potentially support future economic assessments and mine plans. Mineralogical studies and metallurgical testing have also been initiated and are expected to continue in the coming months. Geophysical surveys have been completed and are being analyzed to identify further targets on the company's private land package. Depending on the exploration program results, Hudbay expects to complete an initial inferred resource estimate before the end of the year and a preliminary economic assessment in the first half of 2022.

Increased Resource Estimate and Positive Preliminary Economic Assessment at Mason

The Mason project is a 100%-owned greenfield copper deposit located in the historic Yerington District of Nevada and is one of the largest undeveloped copper porphyry deposits in North America. In March 2021, Hudbay announced its first compiled resource estimate for the Mason project based on a resource model constructed using the same methods applied at Constancia. This resulted in a measured and indicated resource estimate of 2.2 billion tonnes at 0.29% copper, which increased from 1.4 billion tonnes at 0.32% copper previously.

The recently completed PEA contemplates a 27-year mine life with average annual copper production of approximately 140,000 tonnes over the first ten years of full production. The mine plan assumes the construction of a 120,000 tonnes per day conventional flotation concentrator and an initial capital cost estimate of approximately $2.1 billion. At a copper price of $3.10 per pound, the after-tax net present value using a 10% discount rate is $519 million and the internal rate of return is approximately 14%. The valuation metrics are highly sensitive to the copper price and at a price of $3.25 per pound, the after-tax net present value using a 10% discount rate increases to $773 million and the internal rate of return increases to approximately 15%.

There remain opportunities to further enhance the project economics through exploration for higher grade satellite deposits on the company's prospective land package in Nevada, including the Mason Valley properties. Much of the Mason Valley property is located on Hudbay's wholly owned private lands and contains highly prospective skarn mineralization in an area that hosts several historical underground copper mines. Historical drilling and production records from the past producing mines at Mason Valley indicate the mineralization is high grade and starts at or near surface, similar to Hudbay's Copper World property in Arizona. The company expects to continue to compile and interpret historical data on its land package near Mason, to be followed by a geophysical survey to refine the exploration targets in preparation for a future drilling campaign.

|

|

TSX, NYSE - HBM 2021 No. 12 |

Other Exploration Update

Constancia Regional Exploration

In addition to increasing Constancia's reserves, the Constancia North discovery also contributed to an improvement in the head grade of the Constancia mine mineral resource estimates: measured and indicated copper grades increased to 0.22% from 0.19% and inferred copper grades increased to 0.30% from 0.18%. A significant portion of the Constancia North resource estimate is classified as inferred due to wide drill spacing but there remains the opportunity to upgrade these inferred resources to a higher classification as the company completes infill drilling. There also remains further opportunity to extend the Constancia North resources by incorporating steeply dipping high-grade skarn mineralization through a potential underground operation and a trade-off study between open pit versus underground development is expected to be completed in 2021. The mineralization remains open down plunge to the north.

Hudbay continues to advance regional exploration programs in Peru. In February 2021, the company commenced drilling on the Quehuincha North high-grade skarn target located approximately 10 kilometres from Constancia, and drilling continues with five holes completed to-date. Discussions continue to progress with the community of Uchucarcco on the Maria Reyna and Caballito properties, both of which are located within ten kilometres of Constancia, and the company expects to reach an agreement this year. Hudbay also expects to commence drilling activities at the Llaguen property in the coming weeks. Llaguen is a copper porphyry target located in northern Peru, near the city of Trujillo and in close proximity to existing infrastructure.

Snow Lake Regional Exploration

Exploration efforts at the Lalor mine in 2020 continued to be successful with the definition of an additional 1.8 million tonnes of mineral resources, increasing total inferred mineral resources at Lalor to 6.2 million tonnes. The inferred resources have the potential to extend the Lalor mine life beyond the current estimate of ten years and maintain the 5,300 tonnes per day production level beyond 2027.

Preliminary results from Hudbay's 2021 winter drill program in the Chisel Basin in Snow Lake indicate that a potential copper-gold feeder zone to the 1901 deposit exists with one hole intersecting 11.6 metres at 2.7% copper and 3.4 grams per tonne gold, which is similar to the known geology at the Lalor deposit. A review is underway to determine next steps for exploration at 1901 and whether it will be best conducted from surface or from underground once development of the deposit has commenced and suitable drill platforms can be established. The company also continues to test other targets within the Chisel Basin.

Senior Unsecured Notes Refinancing

On March 8, 2021, Hudbay completed the offering of $600.0 million aggregate principal amount of 4.5% senior notes due April 2026 (the "New Notes"). The New Notes are governed by an indenture, dated as of March 8, 2021, among the company, the subsidiaries of the company party thereto as guarantors and U.S. Bank National Association, as trustee.

The proceeds from this offering, together with available cash on hand, were used to redeem all $600.0 million of Hudbay's outstanding 7.625% senior notes due 2025 (the "Redeemed Notes"), including the payment of accrued and unpaid interest and $31.0 million in net transaction and early redemption costs associated with the New Notes. The lower interest rate on the New Notes, versus the rate on the Redeemed Notes, will result in reduced cash interest payments of almost $19 million annually.

|

|

TSX, NYSE - HBM 2021 No. 12 |

Collective Bargaining Agreements

The collective bargaining agreements with Hudbay's unionized workforces at each of its Peru and Manitoba operations expired on or about December 31, 2020. The company continues to advance the collective bargaining process with the labour unions in each jurisdiction as it works toward renewing the collective agreements.

Wheaton Agreement Amendment related to Pampacancha Delivery Obligation

On May 10, 2021, an amendment to the Constancia streaming agreement was signed with Wheaton. The amendment eliminates the requirement to deliver an additional 8,020 ounces of gold to Wheaton for not mining four million tonnes of ore from the Pampacancha deposit by June 30, 2021. As part of this amendment, Hudbay has agreed to increase the fixed gold recoveries that apply to Constancia ore production from 55% to 70% during the reserve life of Pampacancha, which matches the fixed rate of recovery that applies to Pampacancha production. In addition, if Hudbay mines and processes four million tonnes of ore from the Pampacancha deposit by December 31, 2021, Wheaton will make an additional deposit payment of $4 million.

Non-IFRS Financial Performance Measures

Adjusted net earnings (loss), adjusted net earnings (loss) per share, adjusted EBITDA, net debt, cash cost, sustaining and all-in sustaining cash cost per pound of copper produced and per ounce of gold produced and combined unit cost are non-IFRS performance measures. These measures do not have a meaning prescribed by IFRS and are therefore unlikely to be comparable to similar measures presented by other issuers. These measures should not be considered in isolation or as a substitute for measures prepared in accordance with IFRS and are not necessarily indicative of operating profit or cash flow from operations as determined under IFRS. Other companies may calculate these measures differently.

Hudbay believes adjusted net earnings (loss) and adjusted net earnings (loss) per share better reflect the company's performance for the current period and are better indications of its expected performance in future periods. These measures are used internally by the company to evaluate the performance of its underlying operations and to assist with its planning and forecasting of future operating results. As such, the company believes these measures are useful to investors in assessing the company's underlying performance. The company provides adjusted EBITDA to help users analyze its results and to provide additional information about the company's ongoing cash generating potential in order to assess its capacity to service and repay debt, carry out investments and cover working capital needs. Net debt is shown because it is a performance measure used by the company to assess its financial position. Cash cost, sustaining and all-in sustaining cash cost per pound of copper produced and per ounce of gold produced are shown because the company believes they help investors and management assess the performance of its current and future operations, including the margin generated by the operations and the company. Combined unit cost is shown because the company believes it helps investors and management assess the cost structure and margins that are not impacted by variability in by-product commodity prices.

For further details on these measures, including reconciliations to the most comparable IFRS measures, please refer to page 39 of Hudbay's management's discussion and analysis for the three months ended March 31, 2021 available on SEDAR at www.sedar.com.

|

|

TSX, NYSE - HBM 2021 No. 12 |

Website Links

Hudbay:

www.hudbay.com

Management's Discussion and Analysis:

http://www.hudbayminerals.com/files/doc_financials/2021/Q1/MDA211.pdf

Financial Statements:

http://www.hudbayminerals.com/files/doc_financials/2021/Q1/FS211.pdf

Conference Call and Webcast

|

Date: |

Wednesday, May 12, 2021 |

|

Time: |

8:30 a.m. ET |

|

Webcast: |

http://services.choruscall.ca/links/hudbay20210512.html |

|

Dial in: |

1-416-915-3239 or 1-800-319-4610 |

Qualified Person and NI 43-101

The technical and scientific information in this news release related to the Rosemont project has been approved by Cashel Meagher, P. Geo, Hudbay's Senior Vice President and Chief Operating Officer. The technical and scientific information related to the company's other material mineral projects contained in this news release has been approved by Olivier Tavchandjian, P. Geo, Hudbay's Vice President, Exploration and Geology. Messrs. Meagher and Tavchandjian are qualified persons pursuant to NI 43-101. For a description of the key assumptions, parameters and methods used to estimate mineral reserves and resources at Hudbay's material properties, as well as data verification procedures and a general discussion of the extent to which the estimates of scientific and technical information may be affected by any known environmental, permitting, legal title, taxation, sociopolitical, marketing or other relevant factors, please see the technical reports for the company's material properties as filed by Hudbay on SEDAR at www.sedar.com.

For further information on the Copper World exploration results, including a detailed summary of the drill hole results to date and the data verification and quality assurance and quality control measures that were used, please refer to Hudbay's news release dated March 29, 2021.

Readers should be aware that the Mason PEA referred to in this news release is preliminary in nature, includes inferred resources that are considered too speculative to have the economic considerations applied to them that would enable them to be categorized as mineral reserves and there is no certainty the preliminary economic assessment for Mason will be realized. For further information on the Mason PEA, please refer to Hudbay's news release dated April 6, 2021.

Forward-Looking Information

This news release contains forward-looking information within the meaning of applicable Canadian and United States securities legislation. All information contained in this news release, other than statements of current and historical fact, is forward-looking information. Often, but not always, forward-looking information can be identified by the use of words such as "plans", "expects", "budget", "guidance", "scheduled", "estimates", "forecasts", "strategy", "target", "intends", "objective", "goal", "understands", "anticipates" and "believes" (and variations of these or similar words) and statements that certain actions, events or results "may", "could", "would", "should", "might" "occur" or "be achieved" or "will be taken" (and variations of these or similar expressions). All of the forward-looking information in this news release is qualified by this cautionary note.

|

|

TSX, NYSE - HBM 2021 No. 12 |

Forward-looking information includes, but is not limited to, production, cost and capital and exploration expenditure guidance and potential revisions to such guidance, anticipated production at Hudbay's mines and processing facilities, expectations regarding the impact of the COVID-19 pandemic on the company's operations, financial condition and prospects, and the company's ability to effectively engage with local communities in Peru and other stakeholders, expectations regarding the timing of mining activities at the Pampacancha deposit and any additional delivery obligations under the Constancia stream agreement, the anticipated timing, cost and benefits of developing the Rosemont project and the outcome of litigation challenging Rosemont's permits, expectations regarding the Copper World exploration program, expectations regarding the Lalor gold strategy, including the refurbishment, commissioning and ramp-up of the New Britannia mill and the expectations regarding the mine plan for the 1901 deposit, increasing the mining rate at Lalor and optimizing the Stall and New Britannia mills, the possibility of converting inferred mineral resource estimates to higher confidence categories, the potential and the company's anticipated plans for advancing its mining properties surrounding Constancia and elsewhere in Peru, anticipated mine plans, anticipated metals prices and the anticipated sensitivity of the company's financial performance to metals prices, events that may affect Hudbay's operations and development projects, anticipated cash flows from operations and related liquidity requirements, the anticipated effect of external factors on revenue, such as commodity prices, estimation of mineral reserves and resources, mine life projections, reclamation costs, economic outlook, government regulation of mining operations, and business and acquisition strategies. Forward-looking information is not, and cannot be, a guarantee of future results or events. Forward-looking information is based on, among other things, opinions, assumptions, estimates and analyses that, while considered reasonable by the company at the date the forward-looking information is provided, inherently are subject to significant risks, uncertainties, contingencies and other factors that may cause actual results and events to be materially different from those expressed or implied by the forward-looking information.

The material factors or assumptions that Hudbay has identified and applied in drawing conclusions or making forecasts or projections are set out in the forward-looking information include, but are not limited to:

- the ability to continue to operate safely and at full capacity during the COVID-19 pandemic;

- the availability, global supply and effectiveness of COVID-19 vaccines, the effective distribution of such vaccines in the countries in which the company operates, the lessening of restrictions related to COVID-19, and the anticipated rate and timing for each of the foregoing;

- the ability to achieve production and unit cost guidance;

- no significant interruptions to the company's operations or significant delays to its development projects in Manitoba and Peru due to the COVID-19 pandemic;

- the availability of spending reductions and liquidity options;

- the timing of development and production activities on the Pampacancha deposit;

- no significant unanticipated delays to the development of Pampacancha;

- the successful completion of the New Britannia project on budget and on schedule;

- the successful outcome of the Rosemont litigation;

- the successful renegotiation of collective agreements with the labour unions that represent certain of the company's employees in Manitoba and Peru;

- the success of mining, processing, exploration and development activities;

- the scheduled maintenance and availability of the company's processing facilities;

- the accuracy of geological, mining and metallurgical estimates;

- anticipated metals prices and the costs of production;

|

|

TSX, NYSE - HBM 2021 No. 12 |

- the supply and demand for metals the company produces;

- the supply and availability of all forms of energy and fuels at reasonable prices;

- no significant unanticipated operational or technical difficulties;

- the execution of the company's business and growth strategies, including the success of its strategic investments and initiatives;

- the availability of additional financing, if needed;

- the ability to complete project targets on time and on budget and other events that may affect the company's ability to develop its projects;

- the timing and receipt of various regulatory and governmental approvals;

- the availability of personnel for the exploration, development and operational projects and ongoing employee relations;

- maintaining good relations with the labour unions that represent certain of the company's employees in Manitoba and Peru;

- maintaining good relations with the communities in which the company operates, including the neighbouring Indigenous communities and local governments;

- no significant unanticipated challenges with stakeholders at the company's various projects;

- no significant unanticipated events or changes relating to regulatory, environmental, health and safety matters;

- no contests over title to the company's properties, including as a result of rights or claimed rights of Indigenous peoples or challenges to the validity of the company's unpatented mining claims;

- the timing and possible outcome of pending litigation and no significant unanticipated litigation;

- certain tax matters, including, but not limited to current tax laws and regulations and the refund of certain value added taxes from the Canadian and Peruvian governments; and

- no significant and continuing adverse changes in general economic conditions or conditions in the financial markets (including commodity prices and foreign exchange rates).

The risks, uncertainties, contingencies and other factors that may cause actual results to differ materially from those expressed or implied by the forward-looking information may include, but are not limited to, risks associated with the COVID-19 pandemic and its effect on the company's operations, financial condition, projects and prospects, the possibility of a global recession arising from the COVID-19 pandemic and attempts to control it, the political situation in Peru, risks generally associated with the mining industry, such as economic factors (including future commodity prices, currency fluctuations, energy prices and general cost escalation), uncertainties related to the development and operation of the company's projects, risks related to the U.S. district court's recent decisions to set aside the U.S. Forest Service's FROD and the Biological Opinion for Rosemont and related appeals and other legal challenges, risks related to the new Lalor mine plan, including the schedule for the refurbishment, commissioning and ramp-up of the New Britannia mill and the ability to convert inferred mineral resource estimates to higher confidence categories, risks related to the schedule for mining the Pampacancha deposit (including risks associated with COVID-19 and risks associated with the impact of any schedule delays), dependence on key personnel and employee and union relations, risks related to political or social unrest or change, risks in respect of Indigenous and community relations, rights and title claims, operational risks and hazards, including the cost of maintaining and upgrading the company's tailings management facilities and any unanticipated environmental, industrial and geological events and developments and the inability to insure against all risks, failure of plant, equipment, processes, transportation and other infrastructure to operate as anticipated, compliance with government and environmental regulations, including permitting requirements and anti-bribery legislation, depletion of the company's reserves, volatile financial markets that may affect the company's ability to obtain additional financing on acceptable terms, the failure to obtain required approvals or clearances from government authorities on a timely basis, uncertainties related to the geology, continuity, grade and estimates of mineral reserves and resources, and the potential for variations in grade and recovery rates, uncertain costs of reclamation activities, the company's ability to comply with its pension and other post-retirement obligations, the company's ability to abide by the covenants in its debt instruments and other material contracts, tax refunds, hedging transactions, as well as the risks discussed under the heading "Financial Risk Management" in the company's Management's Discussion and Analysis dated May 11, 2021 and under the heading "Risk Factors" in Hudbay's most recent Annual Information Form.

|

|

TSX, NYSE - HBM 2021 No. 12 |

Should one or more risk, uncertainty, contingency or other factor materialize or should any factor or assumption prove incorrect, actual results could vary materially from those expressed or implied in the forward-looking information. Accordingly, the reader should not place undue reliance on forward-looking information. Hudbay does not assume any obligation to update or revise any forward-looking information after the date of this news release or to explain any material difference between subsequent actual events and any forward-looking information, except as required by applicable law.

Note to United States Investors

This news release has been prepared in accordance with the requirements of the securities laws in effect in Canada, which may differ materially from the requirements of United States securities laws applicable to U.S. issuers.

About Hudbay

Hudbay (TSX, NYSE: HBM) is a diversified mining company primarily producing copper concentrate (containing copper, gold and silver) and zinc metal. Directly and through its subsidiaries, Hudbay owns three polymetallic mines, four ore concentrators and a zinc production facility in northern Manitoba and Saskatchewan (Canada) and Cusco (Peru), and copper projects in Arizona and Nevada (United States). The company's growth strategy is focused on the exploration, development, operation and optimization of properties it already controls, as well as other mineral assets it may acquire that fit its strategic criteria. Hudbay's vision is to be a responsible, top-tier operator of long-life, low-cost mines in the Americas. Hudbay's mission is to create sustainable value through the acquisition, development and operation of high-quality, long-life deposits with exploration potential in jurisdictions that support responsible mining, and to see the regions and communities in which the company operates benefit from its presence. The company is governed by the Canada Business Corporations Act and its shares are listed under the symbol "HBM" on the Toronto Stock Exchange, New York Stock Exchange and Bolsa de Valores de Lima. Further information about Hudbay can be found on www.hudbay.com.

For further information, please contact:

Candace Brûlé

Director, Investor Relations

(416) 814-4387

______________________________

i Adjusted net loss and adjusted net loss per share, adjusted EBITDA, cash cost, all-in sustaining cash cost per pound of copper produced, net of by-product credits, and net debt are non-IFRS financial performance measures with no standardized definition under IFRS. For further information, please see the "Non-IFRS Financial Reporting Measures" section of this news release.

ii Copper and gold production growth based on mid-point of 2023 guidance ranges and 2020 actual production of 95,333 tonnes of copper and 124,622 ounces of gold. 2020 levels were partially impacted by an eight-week temporary mine interruption related to a government-declared state of emergency.

iii Based on a 10% discount rate.