Management's

Discussion and Analysis of

Results of Operations and

Financial Condition

For the three and six months ended

June 30, 2019

August 8, 2019

INTRODUCTION

This Management's Discussion and Analysis ("MD&A") dated August 8, 2019 is intended to supplement Hudbay Minerals Inc.'s unaudited condensed consolidated interim financial statements and related notes for the three and six months ended June 30, 2019 and 2018 (the "consolidated interim financial statements"). The consolidated interim financial statements have been prepared in accordance with International Financial Reporting Standards (“IFRS"), including International Accounting Standard 34, Interim Financial Reporting, as issued by the International Accounting Standards Board (“IASB”).

References to “Hudbay”, the “Company”, “we”, “us”, “our” or similar terms refer to Hudbay Minerals Inc. and its direct and indirect subsidiaries as at June 30, 2019. "Hudbay Peru" refers to HudBay Peru S.A.C., our wholly-owned subsidiary which owns a 100% interest in the Constancia mine, and “Hudbay Arizona” refers to Hudbay Arizona Inc., our wholly-owned subsidiary, which indirectly owns a 100% interest in the Rosemont project.

Readers should be aware that:

| – | This MD&A contains certain “forward-looking statements” and “forward-looking information” (collectively, “forward-looking information”) that are subject to risk factors set out in a cautionary note contained in our MD&A. |

| – | This MD&A has been prepared in accordance with the requirements of the securities laws in effect in Canada, which may differ materially from the requirements of United States securities laws applicable to US issuers. |

| – | We use a number of non-IFRS financial performance measures in our MD&A. |

| – | The technical and scientific information in this MD&A has been approved by qualified persons based on a variety of assumptions and estimates. |

For a discussion of each of the above matters, readers are urged to review the “Notes to Reader” discussion beginning on page 43 of this MD&A.

Additional information regarding Hudbay, including the risks related to our business and those that are reasonably likely to affect our financial statements in the future, is contained in our continuous disclosure materials, including our most recent Annual Information Form (“AIF”), consolidated financial statements and Management Information Circular available on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

As of January 1, 2019 we have adopted IFRS 16, Leases (“IFRS 16”). The Company applied this amendment prospectively. A reconciliation from the December 31, 2018 previously reported balances to the revised January 1, 2019 opening balances is disclosed in Note 4(b) of the consolidated interim financial statements.

All amounts are in US dollars unless otherwise noted.

OUR BUSINESS

We are an integrated mining company primarily producing copper concentrate (containing copper, gold, and silver), molybdenum concentrate and zinc metal. With assets in North and South America, we are focused on the discovery, production and marketing of base and precious metals. Directly and through our subsidiaries, we own three polymetallic mines, four ore concentrators and a zinc production facility in northern Manitoba and Saskatchewan (Canada) and Cusco (Peru), and copper projects in Arizona and Nevada (United States). Our growth strategy is focused on the exploration and development of properties we already control, as well as other mineral assets we may acquire that fit our strategic criteria. Our vision is to be a responsible, top-tier operator of long-life, low-cost mines in the Americas. We are governed by the Canada Business Corporations Act and our shares are listed under the symbol "HBM" on the Toronto Stock Exchange, New York Stock Exchange and Bolsa de Valores de Lima.

1

SUMMARY

| – |

Delivered a solid operating quarter, which included record mine production at Lalor and record throughput at the Stall concentrator. |

| – |

777 and Lalor ore mined increased by 35% and 21%, respectively, in the second quarter of 2019 compared to the same period in 2018. |

| – |

Second quarter 2019 results are on track to meet all production and cost guidance for 2019. |

| – |

Following the previously announced U.S. court decision suspending construction work at Rosemont, we intend to appeal the decision and evaluate options for advancing the project. |

| – |

Announced an initial National Instrument ("NI") 43-101 resource estimate for the recently discovered zinc-rich 1901 deposit near Lalor. |

| – |

Progressed other key strategic initiatives, including engineering and permitting for the Lalor Gold strategy and community negotiations near Constancia. |

| – |

Cash generated from operating activities increased to $107.0 million in the second quarter of 2019 from $97.0 million in the same quarter of 2018, while operating cash flow before change in non-cash working capital decreased to $81.1 million in the quarter from $131.6 million in the same quarter of 2018 as a result of lower realized prices and sales volumes. |

| – |

Cash and cash equivalents increased from $485.9 million at March 31, 2019 to $489.5 million at June 30, 2019, as free cash flow from our operations more than funded the $45.0 million upfront cost to acquire the Rosemont minority joint venture interest and $50.0 million of capital expenditures. |

Summary of Second Quarter Results

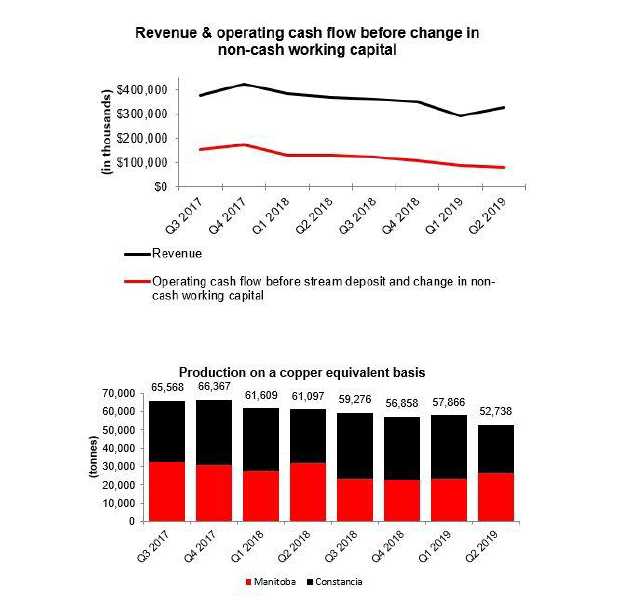

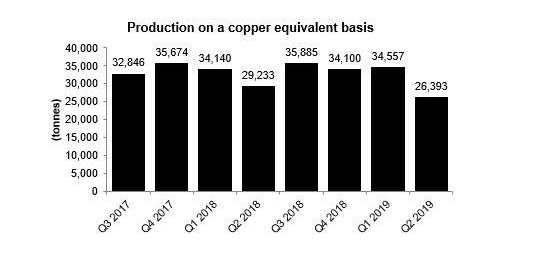

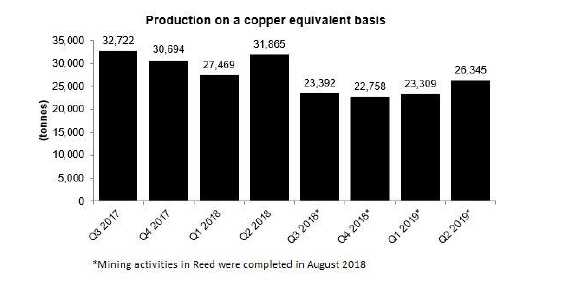

Cash generated from operating activities increased to $107.0 million in the second quarter of 2019 from $97.0 million in the same quarter of 2018. Operating cash flow before change in non-cash working capital was $81.1 million during the second quarter of 2019, reflecting a decrease of $50.5 million compared to the second quarter of 2018. The decrease in operating cash flow is primarily the result of lower realized copper and zinc prices and lower sales volumes of copper and zinc, compared to the second quarter of 2018. Copper-equivalent production in the second quarter of 2019 decreased by 14% compared to the same period in 2018, primarily as a result of lower mine grades at Constancia, as planned, and the closure of the Reed mine.

Net loss and loss per share in the second quarter of 2019 were $54.1 million and $0.21, respectively, compared to a net profit and earnings per share of $24.7 million and $0.09, respectively, in the second quarter of 2018.

Net loss and loss per share in the second quarter of 2019 were affected by, among other things, the following items:

| (in $ millions, except per share amounts) | Pre-tax gain (loss) | After-tax gain | Per share gain |

| (loss) | (loss) | ||

| Non-cash deferred tax adjustments

Write down of UCM receivable Costs associated with recent proxy contest |

— | (15.1) | (0.06) |

| (26.0) | (26.0) | (0.10) | |

| (3.0) | (2.2) | (0.01) |

As previously disclosed, as part of the orderly acquisition of the remaining interest in the Rosemont copper project on April 25, 2019, Hudbay, immediately prior to closing the acquisition, agreed to release United Copper & Moly LLC ("UCM") from its repayment obligations under the Rosemont project loan in exchange for an increase in equity interest in Rosemont. As a result, the loan receivable balance was written down in the income statement and other capital reserves, a component of shareholder's equity, was subsequently increased.

2

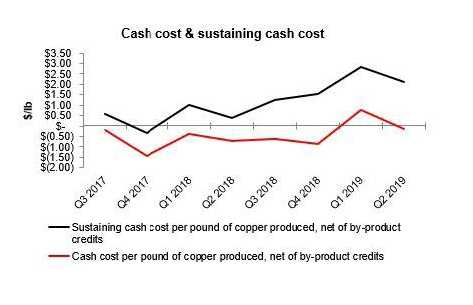

In the second quarter of 2019, consolidated cash cost per pound of copper produced, net of by-product credits1, was $1.27, an increase compared to $0.96 in the same period last year. Cash costs per pound of copper produced, net of by–product credits, increased as a result of lower copper and zinc production and lower realized zinc prices. Incorporating sustaining capital, capitalized exploration, royalties, selling, administrative and regional costs, consolidated all-in sustaining cash cost per pound of copper produced, net of by-product credits1, in the second quarter of 2019 was $2.26, which increased from $1.50 in the same period last year, driven mainly by higher cash costs and increased sustaining capital expenditures.

Net debt1 decreased by $3.8 million from March 31, 2019 to $487.7 million at June 30, 2019, as the upfront payment to acquire the Rosemont minority joint venture interest and other capital expenditures was offset by free cash flow from our operations. At June 30, 2019, total liquidity, including cash and available credit facilities, was $910.7 million, down from $940.3 million as at March 31, 2019 due to additional letters of credit posted to support reclamation obligations.

3

Lower copper-equivalent production in the Manitoba business unit as compared to the second quarter of 2018 reflects the closure of the Reed mine in August 2018.

|

1 Cash cost, all-in sustaining cash cost per pound of copper produced, net of by-product credits, and net debt are non-IFRS financial performance measures with no standardized definition under IFRS. For further information and a detailed reconciliation, please see the discussion under the "Non-IFRS Financial Reporting Measures" section of this MD&A. |

4

KEY FINANCIAL RESULTS

| Financial Condition

(in $ thousands) |

Jun. 30,

2019 |

Dec. 31, 2018

|

| Cash and cash equivalents

Total long-term debt Net debt1 Working capital Total assets Equity |

489,527 | 515,497 |

| 977,196 | 981,030 | |

| 487,669 | 465,533 | |

| 428,078 | 445,228 | |

| 4,737,938 | 4,685,635 | |

| 2,130,719 | 2,178,856 |

| 1 | Net debt is a non-IFRS financial performance measure with no standardized definition under IFRS. For further information and a detailed reconciliation, please see discussion under the "Non-IFRS Financial Reporting Measures" section of this MD&A. |

| Financial

Performance (in $ thousands, except per share amounts) |

Three months ended | Six months ended | ||

| Jun. 30, | Jun. 30, | Jun. 30, | Jun. 30, | |

| 2019 | 2018 | 2019 | 2018 | |

| Revenue Cost of sales (Loss) profit before tax (Loss) profit Basic and diluted (loss) earnings per share Operating cash flow before change in non-cash working capital |

329,414 | 371,288 | 621,672 | 757,944 |

| 286,271 | 278,827 | 526,718 | 544,712 | |

| (43,931) | 49,797 | (62,044) | 122,900 | |

| (54,145) | 24,673 | (67,562) | 66,118 | |

| (0.21) | 0.09 | (0.26) | 0.25 | |

| 81,146 | 131,635 | 170,740 | 263,428 | |

5

KEY PRODUCTION RESULTS

| Three months ended | Three months ended | ||||||

| Jun. 30, 2019 | Jun. 30, 2018 | ||||||

| Peru | Manitoba | Total | Peru | Manitoba | Total | ||

| Contained metal in concentrate produced1 | |||||||

| Copper Gold Silver Zinc Molybdenum Payable metal sold Copper Gold Silver Zinc 2 Molybdenum Cash cost 3 Sustaining cash cost 3 All-in sustaining cash cost3 |

tonnes | 24,232 | 6,131 | 30,363 | 26,818 | 10,807 | 37,625 |

| oz | 3,794 | 24,305 | 28,099 | 5,190 | 27,290 | 32,480 | |

| oz | 551,807 | 260,000 | 811,807 | 596,570 | 355,091 | 951,661 | |

| tonnes | — | 31,838 | 31,838 | — | 33,170 | 33,170 | |

| tonnes | 334 | — | 334 | 141 | — | 141 | |

| tonnes | 25,778 | 7,393 | 33,171 | 25,409 | 10,062 | 35,471 | |

| oz | 4,056 | 26,482 | 30,538 | 3,764 | 25,932 | 29,696 | |

| oz | 504,259 | 300,042 | 804,301 | 438,532 | 250,952 | 689,484 | |

| tonnes | — | 24,224 | 24,224 | — | 28,168 | 28,168 | |

| tonnes | 419 | — | 419 | — | — | — | |

| $/lb | 1.63 | (0.15) | 1.27 | 1.64 | (0.71) | 0.96 | |

| $/lb | 2.09 | 2.11 | 1.82 | 0.38 | |||

| $/lb | 2.26 | 1.50 | |||||

| Six months ended | Six months ended | ||||||

| Jun. 30, 2019 | Jun. 30, 2018 | ||||||

| Peru | Manitoba | Total | Peru | Manitoba | Total | ||

| Contained metal in

concentrate produced1 Copper Gold Silver Zinc Molybdenum Payable metal sold Copper Gold Silver Zinc 2 Molybdenum Cash cost 3 Sustaining cash cost 3 All-in sustaining cash cost3 |

|||||||

| tonnes | 56,075 | 12,260 | 68,335 | 58,369 | 18,462 | 76,831 | |

| oz | 9,151 | 44,510 | 53,661 | 10,608 | 52,965 | 63,573 | |

| oz | 1,186,737 | 544,265 | 1,731,002 | 1,242,456 | 686,343 | 1,928,799 | |

| tonnes | — | 59,875 | 59,875 | — | 61,952 | 61,952 | |

| tonnes | 638 | — | 638 | 205 | — | 205 | |

| tonnes | 52,440 | 12,448 | 64,888 | 54,977 | 17,000 | 71,977 | |

| oz | 10,274 | 42,893 | 53,167 | 8,671 | 47,082 | 55,753 | |

| oz | 1,256,518 | 530,689 | 1,787,207 | 1,034,162 | 541,778 | 1,575,940 | |

| tonnes | — | 47,178 | 47,178 | — | 53,620 | 53,620 | |

| tonnes | 653 | — | 653 | 137 | — | 137 | |

| $/lb | 1.38 | 0.31 | 1.19 | 1.46 | (0.58) | 0.97 | |

| $/lb | 1.69 | 2.48 | 1.63 | 0.65 | |||

| $/lb | 2.01 | 1.48 | |||||

|

1 |

Metal reported in concentrate is prior to deductions associated with smelter contract terms. |

|

2 |

Includes refined zinc metal sold and payable zinc in concentrate sold. |

|

3 |

Cash cost, sustaining cash cost and all-in sustaining cash cost per pound of copper produced, net of by-product credits are non-IFRS financial performance measures with no standardized definition under IFRS. For further information and a detailed reconciliation, please see the discussion under the "Non-IFRS Financial Reporting Measures" section of this MD&A. |

6

7

RECENT DEVELOPMENTS

Settlement Agreement with Waterton

In May 2019, Hudbay and certain funds managed by Waterton Global Resource Management, Inc ("Waterton"). entered into a settlement agreement that resulted in the appointment of three of Waterton's proposed nominees to Hudbay’s eleven-person Board at our annual and special meeting of shareholders. A copy of the settlement agreement is available under Hudbay’s profile on SEDAR.

Senior Management Change

On July 10, 2019, we announced that Alan Hair stepped down as Hudbay's President and Chief Executive Officer and as a director of the Company. Peter Kukielski has been appointed Interim CEO. Mr. Kukielski has more than 30 years of extensive global experience within the base metals, precious metals and bulk materials sectors, having overseen operations across the globe.

The Board has commenced a search for a permanent CEO, which may include internal and external candidates.

Peru Logistics Update

The southern Peru copper mining corridor has seen heightened political activity over the past several months, including large protests related to the granting of a permit to another company’s mining project. These protests have blocked the entrance to the port of Matarani since mid-July. While the protests are unrelated to Constancia, we, as well as other copper miners, use the Matarani port to ship copper concentrates and import consumables. Mining and milling operations have continued at Constancia, but there has been a substantial concentrate inventory buildup at the Constancia site, costs for consumables such as diesel have increased, and Constancia’s molybdenum production has been affected due to the unavailability of necessary consumables.

The Peruvian government has taken recent steps to address the road blockages with some intermittent access currently available to the port of Matarani. We are continuing to work to manage the impact of these disruptions.

Rosemont Developments

On April 25, 2019, we completed the previously announced acquisition of UCM's 7.95% joint venture interest in Rosemont and paid UCM initial cash consideration of $45.0 million, plus three future expected annual installments of $10.0 million per year, commencing July 1, 2022. This provides us with 100% ownership of Rosemont, allowing greater strategic flexibility with respect to capital structure and project financing alternatives.

On July 31, 2019, the U.S. District Court for the District of Arizona (“Court”) issued a ruling in the lawsuits challenging the U.S. Forest Service’s issuance of the Final Record of Decision (“FROD”) for the Rosemont project in Arizona. The Court ruled to vacate and remand the FROD such that Rosemont cannot proceed with construction at this time. We strongly believe that the Court has misinterpreted federal mining laws and Forest Service regulations as they apply to Rosemont. As such we intend to appeal the Court’s decision to the U.S. Ninth Circuit Court of Appeals and are evaluating other options to advance Rosemont. We are also reassessing the optimal timeline for financing Rosemont, including the previously announced process to identify a joint venture partner for Rosemont.

8

We had previously initiated an early works program for Rosemont with anticipated 2019 project capital spending of $122 million. We have suspended most of the early works activities and now expect Rosemont project spending of approximately $30 million in 2019, including costs to demobilize engineering work and complete committed procurement. These costs are in addition to $20 million of Rosemont non-project costs that are still expected to be incurred in 2019.

Snow Lake Exploration Update

1901 Deposit Initial Resource Estimate

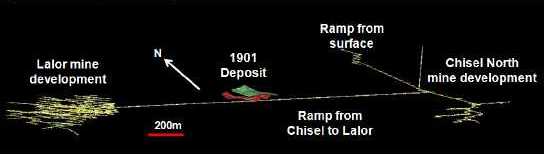

Since its discovery in February 2019, drilling has continued to define the extent and geometry of the 1901 deposit. This focused drill program, along with geological interpretation and resource modeling, has resulted in an initial resource estimate a mere six months from discovery. The deposit is located between the former producing Chisel North mine and Lalor mine, less than 1,000 metres from an active underground ramp at a depth ranging from 550 to 650 metres and within 15 kilometres trucking distance of the Stall concentrator. The property is 100% owned by us, free of any royalties or streams. The mineralization is interpreted as two zinc-rich volcanogenic massive sulphide lenses with locally high-grade gold and silver content. The mineralization occurs along the hanging wall contact of the stratigraphic horizon hosting the Chisel North deposit.

Based on these recent drilling results, we are pleased to announce an initial mineral resource estimate for the 1901 deposit:

1901 Deposit Mineral Resource Estimate 1,2,3,4,5 |

Tonnes (millions) |

Zn Grade (%) |

Au Grade (g/t) |

Ag Grade (g/t) |

Cu Grade

(%) |

| Inferred | 2.1 | 9.67 | 0.87 | 30.7 | 0.25 |

| 1 |

CIM definitions were followed for the estimation of mineral resources. Mineral resources that are not mineral reserves do not have demonstrated economic viability. |

| 2 |

Mineral resources are reported within an economic envelope defined by a mineral stope optimization algorithm assuming a selective mining method. |

| 3 |

Long-term metal prices of $1,260/oz gold, $18.00/oz silver, $3.10/lb copper and $1.10/lb zinc were used for the estimation of the mineral resources. |

| 4 |

Metal recovery estimates are based on the assumption that this mineralization would be processed at Hudbay’s Stall concentrator and would present a similar performance to those experienced historically for the Chisel and Lalor zinc-rich lenses. |

| 5 |

Specific gravity measurements using industry standard techniques were completed on all assayed intervals. |

The methodology followed to estimate mineral resources at the 1901 deposit was identical to the approach used to recently update the mineral resource estimates for the Lalor mine (please refer to the NI 43-101 Technical Report for Lalor dated March 28, 2019 for more details) and constrains the resource within a stope optimization envelope that is expected to lead to a higher mineral resource to mineral reserve conversion factor.

There remain opportunities for extension of the mineralization discovered at the 1901 deposit. Exploration targets for new discrete lenses also exist in the immediate vicinity of 1901 and two drills are actively exploring in the area. We are studying alternatives to develop the 1901 deposit to optimize the net present value of the Manitoba business unit.

9

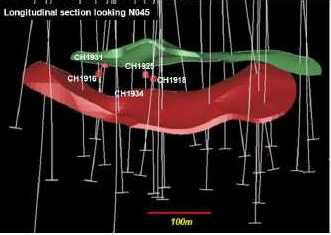

High-Grade Gold and Copper-Gold Intercepts

In addition to the initial resource estimate on the 1901 deposit, drilling has also identified several high-grade gold and copper-gold zones but drilling density is not yet at a level to establish a mineral resource estimate. Highlights of the drill hole intersections occurring in the footwall of the zinc rich lenses are summarized in the table below. Drill hole CH1916 assayed 29.8g/t Au and 401.8g/t Ag over 7.5 metres from 580.5 to 588.0 metres and drill hole CH1925 assayed 3.2g/t Au, 19.9g/t Ag and 2.83% Cu over 9 metres from 637.5 to 646.5 metres. Several other high-grade copper and gold intersections of less than 3 metres occur throughout the footwall zone in altered felsic units. As drilling progresses to an infill stage to convert the inferred zinc-rich resource estimates to an indicated category, we also expect to establish the continuity of the gold and copper-gold rich mineralization and report a mineral resource estimate for this portion of the mineralization. The gold and copper-gold rich mineralization is likely to constitute a suitable feed for the New Britannia gold mill after its refurbishment is completed in 2022 and could further enhance the gold production profile from the Snow Lake camp.

Hole ID |

From (m) |

To (m) |

Intercept 1 (m) |

Depth (m) |

Au (g/t) |

Ag (g/t) |

Cu (%) |

Zn (%) |

| CH1916 | 580.5 | 588.0 | 7.5 | 574 | 29.8 | 401.8 | 0.16 | 0.04 |

| CH1918 | 570.0 | 575.5 | 5.5 | 570 | 14.2 | 105.3 | 0.13 | 0.21 |

| CH1931 | 617.9 | 625.0 | 7.1 | 565 | 13.4 | 28.3 | 0.04 | 0.75 |

| CH1934 | 692.8 | 696.0 | 3.2 | 646 | 14.3 | 181.2 | 0.21 | 0.04 |

| CH1925 | 637.5 | 646.5 | 9.0 | 621 | 3.2 | 19.9 | 2.83 | 0.17 |

| Note: | all grade values are uncut. |

| 1 | True widths cannot be estimated at this stage as there is insufficient knowledge on the orientation of the gold and copper-gold mineralization. |

Hole ID |

From (m) | To (m) | Azimuth at Intercept |

Dip at Intercept | ||||

| Easting | Northing | Elevation | Easting | Northing | Elevation | |||

| CH1916 | 427067 | 6078909 | -270 | 427068 | 6078909 | -278 | 087 | -85 |

| CH1918 | 427094 | 6078818 | -265 | 427094 | 6078818 | -271 | 052 | -83 |

| CH1931 | 427083 | 6078909 | -259 | 427081 | 6078908 | -266 | 247 | -65 |

| CH1934 | 427072 | 6078847 | -322 | 427070 | 6078846 | -326 | 237 | -64 |

| CH1925 | 427185 | 6078904 | -307 | 427183 | 6078903 | -315 | 229 | -75 |

Other Snow Lake Regional Exploration

During the second quarter of 2019, we have also continued in-mine exploration activities at the Lalor mine and progressed engineering studies for our other 100%-owned deposits in the Snow Lake area, including the WIM, Pen II and New Britannia mine properties. Drilling and studies will continue throughout the year and are expected to be incorporated in the annual mineral reserve and resource estimate.

Dividend Declared

A semi-annual dividend of C$0.01 per share was declared on August 8, 2019. The dividend will be paid on September 27, 2019 to shareholders of record as of September 6, 2019.

10

CONSTANCIA OPERATIONS REVIEW

| Three months ended | Six months ended | Guidance | ||||

| Jun. 30, | Jun. 30, | Annual | ||||

| 2019 | Jun. 30, 2018 | 2019 | Jun. 30, 2018 | 2019 | ||

| Ore mined 1 | tonnes | 8,211,166 | 8,744,200 | 16,845,939 | 18,233,969 | |

| Copper | % | 0.39 | 0.47 | 0.43 | 0.49 | |

| Gold | g/tonne | 0.04 | 0.05 | 0.04 | 0.05 | |

| Silver | g/tonne | 3.68 | 4.03 | 3.61 | 4.11 | |

| Ore milled | tonnes | 7,679,739 | 7,726,606 | 15,672,801 | 15,577,775 | |

| Copper | % | 0.37 | 0.44 | 0.42 | 0.47 | |

| Gold | g/tonne | 0.04 | 0.05 | 0.04 | 0.05 | |

| Silver | g/tonne | 3.40 | 3.92 | 3.47 | 4.01 | |

| Copper concentrate | tonnes | 103,796 | 113,738 | 238,519 | 242,286 | |

| Concentrate grade | % Cu | 23.35 | 23.58 | 23.51 | 24.09 | |

| Copper recovery | % | 84.7 | 79.7 | 85.6 | 80.3 | |

| Gold recovery | % | 41.3 | 44.8 | 47.1 | 44.9 | |

| Silver recovery | % | 65.7 | 61.2 | 67.9 | 61.9 | |

| Combined unit operating costs2,3 | $/tonne | 10.39 | 10.33 | 9.62 | 9.62 | 7.90 - 9.70 |

|

1 |

Reported tonnes and grade for ore mined are estimates based on mine plan assumptions and may not reconcile fully to ore milled. |

|

2 |

Reflects combined mine, mill and general and administrative ("G&A") costs per tonne of ore milled. Reflects the deduction of expected capitalized stripping costs. |

|

3 |

Combined unit costs is a non-IFRS financial performance measure with no standardized definition under IFRS. For further information and a detailed reconciliation, please see the discussion under the "Non-IFRS Financial Reporting Measures" section of this MD&A. |

Ore mined at our Constancia mine during the second quarter of 2019 was 6% lower compared to the same period in 2018 due to mining from areas with a higher stripping ratio than the areas mined in the second quarter of 2018, in line with the mine plan. Milled copper grades in the second quarter were approximately 16% lower than the same period in 2018 as lower grade phases continue to be mined, in line with the mine plan. Mill throughput in the second quarter of 2019 was consistent compared to the same period in 2018.

Copper recoveries in the second quarter of 2019 improved by 6% compared to the same period in 2018. The increased copper recoveries were a result of sustained metallurgical improvements initiated in 2018. While recoveries vary from quarter to quarter depending on the complexity and grade of the ore feed, the Company is seeing results from ongoing recovery improvement initiatives. These initiatives include those targeting flotation operating efficiencies (improvement at the washing station in column cells and water distribution in the processing plant), and the integration of an automated, advanced process control system in the grinding and bulk flotation circuits.

During the second quarter of 2019, a six-day scheduled maintenance shutdown of the Constancia mill was performed. Combined mine, mill and G&A unit operating costs in the second quarter of 2019 were consistent with the same period in 2018, reflecting correspondingly lower ore throughput and higher maintenance costs due to the plant shutdown. In addition, in line with the mine plan and our first quarter 2019 operations update, mined copper grades during the second quarter of 2019 were below the expected annual average. The maintenance shutdown and the variations in copper grade are consistent with the full year plan for Constancia, and we continue to expect production and cost guidance to be met for the full year 2019.

11

The year-to-date production variances were driven by the same factors as the second quarter variances versus prior year.

| Three months ended | Six months ended | Guidance | ||||

| Contained metal in | Jun. 30, | Jun. 30, | Jun. 30, | Jun. 30, | Annual | |

| concentrate produced | 2019 | 2018 | 2019 | 2018 | 2019 | |

| Copper | tonnes | 24,232 | 26,818 | 56,075 | 58,369 | 100,000 - 125,000 |

| Gold | oz | 3,794 | 5,190 | 9,151 | 10,608 | |

| Silver | oz | 551,807 | 596,570 | 1,186,737 | 1,242,456 | |

| Molybdenum | tonnes | 334 | 141 | 638 | 205 | 1,100 - 1,200 |

| Precious metals1 | oz | 11,677 | 13,712 | 26,104 | 28,357 | 45,000 - 55,000 |

| 1 |

Precious metals production includes gold and silver production on a gold-equivalent basis. Silver is converted to gold at a ratio of 70:1. |

In the second quarter of 2019 production of copper was lower than the same period in 2018, mainly due to lower copper grades, as per the mine plan, partially offset by higher copper recoveries from recent metallurgical initiatives. Production of gold and silver during the second quarter of 2019 was lower than the same period in 2018 due to lower grades. Production results for the first half of 2019 were driven by the same factors as the second quarter variances versus prior year, including the regularly scheduled mill maintenance shutdown occurring in the second quarter each year.

We expect production of all metals and costs at Constancia to be in line with the full year guidance for 2019.

Peru Cash Cost and Sustaining Cash Cost

12

| Three months ended | Six months ended | ||||

| Jun. 30, | Jun. 30, | Jun. 30, | Jun. 30, | ||

| 2019 | 2018 | 2019 | 2018 | ||

| Cash cost per pound of copper produced, net of | |||||

| by-product credits1 | $/lb | 1.63 | 1.64 | 1.38 | 1.46 |

| Sustaining cash cost per pound of copper | |||||

| produced, net of by-product credits1 | $/lb | 2.09 | 1.82 | 1.69 | 1.63 |

| 1 | Cash cost and sustaining cash costs per pound of copper produced, net of by-product credits, are not recognized under IFRS. For more detail on these non-IFRS financial performance measures, please see the discussion under the "Non-IFRS Financial Performance Measures" section of this MD&A. |

Cash cost per pound of copper produced, net of by-product credits, for the second quarter of 2019 is in line with the same period in 2018 due to lower copper production being offset by higher by-product credits.

Sustaining cash cost per pound of copper produced, net of by-product credits, for the three and six months ended June 30, 2019 was $2.09 and $1.69, respectively. This represents an increase of 15% and 4%, respectively, from the same period in 2018, due to higher sustaining costs in heavy civil works, mine equipment overhauls and lower copper production.

Metal Sold

| Three months ended | Six months ended | ||||

| Jun. 30, | Jun. 30, | ||||

| 2019 | Jun. 30, 2018 | 2019 | Jun. 30, 2018 | ||

| Payable metal in concentrate | |||||

| Copper | tonnes | 25,778 | 25,409 | 52,440 | 54,977 |

| Gold | oz | 4,056 | 3,764 | 10,274 | 8,671 |

| Silver | oz | 504,259 | 438,532 | 1,256,518 | 1,034,162 |

| Molybdenum | tonnes | 419 | — | 653 | 137 |

13

MANITOBA OPERATIONS REVIEW

Mines

| Three months ended | Six months ended | ||||

| Jun. 30, | Jun. 30, | ||||

| 2019 | Jun. 30, 2018 | 2019 | Jun. 30, 2018 | ||

| 777 | |||||

| Ore | tonnes | 288,599 | 213,134 | 567,121 | 471,520 |

| Copper | % | 1.34 | 1.55 | 1.49 | 1.37 |

| Zinc | % | 3.37 | 5.09 | 3.28 | 4.96 |

| Gold | g/tonne | 1.60 | 1.99 | 1.65 | 2.04 |

| Silver | g/tonne | 18.92 | 31.18 | 20.31 | 30.60 |

| Lalor | |||||

| Ore | tonnes | 411,701 | 339,064 | 800,184 | 661,618 |

| Copper | % | 0.73 | 0.81 | 0.75 | 0.74 |

| Zinc | % | 6.34 | 6.30 | 6.51 | 5.99 |

| Gold | g/tonne | 2.12 | 2.30 | 1.90 | 2.18 |

| Silver | g/tonne | 22.32 | 26.79 | 24.09 | 27.01 |

| Reed1 | |||||

| Ore | tonnes | — | 142,132 | — | 264,441 |

| Copper | % | — | 3.25 | — | 3.39 |

| Zinc | % | — | 0.75 | — | 0.84 |

| Gold | g/tonne | — | 0.79 | — | 0.75 |

| Silver | g/tonne | — | 8.34 | — | 8.84 |

| Total Mines | |||||

| Ore | tonnes | 700,300 | 694,330 | 1,367,305 | 1,397,579 |

| Copper | % | 0.98 | 1.54 | 1.06 | 1.45 |

| Zinc | % | 5.12 | 4.79 | 5.17 | 4.67 |

| Gold | g/tonne | 1.90 | 1.89 | 1.80 | 1.86 |

| Silver | g/tonne | 20.92 | 24.36 | 22.52 | 24.78 |

| 1 | Mining activities at Reed were completed in August 2018. Comparable 2018 numbers include 100% of Reed mine production. Hudbay purchased 30% of the Reed ore production from its joint venture partner on market-based terms. |

| Three months ended | Six months ended | ||||

| Jun. 30, | Jun. 30, | ||||

| Unit Operating Costs1,2 | 2019 | Jun. 30, 2018 | 2019 | Jun. 30, 2018 | |

| Mines | |||||

| 777 | C$/tonne | 77.12 | 85.36 | 76.59 | 82.53 |

| Lalor | C$/tonne | 113.18 | 86.35 | 107.60 | 86.56 |

| Reed | C$/tonne | — | 67.48 | — | 79.11 |

| Total Mines | C$/tonne | 98.32 | 83.14 | 94.74 | 84.07 |

| 1 | Reflects costs per tonne of ore mined. |

| 2 | Unit costs is a non-IFRS financial performance measure with no standardized definition under IFRS. For further information and a detailed reconciliation, please see the discussion under the "Non-IFRS Financial Reporting Measures" section of this MD&A. |

14

Ore mined at our Manitoba operations during the second quarter of 2019 increased by 1% compared to the same period in 2018. This increase is due to higher production volumes at both 777 and Lalor, offset by the closure of the Reed mine in August 2018.

Overall, copper and silver grades were 36% and 14% lower, respectively, in the second quarter of 2019 compared to the same period of 2018 while zinc grades were 7% higher and gold grades were consistent over the period. Lower copper grades reflect the cessation of high-grade copper production from Reed following its closure, while grade variances for zinc and silver were due to planned stope sequencing at 777 and Lalor.

Ore mined at 777 in the second quarter of 2019 increased by 35%, compared to the same period last year. The higher production is attributable to implementation of management systems designed to improve mobile equipment availability and the key performance indicators for drilling, blasting and backfilling processes. Unit operating costs for 777 decreased by 10% for the second quarter of 2019 when compared to the same period in 2018 due to higher production volumes.

Ore mined at Lalor in the second quarter of 2019 increased by 21% compared to the same period last year. The higher production is attributable to a number of initiatives implemented as part of the production ramp up to 4,500 tonnes per day, including mine design changes, contract strategies, asset integrity and work management programs. Unit operating costs for Lalor for the second quarter of 2019 increased by 31% compared to the same period in 2018 due to the costs associated with some of these initiatives, together with increases to development metres required as part of the mine design changes.

Year-to-date ore mined at our Manitoba operations was 2% lower than the same period in 2018 due to the closure of the Reed mine, which was offset by higher year-to-date production volumes at both 777 and Lalor. Year-to-date copper, gold and silver grades were 27%, 3%, and 9% lower, respectively, compared to the same period of 2018. Zinc grade was 11% higher in the first half of 2019 compared to the same period of 2018. Year-to-date total mine unit costs were 13% higher than the same period in 2018 due to higher unit operating costs at Lalor, partially offset by lower unit operating costs for 777. The year-to-date operating variances were driven by the same factors that impacted second quarter operating variances.

15

Processing Facilities

| Three months ended | Six months ended | ||||

| Jun. 30, | Jun. 30, | ||||

| 2019 | Jun. 30, 2018 | 2019 | Jun. 30, 2018 | ||

| Flin Flon Concentrator | |||||

| Ore | tonnes | 367,017 | 439,327 | 656,261 | 830,954 |

| Copper | % | 1.26 | 2.14 | 1.39 | 1.95 |

| Zinc | % | 3.84 | 3.61 | 3.69 | 3.87 |

| Gold | g/tonne | 1.71 | 1.66 | 1.69 | 1.71 |

| Silver | g/tonne | 19.82 | 22.25 | 20.68 | 23.33 |

| Copper concentrate | tonnes | 18,081 | 38,384 | 34,825 | 65,560 |

| Concentrate grade | % Cu | 22.54 | 22.82 | 23.02 | 22.86 |

| Zinc concentrate | tonnes | 23,455 | 27,371 | 40,365 | 55,179 |

| Concentrate grade | % Zn | 51.71 | 49.55 | 50.74 | 49.56 |

| Copper recovery | % | 88.0 | 93.3 | 88.0 | 92.7 |

| Zinc recovery | % | 86.0 | 85.6 | 84.7 | 85.2 |

| Gold recovery | % | 61.3 | 65.3 | 61.5 | 65.0 |

| Silver recovery | % | 53.0 | 63.4 | 52.7 | 61.1 |

| Contained metal in concentrate produced | |||||

| Copper | tonnes | 4,075 | 8,760 | 8,016 | 14,986 |

| Zinc | tonnes | 12,128 | 13,563 | 20,482 | 27,347 |

| Precious metals1 | oz | 14,162 | 18,131 | 25,195 | 35,069 |

| Stall Concentrator | |||||

| Ore | tonnes | 339,616 | 318,275 | 661,139 | 595,017 |

| Copper | % | 0.71 | 0.76 | 0.74 | 0.69 |

| Zinc | % | 6.36 | 6.56 | 6.55 | 6.23 |

| Gold | g/tonne | 2.08 | 2.14 | 1.92 | 2.11 |

| Silver | g/tonne | 22.03 | 26.35 | 24.39 | 26.99 |

| Copper concentrate | tonnes | 9,886 | 9,733 | 20,998 | 17,442 |

| Concentrate grade | % Cu | 20.79 | 21.03 | 20.21 | 19.93 |

| Zinc concentrate | tonnes | 38,122 | 38,356 | 76,615 | 67,759 |

| Concentrate grade | % Zn | 51.70 | 51.12 | 51.42 | 51.07 |

| Copper recovery | % | 85.6 | 84.5 | 86.4 | 84.8 |

| Zinc recovery | % | 91.2 | 94.0 | 91.0 | 93.4 |

| Gold recovery | % | 52.5 | 54.8 | 55.4 | 57.9 |

| Silver recovery | % | 56.5 | 57.8 | 60.6 | 59.1 |

| Contained metal in concentrate produced | |||||

| Copper | tonnes | 2,056 | 2,047 | 4,244 | 3,476 |

| Zinc | tonnes | 19,710 | 19,607 | 39,393 | 34,605 |

| Precious metals1 | oz | 13,857 | 14,232 | 27,090 | 27,701 |

| 1 |

Precious metals production includes gold and silver production on a gold-equivalent basis. Silver is converted to gold at a ratio of 70:1. |

16

| Three months ended | Six months ended | Guidance | ||||

| Jun. 30, | Jun. 30, | Jun. 30, | Jun. 30, | Annual | ||

| Unit Operating Costs1 | 2019 | 2018 | 2019 | 2018 | 2019 | |

| Concentrators | ||||||

| Flin Flon | C$/tonne | 20.67 | 19.99 | 22.90 | 21.38 | |

| Stall | C$/tonne | 24.61 | 25.44 | 25.18 | 26.33 | |

| Combined mine/mill unit operating costs2,3 | ||||||

| Manitoba | C$/tonne | 135 | 120 | 140 | 129 | 115 - 135 |

|

1 |

Reflects costs per tonne of milled ore. |

|

2 |

Reflects combined mine, mill and G&A costs per tonne of milled ore. Comparable 2018 numbers include the cost of ore purchased from our joint venture partner at Reed mine. |

|

3 |

Combined unit costs is a non-IFRS financial performance measure with no standardized definition under IFRS. For further information and a detailed reconciliation, please see the discussion under the "Non-IFRS Financial Reporting Measures" section of this MD&A. |

Ore processed in Flin Flon in the second quarter of 2019 was 16% lower than the same period in 2018 due to the Reed mine closure, partially offset by increased production from the 777 mine. Copper, gold and silver recoveries in the second quarter of 2019 were 6%, 6%, and 16% lower, respectively, compared with the same period in 2018 due to lower head grades. Zinc recoveries were consistent quarter-over-quarter. Unit operating costs at the Flin Flon concentrator were higher in the second quarter of 2019 compared to the same period in 2018 as a result of lower processed volumes.

Ore processed for the first half of 2019 in Flin Flon was 21% lower than 2018 for the same reasons noted above. Copper, zinc, gold and silver recoveries for the year-to-date were 5%, 1%, 5% and 14% lower, respectively, compared to 2018 as a result of lower grades. Year-to-date unit operating costs at the Flin Flon concentrator were 7% higher when compared to 2018 as a result of lower production volumes from the mines.

The Stall concentrator achieved record ore throughput which was 7% higher than the same period in 2018 due to ongoing operational and maintenance improvements. Copper recoveries were 1% higher and zinc recoveries were 3% lower in the second quarter of 2019 compared with the same period in 2018. Unit operating costs at the Stall concentrator were 3% lower in the second quarter of 2019 compared to the same period in 2018 as a result of increased throughput. Ore processed for the first half of 2019 at Stall was 11% higher, and recoveries for copper at the Stall concentrator were higher than the comparative 2018 period. Year-to-date unit operating costs at the Stall concentrator were 4% lower than 2018, primarily as a result of higher production and improved mill reliability.

Manitoba combined mine, mill and G&A unit operating costs in the second quarter of 2019 were 13% higher than in the same period in 2018 due mainly to the Reed closure and higher mining costs at Lalor associated with the production ramp up. In addition, combined unit costs were negatively impacted due to the timing of batching the Lalor ore in the Flin Flon mill, as not all of the ore that was transported to Flin Flon was milled during the quarter. Manitoba combined unit costs are expected to be within guidance ranges for the full year 2019.

17

| Three months ended | Six months ended | Guidance | ||||

| Manitoba contained metal in | Jun. 30, | Jun. 30, | Jun. 30, | Jun. 30, | Annual | |

| concentrate produced1,2 | 2019 | 2018 | 2019 | 2018 | 2019 | |

| Copper | tonnes | 6,131 | 10,807 | 12,260 | 18,462 | 22,000 - 25,000 |

| Gold | oz | 24,305 | 27,290 | 44,510 | 52,965 | |

| Silver | oz | 260,000 | 355,091 | 544,265 | 686,343 | |

| Zinc | tonnes | 31,838 | 33,170 | 59,875 | 61,952 | 100,000 - 115,000 |

| Precious metals3 | oz | 28,019 | 32,363 | 52,285 | 62,770 | 105,000 - 125,000 |

|

1 |

Includes 100% of Reed mine production. |

|

2 |

Metal reported in concentrate is prior to deductions associated with smelter terms. |

|

3 |

Precious metals production includes gold and silver production on a gold-equivalent basis. Silver is converted to gold at a ratio of 70:1. |

In the second quarter of 2019, copper, gold, zinc, and silver production were 43%, 11%, 4% and 27% lower, respectively, compared to the same period in 2018 due to the closure of Reed mine, partially offset by increased production at 777 and Lalor. Precious metals production in the second quarter of 2019 was also affected by the stope sequencing of Lalor gold zone ores and the timing of processing as this material is currently transported to the Flin Flon mill and blended to achieve optimal recoveries. Full year production of all metals is expected to be within the annual guidance ranges.

Zinc Plant

| Three months ended | Six months ended | Guidance | ||||

| Jun. 30, | Jun. 30, | Jun. 30, | Jun. 30, | Annual | ||

| Zinc Production | 2019 | 2018 | 2019 | 2018 | 2019 | |

| Zinc Concentrate Treated | ||||||

| Domestic | tonnes | 57,929 | 53,865 | 108,023 | 108,273 | |

| Refined Metal Produced | ||||||

| Domestic | tonnes | 27,486 | 25,520 | 51,205 | 50,851 | 95,000 - 105,000 |

18

| Three months ended | Six months ended | Guidance | ||||

| Jun. 30, | Jun. 30, | Jun. 30, | Jun. 30, | Annual | ||

| Unit Operating Costs | 2019 | 2018 | 2019 | 2018 | 2019 | |

| Zinc Plant 1,2 | C$/lb | 0.44 | 0.49 | 0.48 | 0.50 | 0.47 - 0.55 |

|

1 |

Zinc unit operating costs include G&A costs. |

|

2 |

Zinc unit costs is a non-IFRS financial performance measure with no standardized definition under IFRS. For further information and a detailed reconciliation, please see the discussion under the "Non-IFRS Financial Reporting Measures" section of this MD&A. |

Production of cast zinc in the second quarter of 2019 was 8% higher compared with the same period in 2018 as a result of increased availability of zinc concentrate at the start of the quarter. Operating costs per pound of zinc metal produced were slightly lower compared with the same periods in 2018 due to higher production volume of refined zinc combined with lower zinc plant costs.

Manitoba Cash Cost and Sustaining Cash Cost

| Three months ended | Six months ended | ||||

| Jun. 30, | Jun. 30, | Jun. 30, | Jun. 30, | ||

| 2019 | 2018 | 2019 | 2018 | ||

| Cost per pound of copper produced | |||||

| Cash cost per pound of copper produced, net | |||||

| of by-product credits 1 | $/lb | (0.15) | (0.71) | 0.31 | (0.58) |

| Sustaining cash cost per pound of copper | |||||

| produced, net of by-product credits 1 | $/lb | 2.11 | 0.38 | 2.48 | 0.65 |

| Cost per pound of zinc produced | |||||

| Cash cost per pound of zinc produced, net of | |||||

| by-product credits 1 | $/lb | 0.38 | 0.11 | 0.52 | 0.36 |

| Sustaining cash cost per pound of zinc | |||||

| produced, net of by-product credits 1 | $/lb | 0.82 | 0.46 | 0.97 | 0.73 |

| 1 | Cash cost and sustaining cash cost per pound of copper & zinc produced, net of by-product credits, are not recognized under IFRS. For more detail on this non-IFRS financial performance measure, please see the discussion under the "Non-IFRS Financial Performance Measures" section of this MD&A. |

Cash cost per pound of copper produced, net of by-product credits, in the second quarter of 2019 was negative $0.15 per pound of copper produced. These costs were higher compared to the same period in 2018, primarily as a result of lower copper production and zinc by-product revenue.

Sustaining cash cost per pound of copper produced, net of by-product credits, in the second quarter of 2019 was $2.11, which is higher than the prior year period due to higher cash costs and increased capital development expenditures at Lalor. Copper produced in the second quarter of 2019 was 43% lower than the same quarter in 2018 as a result of the closure of Reed mine, offset by increased production at 777 and Lalor.

Cash cost and sustaining cash cost per pound of zinc produced, net of by-product credits, in the second quarter of 2019 were higher compared to the same period last year as a result of lower copper and precious metals by-product revenue and higher capital spending.

Cash costs and sustaining cash costs were higher in the first half of 2019 compared to the corresponding period of 2018 due to the same factors that affected second quarter results.

19

Metal Sold

| Three months ended | Six months ended | ||||

| Jun. 30, | Jun. 30, | Jun. 30, | Jun. 30, | ||

| 2019 | 2018 | 2019 | 2018 | ||

| Payable metal in concentrate | |||||

| Copper | tonnes | 7,393 | 10,062 | 12,448 | 17,000 |

| Gold | oz | 26,482 | 25,932 | 42,893 | 47,082 |

| Silver | oz | 300,042 | 250,952 | 530,689 | 541,778 |

| Zinc | tonnes | — | 975 | — | 2,675 |

| Refined zinc | tonnes | 24,224 | 27,193 | 47,178 | 50,945 |

20

FINANCIAL REVIEW

Financial Results

In the second quarter of 2019, we recorded a net loss of $54.1 million compared to a profit of $24.7 million for the same period in 2018, a decrease in profit of $78.8 million.

Year-to date in 2019, we recorded a net loss of $67.6 million compared to a profit of $66.1 million in the same period in 2018, a decrease in profit of $133.7 million.

The following table provides further details on these variances:

| Three months ended | Six months ended | |

| (in $ millions) | June 30, 2019 | June 30, 2019 |

| (Decrease) increase in components of profit or loss: | ||

| Revenues | (41.9) | (136.3) |

| Cost of sales | ||

| Mine operating costs | 0.2 | 22.2 |

| Depreciation and amortization | (7.6) | (4.2) |

| Selling and administrative expenses | (4.3) | (13.5) |

| Other operating expenses | (28.7) | (32.5) |

| Net finance expense | (10.9) | (22.1) |

| Other | (0.5) | 1.4 |

| Tax | 14.9 | 51.3 |

| (Decrease) increase in profit for the period | (78.8) | (133.7) |

Revenue

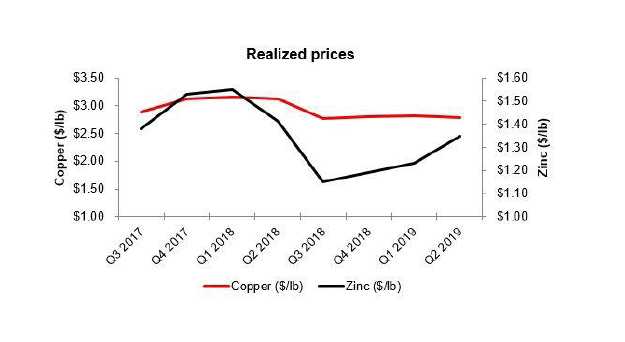

Revenue for the second quarter of 2019 was $329.4 million, $41.9 million lower than the same period in 2018, primarily as a result of lower metal prices for most commodities, and lower copper and zinc sales volumes.

Year-to-date revenue in 2019 was $621.7 million, $136.3 million lower than 2018, due to the same reasons as described for the quarterly variance above.

21

| Three months ended | Six months ended | |

| (in $ millions) | June 30, 2019 | June 30, 2019 |

| Metals prices1 | ||

| Lower copper prices | (22.7) | (46.6) |

| Lower zinc prices | (7.7) | (26.2) |

| Higher gold prices | 1.2 | 0.3 |

| Lower silver prices | (1.0) | (1.3) |

| Sales volumes | ||

| Lower copper sales volumes | (15.2) | (46.3) |

| Lower zinc sales volumes | (13.0) | (22.2) |

| Higher (lower) gold sales volumes | 1.1 | (4.3) |

| Higher silver sales volumes | 3.0 | 6.0 |

| Other | ||

| Higher derivative mark-to-market gains | 0.7 | 2.1 |

| Molybdenum and other volume and pricing differences | 11.3 | 14.4 |

| Variable consideration adjustments | — | (16.5) |

| Effect of lower treatment and refining charges | 0.4 | 4.3 |

| Decrease in revenue in 2019 compared to 2018 | (41.9) | (136.3) |

| 1 |

See discussion below for further information regarding metals prices. |

Our revenue by significant product type is summarized below:

| Three months ended | Six months ended | |||

| (in $ millions) | Jun. 30, 2019 | Jun. 30, 2018 | Jun. 30, 2019 | Jun. 30, 2018 |

| Copper | 205.3 | 242.8 | 407.6 | 499.6 |

| Zinc | 71.6 | 93.3 | 138.8 | 184.2 |

| Gold | 42.3 | 41.6 | 70.8 | 78.2 |

| Silver | 19.8 | 19.0 | 46.4 | 41.2 |

| Molybdenum | 11.2 | — | 17.6 | 3.3 |

| Other metals | 1.4 | 1.5 | 2.5 | 2.4 |

| Gross revenue | 351.6 | 398.2 | 683.7 | 808.9 |

| Variable consideration adjustments | — | — | (16.3) | 0.2 |

| Pricing and volume adjustments1 | (0.3) | (4.6) | (3.6) | (4.8) |

| Treatment and refining charges | (21.9) | (22.3) | (42.1) | (46.4) |

| Revenue | 329.4 | 371.3 | 621.7 | 757.9 |

1 Pricing and volume adjustments represents mark-to-market adjustments on provisionally prices sales, realized and unrealized changes to fair value for non-hedge derivative contracts and adjustments to originally invoiced weights and assays.

For further detail on variable consideration adjustments, refer to note 15 of our consolidated interim financial statements.

22

Realized sales prices

This measure is intended to enable management and investors to understand the average realized price of metals sold to third parties in each reporting period. The average realized price per unit sold does not have any standardized meaning prescribed by IFRS, is unlikely to be comparable to similar measures presented by other issuers, and should not be considered in isolation or a substitute for measures of performance prepared in accordance with IFRS.

For sales of copper, gold and silver we may enter into non-hedge derivatives (“QP hedges”) which are intended to manage the provisional pricing risk arising from quotational period terms in concentrate sales agreements. The QP hedges are not removed from the calculation of realized prices. We expect that gains and losses on QP hedges will offset provisional pricing adjustments on concentrate sales contracts.

Our realized prices for the second quarter in 2019 and 2018, respectively, are summarized below:

| Realized prices1 for the | Realized prices1 for the | ||||||

| Three months ended | Six months ended | ||||||

| LME QTD | LME YTD | ||||||

| 20192 | Jun. 30, 2019 | Jun. 30, 2018 | 20192 | Jun. 30, 2019 | Jun. 30, 2018 | ||

| Prices | |||||||

| Copper | $/lb | 2.77 | 2.78 | 3.08 | 2.80 | 2.81 | 3.12 |

| Zinc | $/lb | 1.25 | 1.35 | 1.50 | 1.24 | 1.33 | 1.56 |

| Gold3 | $/oz | 1,441 | 1,404 | 1,401 | 1,375 | ||

| Silver3 | $/oz | 24.60 | 25.81 | 25.00 | 27.58 | ||

| Molybdenum | $/lb | 12.24 | — | 12.32 | 12.93 | ||

|

1 |

Realized prices exclude refining and treatment charges and are on the sale of finished metal or metal in concentrate. Realized prices include the effect of provisional pricing adjustments on prior period sales. |

|

|

|

|

2 |

London Metal Exchange average for copper and zinc prices. |

|

|

|

|

3 |

Sales of gold and silver from our 777 and Constancia mines are subject to our precious metals stream agreement with Wheaton Precious Metals, pursuant to which we recognize deferred revenue for precious metals deliveries and also receive cash payments. Stream sales are included within realized prices and their respective deferred revenue and cash payment rates can be found on page 23. |

23

The following table provides a reconciliation of average realized price per unit sold, by metal, to revenues as shown in the consolidated financial statements.

| Three months ended June 30, 2019 | |||||||

| (in $ millions) 1 | Copper | Zinc | Gold | Silver | Molybdenum | Other | Total |

| Revenue per financial statements | 205.3 | 71.6 | 42.3 | 19.8 | 11.2 | 1.4 | 351.6 |

| Pricing and volume adjustments2 | (2.1) | — | 1.7 | 0.0 | 0.1 | — | (0.3) |

| Derivative mark-to-market3 | — | 0.6 | — | — | — | — | 0.6 |

| Revenue, excluding mark-to-market | |||||||

| on non-QP hedges | 203.2 | 72.2 | 44.0 | 19.8 | 11.3 | 1.4 | 351.9 |

| Payable metal in concentrate sold 4 | 33,171 | 24,224 | 30,538 | 804,301 | 419 | — | — |

| Realized price 5 | 6,128 | 2,981 | 1,441 | 24.60 | 26,987 | — | — |

| Realized price 6 | 2.78 | 1.35 | — | — | 12.24 | — | — |

| Six Months Ended June 30, 2019 | |||||||

| (in $ millions) 1 | Copper | Zinc | Gold | Silver | Molybdenum | Other | Total |

| Revenue per financial statements | 407.6 | 138.8 | 70.8 | 46.4 | 17.6 | 2.5 | 683.7 |

| Pricing and volume adjustments2 | (5.7) | (0.1) | 3.7 | (1.7) | 0.2 | — | (3.6) |

| Derivative mark-to-market3 | — | (0.3) | — | — | — | — | (0.3) |

| Revenue, excluding mark-to-market | |||||||

| on non-QP hedges | 401.9 | 138.4 | 74.5 | 44.7 | 17.8 | 2.5 | 679.8 |

| Payable metal in concentrate sold 4 | 64,888 | 47,178 | 53,167 | 1,787,207 | 653 | ||

| Realized price 5 | 6,194 | 2,933 | 1,401 | 25.00 | 27,166 | ||

| Realized price 6 | 2.81 | 1.33 | — | — | 12.32 | ||

| Three months ended June 30, 2018 | |||||||

| (in $ millions) 1 | Copper | Zinc | Gold | Silver | Molybdenum | Other | Total |

| Revenue per financial statements | 242.8 | 93.3 | 41.6 | 19.0 | — | 1.5 | 398.2 |

| Pricing and volume adjustments2 | (1.7) | (1.7) | 0.1 | (1.2) | — | (0.1) | (4.6) |

| Derivative mark-to-market3 | — | 1.3 | — | — | — | — | 1.3 |

| Revenue, excluding mark-to-market | |||||||

| on non-QP hedges | 241.1 | 92.9 | 41.7 | 17.8 | — | 1.4 | 394.9 |

| Payable metal in concentrate sold 4 | 35,471 | 28,168 | 29,696 | 689,484 | — | — | — |

| Realized price 5 | 6,798 | 3,299 | 1,404 | 25.81 | — | — | — |

| Realized price 6 | 3.08 | 1.50 | — | — | — | — | — |

| Six months ended June 30, 2018 | |||||||

| (in $ millions) 1 | Copper | Zinc | Gold | Silver | Molybdenum | Other | Total |

| Revenue per financial statements | 499.6 | 184.2 | 78.2 | 41.2 | 3.3 | 2.4 | 808.9 |

| Pricing and volume adjustments2 | (4.7) | (1.3) | (1.6) | 2.2 | 0.6 | — | (4.8) |

| Derivative mark-to-market3 | — | 1.8 | — | — | — | — | 1.8 |

| Revenue, excluding mark-to-market | |||||||

| on non-QP hedges | 494.9 | 184.7 | 76.6 | 43.4 | 3.9 | 2.4 | 805.9 |

| Payable metal in concentrate sold 4 | 71,977 | 53,620 | 55,753 | 1,575,940 | 137 | — | — |

| Realized price 5 | 6,875 | 3,444 | 1,375 | 27.58 | 28,511 | — | — |

| Realized price 6 | 3.12 | 1.56 | — | — | 12.93 | — | — |

|

1 |

Average realized price per unit sold may not calculate based on amounts presented in this table due to rounding. |

|

2 |

Pricing and volume adjustments represents mark-to-market adjustments on provisionally priced sales, realized and unrealized changes to fair value for non-hedge derivative contracts and adjustments to originally invoiced weights and assays. |

|

3 |

Derivative mark-to-market excludes mark-to-market on QP hedges. |

|

4 |

Copper and zinc shown in metric tonnes and gold and silver shown in ounces. |

|

5 |

Realized price for copper, zinc and molybdenum in $/metric tonne and realized price for gold and silver in $/oz. |

| 6 |

Realized price for copper, zinc and molybdenum in $/lb. |

24

The price, quantity and mix of metals sold, affect our revenue, operating cash flow and profit. Revenue from metals sales can vary from quarter to quarter due to production levels, shipping volumes and transfer of risk and title to customers.

Stream Sales

The following table shows stream sales included within realized prices and their respective deferred revenue and cash payment rates:

| Three months ended | Six months ended | ||||

| Jun. 30, 2019 | Jun. 30, 2019 | ||||

| Manitoba | Peru | Manitoba | Peru | ||

| Gold | oz | 5,294 | 2,404 | 8,908 | 5,910 |

| Silver | oz | 108,667 | 477,927 | 208,100 | 1,212,452 |

| Gold deferred revenue drawdown rate1,2 | $/oz | 1,168 | 948 | 1,172 | 948 |

| Gold cash rate3 | $/oz | 416 | 400 | 416 | 400 |

| Silver deferred revenue drawdown rate1,2 | $/oz | 22.34 | 21.77 | 22.42 | 21.77 |

| Silver cash rate3 | $/oz | 6.14 | 5.90 | 6.14 | 5.90 |

| Three months ended | Six months ended | ||||

| Jun. 30, 2018 | Jun. 30, 2018 | ||||

| Manitoba | Peru | Manitoba | Peru | ||

| Gold | oz | 3,812 | 2,172 | 8,944 | 5,419 |

| Silver | oz | 69,565 | 409,802 | 222,471 | 984,194 |

| Gold deferred revenue drawdown rate1 | $/oz | 1,265 | 967 | 1,279 | 967 |

| Gold cash rate 3 | $/oz | 412 | 400 | 412 | 400 |

| Silver deferred revenue drawdown rate1 | $/oz | 24.60 | 21.79 | 24.84 | 21.79 |

| Silver cash rate 3 | $/oz | 6.08 | 5.90 | 6.08 | 5.90 |

| 1 | For the three and six months ended June 30, 2019 deferred revenue amortization is recorded in Manitoba at C$1,562/oz and C$29.89/oz for gold and silver (June 30, 2018 - C$1,635/oz and C$31.88/oz for gold and silver), respectively, and converted to US dollars at the exchange rate in effect at the time of revenue recognition. |

| 2 | Deferred revenue drawdown rates for gold and silver do not include variable consideration adjustments. |

| 3 | The gold and silver cash rate for Manitoba increased by 1% from $400/oz and $5.90/oz effective August 1, 2015. Subsequently every year, on August 1, the cash rate will increase by 1% compounded. The weighted average cash rate is disclosed. |

25

Cost of Sales

Our detailed cost of sales is summarized as follows:

| Three months ended | Six months ended | |||

| Jun. 30, | Jun. 30, | |||

| (in thousands) | 2019 | Jun. 30, 2018 | 2019 | Jun. 30, 2018 |

| Peru | ||||

| Mining | 21,725 | 23,513 | 45,611 | 47,351 |

| Milling | 42,953 | 42,193 | 77,989 | 74,644 |

| Changes in product inventory | 1,680 | (5,289) | (5,647) | (6,670) |

| Depreciation and amortization | 55,636 | 51,563 | 104,953 | 105,259 |

| G&A | 14,677 | 12,494 | 27,203 | 29,950 |

| Freight, royalties and other charges | 13,616 | 12,714 | 27,690 | 27,097 |

| Total Peru cost of sales | 150,287 | 137,188 | 277,799 | 277,631 |

| Manitoba | ||||

| Mining | 51,466 | 42,007 | 97,112 | 86,750 |

| Milling | 11,918 | 13,080 | 23,755 | 26,167 |

| Zinc plant | 17,213 | 17,928 | 34,244 | 36,762 |

| Purchased ore and concentrate (before | ||||

| inventory changes) | — | 9,747 | — | 17,275 |

| Changes in product inventory | (1,107) | 3,712 | (10,996) | (5,732) |

| Depreciation and amortization | 35,558 | 31,989 | 63,372 | 58,901 |

| G&A | 10,786 | 11,671 | 24,067 | 25,144 |

| Freight, royalties and other charges | 10,150 | 11,505 | 17,365 | 21,814 |

| Total Manitoba cost of sales | 135,984 | 141,639 | 248,919 | 267,081 |

| Cost of sales | 286,271 | 278,827 | 526,718 | 544,712 |

Total cost of sales for the second quarter of 2019 was $286.3 million, reflecting an increase of $7.4 million from the second quarter of 2018. Cost of sales related to Peru increased for the second quarter of 2019 compared to the same period of 2018 by $13.1 million. The increase is primarily the result of an increase in product inventory in the second quarter of 2018 and higher depreciation. In Manitoba, cost of sales decreased by $5.7 million compared to the second quarter of 2018 primarily as a result of the closure of the Reed mine and the associated elimination of Reed ore purchases, as well as lower milling, freight, royalties and other charges. This decrease was partially offset by higher depreciation costs and mining costs.

For details on unit operating costs refer to the respective tables in the “Operations Review” section of this MD&A.

For the second quarter of 2019, other significant variances in expenses from operations, compared to the same period in 2018, include the following:

| – |

Selling and administrative expenses increased by $4.3 million compared to the same period in 2018. This increase was mainly due to costs of $3.0 million associated with the recent proxy contest as well as fees associated with the purchase of UCM's remaining interest in the Rosemont project. |

| – |

Other operating expenses increased by $28.7 million compared to the second quarter of 2018 primarily as a result of the write down of the UCM receivable for $26.0 million and other regional costs. |

| – |

Other finance losses increased by $11.0 million compared to the same period in 2018 as a result of: |

| – | decreased foreign exchange gains of $6.6 million when compared to the same period last year, related to foreign exchange rate movements impacting certain monetary assets in the Manitoba business unit; and | |

| – | net gains on the Company's financial assets and liabilities recognized at fair value through profit or loss decreased by $4.4 million when compared to the same period last year. |

26

For 2019 year-to-date, other significant variances in expenses from operations, compared to 2018, include the following:

|

– |

Selling and administrative expenses increased by $13.5 million compared to the same period in 2018. This increase was due mainly to higher stock based compensation charges as a result of the revaluation of previously issued shares to higher share prices during the current year compared to the prior year, as well as costs associated with the recent proxy contest. | |

|

– |

Other operating expenses increased by $32.5 million primarily as a result of the write down of the UCM receivable for $26.0 million, as well as losses on disposition of certain fixed assets and other regional costs. | |

|

– |

Finance expenses increased by $7.0 million primarily due to an increase in non-cash financing charges for our precious metals steam contracts in 2019. This charge was the result of the deferred revenue adjustments for the 777 stream arrangement driven by an increase in 777's reserve and resource estimates. | |

|

– |

Other finance gains decreased by $16.6 million as a result of: | |

|

– |

decreased foreign exchange gains of $11.5 million when compared to the same period last year, related to foreign exchange rate movements impacting certain monetary assets in the Manitoba business unit; and | |

|

– |

net gains on the Company's financial assets and liabilities recognized at fair value through profit or loss decreased by $5.1 million when compared to the same period last year. | |

Tax Expense (Recovery)

For the three and six months ended June 30, 2019, tax expense decreased by $14.9 million and 51.3 million compared to the same period in 2018. The following table provides further details:

| Three months ended | Six months ended | ||||||||||

| Jun. 30, | Jun. 30, | ||||||||||

| (in $ thousands) | 2019 | Jun. 30, 2018 | 2019 | Jun. 30, 2018 | |||||||

| Deferred tax (recovery) expense - income tax 1 | $ | 9,358 | $ | 16,048 | $ | (3,020) | $ | 25,084 | |||

| Deferred tax (recovery) expense - mining tax 1 | (5,340) | (188) | (2,331) | (488) | |||||||

| Total deferred tax (recovery) expense | 4,018 | 15,860 | (5,351) | 24,596 | |||||||

| Current tax expense - income tax | (1,417) | 1,682 | 4,591 | 17,661 | |||||||

| Current tax (recovery) expense - mining tax | 7,613 | 7,582 | 6,278 | 14,525 | |||||||

| Total current tax expense | 6,196 | 9,264 | 10,869 | 32,186 | |||||||

| Tax (recovery) expense | $ | 10,214 | $ | 25,124 | $ | 5,518 | $ | 56,782 | |||

| 1 |

Deferred tax expense (recovery) represents our draw down/increase of non-cash deferred income and mining tax assets/liabilities. |

27

Income Tax Expense

Applying the estimated Canadian statutory income tax rate of 27.0% to our loss before taxes of $62.0 million for the year-to-date period in 2019 would have resulted in a tax recovery of approximately $16.7 million; however, we recorded an income tax expense of $1.6 million. The significant items causing our effective income tax rate to be different than the 27.0% estimated Canadian statutory income tax rate include:

| – | Certain deductible temporary differences with respect to Manitoba, mostly relating to decommissioning and restoration liabilities, were not recognized as we have determined that it is not probable that we will realize the recovery of these deferred tax assets based on the timing of the reversals of the deductible temporary differences and the future projected taxable profit of the Manitoba operations. Adjusted for the average annual effective tax rate methodology, this resulted in an increase in deferred tax expense of approximately $12.2 million; |

| – | The write down of the UCM receivable of $26.0 million is not deductible for local income tax purposes and therefore results in an increase in deferred tax expense of approximately $7.0 million; |

| – | Certain deductible temporary differences with respect to Peru, mostly relating to decommissioning and restoration liabilities, were not recognized as we have determined that it is not probable that we will realize the recovery of these deferred tax assets based on the timing of the reversals of the deductible temporary differences and the future projected taxable profit of the Peru operations. This resulted in an increase in deferred tax expense of approximately $3.3 million; and |

| – | A decrease in the deferred tax expense of $5.3 million is due to the fact that certain Canadian non-monetary assets are recognized at historical cost while the tax bases of the underlying assets change as exchange rates fluctuate, giving rise to temporary differences. |

Mining Tax Expense

Applying the estimated Manitoba mining tax rate of 10.0% to our loss before taxes of $62.0 million for the year-to-date period in 2019 would have resulted in a tax recovery of approximately $6.2 million and we recorded a mining tax expense of $4.0 million. Effective mining tax rates can vary significantly based on the composition of our earnings and the expected amount of mining taxable profits. Corporate costs and other costs not related to mining operations are not deductible in computing mining profits. A brief description of how mining taxes are calculated in our various business units is discussed below.

Manitoba

The Province of Manitoba imposes mining tax on profit related to the sale of mineral products mined in the Province of Manitoba (mining taxable profit) at the following rates:

| – | 10% of total mining taxable profit if mining profit is C$50 million or less; |

| – | 15% of total mining taxable profit if mining profits are between C$55 million and C$100 million; and |

| – | 17% of total mining taxable profit if mining profits exceed C$105 million. |

We estimate that the tax rate that will be applicable when temporary differences reverse will be approximately 10.0% .

Peru

The Peruvian government imposes two parallel mining tax regimes, the Special Mining Tax and the Modified Royalty, on companies' operating mining income on a sliding scale, with progressive rates ranging from 2.0% to 8.4% and 1.0% to 12.0%, respectively. Based on financial forecasts, we have recorded a deferred tax liability as at June 30, 2019, at the tax rate we expect to apply when temporary differences reverse.

28

LIQUIDITY AND CAPITAL RESOURCES

Senior Secured Revolving Credit Facilities

We have two revolving credit facilities (the “Credit Facilities”) for our Canadian and Peruvian businesses, with combined total availability of $550 million and substantially similar terms and conditions. As at June 30, 2019, between our Credit Facilities we have drawn $128.8 million in letters of credit, leaving total undrawn availability of $421.2 million. As at June 30, 2019, we were in compliance with our covenants under the Credit Facilities.

Financial Condition

Financial Condition as at June 30, 2019 compared to December 31, 2018

Cash and cash equivalents decreased by $26.0 million during the first half of the year to $489.5 million as at June 30, 2019. This decrease was mainly a result of $92.3 million of funding for capital investments primarily at our Peru and Manitoba operations, our acquisition of the remaining interest in the Rosemont project for $45.0 million and cash used in financing activities of $64.3 million. This decrease was partially offset by cash flow from operating activities of $168.7 million. We hold the majority of our cash and cash equivalents in low-risk, liquid investments with major Canadian and Peruvian financial institutions.

Working capital decreased by $17.2 million to $428.1 million from December 31, 2018 to June 30, 2019, primarily due to the decrease in our cash and cash equivalents position by $26.0 million, as well as a decrease in our current receivables by $31.3 million primarily as a result of a reduction in trade receivables. This decrease in working capital was partially offset by an increase in current inventories of $29.4 million as a result of the timing of zinc and copper metal and concentrate shipments, as well as an increase in zinc and copper concentrate work in progress and stockpile inventories during 2019.

Cash Flows

The following table summarizes our cash flows for the three and six months ended June 30, 2019 and June 30, 2018:

| Three months ended | Six months ended | |||

| Jun. 30, | Jun. 30, | Jun. 30, | Jun. 30, | |

| (in $ thousands) | 2019 | 2018 | 2019 | 2018 |

| Operating cash flow before changes in non-cash working capital | 81,146 | 131,635 | 170,740 | 263,428 |

| Change in non-cash working capital | 25,863 | (34,595) | (2,032) | (35,024) |

| Cash generated from operating activities | 107,009 | 97,040 | 168,708 | 228,404 |

| Cash (used in) generated by investing activities | (90,881) | (39,175) | (130,144) | (85,149) |

| Cash (used in) generated by financing activities | (12,089) | (11,514) | (64,342) | (60,253) |

| Effect of movement in exchange rates on cash and cash equivalents | (379) | 429 | (192) | 75 |

| (Decrease) increase in cash and cash equivalents | 3,660 | 46,780 | (25,970) | 83,077 |

29

Cash Flow from Operating Activities

Cash generated from operating activities was $107.0 million during the second quarter of 2019, an increase of $10.0 million compared with the same period last year. Operating cash flow before change in non-cash working capital was $81.1 million during the second quarter of 2019, reflecting a decrease of $50.5 million compared to the second quarter of 2018, which was offset by favourable working capital movements in the second quarter of 2019 compared to the same quarter of 2018. The decrease in operating cash flow is the result of lower realized prices and lower sales volumes of copper and zinc, as well as higher cash costs when compared to the second quarter of 2018. The decrease is partially offset by higher realized prices and higher sales volumes for gold.

Year-to-date cash generated from operating activities was $168.7 million in the first half of 2019, a decrease of $59.7 million compared to 2018. Operating cash flow before changes in non-cash working capital was $170.7 million year-to-date in 2019, a decrease of $92.7 million compared to 2018. The year-to-date decrease in operating cash flow is due to the same reasons described above for the quarter over quarter change.

Cash Flow from Investing and Financing Activities

During the second quarter of 2019, we used $103.0 million in investing and financing activities, primarily driven by $50.0 million of capital expenditures, $44.7 million net paid for the acquisition of the remaining interest in the Rosemont project, finance lease payments of $7.4 million and net financing fees paid of $4.7 million.

Year-to-date, we used $194.5 million of cash in investing and financing activities, primarily driven by $92.3 million of capital expenditures, $44.7 million paid for the acquisition of the remaining interest in the Rosemont project, interest payments of $37.4 million, finance lease payments of $14.8 million and net financing fees paid of $10.2 million.

30

Capital Expenditures

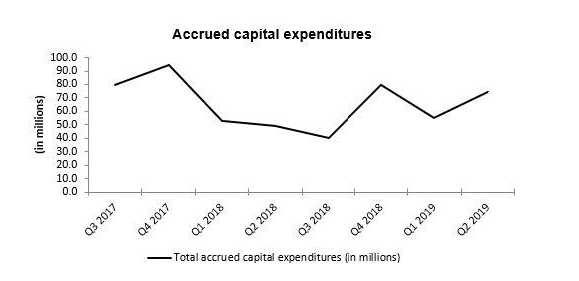

The following summarizes accrued and cash additions to capital assets for the periods indicated:

| Three months ended | Six months ended | Guidance | |||

| Jun. 30, | Jun. 30, | Jun. 30, | Jun. 30, | Annual1 | |

| (in $ millions) | 2019 | 2018 | 2019 | 2018 | 2019 |

| Manitoba sustaining capital expenditures | 27.1 | 23.6 | 51.2 | 43.8 | 100.0 |

| Peru sustaining capital expenditures 2 | 18.1 | 8.5 | 28.5 | 17.8 | 95.0 |

| Total sustaining capital expenditures | 45.2 | 32.1 | 79.7 | 61.6 | 195.0 |

| Arizona capitalized costs3 | 8.8 | 5.0 | 13.4 | 10.4 | 50.0 |

| Peru growth capitalized expenditures | 0.3 | 0.4 | 0.6 | 1.8 | 45.0 |

| Manitoba growth capitalized expenditures | 3.1 | 8.4 | 3.2 | 17.0 | 10.0 |

| Other capitalized costs 4 | 12.2 | 0.1 | 23.1 | 3.3 | |

| Capitalized exploration | 1.1 | 0.1 | 2.0 | 1.3 | 15.0 |

| Capitalized interest | 3.3 | 3.3 | 6.6 | 6.6 | |

| Total other capitalized costs | 28.8 | 17.3 | 48.9 | 40.4 | |

| Total accrued capital additions | 74.0 | 49.4 | 128.6 | 102.0 | |

| Reconciliation to cash capital additions: | |||||

| Decommissioning and restoration obligation | (11.8) | 0.3 | (26.5) | (0.8) | |

| Capitalized interest | (3.3) | (3.3) | (6.6) | (6.6) | |

| ROU asset additions | (2.1) | — | (4.6) | — | |

| Changes in capital accruals and other | (6.8) | (6.3) | 1.4 | (8.0) | |

| Total cash capital additions | 50.0 | 40.1 | 92.3 | 86.6 | |

| 1 |

Sustaining capital expenditure guidance excludes capitalized interest. |

| 2 |

Peru sustaining capital expenditures includes capitalized stripping costs. |

| 3 |

Initial guidance of $20.0 million. |

| 4 |

Other capitalized costs include decommissioning and restoration adjustments. |

Sustaining capital expenditures in Manitoba for the three and six months ended June 30, 2019 were $27.1 million and $51.2 million, respectively, an increase of $3.5 million and $7.4 million compared to the same periods in 2018. The increase in Manitoba sustaining capital expenditures compared to the same periods last year was due to increased capital development expenditures at Lalor.

Sustaining capital expenditures in Peru for the three and six months ended June 30, 2019 were $18.1 million and $28.5 million, respectively, which is an increase of $9.6 million and $10.7 million compared to the same periods in 2018. The increase in Peru sustaining capital expenditures compared to the same periods last year was the result of increased civil works projects.

As disclosed in March 2019, the Board approved a $122 million early works program for Rosemont in addition to the $20 million of initial guidance for Arizona capitalized costs. As a result of the Court's ruling issued on July 31, 2019, we have suspended most of the early works activities and now expect Rosemont project spending of approximately $30 million in 2019, together with $20 million of non-project spending.

31

Capital Commitments

As at June 30, 2019, we had outstanding capital commitments in Canada of approximately $5.1 million primarily related to Lalor mine equipment, all of which can be terminated, approximately $37.0 million in Peru primarily related to exploration option agreements, all of which can be terminated, and approximately $207.5 million in Arizona, primarily related to our Rosemont project, of which approximately $87.3 million cannot be terminated.

Contractual Obligations

The following table summarizes our significant contractual obligations as at June 30, 2019:

| Less than | 13 - 36 | 37 - 60 | More than | ||

| Payment Schedule (in $ millions) | Total | 12 months | months | months | 60 months |

| Long-term debt obligations1 | 1,400.8 | 79.6 | 154.9 | 520.5 | 645.8 |

| Lease obligations | 138.1 | 45.2 | 77.2 | 11.4 | 4.3 |

| Purchase obligation - capital commitments | 249.6 | 47.7 | 51.7 | 4.9 | 145.3 |

| Purchase obligation - other commitments2 | 687.4 | 247.6 | 221.3 | 131.1 | 87.4 |

| Pension and other employee future benefits obligations3 | 135.0 | 14.9 | 31.2 | 6.8 | 82.1 |

| Decommissioning and restoration obligations4 | 206.9 | 1.4 | 0.9 | 8.8 | 195.8 |

| Total | 2,817.8 | 436.4 | 537.2 | 683.5 | 1,160.7 |

| 1 | Long-term debt obligations include scheduled interest payments, as well as principal repayments. |

| 2 | Primarily made up of long-term agreements with operational suppliers, obligations for power purchase, concentrate handling, fleet and port |

| services, as well as deferred consideration arising from the acquisition of Rosemont's minority interest. | |

| 3 | Discounted. |

| 4 | Before inflation. |

In addition to the contractual obligations included in the above payment schedule, we also have the following commitments which impact our financial position:

| – | A profit-sharing plan with most Manitoba employees; |

| – | A profit-sharing plan with all Peru employees; |