UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21727

First Trust Mortgage Income Fund

(Exact name of registrant as specified in charter)

120 East Liberty Drive, Suite 400

Wheaton, IL 60187

(Address of principal executive offices) (Zip code)

W. Scott Jardine, Esq.

First Trust Portfolios L.P.

120 East Liberty Drive, Suite 400

Wheaton, IL 60187

(Name and address of agent for service)

registrant’s telephone number, including

area code: 630-765-8000

Date of fiscal year end: October 31

Date of reporting period: April 30, 2021

Form N-CSR is to be used by management investment

companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required

to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use

the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information

specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection

of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”)

control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing

the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection

of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

| (a) | | The Report to Shareholders is attached herewith. |

First Trust

Mortgage Income

Fund (FMY)

Semi-Annual

Report

For the Six

Months Ended

April 30,

2021

First Trust Mortgage Income Fund

(FMY)

Semi-Annual Report

April 30, 2021

| 1

|

| 2

|

| 3

|

| 5

|

| 12

|

| 13

|

| 14

|

| 15

|

| 16

|

| 23

|

Caution Regarding

Forward-Looking Statements

This report contains

certain forward-looking statements within the meaning of the Securities Act of 1933, as amended, and the Securities Exchange Act of 1934, as amended. Forward-looking statements include statements regarding the goals,

beliefs, plans or current expectations of First Trust Advisors L.P. (“First Trust” or the “Advisor”) and its representatives, taking into account the information currently available to them.

Forward-looking statements include all statements that do not relate solely to current or historical fact. For example, forward-looking statements include the use of words such as “anticipate,”

“estimate,” “intend,” “expect,” “believe,” “plan,” “may,” “should,” “would” or other words that convey uncertainty of

future events or outcomes.

Forward-looking

statements involve known and unknown risks, uncertainties and other factors that may cause the actual results, performance or achievements of First Trust Mortgage Income Fund (the “Fund”) to be materially

different from any future results, performance or achievements expressed or implied by the forward-looking statements. When evaluating the information included in this report, you are cautioned not to place undue

reliance on these forward-looking statements, which reflect the judgment of the Advisor and its representatives only as of the date hereof. We undertake no obligation to publicly revise or update these forward-looking

statements to reflect events and circumstances that arise after the date hereof.

Performance and Risk

Disclosure

There is no assurance

that the Fund will achieve its investment objectives. The Fund is subject to market risk, which is the possibility that the market values of securities owned by the Fund will decline and that the value of the

Fund’s shares may therefore be less than what you paid for them. Accordingly, you can lose money by investing in the Fund. See “Principal Risks” in the Additional Information section of this report

for a discussion of certain other risks of investing in the Fund.

Performance data quoted

represents past performance, which is no guarantee of future results, and current performance may be lower or higher than the figures shown. For the most recent month-end performance figures, please visit www.ftportfolios.com or speak with your financial advisor. Investment returns, net asset value and common share price will fluctuate and Fund shares, when sold,

may be worth more or less than their original cost.

The Advisor may also

periodically provide additional information on Fund performance on the Fund’s web page at www.ftportfolios.com.

How to Read This

Report

This report contains

information that may help you evaluate your investment in the Fund. It includes details about the Fund and presents data and analysis that provide insight into the Fund’s performance and investment approach.

By reading the portfolio

commentary by the portfolio management team of the Fund, you may obtain an understanding of how the market environment affected the Fund’s performance. The statistical information that follows may help you

understand the Fund’s performance compared to that of a relevant market benchmark.

It is important to keep

in mind that the opinions expressed by personnel of the Advisor are just that: informed opinions. They should not be considered to be promises or advice. The opinions, like the statistics, cover the period through the

date on the cover of this report. The material risks of investing in the Fund are spelled out in the prospectus, the statement of additional information, this report and other Fund regulatory filings.

First Trust Mortgage Income Fund

(FMY)

Semi-Annual Letter from the Chairman

and CEO

April 30, 2021

Dear Shareholders,

First Trust is pleased

to provide you with the semi-annual report for the First Trust Mortgage Income Fund (the “Fund”), which contains detailed information about the Fund for the six months ended April 30, 2021.

I would like to begin my

remarks by saying that this is a time for all of us to be thankful. It is astounding to me that our scientists and extended health care community successfully discovered, developed, and distributed multiple effective

vaccines to treat the coronavirus (“COVID-19”) in the span of just 15 months. Suffice it to say that we are witnessing history in the making. We even received some good news recently with respect to

wearing masks in public, a polarizing act for many politicians and Americans. The Centers for Disease Control and Prevention released a new set of guidelines in mid-May for those individuals who have been fully

vaccinated. It essentially says fully vaccinated Americans can quit wearing their masks outdoors (even in crowds), in most indoor settings, and can drop social distancing altogether. This is a big step towards

expediting the reopening of the U.S. economy.

For those who may not

know, we subscribe to the buy-and-hold philosophy of investing here at First Trust Advisors L.P., even though it means enduring lots of tough times. While the notion of being able to time the market is seductive on

its face, very few investors are skilled enough to make it work over time. I can think of no better example than the COVID-19 pandemic. The degree of uncertainty surrounding the onset of the virus alone was enough to

make the average investor want to run for cover. And if that was not enough, the 33.8% plunge in the S&P 500® Index (the “Index”) from February 19, 2020, through March 23, 2020 (23 trading days) was a real gut check

for most of us. But a funny thing happened on the way to another potential collapse of the market − it did not happen. In fact, thanks to the U.S. Federal government stepping up with trillions of dollars of

timely fiscal and monetary support, the stock market roared. From March 23, 2020 through May 14, 2021, the Index posted a total return of 90.14%, according to Bloomberg. What a shame for those investors who may have

moved some, or all, of their capital out of equities. What looked like a great time to de-risk turned out to be just the opposite.

The overall climate for

investing looks bright for a few reasons. First, U.S. real gross domestic product (“GDP”) growth is expected to grow by 6.4% year-over-year in 2021, according to the International Monetary Fund. The last

time the U.S. economy grew that fast was in 1984, when real GDP growth reached 7.2%. Second, corporate earnings are expected to recover from their 2020 slide. Bloomberg’s consensus year-over-year earnings growth

rate estimates for the Index for 2021 and 2022 were 33.17% and 12.87%, respectively, as of May 14, 2021. That is a significant rebound from the 12.44% decline in earnings in 2020. Third, inflation is rising, and that

is exactly what the Federal Reserve has been wanting for some time. Central banks around the world have spent years battling deflationary pressures, so a little bit of inflation is welcome at this stage of the

recovery. Lastly, the U.S. labor market is robust despite the talk about the millions of people who lost their jobs in the COVID-19 pandemic and are living off unemployment benefits. As of March 31, 2021, there were

8.12 million job openings in the U.S., the highest total since record-keeping began in December 2000, according to the Bureau of Labor Statistics. We need to get people back to work.

While it seems

fashionable to sell fear these days, we choose to follow the data. Remember, the Index has never failed to fully recoup the losses sustained in a market correction or bear market. Stay the course!

Thank you for giving

First Trust the opportunity to play a role in your financial future. We value our relationship with you and will report on the Fund again in six months.

Sincerely,

James A. Bowen

Chairman of the Board of Trustees

Chief Executive Officer of First Trust

Advisors L.P.

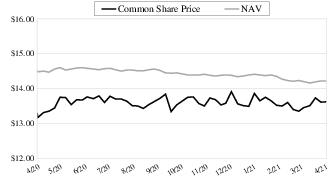

First Trust Mortgage Income Fund (FMY)

“AT A GLANCE”

As of April 30, 2021

(Unaudited)

| Fund Statistics

|

|

| Symbol on New York Stock Exchange

| FMY

|

| Common Share Price

| $13.62

|

| Common Share Net Asset Value (“NAV”)

| $14.22

|

| Premium (Discount) to NAV

| (4.22)%

|

| Net Assets Applicable to Common Shares

| $59,897,020

|

| Current Distribution per Common Share(1)

| $0.0600

|

| Current Annualized Distribution per Common Share

| $0.7200

|

| Current Distribution Rate on Common Share Price(2)

| 5.29%

|

| Current Distribution Rate on NAV(2)

| 5.06%

|

Common Share Price & NAV (weekly closing price)

| Performance

|

|

|

|

|

|

|

|

| Average Annual Total Returns |

|

| 6 Months Ended

4/30/21

| 1 Year Ended

4/30/21

| 5 Years Ended

4/30/21

| 10 Years Ended

4/30/21

| Inception

(5/25/05)

to 4/30/21

|

| Fund Performance(3)

|

|

|

|

|

|

| NAV

| 1.03%

| 3.23%

| 3.65%

| 3.53%

| 5.24%

|

| Market Value

| 4.35%

| 8.02%

| 4.25%

| 2.52%

| 4.66%

|

| Index Performance

|

|

|

|

|

|

| Bloomberg Barclays U.S. Mortgage Backed Securities (MBS) Index

| -0.27%

| -0.17%

| 2.50%

| 2.78%

| 3.90%

|

| Portfolio Characteristics

|

|

| Weighted Average Effective Duration

| 3.0 Years

|

| Weighted Average Effective Maturity

| 5.7 Years

|

| Fund Allocation

| % of Net Assets

|

| U.S. Government Agency Mortgage-Backed Securities

| 56.0%

|

| Mortgage-Backed Securities

| 34.9

|

| Asset-Backed Securities

| 3.4

|

| Net Other Assets and Liabilities(4)

| 5.7

|

| Total

| 100.0%

|

| Credit Quality(5)

| % of Total

Fixed-Income

Investments

|

| AAA

| 5.8%

|

| AA+

| 5.3

|

| AA

| 3.1

|

| AA-

| 1.1

|

| A+

| 1.6

|

| A

| 1.1

|

| BBB+

| 0.9

|

| BBB

| 0.9

|

| BB

| 2.3

|

| B

| 0.3

|

| B-

| 1.1

|

| CCC-

| 0.1

|

| CC

| 5.1

|

| Not Rated

| 10.4

|

| Government

| 57.2

|

| Cash & Cash Equivalents

| 3.7

|

| Total

| 100.0%

|

| (1)

| Most recent distribution paid or declared through 4/30/2021. Subject to change in the future.

|

| (2)

| Distribution rates are calculated by annualizing the most recent distribution paid or declared through the report date and then dividing by Common Share Price or NAV, as applicable, as of 4/30/2021.

Subject to change in the future.

|

| (3)

| Total return is based on the combination of reinvested dividend, capital gain, and return of capital distributions, if any, at prices obtained by the Dividend Reinvestment Plan and changes in NAV per

share for NAV returns and changes in Common Share Price for market value returns. Total returns do not reflect sales load and are not annualized for periods of less than one year. Past performance is not indicative of

future results.

|

| (4)

| Includes variation margin on futures.

|

| (5)

| The credit quality and ratings information presented above reflect the ratings assigned by one or more nationally recognized statistical rating organizations (NRSROs), including Standard &

Poor’s Ratings Group, a division of the McGraw Hill Companies, Inc., Moody’s Investors Service, Inc., Fitch Ratings or a comparably rated NRSRO. For situations in which a security is rated by more than one

NRSRO and the ratings are not equivalent, the highest rating is used. Sub-investment grade ratings are those rated BB+/Ba1 or lower. Investment grade ratings are those rated BBB-/Baa3 or higher. The credit ratings

shown relate to the creditworthiness of the issuers of the underlying securities in the Fund, and not to the Fund or its shares. U.S. Treasury, U.S. Agency and U.S. Agency mortgage-backed securities appear under

“Government.” Credit ratings are subject to change.

|

Portfolio Commentary

First Trust Mortgage

Income Fund (FMY)

Semi-Annual Report

April 30, 2021

(Unaudited)

Advisor

First Trust Advisors L.P.

(“First Trust” or the “Advisor”) serves as the investment advisor to the First Trust Mortgage Income Fund (the “Fund” or “FMY”) and offers customized portfolio

management using its structured, quantitative approach to security selection.

Portfolio Management

Team

Jeremiah Charles –

Senior Vice President and Senior Portfolio Manager, First Trust Securitized Products Group

James Snyder – Senior

Vice President and Senior Portfolio Manager, First Trust Securitized Products Group

Commentary

First Trust Mortgage Income

Fund

The Fund’s primary

investment objective is to seek a high level of current income. As a secondary objective, the Fund seeks to preserve capital. The Fund pursues its objectives by investing primarily in mortgage-backed securities

(“MBS”) representing part ownership in a pool of either residential or commercial mortgage loans that, in the opinion of the Fund’s investment advisor, offer an attractive combination of credit

quality, yield and maturity. There can be no assurance the Fund will achieve its investment objectives. The Fund may not be appropriate for all investors.

Market Recap

The 2021 fiscal year

began in earnest as markets reacted to shifting and uncertain results surrounding U.S. elections. Meanwhile, the effects of the coronavirus (“COVID-19”) pandemic continued to ripple through both global and

domestic economies alike. Post-election, on the back of incredibly positive vaccine developments, risk markets staged a very strong and very broad-based rally as market expectations for a faster economic recovery than

earlier anticipated began to be priced into forward data. After another round of Federal stimulus, the calendar year turned over, election results were certified, and immediately the details of yet another round of an

even larger scale stimulus program began to take shape. Market participants took notice, and when considering another massive stimulus bill alongside a blow out in M2 money supply during the pandemic, two factors

weighed heavily on the intermediate and longer dated maturity segment of the U.S. yield curve – inflation and treasury debt issuance. Over the preceding 12 months, treasury issuance had already soared to buoy

government deficit spending. Plans for additional rounds of stimulus only heightened fears of further treasury supply. As a result, the 5-Year Treasury sold off 46 basis points (“bps”), the 10-Year +75 bps

and the 30-year +64 bps, while the 2-Year Treasury, firmly anchored by the Federal Reserve (the “Fed”), was basically unchanged. This drove the yield curve in the 2/10 (the 2-Year and 10-Year Treasury

notes) 75 bps steeper to settle at 146 bps to end the fiscal period. As rates rose, yield hungry investors remained in an aggressive risk-on stance, as economic data showed the recovery was well underway. As such,

Agency MBS spreads tightened dramatically, starting the period at 64 bps Option-Adjusted Spread (“OAS”), and ending the semi-annual period at -12 bps OAS.

Performance Analysis

During the first half of

the 2021 fiscal year, the Fund returned 1.03% on a net asset value (“NAV”) basis, and 4.35% on a market price basis.

During the same period,

the Bloomberg/Barclays US MBS Index (the “Index”) returned -0.27%.

During the same period,

the Fund outperformed the Index by 1.30% net of fees, on a NAV basis and 4.62% on a market price basis. The Fund maintained significant exposures to Non-Agency Residential Mortgage-Backed Securities

(“RMBS”), and Interest Only Agency MBS securities that continued to tighten over the period, which was a strong contributor to the outperformance. Additionally, the Fund maintained a lower, and more stable

overall effective duration than its more negatively convex benchmark, which saw its duration extend as interest rates moved higher. The Fund’s usage of futures positions to help manage interest rate risk and to

structurally position a lower overall effective duration, was mildly beneficial to the Fund’s performance. During the period, the Fund deployed a very minimal amount of leverage for a short period of time, which

very minimally detracted from the Fund’s performance, as interest rates continued their sell off during the first quarter of 2021. The Fund continues to recover from the severe illiquidity that gripped financial

markets in March of 2020. Since the NAV low on March 25, 2020, the Fund has outperformed its Agency MBS benchmark by more than 800 bps.

Fund and Market Outlook

As expected, we saw an

acceleration in overall consumer and economic data to start the fiscal year. We expect strong and robust data over the remainder of the year as well, as the United States continues to fully reopen the economy. With

the massive increase in M2 money supply, and with stimulus dollars in consumers’ hands, we do expect inflationary risks to continue to build. We are ever mindful

Portfolio Commentary (Continued)

First Trust Mortgage

Income Fund (FMY)

Semi-Annual Report

April 30, 2021

(Unaudited)

of the impacts this can

have on term premium pricing along the U.S. yield curve, and believe heightened uncertainty will ultimately drive intermediate to long rates higher, before the Fed will confront how hot it wants the U.S. economy to

run, and what magnitude of ongoing inflation it is comfortable within the economy. At the outset of the pandemic, the Fed deployed emergency rate cuts, large scale quantitative easing and unprecedented lending

programs. Over one year later, it remains highly accommodative. We do anticipate that the Fed will begin to taper its bond purchasing program later this year, and potentially could implement a curve twist type program

with the reinvestment of MBS paydowns back into U.S. treasuries. Overall, we believe that as long as the Fed maintains its view that inflation pressures are ‘transitory’, the front end of the yield curve

will remain fairly anchored in place in the near term, with any rate volatility centralized in the intermediate to longer maturity segments. While we continue to redeploy capital into what we believe are attractively

priced opportunities in the broader securitized mortgage market, we have turned negative on generic Agency MBS spread valuations, the types of securities of which constitute the majority of the Fund’s benchmark,

and believe there is the potential for spread widening.

Given our outlook on the

broader bond markets, we plan to continue to actively manage the Fund versus the Index from a duration standpoint. To the extent the curve sees a large bear steepening, likely due to inflationary pressures, treasury

supply or volatility, we will look to take advantage of higher longer maturity yields and potentially look to increase interest rate hedges on the front end. From an asset allocation perspective, we plan to continue

to reinvest legacy portfolio runoff into both Agency RMBS and Agency Commercial Mortgage-Backed Securities (“CMBS”) interest only securities. The Fund will also look to invest in select opportunities that

the managers find to be attractively priced in Non-Agency CMBS and Non-Agency RMBS, with an emphasis on floating rate instruments. In our view, this approach would provide some yield, income, dividend, and spread

protection for shareholders. As a reminder, as part of the investment team’s Agency MBS strategy, a substantial portion of the agency securities have been, and will continue to be, invested in the interest-only

sectors to increase the income and economic earnings of the portfolio. This strategy can be very effective with proper security selection, particularly when combined with appropriate yield curve management. We plan to

continue to maintain a tradeable portfolio as that is critical to being able to act should opportunities arise.

First Trust Mortgage Income Fund (FMY)

Portfolio of Investments

April 30, 2021

(Unaudited)

Principal

Value

|

| Description

|

| Stated

Coupon

|

| Stated

Maturity

|

| Value

|

| U.S. GOVERNMENT AGENCY MORTGAGE-BACKED SECURITIES – 56.0%

|

|

|

| Collateralized Mortgage Obligations – 33.8%

|

|

|

|

|

|

|

|

|

| Federal Home Loan Mortgage Corp.

|

|

|

|

|

|

|

| $7,373

|

| Series 1394, Class ID, Cost of Funds 11th District of San Fransisco x -4.67 + 44.56%, Capped at 9.57% (a)

|

| 9.57%

|

| 10/15/22

|

| $7,765

|

| 10,386

|

| Series 2303, Class SW, Cost of Funds 11th District of San Fransisco x -15.87 + 121.11%, Capped at 10.00% (a)

|

| 10.00%

|

| 03/01/24

|

| 1,066

|

| 53,708

|

| Series 2334, Class QS, 1 Mo. LIBOR x -3.5 + 28.18% (a)

|

| 27.77%

|

| 07/15/31

|

| 80,295

|

| 203,050

|

| Series 2439, Class XI, IO, if 1 Mo. LIBOR x -1 + 7.74% is less than 7.50%, then 6.50%, otherwise 0.00% (a)

|

| 6.50%

|

| 03/01/32

|

| 34,269

|

| 435,406

|

| Series 2807, Class SB, IO, 1 Mo. LIBOR x -1 + 7.45% (a)

|

| 7.34%

|

| 11/15/33

|

| 78,912

|

| 997,004

|

| Series 2975, Class SJ, IO, 1 Mo. LIBOR x -1 + 6.65% (a)

|

| 6.54%

|

| 05/15/35

|

| 189,957

|

| 234,021

|

| Series 3012, Class GK, 1 Mo. LIBOR x -4.5 + 24.75% (a)

|

| 24.23%

|

| 06/15/35

|

| 406,373

|

| 247,870

|

| Series 3108, Class QZ

|

| 6.00%

|

| 02/01/36

|

| 351,280

|

| 13,874

|

| Series 3195, Class SX, 1 Mo. LIBOR x -6.5 + 46.15% (a)

|

| 45.40%

|

| 07/15/36

|

| 46,902

|

| 110,481

|

| Series 3410, Class HC

|

| 5.50%

|

| 02/01/38

|

| 130,045

|

| 48,293

|

| Series 3451, Class SB, IO, 1 Mo. LIBOR x -1 + 6.03% (a)

|

| 5.92%

|

| 05/15/38

|

| 7,420

|

| 353,986

|

| Series 3471, Class SD, IO, 1 Mo. LIBOR x -1 + 6.08% (a)

|

| 5.97%

|

| 12/15/36

|

| 63,430

|

| 250,000

|

| Series 3797, Class KB

|

| 4.50%

|

| 01/01/41

|

| 296,636

|

| 217,293

|

| Series 3985, Class GI, IO

|

| 3.00%

|

| 10/01/26

|

| 5,107

|

| 30,311

|

| Series 4021, Class IP, IO

|

| 3.00%

|

| 03/01/27

|

| 1,579

|

| 499,490

|

| Series 4057, Class YI, IO

|

| 3.00%

|

| 06/01/27

|

| 29,104

|

| 904,735

|

| Series 4082, Class PI, IO

|

| 3.00%

|

| 06/01/27

|

| 50,927

|

| 4,570,996

|

| Series 4142, Class IO, IO

|

| 3.00%

|

| 12/01/27

|

| 260,677

|

| 537,194

|

| Series 4206, Class IA, IO

|

| 3.00%

|

| 03/01/33

|

| 55,540

|

| 613,822

|

| Series 4258, Class CO

|

| (b)

|

| 06/01/43

|

| 517,103

|

| 3,700,284

|

| Series 4459, Class EI, IO

|

| 6.00%

|

| 06/01/36

|

| 499,422

|

| 368,006

|

| Series 4615, Class GT, 1 Mo. LIBOR x -4 + 16.00%, Capped at 4.00% (a)

|

| 4.00%

|

| 10/15/42

|

| 345,686

|

| 2,696,086

|

| Series 4619, Class IB, IO

|

| 4.00%

|

| 12/01/47

|

| 126,808

|

| 6,455,557

|

| Series 4938, Class IB, IO

|

| 4.00%

|

| 07/01/49

|

| 821,645

|

|

|

| Federal Home Loan Mortgage Corp. Structured Pass-Through

Certificates

|

|

|

|

|

|

|

| 48,509

|

| Series T-56, Class APO

|

| (b)

|

| 05/01/43

|

| 48,180

|

|

|

| Federal Home Loan Mortgage Corp., STRIPS

|

|

|

|

|

|

|

| 54,311

|

| Series 177, IO

|

| 7.00%

|

| 07/01/26

|

| 6,338

|

| 779,718

|

| Series 243, Class 2, IO

|

| 5.00%

|

| 11/01/35

|

| 123,672

|

| 3,179,982

|

| Series 303, Class C17, IO

|

| 3.50%

|

| 01/01/43

|

| 467,547

|

| 1,116,014

|

| Series 324, Class C21, IO

|

| 6.00%

|

| 06/01/39

|

| 268,779

|

|

|

| Federal National Mortgage Association

|

|

|

|

|

|

|

| 51,338

|

| Series 1996-46, Class ZA

|

| 7.50%

|

| 11/01/26

|

| 57,148

|

| 143,760

|

| Series 1997-85, Class M, IO

|

| 6.50%

|

| 12/01/27

|

| 7,916

|

| 34,163

|

| Series 2002-80, Class IO, IO

|

| 6.00%

|

| 09/01/32

|

| 3,286

|

| 71,375

|

| Series 2003-15, Class MS, IO, 1 Mo. LIBOR x -1 + 8.00% (a)

|

| 7.89%

|

| 03/25/33

|

| 14,318

|

| 93,138

|

| Series 2003-44, Class IU, IO

|

| 7.00%

|

| 06/01/33

|

| 18,533

|

| 510,261

|

| Series 2003-62, Class PO

|

| (b)

|

| 07/01/33

|

| 478,490

|

| 420,677

|

| Series 2004-49, Class SN, IO, 1 Mo. LIBOR x -1 + 7.10% (a)

|

| 6.99%

|

| 07/25/34

|

| 72,675

|

| 14,034

|

| Series 2004-74, Class SW, 1 Mo. LIBOR x -2 + 15.50% (a)

|

| 15.27%

|

| 11/25/31

|

| 18,093

|

| 278,388

|

| Series 2004-W10, Class A6

|

| 5.75%

|

| 08/01/34

|

| 305,417

|

| 273,214

|

| Series 2005-122, Class SN, 1 Mo. LIBOR x -4 + 28.60% (a)

|

| 28.18%

|

| 01/25/36

|

| 456,695

|

| 21,639

|

| Series 2005-59 SU, 1 Mo. LIBOR x -5 + 25.50% (a)

|

| 24.97%

|

| 06/25/35

|

| 34,004

|

| 91,583

|

| Series 2005-6, Class SE, IO, 1 Mo. LIBOR x -1 + 6.70% (a)

|

| 6.59%

|

| 02/25/35

|

| 17,125

|

| 446,949

|

| Series 2005-74, Class NZ

|

| 6.00%

|

| 09/01/35

|

| 598,220

|

| 302,481

|

| Series 2006-105, Class ZA

|

| 6.00%

|

| 11/01/36

|

| 402,057

|

| 548,798

|

| Series 2006-5, Class 3A2 (c)

|

| 2.12%

|

| 05/01/35

|

| 562,028

|

| 44,474

|

| Series 2007-100, Class SM, IO, 1 Mo. LIBOR x -1 + 6.45% (a)

|

| 6.34%

|

| 10/25/37

|

| 9,077

|

| 249,003

|

| Series 2007-30, Class ZM

|

| 4.25%

|

| 04/01/37

|

| 289,659

|

See Notes to Financial Statements

Page 5

First Trust Mortgage Income Fund (FMY)

Portfolio of Investments

(Continued)

April 30, 2021

(Unaudited)

Principal

Value

|

| Description

|

| Stated

Coupon

|

| Stated

Maturity

|

| Value

|

| U.S. GOVERNMENT AGENCY MORTGAGE-BACKED SECURITIES (Continued)

|

|

|

| Collateralized Mortgage Obligations (Continued)

|

|

|

|

|

|

|

|

|

| Federal National Mortgage Association (Continued)

|

|

|

|

|

|

|

| $242,000

|

| Series 2007-37, Class SB, IO, 1 Mo. LIBOR x -1 + 6.75% (a)

|

| 6.64%

|

| 05/25/37

|

| $48,407

|

| 294,177

|

| Series 2008-17, Class BE

|

| 5.50%

|

| 10/01/37

|

| 357,949

|

| 682,000

|

| Series 2008-2, Class PH

|

| 5.50%

|

| 02/01/38

|

| 823,967

|

| 494,000

|

| Series 2009-28, Class HX

|

| 5.00%

|

| 05/01/39

|

| 594,609

|

| 199,737

|

| Series 2009-37, Class NZ

|

| 5.71%

|

| 02/01/37

|

| 252,656

|

| 1,056,699

|

| Series 2010-103, Class ID, IO

|

| 5.00%

|

| 09/01/40

|

| 210,656

|

| 527,750

|

| Series 2010-59, Class EI, IO

|

| 6.00%

|

| 06/01/40

|

| 103,013

|

| 64,847

|

| Series 2010-99, Class SG, 1 Mo. LIBOR x -5 + 25.00% (a)

|

| 24.42%

|

| 09/01/40

|

| 106,190

|

| 714,497

|

| Series 2011-52, Class LB

|

| 5.50%

|

| 06/01/41

|

| 824,677

|

| 13,434

|

| Series 2011-66, Class QI, IO

|

| 3.50%

|

| 07/01/21

|

| 1

|

| 1,177,409

|

| Series 2011-81, Class PI, IO

|

| 3.50%

|

| 08/01/26

|

| 63,376

|

| 88,887

|

| Series 2012-111, Class B

|

| 7.00%

|

| 10/01/42

|

| 107,552

|

| 760,846

|

| Series 2012-112, Class BI, IO

|

| 3.00%

|

| 09/01/31

|

| 31,908

|

| 2,244,690

|

| Series 2012-125, Class MI, IO

|

| 3.50%

|

| 11/01/42

|

| 322,337

|

| 16,656

|

| Series 2012-74, Class OA

|

| (b)

|

| 03/01/42

|

| 15,807

|

| 16,656

|

| Series 2012-75, Class AO

|

| (b)

|

| 03/01/42

|

| 15,796

|

| 858,214

|

| Series 2013-130, Class GS, IO, 1 Mo. LIBOR x -1 + 6.25% (a)

|

| 6.14%

|

| 09/25/33

|

| 112,812

|

| 37,857

|

| Series 2013-132, Class SW, 1 Mo. LIBOR x -2.67 + 10.67% (a)

|

| 10.36%

|

| 01/01/44

|

| 45,260

|

| 1,118,194

|

| Series 2013-32, Class IG, IO

|

| 3.50%

|

| 04/01/33

|

| 125,082

|

| 321,462

|

| Series 2013-51, Class PI, IO

|

| 3.00%

|

| 11/01/32

|

| 30,348

|

| 2,464,986

|

| Series 2015-20, Class ES, IO, 1 Mo. LIBOR x -1 + 6.15% (a)

|

| 6.04%

|

| 04/25/45

|

| 445,362

|

| 488,135

|

| Series 2015-76, Class BI, IO

|

| 4.00%

|

| 10/01/39

|

| 31,175

|

| 1,708,328

|

| Series 2015-97, Class AI, IO

|

| 4.00%

|

| 09/01/41

|

| 80,870

|

| 168,142

|

| Series 2016-74, Class LI, IO

|

| 3.50%

|

| 09/01/46

|

| 52,430

|

| 4,805,047

|

| Series 2017-109, Class SJ, IO, 1 Mo. LIBOR x -1+ 6.20% (a)

|

| 6.09%

|

| 01/25/48

|

| 871,092

|

|

|

| Federal National Mortgage Association, STRIPS

|

|

|

|

|

|

|

| 36,513

|

| Series 305, Class 12, IO (d)

|

| 6.50%

|

| 12/01/29

|

| 4,775

|

| 49,602

|

| Series 355, Class 18, IO

|

| 7.50%

|

| 11/01/33

|

| 9,807

|

| 1,676,650

|

| Series 387, Class 10, IO

|

| 6.00%

|

| 04/01/38

|

| 338,482

|

| 774,801

|

| Series 406, Class 6, IO (d)

|

| 4.00%

|

| 01/01/41

|

| 106,263

|

| 659,603

|

| Series 413, Class 173, IO (d)

|

| 4.50%

|

| 07/01/42

|

| 108,980

|

|

|

| Government National Mortgage Association

|

|

|

|

|

|

|

| 330,758

|

| Series 2004-95, Class QZ

|

| 4.50%

|

| 11/01/34

|

| 362,350

|

| 189,656

|

| Series 2005-33, Class AY

|

| 5.50%

|

| 04/01/35

|

| 212,402

|

| 68,642

|

| Series 2005-68, Class DP, 1 Mo. LIBOR x -2.41 + 16.43% (a)

|

| 16.16%

|

| 06/17/35

|

| 86,058

|

| 251,564

|

| Series 2005-68, Class KI, IO, 1 Mo. LIBOR x -1 + 6.30% (a)

|

| 6.18%

|

| 09/20/35

|

| 52,103

|

| 37,303

|

| Series 2006-28, Class VS, 1 Mo. LIBOR x -13 + 87.10% (a)

|

| 85.59%

|

| 06/20/36

|

| 114,603

|

| 396,523

|

| Series 2007-14, Class PB

|

| 5.40%

|

| 03/01/37

|

| 443,330

|

| 62,088

|

| Series 2007-50, Class AI, IO, 1 Mo. LIBOR x -1 + 6.78% (a)

|

| 6.66%

|

| 08/20/37

|

| 2,693

|

| 206,444

|

| Series 2007-68, Class PI, IO, 1 Mo. LIBOR x -1 + 6.65% (a)

|

| 6.53%

|

| 11/20/37

|

| 29,788

|

| 100,000

|

| Series 2008-2, Class HB

|

| 5.50%

|

| 01/01/38

|

| 115,704

|

| 304,000

|

| Series 2008-32, Class JD

|

| 5.50%

|

| 04/01/38

|

| 354,800

|

| 181,586

|

| Series 2008-73, Class SK, IO, 1 Mo. LIBOR x -1 + 6.74% (a)

|

| 6.62%

|

| 08/20/38

|

| 30,977

|

| 113,825

|

| Series 2009-100, Class SL, IO, 1 Mo. LIBOR x -1 + 6.50% (a)

|

| 6.38%

|

| 05/16/39

|

| 1,801

|

| 143,470

|

| Series 2009-12, Class IE, IO

|

| 5.50%

|

| 03/01/39

|

| 20,959

|

| 141,815

|

| Series 2009-79, Class PZ

|

| 6.00%

|

| 09/01/39

|

| 176,557

|

| 341,241

|

| Series 2013-104, Class YS, IO, 1 Mo. LIBOR x -1 + 6.15% (a)

|

| 6.03%

|

| 07/16/43

|

| 59,686

|

| 158,047

|

| Series 2014-41, Class St, 1 Mo. LIBOR x -2.67 + 11.47% (a)

|

| 11.16%

|

| 11/20/42

|

| 163,956

|

| 5,621,251

|

| Series 2015-158, Class KS, IO, 1 Mo. LIBOR x -1 + 6.25% (a)

|

| 6.13%

|

| 11/20/45

|

| 1,068,054

|

| 73,478

|

| Series 2016-139, Class MZ

|

| 1.50%

|

| 07/01/45

|

| 62,589

|

| 149,926

|

| Series 2017-4, Class CZ

|

| 3.00%

|

| 01/01/47

|

| 155,846

|

| 117,854

|

| Series 2017-H18, Class DZ (d)

|

| 4.61%

|

| 09/01/67

|

| 141,028

|

| 17,290,147

|

| Series 2020-13, Class BT, IO, 1 Mo. LIBOR x -1 + 6.20%, Capped at 0.50% (a)

|

| 0.50%

|

| 11/20/45

|

| 363,809

|

Page 6

See Notes to Financial Statements

First Trust Mortgage Income Fund (FMY)

Portfolio of Investments

(Continued)

April 30, 2021

(Unaudited)

Principal

Value

|

| Description

|

| Stated

Coupon

|

| Stated

Maturity

|

| Value

|

| U.S. GOVERNMENT AGENCY MORTGAGE-BACKED SECURITIES (Continued)

|

|

|

| Collateralized Mortgage Obligations (Continued)

|

|

|

|

|

|

|

|

|

| Government National Mortgage Association (Continued)

|

|

|

|

|

|

|

| $4,901,097

|

| Series 2020-146, Class CI, IO

|

| 2.50%

|

| 10/01/50

|

| $591,425

|

| 6,206,821

|

| Series 2021-23, Class BI, IO

|

| 2.00%

|

| 02/01/51

|

| 748,781

|

|

|

|

|

| 20,268,143

|

|

|

| Commercial Mortgage-Backed Securities – 16.7%

|

|

|

|

|

|

|

|

|

| Federal Home Loan Mortgage Corp. Multifamily Structured

Pass-Through Certificates

|

|

|

|

|

|

|

| 4,000,000

|

| Series K110, Class X3, IO (c)

|

| 3.52%

|

| 06/01/48

|

| 1,022,670

|

| 3,330,000

|

| Series K112, Class X3, IO (c)

|

| 3.10%

|

| 07/01/48

|

| 759,496

|

| 4,605,411

|

| Series K115, Class X3, IO (c)

|

| 3.06%

|

| 09/01/48

|

| 1,038,699

|

| 4,326,216

|

| Series K118, Class X3, IO (c)

|

| 2.79%

|

| 10/25/53

|

| 906,930

|

| 1,900,000

|

| Series K122, Class X3, IO (c)

|

| 2.72%

|

| 01/01/49

|

| 394,058

|

| 3,343,856

|

| Series K128, Class X3, IO (c)

|

| 2.79%

|

| 04/01/31

|

| 751,072

|

| 3,250,000

|

| Series K-1517, Class X3, IO (c)

|

| 3.40%

|

| 08/01/38

|

| 1,108,174

|

| 3,000,000

|

| Series K-1520, Class X3, IO (c)

|

| 3.09%

|

| 04/01/39

|

| 999,253

|

| 1,831,144

|

| Series K739, Class X3, IO (c)

|

| 2.95%

|

| 09/25/27

|

| 287,219

|

|

|

| Federal National Mortgage Association, ACES

|

|

|

|

|

|

|

| 13,100,000

|

| Series 2019-M9, Class X4, IO

|

| 0.70%

|

| 03/01/29

|

| 549,724

|

|

|

| Government National Mortgage Association

|

|

|

|

|

|

|

| 218,000

|

| Series 2013-57, Class D (d)

|

| 2.35%

|

| 06/01/46

|

| 220,039

|

| 2,953,380

|

| Series 2016-11, Class IO (d)

|

| 0.86%

|

| 01/01/56

|

| 147,048

|

| 4,661,611

|

| Series 2016-143, Class IO

|

| 0.88%

|

| 10/01/56

|

| 262,658

|

| 7,431,814

|

| Series 2016-166, Class IO (d)

|

| 1.02%

|

| 04/01/58

|

| 447,229

|

| 10,345,022

|

| Series 2017-126, Class IO (c)

|

| 0.77%

|

| 08/01/59

|

| 612,510

|

| 9,742,166

|

| Series 2017-7, Class IO (d)

|

| 0.76%

|

| 12/01/58

|

| 506,324

|

|

|

|

|

| 10,013,103

|

|

|

| Pass-through Security – 5.5%

|

|

|

|

|

|

|

|

|

| Federal Home Loan Mortgage Corp.

|

|

|

|

|

|

|

| 382,497

|

| Pool K36017

|

| 5.00%

|

| 09/01/47

|

| 417,847

|

| 766,944

|

| Pool U99176

|

| 4.00%

|

| 12/01/47

|

| 852,798

|

|

|

| Federal National Mortgage Association

|

|

|

|

|

|

|

| 508,004

|

| Pool 831145

|

| 6.00%

|

| 12/01/35

|

| 604,501

|

| 557,530

|

| Pool 843971

|

| 6.00%

|

| 11/01/35

|

| 652,762

|

| 690,214

|

| Pool AB5688

|

| 3.50%

|

| 07/01/37

|

| 752,216

|

|

|

|

|

| 3,280,124

|

|

|

| Total U.S. Government Agency Mortgage-Backed Securities

|

| 33,561,370

|

|

|

| (Cost $34,215,478)

|

|

|

|

|

|

|

| MORTGAGE-BACKED SECURITIES – 34.9%

|

|

|

| Collateralized Mortgage Obligations – 29.0%

|

|

|

|

|

|

|

|

|

| Accredited Mortgage Loan Trust

|

|

|

|

|

|

|

| 226,046

|

| Series 2003-2, Class A1

|

| 4.98%

|

| 10/01/33

|

| 237,225

|

|

|

| ACE Securities Corp. Home Equity Loan Trust

|

|

|

|

|

|

|

| 762,997

|

| Series 2006-ASAP6, Class A2D, 1 Mo. LIBOR + 0.22% (e)

|

| 0.33%

|

| 12/25/36

|

| 376,354

|

|

|

| Banc of America Mortgage Trust

|

|

|

|

|

|

|

| 47,056

|

| Series 2002-L, Class 1A1 (c)

|

| 3.07%

|

| 12/01/32

|

| 41,218

|

| 104,945

|

| Series 2005-A, Class 2A1 (c)

|

| 2.58%

|

| 02/01/35

|

| 108,821

|

|

|

| Chase Mortgage Finance Trust

|

|

|

|

|

|

|

| 62,273

|

| Series 2007-A1, Class 1A3 (c)

|

| 2.65%

|

| 02/01/37

|

| 63,241

|

|

|

| Citigroup Mortgage Loan Trust

|

|

|

|

|

|

|

| 131,892

|

| Series 2005-6, Class A1, US Treasury Yield Curve Rate T Note Constant Maturity 1 Year + 2.10% (e)

|

| 2.22%

|

| 09/01/35

|

| 137,936

|

See Notes to Financial Statements

Page 7

First Trust Mortgage Income Fund (FMY)

Portfolio of Investments

(Continued)

April 30, 2021

(Unaudited)

Principal

Value

|

| Description

|

| Stated

Coupon

|

| Stated

Maturity

|

| Value

|

| MORTGAGE-BACKED SECURITIES (Continued)

|

|

|

| Collateralized Mortgage Obligations (Continued)

|

|

|

|

|

|

|

|

|

| Citigroup Mortgage Loan Trust (Continued)

|

|

|

|

|

|

|

| $25,001

|

| Series 2009-10, Class 1A1 (c) (f)

|

| 2.76%

|

| 09/01/33

|

| $25,283

|

| 308,284

|

| Series 2012-7, Class 10A2 (c) (f)

|

| 2.91%

|

| 09/01/36

|

| 283,253

|

|

|

| Connecticut Avenue Securities Trust

|

|

|

|

|

|

|

| 1,000,000

|

| Series 2019-RO2, Class 1B1, 1 Mo. LIBOR + 4.15% (e) (f)

|

| 4.26%

|

| 08/25/31

|

| 1,034,290

|

|

|

| Countrywide Home Loan Mortgage Pass-Through Trust

|

|

|

|

|

|

|

| 172,413

|

| Series 2003-46, Class 2A1 (c)

|

| 2.81%

|

| 01/01/34

|

| 175,191

|

| 54,015

|

| Series 2005-HYB3, Class 2A6B (c)

|

| 3.14%

|

| 06/01/35

|

| 56,276

|

| 183,509

|

| Series 2006-21, Class A8

|

| 5.75%

|

| 02/01/37

|

| 133,544

|

| 327,865

|

| Series 2006-HYB5, Class 3A1A (c)

|

| 2.92%

|

| 09/01/36

|

| 312,821

|

|

|

| Credit Suisse Commercial Mortgage Securities Corp. Pass-Through

Certificates

|

|

|

|

|

|

|

| 1,000,000

|

| Series 2020-UNFI, Class A, 1 Mo. LIBOR + 0.50%, 4.25% minimum (e) (f)

|

| 4.25%

|

| 12/06/22

|

| 1,004,993

|

|

|

| Credit Suisse First Boston Mortgage Securities Corp.

|

|

|

|

|

|

|

| 326,263

|

| Series 2004-AR2, Class 1A1 (c)

|

| 2.93%

|

| 03/01/34

|

| 340,054

|

| 188,413

|

| Series 2005-5, Class 3A2, 1 Mo. LIBOR + 0.30% (e)

|

| 0.41%

|

| 07/25/35

|

| 185,057

|

|

|

| Credit Suisse Mortgage Trust

|

|

|

|

|

|

|

| 364,261

|

| Series 2017-FHA1, Class A1 (f)

|

| 3.25%

|

| 04/01/47

|

| 373,421

|

|

|

| Deutsche ALT-A Securities, Inc., Mortgage Loan Trust

|

|

|

|

|

|

|

| 2,734

|

| Series 2003-3, Class 3A1

|

| 5.00%

|

| 10/25/33

|

| 2,731

|

|

|

| DSLA Mortgage Loan Trust

|

|

|

|

|

|

|

| 388,370

|

| Series 2004-AR3, Class 2A2A, 1 Mo. LIBOR + 0.74% (e)

|

| 0.86%

|

| 07/19/44

|

| 375,666

|

| 479,706

|

| Series 2007-AR1, Class 2A1A, 1 Mo. LIBOR + 0.14% (e)

|

| 0.26%

|

| 03/01/37

|

| 457,428

|

|

|

| Federal National Mortgage Association Connecticut Avenue

Securities

|

|

|

|

|

|

|

| 913,843

|

| Series 2018-CO3, Class 1M2, 1 Mo. LIBOR + 2.15% (e)

|

| 2.26%

|

| 10/25/30

|

| 925,092

|

|

|

| Galton Funding Mortgage Trust

|

|

|

|

|

|

|

| 55,677

|

| Series 2018-2, Class A41 (f)

|

| 4.50%

|

| 10/01/58

|

| 56,220

|

|

|

| GSR Mortgage Loan Trust

|

|

|

|

|

|

|

| 5,271

|

| Series 2003-10, Class 1A12 (c)

|

| 2.84%

|

| 10/01/33

|

| 5,276

|

| 150,111

|

| Series 2005-AR1, Class 4A1 (c)

|

| 2.80%

|

| 01/01/35

|

| 148,459

|

|

|

| Harborview Mortgage Loan Trust

|

|

|

|

|

|

|

| 245,751

|

| Series 2004-6, Class 3A1 (c)

|

| 3.24%

|

| 08/01/34

|

| 246,418

|

|

|

| Home Equity Asset Trust

|

|

|

|

|

|

|

| 15,024

|

| Series 2005-3, Class M4, 1 Mo. LIBOR + 0.96% (e)

|

| 1.07%

|

| 08/25/35

|

| 15,049

|

| 329,763

|

| Series 2005-9, Class M1, 1 Mo. LIBOR + 0.62% (e)

|

| 0.72%

|

| 04/25/36

|

| 328,078

|

|

|

| Impac CMB Trust

|

|

|

|

|

|

|

| 102,739

|

| Series 2004-6, Class 1A2, 1 Mo. LIBOR + 0.78% (e)

|

| 0.89%

|

| 10/25/34

|

| 104,336

|

|

|

| IXIS Real Estate Capital Trust

|

|

|

|

|

|

|

| 1,044,554

|

| Series 2007-HE1, Class A3, 1 Mo. LIBOR + 0.16% (e)

|

| 0.27%

|

| 05/25/37

|

| 367,381

|

|

|

| JP Morgan Mortgage Trust

|

|

|

|

|

|

|

| 594,977

|

| Series 2005-ALT1, Class 4A1 (c)

|

| 2.97%

|

| 10/01/35

|

| 538,295

|

| 346,821

|

| Series 2006-A2, Class 4A1 (c)

|

| 3.05%

|

| 08/01/34

|

| 364,709

|

| 85,555

|

| Series 2006-A2, Class 5A3 (c)

|

| 2.54%

|

| 11/01/33

|

| 89,548

|

| 58,033

|

| Series 2014-2, Class 1A1 (f)

|

| 3.00%

|

| 06/01/29

|

| 59,513

|

|

|

| MASTR Adjustable Rate Mortgages Trust

|

|

|

|

|

|

|

| 24,783

|

| Series 2004-13, Class 3A7B, US Treasury Yield Curve Rate T Note Constant Maturity 1 Year + 2.00% (e)

|

| 2.06%

|

| 11/01/34

|

| 25,300

|

|

|

| MASTR Alternative Loan Trust

|

|

|

|

|

|

|

| 3,572,419

|

| Series 2006-2, Class 2A3, 1 Mo. LIBOR + 0.35% (e)

|

| 0.46%

|

| 03/25/36

|

| 206,553

|

|

|

| MASTR Asset Backed Securities Trust

|

|

|

|

|

|

|

| 691,911

|

| Series 2006-HE5, Class A3, 1 Mo. LIBOR + 0.16% (e)

|

| 0.27%

|

| 11/25/36

|

| 513,618

|

| 1,154,102

|

| Series 2006-NC2, Class A3, 1 Mo. LIBOR + 0.22% (e)

|

| 0.33%

|

| 08/25/36

|

| 611,761

|

| 526,792

|

| Series 2006-NC2, Class A5, 1 Mo. LIBOR + 0.48% (e)

|

| 0.59%

|

| 08/25/36

|

| 286,483

|

Page 8

See Notes to Financial Statements

First Trust Mortgage Income Fund (FMY)

Portfolio of Investments

(Continued)

April 30, 2021

(Unaudited)

Principal

Value

|

| Description

|

| Stated

Coupon

|

| Stated

Maturity

|

| Value

|

| MORTGAGE-BACKED SECURITIES (Continued)

|

|

|

| Collateralized Mortgage Obligations (Continued)

|

|

|

|

|

|

|

|

|

| MASTR Asset Securitization Trust

|

|

|

|

|

|

|

| $12,034

|

| Series 2003-11, Class 5A2

|

| 5.25%

|

| 12/01/23

|

| $12,248

|

| 39,860

|

| Series 2003-11, Class 6A16

|

| 5.25%

|

| 12/01/33

|

| 40,717

|

|

|

| Mellon Residential Funding Corp. Mortgage Pass-Through Trust

|

|

|

|

|

|

|

| 164,602

|

| Series 2001-TBC1, Class A1, 1 Mo. LIBOR + 0.70% (e)

|

| 0.81%

|

| 11/15/31

|

| 167,653

|

| 175,619

|

| Series 2002-TBC2, Class A, 1 Mo. LIBOR + 0.86% (e)

|

| 0.97%

|

| 08/15/32

|

| 167,857

|

|

|

| Meritage Mortgage Loan Trust

|

|

|

|

|

|

|

| 2,469

|

| Series 2004-2, Class M3, 1 Mo. LIBOR + 0.98% (e)

|

| 1.08%

|

| 01/25/35

|

| 2,667

|

|

|

| Morgan Stanley Mortgage Loan Trust

|

|

|

|

|

|

|

| 268,379

|

| Series 2004-7AR, Class 2A6 (c)

|

| 2.57%

|

| 09/01/34

|

| 274,183

|

|

|

| MortgageIT Trust

|

|

|

|

|

|

|

| 113,560

|

| Series 2005-2, Class 2A, 1 Mo. LIBOR + 1.65% (e)

|

| 1.77%

|

| 05/01/35

|

| 113,847

|

|

|

| New Residential Mortgage Loan Trust

|

|

|

|

|

|

|

| 316,645

|

| Series 2014-2A, Class A2 (f)

|

| 3.75%

|

| 05/01/54

|

| 337,557

|

| 388,048

|

| Series 2016-1A, Class A1 (f)

|

| 3.75%

|

| 03/01/56

|

| 411,984

|

| 313,242

|

| Series 2016-3A, Class A1 (f)

|

| 3.75%

|

| 09/01/56

|

| 335,847

|

|

|

| Nomura Asset Acceptance Corporation Alternative Loan Trust

|

|

|

|

|

|

|

| 630,973

|

| Series 2004-AR4, Class M1, 1 Mo. LIBOR + 1.10% (e)

|

| 1.21%

|

| 12/25/34

|

| 630,330

|

|

|

| Residential Accredit Loans, Inc.

|

|

|

|

|

|

|

| 102,378

|

| Series 2006-QO1, Class 2A1, 1 Mo. LIBOR + 0.54% (e)

|

| 0.65%

|

| 02/25/46

|

| 74,102

|

| 1,023,327

|

| Series 2006-QS6, Class 1AV, IO (c)

|

| 0.76%

|

| 06/01/36

|

| 23,362

|

|

|

| Residential Asset Securitization Trust

|

|

|

|

|

|

|

| 24,332

|

| Series 2004-A3, Class A7

|

| 5.25%

|

| 06/01/34

|

| 25,181

|

|

|

| Saxon Asset Securities Trust

|

|

|

|

|

|

|

| 721,066

|

| Series 2007-2, Class A2D, 1 Mo. LIBOR + 0.30% (e)

|

| 0.41%

|

| 05/25/47

|

| 623,756

|

|

|

| Sequoia Mortgage Trust

|

|

|

|

|

|

|

| 37,346

|

| Series 2017-CH2, Class A10 (f)

|

| 4.00%

|

| 12/01/47

|

| 37,399

|

| 13,809

|

| Series 2018-CH2, Class A12 (f)

|

| 4.00%

|

| 06/01/48

|

| 13,829

|

|

|

| Structured Adjustable Rate Mortgage Loan Trust

|

|

|

|

|

|

|

| 178,621

|

| Series 2004-2, Class 4A2 (c)

|

| 2.52%

|

| 03/01/34

|

| 176,976

|

|

|

| Structured Asset Securities Corp. Mortgage Pass-Through

Certificates

|

|

|

|

|

|

|

| 25,449

|

| Series 2001-SB1, Class A2

|

| 3.38%

|

| 08/01/31

|

| 24,857

|

|

|

| Thornburg Mortgage Securities Trust

|

|

|

|

|

|

|

| 161,844

|

| Series 2003-4, Class A1, 1 Mo. LIBOR + 0.64% (e)

|

| 0.75%

|

| 09/25/43

|

| 165,039

|

|

|

| Vendee Mortgage Trust

|

|

|

|

|

|

|

| 55,022,733

|

| Series 2010-1, Class DI, IO (c)

|

| 0.29%

|

| 04/01/40

|

| 530,920

|

|

|

| Wachovia Mortgage Loan Trust, LLC

|

|

|

|

|

|

|

| 88,333

|

| Series 2006-A, Class 3A1 (c)

|

| 3.12%

|

| 05/01/36

|

| 85,388

|

|

|

| WaMu Mortgage Pass-Through Certificates

|

|

|

|

|

|

|

| 121,943

|

| Series 2003-AR5, Class A7 (c)

|

| 3.49%

|

| 06/01/33

|

| 124,292

|

| 210,621

|

| Series 2004-AR1, Class A (c)

|

| 2.41%

|

| 03/01/34

|

| 217,269

|

| 239,072

|

| Series 2004-AR10, Class A1B, 1 Mo. LIBOR + 0.84% (e)

|

| 0.95%

|

| 07/25/44

|

| 242,574

|

| 220,439

|

| Series 2004-AR13, Class A1A, 1 Mo. LIBOR + 0.72% (e)

|

| 0.83%

|

| 11/25/34

|

| 216,479

|

| 30,122

|

| Series 2004-AR3, Class A2 (c)

|

| 3.17%

|

| 06/01/34

|

| 31,021

|

| 270,811

|

| Series 2005-AR1, Class A1A, 1 Mo. LIBOR + 0.64% (e)

|

| 0.75%

|

| 01/25/45

|

| 269,427

|

| 389,474

|

| Series 2005-AR6, Class 2A1A, 1 Mo. LIBOR + 0.46% (e)

|

| 0.57%

|

| 04/25/45

|

| 384,464

|

| 135,659

|

| Series 2005-AR9, Class A1A, 1 Mo. LIBOR + 0.64% (e)

|

| 0.75%

|

| 07/25/45

|

| 136,022

|

| 250,320

|

| Series 2006-AR2, Class 1A1 (c)

|

| 2.93%

|

| 03/01/36

|

| 250,475

|

|

|

| Washington Mutual Alternative Mortgage Pass-Through Certificates

|

|

|

|

|

|

|

| 15,301

|

| Series 2007-5, Class A11, 1 Mo. LIBOR x -6 + 39.48% (a)

|

| 38.84%

|

| 06/25/37

|

| 29,651

|

|

|

| Washington Mutual MSC Mortgage Pass-Through Certificates

|

|

|

|

|

|

|

| 221,613

|

| Series 2004-RA1, Class 2A

|

| 7.00%

|

| 03/01/34

|

| 236,299

|

See Notes to Financial Statements

Page 9

First Trust Mortgage Income Fund (FMY)

Portfolio of Investments

(Continued)

April 30, 2021

(Unaudited)

Principal

Value

|

| Description

|

| Stated

Coupon

|

| Stated

Maturity

|

| Value

|

| MORTGAGE-BACKED SECURITIES (Continued)

|

|

|

| Collateralized Mortgage Obligations (Continued)

|

|

|

|

|

|

|

|

|

| WinWater Mortgage Loan Trust

|

|

|

|

|

|

|

| $319,411

|

| Series 2015-3, Class B1 (c) (f)

|

| 3.88%

|

| 03/01/45

|

| $339,389

|

|

|

|

|

| 17,369,953

|

|

|

| Commercial Mortgage-Backed Securities – 5.9%

|

|

|

|

|

|

|

|

|

| BBCMS Trust

|

|

|

|

|

|

|

| 607,936

|

| Series 2013-TYSN, Class A2 (f)

|

| 3.76%

|

| 09/01/32

|

| 608,983

|

|

|

| Citigroup Commercial Mortgage Trust

|

|

|

|

|

|

|

| 4,474,642

|

| Series 2015-GC29, Class XA (c)

|

| 1.17%

|

| 04/01/48

|

| 158,043

|

| 9,890,769

|

| Series 2016-GC37, Class XA (c)

|

| 1.85%

|

| 04/01/49

|

| 675,341

|

| 1,451,843

|

| Series 2016-P4, Class XA (c)

|

| 2.11%

|

| 07/01/49

|

| 104,365

|

|

|

| COMM Mortgage Trust

|

|

|

|

|

|

|

| 537,652

|

| Series 2013-LC13, Class XA (c)

|

| 1.29%

|

| 08/01/46

|

| 10,692

|

| 25,178,907

|

| Series 2013-LC6, Class XA (c)

|

| 1.46%

|

| 01/01/46

|

| 404,071

|

| 122,774,000

|

| Series 2014-UBS6, Class XB (c) (f)

|

| 0.11%

|

| 12/01/47

|

| 277,064

|

| 1,123,000

|

| Series 2015-CCRE26, Class XD (c) (f)

|

| 1.38%

|

| 10/01/48

|

| 54,897

|

|

|

| Hudsons Bay Simon JV Trust

|

|

|

|

|

|

|

| 510,000

|

| Series 2015-HBFL, Class DFL, 1 Mo. LIBOR + 3.90% (e) (f)

|

| 4.01%

|

| 08/05/34

|

| 371,605

|

|

|

| JP Morgan Chase Commercial Mortgage Securities Trust

|

|

|

|

|

|

|

| 3,555,947

|

| Series 2016-JP4, Class XA (c)

|

| 0.81%

|

| 12/01/49

|

| 86,430

|

|

|

| Morgan Stanley Bank of America Merrill Lynch Trust

|

|

|

|

|

|

|

| 2,121,776

|

| Series 2014-C19, Class XA (c)

|

| 1.15%

|

| 12/01/47

|

| 61,155

|

| 5,632,500

|

| Series 2014-C19, Class XE (c) (f)

|

| 1.36%

|

| 12/01/47

|

| 244,020

|

| 506,349

|

| Series 2016-C31, Class XA (c)

|

| 1.48%

|

| 11/01/49

|

| 27,106

|

|

|

| Wells Fargo Commercial Mortgage Trust

|

|

|

|

|

|

|

| 1,431,806

|

| Series 2015-C26, Class XA (c)

|

| 1.35%

|

| 02/01/48

|

| 54,908

|

|

|

| WFRBS Commercial Mortgage Trust

|

|

|

|

|

|

|

| 400,000

|

| Series 2011-C5, Class C (c) (f)

|

| 5.85%

|

| 11/01/44

|

| 403,910

|

|

|

|

|

| 3,542,590

|

|

|

| Total Mortgage-Backed Securities

|

| 20,912,543

|

|

|

| (Cost $22,189,464)

|

|

|

|

|

|

|

| ASSET-BACKED SECURITIES – 3.4%

|

|

|

| Affirm Asset Securitization Trust

|

|

|

|

|

|

|

| 750,000

|

| Series 2021-A, Class C (f)

|

| 1.66%

|

| 08/15/25

|

| 753,975

|

| 750,000

|

| Series 2021-A, Class D (f)

|

| 3.49%

|

| 08/15/25

|

| 755,722

|

|

|

| Green Tree Financial Corp.

|

|

|

|

|

|

|

| 16,353

|

| Series 1998-4, Class A7

|

| 6.87%

|

| 04/01/30

|

| 16,613

|

|

|

| Mid-State Capital Corp. Trust

|

|

|

|

|

|

|

| 205,451

|

| Series 2004-1, Class M1

|

| 6.50%

|

| 08/01/37

|

| 219,014

|

| 258,067

|

| Series 2005-1, Class A

|

| 5.75%

|

| 01/01/40

|

| 277,669

|

|

|

| Total Asset-Backed Securities

|

| 2,022,993

|

|

|

| (Cost $1,981,496)

|

|

|

|

|

|

|

|

| Total Investments – 94.3%

|

| 56,496,906

|

|

| (Cost $58,386,438) (g)

|

|

|

|

| Net Other Assets and Liabilities – 5.7%

|

| 3,400,114

|

|

| Net Assets – 100.0%

|

| $59,897,020

|

Page 10

See Notes to Financial Statements

First Trust Mortgage Income Fund (FMY)

Portfolio of Investments

(Continued)

April 30, 2021

(Unaudited)

Futures Contracts (See Note 2D - Futures Contracts in the Notes to Financial Statements):

| Futures Contracts

|

| Position

|

| Number of

Contracts

|

| Expiration

Date

|

| Notional

Value

|

| Unrealized

Appreciation

(Depreciation)/

Value

|

| U.S. Treasury Long Bond Futures

|

| Long

|

| 1

|

| Jun 2021

|

| $ 157,250

|

| $(687)

|

| Ultra 10-Year U.S. Treasury Note Futures

|

| Long

|

| 10

|

| Jun 2021

|

| 1,455,469

|

| (4,047)

|

| Total Futures Contracts

|

|

|

|

|

|

|

| $1,612,719

|

| $(4,734)

|

|

| (a)

| Inverse floating rate security.

|

| (b)

| Zero coupon security.

|

| (c)

| Collateral Strip Rate security. Coupon is based on the weighted net interest rate of the investment’s underlying collateral. The interest rate resets periodically.

|

| (d)

| Weighted Average Coupon security. Coupon is based on the blended interest rate of the underlying holdings, which may have different coupons. The coupon may change in any period.

|

| (e)

| Floating or variable rate security.

|

| (f)

| This security, sold within the terms of a private placement memorandum, is exempt from registration upon resale under Rule 144A under the Securities Act of 1933, as amended (the

“1933 Act”), and may be resold in transactions exempt from registration, normally to qualified institutional buyers. Pursuant to procedures adopted by the Fund’s Board of Trustees, this security has

been determined to be liquid by First Trust Advisors L.P. (the “Advisor”). Although market instability can result in periods of increased overall market illiquidity, liquidity for each security is

determined based on security specific factors and assumptions, which require subjective judgment. At April 30, 2021, securities noted as such amounted to $7,783,154 or 13.0% of net assets.

|

| (g)

| Aggregate cost for financial reporting purposes approximates the aggregate cost for federal income tax purposes. As of April 30, 2021, the aggregate gross

unrealized appreciation for all investments in which there was an excess of value over tax cost was $2,361,306 and the aggregate gross unrealized depreciation for all investments in which there was an excess of tax

cost over value was $4,255,572. The net unrealized depreciation was $1,894,266. The unrealized amounts presented are inclusive of derivative contracts.

|

| ACES

| Alternative Credit Enhancement Securities

|

| IO

| Interest-Only Security - Principal amount shown represents par value on which interest payments are based.

|

| LIBOR

| London Interbank Offered Rate

|

| STRIPS

| Separate Trading of Registered Interest and Principal of Securities

|

Valuation Inputs

A summary of the inputs

used to value the Fund’s investments as of April 30, 2021 is as follows (see Note 2A - Portfolio Valuation in the Notes to Financial Statements):

| ASSETS TABLE

|

|

| Total

Value at

4/30/2021

| Level 1

Quoted

Prices

| Level 2

Significant

Observable

Inputs

| Level 3

Significant

Unobservable

Inputs

|

U.S. Government Agency Mortgage-Backed Securities

| $ 33,561,370

| $ —

| $ 33,561,370

| $ —

|

Mortgage-Backed Securities

| 20,912,543

| —

| 20,912,543

| —

|

Asset-Backed Securities

| 2,022,993

| —

| 2,022,993

| —

|

Total Investments

| $ 56,496,906

| $—

| $ 56,496,906

| $—

|

LIABILITIES TABLE |

|

| Total

Value at

4/30/2021

| Level 1

Quoted

Prices

| Level 2

Significant

Observable

Inputs

| Level 3

Significant

Unobservable

Inputs

|

Futures Contracts

| $ (4,734)

| $ (4,734)

| $ —

| $ —

|

See Notes to Financial Statements

Page 11

First Trust Mortgage Income Fund (FMY)

Statement of Assets and

Liabilities

April 30, 2021

(Unaudited)

| ASSETS:

|

|

Investments, at value

(Cost $58,386,438)

| $ 56,496,906

|

Cash

| 2,179,881

|

Restricted Cash

| 38,214

|

| Receivables:

|

|

Investment securities sold

| 2,863,036

|

Interest

| 465,000

|

Prepaid expenses

| 19,952

|

Total Assets

| 62,062,989

|

| LIABILITIES:

|

|

| Payables:

|

|

Investment securities purchased

| 2,025,735

|

Audit and tax fees

| 53,297

|

Investment advisory fees

| 41,773

|

Administrative fees

| 13,254

|

Shareholder reporting fees

| 10,114

|

Custodian fees

| 9,307

|

Variation margin

| 4,734

|

Legal fees

| 2,841

|

Transfer agent fees

| 2,680

|

Trustees’ fees and expenses

| 1,400

|

Financial reporting fees

| 771

|

Other liabilities

| 63

|

Total Liabilities

| 2,165,969

|

NET ASSETS

| $59,897,020

|

| NET ASSETS consist of:

|

|

Paid-in capital

| $ 66,237,538

|

Par value

| 42,131

|

Accumulated distributable earnings (loss)

| (6,382,649)

|

NET ASSETS

| $59,897,020

|

NET ASSET VALUE, per Common Share (par value $0.01 per Common Share)

| $14.22

|

Number of Common Shares outstanding (unlimited number of Common Shares has been authorized)

| 4,213,115

|

Page 12

See Notes to Financial Statements

First Trust Mortgage Income Fund (FMY)

Statement of Operations

For the Six Months Ended

April 30, 2021 (Unaudited)

| INVESTMENT INCOME:

|

|

Interest

| $ 751,946

|

Other

| 608,893

|

Total investment income

| 1,360,839

|

| EXPENSES:

|

|

Investment advisory fees

| 254,329

|

Administrative fees

| 33,191

|

Audit and tax fees

| 29,749

|

Transfer agent fees

| 16,899

|

Shareholder reporting fees

| 15,032

|

Listing expense

| 10,100

|

Trustees’ fees and expenses

| 7,630

|

Legal fees

| 4,829

|

Financial reporting fees

| 4,625

|

Custodian fees

| 2,963

|

Other

| 10,018

|

Total expenses

| 389,365

|

NET INVESTMENT INCOME (LOSS)

| 971,474

|

| NET REALIZED AND UNREALIZED GAIN (LOSS):

|

|

| Net realized gain (loss) on:

|

|

Investments

| 119,069

|

Futures contracts

| 102,161

|

Net realized gain (loss)

| 221,230

|

| Net change in unrealized appreciation (depreciation) on:

|

|

Investments

| (649,274)

|

Futures contracts

| (7,359)

|

Net change in unrealized appreciation (depreciation)

| (656,633)

|

NET REALIZED AND UNREALIZED GAIN (LOSS)

| (435,403)

|

NET INCREASE (DECREASE) IN NET ASSETS RESULTING FROM OPERATIONS

| $ 536,071

|

See Notes to Financial Statements

Page 13

First Trust Mortgage Income Fund (FMY)

Statements of Changes in

Net Assets

|

| Six Months

Ended

4/30/2021

(Unaudited)

|

| Year

Ended

10/31/2020

|

| OPERATIONS:

|

|

|

|

Net investment income (loss)

| $ 971,474

|

| $ 1,868,860

|

Net realized gain (loss)

| 221,230

|

| (154,999)

|

Net change in unrealized appreciation (depreciation)

| (656,633)

|

| (634,287)

|