UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2015

or

[_] TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ___________to ___________

Commission file number 001-33997

KANDI TECHNOLOGIES GROUP, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 90-0363723 |

| (State or other jurisdiction of incorporation | (I.R.S. Employer Identification No.) |

| or organization) |

Jinhua City Industrial Zone

Jinhua, Zhejiang

Province

People's Republic of China

Post Code 321016

(Address of principal executive offices) (Zip Code)

(86-579) 82239856

(Registrant's telephone

number, including area code)

Securities Registered Pursuant to Section 12(b) of the Act:

| Common Stock, Par Value $0.001 Per Share | NASDAQ Global Select Market |

| (Title of each class) | (Name of exchange on which registered) |

Securities Registered Pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes [_] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act.

Yes [_] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes [X] No [_]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulations S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes [X] No [_]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [_]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer [_] | Accelerated filer [X] |

| Non-accelerated filer [_] | Smaller reporting company [_] |

| (Do not check if a smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

Yes [_] No [X]

The aggregate market value of voting common stock held by non-affiliates of the registrant as of June 30, 2015, the last business day of the registrant's second fiscal quarter, was approximately $300,605,113.

The number of shares of common stock outstanding as of March 7, 2016 was 47,019,638.

DOCUMENTS INCORPORATED BY REFERENCE:

None.

TABLE OF CONTENTS

| PART I | ||

| Item 1. | Business. | 1 |

| Item 1A. | Risk Factors. | 13 |

| Item 1B. | Unresolved Staff Comments. | 23 |

| Item 2. | Properties. | 23 |

| Item 3. | Legal Proceedings. | 25 |

| Item 4. | Mine Safety Disclosures. | 25 |

| PART II | ||

| Item 5. | Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchase Equity Securities. | 26 |

| Item 6. | Selected Financial Data. | 28 |

| Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations. | 29 |

| Item 7A. | Quantitative and Qualitative Disclosures about Market Risk. | 44 |

| Item 8. | Financial Statements and Supplementary Data. | 44 |

| Item 9. | Changes In and Disagreements With Accountants on Accounting and Financial Disclosure. | 45 |

| Item 9A. | Controls and Procedures. | 46 |

| Item 9B. | Other Information. | |

| PART III | ||

| Item 10. | Directors, Executive Officers and Corporate Governance. | 47 |

| Item 11. | Executive Compensation. | 50 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters. | 56 |

| Item 13. | Certain Relationships and Related Transactions and Director Independence. | 57 |

| Item 14. | Principal Accounting Fees and Services. | 58 |

| PART IV | ||

| Item 15. | Exhibits, Financial Statement Schedules. | 59 |

| SIGNATURES | 62 |

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (this “Annual Report”) contains certain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These include statements about our expectations, beliefs, intentions or strategies for the future, which we indicate by words or phrases such as “anticipate,” “expect,” “intend,” “plan,” “will,” “we believe,” “our company believes,” “management believes” and similar language. These forward-looking statements are based on our current expectations and are subject to certain risks, uncertainties and assumptions, including those set forth in the discussion under Item 1, “Business”, Item 1A, “Risk Factors” and Item 7, “Management's Discussion and Analysis of Financial Condition and Results of Operations.” Our actual results may differ materially from results anticipated in these forward-looking statements. We base our forward-looking statements on information currently available to us, and we assume no obligation to update them. In addition, our historical financial performance is not necessarily indicative of the results that may be expected in the future and we believe such comparisons cannot be relied upon as indicators of future performance.

Although we believe that the expectations reflected in the forward looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Except as required by applicable law, including the securities laws of the United States, we do not intend to update any of the forward-looking statements to conform these statements to actual results.

PART I

Except as otherwise indicated by the context, references in this Annual Report to “we,” “us,” “our,” “Kandi,” or the “Company” are to the combined businesses of Kandi Technologies Group, Inc. and its subsidiaries.

Item 1. Business Introduction

Our Core Business

Before the year 2013, the Company had been mainly engaged in the design, production and distribution of the off-road vehicle products. Due to various market factors and the environment with positive government supports, starting from the year 2013, the Company gradually shifted its main focus towards the development on pure electric vehicles (“EV”) products and manufacturing electric vechicles parts. Also in the year 2013, the Company set up a Joint Venture with Geely Automobile Holdings Ltd. (“Geely”) to focus on EV production, based on the agreement, EV production should be transferred to the Joint Venture. At the end of 2014, this transfer had been completed. Starting from 2015, the majority of the Company’s revenue and profit were generated from the sale of EV parts.

The Market for Electric Vehicles

Business Environment and Policy

Research and development of major EV technology projects in China began in 2001. Driven by two central government five-year plans for scientific and technological research as well as by the Olympics, World Expo and the “1000 cars in 10 cities” demonstration platform, the Chinese electric automobile sector was officially born, which brings a positive basis for EV business.

1

With the growing consumer demand for motor vehicles in China, many cities are experiencing severe problems from environmental pollution. At the same time, with the lack of the efficient traffic planning, major Chinese cities are crippled by traffic congestion. Thus, major cities, such as Beijing, Shanghai, Guangzhou, Guiyang, Shijiazhuang, Tianjin, Hangzhou, Shenzhen, have begun to implement various policies restricting the purchase and usage of traditional cars. We expect that more cities will have no choices but to adopt similar policies in the future.

To improve the environment of the urban areas, the China Central Government, along with many municipalities, has been introducing numerous supporting policies that encouraged the usage and adoption of EVs, including subsidies, tax exemptions, special treatment of tag and license. Among these policies, the most significant development involved the availability of subsidies from central and local government for the sale of EVs. The process of receiving government subsidies is as follows: manufacturers receive central government subsidies through application and sell the EVs to local dealers at a discounted price, reflecting the deduction of the central government subsidy from the normal sale price. Local dealers then establish their retail price based upon the prevailing purchase price from the manufacturers, and then deduct the local government subsidy from the retail price before selling the EVs to consumers. Through these steps, consumers receive both subsidies from the central and local governments when they purchase EVs.

Because the central and local government subsidies are disclosed to the public and all the subsidies are reviewed and verified by the respective governments, consumers know what subsidies they will receive along with the price they expect to pay for EVs. Therefore, even though dealers can sell vehicles at prices established at their discretion, programs are designed to assure that consumers receive the entire benefit from both subsidies. This allows full disclosure for consumers in the costs associated with purchasing EVs, along with the added benefits of the respective subsidies.

Issues confronting the market

Although the basis for the EV industry in China has already been established, the development of Chinese EV industry is still ongoing due to five major obstacles towards extensive commercialization of EVs and the full development of the EV market in China, these obstacles include the comparatively higher cost of EVs, compared with traditional automobiles, the shorter driving range between battery charges, long charging times for standard EV batteries, the limited infrastructure of EV charging facilities, and EV battery attenuation and maintenance. Among which, the main obstacle is the lack of the charging facilities. Now the government is driving to resolve this issue. In the State Council general meeting on September 23, 2015, the central government decided that the charging facilities needs to be 100% equipped with or available for the new residential areas and 10% for the public buildings and public parking places. On October 9, 2015, the central government issued the guidance of EV charging infrastructure development 2015-2020, and the target is to build up 12,000 stations for the centralized charging and quick exchange, 4.8 million more for the scrattered charging spots, to serve the needs of power charge for 5 million EVs all over the country.

Our Solutions and Growth Strategy

To resolve the key market issues as stated above, given the economic and population growth in China, we believe there is an opportunity for a new business model. Kandi has been advocating, and through the Service Company, as defined below, implemented the “Micro Public Transportation” (“MPT”) program, which provides a shared pure EV transportation platform to urban residents. While it is less expensive than standard taxis, the MPT is designed as a new business model for public transportation that maximizes the advantages of our existing EV products and technologies, and further stimulates the expansion of the EVs markets to urban communities. Since its inception, the MPT program has made impressive progress, and received great recognition and support from government officials, the end users, and our business partners throughout China. In order to smoothly move the MPT concept forward, Zhejiang Kandi Vehicles Co., Ltd., our 100% subsidery ,participated in the establishing of Zhejiang ZuoZhongYou Electric Vehicle Service Co., Ltd. (the “Service Company”), of which the Company has 9.5% of ownership interest. As of the end of 2015, the EV-Share Program had been launched, through the Service Company, in sixteen cities including Hangzhou, Shanghai, Chengdu, Nanjing, Guangzhou, Wuhan, Changsha, Changzhou, Rugao, Kunming, Jinhua, Tianjin, Chongqing, Haikou,Shenzhen, Xiangtan.

2

Today, cities in China face four critical challenges in the traffic environment, including pollution, traffic congestion, insufficient parking space and growing scarcity of energy supplies, which are mainly the result of ever growing volume of gas-powered automobiles. One solution to solve these problems is to create cleaner and more affordable public transportation to urban residents. Currently, subway and bus are the most popular public transportation options available. In this regard, the Company advocates the MPT program to reduce the total number of private cars in use, which will improve environmental conditions, ease traffic congestion, alleviate parking availability, and reduce the reliance and use of fossil fuels.

Besides the zero-emission benefit, the MPT program combines the advantages of city taxis, resident vehicular transport, rental cars and traditional mass transportation, along with the benefits of the availability of the vertical automatic charging/parking garage and the street-level service stations. It is a seamless transportation tool in all dimensions for urban public transportation, designed to greatly improve the efficiency of urban EV usage, while easing traffic congestion and allowing for greater parking resources. Additionally, it will likely promote the fast adoption of the pure EVs among Chinese consumers as the MPT enables consumers to rent pure EVs on a short-term hourly base or lease them on the long-term base, without concerns on the costs and issues associated with owning and maintaining EVs individually.

The MPT program is supported by a network of charging/parking stations, which provides charging, maintenance and battery recycling facilities. The stations locate at airports, train stations, hotels, business centers, selected residential areas and other strategic locations close to city public transportation network. A centralized tracking system allows the service provider of EV-Share program to keep a close watch at the status and precise location of each vehicle. In addition to the short-term rental and long term leasing options to consumers described above, the Service Company also offers long-term leasing options to large enterprises, government entities and residential communities so they can use pure EVs for extended periods of time (the “Long-term Leasing Program”). In 2015, we have greatly benefited from the success of various MPT initiatives in China, especially the short-term hourly rental and the Long-term Leasing Program.

Our Organizational Structure

The Company was incorporated under the laws of the State of Delaware on March 31, 2004. The Company changed its name from Stone Mountain Resources, Inc. to Kandi Technologies, Corp. on August 13, 2007. On December 21, 2012, the Company changed its name to Kandi Technologies Group, Inc.

Headquartered in the Jinhua city, Zhejiang Province, China, the Company’s primary business operations are the design, development, manufacturing and commercialization of electric vehicles, electric vehicle parts and off-road vehicles, which are distributed in China and global markets. The Company conducts its primary business operations through its wholly-owned subsidiary, Zhejiang Kandi Vehicles Co., Ltd. (“Kandi Vehicles”) and the partial and wholly-owned subsidiaries of Kandi Vehicles. As part of its strategic objective to become a leader in EV market in China, the Company focuses on fuel efficient, pure EV parts manufacturing with a particular emphasis on expanding its market share in China.

3

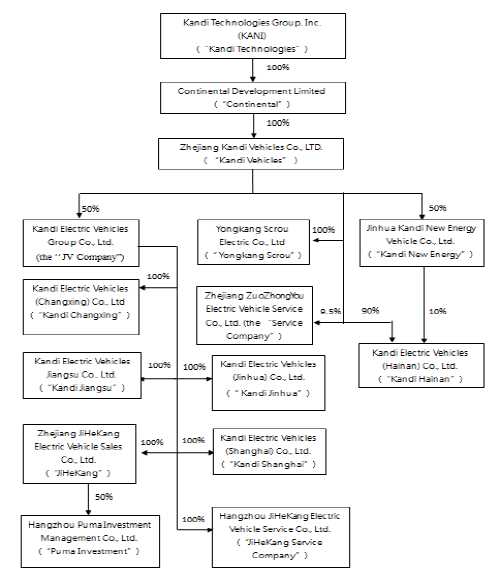

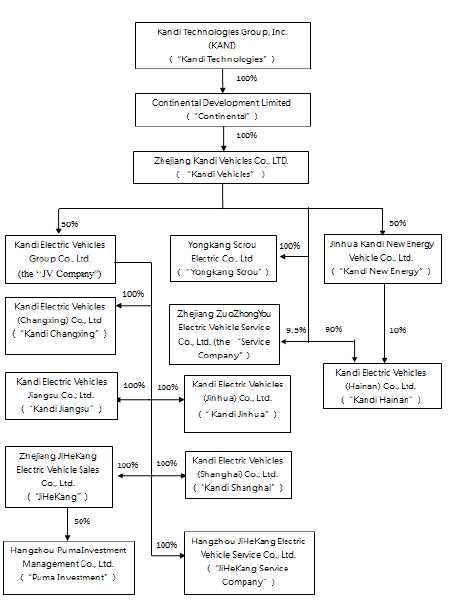

The Company's organizational chart is as follows:

Operating Subsidiaries:

Pursuant to relevant agreements executed in January 2011, Kandi Vehicles is entitled to 100% of the economic benefits, voting rights and residual interests (100% profits and loss absorption rate) of Jinhua Kandi New Energy Vehicles Co., Ltd. (“Kandi New Energy”). Kandi New Energy currently holds battery packing production rights (license), and supplies the battery pack to the JV Company. It also holds the Special-purpose vehicle production rights (license) on manufacturing Kandi brand electric utility vehicles, However, according to the JV Agreement, EV proucts should only be manufactured by the JV Company, Kandi New Energy need not to keep the Special-purpose vehicle production rights (license). In order to avoid the maintenance fee for this license, the Company plans to sell it to others.

4

In April 2012, pursuant to a share exchange agreement, the Company acquired 100% of Yongkang Scrou Electric Co, Ltd. (“Yongkang Scrou”), a manufacturer of parts for automobile and electric vehicle, including EV drive motors, EV controllers, air conditioners and other electrical products.

As a part of our EV business strategy, we believe we need more production resources to timely and efficiently satisfy the market demands. In March 2013, pursuant to a joint venture agreement (the “JV Agreement”) entered into between Kandi Vehicles and Shanghai Maple Guorun Automobile Co., Ltd. (“Shanghai Guorun”), a 99%-owned subsidiary of Geely Automobile Holdings Ltd. (“Geely”), the parties established Zhejiang Kandi Electric Vehicles Co., Ltd. (the “JV Company”) to develop, manufacture and sell EV products and related auto parts, and to invest in other companies with related or similar business. Each of Kandi Vehicles and Shanghai Guorun has 50% ownership interest in the JV Company. In March 2014, the JV Company changed its name to Kandi Electric Vehicles Group Co., Ltd. At present, the JV Company is a holding company with products that are manufactured by its subsidiaries.

In March 2013, Kandi Vehicles formed Kandi Electric Vehicles (Changxing) Co., Ltd. (“Kandi Changxing”) in the Changxing (National) Economic and Technological Development Zone. Kandi Changxing is engaged in the production of EV products. In the fourth quarter of 2013, Kandi Vehicles entered into an ownership transfer agreement with JV Company pursuant to which Kandi Vehicles transferred 100% of its ownership in Kandi Changxing to the JV Company. The Company, indirectly through its 50% ownership interest in the JV Company, has 50% economic interest in Kandi Changxing.

In July 2013, Zhejiang ZuoZhongYou Electric Vehicle Service Co., Ltd. (the “Service Company”) was formed. The Service Company is engaged in various pure EV leasing businesses, which is called “Micro Public Transportation”(“MPT”) program. The Company has 9.5% ownership interest in the Service Company through Kandi Vehicles.And the Company Chairman and CEO, Mr. Huxiaoming, also has 13% ownership interest in the Service Company.

In November 2013, Zhejiang Kandi Electric Vehicles Jinhua Co., Ltd. (“Kandi Jinhua”) was formed by the JV Company. The JV Company has 100% ownership interest in Kandi Jinhua, and the Company, indirectly through its JV Company, has 50% economic interest in Kandi Jinhua.

In November 2013, Zhejiang JiHeKang Electric Vehicle Sales Co., Ltd. (“JiHeKang”) was formed by the JV Company and is engaged in car sales business. The JV Company has 100% ownership interest in JiHeKang, and the Company, indirectly through its JV Company, has 50% economic interest in JiHeKang.

In December 2013, the JV Company entered into an ownership transfer agreement with Shanghai Guorun pursuant to which the JV Company acquired 100% ownership of Kandi Electric Vehicles (Shanghai) Co., Ltd. (“Kandi Shanghai”). As a result, Kandi Shanghai is a wholly-owned subsidiary of the JV Company, and the Company, indirectly through its JV Company, has 50% economic interest in Kandi Shanghai.

In January 2014, Zhejiang Kandi Electric Vehicles Jiangsu Co., Ltd. (“Kandi Jiangsu”) was formed by the JV Company. The JV Company has 100% ownership interest in Kandi Jiangsu, and the Company, indirectly through its JV Company, has 50% economic interest in Kandi Jiangsu.

In November 2015, Hangzhou Puma Investment Management Co,. Ltd.(“Puma Investment”) was formed by the JV Company, which focuses on the investment and consulting service. The JV Company has 50% ownership interest in Puma Investment; And the Company, indirectly through its JV Company, has 25% economic interest in Puma Investment.

5

In November 2015,Hangzhou JiHeKang Electric Vehicle Service Co., Ltd. (“JiHeKang Service Company”) was formed by the JV Company, which focuses on the after-marketing service for the EV sold. The JV Company has 100% ownership interest in JiHeKang Service Company; And the Company, indirectly through its JV Company, has 50% economic interest in JiHeKang Service Company.

In January 2016, Kandi Electric Vehicles (Hainan) Co., Ltd.(“Kandi Hainan”) was renamed from Kandi Electric Vehicles (Wanning) Co., Ltd. (“Kandi Wanning”) which was originally formed in Wanning City of Hainan Province by Kandi Vehicles and Kandi New Energy in April 2013 and then was transferred to Haikou City in January 2016. Kandi Vehicles has 90% ownership in Kandi Hainan, and Kandi New Energy has the remaining 10% interest. However, by contract, Kandi Vehicles is, effectively, entitled to 100% of the economic benefits, voting rights and residual interests (100% profits and losses) of Kandi Hainan. Hainan Province is planned as an international tourism island by the Chinese government and EVs will strongly promoted for the sharing and individual transportation to protect the environment. Therefore, the Company believes EV business has a great potential growth rate in Hainan province. To capture this opportunity, the Company plans to invest about a total of RMB 1 billion (approximately $154,019,129) to develop a factory in Haikou with an expected annual production of 100,000 EV products. This project is expected to launch its trial production in the middle of 2017.

Our Products

General

For the years ended December 31, 2015, 2014 and 2013, our products include EV parts, EV products, and off-road vehicles including ATVs, utility vehicles (“UTVs”), go-karts, and others. According to our market research on consumer demand trends, we have adjusted our production line strategically and continued to develop and manufacture new EV products in an effort to meet market demands and better serve our customers.

| Years Ended December 31 | |||||||||

| 2015 | 2014 | 2013 | |||||||

| Sales | Sales | Sales | |||||||

| EV parts | $ | 196,053,058 | $ | 116,431,309 | $ | 1,724,031 | |||

| EV products | - | 33,978,619 | 46,619,203 | ||||||

| Off-road vehicles | 5,016,115 | 19,819,078 | 46,192,811 | ||||||

| Total | $ | 201,069,173 | $ | 170,229,006 | $ | 94,536,045 | |||

EV Parts

During the year ended December 31, 2015, our revenues from the sale of EV parts were $196,053,058. We sold our EV parts mostly to the JV Company for manufacturing of the EV products. We started the EV parts business to the JV Company in the first quarter of 2014 and achieved significant growth during the year of 2015 and 2014. Among the total EV parts sales for the year ended December 31, 2015, approximately 83.5% or the majority of the sales were related to the sales of battery packs. Due to various Chinese auto industry regulations, we hold the necessary production license to manufacture battery packs to be exclusively used in the EV products manufactured by the JV Company under the Kandi brand.

6

EV Products

According to JV Agreement, the EVs production was transferred to the JV Company, which was completed at the end of 2014. In 2015, the Company has no EV products sold. Therefore, our revenues from the sale of EV products for the fiscal year of 2015 were $0, a decrease of $33,978,619 or 100% from $33,978,619 for the year ended December 31, 2014.

Off-Road Vehicles

During the year ended December 31, 2015, our revenues from the sale of the off-road vehicles declined by $14,802,963, or 74.7%, to $5,016,115 from $19,819,078 for the year ended December 31, 2014. The decrease was primarily due to the rearrangement of our product portfolio for more efficient use of resources to capture more sales opportunities in the fast-growing EV market in China.

The following table shows the breakdown of Kandi's revenues from its customers by geographic markets:

| Years Ended December 31 | ||||||||||||||||||

| 2015 | 2014 | 2013 | ||||||||||||||||

| Sales Revenue | Percentage | Sales Revenue | Percentage | Sales Revenue | Percentage | |||||||||||||

| Overseas | $ | 4,713,441 | 2% | $ | 8,629,824 | 5% | $ | 9,301,755 | 10% | |||||||||

| China | 196,355,732 | 98% | 161,599,182 | 95% | 85,234,290 | 90% | ||||||||||||

| Total | $ | 201,069,173 | 100% | $ | 170,229,006 | 100% | $ | 94,536,045 | 100% | |||||||||

Recent Development Activities

On November 2, 2015, the government of Zhejiang Province announced that the R&D institute of the JV Company will be entitled as the key enterprise R&D center in Zhejiang Province. Therefore, the R&D Institute of JV Company will get strong financial support for new products development and senior talent recruiting from the government.

On November 11, 2015, we announced that we signed a manifesto for the strategic development of "Car-Share 4.0" to promote connected electric vehicles with Zhejiang Geely Automobile Holding Group, Alibaba Group Holding, Ltd., ZTE Corporation, Uber China and China Minsheng Banking Corp. during a ceremony in Hangzhou. The Service Company has started the cooperation with Uber China, currently it delivered more than 200 EV products for Uber car lease project. The feedback was well after two months trial operation. We believe there is a big opportunity for future growth.

On November 23, 2015, we announced that the JV Company signed a strategic cooperation agreement with Nanjing Bustil Technology Co., Ltd. and its related subsidiaries for the sale of up to 3,000 Kandi K17 pure electric vehicles with the "Global Hawk" trademark to the MPT program in Nanjing. The initial delivery of 500 Kandi Global Hawk K17 units has been delivered by the end of 2015.

On November 24, 2015, we announced that the JV Company signed a direct sales contract with Tianjin Pang Da, a subsidiary of Pang Da Automobile Trade Co., Ltd., for an initial order of 1,000 Kandi-brand model K10 pure electric vehicles, And Pang Da Company plans to launch an EV-sharing program with the purchased vehicles in Tianjin. By the end of 2015, the delivery of the 1,000 EV units has been completed.

7

On December 1, 2015, we announced that the JV Company plans to deliver 2,000 Kandi Brand pure EV products to ZuoZhongYou (Hainan) Electric Vehicle Service Co., Ltd.to launch the MPT program in Haikou. The 2,000 EV products has been delivered by the end of 2015.

On December 15, 2015, we announced that Zhejiang Kandi Vehicles Co., Ltd. signed a cooperation agreement with the Haikou municipal government and the Haikou National Hi-Tech Industrial Development Zone on December 11, 2015 to establish a production facility in Haikou with an annual capacity of 100,000 EV products. The Haikou Facility will include equipment transferred from Kandi Vehicles’ facility that was previously under construction in Wanning City due to strategic changes in Wanning’s urban planning. The Agreement marks Hainan’s strategic effort to accelerate adjustment in the industrial planning process. We believe the new location will accelerate Kandi’s expansion in Hainan with favorable policies.

On December 22, 2015, we endorsed the announcement from Zhejiang ZuoZhongYou Electric Vehicle Service Co., Ltd of receiving an initial subsidy payment of RMB200 Million, or approximately US$30.9 million, from the Hangzhou local government. The payment is a result of 4,806 Kandi brand EV products used in the MPT program to support Zhejiang province’s target of promoting the use of 6,000 EVs from 2013 to 2015. The initial subsidy payment demonstrates the Hangzhou government’s commitment to promoting the adoption of renewable energy vehicles, while providing a solid foundation to achieve its goals for 2016-2020. We believe the unique MPT program will receive further recognition and support, and its expansion will be one of the key engines for Kandi’s future growth.

On January 21, 2016, we endorsed that Zhejiang ZuoZhongYou Electric Vehicle Service Co., Ltd (the “Service Company” or “ZZY”) has signed a strategic partnership memorandum with China (Yangtze River Delta) High-speed Railway Tourism Alliance (“Yangtze Alliance”) to provide hourly car rental services under the MPT program at railway stations within Yangtze Alliance’s network. ZZY and Yangtze Alliance aim to jointly establish a “Railway + MPT hourly rental” model to promote an environmentally friendly alternative for tourists’ self-guided trips. The partnership between ZZY and Yangtze Alliance will significantly increase the number of MPT stations within the regional high-speed railway tourism network, while accelerating the adoption of electric vehicle hourly rental services. We believe our unique MPT program will receive further recognition and support, and its rapid expansion will become one of Kandi’s key growth engines.

On Janurary 26, 2016, we announced that the JV Company has signed a strategic cooperation framework agreement with Pang Da Automobile Trade Co. Ltd. (“Pang Da”), a listed company on Shanghai Stock Exchange (601258.SS). The scope of the agreement includes, but is not limited to, establishment of Kandi and Pang Da sales teams that will share marketing resources, development of customized new energy vehicle for use at campus, and additionally, Pang Da is authorized to sell Kandi Brand pure electric vehicles (“EVs”) in specific regions. We believe this cooperation will well benefit our EV products direct sales channel in the future.

On Janurary 28, 2016, We announced that Kandi Hainan held a groundbreaking ceremony at the construction site of the Haikou production facility at Haikou Mei’An Hi-tech Zone. After completed the Haikou Facility, we expected to have an annual capacity of 100,000 electric vehicle (EV) products. The ceremony marks the beginning of Haikou Hi-tech Zone’s first project under the government’s 13th Five-Year Plan. Attendees of the ceremony include Ni Qiang, Mayor of Haikou, Ju Lei, Deputy Mayor, Hu Xiaoming, Chairman and CEO of Kandi and other officials of the municipal government. Our Haikou facility will help the company’s future growth and will also contribute to Hainan’s economic and eco-environmental development.

8

In the second half year of 2015, the Company started to cooperate with the Micro Mobility System, a Switzerland Private Company which prodcues the famous Razor scooter on the market from 1999, to develop a new generation of micro EV product called “Mircolino”, which provides efficient methods to faciliate city mobility. The microlino could become the next big thing in urban electric mobility, and we expect this new product will bring Kandi into the international EV market.

In early 2016, Mr. Hu Xiaoming, the Chariman of the Company, initiated a project with the wireless conductive technology and its application on EV products, and built a team with Tsinghua University and Zhejiang University to research and develop on this project. The team had certain initial progresses that successfully developed the model for the wireless conductive technology. We believe this technology may bring the revolution for the EV industry.

Sales and Distribution

The Company has two main products: electric vehicle parts and off-road vehicles in year 2015 while it featured EV products before 2015. As the EV production was completely transferred to the JV Company at the end of 2014 according to the JV Agreement, Kandi focuses on the EV parts production and supply EV parts to the JV Company. Additionally, Kandi continues to produce and sell the off-road vehicles, which are our traditional products.

Customers

As of December 31, 2015, our major customers, in the aggregate, accounted for 97% of our sales. Currently, the Company is developing new business partners and clients for our products to reduce our dependence on existing customers and focusing the new business development efforts on our pure EV business.

The Company's major customers, each of whom accounted for more than 10% of our consolidated revenue, were as follows:

|

|

Sales | Accounts Receivable | ||||||

|

|

Year | Year | Year | |||||

|

|

Ended | Ended | Ended | |||||

|

|

December 31 | December 31 | December 31 | December 31 | December 31 | December 31 | ||

|

Major Customers |

2015 | 2014 | 2013 | 2015 | 2014 | 2013 | ||

|

Kandi Electric Vehicles Group Co., Ltd. |

34% | - | - | 46% | - | - | ||

|

Kandi Electric Vehicles (Changxing) Co., Ltd. |

22% | 38% | - | 1% | 17% | - | ||

|

Zhejiang Zuozhongyou Electric Vehicle Service Co., Ltd. |

21% | - | - | 38% | - | - | ||

|

Kandi Electric Vehicles (Shanghai) Co., Ltd. |

20% | 23% | - | - | 16% | - | ||

|

Shanghai Maple Auto Co., Ltd |

- | 10% | 23% | - | 3% | 47% | ||

9

Sources of Supply

All the raw materials are purchased from the suppliers. The major parts of our products are mainly manufactured by Kandi. Other components and parts that are needed are purchased from third-party suppliers. Kandi does not have, and does not anticipate having, any difficulty in obtaining required materials from its suppliers.

The Company's material suppliers, each of whom accounted for more than 10% of our total purchases, were as follows:

|

|

Purchases | Accounts Payable | |||||

|

|

Year | Year | Year | ||||

|

|

Ended | Ended | Ended | ||||

|

|

December 31 | December 31 | December 31 | December 31 | December 31 | December 31 | |

|

Major Suppliers |

2015 | 2014 | 2013 | 2015 | 2014 | 2013 | |

|

Dongguan Chuangming Battery Technology Co., Ltd. |

26% | - | - | 15% | - | - | |

|

Zhejiang Tianneng Energy Technology Co., Ltd. |

20% | - | - | 24% | - | - | |

|

Zhejiang New Energy Auto System Co., Ltd. |

13% | 31% | 33% | - | 12% | 12% | |

|

Shandong Henyuan New Energy Tech Co., Ltd. |

7% | 25% | - | 14% | 32% | - | |

|

Zhongju (Tianjin) New Energy Investment Co., Ltd. |

- | 11% | - | - | 29% | - | |

Competitors

Our EV business faces the competition from two parts, one is the competition with traditional vehicles and the other is the competition from other EV manufacturers.

In terms of the competition with the traditional vehicle manufacturers, many competitors are larger and having greater financial resources than us. But the traditional automobile companies face many urban traffic challenges, including urban pollution, traffic congestion, insufficient parking space and energy crisis, which give us great opportunities for EVs’ development. The government grants great support and issues favorable policies to promote EVs development, which is a clear evidence for EVs growth. We believe electric vehicle industry in China has many years of great potential growth ahead.

Within the electric vehicle market, the competitions are fierce as we have to compete with many domestic and global EV manufactures with greater brand recognition and financial resources. However, being one of the earliest companies to engage in the research, production and distribution of electric vehicles, we believe we have the advantage on technology, innovation on the vehicle business operation and distribution channel. In particular, the innovative MPT program we have been advocated as being different from the offering of our competitors, and has been well accepted and praised by the government and the end users. This business model, along with our continuous efforts on research and development as well as strategic alliance, shall help us to build competitive advantages over other EV manufacturers.

10

Intellectual Property and Licenses

Our success depends, at least in part, on our ability to protect our core technology and intellectual property. We rely on a combination of patents, patent applications, trademarks, copyrights and trade secret protection laws in China and other jurisdictions, as well as confidentiality procedures and contractual provisions to protect our intellectual property and our brand. As of December 31, 2015, we had 35 issued patents, 2 issued software copyrights and 13 pending patent applications with Chinese patent authority related to electrical vehicle products, electrical vehicle parts and off-road vehicle products. Under the PRC Patent Law, an invention patent is valid for a term of 20 years and a utility or design patent is valid for a term of 10 years. Our patents are valid for 10 years. In addition, we are authorized to use the trademark “Kandi” and we are the owner of the trademark “JASSCOL”. We intend to continue to file additional patent applications with respect to our technology.

Employees

As of December 31, 2015, excluding the contractors, Kandi had a total of 557 full-time employees as compared to 516 full-time employees on December 31, 2014, of which 415 employees are production personnel, 23 employees are sales personnel, 48 employees are research and development personnel, and 71 employees are administrative personnel. None of our employees are covered by collective bargaining agreements. We consider our relationships with our employees to be good. We also employ consultants on an as needed basis.

Pure Electric Vehicles Subsidies

Currently, there are two subsidies from central and local governments for the pure EV sales in China – one from each of the central and local governments. The ultimate beneficiary for these subsidies is the consumer and the actual prices that consumers pay reflect the deduction of both subsidies.

a) The central government provides a subsidy to manufacturers paid in advance quarterly upon application and approval and settled annually. After selling product to dealers, manufacturers can submit subsidy payment applications with invoices and other supporting documents at the end of each quarter to the requisite central government agencies through their regional offices. After the review and approval by the agencies, the central government makes advance subsidy payments to the manufacturers. At the end of the year, the final subsidy amounts are verified, reconciled according to the number of vehicles actually sold to consumers and settled on an annual basis.

b) Pursuant to the requirement of the central government, the local governments provide a subsidy to consumers who purchase EVs from the dealer. After the consumer purchases an EV at a reduced selling price provided by the dealer, the dealer submits a subsidy application to the local government, including a consumer authorization letter for subsidy application, consumer personal I.D., EV Vehicle License, EV purchase invoice and other required documents and requests of reimbursement (to the dealer) for the local government subsidy.

Environmental and Safety Regulation

Emissions

Our products are all subject to international laws and emissions related regulations, including regulations and related standards established by China Environmental Protection Agency, the United States Environmental Protection Agency (“EPA”), the California Air Resources Board (“CARB”), Europe and Canada.

11

All Kandi's products comply with all applicable emission standards and regulations in China Environmental Protection Agency, the United States and internationally, the California Air Resources Board (“CARB”), Europe and Canada. However, we are unable to predict the ultimate impact of standards and regulations adopted in the future or proposed regulations on Kandi and its business.

Use regulation

The sale and use of products must be subject to the "Traffic Law" and relevant laws & regulations in China. National, State, and federal laws and regulations have been promulgated, or are under consideration, that impact the use or manner of use of Kandi's products. Certain states and local authorities have adopted, or are considering the adoption of, legislation and local ordinances which restrict the use of ATVs and off-road vehicles to specified hours and locations. The federal government also has restricted the use of ATVs and off-road vehicles in some national parks and federal lands. In several instances, the restriction has been a complete ban on the recreational use of these vehicles. Kandi is unable to predict the outcome of such actions or the possible effect on its business. Kandi believes that its off-road vehicle business would be no more adversely affected than those of its competitors by the adoption of any such pending laws or regulations.

Product Safety and Regulation

Safety Regulation

The U.S. federal government and individual states have adopted, or are considering the adoption of, laws and regulations relating to the use and safety of Kandi's products. The federal government is the primary regulator of product safety. The Consumer Product Safety Commission (“CPSC”) has federal oversight over product safety issues related to ATVs and off-road vehicles. The National Highway Transportation Safety Administration (“NHTSA”) has federal oversight over product safety issues related to on-road motorcycles.

In August 2008, the Consumer Product Safety Improvement Act (the “Act”) was passed. The Act requires all manufacturers and distributors who import into or distribute ATVs within the United States to comply with the ANSI/SVIA safety standards, which were previously voluntary. The Act also requires the same manufacturers and distributors to have ATV action plans filed with the CPSC that are substantially similar to the voluntary action plans that were previously in effect. Kandi currently complies with the ANSI/SVIA standards.

Kandi's motorcycles are subject to federal vehicle safety standards administered by NHTSA. Kandi's motorcycles are also subject to various state vehicle safety standards. Kandi believes that its motorcycles comply with safety standards applicable to motorcycles.

Kandi's products are also subject to international safety standards in places where it sells its products outside the United States. Kandi believes that its motorcycles and EV products comply with applicable safety standards in the United States and internationally.

12

Principal Executive Offices

Our principal executive office is located in the Jinhua City Industrial Zone in Jinhua, Zhejiang Province, PRC, 321016 and our telephone number is (86-579) 82239856.

Item 1A. Risk Factors.

You should carefully consider the risks described below together with all of the other information included in this report before making an investment decision with regard to our securities. The statements contained in or incorporated into this Annual Report that are not historic facts are forward-looking statements that are subject to risks and uncertainties that could cause actual results to differ materially from those set forth in or implied by forward-looking statements. If any of the following risks actually occurs, our business, financial condition or results of operations could be harmed. In that case, the trading price of our common stock could decline, and you may lose all or part of your investment.

Risks Relating to Our Business

Our future growth is dependent upon consumers’ willingness to adopt EVs.

Our growth is highly dependent upon the adoption by consumers of, and we are subject to a risk of any reduced demand for, alternative fuel vehicles in general and EVs in particular. The market for alternative fuel vehicles (including EVs) is relatively new, rapidly evolving, characterized by rapidly changing technologies, price competition, additional competitors, evolving government regulation and industry standards, frequent new vehicle announcements and changing consumer demands and behaviors. If the market for EVs in China does not develop as we expect or develops slowlier than we expect, our business, prospects, financial condition and operating results will be harmed.

The unavailability, reduction or elimination of government and economic incentives could have a material adverse effect on our business, financial condition, operating results and prospects.

Chinese government has made significant efforts in actively advocating the development of new energy vehicles. In November 2015, it issued the 10-year road map of EV industry development and set the annual EV sales target for 5% of the annual auto sale volume by year 2020 and 20% by year 2025. The central government also has a clear policy providing subsidies to the qualified EVs till 2020. Any reduction, elimination or discriminatory application of government subsidies and economic incentives because of policy changes, the reduced need for such subsidies and incentives due to the customer base of our EV products, fiscal tightening or other reasons may result in the diminished competitiveness of the alternative fuel vehicle industry generally or our EV products in particular. This could materially and adversely affect the growth of the alternative fuel automobile markets and our business, prospects, financial condition and operating results.

Our growth depends in part on the availability and amounts of government subsidies and economic incentives for alternative fuel vehicles generally and performance EVs specifically. For example, purchasers of three models of Kandi brand EV products are eligible to receive purchase tax exemption at the amount of 10% of the vehicle’s total purchase price excluding VAT during the three-year period from September 1, 2014. Purchasers of Kandi's SMA7000BEV and SMA7001BEV models are the ultimate beneficiaries, on a per car basis, the national government subsidy of RMB 45,000.00 (Approximately $6,931) in 2015, many cities also provide local subsidies, which differ according to the related local policies. Additionally, these two vehicle models also qualify for free license plates in many cities. Especially in Shanghai, the license plates in Shanghai are auctioned to the public at an average price between RMB74,000 to RMB85,300 ($11,400 to $13,140) per license plate. While we believe the latest tax exemption, along with a series of government incentives and subsidies, may have a very positive impact on the sales of Kandi Brand EVs in China going forward, we cannot assure you it is always the case. In the event such favored policy and treatment discontinue, our business outlook and financial conditions could be negatively impacted.

13

Developments in alternative technologies or improvements in the internal combustion engine may materially adversely affect the demand for our EV Products.

Significant developments in alternative technologies, such as advanced diesel, ethanol, fuel cells or compressed natural gas, or improvements in the fuel economy of the internal combustion engine, may materially and adversely affect our business and prospects in ways we do not currently anticipate. Any failure by us to develop new or enhanced technologies or processes, or to react to changes in existing technologies, could materially delay our development and introduction of new and enhanced EV products, which could result in the loss of competitiveness of our vehicles, decreased revenue and a loss of market share to competitors.

If we are unable to keep up with advances in electric vehicle technology, we may suffer a decline in our competitive position.

We may be unable to keep up with changes in EV technology, and we may suffer a decline in our competitive position. Any failure to keep up with advances in EV technology would result in a decline in our competitive position which would materially and adversely affect our business, prospects, operating results and financial condition. Our research and development efforts may not be sufficient to adapt to changes in EV technology. As technologies change, we plan to upgrade or adapt our vehicles and introduce new models in order to continue to provide vehicles with the latest technology, in particular battery cell technology. However, our vehicles may not compete effectively with alternative vehicles if we are not able to source and integrate the latest technology into our vehicles. For example, we do not manufacture battery cells, which makes us dependent upon other suppliers of battery cell technology for our battery packs.

Our business depends substantially on the continuing efforts of our executive officers, and our business may be severely disrupted if we lose their services.

Our future success depends substantially on the continued services of our executive officers, especially our CEO and Chairman of the Board of Directors, Mr. Hu Xiaoming. We do not maintain key man life insurance on any of our executive officers. If any of our executive officers are unable or unwilling to continue in their present positions, we may not be able to replace them readily, if at all. Therefore, our business may be severely disrupted, and we may incur additional expenses to recruit and retain new officers. In addition, if any of our executive officers joins a competitor or forms a competing company, we may lose some of our customers.

We may be subject to product liability claims, or recalls which could be expensive, damage our reputation and result in a diversion of management resources.

We may be subject to lawsuits resulting from injuries associated with the use of the vehicles that we sell or produce. We may incur losses relating to these claims or the defense of these claims. There is a risk that claims or liabilities will exceed our insurance coverage. In addition, we may be unable to retain adequate liability insurance in the future.

14

We may also be required to participate in recalls involving our vehicles, if any prove to be defective, or we may voluntarily initiate a recall or make payments related to such claims as a result of various industry or business practices or the need to maintain good customer relationships. Such a recall would result in a diversion of resources. While we do maintain product liability insurance, we cannot assure you that it will be sufficient to cover all product liability claims, that such claims will not exceed our insurance coverage limits or that such insurance will continue to be available on commercially reasonable terms, if at all. Any product liability claim brought against us could have a material adverse effect on our results of operations.

We retain certain personal information about our customers and may be subject to various privacy and consumer protection laws.

We and our operating companies use the electronic systems of our vehicles to log information about each vehicle’s condition, performance and use in order to aid us in providing customer service, including vehicle diagnostics, repair and maintenance, as well as to help us collect data regarding our customers’ charge time, battery usage, mileage and efficiency habits and to improve our vehicles. We also collect information about our customers through our website, at our stores and facilities, and via telephone.

Our customers may object to the processing of this data, which may negatively impact our ability to provide effective customer service and develop new vehicles and products. Collection and use of our customers’ personal information in conducting our business may be subject to national and local laws and regulations in the PRC, and such laws and regulations may restrict our processing of such personal information and hinder our ability to attract new customers or market to existing customers. We may incur significant expenses to comply with privacy, consumer protection and security standards and protocols imposed by law, regulation, industry standards or contractual obligations. Although we take steps to protect the security of our customers’ personal information, we may be required to expend significant resources to comply with data breach requirements if third parties improperly obtain and use the personal information of our customers or we otherwise experience a data loss with respect to customers’ personal information. A major breach of our network security and systems could have serious negative consequences for our businesses and future prospects, including possible fines, penalties and damages, reduced customer demand for our vehicles, and harm to our reputation and brand.

Our business will be adversely affected if we are unable to protect our intellectual property rights from unauthorized use or infringement by third parties.

Any failure to adequately protect our proprietary rights could result in weakening or loss of such rights, which may allow our competitors to offer similar or identical products or use identical or confusingly similar branding, potentially resulting in the loss of some of our competitive advantage, a decrease in our revenue and an attribution of potentially lower quality products to us, which would adversely affect our business, prospects, financial condition and operating results. Our success depends, at least in part, on our ability to protect our core technology and intellectual property. To accomplish this, we rely on a combination of patents, patent applications, trade secrets, including know-how, employee and third party nondisclosure agreements, copyright protection, trademarks, intellectual property licenses and other contractual rights to establish and protect our proprietary rights in our technology. We have also received from third parties patent licenses related to manufacturing our vehicles.

The protection provided by the patent laws is and will be important to our future opportunities. However, such patents and agreements and various other measures we take to protect our intellectual property from use by others may not be effective for various reasons, including the following:

15

- our pending patent applications may not result in the issuance of patents;

- our patents, if issued, may not be broad enough to protect our commercial endeavors;

- the patents we have been granted may be challenged, invalidated or circumvented because of the pre-existence of similar patented or unpatented technology or for other reasons;

- the costs associated with obtaining and enforcing patents, confidentiality and invention agreements or other intellectual property rights may make aggressive enforcement impracticable; and

- current and future competitors may independently develop similar technology, duplicate our vehicles or design new vehicles in a way that circumvents our intellectual property.

Existing trademark and trade secret laws and confidentiality agreements afford only limited protection. In addition, the laws of some foreign countries do not protect our proprietary rights to the same extent as do the laws of the United States, and policing the unauthorized use of our intellectual property is difficult.

We may need to defend ourselves against patent or trademark infringement claims, which may be time-consuming and would cause us to incur substantial costs.

Companies, organizations or individuals, including our competitors, may hold or obtain patents, trademarks or other proprietary rights that would prevent, limit or interfere with our ability to make, use, develop, sell or market our vehicles or components, which could make it more difficult for us to operate our business. From time to time, we may receive inquiries from holders of patents or trademarks regarding their proprietary rights. Companies holding patents or other intellectual property rights may bring suits alleging infringement of such rights or otherwise assert their rights and seek licenses. In addition, if we are determined to have infringed upon a third party’s intellectual property rights, we may be required to do one or more of the following:

- cease selling, incorporating or using vehicles or offering goods or services that incorporate or use the challenged intellectual property;

- pay substantial damages;

- obtain a license from the holder of the infringed intellectual property right, which license may not be available on reasonable terms or at all; or

- redesign our vehicles or other goods or services.

In the event of a successful claim of infringement against us and our failure or inability to obtain a license to the infringed technology or other intellectual property right, our business, prospects, operating results and financial condition could be materially adversely affected. In addition, any litigation or claims, whether or not valid, could result in substantial costs and diversion of resources and management attention.

We may also face claims that our use of technology licensed or otherwise obtained from a third party infringes the rights of others. In such cases, we may seek indemnification from our licensors/suppliers under our contracts with them. However, indemnification may be unavailable or insufficient to cover our costs and losses, depending on our use of the technology, whether we choose to retain control over conduct of the litigation, and other factors.

Our vehicles make use of lithium-ion battery cells, which could catch fire or vent smoke and flame. This may lead to additional concerns, about the batteries used in automotive applications.

The battery pack in our EV products makes use of lithium-ion cells. We also currently intend to make use of lithium-ion cells in battery packs on any future vehicles we may produce. On rare occasions, lithium-ion cells can rapidly release the energy they contain by venting smoke and flames in a manner that can ignite nearby materials as well as other lithium-ion cells. Extremely rare incidents of laptop computers, cell phones and EV battery packs catching fire have focused consumer attention on the safety of these cells.

16

These events have raised concerns about the batteries used in automotive applications. To address these questions and concerns, a number of cell manufacturers are pursuing alternative lithium-ion battery cell chemistries to improve safety. We may have to recall our vehicles or participate in a recall of a vehicle that contains our battery packs, and redesign our battery packs, which would be time consuming and expensive. Also, negative public perceptions regarding the suitability of lithium-ion cells for automotive applications or any future incident involving lithium-ion cells such as a vehicle or other fire, even if such incident does not involve us, could seriously harm our business.

In addition, we store a significant number of lithium-ion cells at our manufacturing facility. Any mishandling of battery cells may cause disruption to the operation of our facilities. While we have implemented safety procedures related to the handling of the cells, there can be no assurance that a safety issue or fire related to the cells would not disrupt our operations. Such damage or injury would likely lead to adverse publicity and potentially a safety recall. Moreover, any failure of a competitor’s EV, may cause indirect adverse publicity for us and our EV products. Such adverse publicity would negatively affect our brand and harm our business, prospects, financial condition and operating results.

Compliance with environmental regulations can be expensive, and noncompliance with these regulations may result in adverse publicity and potentially significant monetary damages and fines.

Our business operations generate noise, waste water, gaseous byproduct and other industrial waste. We are required to comply with all national and local regulations regarding protection of the environment. We are in compliance with current environmental protection requirements and have all necessary environmental permits to conduct our business. However, if more stringent regulations are adopted in the future, the costs of compliance with these new regulations could be substantial. Additionally, if we fail to comply with present or future environmental regulations, we may be required to pay substantial fines, suspend production or cease operations. Any failure by us to control the use of, or to adequately restrict the unauthorized discharge of, hazardous substances could subject us to potentially significant monetary damages and fines or suspensions to our business operations. Certain laws, ordinances and regulations could limit our ability to develop, use, or sell our products.

The electric vehicle industry is highly competitive, and we are subject to risks relating to competition that may adversely affect our performance.

The electric vehicle industry is highly competitive, and our continued success depends upon our ability to compete effectively in markets that contain many competitors, some of which have significantly greater financial, marketing and other resources than we have. Competition may affect our pricing structures, potentially causing us to lower our prices, which may adversely impact our profits. New or existing competition that uses a business model that is different from our business model may put pressure on us to change our model so that we can remain competitive.

Our high concentration of sales to relatively few customers may result in significant impact our liquidity, business, results of operations and financial condition.

As of December 31, 2015 and 2014, our major customers (above 10% of the total revenue), in the aggregate, accounted for 97% and 84%, respectively, of our sales. Due to the concentration of sales to relatively few customers, loss of one or more of these customers will have relatively high impact on our operational results.

17

Our business is subject to the risk of supplier concentrations.

We depend on a limited number of suppliers for the sourcing of major components and parts and principal raw materials. For the years ended December 31, 2015 and 2014, the top two suppliers accounted for 46% and 57% of our purchases, respectively. As a result of this concentration in our supply chain, our business and operations would be negatively affected if any of our key suppliers were to experience significant disruption affecting the price, quality, availability or timely delivery of their products. The partial or complete loss of these suppliers, or a significant adverse change in our relationship with any of these suppliers, could result in lost revenue, added costs and distribution delays that could harm our business and customer relationships. In addition, concentration in our supply chain can exacerbate our exposure to risks associated with the termination by key suppliers of our distribution agreements or any adverse change in the terms of such agreements, which could have a negative impact on our revenues and profitability.

Our facilities or operations could be damaged or adversely affected as a result of disasters or unpredictable events.

Our headquarters and facilities are located in several cities in China such as Jinhua, Yongkang and Haikou. If major disasters such as earthquakes, fires, floods, hurricanes, wars, terrorist attacks, computer viruses, pandemics or other events occur, or our information system or communications network breaks down or operates improperly, our headquarters and production facilities may be seriously damaged, or we may have to stop or delay production and shipment of our products. We may incur expenses relating to such damages, which could have a material adverse impact on our business, operating results and financial condition.

If we fail to maintain an effective system of internal controls, we may not be able to accurately report our financial results or prevent fraud. As a result, current and potential shareholders could lose confidence in our financial reporting, which would harm our business and the trading price of our stock.

Effective internal controls are necessary for us to provide reliable financial reports and effectively prevent fraud. As directed by Section 404 of the Sarbanes-Oxley Act of 2002, or SOX 404, the SEC adopted rules requiring public companies to include a report of management on our internal controls over financial reporting in their annual reports.

Despite that we continued to maintain and improved our internal control procedures, we cannot provide assurance that we will not fail to achieve and maintain an effective internal control environment on an ongoing basis, which may cause investors to lose confidence in our reported financial information and have a material adverse effect on the price of our common stock.

The audit report included in this Annual Report was prepared by auditors who are not inspected by the Public Company Accounting Oversight Board and, as a result, you are deprived of the benefits of such inspection

The independent registered public accounting firm that issues the audit reports included in our annual reports filed with the SEC, as auditors of companies that are traded publicly in the United States and a firm registered with the Public Company Accounting Oversight Board (United States), or the “PCAOB”, is required by the laws of the United States to undergo regular inspections by the PCAOB to assess its compliance with the laws of the United States and professional standards. Because our auditors are located in Hongkong, a jurisdiction where the PCAOB is currently unable to conduct inspections without the approval of the PRC authorities, our auditors are not currently inspected by the PCAOB.

18

Inspections of other firms that the PCAOB has conducted outside China have identified deficiencies in those firms' audit procedures and quality control procedures, which may be addressed as part of the inspection process to improve future audit quality. The inability of the PCAOB to conduct inspections in China prevents the PCAOB from regularly evaluating our auditor's statements, audits and quality control procedures. As a result, investors may be deprived of the benefits of PCAOB inspections.

The inability of the PCAOB to conduct inspections of auditors in China makes it more difficult to evaluate the effectiveness of our auditor's quality control and audit procedures as compared to auditors outside of China that are subject to PCAOB inspections. Investors may lose confidence in our reported financial information and procedures and the quality of our financial statements.

Risks Related to Doing Business in China

The economy of China had experienced unprecedented growth. This growth has slowed in the recent years, and if the growth of the economy continues to slow or if the economy contracts, our financial condition may be materially and adversely affected.

The rapid growth of the PRC economy had historically resulted in widespread growth opportunities in industries across China. This growth has slowed in the recent years. As a result of the global financial crisis and the inability of enterprises to gain comparable access to the same amounts of capital available in past years, there may be an adverse effect on the business climate and growth of private enterprise in the PRC. An economic slowdown could have an adverse effect on our sales and may increase our costs. Further, if economic growth continues to slow, and if, in conjunction, inflation is to proceed unchecked, our costs would likely to increase, and there can be no assurance that we would be able to increase our prices to an extent that would offset the increase in our expenses.

In addition, a tightening of the labor markets in our geographic region may result in fewer qualified applicants for job openings in our facilities. Further, higher wages, related labor costs and other increasing cost trends may negatively impact our results.

Changes in political and economic conditions may affect our business operations and profitability.

Since our business operations are primarily located in China, our business operations and financial position are subject, to a significant degree, to the economic, political and legal developments in China.

While the Chinese government has not halted its economic reform policy since 1978, any significant adverse changes in the social, political and economic conditions of China may fundamentally impact China's economic reform policies, and thus the Company's operations and profits may be adversely affected.

Uncertainties with respect to the Chinese legal system could have a material adverse effect on us and may restrict the level of legal protections to foreign investors.

China's legal system is based on statutory law. Unlike the common law system, statutory law is based primarily on written statutes. Previous court decisions may be cited as persuasive authority but do not have a binding effect. Since 1979, the PRC government has been promulgating and amending the laws and regulations regarding economic matters, such as corporate organization and governance, foreign investment, commerce, taxation and trade. However, since these laws and regulations are relatively new, and the PRC legal system continues to rapidly evolve, the interpretation of many laws, regulations and rules is not always uniform and enforcement of these laws, regulations and rules involves uncertainties, which may limit legal protections available to us.

19

In addition, any litigation in China may be protracted and may result in substantial costs and diversion of resources and management's attention. The legal system in China cannot provide investors with the same level of protection as in the U.S. The Company is governed by laws and regulations generally applicable to local enterprises in China. Many of these laws and regulations were recently introduced and remain experimental in nature and subject to changes and refinements. Interpretation, implementation and enforcement of the existing laws and regulations can be uncertain and unpredictable and therefore may restrict the legal protections available to foreign investors.

Changes in Currency Conversion Policies in China may have a material adverse effect on us.

Renminbi (“RMB”) is still not a freely exchangeable currency. Since 1998, the State Administration of Foreign Exchange of China has promulgated a series of circulars and rules in order to enhance verification of foreign exchange payments under a Chinese entity's current account items, and has imposed strict requirements on borrowing and repayments of foreign exchange debts from and to foreign creditors under the capital account items and on the creation of foreign security in favor of foreign creditors.

This may complicate foreign exchange payments to foreign creditors under the current account items and thus may affect the ability to borrow under international commercial loans, the creation of foreign security, and the borrowing of RMB under guarantees in foreign currencies. Moreover, the value of RMB may become subject to supply and demand, which could be largely impacted by international economic and political environments. Any fluctuations in the exchange rate of RMB could have an adverse effect on the operational and financial condition of the Company and its subsidiaries in China.

You may experience difficulties in effecting service of legal process, enforcing foreign judgments or bringing original actions based on United States or foreign laws against us, our management or the experts named in the prospectus.

We conduct substantially all of our operations in China and almost all of our assets are located in China. In addition, almost all of our senior executive officers reside in China. As a result, it may not be possible to effect service of process on our senior executive officers within the United States or elsewhere outside China, including with respect to matters arising under U.S. federal securities laws or applicable state securities laws. Moreover, our PRC counsel has advised us that the PRC does not have treaties with the United States or many other countries providing for the reciprocal recognition and enforcement of court orders and final judgments.

Delays surrounding the updates with respect to the official list of qualified EV models to receive national subsidies from the governments in the PRC may delay the sale of our EV products.

In January and February 2016, the PRC Ministry of Industry and Information Technology (the “MITT”) announced new lists of qualified EV models to receive the national subsidy each month. The new lists overruled the right to receive the national subsidy for all the EV models that were included in the previously announced lists. Meanwhile, an updated list of qualified EV models to receive purchase tax exempt in 2016 is still forthcoming from the State Administration of Taxation. To apply for tax exemption, a product must be listed on the approved lists by the MITT. A total of four EV models from the JV Company are on the updated lists. The JV Company is currently in the process of applying for tax exemption for those four EV models. As such, sales for EV manufacturers, including our JV Company, have been significantly delayed in the first quarter of 2016. If the Company failed to receive approval from the PRC government to be listed for national subsidies for any of its models, our sales and profits may be adversely affected.

20

Risks Relating to Ownership of Our Securities

Our stock price may be volatile, which may result in losses to our shareholders.

The stock markets have experienced significant price and trading volume fluctuations and the market prices and trading volumes of companies listed on the NASDAQ Global Market and the NASDAQ Global Select Market have been volatile. Although our stock was listed on the NASDAQ Global Market and upgraded to the NASDAQ Global Select Market on January 2, 2014, the trading price of our common stock is likely to be volatile and could fluctuate significantly in response to many factors, including the following, some of which are beyond our control:

- variations in our operating results;

- changes in expectations of our future financial performance, including financial estimates by securities analysts and investors;

- changes in operating and stock price performance of other companies in our industry;

- additions or departures of key personnel; and

- future sales of our common stock.

Domestic and international stock markets often experience significant price and volume fluctuations. These fluctuations, as well as general economic and political conditions unrelated to our performance, may adversely affect the price of our common stock.

Mr. Hu, our CEO, President and Chairman of our Board of Directors is the beneficial owner of a substantial portion of our outstanding common stock, which may enable Mr. Hu to exert significant influence on corporate actions.

Excelvantage Group Limited controls approximately 25.52% of our outstanding shares of common stock as of March 7, 2016. Hu Xiaoming, the Company's Chief Executive Officer, President and Chairman of the Board of Directors, is the sole stockholder of Excelvantage Group Limited. Together with the shares held through Excelvantage Group Limited, Mr. Hu has 27.73% of our outstanding shares of common stock which could have a substantial impact on matters requiring the vote of our shareholders, including the election of our directors and most corporate actions. This control could delay, defer or prevent others from initiating a potential merger, takeover or other change in our control, even if these actions would benefit our other shareholders and the Company. This control could adversely affect the voting and other rights of our other shareholders and could depress the market price of our common stock.

We do not anticipate paying any cash dividends to our common shareholders.

We presently do not anticipate that we will pay dividends on any of our common stock in the foreseeable future. If payment of dividends does occur at some point in the future, it would be contingent upon our revenues and earnings, if any, capital requirements, and general financial condition. The payment of any common stock dividends will be within the discretion of our Board of Directors. We presently intend to retain all earnings to implement our business plan; accordingly, we do not anticipate the declaration of any dividends for common stock in the foreseeable future.

21

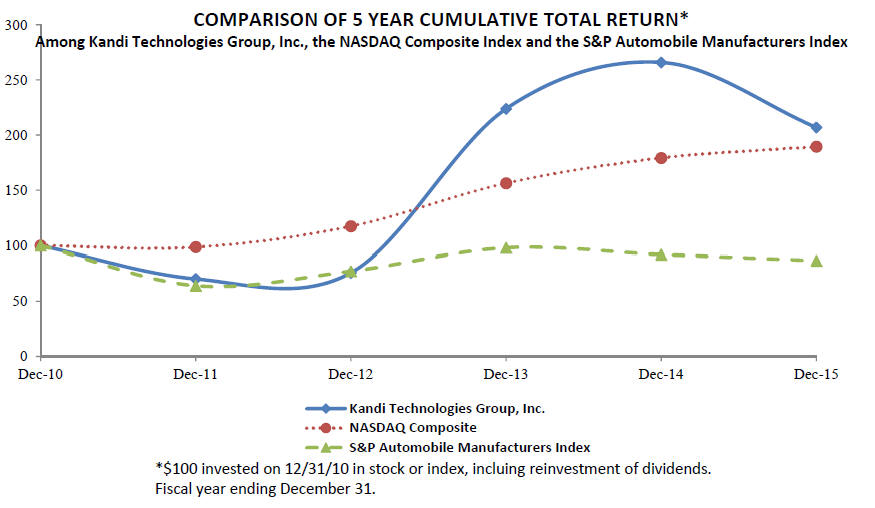

Fluctuation in the value of the RMB may have a material adverse effect on your investment.