united

states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

Investment Company Act file number 811-21720

Northern Lights Fund Trust

(Exact name of registrant as specified in charter)

225 Pictoria Drive, Suite 450, Cincinnati, Ohio 45246

(Address of principal executive offices) (Zip code)

Eric Kane, Ultimus Fund Solutions, LLC.

4221 North 203rd Street, Suite 100, Elkhorn, NE 68022

(Name and address of agent for service)

Registrant's telephone number, including area code: 631-470-2600

Date of fiscal year end: 12/31

Date of reporting period: 12/31/22

Item 1. Reports to Stockholders.

December 31, 2022

The Altegris Mutual Funds

A SERIES OF NORTHERN LIGHTS FUND TRUST

Annual Report

Altegris/AACA Opportunistic Real Estate Fund

Advised by:

Altegris Advisors, LLC

1200 Prospect, Suite 400

La Jolla, CA 92037

877.524.9441 | WWW.ALTEGRIS.COM

ALTEGRIS/AACA Opportunistic Real Estate Fund

January 1, 2021 – December 31, 2022

Fund Performance Summary

As shown in Figure 1, the Altegris/AACA Opportunistic Real Estate Fund’s (“Fund”) Class A (at NAV), Class C, Class I, and Class N shares delivered returns over the 12 months ended 12/31/2022 of -40.19%, -40.66%, -40.06%, and -40.20%, respectively. Meanwhile, the Dow Jones US Real Estate Total Return (TR) Index and S&P 500 Total Return (TR) Index returned -25.17% and - 18.11%, respectively. The Fund’s net assets under management totaled approximately $225 million as of December 31, 2022.

| Figure 1: Altegris/AACA Opportunistic Real Estate Fund Performance Review | ||||||

| January 1, 2022 – December 31, 2022 | ||||||

| 1-Year | Since Inc.* | Q4 2022 | Q3 2022 | Q2 2022 | Q1 2022 | |

| Class A (NAV) | -40.19% | 7.43% | -3.08% | -12.93% | -19.04% | -12.45% |

| Class A (max load)** | -43.62% | 6.90% | -8.67% | -17.93% | -23.69% | -17.47% |

| Class C (NAV) | -40.66% | -16.78% | -3.29% | -13.15% | -19.16% | -12.60% |

| Class I (NAV) | -40.06% | 7.62% | -3.05% | -12.87% | -19.01% | -12.38% |

| Class N (NAV) | -40.20% | 7.43% | -3.08% | -12.98% | -19.02% | -12.44% |

| Dow Jones US Real Estate TR Index | -25.17% | 7.25% | 4.44% | -10.41% | -14.46% | -6.50% |

| S&P 500 TR Index | -18.11% | 11.65% | 7.56% | -4.88% | -16.10% | -4.60% |

| * | The inception date of the Predecessor Fund was February 1, 2011. Past performance is not indicative of future results. Returns for periods longer than one year are annualized. The inception date of Class C shares was 12/1/2020. |

| ** | Class A’s maximum sales charge (load) is 5.75%. Class A Share investors may be eligible for a reduction in sales charges. |

The total annual fund operating expense ratio, gross of any fee waivers or expense reimbursements, is 2.17% for Class A, 2.92% for Class C, 1.91% for Class I, and 2.17% for Class N. The Adviser has contractually agreed to reduce its fees and/or absorb expenses of the Fund as described in the Fund Summary until at least October 31, 2023, to ensure that total Annual Fund operating expenses after fee waiver and/or expense reimbursement will not exceed 1.80%, 2.55%, 1.55%, and 1.80% of average daily net assets attributable to Class A, Class C, Class I, and Class N shares, respectively.

It is important to note that the Fund inherited the track record of its predecessor, the American Assets Real Estate Securities, L.P. (“Predecessor Fund”), which AACA managed, the Fund’s sub-adviser. The Predecessor Fund was not registered under the Investment Company Act of 1940. Since its inception on February 1, 2011, the Predecessor Fund was managed by AACA in the same style and pursuant to substantially identical real estate long-short strategies, investment goals, and guidelines as are presently being pursued on behalf of the Fund by AACA as its sub-adviser.

The performance quoted for periods prior to 1/9/2014 is that of the Predecessor Fund (while it was a limited partnership) and is net of applicable management fees, performance fees, and other actual expenses of the Predecessor Fund. From its inception on February 1, 2011, the Predecessor Fund was not subject to the same investment restrictions, diversification requirements, limitations on leverage, and other regulatory or Internal Revenue Code restrictions of the Fund, which might have adversely affected its performance. In addition, the Predecessor Fund was not subject to sales loads that apply to certain classes of Fund shares, which would have reduced returns.

1

The performance data quoted here represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance data quoted above. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original costs. A Fund’s performance, especially for very short periods, should not be the sole factor in making investment decisions. For performance information current to the most recent month-end, please call (888) 524-9441.

Effective September 8, 2016, the fund changed its name to the Altegris/AACA Opportunistic Real Estate Fund to align with the fund’s investment objectives more closely. The principal investment strategies and risks have not changed.

Fund Overview

The Altegris/AACA Opportunistic Real Estate Fund seeks to provide total return through long-term capital appreciation and current income by investing, both long and short, in equity securities of real estate and real estate-related companies. The Fund seeks to achieve its goals by accessing an experienced long/short real estate manager, American Assets Capital Advisers (AACA). AACA focuses on quality assets in “A” quality locations and believes that ownership of high-quality real estate creates the potential for durable inflation-hedged income over time. 1 From a fundamental standpoint, AACA believes real estate performs better over periods when it is more difficult to supply, demand is less cyclical, and tenants are reluctant to leave. Rather than mimicking exposures like an index, the Fund is heavily over-weighted in segments that share these four characteristics:

| ■ | Oligopoly or duopoly real estate structure |

| ■ | High barriers to entry for new owners/developers |

| ■ | High barriers to exit for tenants |

| ■ | Secular demand drivers underlying the user side of the business |

AACA believes the combination of these four characteristics (or some subset) creates a competitive landscape in which tenants have fewer options to move or play one building owner against another. In addition, AACA has found that properties with these characteristics command higher occupancy rates and better rents, which helps create more valuable portfolios for shareholders through enhanced dividends and higher real estate values.

Fund Performance

The Fund returned -40.19% during 2022, underperforming the Dow Jones US Real Estate Total Return Index’s (DJUSRET) return of -25.17% and the Morningstar Real Estate Category return of -25.67%. The Fund gave back much of its 2020 relative gains to DJUSRE during 2021 and 2022, despite maintaining its strategy of owning what we believe are long-term secular opportunities in oligopolistic real estate without “chasing cheap” or buying companies that had significant COVID-19 sell-offs. These companies subsequently rallied the most in the 2021 rebound. As a side note, we never “chase cheap” and have high conviction in our strategy’s long-term ability to generate returns above the benchmark and Morningstar category.

Performance Drivers

The primary drivers of performance in 2022 were domestic data centers, lab space, and (short) retail positions. Conversely, the most significant detractors were communications infrastructure, industrial, and international data centers positions.

| 1 | This assessment reflects the opinion and view of AACA based on their proprietary evaluation methods and is not based on any nationally recognized rating entity or real estate value standards. |

2

| Figure 2: Performance Attribution by Segment | January 1, 2022 – December 31, 2022 |

Performance attribution reflects a weight-adjusted allocation based on segment exposure to account for fees and an expense for Class A. Past performance is not indicative of future results.

The Fund’s top five attributors this year were: FTAI Aviation, IQHQ, Switch, FTAI Infrastructure, and Vornado (short).

| ■ | FTAI Aviation, Ltd (“FTAI”) | Infrastructure: FTAI Aviation provides an array of aviation products, including aircraft leasing, engine (CFM56) leasing, engine repair, and used serviceable material. FTAI recently split into aviation and infrastructure companies and elected C-Corp status, which we believe will enhance shareholder value. In addition, due to carbon regulations, airlines will have to replace, update, or repair engines, creating built-in demand for a core FTAI business segment. In contrast, the infrastructure segment will continue to see tailwinds from strong energy demand. |

| ■ | IQHQ, Inc. | Lab Space: IQHQ operates premier life science real estate, and it is rapidly expanding in 3 major markets: San Francisco, San Diego, and Boston. With the growing demand for life science assets and vaccine research, we have strong confidence in the company’s trajectory. |

| ■ | Switch, Inc. (“SWCH”) | Domestic Data Centers: SWCH owns and develops purpose-built high-tech data centers that boast more than 500 issued and pending patents on their data center designs which hold the highest reliability ratings in the industry. We consider the SWCH management team to be among the best globally. SWCH has been acquired by Digital Bridge (DBRG). |

| ■ | Fortress Transportation & Infrastructure Investors LLC (“FTAI”) | Infrastructure: FTAI owns infrastructure assets in the energy, intermodal, and rail sectors. They have three large-scale infrastructure projects - each unique with tremendous earnings potential. FTAI recently split into aviation and infrastructure companies and elected C-Corp status. We believe this restructuring will enhance shareholder value. Due to carbon regulations, airlines will have to replace, update, or |

3

repair engines, creating built-in demand for a core FTAI business segment. In addition, the infrastructure segment will continue to see tailwinds from strong energy demand.

| ■ | Vornado (Short) | Office: VNO is a REIT that primarily invests in office buildings and street retail in Manhattan with approximately 20 million rentable square feet. Like our other office sector investments, we believe that the work-from-home trend will continue to affect office and retail space in New York City negatively. |

This year, the portfolio’s top five detractors were WeWork, Digital Bridge, Caesars, GDS, and Drive Shack.

| ■ | WeWork, Inc. (“WE”) | Office: WE is a provider of shared working spaces (coworking), including physical and virtual shared spaces. Its portfolio spans 762 locations and 887K desks across six continents, headquartered in New York City. WE has recently transformed management, and we are excited about the company’s direction. But unfortunately, shares have gotten caught up in the negative sentiment on Softbank, unicorns in general, and office use if we hit a meaningful uptick in unemployment. We think a recession would add to demand. |

| ■ | Digital Bridge Group, Inc. (“DBRG”) | Communications Infrastructure: DBRG is a digital infrastructure investment firm built from the remnants of a REIT. For lack of a better comparison, they aim to be the ‘Blackstone for digital,’ which we think is a good idea. In addition, they recently bought Switch, Inc. in their investment management business with institutional capital. With that said, DBRG’s performance is puzzling to us. From personal interactions and interactions with other management teams at conferences, I know firsthand that DBRG CEO Marc Ganzi is deeply and widely respected by peers and colleagues. We suspect the company is somewhat of an orphan without an investor base. Further, it is not a REIT, and the “Blackstone for Digital” story has not taken hold yet. Notwithstanding this, we expect that, given their excellent management and asset-light, institutionally-funded model, their future returns on assets will exceed the REIT cohort. |

| ■ | Caesars Entertainment (“CZR”) | Gaming: CZR is a large regional gaming company that merged with Eldorado Resorts to create the largest and most diverse portfolio of gaming destinations across the U.S. The new entity boasts more than 50 resorts managed by Eldorado’s premier management team. Additionally, we believe the next frontier in gaming will be sports betting and iGaming, and CZR is in the pole position to capture a disproportionate share of this market. CZR is, in our opinion, perhaps the most underpriced company we own. |

| ■ | GDS Holdings, Ltd. (“GDS”) | Data Centers: GDS is a developer and operator of data centers in the People’s Republic of China (PRC). GDS operates as a private carrier and is cloud-neutral, enabling its customers to connect to all PRC’s telecommunications carriers and access several of the PRC’s cloud service providers, whom it hosts in its facilities. Despite the compelling digital revolution in China and Southeast Asia, we have since sold our entire position in CD and the entire Chinese data center sector, concluding that the international policy risk is too high for our tolerance. |

| ■ | DriveShack, Inc. (“DS”) | Golf: DS invests in and manages various golf properties, including traditional courses, driving venues, and putting/entertainment properties. In a surprise announcement in December 2022, management announced a delisting from the NYSE. Due to our illiquid position and 40 Act restraints, we were forced to sell our entire position. Fortunately, at the time of sale, DS represented a very small (~75bps) position in the portfolio. However, we are nonetheless disappointed in the lack of communication from the management team. The stock will trade OTC, and we will continue monitoring it. |

Portfolio Review

In 2022, the Federal Reserve raised interest rates at the fastest pace since Paul Volker’s term in the early 1980s, creating an ‘inverse cap rate compression.’ Typically, higher-quality sectors with scarcer supply and more secular demand sell at lower cap rates than sectors with less growth and demand and more supply. This is almost economics 101. For example, a portfolio of cell towers historically sells at a lower cap rate than a portfolio of dollar stores to reflect the disparity in NOI growth. This relationship is also observable in stock prices, as growth companies typically have higher multiples than value companies. However, this relationship broke when the recent cycle began in March 2022. Lower cap rate assets (cell towers and industrial, for instance) generally saw their cap rates increase by a greater amount than the increase in triple net lease and open-air retail cap rates, essentially a cap-rate curve flattening. So, lower-quality portfolios performed better than higher-quality portfolios in 2022. The flattening cap-rate environment also reflects competition from bonds from an asset allocation perspective. When the

4

U.S. 2-year Treasury Note yields 4.3%, it becomes a hurdle against which other yields are measured. We believe this trend will reverse in 2023 as inflation continues to recede and the Fed eases off the gas pedal.

Our investment approach primarily involves meeting with company management, touring assets, and gathering and analyzing other granular data. This approach was practical until November 2021, when macroeconomic uncertainty and the Fed’s ‘bull-in-a-china-shop’ approach to rate hikes became the dominant factors in market pricing. Increasingly, REITs are being priced like equities. Historically REIT correlation to equities and fixed income is typically 0.6 and 0.2, respectively. In 2022, REITs’ equity and fixed income correlations were 0.9 and 0.6, respectively.2 . We believe a recession is inevitable, but the real questions are when it will happen and how severe it will be. In my experience, stocks and REITs usually rally in anticipation of a Fed pivot and lower rates.

Thinking about 12-18 months forward, we view these as the most important market drivers:

| ■ | Macro: We think a recession is near, so we wait for the magnitude of government reaction. |

| ○ | What impact does this have on our outlook? The recent aggressive tightening cycle has driven cap rates from 4.6% on December 31, 2021, to 5.9% on December 31, 2022. We believe the ‘once the dust settles’ cap rate level is about 5%, which implies that REITs are currently at least 17% underpriced. 3 |

| ○ | In an alternative scenario where both CPI and rates remain elevated (like in the 1970s), rent growth may also increase, as it has tracked CPI closely in the past and helps real estate weather the effects of inflation. Higher CPI and rents may equate to higher NOI growth, drive higher forward-looking return expectations, and cause property values to hold or appreciate. For example, US REITs returned 76% during the two calendar years following the 1974 oil embargo, despite inflation running between 6-9%.4 |

| ■ | Home Mortgage. Post-pandemic housing price increases combined with the more recent Fed hiking cycle have combined to deal home price affordability a crushing one-two punch. The 30-year mortgage hit 6.7% as of 12/31/22. The (perhaps intended) spillover effect of these rate hikes will likely be a massive slowdown in new home sales and resales continuing into 2023. The housing business generally makes up 15-18% of US GDP, and there are likely layoffs and downsizing happening now. In addition, the 7% mortgage locks people into their existing homes, as homeowners cannot replace their homes at today’s rates. We believe home price affordability will limit the great migration to renters and retirees not needing mortgages and have positioned accordingly. |

| ■ | Inflation. Current data indicated that most of the components of CPI are falling. Some of these components, like rents, are particularly lagging. Spot market rents (call a landlord and ask) are rolling over and are now running at ~3% and lead the Fed’s calculation by about 8 months. As these data points filter in, the CPI number should decline. Longer term, there are global issues of trade and energy that suggest the benefits to inflation of globalization may turn from tailwind to headwind. |

| ■ | Private vs Public Real Estate Performance. As of the most recent print available, NCREIF reports a YTD performance of 9.35% (as of 9/30/2022), and Blackstone’s BREIT reported a return of 4.06% (as of 11/30/2022). Private real estate marks are difficult to make sense of when public real estate is down ~-25% YTD. Private real estate returns require appraisals and have committees that take a measured approach to the process. As a result, valuations are not as subject to market liquidity. Markdowns of private real estate would reduce the valuation gap between public and private real estate, but we do not think this is all that likely. The public/private discount story resonates loudly. |

| ■ | Migration. In our opinion, the US is undergoing one of the largest, if not the largest internal migration in history. In unprecedented numbers, the uncoupling of the workforce from the workplace has created a secular shift in our country, which we believe will continue indefinitely. While migration is not a new phenomenon, its scope and breadth over the last two years have exceeded expectations. For example, Californians moving to Texas increased by 19% in 2020 compared to 2019, according to a CBRE study. Nearly one-hundred thousand people migrated to Austin, TX, alone over 2019-2020, and experts predict another 182k over the 2021-2023 period. Taken together, this represents about 12.3% growth in aggregate or 3% per year, which is four times as fast as the national average of 0.8%. Additionally, almost all |

| 2 | Source: Bloomberg |

| 3 | See our recent white paper Exploring REITs Valuation – Is it Time to Buy for more detail on our forecasting process. |

| 4 | US REIT performance is FTSE NAREIT All Equity REITs Total Return Index. |

5

are highly paid white-collar or engineering/software types. I have never seen anything like this in my 40-year career. During the massive build of strip casinos 20 years ago, Las Vegas experienced a similar influx of lower-paid workers. We believe the demographics of the current migration will drive several knock-on effects due to the higher-paid nature of those involved.

Portfolio Positioning & Themes

We believe the best opportunity lies in short-duration leases in full assets with a structural possibility to capture top-line rental growth ‘equal-to-or-better-than’ inflation. Amongst that backdrop, we believe those assets with modest-to-low levels of on-site labor (limiting labor and potential energy spikes) in their operating model should produce robust NOI/FFO growth and outpace inflation. Core sectors include Single Family Rental (8.5% of the portfolio), Multi-Family Rental (4.9%), Self-Storage (7.1%), Manufactured Home Communities (7.1%), and Industrial/Specialized Ag (22.2%). In this section, we will dive deeper into sectors to share our thought process.

| ■ | Industrial. The industrial business has morphed since covid in some meaningful ways: Covid promoted e-commerce, infill land has become scarcer, retailers have rationalized their footprints and closed marginal locations, the supply chain broke, and industrial companies have begun focusing on warehouse space near the consumer. This has collectively led to very strong demand for industrial and limited supply, particularly in port-centric, coastal infill markets. Green Street Associates, a well-respected research shop dedicated to REITs, predicts rent growth nationally at 9.7% per year for the next five years. This national number includes non-coastal markets like Chicago, Phoenix, and Orlando, which have much lower barriers to entry, so this number is probably understated slightly. |

| ■ | Lab Space. Demand for wet lab space, already strong before COVID, has been off the charts since COVID. There is a heightened demand driver from big pharma and life science for research and a concerted national effort to ‘re-shore’ certain functions that had been offshored during the prior 30 years. Occupancy runs 95-99% in the three core markets of San Diego, South San Francisco, and Cambridge, and rents are predicted to grow 9% annually until at least 2025.5 The Fund’s largest lab space holding is IQHQ, Inc., a private company. We purchased this security in November 2019 at $15 per share and have seen the company expand from about 1 million square feet of development to a portfolio of 10 million feet today. More recently, IQHQ raised capital at a valuation of $28 per share, and we marked our position accordingly. The Fund’s other lab space position, Alexandra Real Estate Equities, Inc. (ARE), finished the quarter trading at a 30% discount to NAV. Based on the expected 2023 FFO of $8.95, the forward-looking price to FFO multiple was 16.7x.6 Comparing this to the 17.9x forward-looking multiple based on the 2018 average share price, for instance, one could view the current price as 35% more earnings (FFO) for ~14% less cost (price to FFO multiple). We continue to like this space. |

| ■ | Gaming. The portfolio’s gaming net exposure totaled 9.3% at quarter end, comprised of operators Ceasars Entertainment (CZR) and MGM Resorts International (MGM), and gaming REIT VICI Properties (VICI). We think leisure travel and group business will provide ongoing tailwinds for CZR and MGM, both of which have insurance against potential future downturns in their robust and growing iGaming and Online Sports Betting (OSB) businesses, in our opinion. CZR and MGM derive 100% and 85% of their revenues from the U.S., respectively, and we believe that CZR and MGM will benefit as more states legalize iGaming and OSB. These tailwinds, combined with the return of in-person M.I.C.E. (meetings, incentives, conventions, and expos), should create long-term growth visibility for Las Vegas. |

Valuation

| ■ | The portfolio’s growth forecast is still multiples of the asset class at large. The Fund has an underlying 2023 funds from operations (FFO) growth rate of 7.51%.7 In comparison, the RE sector has a growth rate of 2.90%.8,9 |

| 5 | Source: Green Street Advisors |

| 6 | Source: S&P Global |

| 7 | FFO Growth rate represents an AACA estimate using S&P Global data |

| 8 | Real Estate Sector Growth rate represented by the S&P Equity REIT Index |

| 9 | According to S&P Global |

6

| ■ | The portfolio’s valuation is very near that of the asset class at large. Aggregate Fund FFO is 16.1x 2023 FFO, while the MSCI US REIT Index trades at 16.6x 2023 FFO.10,11 |

| ■ | The portfolio is less levered than the aggregate leverage in the asset class. The S&P Equity REIT index carries an underlying leverage ratio of about 42.28%, while the Fund’s leverage ratio is 23.92%.12,13 |

Put simply, the Fund’s investments have significantly higher growth forecasts (per S&P Global) with about half the risk (or leverage, per S&P Global) while selling for a similar valuation (price/FFO multiple valuation). Current valuations seem unusually de-coupled from long-term prospects as global turmoil related to war, inflation, energy prices, and Fed rate hikes add uncertainty. Many stocks’ prices appear to have discounted a recession as well.

Outlook

We believe the portfolio is positioned in secular real estate growth opportunities that offer exposure to high-quality, same- store net operating income growth, resulting in potentially higher asset value cash flow and dividends. We have no exposure to sectors that, in our opinion, face significant structural headwinds, such as the retail sector. Further, we do not have exposure to other sectors with long-duration leases with an inability to capture inflation, which we believe would fare worse in the Fed tightening cycle. We believe these sectors depend on raising capital and buying new assets as their primary means of increasing earnings. These types of business plans typically underperform in rising-rate environments.

Many REITs have adjusted in price; more than 80% of the S&P REIT Index names traded at a discount to NAV on 12/31/2022. The average REIT traded at an 18% discount to NAV at year-end.

Our focus is on ownership of companies that own real estate where the tenant is denied choice. This is most prevalent when some subset (or all) of these characteristics is in place:

| 1) | the sub-sector of real estate is a monopoly, duopoly, or oligopoly; |

| 2) | there are high barriers to entry for new competitors; |

| 3) | there are high barriers to tenants leaving/exiting buildings; and |

| 4) | the basic underlying economics of the tenant’s business is healthy. |

We have found that when these four characteristics are present, companies in that space can potentially generate consistently higher same-store net operating income growth over long periods. Typically, sectors and companies that exhibit these characteristics comprise 65% to 80% of the portfolio.

Sincerely,

Burland

East, CFA

Chief Executive Officer

Sub-Adviser Portfolio Manager

American Assets Capital Advisers (AACA)

| 10 | Fund FFO is an AACA estimate using S&P Global data |

| 11 | S&P Global REIT Index FFO sourced from S&P Global |

| 12 | S&P Equity REIT Index sourced from S&P Global |

| 13 | Fund leverage is an AACA estimate using data from S&P Global |

7

INDEX DEFINITIONS

Dow Jones US Real Estate Total Return Index is the total return version of the Dow Jones US Real Estate Index and is calculated with gross dividends reinvested. The base date for the index is December 31, 1991, with a base value of 100.

S&P 500 Total Return Index is the total return version of the S&P 500 index. The S&P 500 index is unmanaged and is generally representative of certain portions of the US equity markets. For the S&P 500 Total Return Index, dividends are reinvested daily, and the base date for the index is January 4, 1988. All regular cash dividends are assumed reinvested in the S&P 500 index on the ex- date. Special cash dividends trigger a price adjustment in the price return index.

MSCI US REIT Index. The MSCI US REIT Index is a free float-adjusted market capitalization weighted index that is comprised of equity Real Estate Investment Trusts (REITs). The index is based on the MSCI USA Investable Market Index (IMI), its parent index, which captures the large, mid, and small cap segments of the USA market. With 129 constituents, it represents about 99% of the US REIT universe and securities are classified under the Equity REITs Industry (under the Real Estate Sector) according to the Global Industry Classification Standard (GICS®), have core real estate exposure (i.e., only selected Specialized REITs are eligible) and carry REIT tax status.

S&P Equity REIT Index. The S&P U.S. Equity All REIT Index is designed to measure the performance of all U.S.-domiciled equity real estate investment trusts (REITs) that own and manage income-producing real estate. These may include offices, residential buildings, industrial properties, healthcare-related properties, shopping centers, hotels/resorts, commercial forests, data centers, cell towers, other infrastructure properties, and properties with diversified ownership across two or more properties. Mortgage REITs are excluded.

GLOSSARY

Alpha. Alpha measures the non-systematic return, which cannot be attributed to the market. It shows the difference between a fund’s actual return and its expected return, given its level of systematic (or market) risk (as measured by beta). A positive alpha indicates that the fund has performed better than its beta would predict. Alpha is widely viewed as a measure of the value-added or lost by a fund manager.

Beta. Beta is a measure of volatility that reflects the tendency of a security’s returns and how it responds to swings in the markets. A beta of 1 indicates that the security’s price will move with the market. A beta of less than 1 means that the security will be less volatile than the market. A beta of greater than 1 indicates that the security’s price will be more volatile than the market.

Long. Buying an asset/security that gives partial ownership to the buyer of the position. Long positions profit from a price increase.

Short. Selling an asset/security that may have been borrowed from a third party with the intention of buying back at a later date. Short positions profit from a price decline. If a short position increases in price, covering the short position at a higher price may result in a loss.

5216-NLD-02142023

8

| Altegris/AACA Opportunistic Real Estate Fund |

| PORTFOLIO REVIEW (Unaudited) |

| December 31, 2022 |

The Fund’s performance figures* for the periods ended December 31, 2022, compared to its benchmarks:

| Annualized | ||||||

| Since Inception | Fund Inception | |||||

| One Year | Five Year | Ten Year | February 1, 2011 | December 1, 2020 | ||

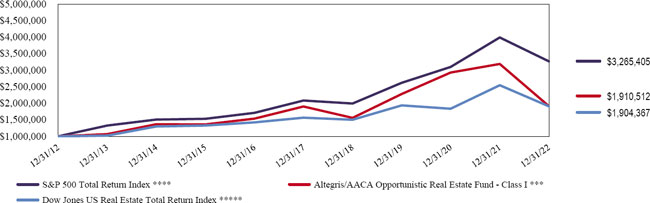

| Altegris/AACA Opportunistic Real Estate Fund - Class A ** | (40.19)% | (0.16)% | 6.46% | 7.43% | N/A | |

| Altegris/AACA Opportunistic Real Estate Fund - Class A with load ***** | (43.62)% | (1.34)% | 5.83% | 6.90% | N/A | |

| Altegris/AACA Opportunistic Real Estate Fund - Class C ** | (40.66)% | N/A | N/A | N/A | (16.78)% | |

| Altegris/AACA Opportunistic Real Estate Fund - Class I ** | (40.06)% | 0.09% | 6.69% | 7.62% | N/A | |

| Altegris/AACA Opportunistic Real Estate Fund - Class N ** | (40.20)% | (0.15)% | 6.47% | 7.43% | N/A | |

| S&P 500 Total Return Index **** | (18.11)% | 9.42% | 12.56% | 11.65% | 3.87% | |

| Dow Jones US Real Estate Total Return Index ***** | (25.17)% | 4.04% | 6.65% | 7.25% | 2.58% | |

| * | The performance data quoted is historical. Past performance is no guarantee of future results. Current performance may be higher or lower than the performance data quoted. The principal value and return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemptions of Fund shares. The Fund’s estimated total operating expense ratios before waiver, per the Fund’s prospectus dated May 1, 2022, are 2.17%, 2.92%, 1.92%, and 2.17% for Class A, Class C, Class I, and Class N shares, respectively. Class A shares are subject to a maximum sales charge of 5.75% imposed on purchases. Class A shares may be subject to a contingent deferred sales charge of up to 1.00% imposed on certain redemptions. All share classes are subject to a redemption fee of 1.00% of the amount redeemed if sold within 30 days of purchase. For performance information current to the most recent month-end, please call 1-888-524- 9441. |

| ** | The prior annual returns and performance track record that follows the Fund inception for Class A, N and I is that of the Predecessor Fund, American Asset Real Estate Securities Fund, L.P., which was managed by American Assets Investment Management, LLC, an affiliate and predecessor firm of AACA. The method used to calculate the Predecessor Fund’s performance differs from the Securities and Exchange Commission’s (“SEC”) standardized method of calculating performance because the Predecessor Fund employed monthly, rather than daily, valuation and this may produce different results. American Asset Real Estate Securities Fund, L.P. was not subject to certain investment restrictions, diversification requirements, limitations on leverage and other restrictions of the Investment Company Act of 1940 and of the Internal Revenue Code of 1986, as amended (“Code”), which if they had been applicable, might have adversely affected its performance. |

| *** | Class A with load total return is calculated using the maximum sales charge of 5.75%. |

| **** | The S&P 500 Total Return Index is an unmanaged composite of 500 large capitalization companies and includes the reinvestment of dividends. This index is widely used by professional investors as a performance benchmark for large-cap stocks. Investors cannot invest directly in an index. |

| ***** | The Dow Jones US Real Estate Total Return Index is an unmanaged index considered to be representative of REITS and other companies that invest directly or indirectly in real estate, and reflects no deductions for fees, expenses or taxes. Investors cannot invest directly in an index. |

Comparison of the Change in Value of a $1,000,000 Investment | December 31, 2012– December 31, 2022

Past performance is not necessary indicative of future results.

| Top Ten Holdings by Industry as of December 31, 2022 | % of Net Assets | |||

| Residential REIT | 20.5 | % | ||

| Industrial REIT | 18.5 | % | ||

| Infrastructure REIT | 14.3 | % | ||

| Health Care REIT | 11.8 | % | ||

| Data Center REIT | 7.9 | % | ||

| Self-Storage REIT | 7.1 | % | ||

| Leisure Facilities & Services | 6.7 | % | ||

| Office REIT | 5.0 | % | ||

| Telecommunications | 4.2 | % | ||

| Other Industries | 18.8 | % | ||

| Other Assets less Liabilities - Net | (9.6 | )% | ||

| Securities Sold Short | (5.2 | )% | ||

| 100.0 | % | |||

Please refer to the Schedule of Investments in this report for a detailed listing of the Fund’s holdings.

9

| ALTEGRIS/AACA OPPORTUNISTIC REAL ESTATE FUND |

| SCHEDULE OF INVESTMENTS |

| December 31, 2022 |

| Shares | Fair Value | |||||||

| COMMON STOCKS — 114.1% | ||||||||

| ASSET MANAGEMENT - 2.1% | ||||||||

| 1,560,439 | FTAI Infrastructure, LLC | $ | 4,603,295 | |||||

| DATA CENTER REIT - 7.9% | ||||||||

| 66,984 | Digital Realty Trust, Inc. | 6,716,486 | ||||||

| 16,815 | Equinix, Inc. | 11,014,329 | ||||||

| 17,730,815 | ||||||||

| FOOD - 1.2% | ||||||||

| 1,085,216 | Cadiz, Inc.(a) | 2,713,040 | ||||||

| GAMING REIT - 2.6% | ||||||||

| 176,452 | VICI Properties, Inc. | 5,717,045 | ||||||

| HEALTH CARE REIT - 11.8% | ||||||||

| 111,892 | Healthpeak Properties, Inc. | 2,805,132 | ||||||

| 890,864 | IQHQ Private Investment, Inc. 144A(a),(b),(c),(d) | 23,584,912 | ||||||

| 26,390,044 | ||||||||

| INDUSTRIAL REIT - 18.5% | ||||||||

| 51,289 | Innovative Industrial Properties, Inc. | 5,198,140 | ||||||

| 138,031 | Prologis, Inc. | 15,560,235 | ||||||

| 254,219 | Rexford Industrial Realty, Inc. | 13,890,526 | ||||||

| 118,264 | Terreno Realty Corporation | 6,725,674 | ||||||

| 41,374,575 | ||||||||

| INFRASTRUCTURE REIT - 14.3% | ||||||||

| 58,645 | American Tower Corporation | 12,424,530 | ||||||

| 73,878 | Crown Castle, Inc. | 10,020,812 | ||||||

| 34,381 | SBA Communications Corporation, A | 9,637,338 | ||||||

| 32,082,680 | ||||||||

| INTERNET MEDIA & SERVICES - 2.4% | ||||||||

| 62,642 | Airbnb, Inc., CLASS A(a) | 5,355,891 | ||||||

| LEISURE FACILITIES & SERVICES - 6.7% | ||||||||

| 179,466 | Caesars Entertainment, Inc.(a) | 7,465,786 | ||||||

| 226,991 | MGM Resorts International | 7,611,008 | ||||||

| 15,076,794 | ||||||||

See accompanying notes to financial statements.

10

| ALTEGRIS/AACA OPPORTUNISTIC REAL ESTATE FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| December 31, 2022 |

| Shares | Fair Value | |||||||

| COMMON STOCKS — 114.1% (Continued) | ||||||||

| OFFICE REIT - 5.0% | ||||||||

| 76,477 | Alexandria Real Estate Equities, Inc. | $ | 11,140,405 | |||||

| REAL ESTATE OWNERS & DEVELOPERS - 2.1% | ||||||||

| 3,280,619 | WeWork, Inc.(a) | 4,691,285 | ||||||

| RESIDENTIAL REIT - 20.5% | ||||||||

| 339,360 | American Homes 4 Rent, Class A | 10,228,311 | ||||||

| 22,535 | AvalonBay Communities, Inc. | 3,639,853 | ||||||

| 21,741 | Camden Property Trust | 2,432,383 | ||||||

| 69,574 | Equity LifeStyle Properties, Inc. | 4,494,480 | ||||||

| 301,668 | Invitation Homes, Inc. | 8,941,440 | ||||||

| 15,389 | Mid-America Apartment Communities, Inc. | 2,415,919 | ||||||

| 79,480 | Sun Communities, Inc. | 11,365,640 | ||||||

| 62,356 | UDR, Inc. | 2,415,048 | ||||||

| 45,933,074 | ||||||||

| SELF-STORAGE REIT - 7.1% | ||||||||

| 30,911 | Extra Space Storage, Inc. | 4,549,481 | ||||||

| 68,774 | Life Storage, Inc. | 6,774,239 | ||||||

| 126,187 | National Storage Affiliates Trust | 4,557,874 | ||||||

| 15,881,594 | ||||||||

| SPECIALTY FINANCE - 3.9% | ||||||||

| 502,559 | FTAI Aviation Ltd. | 8,603,810 | ||||||

| SPECIALTY REIT - 3.8% | ||||||||

| 531,456 | NewLake Capital Partners, Inc. | 8,513,925 | ||||||

| TELECOMMUNICATIONS - 4.2% | ||||||||

| 896,908 | DigitalBridge Group, Inc. | 9,812,174 | ||||||

| TOTAL COMMON STOCKS (Cost $317,617,878) | 255,620,446 | |||||||

See accompanying notes to financial statements.

11

| ALTEGRIS/AACA OPPORTUNISTIC REAL ESTATE FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| December 31, 2022 |

| Coupon Rate | ||||||||||||

| Shares | (%) | Maturity | Fair Value | |||||||||

| PREFERRED STOCKS — 0.7% (Continued) | ||||||||||||

| SPECIALTY FINANCE — 0.2% | ||||||||||||

| 20,000 | FTAI Aviation Ltd. | 8.0000 | Perpetual | $ | 383,000 | |||||||

| TELECOMMUNICATIONS — 0.5% | ||||||||||||

| 19,918 | DigitalBridge Group, Inc. | 7.1250 | Perpetual | 373,861 | ||||||||

| 25,000 | DigitalBridge Group, Inc. - Series I | 7.1500 | Perpetual | 469,000 | ||||||||

| 13,735 | DigitalBridge Group, Inc. - Series H | 7.1250 | Perpetual | 259,590 | ||||||||

| 1,102,451 | ||||||||||||

| TOTAL PREFERRED STOCKS (Cost $1,719,964) | 1,485,451 | |||||||||||

| TOTAL INVESTMENTS - 114.8% (Cost $319,337,842) | $ | 257,105,897 | ||||||||||

| LIABILITIES IN EXCESS OF OTHER ASSETS - (14.8)% | (33,161,990 | ) | ||||||||||

| NET ASSETS - 100.0% | $ | 223,943,907 | ||||||||||

| LLC | - Limited Liability Company |

| LTD | - Limited Company |

| REIT | - Real Estate Investment Trust |

| (a) | Non-income producing security. |

| (b) | Security exempt from registration under Rule 144A or Section 4(2) of the Securities Act of 1933. The security may be resold in transactions exempt from registration, normally to qualified institutional buyers. As of December 31, 2022 the total market value of 144A securities is 23,584,912 or 10.5% of net assets. |

| (c) | Illiquid security. The total fair value of these securities as of December 31, 2022 was $23,584,912, representing 10.40% of net assets. |

| (d) | Fair Value was determined using significant unobservable inputs. |

12

| ALTEGRIS/AACA OPPORTUNISTIC REAL ESTATE FUND |

| SCHEDULE OF SECURITIES SOLD SHORT |

| December 31, 2022 |

| Shares | Fair Value | |||||||

| COMMON STOCKS — (5.2)% | ||||||||

| INSURANCE - (2.3)% | ||||||||

| (260,971 | ) | Radian Group, Inc. | $ | (4,976,717 | ) | |||

| MULTI ASSET CLASS REIT - (1.0)% | ||||||||

| (110,405 | ) | Vornado Realty Trust | (2,297,528 | ) | ||||

| OFFICE REIT - (1.9)% | ||||||||

| (447,917 | ) | Empire State Realty Trust, Inc., Class A | (3,018,961 | ) | ||||

| (38,127 | ) | SL Green Realty Corporation | (1,285,642 | ) | ||||

| (4,304,603 | ) | |||||||

| TOTAL SECURITIES SOLD SHORT - (Proceeds - $12,146,323) | $ | (11,578,848 | ) | |||||

See accompanying notes to financial statements.

13

| Altegris/AACA Opportunistic Real Estate Fund |

| Statement of Assets and Liabilities |

| December 31, 2022 |

| Altegris/AACA | ||||

| Opportunistic Real | ||||

| Estate Fund | ||||

| ASSETS | ||||

| Investment in securities, at cost | $ | 319,337,842 | ||

| Investment in securities, at value | $ | 257,105,897 | ||

| Cash and cash equivalents | 5,620,989 | |||

| Receivable for securities sold | 5,188,599 | |||

| Receivable for Fund shares sold | 231,008 | |||

| Dividends and interest receivable | 1,452,106 | |||

| Prepaid expenses and other assets | 56,802 | |||

| TOTAL ASSETS | 269,655,401 | |||

| LIABILITIES | ||||

| Securities sold short, at value (proceeds $12,146,323) | 11,578,848 | |||

| Due to custodian | 32,630,812 | |||

| Payable for Fund shares redeemed | 1,023,840 | |||

| Investment advisory fees payable | 225,390 | |||

| Dividends payable on securities sold short | 94,628 | |||

| Payable to Related Parties | 30,311 | |||

| Distribution fees (12b-1) payable | 5,287 | |||

| Accrued expenses and other liabilities | 122,378 | |||

| TOTAL LIABILITIES | 45,711,494 | |||

| NET ASSETS | $ | 223,943,907 | ||

| Net Assets Consist Of: | ||||

| Paid-in capital | $ | 342,882,138 | ||

| Accumulated Loss | (118,938,231 | ) | ||

| NET ASSETS | $ | 223,943,907 | ||

| NET ASSET VALUE PER SHARE: | ||||

| Class A Shares: | ||||

| Net Assets | $ | 4,682,582 | ||

| Shares of beneficial interest outstanding [$0 par value, unlimited shares authorized] | 411,439 | |||

| Net asset value (Net Assets ÷ Shares Outstanding) and redemption price per share (a,b) | $ | 11.38 | ||

| Maximum offering price per share (net asset value plus maximum sales charge of 5.75%) (c) | $ | 12.07 | ||

| Class C Shares: | ||||

| Net Assets | $ | 205,993 | ||

| Shares of beneficial interest outstanding [$0 par value, unlimited shares authorized] | 18,402 | |||

| Net asset value (Net Assets ÷ Shares Outstanding), offering price and redemption price per share (b) | $ | 11.19 | ||

| Class I Shares: | ||||

| Net Assets | $ | 203,502,387 | ||

| Shares of beneficial interest outstanding [$0 par value, unlimited shares authorized] | 17,659,019 | |||

| Net asset value (Net Assets ÷ Shares Outstanding), offering price and redemption price per share (b) | $ | 11.52 | ||

| Class N Shares: | ||||

| Net Assets | $ | 15,552,945 | ||

| Shares of beneficial interest outstanding [$0 par value, unlimited shares authorized] | 1,365,052 | |||

| Net asset value (Net Assets ÷ Shares Outstanding), offering price and redemption price per share (b) | $ | 11.39 | ||

| (a) | Investments in Class A shares made at or above the $1 million breakpoint are not subject to an initial sales charge and may be subject to a 1.00% contingent deferred sales charge (“CDSC”) on shares redeemed less than 18 months after the date of purchase (excluding shares purchases with reinvested dividends and/or distributions). |

| (b) | Shares redeemed within 12 months after purchase will be charged a contingent deferred sales charge (“CDSC”) of up to 1.00%. |

| (c) | On investments of $25,000 or more, the sales load is reduced. |

See accompanying notes to financial statements.

14

| Altegris/AACA Opportunistic Real Estate Fund |

| Statement of Operations |

| For the Year Ended December 31, 2022 |

| INVESTMENT INCOME | ||||

| Dividends (Tax Withholding $9,811) | $ | 8,749,484 | ||

| TOTAL INVESTMENT INCOME | 8,749,484 | |||

| EXPENSES | ||||

| Investment advisory fees | 5,716,184 | |||

| Interest expense | 1,752,614 | |||

| Short sale dividend expense | 1,022,970 | |||

| Distribution (12b-1) fees: | ||||

| Class A | 35,096 | |||

| Class N | 67,340 | |||

| Class C | 1,521 | |||

| Third party administrative services fees | 323,065 | |||

| Administrative services fees | 314,683 | |||

| Registration fees | 140,636 | |||

| Transfer agent fees | 95,201 | |||

| Custodian fees | 54,043 | |||

| Accounting services fees | 45,112 | |||

| Printing | 34,518 | |||

| Professional fees | 41,001 | |||

| Audit fees | 28,178 | |||

| Trustees fees and expenses | 13,890 | |||

| Legal fees | 6,121 | |||

| Insurance expense | 10,757 | |||

| Other expenses | 17,066 | |||

| TOTAL EXPENSES | 9,719,996 | |||

| Less: Fees waived by the Advisor | (44,986 | ) | ||

| NET EXPENSES | 9,675,010 | |||

| NET INVESTMENT INCOME | (925,526 | ) | ||

| REALIZED AND UNREALIZED GAIN/(LOSS) ON INVESTMENTS, OPTIONS AND SECURITIES | ||||

| SOLD SHORT | ||||

| Net realized gain/(loss) from: | ||||

| Investments | (66,939,866 | ) | ||

| Written options | 231,866 | |||

| Securities sold short | 10,104,113 | |||

| (56,603,887 | ) | |||

| Net change in unrealized depreciation from: | ||||

| Investments | (183,773,227 | ) | ||

| Securities sold short | (2,812,133 | ) | ||

| (186,585,360 | ) | |||

| REALIZED AND UNREALIZED LOSS ON INVESTMENTS, OPTIONS AND SECURITIES SOLD SHORT | (243,189,247 | ) | ||

| NET DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | (244,114,773 | ) | |

See accompanying notes to financial statements.

15

| Altegris/AACA Opportunistic Real Estate Fund |

| STATEMENTS OF CHANGES IN NET ASSETS |

| For the Year Ended | For the Year Ended | |||||||

| December 31, | December 31, | |||||||

| 2022 | 2021 | |||||||

| FROM OPERATIONS | ||||||||

| Net investment income/(loss) | $ | (925,526 | ) | $ | (3,214,131 | ) | ||

| Net realized gain/(loss) from investments, options written and securities sold short | (56,603,887 | ) | 96,476,857 | |||||

| Net change in unrealized depreciation on investments, options written and securities sold short | (186,585,360 | ) | (41,057,985 | ) | ||||

| Net increase/(decrease) in net assets resulting from operations | (244,114,773 | ) | 52,204,741 | |||||

| DISTRIBUTIONS TO SHAREHOLDERS | ||||||||

| Total Distributions Paid: | ||||||||

| Class A | (402,670 | ) | (3,040,217 | ) | ||||

| Class C | (13,507 | ) | (9,677 | ) | ||||

| Class I | (15,573,916 | ) | (74,625,994 | ) | ||||

| Class N | (1,233,573 | ) | (4,683,251 | ) | ||||

| Net decrease in net assets from distributions to shareholders | (17,223,666 | ) | (82,359,139 | ) | ||||

| FROM CAPITAL SHARE TRANSACTIONS | ||||||||

| Proceeds from shares sold: | ||||||||

| Class A | 3,771,258 | 12,248,021 | ||||||

| Class C | 221,710 | 110,118 | ||||||

| Class I | 127,649,973 | 182,550,451 | ||||||

| Class N | 4,327,833 | 14,691,533 | ||||||

| Net asset value of shares issued in reinvestment of distributions: | ||||||||

| Class A | 345,184 | 2,837,321 | ||||||

| Class C | 13,507 | 9,677 | ||||||

| Class I | 10,996,664 | 56,769,993 | ||||||

| Class N | 1,218,028 | 4,574,220 | ||||||

| Payments for shares redeemed: | ||||||||

| Class A | (16,473,376 | ) | (13,671,450 | ) | ||||

| Class C | (24,601 | ) | (28,397 | ) | ||||

| Class I | (319,465,581 | ) | (109,239,984 | ) | ||||

| Class N | (13,891,232 | ) | (15,857,886 | ) | ||||

| Redemption fee proceeds: | ||||||||

| Class A | 13 | 310 | ||||||

| Class C | — | — | ||||||

| Class I | 4,141 | 2,264 | ||||||

| Class N | 492 | 3,075 | ||||||

| Net increase/(decrease) in net assets from capital share transactions | (201,305,987 | ) | 134,999,266 | |||||

| TOTAL INCREASE/(DECREASE) IN NET ASSETS | (462,644,426 | ) | 104,844,868 | |||||

| NET ASSETS | ||||||||

| Beginning of Year | 686,588,333 | 581,743,465 | ||||||

| End of Year | $ | 223,943,907 | $ | 686,588,333 | ||||

See accompanying notes to financial statements.

16

| Altegris/AACA Opportunistic Real Estate Fund |

| STATEMENTS OF CHANGES IN NET ASSETS (Continued) |

| For the Year Ended | For the Year Ended | |||||||

| December 31, | December 31, | |||||||

| 2022 | 2021 | |||||||

| CAPITAL SHARE ACTIVITY | ||||||||

| Class A | ||||||||

| Shares Sold | 227,565 | 548,881 | ||||||

| Shares Reinvested | 28,155 | 149,964 | ||||||

| Shares Redeemed | (1,080,435 | ) | (625,098 | ) | ||||

| Net increase/(decrease) in shares outstanding | (824,715 | ) | 73,747 | |||||

| Class C | ||||||||

| Shares Sold | 14,920 | 4,932 | ||||||

| Shares Reinvested | 1,120 | 516 | ||||||

| Shares Redeemed | (1,791 | ) | (1,296 | ) | ||||

| Net increase in shares outstanding | 14,249 | 4,152 | ||||||

| Class I | ||||||||

| Shares Sold | 8,486,957 | 8,106,581 | ||||||

| Shares Reinvested | 886,113 | 2,973,808 | ||||||

| Shares Redeemed | (21,891,390 | ) | (4,998,285 | ) | ||||

| Net increase/decrease in shares outstanding | (12,518,320 | ) | 6,082,104 | |||||

| Class N | ||||||||

| Shares Sold | 274,816 | 664,208 | ||||||

| Shares Reinvested | 99,269 | 241,511 | ||||||

| Shares Redeemed | (968,303 | ) | (703,455 | ) | ||||

| Net increase/(decrease) in shares outstanding | (594,218 | ) | 202,264 | |||||

See accompanying notes to financial statements.

17

| Altegris/AACA Opportunistic Real Estate Fund |

| FINANCIAL HIGHLIGHTS |

Per Share Data and Ratios for a Share of Beneficial Interest Outstanding Throughout Each Year

| Class A | ||||||||||||||||||||

| Year Ended | Year Ended | Year Ended | Year Ended | Year Ended | ||||||||||||||||

| December 31, | December 31, | December 31, | December 31, | December 31, | ||||||||||||||||

| 2022 | 2021 | 2020 | 2019 | 2018 | ||||||||||||||||

| Net asset value, beginning of year | $ | 20.40 | $ | 21.43 | $ | 17.97 | $ | 12.57 | $ | 16.02 | ||||||||||

| Income/(loss) from investment operations: | ||||||||||||||||||||

| Net investment income/(loss) (1) | (0.08 | ) | (0.16 | ) | 0.00 | 0.09 | 0.04 | |||||||||||||

| Net realized and unrealized gain/(loss) on investments | (8.05 | ) | 1.79 | 5.04 | 5.68 | (2.98 | ) | |||||||||||||

| Total income/(loss) from investment operations | (8.13 | ) | 1.63 | 5.04 | 5.77 | (2.94 | ) | |||||||||||||

| Less distributions from: | ||||||||||||||||||||

| Net investment income | — | — | (0.09 | ) | (0.06 | ) | — | |||||||||||||

| Net realized gains | (0.89 | ) | (2.66 | ) | (1.49 | ) | (0.31 | ) | (0.51 | ) | ||||||||||

| Total distributions | (0.89 | ) | (2.66 | ) | (1.58 | ) | (0.37 | ) | (0.51 | ) | ||||||||||

| Redemption fees collected (2) | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |||||||||||||||

| Net asset value, end of year | $ | 11.38 | $ | 20.40 | $ | 21.43 | $ | 17.97 | $ | 12.57 | ||||||||||

| Total return (3,4) | (40.19 | )% | 8.58 | % | 28.16 | % | 46.00 | % | (18.40 | )% | ||||||||||

| Net assets, at end of year (000s) | $ | 4,683 | $ | 25,215 | $ | 24,905 | $ | 15,191 | $ | 16,066 | ||||||||||

| Ratios/Supplemental Data: | ||||||||||||||||||||

| Ratios to average net assets (including securities sold short and interest expense): | ||||||||||||||||||||

| Expenses, before waiver and reimbursement (6,8) | 2.44 | % | 2.17 | % | 2.23 | % | 2.30 | % | 2.97 | % | ||||||||||

| Expenses, after waiver and reimbursement (6,8) | 2.43 | % (5) | 2.17 | % (5) | 2.22 | % | 2.30 | % | 3.04 | % | ||||||||||

| Ratio of net investment income to average net assets (7) | (0.48 | )% | (0.72 | )% | 0.01 | % | 0.55 | % | 0.26 | % | ||||||||||

| Portfolio Turnover Rate | 42 | % | 63 | % | 61 | % | 36 | % | 36 | % | ||||||||||

| (1) | Per share amounts calculated using the average shares method, which more appropriately presents the per share data for the year. |

| (2) | Represents less than $0.01 per share. |

| (3) | Total returns shown exclude the effect of applicable sales charges and redemption fees and assumes reinvestment of all distributions. |

| (4) | Includes adjustments in accordance with accounting principles generally accepted in the United States and consequently the net asset value for financial reporting purposes and the returns based upon those net asset values may differ from the net asset values and returns for shareholder transactions. |

| (5) | Represents the ratio of expenses to average net assets absent fee waivers and/or expense reimbursements by the advisor. |

| (6) | The ratios of expenses and net investment income/(loss) to average net assets do not reflect the Fund’s proportionate share of income and expenses of underlying investment companies or REITs in which the Fund invests. |

| (7) | Recognition of net investment income by the Fund is affected by the timing of the declaration of dividends by the underlying investment companies in which the Fund invests. |

| (8) | Ratios to average net assets (excluding securities sold short and interest expense): |

| Expenses, before waiver and reimbursement | 1.81 | % | 1.80 | % | 1.81 | % | 1.78 | % | 1.67 | % | ||||||||||

| Expenses, after waiver and reimbursement | 1.80 | % | 1.80 | % | 1.80 | % | 1.78 | % | 1.73 | % |

See accompanying notes to financial statements.

18

| Altegris/AACA Opportunistic Real Estate Fund |

| FINANCIAL HIGHLIGHTS |

Per Share Data and Ratios for a Share of Beneficial Interest Outstanding Throughout Each Year/Period

| Class C | ||||||||||||

| Year Ended | Year Ended | Period Ended | ||||||||||

| December 31, | December 31, | December 31, | ||||||||||

| 2022 | 2021 | 2020 * | ||||||||||

| Net asset value, beginning of year/period | $ | 20.24 | $ | 21.43 | $ | 21.56 | ||||||

| Income/(loss) from investment operations: | ||||||||||||

| Net investment income/(loss) (1) | (0.11 | ) | (0.25 | ) | 0.00 | (2) | ||||||

| Net realized and unrealized gain on investments | (8.05 | ) | 1.72 | 1.40 | ||||||||

| Total income from investment operations | (8.16 | ) | 1.47 | 1.40 | ||||||||

| Less distributions from: | ||||||||||||

| Net investment income | — | — | (0.04 | ) | ||||||||

| Net realized gains | (0.89 | ) | (2.66 | ) | (1.49 | ) | ||||||

| Total distributions | (0.89 | ) | (2.66 | ) | (1.53 | ) | ||||||

| Redemption fees collected (2) | 0.00 | 0.00 | 0.00 | |||||||||

| Net asset value, end of year/period | $ | 11.19 | $ | 20.24 | $ | 21.43 | ||||||

| Total return (3,5) | (40.66 | )% | 7.83 | % | 6.61 | % (4) | ||||||

| Net assets, at end of year/period (000s) | $ | 206 | $ | 84 | $ | 0 | (6) | |||||

| Ratios/Supplemental Data: | ||||||||||||

| Ratios to average net assets (including securities sold short and interest expense): | ||||||||||||

| Expenses, before waiver and reimbursement (7,8,11) | 3.19 | % | 2.92 | % | 2.98 | % (10) | ||||||

| Expenses, after waiver and reimbursement (7,8,11) | 3.18 | % (7) | 2.92 | % (7) | 2.97 | % (10) | ||||||

| Ratio of net investment income to average net assets (9) | (0.77 | )% | (1.14 | )% | 0.19 | % (10) | ||||||

| Portfolio Turnover Rate | 42 | % | 63 | % | 61 | % (4) | ||||||

| * | Class C commenced operations on December 1, 2020 |

| (1) | Per share amounts calculated using the average shares method, which more appropriately presents the per share data for the year/period. |

| (2) | Represents less than $0.01 per share. |

| (3) | Total returns shown exclude the effect of applicable sales charges and redemption fees and assumes reinvestment of all distributions. |

| (4) | Not annualized. |

| (5) | Includes adjustments in accordance with accounting principles generally accepted in the United States and consequently the net asset value for financial reporting purposes and the returns based upon those net asset values may differ from the net asset values and returns for shareholder transactions. |

| (6) | Amount less than 1,000. |

| (7) | Represents the ratio of expenses to average net assets absent fee waivers and/or expense reimbursements by the advisor. |

| (8) | The ratios of expenses and net investment income (loss) to average net assets do not reflect the Fund’s proportionate share of income and expenses of underlying investment companies or REITs in which the Fund invests. |

| (9) | Recognition of net investment income by the Fund is affected by the timing of the declaration of dividends by the underlying investment companies in which the Fund invests. |

| (10) | Annualized. |

| (11) | Ratios to average net assets (excluding securities sold short and interest expense): |

| Expenses, before waiver and reimbursement | 2.56 | % | 2.55 | % | 2.56 | % | ||||||

| Expenses, after waiver and reimbursement | 2.55 | % | 2.55 | % | 2.55 | % |

See accompanying notes to financial statements.

19

| Altegris/AACA Opportunistic Real Estate Fund |

| FINANCIAL HIGHLIGHTS |

Per Share Data and Ratios for a Share of Beneficial Interest Outstanding Throughout Each Year

| Class I | ||||||||||||||||||||

| Year Ended | Year Ended | Year Ended | Year Ended | Year Ended | ||||||||||||||||

| December 31, | December 31, | December 31, | December 31, | December 31, | ||||||||||||||||

| 2022 | 2021 | 2020 | 2019 | 2018 | ||||||||||||||||

| Net asset value, beginning of year | $ | 20.59 | $ | 21.55 | $ | 18.08 | $ | 12.64 | $ | 16.05 | ||||||||||

| Income/(loss) from investment operations: | ||||||||||||||||||||

| Net investment income/(loss) (1) | (0.03 | ) | (0.10 | ) | 0.05 | 0.14 | 0.09 | |||||||||||||

| Net realized and unrealized gain/(loss) on investments | (8.15 | ) | 1.80 | 5.06 | 5.70 | (2.99 | ) | |||||||||||||

| Total income/(loss) from investment operations | (8.18 | ) | 1.70 | 5.11 | 5.84 | (2.90 | ) | |||||||||||||

| Less distributions from: | ||||||||||||||||||||

| Net investment income | — | — | (0.15 | ) | (0.09 | ) | — | |||||||||||||

| Net realized gains | (0.89 | ) | (2.66 | ) | (1.49 | ) | (0.31 | ) | (0.51 | ) | ||||||||||

| Total distributions | (0.89 | ) | (2.66 | ) | (1.64 | ) | (0.40 | ) | (0.51 | ) | ||||||||||

| Redemption fees collected (2) | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |||||||||||||||

| Net asset value, end of year | $ | 11.52 | $ | 20.59 | $ | 21.55 | $ | 18.08 | $ | 12.64 | ||||||||||

| Total return (3,4) | (40.06 | )% | 8.86 | % | 28.45 | % | 46.34 | % | (18.11 | )% | ||||||||||

| Net assets, at end of year (000s) | $ | 203,502 | $ | 621,281 | $ | 519,163 | $ | 329,530 | $ | 225,944 | ||||||||||

| Ratios/Supplemental Data: | ||||||||||||||||||||

| Ratios to average net assets (including securities sold short and interest expense): | ||||||||||||||||||||

| Expenses, before waiver and reimbursement (6,8) | 2.19 | % | 1.92 | % | 1.99 | % | 2.02 | % | 2.73 | % | ||||||||||

| Expenses, after waiver and reimbursement (6,8) | 2.18 | % (5) | 1.92 | % (5) | 1.97 | % | 2.02 | % | 2.79 | % | ||||||||||

| Ratio of net investment income to average net assets (7) | (0.19 | )% | (0.45 | )% | 0.24 | % | 0.83 | % | 0.57 | % | ||||||||||

| Portfolio Turnover Rate | 42 | % | 63 | % | 61 | % | 36 | % | 36 | % | ||||||||||

| (1) | Per share amounts calculated using the average shares method, which more appropriately presents the per share data for the year. |

| (2) | Represents less than $0.01 per share. |

| (3) | Total returns shown exclude the effect of applicable sales charges and redemption fees and assumes reinvestment of all distributions. |

| (4) | Includes adjustments in accordance with accounting principles generally accepted in the United States and consequently the net asset value for financial reporting purposes and the returns based upon those net asset values may differ from the net asset values and returns for shareholder transactions. |

| (5) | Represents the ratio of expenses to average net assets absent fee waivers and/or expense reimbursements by the advisor. |

| (6) | The ratios of expenses and net investment income (loss) to average net assets do not reflect the Fund’s proportionate share of income and expenses of underlying investment companies or REITs in which the Fund invests. |

| (7) | Recognition of net investment income by the Fund is affected by the timing of the declaration of dividends by the underlying investment companies in which the Fund invests. |

| (8) | Ratios to average net assets (excluding securities sold short and interest expense): |

| Expenses, before waiver and reimbursement | 1.56 | % | 1.56 | % | 1.56 | % | 1.54 | % | 1.42 | % | ||||||||||

| Expenses, after waiver and reimbursement | 1.55 | % | 1.55 | % | 1.55 | % | 1.54 | % | 1.48 | % |

See accompanying notes to financial statements.

20

| Altegris/AACA Opportunistic Real Estate Fund |

| FINANCIAL HIGHLIGHTS |

Per Share Data and Ratios for a Share of Beneficial Interest Outstanding Throughout Each Year

| Class N | ||||||||||||||||||||

| Year Ended | Year Ended | Year Ended | Year Ended | Year Ended | ||||||||||||||||

| December 31, | December 31, | December 31, | December 31, | December 31, | ||||||||||||||||

| 2022 | 2021 | 2020 | 2019 | 2018 | ||||||||||||||||

| Net asset value, beginning of year | $ | 20.42 | $ | 21.44 | $ | 17.97 | $ | 12.57 | $ | 16.01 | ||||||||||

| Income/(loss) from investment operations: | ||||||||||||||||||||

| Net investment income/(loss) (1) | (0.06 | ) | (0.15 | ) | (0.01 | ) | 0.09 | 0.04 | ||||||||||||

| Net realized and unrealized gain/(loss) on investments | (8.08 | ) | 1.79 | 5.04 | 5.68 | (2.97 | ) | |||||||||||||

| Total income/(loss) from investment operations | (8.14 | ) | 1.64 | 5.03 | 5.77 | (2.93 | ) | |||||||||||||

| Less distributions from: | ||||||||||||||||||||

| Net investment income | — | — | (0.08 | ) | (0.06 | ) | — | |||||||||||||

| Net realized gains | (0.89 | ) | (2.66 | ) | (1.49 | ) | (0.31 | ) | (0.51 | ) | ||||||||||

| Total distributions | (0.89 | ) | (2.66 | ) | (1.57 | ) | (0.37 | ) | (0.51 | ) | ||||||||||

| Redemption fees collected (2) | 0.00 | 0.00 | 0.01 | 0.00 | 0.00 | |||||||||||||||

| Net asset value, end of year | $ | 11.39 | $ | 20.42 | $ | 21.44 | $ | 17.97 | $ | 12.57 | ||||||||||

| Total return (3,4) | (40.20 | )% | 8.62 | % | 28.18 | % | 46.01 | % | (18.34 | )% | ||||||||||

| Net assets, at end of year (000s) | $ | 15,553 | $ | 40,008 | $ | 37,676 | $ | 30,155 | $ | 16,245 | ||||||||||

| Ratios/Supplemental Data: | ||||||||||||||||||||

| Ratios to average net assets (including securities sold short and interest expense): | ||||||||||||||||||||

| Expenses, before waiver and reimbursement (6,8) | 2.47 | % | 2.17 | % | 2.23 | % | 2.17 | % | 2.97 | % | ||||||||||

| Expenses, after waiver and reimbursement (6,8) | 2.45 | % (5) | 2.17 | % (5) | 2.22 | % | 2.17 | % | 3.02 | % | ||||||||||

| Ratio of net investment income/(loss) to average net assets (7) | (0.41 | )% | (0.69 | )% | (0.04 | )% | 0.56 | % | 0.25 | % | ||||||||||

| Portfolio Turnover Rate | 42 | % | 63 | % | 61 | % | 36 | % | 36 | % | ||||||||||

| (1) | Per share amounts calculated using the average shares method, which more appropriately presents the per share data for the year. |

| (2) | Represents less than $0.01 per share. |

| (3) | Total returns shown exclude the effect of applicable sales charges and redemption fees and assumes reinvestment of all distributions. |

| (4) | Includes adjustments in accordance with accounting principles generally accepted in the United States and consequently the net asset value for financial reporting purposes and the returns based upon those net asset values may differ from the net asset values and returns for shareholder transactions. |

| (5) | Represents the ratio of expenses to average net assets absent fee waivers and/or expense reimbursements by the advisor. |

| (6) | The ratios of expenses and net investment income (loss) to average net assets do not reflect the Fund’s proportionate share of income and expenses of underlying investment companies or REITs in which the Fund invests. |

| (7) | Recognition of net investment income by the Fund is affected by the timing of the declaration of dividends by the underlying investment companies in which the Fund invests. |

| (8) | Ratios to average net assets (excluding securities sold short and interest expense): |

| Expenses, before waiver and reimbursement | 1.81 | % | 1.80 | % | 1.81 | % | 1.79 | % | 1.67 | % | ||||||||||

| Expenses, after waiver and reimbursement | 1.80 | % | 1.80 | % | 1.80 | % | 1.79 | % | 1.72 | % |

See accompanying notes to financial statements.

21

| Altegris/AACA Opportunistic Real Estate Fund |

| NOTES TO FINANCIAL STATEMENTS |

| December 31, 2022 |

| 1. | ORGANIZATION |

Altegris/AACA Opportunistic Real Estate Fund (the “Fund”) is a non-diversified series of shares of beneficial interest of Northern Lights Fund Trust (the “Trust”), a statutory trust organized under the laws of the State of Delaware on January 19, 2005 and registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end management investment company. The Fund commenced operations on January 9, 2014 and seeks to provide total return through long term capital appreciation and current income by investing in both long and short, in equity securities of real estate and real estate related companies.

The Fund offers Class A, Class C, Class I, and Class N shares. Class A shares are offered at net asset value (“NAV”) plus a maximum sales charge of 5.75%. Investors that purchase $1,000,000 or more of the Fund’s Class A shares will not pay any initial sales charge on the purchase; however, may be subject to a contingent deferred sales charge (“CDSC”) on shares redeemed during the first 18 months after their purchase in the amount of the commissions paid on the shares redeemed. Class C shares commenced operations on December 1, 2020 and are offered at their NAV without an initial sales charge and are subject to 12b-1. Class N shares are offered at their NAV without an initial sales charge and are subject to 12b-1. Class I shares of the Fund are sold at NAV without an initial sales charge and are not subject to distribution fees, but have a higher minimum initial investment than Class A and Class N shares. All classes are subject to a 1.00% redemption fee on redemptions made with 30 days of the original purchase. Each share class represents an interest in the same assets of the Fund and classes are identical except for differences in their sales charge structures and ongoing service and distribution charges. All classes of shares have equal voting privileges except that each class has exclusive voting rights with respect to its service and/or distribution plans. The Fund’s income, expenses (other than class specific distribution fees) and realized and unrealized gains and losses are allocated proportionately each day based upon the relative net assets of each class of the Fund.

| 2. | SIGNIFICANT ACCOUNTING POLICIES |

The following is a summary of significant accounting policies followed by the Fund in preparation of its financial statements. The policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”). The preparation of the financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses for the period. Actual results could differ from those estimates. Due to custodian liabilities shown on the Statement of Assets and Liabilities are carried at cost and approximate fair value as of December 31, 2022 using level 2 inputs. The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standard Codification Topic 946.

Security Valuation – Securities listed on an exchange are valued at the last reported sale price at the close of the regular trading session of the exchange on the business day the value is being determined, or in the case of securities listed on NASDAQ at the NASDAQ Official Closing Price. In the absence of a sale such securities shall be valued at the mean between the current bid and ask prices on the day of valuation. Short-term debt obligations having 60 days or less remaining until maturity, at time of purchase may be valued at amortized cost (which approximates fair value). Investments in open-end investment companies are valued at net asset value.

Valuation of Fund of Funds – The Fund may invest in portfolios of open-end or closed-end investment companies (the “Underlying Funds”). The Underlying Funds value securities in their portfolios for which market quotations are readily available at their market values (generally the last reported sale price) and all other securities and assets at their fair value by the methods established by the board of directors of the Underlying Funds.

Open-end investment companies are valued at their respective NAVs as reported by such investment companies. The shares of many closed-end investment companies, after their initial public offering, frequently trade at a price per share, which is different than the net asset value per share. The difference represents a market premium or market discount of such shares. There can be no assurances that the market discount or market premium on shares of any closed-end investment company purchased by the Fund will not change.

22

| Altegris/AACA Opportunistic Real Estate Fund |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| December 31, 2022 |

The Fund may hold securities, such as private investments, interests in commodity pools, other non-traded securities or temporarily illiquid securities, for which market quotations are not readily available or are determined to be unreliable. These securities will be valued using the “fair value” procedures approved by the Board. The Board has delegated execution of these procedures to the Adviser as its valuation designee (the “Valuation Designee”). The Valuation Designee may also enlist third party consultants such a valuation specialist at a public accounting firm, valuation consultant or financial officer of a security issuer on an as-needed basis to assist in determining a security-specific fair value. The Board is responsible for reviewing and approving fair value methodologies utilized by the Valuation Designee, which approval shall be based upon whether the Valuation Designee followed the valuation procedures established by the Board.

Fair Valuation Process – The applicable investments are valued by the Valuation Designee pursuant to valuation procedures established by the Board. For example, fair value determinations are required for the following securities: (i) securities for which market quotations are insufficient or not readily available on a particular business day (including securities for which there is a short and temporary lapse in the provision of a price by the regular pricing source); (ii) securities for which, in the judgment of the Valuation Designee, the prices or values available do not represent the fair value of the instrument; factors which may cause the Valuation Designee to make such a judgment include, but are not limited to, the following: only a bid price or an ask price is available; the spread between bid and ask prices is substantial; the frequency of sales; the thinness of the market; the size of reported trades; and actions of the securities markets, such as the suspension or limitation of trading; (iii) securities determined to be illiquid; and (iv) securities with respect to which an event that will affect the value thereof has occurred (a “significant event”) since the closing prices were established on the principal exchange on which they are traded, but prior to a Fund’s calculation of its net asset value. Specifically, interests in commodity pools or managed futures pools are valued on a daily basis by reference to the closing market prices of each futures contract or other asset held by a pool, as adjusted for pool expenses. Restricted or illiquid securities, such as private investments or non-traded securities are valued based upon the current bid for the security from two or more independent dealers or other parties reasonably familiar with the facts and circumstances of the security (who should take into consideration all relevant factors as may be appropriate under the circumstances). If a current bid from such independent dealers or other independent parties is unavailable, the Valuation Designee shall determine, the fair value of such security using the following factors: (i) the type of security; (ii) the cost at date of purchase; (iii) the size and nature of the Fund’s holdings; (iv) the discount from market value of unrestricted securities of the same class at the time of purchase and subsequent thereto; (v) information as to any transactions or offers with respect to the security; (vi) the nature and duration of restrictions on disposition of the security and the existence of any registration rights; (vii) how the yield of the security compares to similar securities of companies of similar or equal creditworthiness; (viii) the level of recent trades of similar or comparable securities; (ix) the liquidity characteristics of the security; (x) current market conditions; and (xi) the market value of any securities into which the security is convertible or exchangeable.

The Fund utilizes various methods to measure the fair value of all of its investments on a recurring basis. GAAP establishes a hierarchy that prioritizes inputs to valuation methods. The three levels of input are:

Level 1 – Unadjusted quoted prices in active markets for identical assets and liabilities.

Level 2 – Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument in an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data.

Level 3 – Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available; representing the Fund’s own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available.

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

23

| Altegris/AACA Opportunistic Real Estate Fund |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| December 31, 2022 |

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. The following table summarizes the level of inputs used as of December 31, 2022, for the Fund’s assets and liabilities measured at fair value:

| Assets* | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Investments | ||||||||||||||||