UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended September 30, 2018

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ______________ to________________

Commission file number: 001-37606

ANAVEX LIFE SCIENCES CORP.

(Exact name of registrant as specified in its charter)

| Nevada | 98-0608404 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

| 51 W 52nd Street, 7th Floor, New York, NY USA | 10019 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code 1-844-689-3939

Securities registered under Section 12(b) of the Act:

| Common Stock, $0.001 par value | NASDAQ Stock Market LLC | |

| Title of each class | Name of each exchange on which registered |

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, $0.001 par value

(Title of class)

| Indicate by checkmark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. | |||

| Yes ☐ No☒ | |||

| Indicate by checkmark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. | |||

| Yes ☐ No ☒ | |||

| Indicate by checkmark whether the registrant has (1) filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | |||

| Yes ☒ No ☐ | |||

| Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). | |||

| Yes ☒ No ☐ | |||

| Indicate by checkmark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. | |||

| ☐ | |||

| Indicate by checkmark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. | |||

| Large accelerated filer ☐ | Smaller reporting company ☒ | ||

| Non-accelerated filer ☐ | Emerging growth company ☐ | ||

| Accelerated filer ☒ | |||

| If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act | |||

| ☐ | |||

| Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). | |||

| Yes ☐ No ☒ | |||

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter: $114,432,887 based on a price of $2.71 per share, being the closing price of the registrant’s common stock on March 31, 2018.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date 46,586,162 issued and outstanding as of December 12, 2018.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Proxy Statement for its 2019 Annual Meeting of Stockholders are incorporated by reference into Part III of this Annual Report on Form 10-K.

TABLE OF CONTENTS

ii

Forward Looking Statements.

This Annual Report on Form 10-K includes forward-looking statements. All statements other than statements of historical facts contained in this Annual Report on Form 10-K, including statements regarding our anticipated future clinical and regulatory milestone events, future financial position, business strategy and plans and objectives of management for future operations, are forward-looking statements. The words “believe,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “expect” “should,” “forecast,” “could,” “suggest,” “plan” and similar expressions, as they relate to us, are intended to identify forward-looking statements. Such forward-looking statements include, without limitation, statements regarding:

| ● | our ability to generate any revenue or to continue as a going concern; |

| ● | our ability to successfully conduct clinical and preclinical trials for our product candidates; |

| ● | our ability to raise additional capital on favorable terms; |

| ● | our ability to execute our development plan on time and on budget; |

| ● | our products ability to demonstrate efficacy or an acceptable safety profile; |

| ● | our ability to obtain the support of qualified scientific collaborators; |

| ● | our ability, whether alone or with commercial partners, to successfully commercialize any of our product candidates that may be approved for sale; |

| ● | our ability to identify and obtain additional product candidates; |

| ● | our ability to obtain and maintain sufficient intellectual property protection for our product candidates; |

| ● | our ability to comply with our intellectual property licensing agreements; |

| ● | our ability to defend against claims of intellectual property infringement; |

| ● | competition; |

| ● | the anticipated start dates, durations and completion dates of our ongoing and future clinical studies; |

| ● | the anticipated designs of our future clinical studies; |

| ● | our anticipated future regulatory submissions and our ability to receive regulatory approvals to develop and market our product candidates; and |

| ● | our anticipated future cash position. |

We have based these forward-looking statements largely on our current expectations and projections about future events, including the responses we expect from the U.S. Food and Drug Administration, (“FDA”), and other regulatory authorities and financial trends that we believe may affect our financial condition, results of operations, business strategy, preclinical and clinical trials, and financial needs. These forward-looking statements are subject to a number of risks, uncertainties and assumptions including without limitation the risks described in “Risk Factors” in Part I, Item 1A of this Annual Report on Form 10-K. These risks are not exhaustive. Other sections of this Annual Report on Form 10-K include additional factors which could adversely impact our business and financial performance. Moreover, we operate in a very competitive and rapidly changing environment. New risk factors emerge from time to time and it is not possible for our management to predict all risk factors, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. You should not rely upon forward-looking statements as predictions of future events. We cannot assure you that the events and circumstances reflected in the forward-looking statements will be achieved or occur and actual results could differ materially from those projected in the forward-looking statements. Except as required by applicable laws including the securities laws of the United States, we assume no obligation to update or supplement forward-looking statements.

As used in this Annual Report on Form 10-K, the terms “we,” “us,” “our,” and “Anavex” mean Anavex Life Sciences Corp., unless the context clearly requires otherwise.

iii

Overview and Strategy

Anavex Life Sciences Corp. is a clinical stage biopharmaceutical company engaged in the development of differentiated therapeutics by applying precision medicine to central nervous system (“CNS”) diseases with high unmet need. Anavex analyzes genomic data from clinical studies to identify biomarkers, which select patients that will receive the therapeutic benefit for the treatment of neurodegenerative and neurodevelopmental diseases.

Our lead compound, ANAVEX®2-73, is being developed to treat Alzheimer’s disease, Parkinson’s disease and potentially other central nervous system diseases, including rare diseases, such as Rett syndrome, a rare severe neurological monogenic disorder caused by mutations in the X-linked gene, methyl-CpG-binding protein 2 (“MECP2”).

Our total portfolio currently consists of five programs. To prioritize the allocation of our resources, we designate certain programs as core programs and others as seed programs, and we currently have two core programs and three seed programs. Our core programs are at various stages of clinical and preclinical development, in neurodegenerative and neurodevelopmental diseases.

The following table summarizes key information about our programs:

1

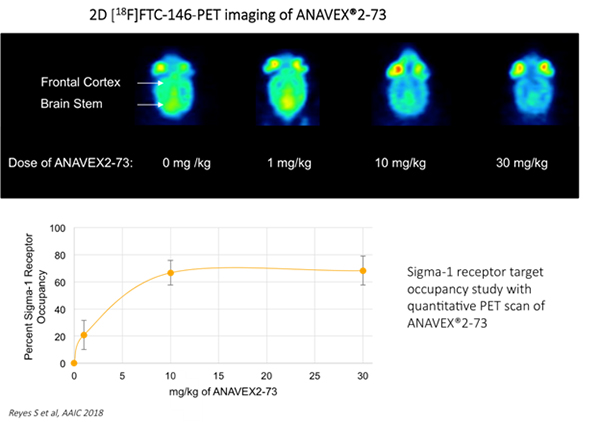

Anavex has a portfolio of compounds varying in sigma-1 receptor (S1R) binding activities. The SIGMAR1 gene encodes the S1R protein, which is an intracellular chaperone protein with important roles in cellular communication. S1R is also involved in transcriptional regulation at the nuclear envelope and restores homeostasis and stimulates recovery of cell function when activated. In order to validate the ability of our compounds to activate quantitatively the S1R, we performed in collaboration with Stanford University a quantitative Positron Emission Tomography (PET) imaging scan in mice, which demonstrated a dose-dependent ANAVEX®2-73 target engagement or receptor occupancy (RO) with S1R in the brain.

Cellular Homeostasis

Many diseases are possibly directly caused by chronic homeostatic imbalances or cellular stress of brain cells. In pediatric diseases like Rett syndrome or infantile spasms, the chronic cellular stress is possibly caused by the presence of a constant genetic mutation. In neurodegenerative diseases, such as Alzheimer’s and Parkinson’s diseases, chronic cellular stress is possibly caused by age-correlated buildup of cellular insult and hence chronic cellular stress. Specifically, defects in homeostasis of protein or ribonucleic acid (“RNA”) lead to the death of neurons and dysfunction of the nervous system. The spreading of protein aggregates resulting in a proteinopathy, a characteristic finding in Alzheimer’s and Parkinson’s diseases that results from disorders of protein synthesis, trafficking, folding, processing or degradation in cells. The clearance of macromolecules in the brain is particularly susceptible to imbalances that result in aggregation and degeneration in nerve cells. For example, Alzheimer’s disease pathology is characterized by the presence of amyloid plaques, neurofibrillary tangles, which are aggregates of hyperphosphorylated Tau protein that are a marker of other diseases known as tauopathies as well as inflammation of microglia. With the SIGMAR1 activation through SIGMAR1 agonists like ANAVEX®2-73, our approach is to restore cellular balance, i.e. homeostasis. Therapies that correct defects in cellular homeostasis might have the potential to halt or delay neurodevelopmental and neurodegenerative disease progression.

2

ANAVEX®2-73-specific Biomarkers

A full genomic analysis of Alzheimer’s disease (AD) patients treated with ANAVEX®2-73 resulted in the identification of actionable genetic variants. A significant impact of the genomic biomarkers SIGMAR1, the direct target of ANAVEX®2-73 and COMT, a gene involved in memory function, on the drug response level was identified, leading to an early ANAVEX®2-73-specific biomarker hypothesis. It is expected that excluding patients with these two identified biomarker variants (approximately 10%-20% of the population) in prospective studies would identify approximately 80%-90% patients that would display clinically significant improved functional and cognitive scores. The consistency between the identified DNA and RNA data related to ANAVEX®2-73, which are considered independent of AD pathology, as well as multiple endpoints and time-points, provides support for precision medicine clinical development of ANAVEX®2-73 by using genetic biomarkers identified within the study population itself to target patients who are most likely to respond to ANAVEX®2-73 treatment in AD as well as indications like Parkinson’s disease dementia (PDD) or Rett syndrome (RTT) in which ANAVEX®2-73 is currently studied or planned to be studied.

Clinical Studies Overview

In November 2016, we completed a Phase 2a clinical trial, consisting of PART A and PART B, which lasted a total of 57 weeks, for ANAVEX®2-73 in mild-to-moderate Alzheimer’s patients. This open-label randomized trial met both primary and secondary endpoints and was designed to assess the safety and exploratory efficacy of ANAVEX®2-73 in 32 patients. ANAVEX®2-73 targets sigma-1 and muscarinic receptors, which have been shown in preclinical studies to reduce stress levels in the brain believed to restore cellular homeostasis and to reverse the pathological hallmarks observed in Alzheimer’s disease. In October 2017, we presented positive pharmacokinetic (PK) and pharmacodynamic (PD) data from the Phase 2a study, which established a concentration-effect relationship between ANAVEX®2-73 and study measurements. These measures obtained from all patients who participated in the entire 57 weeks include exploratory cognitive and functional scores as well as biomarker signals of brain activity. Additionally, the study appears to show that ANAVEX®2-73 activity is enhanced by its active metabolite (ANAVEX19-144), which also targets the sigma-1 receptor and has a half-life approximately twice as long as the parent molecule.

In March 2016, we received approval from the Ethics Committee in Australia to extend the Phase 2a clinical trial by an additional 108 weeks, which had been requested by patients and their caregivers. Subsequently, in May 2018, we received approval from the Ethics Committee in Australia to further extend the Phase 2a extension trial for an additional two years. The two consecutive trial extensions have allowed participants who completed the 52-week PART B of the study to continue taking ANAVEX®2-73, providing an opportunity to gather extended safety data for a cumulative time period of five years.

In October 2018, we presented new long-term clinical data for ANAVEX®2-73 in a presentation at the 2018 Clinical Trials on Alzheimer’s Disease (CTAD) Meeting. At 148 weeks into the five-year extended Phase 2a clinical study, data confirmed a significant association between ANAVEX®2-73 concentration and both exploratory functional and cognitive endpoints as measured by the Alzheimer’s Disease Cooperative Study-Activities of Daily Living (ADCS-ADL) evaluation and the Mini Mental State Examination (MMSE), respectively. The cohort of patients treated with higher ANAVEX®2-73 concentration maintained ADCS-ADL performance compared to the lower concentration cohort (p<0.0001). As well, the patient cohort with the higher ANAVEX®2-73 concentration performed better at MMSE compared to the lower concentration cohort (p<0.0008). A significant impact on the drug response levels of both the SIGMAR1 (p<0.0080) and COMT (p<0.0014) genomic biomarkers, identified and specified at week 57, was also confirmed over the 148-week period. Further, ANAVEX®2-73 demonstrated continued favorable safety and tolerability through 148 weeks.

3

A larger Phase 2b/3 double-blind, placebo-controlled study of ANAVEX®2-73 in Alzheimer’s disease commenced in October 2018, which is independent of the ongoing Phase 2a extension study. The Phase 2b/3 study will enroll approximately 450 patients for 48 weeks, randomized 1:1:1 to two different ANAVEX®2-73 doses or placebo. The trial is currently taking place in Australia; however, North American sites may also be added. The ANAVEX®2-73 Phase 2b/3 study design incorporates genomic precision medicine biomarkers identified in the ANAVEX®2-73 Phase 2a study. Primary and secondary endpoints will assess safety and both cognitive and functional efficacy, measured through Alzheimer’s Disease Assessment Scale – Cognition (ADAS-Cog), ADCS-ADL and Clinical Dementia Rating – Sum of Boxes for cognition and function (CDR-SB).

In February 2016, we presented positive preclinical data for ANAVEX®2-73 in Rett syndrome, a rare neurodevelopmental disease. The study was funded by the International Rett Syndrome Foundation (“Rettsyndrome.org”). In January 2017, we were awarded a financial grant from Rettsyndrome.org of a minimum of $0.6 million to cover some of the costs of a multicenter Phase 2 clinical trial of ANAVEX®2-73 for the treatment of Rett syndrome. This award is being received in quarterly instalments which commenced during fiscal 2018. Further, in October 2018, the Company received confirmation from the FDA that its investigational new drug (IND) application is now open for a Phase 2 clinical trial of ANAVEX®2-73 for the treatment of Rett syndrome. The Phase 2 study is a randomized double-blind, placebo-controlled safety, tolerability, pharmacokinetic and efficacy study of oral liquid ANAVEX®2-73 formulation to treat Rett syndrome. Pharmacokinetic and dose findings will be investigated in a total of 15 patients over a 7-week treatment period including ANAVEX®2-73-specific genomic precision medicine biomarkers. All patients who participate in the study will be eligible to receive ANAVEX®2-73 under a voluntary open label extension protocol. This study will be followed by a planned placebo-controlled safety and efficacy evaluation of ANAVEX®2-73 over a 3-month treatment period. Primary and secondary endpoints include safety as well as Rett syndrome conditions such as cognitive impairment, motor impairment, behavioral symptoms and seizure activity. The ANAVEX®2-73 Phase 2 Rett syndrome study design incorporates genomic precision medicine biomarkers identified in the ANAVEX®2-73 Phase 2a Alzheimer’s disease study.

In September 2016, we presented positive preclinical data for ANAVEX®2-73 in Parkinson’s disease, which demonstrated significant improvements on all measures: behavioral, histopathological, and neuroinflammatory endpoints. The study was funded by the Michael J. Fox Foundation. Additional data was announced in October 2017 from the model for experimental parkinsonism. The data presented indicates that ANAVEX®2-73 induces robust neurorestoration in experimental parkinsonism. The encouraging results we have gathered in this model, coupled with the favorable profile of this compound in the Alzheimer’s disease trial, support the notion that ANAVEX®2-73 is a promising clinical candidate drug for Parkinson’s disease.

The Company initiated in October 2018 in Spain, Europe a double-blind, randomized, placebo-controlled Phase 2 trial with ANAVEX®2-73 in Parkinson’s Disease Dementia (PDD), which will study the effect of the compound on both the cognitive and motor impairment of Parkinson’s disease. The Phase 2 study will enroll approximately 120 patients for 14 weeks, randomized 1:1:1 to two different ANAVEX®2-73 doses or placebo. The ANAVEX®2-73 Phase 2 PDD study design incorporates genomic precision medicine biomarkers identified in the ANAVEX®2-73 Phase 2a study.

Our Pipeline

Our research and development pipeline includes ANAVEX®2-73 currently in three different clinical studies, and several compounds in different stages of pre-clinical study.

Our proprietary SIGMACEPTOR™ Discovery Platform produced small molecule drug candidates with unique modes of action, based on our understanding of sigma receptors. Sigma receptors may be targets for therapeutics to combat many human diseases, both of neurodegenerative nature, including Alzheimer’s disease, as well as of neurodevelopmental nature, like Rett syndrome. When bound by the appropriate ligands, sigma receptors influence the functioning of multiple biochemical signals that are involved in the pathogenesis (origin or development) of disease.

4

Compounds that have been subjects of our research include the following:

ANAVEX®2-73

ANAVEX®2-73 may offer a disease-modifying approach in neurodegenerative and neurodevelopmental diseases by activation of sigma-1 receptors.

In Rett syndrome, administration of ANAVEX®2-73 resulted in both significant and dose related improvements in an array of behavioral paradigms in the MECP2 HET Rett syndrome disease model. In addition, in a further experiment sponsored by Rettsyndrome.org, ANAVEX®2-73 was evaluated in automatic visual response and respiration tests in 7-month old mice, an age at which advanced pathology is evident. Vehicle-treated MECP2 mice demonstrated fewer automatic visual responses than wild-type mice. Treatment with ANAVEX®2-73 for four weeks significantly increased the automatic visual response in the MECP2 Rett syndrome disease mouse. Additionally, chronic oral dosing daily for 6.5 weeks of ANAVEX®2-73 starting at ~5.5 weeks of age was conducted in the MECP2 HET Rett syndrome disease mouse model assessed the different aspects of muscular coordination, balance, motor learning and muscular strengths, some of the core deficits observed in Rett syndrome. Administration of ANAVEX®2-73 resulted in both significant and dose related improvements in an array of these behavioral paradigms in the MECP2 HET Rett syndrome disease model.

In October 2018, the Company received confirmation from the FDA that its IND application is now open for a Phase 2 clinical trial of ANAVEX®2-73 for the treatment of Rett syndrome.

In May 2016 and June 2016, the FDA granted Orphan Drug Designation to ANAVEX®2-73 for the treatment of Rett syndrome and infantile spasms, respectively.

For Parkinson’s disease, data demonstrates significant improvements and restoration of function in a disease modifying animal model of Parkinson’s disease. Significant improvements were seen on all measures tested: behavioral, histopathological, and neuroinflammatory endpoints. In July 2018 the Company received approval from the Spanish Agency for Medicinal Products and Medical Devices (AEMPS), to initiate its Phase 2, double-blind, placebo-controlled 14-week trial of the safety and efficacy of ANAVEX®2-73 for the treatment of Parkinson’s disease dementia. The Phase 2 study commenced in October 2018 and will involve approximately 120 patients, randomized 1:1:1 to two different ANAVEX®2-73 doses or placebo, in up to 24 clinical study sites.

In Alzheimer’s disease (AD) animal models, ANAVEX®2-73 has shown pharmacological, histological and behavioral evidence as a potential neuroprotective, anti-amnesic, anti-convulsive and anti-depressive therapeutic agent, due to its potent affinity to sigma-1 receptors and moderate affinities to M1-4 type muscarinic receptors. In addition, ANAVEX®2-73 has shown a potential dual mechanism which may impact both amyloid and tau pathology. In a transgenic AD animal model Tg2576, ANAVEX®2-73 induced a statistically significant neuroprotective effect against the development of oxidative stress in the mouse brain, as well as significantly increased the expression of functional and synaptic plasticity markers that is apparently amyloid-beta independent. It also statistically alleviated the learning and memory deficits developed over time in the animals, regardless of sex, both in terms of spatial working memory and long-term spatial reference memory.

Based on the results of pre-clinical testing, we initiated and completed a Phase 1 single ascending dose (SAD) clinical trial of ANAVEX®2-73. In this Phase 1 SAD trial, the maximum tolerated single dose was defined per protocol as 55-60 mg. This dose is above the equivalent dose shown to have positive effects in mouse models of AD. There were no significant changes in laboratory or electrocardiogram (ECG) parameters. ANAVEX®2-73 was well tolerated below the 55-60 mg dose with only mild adverse events in some subjects. Observed adverse events at doses above the maximum tolerated single dose included headache and dizziness, which were moderate in severity and reversible. These side effects are often seen with drugs that target CNS conditions, including AD.

5

The ANAVEX®2-73 Phase 1 SAD trial was conducted as a randomized, placebo-controlled study. Healthy male volunteers between the ages of 18 and 55 received single, ascending oral doses over the course of the trial. Study endpoints included safety and tolerability together with pharmacokinetic parameters. Pharmacokinetics includes the absorption and distribution of a drug, the rate at which a drug enters the blood and the duration of its effect, as well as chemical changes of the substance in the body. This study was conducted in Germany in collaboration with ABX-CRO, a clinical research organization that has conducted several Alzheimer’s disease studies, and the Technical University of Dresden.

In December 2014, a Phase 2a clinical trial was initiated for ANAVEX®2-73, which is being evaluated for the treatment of Alzheimer’s disease. The open-label randomized trial was designed to assess the safety and exploratory efficacy of ANAVEX®2-73 in 32 patients with mild-to-moderate Alzheimer’s disease. ANAVEX®2-73 targets sigma-1 and muscarinic receptors, which have been shown in preclinical studies to reduce stress levels in the brain believed to restore cellular homeostasis and to reverse the pathological hallmarks observed in Alzheimer’s disease.

The Phase 2a study met both primary and secondary objectives of the study. The 31-week preliminary exploratory safety and efficacy data from the Phase 2a study of ANAVEX®2-73 in Alzheimer’s patients, with most receiving also donepezil, the current standard of care, demonstrated favorable safety, maximum tolerated dose, positive dose response, sustained efficacy response through 31 weeks for both cognitive and functional measures, as well as positive unexpected therapeutic response events. ANAVEX®2-73 continued to demonstrate a favorable adverse event (AE) profile through 31 weeks in a patient population of elderly Alzheimer’s patients with varying degrees of physical fragility. The most common side effects across all AE categories tended to be of mild severity grade 1 and were resolved with dose reductions that were anticipated within the adaptive design of the study protocol.

Through 57 weeks, Alzheimer’s patients taking a daily oral dose between 10mg and 50mg of ANAVEX®2-73 was well tolerated. There were no clinically significant treatment-related adverse events and no serious adverse events. Despite non-optimized dosing of ANAVEX®2-73 throughout the 57-week study, continued significant improvements from baseline of cognitive, functional and behavioral scores in a group of patients were observed, respectively. This data was analyzed using refined mathematical modeling methods in conjunction with the detailed pharmacokinetic (PK) information.

In October 2017, we presented positive PK and PD data from the Phase 2a study, which established a concentration-effect relationship between ANAVEX®2-73 and study measurements. These measures, obtained from all patients who participated in the entire 57 weeks, include exploratory cognitive and functional scores as well as biomarker signals of brain activity. Additionally, the study appears to show that ANAVEX®2-73 activity is enhanced by its active metabolite (ANAVEX19-144), which also targets the sigma-1 receptor and has a half-life approximately twice as long as the parent molecule.

Pre-specified exploratory analyses included the cognitive (MMSE) and the functional (ADCS-ADL) changes from baseline. A continued stabilization of both cognitive and functional measures in patients treated with ANAVEX®2-73 was observed. This correlation was positive within all measured scores (MMSE, ADCS-ADL, Cogstate, HAM-D and EEG/ERP).

In July 2018, we presented the results of a genomic DNA and RNA evaluation of the participants in the Phase 2a study. More than 33,000 genes were analyzed using unbiased, data driven, machine learning, artificial intelligence (AI) system for analyzing DNA & RNA data in patients exposed to ANAVEX®2-73. The analysis identified genetic variants that impacted response to ANAVEX®2-73, among them variants related to the Sigma-1 receptor (SIGMAR1), the target for ANAVEX®2-73. Results showed that study participants without the SIGMAR1 (rs1800866) variants, which is about 80 percent of the population worldwide, demonstrated improved cognitive (MMSE) and the functional (ADCS-ADL) scores. The results from this evaluation may enable a precision medicine approach, since these signatures can now be applied to neurological indications tested in clinical studies with ANAVEX®2-73 including Alzheimer’s disease, Parkinson’s disease dementia and Rett syndrome.

6

ANAVEX®2-73 data presented met prerequisite information in order to progress into a Phase 2b/3 placebo-controlled study. On July 2, 2018, the Human Research Ethics Committee in Australia approved the initiation of our Phase 2b/3, double-blind, randomized, placebo-controlled 48-week safety and efficacy trial of ANAVEX®2-73 for the treatment of early Alzheimer’s disease. This Phase 2b/3 study design incorporates inclusion of genomic precision medicine biomarkers identified in the ANAVEX®2-73 Phase 2a study. The Phase 2b/3 study, which is expected to enroll approximately 450 patients, randomized 1:1:1 to either two different ANAVEX®2-73 doses or placebo, commenced in October 2018.

Preclinical data also validates ANAVEX®2-73 as a prospective platform drug for other neurodegenerative diseases beyond Alzheimer’s disease, Parkinson’s disease or Rett syndrome, more specifically, epilepsy, infantile spasms, Fragile X syndrome, Angelman syndrome, multiple sclerosis and, more recently, tuberous sclerosis complex (TSC). ANAVEX®2-73 demonstrated significant improvements in all of these indications in the respective preclinical animal models.

In a study sponsored by the Foundation for Angelman Syndrome, ANAVEX®2-73 was assessed in a mouse model for the development of audiogenic seizures. The results indicated that ANAVEX®2-73 administration significantly reduced audiogenic-induced seizures. In a study sponsored by FRAXA Research Foundation regarding Fragile X syndrome, data demonstrated that ANAVEX®2-73 restored hippocampal brain-derived neurotrophic factor (BDNF) expression to normal levels. BDNF under-expression has been observed in many neurodevelopmental and neurodegenerative pathologies. BDNF signaling promotes maturation of both excitatory and inhibitory synapses. ANAVEX®2-73 normalization of BDNF expression could be a contributing factor for the positive data observed in both neurodevelopmental and neurodegenerative disorders like Angelman and Fragile X syndromes.

Preclinical data presented also indicates that ANAVEX®2-73 demonstrates protective effects of mitochondrial enzyme complexes during pathological conditions, which, if impaired, are believed to play a role in the pathogenesis of neurodegenerative and neurodevelopmental diseases.

Preclinical data on ANAVEX®2-73 related to multiple sclerosis indicates that ANAVEX®2-73 may promote remyelination in multiple sclerosis disease. Further, data also demonstrates that ANAVEX®2-73 provides protection for oligodendrocytes (“OL’s”) and oligodendrocyte precursor cells (“OPC’s”), as well as central nervous system neurons in addition to helping repair by increasing OPC proliferation and maturation in tissue culture.

In March 2018, we presented preclinical data of ANAVEX®2-73 in a genetic mouse model of tuberous sclerosis complex (“TSC”). TSC is a rare genetic disorder characterized by the growth of numerous benign tumors in many parts of the body with a high incidence of seizures. The new preclinical data demonstrates that treatment with ANAVEX®2-73 significantly increases survival and reduces seizures.

ANAVEX®3-71

ANAVEX®3-71 is a preclinical drug candidate with a novel mechanism of action via sigma-1 receptor activation and M1 muscarinic allosteric modulation, which has been shown to enhance neuroprotection and cognition in Alzheimer’s disease models. ANAVEX®3-71 is a CNS-penetrable mono-therapy that bridges treatment of both cognitive impairments with disease modifications. It is highly effective in very small doses against the major Alzheimer’s hallmarks in transgenic (3xTg-AD) mice, including cognitive deficits, amyloid and tau pathologies, and also has beneficial effects on inflammation and mitochondrial dysfunctions. ANAVEX®3-71 indicates extensive therapeutic advantages in Alzheimer’s and other protein-aggregation-related diseases given its ability to enhance neuroprotection and cognition via sigma-1 receptor activation and M1 muscarinic allosteric modulation.

7

A preclinical study examined the response of ANAVEX®3-71 in aged transgenic animal models and showed a significant reduction in the rate of cognitive deficit, amyloid beta pathology and inflammation with the administration of ANAVEX 3-71. In April 2016, the FDA granted Orphan Drug Designation to ANAVEX®3-71 for the treatment of Frontotemporal dementia (FTD).

During pathological conditions ANAVEX®3-71 demonstrated the formation of new synapses between neurons (synaptogenesis) without causing an abnormal increase in the number of astrocytes. In neurodegenerative diseases such as Alzheimer’s and Parkinson’s disease, synaptogenesis is believed to be impaired. Additional preclinical data presented also indicates that in addition to reducing oxidative stress, ANAVEX®3-71 demonstrates protective effects of mitochondrial enzyme complexes during pathological conditions, which, if impaired, are believed to play a role in the pathogenesis of neurodegenerative and neurodevelopmental diseases.

ANAVEX®1-41

ANAVEX®1-41 is a sigma-1 agonist. Pre-clinical tests revealed significant neuroprotective benefits (i.e., protects nerve cells from degeneration or death) through the modulation of endoplasmic reticulum, mitochondrial and oxidative stress, which damages and impairs cell viability. In addition, in animal models, ANAVEX®1-41 prevented the expression of caspase-3, an enzyme that plays a key role in apoptosis (programmed cell death) and loss of cells in the hippocampus, the part of the brain that regulates learning, emotion and memory. These activities involve both muscarinic and sigma-1 receptor systems through a novel mechanism of action.

Preclinical data presented also indicates that ANAVEX®1-41 demonstrates protective effects of mitochondrial enzyme complexes during pathological conditions, which, if impaired, are believed to play a role in the pathogenesis of neurodegenerative and neurodevelopmental diseases.

ANAVEX®1066

ANAVEX®1066, a mixed sigma-1/sigma-2 ligand is designed for the potential treatment of neuropathic and visceral pain. ANAVEX®1066 was tested in two preclinical models of neuropathic and visceral pain that have been extensively validated in rats. In the chronic constriction injury model of neuropathic pain, a single oral administration of ANAVEX®1066 dose-dependently restored the nociceptive threshold in the affected paw to normal levels while leaving the contralateral healthy paw unchanged. Efficacy was rapid and remained significant for two hours. In a model of visceral pain, chronic colonic hypersensitivity was induced by injection of an inflammatory agent directly into the colon and a single oral administration of ANAVEX®1066 returned the nociceptive threshold to control levels in a dose-dependent manner. Companion studies in rats demonstrated the lack of any effects on normal gastrointestinal transit with ANAVEX®1066 and a favorable safety profile in a battery of behavioral measures.

Our compounds are in the pre-clinical and clinical testing stages of development, and there is no guarantee that the activity demonstrated in pre-clinical models will be shown in human testing.

ANAVEX®1037

ANAVEX®1037 is designed for the treatment of prostate and pancreatic cancer. It is a low molecular weight, synthetic compound exhibiting high affinity for sigma-1 receptors at nanomolar levels and moderate affinity for sigma-2 receptors and sodium channels at micromolar levels. In advanced pre-clinical studies, this compound revealed antitumor potential. It has also been shown to selectively kill human cancer cells without affecting normal/healthy cells and also to significantly suppress tumor growth in immune-deficient mice models. Scientific publications highlight the possibility that these ligands may stop tumor growth and induce selective cell death in various tumor cell lines. Sigma receptors are highly expressed in different tumor cell types. Binding by appropriate sigma-1 and/or sigma-2 ligands can induce selective apoptosis. In addition, through tumor cell membrane reorganization and interactions with ion channels, our drug candidates may play an important role in inhibiting the processes of metastasis (spreading of cancer cells from the original site to other parts of the body), angiogenesis (the formation of new blood vessels) and tumor cell proliferation.

8

We continue to identify and initiate discussions with potential strategic and commercial partners to most effectively advance our programs and realize maximum shareholder value. Further, we may acquire or develop new intellectual property and assign, license, or otherwise transfer our intellectual property to further our goals.

Our Target Indications

We have developed compounds with potential application to two broad categories and several specific indications. including:

Central Nervous System Diseases

| ● | Alzheimer’s disease – In 2018, an estimated 5.5 million Americans were suffering from Alzheimer’s disease. The Alzheimer’s Association® reports that by 2025, 7.1 million Americans will be afflicted by the disease, about a 29 percent increase from currently affected patients. Medications on the market today treat only the symptoms of Alzheimer’s disease and do not have the ability to stop its onset or its progression. There is an urgent and unmet need for both a disease modifying cure for Alzheimer’s disease as well as for better symptomatic treatments. |

| ● | Parkinson’s disease – Parkinson’s disease is a progressive disease of the nervous system marked by tremors, muscular rigidity, and slow, imprecise movement. It is associated with degeneration of the basal ganglia of the brain and a deficiency of the neurotransmitter dopamine. Parkinson’s disease afflicts more than 10 million people worldwide, typically middle-aged and elderly people. The Parkinson’s disease market is set to expand from $2.1 billion in 2014 to $3.2 billion by 2021, according to business intelligence provider GBI Research. |

| ● | Rett syndrome - Rett syndrome is a rare X-linked genetic neurological and developmental disorder that affects the way the brain develops, including protein transcription, which is altered and as a result leads to severe disruptions in neuronal homeostasis. It is considered a rare, progressive neurodevelopmental disorder and is caused by a single mutation in the MECP2 gene. Because males have a different chromosome combination from females, boys who have the genetic MECP2 mutation are affected in devastating ways. Most of them die before birth or in early infancy. For females who survive infancy, Rett syndrome leads to severe impairments, affecting nearly every aspect of the child’s life; severe mental retardation, their ability to speak, walk and eat, sleeping problems, seizures and even the ability to breathe easily. Rett syndrome affects approximately 1 in every 10,000-15,000 females. |

| ● | Depression - Depression is a major cause of morbidity worldwide according to the World Health Organization. Pharmaceutical treatment for depression is dominated by blockbuster brands, with the leading nine brands accounting for approximately 75% of total sales. However, the dominance of the leading brands is waning, largely due to the effects of patent expiration and generic competition. |

9

| ● | Epilepsy - Epilepsy is a common chronic neurological disorder characterized by recurrent unprovoked seizures. These seizures are transient signs and/or symptoms of abnormal, excessive or synchronous neuronal activity in the brain. According to the Centers for Disease Control and Prevention, epilepsy affects 3.4 million Americans. Today, epilepsy is often controlled, but not cured, with medication that is categorized as older traditional anti-epileptic drugs and second generation anti-epileptic drugs. Because epilepsy afflicts sufferers in different ways, there is a need for drugs used in combination with both traditional anti-epileptic drugs and second generation anti-epileptic drugs. GBI Research estimates that the epilepsy market will increase to $4.5 billion by 2019. |

| ● | Neuropathic Pain – We define neuralgia, or neuropathic pain, as pain that is not related to activation of pain receptor cells in any part of the body. Neuralgia is more difficult to treat than some other types of pain because it does not respond well to normal pain medications. Special medications have become more specific to neuralgia and typically fall under the category of membrane stabilizing drugs or antidepressants. |

Cancer

| ● | Malignant Melanoma - Predominantly a skin cancer, malignant melanoma can also occur in melanocytes found in the bowel and the eye. Malignant melanoma accounts for 75% of all deaths associated with skin cancer. The treatment includes surgical removal of the tumor, adjuvant treatment, chemo and immunotherapy, or radiation therapy. According to IMS Health the worldwide malignant melanoma market is expected to grow to $4.4 billion by 2022. |

| ● | Prostate Cancer – Specific to men, prostate cancer is a form of cancer that develops in the prostate, a gland in the male reproductive system. The cancer cells may metastasize from the prostate to other parts of the body, particularly the bones and lymph nodes. Drug therapeutics for prostate cancer are expected to increase to nearly $13.5 billion in 2024 according to Datamonitor Healthcare. |

| ● | Pancreatic Cancer - Pancreatic cancer is a malignant neoplasm of the pancreas. In the United States, approximately 55,000 new cases of pancreatic cancer will be diagnosed this year and approximately 44,000 patients will die as a result of their cancer, according to the American Cancer Society. Sales predictions by GBI Research forecast that the market for the pharmaceutical treatment of pancreatic cancer in the United States and five largest European countries will increase to $2.9 billion by 2021. |

Competition

The pharmaceutical industry is intensely competitive.

At this time, our competitors are other biomedical development companies that are trying to discover and develop compounds to be used in the treatment of Alzheimer’s disease and other CNS diseases, and those companies already doing so. Those companies include Biogen (NASDAQ:BIIB), Axovant Sciences Ltd. (NYSE: AXON), Perrigo Company Plc (NYSE:PRGO), Pfizer Inc. (NYSE:PFE), Allergan Plc (NYSE:AGN), Novartis AG (NYSE:NVS), GlaxoSmithKline Plc (NYSE:GSK), Merck & Co. Inc. (NYSE:MRK), Eli Lilly & Co. (NYSE: LLY), Johnson & Johnson (NYSE:JNJ) and Roche Holding AG (VTX:ROG). For additional discussion of the risks related to competition, see Item 1A “Risk Factors.”

Patents, Trademarks and Intellectual Property

Anavex holds ownership or exclusive rights to four U.S. patents, nine U.S. patent applications, and various PCT or ex-U.S. patent applications relating to our drug candidates, methods associated therewith, and to our research programs.

We own one issued U.S. patent entitled “ANAVEX®2-73 and certain anticholinesterase inhibitors composition and method for neuroprotection” claims a composition of matter of ANAVEX®2-73 directed to a novel and synergistic neuroprotective compound combined with donepezil and other cholinesterase inhibitors. This patent is expected to expire in June 2034, absent any patent term extension for regulatory delays. A related continuation application is also pending in the U.S. In addition, we own one issued U.S. Patent with claims directed to methods of treating melanoma with a compound related to ANAVEX®2-73. This patent is expected to expire in February 2030, absent any patent term extension for regulatory delays.

10

With regard to ANAVEX®3-71, we own exclusive rights to two issued U.S. patents with claims respectively directed to the ANAVEX®3-71 compound and methods of treating various diseases including Alzheimer’s with the same. These patents are expected to expire in April 2030, and January 2030, respectively, absent any patent term extension for regulatory delays. We also own exclusive rights to related patents or applications that are granted or pending in Australia, Canada, China, Europe, Japan, Korea, New Zealand, Russia, and South Africa, and are expected to expire in January 2030.

We also own other patent applications directed to enantiomers, formulations and uses that may provide additional protection for one or more of our product candidates.

We regard patents and other intellectual property rights as corporate assets. Accordingly, we attempt to optimize the value of intellectual property in developing our business strategy including the selective development, protection, and exploitation of our intellectual property rights. In addition to filings made with intellectual property authorities, we protect our intellectual property and confidential information by means of carefully considered processes of communication and the sharing of information, and by the use of confidentiality and non-disclosure agreements and provisions for the same in contractor’s agreements. While no agreement offers absolute protection, such agreements provide some form of recourse in the event of disclosure, or anticipated disclosure.

Our intellectual property position, like that of many biomedical companies, is uncertain and involves complex legal and technical questions for which important legal principles are unresolved. For more information regarding challenges to our existing or future patents, see Item 1A “Risk Factors.”

Government Approval

Regulation by governmental authorities in the United States and foreign countries is a significant factor in the development, manufacture, and expected marketing of our potential drug compounds and in potential future research and development activities. The nature and extent to which such regulation will apply to us will vary depending on the nature of any potential drug compounds developed. We anticipate that all of our potential drug compounds will require regulatory approval by governmental agencies prior to commercialization.

The process of obtaining these approvals and the subsequent compliance with the appropriate federal statutes and regulations requires substantial time and financial resources. For more information regarding the risks related to obtaining government approvals, see Item 1A “Risk Factors.”

The steps ordinarily required before a new drug may be marketed in the United States, which are similar to steps required in most other countries, include:

| ● | non-clinical laboratory tests, non-clinical studies in animals, formulation studies and the submission to the FDA of an IND; |

| ● | adequate and well-controlled clinical trials to establish the safety and efficacy of the drug; |

| ● | the submission of a new drug application, or NDA, or biologic license application, or BLA, to the FDA; and |

| ● | FDA review and approval of the New Drug Application (NDA) or biologics license application (BLA). |

11

Non-clinical tests include laboratory evaluation of potential drug compound chemistry, formulation and toxicity, as well as animal studies. The results of non-clinical testing are submitted to the FDA as part of an IND. A 30-day waiting period after the filing of each IND is required prior to commencement of clinical testing in humans. At any time during the 30-day period or at any time thereafter, the FDA may halt proposed or ongoing clinical trials until the FDA authorizes trials under specified terms. The FDA may require additional animal testing after an initial IND is approved and prior to Phase III trials.

Clinical trials to support NDAs are typically conducted in three sequential phases, although the phases may overlap. During Phase I, clinical trials are conducted with a small number of subjects to assess metabolism, pharmacokinetics, and pharmacological actions and safety, including side effects associated with increasing doses. Phase II usually involves studies in a limited patient population to assess the efficacy of the drug in specific, targeted indications; assess dosage tolerance and optimal dosage; and identify possible adverse effects and safety risks.

If a compound is found to be potentially effective and to have an acceptable safety profile in Phase I and II evaluations, Phase III trials are undertaken to further demonstrate clinical efficacy and to further test for safety within an expanded patient population at geographically dispersed clinical trial sites.

After successful completion of the required clinical trials, a NDA is generally submitted. The FDA may request additional information before accepting the NDA for filing, in which case the NDA must be resubmitted with the additional information. Once the submission has been accepted for filing, the FDA reviews the NDA and responds to the applicant. The FDA’s requests for additional information or clarification often significantly extends the review process. The FDA may refer the NDA to an appropriate advisory committee for review, evaluation, and recommendation as to whether the NDA should be approved, although the FDA is not bound by the recommendation of an advisory committee.

Under the United States Orphan Drug Act, a sponsor may request that the FDA designate a drug intended to treat a “rare disease or condition” as an “orphan drug.” A “rare disease or condition” is one which affects less than 200,000 people in the United States, or which affects more than 200,000 people, but for which the cost of developing and making available the product is not expected to be recovered from sales of the product in the United States. Upon the approval of the first NDA or BLA for a drug designated as an orphan drug for a specified indication, the sponsor of that NDA or BLA is entitled to seven years of exclusive marketing rights in the United States unless the sponsor cannot assure the availability of sufficient quantities to meet the needs of persons with the disease. However, orphan drug status is particular to the approved indication and does not prevent another company from seeking approval of an off-patent drug that has other labeled indications that are not under orphan or other exclusivities. Orphan drugs may also be eligible for federal income tax credits for costs associated with the drugs’ development. In order to increase the development and marketing of drugs for rare disorders, regulatory bodies outside the United States have enacted regulations similar to the Orphan Drug Act.

Sales outside the United States of potential drug compounds we develop will also be subject to foreign regulatory requirements governing human clinical trials and marketing for drugs. The requirements vary widely from country to country, but typically the registration and approval process takes several years and requires significant resources. In most cases, if the FDA has not approved a potential drug compound for sale in the United States, the potential drug compound may be exported for sale outside of the United States, only if it has been approved in any one of the following: the European Union, Canada, Australia, New Zealand, Japan, Israel, Switzerland and South Africa. There are specific FDA regulations that govern this process.

12

Research and Development Expenses

Historically, a significant portion of our operating expenses has related to research and development. See our Consolidated Financial Statements contained elsewhere in this Annual Report for costs and expenses related to research and development, and other financial information for fiscal years 2018, 2017 and 2016.

Scientific Advisors

We are advised by scientists and physicians with experience relevant to our Company and our product candidates. Our scientific advisors include clinicians and scientists who are affiliated with a number of highly regarded medical institutions.

Employees

We currently have thirteen full-time employees, and we retain several independent contractors on an as-needed basis. We believe that we have good relations with our employees.

Available Information

Our internet website address is www.anavex.com. Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to section 13(a) or 15(d) of the Exchange Act are available free of charge through our website. We include our website address in this report only as an inactive textual reference and do not intend it to be an active link to our website. The contents of our website are not incorporated into this report.

In addition to other information in this Annual Report on Form 10-K, the following risk factors should be carefully considered in evaluating our business because such factors may have a significant impact on our business, operating results, liquidity and financial condition. As a result of the risk factors set forth below, actual results could differ materially from those projected in any forward-looking statements. Additional risks and uncertainties not presently known to us, or that we currently consider to be immaterial, may also impact our business, operating results, liquidity and financial condition. If any such risks occur, our business, operating results, liquidity and financial condition could be materially affected in an adverse manner. Under such circumstances, the trading price of our securities could decline, and you may lose all or part of your investment.

Risks Related to our Company

We have had a history of losses and no revenue, which raise substantial doubt about our ability to continue as a going concern.

Since inception on January 23, 2004 through September 30, 2018, we have an accumulated deficit of $108,931,967. We can offer no assurance that we will ever operate profitably or that we will generate positive cash flow in the future. To date, we have not generated any revenues from our operations. Our history of losses and no revenues raise substantial doubt about our ability to continue as a going concern. As a result, our management expects the business to continue to experience negative cash flows for the foreseeable future and cannot predict when, if ever, our business might become profitable. We will need to raise additional funds, and such funds may not be available on commercially acceptable terms, if at all. If we are unable to raise funds on acceptable terms, we may not be able to execute our business plan, take advantage of future opportunities, or respond to competitive pressures or unanticipated requirements. This may seriously harm our business, financial condition and results of operations.

13

We are an early stage pharmaceutical research and development company and may never be able to successfully develop marketable products or generate any revenue. We have a very limited relevant operating history upon which an evaluation of our performance and prospects can be made. There is no assurance that our future operations will result in profits. If we cannot generate sufficient revenues, we may suspend or cease operations.

We are an early stage company and have not generated any revenues to date and have no operating history. All of our potential drug compounds are in the concept stage or early clinical development stage. Moreover, we cannot be certain that our research and development efforts will be successful or, if successful, that our potential drug compounds will ever be approved for sales to pharmaceutical companies or generate commercial revenues. We have no relevant operating history upon which an evaluation of our performance and prospects can be made. We are subject to all of the business risks associated with a new enterprise, including, but not limited to, risks of unforeseen capital requirements, failure of potential drug compounds either in non-clinical testing or in clinical trials, failure to establish business relationships and competitive disadvantages against larger and more established companies. If we fail to become profitable, we may suspend or cease operations.

We will need additional funding and may be unable to raise additional capital when needed, which would force us to delay, reduce or eliminate our research and development activities.

We will need to raise additional funding and the current economic conditions may have a negative impact on our ability to raise additional needed capital on terms that are favorable to our Company or at all. We may not be able to generate significant revenues for several years, if at all. Until we can generate significant revenues, if ever, we expect to satisfy our future cash needs through equity or debt financing. We cannot be certain that additional funding will be available on acceptable terms, or at all. If adequate funds are not available, we may be required to delay, reduce the scope of, or eliminate one or more of our research and development activities.

Risks Related to our Business

Even if we are able to develop our potential drug compounds, we may not be able to receive regulatory approval, or if approved, we may not be able to generate significant revenues or successfully commercialize our products, which will adversely affect our financial results and financial condition and we will have to delay or terminate some or all of our research and development plans which may force us to cease operations.

All of our potential drug compounds will require extensive additional research and development, including non-clinical testing and clinical trials, as well as regulatory approvals, before we can market them. In particular, human therapeutic products are subject to rigorous non-clinical and clinical testing and other approval procedures of the FDA and similar regulatory authorities in other countries. Various federal statutes and regulations also govern or influence testing, manufacturing, safety, labeling, storage, and record-keeping related to such products and their marketing. We cannot predict if or when any of the potential drug compounds we intend to develop will be approved for marketing. There are many reasons that we may fail in our efforts to develop our potential drug compounds. These include:

| ● | the possibility that non-clinical testing or clinical trials may show that our potential drug compounds are ineffective and/or cause harmful side effects; |

| ● | our potential drug compounds may prove to be too expensive to manufacture or administer to patients; |

| ● | our potential drug compounds may fail to receive necessary regulatory approvals from the United States Food and Drug Administration or foreign regulatory authorities in a timely manner, or at all; |

| ● | even if our potential drug compounds are approved, we may not be able to produce them in commercial quantities or at reasonable costs; |

| ● | even if our potential drug compounds are approved, they may not achieve commercial acceptance; |

14

| ● | regulatory or governmental authorities may apply restrictions to any of our potential drug compounds, which could adversely affect their commercial success; and |

| ● | the proprietary rights of other parties may prevent us or our potential collaborative partners from marketing our potential drug compounds. |

If we fail to develop our potential drug compounds, our financial results and financial condition will be adversely affected, we will have to delay or terminate some or all of our research and development plans and may be forced to cease operations.

Our research and development plans will require substantial additional future funding which could impact our operations and financial condition. Without the required additional funds, we will likely cease operations.

It will take several years before we can develop potentially marketable products, if at all. Our research and development plans will require substantial additional capital, arising from costs to:

| ● | conduct research, non-clinical testing and human studies; |

| ● | establish pilot scale and commercial scale manufacturing processes and facilities; and |

| ● | establish and develop quality control, regulatory, marketing, sales, finance and administrative capabilities to support these programs. |

Our future operating and capital needs will depend on many factors, including:

| ● | the pace of scientific progress in our research and development programs and the magnitude of these programs; |

| ● | the scope and results of pre-clinical testing and human studies; |

| ● | the time and costs involved in obtaining regulatory approvals; |

| ● | the time and costs involved in preparing, filing, prosecuting, securing, maintaining and enforcing patents; |

| ● | competing technological and market developments; |

| ● | our ability to establish additional collaborations; |

| ● | changes in our existing collaborations; |

| ● | the cost of manufacturing scale-up; and |

| ● | the effectiveness of our commercialization activities. |

We base our outlook regarding the need for funds on many uncertain variables. Such uncertainties include the success of our research initiatives, regulatory approvals, the timing of events outside our direct control such as negotiations with potential strategic partners and other factors. Any of these uncertain events can significantly change our cash requirements as they determine such one-time events as the receipt or payment of major milestones and other payments.

Additional funds will be required to support our operations and if we are unable to obtain them on favorable terms, we may be required to cease or reduce further research and development of our drug product programs, sell some or all our intellectual property, merge with another entity or cease operations.

If we fail to demonstrate efficacy in our non-clinical studies and clinical trials our future business prospects, financial condition and operating results will be materially adversely affected.

The success of our research and development efforts will be greatly dependent upon our ability to demonstrate potential drug compound efficacy in non-clinical studies, as well as in clinical trials. Non-clinical studies involve testing potential drug compounds in appropriate non-human disease models to demonstrate efficacy and safety. Regulatory agencies evaluate these data carefully before they will approve clinical testing in humans. If certain non-clinical data reveals potential safety issues or the results are inconsistent with an expectation of the potential drug compound’s efficacy in humans, the regulatory agencies may require additional more rigorous testing before allowing human clinical trials. This additional testing will increase program expenses and extend timelines. We may decide to suspend further testing on our potential drug compounds if, in the judgment of our management and advisors, the non-clinical test results do not support further development.

15

Moreover, success in non-clinical testing and early clinical trials does not ensure that later clinical trials will be successful, and we cannot be sure that the results of later clinical trials will replicate the results of prior clinical trials and non-clinical testing. The clinical trial process may fail to demonstrate that our potential drug compounds are safe for humans and effective for indicated uses. This failure would cause us to abandon a drug candidate and may delay development of other potential drug compounds. Any delay in, or termination of, our non-clinical testing or clinical trials will delay the filing of an IND and NDA with the Food and Drug Administration or the equivalent applications with pharmaceutical regulatory authorities outside the United States and, ultimately, our ability to commercialize our potential drug compounds and generate product revenues. In addition, we expect that our early clinical trials will involve small patient populations. Because of the small sample size, the results of these early clinical trials may not be indicative of future results. Also, the IND process may be extremely costly and may substantially delay the development of our potential drug compounds. Moreover, positive results of non-clinical tests will not necessarily indicate positive results in subsequent clinical trials.

Following successful non-clinical testing, potential drug compounds will need to be tested in a clinical development program to provide data on safety and efficacy prior to becoming eligible for product approval and licensure by regulatory agencies. From the first human trial through to regulatory approval can take many years and 10-12 years is not unusual for certain compounds.

If any of our future clinical development potential drug compounds become the subject of problems, our ability to sustain our development programs will become critically compromised. For example, efficacy or safety concerns may arise, whether or not justified, that could lead to the suspension or termination of our clinical programs. Examples of problems that could arise include, among others:

| ● | efficacy or safety concerns with the potential drug compounds, even if not justified; |

| ● | manufacturing difficulties or concerns; |

| ● | regulatory proceedings subjecting the potential drug compounds to potential recall; |

| ● | publicity affecting doctor prescription or patient use of the potential drug compounds; |

| ● | pressure from competitive products; or |

| ● | introduction of more effective treatments. |

Each clinical phase is designed to test attributes of the drug and problems that might result in the termination of the entire clinical plan can be revealed at any time throughout the overall clinical program. The failure to demonstrate efficacy in our clinical trials would have a material adverse effect on our future business prospects, financial condition and operating results.

If we do not obtain the support of qualified scientific collaborators, our revenue, growth and profitability will likely be limited, which would have a material adverse effect on our business.

We will need to establish relationships with leading scientists and research institutions. We believe that such relationships are pivotal to establishing products using our technologies as a standard of care for various indications. Additionally, although in discussion, there is no assurance that our current research partners will continue to work with us or that we will be able to attract additional research partners. If we are not able to establish scientific relationships to assist in our research and development, we may not be able to successfully develop our potential drug compounds. If this happens, our business will be adversely affected.

16

We may not be able to develop, market or generate sales of our products to the extent anticipated. Our business may fail and investors could lose all their investment in our Company.

Assuming that we are successful in developing our potential drug compounds and receiving regulatory clearances to market our products, our ability to successfully penetrate the market and generate sales of those products may be limited by a number of factors, including the following:

| ● | If our competitors receive regulatory approvals for and begin marketing similar products in the United States, the European Union, Japan and other territories before we do, greater awareness of their products as compared to ours will cause our competitive position to suffer; |

| ● | Information from our competitors or the academic community indicating that current products or new products are more effective or offer compelling other benefits than our future products could impede our market penetration or decrease our future market share; and |

| ● | The pricing and reimbursement environment for our future products, as well as pricing and reimbursement decisions by our competitors and by payers, may have an effect on our revenues. |

If this happens, our business will be adversely affected.

None of our potential drug compounds may reach the commercial market for a number of reasons and our business may fail.

Successful research and development of pharmaceutical products is high risk. Most products and development candidates fail to reach the market. Our success depends on the discovery of new drug compounds that we can commercialize. It is possible that our products may never reach the market for a number of reasons. They may be found ineffective or may cause harmful side-effects during non-clinical testing or clinical trials or fail to receive necessary regulatory approvals. We may find that certain products cannot be manufactured at a commercial scale and, therefore, they may not be economical to produce. Our potential products could also fail to achieve market acceptance or be precluded from commercialization by proprietary rights of third parties. Our patents, patent applications, trademarks and other intellectual property may be challenged, and this may delay or prohibit us from effectively commercializing our products. Furthermore, we do not expect our potential drug compounds to be commercially available for a number of years, if at all. If none of our potential drug compounds reach the commercial market, our business will likely fail and investors will lose all of their investment in our Company. If this happens, our business will be adversely affected.

If our competitors succeed in developing products and technologies faster or that are more effective or with a better profile than our own, or if scientific developments change our understanding of the potential scope and utility of our potential products, then our technologies and future products may be rendered undesirable or obsolete.

We face significant competition from industry participants that are pursuing technologies in similar disease states to those that we are pursuing and are developing pharmaceutical products that are competitive with our products. Nearly all of our industry competitors have greater capital resources, larger overall research and development staffs and facilities, and a longer history in drug discovery and development, obtaining regulatory approval and pharmaceutical product manufacturing and marketing than we do. With these additional resources, our competitors may be able to respond to the rapid and significant technological changes in the biotechnology and pharmaceutical industries faster than we can. Our future success will depend in large part on our ability to maintain a competitive position with respect to these technologies. Rapid technological development, as well as new scientific developments, may result in our products becoming obsolete before we can recover any of the expenses incurred to develop them. For example, changes in our understanding of the appropriate population of patients who should be treated with a targeted therapy like we are developing may limit the drug’s market potential if it is subsequently demonstrated that only certain subsets of patients should be treated with the targeted therapy.

17

Our reliance on third parties, such as university laboratories, contract manufacturing organizations and contract or clinical research organizations, may result in delays in completing, or a failure to complete, non-clinical testing or clinical trials if they fail to perform under our agreements with them.

In the course of product development, we may engage university laboratories, other biotechnology companies or contract or clinical manufacturing organizations to manufacture drug material for us to be used in non-clinical and clinical testing and contract research organizations to conduct and manage non-clinical and clinical studies. If we engage these organizations to help us with our non-clinical and clinical programs, many important aspects of this process have been and will be out of our direct control. If any of these organizations we may engage in the future fail to perform their obligations under our agreements with them or fail to perform non-clinical testing and/or clinical trials in a satisfactory manner, we may face delays in completing our clinical trials, as well as commercialization of any of our potential drug compounds. Furthermore, any loss or delay in obtaining contracts with such entities may also delay the completion of our clinical trials, regulatory filings and the potential market approval of our potential drug compounds.

If we fail to compete successfully with respect to partnering, licensing, mergers, acquisitions, joint venture and other collaboration opportunities, we may be limited in our ability to research and develop our potential drug compounds.

Our competitors compete with us to attract established biotechnology and pharmaceutical companies or organizations for partnering, licensing, mergers, acquisitions, joint ventures or other collaborations. Collaborations include contracting with academic research institutions for the performance of specific scientific testing. If our competitors successfully enter into partnering arrangements or license agreements with academic research institutions, we will then be precluded from pursuing those specific opportunities. Since each of these opportunities is unique, we may not be able to find a substitute. Other companies have already begun many drug development programs, which may target diseases that we are also targeting, and have already entered into partnering and licensing arrangements with academic research institutions, reducing the pool of available opportunities.

Universities and public and private research institutions also compete with us. While these organizations primarily have educational or basic research objectives, they may develop proprietary technology and acquire patent applications and patents that we may need for the development of our potential drug compounds. In some instances, we will attempt to license this proprietary technology, if available. These licenses may not be available to us on acceptable terms, if at all. If we are unable to compete successfully with respect to acquisitions, joint venture and other collaboration opportunities, we may be limited in our ability to develop new products.

The use of any of our products in clinical trials may expose us to liability claims, which may cost us significant amounts of money to defend against or pay out, causing our business to suffer.

The nature of our business exposes us to potential liability risks inherent in the testing, manufacturing and marketing of our products. We currently have one drug compound in clinical trials, however, when any of our products enter clinical trials or become marketed products, they could potentially harm people or allegedly harm people possibly subjecting us to costly and damaging product liability claims. Some of the patients who participate in clinical trials are already ill when they enter a trial or may intentionally or unintentionally fail to meet the exclusion criteria. The waivers we obtain may not be enforceable and may not protect us from liability or the costs of product liability litigation. Although we intend to obtain product liability insurance, which we believe is adequate, we are subject to the risk that our insurance will not be sufficient to cover claims. The insurance costs along with the defense or payment of liabilities above the amount of coverage could cost us significant amounts of money and management distraction from other elements of the business, causing our business to suffer.

18

If we are unable to safeguard against security breaches with respect to our information systems, our business may be adversely affected.

In the course of our business, we gather, transmit and retain confidential information through our information systems. Although we endeavor to protect confidential information through the implementation of security technologies, processes and procedures, it is possible that an individual or group could defeat security measures and access sensitive information about our business and employees. Any misappropriation, loss or other unauthorized disclosure of confidential information gathered, stored or used by us could have a material impact on the operation of our business, including damaging our reputation with our employees, third parties and investors. We could also incur significant costs implementing additional security measures and organizational changes, implementing additional protection technologies, training employees or engaging consultants. In addition, we could incur increased litigation as a result of any potential cyber-security breach. We are not aware that we have experienced any material misappropriation, loss or other unauthorized disclosure of confidential or personally identifiable information as a result of a cyber-security breach or other act, however, a cyber-security breach or other act and/or disruption to our information technology systems could have a material adverse effect on our business, prospects, financial condition or results of operations.

Risks Related to our Common Stock