Table of Contents

As filed with the Securities and Exchange Commission on April 20, 2016

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 20-F

(Mark One)

| ¨ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

or

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2015

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

or

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number: 000-51138

GRAVITY CO., LTD.

(Exact name of registrant as specified in its charter)

| N/A | The Republic of Korea | |

| (Translation of registrant’s name into English) | (Jurisdiction of incorporation or organization) |

15F, 396 World Cup buk-ro, Mapo-gu,

Seoul 121-795, Korea

(Address of principal executive offices)

Heung Gon Kim

Chief Financial Officer

15F, 396 World Cup buk-ro, Mapo-gu,

Seoul 121-795, Korea

Telephone: 82-2-2132-7000

Fax: 82-2-2132-7070

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of Each Exchange on Which Registered | |

| Common stock, par value Won 500 per share* | The NASDAQ Capital Market | |

| American depositary shares, each representing two shares of common stock |

| * | Not for trading, but only in connection with the listing of American depositary shares on the NASDAQ Capital Market pursuant to the requirements of the Securities and Exchange Commission. |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: Shares, par value Won 500: 6,948,900

Indicated by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No þ

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer ¨ | Non-accelerated filer þ |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP þ International Financial Reporting Standards as issued by the International Accounting Standards Board ¨ Other ¨

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ¨ Item 18 ¨

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

Table of Contents

| 4 | ||||||

| 4 | ||||||

| 6 | ||||||

| 6 | ||||||

| 6 | ||||||

| 6 | ||||||

| 6 | ||||||

| 8 | ||||||

| 8 | ||||||

| 8 | ||||||

| 26 | ||||||

| 26 | ||||||

| 27 | ||||||

| 61 | ||||||

| 61 | ||||||

| 61 | ||||||

| 61 | ||||||

| 62 | ||||||

| 78 | ||||||

| 80 | ||||||

| 80 | ||||||

| 80 | ||||||

| 80 | ||||||

| 82 | ||||||

| 82 | ||||||

| 82 | ||||||

| 84 | ||||||

| 85 | ||||||

| 87 | ||||||

| 89 | ||||||

| 90 | ||||||

| 90 | ||||||

| 90 | ||||||

| 94 | ||||||

| 94 | ||||||

| 94 | ||||||

| 95 | ||||||

| 95 | ||||||

| 95 | ||||||

| 96 | ||||||

| 96 | ||||||

| 96 | ||||||

| 96 | ||||||

| 96 | ||||||

| 96 | ||||||

| 96 | ||||||

| 97 | ||||||

| 102 | ||||||

| 104 | ||||||

| 106 | ||||||

2

Table of Contents

3

Table of Contents

Unless the context otherwise requires, references in this annual report on Form 20-F (this “Annual Report”) to:

| • | “ADRs” are to the American depositary receipts that evidence our ADSs; |

| • | “ADSs” are to our American depositary shares, each of which represents two shares of our common stock; |

| • | “China” or the “PRC” are to the People’s Republic of China (excluding, for the purposes of this annual report on Form 20-F, Taiwan, Hong Kong and Macau, unless specifically indicated otherwise); |

| • | “Chinese Yuan” are to the currency of China; |

| • | “EUR” or “Euro” are to the currency of the Eurozone consisting of Austria, Belgium, Cyprus, Estonia, Finland, France, Germany, Greece, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, the Netherlands, Portugal, Slovakia, Slovenia and Spain; |

| • | “Gravity,” “the Company,” “we,” “us,” “our,” or “our company” are to Gravity Co., Ltd. and our subsidiaries, except as otherwise indicated or required by context; |

| • | “Hong Kong” are to the Hong Kong Special Administrative Region of the PRC; |

| • | “Japanese Yen” or “JPY” are to the currency of Japan; |

| • | “Korea” are to the Republic of Korea; |

| • | “Macau” are to the Macau Special Administrative Region of the PRC; |

| • | “NT dollar” or “NT$” are to the currency of Taiwan; |

| • | “Taiwan” or the “ROC” are to Taiwan, the Republic of China; |

| • | “Thai Baht” are to the currency of the Kingdom of Thailand; |

| • | “US$,” “U.S. dollar,” or “Dollar” are to the currency of the United States of America; and |

| • | “Won,” “Korean Won,” or “ |

For your convenience, and unless otherwise stated, this Annual Report contains translations of certain Won amounts into U.S. dollars at the noon buying rate in New York City for cable transfers in Korean Won as certified by the Federal Reserve Bank of New York for customs purposes in effect on December 31, 2015, which was Won 1,169.26 to US$1.00. No assurance is given that any Won or Dollar amounts could have been or may now be converted into Dollars or Won, as the case may be, at such rate, or any other rate, or at all.

Discrepancies in tables between totals and sums of the amounts listed are due to rounding.

This Annual Report for the year ended December 31, 2015 contains “forward- looking statements,” as defined in Section 27A of the U.S. Securities Act of 1933, as amended, or the “Securities Act,” and Section 21E of the U.S. Securities Exchange Act of 1934, as amended, or the “Exchange Act.” The forward-looking statements are based on our current expectations, assumptions, estimates and projections about us and our industry, and are subject to various risks and uncertainties. Generally, these forward-looking statements can be identified by the use of forward-looking terminology such as “anticipate,” “believe,” “considering,” “depends,” “estimate,” “expect,” “intend,” “plan,” “planning,” “planned,” “predict,” “project,” “continue” and variations of these words, similar expressions, or that certain events, actions or results “will,” “may,” “might,” “should,” “would” or “could” occur, be taken or be achieved.

4

Table of Contents

Forward-looking statements include, but are not limited to, the following:

| • | future prices of and demand for our products; |

| • | future earnings and cash flow; |

| • | estimated development and commercial launch schedule of our games in development; |

| • | our ability to attract new customers and retain existing customers; |

| • | the expected growth of the Korean and worldwide online gaming industry; |

| • | the effect that economic, political or social conditions in Korea have on the revenue generated from our online or mobile game products and our results of operations; |

| • | the effect that any global financial crisis or global economic recession will or may have on our business prospects, financial condition and results of operations; and |

| • | our future business development and prospects, results of operations and financial condition. |

We caution you not to place undue reliance on any forward-looking statement, each of which involves risks and uncertainties. Although we believe that the assumptions on which our forward-looking statements are based are reasonable, any of those assumptions could prove to be inaccurate, and as a result, the forward-looking statements based on those assumptions could be incorrect. All forward-looking statements are based on our management’s current expectations, assumptions, estimates and projections of future events and are subject to a number of factors that could cause actual results to differ materially from those described in the forward-looking statements. Risks and uncertainties associated with our business include, but are not limited to, risks related to changes in the regulatory environment; technology changes; potential litigation and governmental actions; changes in the competitive environment; changes in customer preference and popular culture and trends, including the online or mobile gaming culture; political changes; global economic events including, but not limited to, a significant downturn in the global economic and financial markets and a tightening of the global credit markets; changes in business and economic conditions; fluctuations in foreign exchange rates; fluctuations in the prices of our products; decreasing consumer confidence and slowing of economic growth generally; and other risks and uncertainties that are more fully described under the heading “Risk Factors” in this Annual Report, and elsewhere in this Annual Report. In light of these and other uncertainties, you should not conclude that we will necessarily achieve any plans and objectives or projected financial results referred to in any of the forward-looking statements. Except as required by law, we undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. All subsequent forward-looking statements attributable to us or any person acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this section.

5

Table of Contents

| ITEM 1. | IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS |

Not applicable.

| ITEM 2. | OFFER STATISTICS AND EXPECTED TIMETABLE |

Not applicable.

| ITEM 3. | KEY INFORMATION |

| ITEM 3.A. | SELECTED FINANCIAL DATA |

You should read the selected financial data below in conjunction with our audited consolidated financial statements as of December 31, 2014 and 2015 and for the years ended December 31, 2013, 2014 and 2015, and the related notes included elsewhere in this Annual Report. The selected financial data as of December 31, 2014 and 2015 and for the years ended December 31, 2013, 2014 and 2015 are derived from our audited consolidated financial statements and the related notes thereto included elsewhere in this Annual Report. Our historical results do not necessarily indicate results expected for any future periods. Our financial statements are prepared in accordance with accounting principles generally accepted in the United States of America, or “U.S. GAAP.”

| As of and for the Years Ended December 31, | ||||||||||||||||||||||||

| 2011 | 2012 | 2013 | 2014 | 2015 | 2015(1) | |||||||||||||||||||

| (In millions of Won and thousands of US$, except share and per share data, operating data and percentages) |

||||||||||||||||||||||||

| Statements of operations |

||||||||||||||||||||||||

| Revenues: |

||||||||||||||||||||||||

| Online games—subscription revenue |

US$ | 5,577 | ||||||||||||||||||||||

| Online games—royalties and license fees |

35,552 | 32,325 | 21,726 | 13,093 | 11,010 | 9,416 | ||||||||||||||||||

| Mobile games and applications |

6,609 | 8,262 | 14,504 | 15,055 | 15,078 | 12,895 | ||||||||||||||||||

| Character merchandising, animation and other revenue |

3,760 | 7,044 | 3,249 | 3,779 | 3,051 | 2,609 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total revenues |

57,477 | 57,781 | 47,685 | 39,889 | 35,660 | 30,497 | ||||||||||||||||||

| Cost of revenues |

24,243 | 34,906 | 35,399 | 34,188 | 30,282 | 25,898 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Gross profit |

33,234 | 22,875 | 12,286 | 5,701 | 5,378 | 4,599 | ||||||||||||||||||

| Operating expenses: |

||||||||||||||||||||||||

| Selling, general and administrative |

22,759 | 20,310 | 17,063 | 12,682 | 11,481 | 9,819 | ||||||||||||||||||

| Research and development |

4,136 | 7,018 | 6,131 | 4,847 | 5,277 | 4,513 | ||||||||||||||||||

| Impairment loss on intangible assets |

3,697 | 14,569 | 5,822 | 1 | 5,849 | 5,002 | ||||||||||||||||||

| Gain on disposal of equity method investments |

— | (528 | ) | — | — | — | — | |||||||||||||||||

| Gain on loss of control in a subsidiary |

(548 | ) | — | — | — | — | — | |||||||||||||||||

| Settlement cost of litigation |

29 | — | — | — | — | — | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Operating income (loss) |

3,161 | (18,494 | ) | (16,730 | ) | (11,829 | ) | (17,229 | ) | (14,735 | ) | |||||||||||||

| Other income, net |

1,876 | 871 | 2,105 | 977 | 1,551 | 1,327 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Income (loss) before income tax expenses (benefit) and equity loss on investments |

5,037 | (17,623 | ) | (14,625 | ) | (10,852 | ) | (15,678 | ) | (13,408 | ) | |||||||||||||

| Income tax expenses (benefit) |

(7,962 | ) | 2,584 | 5,108 | 10,147 | 1,351 | 1,155 | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Income (loss) before equity loss on investments |

12,999 | (20,207 | ) | (19,733 | ) | (20,999 | ) | (17,029 | ) | (14,563 | ) | |||||||||||||

| Equity loss on investments, net |

(242 | ) | (333 | ) | (18 | ) | — | — | — | |||||||||||||||

| Net income (loss) |

12,757 | (20,540 | ) | (19,751 | ) | (20,999 | ) | (17,029 | ) | (14,563 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net income (loss) attributable to: |

||||||||||||||||||||||||

| Non-controlling interest |

(2,171 | ) | (8,316 | ) | (1,163 | ) | (92 | ) | (64 | ) | (55 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Parent company |

US$ | (14,508 | ) | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

6

Table of Contents

| As of and for the Years Ended December 31, | ||||||||||||||||||||||||

| 2011 | 2012 | 2013 | 2014 | 2015 | 2015(1) | |||||||||||||||||||

| (In millions of Won and thousands of US$, except share and per share data, operating data and percentages) |

||||||||||||||||||||||||

| Earnings (loss) per share: |

||||||||||||||||||||||||

| Basic and diluted per share |

US$ | (2.09 | ) | |||||||||||||||||||||

| Basic and diluted per ADS(2) |

4,296 | (3,518 | ) | (5,350 | ) | (6,018 | ) | (4,882 | ) | (4.18 | ) | |||||||||||||

| Weighted average number of shares outstanding (basic and diluted) |

6,948,900 | 6,948,900 | 6,948,900 | 6,948,900 | 6,948,900 | 6,948,900 | ||||||||||||||||||

| Other comprehensive income (loss) Foreign currency translation adjustment |

(510 | ) | (41 | ) | (1,327 | ) | (153 | ) | (827 | ) | (707 | ) | ||||||||||||

| Comprehensive income (loss) |

12,247 | (20,581 | ) | (21,078 | ) | (21,152 | ) | (17,856 | ) | (15,270 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Comprehensive income (loss) attributable to: |

||||||||||||||||||||||||

| Non-controlling interest |

(2,171 | ) | (8,316 | ) | (1,163 | ) | (92 | ) | (64 | ) | (55 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Parent company |

US$ | (15,215 | ) | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Balance sheet data: |

||||||||||||||||||||||||

| Cash and cash equivalents |

US$ | 21,303 | ||||||||||||||||||||||

| Total current assets |

71,833 | 67,929 | 58,651 | 50,692 | 43,676 | 37,353 | ||||||||||||||||||

| Property and equipment, net |

2,731 | 3,524 | 2,315 | 1,213 | 882 | 754 | ||||||||||||||||||

| Total assets |

132,878 | 110,555 | 87,765 | 63,096 | 45,729 | 39,110 | ||||||||||||||||||

| Total current liabilities |

12,062 | 10,375 | 11,400 | 9,651 | 8,804 | 7,530 | ||||||||||||||||||

| Total liabilities |

22,219 | 20,477 | 18,765 | 15,248 | 15,737 | 13,460 | ||||||||||||||||||

| Total parent company shareholders’ equity |

101,834 | 89,569 | 69,335 | 48,275 | 30,483 | 26,071 | ||||||||||||||||||

| Non-controlling interest |

8,825 | 509 | (335 | ) | (427 | ) | (491 | ) | (421 | ) | ||||||||||||||

| Total equity |

110,659 | 90,078 | 69,000 | 47,848 | 29,992 | 25,650 | ||||||||||||||||||

| Selected operating data and financial ratios (unaudited): |

||||||||||||||||||||||||

| Gross profit margin(3) |

57.8 | % | 39.6 | % | 25.8 | % | 14.3 | % | 15.1 | % | 15.1 | % | ||||||||||||

| Operating profit (loss) margin(4) |

5.5 | % | (32.0 | )% | (35.1 | )% | (29.7 | )% | (48.3 | )% | (48.3 | )% | ||||||||||||

| Net profit (loss) margin(5) |

26.0 | % | (21.2 | )% | (39.0 | )% | (52.4 | )% | (47.6 | )% | (47.6 | )% | ||||||||||||

Notes:

| (1) | For convenience only, the Won amounts are expressed in U.S. dollars at the rate of Won 1,169.26 to US$1.00, the noon buying rate in effect on December 31, 2015 as certified by the Federal Reserve Bank of New York for customs purposes. |

| (2) | Each ADS represents two shares of our common stock. On May 11, 2015, we effected a change of our ADS to common shares ratio from four ADSs to one common share (4:1) to one ADS to two common shares (1:2), which had the effect of a 1-for-8 reverse split of our ADSs. For ease of comparison purposes, the earnings per ADS values before such ratio change on May 11, 2015 have been retroactively adjusted to reflect this ratio change. |

| (3) | Gross profit margin for each period is calculated by dividing gross profit by total net revenues for each period. |

| (4) | Operating profit (loss) margin for each period is calculated by dividing operating income (loss) by total net revenues for each period. |

| (5) | Net profit margin (loss) for each period is calculated by dividing net income (loss) attributable to parent company by total net revenues for each period. |

7

Table of Contents

Exchange Rate Information

The following table sets forth information concerning the noon buying rate as certified by the Federal Reserve Bank of New York for customs purposes for the years 2011 through 2015 and for each month and period indicated, expressed in Won per U.S. dollar.

| Period |

At End of Period | Average Rate(1) | High | Low | ||||||||||||

| 2011 |

1,158.5 | 1,105.2 | 1,197.5 | 1,049.2 | ||||||||||||

| 2012 |

1,063.2 | 1,119.6 | 1,185.0 | 1,063.2 | ||||||||||||

| 2013 |

1,055.3 | 1,094.6 | 1,161.3 | 1,050.1 | ||||||||||||

| 2014 |

1,090.9 | 1,054.0 | 1,117.7 | 1,008.9 | ||||||||||||

| 2015 |

1,169.3 | 1,133.7 | 1,196.4 | 1,063.0 | ||||||||||||

| October |

1,140.5 | 1,143.2 | 1,180.0 | 1,120.9 | ||||||||||||

| November |

1,149.4 | 1,153.5 | 1,172.7 | 1,136.5 | ||||||||||||

| December |

1,169.3 | 1,169.9 | 1,188.0 | 1,140.7 | ||||||||||||

| 2016 |

||||||||||||||||

| January |

1,210.0 | 1,203.3 | 1,217.0 | 1,190.4 | ||||||||||||

| February |

1,238.1 | 1,216.2 | 1,242.6 | 1,186.1 | ||||||||||||

| March |

1,138.9 | 1,181.6 | 1,229.6 | 1,138.9 | ||||||||||||

| April (through April 8) |

1,148.9 | 1,153.0 | 1,158.4 | 1,147.2 | ||||||||||||

Note:

| (1) | The average rates for the annual periods were calculated based on the average noon buying rate on the last business day of each month during the period. The average rates for the monthly periods (or portion thereof) were calculated based on the average noon buying rate of each business day of the month (or portion thereof). |

| ITEM 3.B. | CAPITALIZATION AND INDEBTEDNESS |

Not applicable.

| ITEM 3.C. | REASONS FOR THE OFFER AND USE OF PROCEEDS |

Not applicable.

| ITEM 3.D. | RISK FACTORS |

RISKS RELATING TO OUR BUSINESS

We currently depend on one online game product, Ragnarok Online, for a significant portion of our revenues.

A significant portion of our revenues has been and is currently derived from a single online game product, Ragnarok Online, which was commercially introduced in August 2002 and is currently commercially offered in 81 countries and markets. We derived Won 14,803 million (US$12,660 thousand) in revenues from Ragnarok Online in 2015 and Won 15,985 million in revenues from Ragnarok Online in 2014, representing approximately 41.5% and 40.1% of our total revenues in 2015 and 2014, respectively.

Ragnarok Online has been on the market for fourteen years and has reached maturity in most of our principal markets. The life cycle of an online game generally lasts between four and seven years, and online games typically reach their peak popularity within the first two years following their introduction, after which time the game’s usage gradually stabilizes and begins to decline over time. The number of users of Ragnarok Online worldwide reached its peak in the first quarter of 2005 and has declined since such time. Our failure to maintain, improve, update or enhance Ragnarok Online in a timely manner or successfully introduce it in new markets is likely to lead to a continual decline in Ragnarok Online’s user base and subscription revenues and royalties. This will likely lead to a decline in our overall revenues, which would materially and adversely affect our business, financial condition and results of operations.

8

Table of Contents

If we are unable to consistently and timely develop, acquire, license, launch, market or operate commercially successful online and mobile games in addition to Ragnarok Online, our business, financial condition and results of operations may be materially and adversely affected.

In order to grow our revenues and net income, we must retain our existing users and attract new users by developing, acquiring, licensing, launching, marketing or operating other commercially successful online and mobile games in addition to Ragnarok Online. In addition to Ragnarok Online, we currently offer four other online games: Ragnarok Online II, Requiem, R.O.S.E. Online and Dragonica, which is also known as Dragon Saga in the United States, Canada and South America except for Brazil. We also offer mobile games which are played using mobile devices and smartphones, including Google Android compatible phones, the Apple iPhone, other feature phones, and tablet computers. In January 2015, we entered into a development agreement with Shanghai The Dream Network Technology Co., Ltd., or “Dream Square,” to develop and distribute two mobile games in China based on the contents of Ragnarok Online. This agreement was amended in March 2016 to grant Dream Square an exclusive right to develop mobile and web games based on the contents of Ragnarok Online and distribute such games in China for five years from March 25, 2016.

None of our other online games to date has proven to be as commercially successful as Ragnarok Online, and none of our mobile games to date has achieved comparable commercial success. We stopped offering Steal Fighter and H.A.V.E. Online in February and March of 2014, respectively, after neither game achieved wide-spread popularity. Further, the limited market acceptance of Ragnarok Online II has resulted in financial losses, including the recognition of an impairment loss on intangible assets of Won 4,605 million in 2015, and the termination or amendment of license agreements with our licensees. Since April 2014, there have been terminations of various license agreements for service of Ragnarok Online II in the Philippines, Brazil, Singapore, Malaysia, Thailand, Vietnam, Japan and Indonesia. As part of the termination of the Ragnarok Online II license agreement in Japan with GungHo, US$5,000 thousand in initial payments received from GungHo will be refunded in four equal payments by the end of December 2017.

Although service of Ragnarok Online II in those jurisdictions will continue to be offered by our subsidiary, Gravity Interactive Inc., our termination of agreements with local licensees could adversely affect our revenues from Ragnarok Online II.

A game’s commercial success largely depends on appealing to the tastes and preferences of a critical mass of users as well as the willingness of such users to purchase the game and/or in-game items, and to continue as paying subscribers, all of which are difficult to predict prior to a game’s development and introduction. Developing games requires substantial development costs, including the costs of employing skilled developers and acquiring or developing game engines which enable the creation of games with the latest technological features. For us to succeed, we must acquire, license or develop promising games at acceptable costs and ensure technical support for the successful operation of such games. The online and mobile gaming industries are highly competitive, and we may not be able to acquire, license or develop promising games at acceptable costs. In order to successfully distribute and operate a game, we also need a sizable game management and support staff, continued investment in technology and a substantial marketing budget. We cannot assure you that the games we develop or publish will be attractive to users or otherwise be commercially successful, launched as scheduled or able to successfully compete with games operated by our competitors. If we are not able to consistently develop, acquire, license, launch, market or operate commercially successful games, we may not be able to generate enough revenues to offset our initial development, acquisition, licensing or marketing costs, and our business, financial condition and results of operation may be materially and adversely affected.

We depend on our overseas licensees for a substantial portion of our revenues and rely on them to distribute, market and operate our games, and comply with applicable laws and government regulations.

In markets other than Korea, the United States, Canada and certain other countries in which we or our subsidiaries directly publish our games, we license our games to overseas operators or distributors for

9

Table of Contents

license fees and royalty payments based on a percentage of revenues generated from our games in such markets. Overseas license fees and royalty payments represented 30.9% of our total revenues in 2015 and 32.7% of our total revenues in 2014. In particular, we are heavily dependent on one licensee for a significant portion of our revenues. In 2015, 26.5% of our total revenues was derived from GungHo Online Entertainment, Inc., or “GungHo,” our licensee in Japan and our majority shareholder. Deterioration of our relationships with material licensees or material adverse changes in the terms of our licenses with such licensees will likely have a material adverse effect on our business, prospects, financial condition and results of operations. In addition, as we are heavily dependent on certain licensees, deterioration or any adverse developments in the operations, including changes in senior management, of our overseas licensees may materially and adversely affect our business, financial condition and results of operations.

Further, our overseas licensees generally have the exclusive right to distribute our games in their respective markets for a term of two or three years and may also operate or publish other online and mobile games developed or offered by our competitors, and we may not be able to easily terminate the license agreements as the agreements do not specify particular financial or performance criteria that need to be met by our licensees. If our overseas licensees devote greater time and resources to marketing their proprietary games or those of our competitors, we may not be able to terminate our license agreements or enter into a new license agreement with a different licensee, and our revenues and net profit may be adversely impacted. Also, a failure to satisfy our obligation to provide technical and other consulting services to the licensees under the license agreements may negatively affect user satisfaction and loyalty and hinder our licensees’ efforts to increase market share, which may lead the licensees to focus their attention on our competitors’ games or request modifications to or terminate our licensing agreements and/or not renew expired license agreements.

Our overseas licensees are responsible for remitting royalty payments to us based on a percentage of sales from our games after deducting certain expenses. Some licensees may be allowed to deduct certain expenses before calculating royalty payments depending on the terms of the applicable contracts. Failure by our licensees to maintain a stable and efficient billing, recording, distribution and payment collection network in their respective markets may result in inaccurate recording of sales or insufficient collection of payments from such markets and may materially and adversely affect our financial condition and results of operations. Although we have audit rights pursuant to our license agreements to ensure that proper payment amounts are being recorded and remitted, such activities can be disruptive and time consuming and as a result, we do not exercise such rights on a regular basis. Although we have taken a number of steps to improve our internal controls and compliance procedures to prevent inaccurate reporting and illicit diversion of payments, we cannot ensure that such incidents will not occur. Any future occurrence of such incidents may materially and adversely affect our business, financial condition and results of operations.

In addition, disruptions in the political environments in which our licensees operate may have a negative impact on the business of our licensees and in turn materially and adversely affect our results of operations and financial condition.

Furthermore, our overseas licensees are responsible for complying with local laws, including obtaining and maintaining the requisite government licenses and permits. Failure by our overseas licensees to do so may result in, among others, a suspension of service of our games in such market which may result in user complaints and a decrease in the use of our games which would likely have a material adverse effect on our business, financial condition and results of operations.

We operate in a highly competitive industry and compete against many large companies.

Increased competition in the online and mobile gaming industry from existing and potential competitors could make it difficult for us to retain existing users and attract new users, and could reduce the number of hours users spend playing our current or future games or cause us and our licensees to reduce the fees charged to play our current or future games. In some of our principal markets, such as

10

Table of Contents

Korea, Japan and Taiwan, growth of the market for online games has continued to be slow while competition remains strong. We expect more companies to enter the online and mobile game industries and a wider range of online and mobile games to be introduced in our current and future markets. If we are unable to compete effectively in our principal markets, our business, financial condition and results of operations could be materially and adversely affected.

Our competitors in the online and mobile game industries vary in size from small companies to very large companies with dominant market shares. Many of our competitors have significantly greater financial, marketing and game development resources than we have. As a result, we may not be able to devote adequate resources to develop, acquire or license new games, undertake extensive marketing campaigns, adopt aggressive pricing policies or adequately compensate our game developers or third-party game developers to the same degree as many of our competitors do.

As the online and mobile game industries are characterized by rapid technological changes, especially in the technical capabilities of devices for mobile games, and changing interests and preferences of users, continuous investment is required to develop and publish new games. Also, as the online and mobile game industries in many of our markets are rapidly evolving, our current or future competitors may adapt to the changing competitive landscape and market conditions and compete more successfully than us. In particular, online and mobile game products are becoming more similar to each other, thus becoming commoditized and undifferentiated. In this environment, larger companies with relative economies of scale have a clear advantage over smaller companies like us, as they are able to develop games in a more cost efficient manner, diversify their risks with a broader category of games and genres and increase their chances of offering widely popular games. In addition, any of our competitors may offer products and services that have significant performance, price, creativity or other advantages over those offered by us. These products and services may weaken the market strength of our brand name and achieve greater market acceptance than ours. In addition, any of our current or future competitors may be acquired by, receive investments from or enter into strategic relationships with larger, better established and better financed companies and therefore may be able to obtain significantly greater financial, marketing and game licensing and development resources than we can. See ITEM 4.B. “BUSINESS OVERVIEW—COMPETITION.”

Our investments in joint ventures or partnerships, or acquisitions of other companies, related to development or service of online and mobile games may not be successful.

Since 2004, we have made investments in joint ventures and entered into partnership arrangements with third parties to invest in online games. In many cases, the success of such joint ventures and partnership arrangements is heavily dependent on third parties and their investment decisions because we do not have significant voting or other control over such entities.

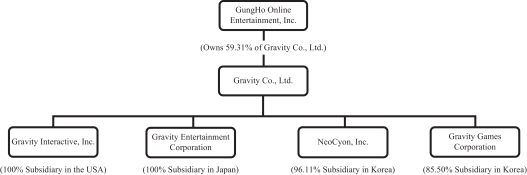

In October 2010, we acquired an aggregate of 50.83% of the total shares of Barunson Interactive Corporation, subsequently named Gravity Games Corporation, or “Gravity Games,” an online game developer in Korea, and increased our ownership in Gravity Games to 85.5% in August 2013. For details of impairment loss from Gravity Games, see ITEM 3.D. “RISK FACTORS—RISKS RELATING TO OUR BUSINESS—We could suffer losses due to asset impairment charges.” Gravity EU SASU, our former wholly-owned subsidiary in France, was converted into a joint venture company in which we had a 25% equity interest, Gravity EU SAS, with Media-Participations Paris SA as the joint venture partner, in July 2011. In November 2014, we sold our 25% equity interest in Gravity EU SAS to Dargaud SA.

If our partners or the joint ventures and partnerships in which we and our partners have invested or companies acquired by us are unable to manage their investments, develop promising online and/or mobile games or market or operate commercially successful online and/or mobile games, such joint ventures and partnerships or companies will be unable to attain their investment, development or other business objectives, which may materially and adversely affect the value of our investments and commitments and which may have a material adverse effect on our business, financial condition and results of operations.

11

Table of Contents

If we fail to hire and retain skilled and experienced game developers or other key personnel to design and develop new online and mobile games and additional game features, we may be unable to achieve our business objectives.

In order to meet our business objectives and maintain our competitiveness, we need to attract and retain qualified employees, including skilled and experienced online and mobile game developers. We compete to attract and retain key personnel with other companies in the online and mobile game industries as well as in the broader entertainment, media and Internet industries, many of which offer superior compensation arrangements and career opportunities. In addition, our ability to train and integrate new employees into our operations may not meet the changing demands of our business. We cannot assure you that we will be able to attract and retain qualified game developers or other key personnel and successfully train and integrate them to achieve our business objectives, which could materially harm our business prospects.

Undetected programming errors or flaws in our games could harm our reputation or decrease market acceptance of our games, which would materially and adversely affect our business prospects, reputation, financial condition and results of operations.

Our current and future games may contain programming errors or flaws which may become apparent only after their release. In addition, our online and mobile games are developed using programs and engines developed by and licensed from third party vendors, which may include programming errors or flaws over which we have little or no control. If our users have negative experiences with our games related to or caused by undetected programming errors or flaws, they may be less inclined to use our games or recommend our games to other potential users.

While we have not experienced any material disruptions to our business from such errors or flaws in our games or in the programs and engines that we use to develop our games, these risks are inherent to our industry and, if realized, could severely harm our reputation, cause our users to cease playing our games, divert our resources or delay market acceptance of our games, any of which could materially and adversely affect our business, financial condition and results of operations.

Unexpected network interruptions, security breaches or computer virus attacks could harm our business and reputation.

Failure to maintain satisfactory performance, reliability, security and availability of our network infrastructure, whether maintained by us or by our licensees, may cause significant harm to our reputation and negatively impact our ability to attract and maintain users. Major risks relating to our network infrastructure include:

| • | any breakdowns or system failures, including from fire, flood, earthquake, hurricane or other natural disasters, power loss or telecommunications failure, resulting in a sustained shutdown of all or a material portion of our servers; |

| • | any disruption or failure in the national or international backbone telecommunications network, which would prevent users in certain countries in which our games are distributed from logging onto or playing our games for which the game servers are located in such countries; and |

| • | any security breach caused by hacking, loss or corruption of data or malfunctions of software, hardware or other computer equipment, and the inadvertent transmission of computer viruses. |

“Hacking” involves efforts to gain unauthorized access to information or systems or to cause intentional malfunctions or loss or corruption of data, software, hardware or other computer equipment. Hackers, if successful, could misappropriate proprietary information or cause disruptions in our service. We may have to spend significant capital and human resources to fix any damage to our system. In addition, we cannot ensure that any measures we take against hacking will be effective. A well-publicized computer security breach could significantly damage our reputation and materially and adversely affect our business.

12

Table of Contents

We have been subject to denial of service attacks that have caused portions of our network to be inaccessible for limited periods of time but did not cause material losses or damages. Although we take a number of measures to ensure that our systems are secure and unaffected by security breaches, including ensuring that our servers are hosted at physically secure sites, real-time monitoring against possible intrusion and saving all logs, preventing any unauthorized access to servers, and using firewalls, server virtualization technology, which allows one physical server to be divided into multiple virtual servers, each of which functions individually as a complete and independent server, and encryption technology, we cannot ensure that the measures we have implemented will be effective against all hacking efforts.

In addition, computer viruses may cause delays or other service interruptions on our systems and expose us to a material risk of loss or litigation and possible liability. We may be required to expend significant capital and other resources to protect our Web sites against the threat of such computer viruses and to address and resolve any problems resulting from such viruses. Moreover, if a computer virus affecting our system is highly publicized, our reputation could be materially damaged and our visitor traffic may decrease.

Any of the foregoing factors could reduce our users’ satisfaction, harm our business and reputation and have a material adverse effect on our business, financial condition and results of operations.

Failure to protect personal information could adversely affect our business, reputation and results of operations.

We collect, process, store and transmit personal information of game users worldwide for our global game service. Our business may be subject to a number of federal, state, local and foreign laws and regulations governing data privacy and security, including with respect to the collection, processing, storage, use, transmission and protection of personal information and other consumer data on the Internet and mobile platforms, the scope of which are continually changing and subject to differing interpretations, and which may be inconsistent among countries or otherwise in conflict with other laws or regulations. Although we strive to comply with all applicable laws, policies, legal obligations and certain industry codes of conduct relating to privacy and data protection to the extent reasonably attainable, it is possible that these obligations may be interpreted and applied in a manner that is inconsistent from one jurisdiction to another and may conflict with other laws or regulations or our practices. Also, while we have developed systems and processes that are designed to protect user information, the failure to prevent or mitigate the loss of personal information data or other game user data, including as a result of breaches of our vendors’ technologies and systems, could expose us or our game users to a risk of loss or misuse of such information. Any such failure or perceived failure by us to comply with our privacy policies, our privacy-related obligations to players or other third parties, or our privacy-related legal obligations, including without limitation any compromise of security that results in the unauthorized release or transfer of personally identifiable information or other player data, may result in governmental enforcement actions, litigation or public statements against us by consumer advocacy groups or others and could cause our players to lose trust in us, which may have an adverse effect on our business, reputation and results of operations. See ITEM 4.B. “BUSINESS OVERVIEW—LAWS AND REGULATIONS” for a detailed discussion regarding Korean, U.S. and Japanese laws that may materially impact our operations.

Electronic embezzlement could negatively impact the popularity of our online and mobile games and adversely affect our reputation and results of operations.

Despite security measures, some of our employees or licensees’ employees with high-level security access to our network, or other employees or persons who hack into or otherwise gain unauthorized access to certain sectors of our network, may succeed in breaching internal security systems and engage in electronic embezzlement by creating or diverting game money used in our online and mobile games and publicly or privately selling the game money for their financial benefit. Although we have internal security procedures in place designed to prevent electronic embezzlement and have not had any incident of electronic embezzlement since early 2006, we cannot assure you that we or our overseas licensees will

13

Table of Contents

be successful in preventing all electronic embezzlement. We have taken a number of procedures to prevent electronic embezzlement, including installing security programs designed to prevent counterfeiting and modification of program files, but cannot assure you such procedures will be sufficient to prevent new methods to engage in electronic embezzlement. Incidents of electronic embezzlement may negatively impact the reputation of our games, which may materially and adversely affect our business, financial condition and results of operations.

Cheating by users of online and mobile games could negatively impact the popularity of our online and mobile games and adversely affect our reputation and results of operations.

We have experienced numerous incidents where users were able to modify the published rules of our online and mobile games. Although these users did not gain unauthorized access to our systems, they were able to modify the rules of our online and mobile games during game play in a manner that allowed them to cheat and disadvantage other online game users. For example, utilizing auto-run programs that enabled the games to be continuously and automatically played without user participation, users have accumulated in-game points quickly, causing many other players to stop using the game and shortening the game’s life cycle. For mobile games, some users have purchased game money or in-game items through cloned mobile phones and sold such illegally obtained property to other users, which resulted in a shortfall between total sales and our actual revenues. Such unauthorized manipulation of our games may negatively impact users’ perception of our games and damage our reputation as well as our results of operations. Although we have taken a number of measures to deter our users from cheating when playing our games, including spot checks and monitoring of game play by game masters and system operators to check for suspicious activity, and encrypting packets, we cannot assure you that we or our licensees will be successful in timely taking the corrective measures necessary to prevent users from modifying the terms of our games.

Unauthorized use of our intellectual property rights by third parties and the expenses incurred in protecting our intellectual property rights may adversely affect our business.

Our intellectual property rights such as copyrights, service marks, trademarks and trade secrets are critical to our business. Unauthorized use of the intellectual property rights used in our business, whether owned by us or licensed to us, may materially and adversely affect our business and reputation. We rely on trademark and copyright law, trade secret protection and confidentiality agreements with our employees, customers, business partners and others to protect our intellectual property rights. Despite certain precautions taken by us, it may be possible for third parties to obtain and use our intellectual property without authorization.

Since the commercialization of Ragnarok Online in August 2002, we have discovered that the server-end software of Ragnarok Online has been unlawfully released on a consistent basis in most of the countries and markets in which Ragnarok Online has been offered. This enables unauthorized parties to set up local server networks to operate Ragnarok Online, which may result in the diversion of a significant number of paying users. We designate certain employees to be responsible for detecting such illegal servers. In Korea, we report offenders to the relevant enforcement authority for possible prosecution relating to crimes on the Internet. In markets outside of Korea, we cooperate with and rely on our licensees to seek enforcement actions against operators of illegal servers. For example, in Japan, we submitted a preliminary written accusation to the Tokyo Metropolitan Police Department in October 2009 and filed criminal charges against an illegal server operator of Ragnarok Online in April 2011 in cooperation with GungHo, our licensee in Japan. The case file was transferred to the Nagano District Public Prosecutor’s Office in December 2014 and the defendant was summarily indicted for copyright violation with fine of Japanese Yen 300,000 in September 2015. In December 2007 and June 2008, Gravity Interactive, Inc., our wholly owned subsidiary in the United States which manages Ragnarok Online game operations in the United States, petitioned the Federal Bureau of Investigation for remission or mitigation of forfeiture of the property of two illegal server operators of Ragnarok Online, which property was deemed proceeds of copyright infringement violations by the illegal server operators, and

14

Table of Contents

US$154,674.73 was returned to Gravity Interactive, Inc. in April 2011. We may incur considerable costs in the future in order to remedy software piracy of our server software and to enforce our rights against the operators of unauthorized server networks.

The validity, enforceability, enforcement mechanisms and scope of protection of intellectual property in Internet-related industries are uncertain and evolving. In particular, the laws and enforcement regimes of Korea, Japan, Thailand and certain other countries in which our games are distributed are uncertain or may not protect intellectual property rights to the same extent as do the laws and enforcement procedures of the United States. Moreover, litigation may be necessary in the future to enforce our intellectual property rights. Such litigation could result in substantial costs and diversion of our resources, disruption of our business, and have a material adverse effect on our business, prospects, financial condition and results of operations.

We may be subject to claims with respect to the infringement of intellectual property rights of others, which could result in substantial costs and diversion of our financial and management resources.

We cannot be certain that our online and mobile games do not or will not infringe upon patents, copyrights or other intellectual property rights held by third parties. We have in the past been and may in the future become subject to legal proceedings and claims from time to time relating to the intellectual property of others. If we are found to have violated the intellectual property rights of others, we may be enjoined from using such intellectual property rights, be required to pay penalties and fines and pay for the unauthorized use of such intellectual property and may need to incur additional license fees or be forced to develop alternative technology or obtain other licenses. We may incur substantial expenses in defending against these third party infringement claims, regardless of their merit. In addition, certain of our employees were recruited from other online and mobile game developers, including current and potential competitors. To the extent these employees have been and are involved in the development of our games that are similar to the games they helped develop at their former employers, we may become subject to claims that we or such employees have improperly used or disclosed trade secrets or other proprietary information. Although we are not aware of any pending or threatened claims of this type, if any such claims were to arise in the future, litigation or other dispute resolution procedures might be necessary to retain our ability to offer our current and future games, which could result in substantial costs and diversion of our financial and management resources.

Successful infringement or licensing claims against us may result in substantial monetary damages, which may materially disrupt our business operations and have a material adverse effect on our reputation, business, financial condition and results of operations.

We may not be able to successfully implement our growth and profit improvement strategies.

We are pursuing a number of growth and profit improvement strategies, including the following:

| • | distributing games developed in-house; |

| • | IP licensing to or from third parties for game development; |

| • | publishing games acquired from or developed by third parties through licensing arrangements; |

| • | offering our games in countries where we currently have little or no presence; |

| • | optimizing our marketing and research and development expenditures; |

| • | cross-selling our popular online games through other lines of businesses, such as mobile games, console games, animation and character merchandising; and |

| • | pursuing joint ventures with game development and service companies. |

We cannot assure you that we will be successful in implementing any of these strategies. Certain of our strategies relate to new services or products for which there are no established markets, or in which we lack experience and expertise. If we are unable to successfully implement our growth and profit improvement strategies, our revenues, profitability and competitiveness may be materially and adversely affected.

15

Table of Contents

We have limited business insurance coverage, and business interruption could have a material adverse effect on our business.

While we carry insurance coverage against certain risks to our property and assets, such as fire, flood and earthquake, as well as directors’ and officers’ liability insurance, we do not separately maintain casualty and liability insurance against litigation, risks or disruptions related to our business. The occurrence of any natural disaster, fire, power loss, telecommunications failure, break-ins, sabotage, computer viruses, intentional acts of Internet vandalism, human error or other similar events may damage our facilities or network servers and disrupt the operation of our business. As we do not carry sufficient natural disaster or business interruption insurance to compensate us for all types or amounts of loss that could arise, any damage or disruption from such events might result in our incurring substantial costs and the diversion of our resources, and have a material adverse effect on our business, financial condition and results of operations. See ITEM 4.B. “BUSINESS OVERVIEW—INSURANCE.”

As we introduce new games, we face the risk that a significant number of users of our existing games may migrate to our new games.

We expect that as we introduce new games, a certain number of our existing users may migrate from our existing games to the new games, which may lead to a decrease in the player base of our existing games and in turn make those existing games less playable to other game players, resulting in decreased revenues from our existing games. Players of our existing games may also spend less money to purchase in-game items in our new games than they would have spent if they had continued playing our existing games. In addition, our game players may migrate from our existing games with a higher profit margin to new games with a lower profit margin. If any of the forgoing occurs, our revenues and profitability are likely to be materially and adversely affected.

We may be required to take significant actions that are contrary to our business objectives in order to avoid being deemed an investment company as defined under the Investment Company Act of 1940, as amended.

Section 3(b)(1) of the Investment Company Act of 1940, or the “Investment Company Act,” provides that a company is not an investment company and, therefore, not required to register under the Investment Company Act as an investment company, if the company is primarily engaged, directly or through a wholly-owned subsidiary or subsidiaries, in a business or businesses other than that of investing, reinvesting or trading in securities (a “Non-Investment Business”). There are several bases on which a company can rely in determining that it is a Non-Investment Business.

Under one set of criteria, the factors to be considered in determining that a company is a Non-Investment Business are: (i) the history of the company; (ii) the manner in which the company represents itself to the investing public; (iii) the activities of its officers and directors; (iv) the nature of its current assets; and (v) the sources of its current income. Based on those factors, we believe that we are engaged primarily and directly in the business of providing online game services, and consequently, that we are a Non-Investment Business, and not an investment company as that term is defined under the Investment Company Act.

However, the determination as to whether a company satisfies the foregoing criteria is fact sensitive and subjective. Accordingly, it is possible that our determination could be challenged by the U.S. Securities and Exchange Commission (the “SEC”), particularly if at any time we own “investment securities” (as defined in the Investment Company Act) having a value in excess of 40% of our total assets (exclusive of cash items and U.S. government securities). We do not currently own investment securities in excess of this threshold. Nonetheless, if this were to become the case, we could be required to take actions to reduce our ownership of investment securities to comply with this standard, such as shifting a portion of our short-term investment portfolio into low-yielding bank deposits. If necessary, such actions would likely reduce the amount of interest or other income that we could otherwise generate from our investments. In addition, we might need to acquire additional income or loss generating assets that we might not otherwise have acquired or forego opportunities to acquire minority interests in companies that could be important to our business strategy.

16

Table of Contents

Alternatively, we could consider other actions, including applying to the SEC for an exemptive order pursuant to Section 3(b)(2) of the Investment Company Act, declaring that we are a company that is primarily engaged in a business or businesses other than that of investing, reinvesting, owning, holding, or trading in securities, without regard to the composition of our assets at any particular time. However, there can be no assurance that we would receive an exemptive order and the process to obtain such an exemptive order could be long and expensive.

The Investment Company Act contains numerous, complex requirements with respect to the organization and operations of investment companies, including restrictions on their capital structure, operations, and transactions with affiliates, as well as restrictions on the composition of the board of directors and other matters which would be incompatible with our business. Also, if we were to be deemed an investment company in the future, we would effectively be precluded from making public offerings of securities in the United States. In addition to disciplinary actions, such as SEC enforcement actions seeking monetary damages, we could also be subject to administrative or legal proceedings and any contracts to which we are a party that violate the Investment Company Act or the rules thereunder might be rendered unenforceable or subject to rescission.

Our status as a passive foreign investment company (“PFIC”) in 2015 and potentially other years could result in adverse U.S. tax consequences for you.

In light of the nature of our business activities and our holding of a significant amount of cash, short-term investments, and other passive assets, we believe that we were a PFIC during our 2008 through 2015 taxable years, and there is a significant risk that we will continue to be a PFIC during our 2016 taxable year. If we are a PFIC for any taxable year during which you hold our ADSs or common shares, you could be subject to adverse U.S. federal income tax consequences. You are urged to consult your tax advisors concerning the U.S. federal income tax consequences of holding our ADSs or common shares if we are considered a PFIC in any taxable year. See ITEM 10.E. “TAXATION—MATERIAL U.S. FEDERAL INCOME TAX CONSIDERATIONS—PFICs.”

If we fail to achieve and maintain an effective system of internal controls over financial reporting, we may be unable to accurately report our financial results or do so on a timely basis and our ability to prevent or detect fraud may be reduced and investor confidence and the market price of our ADSs may be adversely affected.

We are subject to Section 404 of the Sarbanes-Oxley Act of 2002, which requires us to, among other things, maintain an effective system of internal controls over financial reporting, and requires our management to provide a certification on the effectiveness of our internal controls on an annual basis.

Although we have determined that our internal controls over financial reporting were effective for the year ended December 31, 2015, we may in the future determine that we have a material weakness in our internal controls over financial reporting. Our registered public accounting firm is not required to and has not audited our internal controls over financial reporting. If we fail to maintain an effective system of internal controls over financial reporting, we may be unable to accurately report our financial results in a timely manner or prevent errors or fraud. Any of these possible outcomes could result in an adverse reaction in the financial marketplace due to loss of investor confidence in the reliability of our consolidated financial statements and could result in investigations or sanctions by the SEC, NASDAQ, or other regulatory authorities or in stockholder litigation. Any of these factors could ultimately harm our business and could adversely impact the market price of our ADSs. See ITEM 15. “CONTROLS AND PROCEDURES.”

Rapid technological developments and changes in market environment may limit our ability to recover game development or licensing costs and adversely affect our financial condition and results of operations due to impairment loss.

The online and mobile game industries are subject to rapid technological developments and changes in market environment, which could render our online and mobile games under development and

17

Table of Contents

commercialized games obsolete or unattractive to users. Any resulting failure to recover capitalized development or licensing costs and the recognition of impairment loss for such costs may materially and adversely affect our financial condition and results of operations. For example, in 2015, we recognized an impairment loss on intangible assets for capitalized research and development costs of Won 4,605 million for Ragnarok Online II and have recognized other similar impairment losses over the last several years.

We could suffer losses due to asset impairment charges.

We held a total of Won 23 million in acquired intangible assets at December 31, 2015. See Note 9 to our consolidated financial statements included in this Annual Report. We test goodwill and indefinite-lived intangible assets at least annually for impairment, and more frequently if an event occurs or circumstances change that would more likely than not reduce the fair value of these assets below their carrying amount. Such an event would include unfavorable variances from established business plans, significant changes in forecasted results or volatility inherent to external markets and industries, which are periodically reviewed by our management. If such an adverse event occurs and has the effect of changing one of the critical assumptions or estimates related to the fair value of our intangible assets or goodwill, an impairment charge could result. For example, in 2015, we recognized impairment losses on goodwill of Won 1,210 million in the reporting unit NeoCyon, Inc., or “NeoCyon,” due to the overall decline in the fair value of NeoCyon and have recognized other similar impairment losses over the last several years.

There can be no assurance that future reviews of our goodwill and other intangible assets will not result in impairment charges. Although it does not affect cash flow, an impairment charge does have the effect of decreasing our earnings, assets and shareholders’ equity.

RISKS RELATING TO OUR COMPANY STRUCTURE

GungHo, the publisher of our games in Japan, our largest market in terms of revenues, is our majority shareholder, which gives them control of our board of directors.

Since April 1, 2008, GungHo has been our largest shareholder and beneficially owns, as of the date hereof, 59.3% of our common shares. As a result, GungHo is able to exert significant control over all matters requiring shareholder approval, including the election of directors and approval of significant corporate transactions, including acquisitions, divestitures, strategic relationships and other matters, and may also exert significant control over decisions related to the status of our ADSs being eligible for quotation and trading on the NASDAQ Capital Market. In addition, as GungHo is also an online and mobile game developer, there may be conflicts of interest. For instance, GungHo may lead our management with strategies and efforts which benefit itself, its affiliates and their respective shareholders to the detriment of our other shareholders. GungHo may also compete directly or indirectly against us for users and customers or increased market share for its games. Furthermore, four of our registered Executive Directors, Mr. Hyun Chul Park, Mr. Yoshinori Kitamura, Mr. Kazuki Morishita and Mr. Kazuya Sakai currently serve as General Manager, Director and Executive General Manager, President and Chief Executive Officer, and Chief Financial Officer and Director, respectively, of GungHo, and there may be conflicts of interest in the decisions made by our Board of Directors and senior management. See ITEM 7.B. “RELATED PARTY TRANSACTIONS—Relationship with GungHo Online Entertainment, Inc.”

We are a “controlled company” within the meaning of the NASDAQ Stock Market Rules and may rely on exemptions from certain corporate governance requirements.

As GungHo controls 59.3% of our outstanding voting power as of the date hereof, we are a “controlled company” within the meaning of the NASDAQ Stock Market Rules and may rely on exemptions from certain corporate governance requirements. As a “controlled company,” we are not required to have a majority of our board of directors be independent, nor are we required to have a compensation committee or independent director oversight of director nominations which meet the requirements set forth in the NASDAQ Stock Market Rules. We are relying on these exemptions as a

18

Table of Contents

controlled company. Accordingly, our shareholders do not have the same protections afforded to shareholders of companies that are subject to all of the corporate governance requirements of the NASDAQ Stock Market Rules. For our corporate governance policies, see ITEM 6.C. “BOARD PRACTICES—CORPORATE GOVERNANCE PRACTICES.”

RISKS RELATING TO OUR REGULATORY ENVIRONMENT

Our online and mobile operations and businesses are subject to laws, rules and regulations in the countries in which our games are distributed, such as Korea, the United States and Japan, changes to which are difficult to predict, and uncertainties in interpretation and enforcement of the laws, rules and regulations in such countries may limit the protections available to us.

The regulatory and legal regimes in many of the countries in which our games are distributed have yet to establish a sophisticated set of laws, rules or regulations designed to regulate the online and mobile game industries. However, in many of our principal markets, such as Korea, the United States and Japan, legislators and regulators have implemented or indicated their intention to implement laws, rules and regulations with respect to issues such as user privacy, defamation, pricing, advertising, taxation, promotions, financial market regulation, consumer protection, content regulation, quality of products and services, and intellectual property ownership and infringement that may directly or indirectly impact our activities. The impact of such laws, rules and regulations on our business and results of operations is difficult to predict as many such laws, rules and regulations are constantly changing. However, as we might unintentionally violate such laws, rules and regulations or such laws, rules or regulations may be modified and new laws, rules and regulations may be enacted in the future, any such developments, or developments stemming from enactment or modification of other laws, rules or regulations, could increase the costs of regulatory compliance, force changes in business practices or otherwise have a material adverse effect on our business, financial condition and results of operations. Further, if the cost of regulatory compliance increases for our licensees as a result of regulatory changes, our licensees may seek to reduce royalties and license fees payable to us, which may materially and adversely affect our business, financial condition and results of operations. See ITEM 4.B. “BUSINESS OVERVIEW—LAWS AND REGULATIONS” for a detailed discussion regarding Korean, U.S. and Japanese laws that may materially impact our operations.

Our online and mobile games may be subject to governmental restrictions or ratings systems, which could delay or prohibit the release of new games or reduce the existing and potential scope of our user base.

Legislation is periodically introduced in many of the countries in which our games are distributed to establish a system for protecting consumers from the influence of graphic violence and sexually explicit materials contained in various types of games. For example, Korean law requires online game companies to obtain ratings classifications and implement procedures to restrict access of online games to certain age groups. Similar mandatory ratings systems and other regulations affecting the content and distribution of our games have been adopted or are under review in Taiwan, China, the United States and other markets for our online games. In the future, we may be required to modify our game content or features or alter our marketing strategies to comply with new governmental regulations or ratings assigned to our current or future games, which could delay or prohibit the release of new games or upgrades and reduce the existing and potential scope of our user base. Moreover, uncertainties regarding governmental restrictions or ratings systems applicable to our business could give rise to market confusion, thereby materially and adversely affecting our business, financial condition and results of operations.

Restrictions and controls on currency exchange in Korea and in certain countries in which our games are distributed may limit our ability to effectively utilize revenues generated in Won to fund our business activities outside Korea or expenditures denominated in foreign currencies, and may limit our ability to receive and remit revenues effectively.

The existing and any future restrictions on currency exchange in Korea, including Korean foreign exchange control regulations, may restrict our ability to convert Won into foreign currencies under

19

Table of Contents

certain emergency circumstances, such as natural calamities, wars, conflicts of arms or grave and sudden changes in domestic or foreign economic circumstances, difficulties in Korea’s international balance of payments and international finance and obstacles in carrying out currency policies, exchange rate policies and other Korean macroeconomic policies. Such restrictions may limit our ability to effectively utilize revenues generated in Won to fund our business activities outside Korea or expenditures denominated in foreign currencies.

In addition, the governments in certain markets in which our games are distributed, including without limitation Taiwan, China and Thailand, impose controls on the convertibility of local currency into foreign currencies and, in some cases, the remittance of currency outside their countries. Under current foreign exchange control regulations of certain markets, shortages in the availability of foreign currency may restrict the ability of our overseas licensees to pay license fees and royalties, most of which are paid in U.S. dollars, to us. Restrictions on our ability to receive license fees, royalties and other payments from our licensees would adversely affect our results of operations, financial condition and liquidity.

Adverse changes in the withholding tax rates in the countries from which we receive license fees and royalties could adversely affect our net income.

We may be subject to income tax withholding in countries where we derive revenues. Such withholding is made by our overseas licensees at the current withholding rates in such countries. To the extent Korea has a tax treaty with any such country, the withholding rate prescribed by such tax treaty will apply. Under the Corporation Tax Law of Korea, we are entitled to and recognize a capped foreign tax credit computed based on the amount of income taxes withheld overseas when filing our corporate income tax return in Korea. Accordingly, the amount of taxes withheld overseas may be offset against taxes payable in Korea.

Recently, there have been a series of amendments to tax treaties that Korea has entered into with various countries. The reduced tax rate applicable to license fees and royalties has reduced (i) from 10% to 5% under the amended tax treaty between Korea and Switzerland as to those payable from January 1, 2013, and (ii) from 15% to 10% in general (10% to 5% in case of consideration paid for provision of commercial or technological know-how) under the amended tax treaty between Korea and Luxembourg as to those payable from September 4, 2013. Further, the tax treaty between Korea and Peru went into effect as of March 3, 2014, and the license fees and royalties payable after January 1, 2015 has been taxed at the reduced rate of 15% (10% in case of consideration paid for technical supports). Around January 2014, Korea and India agreed on and initialed a proposed amendment of the tax treaty under which the reduced tax rate applicable to license fees and royalties shall be reduced from 15% to 10%. This amended version was signed by both countries on May 18, 2015, but has not yet been ratified by the national assemblies of the respective countries. On July 8, 2014, Korea and Hong Kong signed on and initialed a new tax treaty which includes a provision promulgating that license fees and royalties shall be subject to tax at the reduced rate of 10%, but such tax treaty has not yet been ratified by the Korean national assembly. These series of promulgations are all intended to eventually further limit the source country’s taxation right with respect to license fees and royalties. Any adverse changes in tax treaties between Korea and the countries from which we receive license fees and royalties, such as in the rate of withholding tax in the countries in which our games are distributed or in Korean tax law enabling us to recognize foreign tax credits for taxes withheld overseas, could adversely affect our net income.

RISKS RELATING TO OUR MARKET ENVIRONMENT

Our businesses may be adversely affected by developments affecting the economies of the countries in which our games are distributed.