November 30, 2022

VIA EDGAR

Ms. Julie Sherman

Division of Corporation Finance

Office of Life Sciences

Securities and Exchange Commission

100 F Street, N.E.

Washington, D.C. 20549

| Re: | China Foods Holdings Ltd. (the “Company”) | |

| Form 10-K for the Fiscal Year Ended December 31, 2021 | ||

| Filed April 15, 2022 | ||

Form 10-Q for the Quarterly Period ended March 31, 2022 Filed May 16, 2022 File No. 001-32522 |

Dear Ms. Sherman:

This letter sets forth certain of the Company’s responses to the comments contained in the letter dated May 25, 2022 from the staff (the “Staff”) of the Securities and Exchange Commission (the “Commission”) regarding the Company’s Form 10-K for the fiscal year ended December 31, 2021 filed with the Commission on April 15, 2022 (the “2021 Form 10-K”). The Staff’s comments are repeated below in bold and are followed by the Company’s responses thereto. All capitalized terms used but not defined in this letter shall have the meaning ascribed to such terms in the 2021 Form 10-K. This response includes the responses previously provided via October 13, 2022 letter.

FORM 10-K FOR THE FISCAL YEAR ENDED DECEMBER 31, 2021

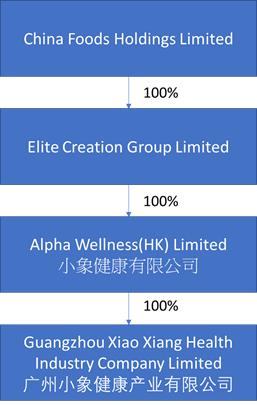

2. At the onset of Part I, please disclose prominently that you are not a Chinese operating company but a Delaware holding company with operations conducted by your subsidiaries. In addition, please provide early in the Business section a diagram of the company’s corporate structure.

The Company proposes to add the following disclosure:

The Company is a Delaware holding company and we conduct our business through our wholly owned subsidiary Guangzhou Xiao Xiang Health Industry Company Limited, a limited liability company organized under the laws of China on March 8, 2017 (“GXXHIC”). GXXHIC is wholly owned by Alpha Wellness (HK) Limited, a limited liability company organized under the laws of Hong Kong on April 24, 2019, which is in turn wholly owned by Elite Creation Group, a limited liability company formed under the laws of the British Virgin Islands formed on September 5, 2018. Alpha Wellness (HK) Limited and Elite Creation Group are holding companies without operations and are wholly owned by the Company.

3. Provide prominent disclosure about the legal and operational risks associated with being based in or having the majority of the company’s operations in China. Your disclosure should make clear whether these risks could result in a material change in your operations and/or the value of the securities you have registered for sale or could significantly limit or completely hinder your ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless. Your disclosure should address how recent statements and regulatory actions by China’s government, such as those related to the use of variable interest entities and data security or anti-monopoly concerns, have or may impact the company’s ability to conduct its business, accept foreign investments, or list on a U.S. or other foreign exchange.

The Company proposes to add the following disclosure:

We are a Delaware corporation and we conduct our primary operations in China through our subsidiary GXXHIC. We face various risks and uncertainties related to doing business in China, Our subsidiary GXXHIC is subject to complex and evolving PRC laws and regulations. Recently, the PRC enacted rules and regulations governing offshore offerings, anti-monopoly actions, and additional oversight on cybersecurity and data privacy.

We do not believe there GXXHIC is in violation of any laws, rules or regulations but since these newly enacted rules are still evolving, we cannot assure you that our business operations comply with such regulations and authorities’ requirements in all respects during the development of these new rules. However, in terms of business operation, GXXHIC expects to adapt to the newly issued rules and take dependent measures to comply with the laws and regulations of the Chinese authorities.

The PRC government’s authority in regulating our operations and its oversight and control over offerings and listings conducted overseas by, and foreign investment in, China-based issuers could significantly limit or completely hinder our ability to offer or continue to offer securities to investors. Implementation of industry-wide regulations in this nature may cause the value of such securities to significantly decline or be worthless. Risks and uncertainties arising from the legal system in China, including risks and uncertainties regarding the enforcement of laws and quickly evolving rules and regulations in China, could result in a material adverse change in our operations and the value of our securities. But so far, the current operation and securities value of the CFO are stable, and we believe that its risks are to the Company are manageable.

4. Please prominently disclose whether your auditor is subject to the determinations announced by the PCAOB on December 16, 2021 and whether and how the Holding Foreign Companies Accountable Act (“HFCAA”) and related regulations will affect your company. Additionally, please disclose prominently that you have been included on the Commission’s conclusive list of issuers identified under the HFCAA as having retained a registered public accounting firm to issue an audit report where the firm has a branch or office that: (1) is located in a foreign jurisdiction and (2) the PCAOB has determined that it is unable to inspect or investigate completely because of a position taken by an authority in the foreign jurisdiction.

The Company proposes to update its disclosures to include:

The Holding Foreign Companies Accountable Act (the “HFCAA”), was enacted on December 18, 2020. Our auditor, HKCM & CPA Co., is subject to the determinations announced by the PCOAB on December 16, 2021 and the HFCAA. The HFCAA states that if the SEC determines that we have filed audit reports issued by a registered public accounting firm that has not been subject to inspection by the PCAOB for three consecutive years beginning in 2021, the SEC shall prohibit our shares from being traded on a national securities exchange or in the over-the-counter trading market in the United States. Since our auditor is located in Hong Kong, a jurisdiction where the PCAOB has been unable to conduct inspections without the approval of the Chinese authorities, our auditor is not currently inspected by the PCAOB. The related risks and uncertainties could cause the value of our shares to significantly decline or be worthless.

5. Clearly disclose how you will refer to the holding company and subsidiaries when providing the disclosure throughout the document so that it is clear to investors which entity the disclosure is referencing and which subsidiaries or entities are conducting the business operations. For example, disclose, if true, that your subsidiaries conduct operations in China.

The Company updated the filing to clarify that GXXHIC is a subsidiary of the Company and operates in China, and proposes to update its disclosure to add:

The Company is a Delaware holding company and we conduct our business through our wholly owned subsidiary Guangzhou Xiao Xiang Health Industry Company Limited, a limited liability company organized under the laws of China on March 8, 2017 (“GXXHIC”).

6. Provide a clear description of how cash is transferred through your organization. Disclose your intentions to distribute earnings. Quantify any cash flows and transfers of other assets by type that have occurred between the holding company and its subsidiaries, and direction of transfer. Quantify any dividends or distributions that a subsidiary have made to the holding company and which entity made such transfer, and their tax consequences. Similarly quantify dividends or distributions made to U.S. investors, the source, and their tax consequences. Your disclosure should make clear if no transfers, dividends, or distributions have been made to date. Describe any restrictions on foreign exchange and your ability to transfer cash between entities, across borders, and to U.S. investors. Describe any restrictions and limitations on your ability to distribute earnings from the company, including your subsidiaries, to the parent company and U.S. investors.

The Company proposes to update the filings by adding the follow disclosure:

Transfers of Cash to and from Our Subsidiaries

China Foods Holdings Ltd is a Delaware holding company with no operations of its own. We conduct our operations in Hong Kong through our subsidiary in Hong Kong, while our operations in PRC through our subsidiary in PRC. We may rely on dividends to be paid by our Hong Kong subsidiary to fund our cash and financing requirements, including the funds necessary to pay dividends and other cash distributions to our shareholders, to service any debt we may incur and to pay our operating expenses. There is a possibility that the PRC could prevent our cash maintained in Hong Kong from leaving or the PRC could restrict the deployment of the cash into our business or for the payment of dividends. Any such controls or restrictions may adversely affect our ability to finance our cash requirements, service debt or make dividend or other distributions to our shareholders. If our Hong Kong subsidiary incurs debt on its own behalf in the future, the instruments governing the debt may restrict its ability to pay dividends or make other distributions to us. To date, our subsidiaries have not made any transfers, dividends or distributions to China Foods Holdings Ltd. and China Foods Holdings Ltd. has not made any transfers, dividends or distributions to our subsidiaries.

China Foods Holdings Ltd. is permitted under the Delaware laws to provide funding to our subsidiaries in Hong Kong through loans or capital contributions without restrictions on the amount of the funds, subject to satisfaction of applicable government registration, approval and filing requirements. Our Hong Kong is also permitted under the laws of Hong Kong to provide funding China Foods Holdings Ltd. through dividend distribution without restrictions on the amount of the funds. As of the date of this prospectus, there has been no dividends or distributions among the holding company or the subsidiaries nor do we expect such dividends or distributions to occur in the foreseeable future among the holding company and its subsidiaries.

We currently intend to retain all available funds and future earnings, if any, for the operation and expansion of our business and do not anticipate declaring or paying any dividends in the foreseeable future. Any future determination related to our dividend policy will be made at the discretion of our board of directors after considering our financial condition, results of operations, capital requirements, contractual requirements, business prospects and other factors the board of directors deems relevant, and subject to the restrictions contained in any future financing instruments.

Subject to the Delaware Statutes and our bylaws, our board of directors may authorize and declare a dividend to shareholders at such time and of such an amount as they think fit if they are satisfied, on reasonable grounds, that immediately following the dividend the value of our assets will exceed our liabilities and we will be able to pay our debts as they become due. There is no further Nevada statutory restriction on the amount of funds which may be distributed by us by dividend.

Under the current practice of the Inland Revenue Department of Hong Kong, no tax is payable in Hong Kong in respect of dividends paid by us. The laws and regulations of the PRC do not currently have any material impact on transfer of cash from China Foods Holdings Ltd. to our Hong Kong subsidiaries or from our Hong Kong subsidiaries to China Foods Holdings Ltd. There are no restrictions or limitation under the laws of Hong Kong imposed on the conversion of HK dollar into foreign currencies and the remittance of currencies out of Hong Kong or across borders and to U.S investors.

Current PRC regulations permit PRC subsidiaries to pay dividends to Hong Kong subsidiaries only out of their accumulated profits, if any, determined in accordance with Chinese accounting standards and regulations. In addition, each of our subsidiaries in China is required to set aside at least 10% of its after-tax profits each year, if any, to fund a statutory reserve until such reserve reaches 50% of its registered capital. Each of such entity in China is also required to further set aside a portion of its after-tax profits to fund the employee welfare fund, although the amount to be set aside, if any, is determined at the discretion of its board of directors. Although the statutory reserves can be used, among other ways, to increase the registered capital and eliminate future losses in excess of retained earnings of the respective companies, the reserve funds are not distributable as cash dividends except in the event of liquidation. As of the date of this prospectus, we do not have any PRC subsidiaries.

The PRC government also imposes controls on the conversion of RMB into foreign currencies and the remittance of currencies out of the PRC. Therefore, we may experience difficulties in completing the administrative procedures necessary to obtain and remit foreign currency for the payment of dividends from our profits, if any. Furthermore, if our subsidiaries in the PRC incur debt on their own in the future, the instruments governing the debt may restrict their ability to pay dividends or make other payments. If we or our subsidiaries are unable to receive all of the revenues from our operations, we may be unable to pay dividends on our common stock.

Cash dividends, if any, on our common stock will be paid in U.S. dollars. If we are considered a PRC tax resident enterprise for tax purposes, any dividends we pay to our overseas shareholders may be regarded as China-sourced income and as a result may be subject to PRC withholding tax at a rate of up to 10.0%.

In order for us to pay dividends to our shareholders, we will rely on payments made from our Hong Kong subsidiary to China Foods. If in the future we have PRC subsidiaries, certain payments from such PRC subsidiaries to Hong Kong subsidiaries will be subject to PRC taxes, including business taxes and VAT. As of the date of this prospectus, we do not have any PRC subsidiaries and our Hong Kong subsidiary has not made any transfers or distributions.

Pursuant to the Arrangement between Mainland China and the Hong Kong Special Administrative Region for the Avoidance of Double Taxation and Tax Evasion on Income, or the Double Tax Avoidance Arrangement, the 10% withholding tax rate may be lowered to 5% if a Hong Kong resident enterprise owns no less than 25% of a PRC entity. However, the 5% withholding tax rate does not automatically apply and certain requirements must be satisfied, including, without limitation, that (a) the Hong Kong entity must be the beneficial owner of the relevant dividends; and (b) the Hong Kong entity must directly hold no less than 25% share ownership in the PRC entity during the 12 consecutive months preceding its receipt of the dividends. In current practice, a Hong Kong entity must obtain a tax resident certificate from the Hong Kong tax authority to apply for the 5% lower PRC withholding tax rate. As the Hong Kong tax authority will issue such a tax resident certificate on a case-by-case basis, we cannot assure you that we will be able to obtain the tax resident certificate from the relevant Hong Kong tax authority and enjoy the preferential withholding tax rate of 5% under the Double Taxation Arrangement with respect to dividends to be paid by a PRC subsidiary to its immediate holding company. As of the date of this prospectus, we do not have a PRC subsidiary. In the event that we acquire or form a PRC subsidiary in the future and such PRC subsidiary desires to declare and pay dividends to our Hong Kong subsidiary, our Hong Kong subsidiary will be required to apply for the tax resident certificate from the relevant Hong Kong tax authority. In such event, we plan to inform the investors through SEC filings, such as a current report on Form 8-K, prior to such actions.

7. Disclose each permission or approval that you or your subsidiaries are required to obtain from Chinese authorities to operate your business and to offer securities to foreign investors. State whether you or your subsidiaries are covered by permissions requirements from the China Securities Regulatory Commission (CSRC), Cyberspace Administration of China (CAC) or any other governmental agency that is required to approve your operations or your subsidiaries’ operations, and state affirmatively whether you have received all requisite permissions or approvals and whether any permissions or approvals have been denied. Please also describe the consequences to you and your investors if you or your subsidiaries: (i) do not receive or maintain such permissions or approvals, (ii) inadvertently conclude that such permissions or approvals are not required, or (iii) applicable laws, regulations, or interpretations change and you are required to obtain such permissions or approvals in the future.

The Company proposes to add the following disclosure:

GXXHIC has received a Business License from the relevant department of the State Administration for Market Regulation. Apart from the Business License, GXXHIC may be subject to additional licensing requirements for our business operation due to the uncertainties of interpretation and implementation of relevant laws and regulations and the enforcement practice by relevant government authorities.

Furthermore, in connection with the operations of GXXHIC, as of the date of this report, neither GXXHIC nor the Company are required to obtain any approval or permission from the CSRC, CAC or any other PRC governmental authorities, nor has the Company or GXXHIC received any formal inquiry, notice, warning or sanction from any PRC governmental authorities in connection with requirements of obtaining such approval or permission, under any currently effective PRC laws, regulations and regulatory rules.

8. We note that you concluded that due to the small size of the company and lack of segregation of duties your disclosure controls and procedures as of the end of the period covered by this report were not effective. However, your management concluded that, as of December 31, 2021, your internal control over financial reporting (ICFR) was effective. Please explain how you reached the conclusion that your ICFR was effective despite the lack of segregation of duties and the fact that you determined that your disclosure controls and procedures were not effective. Please clarify whether you identified any material weaknesses in your ICFR. Refer to the requirements of Item 308(a) of Regulation S-K

In the Company’s Annual Report on Form 10-K for the period ending December 31, 2021, the Company concluded and reported that due to the small size of the company and lack of segregation of duties its disclosure controls and procedures as of the end of the period covered by this report were not effective. This conclusion was accurate. The management conclusion was inaccurately reported and will be amended to clarify this confusion.

9. We note that your disclosure both here and in your previous filings that Kong Xiao Jun was paid no compensation for his roles as CEO, CFO and director for the years 2018, 2019, 2020 and 2021. Please disclose other positions held by your CEO outside of the company and how much time he dedicates to such roles, as applicable. Please indicate whether such companies are competitors of the company and whether such roles present conflicts of interest in relation to his role as CEO, CFO and director of the company.

The Company proposes to add the following disclosures:

Mr. Kong was paid no compensation for his roles as CEO, CFO and director for the years 2018, 2019, 2020 and 2021. Mr. Kong agreed to take no compensation during this time frame to voluntarily reduce the financial obligation of the Company. He currently serves as the Chief Executive Officer of Guangdong HY Capital Management CO. LTD. These companies are not competitors of the company, and these roles do not conflict of interest with his role as CEO, CFO and director of the company.

11. Please disclose the risks that your corporate structure and being based in or having the majority of the company’s operations in China poses to investors. In particular, describe the significant regulatory, liquidity, and enforcement risks. For example, specifically discuss risks arising from the legal system in China, including risks and uncertainties regarding the enforcement of laws and that rules and regulations in China can change quickly with little advance notice; and the risk that the Chinese government may intervene or influence your operations at any time, or may exert more control over offerings conducted overseas and/or foreign investment in China-based issuers, which could result in a material change in your operations and/or the value of your securities. Acknowledge any risks that any actions by the Chinese government to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers could significantly limit or completely hinder your ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless.

The Company proposes to add the following disclosure:

Substantially all of our operations are conducted in China, and are governed by Chinese laws, rules and regulations. The Chinese legal system is a civil law system based on written statutes. Unlike common law systems, it is a system in which legal cases may be cited for reference but have limited value as precedents. In the late 1970s, the Chinese government began to promulgate a comprehensive system of laws and regulations governing economic matters in general. The overall effect of legislation over the past four decades has significantly increased the protections afforded to various forms of foreign or private-sector investment in China. However, since these laws and regulations are relatively new and the Chinese legal system continues to rapidly evolve, the interpretations of many laws, regulations and rules are not always uniform and enforcement of these laws, regulations and rules involve uncertainties.

From time to time, we may have to resort to administrative and court proceedings to interpret and/or enforce our legal rights. However, since Chinese administrative and court authorities have significant discretion in interpreting and implementing statutory and contractual terms, it may be more difficult to evaluate the outcome of administrative and court proceedings, and the level of legal protection we enjoy, than in more developed legal systems. Any administrative and court proceedings in China may be protracted, resulting in substantial costs and diversion of resources and management attention. Furthermore, the Chinese legal system is based in part on government policies and internal rules (some of which are not published in a timely manner or at all) that may have retroactive effect.

As a result, we may not be aware of our violation of these policies and rules until sometime after the violation. Such uncertainties, including uncertainty over the scope and effect of our contractual, property (including intellectual property) and procedural rights, and any failure to respond to changes in the regulatory environment in China could affect our business and our ability to continue our operations.

12. Please revise your disclosure to state that trading in your securities may be prohibited under the Holding Foreign Companies Accountable Act if the PCAOB determines that it cannot inspect or fully investigate your auditor, and that as a result an exchange may determine to delist your securities. In addition, please disclose that the United States Senate has passed the Accelerating Holding Foreign Companies Accountable Act, which, if enacted, would decrease the number of “non-inspection years” from three years to two years, and thus, would reduce the time before your securities may be prohibited from trading or delisted. Update your disclosure to reflect that the Commission adopted rules to implement the HFCAA and that, pursuant to the HFCAA, the PCAOB has issued its report notifying the Commission of its determination that it is unable to inspect or investigate completely accounting firms headquartered in mainland China or Hong Kong.

The Company proposes to update its disclosures to include:

The Holding Foreign Companies Accountable Act (the “HFCAA”), was enacted on December 18, 2020. Our auditor, HKCM & CPA Co., is subject to the determinations announced by the PCOAB on December 16, 2021 and the HFCAA. The HFCAA states that if the SEC determines that we have filed audit reports issued by a registered public accounting firm that has not been subject to inspection by the PCAOB for three consecutive years beginning in 2021, the SEC shall prohibit our shares from being traded on a national securities exchange or in the over-the-counter trading market in the United States. Since our auditor is located in Hong Kong, a jurisdiction where the PCAOB has been unable to conduct inspections without the approval of the Chinese authorities, our auditor is not currently inspected by the PCAOB. The related risks and uncertainties could cause the value of our shares to significantly decline or be worthless.

13. Given the Chinese government’s significant oversight and discretion over the conduct of your business, please revise to highlight the risk that the Chinese government may intervene or influence your operations at any time, which could result in a material change in your operations and/or the value of your securities. Also, given recent statements by the Chinese government indicating an intent to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers, acknowledge the risk that any such action could significantly limit or completely hinder your ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless.

The Company proposes to add the following disclosure:

However, the PRC government has recently indicated an intent to exert more oversight over offerings that are conducted overseas and/or foreign investment in China-based issuers like us, and published a series of proposed rules for public comments in this regard, the enaction timetable, final content, interpretation and implementation of which remains uncertain. Therefore, there are substantial uncertainties as to how PRC governmental authorities will regulate overseas listing in general and whether we are required to complete filing or obtain any specific regulatory approvals from the CSRC, CAC or any other PRC governmental authorities for our future offshore offerings. If we had inadvertently concluded that such approvals were not required, or if applicable laws, regulations or interpretations change in a way that requires us to obtain such approval in the future, we may be unable to obtain such necessary approvals in a timely manner, or at all, and such approvals may be rescinded even if obtained. Any such circumstance could subject us to penalties, including fines, suspension of business and revocation of required licenses, significantly limit or completely hinder our ability to continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless.

14. In light of recent events indicating greater oversight by the Cyberspace Administration of China (CAC) over data security, particularly for companies seeking to list on a foreign exchange, please revise your disclosure to explain how this oversight impacts your business and to what extent you believe that you are compliant with the regulations or policies that have been issued by the CAC to date.

The Company proposes to add the following disclosure:

For example, the recently promulgated PRC Data Security Law and the PRC Personal Information Protection Law in 2021 posed additional challenges to our cybersecurity and data privacy compliance. The Cybersecurity Review Measures issued by the Cyberspace Administration of China, or the CAC and several other PRC governmental authorities in December 2021, as well as the Administration Regulations on Cyber Data Security (Draft for Comments) published by the CAC for public comments in November 2021, exposes uncertainties and potential additional restrictions on China-based overseas-listed companies like us. If the detailed rules, implementations, or the enacted version of the draft measures mandate clearance of cybersecurity review and other specific actions to be completed by us, we face uncertainties as to whether such clearance can be timely obtained, the failure of which may subject us to penalties, which could materially and adversely affect our business and results of operations and the price of our securities. However, as the Company operates in a traditional food industry, we believe the promulgation of the above laws will have a low impact on the Company and CFOO believes it is in compliance with the above laws.

15. It appears from your disclosure that 100% of your sales for the three months ended March 31, 2021 were returned. Please revise to disclose the reason for the significant returns and how these are reflected in your financial statements. In addition, clarify why revenue was recognized for these sales and how these returns impact your revenue recognition policy. Your revenue recognition accounting policy should be revised to address returns.

Per the financial statement on page 11 of the Form 10-Q for the Three Months Ended March 31, 2021, the Company experienced no product returns and recorded no reserve for sales returns for the three months ended March 31, 2021 and 2020. The Company proposes to revise the disclosure on pages 9 in response to the Staff’s comment as follows:

Wine Business mainly provides the wine products to the customers. Revenue is recognized from the sale of wine products upon delivery to the customers, whereas the title and risk of loss are fully transferred to the customers. The Company records its revenues, net of value added taxes (“VAT”) on the majority of the products at the rate of 17% on the invoiced value of sales. The revenues are presented net of sales returns and discounts. The Company recorded product sales returns of $4,741 and $0 for the period ended March 31, 2022 and 2021, respectively. The cost, such as shipping cost and material cost, is recognized when the product delivered to the customers. The Company records its cost including taxes.

16. In this regard, please reconcile the disclosure on page 13 that indicates the $167,643 relates to consultancy service fee income with the disclosure in the table in Note 3 on page 14 that this represents the sale of wine products. These tables should be revised to indicate the correct periods (i.e., three months rather than year ended). Your revenue recognition policy should also clearly indicate whether this revenue is from the sale of products or services and is recognized on a gross or net basis. Refer to ASC 606-10-55-36.

The Company proposes to amend its disclosures as follows:

(on page 13)

Disaggregation of Revenue

The following table provides information about disaggregated revenue from customers into the nature of the products and services, and geographic regions, and includes a reconciliation of the disaggregated revenue with reportable segments.

| For the Period Ended March 31, 2022 | For the Period Ended March 31, 2021 | |||||||

| Consultancy service fee income | $ | 64,058 | $ | - | ||||

| Sales of healthcare | 4,741 | 167,643 | ||||||

| TOTAL | $ | 68,799 | $ | 167,643 | ||||

(On Page 9) :

Revenue recognition

The Company adopted Accounting Standards Codification (“ASC”) 606 – Revenue from Contracts with Customers” (“ASC 606”). Under ASC 606, a performance obligation is a promise within a contract to transfer a distinct good or service, or a series of distinct goods and services, to a customer. Revenue is recognized when performance obligations are satisfied and the customer obtains control of promised goods or services. The amount of revenue recognized reflects the consideration to which the Company expects to be entitled to receive in exchange for goods or services. Under the standard, a contract’s transaction price is allocated to each distinct performance obligation. To determine revenue recognition for arrangements that the Company determines are within the scope of ASC 606, the Company performs the following five steps:

| ● | identify the contract with a customer; | |

| ● | identify the performance obligations in the contract; | |

| ● | determine the transaction price; | |

| ● | allocate the transaction price to performance obligations in the contract; and | |

| ● | recognize revenue as the performance obligation is satisfied. |

Currently, the Company operates two business segments.

Healthcare Business mainly provides health consulting advisory services and healthcare and wellness products to the customers.

Revenue is earned from the rendering of health consulting advisory services to the customers. The Company recognizes services revenue over the period in which such services are performed. Amounts expected to be recognized as revenue within the 12 months following the balance sheet date are classified as current portion of deferred revenue in the accompanying consolidated balance sheets. Amounts not expected to be recognized as revenue within the 12 months following the balance sheet date are classified as deferred revenue, net of current portion.

The sale and distribution of the healthcare products, such as (i) Nutrition Catering (ii) Special Health Food (iii) Health Supplement and (iv) Skincare, is the only performance obligation under the fixed-fee arrangements. Revenue is recognized from the sale of their healthcare products upon delivery to the customers, whereas the title and risk of loss are fully transferred to the customers. The Company records its revenues, net of value added taxes (“VAT”) on the majority of the products at the rate of 17% on the invoiced value of sales. The cost, such as shipping cost and material cost, is recognized when the product delivered to the customers. The Company records its cost including taxes.

Wine Business mainly provides the wine products to the customers. The Company acts as the principal in substantially all of its customer arrangements and as such, generally records revenues on a gross basis. Revenues exclude any taxes that the Company collects from customers and remits to tax authorities.

Revenue is recognized from the sale of wine products upon delivery to the customers, whereas the title and risk of loss are fully transferred to the customers. The Company records its revenues, net of value added taxes (“VAT”) on the majority of the products at the rate of 17% on the invoiced value of sales. The revenues are presented net of sales returns and discounts. The Company recorded product sales returns of $4,741 and $167,6430 for the period ended March 31, 2022 and 20201, respectively. The cost, such as shipping cost and material cost, is recognized when the product delivered to the customers. The Company records its cost including taxes.

17. Please revise to explain the specific reason for the significant drop in sales in the PRC.

The Company proposes to amend its disclosures as follows:

Revenue. For the three months ended March 31, 2022, we generated revenues of $68,799 and three months ended March 31, 2021, we generated revenues of $167,643 from our current business operations, respectively. The significant decrease due to the significant drop in the sales of wine products from the continued lockdown under the tight pandemic measure in China. The major customers are located in the HK during the period ended March 31, 2022, while all the major customers are located in the PRC during the period ended March 31, 2021.

18. We note that the certification filed as Exhibits 31.1 is not in the proper form. Please revise the language related to internal control over financial reporting in an amendment to comply with the guidance set forth in Item 601(b)(31) of Regulation S-K.

The Company acknowledges the proper form and will amend he certifications.

Sincerely,

Conn Flanigan

NewRev General Counsel, LLC

On Behalf of China Foods Holdings Ltd.