UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

For

the quarterly period ended

For the transition period from __________to _________

Commission file number

(Exact name of registrant as specified in its charter)

State or other jurisdiction of incorporation or organization |

(I.R.S. Employer Identification No.) |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code

(Former name, former address and former fiscal year, if changed since last report)

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days.

Indicate

by check mark whether the registrant has submitted electronically on its corporate Web site, if any, every Interactive Data File required

to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter

period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☐ | Smaller reporting company | ||

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐

APPLICABLE ONLY TO CORPORATE ISSUERS:

State the number of shares outstanding of each of the issuer’s classes of common equity, as of the latest practicable date.

| Class | Outstanding November 14, 2022 | |

| Common Stock, with $0.0001 par value | shares |

Table of Contents

| Page | ||

| No. | ||

| PART I – FINANCIAL INFORMATION | ||

| Item 1. | Condensed Consolidated Financial Statements (Unaudited) | 3 |

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 21 |

| Item 3. | Quantitative and Qualitative Disclosures about Market Risk | 25 |

| Item 4. | Controls and Procedures | 25 |

| PART II – OTHER INFORMATION | ||

| Item 1. | Legal Proceedings | 25 |

| Item 1A. | Risk Factors | 25 |

| Item 2. | Unregistered Sales of Equity Securities and Proceeds | 25 |

| Item 3. | Defaults Upon Senior Securities | 25 |

| Item 4. | Mine Safety Disclosure | 25 |

| Item 5. | Other Information | 25 |

| Item 6. | Exhibits | 26 |

| SIGNATURES | 27 | |

| 2 |

PART I – FINANCIAL INFORMATION

Item 1. Financial Statements

China Foods Holdings Ltd.

Condensed Consolidated Balance Sheets

September 30, 2022 | December 31, 2021 | |||||||

| $ | $ | |||||||

| (Unaudited) | (Audited) | |||||||

| ASSETS | ||||||||

| Current Assets | ||||||||

| Cash and cash equivalents | ||||||||

| Prepayments and other receivables | ||||||||

| Inventories | ||||||||

| Tax recoverable | ||||||||

| Right-of-use assets | ||||||||

| Total Current Assets | ||||||||

| Non-Current Assets | ||||||||

| Plant and equipment, net | ||||||||

| Intangible assets | ||||||||

| Total Non-Current Assets | ||||||||

| TOTAL ASSETS | ||||||||

| LIABILITIES AND SHAREHOLDERS’ EQUITY | ||||||||

| Current Liabilities | ||||||||

| Accrued liabilities and other payables | ||||||||

| Customer deposits | ||||||||

| Lease liabilities | ||||||||

| Amount due to a director | ||||||||

| Amount due to a related company | ||||||||

| Total Current Liabilities | ||||||||

| Non-Current Liabilities | ||||||||

| Lease liabilities | ||||||||

| Total Non-Current Liabilities | ||||||||

| Stockholders’ Equity | ||||||||

| Common stock $ par value, shares authorized, and shares issued and outstanding as of September 30, 2022 and December 31, 2021 respectively | ||||||||

| Additional paid-in capital | ||||||||

| Accumulated other comprehensive income | ( | ) | ||||||

| Accumulated deficit | ( | ) | ( | ) | ||||

| Total Shareholders’ Equity | ||||||||

| TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY | ||||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

| 3 |

China Foods Holdings Ltd.

Condensed Consolidated Statements of Operations and Comprehensive Loss

(Unaudited)

| Three Months Ended | Three Months Ended | Nine Months Ended | Nine Months Ended | |||||||||||||

| September 30, 2022 | September 30, 2021 | September 30, 2022 | September 30, 2021 | |||||||||||||

| Revenue, net | ||||||||||||||||

| Cost of revenue | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Gross (loss) profit | ( | ) | ||||||||||||||

| Operating expenses | ||||||||||||||||

| Selling and distribution expenses | ||||||||||||||||

| General and administrative expenses | ||||||||||||||||

| Total operating expenses | ||||||||||||||||

| Loss from operation | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Other income (expense): | ||||||||||||||||

| Interest income | ||||||||||||||||

| Other expense | ( | ) | ||||||||||||||

| Sundry income | ||||||||||||||||

| Total other income, net | ||||||||||||||||

| Loss before income tax | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Income tax credit (expenses) | ( | ) | ||||||||||||||

| Net loss | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Other comprehensive loss | ||||||||||||||||

| Foreign currency translation adjustment (loss) gain | ( | ) | ( | ) | ( | ) | ||||||||||

| Comprehensive loss | ( | ) | ( | ) | ( | ) | ( | ) | ||||||||

| Net loss per common share | ||||||||||||||||

| Basic and diluted* | $ | ( | ) | $ | ( | ) | $ | ( | ) | $ | ( | ) | ||||

| Weighted average number of common share | ||||||||||||||||

| Basic and diluted | ||||||||||||||||

| * |

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

| 4 |

CHINA FOODS HOLDINGS LTD.

Condensed Consolidated Statements of Changes in Shareholders’ Equity

(Unaudited)

| Common Stock | Additional paid-in | Accumulated | Accumulated other comprehensive | Total shareholders’ | ||||||||||||||||||||

| Share | Amount | capital | Deficit | income (loss) | equity | |||||||||||||||||||

| $ | $ | $ | $ | $ | ||||||||||||||||||||

| Balance at January 1, 2022 | $ | $ | $ | ( | ) | $ | $ | |||||||||||||||||

| Net loss for the period | - | ( | ) | ( | ) | |||||||||||||||||||

| Foreign currency translation adjustment | - | ( | ) | ( | ) | |||||||||||||||||||

| Balance at March 31, 2022 | ( | ) | ||||||||||||||||||||||

| Net loss for the period | - | ( | ) | ( | ) | |||||||||||||||||||

| Foreign currency translation adjustment | - | ( | ) | ( | ) | |||||||||||||||||||

| Balance at June 30, 2022 | ( | ) | ||||||||||||||||||||||

| Net loss for the period | - | ( | ) | ( | ) | |||||||||||||||||||

| Foreign currency translation adjustment | - | ( | ) | ( | ) | |||||||||||||||||||

| Balance at September 30, 2022 | $ | $ | $ | ( | ) | $ | ( | ) | $ | |||||||||||||||

| Common Stock | Additional paid-in | Accumulated | Accumulated other comprehensive | Total shareholders’ | ||||||||||||||||||||

| Share | Amount | capital | Deficit | income (loss) | equity | |||||||||||||||||||

| $ | $ | $ | $ | $ | ||||||||||||||||||||

| Balance at January 1, 2021 | $ | $ | $ | ( | ) | $ | $ | |||||||||||||||||

| Net loss for the period | - | ( | ) | ( | ) | |||||||||||||||||||

| Foreign currency translation adjustment | - | |||||||||||||||||||||||

| Balance at March 31, 2021 | ( | ) | ||||||||||||||||||||||

| Net income for the period | - | |||||||||||||||||||||||

| Foreign currency translation adjustment | - | |||||||||||||||||||||||

| Balance at June 30, 2021 | ( | ) | ||||||||||||||||||||||

| Net loss for the period | - | ( | ) | ( | ) | |||||||||||||||||||

| Foreign currency translation adjustment | - | ( | ) | ( | ) | |||||||||||||||||||

| Balance at September 30, 2021 | $ | $ | $ | ( | ) | $ | $ | |||||||||||||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

| 5 |

China Foods Holdings Ltd.

Condensed Consolidated Statements of Cash Flows

(Unaudited)

| Nine months ended September 30, | ||||||||

| 2022 | 2021 | |||||||

| Cash flows from operating activities: | ||||||||

| Net loss | $ | ( | ) | $ | ( | ) | ||

| Adjustments to reconcile net loss to net cash used in operating activities | ||||||||

| Depreciation | ||||||||

| Gain from sale of plant and equipment | ( | ) | ||||||

| Amortization | ||||||||

| Non-cash lease expense | ||||||||

| ( | ) | ( | ) | |||||

| Change in operating assets and liabilities: | ||||||||

| Accounts receivable | ( | ) | ||||||

| Prepayments and other receivables | ( | ) | ||||||

| Inventories | ||||||||

| Accrued liabilities and other payables | ( | ) | ||||||

| Accounts payable | ( | ) | ||||||

| Tax recoverable | ||||||||

| Tax payable | ( | ) | ||||||

| Customer deposits | ( | ) | ( | ) | ||||

| Lease liabilities | ||||||||

| Net cash used in operating activities | ( | ) | ( | ) | ||||

| Cash flows from investing activities: | ||||||||

| Addition of plant and equipment | ( | ) | ||||||

| Proceeds from sale of plant and equipment | ||||||||

| Net cash provided by (used in) investing activities | ( | ) | ||||||

| Cash flows from financing activities: | ||||||||

| Repayment of lease liabilities | ( | ) | ( | ) | ||||

| (Repayment to) advances from a director | ( | ) | ||||||

| Net cash (used in) provided by financing activities | ( | ) | ||||||

| Foreign currency translation adjustment | ( | ) | ||||||

| Net change in cash and cash equivalents | ( | ) | ( | ) | ||||

| CASH AND CASH EQUIVALENTS, BEGINNING OF PERIOD | ||||||||

| CASH AND CASH EQUIVALENTS, END OF PERIOD | $ | $ | ||||||

| SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION | ||||||||

| Cash paid for interest | $ | $ | ||||||

| Cash paid for income taxes | $ | $ | ||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

| 6 |

China Foods Holdings Ltd.

Notes to the Unaudited Condensed Consolidated Financial Statements

Nine months ended September 30, 2022

NOTE 1 – NATURE OF OPERATIONS

China Foods Holdings Ltd. (the “Company”, “CFOO”, or “we”) was incorporated in Delaware on January 10, 2019. On January 23, 2019, the Company entered into an Agreement and Plan of Merger (the “Agreement”) with Trafalgar Resources, Inc., a Utah corporation (“Trafalgar”). Pursuant to the Agreement, the Company merged with Trafalgar (the “Merger”) with the Company as the surviving entity. Prior to the Merger, Trafalgar had not commenced operations for several years that had resulted in significant revenue and Trafalgar’s efforts had been devoted primarily to activities related to raising capital and attempting to acquire an operating entity.

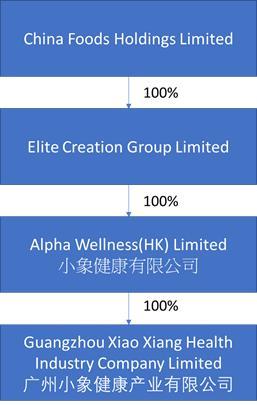

The Company is a Delaware holding company and we conduct our business through our wholly owned subsidiary Guangzhou Xiao Xiang Health Industry Company Limited, a limited liability company organized under the laws of China on March 8, 2017 (“GXXHIC”). GXXHIC is wholly owned by Alpha Wellness (HK) Limited, a limited liability company organized under the laws of Hong Kong on April 24, 2019, which is in turn wholly owned by Elite Creation Group, a limited liability company formed under the laws of the British Virgin Islands formed on September 5, 2018. Alpha Wellness (HK) Limited and Elite Creation Group are holding companies without operations and are wholly owned by the Company.

Substantially all of our operations are conducted in China, and are governed by Chinese laws, rules and regulations. Our subsidiary, GXXHIC, is subject to Chinese laws, rules, and regulations. Uncertainties with respect to the interpretation and enforcement of Chinese laws, rules and regulations could have a material adverse effect on us. Risks and uncertainties arising from the legal system in China, including risks and uncertainties regarding that the rules and regulations in China can change quickly with little advance notice and that the Chinese government may intervene or influence our operations at any time, could result in a material adverse change in our operations and the value of our securities.

Our History

Prior to the Merger, Trafalgar’s majority stockholder

who owned shares (approximately

Pursuant to the Merger, each share of Trafalgar’s common stock was converted into one share of the Company’s common stock. After the Merger, HY (HK) Financial Investments Co., Ltd. owns shares of common stock of the Company. The Merger was effective on March 13, 2019.

On December 11, 2019, the Board of Directors approved a change to its fiscal year-end from September 30 to December 31. As a result of this change, the fiscal year is a 3 months transition period beginning October 1, 2019 through December 31, 2020. In these statements, including the notes thereto, financial results for fiscal 2019 are for a 3-month period. Corresponding results for the years ended September 30, 2019 and 2018 are both for 12-month periods.

On July 9, 2020, the Company consummated the Share Exchange Agreement (“the “Share Exchange Agreement”) with Elite Creation Group Limited, a private limited company organized under the laws of British Virgin Islands (“ECGL”). As a result of the acquisition of ECGL, the Company entered into the healthcare product distributing and marketing industry, pursuing a new strategy of developing and distributing health related products, including supplements, across the globe with a focus on mainland China, Europe and Australia.

ECGL will comprise the ongoing operations of the combined entity and its senior management will serve as the senior management of the combined entity, ECGL is deemed to be the accounting acquirer for accounting purposes. The transaction will be treated as a recapitalization of the Company. Accordingly, the consolidated assets, liabilities and results of operations of the Company will become the historical financial statements of ECGL, and the Company’s assets, liabilities and results of operations will be consolidated with ECGL beginning on the acquisition date. ECGL was the legal acquiree but deemed to be the accounting acquirer. The Company was the legal acquirer but deemed to be the accounting acquiree in the reverse merger. The historical financial statements prior to the acquisition are those of the accounting acquirer (ECGL). After completion of the Share Exchange Transaction, the Company’s consolidated financial statements include the assets and liabilities, the operations and cash flow of the accounting acquirer.

Effective July 9, 2020, we consummated the acquisition of ECGL, and its wholly owned subsidiary GXXHIC, a limited liability company organized under the laws of China on March 8, 2017. Alpha Wellness (HK) Limited, a limited liability company organized under the laws of Hong Kong on April 24, 2019, is a holding company without operations.

Corporate Org Chart

| 7 |

Our Products

Our health products are designed to help enhance immunity and improve general wellbeing. We provide the following categories of healthcare products and customized healthcare consultation services in China: (i) Nutrition Catering (ii) Special Health Food (iii) Health Supplement and (iv) Skincare. The products target all age groups with different needs.

Our products are taken as healthcare supplements in accordance with the principles of traditional Chinese medicine including the principle complementary medicine and ideal ratios and combinations of ingredients.

Due to the impact of the COVID-19 pandemic in the healthcare industry, we have also offered a new line of high-end wine products in our online and offline sales platform, to diversify the market demand and customer needs.

Our services

We also extend our service scope to provide the personalized health consulting services to our clients, as well as consultancy services such as tailor-made natural food supplement solutions.

Markets and Regions

The Great Health Industry refers to production, operation, service and information dissemination, maintenance, restoration, and promotions linked to health. It covers medical products, health supplements, nutritional foods, medical devices, health appliances, fitness, health management, health consulting and many other production and service areas closely related to human health. The Great Health Industry is an emerging industry with huge market potential, especially in China.

According to the “China Great Health Industry

Strategic Planning and Enterprise Strategy Consulting Report” published by Qianzhan Industry Institute (前瞻產業研究院),

the scale of the Great Health Industry in 2017 was USD

Our Strategies

We are focused on achieving long-term growth in revenues, cash flow and profit. We believe that we can achieve this by developing multiple distribution channels and strengthening our marketing and promotions, leading to better product turnover and revenue. We also expect to broaden our product range as well as product differentiation in the future. Based on the business experience accumulated over the years, we believe we can improve the efficiency of our supply chain with time-saving and cost-saving supply chain management and marketing planning for the target customer base with our one-stop service.

Our primary aims are (i) to strengthen our product salability; (ii) to cut logistics cost and time spent and (iii) to further expand the market share in China. Toward this end, we plan to pursue the following business strategies:

| ● | Collaborate with third-party e-commerce platforms to boost product exposure, e.g. Tmall, Jingdong mall | |

| ● | Deliver healthcare knowledge and consultation service via social media and We-media | |

| ● | Build brand image and reputation through customer experience and word of mouth | |

| ● | Increase the number of downstream distributors and wholesalers | |

| ● | Strengthen the relationship with manufacturers, suppliers, drug agents and distributors | |

| ● | Pursue strategic acquisitions and partnerships |

We intend to develop both online and offline distribution channels to increase sales volume and revenue. We expect to partner with third party e-commerce platforms, social media and We-media such as Wechat, TikTok and Xiaohongshu to build our online presence. We believe that online channels will allow us to provide real-time nutrition and healthcare consultation services as well as increase customer engagement and retention. Starting from the second half of 2020, we have launched our “nutrition consulting” support services using a major social media software to allow customer groups to receive pre-purchase consultation and after-sales service for products anytime and anywhere.

Our current offline sales channel relies on distributors and sales agents. To enhance the visibility and marketability of our products and services and to improve brand recognition and awareness, we hope to develop store-in-shop and counter experiences. We also intend to partner with high-end gyms to form nutrition clubs and hold weight-loss training camps, health assessment and fitness training camps and other activities.

We intend to create a ‘one-stop’ solution for our customers by creating a multi-channel health product supply and retail system. We not only provide personalized consultation service to our customers, but also summarize and analyze our customer feedback and experiences through our consultation service and after-sales service. We intend to share this data with our manufacturers and supply chain partners to develop products and services that better meet the demands of our customers. By pooling and addressing the needs of downstream businesses and combining it with the Consumer to Manufacturer model for upstream transformation, we anticipate establishing a close relationship between manufacturers and suppliers. We believe this model can also reduce circulation costs and improve the efficiency of our supply chain.

NOTE 2 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of presentation and consolidation

The accompanying unaudited condensed consolidated financial statements of the Company have been prepared in accordance with generally accepted accounting principles in the United States (“GAAP”) for interim financial reporting, and in accordance with instructions for Form 10-Q and Article 10 of Regulation S-X. Accordingly, they do not include all of the information and footnotes required by generally accepted accounting principles for complete financial statements. In the opinion of management, the unaudited condensed consolidated financial statements contained in this report reflect all adjustments that are normal and recurring in nature and considered necessary for a fair presentation of the financial position and the results of operations for the interim periods presented. The year-end balance sheet data was derived from audited financial statements but does not include all disclosures required by GAAP. The results of operations for the interim period are not necessarily indicative of the results expected for the full year. These unaudited condensed consolidated financial statements, footnote disclosures and other information should be read in conjunction with the financial statements and the notes thereto included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2021.

The unaudited condensed consolidated financial statements are presented in US Dollars and include the accounts of the Company and its subsidiaries. All significant inter-company accounts and transactions have been eliminated in consolidation.

| 8 |

The following table depicts the description of the Company’s subsidiaries:

| Name | Place of incorporation and kind of legal entity | Principal activities | Particulars of registered/ paid up share capital | Effective interest held | ||||||

| Elite Creation Group Limited | issued shares of US$ | % | ||||||||

| Alpha Wellness (HK) Limited | issued shares for HK$ | % | ||||||||

| Guangzhou Xiao Xiang Health Industry Company Limited | RMB | % | ||||||||

Cash and cash equivalents

Cash and cash equivalents are carried at cost and represent cash on hand, demand deposits placed with banks or other financial institutions and all highly liquid investments with an original maturity of three months or less as of the purchase date of such investments.

Inventories

Inventories are stated at the lower of cost or market value (net realizable value), cost being determined on a first-in-first-out method. Costs include material and manufacturing overhead costs. The Company provides inventory allowances based on excess and obsolete inventories determined principally by customer demand. As of September 30, 2022 and December 31, 2021, the Company did not record an allowance for obsolete inventories, nor have there been any write-offs.

Plant and equipment

Plant and equipment are stated at cost less accumulated depreciation and accumulated impairment losses, if any. Depreciation is calculated on the straight-line basis over the following expected useful lives from the date on which they become fully operational and after taking into account their estimated residual values:

| Expected useful lives | Residual value | |||||

| Furniture, fixture and equipment | % | |||||

| Motor vehicle | % | |||||

| Leasehold improvement | % | |||||

Expenditures for repairs and maintenance are expensed as incurred. When assets have been retired or sold, the cost and related accumulated depreciation are removed from the accounts and any resulting gain or loss is recognized in the results of operations.

Depreciation

expense for the three and nine months ended September 30, 2022 were $

Intangible assets

Intangible

assets represented trademarks of their products and are stated at cost less accumulated amortization and any recognized impairment loss.

Amortization is provided over the term of their registrations on a straight-line basis, which is

Amortization

expense for the three and nine months ended September 30, 2022 were $

Amortization

expense for the three and nine months ended September 30, 2021 were $

Impairment of long-lived assets

In accordance with the provisions of ASC Topic 360, “Impairment or Disposal of Long-Lived Assets”, all long-lived assets such as plant and equipment, as well as intangible assets held and used by the Company are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. Recoverability of assets to be held and used is evaluated by a comparison of the carrying amount of an asset to its estimated future undiscounted cash flows expected to be generated by the asset. If such assets are considered to be impaired, the impairment to be recognized is measured by the amount by which the carrying amounts of the assets exceed the fair value of the assets. There has been no impairment charge for the periods presented.

| 9 |

Revenue recognition

The Company adopted Accounting Standards Codification (“ASC”) Topic 606 – Revenue from Contracts with Customers” (“ASC Topic 606”). Under ASC Topic 606, a performance obligation is a promise within a contract to transfer a distinct good or service, or a series of distinct goods and services, to a customer. Revenue is recognized when performance obligations are satisfied and the customer obtains control of promised goods or services. The amount of revenue recognized reflects the consideration to which the Company expects to be entitled to receive in exchange for goods or services. Under the standard, a contract’s transaction price is allocated to each distinct performance obligation. To determine revenue recognition for arrangements that the Company determines are within the scope of ASC Topic 606, the Company performs the following five steps:

| ● | identify the contract with a customer; | |

| ● | identify the performance obligations in the contract; | |

| ● | determine the transaction price; | |

| ● | allocate the transaction price to performance obligations in the contract; and | |

| ● | recognize revenue as the performance obligation is satisfied. |

Currently, the Company operates two business segments.

Healthcare Business mainly provides health consulting advisory services and healthcare and wellness products to the customers.

Revenue is earned from the rendering of health consulting advisory services to the customers. The Company recognizes services revenue over the period in which such services are performed. Amounts expected to be recognized as revenue within the 12 months following the balance sheet date are classified as current portion of deferred revenue in the accompanying consolidated balance sheets. Amounts not expected to be recognized as revenue within the 12 months following the balance sheet date are classified as deferred revenue, net of current portion.

The

sale and distribution of the healthcare products, such as (i) Nutrition Catering (ii) Special Health Food (iii) Health Supplement and

(iv) Skincare, is the only performance obligation under the fixed-fee arrangements. Revenue is recognized from the sale of their healthcare

products upon delivery to the customers, whereas the title and risk of loss are fully transferred to the customers. The Company records

its revenues, net of value added taxes (“VAT”) on the majority of the products at the rate of

Wine

Business mainly provides the wine products to the customers. Revenue is recognized from the sale of wine products upon delivery to the

customers, whereas the title and risk of loss are fully transferred to the customers. The Company records its revenues, net of value

added taxes (“VAT”) on the majority of the products at the rate of

The following table provides information about disaggregated revenue from customers into the nature of the products and services, and geographic regions, and includes a reconciliation of the disaggregated revenue with reportable segments.

| For the Three Months Ended September 30, 2022 | For the Three Months Ended September 30, 2021 | |||||||

| Consultancy service income | $ | $ | ||||||

| Sales of healthcare | ||||||||

| TOTAL | $ | $ | ||||||

| For the Nine Months Ended September 30, 2022 | For the Nine Months Ended September 30, 2021 | |||||||

| Consultancy service income | $ | $ | ||||||

| Sales of healthcare | ||||||||

| TOTAL | $ | $ | ||||||

Income taxes

The

Company adopted the ASC Topic 740, “Income Taxes” paragraph 740-10-25-13, which addresses the determination of whether

tax benefits claimed or expected to be claimed on a tax return should be recorded in the unaudited condensed consolidated financial statements.

Under paragraph 740-10-25-13, the Company may recognize the tax benefit from an uncertain tax position only if it is more likely than

not that the tax position will be sustained on examination by the taxing authorities, based on the technical merits of the position.

The tax benefits recognized in the condensed consolidated financial statements from such a position should be measured based on the largest

benefit that has a

| 10 |

The estimated future tax effects of temporary differences between the tax basis of assets and liabilities are reported in the accompanying balance sheets, as well as tax credit carry-backs and carry-forwards. The Company periodically reviews the recoverability of deferred tax assets recorded on its balance sheets and provides valuation allowances as management deems necessary.

Uncertain tax positions

The Company did not take any uncertain tax positions and had no adjustments to its income tax liabilities or benefits pursuant to the ASC Topic 740 provisions of Section 740-10-25 for the three and nine months ended September 30, 2022 and 2021, respectively.

Foreign currencies translation

Transactions denominated in currencies other than the functional currency are translated into the functional currency at the exchange rates prevailing at the dates of the transaction. Monetary assets and liabilities denominated in currencies other than the functional currency are translated into the functional currency using the applicable exchange rates at the balance sheet dates. The resulting exchange differences are recorded in the condensed consolidated statement of operations.

The reporting currency of the Company is United States Dollar (“US$”) and the accompanying financial statements have been expressed in US$. In addition, the Company is operating in Hong Kong SAR and the People’s Republic of China and maintain its books and record in its local currency, Hong Kong Dollars (“HK$”) and Renminbi (“RMB”), which is a functional currency as being the primary currency of the economic environment in which their operations are conducted. In general, for consolidation purposes, assets and liabilities of its subsidiaries whose functional currency is not US$ are translated into US$, in accordance with ASC Topic 830-30, “Translation of Financial Statement”, using the exchange rate on the balance sheet date. Revenues and expenses are translated at average rates prevailing during the year. The gains and losses resulting from translation of financial statements of foreign subsidiaries are recorded as a separate component of accumulated other comprehensive income within the statements of changes in shareholders’ equity.

Translation of amounts from HK$ and RMB into US$ has been made at the following exchange rates for the nine months ended September 30, 2022 and 2021:

| 2022 | 2021 | |||||||

| Period-end HK$:US$ exchange rate | ||||||||

| Period average HK$:US$ exchange rate | ||||||||

| Period-end RMB:US$ exchange rate | ||||||||

| Period average RMB:US$ exchange rate | ||||||||

The Company calculates net loss per share in accordance with ASC Topic 260, “Earnings per Share.” Basic income per share is computed by dividing the net income by the weighted-average number of common shares outstanding during the period. Diluted income per share is computed similar to basic income per share except that the denominator is increased to include the number of additional common shares that would have been outstanding if the potential common stock equivalents had been issued and if the additional common shares were dilutive.

Comprehensive income

ASC Topic 220, “Comprehensive Income”, establishes standards for reporting and display of comprehensive income, its components and accumulated balances. Comprehensive income as defined includes all changes in equity during a period from non-owner sources. Accumulated other comprehensive income, as presented in the accompanying condensed consolidated statements of changes in stockholders’ equity, consists of changes in unrealized gains and losses on foreign currency translation. This comprehensive income is not included in the computation of income tax expense or benefit.

Leases

The Company adopted ASC Topic 842, “Leases”, using the modified retrospective approach through a cumulative-effect adjustment and utilizing the effective date of January 1, 2019 as its date of initial application, with prior periods unchanged and presented in accordance with the previous guidance in ASC Topic 840, “Leases”.

| 11 |

At the inception of an arrangement, the Company determines whether the arrangement is or contains a lease based on the unique facts and circumstances present. Leases with a term greater than one year are recognized on the balance sheet as right-of-use (“ROU”) assets, lease liabilities and long-term lease liabilities. The Company has elected not to recognize on the balance sheet leases with terms of one year or less. Operating lease liabilities and their corresponding right-of-use assets are recorded based on the present value of lease payments over the expected remaining lease term. However, certain adjustments to the right-of-use asset may be required for items such as prepaid or accrued lease payments. The interest rate implicit in lease contracts is typically not readily determinable. As a result, the Company utilizes its incremental borrowing rates, which are the rates incurred to borrow on a collateralized basis over a similar term an amount equal to the lease payments in a similar economic environment.

In accordance with the guidance in ASC Topic 842, components of a lease should be split into three categories: lease components (e.g. land, building, etc.), non-lease components (e.g. common area maintenance, consumables, etc.), and non-components (e.g. property taxes, insurance, etc.). Subsequently, the fixed and in-substance fixed contract consideration (including any related to non-components) must be allocated based on the respective relative fair values to the lease components and non-lease components.

Lease expense is recognized on a straight-line basis over the lease terms. Lease expense includes amortization of the ROU assets and accretion of the lease liabilities. Amortization of ROU assets is calculated as the periodic lease cost less accretion of the lease liability. The amortized period for ROU assets is limited to the expected lease term.

The Company has elected a practical expedient to combine the lease and non-lease components into a single lease component. The Company also elected the short-term lease measurement and recognition exemption and does not establish ROU assets or lease liabilities for operating leases with terms of 12 months or less.

Related parties

The Company follows the ASC Topic 850-10, “Related Party Disclosures” for the identification of related parties and disclosure of related party transactions.

Pursuant to section 850-10-20 the related parties include a) affiliates of the Company; b) entities for which investments in their equity securities would be required, absent the election of the fair value option under the Fair Value Option Subsection of section 825–10–15, to be accounted for by the equity method by the investing entity; c) trusts for the benefit of employees, such as pension and Income-sharing trusts that are managed by or under the trusteeship of management; d) principal owners of the Company; e) management of the Company; f) other parties with which the Company may deal if one party controls or can significantly influence the management or operating policies of the other to an extent that one of the transacting parties might be prevented from fully pursuing its own separate interests; and g) other parties that can significantly influence the management or operating policies of the transacting parties or that have an ownership interest in one of the transacting parties and can significantly influence the other to an extent that one or more of the transacting parties might be prevented from fully pursuing its own separate interests.

The financial statements shall include disclosures of material related party transactions, other than compensation arrangements, expense allowances, and other similar items in the ordinary course of business. However, disclosure of transactions that are eliminated in the preparation of consolidated or combined financial statements is not required in those statements. The disclosures shall include: a) the nature of the relationship(s) involved; b) a description of the transactions, including transactions to which no amounts or nominal amounts were ascribed, for each of the periods for which income statements are presented, and such other information deemed necessary to an understanding of the effects of the transactions on the financial statements; c) the dollar amounts of transactions for each of the periods for which income statements are presented and the effects of any change in the method of establishing the terms from that used in the preceding period; and d) amount due from or to related parties as of the date of each balance sheet presented and, if not otherwise apparent, the terms and manner of settlement.

Commitments and contingencies

The Company follows the ASC Topic 450-20, “Contingencies” to report accounting for contingencies. Certain conditions may exist as of the date the financial statements are issued, which may result in a loss to the Company but which will only be resolved when one or more future events occur or fail to occur. The Company assesses such contingent liabilities, and such assessment inherently involves an exercise of judgment. In assessing loss contingencies related to legal proceedings that are pending against the Company or un-asserted claims that may result in such proceedings, the Company evaluates the perceived merits of any legal proceedings or un-asserted claims as well as the perceived merits of the amount of relief sought or expected to be sought therein.

| 12 |

If the assessment of a contingency indicates that it is probable that a material loss has been incurred and the amount of the liability can be estimated, then the estimated liability would be accrued in the Company’s financial statements. If the assessment indicates that a potentially material loss contingency is not probable but is reasonably possible, or is probable but cannot be estimated, then the nature of the contingent liability, and an estimate of the range of possible losses, if determinable and material, would be disclosed.

Loss contingencies considered remote are generally not disclosed unless they involve guarantees, in which case the guarantees would be disclosed. Management does not believe, based upon information available at this time that these matters will have a material adverse effect on the Company’s financial position, results of operations or cash flows. However, there is no assurance that such matters will not materially and adversely affect the Company’s business, financial position, and results of operations or cash flows.

Fair value of financial instruments

The Company follows ASC Topic 825 “Financial Instruments” paragraph 825-10-50-10 for disclosures about fair value of its financial instruments and has adopted paragraph 820-10-35-37 to measure the fair value of its financial instruments. Paragraph 820-10-35-37 establishes a framework for measuring fair value in generally accepted accounting principles (GAAP), and expands disclosures about fair value measurements. To increase consistency and comparability in fair value measurements and related disclosures, paragraph 820-10-35-37 establishes a fair value hierarchy which prioritizes the inputs to valuation techniques used to measure fair value into three (3) broad levels. The fair value hierarchy gives the highest priority to quoted prices (unadjusted) in active markets for identical assets or liabilities and the lowest priority to unobservable inputs. The three (3) levels of fair value hierarchy defined by paragraph 820-10-35-37 are described below:

| Level 1 | Quoted market prices available in active markets for identical assets or liabilities as of the reporting date. | ||

| Level 2 | Pricing inputs other than quoted prices in active markets included in Level 1, which are either directly or indirectly observable as of the reporting date. | ||

| Level 3 | Pricing inputs that are generally observable inputs and not corroborated by market data. |

Financial assets are considered Level 3 when their fair values are determined using pricing models, discounted cash flow methodologies or similar techniques and at least one significant model assumption or input is unobservable.

The fair value hierarchy gives the highest priority to quoted prices (unadjusted) in active markets for identical assets or liabilities and the lowest priority to unobservable inputs. If the inputs used to measure the financial assets and liabilities fall within more than one level described above, the categorization is based on the lowest level input that is significant to the fair value measurement of the instrument.

The carrying amounts of the Company’s financial assets and liabilities, such as cash and cash equivalents, approximate their fair values because of the short maturity of these instruments.

Segment Reporting

ASC

Topic 280, “Segment Reporting” establishes standards for reporting information about operating segments on a basis

consistent with the Company’s internal organization structure as well as information about geographical areas, business segments

and major customers in consolidated financial statements. Currently, the Company operates in

The Company has reviewed all recently issued, but not yet effective, accounting pronouncements and does not believe the future adoption of any such pronouncements may be expected to cause a material impact on its financial condition or the results of its operations.

Recent accounting pronouncements

From time to time, new accounting pronouncements are issued by the Financial Accounting Standard Board (“FASB”) or other standard setting bodies and adopted by the Company as of the specified effective date. Unless otherwise discussed, the Company believes that the impact of recently issued standards that are not yet effective will not have a material impact on its financial position or results of operations upon adoption.

In May 2021, the FASB issued ASU 2021-04, Earnings Per Share (Topic 260), Debt-Modifications and Extinguishments (Subtopic 470-50), Compensation-Stock Compensation (Topic 718), and Derivatives and Hedging-Contracts in Entity’s Own Equity (Subtopic 815-40), (“ASU 2021-04”). This ASU reduces diversity in an issuer’s accounting for modifications or exchanges of freestanding equity-classified written call options (for example, warrants) that remain equity classified after modification or exchange. This ASU provides guidance for a modification or an exchange of a freestanding equity-classified written call option that is not within the scope of another Topic. It specifically addresses: (1) how an entity should treat a modification of the terms or conditions or an exchange of a freestanding equity-classified written call option that remains equity classified after modification or exchange; (2) how an entity should measure the effect of a modification or an exchange of a freestanding equity-classified written call option that remains equity classified after modification or exchange; and (3) how an entity should recognize the effect of a modification or an exchange of a freestanding equity-classified written call option that remains equity classified after modification or exchange. This ASU will be effective for all entities for fiscal years beginning after December 15, 2021. An entity should apply the amendments prospectively to modifications or exchanges occurring on or after the effective date of the amendments. Early adoption is permitted, including adoption in an interim period. The adoption of ASU 2021-04 on January 1, 2022 did not have a material impact on the Company’s financial statements or disclosures.

| 13 |

NOTE 3 - SEGMENT REPORTING

Currently,

the Company has

| (i) | Healthcare Segment, mainly provides health consulting advisory services and healthcare and wellness products to the customers; and |

| (ii) | Wine Segment, mainly provides the wine products to the customers. |

| Three months ended 30 September, 2022 | ||||||||||||

| Healthcare Segment | Wine Segment | Total | ||||||||||

| Revenue from external customers: | ||||||||||||

| Consulting service income | $ | $ | $ | |||||||||

| Sale of healthcare products | ||||||||||||

| Total revenue | ||||||||||||

| Cost of sales: | ||||||||||||

| Consulting service income | ( | ) | ( | ) | ||||||||

| Sale of healthcare products | ( | ) | ( | ) | ||||||||

| Total cost of revenue | ( | ) | ( | ) | ( | ) | ||||||

| Gross (loss) profit | ( | ) | ( | ) | ||||||||

| Operating Expenses | ||||||||||||

| Selling and distribution | ||||||||||||

| General and administrative | ( | ) | ( | ) | ( | ) | ||||||

| Total operating expenses | ( | ) | ( | ) | ( | ) | ||||||

| Segment loss | $ | ( | ) | $ | ( | ) | $ | ( | ) | |||

| Three months ended 30 September, 2021 | ||||||||||||

| Healthcare Segment | Wine Segment | Total | ||||||||||

| Revenue from external customers: | ||||||||||||

| Consulting service income | $ | $ | $ | |||||||||

| Sale of healthcare products | ||||||||||||

| Total revenue | ||||||||||||

| Cost of sales: | ||||||||||||

| Consulting service income | ( | ) | ( | ) | ||||||||

| Sale of healthcare products | ||||||||||||

| Total cost of revenue | ( | ) | ( | ) | ||||||||

| Gross profit | ||||||||||||

| Operating Expenses | ||||||||||||

| Selling and distribution | ( | ) | ( | ) | ||||||||

| General and administrative | ( | ) | ( | ) | ( | ) | ||||||

| Total operating expenses | ( | ) | ( | ) | ( | ) | ||||||

| Segment income (loss) | $ | $ | ( | ) | $ | ( | ) | |||||

| Nine months ended September 30, 2022 | ||||||||||||

| Healthcare Segment | Wine Segment | Total | ||||||||||

| Revenue from external customers: | ||||||||||||

| Consulting service income | $ | $ | $ | |||||||||

| Sale of healthcare products | ||||||||||||

| Total revenue | ||||||||||||

| Cost of sales: | ||||||||||||

| Consulting service income | ( | ) | ( | ) | ||||||||

| Sale of healthcare products | ( | ) | ( | ) | ||||||||

| Total cost of revenue | ( | ) | ( | ) | ( | ) | ||||||

| Gross profit | ||||||||||||

| Operating Expenses | ||||||||||||

| Selling and distribution | ( | ) | ( | ) | ||||||||

| General and administrative | ( | ) | ( | ) | ( | ) | ||||||

| Total operating expenses | ( | ) | ( | ) | ( | ) | ||||||

| Segment loss | $ | ( | ) | $ | ( | ) | $ | ( | ) | |||

| 14 |

| Nine months ended September 30, 2021 | ||||||||||||

| Healthcare Segment | Wine Segment | Total | ||||||||||

| Revenue from external customers: | ||||||||||||

| Consulting service income | $ | $ | $ | |||||||||

| Sale of health | ||||||||||||

| Total revenue | ||||||||||||

| Cost of sales: | ||||||||||||

| Consulting service income | ||||||||||||

| Sale of healthcare products | ( | ) | ( | ) | ||||||||

| Total cost of revenue | ( | ) | ( | ) | ||||||||

| Gross profit | ||||||||||||

| Operating Expenses | ||||||||||||

| Selling and distribution | ( | ) | ( | ) | ||||||||

| General and administrative | ( | ) | ( | ) | ( | ) | ||||||

| Total operating expenses | ( | ) | ( | ) | ( | ) | ||||||

| Segment income (loss) | $ | $ | ( | ) | $ | ( | ) | |||||

NOTE 4 - PREPAYMENTS AND OTHER RECEIVABLES

Prepayments and other receivables consisted of the following:

September 30, 2022 | December 31, 2021 | |||||||

| Prepayments | $ | $ | ||||||

| Other deposits | ||||||||

| Other receivables | ||||||||

| $ | $ | |||||||

Other receivables represented deposit payments made to suppliers for daily operation and procurement, which are interest-free, unsecured and received by the Company when the cooperation with suppliers are terminated.

NOTE 5 - INVENTORIES

Inventories consisted of the following:

September 30, 2022 |

December 31, 2021 |

|||||||

| Finished goods - wine | $ | $ | ||||||

For

the three and nine months ended September 30, 2022 and 2021,

| 15 |

NOTE 6 - LEASE

Right of use assets and lease liability – right of use are as follows:

September 30, 2022 |

December 31, 2021 |

|||||||

| Right-of-use assets | $ | $ | ||||||

The lease liability – right of use is as follows:

September 30, 2022 | December 31, 2021 | |||||||

| Current portion | ||||||||

| Non-current portion | ||||||||

| Total | $ | $ | ||||||

As

of September 30, 2022, the operating lease payment of $

NOTE 7 - PLANT AND EQUIPMENT

September 30, 2022 |

December 31, 2021 |

|||||||

| Motor vehicle | $ | $ | ||||||

| Furniture, fixture and equipment | ||||||||

| Leasehold improvement | ||||||||

| Foreign translation adjustment | ( |

) | ||||||

| Less: accumulated depreciation | ( |

) | ( |

) | ||||

| Foreign translation adjustment | ( |

) | ||||||

| Plant and equipment, net | $ | $ | ||||||

Depreciation

expense for the three and nine months ended September 30, 2022 were $

Depreciation

expense for the three and nine months ended September 30, 2021 were $

NOTE - 8 AMOUNTS DUE TO A DIRECTOR AND A RELATED COMPANY

As of September 30, 2022 and December 31, 2021, the amounts represented temporary advances to the Company by its director and its related company which were unsecured, interest-free and have no fixed terms of repayments.

NOTE 9 – SHAREHOLDERS’ EQUITY

Preferred Stock

The Company is not currently authorized to issue shares of preferred stock. The Certificate of Incorporation however, allows the board of directors to authorize the issuance of preferred stock with voting or conversion rights that could adversely affect the voting power or other rights of the holders of the common stock in the event that shares of preferred stock are authorized in the future. The issuance of preferred stock, while providing flexibility in connection with possible acquisitions and other corporate purposes, could, among other things, have the effect of delaying, deferring or preventing a change in control of our company and may adversely affect the market price of our common stock and the voting and other rights of the holders of common stock. The Company has no current plans to issue any shares of preferred stock.

Common Stock

The Company is authorized, subject to limitations prescribed by Delaware law, to issue up to shares of common stock with a nominal par value of $.

| 16 |

Dividend Rights

Subject to preferences that may apply to shares of preferred stock outstanding at the time, the holders of outstanding shares of our common stock are entitled to receive dividends out of funds legally available if our board of directors, in its discretion, determines to issue dividends and only then at the times and in the amounts that our board of directors may determine.

Voting Rights

Each holder of common stock is entitled to one vote for each share of common stock held on all matters submitted to a vote of stockholders. Under our Certificate of Incorporation, stockholders do not have the right to cumulate votes for the election of directors.

No Preemptive or Similar Rights

Our common stock is not entitled to preemptive rights and is not subject to conversion, redemption or sinking fund provisions.

Right to Receive Liquidation Distributions

Upon our dissolution, liquidation or winding-up, the assets legally available for distribution to our stockholders are distributable ratably among the holders of our common stock, subject to prior satisfaction of all outstanding debt and liabilities and the preferential rights and payment of liquidation preferences, if any, on any outstanding shares of preferred stock.

As of September 30, 2022 and December 31, 2021, a total of and outstanding shares of common stock were issued, respectively.

NOTE 10 - INCOME TAXES

The provision for income taxes consisted of the following:

| Nine months ended September 30, | ||||||||

| 2022 | 2021 | |||||||

| Current tax | $ | $ | ||||||

| Deferred tax | ||||||||

| Income tax expense | $ | $ | ||||||

The Company mainly operates in the PRC that is subject to taxes in the governing jurisdictions in which it operates. The effective tax rate in the years presented is the result of the mix of income earned in various tax jurisdictions that apply a broad range of income tax rate, as follows:

BVI

Under the current BVI law, the Company is not subject to tax on income.

| 17 |

The PRC

| Nine months ended September 30, | ||||||||

| 2022 | 2021 | |||||||

| Loss before income taxes | $ | ( | ) | $ | ( | ) | ||

| Statutory income tax rate | % | % | ||||||

| Income tax expense at statutory rate | ( | ) | ( | ) | ||||

| Net operating loss | ||||||||

| Income tax expense | $ | $ | ||||||

Hong Kong

| Nine months ended September 30, | ||||||||

| 2022 | 2021 | |||||||

| Profit before income taxes | $ | $ | ||||||

| Statutory income tax rate | % | % | ||||||

| Income tax expense at statutory rate | ||||||||

| Tax adjustments | ||||||||

| One-off tax reduction | ( | ) | ||||||

| Income tax expense | $ | $ | ||||||

The following table sets forth the significant components of the deferred tax assets of the Company as of September 30, 2022 and December 31, 2021:

September 30, 2022 | December 31, 2021 | |||||||

| Deferred tax assets: | ||||||||

| Net operating loss carryforwards | ||||||||

| - United States | $ | |||||||

| - PRC | ||||||||

| Less: valuation allowance | ( | ) | ( | ) | ||||

| Deferred tax assets, net | $ | $ | ||||||

NOTE 11 - RELATED PARTY TRANSACTIONS

From time to time, the Company’s director advanced funds to the Company for working capital purpose. Those advances are unsecured, non-interest bearing and due on demand.

The Company has been provided free office space by its stockholder. The management determined that such cost is nominal and did not recognize the rent expense in its unaudited condensed consolidated financial statements.

Apart from the transactions and balances detailed elsewhere in these accompanying unaudited condensed consolidated financial statements, the Company has no other significant or material related party transactions during the periods presented.

| 18 |

NOTE 12 - CONCENTRATIONS OF RISK

The Company is exposed to the following concentrations of risk:

(a) Major customers

For the three and nine months ended September 30, 2022 and 2021, the customers who accounts for 10% or more of the Company’s revenues and its outstanding receivables balance as at period-end dates, are presented as follows:

| Three Months ended September 30, 2022 | ||||||||

| Customer | Revenues | Percentage of revenues | ||||||

| Customer D | $ | % | ||||||

| Nine months ended September 30, 2022 | As of September 30, 2022 | |||||||||||||||||||

| Customer | Revenues | Percentage of revenues | Accounts receivable | Percentage of Accounts Receivable | ||||||||||||||||

| Customer C | % | |||||||||||||||||||

| Customer D | % | |||||||||||||||||||

| Total: | $ | % | Total | |||||||||||||||||

| Three Months ended September 30, 2021 | ||||||||

| Customer | Revenues | Percentage of revenues | ||||||

| Customer B | $ | % | ||||||

| Nine Months ended September 30, 2021 | September 30,2021 | |||||||||||||||

| Customer | Revenues | Percentage of revenues | Accounts receivable | Percentage of Accounts Receivable | ||||||||||||

| Customer B | $ | % | ||||||||||||||

| Customer A | % | |||||||||||||||

| Customer C | % | |||||||||||||||

| Total: | $ | % | ||||||||||||||

The Company’s customers are located in the People’s Republic of China and Hong Kong.

(a) Major vendors

For the three and nine months ended September 30, 2022, there is no single vendor represented more than 10% of the Company’s purchases.

For

the three and nine months ended September 30, 2021, a single vendor represented more than 10% of the Company’s purchases. This

vendor accounted for

| 19 |

All of the Company’s vendors are located in the People’s Republic of China.

(c) Credit risk

Financial instruments that are potentially subject to credit risk consist principally of trade receivables. The Company believes the concentration of credit risk in its trade receivables is substantially mitigated by its ongoing credit evaluation process and relatively short collection terms. The Company does not generally require collateral from customers. The Company evaluates the need for an allowance for doubtful accounts based upon factors surrounding the credit risk of specific customers, historical trends and other information.

(d) Economic and political risk

The Company’s major operations are conducted in the People’s Republic of China. Accordingly, the political, economic, and legal environments in PRC, as well as the general state of PRC’s economy may influence the Company’s business, financial condition, and results of operations.

(e) Exchange rate risk

The Company cannot guarantee that the current exchange rate will remain steady; therefore there is a possibility that the Company could post the same amount of profit for two comparable periods and because of the fluctuating exchange rate actually post higher or lower profit depending on exchange rate of RMB converted to US$ on that date. The exchange rate could fluctuate depending on changes in political and economic environments without notice.

NOTE 13 - COMMITMENTS AND CONTINGENCIES

As of September 30, 2022, the Company has no material commitments or contingencies.

NOTE 14 - SUBSEQUENT EVENTS

In accordance with ASC Topic 855, “Subsequent Events”, which establishes general standards of accounting for and disclosure of events that occur after the balance sheet date but before financial statements are issued, the Company has evaluated all events or transactions that occurred after September 30, 2022 up through the date the Company issued the unaudited condensed consolidated financial statements. During the period, the Company did not have any material recognizable subsequent events.

| 20 |

Item 2. Management’s Discussion and Analysis or Plan of Operation.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This periodic report contains certain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 with respect to the financial condition, results of operations, business strategies, operating efficiencies or synergies, competitive positions, growth opportunities for existing products, plans and objectives of management. Statements in this periodic report that are not historical facts are hereby identified as forward-looking statements. Our Company and our representatives may from time to time make written or oral statements that are “forward-looking,” including statements contained in this Quarterly Report and other filings with the Securities and Exchange Commission and in reports to our Company’s stockholders. Management believes that all statements that express expectations and projections with respect to future matters, as well as from developments beyond our Company’s control including changes in global economic conditions are forward-looking statements within the meaning of the Act. These statements are made on the basis of management’s views and assumptions, as of the time the statements are made, regarding future events and business performance. There can be no assurance, however, that management’s expectations will necessarily come to pass. Factors that may affect forward-looking statements include a wide range of factors that could materially affect future developments and performance, including the following:

Changes in Company-wide strategies, which may result in changes in the types or mix of businesses in which our Company is involved or chooses to invest; changes in U.S., global or regional economic conditions; changes in U.S. and global financial and equity markets, including significant interest rate fluctuations, which may impede our Company’s access to, or increase the cost of, external financing for our operations and investments; increased competitive pressures, both domestically and internationally; legal and regulatory developments, such as regulatory actions affecting environmental activities; the imposition by foreign countries of trade restrictions and changes in international tax laws or currency controls; adverse weather conditions or natural disasters, such as hurricanes and earthquakes; and labor disputes, which may lead to increased costs or disruption of operations.

This list of factors that may affect future performance and the accuracy of forward-looking statements are illustrative, but by no means exhaustive. Accordingly, all forward-looking statements should be evaluated with the understanding of their inherent uncertainty.

Business Overview

We are a health and wellness company that develops, markets, promotes and distributes a variety of customized health and wellness care products and services, including supplements, healthy snacks, meal replacements, skincare products, and nutritional consultation services to consumers in China. We work with certain licensed healthcare food factories to develop and manufacture products and services that are distributed conventionally through sales agents and also through a network of e-commerce and social media platforms.

In addition to products, we are committed to providing customized science based wellness consultation and service programs to customers. Our diverse products and services target health conscious customers and differentiate based upon age and gender and seek to manage different conditions. We reach out to customers fitting certain health and lifestyle profiles through our offline and online consultation services, and track eating habits and health indicators to provide customized products such as supplements. We believe this will facilitate the ability of customers to monitor, understand and adjust their health practices and lifestyle anytime and anywhere for increased customer engagement and retention.

We conduct our business through our wholly owned subsidiary Guangzhou Xiao Xiang Health Industry Company Limited, a limited liability company organized under the laws of China on March 8, 2017 and Alpha Wellness (HK) Limited, a limited liability company organized under the laws of Hong Kong on April 24, 2019. Elite Creation Group, a limited liability company formed under the laws of the British Virgin Islands formed on September 5, 2018, is holding companies without operations.

| 21 |

Discussion and Analysis of Financial Condition and Results of Operations

RESULTS OF OPERATIONS

We have been significantly impacted by COVID-19 global pandemic. In addition to the devastating effects on human life, the pandemic is having a negative ripple effect on the global economy, leading to disruptions and volatility in the global financial markets. China and many other countries have issued policies intended to stop or slow the further spread of the disease.

COVID-19 and China’s response to the pandemic are significantly affecting the economy. There are no comparable events that provide guidance as to the effect the COVID-19 pandemic may have, and, as a result, the ultimate effect of the pandemic is highly uncertain and subject to change. We do not yet know the full extent of the effects on the economy, the markets we serve, our business or our operations.

The following table sets forth certain operational data for the three and nine months ended September 30, 2022 and 2021:

| Three Months Ended | Three Months Ended | |||||||

| September 30, 2022 | September 30, 2021 | |||||||

| Revenue, net | $ | 5,395 | $ | 69,726 | ||||

| Cost of revenue | (22,498 | ) | (6,079 | ) | ||||

| Gross (loss) profit | (17,103 | ) | 63,647 | |||||

| Total operating expenses | (99,309 | ) | (145,684 | ) | ||||

| Total other income | 19,622 | 247 | ||||||

| Loss before income tax | (96,790 | ) | (81,790 | ) | ||||

| Income tax expenses | 2,607 | - | ||||||

| Net loss | (94,183 | ) | (81,790 | ) | ||||

| Nine Months Ended | Nine Months Ended | |||||||

| September 30, 2022 | September 30, 2021 | |||||||

| Revenue, net | $ | 169,029 | $ | 504,295 | ||||

| Cost of revenue | (69,809 | ) | (202,506 | ) | ||||

| Gross profit | 99,220 | 301,789 | ||||||

| Total operating expenses | (334,650 | ) | (561,413 | ) | ||||

| Total other income | 30,666 | 7,437 | ||||||

| Loss before income tax | (204,764 | ) | (252,187 | ) | ||||

| Income tax expenses | (3,966 | ) | - | |||||

| Net loss | (208,730 | ) | (252,187 | ) | ||||

Revenue. For the three and nine months ended September 30, 2022, we generated revenues of $5,395 and $169,029, respectively. For the comparative three and nine months ended September 30, 2021, we generated revenues of $69,726 and $504,295, respectively. The significant decrease in revenue because a significant drop in the sales of $240,831 in the PRC. The major customers are located in Hong Kong during the period ended September 30, 2022, while the major customers are located in the PRC during the period ended September 30, 2021.

Cost of Revenue. For the three and nine months ended September 30, 2022, the cost of revenue was $22,498 and $69,809, respectively, and as a percentage of net revenue, approximately 417% and 41%. Cost of revenue for the three and nine months ended September 30, 2021 was $6,079 and $202,506, respectively, and as a percentage of net revenue, approximately 9% and 40%, respectively. The cost of revenue decreased due to a significant drop in the sales in the PRC and the major income was from Hong Kong mentioned above.

| 22 |

Operation expenses. For the three and nine months ended September 30, 2022, the operation cost was $99,309 and $334,650, respectively, and while for the three and nine months ended September 30, 2021 was $145,684 and $561,413, respectively. The operation expenses decreased due to a decrease in administrative expenses.

Other income. For the three and nine months ended September 30, 2022, the other income was $19,622 and $30,666, respectively and while for the three and nine months ended September 30, 2021 was $247 and $7,437, respectively. The other income increased due to receipt of government subsidies and gain on sale of motor vehicles during the period ended September 30, 2022.

Net Loss. For the three and nine months ended September 30, 2022, we incurred a net loss of $94,183 and $208,730, respectively and while for the three and nine months ended September 30, 2021, we incurred a net loss of $81,790 and net loss of $252,187, respectively. The decrease in net loss is primarily attributable to the decrease in administrative expenses and decrease in revenue.

Liquidity and Capital Resources

As of September 30, 2022, we had cash and cash equivalents of $421,699, inventories of $278,187, right of use assets of $236,796, tax recoverable of $1,021, and prepayments and other receivables of $97,687.

As of December 31, 2021, we had cash and cash equivalents of $609,434, inventories of $327,551, right-of- use assets of $350,563, tax recoverable of $8,910, and prepayments and other receivables of $139,254.

We believe that our current cash and other sources of liquidity discussed below are adequate to support general operations for at least the next 12 months.

| Nine Months Ended September 30, | ||||||||

| 2022 | 2021 | |||||||

| Net cash used in operating activities | $ | (113,647 | ) | $ | (377,470 | ) | ||

| Net cash provided by (used in) investing activities | 22,930 | (27,358 | ) | |||||

| Net cash (used in) provided by financing activities | (77,990 | ) | 43,672 | |||||

Net Cash Used In Operating Activities.

For the nine months ended September 30, 2022, net cash used in operating activities was $113,647, which consisted primarily of decrease in prepayments and other receivables of $41,567, decrease in inventories of $49,364, decrease in accrued liabilities and other payables of $1,701, decrease in income tax recoverable of $7,889, and decrease in customers deposits of $108,265.

For the nine months ended September 30, 2021, net cash used in operating activities was $377,470, which consisted primarily of the increase in accounts receivables of $167,183, increase in prepayments and other receivables of $8,692, decrease in inventories of $7,035, increase in accrued liabilities and other payables of $48,205, decrease in accounts payable of $7,827, decrease in income tax payable of $5,058, decrease in customers deposits of $134,334, and increase in lease liabilities of $63,522.

We expect to continue to rely on cash generated through financing from our existing shareholders and private placements of our securities, however, to finance our operations and future acquisitions.

Net Cash Provided By (Used In) Investing Activities.

For the nine months ended September 30, 2022, net cash provided by investing activities was $22,930, consisted primarily of proceeds from sale of motor vehicle.

For the nine months ended September 30, 2021, net cash used in investing activities was $27,358, consisted primarily of addition of leasehold improvement.

Net Cash (Used In) Provided By Financing Activities.

For the nine months ended September 30, 2022, net cash provided by financing activities was $43,672, which consisted primarily of advance from a director of $1,974 and repayment of lease liabilities of $76,016.

For the nine months ended September 30, 2021 net cash provided by financing activities was $43,672, which consisted primarily of advance from a director of $112,153 and repayment of lease liabilities of $68,481

| 23 |

Off Balance Sheet Arrangements

We have not entered into any off-balance sheet arrangements and it is not anticipated that the Company will enter into any off-balance sheet arrangements.

Critical Accounting Policies, Judgments and Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States requires our management to make assumptions, estimates and judgments that affect the amounts reported, including the notes thereto, and related disclosures of commitments and contingencies, if any. We have identified certain accounting policies that are significant to the preparation of our financial statements. These accounting policies are important for an understanding of our financial condition and results of operations. Critical accounting policies are those that are most important to the presentation of our financial condition and results of operations and require management’s subjective or complex judgment, often as a result of the need to make estimates about the effect of matters that are inherently uncertain and may change in subsequent periods. Certain accounting estimates are particularly sensitive because of their significance to financial statements and because of the possibility that future events affecting the estimate may differ significantly from management’s current judgments. We believe the following accounting policies are critical in the preparation of our financial statements.

The Company’s accounting policies are more fully described in Note 2 of the financial statements. As discussed in Note 2, the preparation of financial statements and related disclosures in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions about the future events that affect the amounts reported in the financial statements and the accompanying notes. Management bases its estimates on historical experience and on various other assumptions that are believed to be reasonable under the circumstances. Actual differences could differ from these estimates under different assumptions or conditions. The Company believes that the following addresses the Company’s most critical accounting policies.

Deferred tax assets and liabilities are measured using enacted tax rates in effect for the year in which the differences are expected to reverse. Deferred tax assets will be reflected on the balance sheet when it is determined that it is more likely than not that the asset will be realized. A valuation allowance has currently been recorded to reduce our deferred tax asset to $0.

Forward-looking Statements

The Private Securities Litigation Reform Act of 1995 (the “Act”) provides a safe harbor for forward-looking statements made by or on behalf of our Company. Our Company and our representatives may from time to time make written or oral statements that are “forward-looking,” including statements contained in this report and other filings with the Securities and Exchange Commission and in reports to our Company’s stockholders. Management believes that all statements that express expectations and projections with respect to future matters, as well as from developments beyond our Company’s control including changes in global economic conditions are forward-looking statements within the meaning of the Act. These statements are made on the basis of management’s views and assumptions, as of the time the statements are made, regarding future events and business performance. There can be no assurance, however, that management’s expectations will necessarily come to pass. Factors that may affect forward-looking statements include a wide range of factors that could materially affect future developments and performance, including the following:

Changes in Company-wide strategies, which may result in changes in the types or mix of businesses in which our Company is involved or chooses to invest; changes in U.S., global or regional economic conditions; changes in U.S. and global financial and equity markets, including significant interest rate fluctuations, which may impede our Company’s access to, or increase the cost of, external financing for our operations and investments; increased competitive pressures, both domestically and internationally; legal and regulatory developments, such as regulatory actions affecting environmental activities; the imposition by foreign countries of trade restrictions and changes in international tax laws or currency controls; adverse weather conditions or natural disasters, such as hurricanes and earthquakes; and labor disputes, which may lead to increased costs or disruption of operations.

This list of factors that may affect future performance and the accuracy of forward-looking statements is illustrative, but by no means exhaustive. Accordingly, all forward-looking statements should be evaluated with the understanding of their inherent uncertainty.

| 24 |

Item 3. Quantitative and Qualitative Disclosures about Market Risk

Not required for smaller reporting companies.

Item 4. Controls and Procedures

Our Chief Executive Officer and Chief Financial Officer are responsible for establishing and maintaining disclosure controls and procedures for the Company.

(a) Evaluation of Disclosure Controls and Procedures