UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |||||

For the fiscal year ended December 31 , 2020

or

| Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 | |||||

For the transition period from _______ to _______

Commission file number 001-35108

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||||||||

| (Address of principal executive offices) | (Zip Code) | ||||||||||

Registrant’s telephone number, including area code (720 ) 889-8500

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||||||

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definition of “large accelerated filer, “accelerated filer”, “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | ☒ | ||||||||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||||||||

| Emerging growth company | ||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C.7262(b)) by the registered public accounting firm that prepared or issued its audit report.

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ☒

The aggregate market value of voting and non-voting common stock held by non-affiliates of the registrant as of June 30, 2020, the last business day of the Registrant’s most recently completed second fiscal quarter, was approximately $83.6 million. Shares of common stock held by each executive officer, director and holder of 5% or more of the outstanding common stock have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status does not reflect a determination that such persons are affiliates of the registrant for any other purpose.

As of February 18, 2021, there were approximately 97,263,099 shares of the registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

TABLE OF CONTENTS

| Page | ||||||||

| PART I | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 1B. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| PART II | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

| Item 7. | ||||||||

| Item 7A. | ||||||||

| Item 8. | ||||||||

| Item 9. | ||||||||

| Item 9A. | ||||||||

| Item 9B. | ||||||||

| PART III | ||||||||

| Item 10. | ||||||||

| Item 11. | ||||||||

| Item 12. | ||||||||

| Item 13. | ||||||||

| Item 14. | ||||||||

| PART IV | ||||||||

| Item 15. | ||||||||

| Item 16. | ||||||||

i

FORWARD LOOKING STATEMENTS

This Annual Report on Form 10-K (this “annual report") includes estimates, projections, statements relating to our business plans, objectives, and expected operating results that are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements may appear throughout this annual report. These forward-looking statements are generally identified by the words “believe,” “project,” "target," "forecast", “expect,” “anticipate,” “estimate,” “intend,” “strategy,” “future,” “opportunity,” “plan,” “may,” “should,” “will,” “would,” “will be,” “will continue,” “will likely result,” and variations of such words or similar expressions. Forward-looking statements are based on current expectations and assumptions that are subject to risks and uncertainties that may cause actual results to differ materially. Factors that could cause or contribute to such differences include, but are not limited to, those identified elsewhere in this annual report, including the risks and uncertainties related to the impact and duration of the COVID-19 pandemic in “Risk Factors” (Part I, Item 1.A. of this Form 10-K) and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” (Part II, Item 7 of this Form 10-K). Except as required by law, we undertake no obligation to update or revise publicly any forward-looking statements, whether because of new information, future events, or otherwise, except as required by applicable law.

“ServiceSource,” “the Company,” “we,” “us,” or “our”, as used herein, refer to ServiceSource International, Inc. and its wholly owned subsidiaries, unless the context indicates otherwise.

For a summary of commonly used industry terms and abbreviations used in this annual report, see the Glossary of Terms.

PART I

| ITEM 1. | BUSINESS | ||||

About ServiceSource

ServiceSource is a leading provider of BPaaS solutions that enable the transformation of go-to-market organizations and functions for global technology clients. We design, deploy, and operate a suite of innovative solutions and complex processes that support and augment our clients’ B2B customer acquisition, engagement, expansion and retention activities. Our clients - ranging from Fortune 500 technology titans to high-growth disruptors and innovators - rely on our holistic customer engagement methodology and process excellence, global scale and delivery footprint, and data analytics and business insights to deliver trusted business outcomes that have a meaningful and material positive impact to their long-term revenue and profitability objectives. Through our unique integration of people, process and technology - leveraged against our more than 20 years of experience and domain expertise in the cloud, software, hardware, medical device and diagnostic equipment, and industrial IoT sectors - we effect and transact billions of dollars of B2B commerce in more than 175 countries on our clients’ behalf annually.

Our services are delivered globally by approximately 2,800 professionals speaking 45 languages. Our net revenue was $194.6 million for the year ended December 31, 2020.

Our Market Opportunity

Our clients operate in rapidly changing and dynamic environments where they face increasing pressure to gain market share, expand globally, accelerate revenue growth, and streamline operating expenses. In an era of more intense competition, rapid technology disruption, and lower customer switching costs, the most successful B2B companies are recognizing the imperative of a customer-centric mindset. Enabling and delivering a superior customer experience is mission-critical for these companies, yet many lack the appropriate internal resources and capabilities required for longstanding success. Increasingly, they are seeking strategic partners and thought leaders who possess the requisite expertise and proven competencies to enhance the loyalty and lifetime value of their customers by accelerating their go-to-market transformation strategies. Against this market opportunity backdrop, we believe ServiceSource is uniquely positioned and competitively differentiated to benefit from the following dynamics:

•Consumerization of B2B commerce. In today’s hyper-connected digital economy, individuals have become accustomed to engaging with B2C brands through channels and interactions that are efficient, effective and effortless. These individuals are bringing their consumer expectations into the workplace, fundamentally reshaping how companies market, sell to and engage with their business customers. The majority of business buyers expect their B2B customer experiences to mirror their B2C encounters and are willing to award a greater share of wallet and higher loyalty to vendors who can meet these raised expectations. While factors such as price, quality and feature functionality remain important considerations, leading B2B companies recognize that durable competitive advantage is increasingly based on facilitating interactions that are proactive, predictive and personalized across all touchpoints of the customer journey. We believe more companies are turning to external specialists like ServiceSource to structure,

1

deploy and operate integrated solutions and processes that can holistically address and serve the unique and heightened demands of this emerging consumerization trend.

•Deployment of customer-centric models that disrupt legacy go-to-market channels. Technology companies have relied for decades on a variety of third-party intermediaries to reach their mid-market customers. For many companies, 50% - 75% or more of their revenue has historically been attributed to indirect channels, including distributors, resellers, system integrators, and managed service providers, among others. These legacy routes to market are rapidly losing relevance due to the consumerization of IT, the growth of as-a-service offerings, the proliferation of cloud delivery and distribution models, and the rapid adoption of subscription and consumption-based billing plans. In light of these shifts and driven by a growing desire for greater customer insight and intimacy, more companies are deprioritizing investments away from these indirect channels, while assigning more focus to direct-to-consumer pathways. We believe these organizations are looking to strategic thought leaders such as ServiceSource who can help them reimagine their go-to-market strategies, accelerate their channel transformation initiatives, and design and manage new customer-centric operating models that will enable them to grow closer to their customers.

•Emergence of customer experience as a competitive differentiator. Increased global competition, lower barriers to entry and shortened product lifecycles are prompting technology companies to reassess their competitive advantage and reevaluate their core competencies. While areas such as intellectual property, engineering, research and development, and product development still remain core, successful forward-thinking organizations realize and appreciate the positive impact of a well-orchestrated customer experience on their revenue and profitability objectives. While these companies are attempting to allocate greater resources to build internal customer-facing capacity in areas including demand generation and conversion, account management, and customer success management, they are often encumbered by pre-existing organizational dynamics, departmental silos, and corporate inertia. We believe more companies will increasingly seek to partner with differentiated BPaaS providers like ServiceSource who can help them to more rapidly scale their customer experience initiatives with a value-driven and outcomes-based business case. Our clients choose us to help them drive greater customer engagement, trust, and loyalty given our integrated solution suite, demonstrable track record, proven process improvement methodology, global scale and infrastructure, and data expertise and insights.

Our Strategy and Solutions

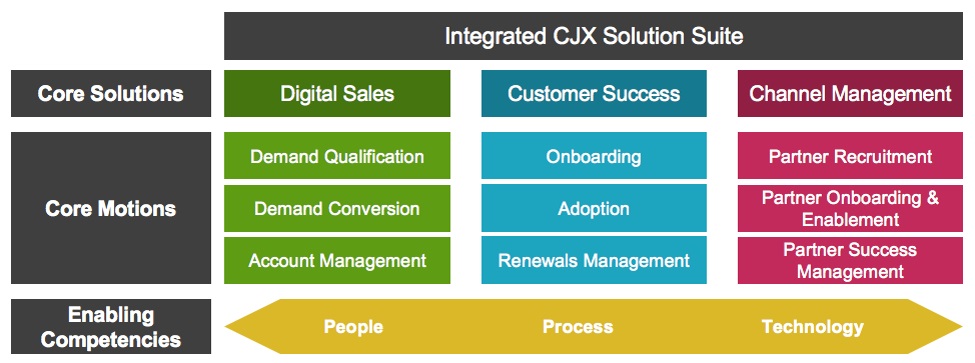

Our strategy is to drive client success by bringing the world’s greatest brands closer to their customers through people-powered, digitally-enabled solutions and data-driven insights. We are pioneers in the CJXTM market and believe our solution scope, process expertise and global operating scale position us as a category leader. Our unified CJXTM solution suite spans the pre- and post-sale B2B customer journey and is deployed through a holistic model that enables our clients to more efficiently and effectively identify, land, adopt, expand and renew their customers and end-users.

The ServiceSource CJXTM solution suite has been built on three primary solution pillars, encompassing digital sales, customer success, and channel management, all underpinned by enabling competencies centered around our highly trained people, proprietary processes, and best-in-class technologies. Depending on our clients’ needs, we can provide our solutions and motions on a fully integrated basis or we can design and deploy them on a discrete, á la carte basis to address our clients’ unique requirements.

2

Digital sales. Through our digital sales solution, we help our clients accelerate their acquisition and expansion efforts across both net-new and installed-base customer accounts. Our core motions of demand qualification, demand conversion, and account management are designed to drive higher quality leads, improved pipeline hygiene, greater marketing and sales funnel velocity, better sales conversion rates, higher net expansion rates, and increased consumption for our clients’ products and services.

•Demand qualification. We serve as a seamless extension to our clients’ advertising, marketing, and digital demand generation activities. Through proactive customer interaction and leveraged with our data analytics expertise, our business development reps digitally engage with marketing-generated leads to evaluate and score their budget, authority, need, and timing to progress them through the funnel into sales-qualified and sales-accepted leads.

•Demand conversion. We serve as a high velocity augmentation to our clients’ inside sales teams, allowing for enhanced coverage and increased conversion of their sales pipeline. Our sales development reps are extensively trained on our clients’ products, services, and features, and are experts at value- and persona-based selling. Through omnichannel media - including voice, chat, email, video, and social - our teams nurture leads, educate prospects, and conduct sales demos to convert qualified opportunities into confirmed orders and closed bookings for our clients.

•Account management. We serve as a natural complement to our clients’ installed-based account management sales motions. Our highly-skilled digital sales professionals develop, formulate, and implement account-based sales plans to identify and execute expansion selling opportunities, driving high margin incremental revenue for our clients through higher cloud consumption levels, upsell and cross-sell rates, multi-year conversions, and service and support attach rates.

Customer success. Through our customer success solution, we are an integrated component of our clients’ customer experience strategies and engagement efforts. Our core motions of onboarding, adoption, and renewals management are uniquely tailored and customized to improve the satisfaction, referenceability, loyalty, retention and lifetime value of our clients’ customers.

•Onboarding. Our onboarding experts engage and communicate with our clients’ new customers to ensure they are positioned for success from the first day of their relationship. We confirm subscriptions were successfully activated, downloads were successfully installed, assets and entitlements were successfully provisioned, and payments and credits were successfully applied. Where required, we further triage and support the coordination of our clients’ technical support and professional services resources to drive higher initial customer satisfaction and issue resolution outcomes.

•Adoption. Our adoption specialists are thoroughly trained and well-versed in the full range of features and functionality of our clients’ products, services and solutions. Leveraging telemetry from a variety of data feeds complemented with proactive real-time customer interaction, we ensure that our clients’ customers are appropriately educated, informed and empowered on how they can best achieve faster speed-to-value and return-on-investment for their subscription or purchase.

•Renewals management. Our renewals representatives are equipped with our industry-leading high-performance sales methodology and complemented by best-in-class technology and processes to manage revenue that may be at risk of loss for our clients. Our systems and global teams cleanse, validate, enhance and supplement our clients’ CRM and ERP data in order to proactively configure, price, quote and sell customer contracts that are nearing expiration or cancellation. Through extensive integration with our clients’ internal systems, teams and processes, we deliver performance outcomes that allow our clients to recognize lower customer churn and attrition, enhanced contract renewal rates, and higher revenue retention metrics.

Channel management. Through our channel management solution, we support the full lifecycle management of our clients’ indirect channels and routes to market. Our core motions of partner recruitment, partner onboarding and enablement, and partner success management are designed to increase partner mindshare, productivity, and sales of our clients’ products and services across both one-tier and two-tier distribution channel models.

•Partner recruitment. Our partner recruitment specialists are dedicated to identifying, vetting, and recruiting new distributors, value-added resellers, resellers, system integrators, managed service providers, agents and related third parties to join our clients’ channel partner programs. Through intensive research and proactive outreach, we ensure that our clients have an opportunity to expand their partner organizations with firms that are best positioned to more effectively market, sell and support our clients’ offerings in their respective regions and territories.

•Partner onboarding and enablement. Our partner onboarding specialists are thoroughly trained in the program design, tiering levels and criteria, and incentives available to partners through our clients’ channel programs. Through early engagement, intervention, and training, we promote greater program awareness, understanding, and focus for new partners, equipping them to achieve better early outcomes with our clients.

3

•Partner success management. Our partner success managers support our clients’ partners in developing and formulating quarterly and annual performance objectives, analyzing and forecasting sales and renewals pipelines, and identifying and resolving barriers to their success. Through ongoing engagement and interaction with our clients’ indirect partners, we proactively manage the relationships to ensure higher levels of success for our clients, the partners, and their mutual customers.

Our CJXTM solution suite is provided to our clients primarily through a unique outcomes-based, pay-for-performance model that ensures optimal alignment to their business growth priorities, return-on-investment mandates and customer experience objectives. Through this model, our clients pay us commissions that are either flat-rate or variable based on the bookings and/or revenue we generate on their behalf. For engagements where other pricing options are more appropriate, including our professional services, sales enablement and data management services, our clients pay us through either fixed-fee or full-time employee-based pricing models. Oftentimes our client contracts incorporate multiple pricing models to most appropriately balance our assessment of the data quality, operational complexity and risk-reward profile of the engagement. For the year ended December 31, 2020, 73% of our revenue was derived from pay-for-performance pricing arrangements and 27% was derived from fixed-fee or full-time employee-based pricing arrangements.

Our relationship with our clients begins in the pre-sales process and continues through the lifecycle of our engagement:

•Sales performance analysis. We typically begin engagements with our prospective clients by conducting a SPA. Through our SPA process, we conduct in-depth executive interviews and data analysis to understand a client’s unique challenges and desired business outcomes, evaluate and benchmark its performance against those outcomes, analyze opportunities for improvement using proprietary analytical models, and deliver expertise and recommendations to drive an enhanced customer experience, improved operational KPIs, and targeted financial gains.

•Business case, pricing and contract structuring. We use our reservoir of data, benchmarks, and best practices to estimate the critical components of the business case, to calculate our ability to improve our clients’ performance based on our extensive track record of execution for similar engagements, to scope and design an optimal delivery model, and to derive an appropriate value-based pricing structure and contractual arrangement.

•Data integration, implementation and launch. Once we have entered into a contract with a client, we deploy our professional services to rapidly integrate our tools and platforms with our clients’ systems, while our data and ops services teams ensure that high velocity data feeds are appropriately configured, mapped, loaded, enabled, and enhanced. Our talent acquisition teams launch a highly selective recruiting and onboarding process, while our learning and development teams build and deliver a robust training curriculum and certification program.

•Performance and execution. Following the implementation and ramp of an engagement, we leverage our reporting platform, data reservoir, and performance optimization tools to continuously monitor, measure, analyze, benchmark, and enhance the performance of our teams to ensure we are positioned to deliver against the business case and exceed our clients’ expectations.

•Client benchmarking and continuous improvement. Our extensive platform and the accumulation of more than 20 years of experience serve as the foundation for benchmarking our clients’ performance against internal parity rates, industry peers, and previous performance periods. We generally conduct monthly and quarterly business review meetings and host frequent executive steering reviews with our clients to assess our results, identify potential process gaps, determine opportunities for continuous improvement, and make recommendations that we believe will allow our clients and us to achieve higher levels of performance and efficiencies.

Markets We Serve

We target our solutions exclusively to B2B technology companies and focus on chosen market segments where we have deep domain expertise, proven competencies and best practices, robust executive relationships, and the ability to leverage existing client references and advocacy.

•Cloud and SaaS. In this segment, we serve companies who provide their solutions via public, private, or hybrid cloud delivery models, including SaaS, PaaS, and IaaS vendors. Within this market, customers and end-users typically purchase from our clients through a recurring subscription or a consumption-based utility billing model. IDC, a market research firm, estimates the total global market for cloud software was approximately $205 billion in 2020 with a forecasted 16% compound annual growth rate through 2024.

•Software. Our clients in this segment include companies who primarily provide their software in an on premise environment, where our clients’ customers and end-users typically pay for a defined number of licenses or subscribers, as well as related software support, maintenance and service contracts. We have developed extensive expertise in a variety of software sub-sectors, supporting vendors of application and system software, collaboration software, CRM software, cyber-security software, open source operating system software, and virtualization software, among others.

4

IDC estimates the total global market for software license and maintenance was approximately $300 billion in 2020, while the software subscription market was approximately $260 billion in 2020 with a forecasted 17% compound annual growth rate through 2024.

•Hardware. In this segment, we serve companies who provide IT hardware and related assets, including data center systems (servers, storage, gateways, and arrays), networking and communications equipment (switches, routers, access points, and appliances), and computing equipment and peripherals (workstations, PCs, thin-clients, and imaging devices), among others. Within this segment, our services are primarily directed at selling, renewing, and extending hardware maintenance and support contracts on our clients’ behalf. IDC estimates the total global market for hardware maintenance and support was approximately $64 billion in 2020 with a forecasted 2% compound annual growth rate through 2024.

•Medical device and diagnostic equipment. Our clients in this segment include companies who provide products, software and services to the healthcare and medical field, including vendors of radiology and diagnostic imaging equipment, surgical and laboratory instruments, and healthcare IT software, among others. Fortune Business Insights, a market research firm, estimates the total global medical device market was approximately $432 billion in 2020 with a forecasted 5% compound annual growth rate through 2028.

•Industrial IoT. In this segment, we serve companies who provide hardware, sensors, software and related services to monitor and automate smart and connected devices for manufacturing environments, process control applications, and energy and utility customers, among others. Grand View Research, a market research firm, estimates the total global market for industrial IoT applications was approximately $215 billion 2020 with a forecasted 35% compound annual growth rate through 2025.

Our Clients

We seek to build long-term, durable relationships with leading companies and high-growth innovators within each of our target markets, where our strategy, solutions, and capabilities provide a compelling client value proposition and opportunity for us to drive enduring client success and trusted business outcomes. We typically enter into multi-year contracts with our clients with average terms ranging from two to four years. Our client contracts are generally comprised of a master services agreement, which is a framework agreement that defines broad governing terms, supplemented by one or multiple order forms or statements of work that outline detailed terms, conditions, pricing, description of services and definition of scope. While most of our contracts may be terminated for convenience with relatively short notice, often subject to the payment of an early termination fee by the client, our top 10 client relationships range in duration from 8 to 14 years, with an average tenure of approximately 11 years.

During the year ended December 31, 2020, our top ten clients each generated more than $4.0 million in revenue and represented a combined 78% of our total net revenue, and four clients each represented over 10% of our revenue during this period. A relatively small number of clients may continue to account for a significant portion of our revenue for the foreseeable future. The loss of revenue from any of our significant clients for any reason may cause a significant decrease in our revenue.

Human Capital

We believe our people are our greatest asset and central to the success of ServiceSource and our clients. Through our core values of trust, caring, collaboration, and dedication, we direct our efforts and invest extensive resources to ensure we attract, hire, develop, incentivize, promote, and retain a world-class workforce. We are committed to building a culture that inspires success for our people and fostering a workplace environment that promotes trust, diversity, and inclusion while providing multiple avenues for continuous personal and professional development.

As of December 31, 2020, we had approximately 2,800 employees worldwide, of which nearly all were full-time, with 70% located outside of the U.S. Our employees are not covered by collective bargaining agreements.

Employee health and well-being. We believe a loyal and productive workforce requires a holistic approach to caring for the whole self. We provide a variety of programs and benefits to support the physical, mental, emotional, and spiritual health and well-being of our employees.

We are committed to the health and safety of our employees. To keep our employees safe during the COVID-19 pandemic, we created a dedicated crisis team to proactively implement business continuity plans and quickly transitioned to a 100% work-from-home model. As a result of this successful work-from-home implementation, we have shifted to a virtual-first operating model whereby our employees will continue to primarily work from their home offices and our facilities will be used for collaboration, innovation, and connection. Additionally, this model includes virtual sourcing, hiring, and onboarding for new employees as well as a process for driving performance and culture in a virtual environment.

Inclusion and diversity. We believe high-performing organizations are defined by policies and practices that encourage and celebrate an inclusive and diverse workforce. We have adopted metrics that measure the racial, ethnic, and gender diversity of

5

our organization and practices to ensure our organization is representative of the communities we serve. We are committed to equal pay for equal work, and continually monitor and analyze our compensation programs for equality.

In 2020, we further advanced our gender equality initiative with women representing half of our total employee base and more than one-third of our leadership ranks.

Benefits. We offer a complete set of benefits for our employees, including competitive base salaries, annual cash bonuses and an equity incentive program, as well as comprehensive health benefits, retirement plans, and a generous time off policy. For our U.S.-based employees, we offer 12 weeks of paid parental (maternal and paternal) leave, providing important support for our employees as they strive to care for, bond with and welcome new family members and integrate family life with work life. In addition, every employee receives a day of birthday time off, to enable that employee to celebrate on a day during the month of their birth.

Community engagement and involvement. We are active and involved members in the communities in which our employees live and work, and we promote a culture of volunteering and giving back. Every employee globally receives eight hours of paid volunteer time off annually, which encourages our employees to serve the communities in which we live and work. Through our paid volunteer time off program, our employees collectively volunteered more than 5,300 hours supporting a variety of charitable causes and organizations in their communities during 2020.

Training, development, and performance. In July 2020, we launched CJXTM University, a world-class learning and development platform designed to help employees grow and develop in their careers. Since launch, our employees have logged more than 18,000 training hours. Additionally, we hold bi-annual unrated performance reviews, designed to encourage employees to have conversations with their managers relating to their areas of strength and growth opportunities and allowing for a plan for future career progression and development.

Competition and Our Competitive Strengths

The market for our BPaaS services and CJXTM solution suite is dynamic and evolving. Historically, B2B companies have managed their customer acquisition, engagement, expansion, and retention efforts internally and have relied upon a variety of third-party technologies and tools - including enterprise resource planning software, customer relationship management software, customer success management software, business intelligence software, channel management software, customer experience management software, and sales enablement software - from vendors such as Adobe, Gainsight, Medallia, Oracle, SAP, salesforce.com, and XANT, to enable their in-house teams and workflows. Some companies have made further investments in this area using firms such as Accenture, Deloitte Digital and McKinsey & Company for customer experience design and digital transformation consulting services for their go-to-market organizations. These internally developed solutions represent the primary alternative to our integrated approach of combining people, processes and technology to provide a purpose-built, end-to-end optimized solution.

We believe we are the only company of scale exclusively focused on serving the unique requirements of B2B technology companies with a solution suite that addresses the entirety of the customer journey experience continuum. Within the broader BPaaS market, at times we may compete with larger, more diversified and less-focused companies such as Cognizant, Convergys, Genpact, TTEC, and Webhelp, as well as smaller companies offering more narrow point solutions such as MarketStar and N3 Results.

We believe our principal competitive strengths and differentiators include our:

•20+ year track record of innovation and market leadership;

•B2B technology industry domain expertise;

•ability to drive client success and value;

•scope and completeness of our solution;

•robust global delivery footprint and infrastructure;

•extensive geographic and language coverage model;

•outcomes-based, pay-for-performance pricing;

•data-driven insights, best practices and benchmarks;

•speed and agility;

•experience and quality of our leadership team;

•reputation and referenceable client base; and

•size and financial stability of our operations.

6

Although we currently have few direct competitors that offer integrated solutions at our scale, we expect competition and competitive pressure, from both new and existing competitors, to increase in the future.

Our Intellectual Property

We believe our ability to innovate is a key driver of value for our clients and our business. The solutions we provide to our clients often include a variety of proprietary tools, technologies, processes, methodologies, and expertise which comprise our intellectual property. In addition, our intellectual property includes patents, trademarks, and copyrights, as well as various trade secrets, which we believe provide us with a competitive advantage in the marketplace. We protect our intellectual property by leveraging U.S. and foreign patent, trademark, copyright, and trade secret laws, in addition to entering into non-competition, confidentiality, non-disclosure, and related intellectual property protection agreements with our clients, employees, contractors and suppliers.

Partnerships and Alliances

We routinely enter into partnerships and alliances with companies that can enhance our solutions, differentiate our capabilities, advance our technologies and tools, and complement our sales and marketing activities. These relationships include strategic go-to-market alliances, joint-selling agreements, “white-labeled” technology integrations and business transformation and consulting partners.

Additional Information

Our predecessor company was founded in 1999 and we were formed as a Delaware limited liability company in 2002 and converted to a Delaware corporation in 2011. Additional information about us is available on our website at http://www.servicesource.com. The information on our website is not incorporated into this annual report by reference and is not a part of this Form 10-K. We make available free of charge on our website our annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K and any amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, as soon as reasonably practicable after those reports are electronically filed with, or furnished to, the SEC. In addition, the SEC maintains a website that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC at http://www.sec.gov. From time to time, we may use our website as a channel of distribution of material information about our company. Financial and other important information regarding our business is routinely posted on and accessible at http://ir.servicesource.com.

| ITEM 1A. | RISK FACTORS | ||||

Investing in our common stock involves risk. Our operations and financial results are subject to various risks and uncertainties, including those described below, that could adversely affect our business, financial condition, results of operations, cash flows and the trading price of our common stock. You should carefully consider the risks described below and the other information in this Annual Report on Form 10-K.

Risks Related to Our Business and Industry

Our business and growth depend substantially on clients renewing their agreements with us and expanding their use of our solution for additional available markets. Any decline in our client renewals, termination of ongoing engagements or failure to expand their relationships with us could harm our future operating results.

In order for us to improve our operating results and grow, it is important that our clients renew their agreements with us when the initial contract term expires and that we expand our client relationships to add new market opportunities and the related revenue management opportunity. Our clients may elect not to renew their contracts with us after the expiration of their initial term, which typically vary between one and two years, or may elect to otherwise terminate our services, and we cannot assure you that our clients will renew service contracts with us at the same or higher level of service, if at all, or provide us with the opportunity to manage additional revenue management opportunities. Although our renewal rates have been historically higher than those achieved by our clients prior to their use of our solution, some clients have still elected not to renew their agreements with us. Our clients’ renewal rates may decline or fluctuate as a result of a number of factors, many of which are beyond our control, including their satisfaction or dissatisfaction with our solution and results, our pricing, mergers and acquisitions affecting our clients or their end customers, the effects of economic conditions or reductions in our clients’ or their end customers’ spending levels. If our clients do not renew their agreements with us, renew on less favorable terms, terminate their services with us or fail to contract with us for additional services, our revenue may decline and our operating results may be adversely affected.

Our revenue will decline if there is a decrease in the overall demand for our clients’ products and services.

A majority of our revenue is based on a pay-for-performance model, which means that we are paid a commission based on the service contracts we sell on behalf of our clients. If a client’s products or services fail to appeal to its end customers, our revenue will decline for our work with that client. In addition, if end customer demand decreases for other reasons, such as

7

negative news regarding our clients or their products, unfavorable economic conditions, shifts in strategy by our clients away from promoting the service contracts we sell in favor of selling their other products or services to their end customers, or if end customers experience financial constraints and terminate or fail to renew the service contracts we sell, we may experience a decrease in our revenue as the demand for our clients’ service contracts declines. Similarly, if our clients come under economic pressure, they may be more likely to terminate their contracts with us or seek to restructure those contracts.

The ongoing COVID-19 pandemic may have material adverse effect on our business, financial position, results of operations and/or cash flows.

We face various risks related to health epidemics, pandemics and similar outbreaks, including the global outbreak of COVID-19. The continued spread of COVID-19 has led to disruption and volatility in the global capital markets, which increases the cost of capital and adversely impacts access to capital. If significant portions of our workforce are unable to work effectively, including because of illness, lack of available internet capacity, or other restrictions in connection with the COVID-19 pandemic, our operations may be impacted.

If our performance falls short of our estimates, our client relationships will be at risk, our revenue will suffer and our ability to grow could be harmed.

A majority of our business depends on driving new or renewal revenue for our clients, and we then receive a commission on the new or renewal revenue that we generate on our clients’ behalf. In some cases, our commission rates vary depending on our performance —for example, if we overperform compared to our estimates then we may receive a higher commission. In addition, our clients rely on us to accurately forecast our performance, especially because we drive revenue on their behalf. These forecasts are based upon the data our clients provide to us, and are subject to significant business, economic and competitive uncertainties and are based on assumptions and estimates that may not prove to be accurate. In addition, these forecasted expectations are based upon historical trends and data that may not be true in subsequent periods. If our performance for a particular client is lower than anticipated, then our revenue for that client will also be lower than projected. If our performance falls short of expectations across a broad range of clients, or if our performance falls below expectations for a particularly large client, then the impact on our revenue and our overall business will be significant. In the event our performance is lower than expected for a given client, our margins will suffer because we will have already incurred a certain level of costs in both personnel and infrastructure to support the engagement. This risk is compounded by the fact that many of our client relationships can be terminated by the client if we fail to meet certain specified sales targets, including bookings rates, over a sustained period of time. If our performance falls to a level at which our revenue and client contracts are at risk, then our financial performance will decline and we may have difficulty attracting and retaining new clients.

We depend on a limited number of clients for a significant portion of our revenue, and the loss of business from one or more of our key clients could adversely affect our results of operations.

Our top ten clients accounted for 78% of our revenue for the year ended December 31, 2020, and four clients each represented over 10% of our revenue during this period. A relatively small number of clients may continue to account for a significant portion of our revenue for the foreseeable future. The loss of revenue from any of our significant clients for any reason, including the failure to renew our contracts, termination of some or all of our services, a change of relationship with any of our key clients, or the acquisition of one of our significant clients, may cause a significant decrease in our revenue.

If we cannot efficiently implement our offering for clients, we may be delayed in generating revenue, fail to generate revenue and/or incur significant costs.

In general, our client engagements are complex and we must undertake lengthy and significant work to implement our offerings. We generally incur sales and marketing expenses related to the commissions owed to our sales representatives and make upfront investments in technology and personnel to support the engagements one to three months before we begin selling end customer contracts on behalf of our clients. Each client’s situation may be different, and unanticipated difficulties and delays may arise as a result of our failure, or that of our client, to meet implementation responsibilities. If the client implementation process is not executed successfully or if execution is delayed, we could incur significant costs without generating revenue, and our relationships with some of our clients and operating results may be adversely impacted.

Because competition for our target employees is intense, we may be unable to attract and retain the highly skilled employees we need to support our planned growth.

To continue to execute on our growth plan, we must attract and retain highly qualified sales representatives, engineers and other key employees in the international markets in which we have operations. Competition for these personnel is intense, especially for highly educated, qualified sales representatives with multiple language skills. We have from time to time in the past experienced, and we expect to continue to experience in the future, difficulty in hiring and retaining highly skilled key employees with appropriate qualifications. We may incur significant costs to attract and retain highly skilled key employees, and we may lose new employees to our competitors or other companies before we realize the benefit of our investment in

8

recruiting and training them. If we fail to attract new sales representatives, engineers and other key employees, or fail to retain and motivate our most successful employees, our business and future growth prospects could be harmed.

If our security measures are breached or fail, resulting in unauthorized access to client data, our solution may be perceived as insecure, the attractiveness of our solution to current or potential clients may be reduced and we may incur significant liabilities.

Our solution involves the storage and transmission of the proprietary information and protected data that we receive from our clients. We rely on proprietary and commercially available systems, software, tools and monitoring, as well as other processes, to provide security for processing, transmission and storage of such information. Despite the implementation of these security measures, our systems may still be vulnerable. If our security measures are breached or fail as a result of third-party action, employee negligence, error, malfeasance or otherwise, unauthorized access to client or end customer data may occur. Techniques used to obtain unauthorized access or to sabotage systems change frequently and generally are not recognized until launched against a target, and we may be unable to anticipate these techniques or implement adequate protective measures. Our security measures may not be effective in preventing these types of activities, and the security measures of our third-party data centers and service providers may not be adequate.

Our client contracts generally provide that we will indemnify our clients for data privacy breaches caused by our acts or omissions. If a data privacy breach occurs, we could face contractual damages, damages and fees arising from our indemnification obligations, penalties for violation of applicable laws or regulations, possible lawsuits by affected individuals and significant remediation costs and efforts to prevent future occurrences. Insurance may not be able to cover these costs in full, in particular if the damages are large. In addition, whether there is an actual or a perceived breach of our security, the market perception of the effectiveness of our security measures could be harmed significantly and we could lose current or potential clients.

We may be liable to our clients or third parties if we make errors in providing our solution or fail to properly safeguard our clients' confidential information.

The solution we offer is complex, and we make errors from time to time. These may include human errors made in the course of managing the sales process for our clients as we interact with their end customers, or errors arising from our technology solution as it interacts with our clients’ systems and the disparate data contained on such systems. For example, our employees enter codes to classify their interactions with our clients’ end customers, and incorrect code entry could result in our clients' end customer not receiving the service or solution they requested, which in turn could lead to customer dissatisfaction or termination causing our client relationships to suffer and our revenue and our clients' revenue to decline. The costs incurred in correcting any material errors may be substantial. Any claims based on errors could subject us to exposure for damages, significant legal defense costs, adverse publicity and reputational harm, regardless of the merits or eventual outcome of such claims.

We conduct operations in a number of countries and are subject to risks of international operations.

Outside of the U.S., we conduct operations in Bulgaria, Ireland, Japan, Malaysia, the Philippines, Singapore and the United Kingdom. In 2020, approximately 43% of our revenue was related to operations located outside of the U.S. In addition, 70% of our employees are located in offices outside of the U.S. We expect to continue our international growth, with international revenue accounting for an increased portion of total revenue in the future. Our international operations involve risks that differ from or are in addition to those faced by our U.S. operations. These risks include different employment laws and rules and related social and cultural factors; different regulatory and compliance requirements, including in the areas of privacy and data protection, anti-bribery and anti-corruption, trade sanctions, marketing and sales and other barriers to conducting business; cultural and language differences; diverse or less stable political, operating and economic environments and market fluctuations; and civil disturbances or other catastrophic events that affect business activity (including the ongoing coronavirus outbreak). If we are not able to efficiently adapt to or effectively manage our business in markets outside of the U.S., our business prospects and operating results could be materially and adversely affected. Although we have business continuity plans in place for our operations, an extended period of civil unrest that halts or significantly impedes operations could have a material adverse effect on our business.

Laws or public perception may eliminate or restrict our ability to use revenue delivery centers not located in the U.S., which could have a material adverse impact on our business and results of operations.

The issue of companies outsourcing services to organizations operating in other countries is a politically sensitive topic and has been under heightened scrutiny in many countries, including the U.S. We provide our outsourced customer success and revenue growth solutions in several non-U.S. locations, including the Philippines and Malaysia, and our growth strategy includes increasing reliance on these “offshore” revenue delivery centers. Many organizations and public figures in the U.S. have publicly expressed concern about a perceived association between offshore outsourcing providers and the loss of jobs in the U.S., and the topic of offshore outsourcing has recently received a great deal of negative attention from the U.S. executive

9

branch. Because of negative public perception about offshore outsourcing, measures aimed at limiting or restricting offshore outsourcing by U.S. companies are periodically considered in the U.S. Congress. Current or prospective clients may elect to perform such services themselves or may be discouraged from transferring these services from onshore to offshore providers to avoid negative perceptions that may be associated with using an offshore provider. Any slowdown or reversal of existing industry trends towards offshore outsourcing, including due to the enactment of any legislation restricting offshore outsourcing by U.S. companies, would harm our ability to provide certain of our services to our clients at a competitive and cost-effective price point and would have a material adverse effect on our business and results of operations.

Changes in the legal and regulatory environment that affect our operations, including laws and regulations relating to the handling of personal data, data security and cross-border data flows, may impede the adoption of our services, disrupt our business or result in increased costs, legal claims, or fines against us.

We are subject to a wide variety of laws and regulations in the U.S. and the other jurisdictions in which we operate, and changes in the level of government regulation of our business have the potential to materially alter our business practices with resultant increases in costs and decreases in profitability. Depending on the jurisdiction, those changes may come about through new legislation, the issuance of new regulations or changes in the interpretation of existing laws and regulations by a court, regulatory body or governmental official. Sometimes those changes have both prospective and retroactive effect, which is particularly true when a change is made through reinterpretation of laws or regulations that have been in effect for some time.

Our international operations and global client base relies increasingly on the movement of data across national boundaries. Legal requirements relating to the collection, storage, handling and transfer of personal data continue to evolve, and additional regulation in those areas, some of it potentially difficult and costly for us to accommodate, is frequently proposed and occasionally adopted. Laws in many countries and jurisdictions, particularly in the European Union and Canada, govern the requirements related to how we store, transfer or otherwise process the private data provided to us by our clients. For example, in the European Union, the GDPR imposes substantial requirements regarding the handling of personal data. The GDPR, as well as other data privacy, cyber security and data localization laws and regulations, has changed in recent years and is likely to continue to evolve in the future. Although we have implemented measures designed to comply with the laws and regulations applicable to our business, our ongoing efforts to comply with the GDPR and other changes in laws and regulations (such as the California Consumer Privacy Act that became effective in January 2020) may entail substantial expenses and divert resources from other initiatives. These changes have in the past increased, and may continue to increase, our cost of providing our services, could limit us from offering solutions in certain jurisdictions, could adversely affect our sales cycles, and could impact our new technology innovation. In addition, the centralized nature of our information systems at the data and operations centers that we use requires the routine flow of data relating to our clients and their respective end customers across national borders, both with respect to the jurisdictions within which we have operations and the jurisdictions in which we provide services to our clients. If this flow of data becomes subject to new or different restrictions, our ability to serve our clients and their respective end customers could be seriously impaired for an extended period of time.

We also have entered into various model contracts and related contractual provisions to enable these data flows. For any jurisdictions in which these measures are not recognized or otherwise not compliant with the laws of the countries in which we process data, or where more stringent data privacy laws are enacted irrespective of international treaty arrangements or other existing compliance mechanisms, we could face increased compliance expenses and face penalties for violating such laws or be excluded from those markets altogether, in which case our operations could be materially damaged.

Consolidation in the technology sector could harm our business in the event that our clients are acquired and their contracts are canceled.

Consolidation among technology companies in our target market has been robust in recent years, and this trend poses a risk for us. Acquisitions of our clients could lead to cancellation of our contracts with those end customers by the acquiring companies and could reduce the number of our existing and potential clients. If mergers and acquisitions take place within our customer base, some of the acquiring companies may terminate, renegotiate and/or elect not to renew our contracts with the companies they acquire, which would reduce our revenue. In addition, acquisitions in our customer base may adversely impact our revenue even if the contract is not terminated. The sales we make on behalf of our customers are processed through our customers’ billing and quoting platforms. If our customers are acquired or merge with another company and as a result, their billing platforms or the procedures for processing closed sales are changed or slowed down, we will be unable to close our sales and our closure rate will fall, and therefore our revenue and our ability to keep our customers, could suffer.

We enter into long-term, commission-based contracts with our clients, and our failure to correctly price these contracts may negatively affect our profitability.

We enter into long-term contracts with our clients that are priced based on multiple factors determined in large part by the performance analysis we conduct for our clients. These factors include opportunity size, anticipated booking rates and expected commission rates at various levels of sales performance. Some of these factors require forward-looking assumptions that may prove incorrect. If our assumptions are inaccurate, or if we otherwise fail to correctly price our client contracts, particularly

10

those with lengthy contract terms, then our revenue, profitability and overall business operations may suffer. Further, if we fail to anticipate any unexpected increase in our cost of providing services, including the costs for employees, office space or technology, we could be exposed to risks associated with cost overruns related to our required performance under our contracts, which could have a negative effect on our margins and earnings.

A substantial portion of our business consists of supporting our clients’ channel partners in the sale of service contracts. If those channel partners become unreceptive to our solution, our business could be harmed.

Many of our clients, including some of our largest clients, sell service contracts through their channel partners and engage our solution to help those channel partners become more effective at selling service contract renewals. In this context, the ultimate buyers of the service contracts are end customers of those channel partners, who then receive the actual services from our clients. In the event our clients’ channel partners become unreceptive to our involvement in the renewals process, those channel partners could discourage our current or future clients from engaging our solution to support channel sales. This risk is compounded by the fact that large channel partners may have relationships with more than one of our clients or prospects, in which case the negative reaction of one or more of those large channel partners could impact multiple client relationships. Accordingly, with respect to those clients and prospective clients who sell service contracts through channel partners, any significant resistance to our solution by their channel partners could harm our ability to attract or retain clients, which would damage our overall business operations.

We face long sales cycles to secure new client contracts, making it difficult to predict the timing of specific new client relationships.

We face a variable selling cycle to secure new client agreements, typically spanning a number of months and requiring our effort to obtain and analyze our prospect’s business through the service performance analysis, for which we are not paid. We recently have also experienced a lengthening of our sales cycles reflecting the hiring of a number of new sales personnel in the past eighteen months who are new to selling our solution as well as slower decision making by a few end customers as well as other end customers considering renewals of large, multi-year contracts. This has adversely affected the conversion rates of new client contracts. Moreover, even if we succeed in developing a relationship with a potential new client, the scope of the potential subscription or service revenue management engagement frequently changes over the course of the business discussions and, for a variety of reasons, our sales discussions may fail to result in new client acquisitions. Consequently, we have only a limited ability to predict the timing and size of specific new client relationships.

The length of time it takes our newly hired sales and customer success representatives to become productive could adversely impact our success rate, the execution of our overall business plan and our costs.

It can take twelve months or longer before our internal sales and customer success representatives are fully trained and productive in selling our solution to prospective clients. This long ramp period presents a number of operational challenges as the cost of recruiting, hiring and carrying new sales and customer success representatives cannot be offset by the revenue such new sales representatives produce until after they complete their long ramp periods. Given the length of the ramp period, we often cannot determine if a sales and customer success representative will succeed until he or she has been employed for a year or more. If we cannot reliably develop our sales and customer success representatives to a productive level, or if we lose productive representatives in whom we have heavily invested, our future growth rates and revenue will suffer.

Our revenue and earnings are affected by foreign currency exchange rate fluctuations.

In 2020, approximately 43% of our revenue was generated outside of the U.S., as compared to 42% of our revenue in 2019. As a result of our continued focus on international markets, we expect that revenue derived from international sources will continue to represent a significant portion of our total revenue in the future.

A portion of the sales commissions earned from our international clients is paid in foreign currencies. As a result, fluctuations in the value of these foreign currencies may make our solution more expensive or cause resulting fluctuations in cost for international clients, which could harm our business. We currently do not undertake hedging activities to manage these currency fluctuations. Even if we were to implement hedging strategies to mitigate this risk, these strategies might not eliminate our exposure to foreign exchange rate fluctuations and would involve costs and risks of their own, such as ongoing management time and expense, external costs to implement the strategies and potential accounting implications. In addition, if the effective price of the contracts we sell to end customers were to increase as a result of fluctuations in the exchange rate of the relevant currencies, demand for such contracts could fall, which in turn would reduce our revenue.

The exit of the United Kingdom from the European Union could adversely affect our business.

In January 2020, the United Kingdom formally left the European Union, an action referred to as Brexit. Several political, legal, regulatory, and economic factors which are currently unknown will influence Brexit’s impact on our business. We have a revenue delivery center in Liverpool, United Kingdom, and Brexit has, and could continue to, create uncertainty in our employee base relating to immigration and other cross-border matters. Brexit could lead to economic and legal uncertainty,

11

including significant volatility in currency exchange rates, reduced customer demand for our services, and increasingly divergent laws and regulations as the United Kingdom determines which European Union laws to replace or replicate. In addition, Brexit could cause a shift or increase in data privacy regulations for data transfers between the United Kingdom and European Union. Any of these effects of Brexit, among others, could adversely affect our operations in the United Kingdom and our financial results.

Claims by others that we infringe or violate their intellectual property could force us to incur significant costs and require us to change the way we conduct our business.

Our services or solutions could infringe the intellectual property rights of others, impacting our ability to deploy our services or solutions with our clients. From time to time, we receive letters from other parties alleging, or inquiring about, possible breaches of their intellectual property rights. These claims could require us to cease activities, incur expensive licensing costs, or engage in costly litigation, each of which could adversely affect our business and results of operations.

In addition, we may incorporate open source software into our technology solution. The terms of many open source licenses have not been interpreted by U.S. or foreign courts, and there is a risk that such licenses could be construed in a manner that imposes unanticipated conditions or restrictions on our commercialization of any of our solutions that may include open source software. As a result, we will be required to analyze and monitor our use of open source software closely. As a result of the use of open source software, we could be required to seek licenses from third parties in order to develop such future products, re-engineer our products, discontinue sales of our solutions or release our software code under the terms of an open source license to the public. Given the nature of open source software, there is also a risk that third parties may assert copyright and other intellectual property infringement claims against us based on any use of such open source software. These claims could result in significant expense to us, which could harm our business.

Interruption of operations at our data centers and revenue delivery centers could have a materially adverse effect on our business.

If we experience a temporary or permanent interruption in our operations at one or more of our data or revenue delivery centers, through natural disaster, casualty, operating malfunction, cyberattack, sabotage or other causes, we may be unable to provide the services we are contractually obligated to deliver. Failure to provide contracted services could result in contractual damages or clients’ termination or renegotiation of their contracts. Although we maintain disaster recovery and business continuity plans and precautions designed to protect our company and our clients from events that could interrupt our delivery of services, there is no guarantee that such plans and precautions will be effective or that any interruption will not be prolonged. Any prolonged interruption in our ability to provide services to our clients for whom our plans and precautions fail to adequately protect us could have a material adverse effect on our business, results of operation and financial condition.

We are dependent on the continued participation and level of service of our third-party platform provider. Any failure or disruption in this service could materially and adversely affect our ability to manage our business effectively.

We rely on salesforce.com to provide the platform supporting many of our technologies and AWS to support a significant portion of our data storage. If salesforce.com or AWS stops supporting our technologies or if they fail to provide a platform that consistently and adequately supports our solution, including as a result of errors or failures in their systems or events beyond their control, or refuse to provide their platforms on terms acceptable to us or at all and we are not able to find suitable alternatives, our business may be materially and adversely affected.

We may be subject to state, local and foreign taxes that could harm our business.

We operate revenue delivery centers in multiple locations. Some of the jurisdictions in which we operate, such as Ireland, give us the benefit of either relatively low tax rates, tax holidays or government grants, in each case, that are dependent on how we operate or how many jobs we create and employees we retain. We plan on utilizing such tax incentives in the future, as opportunities are made available to us. Any failure on our part to operate in conformity with applicable requirements to remain qualified for any such tax incentives or grants may result in an increase in our taxes. In addition, jurisdictions may choose to increase rates at any time due to economic or other factors. Any such rate increases may harm our results of operations.

We may lose sales or incur significant costs should various tax jurisdictions impose taxes on either a broader range of services or services that we have performed in the past. We may be subject to audits of the taxing authorities in the jurisdictions where we do business that would require us to incur costs in responding to such audits. Imposition of such taxes on our services could result in substantial unplanned costs, would effectively increase the cost of such services to our clients and may adversely affect our ability to retain existing clients or to gain new clients in the areas in which such taxes are imposed.

We may incur material restructuring charges.

We continually evaluate ways to reduce our operating expenses and adapt to changing industry and market conditions through new restructuring opportunities, including more effective utilization of our assets, workforce and operating facilities. We have

12

recorded restructuring charges in the past and we may incur material restructuring charges in the future. The risk that we incur material restructuring charges may be heightened during economic downturns or with expanded global operations.

We have incurred indebtedness in connection with our business and may incur additional indebtedness in the future.

In July 2018, we entered into a $40.0 million Revolver that allows us to borrow against our domestic receivables as defined in the credit agreement. As of February 24, 2021, we had $15.0 million of borrowings under the Revolver through a one-month Eurodollar borrowing at an effective interest rate of 2.12% maturing at the end of February 2021. An additional $11.2 million was available for borrowing under the Revolver as of February 24, 2021. The Eurodollar borrowings may be extended upon maturity, converted into a base rate borrowing upon maturity or require an incremental payment if the Company's borrowing base decreases below the current amount outstanding during the term of the Eurodollar borrowing. We may incur additional indebtedness in connection with financing acquisitions, strategic transactions or for other purposes.

If we are unable to secure additional borrowing options in the future, it may have an adverse effect on our business.

The Revolver matures in July 2021 and we are subject to the risks normally associated with debt obligations, including the risk that we will be unable to refinance our indebtedness, or that the terms of such refinancing will not be as favorable as the terms of our indebtedness. If we are unable to generate sufficient cash flow or otherwise obtain funds necessary to make required payments or otherwise refinance any debt that we incur, our business could suffer.

Our financial condition and results of operations could suffer if there is an impairment of goodwill.

We are required to test goodwill annually or more frequently if certain circumstances change that would more-likely-than-not indicate the carrying value of the reporting unit may not be recoverable. As of December 31, 2020, our goodwill was $6.3 million. When the carrying value of a reporting unit exceeds its fair value, an impairment loss equal to the difference is recorded. This would result in incremental expenses for that period, which would reduce any earnings or increase any loss for the period in which the impairment was determined to have occurred. Declines in our level of revenues or declines in our operating margins, or sustained declines in our stock price, increase the risk that goodwill may become impaired in future periods. Our goodwill impairment analysis is sensitive to changes in key assumptions used in our analysis, such as expected future cash flows and our stock price. If the assumptions used in our analysis are not realized, it is possible that an impairment charge may need to be recorded in the future. We cannot accurately predict the amount and timing of any impairment of goodwill.

If we were to experience an ownership change, we could be limited in our ability to use NOLs arising prior to the ownership change to offset future taxable income. In addition, our ability to use NOLs to reduce future tax payments may be limited if our taxable income does not reach sufficient levels.

As of December 31, 2020, we had net operating losses of $316.7 million. If we were to experience an “ownership change,” as determined under Section 382 of the IRC, our ability to offset taxable income arising after the ownership change with net operating losses arising prior to the ownership change would be limited, possibly substantially. In addition, our ability to use our net operating losses is dependent on our ability to generate taxable income, and the net operating losses could expire before we generate sufficient taxable income to make use of our net operating losses.

General Risk Factors

Anti-takeover provisions contained in our certificate of incorporation and bylaws, as well as provisions of Delaware law, could impair a takeover attempt.

Our certificate of incorporation, bylaws and Delaware law contain provisions that could have the effect of rendering more difficult or discouraging an acquisition deemed undesirable by our board of directors. Our corporate governance documents include provisions:

•authorizing blank check preferred stock, which could be issued by our board of directors without stockholder approval, with voting, liquidation, dividend and other rights superior to our common stock;

•limiting the liability of, and providing indemnification to, our directors and officers;

•limiting the ability of our stockholders to call and bring business before special meetings and to take action by written consent in lieu of a meeting;

•requiring advance notice of stockholder proposals for business to be conducted at meetings of our stockholders and for nominations of candidates for election to our board of directors;

•controlling the procedures for the conduct and scheduling of stockholder meetings;

•providing the board of directors with the express power to postpone previously scheduled annual meetings and to cancel previously scheduled special meetings;

13

•limiting the determination of the number of directors on our board and the filling of vacancies or newly created seats on the board to our board of directors then in office; and

•providing that directors may be removed by stockholders only for cause.

These provisions, alone or together, could delay hostile takeovers and changes in control or changes in our management. As a Delaware corporation, we are also subject to provisions of Delaware law, including Section 203 of the Delaware General Corporation law, which limits the ability of stockholders owning in excess of 15% of our outstanding common stock to merge or combine with us.

Any provision of our certificate of incorporation, bylaws or Delaware law that has the effect of delaying or deterring a change in control could limit the opportunity for our stockholders to receive a premium for their shares of our common stock, and could also affect the price that some investors are willing to pay for our common stock.

If securities or industry analysts do not publish or cease publishing research or reports about us, our business or our market, or if they change their recommendations regarding our stock, our stock price and trading volume could decline.

The trading market for our common stock could depend in part on the research and reports that securities or industry analysts publish about us or our business, which in part depends on our market capitalization. If analysts downgrade our stock or publish inaccurate or unfavorable research about our business, our stock price could also likely decline. If analysts cease coverage of us, the trading price and trading volume of our stock could be negatively impacted. As of December 31, 2020, the Company is not aware of any active analyst coverage.

Because we currently do not intend to pay dividends, stockholders will benefit from an investment in our common stock only if it appreciates in value.