UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1

to

FORM

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

(Exact name of Registrant as specified in its charter) |

| 1311 |

| ||

(State or other jurisdiction of incorporation or organization) |

| (Primary Standard Industrial Classification code number) |

| (I.R.S. Employer Identification No.) |

Telephone: (

(Address, including zip code, and telephone number, including

area code, of Registrant’s principal executive offices)

James A. Doris

Chief Executive Officer

15915 Katy Freeway, Suite 450

Houston, Texas 77094

Telephone: (281) 404-4387

(Name, address, including zip code, and telephone number,

including area code, of agent for service)

Copies to: | |

| |

James B. Marshall Baker Botts L.L.P. 910 Louisiana Street Houston, Texas 77002 Telephone: (713) 229-1234 | Lance Brunson Brunson Chandler & Jones, PLLC Walker Center 175 S. Main Street, Suite 1410 Salt Lake City, Utah 84111 Telephone: (801) 303-5737 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If the securities being registered on this form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box: ☐

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier registration statement for the same offering. ☐

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | Accelerated filer | ☐ |

☒ | Smaller reporting company | ||

|

| Emerging growth company |

If an emerging growth company, indicate by check mark if the Registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer) ☐

Exchange Act Rule 14d-1(d) (Cross-Border Third-Party Tender Offer) ☐

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this joint proxy statement/prospectus is not complete and may be changed. A registration statement relating to the securities described in this joint proxy statement/prospectus has been filed with the U.S. Securities and Exchange Commission. These securities may not be issued until the registration statement filed with the U.S. Securities and Exchange Commission is effective. This joint proxy statement/prospectus does not constitute an offer to sell or the solicitation of offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

PRELIMINARY—SUBJECT TO COMPLETION—DATED MAY 23, 2023

JOINT LETTER TO STOCKHOLDERS OF CAMBER ENERGY, INC.

AND STOCKHOLDERS OF VIKING ENERGY GROUP, INC.

Dear Stockholders:

Camber Energy, Inc. (which we refer to as “Camber”) and Viking Energy Group, Inc. (which we refer to as “Viking”) have entered into an Agreement and Plan of Merger, dated as of February 15, 2021, as amended on April 18, 2023 (which, as it may be further amended from time to time, we refer to as the “Merger Agreement”), providing for the acquisition of Viking by Camber pursuant to a merger between Viking Merger Sub, Inc., a Nevada corporation and wholly owned subsidiary of Camber (“Merger Sub”) and Viking (which we refer to as the “Merger”) on the terms and subject to the conditions of the Merger Agreement, with Viking continuing as the surviving entity in the Merger and a wholly-owned subsidiary of Camber. We sometimes refer to Camber following the Merger and in its capacity as parent company of Viking as the “combined company.”

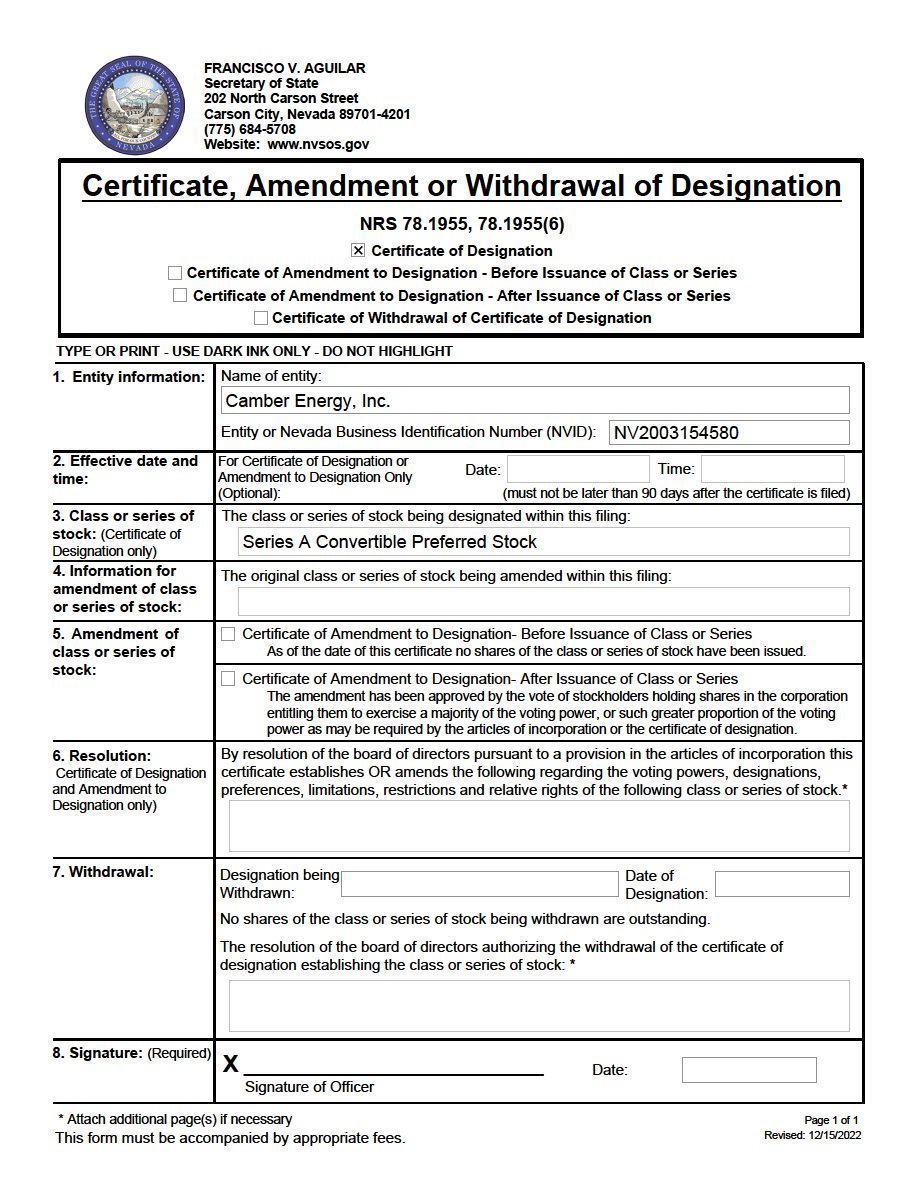

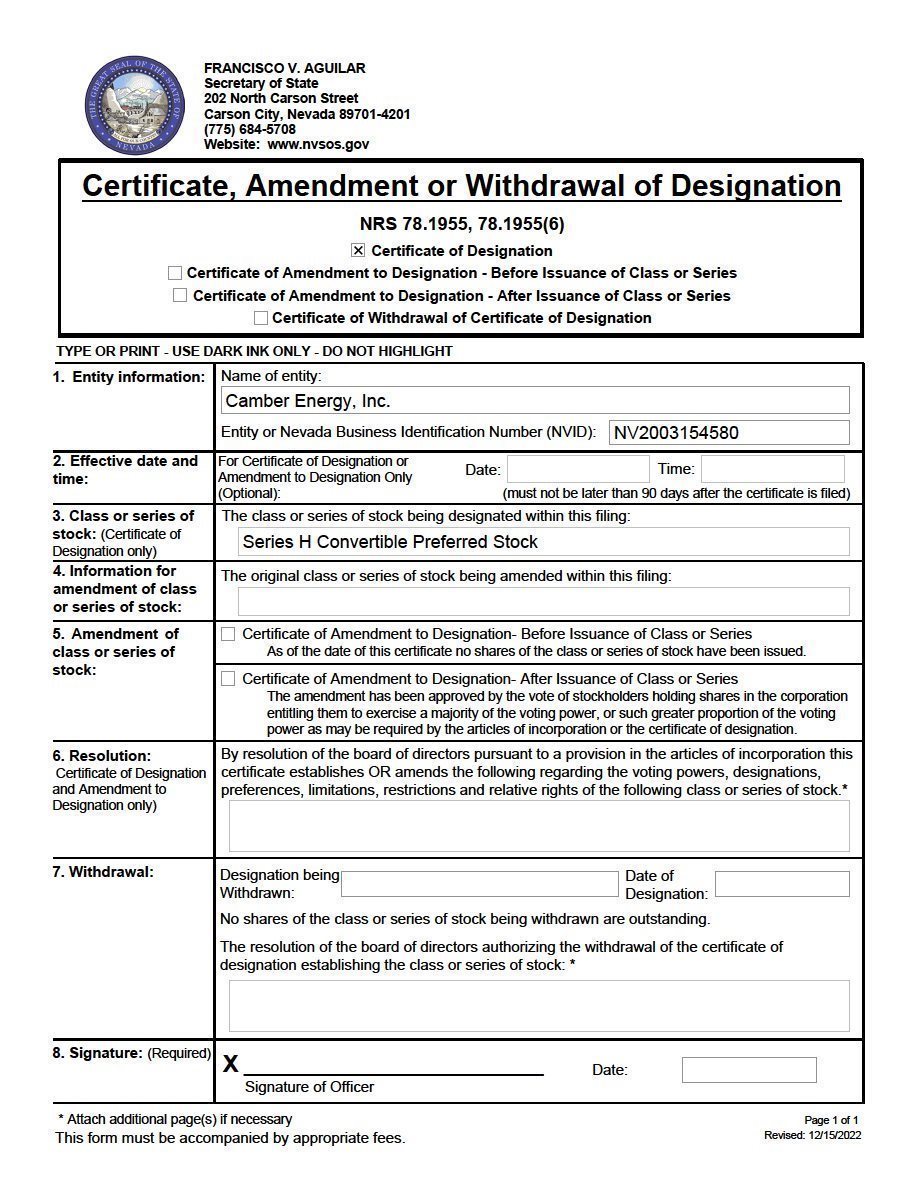

Stockholders of Camber (which we refer to as the “Camber Stockholders”) as of the close of business on , 2023, the record date, are invited to virtually attend a special meeting of Camber Stockholders (which we refer to as the “Camber Special Meeting”) on , 2023, at 10:00 a.m. (Houston time) via virtual format only. The virtual meeting may be accessed at https://agm.issuerdirect.com/cei. There is no in-person meeting for you to attend. Registration to attend the Camber Special Meeting will begin at 9:45 a.m. (15 minutes before the Camber Special Meeting begins), which can be accomplished using your control number and other information. Once your registration is complete, you can access the Camber Special Meeting at https://agm.issuerdirect.com/cei and click on “Vote My Shares,” which will direct you to www.iproxydirect.com/CEI to cast your vote on the proposals being considered at the Camber Special Meeting. At the Camber Special Meeting, Camber Stockholders will be asked to consider and vote upon: (1) a proposal to approve the issuance of shares of common stock, par value $0.001 per share, of Camber (which we refer to as “Camber Common Stock”) in connection with the Merger (which we refer to as the “Camber Common Stock Issuance Proposal”), (2) a proposal to approve the potential issuance of Camber Common Stock representing more than 20% of the outstanding Camber Common Stock pursuant to the conversion of the shares of Camber’s Series A Convertible Preferred Stock (“Camber Series A Preferred Stock”) that Camber plans to issue in connection with the Merger, and the voting rights associated therewith (the “Camber Series A Preferred Stock Issuance Proposal”), (3) a proposal to approve the potential issuance of Camber Common Stock representing more than 20% of the outstanding Camber Common Stock pursuant to the conversion of the shares of Camber’s Series H Convertible Preferred Stock (“Camber Series H Preferred Stock”) that Camber plans to issue in connection with the Merger, and the voting rights associated therewith (the “Camber Series H Preferred Stock Issuance Proposal” and together with the Camber Common Stock Issuance Proposal and the Camber Series A Preferred Stock Issuance Proposal, the “Camber Issuance Proposals”), and (4) a proposal to adjourn the Camber Special Meeting, if necessary or appropriate, to solicit additional proxies if, immediately prior to such adjournment, there are not sufficient votes to approve the Camber Issuance Proposals or to ensure that any supplement or amendment to the accompanying joint proxy statement/prospectus is timely provided to Camber Stockholders (the “Camber Adjournment Proposal” and, together with the Camber Issuance Proposals, the “Camber Proposals”). The aggregate shares of Camber Common Stock issuable in connection with the Merger, upon conversion of the Camber Series A Preferred Stock and Camber Series H Preferred Stock issued in connection with the Merger will exceed 20% of both the voting power and the Camber Common Stock outstanding before such issuance. In accordance with Section 712 of the NYSE American Company Guide, Camber is therefore requesting stockholder approval with respect to the issuance of shares in connection with the Merger and in connection with the conversion into Camber Common Stock of Camber Series A Preferred Stock and Camber Series H Preferred stock to be issued in connection with the Merger.

Stockholders of Viking (which we refer to as the “Viking Stockholders”) as of the close of business on , 2023, the record date, are invited to virtually attend a special meeting of Viking Stockholders (which we refer to as the “Viking Special Meeting”) on , 2023, at 2:00 p.m. (Houston time) via virtual format only. The virtual meeting may be accessed at https://agm.issuerdirect.com/vkin. There is no in-person meeting for you to attend. Registration to attend the Viking Special Meeting will begin at 1:45 p.m. (15 minutes before the Viking Special Meeting begins), which can be accomplished using your control number and other information. Once your registration is complete, you can access the Viking Special Meeting at https://agm.issuerdirect.com/vkin and click on “Vote My Shares,” which will direct you to www.iproxydirect.com/vkin to cast your vote on the proposals being considered at the Viking Special Meeting. At the Viking Special Meeting, Viking Stockholders will be asked to consider and vote upon: (1) a proposal to adopt the Merger Agreement (which we refer to as the “Viking Merger Proposal”) and (2) a proposal to adjourn the Viking Special Meeting, if necessary or appropriate, to solicit additional proxies if, immediately prior to such adjournment, there are not sufficient votes to approve the Viking Merger Proposal or to ensure that any supplement or amendment to the accompanying joint proxy statement/prospectus is timely provided to Viking Stockholders (the “Viking Adjournment Proposal” and, together with the Viking Merger Proposal, the “Viking Proposals”).

ii |

For Viking Stockholders, if the Merger is completed, you will be entitled to receive, (1) for each issued and outstanding share of common stock, par value $0.001 per share, of Viking (which we refer to as “Viking Common Stock”) owned by you immediately prior to the effective time of the Merger (other than shares of Viking Common Stock owned by Camber, Viking or Merger Sub), one (1) share of Camber Common Stock (which we refer to as the “Common Stock Merger Consideration”), (2) for each issued and outstanding share of Viking Series C Preferred Stock (the “Viking Series C Preferred Stock”) owned by you immediately prior to the effective time of the Merger, one (1) share of Camber Series A Preferred Stock (the “Series A Preferred Stock Merger Consideration”), and (3) for each issued and outstanding share of Viking Series E Preferred Stock (the “Viking Series E Preferred Stock”) owned by you immediately prior to the effective time of the Merger, one (1) share of Camber Series H Preferred Stock (the “Series H Preferred Stock Merger Consideration” and, together with the Common Stock Merger Consideration and the Series A Preferred Stock Merger Consideration, the “Merger Consideration”), each as further described in the joint proxy statement/prospectus accompanying this notice. The market value of the Merger Consideration will fluctuate with the price of the Camber Common Stock. Camber’s Common Stock is traded on the NYSE American under the symbol “CEI.” Viking Common Stock is traded on the over-the-counter OTC Link Alternative Trading System (ATS) operated by OTC Markets Group, Inc. under the symbol “VKIN.” Based on the closing price of the Camber Common Stock on the NYSE American stock exchange on April 18, 2023, the last trading day before public announcement of entry into the Merger Agreement amendment and the fully diluted number of shares of Camber and Viking on that date (without taking into account shares of Camber Common Stock issuable upon conversion of Camber’s Series C Redeemable Convertible Preferred Stock or Camber’s Series G Redeemable Convertible Preferred Stock), the exchange ratio represented approximately $1.62 in value for each share of Viking Common Stock. The value of the Camber Common Stock at the time of completion of the Merger could be greater than, less than or the same as, the value of Camber Common Stock on the date of the accompanying joint proxy statement/prospectus. We urge you to obtain current market quotations of Camber Common Stock (trading symbol “CEI”) and Viking Common Stock (trading symbol “VKIN”). Following the completion of the Merger, the common stock of the combined company is expected to be listed on the NYSE American stock exchange under the symbol “CEI.”

The Camber board of directors (1) has unanimously determined that the Merger Agreement and the transactions contemplated by the Merger Agreement, including the issuance of shares of Camber Common Stock, Camber Series A Preferred Stock and Camber Series H Preferred Stock in connection with the Merger (the “Share Issuances”) is fair to, and in the best interests of, Camber and its stockholders; (2) has unanimously approved and declared advisable the Merger Agreement and the transactions contemplated by the Merger Agreement, including the Share Issuances; (3) has unanimously directed that the Share Issuances be submitted to the Camber Stockholders for their approval; and (4) unanimously recommends that the Camber Stockholders vote “FOR” the Camber Common Stock Issuance Proposal, “FOR” the Camber Series A Preferred Stock Issuance Proposal, “FOR” the Camber Series H Preferred Stock Issuance Proposal and “FOR” the Camber Adjournment Proposal.

The Viking board of directors (1) has unanimously determined that the Merger Agreement and the transactions contemplated by the Merger Agreement, including the Merger, are fair to, and in the best interests of, Viking and its stockholders; (2) has unanimously approved and declared advisable the Merger Agreement and the transactions contemplated by the Merger Agreement, including the Merger; (3) has directed that the Merger Agreement be submitted to the Viking Stockholders for their adoption; and (4) unanimously recommends that the Viking Stockholders vote “FOR” the Viking Merger Proposal and “FOR” the Viking Adjournment Proposal.

Camber and Viking will each hold a virtual special meeting of its stockholders to consider certain matters relating to the Merger, which may be attended via the Camber Special Meeting website and the Viking Special Meeting website, respectively. Camber and Viking cannot complete the Merger unless, among other things, the Camber Stockholders approve the Share Issuances in connection with the Merger and the Viking Stockholders adopt the Merger Agreement.

Your vote is very important. To ensure your representation at your company’s special meeting, complete and return the applicable enclosed proxy card or submit your proxy by phone or the Internet. Please vote promptly whether or not you expect to virtually attend your company’s special meeting. Submitting a proxy now will not prevent you from being able to vote at your company’s special meeting.

iii |

The joint proxy statement/prospectus accompanying this notice is also being delivered to the Viking Stockholders as Camber’s prospectus for its Share Issuances in connection with the Merger.

The obligations of Camber and Viking to complete the Merger are subject to the satisfaction or waiver of the conditions set forth in the Merger Agreement, a copy of which is included as part of the accompanying joint proxy statement/prospectus. The joint proxy statement/prospectus provides you with detailed information about the Merger. It also contains or references information about Camber and Viking and certain related matters. You are encouraged to read the joint proxy statement/prospectus carefully and in its entirety. In particular, you should carefully read the section entitled “Risk Factors” beginning on page 39 of the joint proxy statement/prospectus for a discussion of risks you should consider in evaluating the Merger and the Share Issuances in connection with the Merger and how they will affect you.

Sincerely, | Sincerely, | Sincerely, |

|

|

|

/s/ Fred Zeidman Fred Zeidman Director Camber Energy, Inc. | /s/ Lawrence Fisher Lawrence Fisher Director Viking Energy Group, Inc. | /s/ James A. Doris James A. Doris President, Chief Executive Officer and Director, Viking Energy Group, Inc. President, Chief Executive Officer and Director, Camber Energy, Inc. |

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities to be issued under the accompanying joint proxy statement/prospectus or passed upon the adequacy or accuracy of the disclosure in this document. Any representation to the contrary is a criminal offense.

The joint proxy statement/prospectus is dated , 2023, and is first being mailed to stockholders of Camber and Viking on or about , 2023.

iv |

CAMBER ENERGY, INC.

15915 Katy Freeway, Suite 450

Houston, Texas 77094

NOTICE OF SPECIAL MEETING OF STOCKHOLDERS

To Be Held on , 2023

Dear Stockholder,

Camber Energy, Inc. (“we”, “us,” “Camber” or the “Company”) cordially invites you to attend a special meeting of stockholders (the “Camber Special Meeting”). The meeting will be held virtually on , 2023, at 10:00 a.m. (Houston time), at 15915 Katy Freeway, Suite 450, Houston, Texas 77094.

Due to the public health impact of the novel coronavirus outbreak (COVID-19) and to support the health and well-being of our management and stockholders, NOTICE IS HEREBY GIVEN that the Camber Special Meeting will be held in a virtual meeting format only. The virtual meeting may be accessed at https://agm.issuerdirect.com/cei. There is no in-person meeting for you to attend. Registration to attend the Camber Special Meeting will begin at 9:45 a.m. (15 minutes before the Camber Special Meeting begins), which can be accomplished using your control number and other information. Once your registration is complete, you can access the Camber Special Meeting at https://agm.issuerdirect.com/cei and click on “Vote My Shares,” which will direct you to www.iproxydirect.com/CEI to cast your vote on the proposals being considered at the Camber Special Meeting. You will also be permitted to submit questions at the time of registration. After registration is complete and you have entered the Camber Special Meeting virtually, the next screen will include a “Ask a Question” box where your questions may be submitted. You may ask questions that are confined to matters properly before the Camber Special Meeting and of general Company concern. All answers to proper questions received at the meeting will be posted to the Investor Relations page of our website upon conclusion of the meeting. The meeting will begin promptly at 10:00 a.m. (Houston time). We encourage you to access the virtual meeting prior to the start time. Online access will open approximately at 9:45 a.m. (Houston time), and you should allow ample time to log in to the meeting and test your computer audio system. We recommend that you carefully review the procedures needed to gain admission in advance. There will be technicians ready to assist you with any technical difficulties you may have accessing the virtual meeting. If you encounter any difficulties accessing the virtual meeting during check-in or during the meeting, please call the technical support number that will be posted on the virtual stockholder meeting login page. Whether or not you plan to attend the Camber Special Meeting, we urge you to vote and submit your proxy in advance of the meeting by one of the methods described in the proxy materials for the Camber Special Meeting.

At the meeting we will be considering and voting on the following matters:

| · | to vote on a proposal to approve the issuance of shares of common stock, par value $0.001 per share, of Camber (which we refer to as “Camber Common Stock”) pursuant to the terms and conditions of the Agreement and Plan of Merger, dated as of February 15, 2021, as amended on April 18, 2023 (which, as it may be further amended from time to time, we refer to as the “Merger Agreement”), by and between the Company and Viking Energy Group, Inc. (“Viking”) (which we refer to as the “Camber Common Stock Issuance Proposal”); |

|

|

|

| · | to vote on a proposal to approve the potential issuance of Camber Common Stock representing more than 20% of the outstanding Camber Common Stock pursuant to the conversion of the shares of Camber’s Series A Convertible Preferred Stock (“Camber Series A Preferred Stock”) that Camber plans to issue in connection with the Merger Agreement, and the voting rights associated therewith (the “Camber Series A Preferred Stock Issuance Proposal”); |

|

|

|

| · | to vote on a proposal to approve the potential issuance of Camber Common Stock representing more than 20% of the outstanding Camber Common Stock pursuant to the conversion of the shares of Camber’s Series H Convertible Preferred Stock (“Camber Series H Preferred Stock”) that Camber plans to issue pursuant to the terms and conditions of the Merger Agreement, and the voting rights associated therewith (the “Camber Series H Preferred Stock Issuance Proposal” and together with the Camber Common Stock Issuance Proposal and the Camber Series A Preferred Stock Issuance Proposal, the “Camber Issuance Proposals”); and |

|

|

|

| · | to vote on a proposal to adjourn the Camber Special Meeting, if necessary or appropriate, to solicit additional proxies if, immediately prior to such adjournment, there are not sufficient votes to approve the Camber Issuance Proposals or to ensure that any supplement or amendment to the accompanying joint proxy statement/prospectus is timely provided to Camber stockholders (the “Camber Adjournment Proposal” and, together with the Camber Issuance Proposals, the “Camber Proposals”). |

v |

Camber will transact no other business at the Camber Special Meeting, except such business as may properly be brought before the Camber Special Meeting by or at the direction of the Camber board of directors (which we refer to as the “Camber Board”) in accordance with Camber’s Amended and Restated Bylaws. Stockholders who owned Camber Common Stock, our Series C Redeemable Convertible Preferred Stock (“Camber Series C Preferred Stock”) or our Series G Redeemable Convertible Preferred Stock (“Camber Series G Preferred Stock”) at the close of business on , 2023 (the “Record Date”), may attend and vote at the meeting, provided that holders of Camber Series C Preferred Stock and Camber Series G Preferred Stock have the right to cast votes on all Camber Proposals above, except any shareholder proposals, equal to the as-converted amount of such Camber Series C Preferred Stock and Camber Series G Preferred Stock, respectively (subject to the beneficial ownership limitations in the Certificate of Designations of Preferences, Powers, Rights and Limitations of Series C Redeemable Convertible Preferred Stock (the “Series C COD”) and the Certificate of Designations of Preferences, Powers, Rights and Limitations of Series G Redeemable Convertible Preferred Stock (the “Series G COD”), respectively). The holders of the Camber Series C Preferred Stock and the Camber Series G Preferred Stock have contractually agreed not to vote any shares except as requested by the Camber Board. A stockholders list will be available at our offices at 15915 Katy Freeway, Suite 450, Houston, Texas 77094, for a period of ten days prior to the meeting. For additional information regarding the Camber Special Meeting, see the section entitled “Special Meeting of Camber Stockholders” beginning on page 82 of the joint proxy statement/prospectus accompanying this notice. We hope that you will be able to virtually attend the meeting.

The Camber Board unanimously recommends that Camber stockholders vote “FOR” the Camber Common Stock Issuance Proposal, “FOR” the Camber Series A Preferred Stock Issuance Proposal, “FOR” the Camber Series H Preferred Stock Issuance Proposal and “FOR” the Camber Adjournment Proposal.

The accompanying joint proxy statement/prospectus describes the Camber Proposals in more detail. Please refer to the attached document, including the Merger Agreement and all other annexes and any documents incorporated by reference, for further information with respect to the business to be transacted at the Camber Special Meeting. You are encouraged to read the entire document carefully before voting. In particular, see the section entitled “The Merger” beginning on page 130 of the joint proxy statement/ prospectus accompanying this notice for a description of the transactions contemplated by the Merger Agreement, including the Camber Issuance Proposals and the Camber Adjournment Proposal, and the section entitled “Risk Factors” beginning on page 39 of the joint proxy statement/prospectus accompanying this notice for an explanation of the risks associated with the merger of Viking with and into a wholly owned subsidiary of Camber (the “Merger”) and the other transactions contemplated by the Merger Agreement, including the Camber Issuance Proposals and the Camber Adjournment Proposal.

PLEASE VOTE AS PROMPTLY AS POSSIBLE, WHETHER OR NOT YOU PLAN TO ATTEND THE CAMBER SPECIAL MEETING VIA THE CAMBER SPECIAL MEETING WEBSITE. IF YOU LATER DESIRE TO REVOKE OR CHANGE YOUR PROXY FOR ANY REASON, YOU MAY DO SO IN THE MANNER DESCRIBED IN THE ACCOMPANYING JOINT PROXY STATEMENT/PROSPECTUS. FOR FURTHER INFORMATION CONCERNING THE PROPOSALS BEING VOTED UPON, USE OF THE PROXY AND OTHER RELATED MATTERS, YOU ARE URGED TO READ THE ACCOMPANYING JOINT PROXY STATEMENT/PROSPECTUS.

If you have any questions concerning the Camber Proposals, the Merger or the accompanying joint proxy statement/prospectus, would like additional copies or need help voting your shares, please contact Camber’s proxy solicitor:

Issuer Direct Corporation

1 Glenwood Ave., Suite 1001

Raleigh, North Carolina

Telephone: (866) 752-8683

Email: proxy@issuerdirect.com

vi |

Your vote is very important. Approval of the Camber Issuance Proposals by the Camber stockholders is a condition to the Merger. The Camber Issuance Proposals each require the affirmative vote of a majority of the Camber shares of stock present via the Camber Special Meeting website or by proxy at the Camber Special Meeting and entitled to vote on the proposal. The Camber Adjournment Proposal requires the affirmative vote of a majority of the Camber shares of stock present via the Camber Special Meeting website or by proxy at the Camber Special Meeting and entitled to vote on the proposal. Camber stockholders are requested to complete, date, sign and return the enclosed proxy in the envelope provided, which requires no postage if mailed in the United States, or to submit their votes by phone or the Internet. Follow the instructions provided on the enclosed proxy card. Abstentions will have the same effect as a vote “AGAINST” the Camber Issuance Proposals and the Camber Adjournment Proposal. If you are a holder of record, failure to submit a proxy or vote via the Camber Special Meeting website will have no effect on the outcome of the vote of the Camber Issuance Proposals and Camber Adjournment Proposal. Broker non-votes will have no effect on the outcome of the vote on the Camber Issuance Proposals and Camber Adjournment Proposal.

BY ORDER OF THE BOARD OF DIRECTORS,

| Sincerely,

| Sincerely,

|

| /s/ Fred Zeidman Fred Zeidman Director Camber Energy, Inc. | /s/ James A. Doris James A. Doris President, Chief Executive Officer and Director Camber Energy, Inc. |

vii |

VIKING ENERGY GROUP, INC.

15915 Katy Freeway, Suite 450

Houston, Texas 77094

NOTICE OF SPECIAL MEETING OF STOCKHOLDERS

To Be Held on , 2023

Dear Stockholder,

Viking Energy Group, Inc. (“we”, “us,” “Viking” or the “Company”) cordially invites you to attend a special meeting of stockholders (the “Viking Special Meeting”). The meeting will be held virtually on , 2023, at 2:00 p.m. (Houston time), at 15915 Katy Freeway, Suite 450, Houston, Texas 77094.

Due to the public health impact of the novel coronavirus outbreak (COVID-19) and to support the health and well-being of our management and stockholders, NOTICE IS HEREBY GIVEN that the Viking Special Meeting will be held in a virtual meeting format only. The virtual meeting may be accessed at https://agm.issuerdirect.com/vkin. There is no in-person meeting for you to attend. Registration to attend the Viking Special Meeting will begin at 1:45 p.m. (15 minutes before the Viking Special Meeting begins), which can be accomplished using your control number and other information. Once your registration is complete, you can access the Viking Special Meeting at https://agm.issuerdirect.com/vkin and click on “Vote My Shares,” which will direct you to www.iproxydirect.com/vkin to cast your vote on the proposals being considered at the Viking Special Meeting. You will also be permitted to submit questions at the time of registration. After registration is complete and you have entered the Viking Special Meeting virtually, the next screen will include a “Ask a Question” box where your questions may be submitted. You may ask questions that are confined to matters properly before the Viking Special Meeting and of general Company concern. All answers to proper questions received at the meeting will be posted to the Investor Relations page of our website upon conclusion of the meeting. The meeting will begin promptly at 2:00 p.m. (Houston time). We encourage you to access the virtual meeting prior to the start time. Online access will open approximately at 1:45 p.m. (Houston time), and you should allow ample time to log in to the meeting and test your computer audio system. We recommend that you carefully review the procedures needed to gain admission in advance. There will be technicians ready to assist you with any technical difficulties you may have accessing the virtual meeting. If you encounter any difficulties accessing the virtual meeting during check-in or during the meeting, please call the technical support number that will be posted on the virtual stockholder meeting login page. Whether or not you plan to attend the Viking Special Meeting, we urge you to vote and submit your proxy in advance of the meeting by one of the methods described in the proxy materials for the Viking Special Meeting.

At the meeting we will be considering and voting on the following matters:

| · | to adopt the Agreement and Plan of Merger, dated as of February 15, 2021, as amended on April 18, 2023 (which, as it may be further amended from time to time, we refer to as the “Merger Agreement”), among Viking and Camber Energy, Inc. (“Camber”) (which we refer to as the “Viking Merger Proposal”) providing for the acquisition of Viking by Camber pursuant to a merger between Viking Merger Sub, Inc., a Nevada corporation and wholly owned subsidiary of Camber (“Merger Sub”) and Viking (which we refer to as the “Merger”); and |

|

|

|

| · | to adjourn the Viking Special Meeting, if necessary or appropriate, to solicit additional proxies if, immediately prior to such adjournment, there are not sufficient votes to approve the Viking Merger Proposal or to ensure that any supplement or amendment to the accompanying joint proxy statement/prospectus is timely provided to Viking stockholders (the “Viking Adjournment Proposal” and, together with the Viking Merger Proposal, the “Viking Proposals”). |

Viking stockholder approval of the Viking Merger Proposal is required to complete the Merger between Merger Sub and Viking, as contemplated by the Merger Agreement. Viking will transact no other business at the Viking Special Meeting, except such business as may properly be brought before the Viking Special Meeting by or at the direction of the Viking board of directors (which we refer to as the “Viking Board”) in accordance with Viking’s Bylaws. Stockholders who owned Viking’s common stock, Viking Series C Preferred Stock or Viking Series E Preferred Stock at the close of business on , 2023 (the “Record Date”), may attend and vote at the meeting. A stockholders list will be available at our offices at 15915 Katy Freeway, Suite 450, Houston, Texas 77094, for a period of ten days prior to the meeting. For additional information regarding the Viking Special Meeting, see the section entitled “Special Meeting of Viking Stockholders” beginning on page 89 of the joint proxy statement/prospectus accompanying this notice.

viii |

The Viking Board unanimously recommends that you vote “FOR” the Viking Merger Proposal and “FOR” the Viking Adjournment Proposal.

The Viking Proposals are described in more detail in the accompanying joint proxy statement/prospectus, which you should read carefully and in its entirety before you vote. A copy of the Merger Agreement is attached as Annex A to the accompanying joint proxy statement/prospectus.

PLEASE VOTE AS PROMPTLY AS POSSIBLE, WHETHER OR NOT YOU PLAN TO ATTEND THE VIKING SPECIAL MEETING VIA THE VIKING SPECIAL MEETING WEBSITE. IF YOU LATER DESIRE TO REVOKE OR CHANGE YOUR PROXY FOR ANY REASON, YOU MAY DO SO IN THE MANNER DESCRIBED IN THE ACCOMPANYING JOINT PROXY STATEMENT/PROSPECTUS. FOR FURTHER INFORMATION CONCERNING THE PROPOSALS BEING VOTED UPON, USE OF THE PROXY AND OTHER RELATED MATTERS, YOU ARE URGED TO READ THE ACCOMPANYING JOINT PROXY STATEMENT/PROSPECTUS.

If you have any questions concerning the Viking Proposals, the Merger or the accompanying joint proxy statement/prospectus, would like additional copies or need help voting your Viking shares, please contact Viking’s proxy solicitor:

Issuer Direct Corporation

1 Glenwood Ave., Suite 1001

Raleigh, North Carolina

Telephone: (866) 752-8683

Email: proxy@issuerdirect.com

Your vote is very important. The Merger is conditioned on the approval of the Viking Merger Proposal by the Viking stockholders and the Viking Merger Proposal requires the affirmative vote of the holders of a majority of the outstanding Viking shares entitled to vote on such proposal. Viking’s stockholders are requested to complete, date, sign and return the enclosed proxy in the envelope provided, which requires no postage if mailed in the United States, or to submit their votes by phone or the Internet. Simply follow the instructions provided on the enclosed proxy card. Abstentions, failure to submit a proxy or vote via the Viking Special Meeting website and broker non-votes will have the same effect as a vote “AGAINST” the Viking Merger Proposal. Abstentions will have the same effect as a vote “AGAINST” the Viking Adjournment Proposal, and broker non-votes will have no effect on the outcome of the vote of the Viking Adjournment Proposal.

BY ORDER OF THE BOARD OF DIRECTORS,

| Sincerely, | Sincerely, |

|

|

|

| /s/ Lawrence Fisher Lawrence Fisher Director Viking Energy Group, Inc. | /s/ James A. Doris James A. Doris President, Chief Executive Officer and Director Viking Energy Group, Inc. |

ix |

ADDITIONAL INFORMATION

This proxy statement/prospectus incorporates important business and financial information about Camber and Viking from documents that are not included in or delivered with this proxy statement/prospectus. This information is available for you to review through Camber’s and Viking’s annual, quarterly and current reports, proxy statements and other information filed with the U.S. Securities and Exchange Commission (which we refer to as the “SEC”). These filings and information are available for you to review free of charge through the SEC’s website at www.sec.gov. See the section entitled “Where You Can Find More Information” for further information.

You may request copies of this joint proxy statement/prospectus and any of the documents incorporated herein or other information concerning Camber or Viking, without charge, upon written or oral request to the applicable company’s principal executive offices. The respective addresses and phone numbers of such principal executive offices are listed below.

For Camber Stockholders: | For Viking Stockholders: |

|

|

Camber Energy, Inc. 15915 Katy Freeway, Suite 450 Houston, Texas 77094 Attention: Investor Relations (281) 404-4387 | Viking Energy Group, Inc. 15915 Katy Freeway, Suite 450 Houston, Texas 77094 Attention: Investor Relations (281) 404-4387 |

To obtain timely delivery of these documents before the Camber Special Meeting (as defined in the section entitled “Questions and Answers about the Merger and the Special Meetings”), Camber stockholders must request the information no later than , 2023 (which is five business days before the date of the Camber Special Meeting).

To obtain timely delivery of these documents before the Viking Special Meeting (as defined in the section entitled “Questions and Answers about the Merger and the Special Meetings”), Viking stockholders must request the information no later than , 2023 (which is five business days before the date of the Viking Special Meeting).

In addition, if you have questions about the Merger or this joint proxy statement/prospectus, would like additional copies of this joint proxy statement/prospectus or need to obtain proxy cards or other information related to the proxy solicitation, contact Issuer Direct Corporation, the proxy solicitor for Camber and Viking, toll-free at (866) 752-8683, or by email at proxy@issuerdirect.com. You will not be charged for any of these documents that you request.

x |

ABOUT THIS JOINT PROXY STATEMENT/PROSPECTUS

This document, which forms part of a registration statement on Form S-4 filed with the SEC by Camber (File No. 333-271395), constitutes a prospectus of Camber under Section 5 of the Securities Act of 1933, as amended (which we refer to as the “Securities Act”), with respect to the shares of common stock of Camber, par value $0.001 per share (which we refer to as “Camber Common Stock”), to be issued to Viking stockholders, or issuable to Viking stockholders upon conversion of the convertible preferred stock to be issued to Viking stockholders pursuant to the Agreement and Plan of Merger, dated as of February 15, 2021, as amended on April 18, 2023 (which, as it may be further amended from time to time, we refer to as the “Merger Agreement”), by and between Camber and Viking.

This document also constitutes a notice of meeting and proxy statement of each of Camber and Viking under Section 14(a) of the Securities Exchange Act of 1934, as amended (which we refer to as the “Exchange Act”).

Camber has supplied all information contained herein relating to Camber, and Viking has supplied all information contained herein relating to Viking. Camber and Viking have both contributed to the information relating to the Merger Agreement contained in this joint proxy statement/prospectus.

Neither Camber nor Viking has authorized anyone to provide any information or to make any representations other than those contained in this joint proxy statement/prospectus in connection with any vote, the giving or withholding of any proxy or any investment decision in connection with the Merger Agreement. Camber and Viking take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This joint proxy statement/prospectus is dated , 2023, and you should not assume that the information contained in this joint proxy statement/prospectus is accurate as of any date other than such date unless otherwise specifically provided herein. Neither the mailing of this joint proxy statement/prospectus to Camber or Viking stockholders nor the issuance by Camber of shares of Camber Common Stock pursuant to the Merger Agreement will create any implication to the contrary.

All currency amounts referenced in this joint proxy statement/prospectus are in U.S. dollars.

xi |

TABLE OF CONTENTS

xii |

| 78 |

| |

| 81 |

| |

| 82 |

| |

| 83 |

| |

| 84 |

| |

| 84 |

| |

| 85 |

| |

| 85 |

| |

| 85 |

| |

| 85 |

| |

| 86 |

| |

| 86 |

| |

| 89 |

| |

| 90 |

| |

| 91 |

| |

| 91 |

| |

| 91 |

| |

| 91 |

| |

| 92 |

| |

| 92 |

| |

| 93 |

| |

| 93 |

| |

| 94 |

| |

| 95 |

| |

| 110 |

| |

| 111 |

| |

CAMBER’S MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

| 113 |

|

VIKING’S MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

| 120 |

|

| 130 |

| |

| 130 |

| |

| 130 |

| |

| 130 |

| |

Camber’s Reasons for the Merger; Recommendation of the Camber Board |

| 146 |

|

| 148 |

| |

Viking’s Reasons for the Merger; Recommendation of the Viking Board |

| 155 |

|

| 157 |

| |

| 165 |

| |

| 169 |

| |

Board of Directors and Management of Camber Following the Completion of the Merger |

| 169 |

|

Interests of Viking Directors and Executive Officers in the Merger |

| 169 |

|

| 171 |

| |

Listing of Camber Common Stock; Delisting and Deregistration of Viking Common Stock |

| 171 |

|

| 171 |

| |

| 172 |

|

xiii |

| 173 |

| |

| 173 |

| |

| 173 |

| |

| 174 |

| |

| 174 |

| |

Treatment of Viking Convertible Securities and Preferred Stock |

| 175 |

|

Treatment of Camber Convertible Securities and Preferred Stock |

| 176 |

|

| 176 |

| |

| 176 |

| |

| 176 |

| |

| 177 |

| |

| 179 |

| |

| 181 |

| |

Stockholder Meetings and Recommendation of Camber’s and Viking’s Boards of Directors |

| 181 |

|

| 182 |

| |

| 183 |

| |

| 184 |

| |

| 185 |

| |

| 185 |

| |

| 185 |

| |

| 185 |

| |

| 186 |

| |

| 186 |

| |

| 187 |

| |

| 191 |

| |

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE |

| 197 |

|

| 197 |

| |

| 200 |

| |

| 200 |

| |

| 205 |

| |

SHARE OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT/DIRECTORS OF CAMBER |

| 206 |

|

| 206 |

| |

SHARE OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT/DIRECTORS OF VIKING |

| 207 |

|

| 207 |

| |

| 208 |

| |

| 210 |

| |

| 210 |

| |

| 210 |

| |

| 210 |

| |

| 210 |

| |

| 210 |

| |

| 211 |

| |

| 211 |

|

xiv |

QUESTIONS AND ANSWERS ABOUT THE MERGER AND THE SPECIAL MEETINGS

The following are answers to certain questions that you may have regarding the Camber and Viking special meetings. Camber and Viking urge you to read carefully the remainder of this document because the information in this section may not provide all the information that might be important to you in determining how to vote. Additional important information is also contained in the annexes to this document.

Q: | Why am I receiving this joint proxy statement/prospectus? |

|

|

A: | You are receiving this joint proxy statement/prospectus because Camber and Viking have entered into the Merger Agreement, pursuant to which, on the terms and subject to the conditions included in the Merger Agreement, Camber has agreed to acquire Viking by means of a merger of Viking Merger Sub, Inc., a Nevada corporation and wholly owned subsidiary of Camber (“Merger Sub”) with and into Viking (which we refer to as the “Merger”), with Viking surviving the Merger as a wholly owned subsidiary of Camber. Your vote is required in connection with the Merger. The Merger Agreement, which governs the terms of the Merger, is attached to this joint proxy statement/prospectus as Annex A. |

|

|

| Camber. In order to consummate the Merger, the stockholders of Camber (which we refer to as the “Camber Stockholders”) must (1) approve the issuance of shares of common stock, par value $0.001 per share, of Camber (which we refer to as “Camber Common Stock”) in connection with the Merger (which we refer to as the “Camber Common Stock Issuance Proposal”), (2) approve the potential issuance of Camber Common Stock representing more than 20% of the outstanding Camber Common Stock pursuant to the conversion of the shares of Camber’s Series A Convertible Preferred Stock (“Camber Series A Preferred Stock”) that Camber plans to issue in connection with the Merger, and the voting rights associated therewith (the “Camber Series A Preferred Stock Issuance Proposal”), and (3) approve the potential issuance of Camber Common Stock representing more than 20% of the outstanding Camber Common Stock pursuant to the conversion of the shares of Camber’s Series H Convertible Preferred Stock (“Camber Series H Preferred Stock”) that Camber plans to issue in connection with the Merger, and the voting rights associated therewith (the “Camber Series H Preferred Stock Issuance Proposal” and together with the Camber Common Stock Issuance Proposal and the Camber Series A Preferred Stock Issuance Proposal, the “Camber Issuance Proposals”) in accordance with the rules of the NYSE American and Camber’s organizational documents. Camber is holding a virtual special meeting of its stockholders (which we refer to as the “Camber Special Meeting”) to obtain these approvals. Camber Stockholders will also be asked to vote on a proposal to adjourn the Camber Special Meeting, if necessary or appropriate, to solicit additional proxies if, immediately prior to such adjournment, there are not sufficient votes to approve the Camber Issuance Proposals or to ensure that any supplement or amendment to the accompanying joint proxy statement/prospectus is timely provided to Camber Stockholders (the “Camber Adjournment Proposal” and, together with the Camber Issuance Proposals, the “Camber Proposals”). Your vote is very important. We encourage you to submit a proxy to have your shares of Camber stock voted as soon as possible.

Viking. In order to consummate the Merger, the Merger Agreement must be adopted by the Viking Stockholders (as defined at the end of this paragraph) (which we refer to as the “Viking Merger Proposal”) in accordance with the Nevada Revised Statutes (which we refer to as the “NRS”). Viking is holding a virtual special meeting of its stockholders (which we refer to as the “Viking Special Meeting”) to obtain this approval. Viking Stockholders will also be asked to vote on a proposal to adjourn the Viking Special Meeting, if necessary or appropriate, to solicit additional proxies if, immediately prior to such adjournment, there are not sufficient votes to approve the Viking Merger Proposal or to ensure that any supplement or amendment to the accompanying joint proxy statement/prospectus is timely provided to Viking Stockholders (the “Viking Adjournment Proposal” and, together with the Viking Merger Proposal, the “Viking Proposals”). Your vote is very important. We encourage you to submit a proxy to have your shares of Viking stock voted as soon as possible. In this joint proxy statement/prospectus, we use the term “Viking Stockholders” to refer to the holders of shares of common stock, par value $0.001 per share, of Viking (which we refer to “Viking Common Stock”) and those shares of Viking’s preferred stock that are eligible to vote on the Viking Proposals along with the Viking Common Stock. |

| 1 |

| Table of Contents |

Q: | When and where will the special meetings take place? |

|

|

A: | Camber. The Camber Special Meeting will be held virtually via live webcast on , 2023, at 10:00 a.m. (Houston time). Camber Stockholders will be able to attend the Camber Special Meeting online at https://agm.issuerdirect.com/cei and vote their shares electronically during the meeting by visiting www.iproxydirect.com/CEI (which we collectively refer to as the “Camber Special Meeting Website”). Because the Camber Special Meeting is completely virtual and being conducted via live webcast, Camber Stockholders will not be able to attend the meeting in person. |

|

|

| Viking. The Viking Special Meeting will be held virtually via live webcast on , 2023, at 2:00 p.m. (Houston time). Viking Stockholders will be able to attend the Viking Special Meeting online at https://agm.issuerdirect.com/vkin and vote their shares electronically during the meeting by visiting www.iproxydirect.com/vkin (which we collectively refer to as the “Viking Special Meeting Website”). Because the Viking Special Meeting is completely virtual and being conducted via live webcast, Viking Stockholders will not be able to attend the meeting in person. |

|

|

Q: | What matters will be considered at the special meetings? |

|

|

A: | Camber. The Camber Stockholders are being asked to consider and vote on: |

| · | a proposal to approve the issuance of Camber Common Stock pursuant to the terms and conditions of the Merger Agreement, which we refer to as the “Camber Common Stock Issuance Proposal”; |

|

|

|

| · | a proposal to approve the potential issuance of Camber Common Stock representing more than 20% of the outstanding Camber Common Stock pursuant to the conversion of the shares of Camber Series A Preferred Stock that Camber plans to issue to certain Viking Stockholders pursuant to the terms and conditions of the Merger Agreement, and the voting rights associated therewith, which we refer to as the “Camber Series A Preferred Stock Issuance Proposal”; |

|

|

|

| · | a proposal to approve the potential issuance of Camber Common Stock representing more than 20% of the outstanding Camber Common Stock pursuant to the conversion of the shares of Camber Series H Preferred Stock that Camber plans to issue to certain Viking Stockholders pursuant to the terms and conditions of the Merger Agreement, and the voting rights associated therewith, which we refer to as the “Camber Series H Preferred Stock Issuance Proposal”; and |

|

|

|

| · | a proposal to adjourn the Camber Special Meeting, if necessary or appropriate, to solicit additional proxies if, immediately prior to such adjournment, there are not sufficient votes to approve the Camber Issuance Proposals or to ensure that any supplement or amendment to the accompanying joint proxy statement/prospectus is timely provided to Camber Stockholders, which we refer to as the “Camber Adjournment Proposal”. |

| Viking. The Viking Stockholders are being asked to consider and vote on: | ||

|

|

|

|

|

| · | a proposal to adopt the Merger Agreement, which we refer to as the “Viking Merger Proposal”; and |

|

|

|

|

|

| · | a proposal to adjourn the Viking Special Meeting, if necessary or appropriate, to solicit additional proxies if, immediately prior to such adjournment, there are not sufficient votes to approve the Viking Merger Proposal or to ensure that any supplement or amendment to the accompanying joint proxy statement/prospectus is timely provided to Viking Stockholders, which we refer to as the “Viking Adjournment Proposal”. |

| 2 |

| Table of Contents |

Q: | Is my vote important? |

|

|

A: | Camber. Yes. Your vote is very important. The Merger cannot be completed unless each of the Camber Issuance Proposals are approved. Each of the Camber Issuance Proposals and the Camber Adjournment Proposal require the affirmative vote of a majority of the Camber shares of stock present via the Camber Special Meeting Website or by proxy at the Camber Special Meeting and entitled to vote on the proposal. Only Camber Stockholders as of the close of business on , 2023 (the “Record Date”), are entitled to vote at the Camber Special Meeting. The board of directors of Camber (which we refer to as the “Camber Board” or the “Camber Board of Directors”) unanimously recommends that such Camber Stockholders vote “FOR” each of the Camber Issuance Proposals and “FOR” the Camber Adjournment Proposal. |

|

|

| Viking. Yes. Your vote is very important. The Merger cannot be completed unless the Viking Merger Proposal is approved by the affirmative vote of a majority of the outstanding Viking shares entitled to vote on such proposal. The Viking Adjournment Proposal requires the affirmative vote of a majority of the shares of Viking stock present via the Viking Special Meeting Website or by proxy at the Viking Special Meeting and entitled to vote on the proposal. Only Viking Stockholders as of the close of business on the Record Date are entitled to vote at the Viking Special Meeting. The board of directors of Viking (which we refer to as the “Viking Board” or the “Viking Board of Directors”) unanimously recommends that such Viking Shareholders vote “FOR” the Viking Merger Proposal and “FOR” the Viking Adjournment Proposal. |

|

|

Q: | If my shares of Camber and/or Viking stock are held in “street name” by my broker, bank or other nominee, will my broker, bank or other nominee automatically vote those shares for me? |

|

|

A: | If your shares are held through a broker, bank or other nominee, you are considered the “beneficial holder” of the shares held for you in what is known as “street name.” The “record holder” of such shares is your broker, bank or other nominee, and not you. If this is the case, this joint proxy statement/prospectus has been forwarded to you by your broker, bank or other nominee. You must provide the record holder of your shares with instructions on how to vote your shares. Otherwise, your broker, bank or other nominee cannot vote your shares on the Camber or the Viking Proposals to be considered at the Camber Special Meeting or the Viking Special Meeting, as applicable. |

|

|

| A so called “broker non-vote” will result if your broker, bank or other nominee returns a proxy but does not provide instruction as to how shares should be voted.

Camber Proposals

Under the current NYSE American rules, brokers, banks or other nominees do not have discretionary authority to vote on the Camber Issuance Proposals. Therefore, if you fail to provide your broker, bank or other nominee with instructions on how to vote your shares with respect to the Camber Issuance Proposals, your shares will be counted as broker non-votes. If there are any broker non-votes, they will have no effect on the Camber Issuance Proposals or the Camber Adjournment Proposal.

Viking Proposals

Brokers, banks or other nominees do not have discretionary authority to vote on any of the Viking Proposals at the Viking Special Meeting. Because the only proposals for consideration at the Viking Special Meeting are non-discretionary proposals, it is not expected that there will be any broker non-votes at the Viking Special Meeting. However, if there are any broker non-votes, they will have (1) the same effect as a vote “AGAINST” the Viking Merger Proposal and (2) no effect on the Viking Adjournment Proposal. |

|

|

Q: | What Camber Stockholder vote is required for the approval of each of the Camber Issuance Proposals and the Camber Adjournment Proposal? |

|

|

A: | The Camber Common Stock Issuance Proposal. Approval of the Camber Common Stock Issuance Proposal requires the affirmative vote of a majority of the shares of Camber stock present at the Camber Special Meeting, whether present via the Camber Special Meeting Website or by proxy, and entitled to vote on the proposal. Abstentions will have the same effect as a vote “AGAINST” the Camber Common Stock Issuance Proposal, while a broker non-vote or the failure of a Camber Stockholder to vote (e.g., by not submitting a proxy and not voting at the Camber Special Meeting) will have no effect on the outcome of the Camber Common Stock Issuance Proposal. |

|

|

| The Camber Series A Preferred Stock Issuance Proposal. Approval of the Camber Series A Preferred Stock Issuance Proposal requires the affirmative vote of a majority of the shares of Camber stock present at the Camber Special Meeting, whether present via the Camber Special Meeting Website or by proxy, and entitled to vote on the proposal. Abstentions will have the same effect as a vote “AGAINST” the Camber Series A Preferred Stock Issuance Proposal, while a broker non-vote or the failure of a Camber Stockholder to vote (e.g., by not submitting a proxy and not voting at the Camber Special Meeting) will have no effect on the outcome of the Camber Series A Preferred Stock Issuance Proposal.

The Camber Series H Preferred Stock Issuance Proposal. Approval of the Camber Series H Preferred Stock Issuance Proposal requires the affirmative vote of a majority of the shares of Camber stock present at the Camber Special Meeting, whether present via the Camber Special Meeting Website or by proxy, and entitled to vote on the proposal. Abstentions will have the same effect as a vote “AGAINST” the Camber Series H Preferred Stock Issuance Proposal, while a broker non-vote or the failure of a Camber Stockholder to vote (e.g., by not submitting a proxy and not voting at the Camber Special Meeting) will have no effect on the outcome of the Camber Series H Preferred Stock Issuance Proposal. |

| 3 |

| Table of Contents |

| The Camber Adjournment Proposal. Approval of the Camber Adjournment Proposal requires the affirmative vote of a majority of the shares of Camber stock present at the Camber Special Meeting, whether present via the Camber Special Meeting Website or by proxy, and entitled to vote on the proposal. Abstentions will have the same effect as a vote “AGAINST” the Camber Adjournment Proposal, while a broker non-vote or the failure of a Camber Stockholder to vote (e.g., by not submitting a proxy and not voting at the Camber Special Meeting) will have no effect on the outcome of the Camber Adjournment Proposal. | |

|

| |

Q: | What Viking Stockholder vote is required for the approval of the Viking Merger Proposal and the Viking Adjournment Proposal? | |

|

| |

A: | The Viking Merger Proposal. Approval of the Viking Merger Proposal requires the affirmative vote of a majority of the outstanding shares of Viking stock entitled to vote on the proposal. Abstentions, broker non-votes, or any failure by a Viking Stockholder to vote (e.g., by not submitting a proxy and not voting at the Viking Special Meeting) will have the same effect as a vote “AGAINST” the Viking Merger Proposal. | |

| ||

| The Viking Adjournment Proposal. Approval of the Viking Adjournment Proposal requires the affirmative vote of a majority of the shares of Viking stock present at the Viking Special Meeting, whether present via the Viking Special Meeting Website or by proxy, and entitled to vote on the proposal. Abstentions will have the same effect as a vote “AGAINST” the proposal, while a broker non-vote or the failure of a Viking Stockholders to vote (e.g., by not submitting a proxy and not voting at the Viking Special Meeting) will have no effect on the outcome of the Viking Adjournment Proposal. | |

|

| |

Q: | Who will count the votes? | |

|

| |

A: | The votes at the Camber Special Meeting will be counted by an independent inspector of elections appointed by the Camber Board. The votes at the Viking Special Meeting will be counted by an independent inspector of elections appointed by the Viking Board. | |

|

| |

Q: | What will Viking Stockholders receive if the Merger is completed? | |

|

| |

A: | As a result of the Merger, each share of Viking Common Stock issued and outstanding immediately prior to the effective time of the Merger (other than shares of Viking Common Stock owned by Camber, Viking or Merger Sub) will be converted into the right to receive the following (the “Common Stock Merger Consideration”): one (1) share of Camber Common Stock (with such exchange ratio referred to as the “Exchange Ratio”). | |

|

| |

| As a result of the Merger, each share of Viking Series C Preferred Stock issued and outstanding immediately prior to the effective time of the Merger will be converted into the right to receive one (1) share of the to-be-designated Series A Convertible Preferred Stock of Camber (the “New Camber Series A Preferred Stock”) which will (1) have no right to vote on any matters, questions or proceedings of Camber, except: (i) on a proposal to increase or reduce Camber’s authorized share capital, (ii) on a resolution to approve the terms of any buy-back agreement, (iii) on a proposal to wind up Camber, (iv) on a proposal for the disposal of all or substantially all of Camber’s property, business and undertaking, (f) during the winding-up of Camber, and/or (g) with respect to a proposed merger or consolidation in which Camber is a party or a subsidiary of Camber is a party, in each case on an as-converted basis (subject to a 9.99% beneficial ownership limitation); (2) receive, upon the occurrence of a liquidation of Camber, the same amount of consideration that would have been due if such shares of New Camber Series A Preferred Stock had been converted into Camber Common Stock immediately prior to such liquidation; (3) provide rights for each such share of New Camber Series A Preferred Stock to convert, at the option of the holder thereof, into 890 shares of Camber Common Stock; and (4) not have any redemption rights and share equally in any dividends authorized by the Camber Board for distribution to holders of Camber Common Stock, on an as-converted basis, along with those other powers, rights, preferences and restrictions set forth in Exhibit A to the Merger Agreement (the “Series C Preferred Stock Merger Consideration”). Currently, all 28,092 shares of Viking Series C Preferred Stock outstanding are held by Viking’s CEO and director, James Doris. | |

| 4 |

| Table of Contents |

| As a result of the Merger, each share of Viking Series E Preferred Stock issued and outstanding immediately prior to the effective time of the Merger will be converted into the right to receive one (1) share of the to-be-designated Series H Convertible Preferred Stock of Camber (the “New Camber Series H Preferred Stock” and together with the New Camber Series A Preferred Stock, the “New Camber Preferred Stock”), with each share of New Camber Series H Preferred Stock having the right to one (1) vote, and the right to convert into that number of shares of Camber Common Stock that each share of Viking Series E Preferred Stock is convertible into (with the conversion ratio based upon achievement of certain milestones by Viking’s subsidiary, Viking Protection Systems, LLC), along with those other powers, rights, preferences and restrictions set forth in Exhibit B to the Merger Agreement (the “Series E Preferred Stock Merger Consideration” and together with the Series C Preferred Stock Merger Consideration, the “Preferred Stock Merger Consideration”). We refer to the Common Stock Merger Consideration and the Preferred Stock Merger Consideration collectively as the “Merger Consideration.” |

|

|

| We refer to such shares of Viking Common Stock, Viking Series C Preferred Stock and the Viking Series E Preferred Stock eligible to receive the applicable Merger Consideration as “Eligible Shares.” |

|

|

| If you receive Merger Consideration and would otherwise be entitled to receive a fractional share of Camber Common Stock or New Camber Preferred Stock, as applicable, you will entitled to have such fractional shares rounded up to the nearest whole share. For additional information regarding the Merger Consideration, see the sections entitled “The Merger Agreement - Merger Consideration; Treatment of Viking Convertible Securities and Preferred Stock; Treatment of Camber Convertible Securities and Preferred Stock. |

|

|

Q: | What will holders of Viking’s warrants, options and convertible promissory notes receive if the Merger is completed? |

|

|

A: | Viking Warrants and Options. At the effective time of the Merger, each then outstanding option or warrant to purchase Viking Common Stock (which we refer to as a “Viking Option”) will, to the extent unvested, automatically become fully vested and will be converted automatically into an option or warrant (which we refer to as an “Adjusted Option”) to purchase, on substantially the same terms and conditions as were applicable to such Viking Option immediately prior to the effective time of the Merger, except that (i) instead of being exercisable into Viking Common Stock, such Adjusted Option will be exercisable into Camber Common Stock, and (ii) all references to the “Company” in the Viking Option agreements will be references to Camber in the Adjusted Option agreements. |

|

|

| Viking Convertible Promissory Notes. At the effective time of the Merger, each promissory note issued by Viking that is convertible into Viking Common Stock (a “Viking Convertible Note”) that, as of immediately prior to the effective time of the Merger, is outstanding and unconverted shall be converted into a promissory note convertible into Camber Common Stock (an “Adjusted Convertible Note”) having substantially the same terms and conditions as applied to the corresponding Viking Convertible Note as of immediately prior to the effective time of the Merger (including, for the avoidance of doubt, any extended post-termination conversion period that applies following consummation of the Merger), except that (i) instead of being convertible into Viking Common Stock, such Adjusted Convertible Note will be convertible into Camber Common Stock, and (ii) all references to the “Company” in the Viking Convertible Note agreements will be references to Camber in the Adjusted Convertible Note agreements. |

|

|

| For additional information regarding the treatment of Viking Options and Viking Convertible Notes, see the section entitled “The Merger Agreement - Treatment of Viking Convertible Securities and Preferred Stock.” |

|

|

Q: | How will the Merger affect Camber’s equity awards? |

|

|

A: | Each warrant or option to purchase shares of Camber Common Stock will not be impacted by the Merger and will continue to be a warrant or option in respect of Camber Common Stock following the effective time of the Merger, subject to the same terms and conditions that were applicable to such warrant or option before the effective time of the Merger. For details on the treatment of Camber’s equity awards, see “The Merger Agreement—Treatment of Camber Convertible Securities and Preferred Stock.” |

| 5 |

| Table of Contents |

Q: | What equity stake will Viking Stockholders hold in Camber immediately following the Merger? | |

|

| |

A: | Based on the number of issued and outstanding shares of Camber Common Stock and Viking Common Stock as of , 2023 (on a fully diluted basis, without taking into account shares of Camber Common Stock issuable upon conversion of Camber’s Series C Redeemable Convertible Preferred Stock or Camber’s Series G Redeemable Convertible Preferred Stock), and the Exchange Ratio, Viking Stockholders as of immediately prior to the effective time of the Merger would hold, in the aggregate, approximately % of the issued and outstanding shares of Camber Common Stock immediately following the effective time of the Merger. The exact equity stake of Viking Stockholders in Camber immediately following the effective time of the Merger will depend on the number of shares of Camber Common Stock and Viking Common Stock issued and outstanding immediately prior to the effective time of the Merger, the number of shares of Camber Preferred Stock and Viking Preferred Stock issued and outstanding immediately prior to the effective time of the Merger (and the applicable conversion ratios thereof at such time), as provided in the section entitled “The Merger Agreement - Treatment of Viking Convertible Securities and Preferred Stock .” | |

|

| |

Q: | How does the Camber Board and Viking Board recommend that I vote? | |

|

| |

A: | Camber. The Camber Board unanimously recommends that Camber Stockholders vote “FOR” the Camber Common Stock Issuance Proposal, “FOR” the Camber Series A Preferred Stock Issuance Proposal, “FOR” the Camber Series H Preferred Stock Issuance Proposal and “FOR” the Camber Adjournment Proposal. For additional information regarding how the Camber Board recommends that Camber Stockholders vote, see the section entitled “The Merger - Camber’s Reasons for the Merger; Recommendation of the Camber Board.” | |

|

| |

| Viking. The Viking Board unanimously recommends that Viking Stockholders vote “FOR” the Viking Merger Proposal and “FOR” the Viking Adjournment Proposal. For additional information regarding how the Viking Board recommends that Viking Stockholders vote, see the section entitled “The Merger - Viking’s Reasons for the Merger; Recommendations of the Viking Board.” | |

|

| |

Q: | Who is entitled to vote at the special meeting? | |

|

| |

A: | Camber Special Meeting. The Camber Board has fixed , 2023, as the record date for the Camber Special Meeting. All holders of record of shares of Camber Common Stock, Camber’s Series C Redeemable Convertible Preferred Stock (“Camber Series C Preferred Stock”) and Camber’s Series G Redeemable Convertible Preferred Stock (“Camber Series G Preferred Stock”) as of the close of business on the record date are entitled to receive notice of, and to vote at, the Camber Special Meeting via the Camber Special Meeting Website or by proxy, provided that those shares remain outstanding on the date of the Camber Special Meeting; provided, further, that holders of the Camber Series C Preferred Stock and the Camber Series G Preferred Stock have the right to cast votes on all Camber Proposals, except any shareholder proposals, equal to the as-converted amount of such Camber Series C Preferred Stock and Camber Series G Preferred Stock, respectively (subject to the beneficial ownership limitations in the Certificate of Designations of Preferences, Powers, Rights and Limitations of Series C Redeemable Convertible Preferred Stock (the “Camber Series C COD”) and the Certificate of Designations of Preferences, Powers, Rights and Limitations of Series G Redeemable Convertible Preferred Stock (the “Camber Series G COD”), respectively). The holders of the Camber Series C Preferred Stock and Camber Series G Preferred Stock have contractually agreed not to vote any shares except as requested by the Camber Board. As of the record date, there were shares of Camber Common Stock issued and outstanding, shares of Camber Series C Preferred Stock issued and outstanding, and shares of Camber Series G Preferred Stock issued and outstanding. The votes associated with such Camber Series C Preferred Stock and Camber Series G Preferred Stock, given beneficial ownership limitations, total , collectively, resulting in an aggregate of total voting shares at the Camber Special Meeting. Attendance at the Camber Special Meeting via the Camber Special Meeting Website is not required to vote. Instructions on how to vote your shares without virtually attending the Camber Special Meeting are provided in this section below. | |

|

| |

| Viking Special Meeting. The Viking Board has fixed , 2023, as the record date for the Viking Special Meeting. All holders of record of shares of Viking Common Stock, Viking Series C Preferred Stock and Viking Series E Preferred Stock as of the close of business on the record date are entitled to receive notice of, and to vote at, the Viking Special Meeting via the Viking Special Meeting Website or by proxy, provided that those shares remain outstanding on the date of the Viking Special Meeting; provided, further, that (i) holders of Viking Common Stock and Viking Series E Preferred Stock have the right to cast one (1) vote for each share of Viking Common Stock and Viking Series E Preferred Stock, and (ii) holders of the Viking Series C Preferred Stock have the right to cast 37,500 votes for each share of Viking Series C Preferred Stock. As of the record date, there were shares of Viking Common Stock outstanding (including shares of Viking Common Stock owned by Camber), shares of Viking Series C Preferred Stock outstanding and shares of Viking Series E Preferred Stock outstanding, resulting in an aggregate of total voting shares at the Viking Special Meeting. Attendance at the Viking Special Meeting via the Viking Special Meeting Website is not required to vote. Instructions on how to vote your shares without virtually attending the Viking Special Meeting are provided in this section below. | |

| 6 |

| Table of Contents |

Q: | How many votes do I have? |

|

|

A: | Camber Common Stock. Each Camber Stockholder of record is entitled to one vote for each share of Camber Common Stock held of record by such stockholder as of the close of business on the record date. |

|

|

| Camber Series C Preferred Stock. Each Camber Stockholder of record, pursuant to the voting rights and beneficial ownership limitation contained in the Camber Series C COD, is entitled to votes for each share of Camber Series C Preferred Stock held of record by such stockholder as of the close of business on the record date; provided, however, that the holders of the Camber Series C Preferred Stock have contractually agreed not to vote any shares except as requested by the Camber Board. |

|

|

| Camber Series G Preferred Stock. Each Camber Stockholder of record, pursuant to the voting rights and beneficial ownership limitation contained in the Camber Series G COD, is entitled to votes for each share of Camber Series G Preferred Stock held of record by such stockholder as of the close of business on the record date; provided, however, that the holders of the Camber Series G Preferred Stock have contractually agreed not to vote any shares except as requested by the Camber Board. |

|

|

| Viking Common Stock. Each Viking Stockholder of record is entitled to one vote for each share of Viking Common Stock held of record by such stockholder as of the close of business on the record date. |

|

|

| Viking Series C Preferred Stock. Each Viking Stockholder of record is entitled to 37,500 votes for each share of Viking Series C Preferred Stock held of record by such stockholder as of the close of business on the record date. |

|

|

| Viking Series E Preferred Stock. Each Viking Stockholder of record is entitled to one vote for each share of Viking Series E Preferred Stock held of record by such stockholder as of the close of business on the record date. |

|

|

Q: | What constitutes a quorum for each of the Camber Special Meeting and the Viking Special Meeting? |

|

|

A: | Quorum for Camber Special Meeting. Under the Amended and Restated Bylaws of Camber (which, as amended prior to the date of this joint proxy statement/prospectus, we refer to as the “Camber Bylaws”), the presence at the Camber Special Meeting, whether via the Camber Special Meeting Website or by proxy, of 33% of all shares of Camber stock issued and outstanding and entitled to vote on each of the Camber Proposals will be necessary to establish a quorum with respect to such proposal. If you submit a properly executed proxy card, even if you vote “against” the proposal or vote to “abstain” in respect of the proposal, your shares of Camber stock will be counted for purposes of calculating whether a quorum is present. Because the Camber Issuance Proposals are non-routine under applicable NYSE American rules, brokers, banks and other nominees do not have discretionary authority to vote on the Camber Issuance Proposals and will not be able to vote on the Camber Issuance Proposals absent instructions from the beneficial owner. Accordingly, the failure of a beneficial owner to provide voting instructions to its broker, bank, or other nominee will result in a broker non-vote, which will not be considered present and entitled to vote on the Camber Issuance Proposals for the purpose of determining the presence of a quorum with respect to the vote thereon. |

|

|

| Quorum for Viking Special Meeting. The presence at the Viking Special Meeting via the Viking Special Meeting Website or by proxy of the holders of a majority of the Viking stock issued and outstanding and entitled to vote thereon constitutes a quorum. If you submit a properly executed proxy card, even if you do not vote “for” any of the proposals or vote to “abstain” in respect of each of the proposals, your shares of Viking stock will be counted for purposes of calculating whether a quorum is present for the transaction of business at the Viking Special Meeting. Because the only proposals for consideration at the Viking Special Meeting are non-discretionary proposals, it is not expected that there will be any broker non-votes at the Viking Special Meeting. Broker non-votes will not be treated as present for determining the presence of a quorum at the Viking Special Meeting. |

|

|

Q: | What will happen to Viking as a result of the Merger? |

|

|

A: | If the Merger is completed, Merger Sub will merge with and into Viking. As a result of the Merger, the separate corporate existence of Merger Sub will cease, and Viking will continue as the surviving corporation in the Merger and as a wholly owned subsidiary of Camber. Furthermore, Viking will no longer be a public company, and the Viking Common Stock will no longer be quoted on the over-the-counter OTC Link Alternative Trading System (ATS) operated by OTC Markets Group, Inc. (“OTCQB”), will be deregistered under the Exchange Act, and will cease to be publicly traded. |

| 7 |

| Table of Contents |

Q: | I own shares of Viking Common Stock or Viking Preferred Stock. What will happen to those shares as a result of the Merger? |